Embed Size (px)

Citation preview

August 2009

OFFICE OF CHIEF ECONOMIST

IInnddoonneessiiaa UUppddaattee

Unlocking Investments Potential in Papua

Indonesia is a vast archipelago with enormous economic growth potential. Each

region presents unique characteristics and competitive advantages. In this edition,

we would like to explore the investment opportunity in Papua Island, including Papua

Province and West Papua Province.

Papua Province, which lies on the eastern tip of Indonesia, is rich with natural

resources. Its soil is very suitable for agriculture and what lies below ground is an

abundant amount of minerals and gases. Geographically, Papua Island is surrounded

by sea with total coast line of 2,000 sea miles in length, with many rivers and lakes.

Hence, Papua Island is an ideal site to promote eco-tourism in the Papua Province.

Furthermore, its indigenous culture has become another special attraction to many

tourists, both local and foreign alike.

West Papua has a strong agriculture sector that provides the biggest contribution in

its GDP. Financial, leasing and service industries experienced the highest growth

among the other sectors, even though their contributions are still relatively low.

Forwarding, communication and construction sectors showed fairly significant

growth during 2003 – 2008.

But investment realization in Papua and West Papua Province is still low, due to poor

inter-departmental coordination as well as central and local government

coordination related to license issuing process, tribe rights, limited infrastructure

facilities, and lack of high skilled work force.

Indonesia economy expanded by 4.0% yoy or 2.3% qoq in 2Q09, higher than ours and

consensus estimates. Despite growing at slower pace compared to the previous

quarter, Indonesia’s economy is among few economies that could grow in 2Q09, the

fastest after China 7.9% yoy according to Bloomberg. Indonesia’s economy expanded

by 4.2% yoy in 1H09. We expect the economy to grow by 4.0% for the full year 09,

although we see an upside risk of the growth given the robust first half results. We

forecast Indonesia economy to grow 5.0% in 2010, which is higher than 2009. Having

said that, coupled with higher inflation risk in 2010, we reiterate our view of no

further rate cut this year.

CCoonntteennttss

Unlocking Investments Potential

In Papua

p.02

2Q09 GDP : Above Expectations p.19

Macro Indicator and Forecast

(Table)

p.22

Indonesia Current Data (Table) p.23

CChhiieeff EEccoonnoommiisstt

Mirza Adityaswara

AAnnaallyysstt

Moch. Doddy Ariefianto

Nina Anggraeni

Rini Setyowati

M. Ajie Maulendra

Nadia Kusuma Dewi

Nurul Yuniataqwa Karunia

Sindi Paramita

PPuubblliiccaattiioonn AAddddrreessss::

Bank Mandiri Head Office

Office of Chief Economist

21st

Floor, Plaza Mandiri

Jl. Jend. Gatot Subroto Kav.36-38

Jakarta 12190, Indonesia

Phone: (62-21) 5245516 / 5272

Fax: (62-21) 5210430

EEmmaaiill::

SSeeee iimmppoorrttaanntt ddiissccllaaiimmeerr aatt tthhee eenndd ooff

tthhiiss mmaatteerriiaall

© Office of Chief Economist Page 2 of 24

Indonesia is a vast archipelago with enormous economic

growth potential. Each region in this country has different

characteristic and competitive advantages. Hence, regional

development policies issued by each regional government that

focus on its competitive advantage is expected to optimize the

economic growth.

Considering the importance of regional economic potency,

Bank Mandiri Office of Chief Economist initiates to conduct

some regional potency studies. One of our studies is Papua

island economic potency that will capture Papua Province and

West Papua Province. We choose this region to analyze

because of many reasons as follows:

1. The significant size of Papua island in Eastern Part of

Indonesia (KTI), where KTI itself has become the big target

of development in Indonesia further. So far, the country’s

development is stressed more in Java island;

2. Papua Island owns a various number of natural resources

which are not fully explored yet because of its poor

infrastructure condition and lack of human resources

capability;

3. Papua is one among the regions that achieve special

autonomous status from the Central Government.

The aim of this study is also to make a preliminary study

before a seminar titled ”Papua Investment Day” which will be

conducted in October 2009.

This study will be undergone in two editions of our Indonesia

Update. The first edition will focus on the sector of economic

potency in Papua Province and West Papua Province, despite

the investment development of those two provinces. While

the second will be stressed on strategic aspects that has big

influence to the investment in Papua, such as decentralization

and region enlargement, migration, special autonomous,

regional fiscal policy, banking sector, investment obstacles

that will involve infrastructure development, human

resources, and local land regulation, as well as input in the

policy.

UNLOCKING INVESTMENTS POTENTIAL IN PAPUA Nadia Kusuma Dewi ([email protected]) M. Ajie Maulendra ([email protected])

© Office of Chief Economist Page 3 of 24

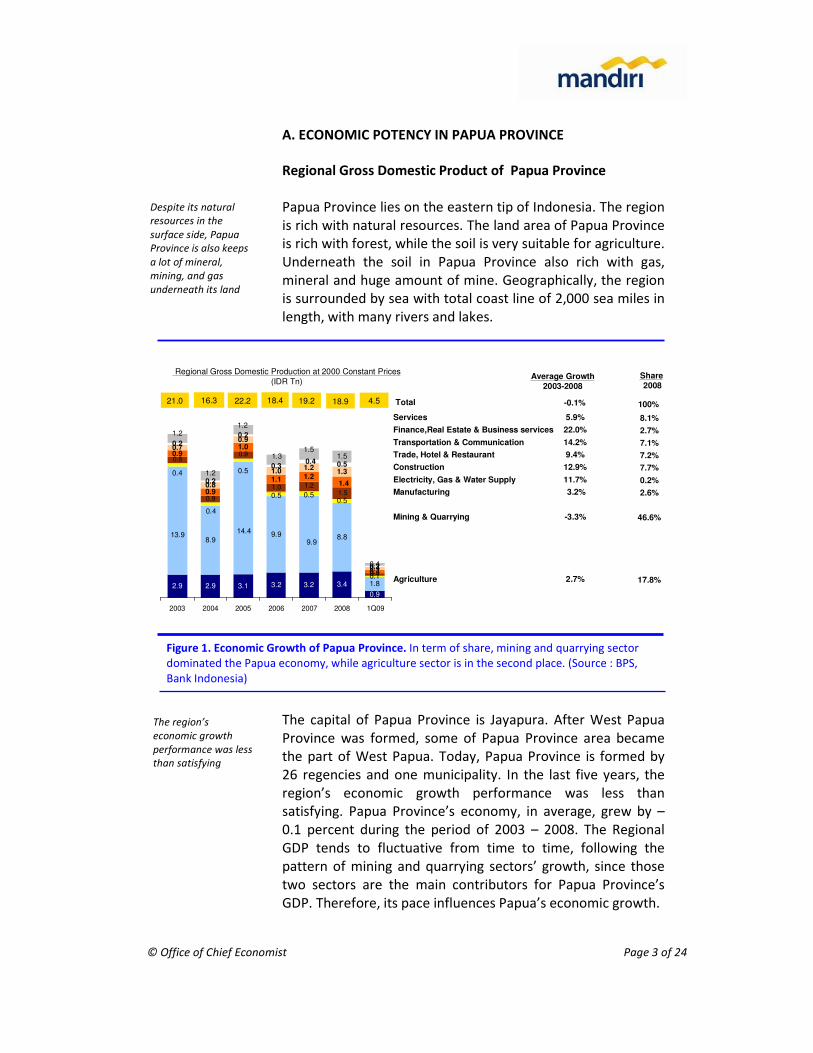

A. ECONOMIC POTENCY IN PAPUA PROVINCE

Regional Gross Domestic Product of Papua Province

Papua Province lies on the eastern tip of Indonesia. The region

is rich with natural resources. The land area of Papua Province

is rich with forest, while the soil is very suitable for agriculture.

Underneath the soil in Papua Province also rich with gas,

mineral and huge amount of mine. Geographically, the region

is surrounded by sea with total coast line of 2,000 sea miles in

length, with many rivers and lakes.

The capital of Papua Province is Jayapura. After West Papua

Province was formed, some of Papua Province area became

the part of West Papua. Today, Papua Province is formed by

26 regencies and one municipality. In the last five years, the

region’s economic growth performance was less than

satisfying. Papua Province’s economy, in average, grew by –

0.1 percent during the period of 2003 – 2008. The Regional

GDP tends to fluctuative from time to time, following the

pattern of mining and quarrying sectors’ growth, since those

two sectors are the main contributors for Papua Province’s

GDP. Therefore, its pace influences Papua’s economic growth.

Despite its natural

resources in the

surface side, Papua

Province is also keeps

a lot of mineral,

mining, and gas

underneath its land

The region’s

economic growth

performance was less

than satisfying

Figure 1. Economic Growth of Papua Province. In term of share, mining and quarrying sector

dominated the Papua economy, while agriculture sector is in the second place. (Source : BPS,

Bank Indonesia)

Regional Gross Domestic Production at 2000 Constant Prices

(IDR Tn)

2.9 2.9 3.1 3.2 3.2 3.4

0.9

8.99.9 8.8

1.8

0.5

0.1

0.8

0.9

0.9

1.0 1.2

0.4

0.9

0.9

1.0

1.1

0.4

0.7

0.8

0.9

1.0 1.3

0.4

0.2

0.2

0.2

0.3 0.5

0.2

1.5

0.4

9.913.9

14.4

0.50.5

0.5

0.4

0.4

1.5

1.41.2

1.20.4

1.51.3

1.2

1.2

1.2

2003 2004 2005 2006 2007 2008 1Q09

Services

Finance,Real Estate & Business services

Transportation & Communication

Trade, Hotel & Restaurant

Construction

Electricity, Gas & Water Supply

Manufacturing

Mining & Quarrying

Agriculture

Average Growth2003-2008

5.9%

22.0%

14.2%

9.4%

12.9%

11.7%

3.2%

-3.3%

2.7%

21.0 16.3 22.2 18.4 19.2 Total -0.1%18.9 4.5

Share 2008

8.1%

2.7%

7.1%

7.2%

7.7%

0.2%

2.6%

46.6%

17.8%

100%

© Office of Chief Economist Page 4 of 24

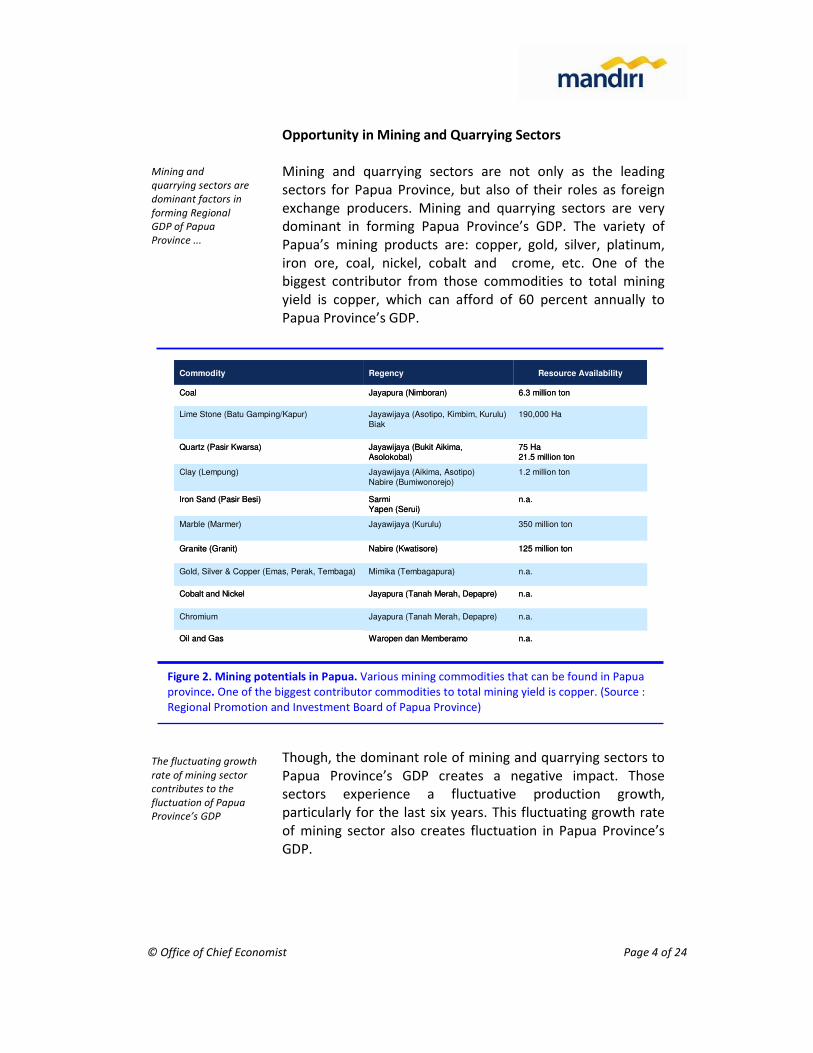

Opportunity in Mining and Quarrying Sectors

Mining and quarrying sectors are not only as the leading

sectors for Papua Province, but also of their roles as foreign

exchange producers. Mining and quarrying sectors are very

dominant in forming Papua Province’s GDP. The variety of

Papua’s mining products are: copper, gold, silver, platinum,

iron ore, coal, nickel, cobalt and crome, etc. One of the

biggest contributor from those commodities to total mining

yield is copper, which can afford of 60 percent annually to

Papua Province’s GDP.

