Embed Size (px)

Citation preview

Managerial Accounting2nd Edition

J. O'Callaghan

Managerial Accounting

by:J. O'Callaghan

Copyright © 2002 John Wiley & Sons, Inc. All rights reserved.

John Wiley & Sons, Inc.New York

0471413658

Due to electronic permissions issues, some material may have been removed from this chapter,though reference to it may occur in the text. The University of Phoenix has determined that thecontent presented herein satisfies the requirements for this course.

ii

Table of Contents

CHAPTER 1MANAGERIAL ACCOUNTING BASICS............................................................................. 5

COMPARING MANAGERIAL AND FINANCIAL ACCOUNTING........................... 6ETHICAL STANDARDS FOR MANAGERIAL ACCOUNTANTS............................... 7MANAGEMENT FUNCTIONS........................................................................................... 7

MANAGERIAL COST CONCEPTS....................................................................................... 9MANUFACTURING COSTS............................................................................................... 9PRODUCT VERSUS PERIOD COSTS............................................................................... 11

MANUFACTURING COSTS IN FINANCIAL STATEMENTS..................................... 13INCOME STATEMENT...................................................................................................... 13BALANCE SHEET............................................................................................................... 16COST CONCEPTS‐A REVIEW.......................................................................................... 18

CONTEMPORARY DEVELOPMENTS IN MANAGERIAL ACCOUNTING............. 20SERVICE INDUSTRY TRENDS......................................................................................... 20VALUE CHAIN MANAGEMENT.................................................................................... 22

APPENDIX 1A ACCOUNTING CYCLE FOR A MANUFACTURING COMPANY... 27WORK SHEET........................................................................................................................... 28CLOSING ENTRIES................................................................................................................ 30SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 1A............................................. 32GLOSSARYū 67

CHAPTER 2COST ACCOUNTING SYSTEMS......................................................................................... 72

JOB ORDER COST SYSTEM.............................................................................................. 73PROCESS COST SYSTEM................................................................................................... 73

JOB ORDER COST FLOW...................................................................................................... 75ACCUMULATING MANUFACTURING COSTS.......................................................... 76ASSIGNING MANUFACTURING COSTS TO WORK IN PROCESS......................... 78ASSIGNING COSTS TO FINISHED GOODS.................................................................. 89ASSIGNING COSTS TO COST OF GOODS SOLD........................................................ 90SUMMARY OF JOB ORDER COST FLOWS.................................................................... 90

REPORTING JOB COST DATA............................................................................................ 92UNDER‐ OR OVERAPPLIED MANUFACTURING OVERHEAD................................ 93

INTERIM BALANCES........................................................................................................ 93YEAR‐END BALANCE....................................................................................................... 94

GLOSSARY.............................................................................................................................. 130CHAPTER 3

THE NATURE OF PROCESS COST SYSTEMS............................................................... 136USES OF PROCESS COST SYSTEMS............................................................................. 136

Managerial AccountingTable of Contents

iii

SIMILARITIES AND DIFFERENCES BETWEEN JOB ORDER COST AND PROCESSCOST SYSTEMS................................................................................................................. 138PROCESS COST FLOW.................................................................................................... 140ASSIGNMENT OF MANUFACTURING COSTS—JOURNAL ENTRIES................ 140

EQUIVALENT UNITS........................................................................................................... 145WEIGHTED‐AVERAGE METHOD................................................................................ 145REFINEMENTS ON THE WEIGHTED‐AVERAGE METHOD.................................. 146PRODUCTION COST REPORT....................................................................................... 148

COMPREHENSIVE EXAMPLE OF PROCESS COSTING............................................. 149COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 149COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 150COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 151PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 152PREPARING THE PRODUCTION COST REPORT..................................................... 153

FINAL COMMENTS.............................................................................................................. 155APPENDIX 3A FIFO METHOD........................................................................................... 162EQUIVALENT UNITS UNDERFIFO................................................................................. 162

ILLUSTRATION................................................................................................................. 163COMPREHENSIVE EXAMPLE........................................................................................... 164

COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 165COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 166COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 167PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 168PREPARING THE PRODUCTION COST REPORT..................................................... 169

FIFO AND WEIGHTED‐AVERAGE................................................................................... 171SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 3A........................................... 171GLOSSARY.............................................................................................................................. 207

