Embed Size (px)

DESCRIPTION

lecture 13

Citation preview

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 1/43

© 2003 The McGraw-Hill Companies, Inc. All rights

Financial Leverageand Capital Structure

Lecture 13

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 2/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.2 Key Concepts and Skills

• Understand the effect of financial leverage oncash flows and cost of equity

• Understand the impact of taxes and

bankruptcy on capital structure choice• Understand the basic components of the

bankruptcy process

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 3/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17. Chapter Outline

•!he "apital #tructure $uestion

• !he %ffect of &inancial 'everage

• "apital #tructure and the "ost of %quity "apital

• ()( *ropositions + and ++ with "orporate !axes

• ,ankruptcy "osts

• -ptimal "apital #tructure

• !he *ie gain

• -bserved "apital #tructures

• $uick 'ook at the ,ankruptcy *rocess

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 4/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17./ Capital Restructuring

•0e are going to look at how changes in capitalstructure affect the value of the firm all else equal

• "apital restructuring involves changing the amount

of leverage a firm has without changing the firms

assets• +ncrease leverage by issuing debt and repurchasing

outstanding shares

• 3ecrease leverage by issuing new shares and retiringoutstanding debt

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 5/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.4 Choosing a Capital Structure

• 0hat is the primary goal of financialmanagers5

6 (aximie stockholder wealth

• 0e want to choose the capital structure thatwill maximie stockholder wealth

• 0e can maximie stockholder wealth by

maximiing firm value or minimiing 0""

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 6/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.8 The Effect of Leverage

•9ow does leverage affect the %*# and :-% of afirm5

• 0hen we increase the amount of debt financing weincrease the fixed interest expense

• +f we have a really good year then we pay our fixedcost and we have more left over for our stockholders

• +f we have a really bad year we still have to pay ourfixed costs and we have less left over for our

stockholders• 'everage amplifies the variation in both %*# and

:-%

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 7/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.7 Example Financial Leverage! E"S and ROE

• 0e will ignore the effect of taxes at this stage• 0hat happens to %*# and :-% when we issue

debt and buy back shares of stock5

Financial Leverage Example

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 8/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

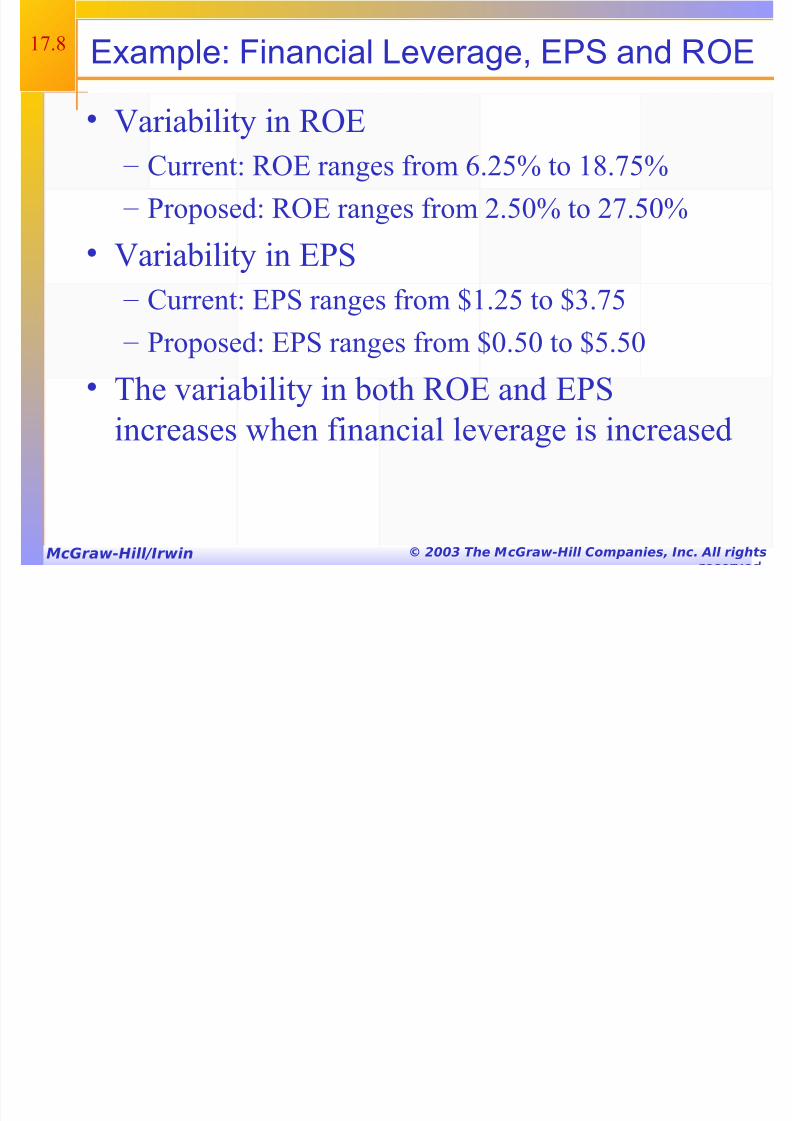

17.; Example Financial Leverage! E"S and ROE

• <ariability in :-% 6 "urrent= :-% ranges from 8.24> to 1;.74>

6 *roposed= :-% ranges from 2.4?> to 27.4?>

• <ariability in %*# 6 "urrent= %*# ranges from @1.24 to @.74

6 *roposed= %*# ranges from @?.4? to @4.4?

• !he variability in both :-% and %*#increases when financial leverage is increased

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 9/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

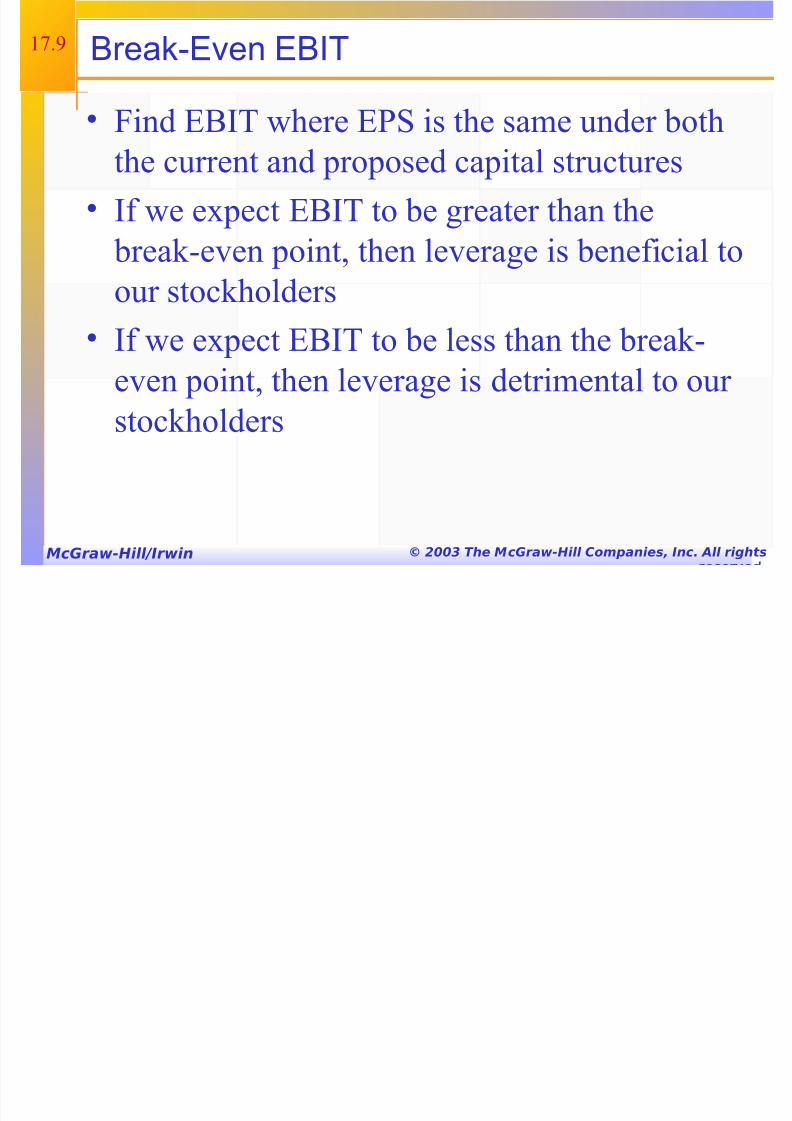

17.A #reak$Even E#%T

• &ind %,+! where %*# is the same under boththe current and proposed capital structures

• +f we expect %,+! to be greater than the

breakBeven point then leverage is beneficial toour stockholders

• +f we expect %,+! to be less than the breakB

even point then leverage is detrimental to ourstockholders

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 10/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

