Embed Size (px)

Citation preview

Inclusive growth in Russia: Achievements and Challenges

Ana RevengaSenior Director

Poverty and Equity Global Practice, The World Bank

Moscow, 7 April 2015

2

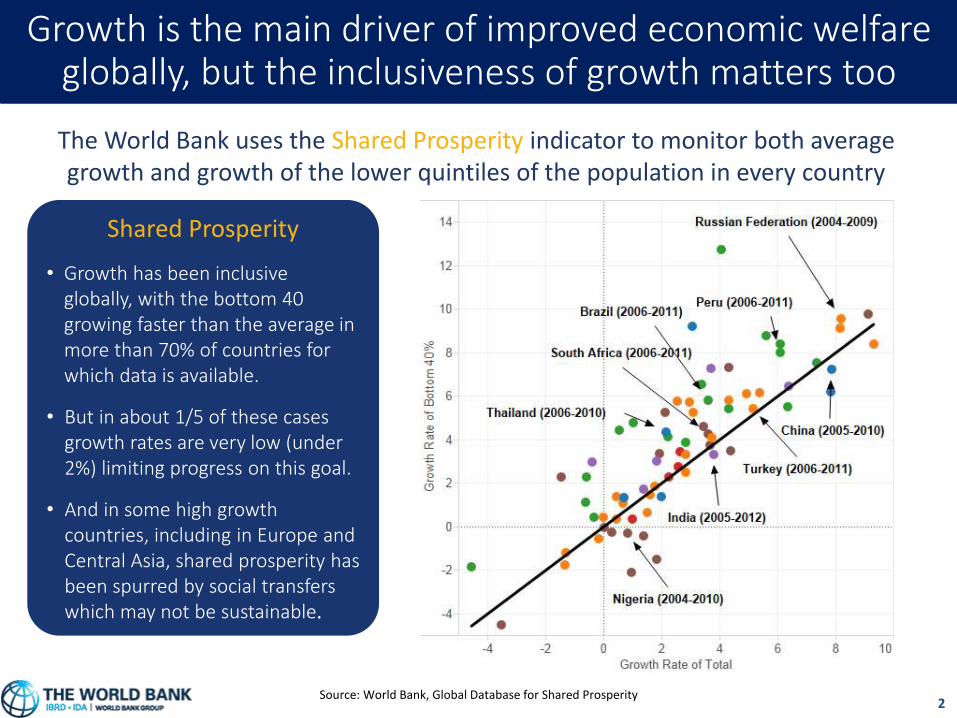

Growth is the main driver of improved economic welfare globally, but the inclusiveness of growth matters too

The World Bank uses the Shared Prosperity indicator to monitor both average growth and growth of the lower quintiles of the population in every country

Shared Prosperity

• Growth has been inclusive globally, with the bottom 40 growing faster than the average in more than 70% of countries for which data is available.

• But in about 1/5 of these cases growth rates are very low (under 2%) limiting progress on this goal.

• And in some high growth countries, including in Europe and Central Asia, shared prosperity has been spurred by social transfers which may not be sustainable.

Source: World Bank, Global Database for Shared Prosperity

3

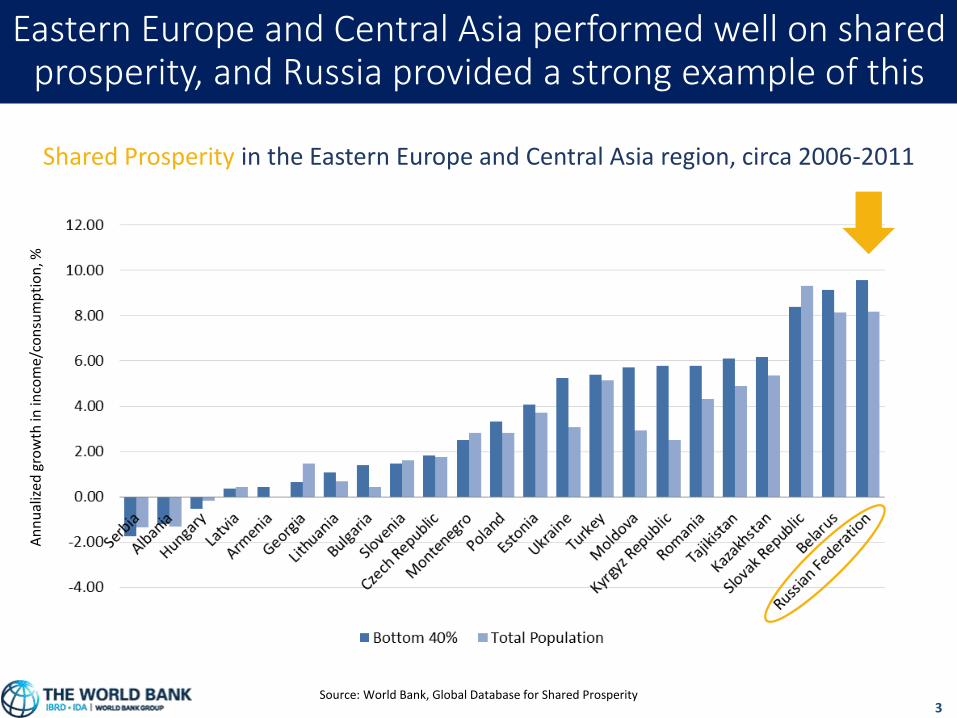

Eastern Europe and Central Asia performed well on shared prosperity, and Russia provided a strong example of this