Though, the dominant role of mining and quarrying sectors to

Papua Province’s GDP creates a negative impact. Those

sectors experience a fluctuative production growth,

particularly for the last six years. This fluctuating growth rate

of mining sector also creates fluctuation in Papua Province’s

GDP.

Mining and

quarrying sectors are

dominant factors in

forming Regional

GDP of Papua

Province ...

The fluctuating growth

rate of mining sector

contributes to the

fluctuation of Papua

Province’s GDP

Figure 2. Mining potentials in Papua. Various mining commodities that can be found in Papua

province. One of the biggest contributor commodities to total mining yield is copper. (Source :

Regional Promotion and Investment Board of Papua Province)

.

n.a.SarmiYapen (Serui)

Iron Sand (Pasir Besi)

n.a.Waropen dan MemberamoOil and Gas

n.a.Jayapura (Tanah Merah, Depapre)Chromium

n.a.Jayapura (Tanah Merah, Depapre)Cobalt and Nickel

n.a.Mimika (Tembagapura)Gold, Silver & Copper (Emas, Perak, Tembaga)

125 million tonNabire (Kwatisore)Granite (Granit)

350 million tonJayawijaya (Kurulu)Marble (Marmer)

1.2 million tonJayawijaya (Aikima, Asotipo)

Nabire (Bumiwonorejo)

Clay (Lempung)

75 Ha21.5 million ton

Jayawijaya (Bukit Aikima, Asolokobal)

Quartz (Pasir Kwarsa)

190,000 HaJayawijaya (Asotipo, Kimbim, Kurulu)

Biak

Lime Stone (Batu Gamping/Kapur)

6.3 million tonJayapura (Nimboran)Coal

Resource Availability RegencyCommodity

n.a.SarmiYapen (Serui)

Iron Sand (Pasir Besi)

n.a.Waropen dan MemberamoOil and Gas

n.a.Jayapura (Tanah Merah, Depapre)Chromium

n.a.Jayapura (Tanah Merah, Depapre)Cobalt and Nickel

n.a.Mimika (Tembagapura)Gold, Silver & Copper (Emas, Perak, Tembaga)

125 million tonNabire (Kwatisore)Granite (Granit)

350 million tonJayawijaya (Kurulu)Marble (Marmer)

1.2 million tonJayawijaya (Aikima, Asotipo)

Nabire (Bumiwonorejo)

Clay (Lempung)

75 Ha21.5 million ton

Jayawijaya (Bukit Aikima, Asolokobal)

Quartz (Pasir Kwarsa)

190,000 HaJayawijaya (Asotipo, Kimbim, Kurulu)

Biak

Lime Stone (Batu Gamping/Kapur)

6.3 million tonJayapura (Nimboran)Coal

Resource Availability RegencyCommodity

© Office of Chief Economist Page 5 of 24

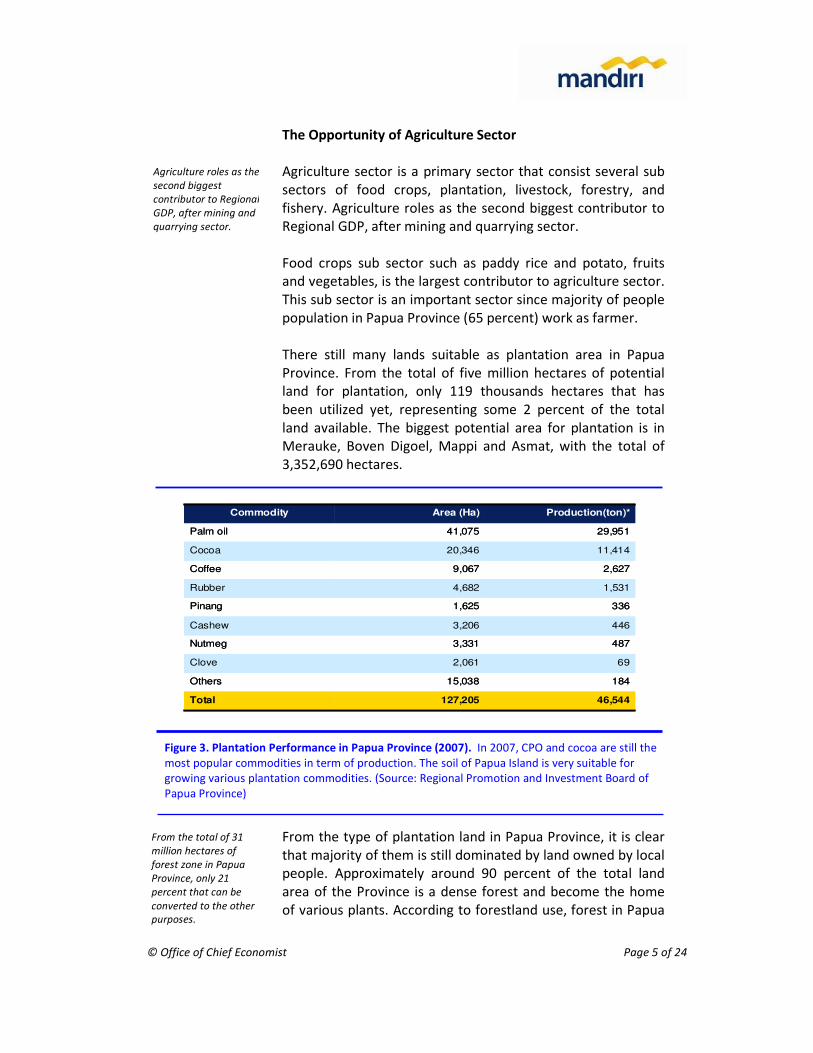

The Opportunity of Agriculture Sector

Agriculture sector is a primary sector that consist several sub

sectors of food crops, plantation, livestock, forestry, and

fishery. Agriculture roles as the second biggest contributor to

Regional GDP, after mining and quarrying sector.

Food crops sub sector such as paddy rice and potato, fruits

and vegetables, is the largest contributor to agriculture sector.

This sub sector is an important sector since majority of people

population in Papua Province (65 percent) work as farmer.

There still many lands suitable as plantation area in Papua

Province. From the total of five million hectares of potential

land for plantation, only 119 thousands hectares that has

been utilized yet, representing some 2 percent of the total

land available. The biggest potential area for plantation is in

Merauke, Boven Digoel, Mappi and Asmat, with the total of

3,352,690 hectares.

From the type of plantation land in Papua Province, it is clear

that majority of them is still dominated by land owned by local

people. Approximately around 90 percent of the total land

area of the Province is a dense forest and become the home

of various plants. According to forestland use, forest in Papua

Figure 3. Plantation Performance in Papua Province (2007). In 2007, CPO and cocoa are still the

most popular commodities in term of production. The soil of Papua Island is very suitable for

growing various plantation commodities. (Source: Regional Promotion and Investment Board of

Papua Province)

Commodity Area (Ha) Production(ton)*

Palm oil 41,075 29,951

Cocoa 20,346 11,414

Coffee 9,067 2,627

Rubber 4,682 1,531

Pinang 1,625 336

Cashew 3,206 446

Nutmeg 3,331 487

Clove 2,061 69

Others 15,038 184

Total 127,205 46,544

Commodity Area (Ha) Production(ton)*

Palm oil 41,075 29,951

Cocoa 20,346 11,414

Coffee 9,067 2,627

Rubber 4,682 1,531

Pinang 1,625 336

Cashew 3,206 446

Nutmeg 3,331 487

Clove 2,061 69

Others 15,038 184

Total 127,205 46,544

Agriculture roles as the

second biggest

contributor to Regional

GDP, after mining and

quarrying sector.

From the total of 31

million hectares of

forest zone in Papua

Province, only 21

percent that can be

converted to the other

purposes.

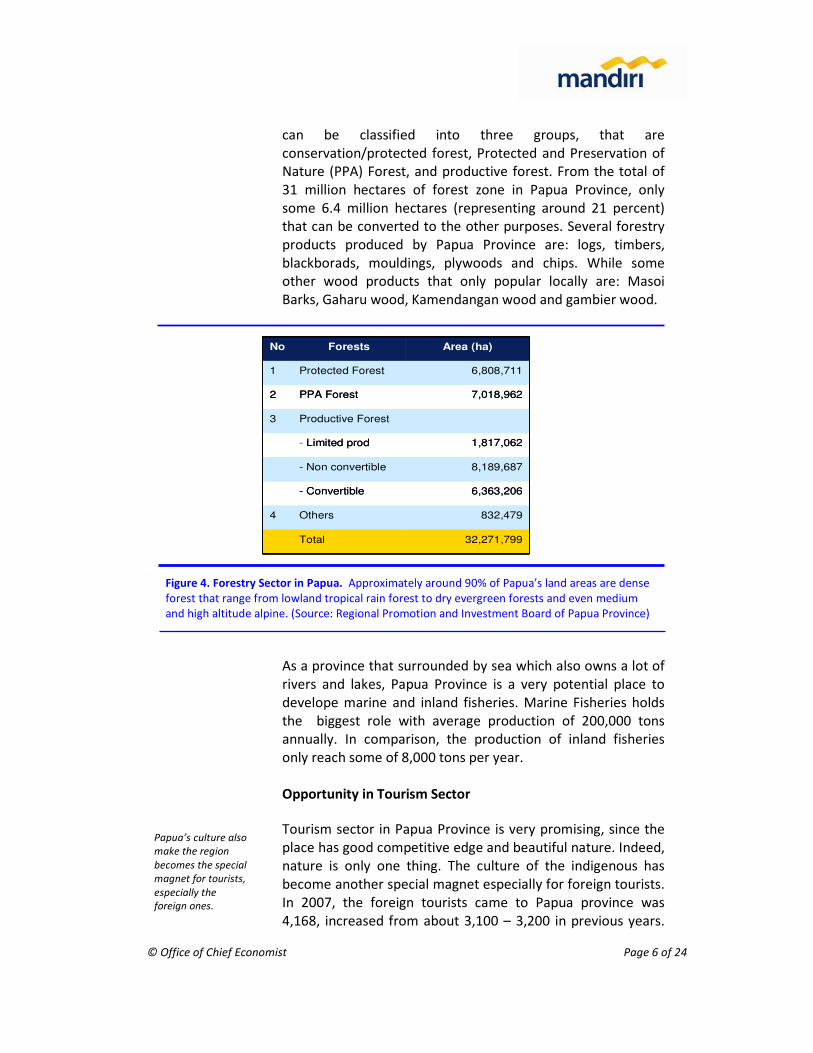

© Office of Chief Economist Page 6 of 24

can be classified into three groups, that are

conservation/protected forest, Protected and Preservation of

Nature (PPA) Forest, and productive forest. From the total of

31 million hectares of forest zone in Papua Province, only

some 6.4 million hectares (representing around 21 percent)

that can be converted to the other purposes. Several forestry

products produced by Papua Province are: logs, timbers,

blackborads, mouldings, plywoods and chips. While some

other wood products that only popular locally are: Masoi

Barks, Gaharu wood, Kamendangan wood and gambier wood.

