Embed Size (px)

DESCRIPTION

Details about economic situation of India and a brief about Joseph Stiglitz

Citation preview

Name Specialization Roll Number

Akshay Wardhane Operations 37313

Bhavik Makwana Operations 37155

Mandeep Sandhu Operations 37204

Manoj Kankani Operations 37207

Karthik M Operations 37190

Gopi Krisha Madiraju Operations 37174

Pooja Deshpande Operations 37229

Chhavi Chauhan HR 37157

Macroeconomics

Assignment 1

Q1. Why Raghuram Rajan should reduce interest rates?

Acc. to the recent data released India's economic growth slowed to around 5.3% percent in the

three months to September, slipping from 5.7 percent in the previous quarter fuelling the need to

cut interest rates to achieve the level of growth the policy makers of India have been striving for

through introduction of recent pro-growth policies. High rates are stifling India’s growth by limiting

the resources required by the companies to build the high growth rate trajectory necessary to build

our economy and improve the lives

of one-third of the world’s extreme

poor living in India.

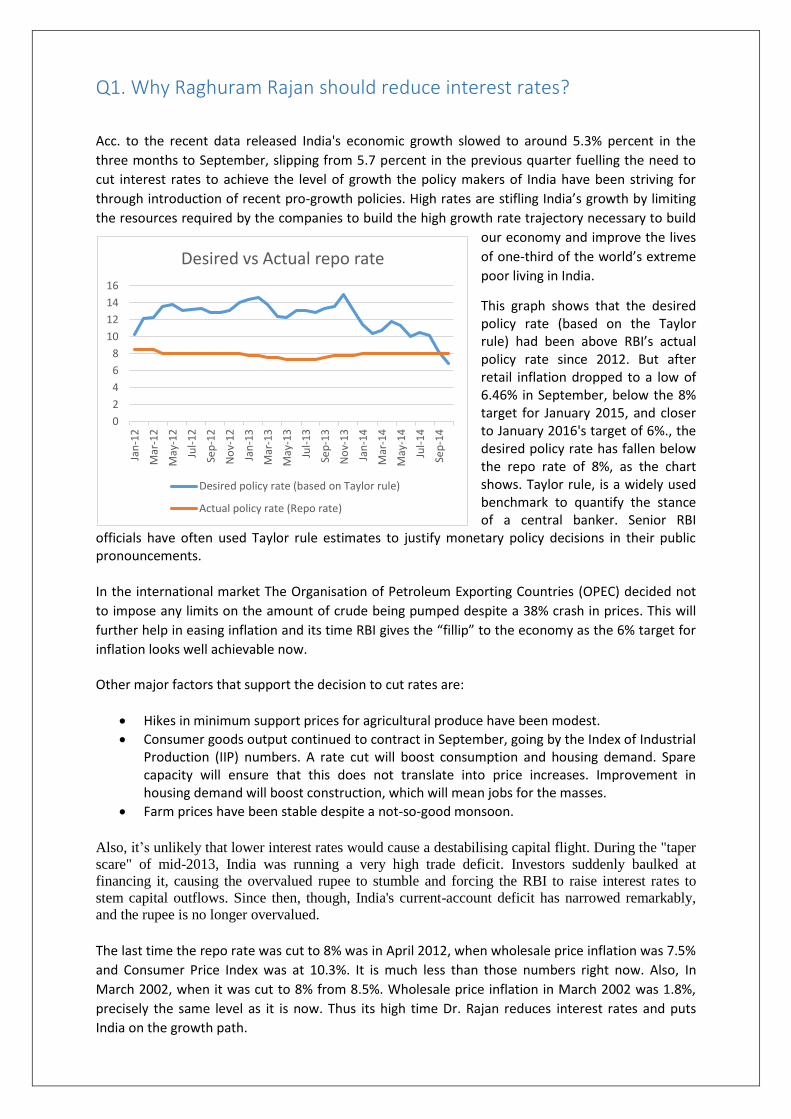

This graph shows that the desired policy rate (based on the Taylor rule) had been above RBI’s actual policy rate since 2012. But after retail inflation dropped to a low of 6.46% in September, below the 8% target for January 2015, and closer to January 2016's target of 6%., the desired policy rate has fallen below the repo rate of 8%, as the chart shows. Taylor rule, is a widely used benchmark to quantify the stance of a central banker. Senior RBI