Shared Prosperity in the Eastern Europe and Central Asia region, circa 2006-2011

An

nu

aliz

ed g

row

th in

inco

me/

con

sum

pti

on

, %

Source: World Bank, Global Database for Shared Prosperity

0

10

20

30

40

50

60

70

80

90

100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

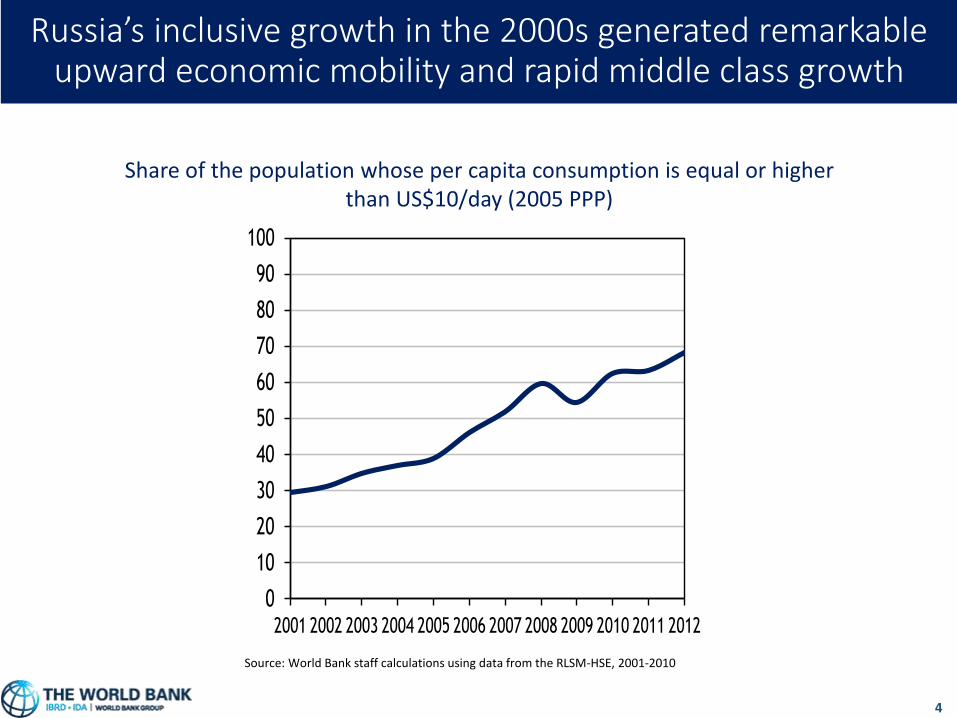

Source: World Bank staff calculations using data from the RLSM-HSE, 2001-2010

Share of the population whose per capita consumption is equal or higher than US$10/day (2005 PPP)

Russia’s inclusive growth in the 2000s generated remarkable upward economic mobility and rapid middle class growth

4

5

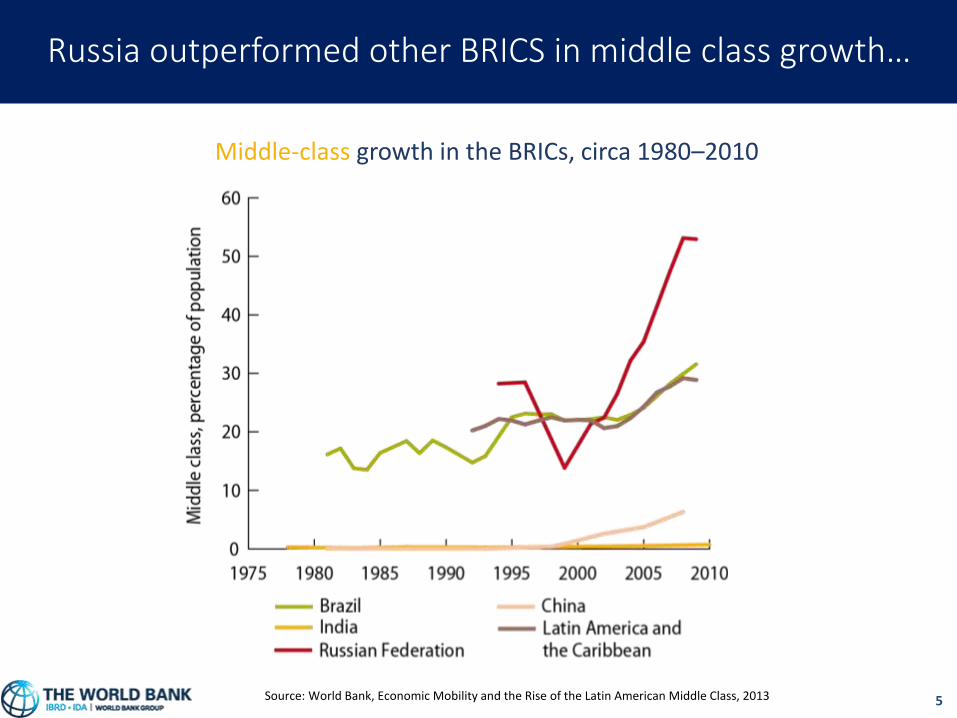

Russia outperformed other BRICS in middle class growth…

Middle-class growth in the BRICs, circa 1980–2010

Source: World Bank, Economic Mobility and the Rise of the Latin American Middle Class, 2013

6

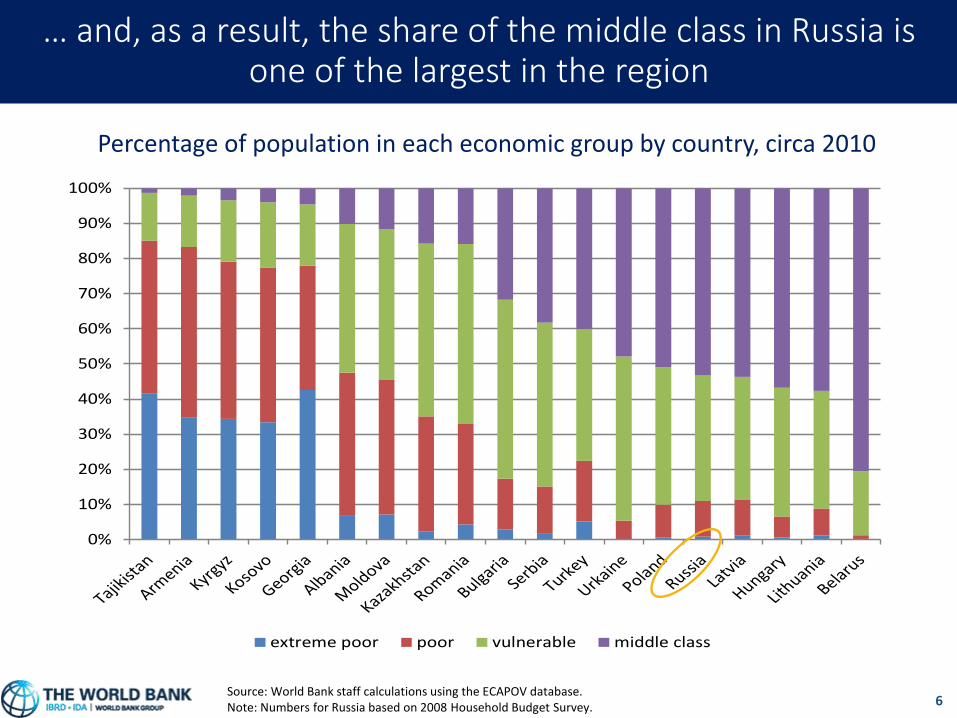

… and, as a result, the share of the middle class in Russia is one of the largest in the region

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

extreme poor poor vulnerable middle class

Source: World Bank staff calculations using the ECAPOV database. Note: Numbers for Russia based on 2008 Household Budget Survey.