As a province that surrounded by sea which also owns a lot of

rivers and lakes, Papua Province is a very potential place to

develope marine and inland fisheries. Marine Fisheries holds

the biggest role with average production of 200,000 tons

annually. In comparison, the production of inland fisheries

only reach some of 8,000 tons per year.

Opportunity in Tourism Sector

Tourism sector in Papua Province is very promising, since the

place has good competitive edge and beautiful nature. Indeed,

nature is only one thing. The culture of the indigenous has

become another special magnet especially for foreign tourists.

In 2007, the foreign tourists came to Papua province was

4,168, increased from about 3,100 – 3,200 in previous years.

Papua’s culture also

make the region

becomes the special

magnet for tourists,

especially the

foreign ones.

Figure 4. Forestry Sector in Papua. Approximately around 90% of Papua’s land areas are dense

forest that range from lowland tropical rain forest to dry evergreen forests and even medium

and high altitude alpine. (Source: Regional Promotion and Investment Board of Papua Province)

No Forests Area (ha)

1 Protected Forest 6,808,711

2 PPA Forest 7,018,962

3 Productive Forest

- Limited prod 1,817,062

- Non convertible 8,189,687

- Convertible 6,363,206

4 Others 832,479

Total 32,271,799

No Forests Area (ha)

1 Protected Forest 6,808,711

2 PPA Forest 7,018,962

3 Productive Forest

- Limited prod 1,817,062

- Non convertible 8,189,687

- Convertible 6,363,206

4 Others 832,479

Total 32,271,799

© Office of Chief Economist Page 7 of 24

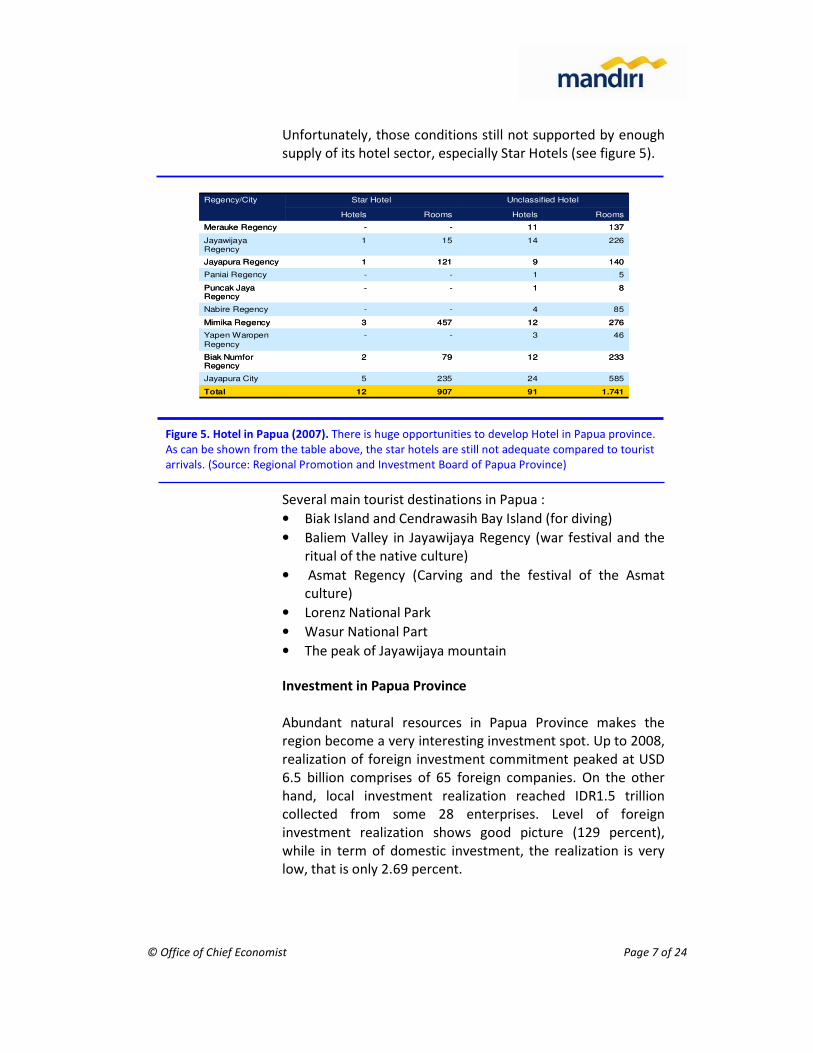

Unfortunately, those conditions still not supported by enough

supply of its hotel sector, especially Star Hotels (see figure 5).

Several main tourist destinations in Papua :

• Biak Island and Cendrawasih Bay Island (for diving)

• Baliem Valley in Jayawijaya Regency (war festival and the

ritual of the native culture)

• Asmat Regency (Carving and the festival of the Asmat

culture)

• Lorenz National Park

• Wasur National Part

• The peak of Jayawijaya mountain

Investment in Papua Province

Abundant natural resources in Papua Province makes the

region become a very interesting investment spot. Up to 2008,

realization of foreign investment commitment peaked at USD

6.5 billion comprises of 65 foreign companies. On the other

hand, local investment realization reached IDR1.5 trillion

collected from some 28 enterprises. Level of foreign

investment realization shows good picture (129 percent),

while in term of domestic investment, the realization is very

low, that is only 2.69 percent.

Figure 5. Hotel in Papua (2007). There is huge opportunities to develop Hotel in Papua province.

As can be shown from the table above, the star hotels are still not adequate compared to tourist

arrivals. (Source: Regional Promotion and Investment Board of Papua Province)

.

Regency/City Star Hotel Unclassified Hotel

Hotels Rooms Hotels Rooms

Merauke Regency - - 11 137

Jayawijaya Regency

1 15 14 226

Jayapura Regency 1 121 9 140

Paniai Regency - - 1 5

Puncak Jaya Regency

- - 1 8

Nabire Regency - - 4 85

Mimika Regency 3 457 12 276

Yapen Waropen

Regency

- - 3 46

Biak Numfor Regency

2 79 12 233

Jayapura City 5 235 24 585

Total 12 907 91 1.741

Regency/City Star Hotel Unclassified Hotel

Hotels Rooms Hotels Rooms

Merauke Regency - - 11 137

Jayawijaya Regency

1 15 14 226

Jayapura Regency 1 121 9 140

Paniai Regency - - 1 5

Puncak Jaya Regency

- - 1 8

Nabire Regency - - 4 85

Mimika Regency 3 457 12 276

Yapen Waropen

Regency

- - 3 46

Biak Numfor Regency

2 79 12 233

Jayapura City 5 235 24 585

Total 12 907 91 1.741

© Office of Chief Economist Page 8 of 24

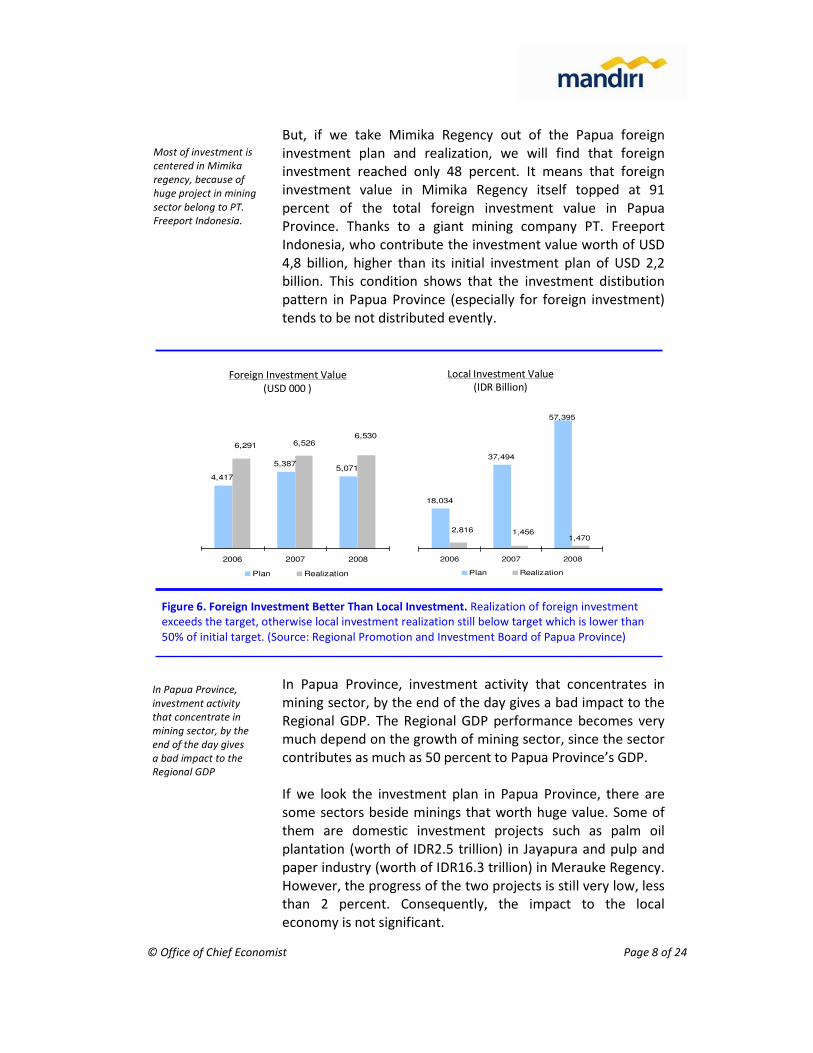

But, if we take Mimika Regency out of the Papua foreign

investment plan and realization, we will find that foreign

investment reached only 48 percent. It means that foreign

investment value in Mimika Regency itself topped at 91

percent of the total foreign investment value in Papua

Province. Thanks to a giant mining company PT. Freeport

Indonesia, who contribute the investment value worth of USD

4,8 billion, higher than its initial investment plan of USD 2,2

billion. This condition shows that the investment distibution

pattern in Papua Province (especially for foreign investment)

tends to be not distributed evently.

In Papua Province, investment activity that concentrates in

mining sector, by the end of the day gives a bad impact to the

Regional GDP. The Regional GDP performance becomes very

much depend on the growth of mining sector, since the sector

contributes as much as 50 percent to Papua Province’s GDP.

If we look the investment plan in Papua Province, there are

some sectors beside minings that worth huge value. Some of

them are domestic investment projects such as palm oil

plantation (worth of IDR2.5 trillion) in Jayapura and pulp and

paper industry (worth of IDR16.3 trillion) in Merauke Regency.

However, the progress of the two projects is still very low, less

than 2 percent. Consequently, the impact to the local

economy is not significant.

Most of investment is

centered in Mimika

regency, because of

huge project in mining

sector belong to PT.

Freeport Indonesia.

Figure 6. Foreign Investment Better Than Local Investment. Realization of foreign investment

exceeds the target, otherwise local investment realization still below target which is lower than

50% of initial target. (Source: Regional Promotion and Investment Board of Papua Province)

18,034

37,494

57,395

1,4701,4562,816

2006 2007 2008

Plan Realization

4,417

5,3875,071

6,5306,5266,291

2006 2007 2008

Plan Realization

Foreign Investment Value

(USD 000 )

Local Investment Value

(IDR Billion)

In Papua Province,

investment activity

that concentrate in

mining sector, by the

end of the day gives

a bad impact to the

Regional GDP

© Office of Chief Economist Page 9 of 24

Therefore, we can conclude that investment performance in

Papua Province still need an improvement, especially in term

of its distribution in correlation with economic sector and its

realization level, both for foreign as well as the domestic.

There are some obstacles found in developing investment in

Papua Province. Some of them are:

� There is still no “one roof office” for license issuing

services yet. Consequently, it becomes too bureaucratic

and creates difficulties for investors.

� There is no certainty in organizing licence since the central

and regional government tries to pull the string against the

other. This situation clearly will hinder investors in

realizing their business.

� There is still claims over land between the tribes and the

investors. The tribes convince that the land is still owned

by their families.

