Embed Size (px)

DESCRIPTION

This report shows the region’s performance based on a variety of indicators in categories such as outreach, growth, credit types, financial structure, and profitability and risk. The data was compiled from a sample of the 47 largest Latin America and the Caribbean MFIs, which cover more than 57% of the clients in the region.

Citation preview

Microfinance Market Trends in

Latin America and the Caribbean 2005 – 2010

This report was written by Renso Martínez, MIX Operations Manager and Regional Manager for Latin

America and the Caribbean.

The contents and the opinions expressed are the author’s and do not necessarily represent the

official position of the Inter-American Development Bank, nor that of any of its members. The

reproduction of this report, partially or totally, is permitted with proper citations of its author and

its sponsors.

Microfinance Information Exchange, Inc.

Contact: Renso Martinez [email protected]

MIX Lima, Perú

Jirón León Velarde 333, Lima 14, Peru

Tel: (51) 1 471-9526 / Fax: (51) 1 471-6816

Headquarter in Washington, D.C., USA:

1901 Pennsylvania Ave., NW, Suite 307

Washington, D.C. 20006 USA

Other locations:

Rabat, Morocco ● Hyderabad, India ● Baku, Azerbaijan

Websites: www.themix.org www.mixmarket.org

Email: [email protected]

Multilateral Investment Fund

Contacts :

Sergio Navajas, Senior Specialist; [email protected]

Omar Villacorta, Consultant; [email protected]

1300 New York Avenue, N.W.

Washington, D.C. 20577

Website: www.fomin.org

Email: [email protected]

Introduction:

MIX and the Multilateral Investment Fund, a member of the Inter-American

Development Bank Group, are please to present the following report,

“Microfinance Market Tendencies for Latin America and the Caribbean 2005 –

2010.”

The objective of this report is to present an early update for the

performance of the Microfinance Institutions (MFIs) in regional, sub-regional and

certain national markets at the close of the 2010 financial year in terms of

coverage credit types, finance structure, and risk and profitability.

As with the previous edition, the report covers information from 47 MFIs

(13% of the sample is from MIX) during the period from 2005 – 2010. These

institutions represent a majority of the market in terms of portfolio and

borrowers in 11 countries, constituting a coverage of 57% of clients.

We would also like to thank the diverse sources of information and our

readers for following each of our publications.

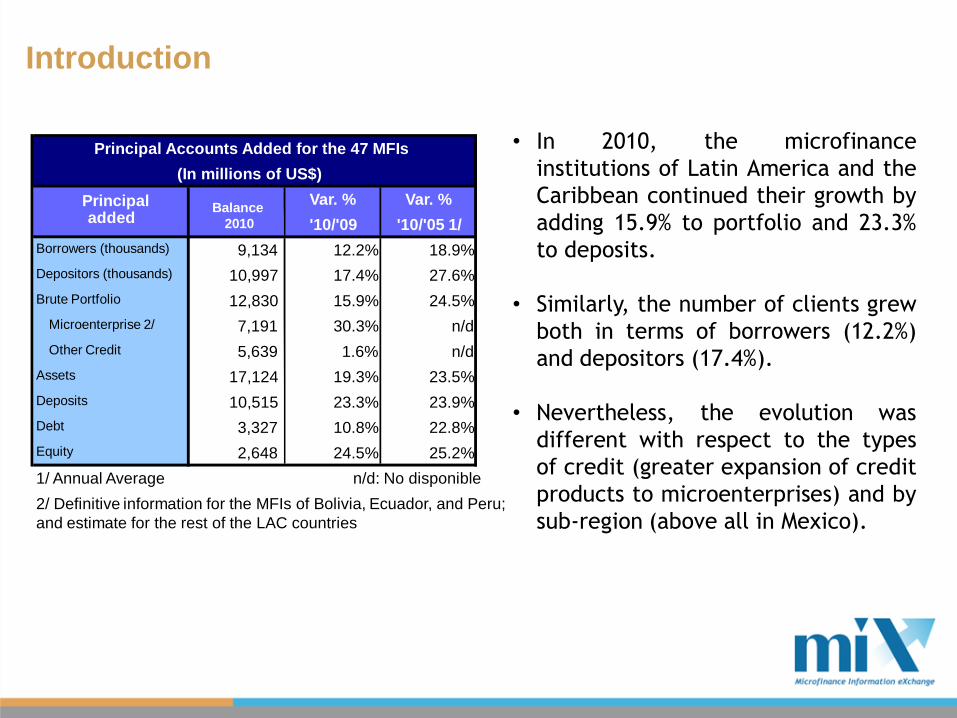

• In 2010, the microfinance

institutions of Latin America and the

Caribbean continued their growth by

adding 15.9% to portfolio and 23.3%

to deposits.

• Similarly, the number of clients grew

both in terms of borrowers (12.2%)

and depositors (17.4%).

• Nevertheless, the evolution was

different with respect to the types

of credit (greater expansion of credit

products to microenterprises) and by

sub-region (above all in Mexico).

Introduction

Principal Accounts Added for the 47 MFIs

(In millions of US$)

Var. % Var. %

'10/'09 '10/'05 1/

Borrowers (thousands) 9,134 12.2% 18.9%

Depositors (thousands) 10,997 17.4% 27.6%

Brute Portfolio 12,830 15.9% 24.5%

Microenterprise 2/ 7,191 30.3% n/d

Other Credit 5,639 1.6% n/d

Assets 17,124 19.3% 23.5%

Deposits 10,515 23.3% 23.9%

Debt 3,327 10.8% 22.8%

Equity 2,648 24.5% 25.2%

1/ Annual Average n/d: No disponible

2/ Definitive information for the MFIs of Bolivia, Ecuador, and Peru;