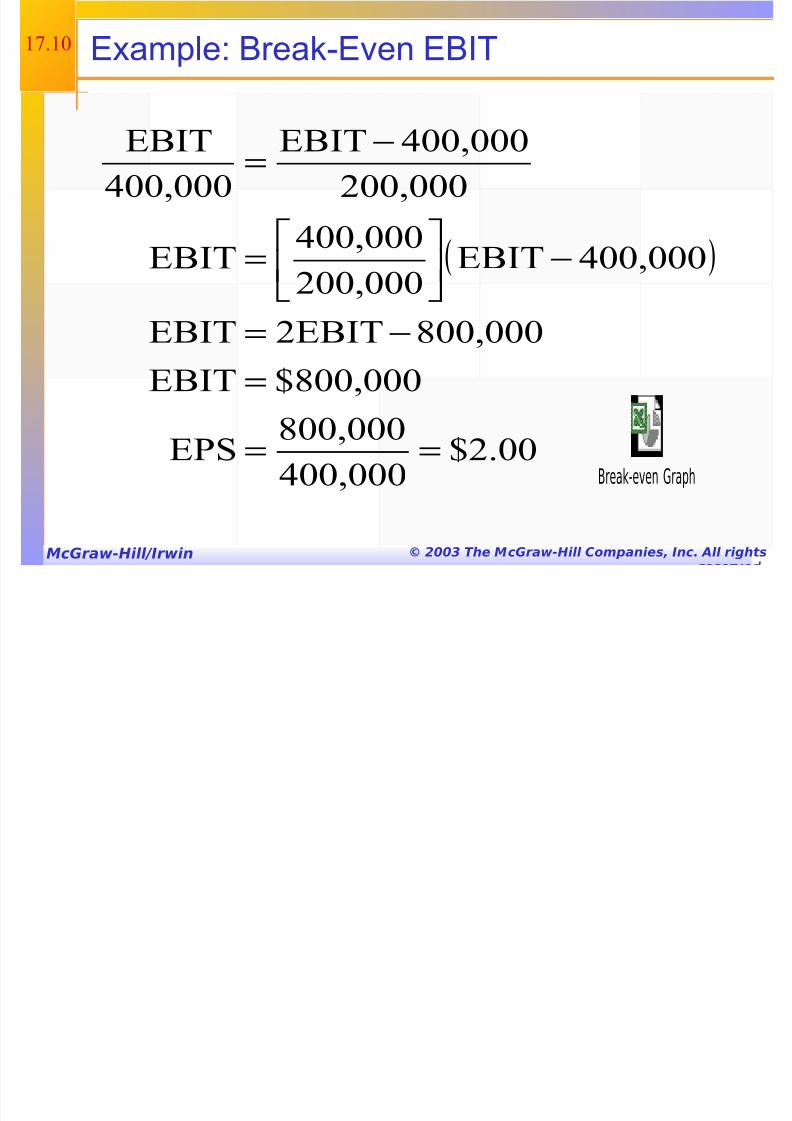

17.1? Example #reak$Even E#%T

( )

@2.??/??1???

;??1???%*#

@;??1???%,+!

;??1???2%,+!%,+!

/??1???%,+!2??1???

/??1???

%,+!

2??1???

/??1???%,+!

/??1???

%,+!

==

=

−=

−

=

−=

Break-even Graph

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 11/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

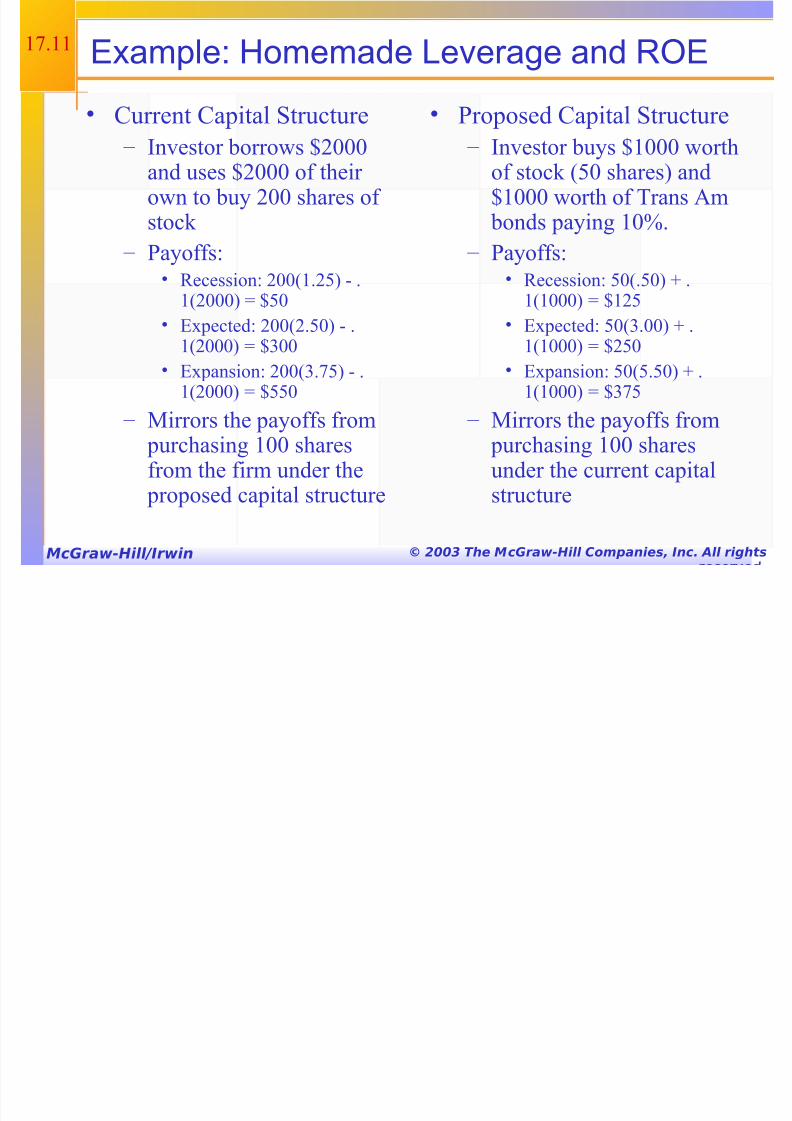

17.11 Example &omemade Leverage and ROE

• "urrent "apital #tructure

6 +nvestor borrows @2???and uses @2??? of theirown to buy 2?? shares ofstock

6 *ayoffs=• :ecession= 2??C1.24D B .

1C2???D E @4?

• %xpected= 2??C2.4?D B .1C2???D E @??

• %xpansion= 2??C.74D B .

1C2???D E @44? 6 (irrors the payoffs from

purchasing 1?? sharesfrom the firm under the

proposed capital structure

• *roposed "apital #tructure

6 +nvestor buys @1??? worthof stock C4? sharesD and@1??? worth of !rans m

bonds paying 1?>.

6 *ayoffs=• :ecession= 4?C.4?D F .

1C1???D E @124

• %xpected= 4?C.??D F .1C1???D E @24?

• %xpansion= 4?C4.4?D F .

1C1???D E @74 6 (irrors the payoffs from

purchasing 1?? sharesunder the current capitalstructure

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 12/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.12 Capital Structure Theory

• (odigliani and (iller !heory of "apital#tructure

6 *roposition + 6 firm value

6 *roposition ++ 6 0""

• !he value of the firm is determined by the cash

flows to the firm and the risk of the assets

• "hanging firm value 6 "hange the risk of the cash flows

6 "hange the cash flows

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 13/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.1 Capital Structure Theory 'nder Three Special Cases

• "ase + 6 ssumptions 6 Go corporate or personal taxes

6 Go bankruptcy costs

• "ase ++ 6 ssumptions 6 "orporate taxes but no personal taxes

6 Go bankruptcy costs

• "ase +++ 6 ssumptions

6 "orporate taxes but no personal taxes

6 ,ankruptcy costs

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 14/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.1/ Case % ( "ropositions % and %%

• *roposition + 6 !he value of the firm is G-! affected by changes

in the capital structure

6 !he cash flows of the firm do not change

therefore value doesnt change

• *roposition ++

6 !he 0"" of the firm is G-! affected by capital

structure

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 15/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

