Embed Size (px)

Citation preview

Introduction to Financial Engineering

Aashish Dhakal

Week 5: Exotics Option

Exotic Option

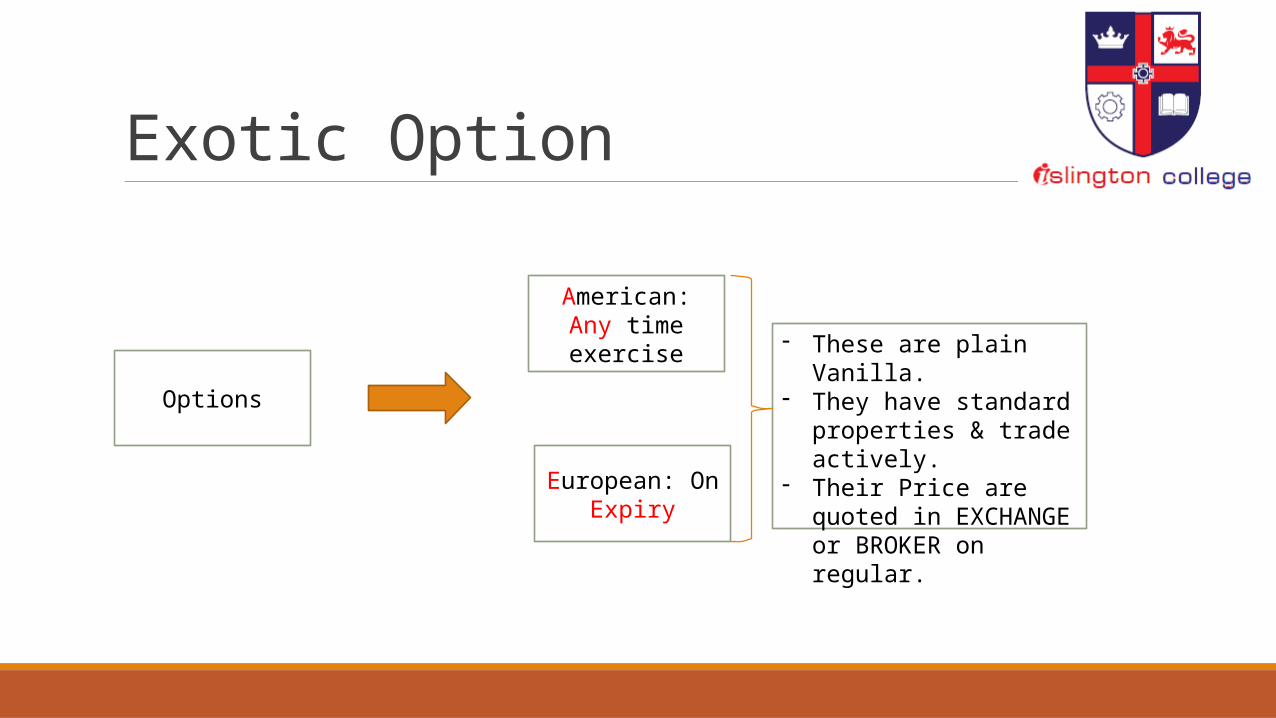

Options

European: On Expiry

American: Any time exercise - These are plain Vanilla.

- They have standard properties & trade actively.

- Their Price are quoted in EXCHANGE or BROKER on regular.

