Embed Size (px)

Citation preview

INSURANCEINSURANCEINDUSTRYINDUSTRY

FRAUDFRAUD

COPYRIGHT © 2006CLIENTELL CONTINUING EDUCATION

A Member of the Success CE Family of Companies

ClienTell Continuing Education2 Corporate Plaza Drive, Suite 100 Newport Beach, CA 92660

Office: (949) 706-9425

Copyright 2006, ClienTell Continuing Education. A Member of the Success CE Family of Companies

All Rights Reserved. No part of this publication may be used or reproduced in any form or by anymeans, transmitted in any form or by any means, electronic or mechanical, for any purpose, without

the express written permission of American Safety Council, Inc. This publication is designed toprovide general information on the seminar topic presented. It is sold with the understanding that the

publisher is not engaged in rendering any legal or professional services. Although professionalsprepared this seminar, it should not be used as a substitute for professional services. If legal or other

professional advice is required, the services of a professional should be sought.

TTABLEABLE OFOF C CONTENTSONTENTS CHAPTER 1....................................................................................................................................1

HISTORY OF FRAUD...............................................................................................................1HUMBLE BEGINNINGS.....................................................................................................................1

THE INITIAL STAGES OF FRAUD...........................................................................................................1JUST WHAT IS FRAUD ANYWAY?..................................................................................................2WHO HAS THE POTENTIAL?...........................................................................................................3FINANCIAL INSTITUTION FRAUD...................................................................................................4

CHAPTER 2....................................................................................................................................5

AUTOMOBILE INSURANCE FRAUD.....................................................................................5IT’S THE LAW....................................................................................................................................5FRAUD “CREATIVITY” IN THE AUTO INDUSTRY..........................................................................6

AUTOMOBILE CLONING......................................................................................................................6REGULATION OF TOWING COMPANIES...................................................................................................7TRANSFER OF TITLE.........................................................................................................................7AIRBAG THEFT................................................................................................................................8ACCIDENT STAGING CAR RINGS.........................................................................................................8CAR JACKING RINGS........................................................................................................................9

HIGHEST THEFT CLAIMS 2000-2002 MODEL VEHICLES.............................................................10TOP VEHICLE THEFTS BY YEAR, MAKE AND MODEL 2002.......................................................10

CHAPTER 3....................................................................................................................................12HEALTH INSURANCE FRAUD................................................................................................................12

THE PHYSICS OF FRAUD.................................................................................................................12IT’S THE LAW....................................................................................................................................13HEALTH CARE RELATED FRAUD...................................................................................................13PUTTING HEALTH CARE FRAUD INTO PERSPECTIVE................................................................14

PHARMACY SCAMS...........................................................................................................................14CHIROPRACTIC................................................................................................................................14HEALTH CARE INSTITUTIONS...............................................................................................................15COSMETIC SURGERY.........................................................................................................................15INSURANCE CARRIER FRAUD..............................................................................................................15MEDICAL EQUIPMENT FRAUD..............................................................................................................15MEDICARE AND MEDICAID SYSTEMS.....................................................................................................15

CASE INFORMATION BY THE DEPARTMENT OF JUSTICE.........................................................16

CHAPTER 4....................................................................................................................................18

WORKER’S COMPENSATION FRAUD..................................................................................18IT’S THE LAW....................................................................................................................................18TYPES OF WORKERS’ COMPENSATION FRAUD.........................................................................19

PROVIDER FRAUD............................................................................................................................19CLAIMANT FRAUD............................................................................................................................19PREMIUMS FRAUD............................................................................................................................20

TROUBLE–SHOOTING METHODS..................................................................................................21THE EMPLOYEE...............................................................................................................................21THE WORKPLACE............................................................................................................................21THE INJURY....................................................................................................................................21THE MEDICAL RELATIONSHIP..............................................................................................................22

THE CLAIM AND THE CLAIMANT’S ATTORNEY.........................................................................................22OTHER ACTIVITIES...........................................................................................................................22THE SOCIAL SECURITY ADMINISTRATION...............................................................................................23SSA AND OIG “ZERO TOLERANCE FOR FRAUD” PLAN..........................................................................25MEDICAID HOSPICE..........................................................................................................................25

CHAPTER 5....................................................................................................................................27

UNAUTHORIZED ENTITIES...................................................................................................27THE LURE OF LOW PREMIUM RATES...........................................................................................27

FRAUDULENT DISCOUNT HEALTH PLANS...............................................................................................27AVOID FRAUDULENT UNFAIR RATING PRACTICES....................................................................................28FALSIFYING STATE INSURANCE REGULATION EXEMPTIONS.........................................................................29

CHAPTER 6....................................................................................................................................30

IDENTITY THEFT.....................................................................................................................30IDENTITY THEFT AND IDENTITY FRAUD.......................................................................................30

DUMPSTER DIVING...........................................................................................................................30SHOULDER SURFING.........................................................................................................................30SKIMMING.......................................................................................................................................31“PHISHING” AND WEBSITE SPOOFING..................................................................................................31MINIMIZING THE RISK........................................................................................................................32

CHAPTER 7....................................................................................................................................34

OTHER TYPES OF FRAUD......................................................................................................34THE BUSINESS OF INSURANCE.....................................................................................................34INTRINSIC FRAUD.............................................................................................................................34INVESTMENT FRAUD.......................................................................................................................35PERFORMANCE SKIMMING.............................................................................................................35INVESTMENT ADVISOR KICKBACKS.............................................................................................35EXCESSIVE RISK..............................................................................................................................36ARSON...............................................................................................................................................36REGULATION OF PUBLIC ADJUSTERS ........................................................................................37UNLAWFUL TRANSACTIONS BY UNLICENSED PERSONS.........................................................37THE USE OF “RUNNERS”................................................................................................................37LIFE INSURANCE FRAUD SCAMS..................................................................................................37ATTORNEY FRAUD...........................................................................................................................38BROKERS FRAUD.............................................................................................................................38MONEY LAUNDERING......................................................................................................................38TELEMARKETING FRAUD................................................................................................................39

CHAPTER 8....................................................................................................................................40

THE RALLY AGAINST FRAUD..............................................................................................40ANTI-FRAUD EFFORTS....................................................................................................................40

INSURERS’ FRAUD MEASURES.............................................................................................................40PUBLIC RESPONSIBILITY....................................................................................................................42

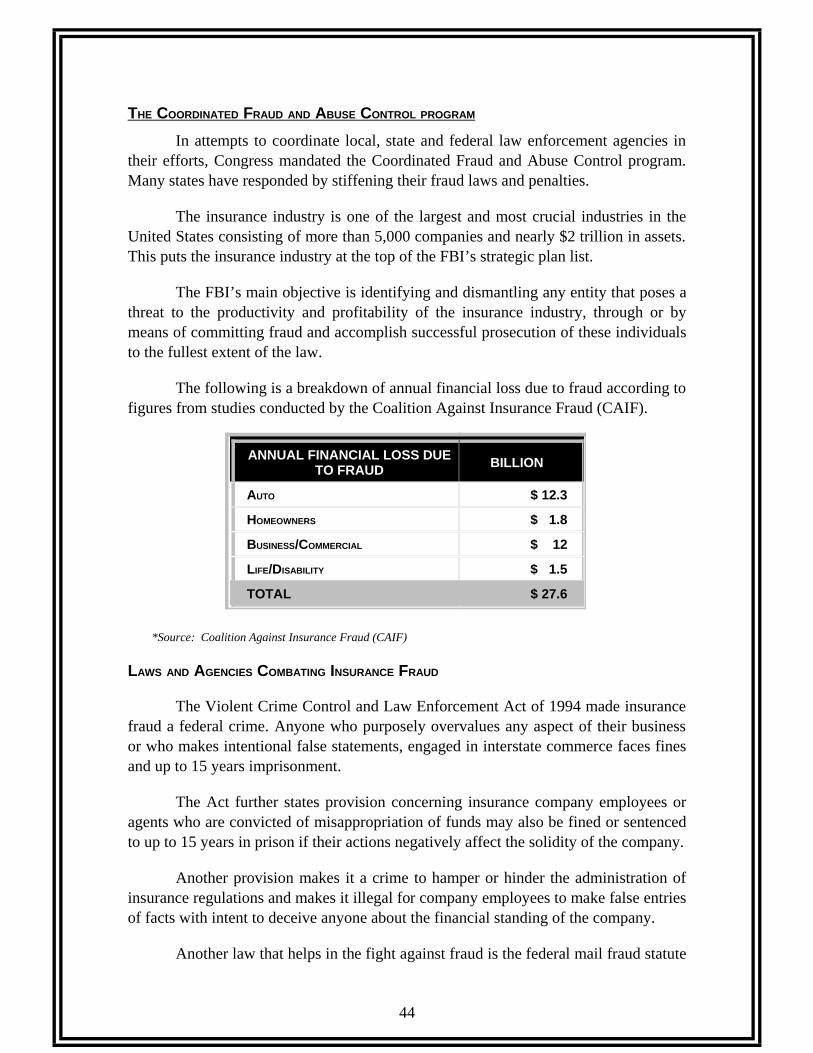

ON THE FEDERAL LEVEL................................................................................................................43THE CORPORATE FRAUD TASK FORCE.................................................................................................43THE COORDINATED FRAUD AND ABUSE CONTROL PROGRAM.....................................................................44LAWS AND AGENCIES COMBATING INSURANCE FRAUD..............................................................................44THE FEDERAL RACKETEER INFLUENCE AND CORRUPT ORGANIZATIONS ACT..................................................45A BRIEF HISTORY OF THE OFFICE OF THE INSPECTOR GENERAL (OIG).......................................................46THE PRESIDENT’S COUNCIL ON INTEGRITY AND EFFICIENCY.......................................................................47

THE HEALTH INSURANCE PORTABILITY ACCOUNTABILITY ACT....................................................................47ON THE STATE LEVEL......................................................................................................................48