and estimate for the rest of the LAC countries

Principaladded

Balance

2010

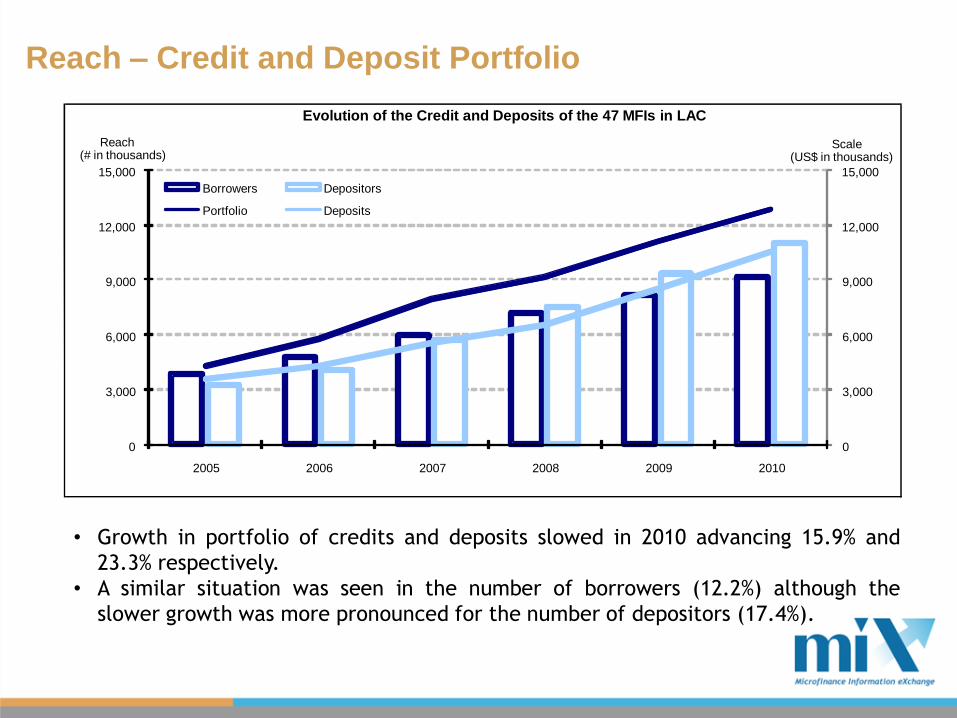

• Growth in portfolio of credits and deposits slowed in 2010 advancing 15.9% and

23.3% respectively.

• A similar situation was seen in the number of borrowers (12.2%) although the

slower growth was more pronounced for the number of depositors (17.4%).

Reach – Credit and Deposit Portfolio

Evolution of the Credit and Deposits of the 47 MFIs in LAC

0

3,000

6,000

9,000

12,000

15,000

0

3,000

6,000

9,000

12,000

15,000

2005 2006 2007 2008 2009 2010

Scale(US$ in thousands)

Reach(# in thousands)

Borrowers Depositors

Portfolio Deposits

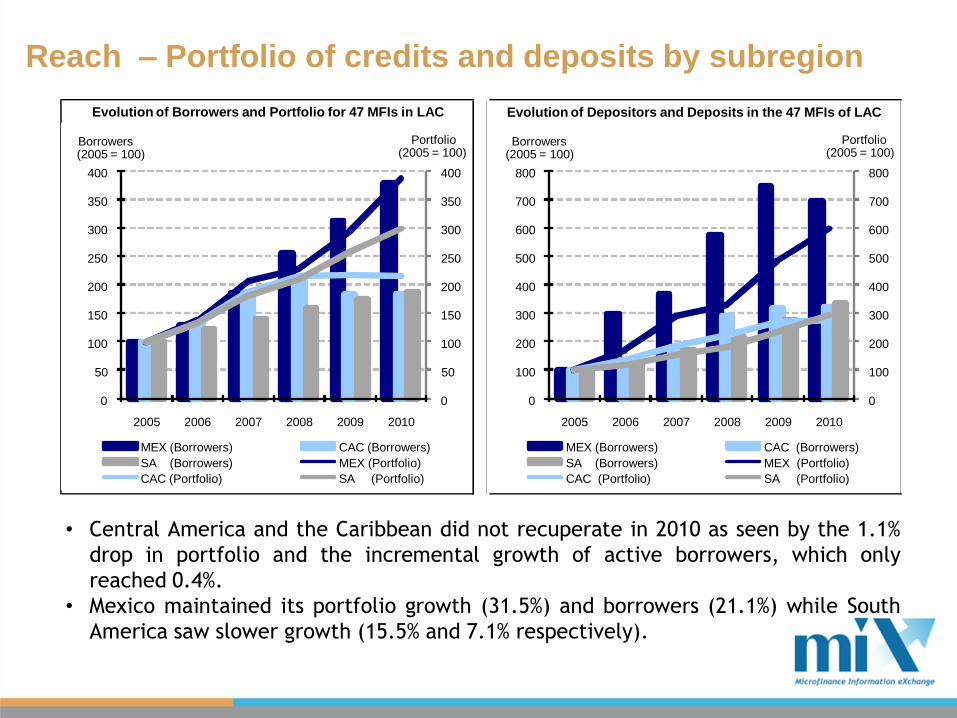

• Central America and the Caribbean did not recuperate in 2010 as seen by the 1.1%

drop in portfolio and the incremental growth of active borrowers, which only

reached 0.4%.

• Mexico maintained its portfolio growth (31.5%) and borrowers (21.1%) while South

America saw slower growth (15.5% and 7.1% respectively).

Reach – Portfolio of credits and deposits by subregion

Evolution of Borrowers and Portfolio for 47 MFIs in LAC Evolution of Depositors and Deposits in the 47 MFIs of LAC

0

50

100

150

200

250

300

350

400

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010

Portfolio(2005 = 100)

Borrowers(2005 = 100)

MEX (Borrowers) CAC (Borrowers)

SA (Borrowers) MEX (Portfolio)

CAC (Portfolio) SA (Portfolio)

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010

Portfolio(2005 = 100)

Borrowers(2005 = 100)

MEX (Borrowers) CAC (Borrowers)

SA (Borrowers) MEX (Portfolio)

CAC (Portfolio) SA (Portfolio)

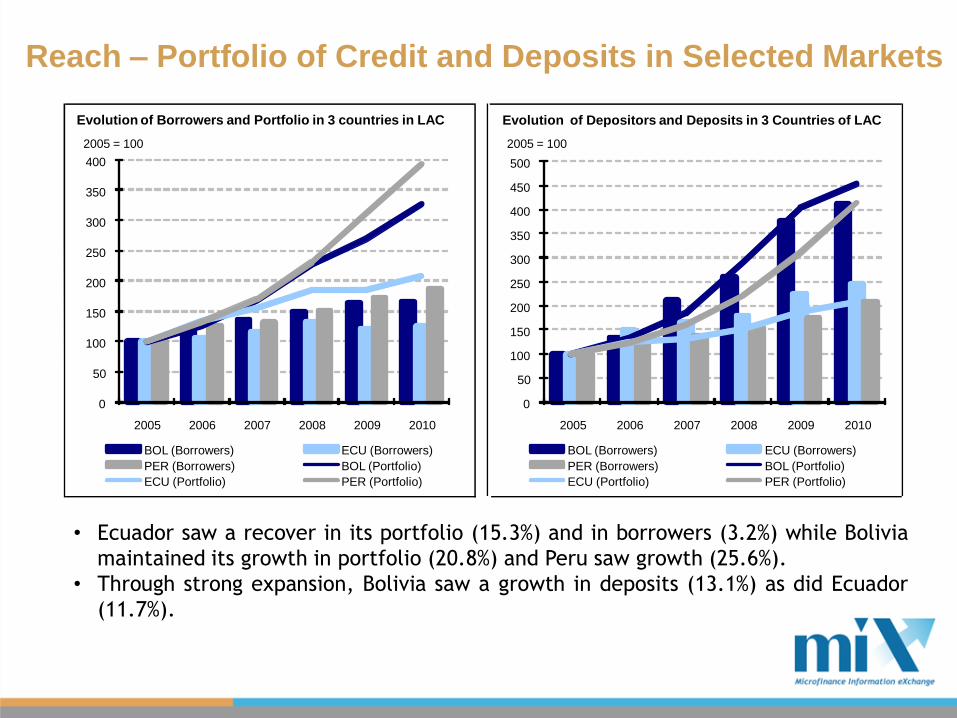

• Ecuador saw a recover in its portfolio (15.3%) and in borrowers (3.2%) while Bolivia

maintained its growth in portfolio (20.8%) and Peru saw growth (25.6%).