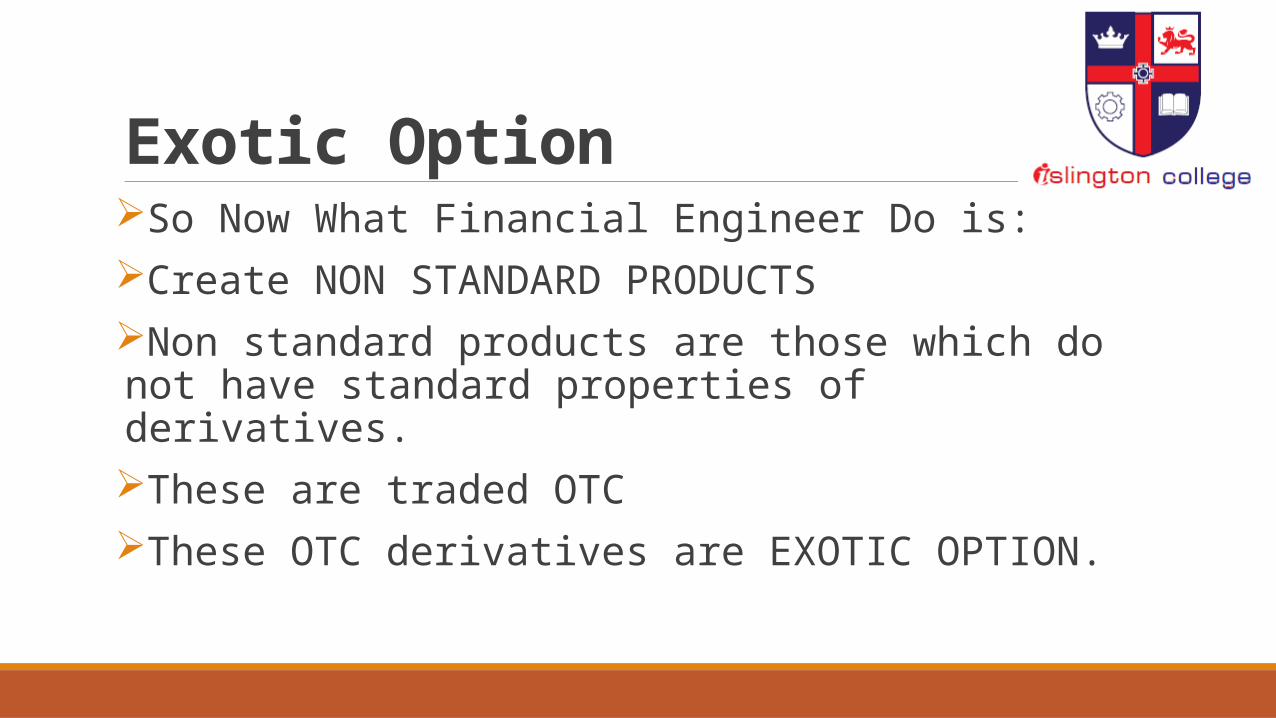

Exotic OptionSo Now What Financial Engineer Do is:Create NON STANDARD PRODUCTSNon standard products are those which do not have standard properties of derivatives.These are traded OTCThese OTC derivatives are EXOTIC OPTION.