CHAPTER 4ACTIVITY‐BASED COSTING VERSUS TRADITIONAL COSTING........................ 213

TRADITIONAL COSTING SYSTEMS............................................................................ 213THE NEED FOR A NEW COSTING SYSTEM.............................................................. 214ACTIVITY‐BASED COSTING.......................................................................................... 215

ILLUSTRATION OF TRADITIONAL COSTING VERSUS ABC................................ 217UNIT COSTS UNDER TRADITIONAL COSTING...................................................... 217UNIT COSTS UNDER ABC.............................................................................................. 217COMPARING UNIT COSTS............................................................................................ 221

ACTIVITY‐BASED COSTING: A CLOSER LOOK......................................................... 224BENEFITS OF ABC............................................................................................................ 224LIMITATIONS OF ABC.................................................................................................... 225WHEN TO SWITCH TO ABC.......................................................................................... 226VALUE‐ADDED VERSUS NONVALUE‐ADDED ACTIVITIES................................ 226

ACTIVITY‐BASED COSTING IN SERVICE INDUSTRIES......................................... 228

Managerial AccountingTable of Contents

iv

TRADITIONAL COSTING EXAMPLE.......................................................................... 229ACTIVITY‐BASED COSTING EXAMPLE..................................................................... 230

JUST‐IN‐TIME PROCESSING............................................................................................ 232OBJECTIVE OF JIT PROCESSING.................................................................................. 233ELEMENTS OF JIT PROCESSING.................................................................................. 233BENEFITS OF JIT PROCESSING..................................................................................... 234

APPENDIX 4A HIERARCHY OF ACTIVITY LEVELS................................................... 238SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 4A........................................... 241GLOSSARY.............................................................................................................................. 280

CHAPTER 5COST BEHAVIOR ANALYSIS............................................................................................ 287

VARIABLE COSTS............................................................................................................ 288FIXED COSTS..................................................................................................................... 289RELEVANT RANGE......................................................................................................... 290MIXED COSTS.................................................................................................................... 292IMPORTANCE OF IDENTIFYING VARIABLE AND FIXED COSTS....................... 295

COST‐VOLUME‐PROFIT ANALYSIS............................................................................... 296BASIC COMPONENTS..................................................................................................... 297CVP INCOME STATEMENT........................................................................................... 297BREAK‐EVEN ANALYSIS............................................................................................... 301MARGIN OF SAFETY....................................................................................................... 307TARGET NET INCOME................................................................................................... 308CVP AND CHANGES IN THE BUSINESS ENVIRONMENT.................................... 310CVP INCOME STATEMENT REVISITED..................................................................... 313

APPENDIX 5A VARIABLE COSTING.............................................................................. 317EFFECTS OF VARIABLE COSTING ON INCOME........................................................ 318RATIONALE FOR VARIABLE COSTING....................................................................... 320SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 5A........................................... 321GLOSSARY.............................................................................................................................. 344

CHAPTER 6BUDGETING BASICS........................................................................................................... 350

BUDGETING AND ACCOUNTING.............................................................................. 351THE BENEFITS OF BUDGETING................................................................................... 351ESSENTIALS OF EFFECTIVE BUDGETING................................................................. 352LENGTH OF THE BUDGET PERIOD............................................................................ 352THE BUDGETING PROCESS.......................................................................................... 352BUDGETING AND HUMAN BEHAVIOR.................................................................... 353BUDGETING AND LONG‐RANGE PLANNING....................................................... 354THE MASTER BUDGET................................................................................................... 355

PREPARING THE OPERATING BUDGETS.................................................................... 356SALES BUDGET................................................................................................................. 356PRODUCTION BUDGET................................................................................................. 357

Managerial AccountingTable of Contents

v

DIRECT MATERIALS BUDGET...................................................................................... 358DIRECT LABOR BUDGET............................................................................................... 360MANUFACTURING OVERHEAD BUDGET............................................................... 360SELLING AND ADMINISTRATIVE EXPENSE BUDGET.......................................... 361BUDGETED INCOME STATEMENT............................................................................. 363

PREPARING THE FINANCIAL BUDGETS..................................................................... 364CASH BUDGET.................................................................................................................. 364BUDGETED BALANCE SHEET...................................................................................... 368