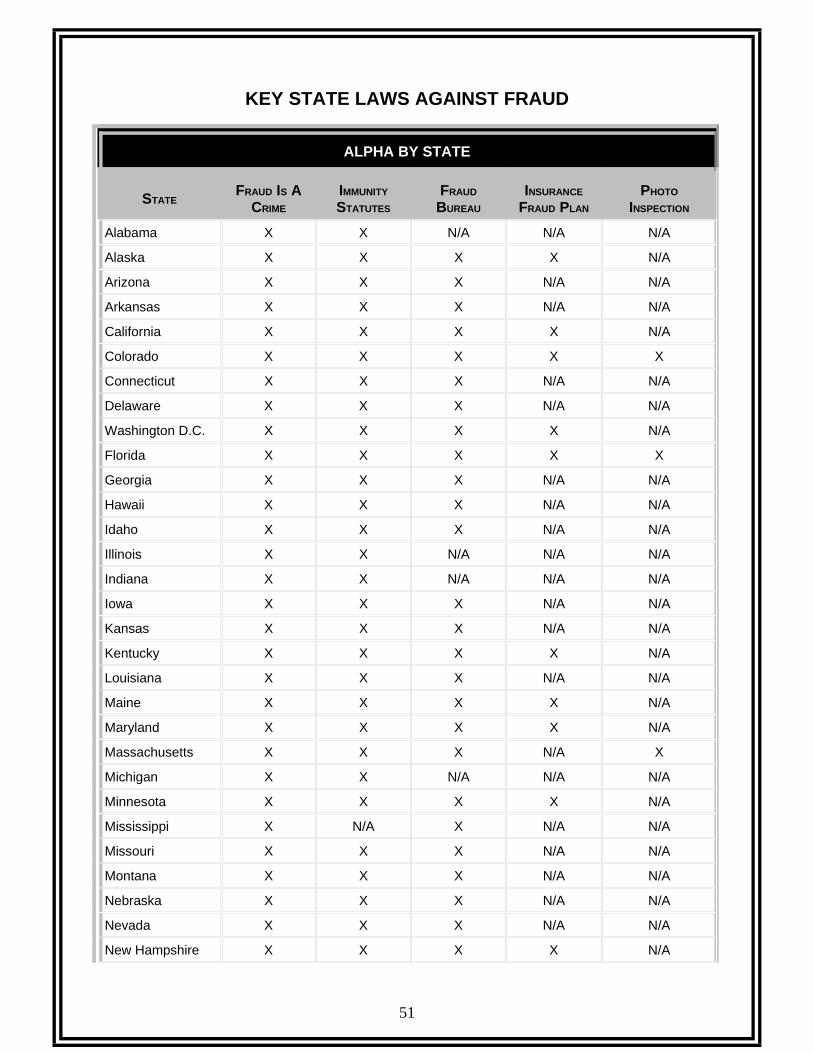

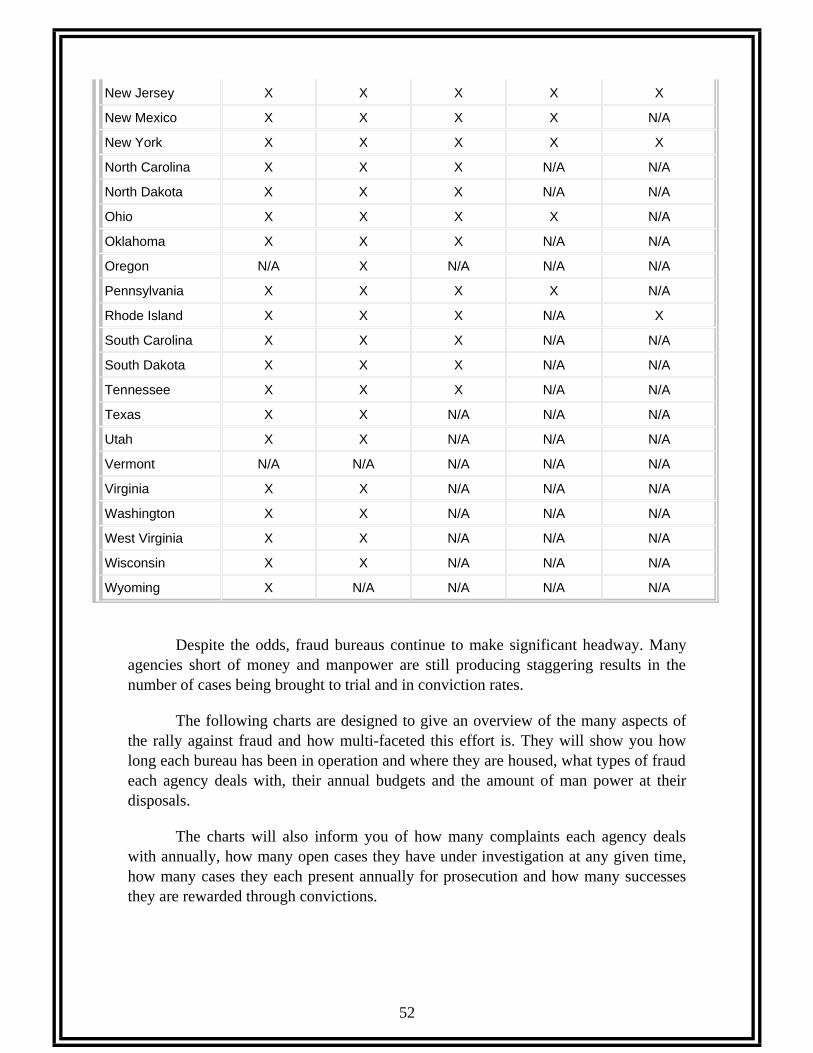

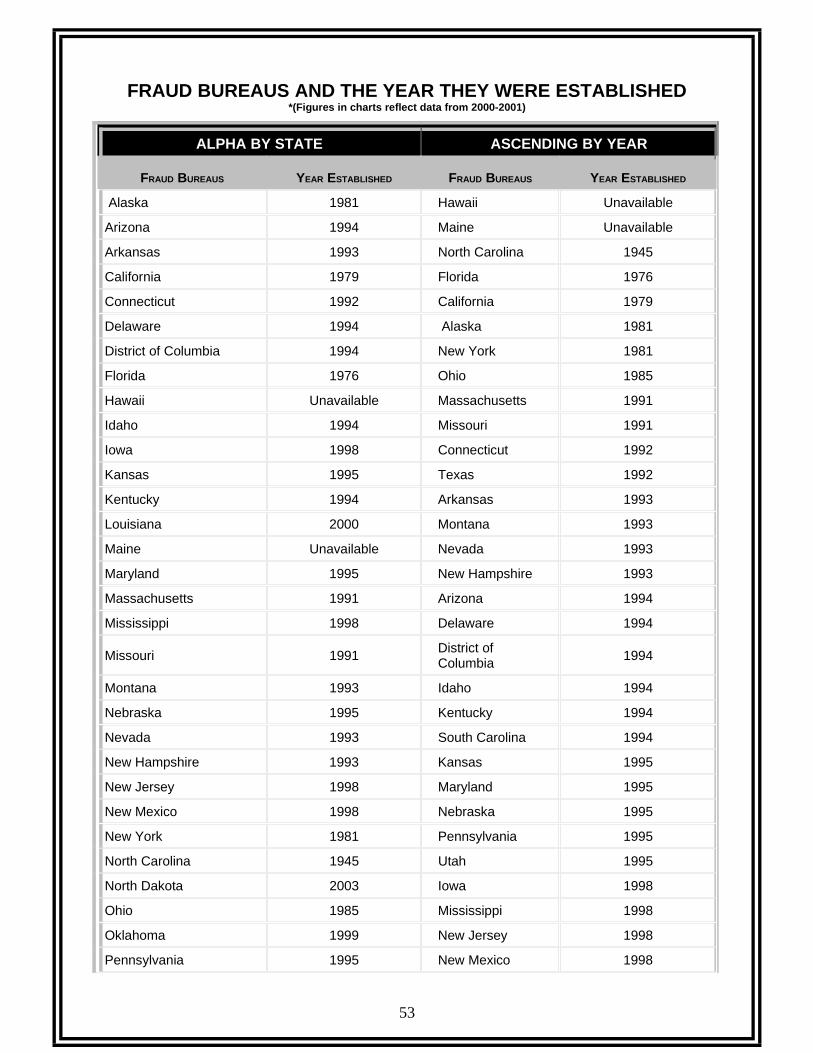

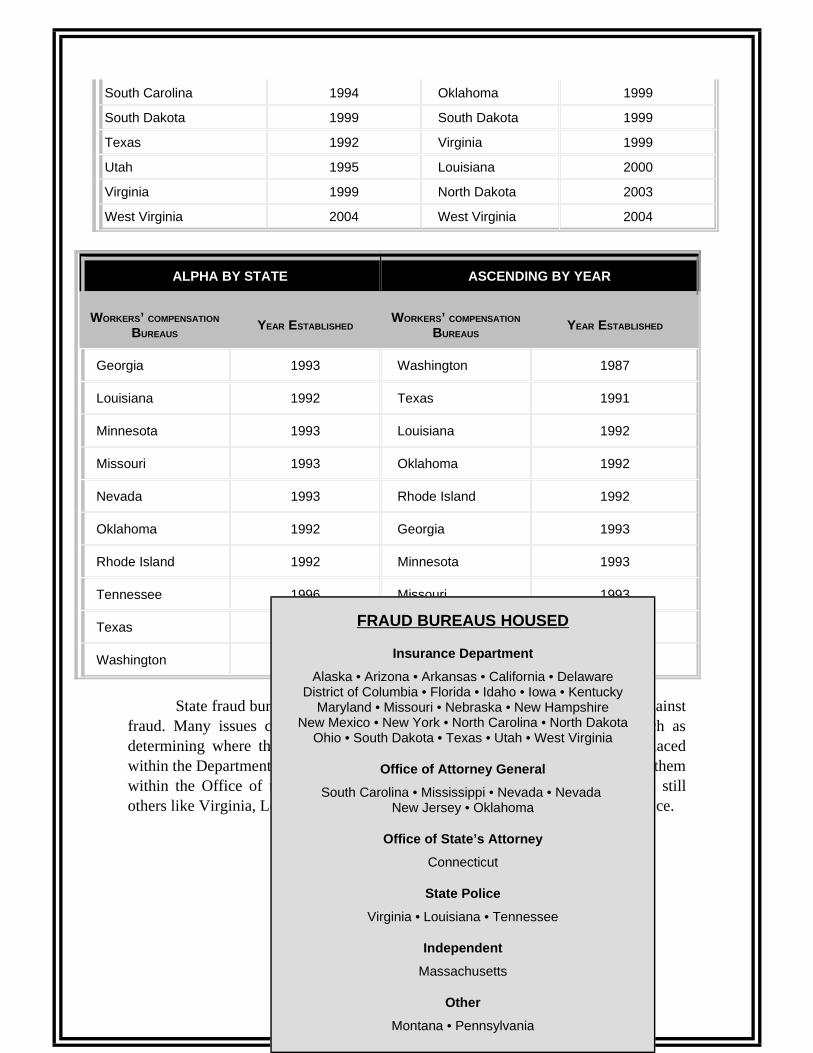

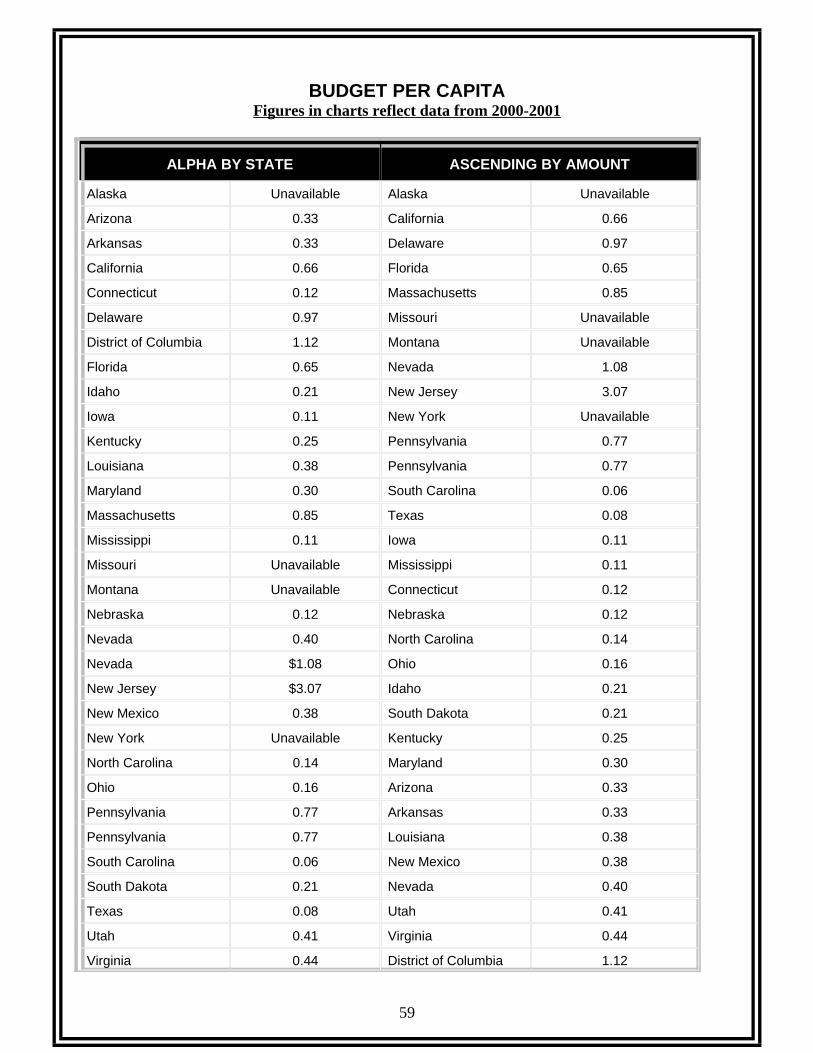

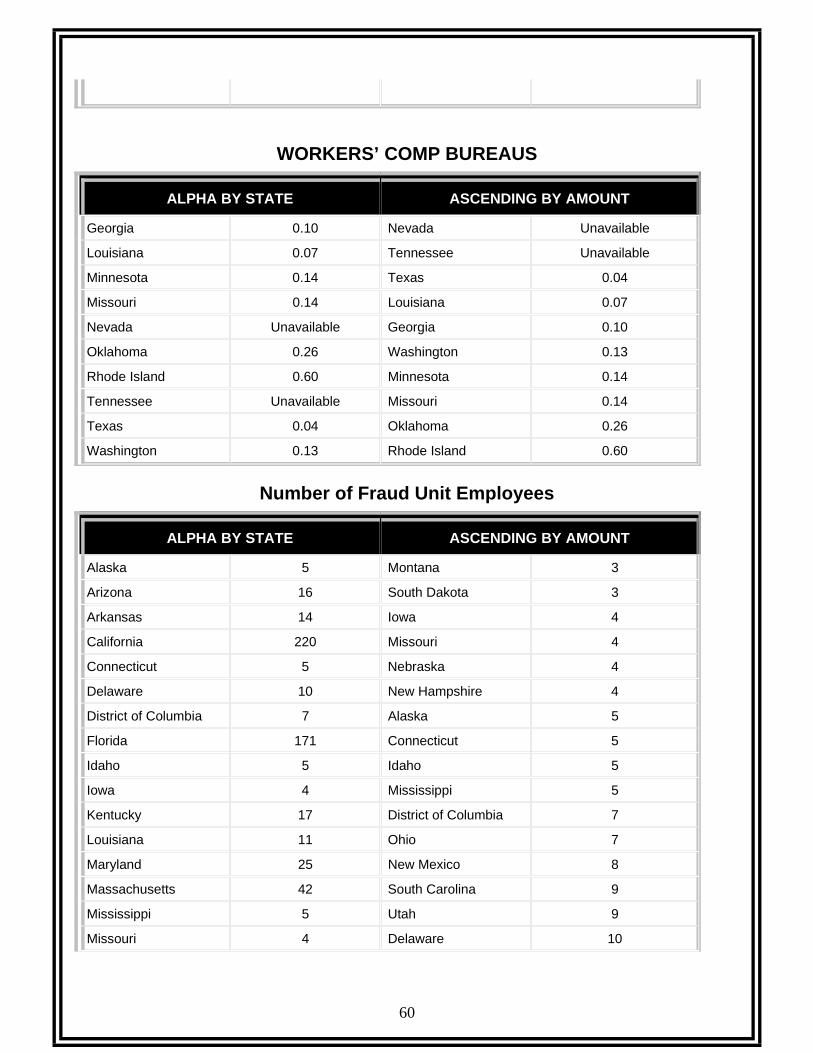

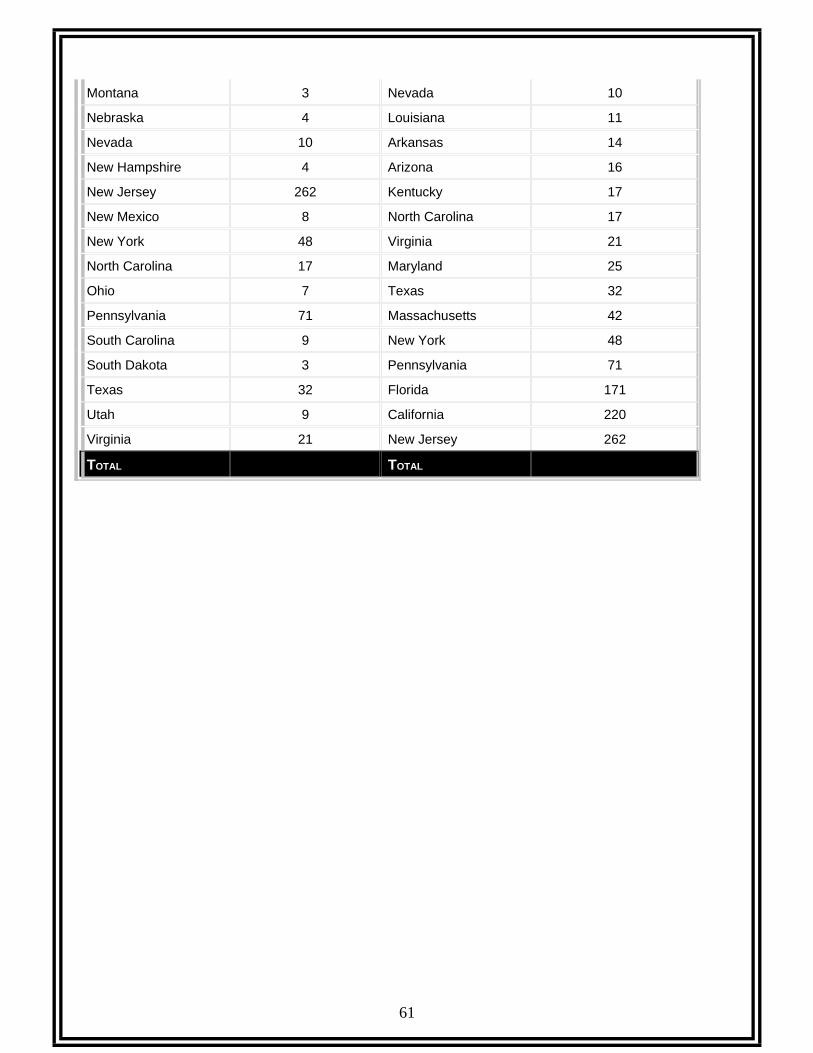

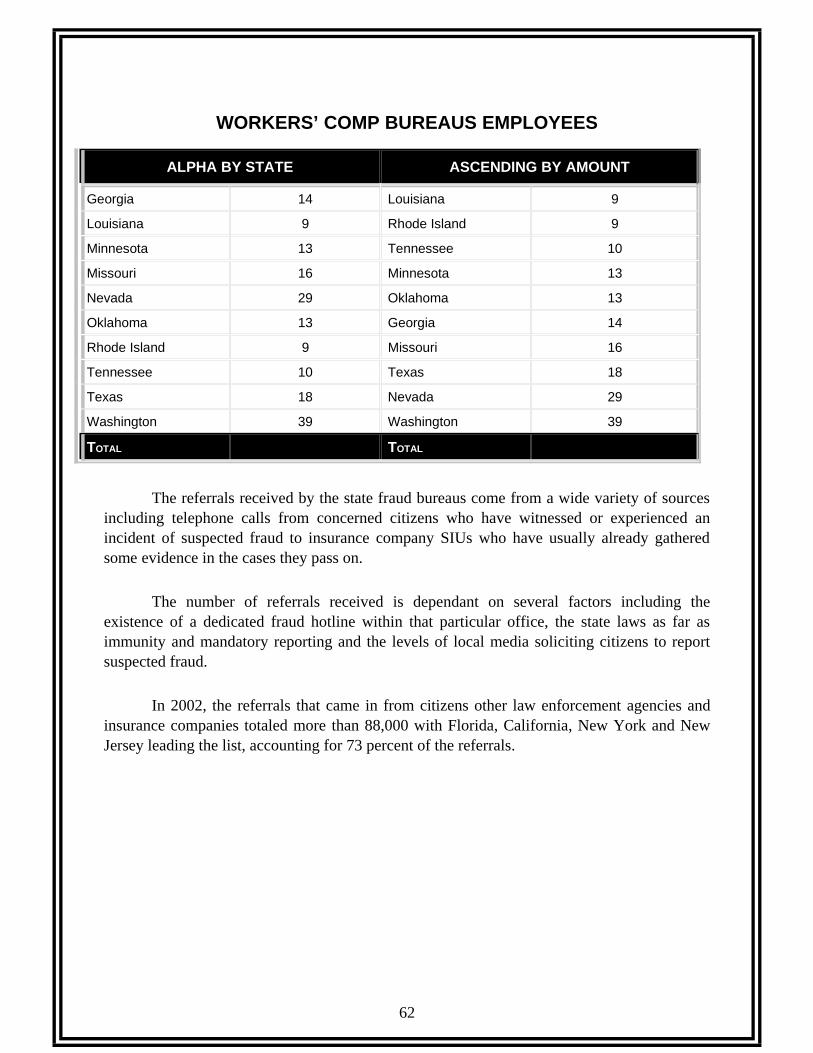

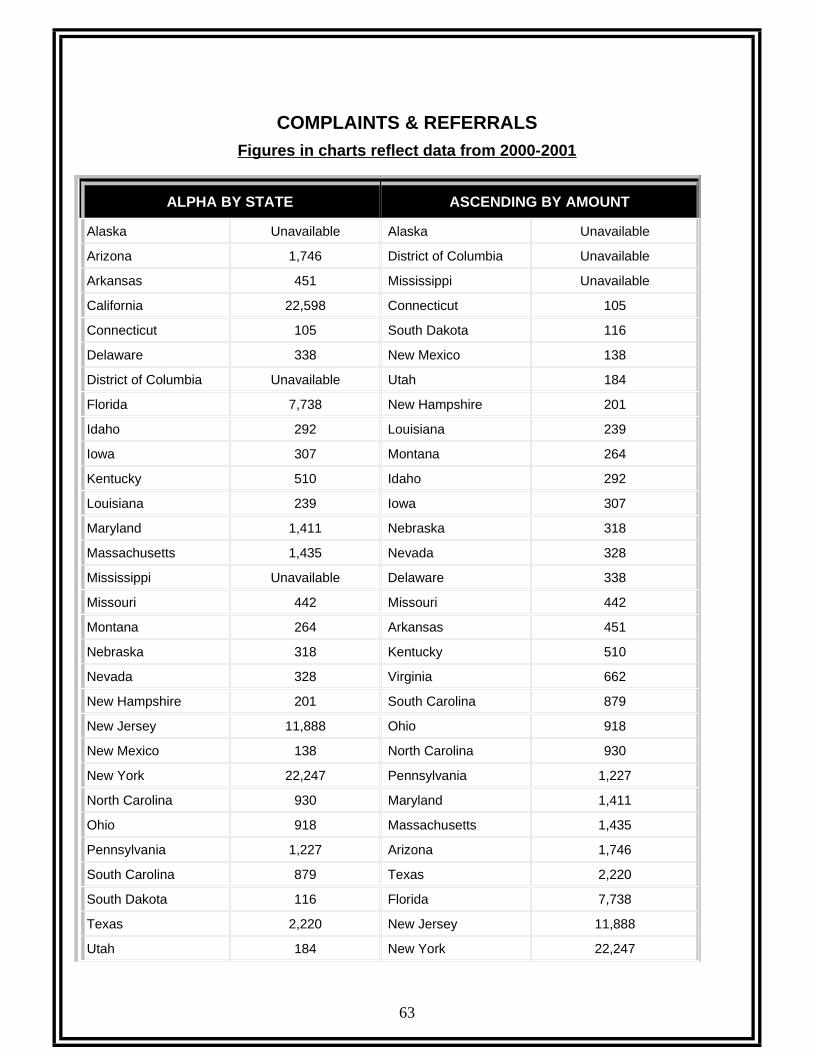

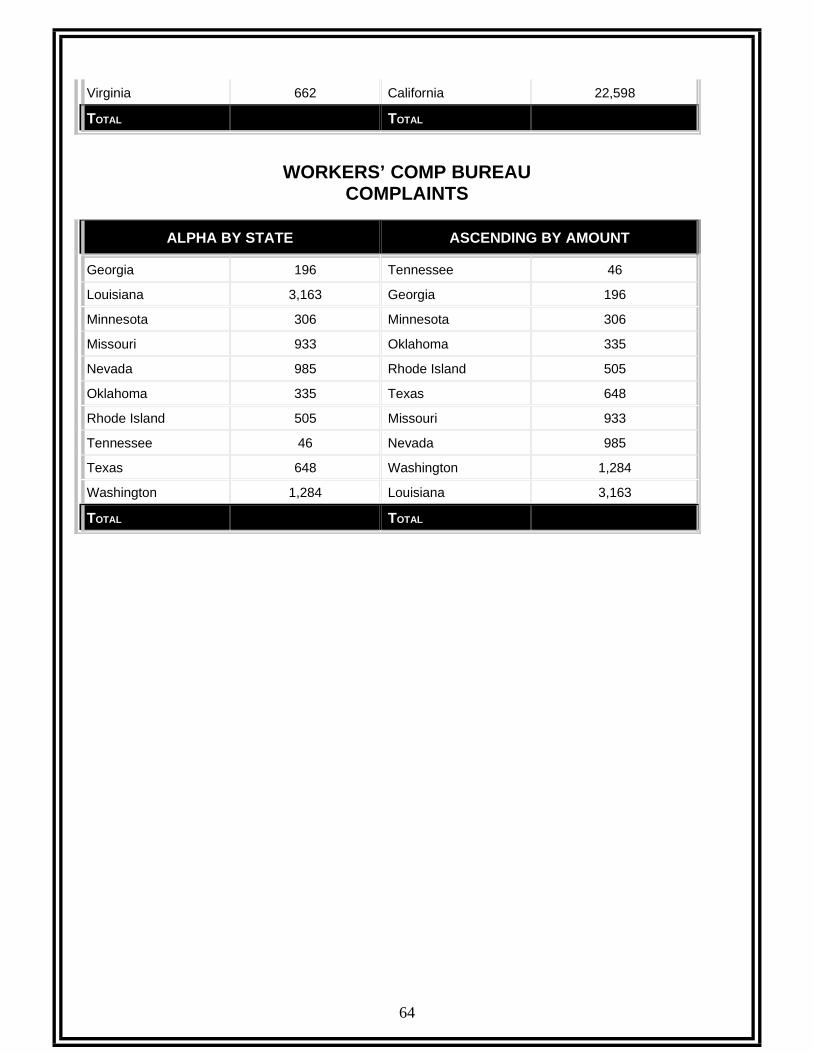

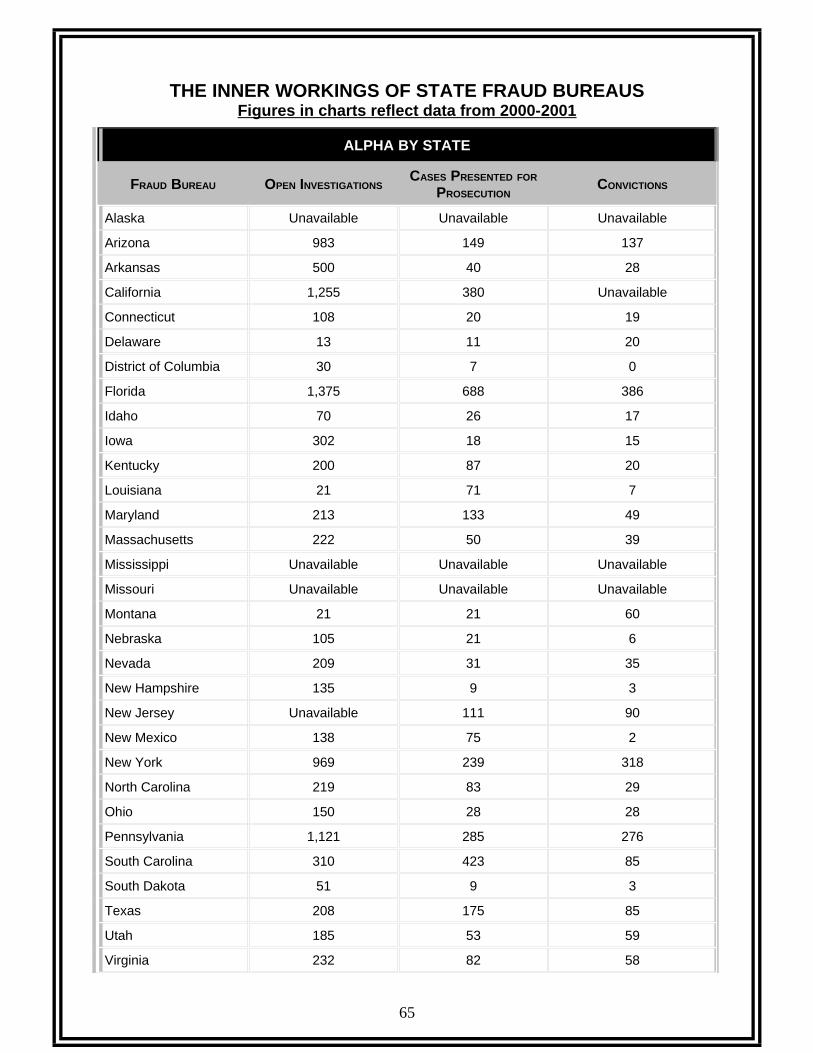

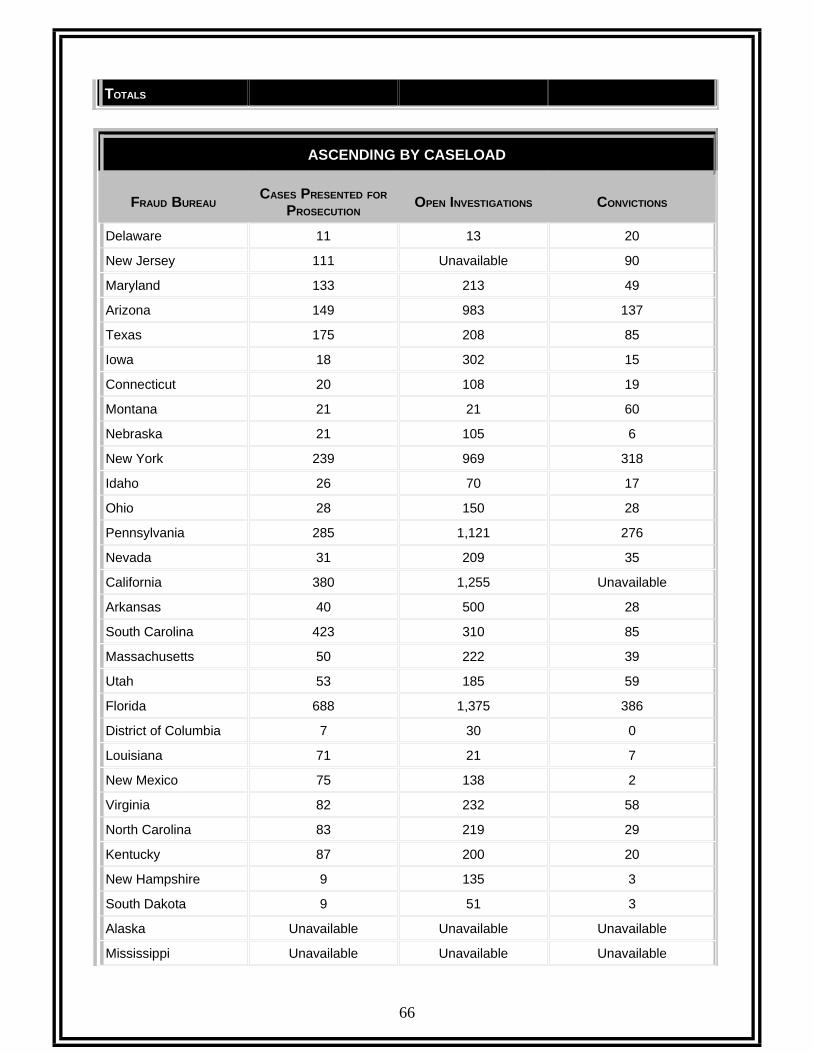

KEY STATE LAWS AGAINST FRAUD.............................................................................................51FRAUD BUREAUS AND THE YEAR THEY WERE ESTABLISHED...............................................53FRAUD BUREAUS HOUSED............................................................................................................54INSURANCE DEPARTMENT.............................................................................................................54FRAUD RESOURCE BREAKDOWN.................................................................................................56SUCCESS FACTORS........................................................................................................................56FRAUD BUREAU BUDGET 2000......................................................................................................57WORKERS’ COMP BUREAUS..........................................................................................................58BUDGET PER CAPITA......................................................................................................................59WORKERS’ COMP BUREAUS..........................................................................................................60NUMBER OF FRAUD UNIT EMPLOYEES........................................................................................60WORKERS’ COMP BUREAUS EMPLOYEES..................................................................................62COMPLAINTS & REFERRALS..........................................................................................................63WORKERS’ COMP BUREAU............................................................................................................64COMPLAINTS.....................................................................................................................................64THE INNER WORKINGS OF STATE FRAUD BUREAUS................................................................65

CONTINUOUS EFFORTS......................................................................................................................68