• Through strong expansion, Bolivia saw a growth in deposits (13.1%) as did Ecuador

(11.7%).

Reach – Portfolio of Credit and Deposits in Selected Markets

Evolution of Borrowers and Portfolio in 3 countries in LAC Evolution of Depositors and Deposits in 3 Countries of LAC

0

50

100

150

200

250

300

350

400

2005 2006 2007 2008 2009 2010

2005 = 100

BOL (Borrowers) ECU (Borrowers)

PER (Borrowers) BOL (Portfolio)

ECU (Portfolio) PER (Portfolio)

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010

2005 = 100

BOL (Borrowers) ECU (Borrowers)

PER (Borrowers) BOL (Portfolio)

ECU (Portfolio) PER (Portfolio)

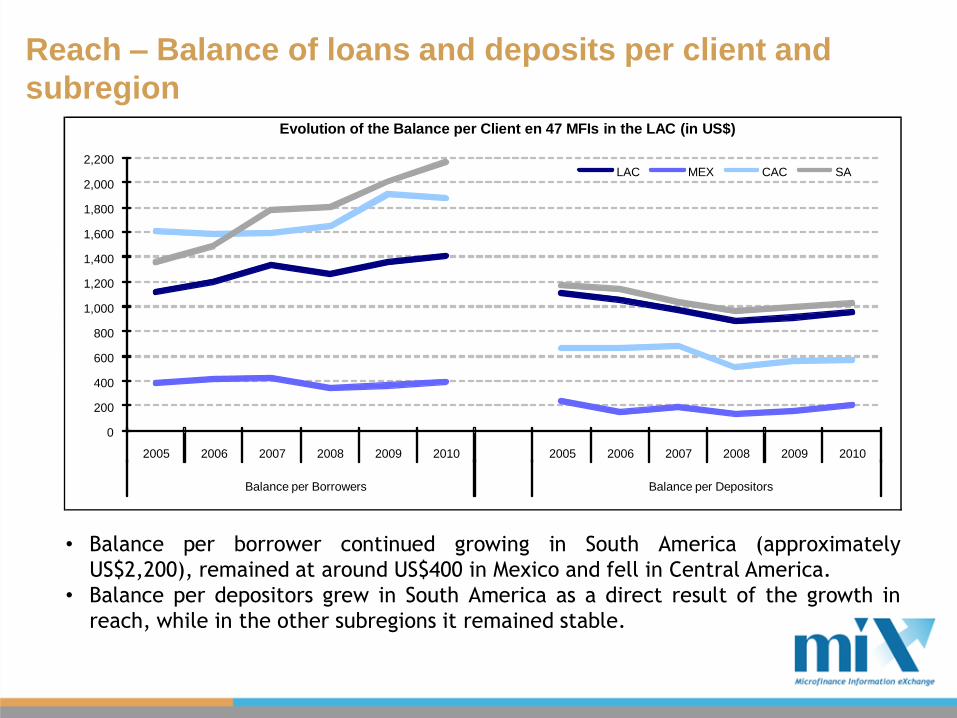

• Balance per borrower continued growing in South America (approximately

US$2,200), remained at around US$400 in Mexico and fell in Central America.

• Balance per depositors grew in South America as a direct result of the growth in

reach, while in the other subregions it remained stable.

Reach – Balance of loans and deposits per client and

subregionEvolution of the Balance per Client en 47 MFIs in the LAC (in US$)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2005 2006 2007 2008 2009 2010 2005 2006 2007 2008 2009 2010

Balance per Borrowers Balance per Depositors

LAC MEX CAC SA

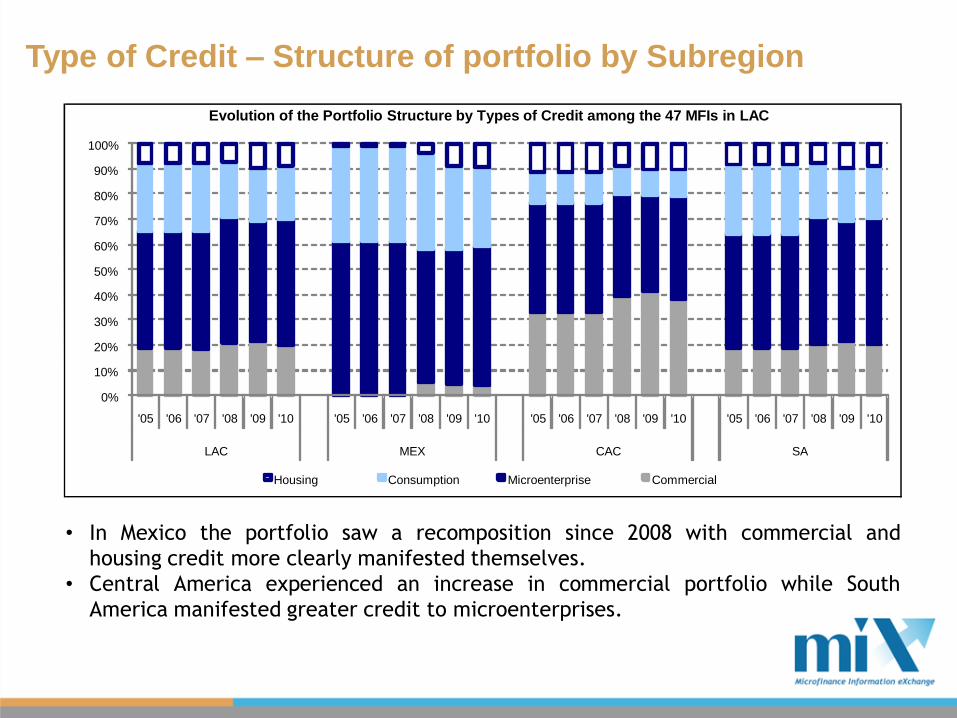

• In Mexico the portfolio saw a recomposition since 2008 with commercial and

housing credit more clearly manifested themselves.

• Central America experienced an increase in commercial portfolio while South

America manifested greater credit to microenterprises.

