Embed Size (px)

Citation preview

Interim Results 2007Interim Results 2007

&&

Proposed acquisition of PGL, Proposed acquisition of PGL, formation of Education divisionformation of Education division

May 2007

2 European specialist holiday groupEuropean specialist holiday group

Important Notice

The information in this document does not constitute or form any part of an offer or invitation to sell, or issue, or any solicitation of any offer to purchase, subscribe for or otherwise acquire any shares or other securities in Holidaybreak plc (“Holidaybreak") in any jurisdiction, nor shall it or any part of it form the basis of, or be relied on in connection with, any contract therefor. No reliance may be placed for any purpose whatsoever on the information or opinions contained in this document or on its completeness. No representation or warranty, expressed or implied, is given on behalf of Holidaybreak or any of its respective directors, employees, agents or advisers as to the accuracy or completeness of the information and no liability is accepted (and all such liability is hereby excluded) for any such information or opinions. Readers of this document are reminded that the information in this document has not been verified and is liable to change and that any decision to acquire shares in Holidaybreak should be made only on the basis of information contained in the final class 1 circular to be issued by Holidaybreak which may be different from the information contained in this document. This document is being supplied to you solely for your information and may not be reproduced or further distributed to any other person or published, in whole or part, for any purpose. This document is intended only for distribution to persons who are persons falling within Articles 19 or 49 (2)(a) to (d) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (all such persons being referred to as "relevant persons"). This document must not be acted on or relied on by or sent to persons who are not relevant persons. The distribution of this document in certain jurisdictions may be restricted by law and therefore persons into whose possession this document comes should inform themselves about and observe any such restrictions. Any such distribution could result in a violation of the law of such jurisdiction.

The information in this document is confidential and, as such, may constitute inside information relating to the securities of Holidaybreak for the purposes of relevant insider dealing laws.

3 European specialist holiday groupEuropean specialist holiday group

Holidaybreak plcAgenda

Bob Ayling (Chairman) - Overview

Carl Michel (Group Chief Executive) and Bob Baddeley (Group Finance Director) - Results

- Highlights- Finance Review- Divisional Review

- Proposed Acquisition of PGL

4 European specialist holiday groupEuropean specialist holiday group

Holidaybreak plcHighlights

Interim results - Solid performance - DPS +10%Current trading broadly in line with expectationsSatisfactory trading outcome anticipated for full year

Proposed acquisition of PGL - An excellent strategic opportunity - A profitable, growing business in the attractive outdoor education and adventure sector

Interim Results for the six Interim Results for the six months ended 31 March 2007months ended 31 March 2007

6 European specialist holiday groupEuropean specialist holiday group

FINANCE DIRECTOR’S REVIEW

BOB BADDELEY

Holidaybreak plcINTERIM RESULTS 2007

7 European specialist holiday groupEuropean specialist holiday group

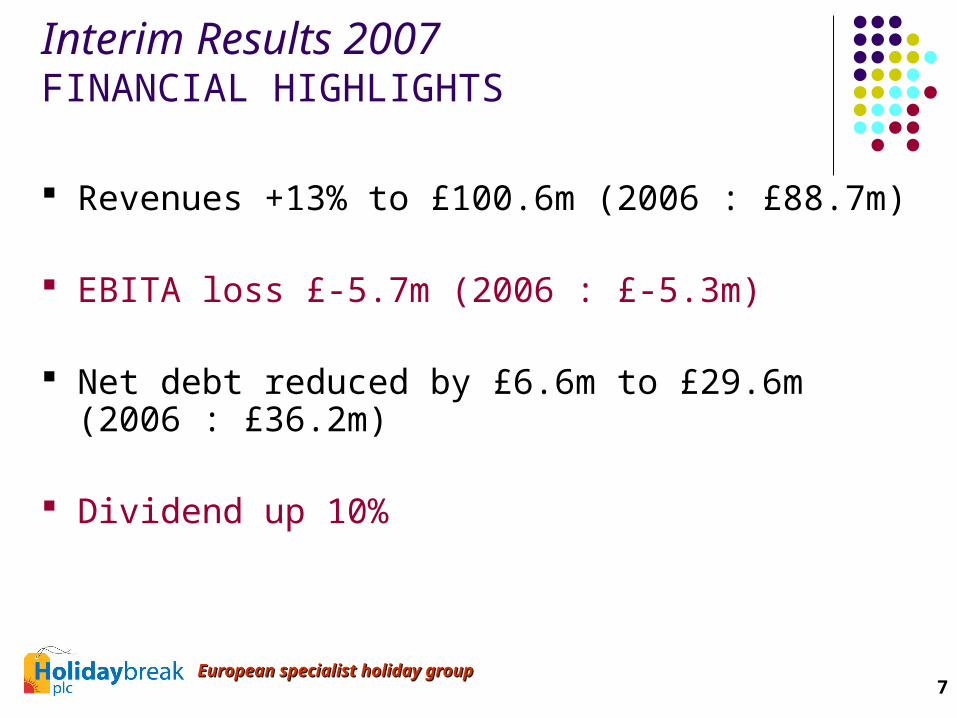

Interim Results 2007FINANCIAL HIGHLIGHTS

Revenues +13% to £100.6m (2006 : £88.7m)

EBITA loss £-5.7m (2006 : £-5.3m)

Net debt reduced by £6.6m to £29.6m (2006 : £36.2m)

