Embed Size (px)

Citation preview

January 2016

Investor Presentation

SAFE HARBOR

2

This presentation includes forward-looking statements. Wayfair Inc. (“Wayfair” or the “Company”) has

based these forward-looking statements largely on its current expectations and projections about future

events and financial trends affecting its business. Forward-looking statements should not be read as

guarantees of future performance or results, and will not necessarily be accurate indications of the times at,

or by, which such performance or results will be achieved. Forward-looking statements are based on

information available at the date of this presentation and management’s good faith belief as of such date

with respect to future events, and are subject to risks and uncertainties that could cause actual

performance or results to differ materially from those expressed in or suggested by the forward-looking

statements. Important factors that could cause such differences include, but are not limited to: our ability to

acquire new customers, our ability to sustain and/or manage our growth, our ability to increase our net

revenue per active customer, our ability to build and maintain strong brands and other factors discussed

under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” in periodic filings with the Securities and Exchange Commission (the “SEC”). In addition, in this

presentation, the words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,”

“predict,” “potential” and similar expressions, as they relate to the Company, business and management,

are intended to identify forward-looking statements. In light of these risks and uncertainties, the future

events and circumstances discussed in this presentation may not occur, and actual results could differ

materially from those anticipated or implied in the forward-looking statements. Forward-looking statements

speak only as of the date of this presentation. You should not put undue reliance on any forward-looking

statement. The Company assumes no obligation to update any forward-looking statements to reflect actual

results, changes in assumptions or changes in other factors affecting future performance or results, except

to the extent required by applicable laws. If the Company updates one or more forward-looking statements,

no inference should be drawn that it will make additional updates with respect to those or other forward-

looking statements.

