Embed Size (px)

Citation preview

Inefficiencies of Income Protection

Petrie MarxProduct Actuary - Sanlam

Efficiencies of Income Protection

Petrie MarxProduct Actuary - Sanlam

Myths around Income Protection

Petrie MarxProduct Actuary - Sanlam

Agenda• Why consider Income Protection?• Myth no.1: The IP market is Inefficient• Myth no.2: Income Protection is complex• Myth no.3: Income Protection is expensive• Myth no.4: “Under-insurance” is penalised• Myth no.5: Showing loss of income is onerous• Myth no.6: (Sadly) IP-contributions will remain

tax-deductible – an update • Conclusion

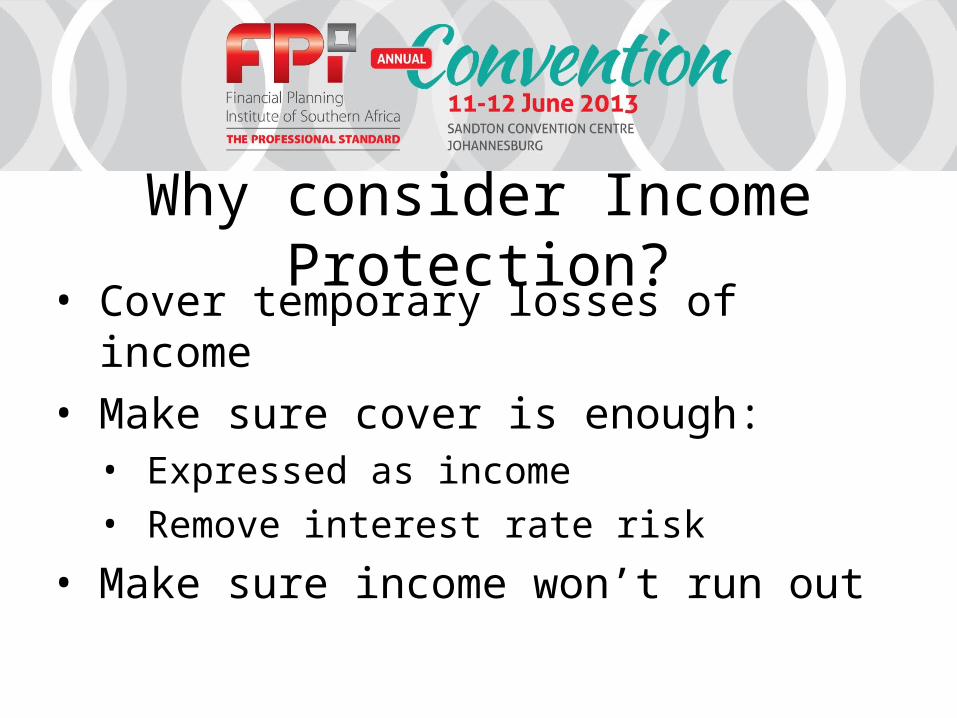

Why consider Income Protection?• Cover temporary losses of income• Make sure cover is enough:

• Expressed as income• Remove interest rate risk

• Make sure income won’t run out

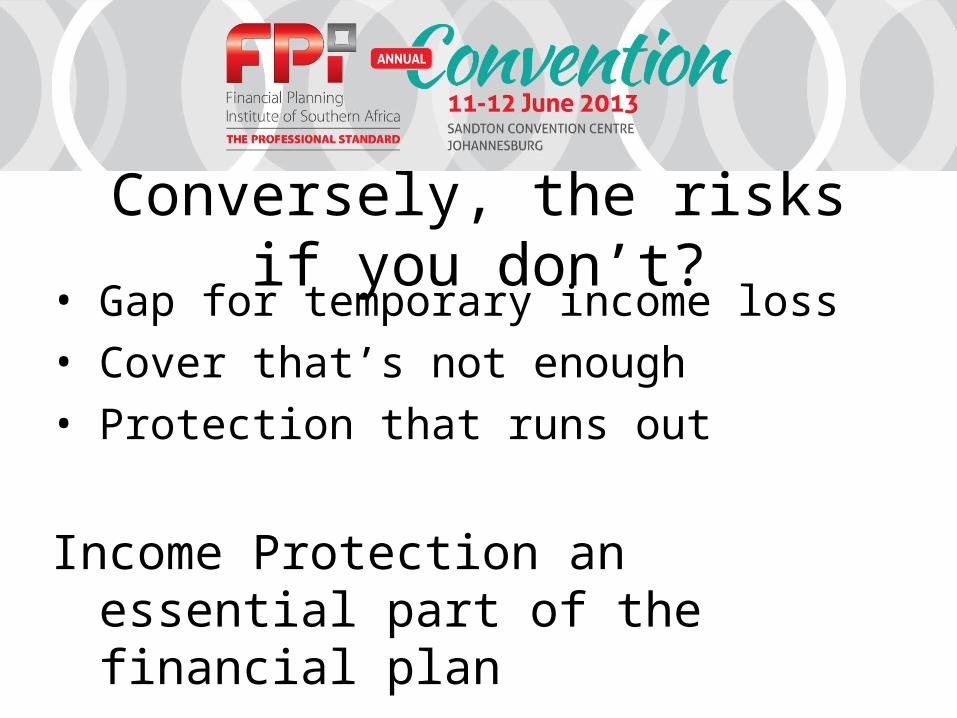

Conversely, the risks if you don’t?• Gap for temporary income loss• Cover that’s not enough• Protection that runs out

Income Protection an essential part of the financial plan

But is the IP market inefficient?

Agree with most observations:• Disability (and IP in particular) under-sold vs.

Death cover• Dread disease over-sold relative to Disability and

IP• Within disability:

• Permanent disability protection over-sold vs. temporary disability protection

• But disagree that the reason is an INEFFICIENT MARKET

Definition of inefficient market• The market prices of stocks/securities are not

always accurately priced and tend to deviate from true value• E.g. low-volume OTC stocks comprise inefficient

market compared to blue chips• Not all information reflected

An inefficient market can create opportunity!

Inefficient market for consumer goods• Consumers pay high prices … • For poor quality products• Concentration of suppliers• Concentration of buyers• Asymmetry of information• Onerous tax / regulation• Unequal incentives• Ineffective distribution / advice

I doubt it, but that’s why we are here!

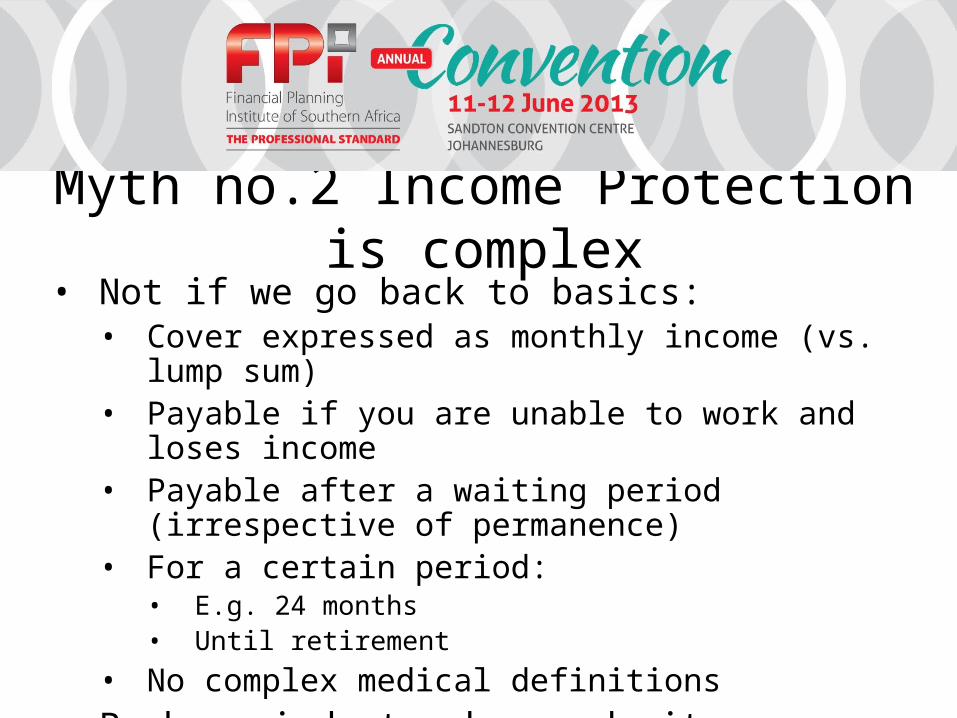

Myth no.2 Income Protection is complex• Not if we go back to basics:

