Embed Size (px)

Citation preview

Last Study Topics

• What To Discount• IM&C Project

Today’s Study Topics

• Project Analysis• Project Interaction– Equivalent Annual Cost– Replacement– Project Interaction– Timing– Fluctuating Load Factors

Project Analysis

• On an analysis of IM&C’s guano project. You started with a simplified statement of assets and income for the project that you used to develop a series of cash-flow forecasts.

• You were lucky to get away with just two NPV calculations. In real situations, it often takes several tries to purge all inconsistencies and mistakes.

Continue

• Then there are “what if” questions. – For example: What if inflation rages at 15 percent

per year, rather than 10? – What if technical problems delay start-up to year

2? – What if gardeners prefer chemical fertilizers to

your natural product?

Equivalent Annual Cost

• Equivalent Annual Cost ;• The cost per period with the same present

value as the cost of buying and operating a machine. OR

• Equivalent annual cost is the annual cash flow sufficient to recover a capital investment, including the cost of capital for that investment, over the investment’s economic life.

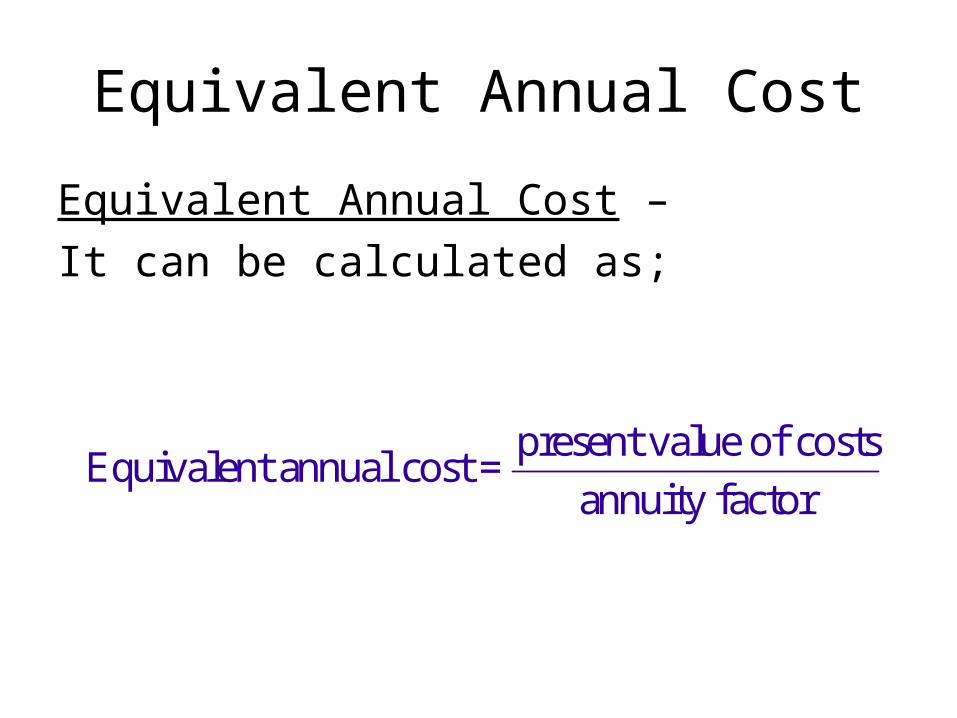

Equivalent Annual Cost

Equivalent Annual Cost – It can be calculated as;

Equivalent annual cost =present value of costs

annuity factor

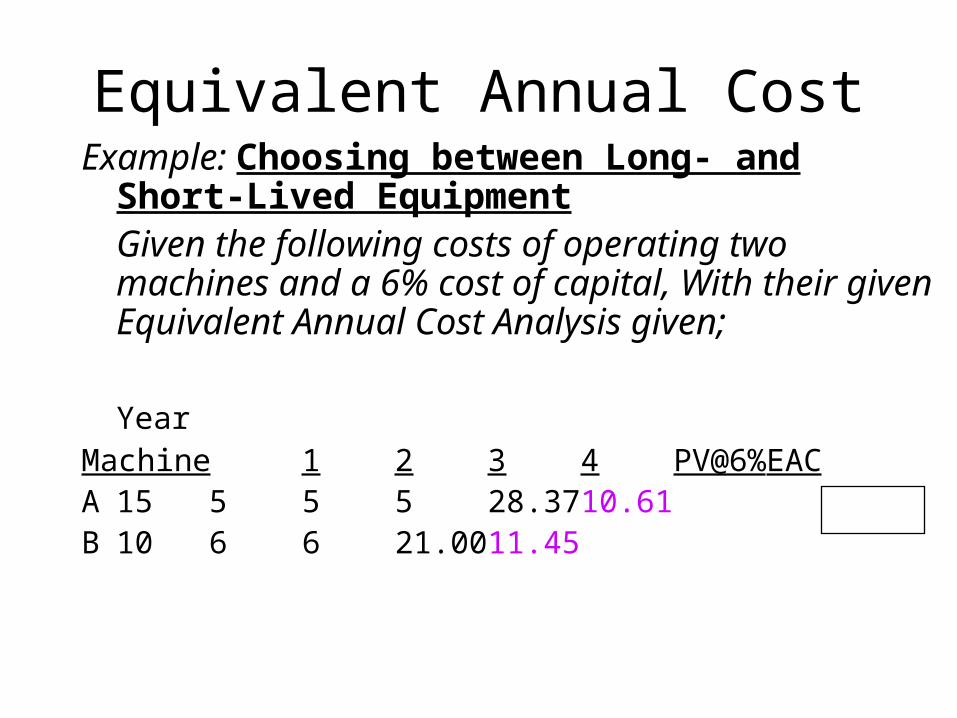

Equivalent Annual CostExample: Choosing between Long- and Short-Lived

EquipmentGiven the following costs of operating two machines and a 6% cost of capital, With their given Equivalent Annual Cost Analysis given;

YearMachine 1 2 3 4 PV@6% EACA 15 5 5 5 28.37 10.61B 10 6 6 21.00 11.45

Continue

• Should we take machine B, the one with the lower present value of costs? – Not necessarily, because B will have to be

replaced a year earlier than A.• Machine with total PV(costs) of $21,000

spread over three years (0, 1, and 2) is not necessarily better than a competing machine with PV(costs) of $28,370 spread over four years (0 through 3).

