Embed Size (px)

Citation preview

Lecture 19Interdependence & Coordination

International Interdependence• Theory:

Interdependence results from capital mobility, even with floating rates.

• Empirical estimates of cross-country effects.

International Coordination• The institutions of international cooperation• Theory: Prisoners’ dilemma

Interdependence under floating exchange ratesRevisited

Two of the results derived previously were too strong to be literally true:

When we first looked at the question, floating rates insulated countries from each other’s economies. But that was when KA=0 (+ORT=0 => CA =0).o Since then, capital mobility has changed things.o US, euroland, Japan, UK, etc., are still visibly correlated.

Under κ=, we found G leaked abroad 100%, through offsetting TD. No effect remained at home.o This overly strong result was a consequence

of the assumption i = .ITF-220 Prof.J.Frankel

Why don’t floating rates insulate? Capital flows => CA is not necessarily = 0.

But the restriction i = is in reality too strong, even for modern conditions of low international capital flow barriers.

Why? Reasons:(1) i i*, when investors are aware of likelihood of future exchange rate changes,and

(2) i* is not exogenous, if domestic country is large in world financial markets (as are US & EU).=> Two-country model.

Implication: Effects of AD expansion are partly felt in domestic country, partly transmitted abroad through TD.

ITF-220 Prof.J.Frankel

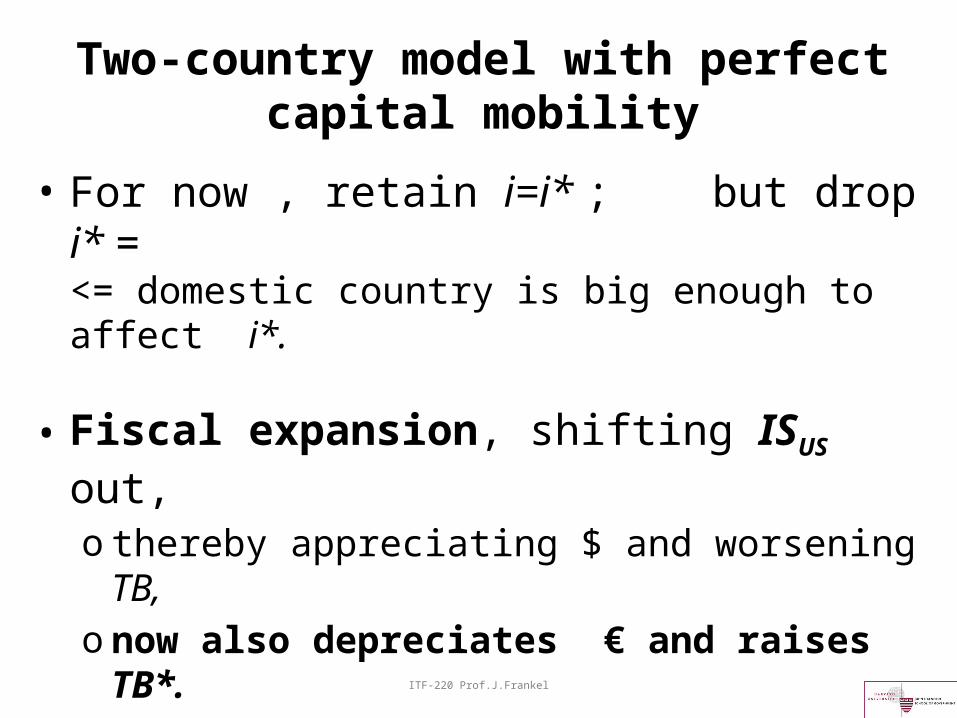

Two-country model with perfect capital mobility

• For now , retain i=i* ; but drop i* = <= domestic country is big enough to affect i*.

• Fiscal expansion, shifting ISUS out, o thereby appreciating $ and worsening TB,o now also depreciates € and raises TB*.o So Y rises (crowding out < 100% ), despite κ=∞,o Y* rises (international transmission), despite floating,o as i and i* rise in tandem.