Dividend up 10%

8 European specialist holiday groupEuropean specialist holiday group

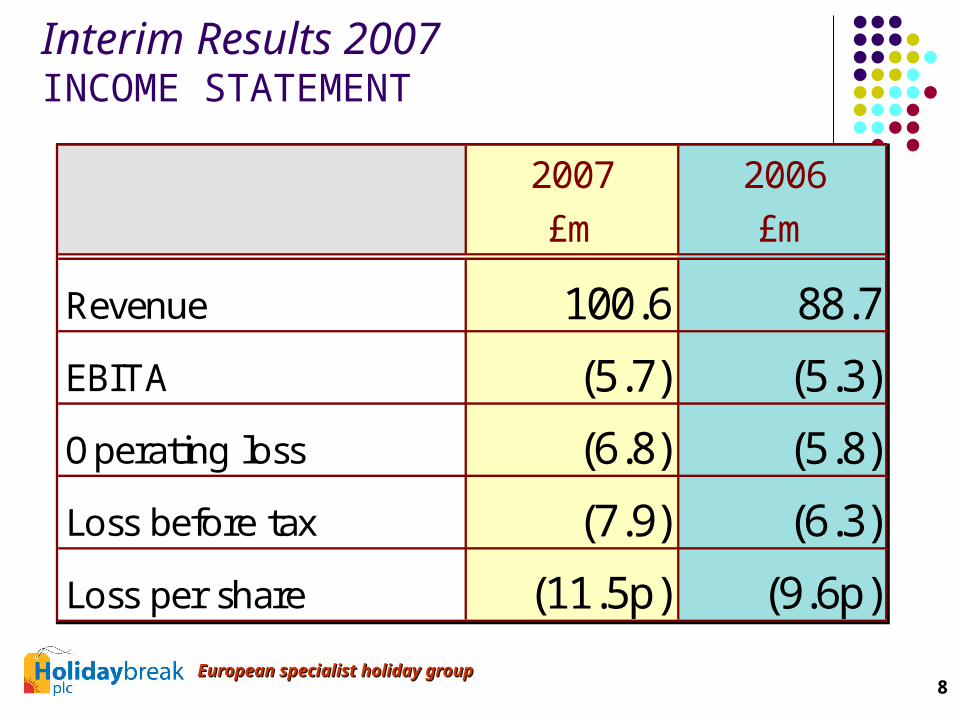

2007 2006£m £m

Revenue 100.6 88.7

EBITA (5.7) (5.3)

Operating loss (6.8) (5.8)

Loss before tax (7.9) (6.3)

Loss per share (11.5p) (9.6p)

Interim Results 2007INCOME STATEMENT

9 European specialist holiday groupEuropean specialist holiday group

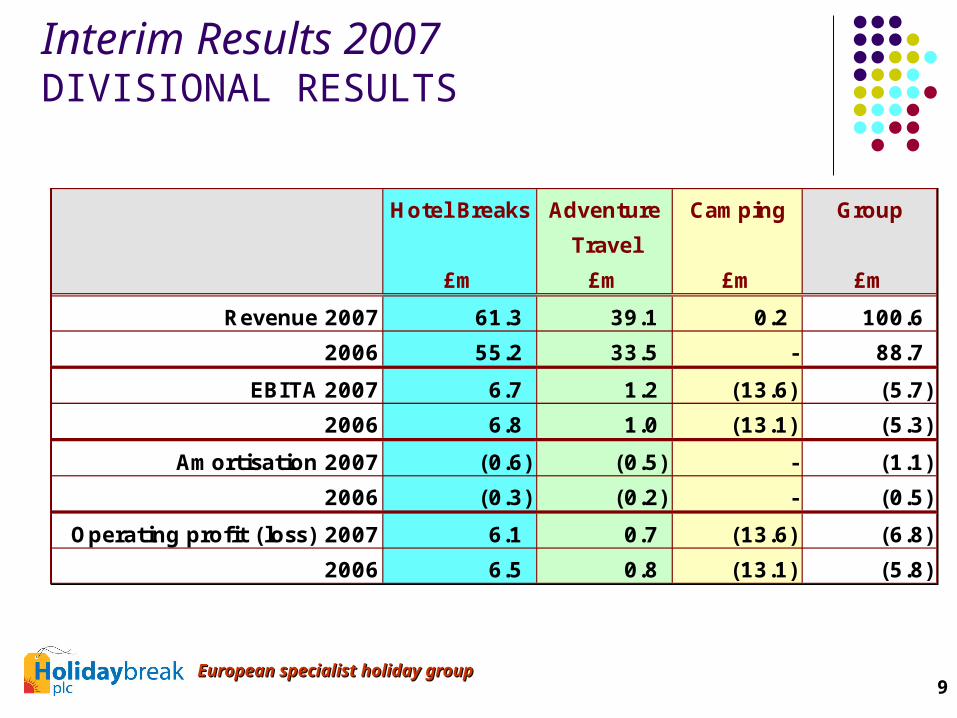

Interim Results 2007DIVISIONAL RESULTS

Hotel Breaks Adventure Camping Group

Travel

£m £m £m £m

Revenue 2007 61.3 39.1 0.2 100.6

2006 55.2 33.5 - 88.7

EBITA 2007 6.7 1.2 (13.6) (5.7)

2006 6.8 1.0 (13.1) (5.3)

Amortisation 2007 (0.6) (0.5) - (1.1)

2006 (0.3) (0.2) - (0.5)

Operating profit (loss) 2007 6.1 0.7 (13.6) (6.8)

2006 6.5 0.8 (13.1) (5.8)

10 European specialist holiday groupEuropean specialist holiday group

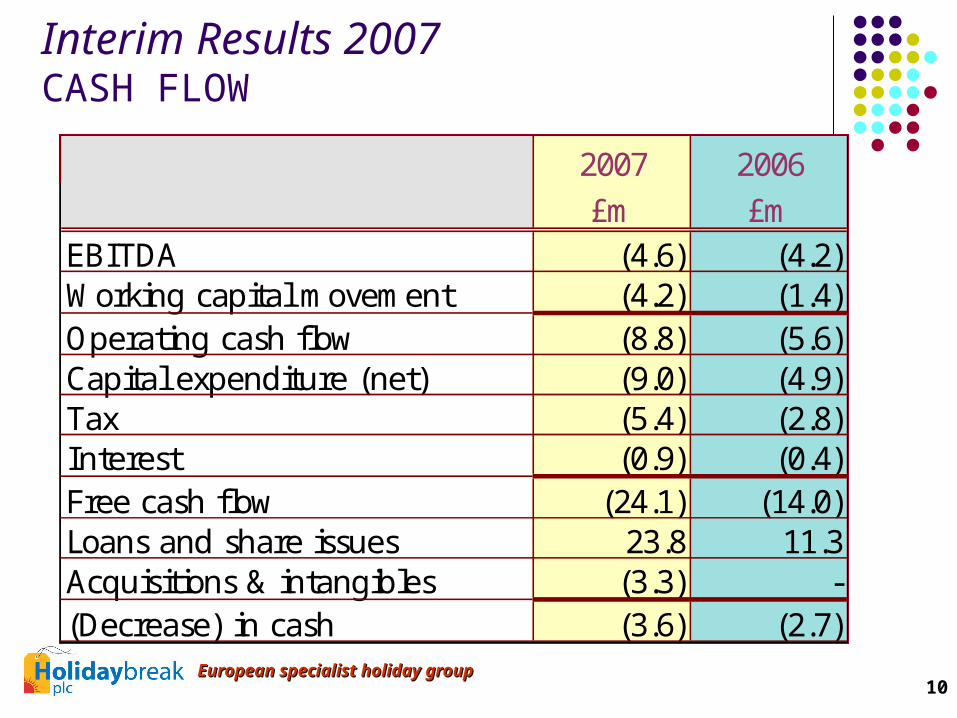

Interim Results 2007CASH FLOW

2007 2006£m £m

EBITDA (4.6) (4.2)Working capital movement (4.2) (1.4)Operating cash flow (8.8) (5.6)Capital expenditure (net) (9.0) (4.9)Tax (5.4) (2.8)Interest (0.9) (0.4)Free cash flow (24.1) (14.0)Loans and share issues 23.8 11.3Acquisitions & intangibles (3.3) -(Decrease) in cash (3.6) (2.7)