Percentage of population in each economic group by country, circa 2010

7

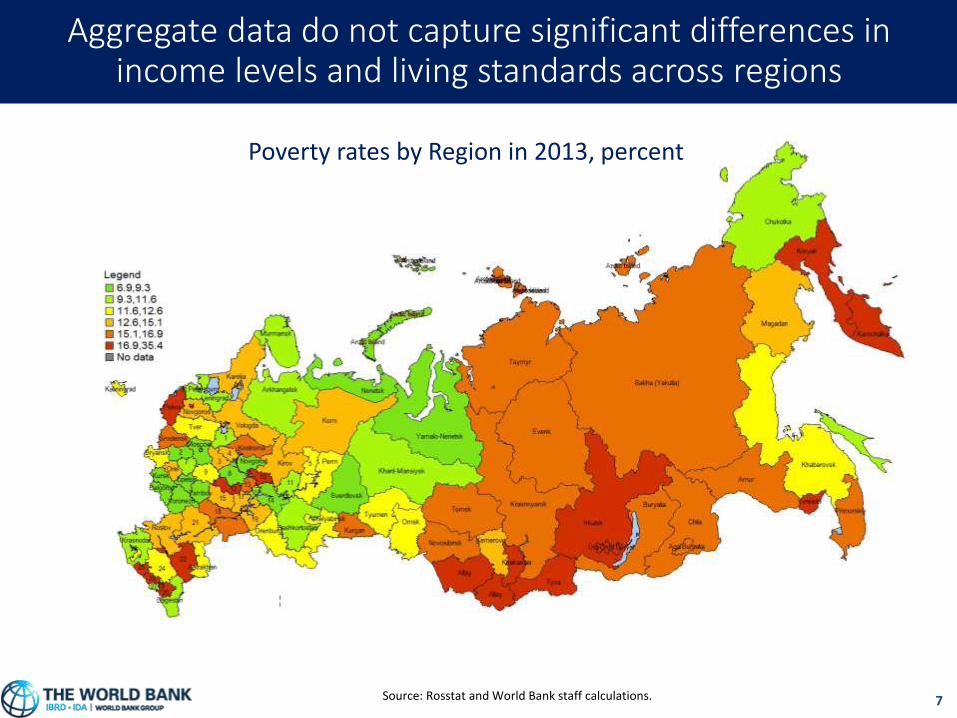

Aggregate data do not capture significant differences in income levels and living standards across regions

Heterogeneity x

Source: Rosstat and World Bank staff calculations.

Poverty rates by Region in 2013, percent

8

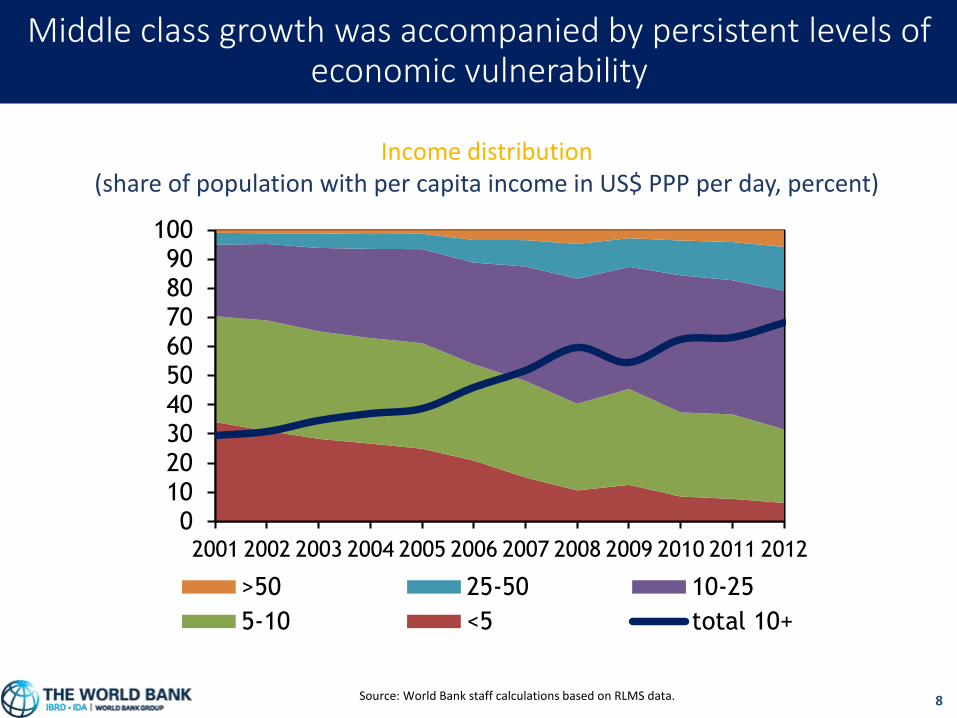

Middle class growth was accompanied by persistent levels of economic vulnerability

Income distribution(share of population with per capita income in US$ PPP per day, percent)

Source: World Bank staff calculations based on RLMS data.