OUR MISSION

3

To transform the way people

shop for their homes

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 LTM

A CLEAR ONLINE LEADER IN HOME GOODS

4

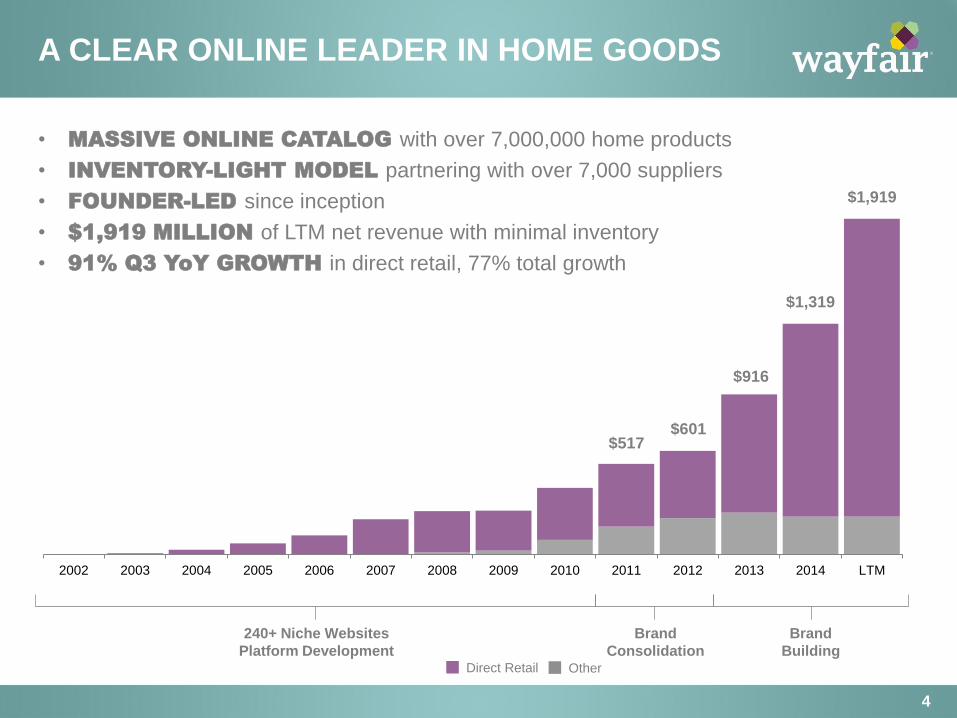

• MASSIVE ONLINE CATALOG with over 7,000,000 home products

• INVENTORY-LIGHT MODEL partnering with over 7,000 suppliers

• FOUNDER-LED since inception

• $1,919 MILLION of LTM net revenue with minimal inventory

• 91% Q3 YoY GROWTH in direct retail, 77% total growth

240+ Niche Websites

Platform Development

Brand

Consolidation

Brand

Building

$1,319

$916

$601 $517

Other Direct Retail

$1,919

FIVE DISTINCT HOME BRANDS

5

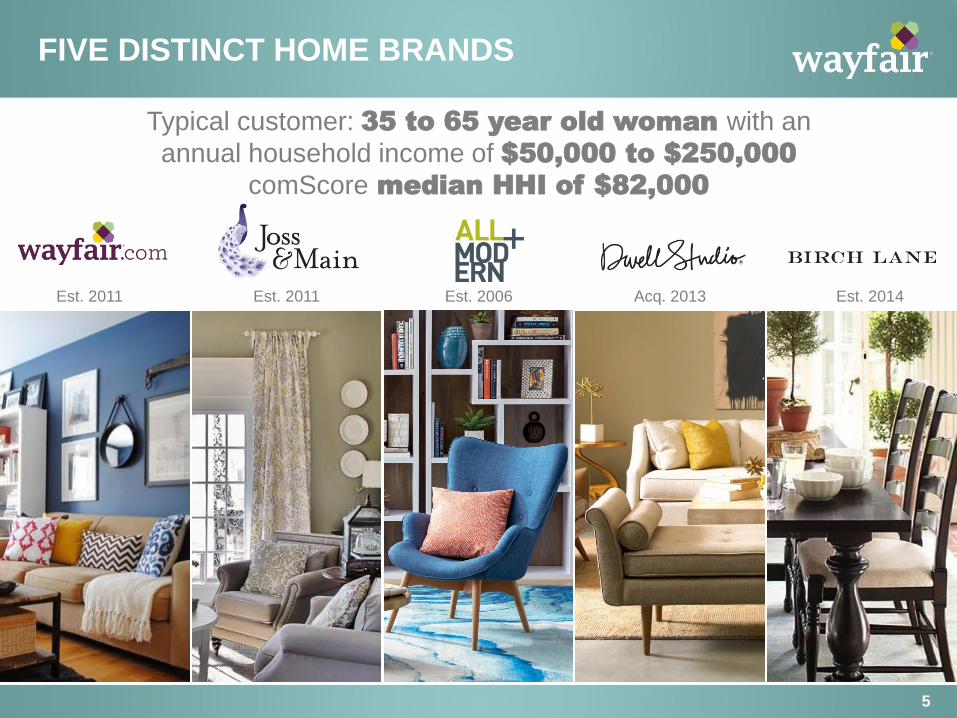

Typical customer: 35 to 65 year old woman with an

annual household income of $50,000 to $250,000

comScore median HHI of $82,000

Est. 2011 Est. 2011 Est. 2006 Est. 2014 Acq. 2013

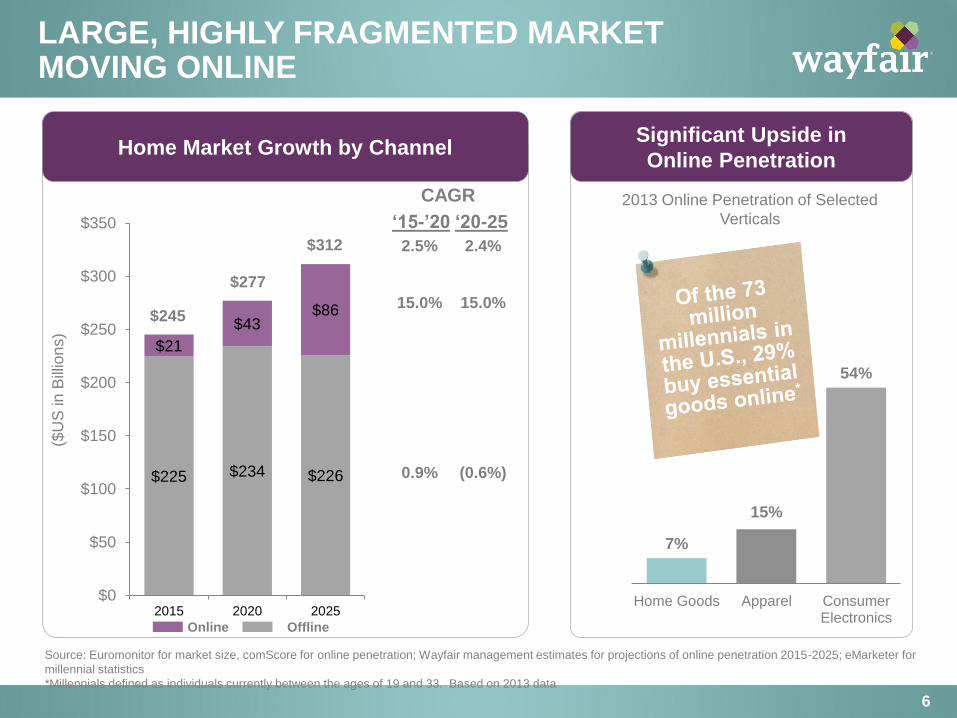

LARGE, HIGHLY FRAGMENTED MARKET MOVING ONLINE

6

Source: Euromonitor for market size, comScore for online penetration; Wayfair management estimates for projections of online penetration 2015-2025; eMarketer for

millennial statistics

*Millennials defined as individuals currently between the ages of 19 and 33. Based on 2013 data

7%

15%

54%

Home Goods Apparel ConsumerElectronics

Significant Upside in

Online Penetration

2013 Online Penetration of Selected

Verticals

Home Market Growth by Channel

15.0% 15.0%

(0.6%) 0.9%

91%

‘15-’20 ‘20-25

CAGR

2.5% 2.4%

$225 $234 $226

$21

$43 $86

$0

$50

$100

$150

$200

$250

$300

$350

2015 2020 2025

$277

$312

$245

($U

S in B

illio

ns)