11 European specialist holiday groupEuropean specialist holiday group

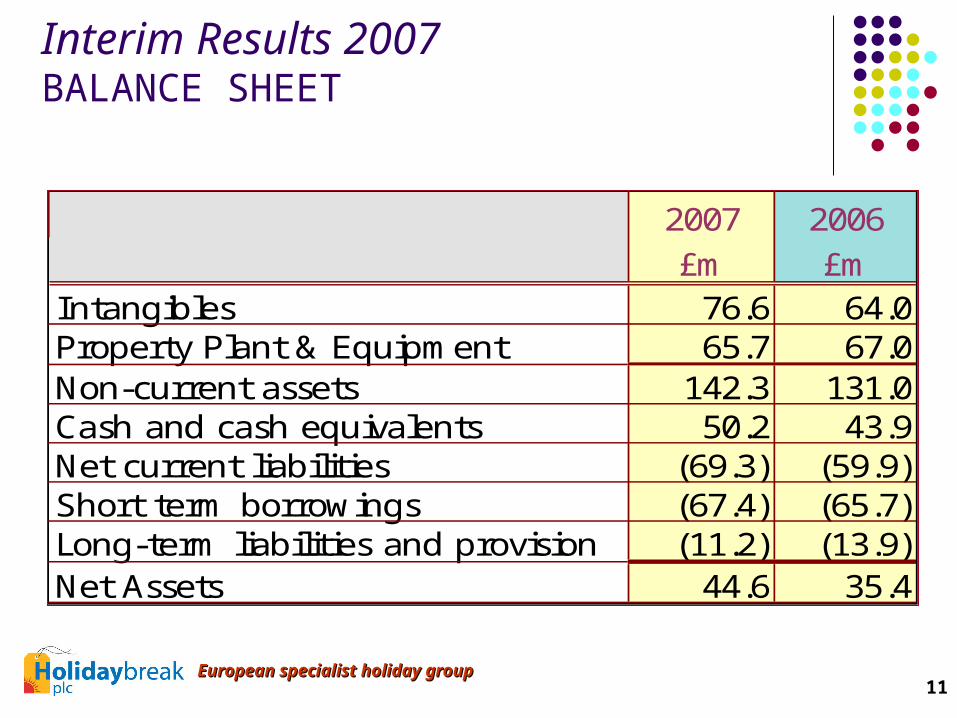

Interim Results 2007BALANCE SHEET

2007 2006£m £m

Intangibles 76.6 64.0Property Plant & Equipment 65.7 67.0Non-current assets 142.3 131.0Cash and cash equivalents 50.2 43.9Net current liabilities (69.3) (59.9)Short term borrowings (67.4) (65.7)Long-term liabilities and provision (11.2) (13.9)Net Assets 44.6 35.4

12 European specialist holiday groupEuropean specialist holiday group

CEO REVIEW

CARL MICHEL

Holidaybreak plcINTERIM RESULTS 2007

13 European specialist holiday groupEuropean specialist holiday group

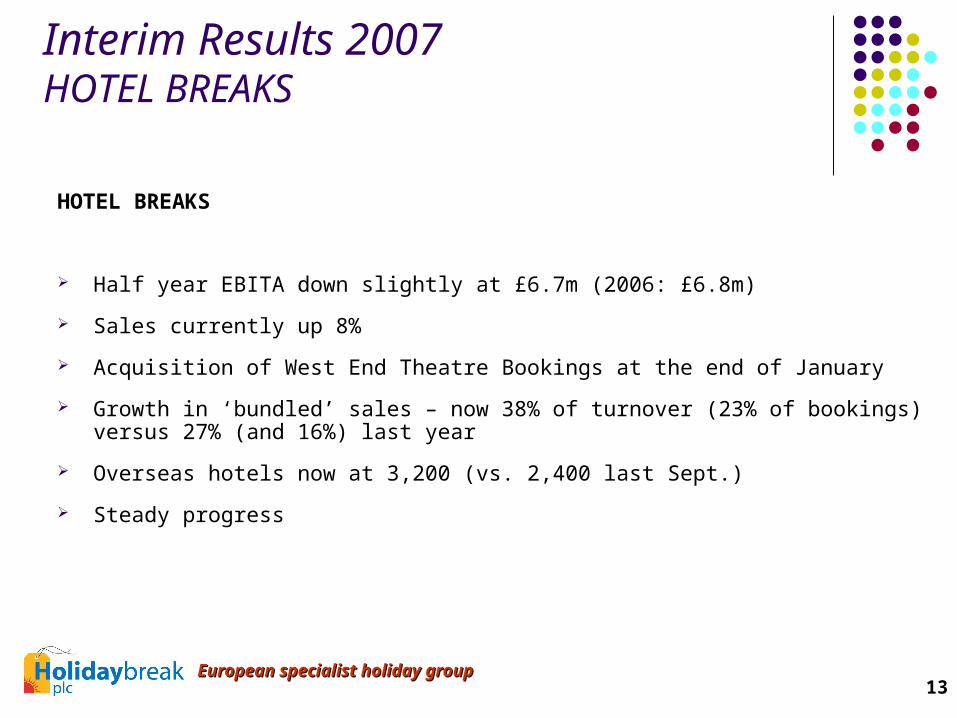

Interim Results 2007HOTEL BREAKS

HOTEL BREAKS

Half year EBITA down slightly at £6.7m (2006: £6.8m)

Sales currently up 8%

Acquisition of West End Theatre Bookings at the end of January

Growth in ‘bundled’ sales – now 38% of turnover (23% of bookings) versus 27% (and 16%) last year

Overseas hotels now at 3,200 (vs. 2,400 last Sept.)