0102030405060708090

100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

>50 25-50 10-25

5-10 <5 total 10+

9

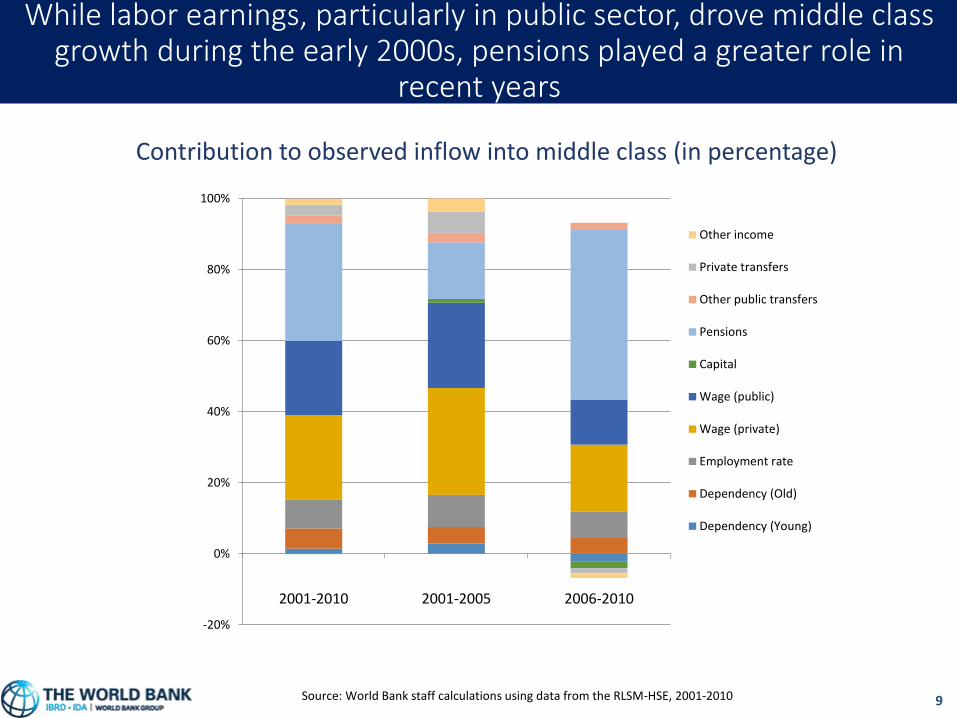

While labor earnings, particularly in public sector, drove middle class growth during the early 2000s, pensions played a greater role in

recent years

Contribution to observed inflow into middle class (in percentage)

Source: World Bank staff calculations using data from the RLSM-HSE, 2001-2010

-20%

0%

20%

40%

60%

80%

100%

2001-2010 2001-2005 2006-2010

Other income

Private transfers

Other public transfers

Pensions

Capital

Wage (public)

Wage (private)

Employment rate

Dependency (Old)

Dependency (Young)

10

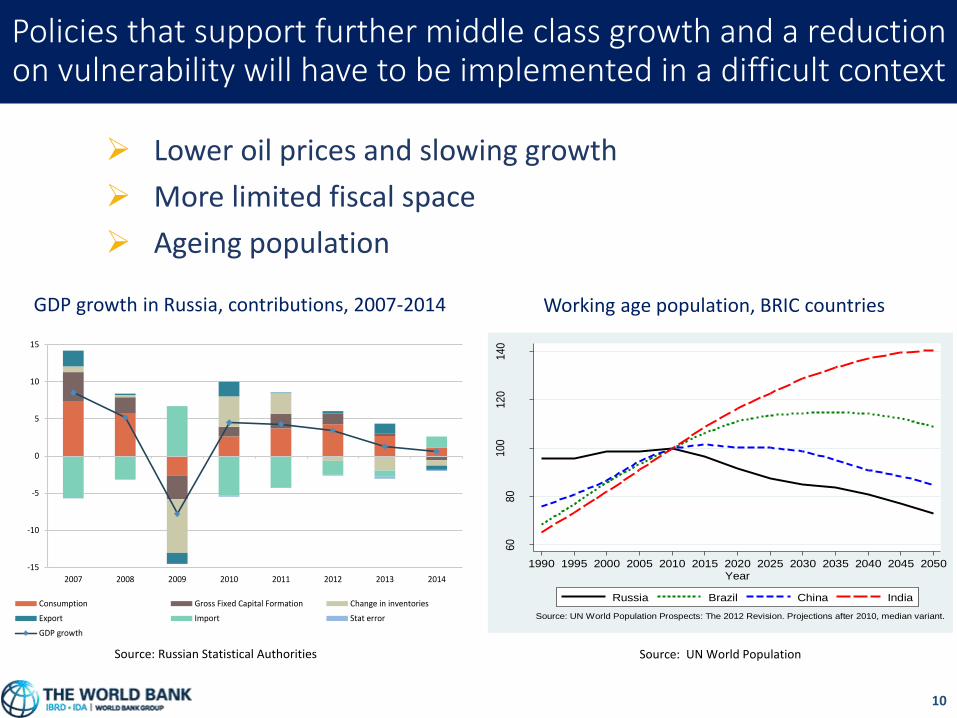

Policies that support further middle class growth and a reduction on vulnerability will have to be implemented in a difficult context

60

80

100

120

140

Popula

tion A

ged

15 t

o 6

4 (

201

0=

100)

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050Year

Russia Brazil China India

Source: UN World Population Prospects: The 2012 Revision. Projections after 2010, median variant.

Working age population, BRIC countries

Source: UN World Population

-15

-10

-5

0

5

10

15

2007 2008 2009 2010 2011 2012 2013 2014

Consumption Gross Fixed Capital Formation Change in inventories

Export Import Stat error

GDP growth

Lower oil prices and slowing growth

More limited fiscal space

Ageing population

GDP growth in Russia, contributions, 2007-2014

Source: Russian Statistical Authorities

11

Russia may benefit from rebalancing its policy strategy in two different dimensions

1. Rebalancing the role of the private vs. public sectors in driving economic activity, productivity growth and job creation, by leveling the playing field

2. Rebalancing the responsibilities and accountability for service delivery between central and regional governments, by strengthening local governance and improving effectiveness

This would need to be done while rationalizing and continuing to provide targeted social insurance and safety net support to

the most vulnerable, the elderly and those unable to work

12

Rebalancing the role of the private vs. public sectorin driving economic activity, productivity growth and