officials have often used Taylor rule estimates to justify monetary policy decisions in their public pronouncements. In the international market The Organisation of Petroleum Exporting Countries (OPEC) decided not

to impose any limits on the amount of crude being pumped despite a 38% crash in prices. This will

further help in easing inflation and its time RBI gives the “fillip” to the economy as the 6% target for

inflation looks well achievable now.

Other major factors that support the decision to cut rates are:

Hikes in minimum support prices for agricultural produce have been modest.

Consumer goods output continued to contract in September, going by the Index of Industrial Production (IIP) numbers. A rate cut will boost consumption and housing demand. Spare capacity will ensure that this does not translate into price increases. Improvement in housing demand will boost construction, which will mean jobs for the masses.

Farm prices have been stable despite a not-so-good monsoon.

Also, it’s unlikely that lower interest rates would cause a destabilising capital flight. During the "taper

scare" of mid-2013, India was running a very high trade deficit. Investors suddenly baulked at

financing it, causing the overvalued rupee to stumble and forcing the RBI to raise interest rates to

stem capital outflows. Since then, though, India's current-account deficit has narrowed remarkably,

and the rupee is no longer overvalued.

The last time the repo rate was cut to 8% was in April 2012, when wholesale price inflation was 7.5%

and Consumer Price Index was at 10.3%. It is much less than those numbers right now. Also, In

March 2002, when it was cut to 8% from 8.5%. Wholesale price inflation in March 2002 was 1.8%,

precisely the same level as it is now. Thus its high time Dr. Rajan reduces interest rates and puts

India on the growth path.

0

2

4

6

8

10

12

14

16

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

Desired vs Actual repo rate

Desired policy rate (based on Taylor rule)

Actual policy rate (Repo rate)

Q.2 Why it is important to keep the interest rates high?

Pressure is mounting on Dr. Rajan, who has acquired a reputation as an ‘Inflation Warrior’ since he

took charge as the 23rd governor of the Reserve Bank of India (RBI). Dr. Rajan, given his Chicago

School moorings, was not expected to adopt a conservative approach. But it is exactly what he did; he

raised benchmark interest rates twice within the first two months and raised them yet again in January

2014.

But combating currency speculators and steadying the rupee was just the immediate priority; there

remained the larger problem of quelling inflation and helping the Centre to pursue its growth agenda.

This is where he took the battle against inflation to the next level by targeting CPI rather than WPI.

As the growth impulse returns in the economy, the RBI would then face the renewed threat of a

bouncing back of inflation.

Little would be achieved if the central bank reduces interest rates and

inflation shoots up as demand picks up, forcing RBI to cut interest rates

again. Also, the RBI governor will wait to see whether lower prices are

sustained. He's said before that it's important not to give up on monetary

tightening efforts until the inflation demon has been slain once and for all. It

would be prudent and beneficial for the economy in the long run to hold on

to interest rate for another quarter till inflation numbers are well under

control.

Retail inflation dropped to a low of 6.46% in September, below the

8% target for January 2015, and closer to target for January 2016 as

6%. But, the catch is that once the base effect fades, the measure

is expected to accelerate again in the first quarter of the next

year. In fact, the RBI model forecasts 7% retail inflation by March

2016, which may be revised lower if commodity prices keep falling.

Dr. Rajan substantiates his claims with appropriate data.

Inflation numbers have fallen mainly on account of a high base effect and low fuel and food

prices

Oil price are not in control of Indian government and could go up anytime

To some extent, food inflation is down on account of seasonal factors; the recent poor ‘kharif’

crop output can push up food inflation again.

The impact of the base effect would be reflected more accurately in the next quarter.

It is not just food prices that are persistently high but even those of other items which remain elevated,

and prices across the board have to come down to enable him to reduce

key rates.