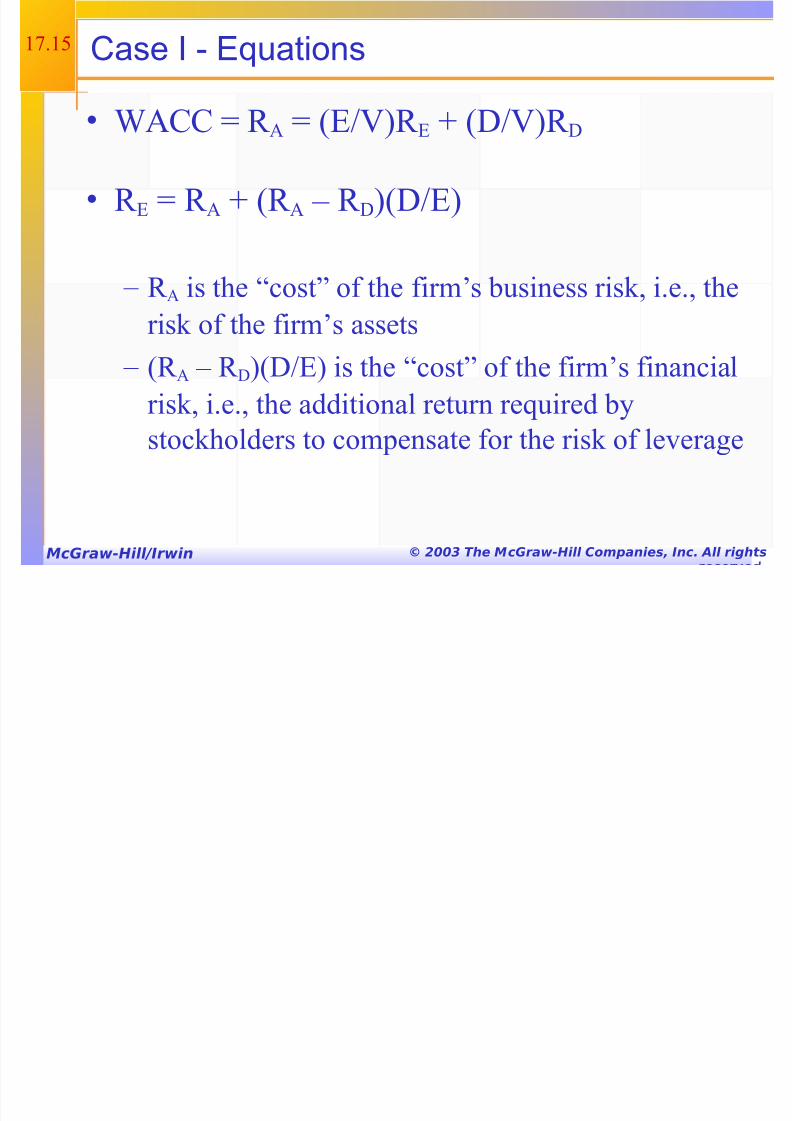

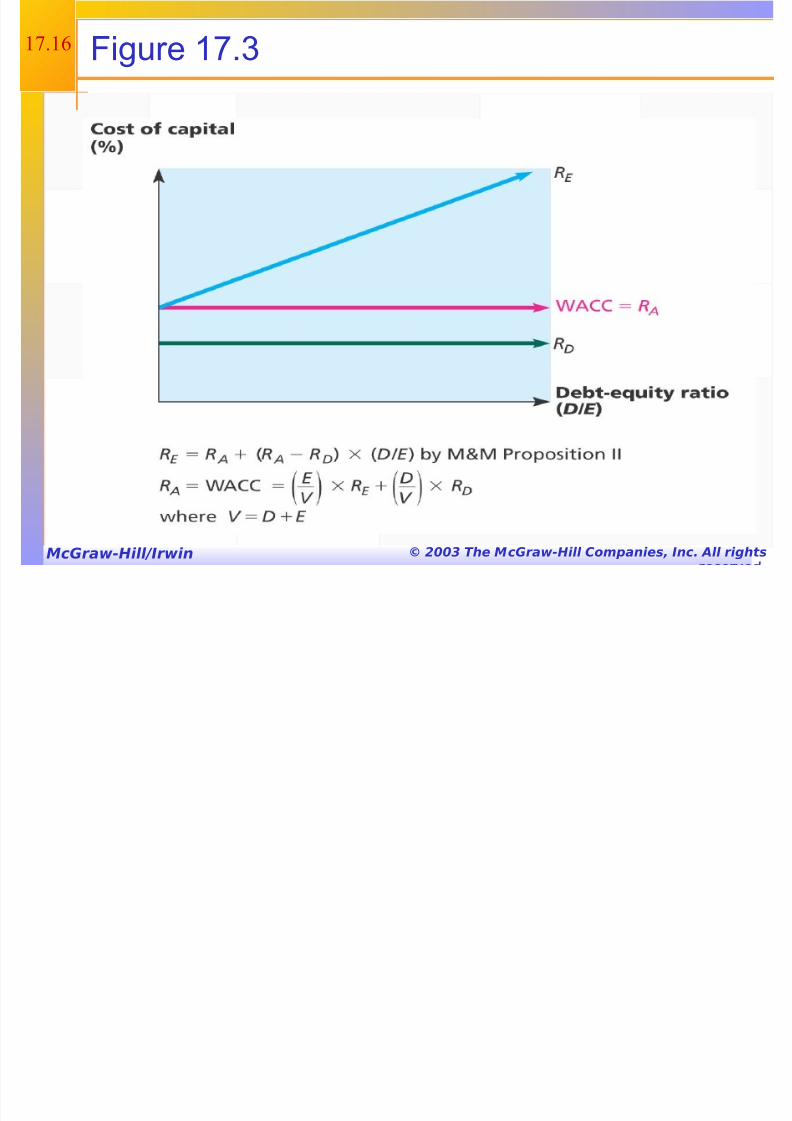

17.14 Case % $ E)uations

• 0"" E : . E C%H<D: % F C3H<D: 3

• : % E : . F C: . 6 : 3DC3H%D

6 : . is the IcostJ of the firms business risk i.e. the

risk of the firms assets

6 C: . 6 : 3DC3H%D is the IcostJ of the firms financial

risk i.e. the additional return required bystockholders to compensate for the risk of leverage

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 16/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

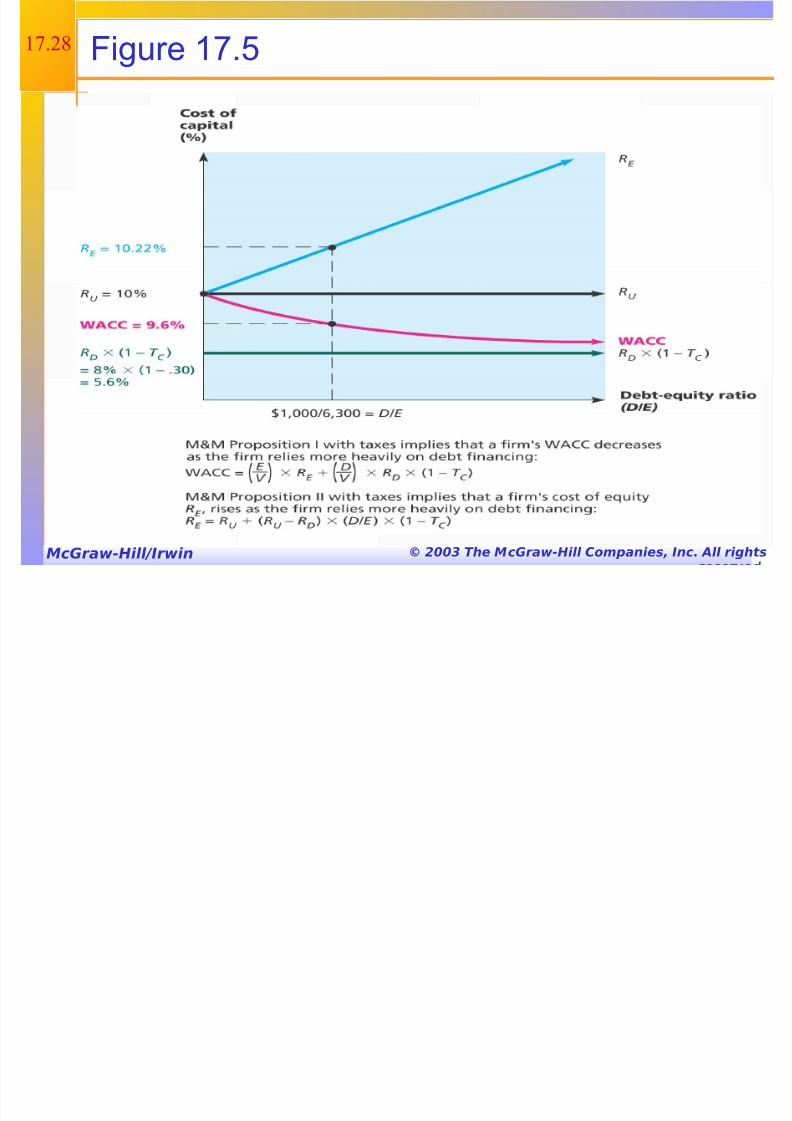

17.18 Figure *+,-

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 17/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.17 Case % $ Example