� Still there is no common perception over forest zone for

investment purposes between central and local

government

Several obstacles in

developing investment

in Papua Province are:

bureaucratic licence

process, uncertainty of

land ownership, and

insufficient

infrastructure facilities

Figure 7. Plantation Sector Investment in Papua Province. There are several projects that

contribute high value of investment such as CPO plantation in Jayapura Regency, also chipwood

and pulp industry in Merauke Regency. (Source: Regional Promotion and Investment Board of

Papua Province)

Regency/City Sector Company Investment Plan Investment

Realization

Jayapura CPO Plantation and

vegetable oil

PT. Sumber Indah Perkasa 2,422,522

(IDR million)

40,672

(IDR million)

CPO plantation and

processing

PT. Sinar Kencana Inti

Perkasa

320,895

(IDR million)

320,895

(IDR million)

CPO plantation and

processing

PT. Rimba Matoa Lestari 1,800,000

(IDR million)

1,000

(IDR million)

Keerom CPO plantation and

processing

PT. Perkebunan Nusantara II 191,973

(IDR million)

180,157

(IDR million)

Sarmi CPO plantation and

processing

PT. Gaharu Prima Lestari 1,800,000

(IDR million)

25

(IDR million)

Merauke Integrated CPO plantation

PT. Papua Agro Lestari 680,200(IDR million)

2,000(IDR million)

CPO plantation and oil

industry

PT. Bio Inti Agrindo 680,000

(IDR million)

10,000

(IDR million)

Chipwood and pulp industry

PT. Medco Papua IndustriLestari

16,304,386(IDR million)

25,000(IDR miliion)

Regency/City Sector Company Investment Plan Investment

Realization

Jayapura CPO Plantation and

vegetable oil

PT. Sumber Indah Perkasa 2,422,522

(IDR million)

40,672

(IDR million)

CPO plantation and

processing

PT. Sinar Kencana Inti

Perkasa

320,895

(IDR million)

320,895

(IDR million)

CPO plantation and

processing

PT. Rimba Matoa Lestari 1,800,000

(IDR million)

1,000

(IDR million)

Keerom CPO plantation and

processing

PT. Perkebunan Nusantara II 191,973

(IDR million)

180,157

(IDR million)

Sarmi CPO plantation and

processing

PT. Gaharu Prima Lestari 1,800,000

(IDR million)

25

(IDR million)

Merauke Integrated CPO plantation

PT. Papua Agro Lestari 680,200(IDR million)

2,000(IDR million)

CPO plantation and oil

industry

PT. Bio Inti Agrindo 680,000

(IDR million)

10,000

(IDR million)

Chipwood and pulp industry

PT. Medco Papua IndustriLestari

16,304,386(IDR million)

25,000(IDR miliion)

© Office of Chief Economist Page 10 of 24

� Insufficient infrastructure facilities to support investment,

such as road condition and power supply.

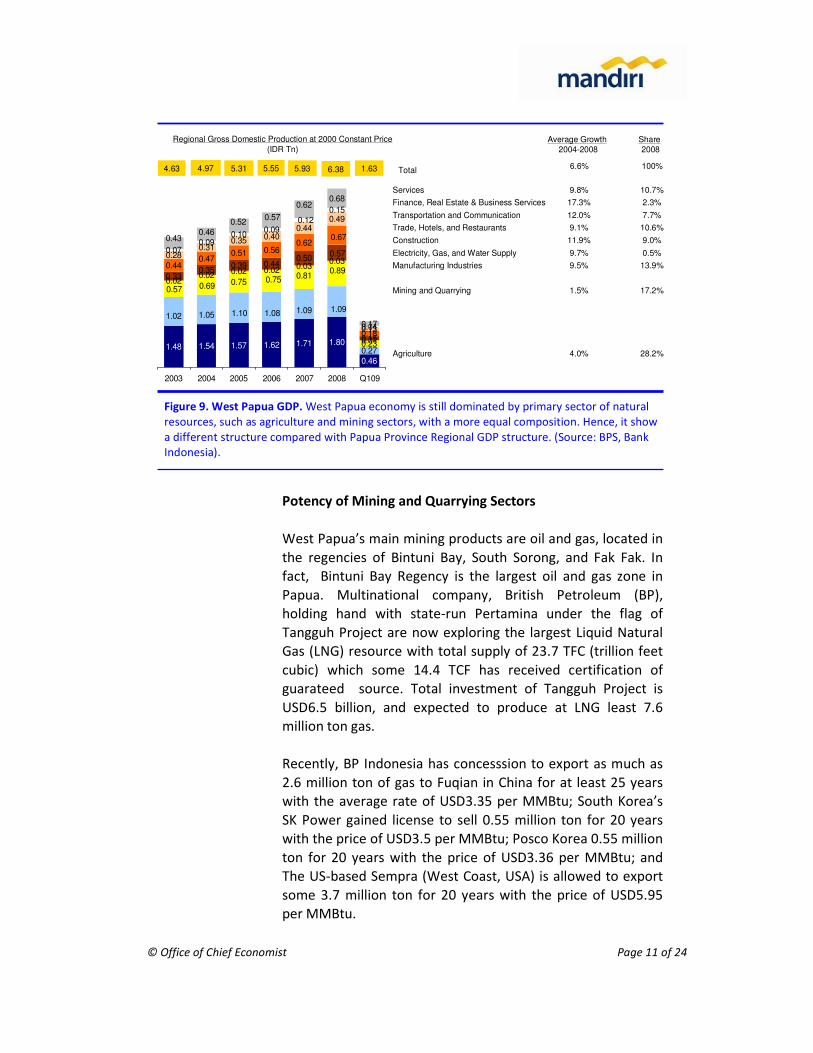

B. ECONOMIC POTENCY OF WEST PAPUA

Regional Gross Domestic Product of West Papua Province

In West Papua, there are eight regencies and one municipality,

with Manokwari as the provincial capital. West Papua’s

economy grew by an average of 6.6 percent during 2003 –

2008. Different from Papua Province’s Gross Domestic Product

structure which mainly dominated by mining and quarrying

sectors, composition of West Papua’s GDP is more diversity,

where agriculture sector provides the biggest contribution

(28.20 percent). Financial, leasing and service industries

experience the highest growth among the other sectors, even

though their contributions are still relatively low. Forwarding,

communication and construction sectors showed a fairly

significant growth during 2003 – 2008.

Different from Papua

Province, the

composition of West

Papua’s GDP is more

diversity

Figure 8. Mining Sector Investment in Papua Province. Copper mining organized by PT. Freeport

Indonesia is the highest value of investments in Papua Province. (Source: Regional Promotion and

Investment Board of Papua Province)

Regency/City Sector Company Investment Plan Investment

Realization

Boven Digul Wood : Logging, Sawnmill, Plywood

PT. Bade Makmur Orissa 430,576(IDR million)

430,576(IDR million)

Biak Numfor Wood: Logging, Sawnmill, Plywood

PT. Wapoga MutiaraTimber Unit III

108,136(IDR million)

10,000(IDR million)

Mimika Airport management service

PT. Airfas Aviation Fasilities Company

110,608(IDR million)

16,971(IDR million)

Mining PT. Freeport Indonesia 2,233,735 (USD 000)

4,842,625(USD 000)

Apartment building PT. Kencana Infra NusaKarya

158,000(USD 000)

73,333(USD 000)

Electricity and power plant management

PT. Puncak Jaya Power 366,400(USD 000)

68,925(USD 000)

Port management PT. Kuala PelabuhanIndonesia

400,000(USD 000)

400(USD 000)

Electricity and power plant management

PT. Nusantara Power Service

250,000(USD 000)

250,000(USD 000)

Regency/City Sector Company Investment Plan Investment

Realization

Boven Digul Wood : Logging, Sawnmill, Plywood

PT. Bade Makmur Orissa 430,576(IDR million)

430,576(IDR million)

Biak Numfor Wood: Logging, Sawnmill, Plywood

PT. Wapoga MutiaraTimber Unit III

108,136(IDR million)

10,000(IDR million)

Mimika Airport management service

PT. Airfas Aviation Fasilities Company

110,608(IDR million)

16,971(IDR million)

Mining PT. Freeport Indonesia 2,233,735 (USD 000)

4,842,625(USD 000)

Apartment building PT. Kencana Infra NusaKarya

158,000(USD 000)

73,333(USD 000)

Electricity and power plant management

PT. Puncak Jaya Power 366,400(USD 000)

68,925(USD 000)

Port management PT. Kuala PelabuhanIndonesia

400,000(USD 000)

400(USD 000)

Electricity and power plant management

PT. Nusantara Power Service

250,000(USD 000)

250,000(USD 000)

© Office of Chief Economist Page 11 of 24

Potency of Mining and Quarrying Sectors

West Papua’s main mining products are oil and gas, located in

the regencies of Bintuni Bay, South Sorong, and Fak Fak. In

fact, Bintuni Bay Regency is the largest oil and gas zone in

Papua. Multinational company, British Petroleum (BP),

holding hand with state-run Pertamina under the flag of

Tangguh Project are now exploring the largest Liquid Natural

Gas (LNG) resource with total supply of 23.7 TFC (trillion feet

cubic) which some 14.4 TCF has received certification of

guarateed source. Total investment of Tangguh Project is

USD6.5 billion, and expected to produce at LNG least 7.6

million ton gas.

Recently, BP Indonesia has concesssion to export as much as

2.6 million ton of gas to Fuqian in China for at least 25 years

with the average rate of USD3.35 per MMBtu; South Korea’s

SK Power gained license to sell 0.55 million ton for 20 years

with the price of USD3.5 per MMBtu; Posco Korea 0.55 million

ton for 20 years with the price of USD3.36 per MMBtu; and

The US-based Sempra (West Coast, USA) is allowed to export

some 3.7 million ton for 20 years with the price of USD5.95

per MMBtu.

Figure 9. West Papua GDP. West Papua economy is still dominated by primary sector of natural

resources, such as agriculture and mining sectors, with a more equal composition. Hence, it show

a different structure compared with Papua Province Regional GDP structure. (Source: BPS, Bank

Indonesia).

Regional Gross Domestic Production at 2000 Constant Price

(IDR Tn)

1.48 1.54 1.57 1.62 1.71 1.80

0.46

0.270.23

0.020.02 0.02 0.02 0.03

0.03

0.01

0.330.35

0.39 0.440.50

0.15

0.440.47

0.51 0.56

0.18

0.280.31

0.35 0.40

0.49

0.13

0.070.09

0.100.09

0.15

0.04

0.68

0.17

1.091.081.051.09

1.02 1.10

0.890.810.750.750.690.57

0.57

0.670.62

0.440.12

0.62

0.570.52

0.460.43

2003 2004 2005 2006 2007 2008 Q109

Services

Finance, Real Estate & Business Services

Transportation and Communication

Trade, Hotels, and Restaurants

Construction

Electricity, Gas, and Water Supply

Manufacturing Industries

Mining and Quarrying

Agriculture

Average Growth

2004-2008

9.8%

17.3%

12.0%

9.1%

11.9%

9.7%

9.5%

1.5%

4.0%

4.63 4.97 5.31 5.55 5.93 Total6.6%6.38 1.63

Share

2008

10.7%

2.3%

7.7%

10.6%

9.0%

0.5%

13.9%

17.2%

28.2%

100%

© Office of Chief Economist Page 12 of 24

While, coal resource base spread out in some places such as

Bintuni Bay, Fak Fak, Sorong and Raja Ampat. Coal reserve in

Bintuni Bay Regency available in Horna (4.5 million metric

tons) and Timbuni with total reserve of 14.29 million metric

tons. Calorie value produced by the coal reaches 5,870 –

7,935 calorie/kg. However the resources have not explored

commercially yet. The other potential mining and quarrying

resources in West Papua are copper, zinc, nickel, iron ore,

granite, gold, lime stone, marble, and phosphate.

The potency of Agriculture, Plantation and Forestry Sectors

In 2006, the percentage of land size used for agriculture

purposes of the total land size that suitable for agriculture in

West Papua is still around 21.3 percent. It means that land for

developing the agriculture business in West Papua is still

available. Some products that potential to develop in this

region are paddy rice, corn, cassava, sweet potato, and

vegetables. So far, some agriculture commodities that have

been developed commercially in large estate are cacao, and

palm oil tree. While, smallhoders estate are more vary, such

as coconut, palm oil, clove, coffee and cacao. Cacao

plantation is concentrated in Manokwari Regency, mainly in

the districts of Ransiki, Oransbari, Warmare and Prafi. One of

the largest cocoa plant in West Papua owned by PT Cokran,

who manage land size of 20,000 Ha. While PTPN II is the

largest state own company who operates palm oil plantation

in West Papua. Other big operator, Medco Papua Hijau

Selaras, will come and join the business further.