job creation, by leveling the playing field

13

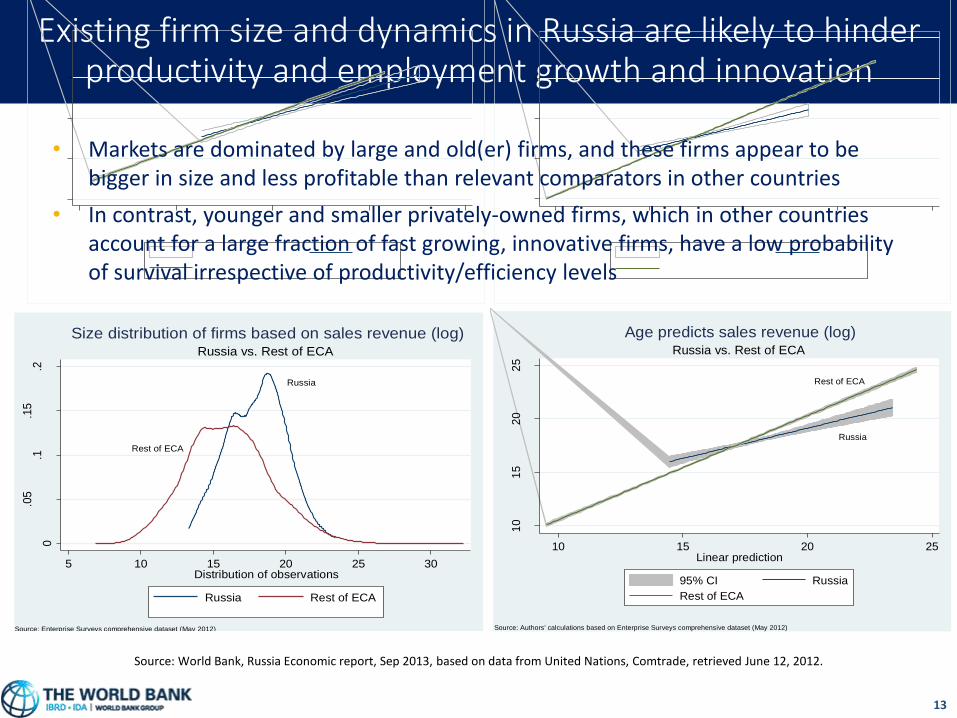

Existing firm size and dynamics in Russia are likely to hinder productivity and employment growth and innovation

RussiaRest of ECA

0

.05

.1.1

5.2

.25

kd

en

sity lab

or

forc

e (

log)

0 2 4 6 8 10Distribution of observations

Russia Rest of ECA

Source: Enterprise Surveys comprehensive dataset (May 2012)

Russia vs. Rest of ECA

Size distribution of firms based on labor force (log)

Russia

Rest of the World

0.1

.2.3

kd

en

sity lab

or

forc

e (

log)

0 5 10Distribution of observations

Russia Rest of the World

Source: Enterprise Surveys comprehensive dataset (May 2012)

Russia vs. Rest of the World

Size distribution of firms based on labor force (log)

Russia

Rest of ECA

0

.05

.1.1

5.2

kd

en

sity s

ale

s r

even

ue

(lo

g)

5 10 15 20 25 30Distribution of observations

Russia Rest of ECA

Source: Enterprise Surveys comprehensive dataset (May 2012)

Russia vs. Rest of ECA

Size distribution of firms based on sales revenue (log)

Russia

Rest of the World

0

.05

.1.1

5.2

kd

en

sity o

f sale

s r

eve

nu

e (

log)

0 10 20 30 40Distribution of observations

Russia Rest of the World

Source: Enteprise Surveys comprehensive dateset (May 2012)

Russia vs. Rest of the World

Size distribution of firms based on sales revenue (log)

Rest of the World

Russia

02

46

8

Actu

al siz

e o

f la

bo

r (l

og

)

0 2 4 6 8Linear prediction

95% CI Russia

Rest of the World

Source: Authors' calculations based on comprehensive dataset of Enterprise Surveys (May 2012)

Russia vs. Rest of the World

Age predicts size of labor force (log)

Rest of the World

Russia

10

15

20

25

30

Actu

al sale

s r

eve

nu

e (

log)

10 15 20 25 30Linear prediction

95% CI Russia

Rest of the World

Source: Authors' calculations based on comprehensive dataset of Enterprise Surveys (May 2012)

Russia vs. Rest of the World

Age predicts sales revenue (log)

Russia

Rest of ECA

02

46

8

Actu

al siz

e o

f la

bo

r fo

rce

(lo

g)

0 2 4 6 8Linear prediction

95% CI Russia

Rest of ECA

Source: Authors' calculatons based on Enterprise Survey comprehensive dataset (May 2012)

Russia vs. Rest of ECA

Age predicts size of labor force (log)

Russia

Rest of ECA

10

15

20

25

Acu

tal sale

s r

eve

nu

e (

log)

10 15 20 25Linear prediction

95% CI Russia

Rest of ECA

Source: Authors' calculations based on Enterprise Surveys comprehensive dataset (May 2012)

Russia vs. Rest of ECA

Age predicts sales revenue (log)

Source: World Bank, Russia Economic report, Sep 2013, based on data from United Nations, Comtrade, retrieved June 12, 2012.

• Markets are dominated by large and old(er) firms, and these firms appear to be bigger in size and less profitable than relevant comparators in other countries

• In contrast, younger and smaller privately-owned firms, which in other countries account for a large fraction of fast growing, innovative firms, have a low probability of survival irrespective of productivity/efficiency levels

14

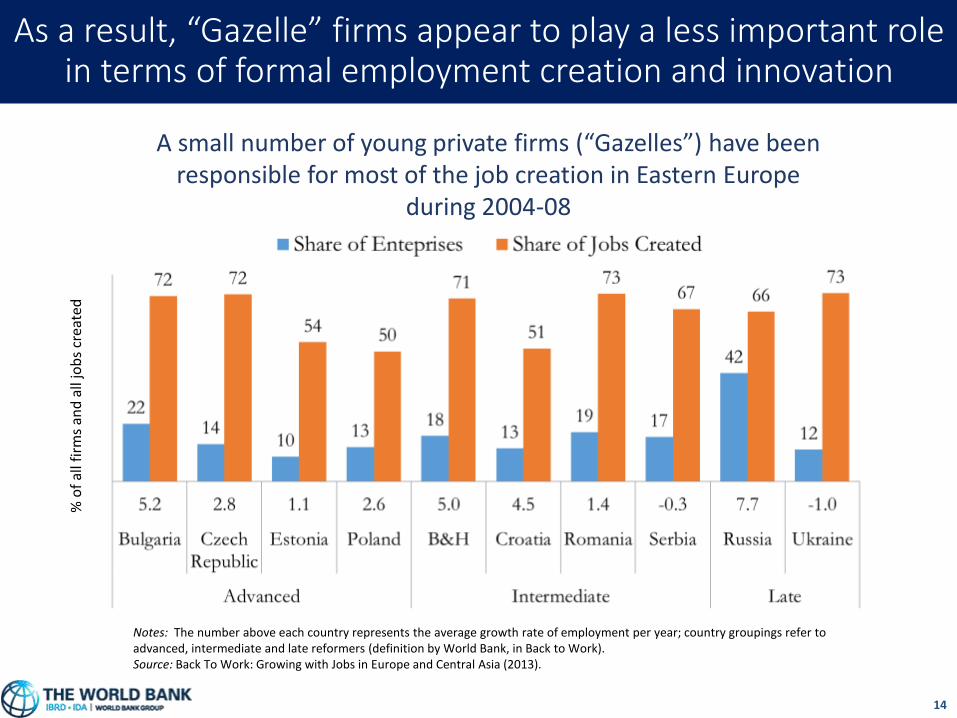

As a result, “Gazelle” firms appear to play a less important role in terms of formal employment creation and innovation

A small number of young private firms (“Gazelles”) have been responsible for most of the job creation in Eastern Europe

during 2004-08

Notes: The number above each country represents the average growth rate of employment per year; country groupings refer to advanced, intermediate and late reformers (definition by World Bank, in Back to Work).Source: Back To Work: Growing with Jobs in Europe and Central Asia (2013).