Steady progress

14 European specialist holiday groupEuropean specialist holiday group

Interim Results 2007ADVENTURE TRAVEL

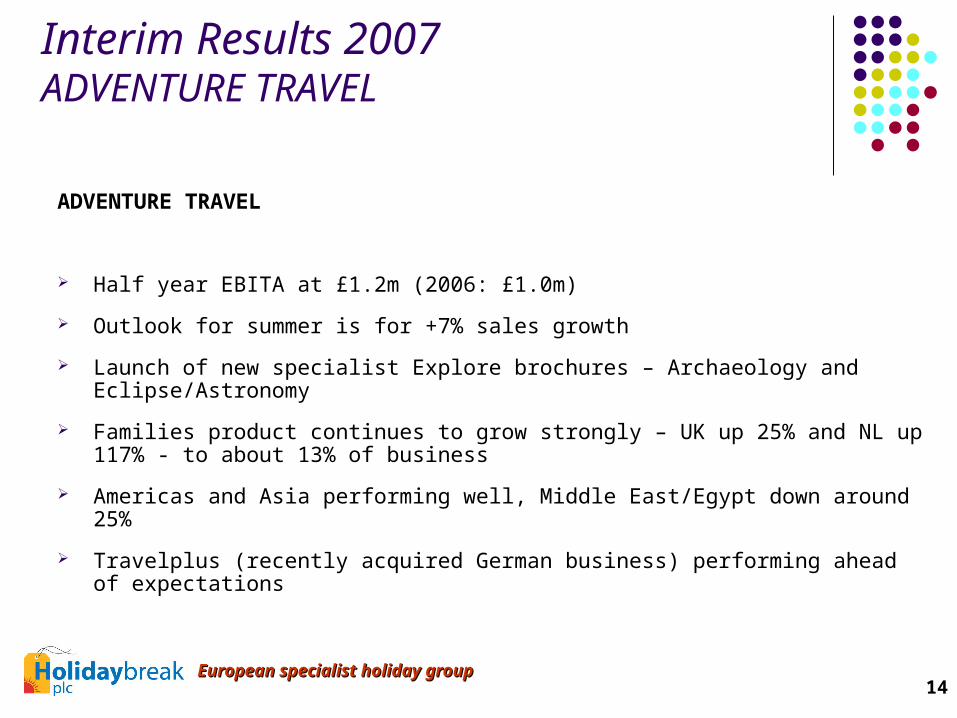

ADVENTURE TRAVEL

Half year EBITA at £1.2m (2006: £1.0m)

Outlook for summer is for +7% sales growth

Launch of new specialist Explore brochures – Archaeology and Eclipse/Astronomy

Families product continues to grow strongly – UK up 25% and NL up 117% - to about 13% of business

Americas and Asia performing well, Middle East/Egypt down around 25%

Travelplus (recently acquired German business) performing ahead of expectations

15 European specialist holiday groupEuropean specialist holiday group

Interim Results 2007CAMPING

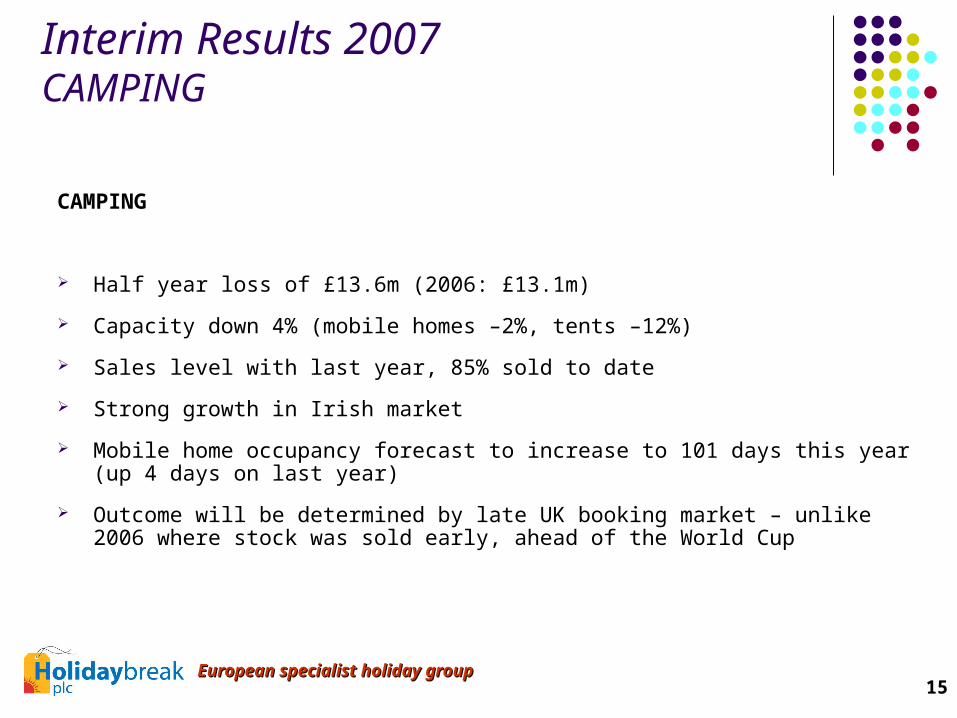

CAMPING

Half year loss of £13.6m (2006: £13.1m)

Capacity down 4% (mobile homes –2%, tents –12%)

Sales level with last year, 85% sold to date

Strong growth in Irish market

Mobile home occupancy forecast to increase to 101 days this year (up 4 days on last year)

Outcome will be determined by late UK booking market – unlike 2006 where stock was sold early, ahead of the World Cup

16 European specialist holiday groupEuropean specialist holiday group

Interim Results 2007STRATEGIC DEVELOPMENTS

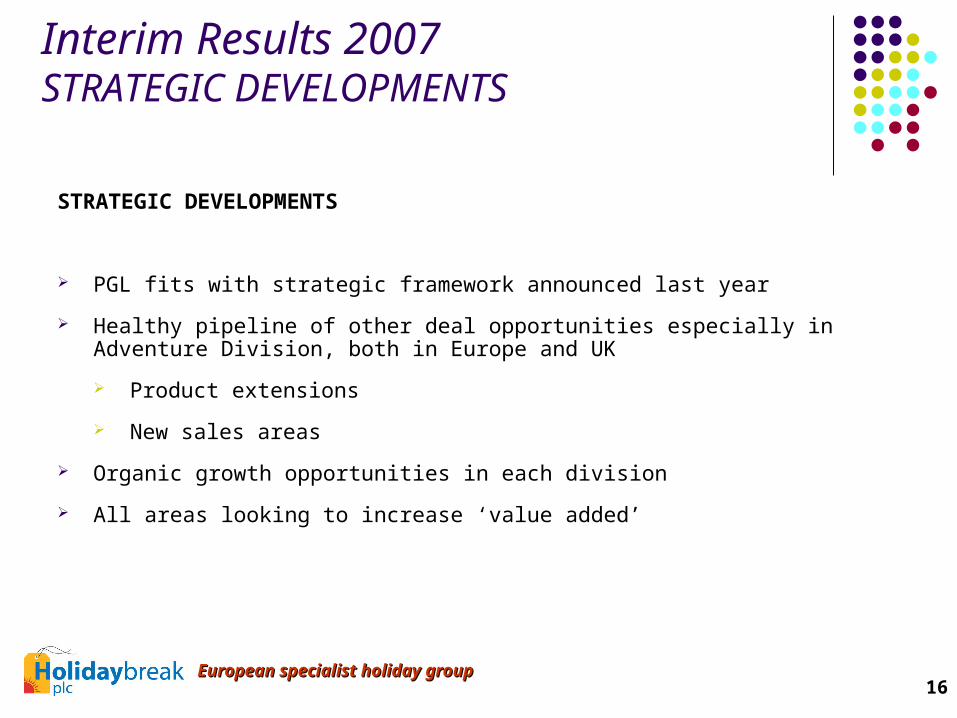

STRATEGIC DEVELOPMENTS

PGL fits with strategic framework announced last year

Healthy pipeline of other deal opportunities especially in Adventure Division, both in Europe and UK