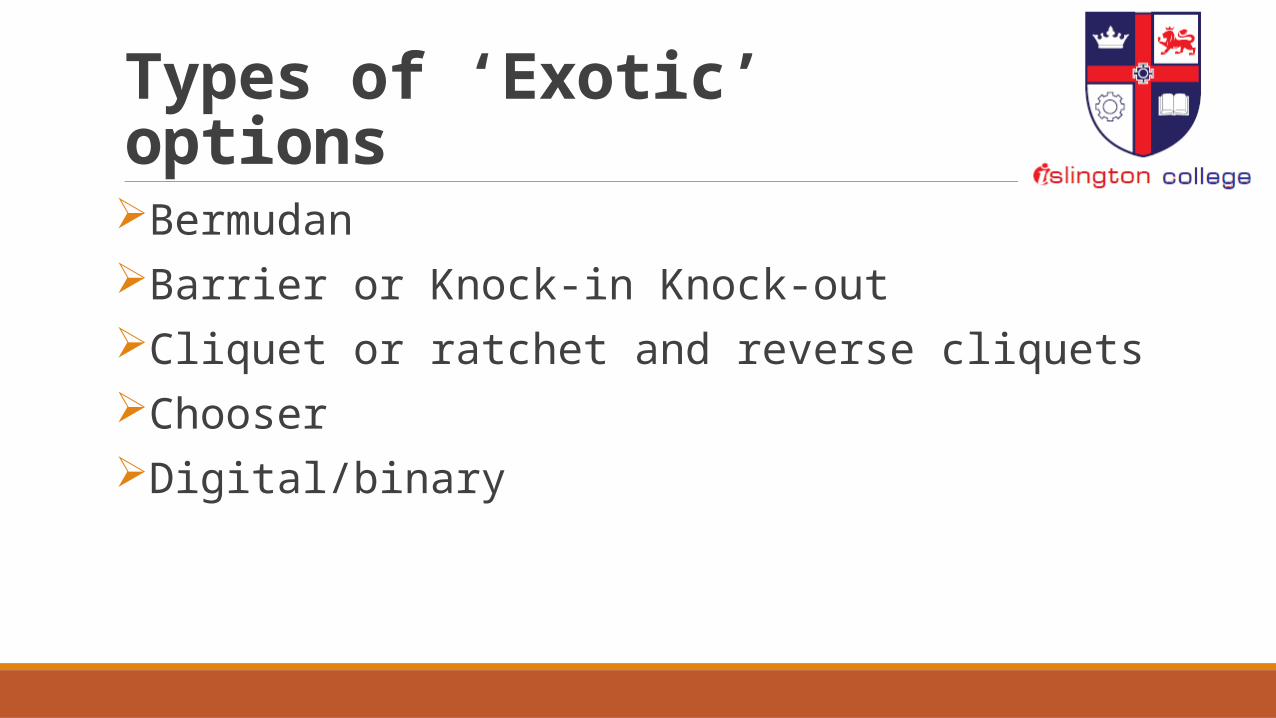

Types of ‘Exotic’optionsBermudanBarrier or Knock-in Knock-outCliquet or ratchet and reverse cliquetsChooserDigital/binary