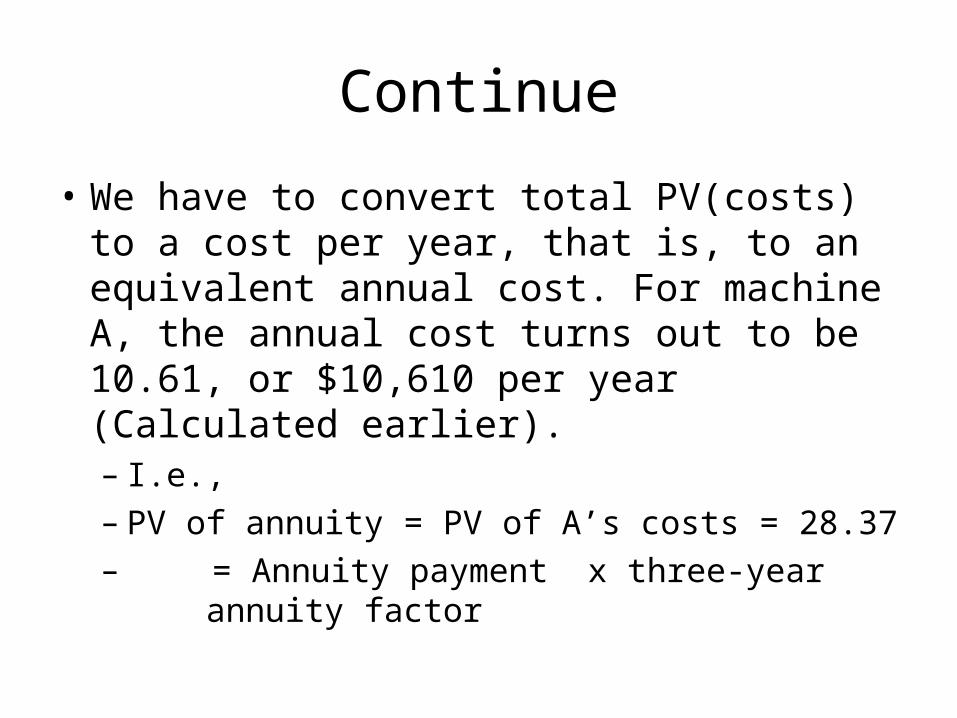

Continue

• We have to convert total PV(costs) to a cost per year, that is, to an equivalent annual cost. For machine A, the annual cost turns out to be 10.61, or $10,610 per year (Calculated earlier).– I.e.,– PV of annuity = PV of A’s costs = 28.37– = Annuity payment x three-

year annuity factor

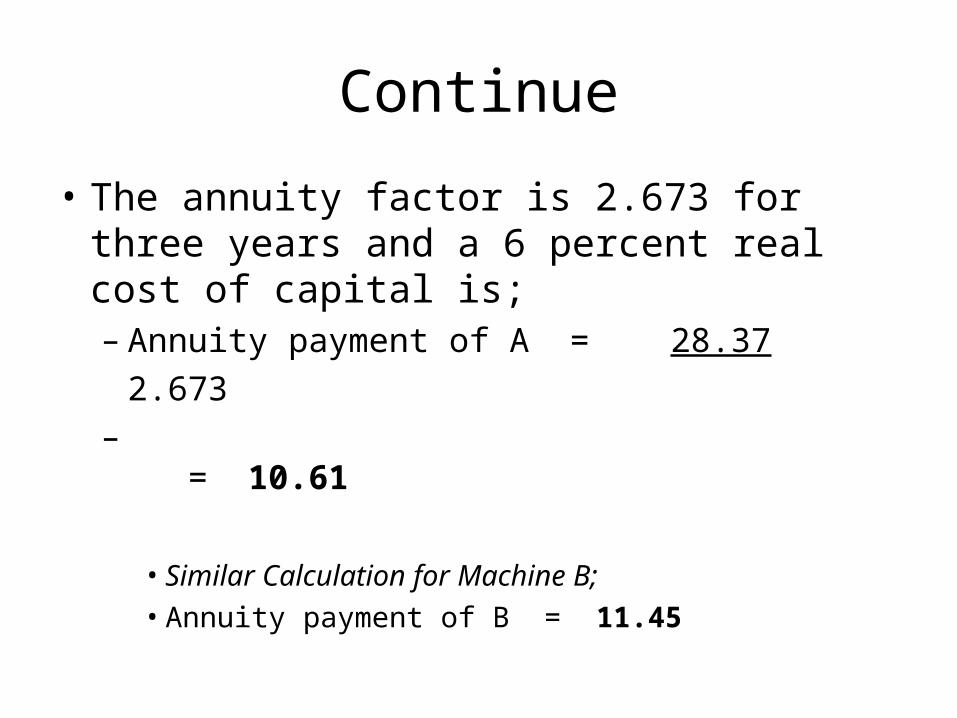

Continue

• The annuity factor is 2.673 for three years and a 6 percent real cost of capital is;– Annuity payment of A = 28.37

2.673– = 10.61

• Similar Calculation for Machine B;• Annuity payment of B = 11.45

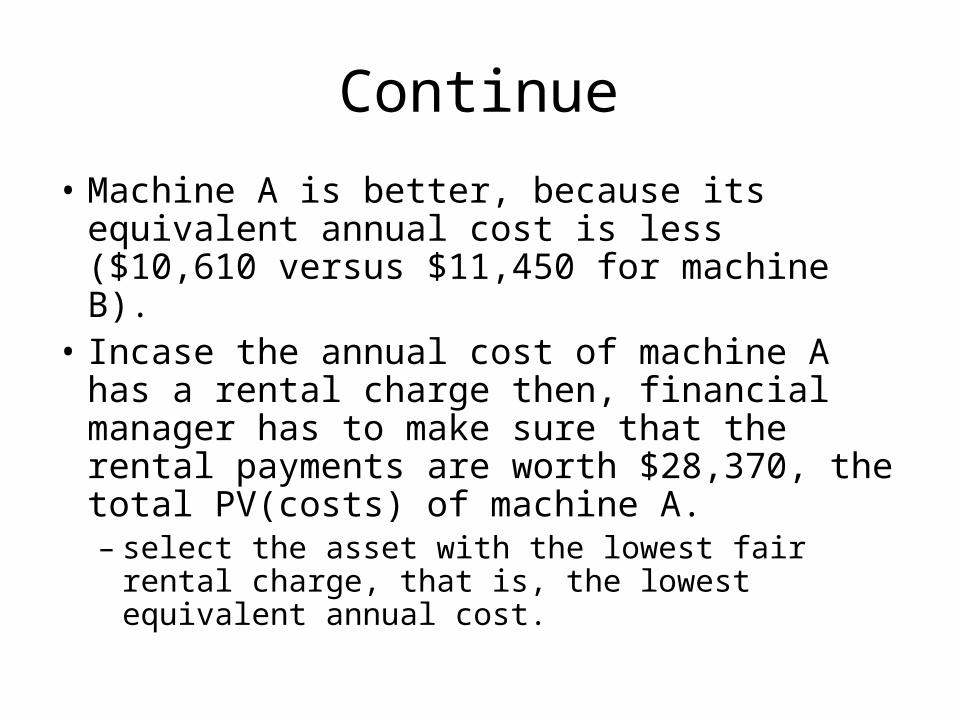

Continue

• Machine A is better, because its equivalent annual cost is less ($10,610 versus $11,450 for machine B).

• Incase the annual cost of machine A has a rental charge then, financial manager has to make sure that the rental payments are worth $28,370, the total PV(costs) of machine A.– select the asset with the lowest fair rental charge,

that is, the lowest equivalent annual cost.