CHAPTER 1HISTORY OF FRAUD

HUMBLE BEGINNINGS

The origin of insurance can be traced back to the time of the first planned city ofMesopotamia as early as 2300 B.C. In order to “cut their losses,” Babylonian merchantscaravanned together across the vast deserts surrounding Mesopotamia, sharing the loss oftransportation costs (during that time — camels) that expired along the way.

In Greece 500 B.C., the Greek and Phoenician merchants who traveled through theports of Bablos, Tyre and Athens pooled their resources to create reserves to be used in case offire, piracy and sunken vessels.

In 1710 A.D., a London, England fire claimed over 13,000 residences and more than80 churches, including St. Paul’s Cathedral, sparking the first organized protection against fireloss deemed, simply and appropriately enough, “The Fire Office.”

THE INITIAL STAGES OF FRAUD

During the time of the civil war, the government was in desperate need of finding away to encourage individuals to help stop fraudulent activities. Suppliers were defraudingthe Union Army by selling the troops supply boxes filled with sawdust rather than suppliesand by selling and reselling the same horses to them over and over again.

In 1863 at the urging of President Abraham Lincoln, the Federal False Claims Actwas enacted. The “Whistleblowers Act” (as it was later nicknamed) offered a 50 percentshare of proceeds to individuals as incentive for speaking up when they witnessed awrongdoing.

The qui tam provisions were amended in 1943 removing the incentive forindividuals to sue on the government’s behalf and share in the proceeds of that suit byadding hurdles that prevented many cases from moving forward.

In 1986, President Ronald Reagan signed into law new amendments to the FalseClaims Act which restored the effectiveness of the Act and has since helped return billionsof dollars to the U.S. Treasury.

1

JUST WHAT IS FRAUD ANYWAY?

The dictionary defines fraud as “the intentional perversion of truth to induce anotherto part with something of value or to surrender a legal right.” An act of fraud is considered“trickery” and a fraudulent individual is described as “an imposter or one who is not what hepretends to be, seems to be or is represented to be.”

The collective cost of fraudulent acts within the insurance industry in some estimationstotal somewhere between $85 billion and $120 billion annually, according to the InsuranceInformation Institute (III). In 2002, the III’s figures for property and casualty insurance lossesalone were $31 billion.