Dr. Raghuram Rajan is facing pressure not only from the government,

industries and analysts but also from his colleagues at the central bank

who feel it is time for a rate cut. Four of the seven external members of

the RBI’s Technical Advisory Committee on Monetary Policy wanted a

rate cut at the last policy meet itself. He's been relentless in his bid to

tame prices, making inflation-targeting the main objective of monetary

policy. While this has won him admirers in the international investor

community and elsewhere, growth-hungry companies, believing he is

out of sync with reality.

“There is no point in cutting interest rates to see inflation pick-up again”, said Dr. Rajan.

“Inflation is high not only in food, but also in non-food items and the best solution for the country is to bring it down. Then I can cut interest rate”, said Dr. Rajan.

“When you do that

then we will do that,

we have no problem”,

said Dr. Rajan to the

bankers at a summit

organised by industry

body.

Q.3 Personality - Joseph Stiglitz

Joseph E. Stiglitz was born in Gary, Indiana in 1943. A

graduate of Amherst College, he received his PHD from

MIT in 1967.Stiglitz helped create a new branch of

economics, “The Economics of Information," exploring the

consequences of information asymmetries and pioneering

such pivotal concepts as adverse selection and moral hazard,

which have now become standard tools not only of theorists,

but also of policy analysts.

His most famous research was on screening, a technique

used by one economic agent to extract otherwise private information from another. It was for this

contribution to the theory of information asymmetry that he shared the Nobel Memorial Prize in

Economics in 2001 for laying the foundations for the theory of markets with asymmetric

information.Before the advent of models of imperfect and asymmetric information,

traditional economics literature had assumed that markets are efficient except for some limited and

well defined market failures.

He also did research on efficiency wages, and helped create what became known as the Shapiro-

Stiglitz model to explain why there is unemployment even in equilibrium, why wages are not bid

down sufficiently by job seekers so that everyone who wants a job finds one, and to question whether

the neoclassical paradigm could explain involuntary unemployment.Unlike other forms of capital,

humans can choose their level of effort.It is costly for firms to determine how much effort workers are

exerting.

He joined the Clinton Administration in 1993.His most important contribution in this period was

helping define a new economic philosophy, a "third way", which postulated the important, but

limited, role of government, that unfettered markets often did not work well, but that government was

not always able to correct the limitations of markets. The academic research that he had been

conducting over the preceding 25 years provided the intellectual foundations for this "third way".

He was approached by the World Bank to be its senior vice president for development policy and its

chief economist, and he assumed that position after his CEA successor was confirmed on February 13,

1997.

As the World Bank began its ten-year review of the transition of the former Communist countries to

the market economy it unveiled failures of the countries that had followed the International Monetary

Fund (IMF) shock therapy policies – both in terms of the declines in GDP and increases in poverty –

that were even worse than the worst that most of its critics had envisioned at the onset of the

transition. Clear links existed between the dismal performances and the policies that the IMF had

advocated, such as the voucher privatization schemes and excessive monetary stringency. Meanwhile,

the success of a few countries that had followed quite different strategies suggested that there were

alternatives that could have been followed. The U.S. Treasury had put enormous pressure on the

World Bank to silence his criticisms of the policies which they and the IMF had pursued.

In July 2000 Stiglitz founded the Initiative for Policy Dialogue (IPD), with support of the Ford,

Rockefeller, McArthur, and Mott Foundations and the Canadian and Swedish governments, to

enhance democratic processes for decision-making in developing countries and to ensure that a

broader range of alternatives are on the table and more stakeholders are at the table.

At the beginning of 2008, he chaired the Commission on the Measurement of Economic Performance

and Social Progress, also known as the Stiglitz-Sen-Fitoussi Commission, initiated by President

Sarkozy of France.

Stiglitz chaired the Commission of Experts on Reforms of the International Monetary and Financial

System to review the workings of the global financial system, including major bodies such as the

World Bank and the IMF, and to suggest steps to be taken by Member States to secure a more

sustainable and just global economic order".