Type of Credit – Structure of portfolio by Subregion

Evolution of the Portfolio Structure by Types of Credit among the 47 MFIs in LAC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

LAC MEX CAC SA

Housing Consumption Microenterprise Commercial

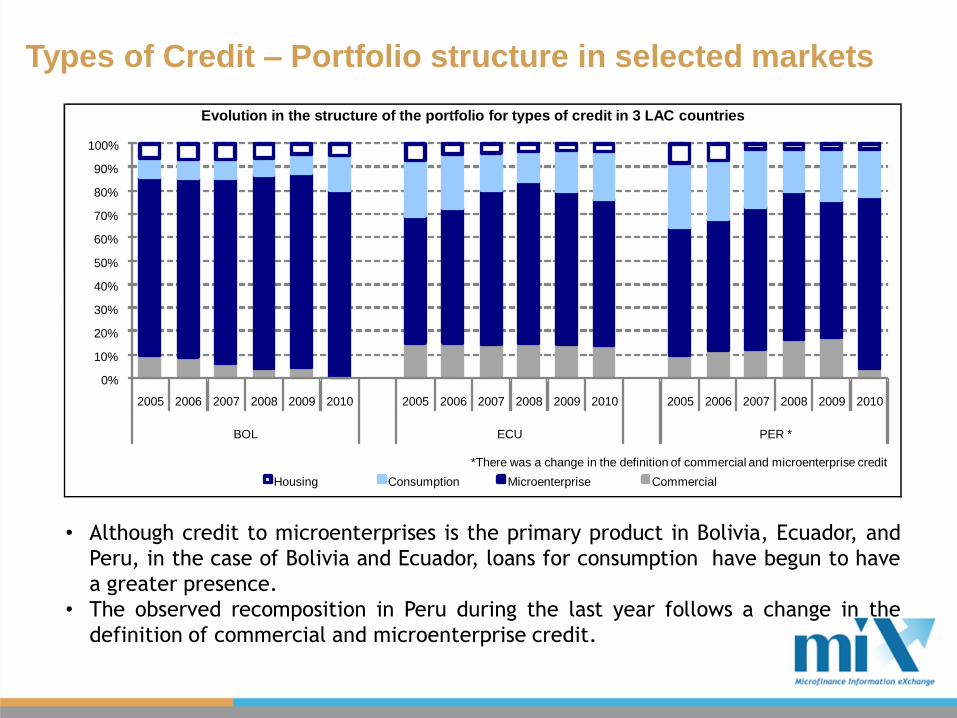

• Although credit to microenterprises is the primary product in Bolivia, Ecuador, and

Peru, in the case of Bolivia and Ecuador, loans for consumption have begun to have

a greater presence.

• The observed recomposition in Peru during the last year follows a change in the

definition of commercial and microenterprise credit.

Types of Credit – Portfolio structure in selected markets

Evolution in the structure of the portfolio for types of credit in 3 LAC countries

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2005 2006 2007 2008 2009 2010 2005 2006 2007 2008 2009 2010

BOL ECU PER *

Housing Consumption Microenterprise Commercial

*There was a change in the definition of commercial and microenterprise credit

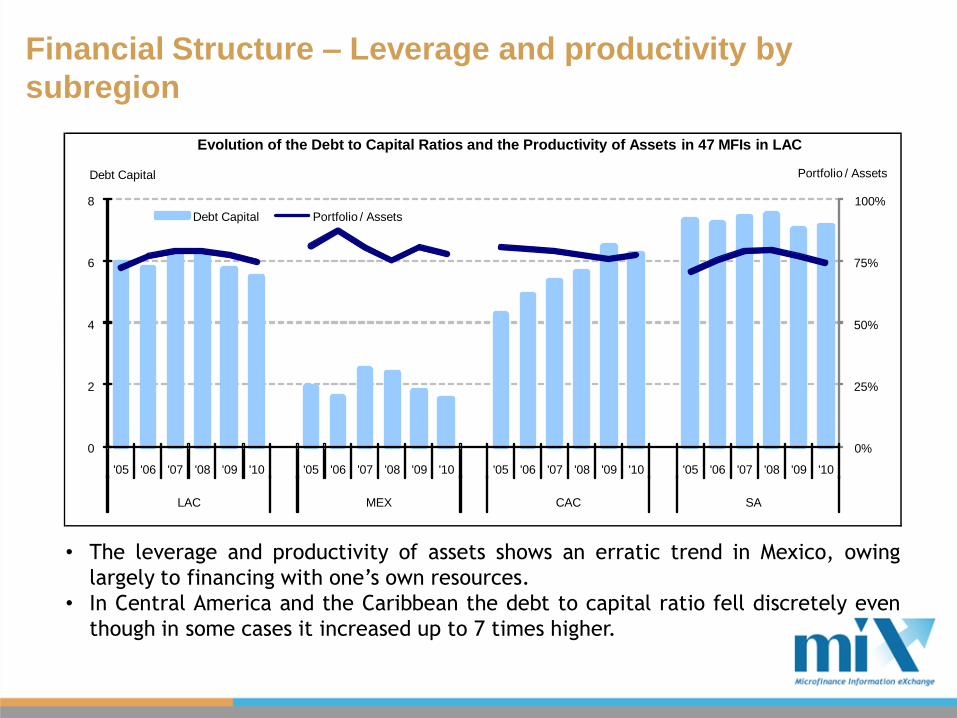

• The leverage and productivity of assets shows an erratic trend in Mexico, owing

largely to financing with one’s own resources.

• In Central America and the Caribbean the debt to capital ratio fell discretely even

though in some cases it increased up to 7 times higher.

Financial Structure – Leverage and productivity by

subregion

Evolution of the Debt to Capital Ratios and the Productivity of Assets in 47 MFIs in LAC