Equivalent Annual Cost and Inflation

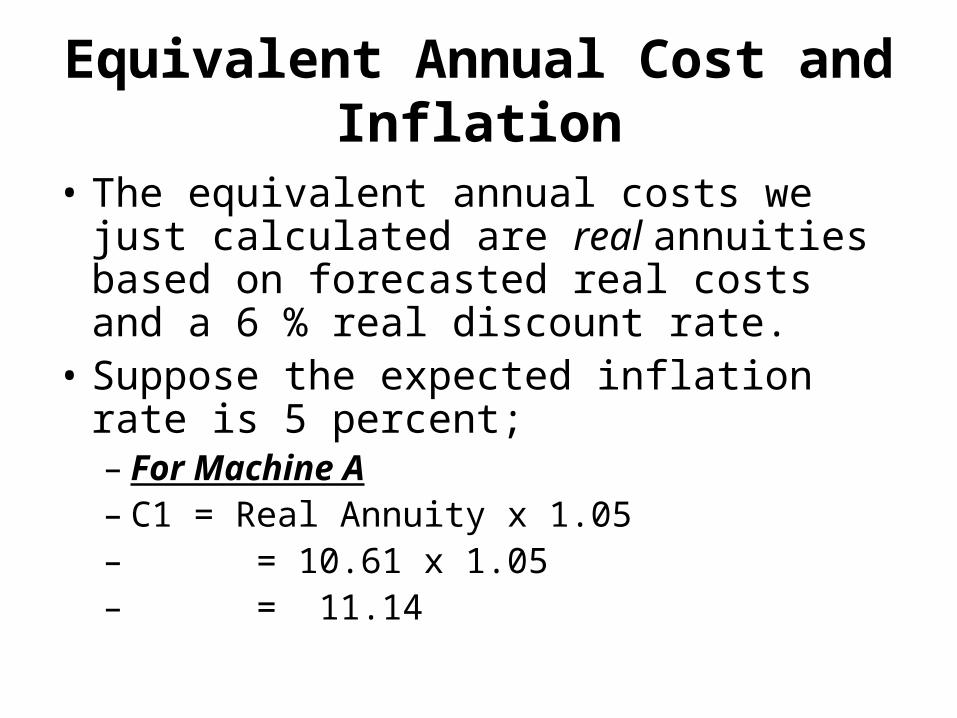

• The equivalent annual costs we just calculated are real annuities based on forecasted real costs and a 6 % real discount rate.

• Suppose the expected inflation rate is 5 percent; – For Machine A– C1 = Real Annuity x 1.05– = 10.61 x 1.05– = 11.14

Continue

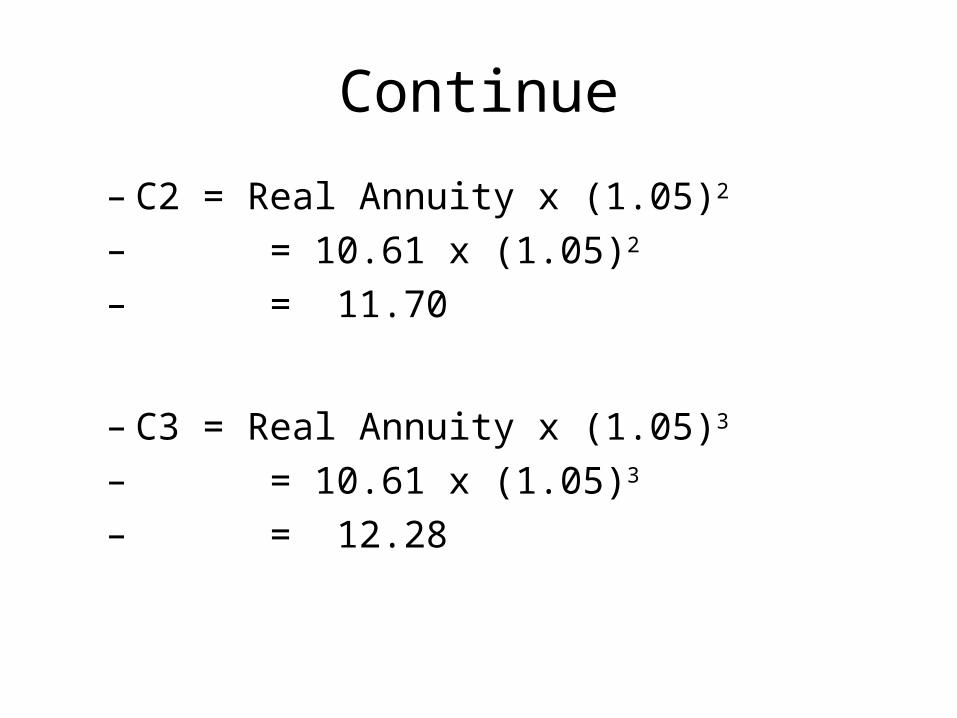

– C2 = Real Annuity x (1.05)2

– = 10.61 x (1.05)2

– = 11.70

– C3 = Real Annuity x (1.05)3

– = 10.61 x (1.05)3

– = 12.28

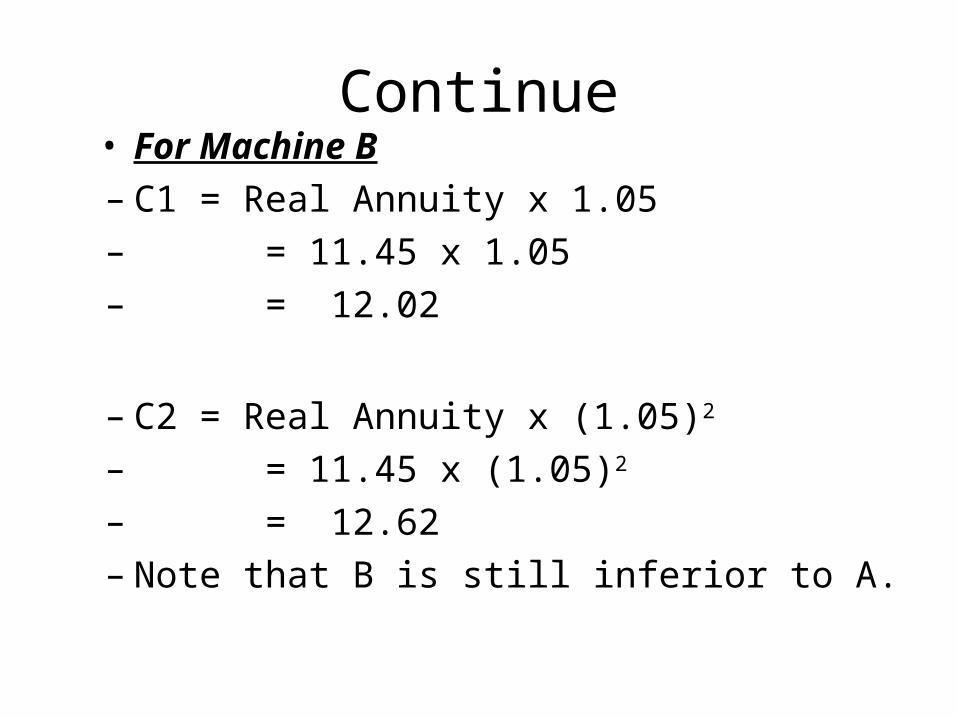

Continue• For Machine B– C1 = Real Annuity x 1.05– = 11.45 x 1.05– = 12.02

– C2 = Real Annuity x (1.05)2

– = 11.45 x (1.05)2

– = 12.62– Note that B is still inferior to A.