In West Papua, some

agriculture

commodities that have

been developed

commercially in large

estate are cacao and

palm oil

© Office of Chief Economist Page 13 of 24

Forestry and its products such as plywood and furniture

products are also potential to developed in West Papua.

Prohibition in shipping log to other region contributes to the

development of local wood processing industry. Furniture

industry can be found in the regency of South Sorong which

spread out in Terminabua District, Ayamaru District,

Moswaren District, Aitinyo Disctrict, and Alfiat District. In

Sorong, a lot of Small and Medium Enterprices (SME) work in

the area of wood processing business. Their machineries and

other equipments are fairly sufficient.

Figure 10. Potential Plantation Business in West Papua. Cacao and Palm Oil are two main

agriculture commodities that can be developed in West Papua, especially in Manokwari regency.

However, the processing industry for those two products are still limited. That is the main reason

why those commodities are still cannot give a significant added value to the West Papua

economy. (Source: Regional Government of West Papua Province, Business and Investment

Opportunity in West Papua Province)

Kokas District, Kaimana District, Teluk Arguni District, and Teluk

Etna District

FakFakCoffee

Teluk Wondama

Raja Ampat

Sorong Selatan

PT Nusa Irian Indah has developed cocoa plantation area in Babo as extensive as 5,000 Ha

Teluk Bintuni

Kebar PlainManokwari

One of the leading commodity to be developed at Fak Fak District

Kokas District, Kaimana District, Teluk Arguni District

Fak FakNutmeg

Manokwari regency has the largest cocoa plantation area in Papua Barat. PT Coklat

Ransiki has developed cocoa plantation area as extensive as 1,668 Ha in Ransiki.

Ransiki District, Oransbari, Warmare, and Prafi

ManokwariCocoa

Teluk Wondama

Sorong Selatan

PT Varita Majutama in Babo will build palm

plantation as extensive as 90,000 Ha

Teluk Bintuni

Teluk Wondama

480,000 Ha is suitable for coconut plantationSorongCoconut

Potential area to be developed as palm plantation

in Buruway District is 18,818.75 Ha

Buruway District, Kokas District,

Kaimana District

Fak Fak

431,000 Ha is suitable for palm plantationSorong

Pam Island, Kofiau, SalawatiRaja Ampat

According to Pusat Penelitian Kelapa Sawit

(PPKS) study, available land suitable and ready to be developed for palm commodity in Prafi plain

is as extensive as 13,855Ha.

Prafi Plain, Ransiki PlainManokwariPalm

District NotesRegency/CityPlantation Sector

Potency

Kokas District, Kaimana District, Teluk Arguni District, and Teluk

Etna District

FakFakCoffee

Teluk Wondama

Raja Ampat

Sorong Selatan

PT Nusa Irian Indah has developed cocoa plantation area in Babo as extensive as 5,000 Ha

Teluk Bintuni

Kebar PlainManokwari

One of the leading commodity to be developed at Fak Fak District

Kokas District, Kaimana District, Teluk Arguni District

Fak FakNutmeg

Manokwari regency has the largest cocoa plantation area in Papua Barat. PT Coklat

Ransiki has developed cocoa plantation area as extensive as 1,668 Ha in Ransiki.

Ransiki District, Oransbari, Warmare, and Prafi

ManokwariCocoa

Teluk Wondama

Sorong Selatan

PT Varita Majutama in Babo will build palm

plantation as extensive as 90,000 Ha

Teluk Bintuni

Teluk Wondama

480,000 Ha is suitable for coconut plantationSorongCoconut

Potential area to be developed as palm plantation

in Buruway District is 18,818.75 Ha

Buruway District, Kokas District,

Kaimana District

Fak Fak

431,000 Ha is suitable for palm plantationSorong

Pam Island, Kofiau, SalawatiRaja Ampat

According to Pusat Penelitian Kelapa Sawit

(PPKS) study, available land suitable and ready to be developed for palm commodity in Prafi plain

is as extensive as 13,855Ha.

Prafi Plain, Ransiki PlainManokwariPalm

District NotesRegency/CityPlantation Sector

Potency

© Office of Chief Economist Page 14 of 24

Potential Opportunity in Marine and Fishery Sectors

West Papua’s large coastal and waters territory makes this

area to be very potential zone to develop fishery industry. The

fishery potency in Arafuru Ocean, especially in the regencies

of Bintuni Bay, Fak Fak and Kaimana is predicted around

799,566 tons. However, only 273,566 ton or representing

some 35.87 percent of the total has been explored yet.

Variety of the marine resource in West Papua are lobsters,

prawns, pomfrets, tunas, cabs, several kinds of seaweeds,

seabass, snappers, shark fins, Spanish Mackerel, squids, and

anchovies. Fishery sector receive a high attention in Sorong.

The city has a sufficient fishery seaport, which is completed

with jetty run by private sector. Fishery industry activities in

Sorong includes fishing, processing and canning.

Opportunity in Tourism Sector

Tourism sector is expected to be one of the leading sector in

West Papua in the future. Tourism activity that can be offered

are eco tourism such as fauna sanctuary in Sidey Wabian and

natural preserve, under water tourism such as small islands of

Raja Ampat, cultural tourism like Papera Monument, and

religious tourism in Mansinam Island. Several investment

opportunities in West Papua are:

1. Organizing/managing tourism objects, and put it into

tourism package.

2. Build up some travel agencies

3. Developing other supporting facilities for tourism activities

such as hotels, restaurants, including its derivatives like

handicraft centre.

Investment in West Papua

West Papua Province needs investors to help the region to

develop in order to boost its economic growth, creating

working opportunities, as well as improving its business

competitive edge. Investor’s interest in investing in West

Papua is fairly high. It can be seen from the escalation in

investment approval level. Local investment approval in 2008

was 40 projects worth IDR7.62 trillion, increased from IDR6.52

trillion from previous year. While investment approval of

West Papua has huge

marine and fishery

potency which are not

fully explored yet

Tourism sector,

which mainly be

stressed on the eco

tourism sector, is

expected to be one

of the leading sector

in the future in West

Papua

Although investment

approval in West

Papua is increasing, its

realization is still fairly

low

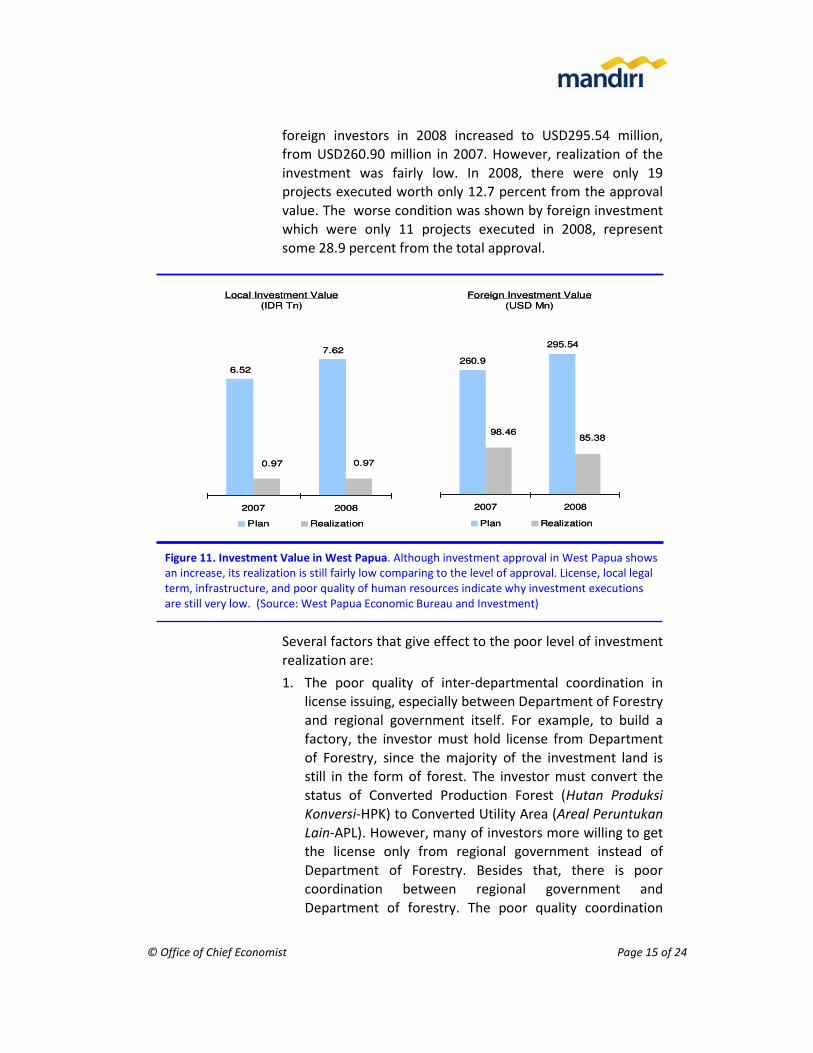

© Office of Chief Economist Page 15 of 24

foreign investors in 2008 increased to USD295.54 million,

from USD260.90 million in 2007. However, realization of the

investment was fairly low. In 2008, there were only 19

projects executed worth only 12.7 percent from the approval

value. The worse condition was shown by foreign investment

which were only 11 projects executed in 2008, represent

some 28.9 percent from the total approval.

Several factors that give effect to the poor level of investment

realization are:

1. The poor quality of inter-departmental coordination in

license issuing, especially between Department of Forestry

and regional government itself. For example, to build a

factory, the investor must hold license from Department

of Forestry, since the majority of the investment land is

still in the form of forest. The investor must convert the

status of Converted Production Forest (Hutan Produksi

Konversi-HPK) to Converted Utility Area (Areal Peruntukan

Lain-APL). However, many of investors more willing to get

the license only from regional government instead of

Department of Forestry. Besides that, there is poor

coordination between regional government and

Department of forestry. The poor quality coordination

Figure 11. Investment Value in West Papua. Although investment approval in West Papua shows

an increase, its realization is still fairly low comparing to the level of approval. License, local legal

term, infrastructure, and poor quality of human resources indicate why investment executions

are still very low. (Source: West Papua Economic Bureau and Investment)

6.52

7.62

0.970.97

2007 2008

Plan Realization

Local Investment Value

(IDR Tn)

Foreign Investment Value

(USD Mn)

260.9

295.54

85.3898.46

2007 2008

Plan Realization

6.52

7.62

0.970.97

2007 2008

Plan Realization

Local Investment Value

(IDR Tn)

Foreign Investment Value

(USD Mn)

260.9

295.54

85.3898.46

2007 2008

Plan Realization

© Office of Chief Economist Page 16 of 24

some of the time resulted to the ongoing investment

project has to be given up before law.

2. Law no. 21 / 2001 regarding Special Autonomy for Papua

and West Papua Provinces, specifically article no. 43

accomodates a protection to local people’s (tribes) rights,

which one of them is rights of land. Consequently,

conflicts between the investors and the tribe are often

occur, disputing the rights of land. Therefore, in practice,

legal certainty on this matter is an urgent thing to settle. A

more detail technical policy is and active role of the local

government needed in overcoming the problem.

3. Limited infrastructure facilities.

4. Human resource quality that is still fairly low

By distribution, Sorong Regency, Sorong City, Manokwari

Regency and Raja Ampat Regency are the most wanted region

for investment. Some big investments in West Papua can be

seen in the table below:

© Office of Chief Economist Page 17 of 24

Conclusion

1. West Papua economy grows by 6.6 percent annually.

Different from the structure of Papua Province’s GDP

which is dominated by mining and quarrying (contribute

about 50% of total Regional GDP), West Papua Province’s

GDP structure is more vary where agriculture sector gives

some 28.2 percent contribution to the Regional Gross

Domestic Product, follows by mining and quarrying,

processing industry, services, trading, hotel and

restaurant.

2. Foreign investment realization in Papua has exceeded the

target, however domestic investment realization still

below target which is lower than 50% of initial target.