0%

25%

50%

75%

100%

0

2

4

6

8

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

LAC MEX CAC SA

Portfolio / AssetsDebt Capital

Debt Capital Portfolio / Assets

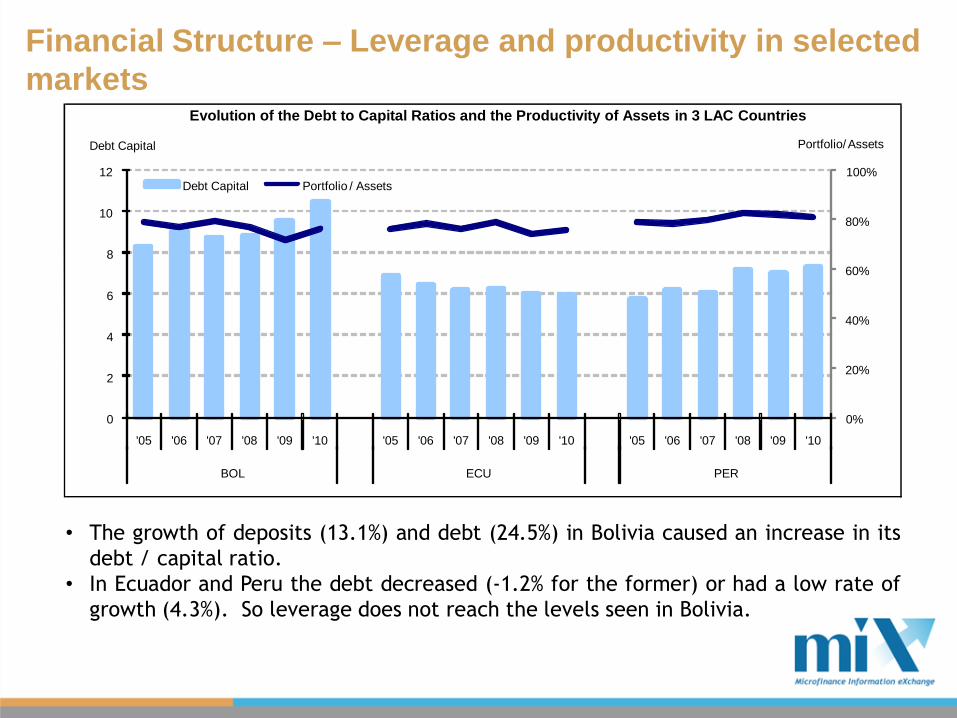

• The growth of deposits (13.1%) and debt (24.5%) in Bolivia caused an increase in its

debt / capital ratio.

• In Ecuador and Peru the debt decreased (-1.2% for the former) or had a low rate of

growth (4.3%). So leverage does not reach the levels seen in Bolivia.

Financial Structure – Leverage and productivity in selected

marketsEvolution of the Debt to Capital Ratios and the Productivity of Assets in 3 LAC Countries

0%

20%

40%

60%

80%

100%

0

2

4

6

8

10

12

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

BOL ECU PER

Portfolio/ AssetsDebt Capital

Debt Capital Portfolio / Assets

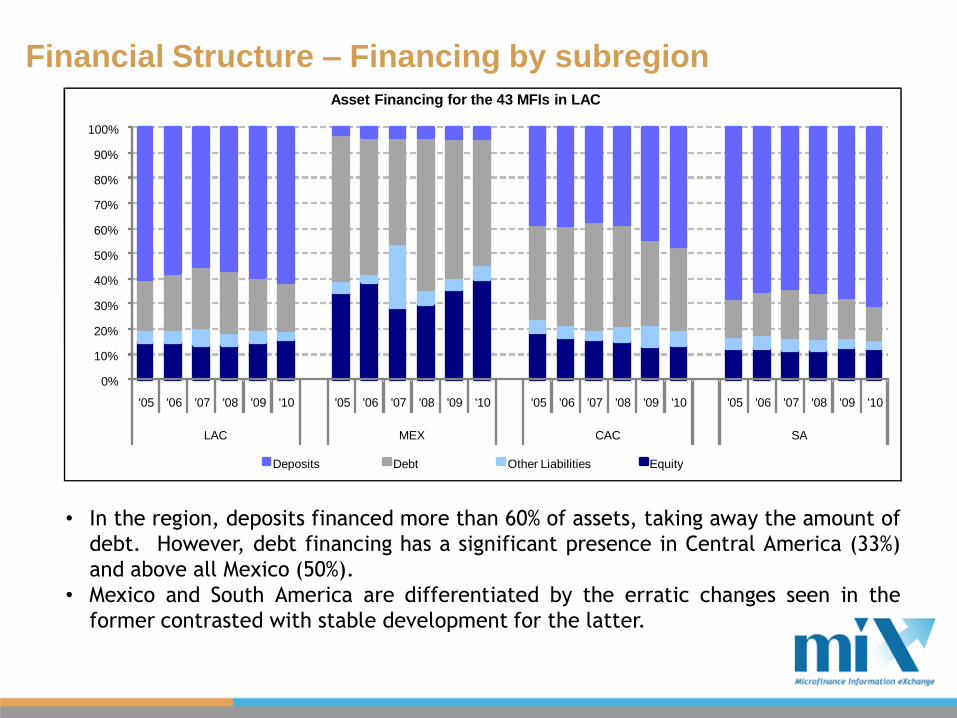

• In the region, deposits financed more than 60% of assets, taking away the amount of

debt. However, debt financing has a significant presence in Central America (33%)

and above all Mexico (50%).

• Mexico and South America are differentiated by the erratic changes seen in the

former contrasted with stable development for the latter.

Financial Structure – Financing by subregion

Asset Financing for the 43 MFIs in LAC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

LAC MEX CAC SA

Deposits Debt Other Liabilities Equity

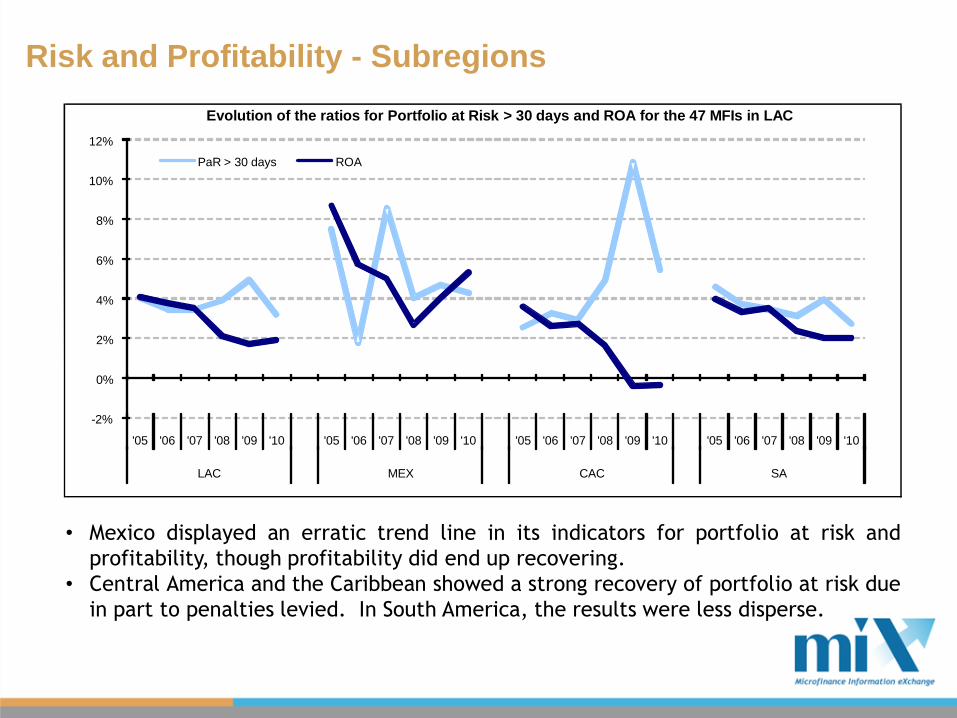

• Mexico displayed an erratic trend line in its indicators for portfolio at risk and

profitability, though profitability did end up recovering.

• Central America and the Caribbean showed a strong recovery of portfolio at risk due

in part to penalties levied. In South America, the results were less disperse.