He has published over 300 technical articles, He is the author of books on issues from patent law to

abuses in international trade. Some of his books include

The Price of Inequality

In The Price of Inequality lays out a comprehensive agenda to create a more dynamic economy and

fairer and more equal society

Freefall

Discusses the causes of the 2008 recession/depression and goes on to propose reforms needed to avoid

a repetition of a similar crisis, advocating government intervention and regulation in a number of

areas.

The Roaring Nineties

Based on the boom and bust of the 1990s. Presented from an insider's point of view, firstly as chair of

President Clinton's Council of Economic Advisors, and later as chief economist of the World Bank.

Q.4 Book Review: Freakonomics – Chapter 3

References:

o Book: Freakonomics – Chapter 3

(Why do drug dealers still live with their moms?)

o TedEx Talk: Steven Levitt - The freakonomics of crack dealing

(http://www.ted.com/talks/steven_levitt_analyzes_crack_economics?language=en)

The book starts with asking the right questions, ‘Conventional

Wisdom’ and then the authors jump to the homelessness in the U.S.

As per the findings of Mr. Mitch Snyder, as wrong as that math was;

one in a hundred extrapolated to 1/3rd of the U.S. population would

die every year. The authors highlight the use and need of ‘Creative

Lying’; with the example of ‘Listerine’ as a surgical antiseptic, later a

floor cleaner and then a mouthwash! They also throw a light on the

positive and negative media publicities and title the journalists as the

‘Expert Architects’ of the conventional wisdom.

Then the authors jump to 1990, when the police of Atlanta

underreported the crime numbers so as to host the 1996’s Olympics.

Nevertheless, 1990’s was the exact time when the drug dealers had

cash and weapons and the media quoted crack dealing as the most

profitable job.*

*Crack cocaine – Softer version of cocaine or as Mr. Steven Levitt quotes the simile, “As extra

chunky version of tomato sauce”

Then the authors introduce the protagonists, Mr. Sudhir Venkatesh, who in 1989 (apparently the year

most of us were born) started his Ph.D. in sociology under William Wilson, who sent Mr. Sudhir with

a questionnaire with 70 questions in the black neighborhood; that dealt in crack dealing. The mindset

behind the crack dealing was to keep the black money in the black community. The story unfolds as