Project Interactions

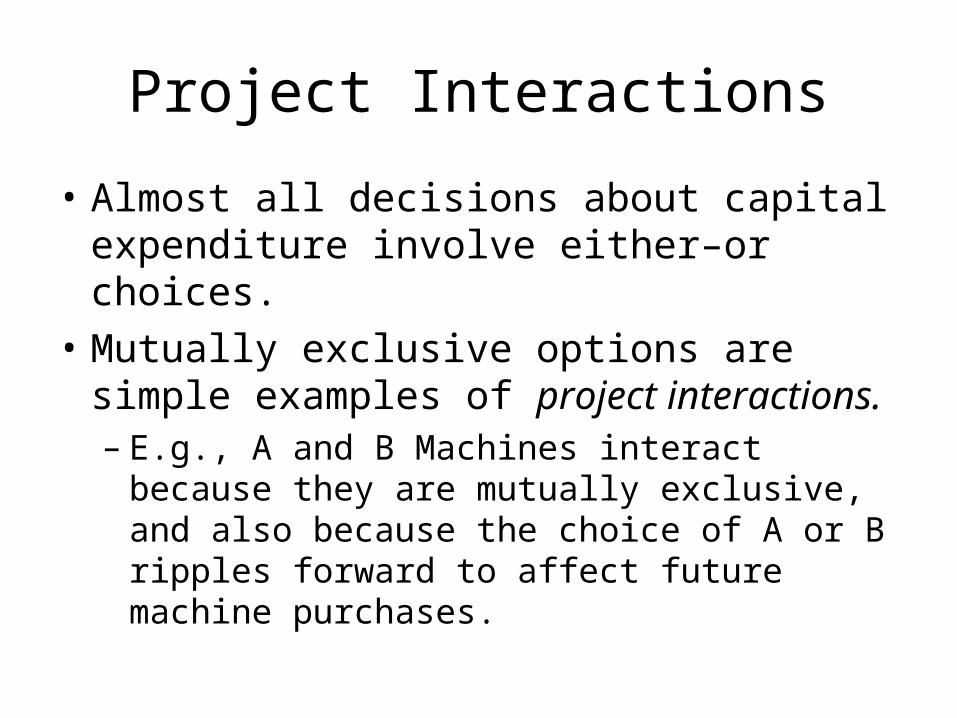

• Almost all decisions about capital expenditure involve either–or choices.

• Mutually exclusive options are simple examples of project interactions.– E.g., A and B Machines interact because they are

mutually exclusive, and also because the choice of A or B ripples forward to affect future machine purchases.

Case1: Timing

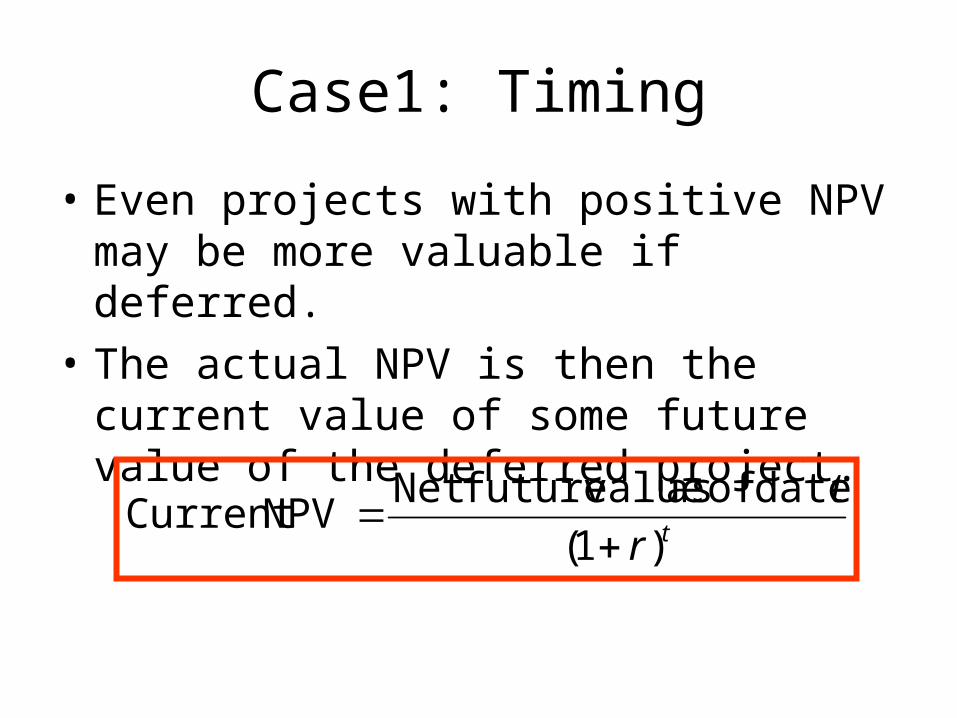

• Even projects with positive NPV may be more valuable if deferred.

• The actual NPV is then the current value of some future value of the deferred project.

tr

t

)1(

date of as valuefutureNet NPVCurrent

Continue

• The question of optimal timing of investment is not difficult under conditions of certainty.

• We first examine alternative dates (t) for making the investment and calculate its net future value as of each date.

• Let us suppose that the net present value of the harvest at different future dates is as given on the next slide.