Risk and Profitability - Subregions

Evolution of the ratios for Portfolio at Risk > 30 days and ROA for the 47 MFIs in LAC

-2%

0%

2%

4%

6%

8%

10%

12%

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

LAC MEX CAC SA

PaR > 30 days ROA

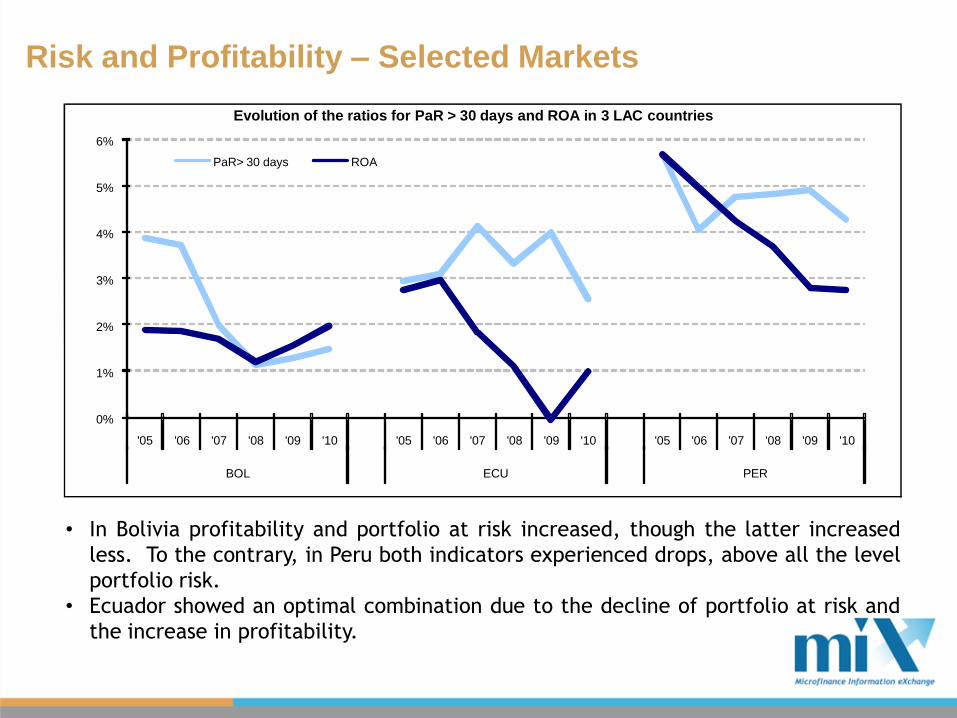

• In Bolivia profitability and portfolio at risk increased, though the latter increased

less. To the contrary, in Peru both indicators experienced drops, above all the level

portfolio risk.

• Ecuador showed an optimal combination due to the decline of portfolio at risk and

the increase in profitability.

Risk and Profitability – Selected Markets

Evolution of the ratios for PaR > 30 days and ROA in 3 LAC countries

0%

1%

2%

3%

4%

5%

6%

'05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10 '05 '06 '07 '08 '09 '10

BOL ECU PER

PaR> 30 days ROA

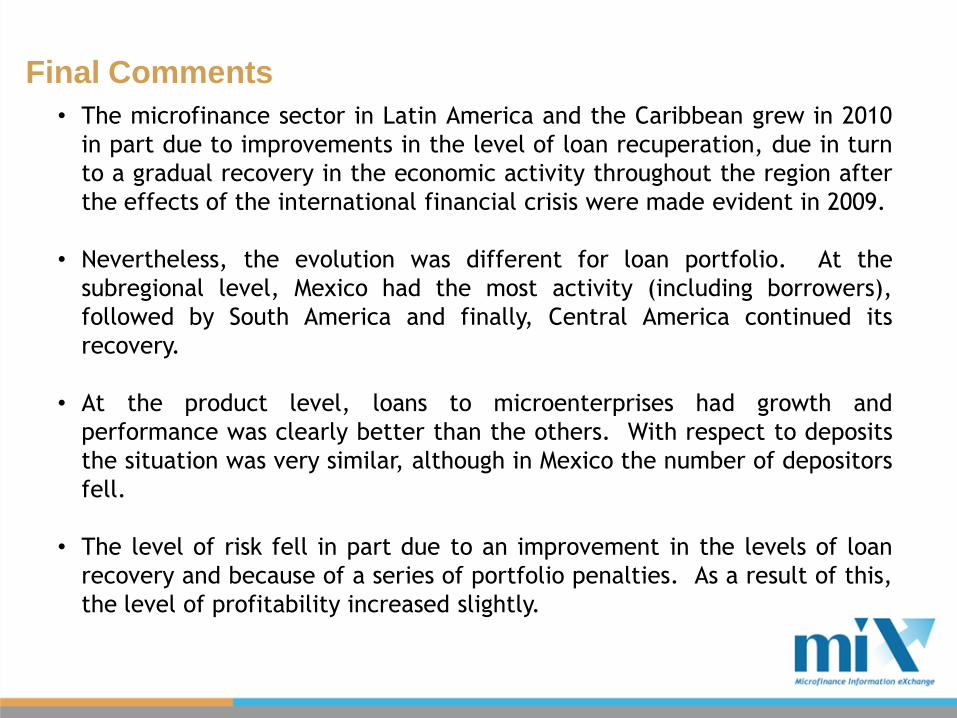

Final Comments

• The microfinance sector in Latin America and the Caribbean grew in 2010

in part due to improvements in the level of loan recuperation, due in turn

to a gradual recovery in the economic activity throughout the region after

the effects of the international financial crisis were made evident in 2009.

• Nevertheless, the evolution was different for loan portfolio. At the

subregional level, Mexico had the most activity (including borrowers),

followed by South America and finally, Central America continued its

recovery.

• At the product level, loans to microenterprises had growth and

performance was clearly better than the others. With respect to deposits

the situation was very similar, although in Mexico the number of depositors

fell.

• The level of risk fell in part due to an improvement in the levels of loan

recovery and because of a series of portfolio penalties. As a result of this,

the level of profitability increased slightly.