However, we recognize that foreign investment

Figure 12. Some Big Investments in West Papua. Some big investors move their wheel of

investments during 2008 in the area of general mining, integrated palm plantations, cacao

plantations, plywoods and forestry, timber and forestry, and fisheries. (Source: West Papua

Economic and Investment Bureau)

42,929 (IDR Mn)44,019 (IDR Mn)KaimanaPT. Avona Mina Lestari

6,445 (IDR Mn)969,300 (IDR Mn)ManokwariPT. Bintuni Mina RayaFrozen Fish

10,000 (IDR Mn)16,950 (IDR Mn)ManokwariPT Inter GalaxiFishery

10,209 (USD 000)10,209 (USD 000)Sorong CityPT Alfa Kurnia Fish

Enterprise

19,222 (USD 000)7,889 (USD000)Sorong CityPT. West Irian Fishing

Industry

Shrimp

37,697 (IDR Mn)106,424 (IDR Mn)Sorong CityPT. Henrison IrianaForestry

-34,200 (USD 000)KaimanaPT. Energi Alam RayaSteam Thermal Coal Power

-105,000 (IDR Mn)Raja AmpatPT. Balerang Bina PersadaSawmill, Moulding, Drykin

17,320 (USD 000)542 (USD 000)Sorong CityPT United Can Co. LtdCan Industry

15,773 (USD 000)700 (USD 000)SorongPT. Tung YangVeneer, Moulding, and Building Materials

21,540 (IDR Mn)70,799 (IDR Mn)SorongPT. Intimpura Timber Co.Logging

15,773 (USD 000)12,310 (USD 000)Raja AmpatPT. Gak NikelMining

-872,000 (IDR Mn)SorongPT. Inti Kebun Sawit

297,857 (IDR Mn)191,973 (IDR Mn)ManokwariPT. Perkebunan Nusantara IIPalm Plantation and Crude Palm Oil

150,992 (IDR Mn)

150,992 (IDR Mn)

14,843 (USD 000)

472,240 (IDR Mn)

Investment Plan (IDR Mn)

12,928 (USD 000)ManokwariPT Coklat RansikiCacao Plantation

-SorongPT. Henrison Inti Persada

128,400 (IDR Mn)Fak FakPT. Prabu AlaskaWood, Plywood, Blackboard

128,400 (IDR Mn)KaimanaPT Adi Jaya Mulia

Regency/CityInvestment Realization

(IDR Mn)CompanySector

42,929 (IDR Mn)44,019 (IDR Mn)KaimanaPT. Avona Mina Lestari

6,445 (IDR Mn)969,300 (IDR Mn)ManokwariPT. Bintuni Mina RayaFrozen Fish

10,000 (IDR Mn)16,950 (IDR Mn)ManokwariPT Inter GalaxiFishery

10,209 (USD 000)10,209 (USD 000)Sorong CityPT Alfa Kurnia Fish

Enterprise

19,222 (USD 000)7,889 (USD000)Sorong CityPT. West Irian Fishing

Industry

Shrimp

37,697 (IDR Mn)106,424 (IDR Mn)Sorong CityPT. Henrison IrianaForestry

-34,200 (USD 000)KaimanaPT. Energi Alam RayaSteam Thermal Coal Power

-105,000 (IDR Mn)Raja AmpatPT. Balerang Bina PersadaSawmill, Moulding, Drykin

17,320 (USD 000)542 (USD 000)Sorong CityPT United Can Co. LtdCan Industry

15,773 (USD 000)700 (USD 000)SorongPT. Tung YangVeneer, Moulding, and Building Materials

21,540 (IDR Mn)70,799 (IDR Mn)SorongPT. Intimpura Timber Co.Logging

15,773 (USD 000)12,310 (USD 000)Raja AmpatPT. Gak NikelMining

-872,000 (IDR Mn)SorongPT. Inti Kebun Sawit

297,857 (IDR Mn)191,973 (IDR Mn)ManokwariPT. Perkebunan Nusantara IIPalm Plantation and Crude Palm Oil

150,992 (IDR Mn)

150,992 (IDR Mn)

14,843 (USD 000)

472,240 (IDR Mn)

Investment Plan (IDR Mn)

12,928 (USD 000)ManokwariPT Coklat RansikiCacao Plantation

-SorongPT. Henrison Inti Persada

128,400 (IDR Mn)Fak FakPT. Prabu AlaskaWood, Plywood, Blackboard

128,400 (IDR Mn)KaimanaPT Adi Jaya Mulia

Regency/CityInvestment Realization

(IDR Mn)CompanySector

© Office of Chief Economist Page 18 of 24

distribution pattern in Papua province is centered in one

regency and focused on mining sector which booked very

high value of investment (Freeport).

3. The investor’s interest to invest in West Papua is actually

fairly high, shown by the increasing investment approval.

However, the projects execution level are still fairly low.

4. Finally, we found some factors causing low investment

realization in Papua and West Papua Province, there are :

poor inter-departmental coordination as well as central

and local government coordination related to license

issuing process, tribe rights, limited infrastructure

facilities, and lack of high skilled work force.

© Office of Chief Economist Page 19 of 24

Indonesia economy expanded by 4.0% yoy or 2.3% qoq in

2Q09, higher than ours and consensus estimates. Despite

growing at slower pace compared to the previous quarter,

Indonesia’s economy is among few economies that could grow

in 2Q09, the fastest after China 7.9% yoy according to

Bloomberg. Indonesia economy expanded by 4.2% yoy in

1H09.

Domestic demand, particularly private consumption continued

to be the back bone of economic growth, albeit moderated.

Private consumption grew 4.8% in 2Q09 vs. 6.0% in 1Q09.

Meanwhile investments remained weak; growing at slower

rate of 2.7% yoy in 2Q09 compared to 3.4% yoy in 1Q09, led

by the decline in machinery and equipment imports (-13% yoy

in 2Q09 vs. -9.0% yoy in 1Q09).

Net exports contribution rose to 2.0ppt to total GDP growth in

2Q09 increased from 1.2ppt in the previous quarter that help

to offset weaker domestic demand. We think this trend would

likely continue for several quarters triggered by recovery in

global economy and relative weak imports demand as the

economy runs below its capacity. IMF on its July World

Economic Outlook update forecasted that world economy is

likely to recover in 2010 growing by 2.5% yoy from a

contraction -1.4% yoy. Figure 2 shows that the net exports

Domestic demand

remained the main

driver of the economy

External demand

compensated softened

domestic demand.

Indonesia slowed

to 4.0% yoy in 2Q09

Figure 13. 2Q09 GDP Summary. We remain positive on the Indonesia’s economic prospect in

the 2H09. Faster government spending, more aggressive banks credit expansion, and

improvement in external demand would support the economy in 2H09. We expect the economy

to grow by 4% for the full year 09, although we see an upside risk of the growth given the robust

first half result. (Source: Bloomberg, CEIC, Mandiri Sekuritas)

Mandiri Consensus

% yoy % yoy % qoq % yoy % yoy % yoy % qoq % yoy

GDP 6.1 4.4 1.7 3.8 3.8 4.0 2.3 4.0

Private Consumption Exp 5.3 6.0 0.9 5.0 - 4.8 0.2 5.3

Government Exp 10.4 19.2 (28.7) 13.8 - 17.0 23.7 13.9

Gross Fixed Capital Formation 11.7 3.4 (5.4) 3.4 - 2.7 2.4 4.6

Export of Goods and Services 9.5 (18.7) (16.7) (17.8) - (15.7) 7.4 (15.6)

Import of Goods and Services 10.0 (26.0) (20.7) (18.8) - (23.9) 7.8 (16.5)

20082Q09F

2009F2Q091Q09

2Q09 GDP: ABOVE EXPECTATIONS Destry Damayanti & Aldian Taloputra, PT Mandiri Sekuritas

© Office of Chief Economist Page 20 of 24

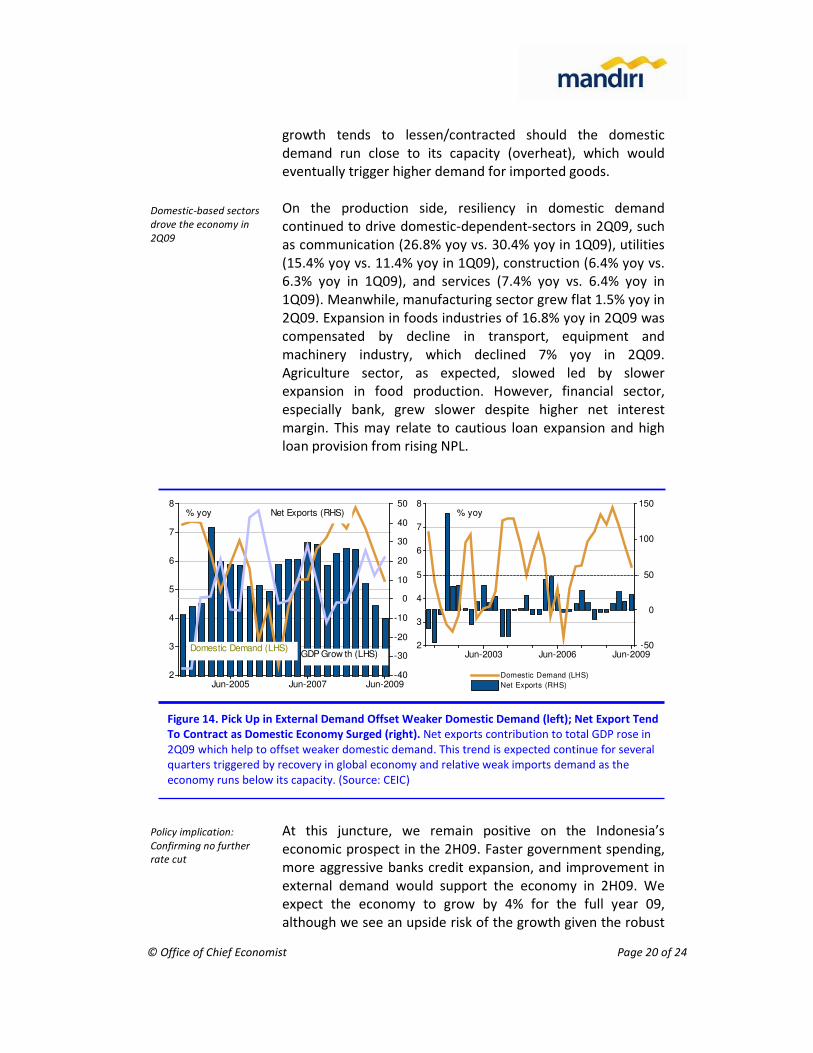

growth tends to lessen/contracted should the domestic

demand run close to its capacity (overheat), which would

eventually trigger higher demand for imported goods.

On the production side, resiliency in domestic demand

continued to drive domestic-dependent-sectors in 2Q09, such

as communication (26.8% yoy vs. 30.4% yoy in 1Q09), utilities

(15.4% yoy vs. 11.4% yoy in 1Q09), construction (6.4% yoy vs.

6.3% yoy in 1Q09), and services (7.4% yoy vs. 6.4% yoy in

1Q09). Meanwhile, manufacturing sector grew flat 1.5% yoy in

2Q09. Expansion in foods industries of 16.8% yoy in 2Q09 was

compensated by decline in transport, equipment and

machinery industry, which declined 7% yoy in 2Q09.

Agriculture sector, as expected, slowed led by slower

expansion in food production. However, financial sector,

especially bank, grew slower despite higher net interest

margin. This may relate to cautious loan expansion and high

loan provision from rising NPL.

At this juncture, we remain positive on the Indonesia’s

economic prospect in the 2H09. Faster government spending,

more aggressive banks credit expansion, and improvement in

external demand would support the economy in 2H09. We

expect the economy to grow by 4% for the full year 09,

although we see an upside risk of the growth given the robust

Domestic-based sectors

drove the economy in

2Q09

Policy implication:

Confirming no further

rate cut

Figure 14. Pick Up in External Demand Offset Weaker Domestic Demand (left); Net Export Tend

To Contract as Domestic Economy Surged (right). Net exports contribution to total GDP rose in

2Q09 which help to offset weaker domestic demand. This trend is expected continue for several

quarters triggered by recovery in global economy and relative weak imports demand as the

economy runs below its capacity. (Source: CEIC)

Jun-2005 Jun-2007 Jun-2009

8

7

6

5

4

3

2

50

40

30

20

10

0

-10

-20

-30

-40

GDP Grow th (LHS)Domestic Demand (LHS)

Net Exports (RHS)% yoy

Jun-2003 Jun-2006 Jun-2009

8

7

6

5

4

3

2

150

100

50

0

-50

Domestic Demand (LHS)

Net Exports (RHS)

% yoy

© Office of Chief Economist Page 21 of 24

first half result. Having said that and coupled with higher

inflation risk in 2010, we reiterate our view of no further rate

cut this year.