Product extensions

New sales areas

Organic growth opportunities in each division

All areas looking to increase ‘value added’

17 European specialist holiday groupEuropean specialist holiday group

Interim Results 2007WEB DEVELOPMENTS

WEB DEVELOPMENTS

Hotel Breaks have launched PayPal processing, ‘My Holiday’ reviews, live hotel connectivity and RSS

Next projects to include gift certificates/vouchers, video streaming and web services (enabling content to be sent to more partners)

Indian software development - new XML links into Hotelnet will dramatically increase overseas supply

New website at Eurocamp Independent

Relaunch of Explore website. Podcasts and Weblogs launched last month

18 European specialist holiday groupEuropean specialist holiday group

Interim Results 2007OUTLOOK

OUTLOOK

Hotel Breaks

Sales intake for Hotel Breaks up 8%

Adventure

Current summer sales up 7%

Camping

Currently over 85% booked for the whole season

In line with plan

Satisfactory trading outcome anticipated

Proposed acquisition of PGL, Proposed acquisition of PGL, formation of Education divisionformation of Education division

20 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGLHighlights

PGL is UK market leader in residential, outdoor education and adventure sector for UK schools

c.250,000 children trips per annum, serve c.4,600 schools

Opportunity for growth

Experienced PGL management team remaining with the business

Creates fourth operating division for Holidaybreak, the Education Division, with good strategic fit

21 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Highlights

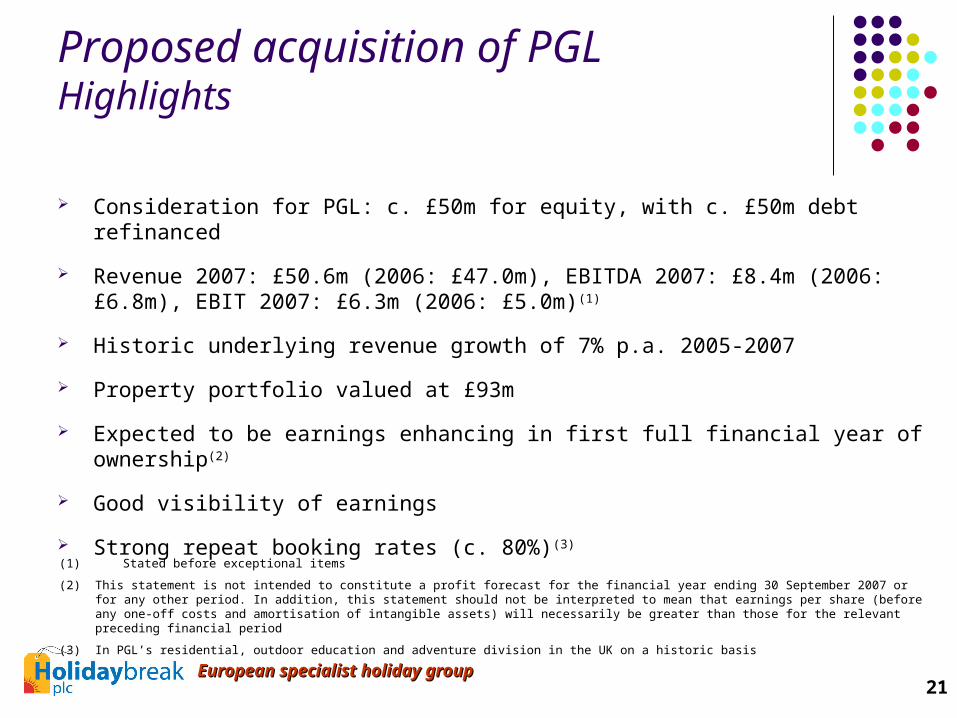

Consideration for PGL: c. £50m for equity, with c. £50m debt refinanced

Revenue 2007: £50.6m (2006: £47.0m), EBITDA 2007: £8.4m (2006: £6.8m), EBIT 2007: £6.3m (2006: £5.0m)(1)

Historic underlying revenue growth of 7% p.a. 2005-2007

Property portfolio valued at £93m

Expected to be earnings enhancing in first full financial year of ownership(2)

Good visibility of earnings

Strong repeat booking rates (c. 80%)(3)

(1) Stated before exceptional items

(2) This statement is not intended to constitute a profit forecast for the financial year ending 30 September 2007 or for any other period. In addition, this statement should not be interpreted to mean that earnings per share (before any one-off costs and amortisation of intangible assets) will necessarily be greater than those for the relevant preceding financial period

(3) In PGL’s residential, outdoor education and adventure division in the UK on a historic basis

22 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL The UK schools outdoor education and adventure market Opportunity for growth

Active promotion of benefits of outdoor learning by UK government

Trend towards more outsourcing to commercial operators

Increasing complexity of organising the trips

Health and safety requirements

Reduction in number of LEA centres

Direct funding of schools has reduced LEA financial resources

Schools have greater freedom to choose location and provider of school trips

23 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Information on PGL (1)

Market leader in the UK outdoor education and adventure sector with a strong brand position

Operates in providing residential activity centres, primarily at key stage two level for 8-12 year olds

Runs overseas school tours and ski trips, mainly targeted at secondary school children (12-18 year olds)