You may think that these figures are so widespread that they do not affect you or yourclients — not so! The National Insurance Crime Bureau (NICB) estimates that fraud costs theaverage household $200 to $300 annually in hiked insurance premiums. Truly accuratecalculations of the cost of fraud are almost impossible to publish due to the nature of thecrime. Fraud often occurs and goes completely undetected despite the efforts of lawenforcement and others. By its very nature, fraud is slippery.

There are many different points throughout an insurance transaction at which timefraud has the opportunity to rear its head. This happens when policy holders pad claims orinsurance applicants falsify information on applications in order to obtain lower premiums(this practice is known as “soft fraud”). Another example is when a professional fraudulentlyfiles erroneous or illegitimate claims; or when someone fakes an auto accident or makes up aclaim (these practices are known as “hard fraud”).

In this age of technology, fraud perpetrators are using increasingly sophisticated meansto defraud insurance companies, and those who commit these crimes are a very diverse bunch;ranging from the ordinary property owners (attempting to cover their deductibles or just makean extra few bucks to make up for what they see as high insurance rates), to professionals andtechnicians (who inflate the cost of services or even charge outright for services that werenever performed at all), to highly organized rings of criminals.

It is so widespread that 43 states have now set up fraud bureaus to report and recordincreasing new incidences for investigation, and tips and cases brought to prosecution. InDecember 2003, a study of the 43 state fraud bureaus found that the bureaus opened a record33,000 cases in 2002. Florida, New York, New Jersey and Pennsylvania led in the largestgains in convictions.

In New York in 2003, over 800 arrests were made by the State Insurance FraudBureau, a fifteen percent increase over the year prior, 2002.

2

In 2003, 49 percent of people polled believed that insurance fraud occurs becausepeople believe they can get away with it. In the 2004 poll, that percentage had raised to 56percent; and over 30 percent of respondents stated they believed that people commit insurancefraud because they believe they pay too much for insurance, 95 percent believed it is importantfor insurance companies to investigate fraudulent claims, and 63 percent said that the primaryreason that insurers should investigate fraud is to control premium prices.