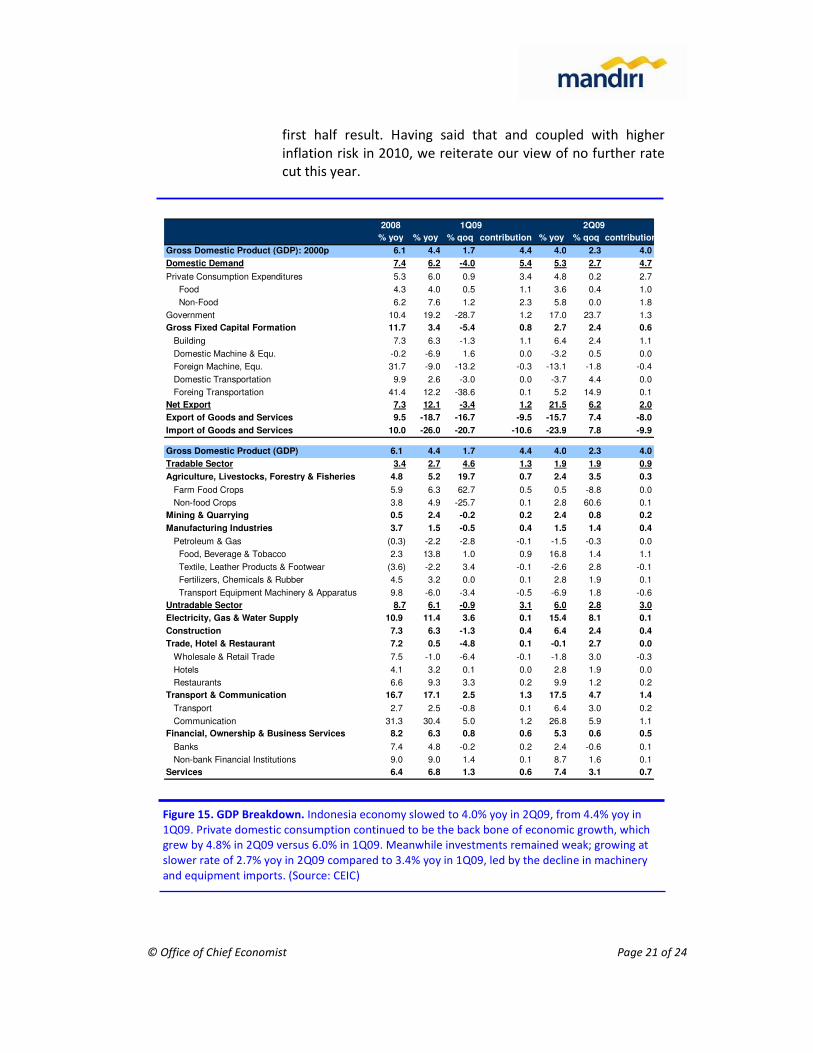

Figure 15. GDP Breakdown. Indonesia economy slowed to 4.0% yoy in 2Q09, from 4.4% yoy in

1Q09. Private domestic consumption continued to be the back bone of economic growth, which

grew by 4.8% in 2Q09 versus 6.0% in 1Q09. Meanwhile investments remained weak; growing at

slower rate of 2.7% yoy in 2Q09 compared to 3.4% yoy in 1Q09, led by the decline in machinery

and equipment imports. (Source: CEIC)

2008

% yoy % yoy % qoq contribution % yoy % qoq contribution

Gross Domestic Product (GDP): 2000p 6.1 4.4 1.7 4.4 4.0 2.3 4.0

Domestic Demand 7.4 6.2 -4.0 5.4 5.3 2.7 4.7

Private Consumption Expenditures 5.3 6.0 0.9 3.4 4.8 0.2 2.7

Food 4.3 4.0 0.5 1.1 3.6 0.4 1.0

Non-Food 6.2 7.6 1.2 2.3 5.8 0.0 1.8

Government 10.4 19.2 -28.7 1.2 17.0 23.7 1.3

Gross Fixed Capital Formation 11.7 3.4 -5.4 0.8 2.7 2.4 0.6

Building 7.3 6.3 -1.3 1.1 6.4 2.4 1.1

Domestic Machine & Equ. -0.2 -6.9 1.6 0.0 -3.2 0.5 0.0

Foreign Machine, Equ. 31.7 -9.0 -13.2 -0.3 -13.1 -1.8 -0.4

Domestic Transportation 9.9 2.6 -3.0 0.0 -3.7 4.4 0.0

Foreing Transportation 41.4 12.2 -38.6 0.1 5.2 14.9 0.1

Net Export 7.3 12.1 -3.4 1.2 21.5 6.2 2.0

Export of Goods and Services 9.5 -18.7 -16.7 -9.5 -15.7 7.4 -8.0

Import of Goods and Services 10.0 -26.0 -20.7 -10.6 -23.9 7.8 -9.9

Gross Domestic Product (GDP) 6.1 4.4 1.7 4.4 4.0 2.3 4.0

Tradable Sector 3.4 2.7 4.6 1.3 1.9 1.9 0.9

Agriculture, Livestocks, Forestry & Fisheries 4.8 5.2 19.7 0.7 2.4 3.5 0.3

Farm Food Crops 5.9 6.3 62.7 0.5 0.5 -8.8 0.0

Non-food Crops 3.8 4.9 -25.7 0.1 2.8 60.6 0.1

Mining & Quarrying 0.5 2.4 -0.2 0.2 2.4 0.8 0.2

Manufacturing Industries 3.7 1.5 -0.5 0.4 1.5 1.4 0.4

Petroleum & Gas (0.3) -2.2 -2.8 -0.1 -1.5 -0.3 0.0

Food, Beverage & Tobacco 2.3 13.8 1.0 0.9 16.8 1.4 1.1

Textile, Leather Products & Footwear (3.6) -2.2 3.4 -0.1 -2.6 2.8 -0.1

Fertilizers, Chemicals & Rubber 4.5 3.2 0.0 0.1 2.8 1.9 0.1

Transport Equipment Machinery & Apparatus 9.8 -6.0 -3.4 -0.5 -6.9 1.8 -0.6

Untradable Sector 8.7 6.1 -0.9 3.1 6.0 2.8 3.0

Electricity, Gas & Water Supply 10.9 11.4 3.6 0.1 15.4 8.1 0.1

Construction 7.3 6.3 -1.3 0.4 6.4 2.4 0.4

Trade, Hotel & Restaurant 7.2 0.5 -4.8 0.1 -0.1 2.7 0.0

Wholesale & Retail Trade 7.5 -1.0 -6.4 -0.1 -1.8 3.0 -0.3

Hotels 4.1 3.2 0.1 0.0 2.8 1.9 0.0

Restaurants 6.6 9.3 3.3 0.2 9.9 1.2 0.2

Transport & Communication 16.7 17.1 2.5 1.3 17.5 4.7 1.4

Transport 2.7 2.5 -0.8 0.1 6.4 3.0 0.2

Communication 31.3 30.4 5.0 1.2 26.8 5.9 1.1

Financial, Ownership & Business Services 8.2 6.3 0.8 0.6 5.3 0.6 0.5

Banks 7.4 4.8 -0.2 0.2 2.4 -0.6 0.1

Non-bank Financial Institutions 9.0 9.0 1.4 0.1 8.7 1.6 0.1

Services 6.4 6.8 1.3 0.6 7.4 3.1 0.7

1Q09 2Q09

© Office of Chief Economist Page 22 of 24

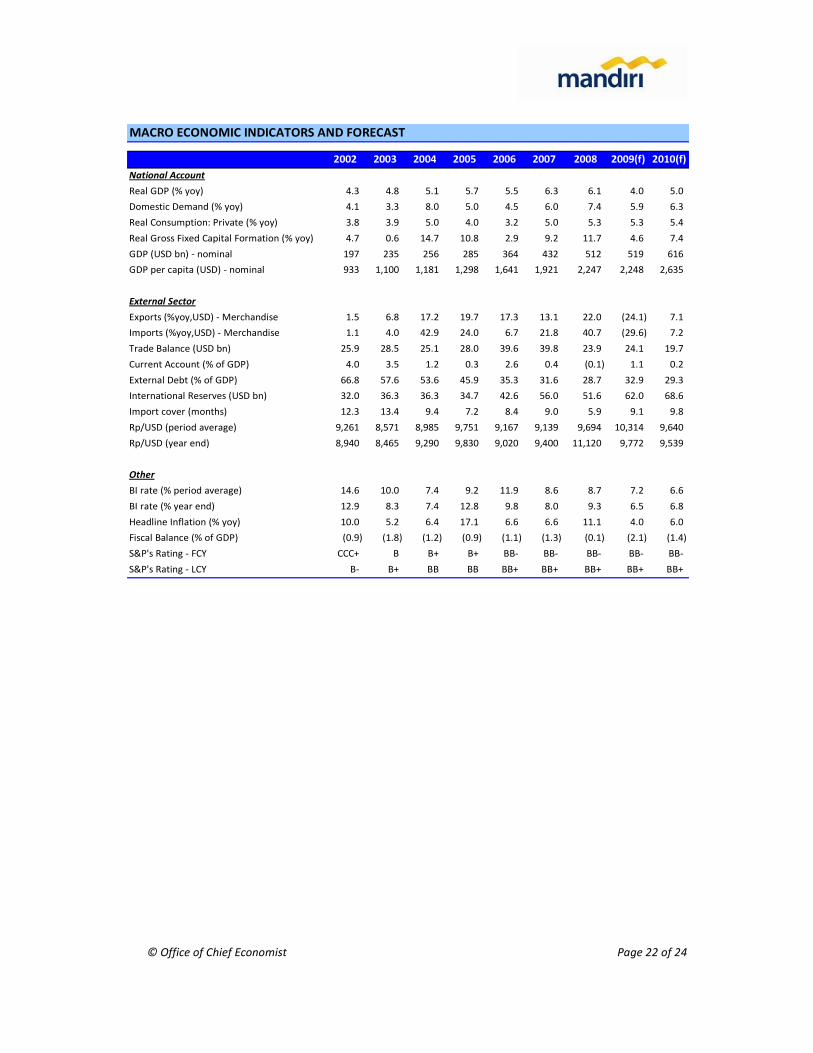

2002 2003 2004 2005 2006 2007 2008 2009(f) 2010(f)

National Account

Real GDP (% yoy) 4.3 4.8 5.1 5.7 5.5 6.3 6.1 4.0 5.0

Domestic Demand (% yoy) 4.1 3.3 8.0 5.0 4.5 6.0 7.4 5.9 6.3

Real Consumption: Private (% yoy) 3.8 3.9 5.0 4.0 3.2 5.0 5.3 5.3 5.4

Real Gross Fixed Capital Formation (% yoy) 4.7 0.6 14.7 10.8 2.9 9.2 11.7 4.6 7.4

GDP (USD bn) - nominal 197 235 256 285 364 432 512 519 616

GDP per capita (USD) - nominal 933 1,100 1,181 1,298 1,641 1,921 2,247 2,248 2,635

External Sector

Exports (%yoy,USD) - Merchandise 1.5 6.8 17.2 19.7 17.3 13.1 22.0 (24.1) 7.1

Imports (%yoy,USD) - Merchandise 1.1 4.0 42.9 24.0 6.7 21.8 40.7 (29.6) 7.2

Trade Balance (USD bn) 25.9 28.5 25.1 28.0 39.6 39.8 23.9 24.1 19.7

Current Account (% of GDP) 4.0 3.5 1.2 0.3 2.6 0.4 (0.1) 1.1 0.2

External Debt (% of GDP) 66.8 57.6 53.6 45.9 35.3 31.6 28.7 32.9 29.3

International Reserves (USD bn) 32.0 36.3 36.3 34.7 42.6 56.0 51.6 62.0 68.6

Import cover (months) 12.3 13.4 9.4 7.2 8.4 9.0 5.9 9.1 9.8

Rp/USD (period average) 9,261 8,571 8,985 9,751 9,167 9,139 9,694 10,314 9,640

Rp/USD (year end) 8,940 8,465 9,290 9,830 9,020 9,400 11,120 9,772 9,539

Other

BI rate (% period average) 14.6 10.0 7.4 9.2 11.9 8.6 8.7 7.2 6.6

BI rate (% year end) 12.9 8.3 7.4 12.8 9.8 8.0 9.3 6.5 6.8

Headline Inflation (% yoy) 10.0 5.2 6.4 17.1 6.6 6.6 11.1 4.0 6.0

Fiscal Balance (% of GDP) (0.9) (1.8) (1.2) (0.9) (1.1) (1.3) (0.1) (2.1) (1.4)