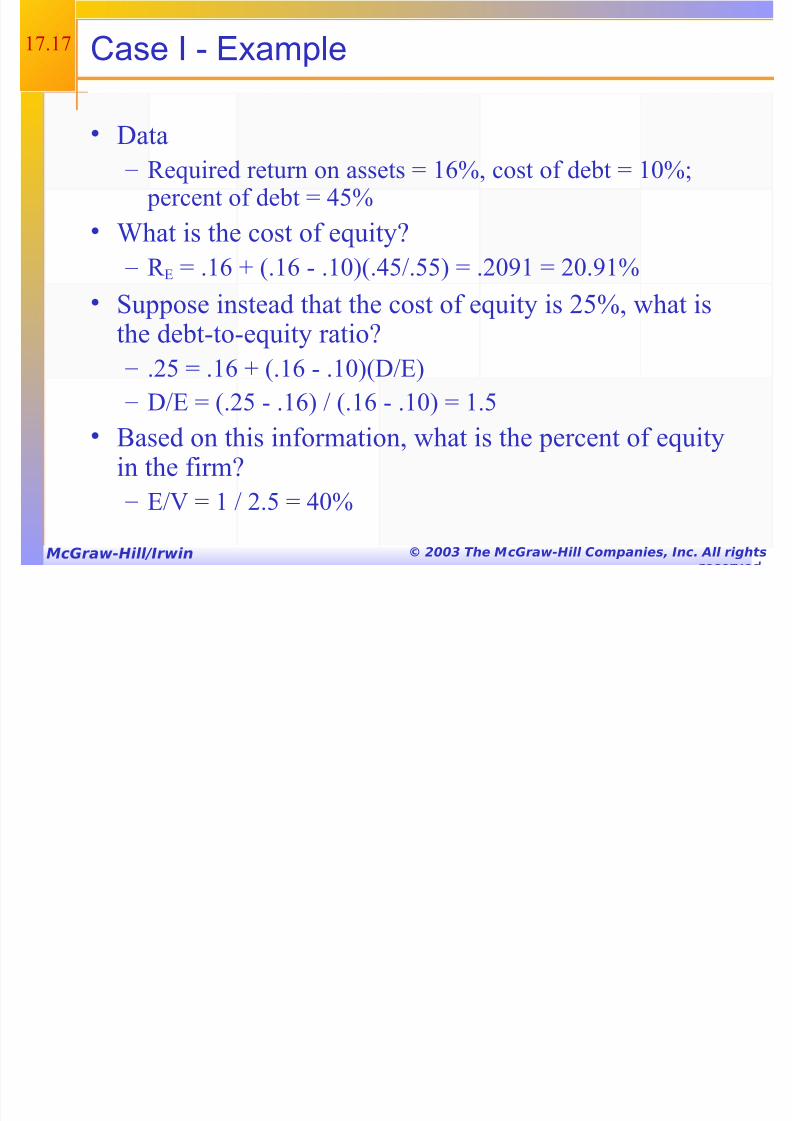

• 3ata 6 :equired return on assets E 18> cost of debt E 1?>K

percent of debt E /4>

• 0hat is the cost of equity5

6 : % E .18 F C.18 B .1?DC./4H.44D E .2?A1 E 2?.A1>• #uppose instead that the cost of equity is 24> what is

the debtBtoBequity ratio5

6 .24 E .18 F C.18 B .1?DC3H%D

6 3H% E C.24 B .18D H C.18 B .1?D E 1.4• ,ased on this information what is the percent of equity

in the firm5

6 %H< E 1 H 2.4 E /?>

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 18/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.1; The C."/! the S/L and "roposition %%

• 9ow does financial leverage affect systematicrisk5

• "*(= : . E : f F β.C: ( 6 : f D

6 0here β. is the firms asset beta and measures thesystematic risk of the firms assets

• *roposition ++

6 :eplace : . with the "*( and assume that thedebt is riskless C: 3 E : f D

6 : % E : f F β.C1F3H%DC: ( 6 : f D

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 19/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.1A #usiness Risk and Financial Risk

• : % E : f F β.C1F3H%DC: ( 6 : f D• "*(= : % E : f F β%C: ( 6 : f D

β% E β.C1 F 3H%D

• !herefore the systematic risk of the stockdepends on=

6 #ystematic risk of the assets β. C,usiness riskD

6 'evel of leverage 3H% C&inancial riskD

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 20/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.2? Case %% ( Cash Flo0

• +nterest is tax deductible• !herefore when a firm adds debt it reduces

taxes all else equal

• !he reduction in taxes increases the cash flowof the firm

• 9ow should an increase in cash flows affect

the value of the firm5

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 21/43McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

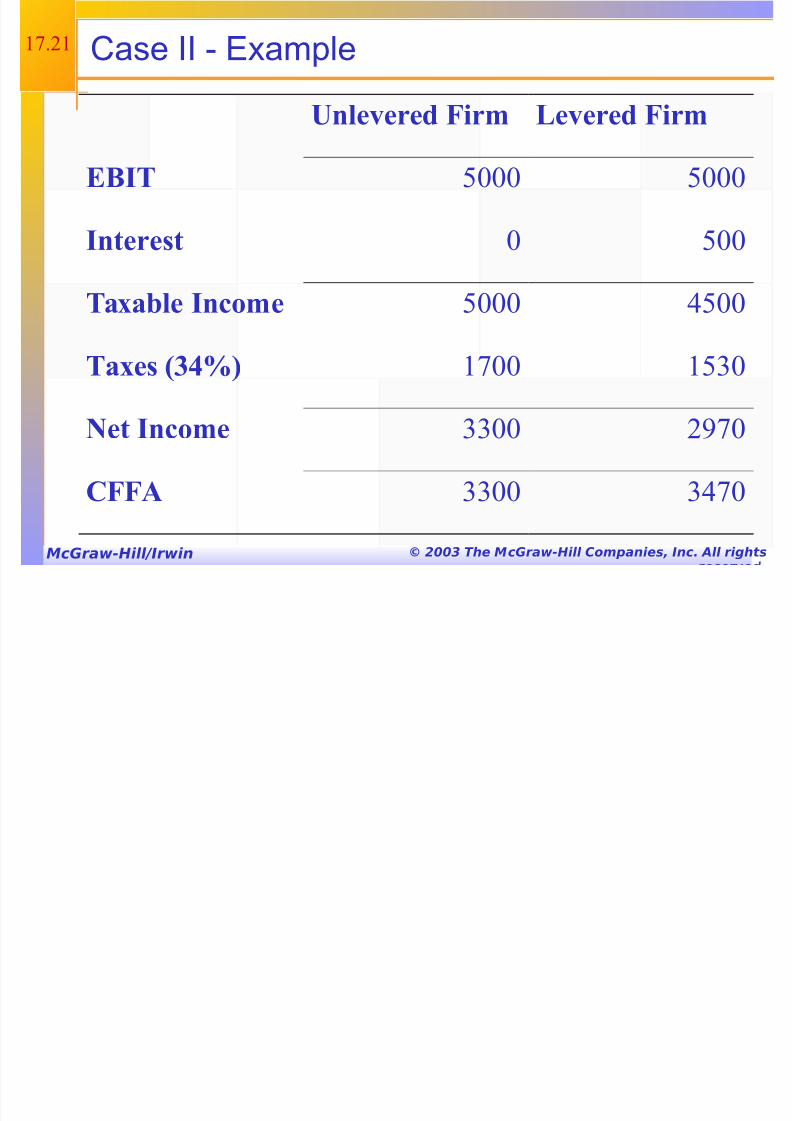

17.21 Case %% $ Example

Unlevered Firm Levered Firm

EBIT 4??? 4???

Interest ? 4??

Taxable Income 4??? /4??

Taxes (34%) 17?? 14?

Net Income ?? 2A7?

FF! ?? /7?

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 22/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

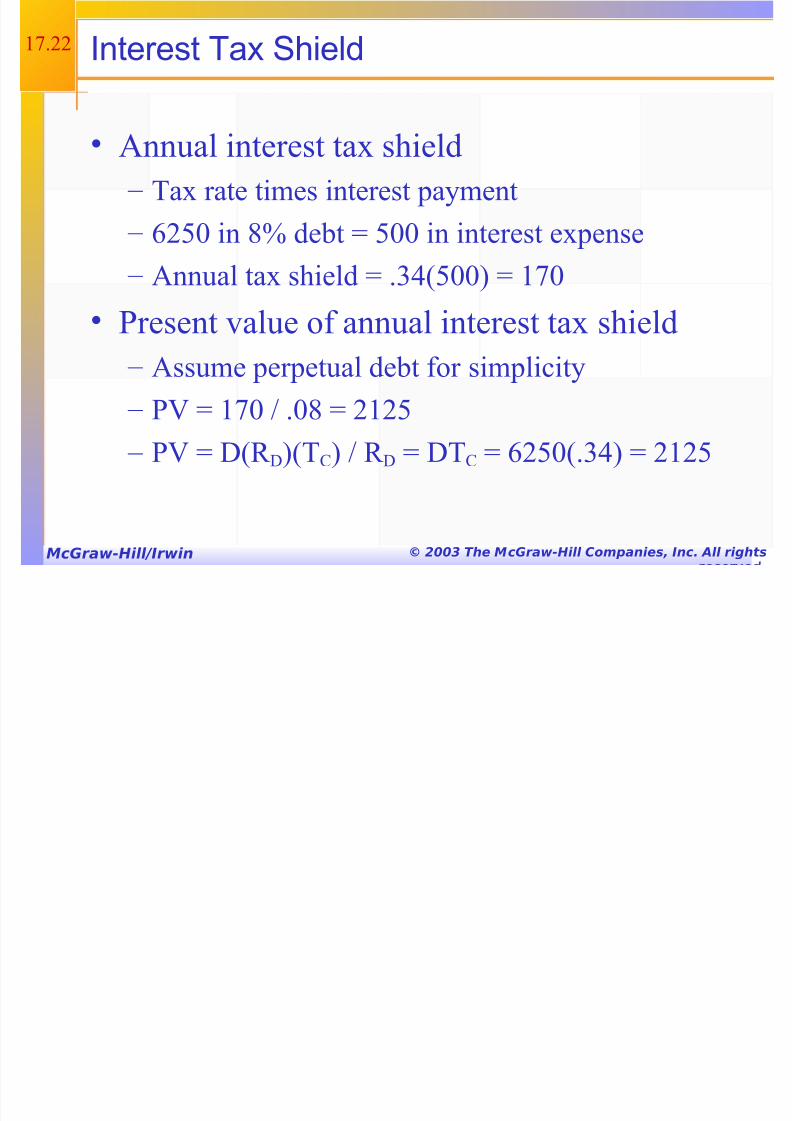

17.22 %nterest Tax Shield

• nnual interest tax shield 6 !ax rate times interest payment

6 824? in ;> debt E 4?? in interest expense

6 nnual tax shield E ./C4??D E 17?