WHO HAS THE POTENTIAL?

Most of the time when you hear someone tell you that you’ve “got potential,” it soundslike a good thing. Would it surprise you to know that most people have the potential to commitinsurance fraud?

The general consensus in today’s society is that insurance companies have moremoney (technically, our money) than they need and it’s not really wrong to get some of it backon filing a claim. But if that claim is anything except above board and accurate, it becomesfraud.

For example, your roof is damaged and it really could be patched. However, you knowsomeone who knows someone who can give you an evaluation and estimate that states theroof cannot be repaired and actually needs to be replaced instead. So the roofing companymakes more money, you get a new roof and the insurance company paid for it all.

Winning situation for all? WRONG! This basic type of case scenario is what’s knownas insurance fraud. And it is just this type of situation that leads to higher premium costs asinsurance companies attempt to recoup their losses. After all, insurers are not in the businessof losing money.

Fraud is far from being a frivolous act — it is a serious crime that attracts a widevariety of perpetrators. Most people consider themselves above such crimes as theft; and yetthat’s exactly what insurance fraud is. The official files of state and government insurancefraud divisions are full of crimes committed by the “average Joe” or “Josephine,” whicheverthe case may be.

The insurance business involves numerous transactions that contain the potential forabuse and fraudulent, illegal activities. Law enforcement agencies on the state and local levelsare charged with the responsibility for investigating and prosecuting fraudulent activities.

Some lines of insurance are more vulnerable to fraud than others. Auto insurance,health care and workers’ compensation are believed to be the most widely affected. Thedetailed aspects of these three types of fraud will be our main focus of discussion in the nextchapters, though our course will broaden to include additional facets, including FinancialInstitution Fraud.

3

FINANCIAL INSTITUTION FRAUD

The Federal Bureau of Investigation (FBI) works to protect our nation's financialsystem. According to the FBI's Criminal Investigative Division (CID), Financial CrimesSection’s annual report on Financial Institution Fraud and Failure, FBI investigations into thefinancial institution fraud arena resulted in over 2,000 federal convictions in 2003.

The Assistant Director of the CID stated, "The FBI's mission in the area of financialinstitution fraud is to identify, target, disrupt and dismantle criminal organizations andindividual operations engaged in fraud schemes which target our nation's financialinstitutions."

The FBI investigates financial institution fraud (FIF) in several different arenas:

• Insider Fraud;

• Identify Theft;

• Check Fraud;

• Counterfeit Negotiable Instruments;

• Check Kiting; and

• Mortgage and Loan Fraud.

Investigations into financial institution fraud are taking the forefront due to increasedtechnology and computer-related banking. The FBI reported that in the past five years, therehave been more than 12,800 convictions on various charges of felonies, misdemeanors andpre-trial diversions, including both employees and non-employees of financial institutions.

During 2003, FBI investigations resulted in $3.8 billion in restitution orders and $35.6million in fines being handed down to subjects in financial institution fraud cases. In addition,the FBI seized $7.7 million in assets, forfeited $3.5 million and posted recoveries of $15.1million in financial institution fraud matters.

Since 1996, the FBI received 268,536 Suspicious Activity Reports (SARs) for criminalactivity related to these crimes. These fraudulent activities accounted for 47 percent of the569,294 SARs filed by U.S. financial institutions (excluding Bank Secrecy Act violations),and equaled approximately $8 billion in losses.

4

CHAPTER 2AUTOMOBILE INSURANCE FRAUD

Automobile insurance fraud is the largest and fastest growing area of insurance fraud,accounting for as much as 20 percent of auto insurance payments. This is a major addedexpense for auto policyholders, especially in urban areas.

The highest numbers of incidents identified as fraudulent automobile activity involvepadding or exaggerating injuries which account for about 33 percent of all bodily injuryclaims. As little as three percent of claims were found to be fraudulent as a result of deliberatescams, such as staged accidents.

The National Insurance Crime Bureau estimates thatautomobile insurance fraud costs consumers upwards of

$14.3 billion annually.

IT’S THE LAW

Licensed professionals who violate any of the following insurance laws are subject tothe loss of their state licenses:

• It is illegal for chiropractors to over bill for treatment or to charge for services thatwere not performed;

• It is illegal to receive treatment for fabricated injuries;

• It is illegal for medical personnel, such as doctors or medical facilities, to bill forservices not rendered;

• It is illegal for people to stage auto accidents;

• It is illegal to make or sell a fake motor vehicle insurance card; and

• It is illegal to make an oral or written statement which is false or misleading inorder to obtain insurance.

5

FRAUD “CREATIVITY” IN THE AUTO INDUSTRY

The examples given below are just a few of the most common ways people have foundto commit automobile fraud and, as you can already see, there are many. It seems that creativeacts of fraud are as limitless as people’s imaginations.

• Staged accidents;

• Phony claims;

• Exaggerated damages or injuries;

• Falsifying application information; and

• Using a phony insurance card.

Whenever a person deceives an insurance company, whether by means of collectingmoney they are not lawfully entitled to (submitting false or altered bills or receipts) or bymeans of not paying the appropriate premium amount (falsifying application information), it isan act of fraud and can be punishable by criminal and civil penalties, including jail time.

Following are some examples of “creative” fraud; ways that people commit fraud thatthe everyday individual citizen might never even think of or identify as fraudulent acts. Theseexamples will give you a good idea of just how appealing and profitable fraud can be to acriminal and why these crimes run so rampant.

In this day and age of “cloning,” the first example we’re going to study is called“automobile cloning” and has become very popular because of its seemingly foolproof natureand high profitability.

AUTOMOBILE CLONING

Fraud involved in automobile cloning is a type of fraud that requires copyingthe vehicle’s Vehicle Identification Number (referred to commonly as the VINnumber) off of a legally owned/registered vehicle that is unoccupied; may be in aparking lot or parked on the street or even in a vehicle dealership lot.

With this number, the thief or thieves can make counterfeit VIN tags.

6

The next step is to then steal a vehicle that fits thedescription of the vehicle from which the VIN numberwas stolen and replace that vehicle’s VIN tag with theillegally manufactured tag. Voila! A few phony papersand you have a clone “FOR SALE.”

REGULATION OF TOWING COMPANIES

Keep in mind that most companies (towing companies included) are totallylegitimate and do not engage in fraudulent practices; however, there are alwaysexceptions in any industry. Since this course deals with the subject matter of fraud, wewill be studying many arenas where the possibility of fraud lies and is being exploitedpredominantly.

Some towing companies inflate fees for the towing and or storage of vehicleswhich have been involved in an accident, abandoned or stolen, which results inindividuals and insurance companies being over charged exorbitant amounts for theseservices.

This problem is compounded when a company tows or stores a vehicle andneglects to contact or inform the owner. By the time the owner finds out where thevehicle is, additional fees and further expenses may be added to the overall bill.

Regulation is necessary in the fight against fraud to prevent individuals frombeing charged for unnecessary or exorbitant fees by towing operators. Permittingtowing operators to bill for other services not encompassed within a fee schedule basedupon the “usual, customary and reasonable” rates should not be acceptable.

TRANSFER OF TITLE

Transfer of title to stolen vehicles is another problem area where universalregulation could provide assistance and control.

Unfortunately as it stands now when title to a vehicle is obtained, there is noinstrument in place to determine if that vehicle has at any point been reported stolen orhas been entered into the National Crime Information Center database. Without havinginstruments such as effective tracking records in place, it is often possible for vehiclethieves to obtain legal title to their stolen vehicles.

7

AIRBAG THEFT

Airbag theft is another newly discovered, popular and very lucrative theftproject for unscrupulous individuals. Airbags are the number one accessory on theftlists for black market parts because of their profitability. A “HOT” airbag goes foraround $100 on the black market. Dishonest repair shop owners are in the market forthem and even at that black market price will net an $800 to $900 profit from just oneair bag replacement job. Insurance companies will pay upwards of $1,000 to replace anairbag.

ACCIDENT STAGING CAR RINGS

In New Jersey, law enforcement officials infiltrated a ring of 49 criminals byposing as participants in one of their staged accidents. This group was indicted forfiling fraudulent Personal Injury Protection (PIP) claims totaling an unbelievable$567,940.

The leader of the ring fled from New Jersey to Florida after her indictment andwas placed on New Jersey’s most wanted list before being caught. She was ultimatelyreturned to New Jersey and sentenced to five years in state prison for her crimes.

This is a brief synopsis of the components involved in car jacking rings. Playersoften include a ring leader who hires someone to be responsible for organizing thevaried aspects of staging an auto accident. These hired hands are often referred to as“cappers.”

The capper is responsible for recruiting drivers to participate in the “accident,”finding cooperative witnesses to be standing by to corroborate the accident details.After the accident occurs, the capper refers cooperating passengers to dishonestattorneys for legal counsel. These attorneys, in turn, refer them to dishonest medicalpractitioners for treatment. These practitioners are experts in billing for exaggerated oreven non-existent treatment procedures.

The attorneys then negotiate settlements with the innocent victims’ insurancecompanies that include faked and exaggerated injuries. Once the case is settled, all theplayers involved split the profits and once again you have a case of automobileinsurance fraud.

Once the insurance companies pay off, all the players in the scam are paid forplaying their parts and on they go to the next unsuspecting motorist.

8

CAR JACKING RINGS

In New Jersey, a 911 caller said he had just been the victim of a carjacking by aman armed with a gun. Police were immediately dispatched to the scene. When thepolice arrived moments later, the victim described in detail the armed and dangerouscarjacker, how he stuck the gun in the victim’s face, and how he took his car.

A witness also volunteered that he had seen the whole thing and confirmed thecar owner’s story. Despite the police department’s diligent efforts, they failed to findthe owner’s car or the carjacker.

The insurance claim that had been filed as a result of this carjacking was to paymore than $16,000. This thief fortunately was a victim himself, of an undercoveroperation. The whole thing had been a scam. Due to the efforts of a pro-activeundercover operation by the Office of the Insurance Fraud Prosecutor, these crookswere caught and prosecuted for this crime.

According to the National Insurance Crime Bureau (NICB), there was a5.7 percent increase in the Federal Bureau of Investigation’s (FBI) stolen car reportfrom the year 2000 to 2001. Estimates bring the number of reported car thefts in 2001to over 1.2 million.

According to the Insurance Information Institute (III), someone steals a car inthe United States every 26 seconds — which translates into $8.2 billion worth ofvanishing vehicles every year.

According to the most recent information available, the United States’ averagecomprehensive insurance premium rose 9.0 percent from 1995 to 1999.