Continue

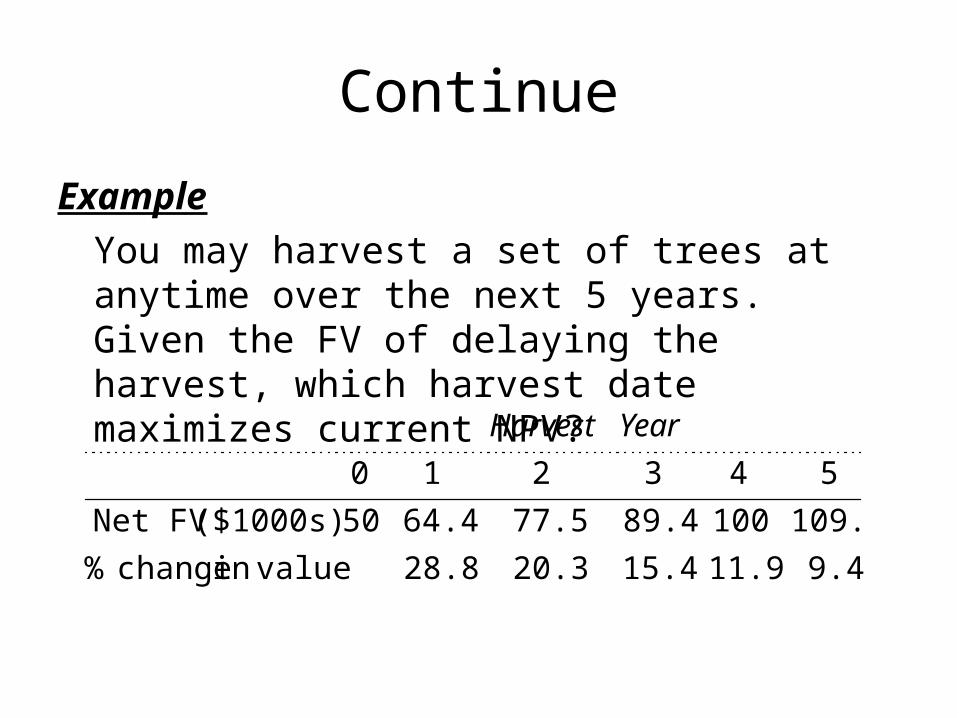

ExampleYou may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

9.411.915.420.328.8 valuein change %

109.410089.477.564.450($1000s) Net FV

543210

YearHarvest

Continue

• The longer you defer cutting the timber, the more money you will make.

• However, your concern is with the date that maximizes the net present value of your investment, that is, its contribution to the value of your firm today.

• Discount the net future value of the harvest back to the present.

Continue

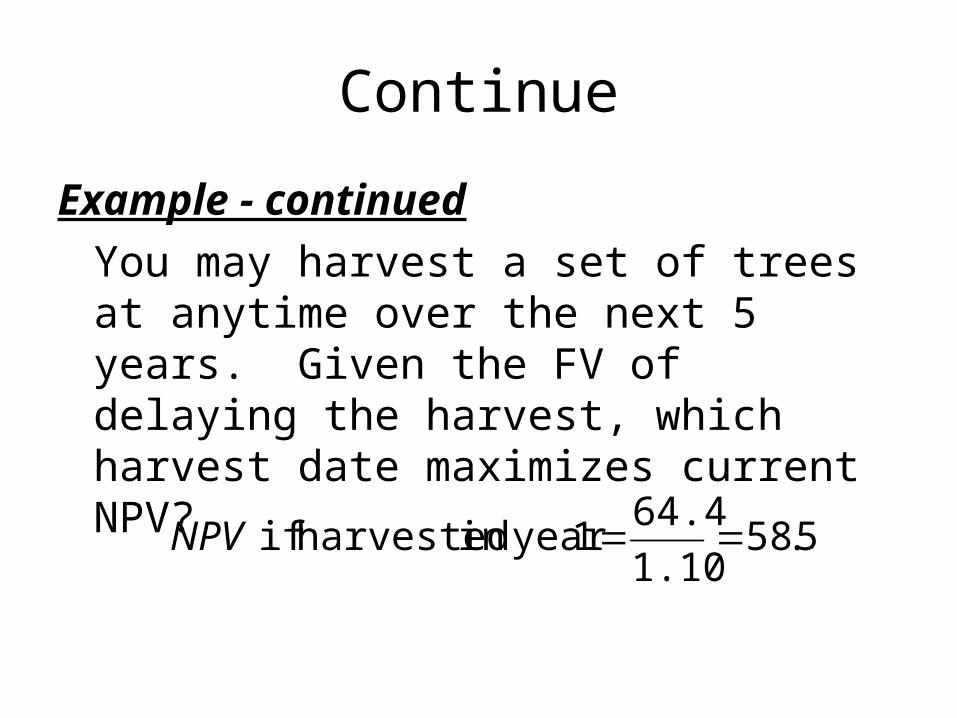

Example - continuedYou may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

5.581.10

64.41 year in harvested if NPV

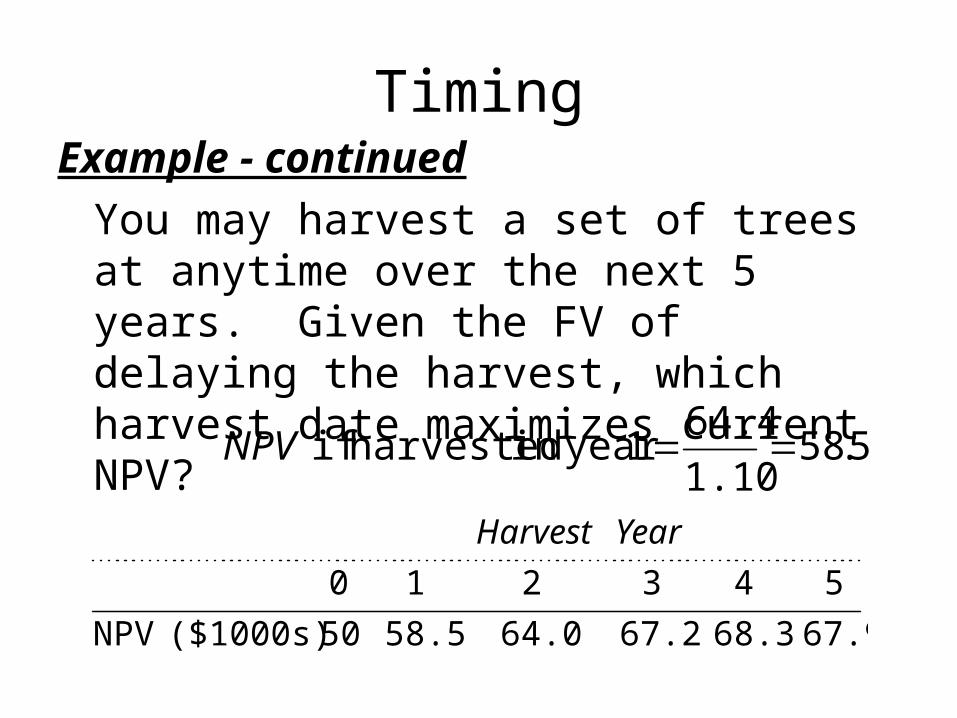

TimingExample - continued

You may harvest a set of trees at anytime over the next 5 years. Given the FV of delaying the harvest, which harvest date maximizes current NPV?