BUDGETING IN NONMANUFACTURING COMPANIES......................................... 370MERCHANDISERS........................................................................................................... 370SERVICE ENTERPRISES.................................................................................................. 372NOT‐FOR‐PROFIT ORGANIZATIONS......................................................................... 373

GLOSSARY.............................................................................................................................. 407CHAPTER 7

CONCEPT OF BUDGETARY CONTROL......................................................................... 413STATIC BUDGET REPORTS............................................................................................... 414

ILLUSTRATIONS.............................................................................................................. 415USES AND LIMITATIONS.............................................................................................. 416

FLEXIBLE BUDGETS............................................................................................................. 417WHY FLEXIBLE BUDGETS?............................................................................................ 418DEVELOPING THE FLEXIBLE BUDGET...................................................................... 421FLEXIBLE BUDGET—A CASE STUDY......................................................................... 421FLEXIBLE BUDGET REPORTS........................................................................................ 424MANAGEMENT BY EXCEPTION................................................................................. 425

THE CONCEPT OF RESPONSIBILITY ACCOUNTING............................................... 427CONTROLLABLE VERSUS NONCONTROLLABLE REVENUES AND COSTS.... 429RESPONSIBILITY REPORTING SYSTEM..................................................................... 430

TYPES OF RESPONSIBILITY CENTERS.......................................................................... 432RESPONSIBILITY ACCOUNTING FOR COST CENTERS......................................... 433RESPONSIBILITY ACCOUNTING FOR PROFIT CENTERS..................................... 434RESPONSIBILITY ACCOUNTING FOR INVESTMENT CENTERS......................... 437PRINCIPLES OF PERFORMANCE EVALUATION.................................................... 440

APPENDIX 7A RESIDUAL INCOME—ANOTHER PERFORMANCEMEASUREMENT.................................................................................................................... 446RESIDUAL INCOME COMPARED TOROI..................................................................... 447RESIDUAL INCOME WEAKNESS.................................................................................... 448SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 7A........................................... 449GLOSSARY.............................................................................................................................. 485