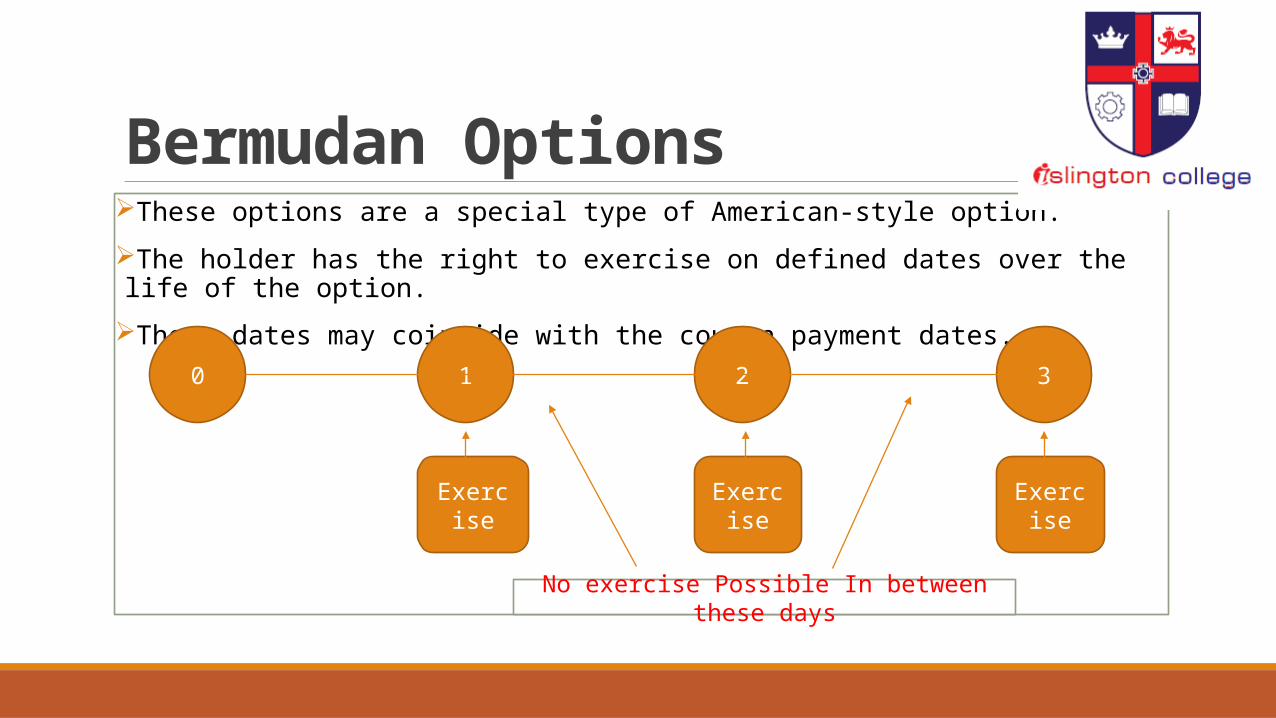

Bermudan OptionsThese options are a special type of American-style option.

The holder has the right to exercise on defined dates over the life of the option.

These dates may coincide with the coupon payment dates.

0 1 2 3

Exercise ExerciseExercise

No exercise Possible In between these days

Barrier OptionsBarrier Options are those option whose Pay-Off depends on whether the underlying asset price reaches a certain level during the period of time.

Barrier OptionsBarrier option can be classified as either: A. Knock-Out Options B. Knock- In Optionsknock – out: Option ceases to exist when the underlying Asset Reaches a certain barrier.Knock-In: Option comes into existence only when the underlying Asset reaches a Barrier.

Example: Knock- In PUT A knock-in put option with strike E = 4000 and barrier H = 3900, will only come in to existence when the index value of 3900 is hit. If it fails to hit the barrier there will be zero pay out even if the underlying (S) is below E at expiration (NB rebates may be paid in some cases)

i.e Even if the option is ITM no exercise until barrier is reached.