ITF-220 Prof.J.Frankel

ITF-220 Prof.J.Frankel

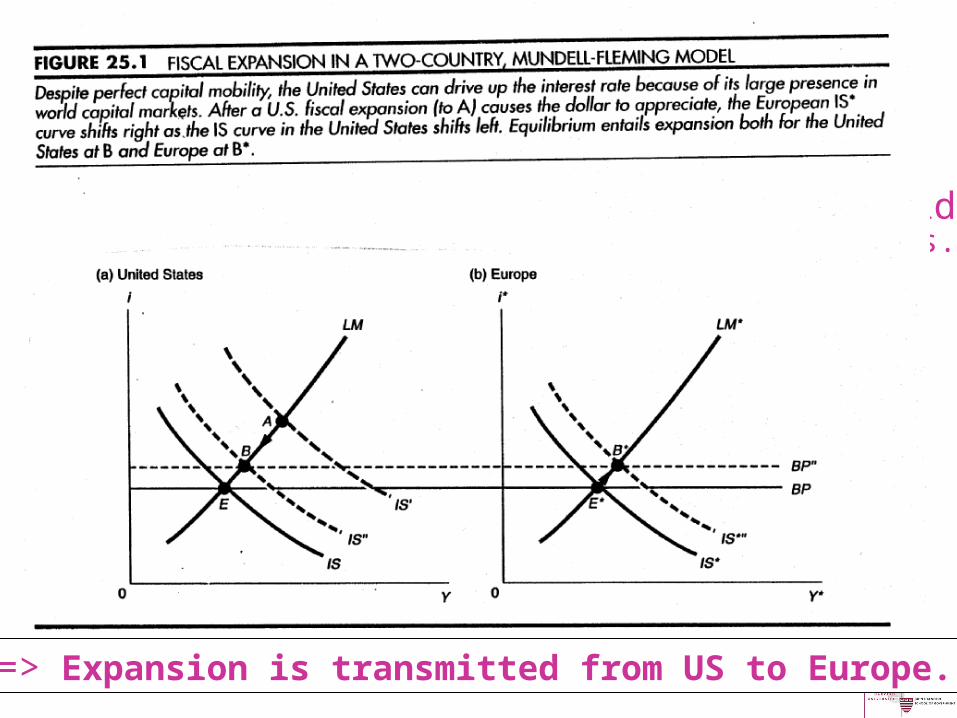

US expansionbecause US is large in world financial markets.

drives up interest rates worldwide,

$↑

€↓

=> Expansion is transmitted from US to Europe.