Online Offline

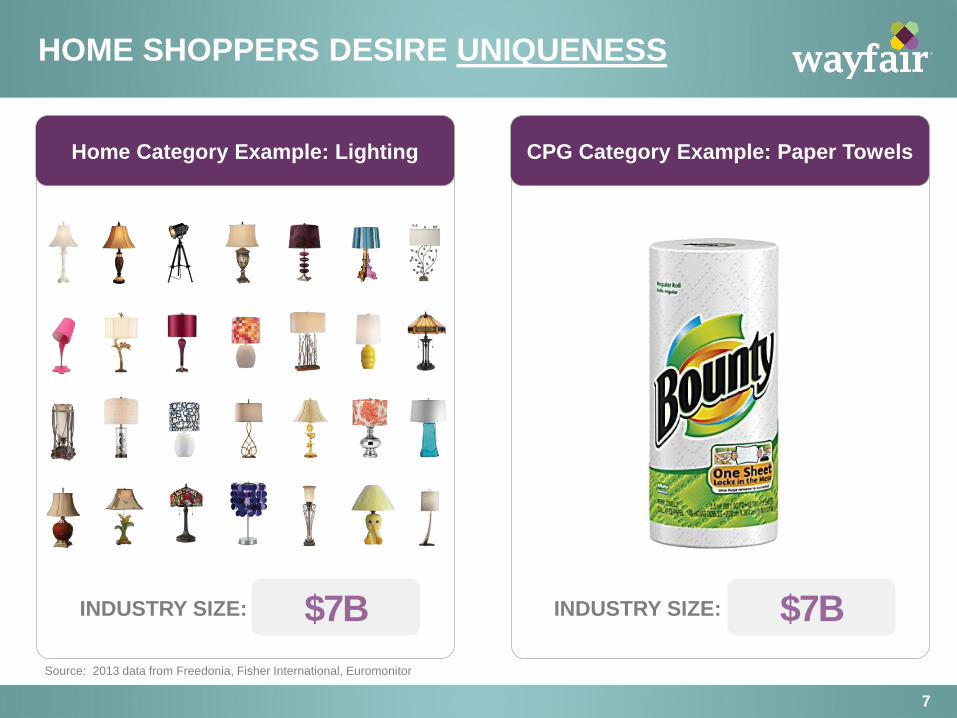

CPG Category Example: Paper Towels Home Category Example: Lighting

HOME SHOPPERS DESIRE UNIQUENESS

7

Source: 2013 data from Freedonia, Fisher International, Euromonitor

INDUSTRY SIZE: $7B INDUSTRY SIZE: $7B

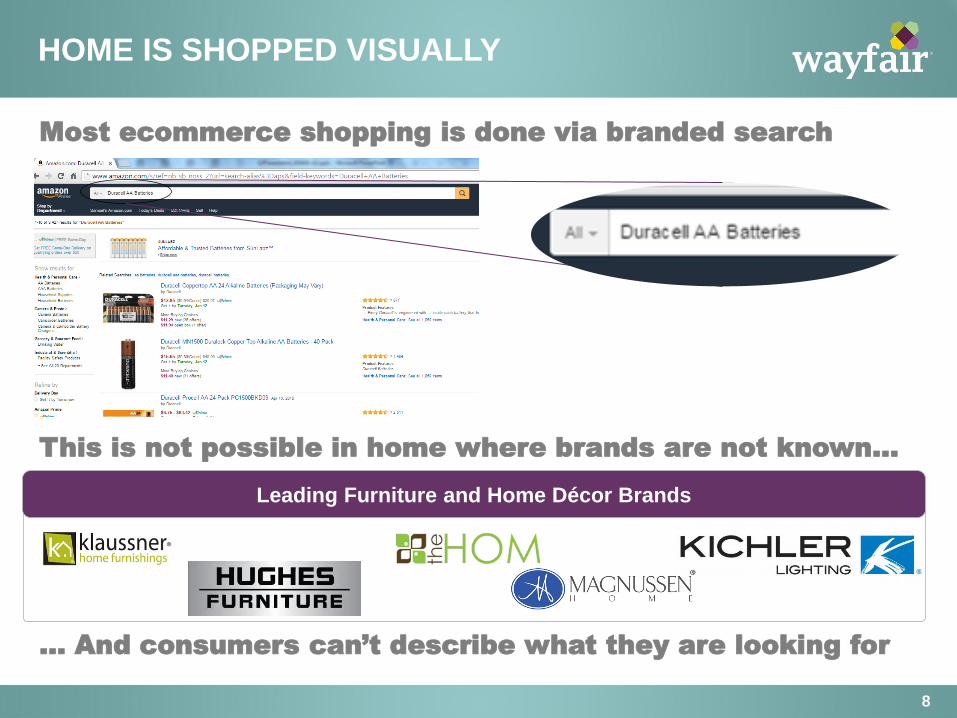

HOME IS SHOPPED VISUALLY

8

Most ecommerce shopping is done via branded search

This is not possible in home where brands are not known…

… And consumers can’t describe what they are looking for

Leading Furniture and Home Décor Brands

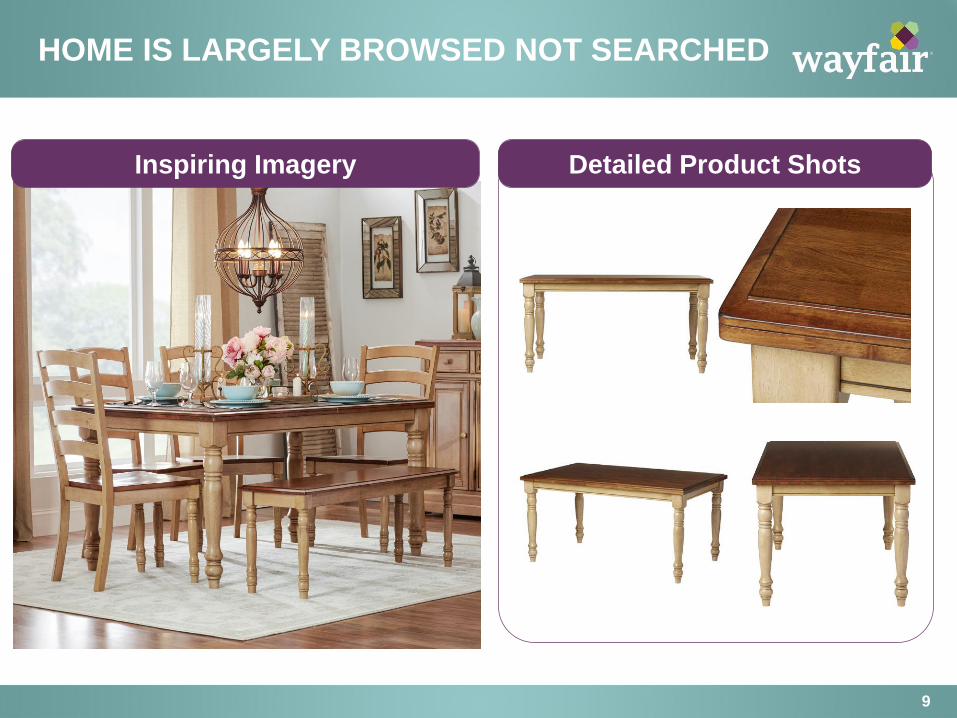

HOME IS LARGELY BROWSED NOT SEARCHED

9

Inspiring Imagery Detailed Product Shots

WAYFAIR IS WELL POSITIONED RELATIVE TO OTHER RETAILERS…

10

High End ($175K+)

Mass Market ($60K-$175K)

Low End ($60K)

Design Centers

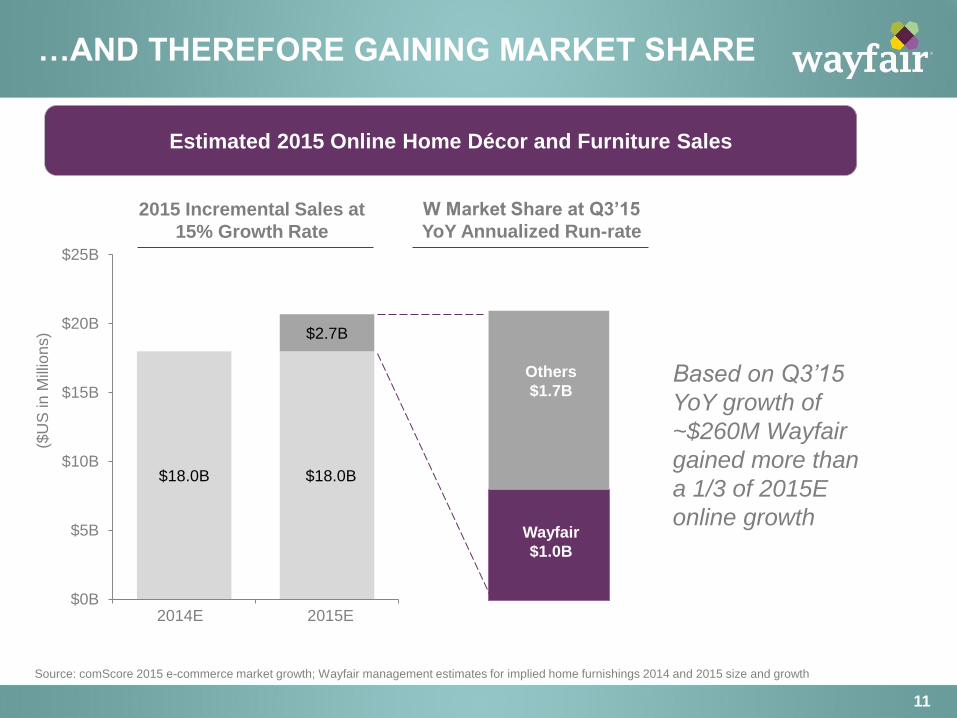

…AND THEREFORE GAINING MARKET SHARE

11

$18.0B $18.0B

$2.7B

$0B

$5B

$10B

$15B

$20B

$25B

1 22014E 2015E

($U

S in M

illio

ns)

Wayfair

$1.0B

Others

$1.7B

Estimated 2015 Online Home Décor and Furniture Sales

2015 Incremental Sales at

15% Growth Rate

W Market Share at Q3’15

YoY Annualized Run-rate

Based on Q3’15

YoY growth of

~$260M Wayfair

gained more than

a 1/3 of 2015E

online growth

Source: comScore 2015 e-commerce market growth; Wayfair management estimates for implied home furnishings 2014 and 2015 size and growth