• *resent value of annual interest tax shield

6 ssume perpetual debt for simplicity

6 *< E 17? H .?; E 2124

6 *< E 3C: 3DC!"D H : 3 E 3!" E 824?C./D E 2124

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 23/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

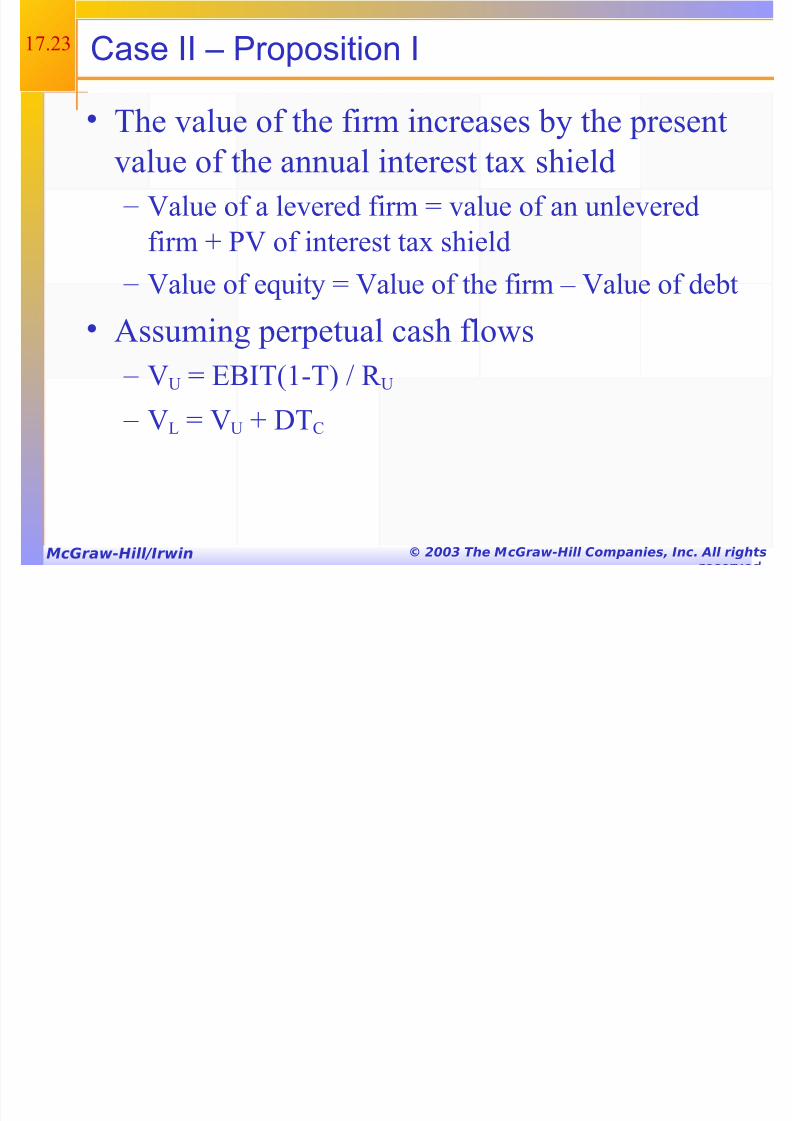

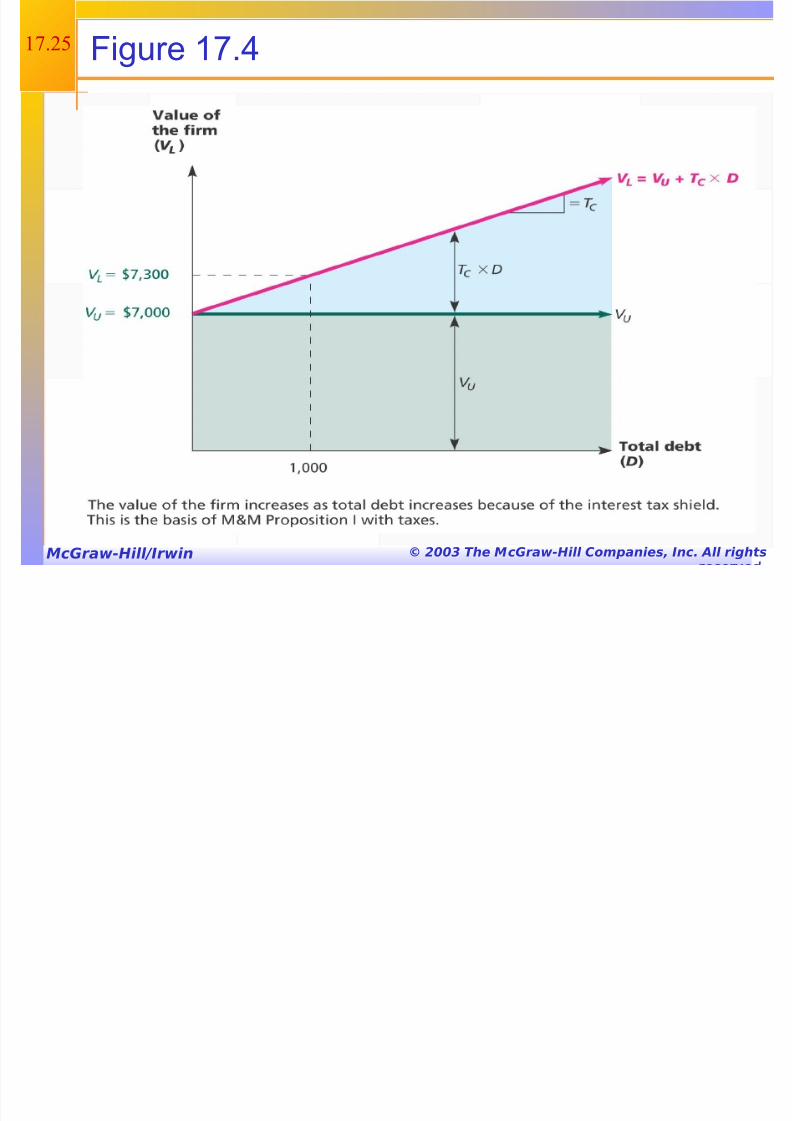

17.2 Case %% ( "roposition %

• !he value of the firm increases by the presentvalue of the annual interest tax shield

6 <alue of a levered firm E value of an unlevered

firm F *< of interest tax shield

6 <alue of equity E <alue of the firm 6 <alue of debt

• ssuming perpetual cash flows

6 <U E %,+!C1B!D H : U

6 <' E <U F 3!"

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 24/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

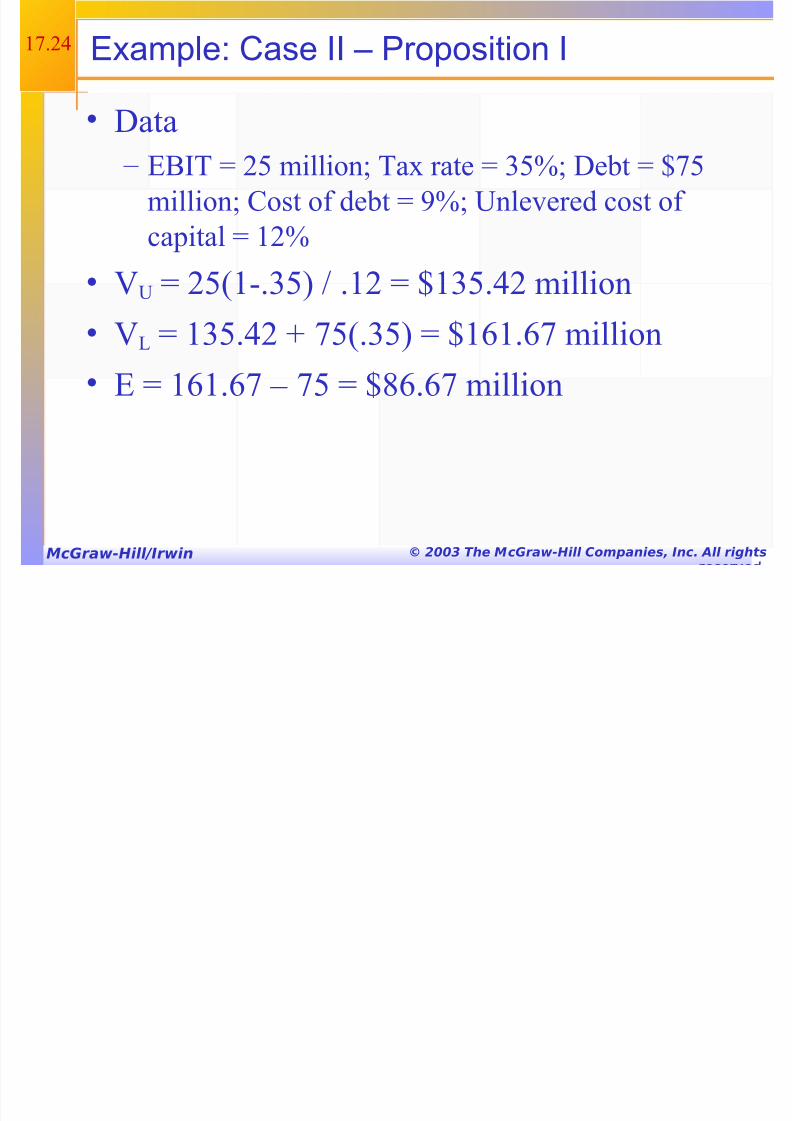

17.2/ Example Case %% ( "roposition %

• 3ata 6 %,+! E 24 millionK !ax rate E 4>K 3ebt E @74

millionK "ost of debt E A>K Unlevered cost of

capital E 12>

• <U E 24C1B.4D H .12 E @14./2 million

• <' E 14./2 F 74C.4D E @181.87 million

• % E 181.87 6 74 E @;8.87 million

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 25/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.24 Figure *+,1