• •

G↑

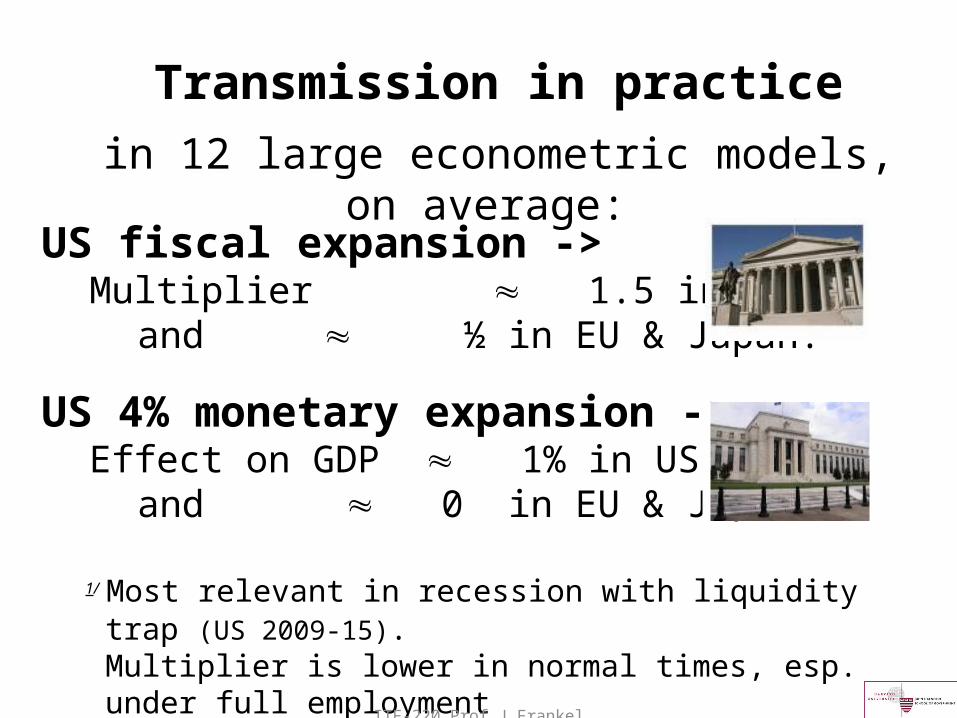

Transmission in practicein 12 large econometric models, on average:

US fiscal expansion ->Multiplier 1.5 in US 1/

and ½ in EU & Japan.

US 4% monetary expansion ->Effect on GDP 1% in US

and 0 in EU & Japan.

1/ Most relevant in recession with liquidity trap (US 2009-15).Multiplier is lower in normal times, esp. under full employment (or under default risk, or in small open economies).