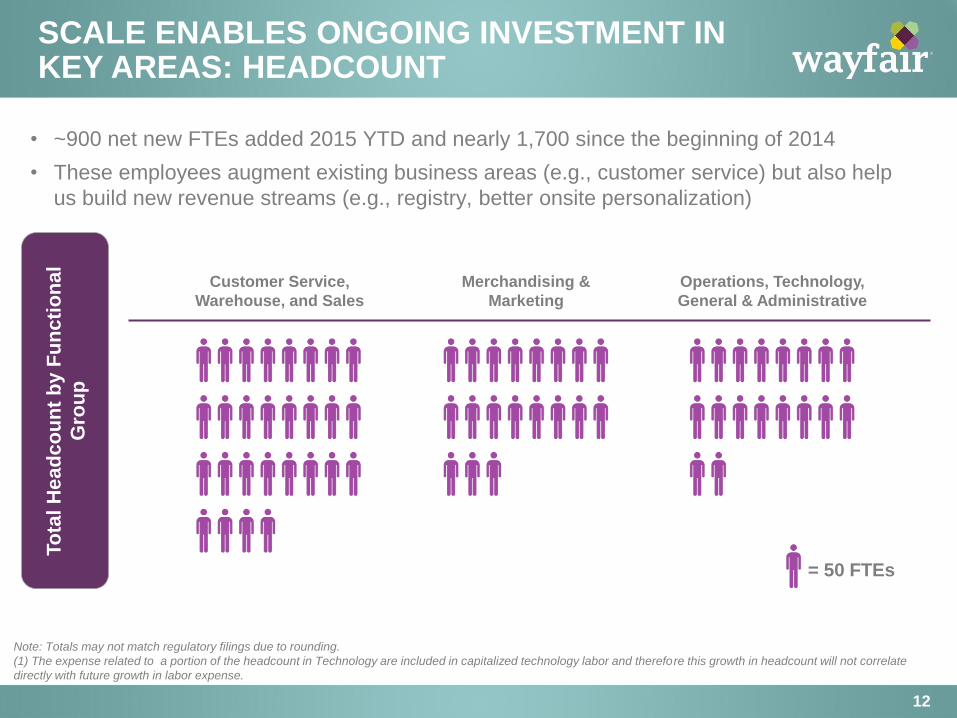

SCALE ENABLES ONGOING INVESTMENT IN KEY AREAS: HEADCOUNT

12

Customer Service,

Warehouse, and Sales

Merchandising &

Marketing

Operations, Technology,

General & Administrative

• ~900 net new FTEs added 2015 YTD and nearly 1,700 since the beginning of 2014

• These employees augment existing business areas (e.g., customer service) but also help

us build new revenue streams (e.g., registry, better onsite personalization)

Note: Totals may not match regulatory filings due to rounding.

(1) The expense related to a portion of the headcount in Technology are included in capitalized technology labor and therefore this growth in headcount will not correlate

directly with future growth in labor expense.

= 50 FTEs

To

tal

He

ad

co

un

t b

y F

un

cti

on

al

Gro

up

SCALE ENABLES ONGOING INVESTMENT IN KEY AREAS: PRIVATE LABEL

13

• Partnering with suppliers to develop proprietary brands with exclusive products and

no inventory

• Products are photographed and merchandized by Wayfair to create a curated brand

experience across multiple aesthetics and price points

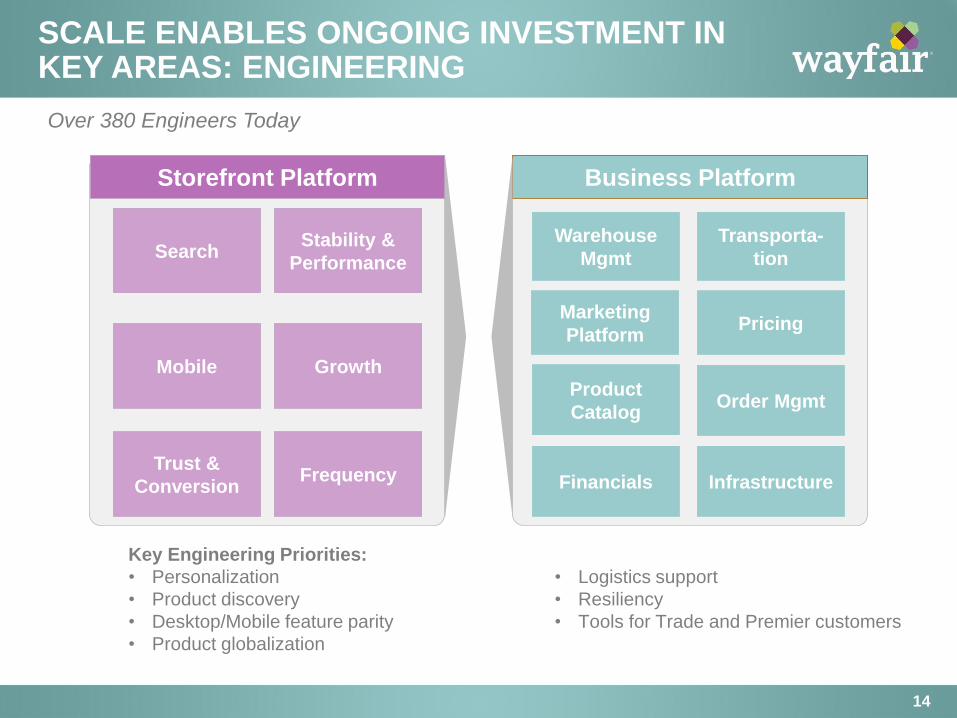

SCALE ENABLES ONGOING INVESTMENT IN KEY AREAS: ENGINEERING

14

Over 380 Engineers Today

Key Engineering Priorities:

• Personalization

• Product discovery

• Desktop/Mobile feature parity

• Product globalization

• Logistics support

• Resiliency

• Tools for Trade and Premier customers

Storefront Platform Business Platform

Search

Mobile

Trust &

Conversion

Stability &

Performance

Growth

Frequency Financials

Warehouse

Mgmt

Pricing

Infrastructure

Transporta-

tion

Product

CatalogOrder Mgmt

Marketing

Platform

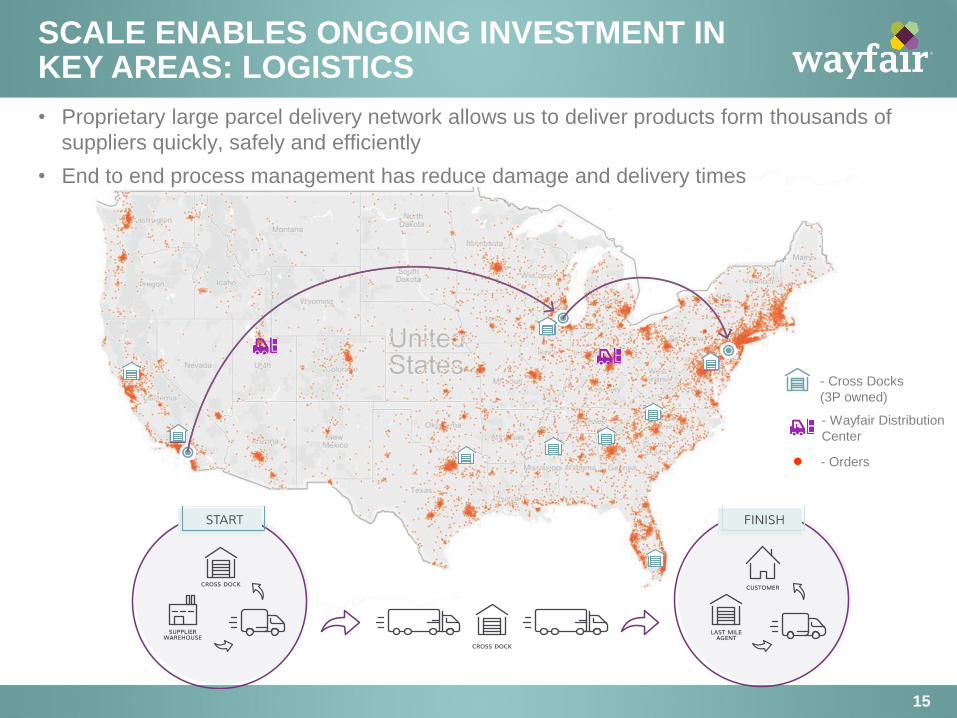

SCALE ENABLES ONGOING INVESTMENT IN KEY AREAS: LOGISTICS

15

- Cross Docks

(3P owned)