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 26/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

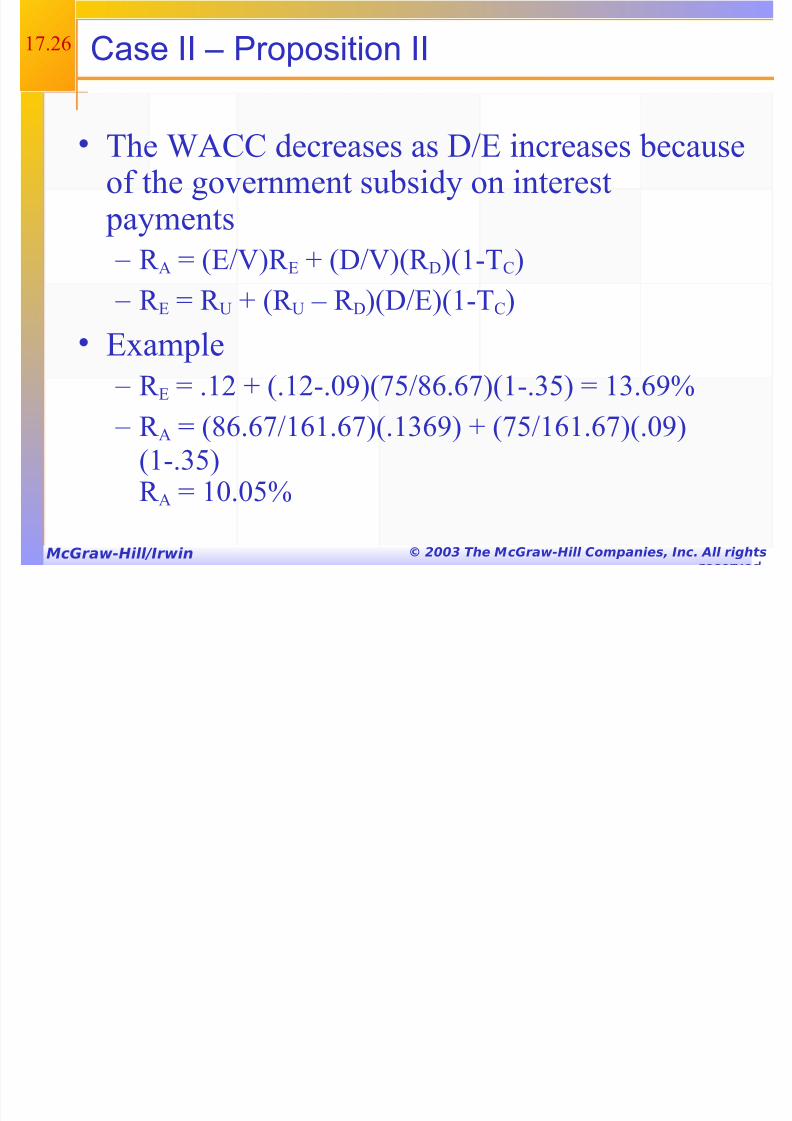

17.28 Case %% ( "roposition %%

• !he 0"" decreases as 3H% increases becauseof the government subsidy on interest payments

6 : . E C%H<D: % F C3H<DC: 3DC1B!"D 6 : % E : U F C: U 6 : 3DC3H%DC1B!"D

• %xample 6

: %

E .12 F C.12B.?ADC74H;8.87DC1B.4D E 1.8A> 6 : . E C;8.87H181.87DC.18AD F C74H181.87DC.?ADC1B.4D: . E 1?.?4>

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 27/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

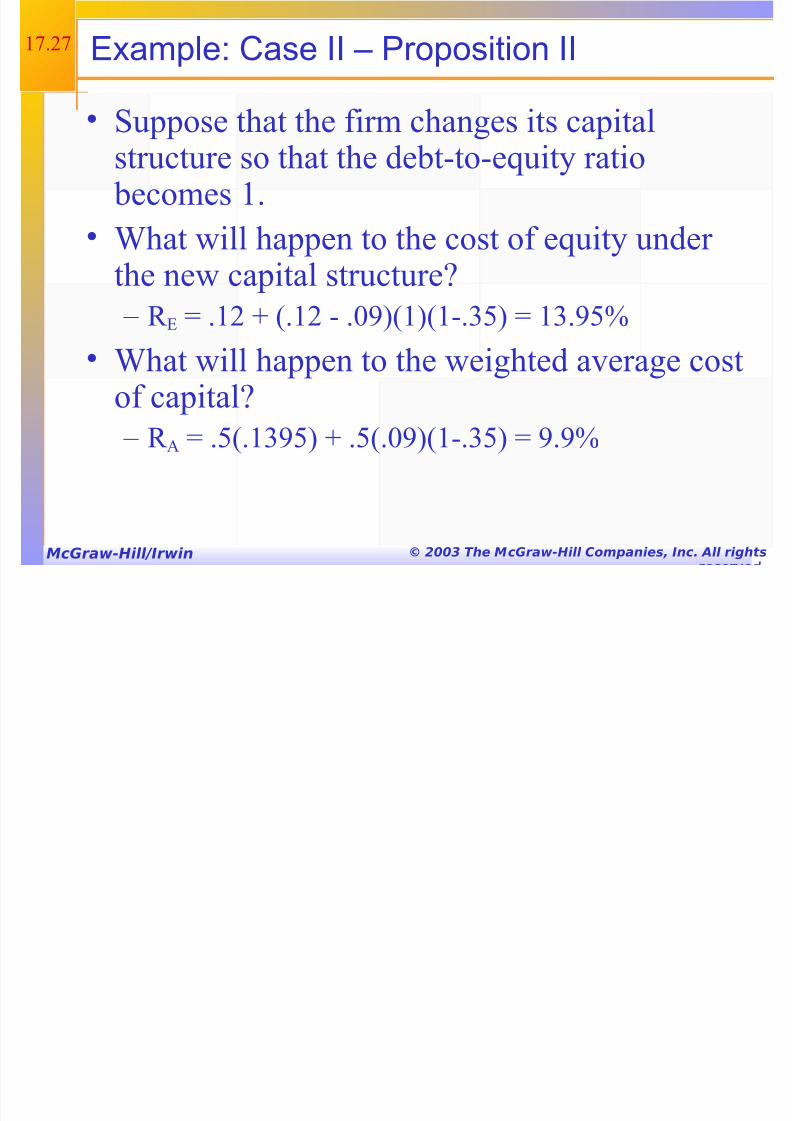

17.27 Example Case %% ( "roposition %%

• #uppose that the firm changes its capitalstructure so that the debtBtoBequity ratio becomes 1.