ITF-220 Prof.J.Frankel

ITF-220 Prof.J.Frankel

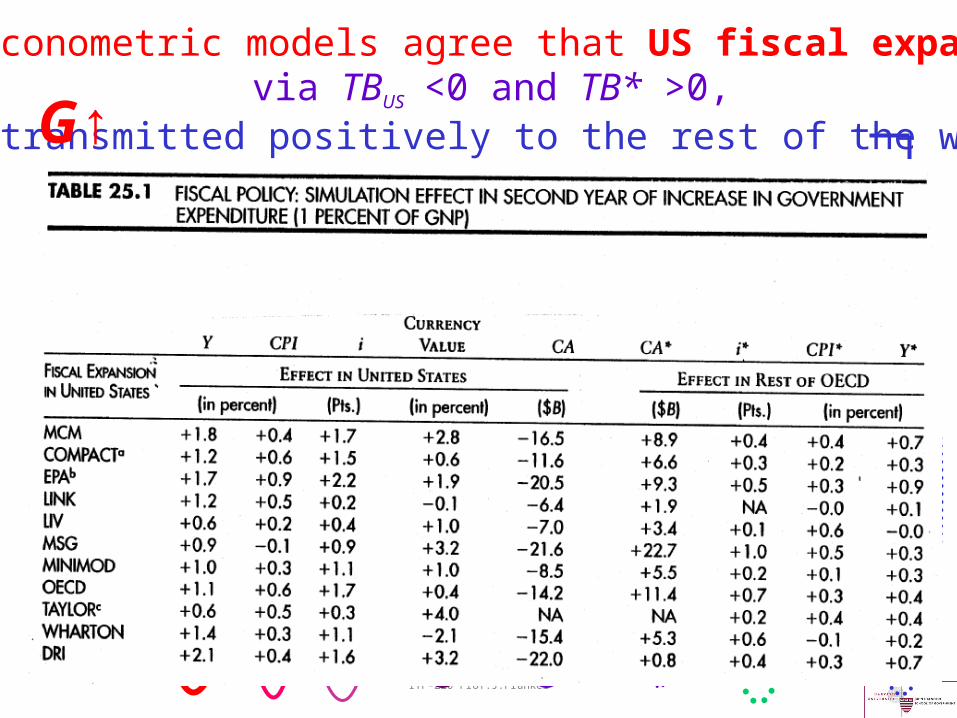

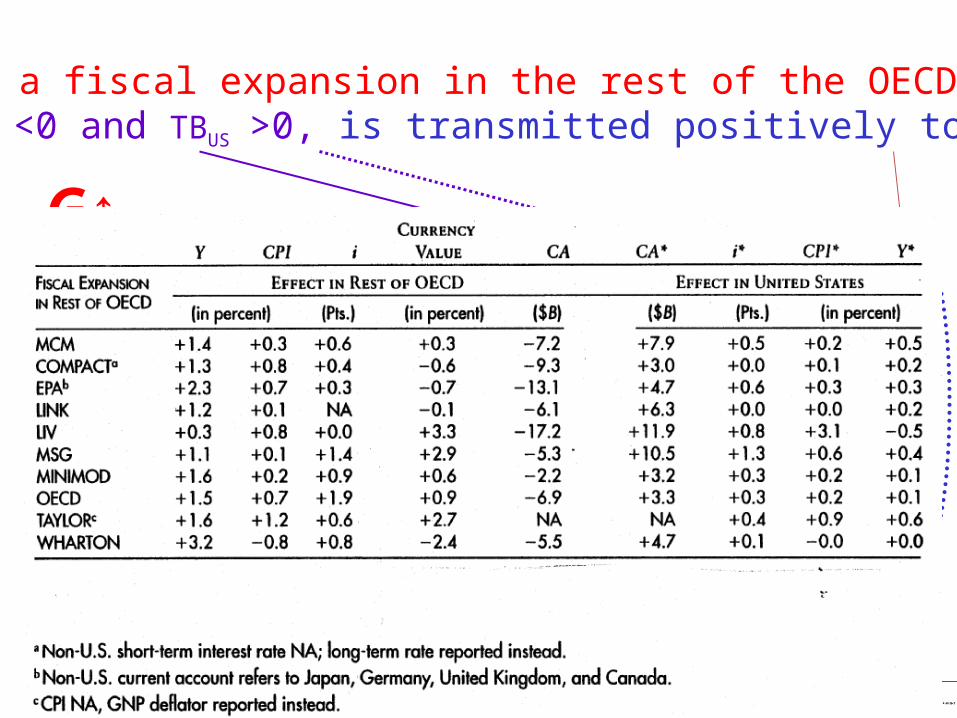

The econometric models agree that US fiscal expansion, via TBUS <0 and TB* >0,

is transmitted positively to the rest of the world.G↑

ITF-220 Prof.J.Frankel

Similarly, a fiscal expansion in the rest of the OECD countries via TBRoW <0 and TBUS >0, is transmitted positively to the US.