5.581.10

64.41 year in harvested if NPV

67.968.367.264.058.550($1000s) NPV

543210

YearHarvest

Continue

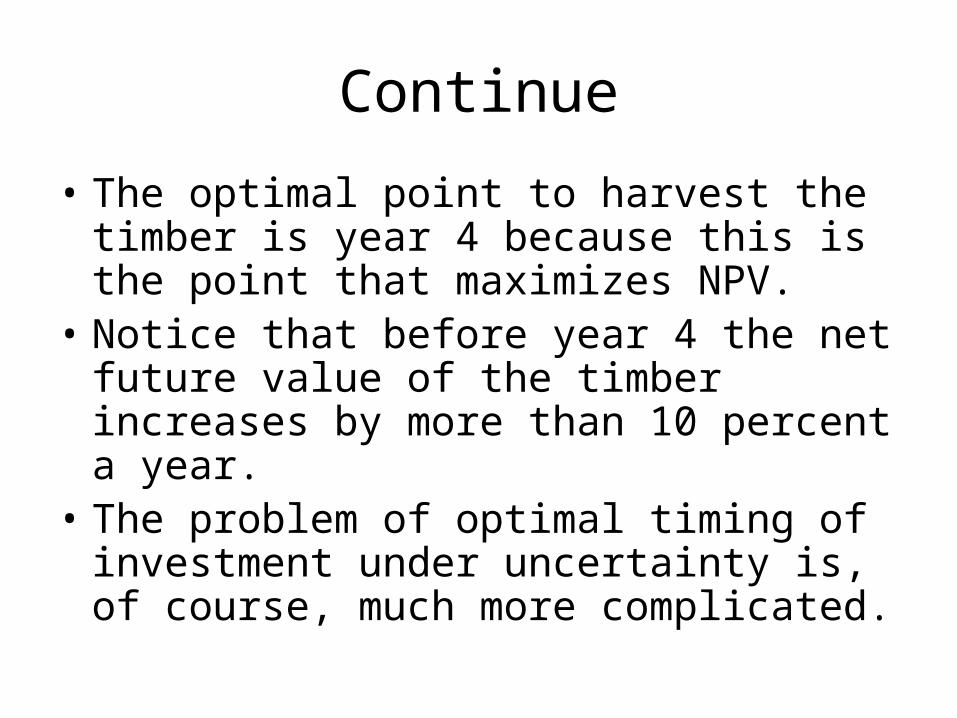

• The optimal point to harvest the timber is year 4 because this is the point that maximizes NPV.

• Notice that before year 4 the net future value of the timber increases by more than 10 percent a year.

• The problem of optimal timing of investment under uncertainty is, of course, much more complicated.

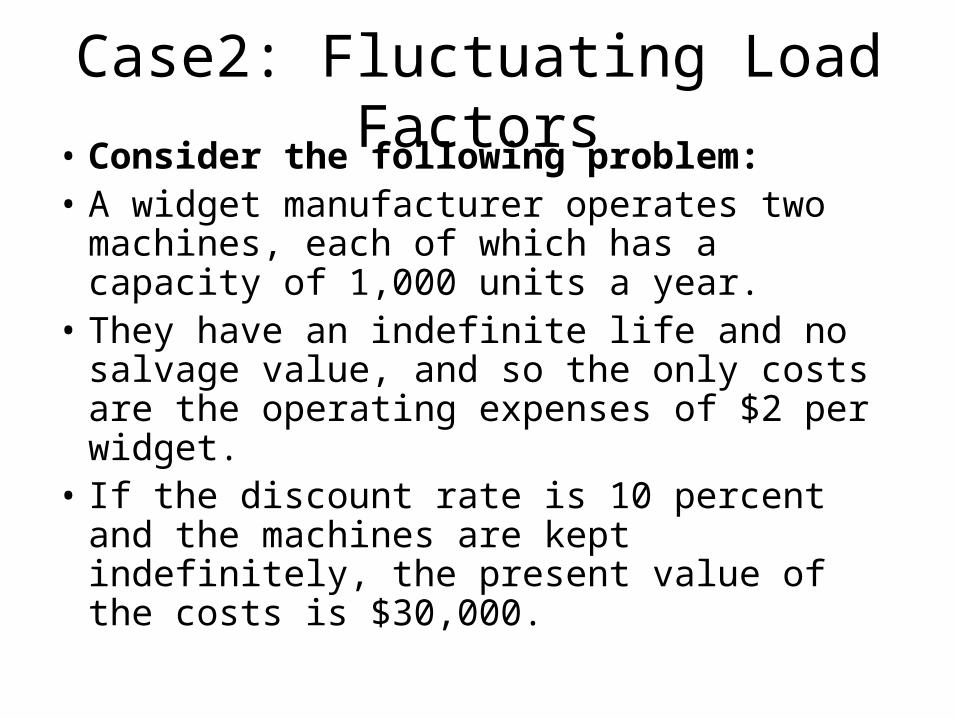

Case2: Fluctuating Load Factors• Consider the following problem: • A widget manufacturer operates two

machines, each of which has a capacity of 1,000 units a year.

• They have an indefinite life and no salvage value, and so the only costs are the operating expenses of $2 per widget.

• If the discount rate is 10 percent and the machines are kept indefinitely, the present value of the costs is $30,000.

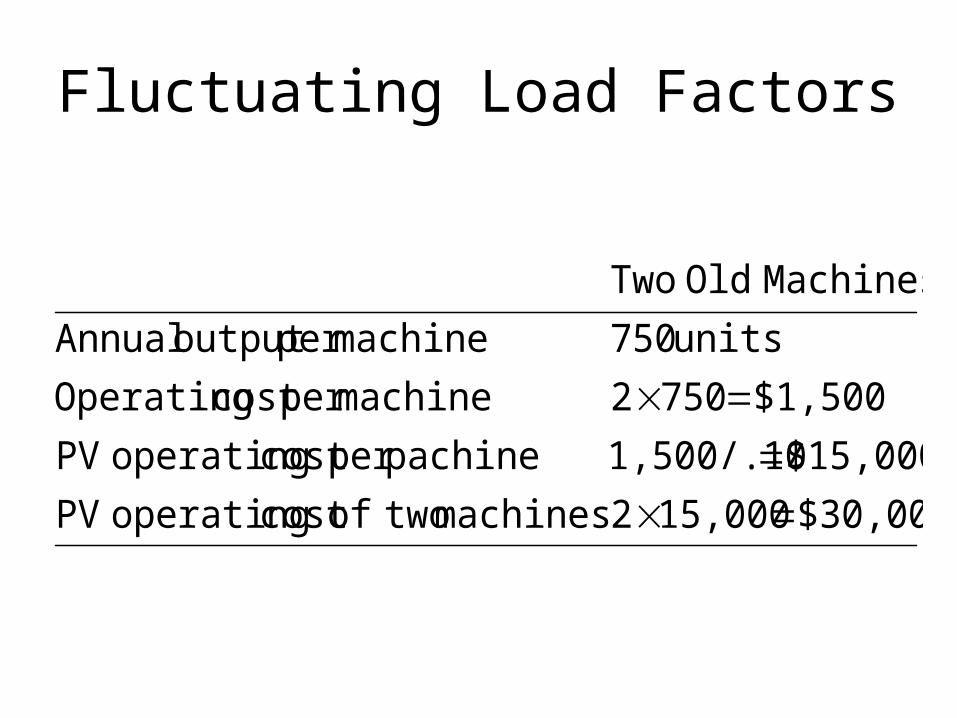

Fluctuating Load Factors

$30,00015,0002machines twoofcost operating PV

$15,0001,500/.10pachineper cost operating PV

$1,5007502machineper cost Operating

units 750machineper output Annual

MachinesOld Two

Continue

• The company is considering whether to replace these machines with newer equipment.

• The new machines have a similar capacity, and so two would still be needed to meet peak demand. Each new machine costs $6,000 and lasts indefinitely.