• 0hat will happen to the cost of equity under

the new capital structure5 6 : % E .12 F C.12 B .?ADC1DC1B.4D E 1.A4>

• 0hat will happen to the weighted average cost

of capital5 6 : . E .4C.1A4D F .4C.?ADC1B.4D E A.A>

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 28/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.2; Figure *+,2

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 29/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

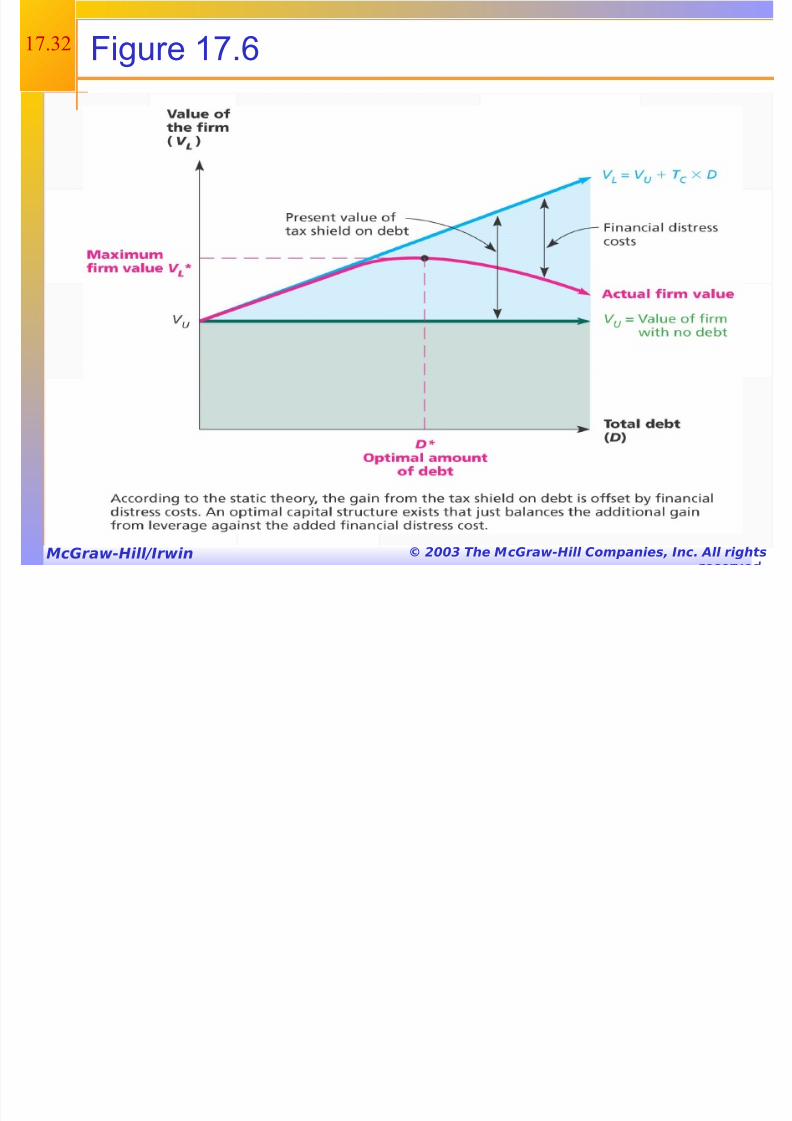

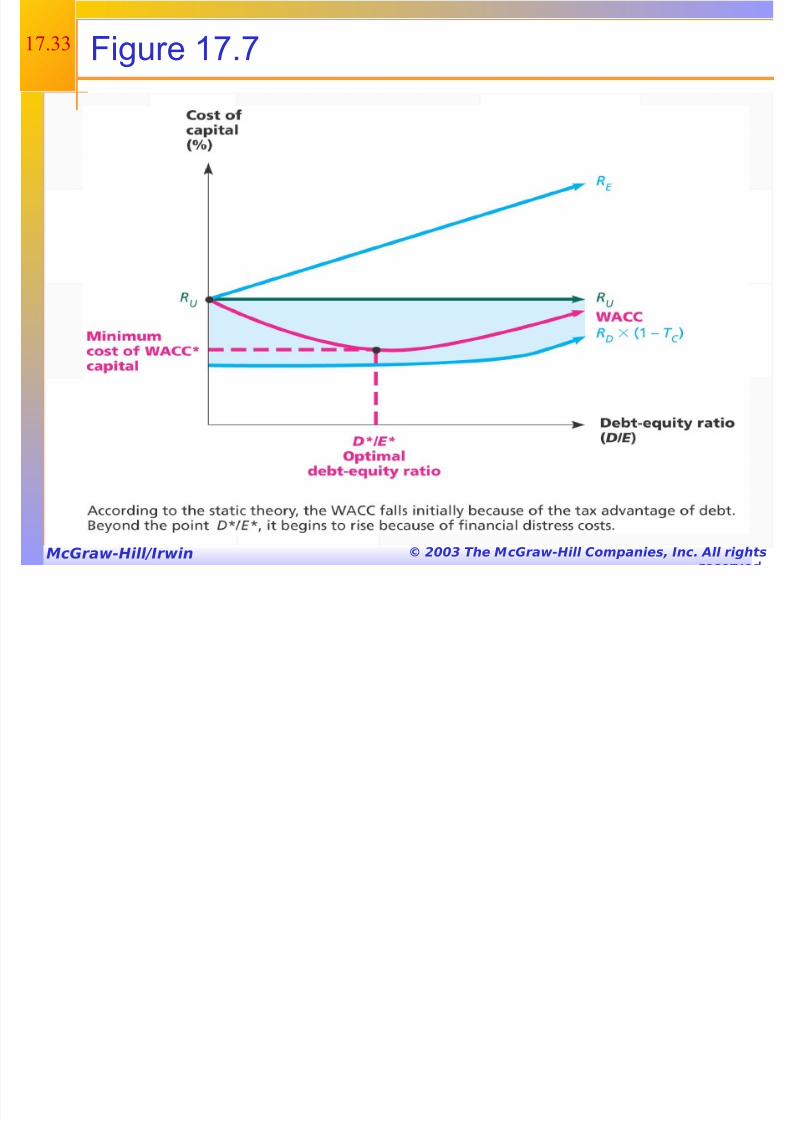

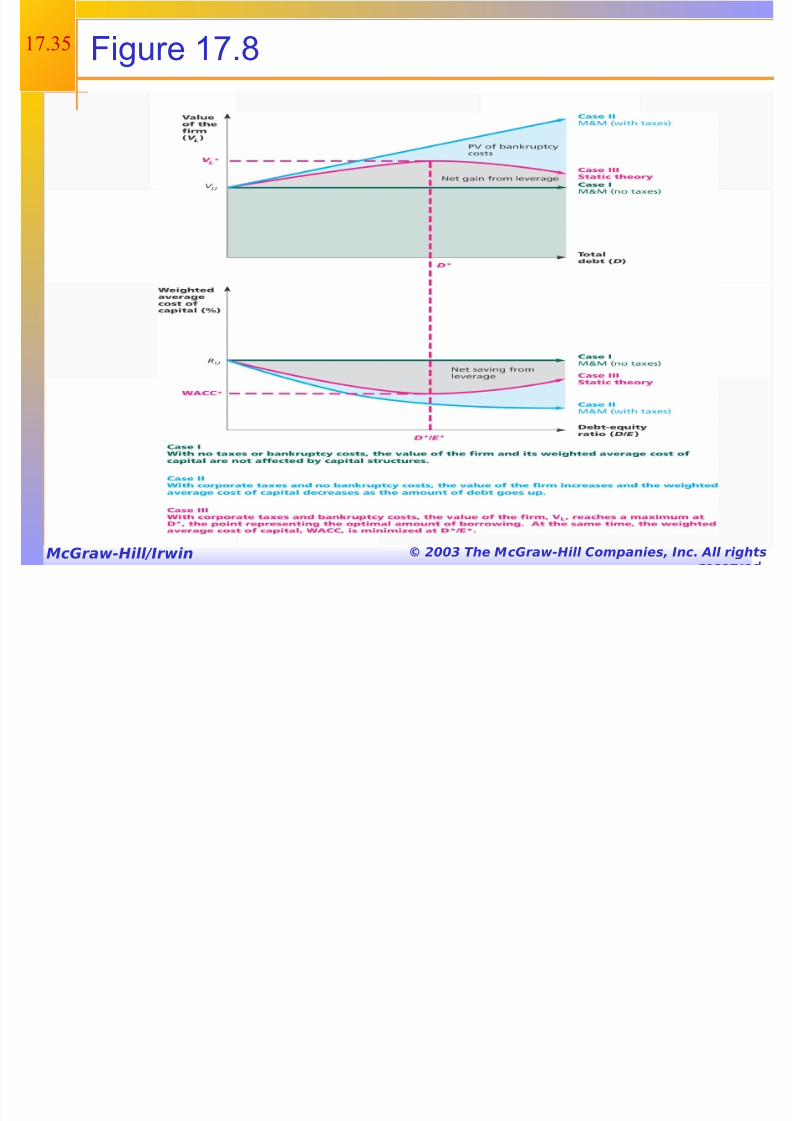

17.2A Case %%%

• Gow we add bankruptcy costs

• s the 3H% ratio increases the probability of bankruptcy increases

• !his increased probability will increase the expected

bankruptcy costs• t some point the additional value of the interest tax

shield will be offset by the expected bankruptcy cost

• t this point the value of the firm will start to

decrease and the 0"" will start to increase as moredebt is added

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 30/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.? #ankruptcy Costs

• 3irect costs 6 'egal and administrative costs

6 Ultimately cause bondholders to incur additional

losses

6 3isincentive to debt financing

• &inancial distress

6 #ignificant problems in meeting debt obligations

6 (ost firms that experience financial distress do

not ultimately file for bankruptcy

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 31/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.1 /ore #ankruptcy Costs

• +ndirect bankruptcy costs 6 'arger than direct costs but more difficult to measure

and estimate

6 #tockholders wish to avoid a formal bankruptcy filing

6 ,ondholders want to keep existing assets intact so theycan at least receive that money

6 ssets lose value as management spends time worryingabout avoiding bankruptcy instead of running the

business 6 lso have lost sales interrupted operations and loss of

valuable employees

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 32/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.2 Figure *+,3