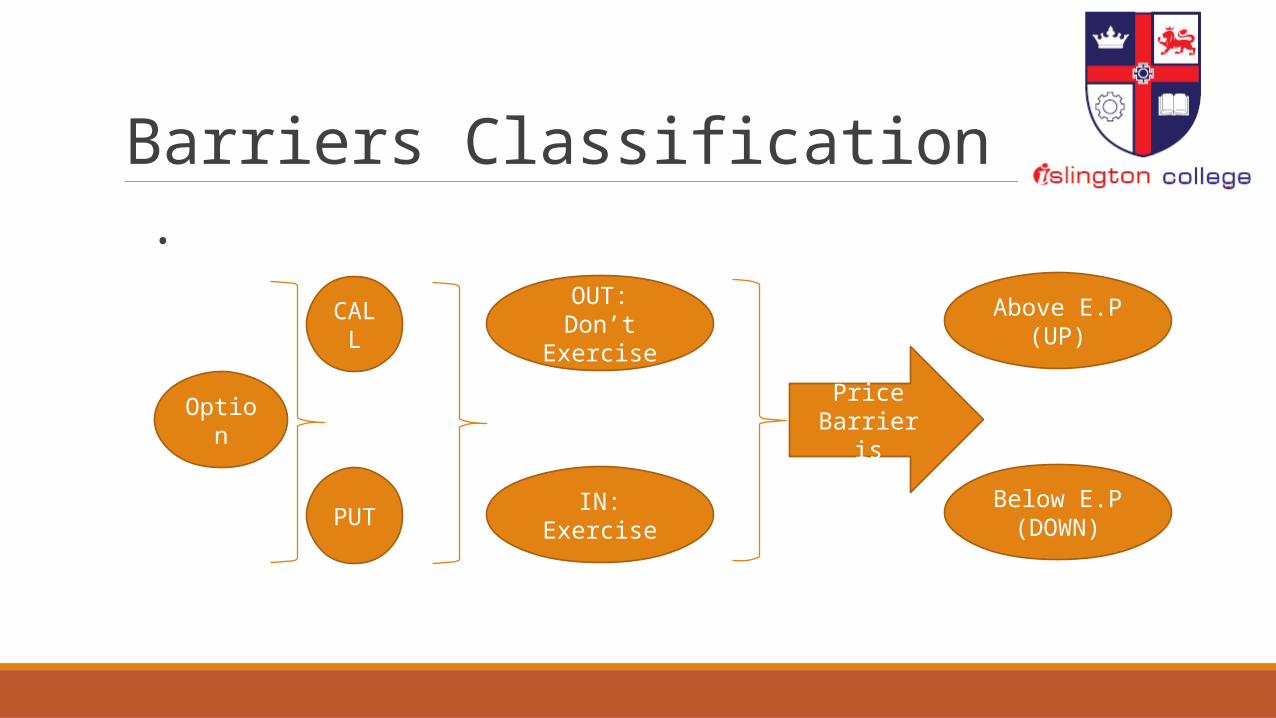

Barriers Classification .

Option

PUT

CALL

IN: Exercise

OUT: Don’t Exercise

Below E.P (DOWN)

Above E.P (UP)

Price Barrier is

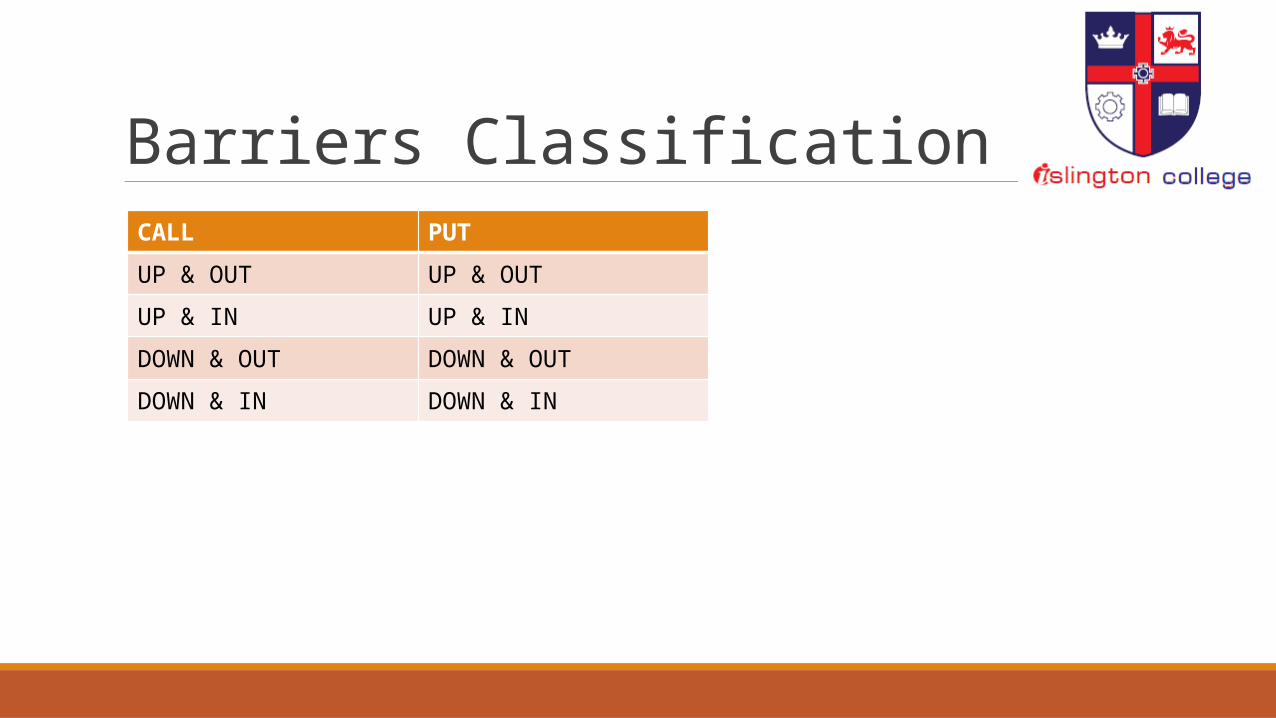

Barriers ClassificationCALL PUT

UP & OUT UP & OUT

UP & IN UP & IN

DOWN & OUT DOWN & OUT

DOWN & IN DOWN & IN

Pricing BarriersPricing is Based on B & S model.So we shall deal the same in Next Class while studying B & S in detail.