9

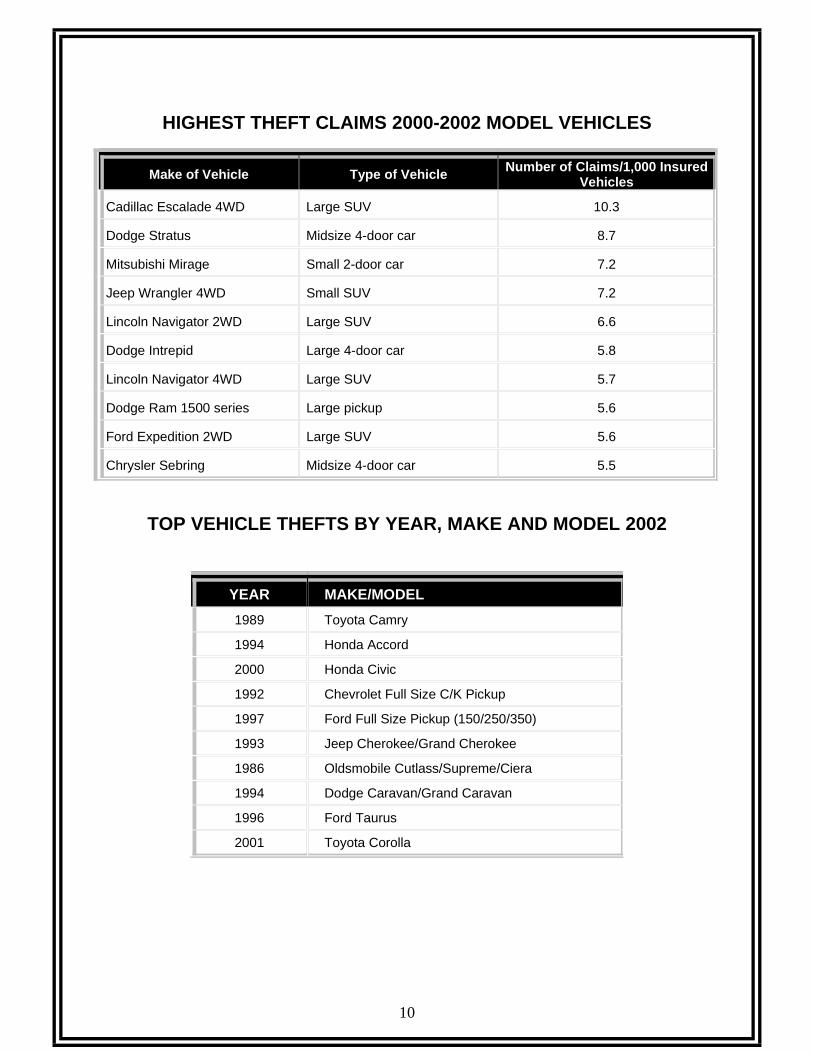

HIGHEST THEFT CLAIMS 2000-2002 MODEL VEHICLES

Make of Vehicle Type of Vehicle Number of Claims/1,000 InsuredVehicles

Cadillac Escalade 4WD Large SUV 10.3

Dodge Stratus Midsize 4-door car 8.7

Mitsubishi Mirage Small 2-door car 7.2

Jeep Wrangler 4WD Small SUV 7.2

Lincoln Navigator 2WD Large SUV 6.6

Dodge Intrepid Large 4-door car 5.8

Lincoln Navigator 4WD Large SUV 5.7

Dodge Ram 1500 series Large pickup 5.6

Ford Expedition 2WD Large SUV 5.6

Chrysler Sebring Midsize 4-door car 5.5

TOP VEHICLE THEFTS BY YEAR, MAKE AND MODEL 2002

10

YEAR MAKE/MODEL1989 Toyota Camry

1994 Honda Accord

2000 Honda Civic

1992 Chevrolet Full Size C/K Pickup

1997 Ford Full Size Pickup (150/250/350)

1993 Jeep Cherokee/Grand Cherokee

1986 Oldsmobile Cutlass/Supreme/Ciera

1994 Dodge Caravan/Grand Caravan

1996 Ford Taurus

2001 Toyota Corolla

11

CHAPTER 3HEALTH INSURANCE FRAUD

Fraud costs consumers billions of dollars annually in added health care costs. Thenation's bill for health care fraud exceeds $95 billion in some estimations. Health insurancefraud is responsible for losses in premium dollars as well as increases in health care costs.

THE PHYSICS OF FRAUD

Fraud takes place throughout many facets of the health care industry. Doctors todiagnostic facilities, pharmacists and hospitals to nursing homes and attorneys have all beencited in fraudulent scams.

According to the National Health Care Anti–Fraud Association,health insurance fraud costs Americans $54 billion a year.

Some studies show that for every one percent raise in insurance premiums,approximately 400,000 more people nationwide will not be able to afford

health insurance.

The Office of Inspector General of the U.S. Department of Health and Human Services(HHS OIG) conducts a formal audit of the Medicare program's fee-for-service claimspayments each year.

In 2002, the Department of Health and Human Services reported that 6.3 percent of theclaims paid in 2001 ($191 billion) should not have been paid for reasons of billing, paymenterror, insufficient provider documentation, or just blatant fraud, amounting to $12.1 billion.

In May, 2002, the National Health Care Anti-Fraud Association (NHCAA) reported inits Anti-Fraud Management Survey that they were responsible for recovering or preventingpayment of claims to the tune of $356 million in 2001 — as a direct result of their anti-fraudefforts.

The NHCAA estimates that of the nation's annual health care outlay, at leastthree percent ($39 billion in calendar year 2000) is lost to fraud. Some estimates bygovernment and law enforcement officials believe the loss to be as high as $130 billion each

12

year.

Insurance fraud can be displayed through various means such as giving false ormisleading information about being an employee or a member of a union or other group inorder to get away with paying lower premiums, deceiving health coverage providers in anattempt to collect money to which one is not entitled, to avoid paying the appropriate premiumamount, concealing any pre-existing medical conditions or submitting false medical receipts,bills or diagnosis, treatment or service.

IT’S THE LAW

• It is illegal to submit a false claim form to an insurance company in order to bepaid for health care services which were not received or provided;

• It is illegal to receive more Medicaid benefits than you're entitled to;

• It is illegal to participate in a scheme to offer or receive kickbacks in connectionwith the furnishing of items or services which are billable to the Medicaidprogram;

• It is illegal to over bill Medicaid for services provided; and

• It is illegal to receive disability benefits if you are not truly disabled and arecapable of performing the functions of your job.

HEALTH CARE RELATED FRAUD

The following is a broad list of the ways in which health care providers conspire to commithealth insurance fraud.

• Billing for services not provided;

• Billing for more expensive services than were provided;

• Billing for separate procedures which must be billed collectively;

• Providing treatments or services which were not medically necessary;

• Billing an insurer for services which the patient believes are free or complimentary;

• Billing for services rendered beyond the scope of a provider’s license;

• Submitting claims for services or treatments not provided;

• Submitting altered or forged receipts for reimbursement;

• Having a medical provider misrepresent diagnosis or treatment to pay forsomething which is not covered;

13

• Creating a fake group or organization to obtain less expensive group coverage; and

• Adding family members or other individuals who are not employees or members ofa group to a group policy.

PUTTING HEALTH CARE FRAUD INTO PERSPECTIVE

To lend a perspective of the vastness of fraud and how much it costs Americanseach year, the following is a selection of real life cases and case results dealing withsome of the more “creative” lengths people have gone to in committing acts of healthinsurance fraud.

PHARMACY SCAMS

Some of the pharmacy scams that have been uncovered include unscrupulouspharmacists who have committed such acts as billing Medicare for prescriptions thatwere never ordered, billing full price for drugs that were being purchased on the blackmarket at cheap prices, billing for refills that had never been ordered by patients,billing for abandoned prescriptions, and billing for costly prescription medicines whichare not medically warranted.

CHIROPRACTIC

Husband and wife chiropractors were targeted in an Office of Insurance FraudProsecutor’s investigation in 2003, and were charged with conspiracy, health careclaims fraud and money laundering.

The charges encompassed the billing of dozens of carriers for more than $1.2million for chiropractic treatments and other services that were never performed. Thecarriers allegedly paid over $430,000 in phony claims over a period of three years.

14

One Arlington, Texas chiropractor pled guilty in 2001 to a scheme responsiblefor submitting $5.7 million in false claims over a five-year period. Of the amountssubmitted, $3.2 million were paid.

A five-year prison sentence was handed down for the crime and one otherphysician was convicted in connection, two more submitted guilty pleas and twoformer physicians were indicted in this scheme.

HEALTH CARE INSTITUTIONS

Institutional cases involving national laboratories, pharmaceutical companies,hospitals, and medical equipment companies in recent years have been responsible forcosting hundreds of millions of dollars fraudulently gained through criminal activity.

There have been several high profile cases in recent years that have resulted incivil and criminal settlements, ranging upwards of $850 million.

COSMETIC SURGERY

Cosmetic surgery has become more easily obtainable for the average individualand misrepresentations of non-covered treatments as medically necessary are wildlyseen in the field of cosmetic surgery.

A procedure such as a nose job, breast augmentation or a tummy tuck can bebilled to the patient’s insurance company along with a medical necessity diagnosissuch as deviated septum repair, hernia repair or lumpectomy procedures often resultingin significant amounts of money being illegally billed to insurance companies.

INSURANCE CARRIER FRAUD

When a claims representative alters evidence in a claim or knowinglymisrepresents the truth to either support or deny a claim, or when they accept an offerof a gift for promise of a referral or the settlement of a claim, it is considered insurancecarrier fraud.

MEDICAL EQUIPMENT FRAUD

When equipment manufacturers offer free products to individuals, then chargetheir insurance companies, it is known as medical equipment fraud. Sometimes in thesecases the “free” equipment promised is billed to the insurance company and never evendelivered to the consumer. Motorized wheel chairs are a particularly hot fraud scamitem because of “big profits” to be made from Medicare reimbursement.

MEDICARE AND MEDICAID SYSTEMS

The Medicare and Medicaid systems seem to be vast areas open to fraudulent activity.Documented cases prove that organized crime is heavily involved in the submission of

15

fraudulent claims.

CASE INFORMATION BY THE DEPARTMENT OF JUSTICE

WASHINGTON, D.C. – A national laboratory has been ordered to pay the UnitedStates $5.2 million to settle allegations it submitted false claims for reimbursement oflaboratory tests under Medicare and Medicaid.

WASHINGTON, D.C. -- The operator of an Oklahoma psychiatric hospital thatallegedly treated children in an unsafe and harmful environment and then billed Medicaid forservices, has been ordered to pay the United States $750,000 to resolve allegations itdefrauded the health insurance program.

WASHINGTON, D.C. -- One of the nation's largest suppliers of durable medicalequipment and three health care providers will pay the United States more than $2 million tosettle allegations they sought to defraud the Medicare program through sham contracts andkickbacks.

WASHINGTON, D.C. -- A New Jersey drug firm has been fined a total of $925,000and its owner has been sentenced to two years in prison and fined a total of $75,000 forillegally importing counterfeit pharmaceuticals from China and laundering money in akickback scheme.

WASHINGTON, D.C. -- One of the nation's largest emergency physician staffingcompanies today agreed to pay the United States and various states $7.75 million to settleallegations it overcharged several federal health care insurance programs millions of dollars.The payments allegedly stemmed from false claims its billing company submitted to thefederal agencies.

WASHINGTON, D.C. -- Four blood product companies and their affiliates will paythe United States more than $12 million to reimburse several federal health care insuranceprograms.

16

In the six cases above, profiled by the Department of Justice, the settlementmonies collected exceeded more than $28 million.

But the cost of medical insurance fraud doesn’t stop there. These figures do not includethe monies involved in the costs of investigation, raised premium rates or lost benefits.

Fraud's impact goes far beyond financial loss when you look further into the dominoeffect of the impact it has on the exploitation of individuals and their insurance information asthe basis for falsified claims, falsification of patients' diagnoses and treatment histories (whichbecome a permanent part of a persons health records) which could endanger a life whenlegitimate health care providers are working from falsified medical record in an emergencysituation. Theft of patient’s lifetime health insurance benefits (fraudulent billing for servicesnever performed go against a patient’s lifetime cap of maximum benefits they are entitled to).

Health insurance fraud creates many legitimate concerns for everyone it touches frompatients and providers to insurance companies and law enforcement agencies and it is a costlysituation that society as a whole can no longer afford to overlook.

17

CHAPTER 4WORKER’S COMPENSATION FRAUD

Workers’ compensation fraud harms both employer and employee. Fraudulent claimsraise the cost of insurance for employers and cast sometimes undue suspicion on employees asto the legitimacy of a claim.

Employers who fraudulently underreport payroll or neglect to report it for allemployees to their insurance company in order to pay a lower workers' compensationpremium add significant costs to honest employers and their employees.

This action also make the competition playing field uneven and creates a disadvantagefor business who are paying the proper amount of workers’ compensation insurance premiumswhile others are showing higher profitability rather than paying the price for the benefits thatthey should be.

Prevention of workers' compensation insurance fraud could help in restoringconfidence in the workers' compensation system.

The NICB estimates the cost of workers’ compensation fraud to be in excessof $2.1 billion dollars annually.

IT’S THE LAW

• It is illegal to collect unemployment benefits while you are working.

• This is theft from the State unemployment insurance fund.

• It is illegal for an employer not to purchase workers' compensation insurance.

• It is illegal to inflate or misrepresent a claim

• Submitting false claims is fraud

• Getting hurt participating in a leisure activity on Sunday and report it on Mondayas a work-related accident is fraud.

• Misclassifying employees or payroll is fraud.

18

• Submitting false medical reports or inflated bills is fraud.

• Attorneys who solicit a person to file a false claim, or insurance carriers who alterevidence to support a denial of benefits are committing fraud.