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 33/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17. Figure *+,+

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 34/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17./ Conclusions

• "ase + 6 no taxes or bankruptcy costs 6 Go optimal capital structure

• "ase ++ 6 corporate taxes but no bankruptcy costs

6 -ptimal capital structure is 1??> debt 6 %ach additional dollar of debt increases the cash flowof the firm

• "ase +++ 6 corporate taxes and bankruptcy costs

6 -ptimal capital structure is part debt and part equity 6 -ccurs where the benefit from an additional dollar of

debt is Lust offset by the increase in expected bankruptcy costs

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 35/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.4 Figure *+,4

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 36/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.8 /anagerial Recommendations

•!he tax benefit is only important if the firmhas a large tax liability

• :isk of financial distress

6 !he greater the risk of financial distress the lessdebt will be optimal for the firm

6 !he cost of financial distress varies across firms

and industries and as a manager you need to

understand the cost for your industry

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 37/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17.7 Figure *+,5

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 38/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

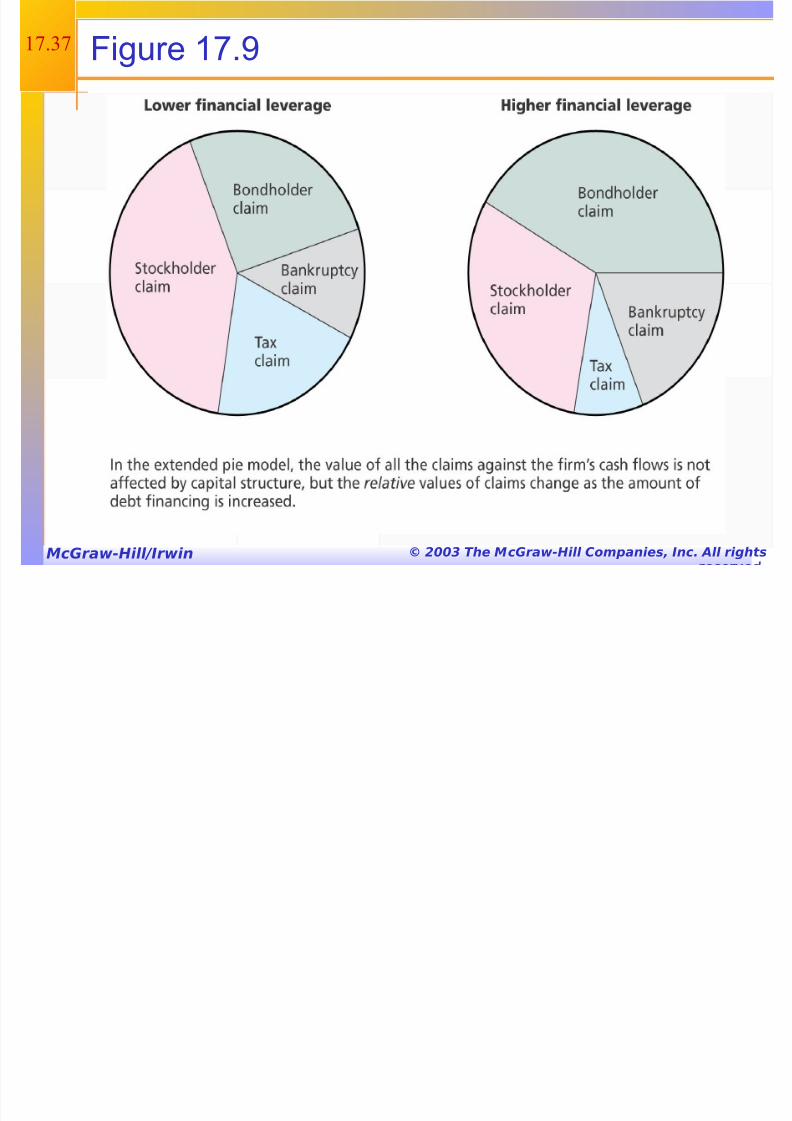

17.; The 6alue of the Firm

•<alue of the firm E marketed claims Fnonmarketed claims 6 (arketed claims are the claims of stockholders

and bondholders

6 Gonmarketed claims are the claims of thegovernment and other potential stakeholders

• !he overall value of the firm is unaffected bychanges in capital structure

• !he division of value between marketedclaims and nonmarketed claims may beimpacted by capital structure decisions

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 39/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

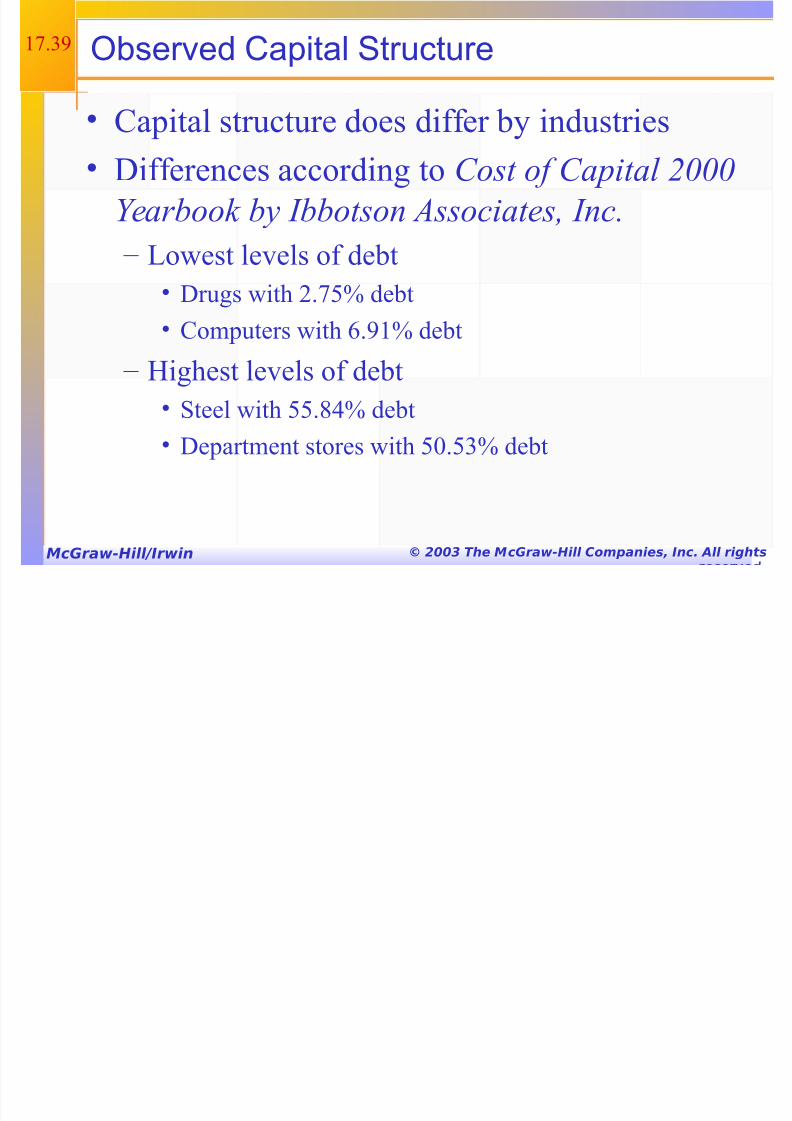

17.A O7served Capital Structure

•"apital structure does differ by industries

• 3ifferences according to Cost of Capital 2000

Yearbook by Ibbotson Associates, Inc.

6 'owest levels of debt• 3rugs with 2.74> debt

• "omputers with 8.A1> debt

6 9ighest levels of debt

• #teel with 44.;/> debt

• 3epartment stores with 4?.4> debt

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 40/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17./? 8ork the 8e7 Example

•Mou can find information about a companyscapital structure relative to its industry sector

and the #)* 4?? at Mahoo (arketguide

• "lick on the web surfer to go to the site

6 "hoose a company and get a quote

6 "hoose ratio comparisons

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 41/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17./1 #ankruptcy "rocess ( "art %

•,usiness failure 6 business has terminatedwith a loss to creditors

• 'egal bankruptcy 6 petition federal court for

bankruptcy

• !echnical insolvency 6 firm is unable to meet

debt obligations

• ccounting insolvency 6 book value of equityis negative

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 42/43

McGraw-Hill!Irwin © 2003 The McGraw-Hill Companies, Inc. All rights

17./2 #ankruptcy "rocess ( "art %%

•'iquidation 6 "hapter 7 of the &ederal ,ankruptcy :eform ct

of 1A7;

6 !rustee takes over assets sells them and

distributes the proceeds according to the absolute priority rule

• :eorganiation 6 "hapter 11 of the &ederal ,ankruptcy :eform ct

of 1A7;

6 :estructure the corporation with a provision torepay creditors

7/17/2019 Lecture 13

http://slidepdf.com/reader/full/lecture-13-568ecdf5f4098 43/43

17./ 9uick 9ui:

•%xplain the effect of leverage on %*# and:-%

• 0hat is the breakBeven %,+!5

• 9ow do we determine the optimal capitalstructure5

• 0hat is the optimal capital structure in the

three cases that were discussed in this chapter5• 0hat is the difference between liquidation and

reorganiation5