Cliquet or RatchetoptionsThese instruments start out as normal call options with a fixed strike price.But as time passes the strike is reset to be equal to the underlying asset.This occurs on PRE-SPECIFIED dates.

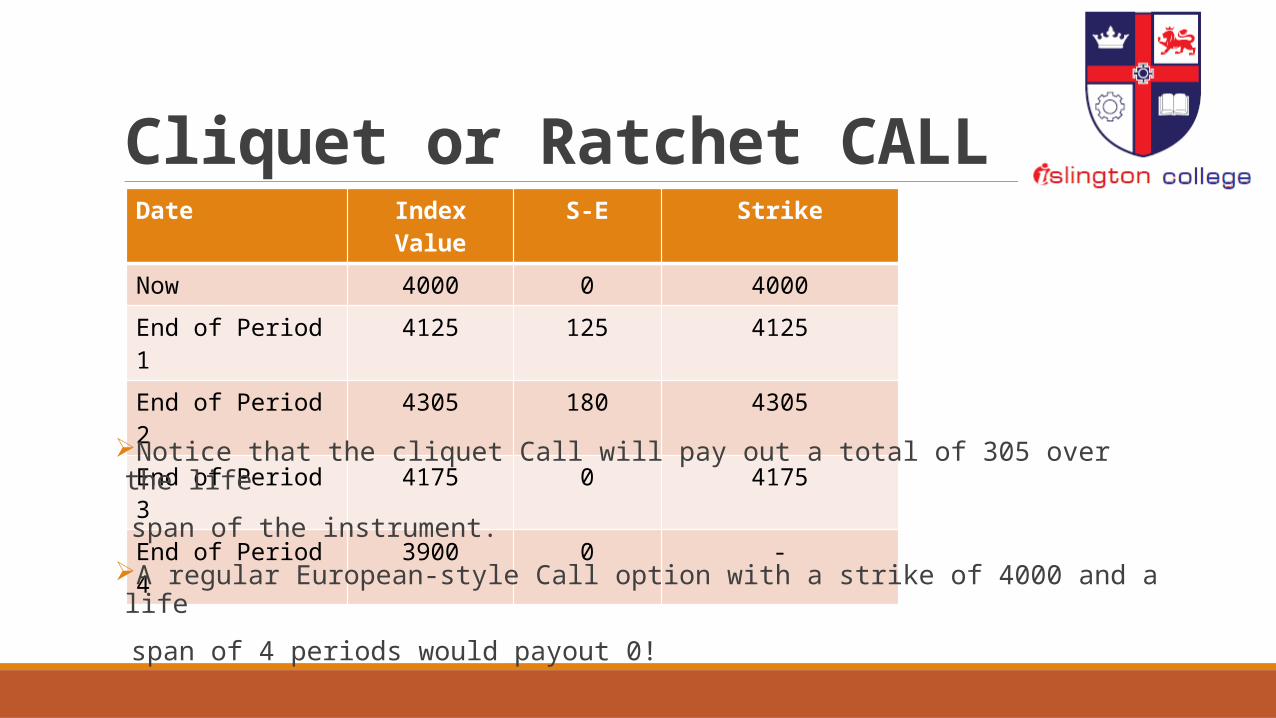

Cliquet or Ratchet CALL Date Index Value S-E Strike

Now 4000 0 4000

End of Period 1 4125 125 4125

End of Period 2 4305 180 4305

End of Period 3 4175 0 4175

End of Period 4 3900 0 -

Notice that the cliquet Call will pay out a total of 305 over the life

span of the instrument.

A regular European-style Call option with a strike of 4000 and a life

span of 4 periods would payout 0!