• Cover expressed as monthly income (vs. lump sum)• Payable if you are unable to work and loses income• Payable after a waiting period (irrespective of permanence)• For a certain period:

• E.g. 24 months• Until retirement

• No complex medical definitions• Perhaps industry has made it unnecessarily complex?

• Impairment criteria, underpins, even guaranteed durations

Myth no.3 Income Protection is expensive• Consider male, non-smoker age 35 next birthday,

R25000 income, with CPI growth:• 1-month waiting period: around R525• 6-month waiting period: around R420

• For R420 he can also buy around R2.4m lump sum disability, but how valuable is that? (4% real interest)

• Over 30 years: around R12 000 p.m.• Over 20 years: around R15 000 p.m.• Over 10 years: around R25 000 p.m.

• For disability at young age: IP more cost-effective

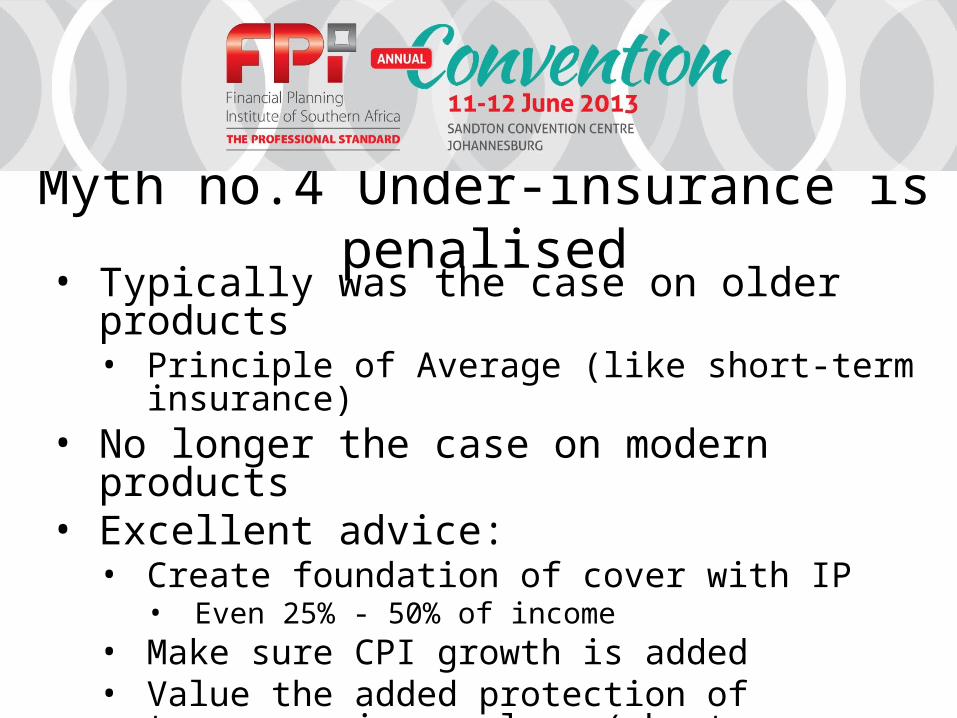

Myth no.4 Under-insurance is penalised• Typically was the case on older products

• Principle of Average (like short-term insurance)• No longer the case on modern products• Excellent advice:

• Create foundation of cover with IP• Even 25% - 50% of income

• Make sure CPI growth is added• Value the added protection of temporary income loss