TYPES OF WORKERS’ COMPENSATION FRAUD

When you hear the words workers’ compensation fraud most of us render a vision ofsomeone faking a work related injury but in truth there are many aspects of workers’compensation fraud and it occurs on a much broader scale than simply the faking of an injury.

The following selections will describe for you the many different aspect of workers’compensation fraud.

PROVIDER FRAUD

The first example is called provider fraud. This is when dishonest medical providersfalsify a diagnosis, unjustly extend a disability period or intentionally bill for service neverrendered.

CLAIMANT FRAUD

Another example of workers’ compensation fraud is called claimant fraud and thisoccurs when a claimant or employee collects benefits by intentionally causing or just outrightfaking an injury.

It can also be defined by a claimant or employee claiming a non- work related injury,working for another employer while collecting benefits, filing multiple claims for the sameinjuries through different employers, lying about lost wages or lying about the severity of theinjuries.

As you can readily see workers’ compensation fraud and the scope of possibilitiesstretches much wider than simply faking a work related injury.

19

PREMIUMS FRAUD

The next example we will examine is called premiums fraud. This type of fraud can becredited with being the most costly and by definition is when an agent or policy holderattempts to escape paying proper premium amounts by misclassifying employees, underreporting payroll or underreports past losses.

Premiums fraud is serious business and new laws have been enacted to stamp it out, inmost states if convicted of premiums fraud the penalty is stiff being 10 years in prison and upto $10,000 in fines.

Described next are a few “real life” case examples of workers’ compensation fraudtaking on its varied shapes and forms.

An Idaho woman was convicted on 10 counts of theft after fraudulently collecting herdeceased mother’s disability benefits for thirteen years after her mother had passed away. Shereceived a nearly five year sentence for defrauding workers’ compensation for more than$180,000.

In California a case of fraud involving employees, medical providers and attorneys wasshown on a television news station. Recruiters or “runners” as they are sometimes referred towere soliciting workers in unemployment lines to file workers’ compensation claims ratherthan unemployment. The solicitors were telling them that workers’ compensation claimswould be more profitable. The workers then filed claims that are typically difficult to prove,injuries such as chronic headache due to stress. Following several series of expensive medicaltesting the attorneys sought lump sum settlements to resolve the cases.

In Washington a 63-year-old Seattle man was ordered to repay the state some $353,000for monies he collected after being diagnosed with tremors, shakes and cognitive difficultiesfrom a work related accident. The results of an investigation proved that he was working andat the same time collecting the benefits from the state for being unable to work.

20

TROUBLE–SHOOTING METHODS

It is illegal to discriminate against workers who have filed workers’ compensationclaims in the past. There are however, signs which may point out possible fraudulent behaviorpatterns that may exist in certain employees, or prospective employees.

THE EMPLOYEE

• Moves out of state following an injury

• Has recently been terminated, demoted, or passed over for a promotion

• Calls soon after the injury asking for a settlement

• Has an unstable work history

• Has a history of reported injuries

• Displays a consistently uncooperative attitude

• Makes excessive demands

THE WORKPLACE

• The injured employee’s workplace is experiencing labor difficulties.

• The accident occurs just prior to the end of the employee’s probationary period,layoff, job termination, or after a formal disciplinary write-up.

THE INJURY

• The details of the accident are unclear or sketchy.

• There were no witnesses to the injury.

• The accident was not promptly reported to the employer.

• The employers’ first notice of the injury is from an attorney’s office or a medicalclinic.

• The injury was a difficult one to prove such as stress, back pain, or headaches.

• Verifying physicians have greatly differing opinions as to the extent of the workersdisability.

• Verifying physicians find no medical basis for the disability.

• The disability claim exceeds that which is normally consistent with such an injury.

21

• Accidents that occur late Friday afternoon or shortly after the employee reports towork on Monday.

• Accidents that occur while the employee is on a break or at lunch.

• Accident that occur while the employee is performing a duty that is out of therealm of normal duties performed.

THE MEDICAL RELATIONSHIP

• The first report of injury differs from the description given in the medical history.

• The injured employee begins a pattern of missing physician’s appointments.

• The employee often changes physicians or changes physicians when a release forwork has been issued.

THE CLAIM AND THE CLAIMANT’S ATTORNEY

• The attorney is known for handling suspicious claims.

• The injured employee’s attorney threatens further legal action unless a quicksettlement is made or contacts the company’s home office to push the issue ofquick settlement.

• The attorney attempts settlement early in the claim.

• The injured employee’s attorney requests that all checks and correspondence besent to the attorney’s office

• The employee is exceedingly familiar with workers’ compensation laws andclaims-handling procedures.

OTHER ACTIVITIES

• When called the injured worker is never home.

• The injured employee has left different daytime and evening telephone numberswhere he or she can be reached.

• The employee has other family members also receiving workers’ compensationbenefits or unemployment benefits.

• Information from fellow employees suggests the injured employee is participatingin strenuous activities, sports or has another job.

• The injured employee’s worker’s rehabilitation report shows evidence of otheractivity.

22

• The injured employee is exaggerating an injury in order to get time off of work topursue personal interests or to work in a seasonal trade such as farming orlandscaping.

THE SOCIAL SECURITY ADMINISTRATION

The Social Security Administration (SSA) has become an essential facet ofmodern life touching more lives than any other equivalent type of program, servingover 50 million participants (beneficiaries) with annual expenditures of over $500billion. The Social Security Administration continuously strives to keep SSA and itsprograms free from fraud, waste, and abuse.

The potential for fraud is inherent in any cash benefit program. The extent ofSupplemental Security Income (SSI) fraud may not be measurable, but it is a criticalconcern to SSA. Even a small amount of any such fraud tends to undermine publicconfidence in and support for the program.

President Franklin D. Roosevelt signed the Social Security Act onAugust 14, 1935 stating:

"We can never insure one-hundred percent of the population against one-hundred percent of the hazards and vicissitudes of life. But we have tried to frame alaw which will give some measure of protection to the average citizen and to his familyagainst the loss of a job and against poverty-ridden old age. This law, too, representsa cornerstone in a structure which is being built, but is by no means complete.... Itis...a law that will take care of human needs and at the same time provide for theUnited States an economic structure of vastly greater soundness."

President Bill Clinton signed legislation establishing the Social SecurityAdministration as an independent agency on August 15, 1994. On February 9, 1998, heis quoted as saying:

"Social Security...reflects some of our deepest values -- the duties we owe toour parents, the duties we owe to each other when we're differently situated in life, theduties we owe to our children and our grandchildren. Indeed, it reflects ourdetermination to move forward across generations and across the income divides inour country, as one America."

The SSA reports that one in six Americans receives a Social Security benefit.Not only have so many beneficiaries depended on their SSA benefits, approximately98 percent of all workers are in jobs covered by Social Security. Social Securitybenefits comprise about five percent of the nation's total economic output. In 1940,approximately 222,000+ individuals received monthly Social Security benefits. Today,

23

almost 45 million people receive such benefits.

Most people believe that SSA is only for the elderly; however in reality, nearlyone in three beneficiaries are not retirees or of retirement age. In the Social SecurityAmendments of 1972, Congress created the SSI program for eligible adults andassigned responsibility for it to the SSA. According to SSI program reports, of the oversix million recipients who receive SSI needed income, 31 percent are aged individuals,56 percent are disabled adults; and 13 percent are disabled children.

Under the 1935 law, what we now think of as Social Security only paidretirement benefits to the primary worker. A 1939 change in the law added survivors’benefits and benefits for the retiree's spouse and children. In 1956, disability benefitswere added.

When fraud strikes the Social Security Administration, it strikes us all in someway. Fraud and abuse in the SSI program generally involves individuals who:

1. File false claims;

2. Make false statements; or

3. Deliberately conceal information affecting initial or continuing eligibility forbenefits.

SSI program fraud falls within three broad categories:

1. Fraudulently claiming residency in the United States in order to receive SSIbenefits;

2. Collaborating with individuals to help them fraudulently obtain disability benefits;and

3. Intentionally failing to comply with reporting requirements by withholdinginformation about earnings, bank accounts, living arrangements, settlements, etc.,to obtain or continue SSI eligibility.

24

SSA AND OIG “ZERO TOLERANCE FOR FRAUD” PLAN

The SSA and OIG work in conjunction with one another to control fraud andabuse in the SSI program through the development of a comprehensive anti-fraud plancalled, appropriately enough, “Zero Tolerance for Fraud.” The National Anti-FraudCommittee, comprised of joint SSA and OIG executive leadership, oversees anddirects the plan. Ten regional committees responsible for local issues provide support.There are 36 anti-fraud initiatives in the plan, whose activities generally fall under thecategories of fraud prevention and detection, referral, and investigation andenforcement. The three major goals of the plan are to:

1. Modify programs, systems and operations to lessen instances of fraud;

2. Identify and eradicate wasteful practices that erode public confidence; and

3. Vigorously prosecute guilty parties, groups or individuals, whose actionsundermine the integrity of SSA’s programs.

Unfortunately, it is a simple fact that any cash benefit program contains aserious potential for fraud and abuse. The SSA views any type or amount of fraud as ameans of undermining public confidence in and support for the program.

MEDICAID HOSPICE

The Office of Inspector General has reported instances of potential kickbacksinvolving nursing homes and some hospice organizations. Specifically suspectedpractices sited are those involving a hospice organization that:

• Offers free goods or goods at below fair market value to induce a nursing home torefer patients to the hospice;

• Pays room and board payments to the nursing home in amounts in excess of whatthe nursing home would have received directly from Medicaid had the patient notbeen enrolled in hospice;

• Pays amounts to the nursing home for additional services that Medicaid considersto be included in its room and board payment to the hospice;

• Pays above fair market value for additional non-core services which Medicaid doesnot consider to be included in its room and board payment to the nursing home;

• Refers its patients to a nursing home to induce the nursing home to reciprocate byreferring its patients to the hospice;

25

• Provides free (or below fair market value) care to nursing home patients, for whomthe nursing home is receiving Medicare payment under the skilled nursing facilitybenefit, with the expectation that after the patient exhausts the skilled nursingfacility benefit, the patient will receive hospice services from that hospice; and

• Provides staff to the nursing home at its own expense to perform duties thatotherwise would be performed by the nursing home.

The medical decision-making process can be devastatingly distorted bykickbacks. A very serious consequence is over-utilization, which lessens the quality ofpatient care. Both Medicare and Medicaid prohibit such practices throughanti-kickback statutes which make it illegal to knowingly and willfully solicit, receive,offer, or pay anything of value to induce referrals of items or services payable by afederal health care program.

Parties that violate the anti-kickback statute may be criminally prosecuted orsubject to civil monetary penalties, and also may be subject to exclusion from federalhealth care programs.

26

CHAPTER 5UNAUTHORIZED ENTITIES

THE LURE OF LOW PREMIUM RATES

Fraudulent companies are becoming more and more creative. Many consumers don’teven know what an unauthorized entity is or realize that there are counterfeit companies whosell insurance products. And these counterfeit companies prey on the unsuspecting out in themarketplace. Individuals are lured with promises of high quality coverage and low premiums.Many people still hold to the old adage, “If it sounds too good to be true, it probably is.”Cautionary flags should be raised.

Unauthorized entities lure employers with low rates for health insurance coverage, butwhat they are really offering consumers is a false sense of security. A state’s high populationand large quantity of small businesses make for an especially vulnerable condition. In theearlier years of unlicensed insurance sales, smaller businesses were primarily targeted;however, larger businesses are recently being targeted as well. Fraudulent companies aregetting more inventive it seems. Many companies have been conducting this type of businessnationwide; by the time they are discovered, thousands of Americans have already been takenfor millions of dollars.

The rising costs of insurance premiums have made insurance more and more difficultfor the average citizen to afford. This predicament has led many to seek “alternative”insurance, purchasing policies with lesser known companies who are offering lower premiumrates and then merely trusting and hoping that the funds will be available for them when theyneed it.