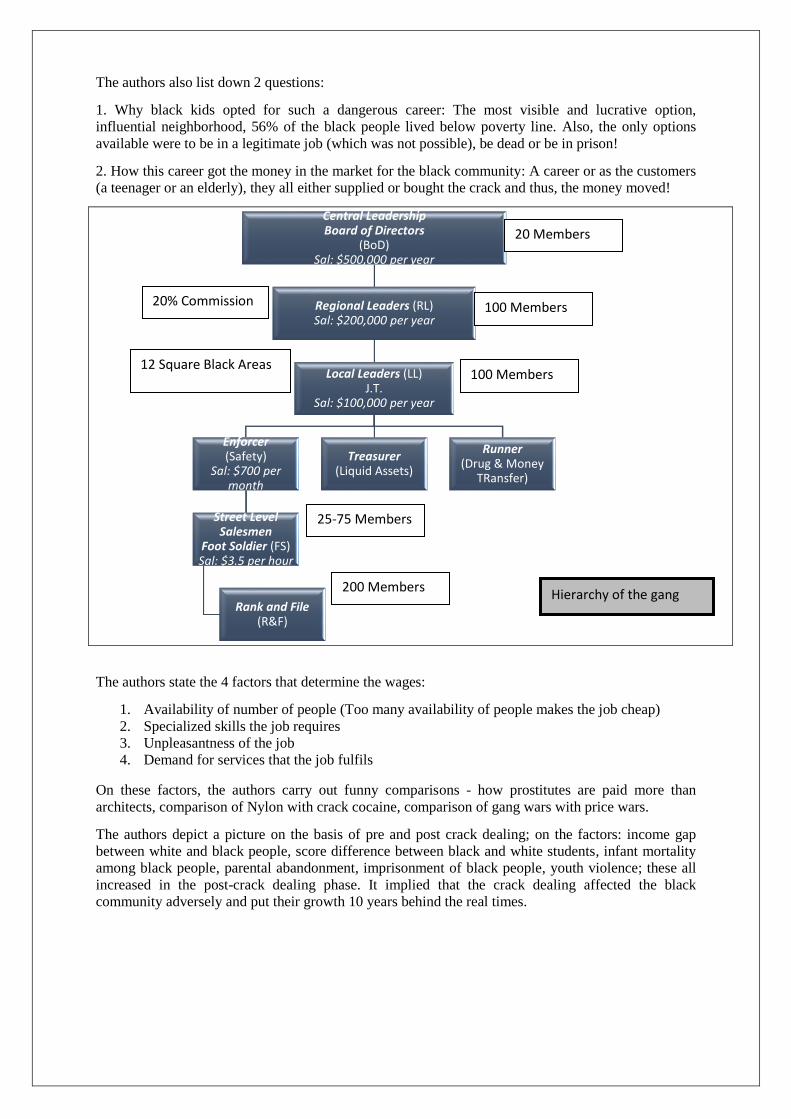

Mr. Booty (gang member) shares the financial transactions book ‘Black Disciples’, the gang. It

comprised complete data on sales, wages, dues, death benefits paid to the families of murdered

members, for all 4 years.

The authors also compare the organization of the gang with that of the McDonald’s. The authors also

mention the fear of community or backlash by the community. However, the discrepancy in the wage

levels, the top 2.2% i.e. 120 people were paid half of the money and the rest 97.8% i.e. 5335 people

were paid the rest of the half money put forth the typical ‘Capitalist Enterprise’ scenario. Also, chance

of getting killed being 25% in 4 years (7% per year) i.e. being the most dangerous job and the less

than minimum wages of $3.5 per hour, made it clear that it was a rat race for being at the top and

earning fortune only at the end of the hierarchy.

However, the increase in the danger was compensated by the more money paid. It reminds me of the

concept of 'Compensating Wage Differential' i.e. the additional amount of income given to the

workers in order to motivate them to accept a given undesirable job. The authors state the importance

of shooting for the Foot Soldiers since it meant making a name which in turn would help in rising up

in the hierarchy. But J.T. never supported shooting since that meant loss of business and more

compensation!

The authors also list down 2 questions:

1. Why black kids opted for such a dangerous career: The most visible and lucrative option,

influential neighborhood, 56% of the black people lived below poverty line. Also, the only options

available were to be in a legitimate job (which was not possible), be dead or be in prison!

2. How this career got the money in the market for the black community: A career or as the customers

(a teenager or an elderly), they all either supplied or bought the crack and thus, the money moved!

The authors state the 4 factors that determine the wages:

1. Availability of number of people (Too many availability of people makes the job cheap)

2. Specialized skills the job requires

3. Unpleasantness of the job

4. Demand for services that the job fulfils

On these factors, the authors carry out funny comparisons - how prostitutes are paid more than

architects, comparison of Nylon with crack cocaine, comparison of gang wars with price wars.

The authors depict a picture on the basis of pre and post crack dealing; on the factors: income gap

between white and black people, score difference between black and white students, infant mortality

among black people, parental abandonment, imprisonment of black people, youth violence; these all

increased in the post-crack dealing phase. It implied that the crack dealing affected the black

community adversely and put their growth 10 years behind the real times.

Central LeadershipBoard of Directors

(BoD)Sal: $500,000 per year

Regional Leaders (RL)Sal: $200,000 per year

Local Leaders (LL)J.T.

Sal: $100,000 per year

Enforcer(Safety)

Sal: $700 per month

Street Level Salesmen

Foot Soldier (FS)Sal: $3.5 per hour

Rank and File(R&F)

Treasurer(Liquid Assets)

Runner(Drug & Money

TRansfer)

20% Commission

12 Square Black Areas

100 Members

100 Members

25-75 Members

200 Members

20 Members

Hierarchy of the gang