(shorter waiting periods)• Combine with lump sum disability cover

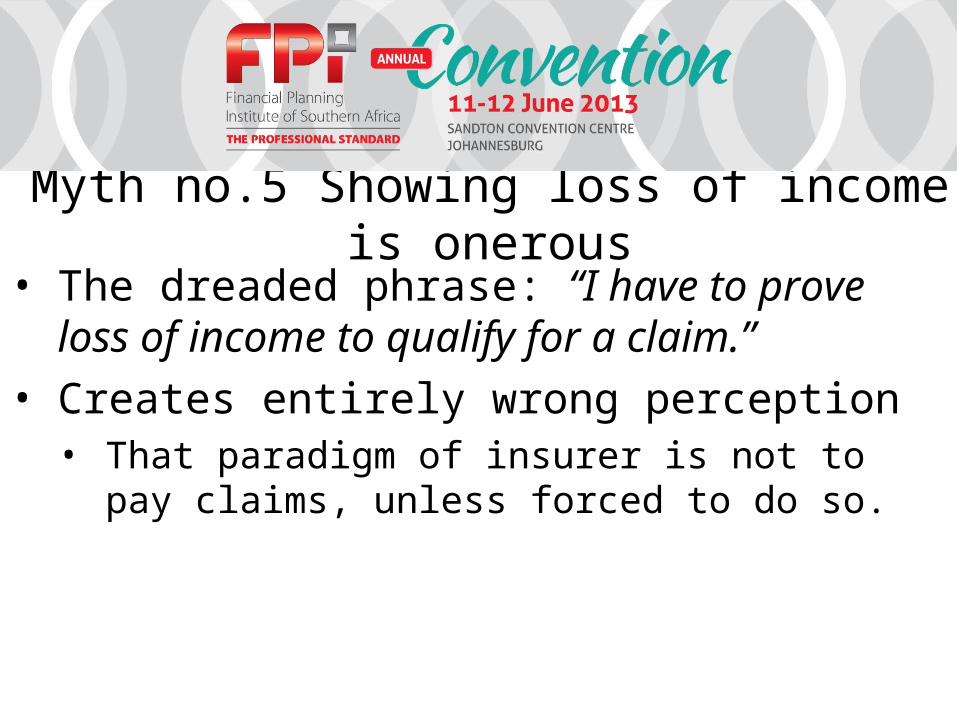

Myth no.5 Showing loss of income is onerous• The dreaded phrase: “I have to prove loss of

income to qualify for a claim.”• Creates entirely wrong perception

• That paradigm of insurer is not to pay claims, unless forced to do so.