% o

f al

l fir

ms

and

all

job

s cr

eate

d

15

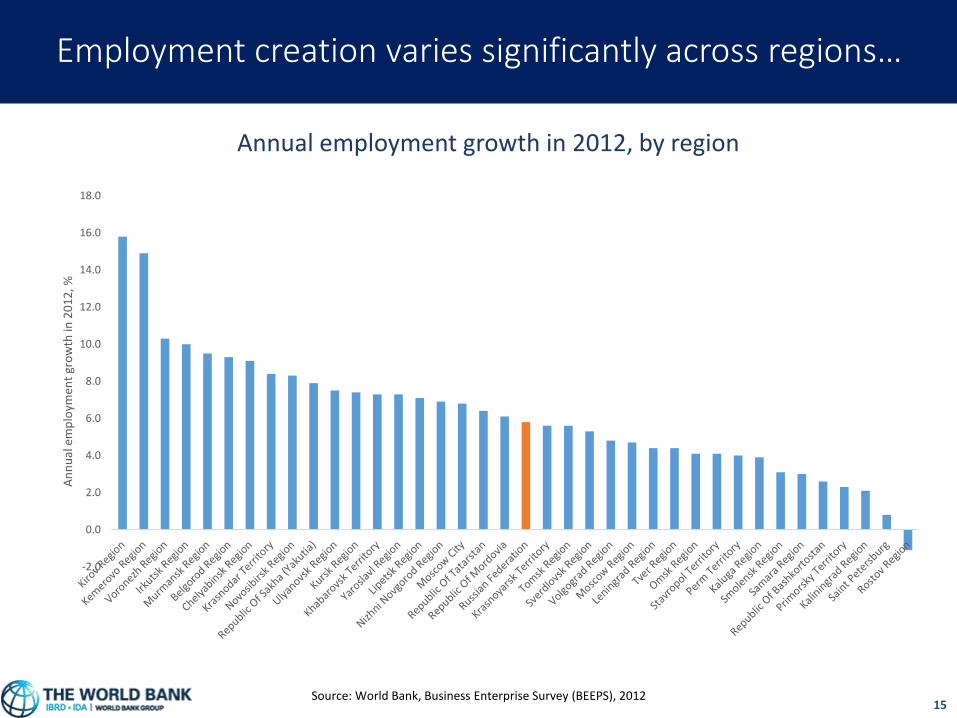

Employment creation varies significantly across regions…

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

An

nu

al e

mp

loym

ent

gro

wth

in 2

01

2, %

Annual employment growth in 2012, by region

Source: World Bank, Business Enterprise Survey (BEEPS), 2012

16

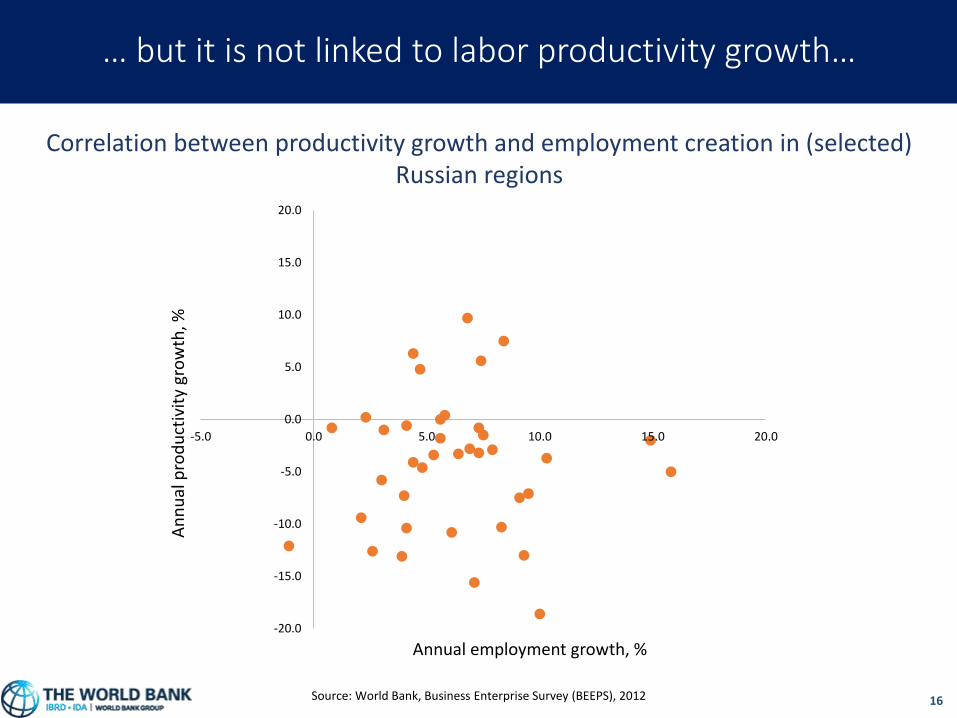

… but it is not linked to labor productivity growth…

Source: World Bank, Business Enterprise Survey (BEEPS), 2012

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

-5.0 0.0 5.0 10.0 15.0 20.0

An

nu

al p

rod

uct

ivit

y gr

ow

th, %

Annual employment growth, %

Correlation between productivity growth and employment creation in (selected) Russian regions