Brand respected in the market with 50 years of operation

Operates 26 activity centres, which are on average larger than other operators

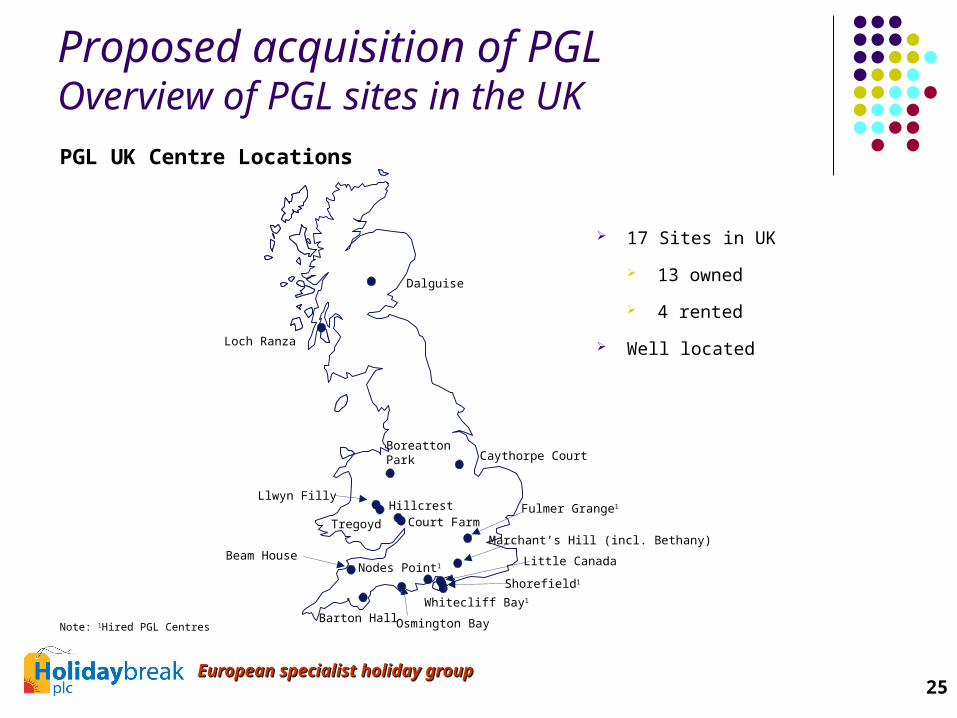

UK: 17 sites (13 owned); France: 8 sites (7 owned); Spain: 1 site

c.7,100 beds

PGL offers a wider range of activities

24 European specialist holiday groupEuropean specialist holiday group

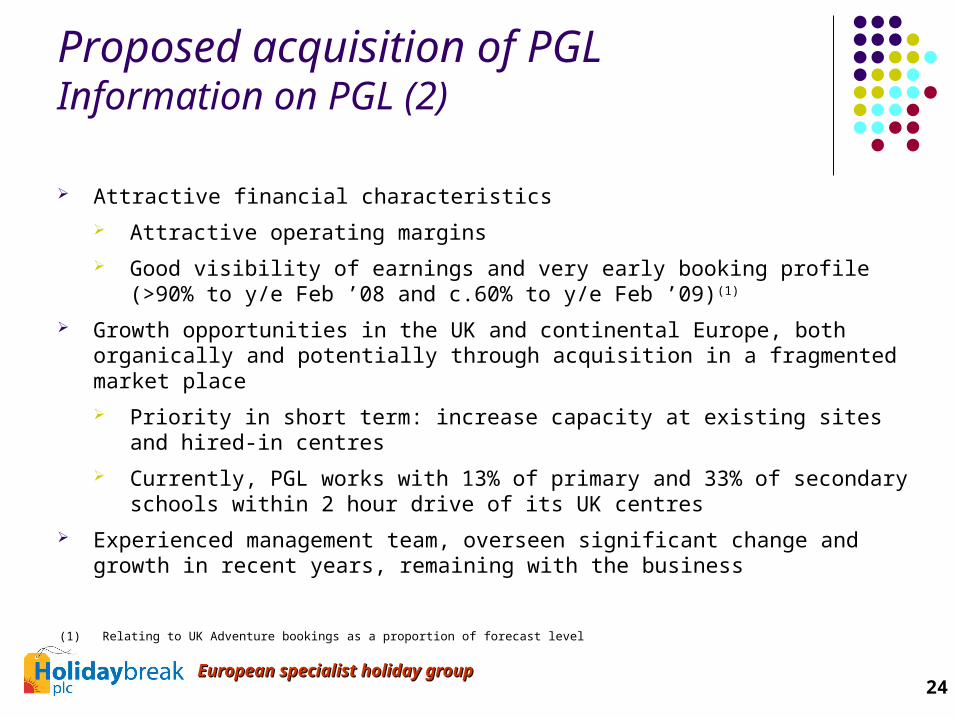

Proposed acquisition of PGL Information on PGL (2)

Attractive financial characteristics

Attractive operating margins

Good visibility of earnings and very early booking profile (>90% to y/e Feb ’08 and c.60% to y/e Feb ’09)(1)

Growth opportunities in the UK and continental Europe, both organically and potentially through acquisition in a fragmented market place

Priority in short term: increase capacity at existing sites and hired-in centres

Currently, PGL works with 13% of primary and 33% of secondary schools within 2 hour drive of its UK centres

Experienced management team, overseen significant change and growth in recent years, remaining with the business

(1) Relating to UK Adventure bookings as a proportion of forecast level

25 European specialist holiday groupEuropean specialist holiday group

17 Sites in UK

13 owned

4 rented

Well located

Dalguise

Caythorpe Court

Marchant’s Hill (incl. Bethany)

Little Canada

Osmington Bay

Beam House

Tregoyd

Hillcrest

Boreatton Park

Barton Hall

Loch Ranza

Llwyn FillyFulmer Grange1

Whitecliff Bay1

Court Farm

PGL UK Centre Locations

Proposed acquisition of PGL Overview of PGL sites in the UK

Note: 1Hired PGL Centres

Nodes Point1

Shorefield1

26 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Strategic rationale

PGL’s strong brand and market leading position consistent with characteristics of Holidaybreak’s other divisions

History of growth and good margins

PGL enjoys a complementary seasonality to Holidaybreak, especially its Camping Division Efficiencies in recruitment, training and retention of seasonal staff Utilisation of Camping Division spare capacity during PGL’s peak periods Enhance Camping Division offering with PGL-supplied activities

Over time, potential to exploit Complementary marketing and distribution (e.g. Explore’s School Adventure product) Transfer of management and operational skills (e.g. capacity management) New product and geographical development (strengthen presence in UK regions with

sparse centre coverage, investigate other sites in NW Europe)

27 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Integration plans

PGL to become the fourth operating division of Holidaybreak – Education Division

Martin Davies, PGL’s CEO, to continue in this role post acquisition as MD of Education Division and join Holidaybreak’s plc board

Other senior PGL management to remain

As with existing three divisions, continue to operate relatively autonomously

28 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Summary terms and financial effects of the acquisition Acquisition to be financed from an increased bank facility

Completion, subject to shareholder approval, expected to occur in June 2007

The acquisition of PGL is expected to:

be earnings enhancing in the first full financial year of ownership(1)

create returns in excess of the Group’s weighted average cost of capital(1)

(1) These statements are not intended to constitute a profit forecast for the financial year ending 30 September 2007 or for any other period. In addition, these statements should not be interpreted to mean that earnings per share (before any one off costs and amortisation of intangible assets) will necessarily be greater than those for the relevant preceding financial period.