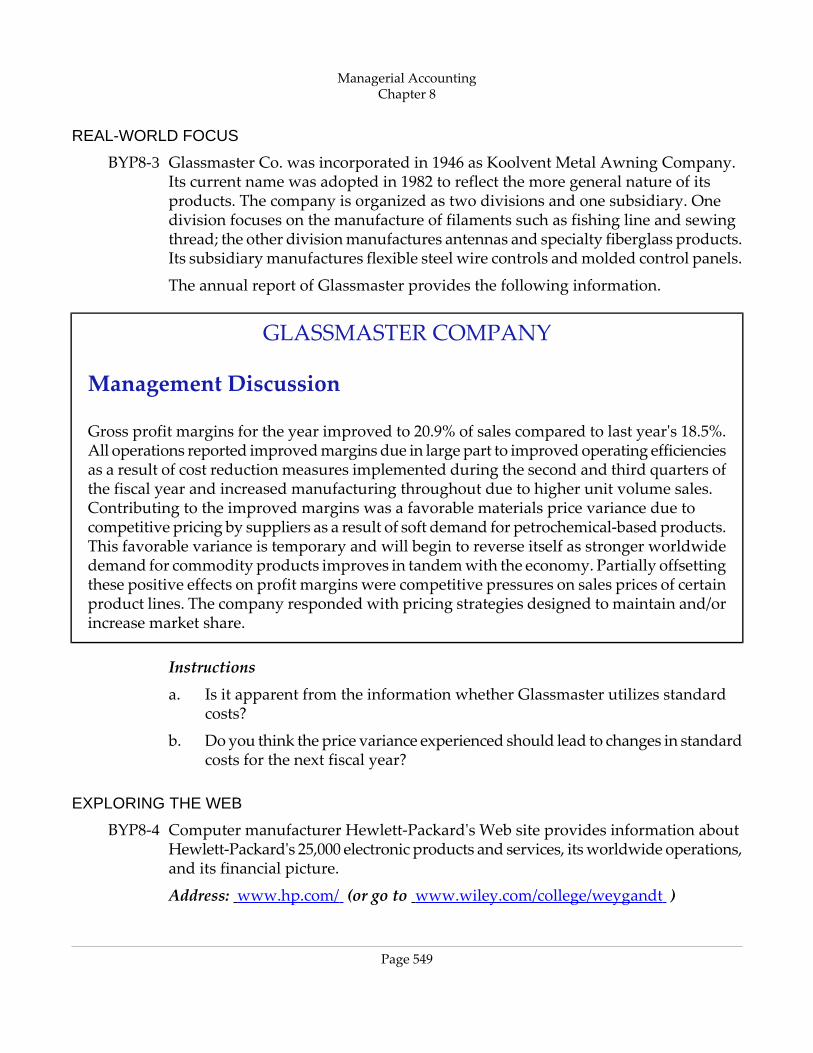

CHAPTER 8THE NEED FOR STANDARDS........................................................................................... 490

DISTINGUISHING BETWEEN STANDARDS AND BUDGETS............................... 491WHY STANDARD COSTS?............................................................................................. 491

Managerial AccountingTable of Contents

vi

SETTING STANDARD COSTS—A DIFFICULT TASK................................................ 492IDEAL VERSUS NORMAL STANDARDS.................................................................... 493A CASE STUDY................................................................................................................. 493

VARIANCES FROM STANDARDS................................................................................... 498ANALYZING VARIANCES............................................................................................. 499REPORTING VARIANCES.............................................................................................. 513STATEMENT PRESENTATION OF VARIANCES....................................................... 514

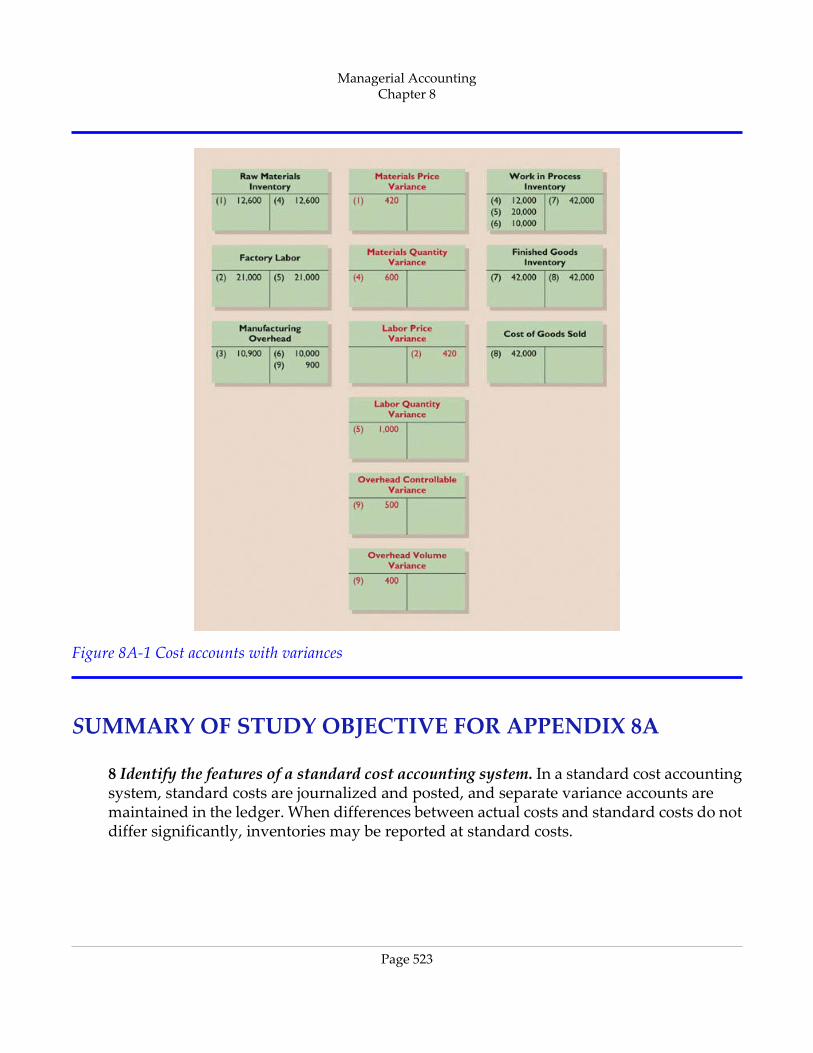

APPENDIX 8A STANDARD COST ACCOUNTING SYSTEM................................... 519JOURNAL ENTRIES.............................................................................................................. 520LEDGER ACCOUNTS........................................................................................................... 522SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 8A........................................... 523GLOSSARY.............................................................................................................................. 551