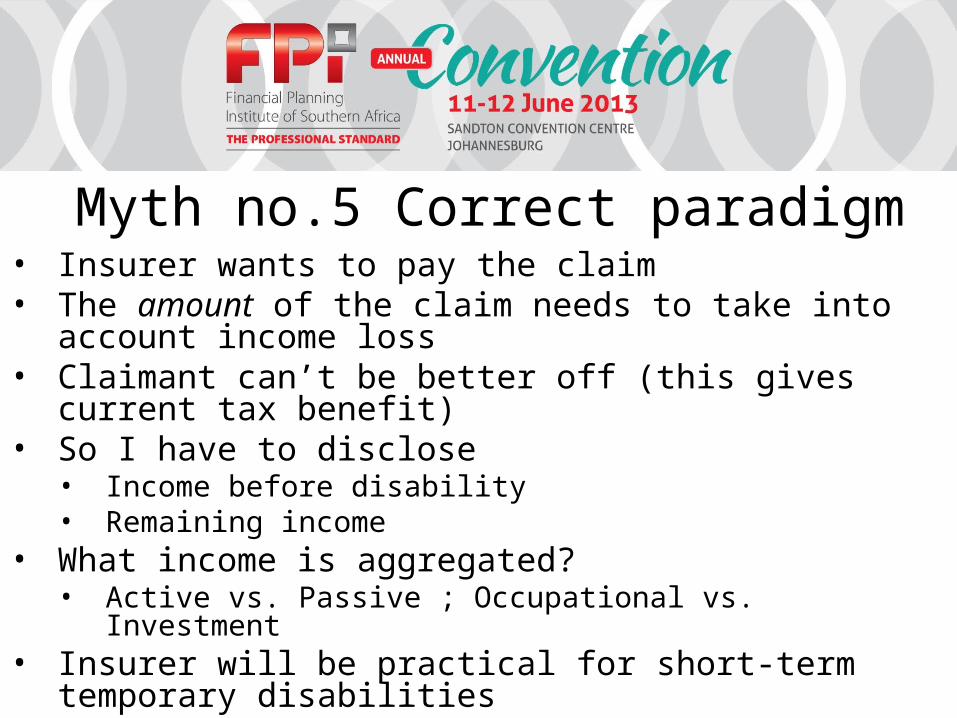

Myth no.5 Correct paradigm• Insurer wants to pay the claim• The amount of the claim needs to take into account income loss• Claimant can’t be better off (this gives current tax benefit)• So I have to disclose

• Income before disability• Remaining income

• What income is aggregated?• Active vs. Passive ; Occupational vs. Investment

• Insurer will be practical for short-term temporary disabilities• For longer-term disabilities not a problem• Alternative Sickness-benefits & longer term impairment

products are available (but different tax treatment)

6. Update on current taxation debate• The industry has been playing with fire• Created excellent products

• But wrongfully positioned it as as tax-efficient as Income Protection• Budget announcement• Industry in a frenzy – submitted response to Treasury• Treasury seems adamant

• Can no longer distinguish between capital and income protection products• Not their responsibility to give tax-advantages to capital/enrichment

products• Sadly everyone will be “penalised”• Including employee scheme / group risk products

• Transition arrangements uncertain• Products may change even more in future

• More innovation, but how will affordability be impacted?

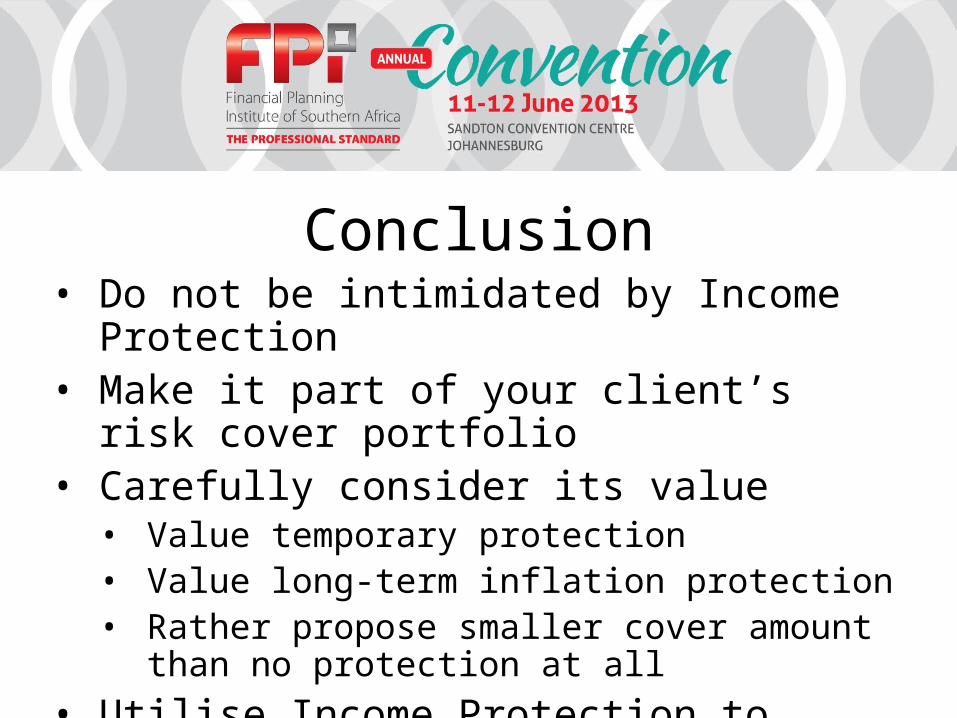

Conclusion• Do not be intimidated by Income Protection• Make it part of your client’s risk cover portfolio• Carefully consider its value

• Value temporary protection• Value long-term inflation protection• Rather propose smaller cover amount than no

protection at all• Utilise Income Protection to close the Disability

Gap

Thank you