29 European specialist holiday groupEuropean specialist holiday group

Proposed acquisition of PGL Summary Acquisition of PGL for c. £50m, with existing c. £50m debt refinanced

Strong brand and market leading position

Excellent repeat bookings and high visibility of earnings due to very early booking profile

A well located property portfolio

Opportunities for growth

Active promotion of benefits of outdoor learning by UK government

Trend to outsourcing

Reduction in number of LEA centres

Potential to exploit opportunities with existing Holidaybreak group

Acquisition expected to be earnings enhancing in the first full financial year of ownership(1)

(1) This statement is not intended to constitute a profit forecast for the financial year ending 30 September 2007 or for any other period. In addition, this statement should not be interpreted to mean that earnings per share (before any one off costs and amortisation of intangible assets) will necessarily be greater than those for the relevant preceding financial period.

AppendicesAppendices

31 European specialist holiday groupEuropean specialist holiday group

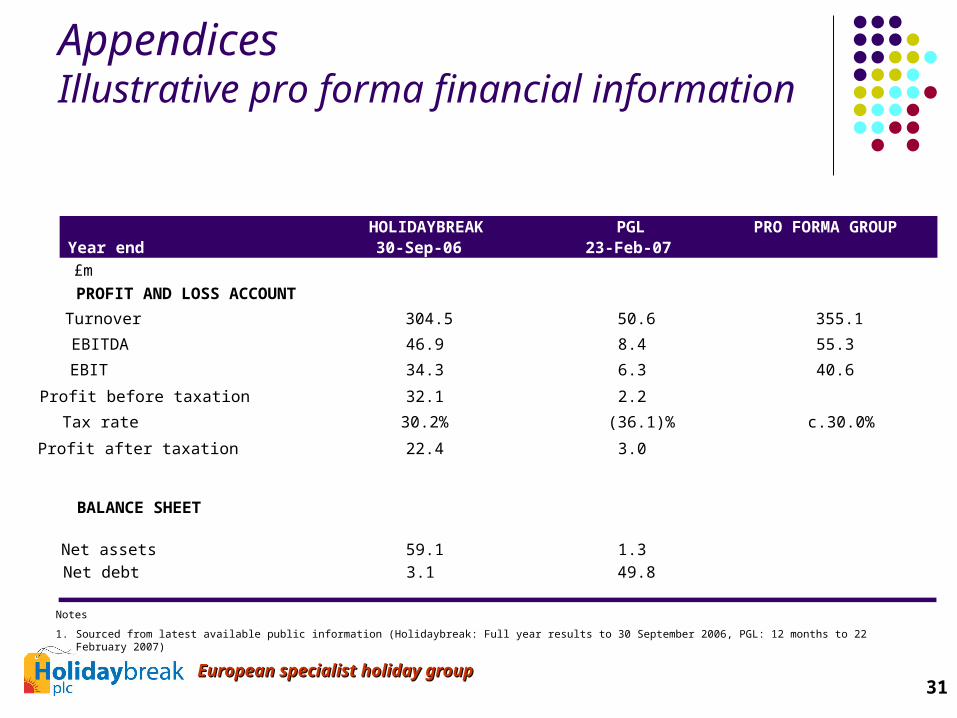

AppendicesIllustrative pro forma financial information

HOLIDAYBREAK PGL PRO FORMA GROUPYear end 30-Sep-06 23-Feb-07

PROFIT AND LOSS ACCOUNT

Turnover 304.5 50.6 355.1

EBITDA 46.9 8.4 55.3

EBIT 34.3 6.3 40.6

Profit before taxation 32.1 2.2

Tax rate 30.2% (36.1)% c.30.0%

Profit after taxation 22.4 3.0

BALANCE SHEET

Net assets 59.1 1.3

Net debt 3.1 49.8

£m

Notes

1. Sourced from latest available public information (Holidaybreak: Full year results to 30 September 2006, PGL: 12 months to 22 February 2007)

32 European specialist holiday groupEuropean specialist holiday group

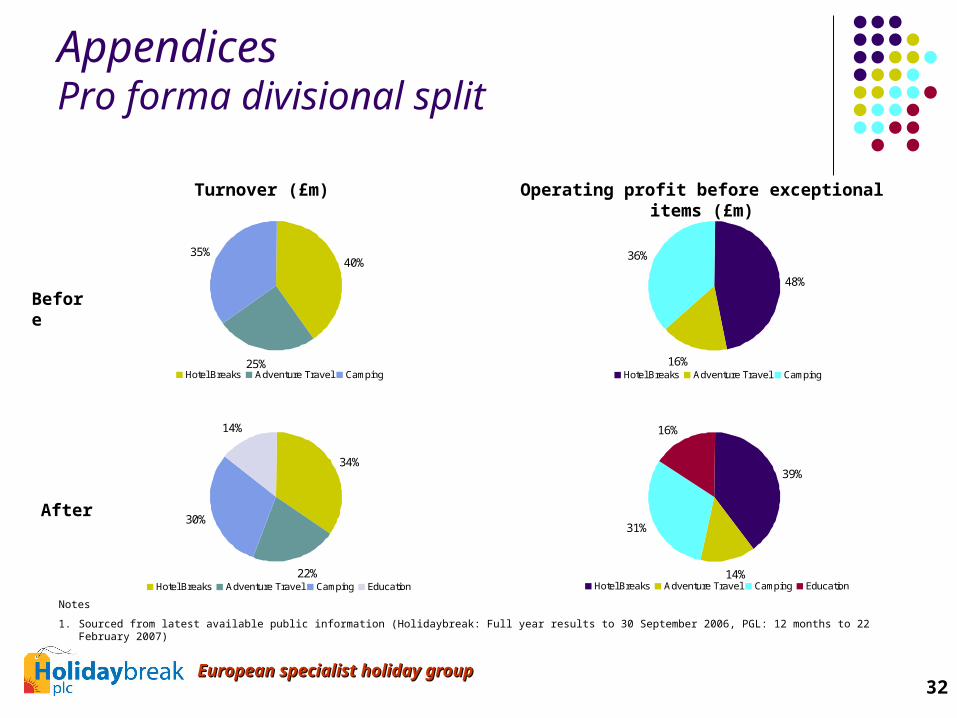

Turnover (£m) Operating profit before exceptional items (£m)

39%

14%

31%

16%

Hotel Breaks Adventure Travel Camping Education

Notes

1. Sourced from latest available public information (Holidaybreak: Full year results to 30 September 2006, PGL: 12 months to 22 February 2007)