CHAPTER 9MANAGEMENT'S DECISION‐MAKING PROCESS.................................................... 557

INCREMENTAL ANALYSIS APPROACH................................................................... 557HOW INCREMENTAL ANALYSIS WORKS................................................................ 558

TYPES OF INCREMENTAL ANALYSIS........................................................................... 559ACCEPT AN ORDER AT A SPECIAL PRICE............................................................... 560MAKE OR BUY.................................................................................................................. 560SELL OR PROCESS FURTHER........................................................................................ 563RETAIN OR REPLACE EQUIPMENT........................................................................... 566ELIMINATE AN UNPROFITABLE SEGMENT............................................................ 567

SALES MIX.............................................................................................................................. 570BREAK‐EVEN SALES....................................................................................................... 570LIMITED RESOURCES..................................................................................................... 572

OTHER CONSIDERATIONS IN DECISION MAKING............................................... 574QUALITATIVE FACTORS............................................................................................... 574RELATIONSHIP OF INCREMENTAL ANALYSIS AND ACTIVITY‐BASED COSTING.5 7 5

GLOSSARY.............................................................................................................................. 604CHAPTER 10

THE CAPITAL BUDGETING EVALUATION PROCESS............................................. 611CASH FLOW INFORMATION....................................................................................... 612ILLUSTRATIVE DATA..................................................................................................... 613

CASH PAYBACK.................................................................................................................... 614NET PRESENT VALUE METHOD..................................................................................... 615

EQUAL ANNUAL CASH FLOWS.................................................................................. 616UNEQUAL ANNUAL CASH FLOWS........................................................................... 617CHOOSING A DISCOUNT RATE.................................................................................. 618SIMPLIFYING ASSUMPTIONS...................................................................................... 619COMPREHENSIVE EXAMPLE....................................................................................... 621

ADDITIONAL CONSIDERATIONS................................................................................. 622

Managerial AccountingTable of Contents

vii

INTANGIBLE BENEFITS................................................................................................. 622MUTUALLY EXCLUSIVE PROJECTS............................................................................ 624RISK ANALYSIS................................................................................................................ 626POST‐AUDIT OF INVESTMENT PROJECTS................................................................ 627

OTHER CAPITAL BUDGETING TECHNIQUES........................................................... 628INTERNAL RATE OF RETURN METHOD.................................................................. 628COMPARING DISCOUNTED CASH FLOW METHODS.......................................... 630ANNUAL RATE OF RETURN METHOD..................................................................... 631

GLOSSARY.............................................................................................................................. 660CHAPTER 11

SECTION 1 EXTERNAL SALES.......................................................................................... 666PRICING IN A COMPETITIVE MARKET....................................................................... 668COST‐PLUS PRICING.......................................................................................................... 669

LIMITATIONS OF COST‐PLUS PRICING.................................................................... 671TIME AND MATERIAL PRICING..................................................................................... 674SECTION 2 INTERNAL SALES.......................................................................................... 678NEGOTIATED TRANSFER PRICES.................................................................................. 680

NO EXCESS CAPACITY................................................................................................... 680EXCESS CAPACITY.......................................................................................................... 681VARIABLE COSTS............................................................................................................ 682SPECIAL ORDER............................................................................................................... 683SUMMARY OF NEGOTIATED TRANSFER PRICING APPROACH....................... 683

COST‐BASED TRANSFER PRICES................................................................................... 684MARKET‐BASED TRANSFER PRICES............................................................................. 685EFFECT OF OUTSOURCING ON TRANSFER PRICING............................................. 686TRANSFERS BETWEEN DIVISIONS IN DIFFERENT COUNTRIES........................ 686APPENDIX 11A OTHER COST APPROACHES TO PRICING.................................... 691ABSORPTION COST APPROACH.................................................................................... 691CONTRIBUTION (VARIABLE COST) APPROACH..................................................... 694SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 11A......................................... 696COMPREHENSIVE PROBLEM: CHAPTERS 1–11.......................................................... 723GLOSSARY.............................................................................................................................. 730