17

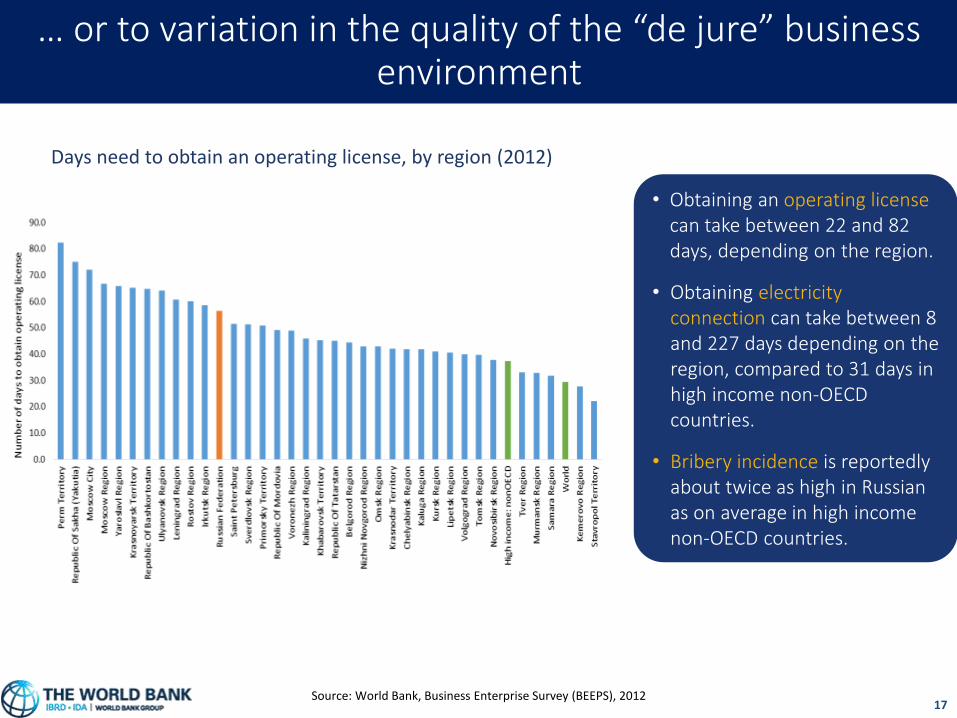

… or to variation in the quality of the “de jure” business environment

Source: World Bank, Business Enterprise Survey (BEEPS), 2012

Days need to obtain an operating license, by region (2012)

• Obtaining an operating license can take between 22 and 82 days, depending on the region.

• Obtaining electricity connection can take between 8 and 227 days depending on the region, compared to 31 days in high income non-OECD countries.

• Bribery incidence is reportedly about twice as high in Russian as on average in high income non-OECD countries.

18

Rebalancing the responsibilities and accountability for service delivery between central and regional

governments, by strengthening local governance while avoiding exacerbating inequalities

19

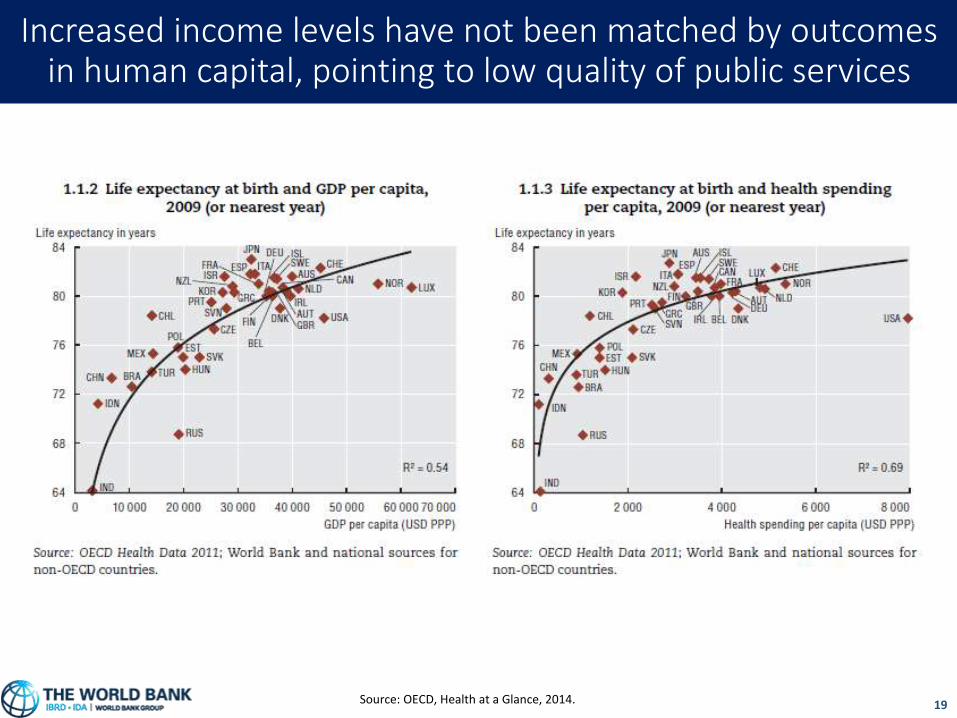

Increased income levels have not been matched by outcomes in human capital, pointing to low quality of public services

Source: OECD, Health at a Glance, 2014.

20

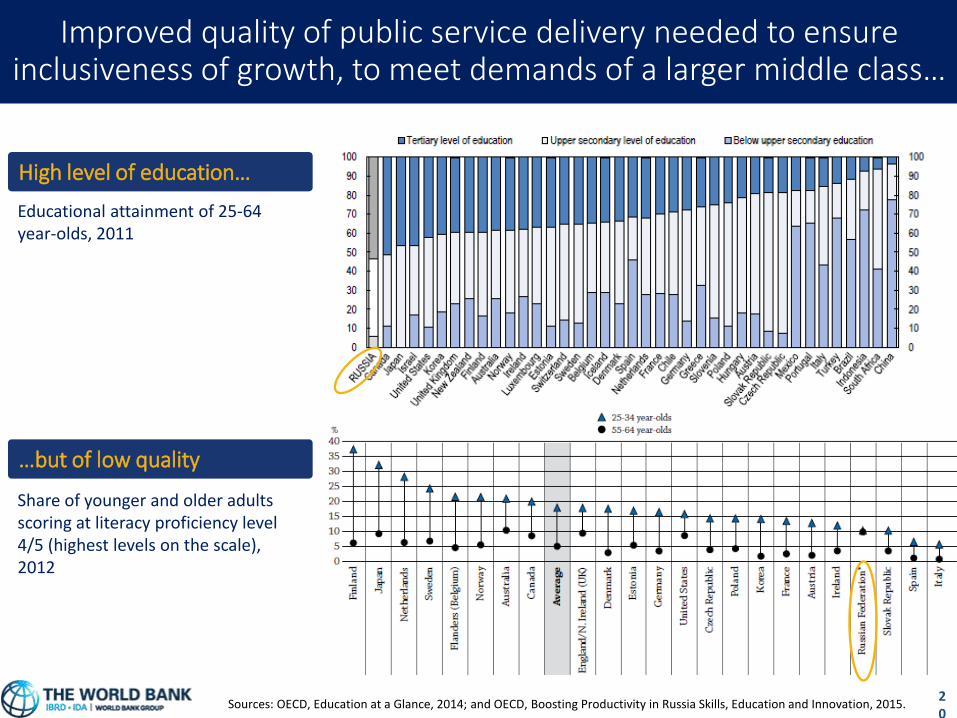

Improved quality of public service delivery needed to ensure inclusiveness of growth, to meet demands of a larger middle class…

Sources: OECD, Education at a Glance, 2014; and OECD, Boosting Productivity in Russia Skills, Education and Innovation, 2015.