• Operating expenses are only $1 per unit.

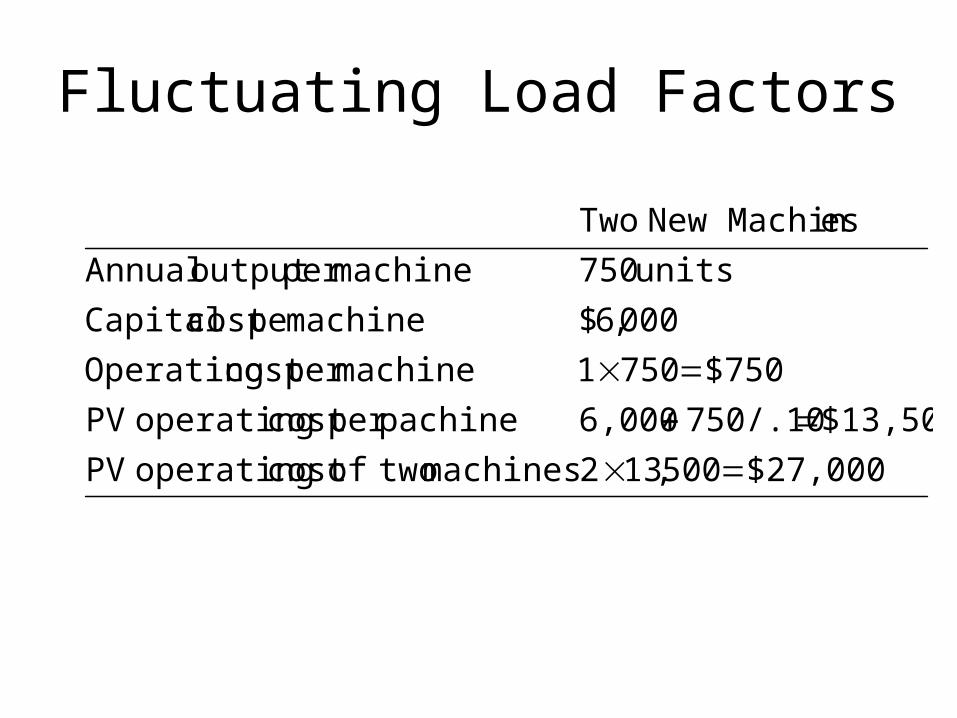

Fluctuating Load Factors

$27,000500,132machines twoofcost operating PV

$13,500750/.106,000pachineper cost operating PV

$7507501machineper cost Operating

000,6$machine pecost Capital

units 750machineper output Annual

esNew Machin Two

Continue

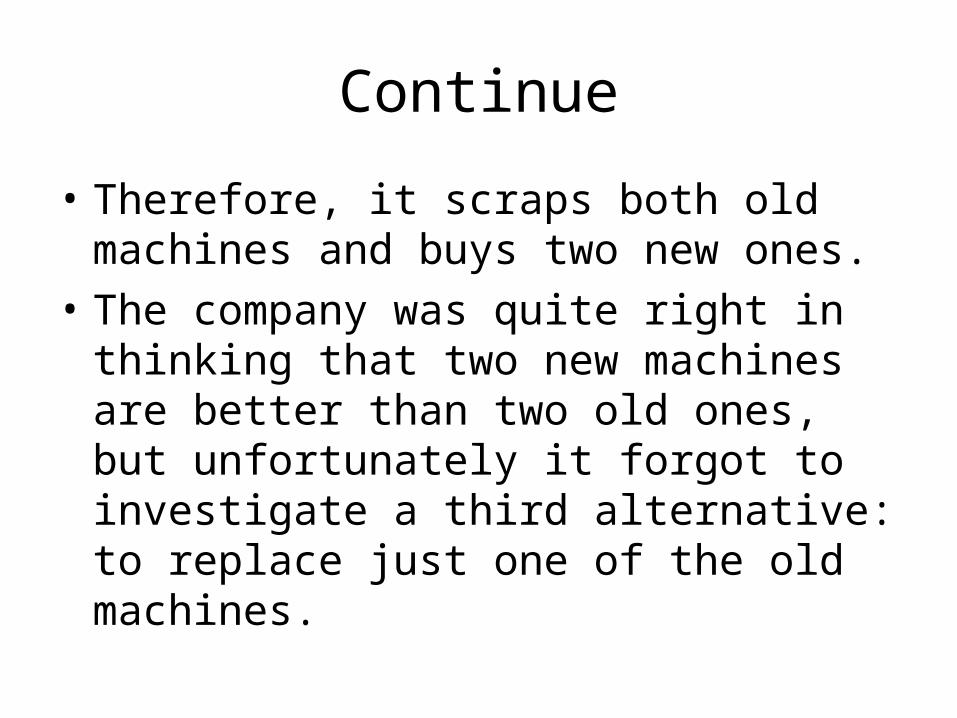

• Therefore, it scraps both old machines and buys two new ones.

• The company was quite right in thinking that two new machines are better than two old ones, but unfortunately it forgot to investigate a third alternative: to replace just one of the old machines.

Fluctuating Load Factors

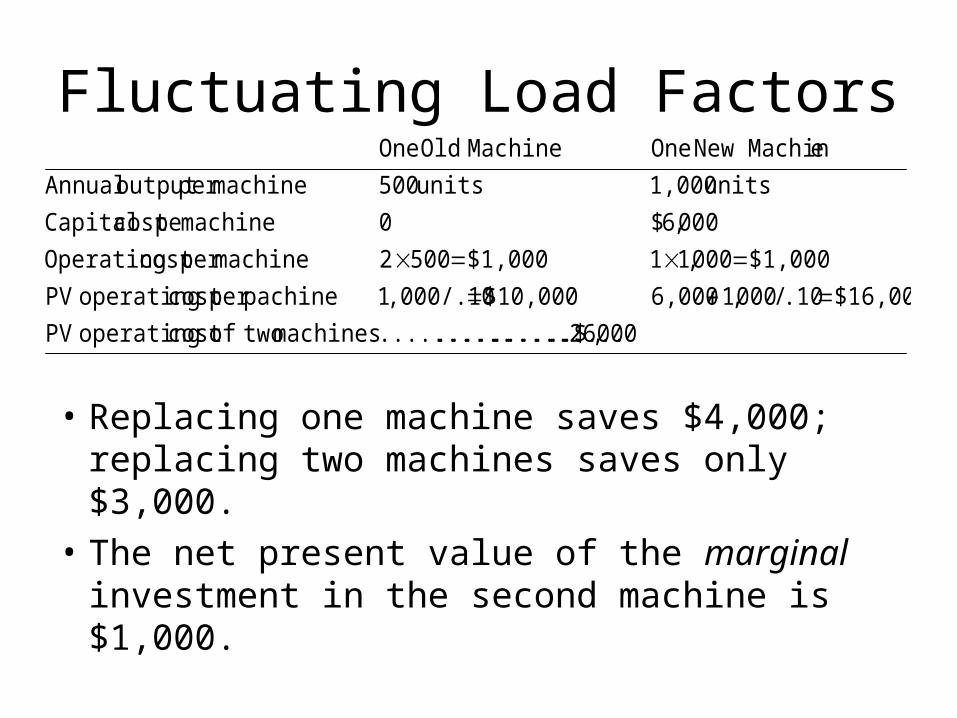

• Replacing one machine saves $4,000; replacing two machines saves only $3,000.