FRAUDULENT DISCOUNT HEALTH PLANS

Some phony insurers attempt to sell coverage through real as well as fakeprofessional and trade associations, unions and professional employee organizations.Some disguise themselves as discount health plans, which are a type of entity that isnot regulated by federal or state governments. Legitimate discount plans aren'tregulated because they don't pay claims; they charge a monthly fee in exchange fornegotiating discounts with doctors and hospitals. Phony discount health plans collectthe monthly fees without negotiating any discounts. These bogus insurers may evenappear to exude a certain air of legitimacy, such as naming themselves after existing,generally more familiar companies or recruiting licensed insurance agents to sell theirphony health plans.

27

AVOID FRAUDULENT UNFAIR RATING PRACTICES

Many illegal or unauthorized health benefit plans use unfair rating practices aswell. For instance, a generally healthy person can get a low premium rate for a healthbenefit plan, but let that “insured” individual get sick or become seriously ill and theirpremiums will shoot up sky high. Many victims have reported that in the beginning,their premium rates were very low; for example, $150 per month. Then the diagnosisof a serious illness, and all of a sudden their premium rates are increased ten-fold, to$1,500 per month.

This practice is often referred to as predatory rating; the “insurer is thepredator” and the “consumer is the prey.” These scenarios are not uncommon, nor arethe figures uncommon. Usually, the victim cannot afford the hiked up rate andtherefore is forced to surrender the policy they thought was such a good deal.

At this point, they are now saddled with a pre-existing condition and may beunable to get private individual insurance protection elsewhere and are therefore forcedinto the ranks of the uninsured. Rates should be priced adequately on the front end toanticipate future losses, premiums should be adjusted as losses are experienced, andrates should remain stable whether the individual is healthy or sick. Rating practicessuch as hitting consumers with significant premium increases once they’ve become illare not permissible in the regulated insurance market.

It is every state’s responsibility to assist with the maintenance of a fair andhonest insurance market and to protect its citizens from entities that attempt to break oreven evade the insurance laws of the state. Each state insurance department isresponsible for maintaining the integrity of the insurance industry. Insurancedepartments make every attempt to ensure that all insurance producers are licensed inthe state to sell insurance products. However, there are always inscrutable entities thatbelieve they are above the law and can skate around the rules.

Some companies are performing insurance functions and selling insurancewithout being licensed. These entities are categorically termed “unauthorized entities.”They have not been authorized to sell in the state; and they may even recruit licensedinsurance agents to sell their bogus products for them. As the cost of health insuranceincreases and consumers seek affordable coverage, licensed agents are often targeted tomarket and sell unauthorized insurance products to consumers. Unauthorized policiesissued by these entities are not covered under any state guaranty fund, and therefore donot offer any protection to the consumers who purchase their policies.

28

And that is why the burden is not entirely on the state insurance departmentsand/or consumers; it is also the responsibility of insurance producers to be aware oftheir products and what is backing them before they market any product. There aremany signals that agents should look out for; certain signals that should raise a red flagin front of their eyes.

Before placing insurance with an insurer, agents should make a reasonableinquiry into the financial condition and operating history of that insurer. Producersshould make it their continuous duty to stay informed of the insurer's solvency and thesoundness of its financial strength, and of the insurer's ability to process claims andpay losses.

FALSIFYING STATE INSURANCE REGULATION EXEMPTIONS

Individuals and entities who produce and market unauthorized insurance scamsoften falsely assert that their “programs” are exempt from state insurance regulation.Their brochures and marketing pamphlets may look extremely impressive as well, andthat is one way they influence consumers. With their extraordinary advertisingtechniques they believe they can get away with breaking the law.

Many entities lead consumers to believe that the products they are offering are"ERISA plans," "ERISA exempt," "union plans," "association plans," or somevariation thereof. They boast low rates and minimal or no underwriting. Unfortunately,this is an all too common tactic. Qualified plans under ERISA cannot sell healthinsurance to the general public.

29

CHAPTER 6IDENTITY THEFT

IDENTITY THEFT AND IDENTITY FRAUD

Identity theft and identity fraud are crimes in which someone obtains and uses anotherperson's personal information in some way that involves fraud or deception, typically foreconomic gain.

The United States Department of Justice issues a special report to advise the public oncurrent trends and developments in identity theft. The United States’ enforcement agencies areseeing a growing trend toward greater use of identity theft as a means of furthering orfacilitating other types of crime, from fraud to organized crime to terrorism. The Federal TradeCommission reports that identity theft complaints increased five-fold from 2000 to 2002.

There are several ways in which identity theft is committed. There are several ways inwhich criminals can get your personal information to be used against you even when they’restanding right next to you.

DUMPSTER DIVING

Often, you will not even see what the thief sees because he’s robbed yourmailbox, confiscating those pre-approved credit card applications we all seem toreceive, no matter how bad the individual’s credit may be. In case this mail does makeit to you before the thief gets his hands on it, he may still be able to get it out of yourtrash. Many people are simply in the habit of throwing this type of mail away as “junkmail.” What is one man’s trash is another man’s treasure. All the thief has to do iscomplete the application, ask for the card to be sent to a different address, and the thiefwill reap the rewards of your credit. Unless you shred and destroy this type ofinformation, you may just reap the agony.

SHOULDER SURFING

You may not even realize it — you certainly don’t want to be rude to theperson who is waiting patiently behind you for his turn at the ATM, so he engages youin conversation or manages to get you distracted in some other way while he (or anaccomplice) pulls the switch — your card with another “look alike.” You walk away,the thief steps up and cleans out your bank account with the pin number he has justwatched you use.

30

SKIMMING

Unlike the shoulder surfing method, this type of theft is most difficult toidentify when it’s happening. You pay with your meal at a restaurant or your gas at thestation with your credit card and, as normal, the attendant “swipes” your card into theelectronic device. Unbeknownst to you, this “skimmer” records the personalinformation data from the magnetic strip on the back of your card and transmits thisdata to another location to be duplicated onto a fraudulently made credit card.Sometimes this information is transferred overseas, making prosecution even moredifficult.

“PHISHING” AND WEBSITE SPOOFING

Phishing is a new scheme that involves the use of e-mails and websitesdesigned to look like e-mails and websites of well-known legitimate businesses,financial institutions, and government agencies in order to deceive internet users intodisclosing their bank and financial account information or other personal data such asusernames and passwords. The "phishers" then take that information and use it forcriminal purposes, such as identity theft and fraud.

The same types of fraud schemes that have victimized consumers and investorsfor many years before the proliferation of internet use are now appearing online. Fraudschemes can be found in chat rooms, e-mail, message boards, or on Websites.

Our email systems are so accessible; unfortunately not only to us, but to thievesas well. The scam is that you receive an email from a business you are legitimatelyfamiliar with and they offer you an incentive to open an account; or, if you have anexisting account, they ask you to update your records for some reason, usuallysomething like “…due to security reasons…” Included in the email is a link to awebsite that looks identical to the legitimate company's website; however, it is far frombeing who it is presenting itself to be. The customer is asked for his or her SocialSecurity number and other personal information stating that the company needs toupdate their records online to enable you to continue to do business with theircompany. You fill out the requested information and the thief gets your personal datato engage in any number of various fraud schemes.

People who receive phishing e-mails also may not realize that the senders mayhave used mass e-mailing (“spam”) techniques to send the e-mail to thousands andthousands of people. Some phishing expeditions also incorporate virus techniques intothe system that allow them access to additional email address through what iscommonly called the “worm.”

Many of the people who receive that spammed e-mail do not have accounts orcustomer relationships with the legitimate business or financial services company thatthe e-mails purport to come from. The people who create phishing e-mails count on thefact that some recipients of those e-mails will have an account or customer relationship

31

with that legitimate business or company, and may be more likely to believe that the e-mail has come from a trusted source, and therefore provide the data they want.

MINIMIZING THE RISK The Department of Justice recommends the following to assist in minimizing

the risk of identity theft:

• Cancel and destroy credit cards you do not use and keep a list of the ones youuse regularly.

• Carry only the identification information and credit cards that you actuallyneed. Do not carry your social security card; leave it in a secure place. Thisapplies also to your passport unless you need it for traveling out of country.

• Pay attention to your billing cycles and follow up with your creditors and utilitycompanies if your bills do not arrive on time.

• Carefully check each of your monthly credit card statements. Immediatelyreport lost or stolen credit cards and any discrepancies in your monthlystatements to the issuing credit card company.

• Shred or destroy paperwork you no longer need, such as bank machine receipts,receipts from electronic and credit card purchases, utility bills, and anydocument that contains personal and/or financial information. Shred or destroypre-approved credit card applications you do not want before putting them inthe trash.

• Secure personal information in your home or office so that it is not readilyaccessible to others who may have access to the premises.

• Do not give personal information out over the phone, through the mail, or overthe Internet unless you are the one who initiated the contact and know theperson or organization with whom you are dealing. Before you share suchinformation, ensure that the organization is legitimate by checking its websiteto see if it has posted any fraud or scam alert when its name has been usedimproperly, or by calling its customer service number listed on your accountstatement or in the phone book.

• Password-protect your credit card, bank, and phone accounts, but do not keep awritten record of your PIN number, social security number, or computerpasswords where an identity thief can easily find them. Do not carry suchinformation in your purse or wallet.

• Order a copy of your credit report from the major credit reporting agencies atleast once every year. Make sure your credit report is accurate and includesonly those activities that you have authorized.

32

33

CHAPTER 7OTHER TYPES OF FRAUD

THE BUSINESS OF INSURANCE

The first monetary gainful goal of an insurance company is to profit from the increasedvalue during the period of time the money is held from when the premiums are received untilthe claims are paid, also known as the “investment income on reserves.”

The second goal of an insurance company is to profit by charging premiums in excessof the claims paid, also known as “underwriting profits.”

Between the two, the investment income is much more important. An insurancecompany can realistically expect to average 8 percent to 12 percent or better annually on itsinvestment returns. No insurance company can expect to approach these profits on its typicalunderwriting activity.

What this means, in essence, is that an insurance company is a bank. Policyholders“loan” money to the insurance company by way of paying premiums. The bank pays back thepolicyholders by way of paying claims.

The main function of an insurance company is investing. The primary fraud threat toinsurance companies is investment fraud, and not, as one might expect, fraudulent claims.Though fraudulent claims can also have a significant impact on profitability, intrinsic fraud isthe largest threat.

INTRINSIC FRAUD

Intrinsic fraud is fraud that occurs within the insurance company by someone in aposition which allows the execution and cover-up of the act.

This is one of the most difficult types of fraud to uncover and usually involves theinteraction of an outside schemer as well. Investment fraud, performance skimming andinvestment advisor kickbacks are all examples of intrinsic fraud.

34

INVESTMENT FRAUD

Investment return is the true profit mechanism of any insurance company. Internalinvestment fraud is difficult to detect because determining the precise amount of investmentincome a company should have earned for the year is very difficult.

PERFORMANCE SKIMMING

If an investment counselor is able to extract even a small percentage of theircompany’s profit off the top each year that amount comparatively could add up to millions ofdollars.

This type of fraud or theft is very difficult to detect because the means used tocalculate the precise annual percentage rate the company should have earned is not an exactscience. Should the company’s profits have exceeded the S&P 500 by 5 percent? Or should ithave been 5 percent under?

There are some ways to safeguard against performance skimming such as the use of aninvestment committee or use of an outside investment counselor, though this safeguard has itsdisadvantages as well, as you will read next.

INVESTMENT ADVISOR KICKBACKS

Financial advisors receive large fees from insurance companies giving themtremendous incentive to keep insurance company’s investment officers happy.

When the relationship between an investment officer and a financial advisor becomesunusually close or when a company begins experiencing large losses in good economic timesthe possibility exists the incentives given to the investment offices by the financial advisorhave gotten out of control and that some form of pay offs are taking place.

35

EXCESSIVE RISK

Excessive risk is also considered a type of intrinsic fraud though it is also classified assoft fraud.

By definition this occurs when an investment officer, in order to generate bonuses oreven to justify their position, takes excessive risks in investments. If the high risk investmentsgo badly the officer may further the damage by attempting to cover up the losses and makeeven riskier investments, in hopes of high dollar returns to quickly make up past losses.

ARSON

Arson is the deliberate act of setting fire to property for fraudulent or maliciouspurposes.

Criminal investigations on fraud also include arson for hire and arson for hire rings.These people intentionally set fires for the purpose of collecting insurance money.