- Orders

- Wayfair Distribution

Center

• Proprietary large parcel delivery network allows us to deliver products form thousands of

suppliers quickly, safely and efficiently

• End to end process management has reduce damage and delivery times

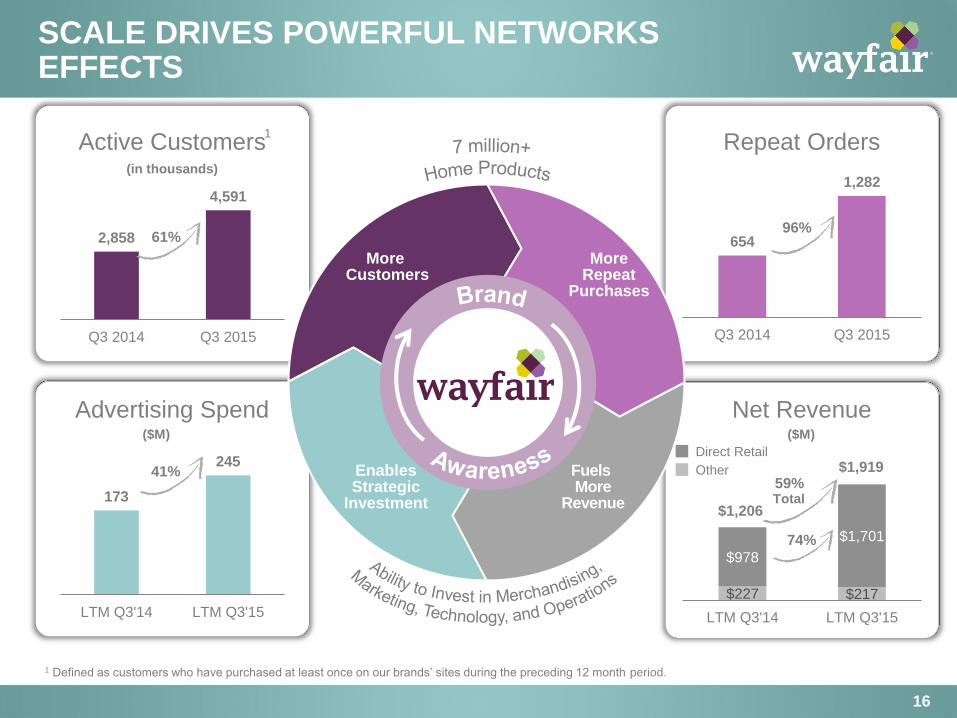

SCALE DRIVES POWERFUL NETWORKS EFFECTS

16

2,858

4,591

Q3 2014 Q3 2015

(in thousands)

Advertising Spend

173

245

LTM Q3'14 LTM Q3'15

654

1,282

Q3 2014 Q3 2015

Net Revenue

$227 $217

$978

$1,701

LTM Q3'14 LTM Q3'15

41%

74%

61%

1 Defined as customers who have purchased at least once on our brands’ sites during the preceding 12 month period.

Active Customers 1 Repeat Orders

59%

$1,206

$1,919 Direct Retail

Other

($M)

Total

Enables Strategic

Investment

Fuels More

Revenue

More Customers

More Repeat

Purchases

($M)

96%

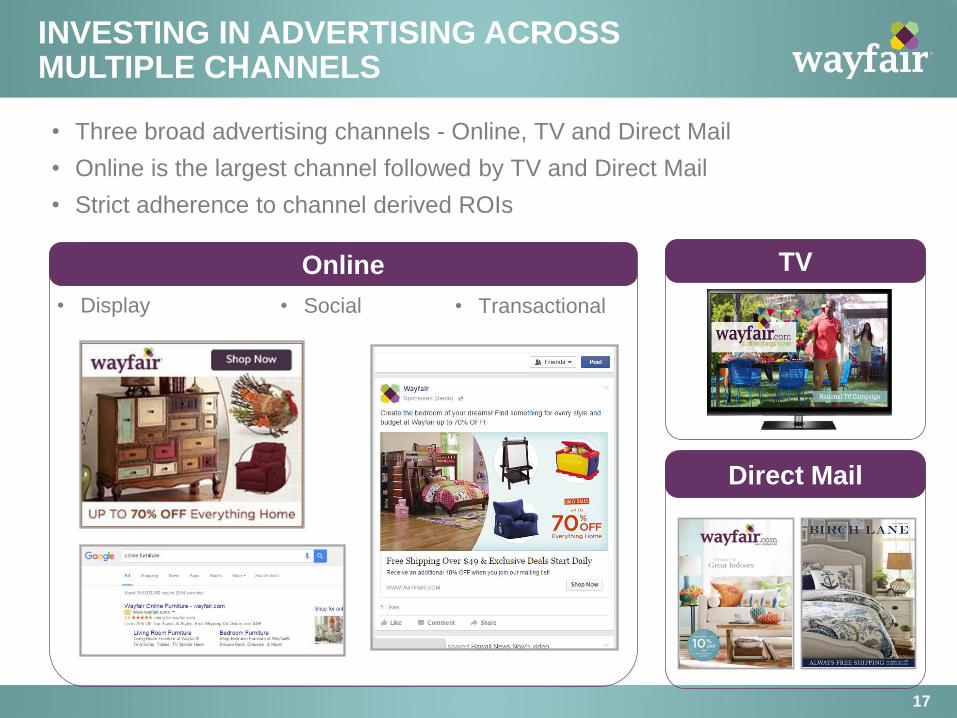

INVESTING IN ADVERTISING ACROSS MULTIPLE CHANNELS

17

• Three broad advertising channels - Online, TV and Direct Mail

• Online is the largest channel followed by TV and Direct Mail

• Strict adherence to channel derived ROIs

Online TV

Direct Mail

• Display

• Social • Transactional

Most 2011 and 2012 customers first purchased before site rebranding

Wayfair.com Gross Revenue Per Customer Per Month

INVESTMENT IN ADVERTISTING SPEND RESULTS IN HIGHER REVENUE/CUSTOMER…

18

Re

ve

nu

e/C

us

tom

er/

Mo

nth

(in

clu

de

s a

ll cu

sto

mers

)