G↑

ITF-220 Prof.J.Frankel

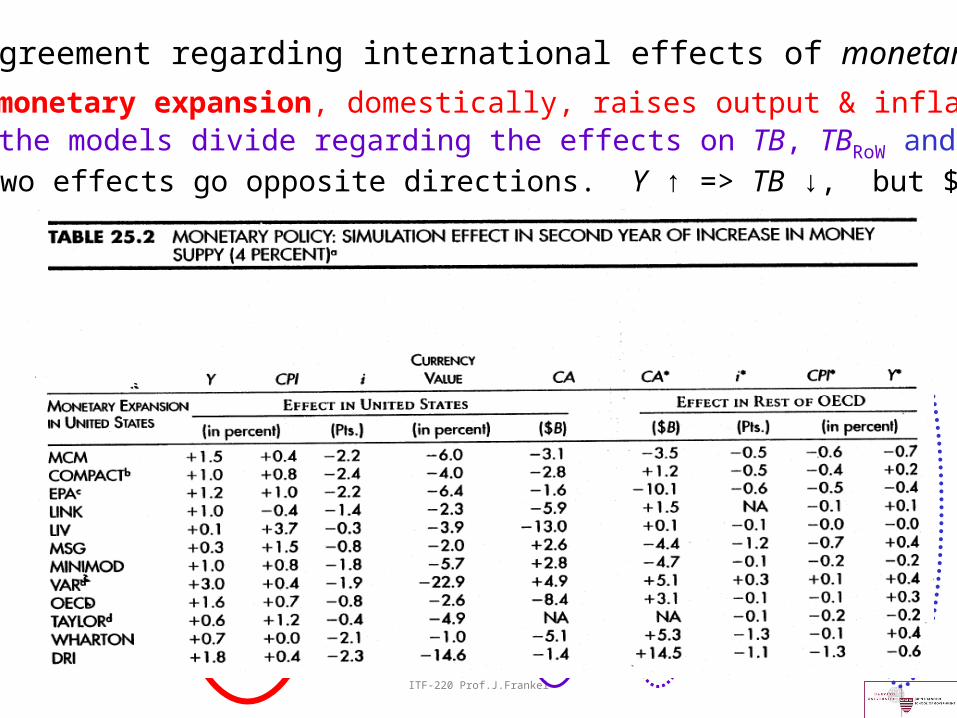

More disagreement regarding international effects of monetary policy.A US monetary expansion, domestically, raises output & inflation.But the models divide regarding the effects on TB, TBRoW and YRoW.

Reason: two effects go opposite directions. Y ↑ => TB ↓, but $↓ => TB ↑

M↑

ITF-220 Prof.J.Frankel

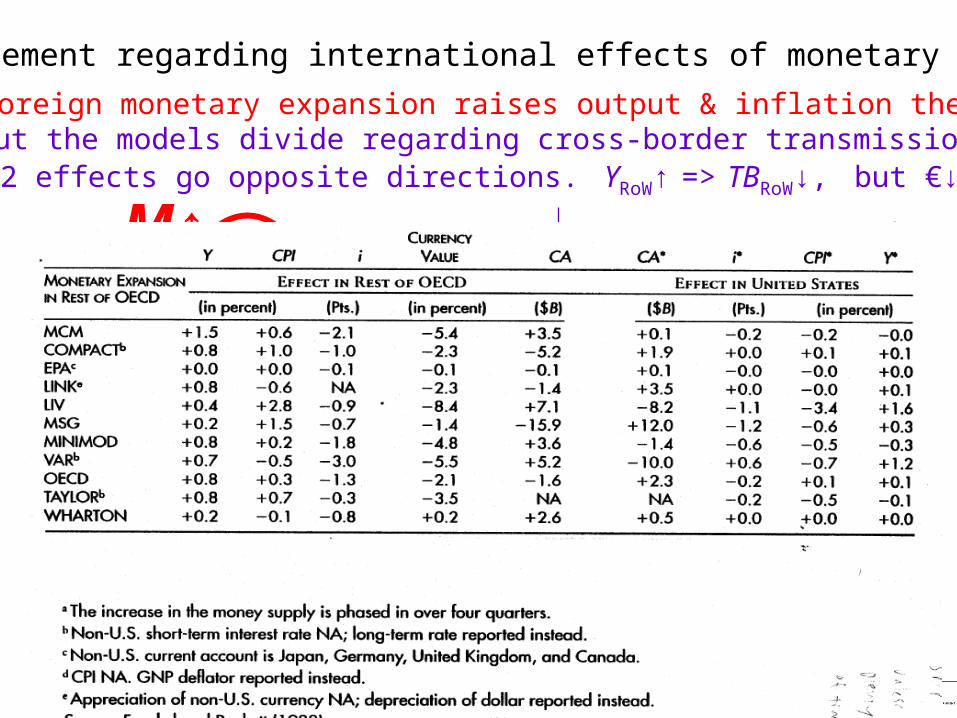

Disagreement regarding international effects of monetary policy.A foreign monetary expansion raises output & inflation there.

But the models divide regarding cross-border transmission.Reason: 2 effects go opposite directions. YRoW↑ => TBRoW↓, but €↓ => TBRoW↑

M↑

International macroeconomic policy coordination, continued

Institutions of coordination: G7 Leaders Summit & Finance Ministers

1975 Rambouillet: ratified floating 1978 Bonn: locomotive theory 1985 Plaza: concerted intervention to depreciate $ 2013 No currency war: Members agree won’t intervene.

BIS & Basel Committee on Banking Supervision • 1988 Basel Accord: set capital adequacy rules for intl. banks• 2007 Basel II: Gov.t bonds should not necessarily get 0 risk weight. • 2011 Basel III: Higher capital requirements.

G20 includes big emerging markets; 2009 London: G20 replaced G7/G8,

responded to global recession with simultaneous stimulus.