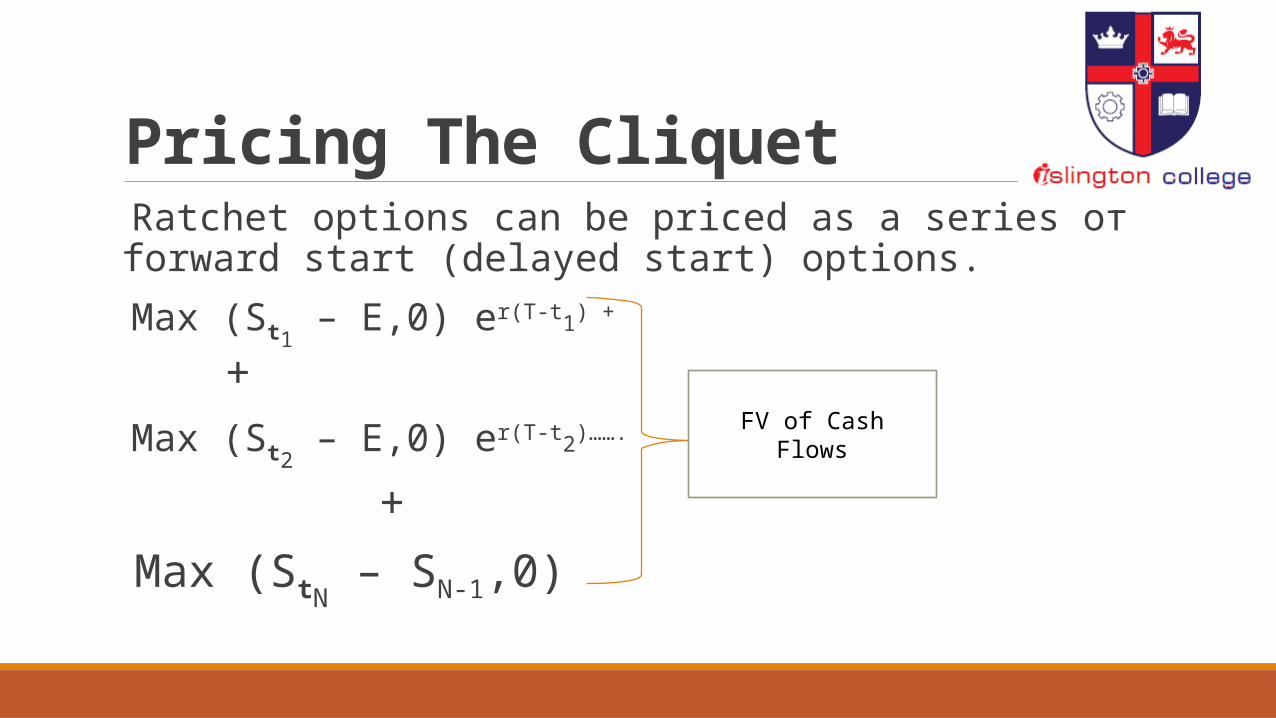

Pricing The Cliquet Ratchet options can be priced as a series of forward start (delayed start) options. Max (St1

– E,0) er(T-t1) +

+ Max (St2

– E,0) er(T-t2)…….

+ Max (StN

– SN-1,0)

FV of Cash Flows

Chooser OptionsThis instrument gives the holder the opportunity at some point in time ti ,

for ti <= T,

to decide whether the option being held is a call or a put.

Pricing can be performed in a B&S framework.

Chooser OptionsThis instrument gives the holder the opportunity at some point in time ti ,

for ti <= T,

to decide whether the option being held is a call or a put.

Pricing can be performed in a B&S framework.

Digital: Cash-or-nothing pay outsA digital call option pays out a fixed sum (Q)

if the underlying finishes above the strike

and nothing if the underlying finishes at or below the strike.

A.

In this type of structure the principal is guaranteed

but the final interest pay out is determined by

the path followed by the underlying reference index.