Time Since Initial Purchase

x$

2x$

4x$

6x$

8x$

10x$

12x$

14x$

16x$

18x$

20x$

22x$

31-6

0 D

ays

61-9

0 D

ays

91-1

20

Days

121

-15

0 D

ays

151

-18

0 D

ays

181

-21

0 D

ays

211

-24

0 D

ays

241

-27

0 D

ays

271

-30

0 D

ays

301

-33

0 D

ays

331

-36

0 D

ays

361

-39

0 D

ays

391

-42

0 D

ays

421

-45

0 D

ays

451

-48

0 D

ays

481

-51

0 D

ays

511

-54

0 D

ays

541

-57

0 D

ays

571

-60

0 D

ays

601

-63

0 D

ays

631

-66

0 D

ays

661

-69

0 D

ays

691

-72

0 D

ays

721

- 7

50

Da

ys

751

- 7

80

Da

ys

781

- 8

10

Da

ys

811

- 8

40

Da

ys

841

- 8

70

Da

ys

871

- 9

00

Da

ys

901

- 9

30

Da

ys

931

- 9

60

Da

ys

961

- 9

90

Da

ys

991

- 1

02

0 D

ays

102

1 -

10

50 D

ays

105

1 -

10

80 D

ays

108

1 -

11

10 D

ays

111

1 -

11

40 D

ays

114

1 -

11

70 D

ays

117

1 -

12

00 D

ays

120

1 -

12

30 D

ays

123

1 -

12

60 D

ays

126

1 -

12

90 D

ays

129

1 -

13

20 D

ays

132

1 -

13

50 D

ays

135

1 -

13

80 D

ays

138

1 -

14

10 D

ays

141

1 -

14

40 D

ays

144

1 -

14

70 D

ays

147

1 -

15

00 D

ays

2011 2012 2013 2014 2015

• Customers acquired in more recent periods

consistently spend more over time than

customers acquired in older periods

• For example in the 6th month post their initial

order 2014 customers spent >2x 2011

customers

31-60

Days

151-180

Days

331-360

Days

511-540

Days

691-720

Days

871-900

Days

1,051-1,080

Days

1,231-1,260

Days

1,411-1,440

Days

2012 2013 2011

2014 2015

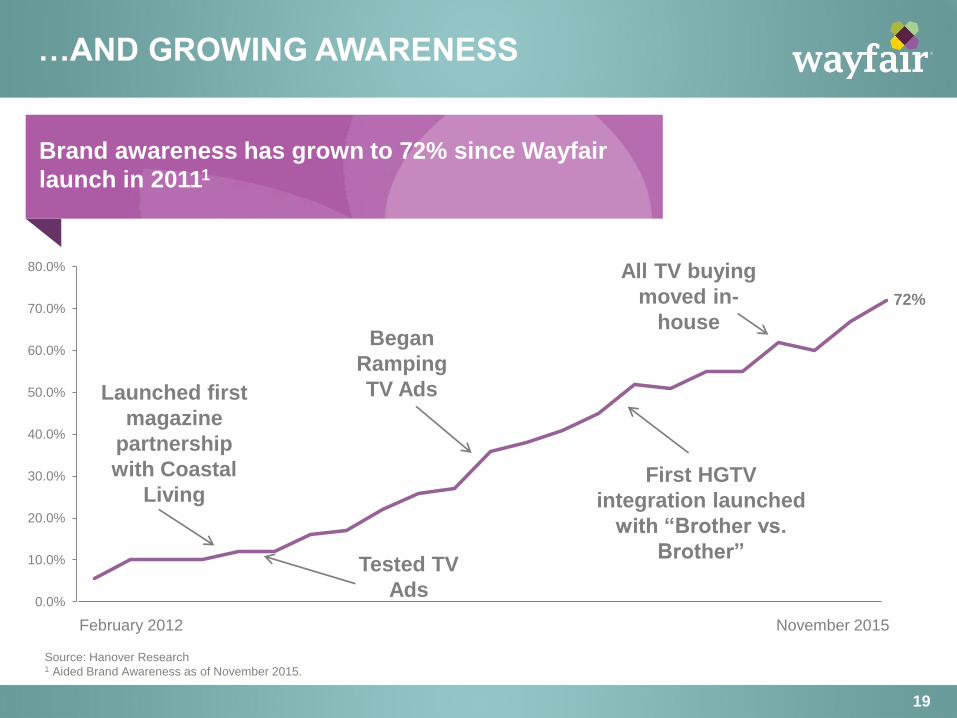

…AND GROWING AWARENESS

19

Source: Hanover Research

1 Aided Brand Awareness as of November 2015.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Brand awareness has grown to 72% since Wayfair

launch in 20111

November 2015 February 2012

72%

Launched first

magazine

partnership

with Coastal

Living

All TV buying

moved in-

house

Tested TV

Ads

First HGTV

integration launched

with “Brother vs.

Brother”

Began

Ramping

TV Ads

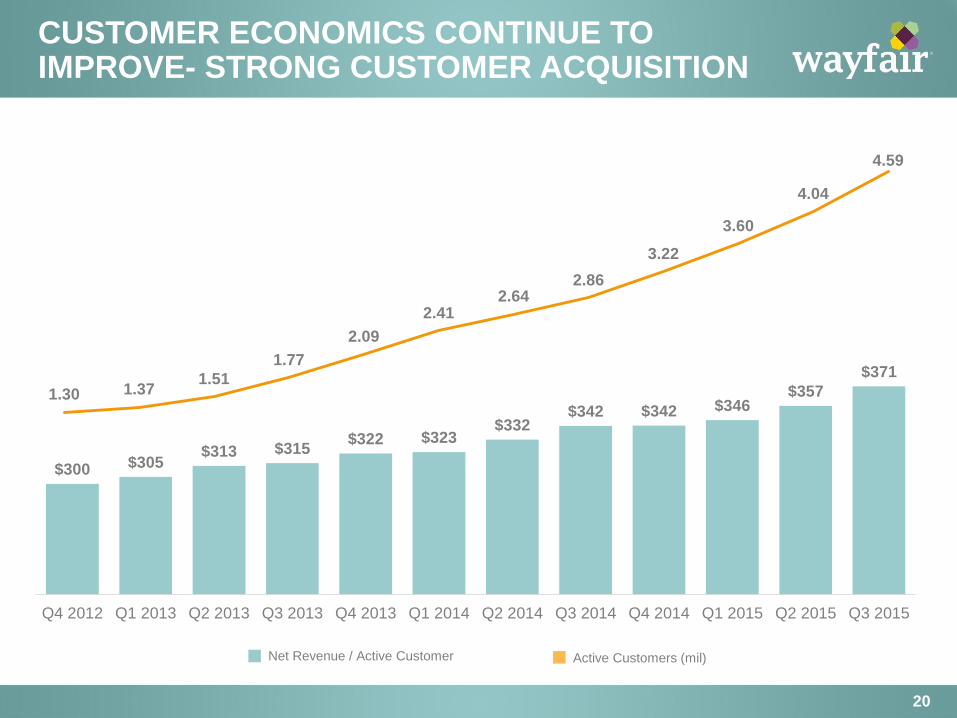

$300 $305 $313 $315

$322 $323 $332

$342 $342 $346 $357

$371

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

1.30 1.37 1.51

1.77

2.09

2.41 2.64

2.86

3.22

3.60

4.04

4.59

CUSTOMER ECONOMICS CONTINUE TO IMPROVE- STRONG CUSTOMER ACQUISITION

20

Net Revenue / Active Customer Active Customers (mil)