• The net present value of the marginal investment in the second machine is $1,000.

000,26..$..............................machines twoofcost operating PV

$16,000.10/000,16,000$10,000,000/.101pachineper cost operating PV

$1,000000,11$1,0005002machineper cost Operating

000,6$0machine pecost Capital

units 1,000units 500machineper output Annual

eNew Machin One MachineOld One

Continue• Example: United Automation is able to sell one of

its two milling machines. Both machines perform the same function but differ in age. The newer machine could be sold today for $50,000. Its operating costs are $20,000 a year, but in five years the machine will require a $20,000 overhaul. Thereafter operating costs will be $30,000 until the machine is finally sold in year 10 for $5,000. The older machine could be sold today for $25,000. If it is kept, it will need an immediate $20,000 overhaul. Thereafter operating costs will be 30,000 a year until the machine is finally sold in year 5 for $5,000.

Continue• The older machine could be sold today for

$25,000. If it is kept, it will need an immediate $20,000 overhaul. Thereafter operating costs will be $30,000 a year until the machine is finally sold in year 5 for $5,000. Both machines are fully depreciated for tax purposes. The company pays tax at 35 percent. Cash flows have been forecasted in real terms. The real cost of capital is 12 percent. Which machine should United Automation sell? Explain the assumptions underlying your answer.

Continue• Solution: In order to solve this problem, we

calculate the equivalent annual cost for each of the two alternatives. (All cash flows are in thousands.)

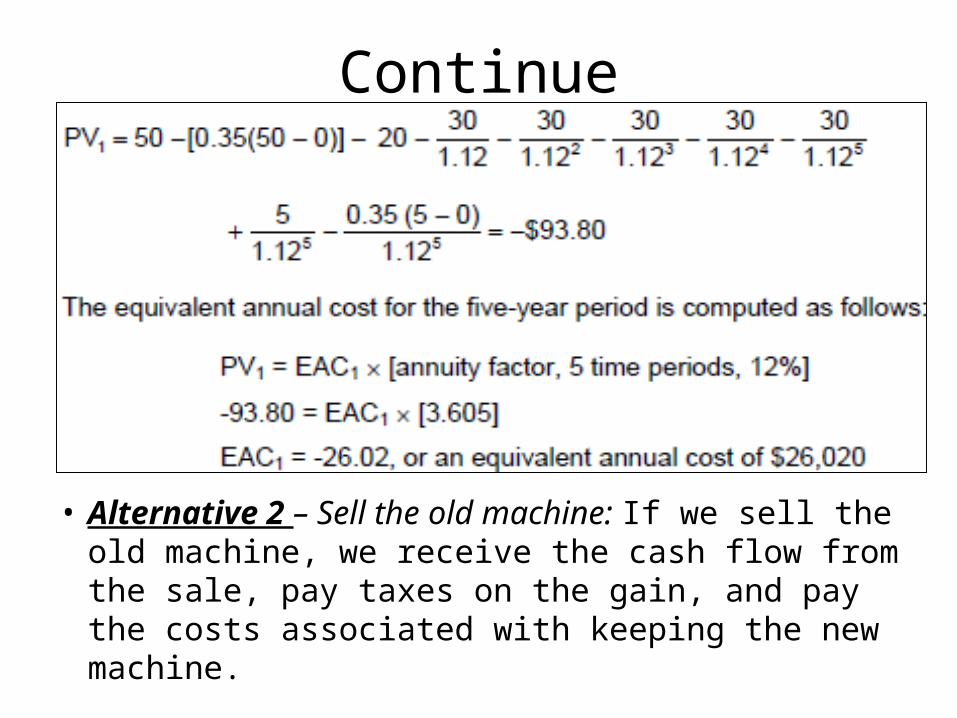

• Alternative 1 – Sell the new machine: If we sell the new machine, we receive the cash flow from the sale, pay taxes on the gain, and pay the costs associated with keeping the old machine. The present value of this alternative is:

Continue

• Alternative 2 – Sell the old machine: If we sell the old machine, we receive the cash flow from the sale, pay taxes on the gain, and pay the costs associated with keeping the new machine.

Continue

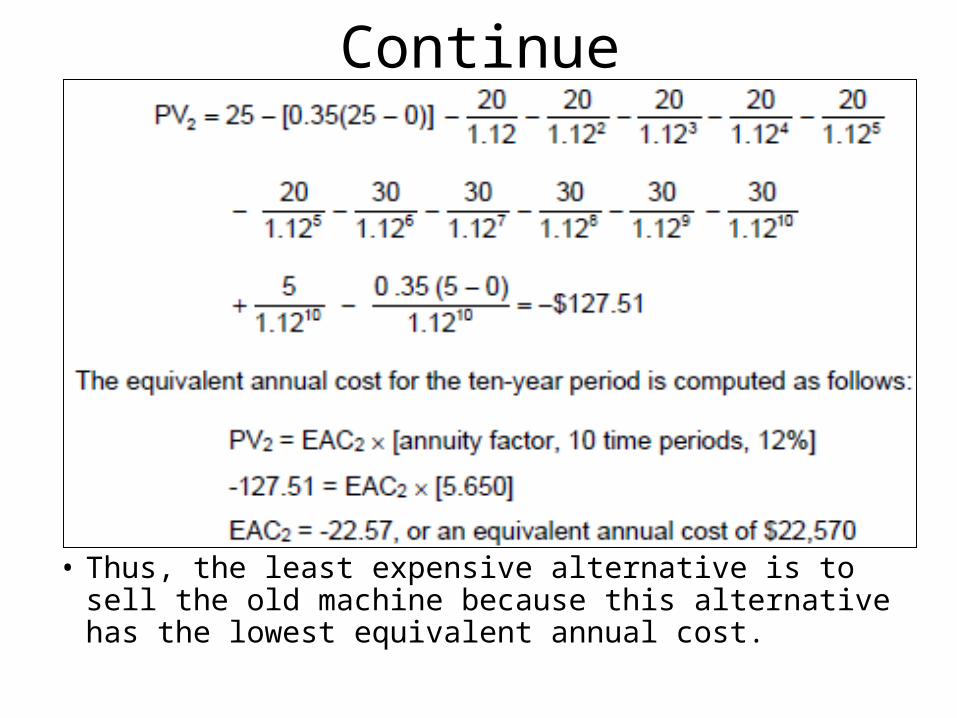

• Thus, the least expensive alternative is to sell the old machine because this alternative has the lowest equivalent annual cost.

Summary

• Project Analysis• Project Interaction– Equivalent Annual Cost– Replacement– Project Interaction– Timing– Fluctuating Load Factors