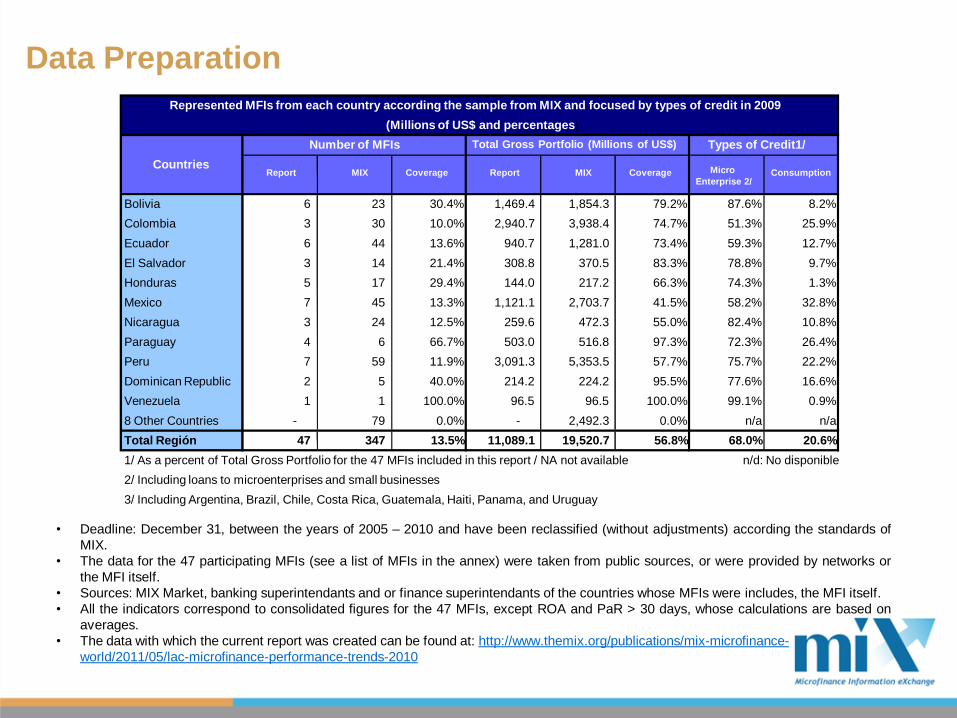

Data Preparation

• Deadline: December 31, between the years of 2005 – 2010 and have been reclassified (without adjustments) according the standards of

MIX.

• The data for the 47 participating MFIs (see a list of MFIs in the annex) were taken from public sources, or were provided by networks or

the MFI itself.

• Sources: MIX Market, banking superintendants and or finance superintendants of the countries whose MFIs were includes, the MFI itself.

• All the indicators correspond to consolidated figures for the 47 MFIs, except ROA and PaR > 30 days, whose calculations are based on

averages.

• The data with which the current report was created can be found at: http://www.themix.org/publications/mix-microfinance-

world/2011/05/lac-microfinance-performance-trends-2010

Represented MFIs from each country according the sample from MIX and focused by types of credit in 2009

(Millions of US$ and percentages)

Number of MFIs Total Gross Portfolio (Millions of US$) Types of Credit1/

Report MIX Coverage Report MIX Coverage Micro

Enterprise 2/Consumption

Bolivia 6 23 30.4% 1,469.4 1,854.3 79.2% 87.6% 8.2%

Colombia 3 30 10.0% 2,940.7 3,938.4 74.7% 51.3% 25.9%

Ecuador 6 44 13.6% 940.7 1,281.0 73.4% 59.3% 12.7%

El Salvador 3 14 21.4% 308.8 370.5 83.3% 78.8% 9.7%

Honduras 5 17 29.4% 144.0 217.2 66.3% 74.3% 1.3%

Mexico 7 45 13.3% 1,121.1 2,703.7 41.5% 58.2% 32.8%

Nicaragua 3 24 12.5% 259.6 472.3 55.0% 82.4% 10.8%

Paraguay 4 6 66.7% 503.0 516.8 97.3% 72.3% 26.4%

Peru 7 59 11.9% 3,091.3 5,353.5 57.7% 75.7% 22.2%

Dominican Republic 2 5 40.0% 214.2 224.2 95.5% 77.6% 16.6%

Venezuela 1 1 100.0% 96.5 96.5 100.0% 99.1% 0.9%

8 Other Countries - 79 0.0% - 2,492.3 0.0% n/a n/a

Total Región 47 347 13.5% 11,089.1 19,520.7 56.8% 68.0% 20.6%

1/ As a percent of Total Gross Portfolio for the 47 MFIs included in this report / NA not available n/d: No disponible

2/ Including loans to microenterprises and small businesses

3/ Including Argentina, Brazil, Chile, Costa Rica, Guatemala, Haiti, Panama, and Uruguay