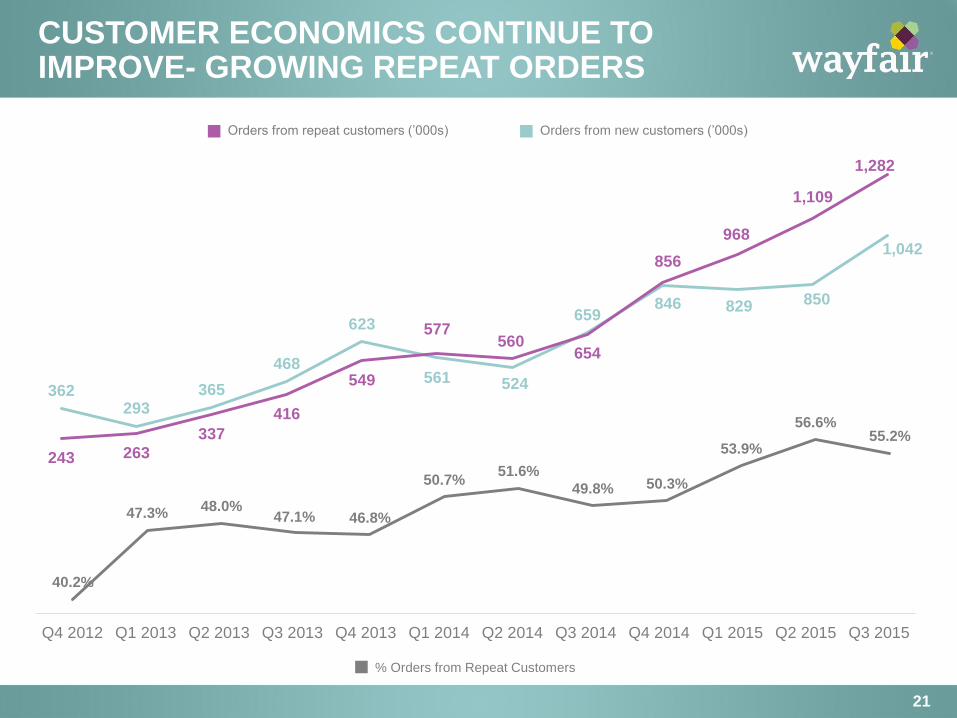

362 293

365

468

623

561 524

659 846 829 850

1,042

243 263

337

416

549

577 560

654

856

968

1,109

1,282

CUSTOMER ECONOMICS CONTINUE TO IMPROVE- GROWING REPEAT ORDERS

21

40.2%

47.3% 48.0% 47.1% 46.8%

50.7% 51.6%

49.8% 50.3%

53.9%

56.6% 55.2%

% Orders from Repeat Customers

Orders from repeat customers (’000s) Orders from new customers (’000s)

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

CAPITAL EFFICIENT WITH MINIMAL INVENTORY

22

Capital Efficient1 Minimal Inventory

1.5

38.5

Days Receivable Days Payable

$916

$1,319

$1,991

$15 $20 $23

2013 2014 LTM

Net Revenue Inventory

($M)

FCF Performance Consistently Better than Adjusted EBITDA

1 Average of last four quarters.

Q1 2014

Long-Term Target

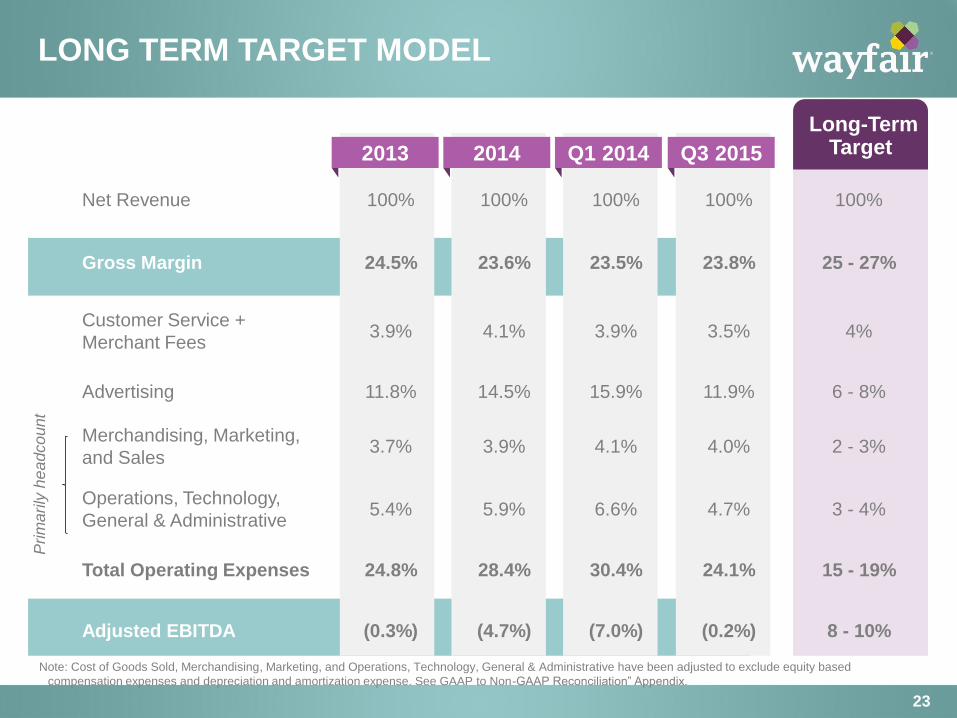

LONG TERM TARGET MODEL

23

Net Revenue 100% 100% 100% 100% 100%

Gross Margin 24.5% 23.6% 23.5% 23.8% 25 - 27%

Customer Service +

Merchant Fees 3.9% 4.1% 3.9% 3.5% 4%

Advertising 11.8% 14.5% 15.9% 11.9% 6 - 8%

Merchandising, Marketing,

and Sales 3.7% 3.9% 4.1% 4.0% 2 - 3%

Operations, Technology,

General & Administrative 5.4% 5.9% 6.6% 4.7% 3 - 4%

Total Operating Expenses 24.8% 28.4% 30.4% 24.1% 15 - 19%

Adjusted EBITDA (0.3%) (4.7%) (7.0%) (0.2%) 8 - 10%

Note: Cost of Goods Sold, Merchandising, Marketing, and Operations, Technology, General & Administrative have been adjusted to exclude equity based

compensation expenses and depreciation and amortization expense. See GAAP to Non-GAAP Reconciliation” Appendix.

Prim

arily

he

adco

unt

2013 2014 Q3 2015

CONTINUE BUILDING LEADING RETAIL HOME BRANDS

• Grow active customer base

• Increase repeat behavior

• Invest in product/technology to further improve the

customer experience

• Enhance logistics infrastructure for faster and

higher quality customer delivery experience

• Invest in and grow international business

KEY STRATEGIC PRIORITIES

24

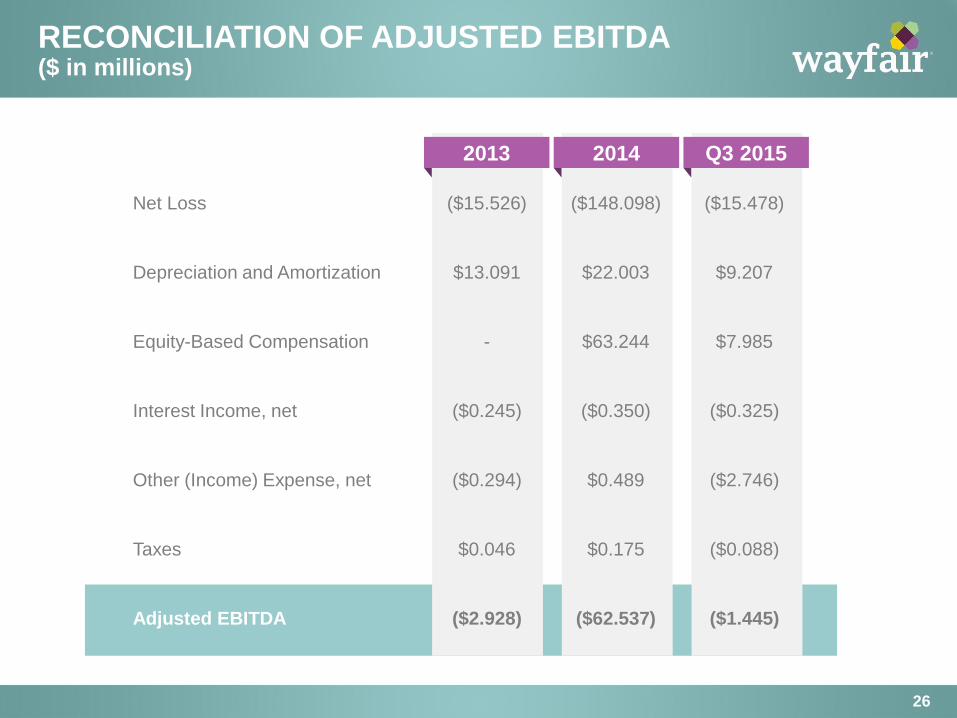

RECONCILIATION OF ADJUSTED EBITDA ($ in millions)