S&P's Rating - FCY CCC+ B B+ B+ BB- BB- BB- BB- BB-

S&P's Rating - LCY B- B+ BB BB BB+ BB+ BB+ BB+ BB+

MACRO ECONOMIC INDICATORS AND FORECAST

© Office of Chief Economist Page 23 of 24

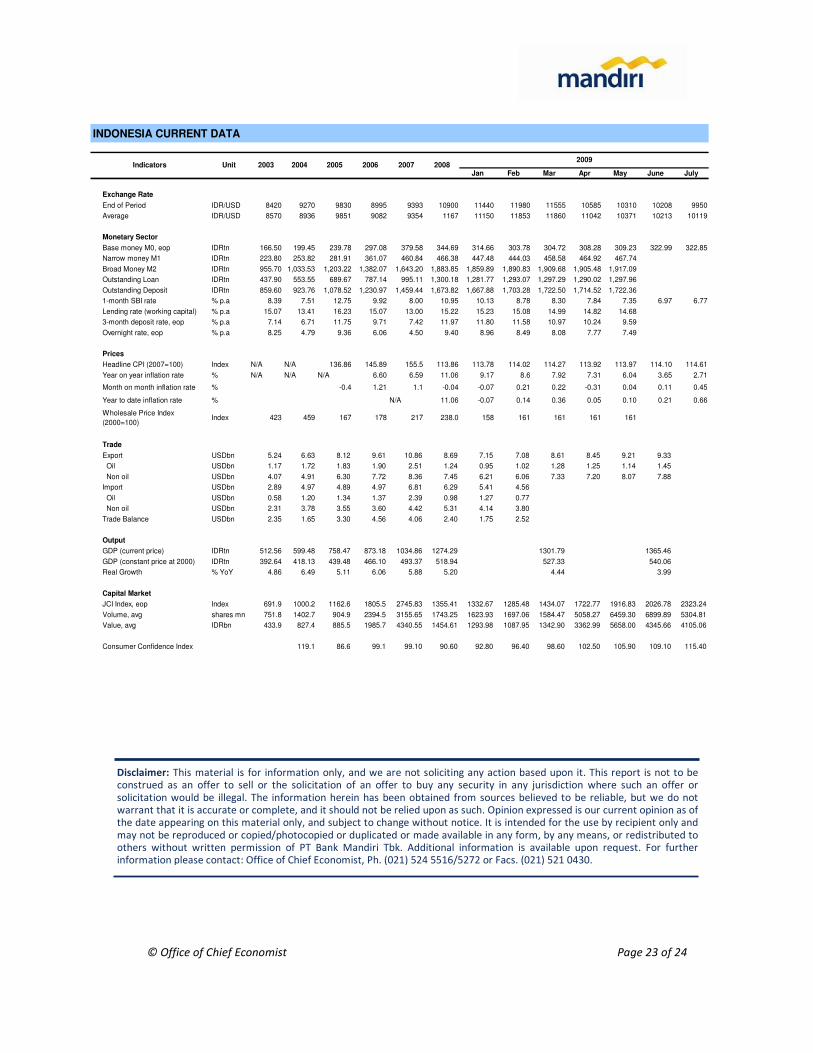

INDONESIA CURRENT DATA

Jan Feb Mar Apr May June July

Exchange Rate

End of Period IDR/USD 8420 9270 9830 8995 9393 10900 11440 11980 11555 10585 10310 10208 9950

Average IDR/USD 8570 8936 9851 9082 9354 1167 11150 11853 11860 11042 10371 10213 10119

Monetary Sector

Base money M0, eop IDRtn 166.50 199.45 239.78 297.08 379.58 344.69 314.66 303.78 304.72 308.28 309.23 322.99 322.85

Narrow money M1 IDRtn 223.80 253.82 281.91 361.07 460.84 466.38 447.48 444.03 458.58 464.92 467.74

Broad Money M2 IDRtn 955.70 1,033.53 1,203.22 1,382.07 1,643.20 1,883.85 1,859.89 1,890.83 1,909.68 1,905.48 1,917.09

Outstanding Loan IDRtn 437.90 553.55 689.67 787.14 995.11 1,300.18 1,281.77 1,293.07 1,297.29 1,290.02 1,297.96

Outstanding Deposit IDRtn 859.60 923.76 1,078.52 1,230.97 1,459.44 1,673.82 1,667.88 1,703.28 1,722.50 1,714.52 1,722.36

1-month SBI rate % p.a 8.39 7.51 12.75 9.92 8.00 10.95 10.13 8.78 8.30 7.84 7.35 6.97 6.77

Lending rate (working capital) % p.a 15.07 13.41 16.23 15.07 13.00 15.22 15.23 15.08 14.99 14.82 14.68

3-month deposit rate, eop % p.a 7.14 6.71 11.75 9.71 7.42 11.97 11.80 11.58 10.97 10.24 9.59

Overnight rate, eop % p.a 8.25 4.79 9.36 6.06 4.50 9.40 8.96 8.49 8.08 7.77 7.49

Prices

Headline CPI (2007=100) Index N/A N/A 136.86 145.89 155.5 113.86 113.78 114.02 114.27 113.92 113.97 114.10 114.61

Year on year inflation rate % N/A N/A N/A 6.60 6.59 11.06 9.17 8.6 7.92 7.31 6.04 3.65 2.71

Month on month inflation rate % -0.4 1.21 1.1 -0.04 -0.07 0.21 0.22 -0.31 0.04 0.11 0.45

Year to date inflation rate % N/A 11.06 -0.07 0.14 0.36 0.05 0.10 0.21 0.66

Wholesale Price Index

(2000=100)Index 423 459 167 178 217 238.0 158 161 161 161 161

Trade

Export USDbn 5.24 6.63 8.12 9.61 10.86 8.69 7.15 7.08 8.61 8.45 9.21 9.33

Oil USDbn 1.17 1.72 1.83 1.90 2.51 1.24 0.95 1.02 1.28 1.25 1.14 1.45

Non oil USDbn 4.07 4.91 6.30 7.72 8.36 7.45 6.21 6.06 7.33 7.20 8.07 7.88

Import USDbn 2.89 4.97 4.89 4.97 6.81 6.29 5.41 4.56

Oil USDbn 0.58 1.20 1.34 1.37 2.39 0.98 1.27 0.77

Non oil USDbn 2.31 3.78 3.55 3.60 4.42 5.31 4.14 3.80

Trade Balance USDbn 2.35 1.65 3.30 4.56 4.06 2.40 1.75 2.52

Output

GDP (current price) IDRtn 512.56 599.48 758.47 873.18 1034.86 1274.29 1301.79 1365.46

GDP (constant price at 2000) IDRtn 392.64 418.13 439.48 466.10 493.37 518.94 527.33 540.06

Real Growth % YoY 4.86 6.49 5.11 6.06 5.88 5.20 4.44 3.99

Capital Market

JCI Index, eop Index 691.9 1000.2 1162.6 1805.5 2745.83 1355.41 1332.67 1285.48 1434.07 1722.77 1916.83 2026.78 2323.24

Volume, avg shares mn 751.8 1402.7 904.9 2394.5 3155.65 1743.25 1623.93 1697.06 1584.47 5058.27 6459.30 6899.89 5304.81

Value, avg IDRbn 433.9 827.4 885.5 1985.7 4340.55 1454.61 1293.98 1087.95 1342.90 3362.99 5658.00 4345.66 4105.06

Consumer Confidence Index 119.1 86.6 99.1 99.10 90.60 92.80 96.40 98.60 102.50 105.90 109.10 115.40

2007 20082009

Indicators 2003 2004Unit 20062005

Disclaimer: This material is for information only, and we are not soliciting any action based upon it. This report is not to beconstrued as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or

solicitation would be illegal. The information herein has been obtained from sources believed to be reliable, but we do not warrant that it is accurate or complete, and it should not be relied upon as such. Opinion expressed is our current opinion as of the date appearing on this material only, and subject to change without notice. It is intended for the use by recipient only and

may not be reproduced or copied/photocopied or duplicated or made available in any form, by any means, or redistributed to others without written permission of PT Bank Mandiri Tbk. Additional information is available upon request. For further information please contact: Office of Chief Economist, Ph. (021) 524 5516/5272 or Facs. (021) 521 0430.

© Office of Chief Economist Page 24 of 24

OOvveerrsseeaass OOffffiicceess

Hongkong Branch

7th

Floor, Far East Finance Centre

16 Harcourt Road, Hongkong

Tel: 852-2527-6611

Fax: 852-2529-8131

Singapore Branch

3 Anson Road #12-01/02, Springleaf Tower

Singapore 079909

Tel: 65-6213-5688

Fax: 65-6438-3363

Cayman Islands Branch

Cardinal Plaza 3rd

Floor

30 Cardinal Avenue, PO Box 10198,

Grand Cayman, KY1-1002, Cayman Islands

Tel: 1-345-945-8891

Fax: 1-345-945-8892

Bank Mandiri (Europe) Limited, London

Cardinal Court (2nd

Floor),

23 Thomas More Street

London EIW IYY, United Kingdom

Tel: 44-207-553-8688

Fax: 44-207-553-8699

Shanghai Representative Office

3401, Bank of China Tower

200 Yin Cheng (M) Road,

Pudong New Area, Shanghai, 200120

People’s Republic of China

Tel: 86-21-5037-2509

Fax: 86-21-5037-2507

Dilli Branch – Timor Leste

Avenida Presidente Nicolao Lobato

No.12, Colmera

Dilli – Timor Leste

Tel: +670-331-7777

Fax: +670-331-7190/74444

HHeeaadd OOffffiiccee

Plaza Mandiri

Jl. Jend. Gatot Subroto Kav. 36-38

Jakarta 12190, Indonesia

Tel: (62-21) 526 5045 – 526 5095

Fax: (62-21) 526 8372 – 526 5008

Website: www.bankmandiri.co.id

Agus Martowardojo

President Director & CEO

Tel: (62-21) 524 5001, Fax: (62-21) 526 3459

I Wayan Agus Mertayasa

Deputy President Director

Tel: (62-21) 524 5969, Fax: (62-21) 526 3408

Riswinandi

Director Corporate Banking

Tel: (62-21) 524 5108, Fax: (62-21) 5296 4053

Zulkifli Zaini

Director Commercial Banking

Tel: (62-21) 524 5274, Fax: (62-21) 526 3617

Budi Gunadi Sadikin

Director Micro & Retail Banking

Tel: (62-21) 524 5649, Fax: (62-21) 252 1585

Thomas Arifin

Director Treasury & International Banking

Tel: (62-21) 524 5245, Fax: (62-21) 526 3763

Abdul Rachman

Director Special Assets Management

Tel: (62-21) 524 5653, Fax: (62-21) 252 4651

Ogi Prastomiyono

Director Compliance & Human Capital

Tel: (62-21) 524 5345, Fax: (62-21) 252 4651

Sentot A. Sentausa

Director Risk Management

Tel: (62-21) 524 5801, Fax: (62-21) 526 8213

Sasmita

Director Technology & Operation

Tel: (62-21) 524 5580, Fax: (62-21) 252 1585

Bambang Setiawan

Director Corporate Secretary, Legal & Customer Care

Tel: (62-21) 524 5040, Fax: (62-21) 252 1585

Pahala N. Mansury

EVP Coordinator Finance & Strategy

Tel: (62-21) 524 5577, Fax: (62-21) 526 8213

Haryanto Budiman

EVP Coordinator Change Management Office

Tel: (62-21) 524 5243, Fax: (62-21) 526 8213

Mansyur S. Nasution

EVP Coordinator Consumer Finance

Tel: (62-21) 524 5036, Fax: (62-21) 5296 4116

Riyani T. Bondan

EVP Coordinator Internal Audit

Tel: (62-21) 524 5131, Fax: (62-21) 526 3623