OECD for industrialized countries .

IMF for everyone (“Surveillance”).

ITF-220 Prof.J.Frankel

ITF-220 Prof.J.Frankel

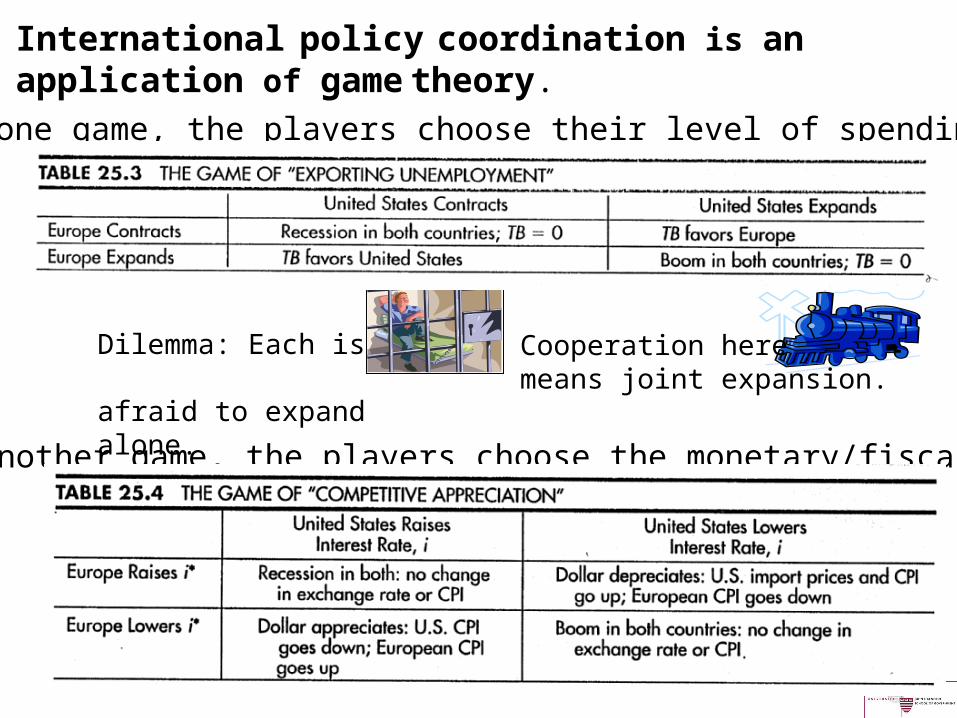

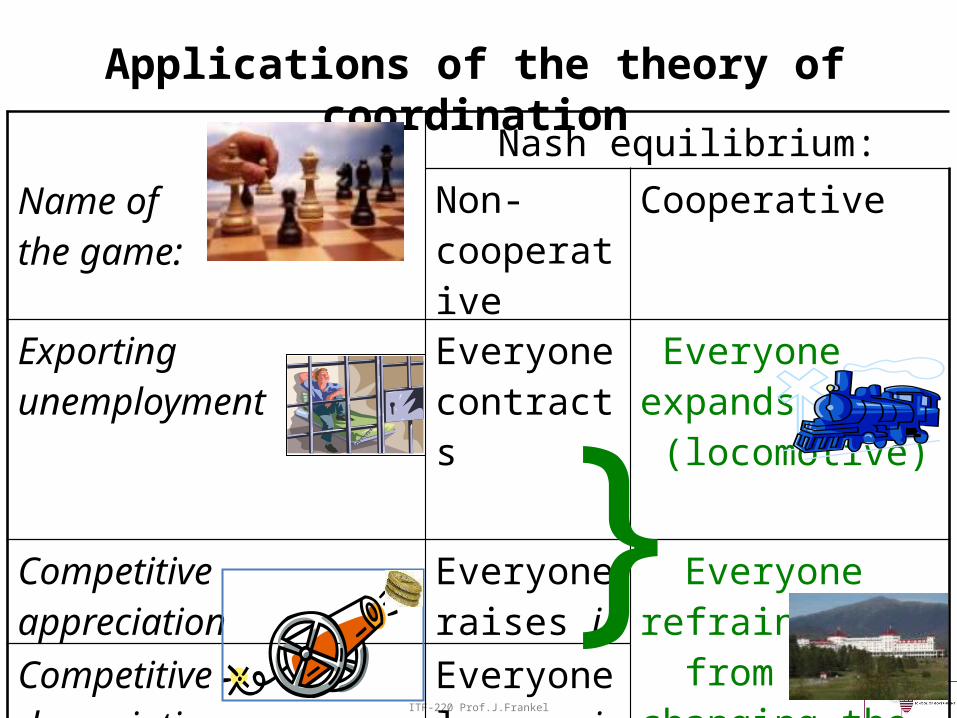

International policy coordination is an application of game theory.

In another game, the players choose the monetary/fiscal mix.

In one game, the players choose their level of spending.

Cooperation here means joint expansion.

Dilemma: Each is afraid to expand alone.

ITF-220 Prof.J.Frankel

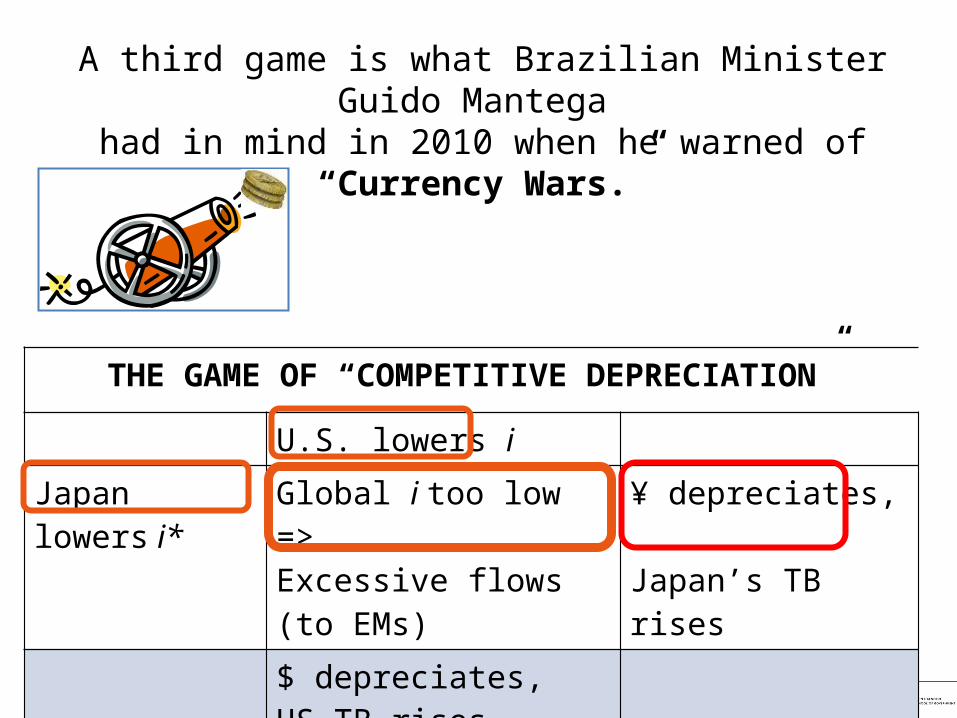

THE GAME OF “COMPETITIVE DEPRECIATION”

U.S. lowers iJapan lowers i* Global i too low =>

Excessive flows (to EMs)¥ depreciates, Japan’s TB rises

$ depreciates, US TB rises

A third game is what Brazilian Minister Guido Mantega had in mind in 2010 when he warned of “Currency Wars.”

ITF-220 Prof.J.Frankel

Applications of the theory of coordination

Name of the game:

Nash equilibrium:

Non-cooperative

Cooperative

Exporting unemployment

Everyone contracts

Everyone expands (locomotive)

Competitive appreciation

Everyone raises i

Everyone refrains from changing the exchange rate.Competitive

depreciationEveryone lowers i

}