26

Net Loss ($15.526) ($148.098) ($15.478)

Depreciation and Amortization $13.091 $22.003 $9.207

Equity-Based Compensation - $63.244 $7.985

Interest Income, net ($0.245) ($0.350) ($0.325)

Other (Income) Expense, net ($0.294) $0.489 ($2.746)

Taxes $0.046 $0.175 ($0.088)

Adjusted EBITDA ($2.928) ($62.537) ($1.445)

2013 2014 Q3 2015

RECONCILIATION OF FREE CASH FLOW ($ in millions)

27

Net Cash Provided by Operating

Activities, Net of Acquisition $34.413 $11.692 $51.504

Purchase of Property, Equipment and

Leasehold Improvements ($6.739) ($39.422) ($11.491)

Site and Software Development Costs ($9.040) ($14.130) ($4.681)

Free Cash Flow $18.634 ($41.860) $35.332

2013 2014 Q3 2015

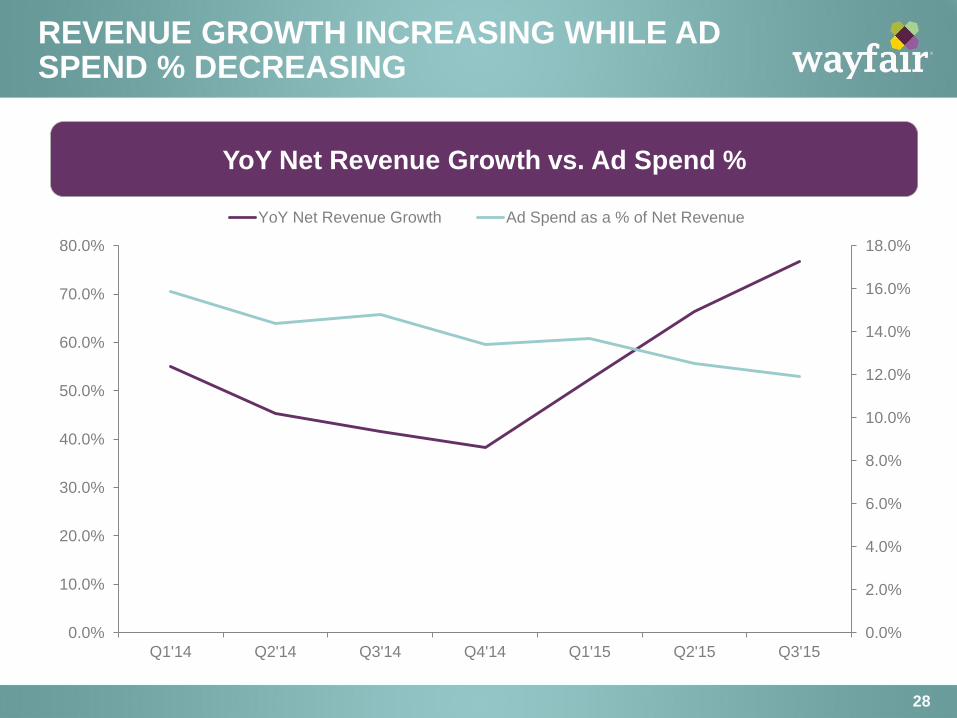

REVENUE GROWTH INCREASING WHILE AD SPEND % DECREASING

28

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15

YoY Net Revenue Growth Ad Spend as a % of Net Revenue

YoY Net Revenue Growth vs. Ad Spend %

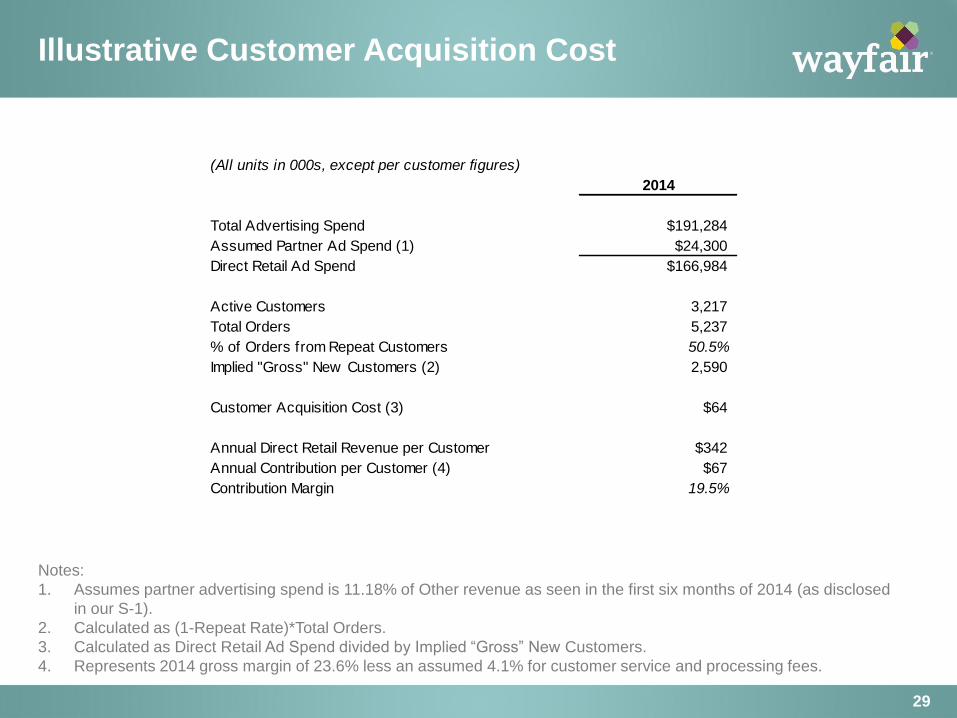

Illustrative Customer Acquisition Cost

29

Notes:

1. Assumes partner advertising spend is 11.18% of Other revenue as seen in the first six months of 2014 (as disclosed

in our S-1).

2. Calculated as (1-Repeat Rate)*Total Orders.

3. Calculated as Direct Retail Ad Spend divided by Implied “Gross” New Customers.

4. Represents 2014 gross margin of 23.6% less an assumed 4.1% for customer service and processing fees.

(All units in 000s, except per customer figures)

2014

Total Advertising Spend $191,284

Assumed Partner Ad Spend (1) $24,300

Direct Retail Ad Spend $166,984

Active Customers 3,217

Total Orders 5,237

% of Orders from Repeat Customers 50.5%

Implied "Gross" New Customers (2) 2,590

Customer Acquisition Cost (3) $64

Annual Direct Retail Revenue per Customer $342

Annual Contribution per Customer (4) $67

Contribution Margin 19.5%