Countries

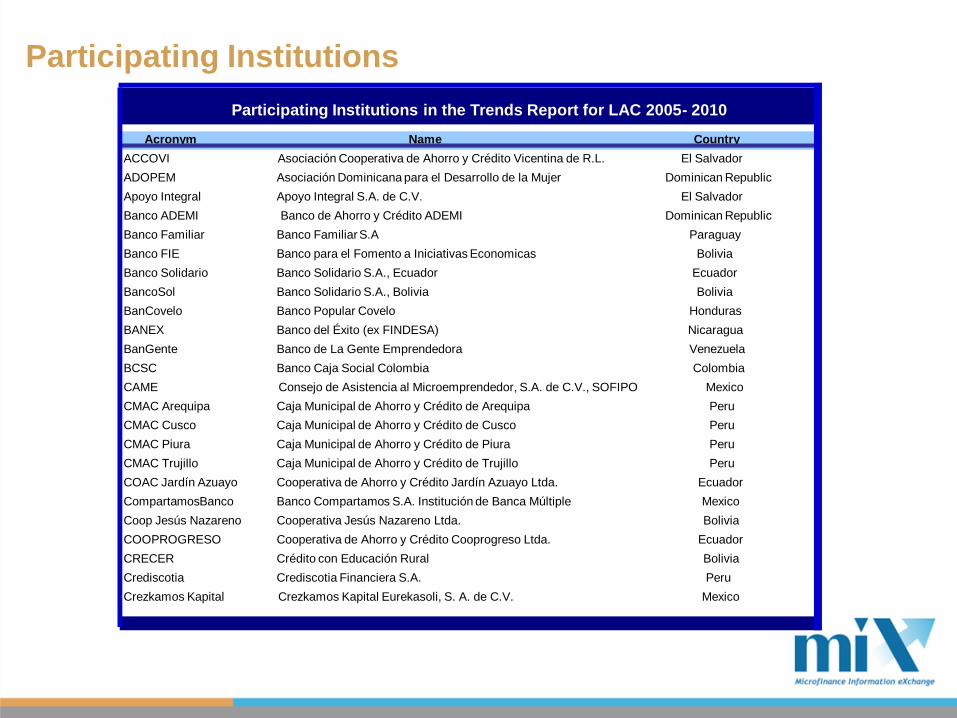

Participating Institutions

Participating Institutions in the Trends Report for LAC 2005- 2010

Acronym Name Country

ACCOVI Asociación Cooperativa de Ahorro y Crédito Vicentina de R.L. El Salvador

ADOPEM Asociación Dominicana para el Desarrollo de la Mujer Dominican Republic

Apoyo Integral Apoyo Integral S.A. de C.V. El Salvador

Banco ADEMI Banco de Ahorro y Crédito ADEMI Dominican Republic

Banco Familiar Banco Familiar S.A Paraguay

Banco FIE Banco para el Fomento a Iniciativas Economicas Bolivia

Banco Solidario Banco Solidario S.A., Ecuador Ecuador

BancoSol Banco Solidario S.A., Bolivia Bolivia

BanCovelo Banco Popular Covelo Honduras

BANEX Banco del Éxito (ex FINDESA) Nicaragua

BanGente Banco de La Gente Emprendedora Venezuela

BCSC Banco Caja Social Colombia Colombia

CAME Consejo de Asistencia al Microemprendedor, S.A. de C.V., SOFIPO Mexico

CMAC Arequipa Caja Municipal de Ahorro y Crédito de Arequipa Peru

CMAC Cusco Caja Municipal de Ahorro y Crédito de Cusco Peru

CMAC Piura Caja Municipal de Ahorro y Crédito de Piura Peru

CMAC Trujillo Caja Municipal de Ahorro y Crédito de Trujillo Peru

COAC Jardín Azuayo Cooperativa de Ahorro y Crédito Jardín Azuayo Ltda. Ecuador

CompartamosBanco Banco Compartamos S.A. Institución de Banca Múltiple Mexico

Coop Jesús Nazareno Cooperativa Jesús Nazareno Ltda. Bolivia

COOPROGRESO Cooperativa de Ahorro y Crédito Cooprogreso Ltda. Ecuador

CRECER Crédito con Educación Rural Bolivia

Crediscotia Crediscotia Financiera S.A. Peru

Crezkamos Kapital Crezkamos Kapital Eurekasoli, S. A. de C.V. Mexico

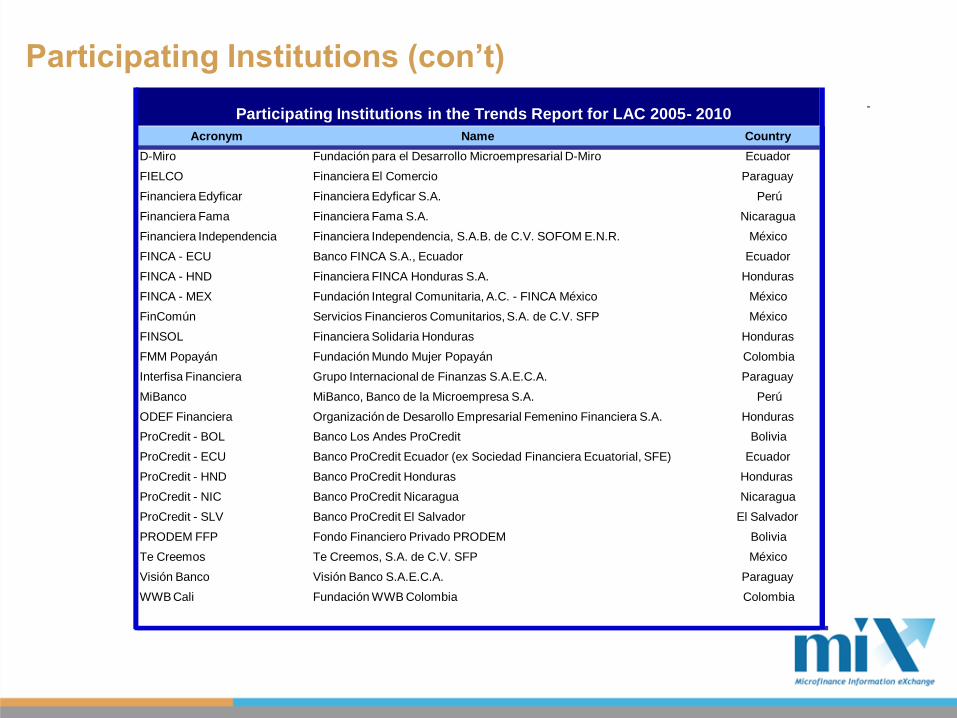

Participating Institutions (con’t)

Participating Institutions in the Trends Report for LAC 2005- 2010

Acronym Name Country

D-Miro Fundación para el Desarrollo Microempresarial D-Miro Ecuador

FIELCO Financiera El Comercio Paraguay

Financiera Edyficar Financiera Edyficar S.A. Perú

Financiera Fama Financiera Fama S.A. Nicaragua

Financiera Independencia Financiera Independencia, S.A.B. de C.V. SOFOM E.N.R. México

FINCA - ECU Banco FINCA S.A., Ecuador Ecuador

FINCA - HND Financiera FINCA Honduras S.A. Honduras

FINCA - MEX Fundación Integral Comunitaria, A.C. - FINCA México México

FinComún Servicios Financieros Comunitarios, S.A. de C.V. SFP México

FINSOL Financiera Solidaria Honduras Honduras

FMM Popayán Fundación Mundo Mujer Popayán Colombia

Interfisa Financiera Grupo Internacional de Finanzas S.A.E.C.A. Paraguay

MiBanco MiBanco, Banco de la Microempresa S.A. Perú

ODEF Financiera Organización de Desarollo Empresarial Femenino Financiera S.A. Honduras

ProCredit - BOL Banco Los Andes ProCredit Bolivia

ProCredit - ECU Banco ProCredit Ecuador (ex Sociedad Financiera Ecuatorial, SFE) Ecuador

ProCredit - HND Banco ProCredit Honduras Honduras

ProCredit - NIC Banco ProCredit Nicaragua Nicaragua

ProCredit - SLV Banco ProCredit El Salvador El Salvador

PRODEM FFP Fondo Financiero Privado PRODEM Bolivia

Te Creemos Te Creemos, S.A. de C.V. SFP México

Visión Banco Visión Banco S.A.E.C.A. Paraguay

WWB Cali Fundación WWB Colombia Colombia

About MIX

MIX is the premier source for objective, qualified and

relevant microfinance performance data and analysis.

Committed to strengthening financial inclusion and the

microfinance sector by promoting transparency, MIX

provides objective, qualified and relevant performance

information on microfinance institutions (MFIs), funders,

networks and service providers dedicated to serving the

financial sector needs for low-income clients.

MIX fulfills its mission through a variety of platforms. On

MIX Market (www.mixmarket.org), we provide instant

access to financial and social performance information

covering approximately 2,000 MFIs around the world. Our

publications, MicroBanking Bulletin and MIX Microfinance

World, feature thorough and timely analysis based on

qualified data and research.

Incorporated in 2002, MIX is a non-profit organization

headquartered in Washington, DC with regional offices in

Azerbaijan, India, Morocco, and Peru. Our efforts are

strengthened through our collaboration with the following

global partners: Bill & Melinda Gates Foundation, CGAP,

Omidyar Network, The MasterCard Foundation, IFAD,

Michael & Susan Dell Foundation, Citi Foundation, and Ford

Foundation. For more information about MIX, please visit

www.themix.org.

About MIF / IDB

Through donations, loans and capital investments,

MIF, member of the IDB group, supports innovative

private projects that expand the access to basic

services, finances, markets, skills and capabilities

for the betterment of Latin America and the

Caribbean. Founded in 1993, MIF is the largest

source of financing in Latin America and the

Caribbean, and concentrates its principal activities

in the development of small and medium

enterprises.