34%

22%

30%

14%

Hotel Breaks Adventure Travel Camping Education

AppendicesPro forma divisional split

48%

16%

36%

Hotel Breaks Adventure Travel Camping

40%

25%

35%

Hotel Breaks Adventure Travel Camping

Before

After

33 European specialist holiday groupEuropean specialist holiday group

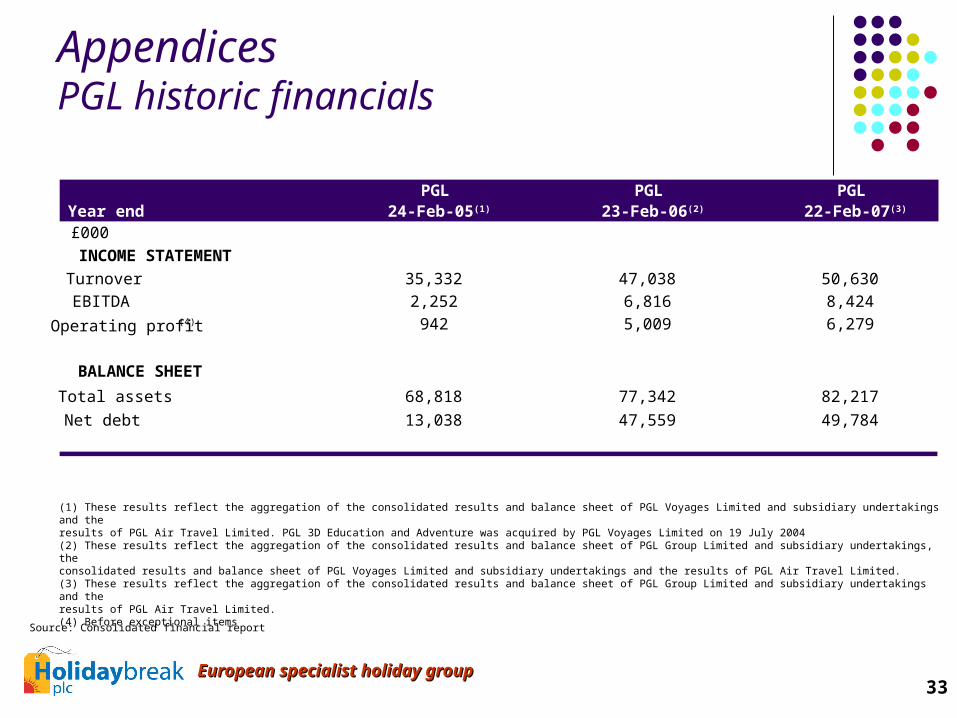

AppendicesPGL historic financials

PGL PGL PGLYear end 24-Feb-05(1) 23-Feb-06(2) 22-Feb-07(3)

£000

INCOME STATEMENT

Turnover 35,332 47,038 50,630

EBITDA 2,252 6,816 8,424

Operating profit(4) 942 5,009 6,279

BALANCE SHEET

Total assets 68,818 77,342 82,217

Net debt 13,038 47,559 49,784

(1) These results reflect the aggregation of the consolidated results and balance sheet of PGL Voyages Limited and subsidiary undertakings and theresults of PGL Air Travel Limited. PGL 3D Education and Adventure was acquired by PGL Voyages Limited on 19 July 2004(2) These results reflect the aggregation of the consolidated results and balance sheet of PGL Group Limited and subsidiary undertakings, theconsolidated results and balance sheet of PGL Voyages Limited and subsidiary undertakings and the results of PGL Air Travel Limited.(3) These results reflect the aggregation of the consolidated results and balance sheet of PGL Group Limited and subsidiary undertakings and theresults of PGL Air Travel Limited.(4) Before exceptional items

Source: Consolidated financial report

34 European specialist holiday groupEuropean specialist holiday group

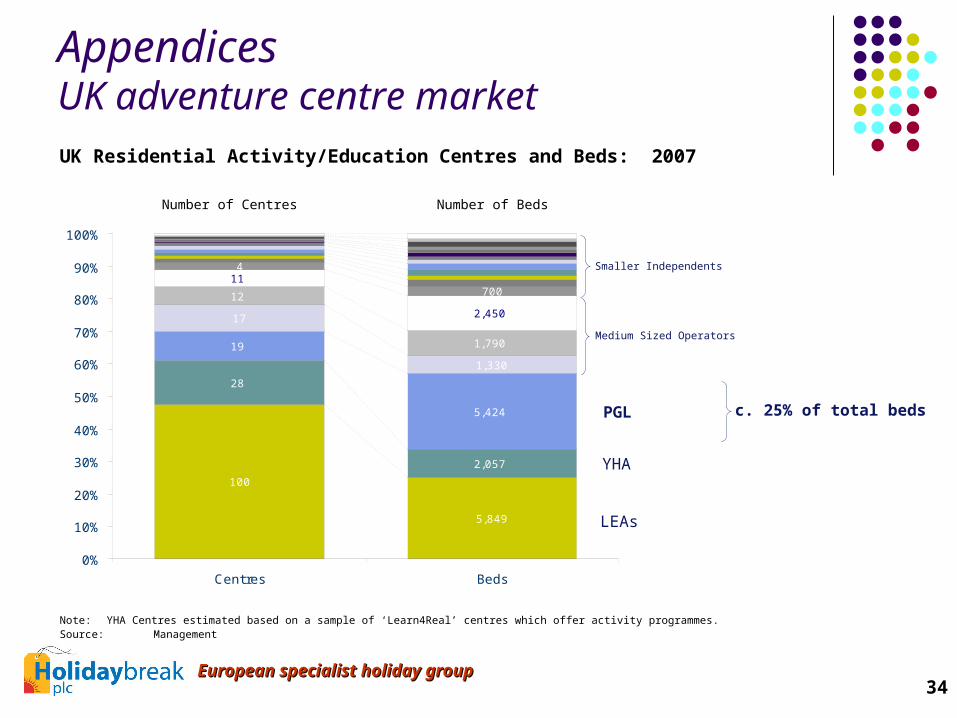

Note: YHA Centres estimated based on a sample of ‘Learn4Real’ centres which offer activity programmes. Source: Management

AppendicesUK adventure centre marketUK Residential Activity/Education Centres and Beds: 2007

Number of Centres Number of Beds

100

5,849

28

19

5,424

17

1,330

12

1,790

11

2,450

4

700

2,057

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Centres Beds

LEAs

YHA

PGL

Smaller Independents

c. 25% of total beds

Medium Sized Operators

35 European specialist holiday groupEuropean specialist holiday group

Appendices Acquisition accounting

Under IFRS, PGL’s forward order book, customer lists and brand value will be treated as intangible assets and shown at fair value in the balance sheet

Approximate values are:

Brand £12m

Customer lists £3.2m

Order book £0.8m

Intangible assets will be amortised as revenue - approx full year charge will be £0.6m.

The amortisation will be above the operating profit line and will impact reported earnings

It is expected that the amortisation will be detailed as a separate line items on the face of the income statement