High level of education…

…but of low quality

Educational attainment of 25-64 year-olds, 2011

Share of younger and older adults scoring at literacy proficiency level 4/5 (highest levels on the scale), 2012

21

…to lift constraints to employment growth, especially among SMEs…

The availability of skilled personnel is limited in Russia

Share of SMEs that have admitted to facing difficulties or barriers in finding skilled personnel in the last two years

Source: Demmou, L. and A. Wörgötter (2015), “Boosting Productivity in Russia: Skills, Education and Innovation”, OECDEconomics Department Working Papers, No. 1189, OECD Publishing.

22

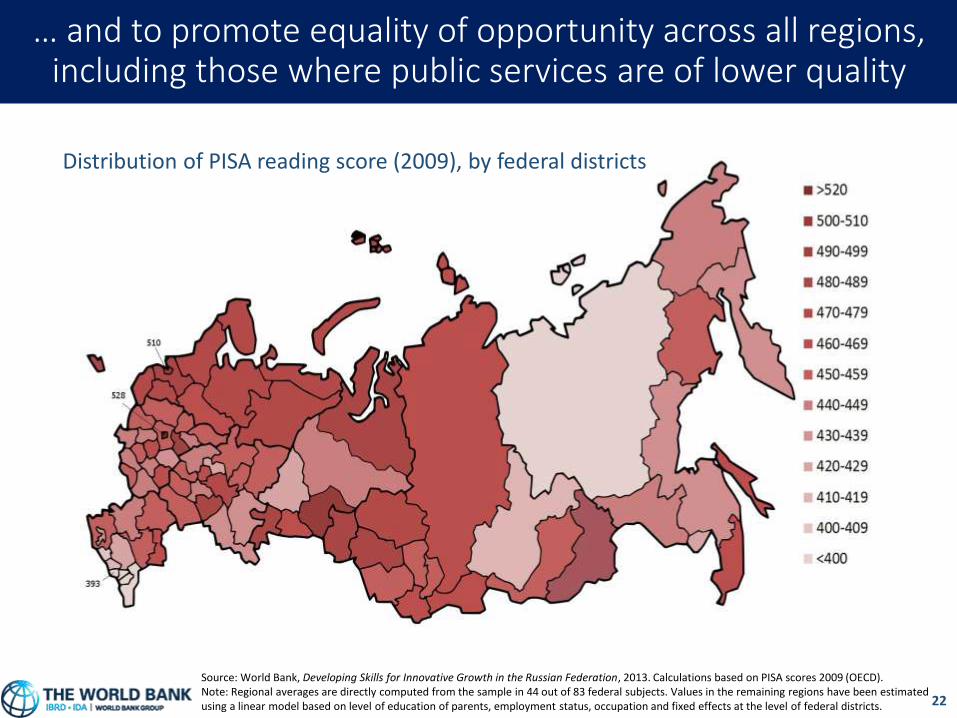

… and to promote equality of opportunity across all regions, including those where public services are of lower quality

Source: World Bank, Developing Skills for Innovative Growth in the Russian Federation, 2013. Calculations based on PISA scores 2009 (OECD).Note: Regional averages are directly computed from the sample in 44 out of 83 federal subjects. Values in the remaining regions have been estimated using a linear model based on level of education of parents, employment status, occupation and fixed effects at the level of federal districts.

Distribution of PISA reading score (2009), by federal districts

23

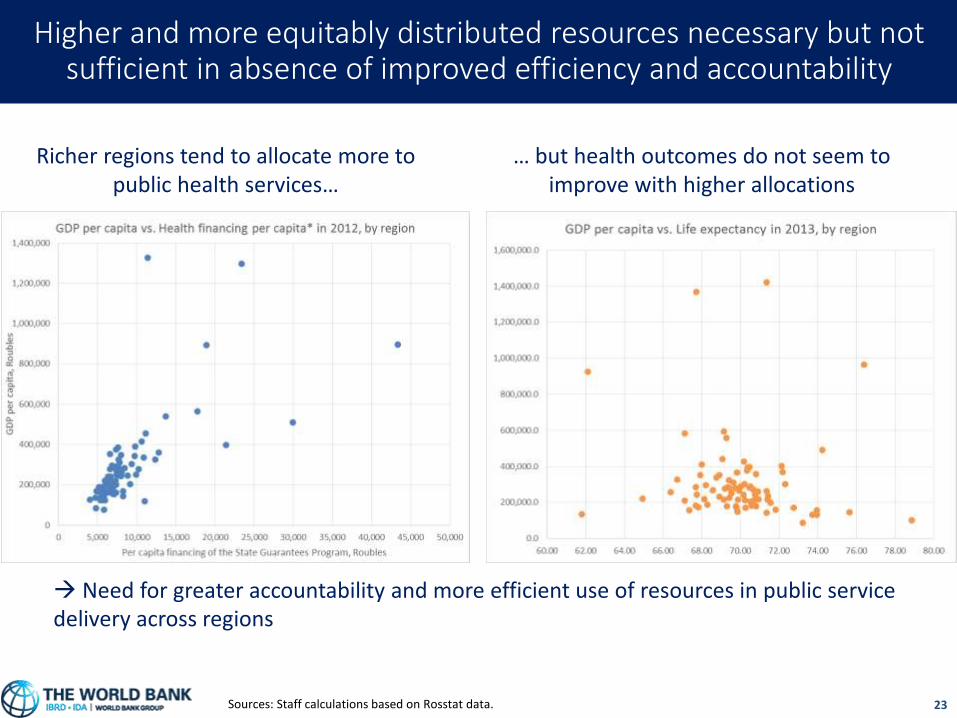

Higher and more equitably distributed resources necessary but not sufficient in absence of improved efficiency and accountability

Sources: Staff calculations based on Rosstat data.

Richer regions tend to allocate more to public health services…

… but health outcomes do not seem to improve with higher allocations

Need for greater accountability and more efficient use of resources in public service delivery across regions

24

Conclusion

Sustaining and deepening progress in income mobility will require:

Improving competitiveness, removing market distortions, and promoting non-oil private sector job creation;

Fostering effectiveness, accountability and responsiveness of public service delivery to needs and demands of several population groups (in terms of income, location etc.).

Thank you