CHAPTER 12THE STATEMENT OF CASH FLOWS: PURPOSE AND FORMAT............................ 735

PURPOSE OF THE STATEMENT OF CASH FLOWS................................................. 736MEANING OF “CASH FLOWS”.................................................................................... 736CLASSIFICATION OF CASH FLOWS........................................................................... 737SIGNIFICANT NONCASH ACTIVITIES....................................................................... 738FORMAT OF THE STATEMENT OF CASH FLOWS.................................................. 740THE CORPORATE LIFE CYCLE..................................................................................... 741USEFULNESS OF THE STATEMENT OF CASH FLOWS.......................................... 743PREPARING THE STATEMENT OF CASH FLOWS................................................... 744

Managerial AccountingTable of Contents

viii

INDIRECT AND DIRECT METHODS........................................................................... 745SECTION 1 STATEMENT OF CASH FLOWS—INDIRECT METHOD..................... 747FIRST YEAR OF OPERATIONS—2002.............................................................................. 747

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 748STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 749STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 751STATEMENT OF CASH FLOWS—2002........................................................................ 752

SECOND YEAR OF OPERATIONS—2003........................................................................ 753STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 754STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 754STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 756STATEMENT OF CASH FLOWS—2003........................................................................ 758SUMMARY OF CONVERSION TO NET CASH PROVIDED BY OPERATINGACTIVITIES—INDIRECT METHOD............................................................................. 758

SECTION 1 STATEMENT OF CASH FLOWS—DIRECT METHOD.......................... 762FIRST YEAR OF OPERATIONS—2002.............................................................................. 762

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 764STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 764STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 769STATEMENT OF CASH FLOWS—2002........................................................................ 770

SECOND YEAR OF OPERATIONS—2003........................................................................ 771STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 772STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 772STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 775STATEMENT OF CASH FLOWS—2003........................................................................ 776

USING CASH FLOWS TO EVALUATE A COMPANY................................................. 779FREE CASH FLOW............................................................................................................ 779CAPITAL EXPENDITURE RATIO.................................................................................. 781ASSESSING LIQUIDITY, SOLVENCY, AND PROFITABILITY USINGCASH FLOWS.................................................................................................................... 782

GLOSSARY.............................................................................................................................. 836CHAPTER 13

EARNING POWER AND IRREGULAR ITEMS.............................................................. 842DISCONTINUED OPERATIONS.................................................................................... 843

Managerial AccountingTable of Contents

ix

EXTRAORDINARY ITEMS.............................................................................................. 844CHANGES IN ACCOUNTING PRINCIPLE................................................................. 847COMPREHENSIVE INCOME......................................................................................... 849

COMPARATIVE ANALYSIS............................................................................................... 849HORIZONTAL ANALYSIS.............................................................................................. 851VERTICAL ANALYSIS..................................................................................................... 855

RATIO ANALYSIS................................................................................................................. 859LIQUIDITY RATIOS.......................................................................................................... 862SOLVENCY RATIOS......................................................................................................... 867PROFITABILITY RATIOS................................................................................................. 870

LIMITATIONS OF FINANCIAL ANALYSIS................................................................... 878ESTIMATES........................................................................................................................ 878COST....ū 878ALTERNATIVE ACCOUNTING METHODS............................................................... 879ATYPICAL DATA............................................................................................................. 879DIVERSIFICATION........................................................................................................... 879

GLOSSARY.............................................................................................................................. 931APPENDIX A

THE ANNUAL REPORT....................................................................................................... 935FINANCIAL HIGHLIGHTS................................................................................................. 936

Corporate Principles ......................................................................................................... 936Corporate Profile ............................................................................................................... 937

LETTER TO THE STOCKHOLDERS................................................................................. 937To Our Shareholders ........................................................................................................ 937Operating Report .............................................................................................................. 939

MANAGEMENT DISCUSSION AND ANALYSIS........................................................ 942Management's Discussion and Analysis of Financial Condition and Results ofOperations .......................................................................................................................... 942

FINANCIAL STATEMENTS AND ACCOMPANYING NOTES................................. 948Notes to Consolidated Financial Statements ................................................................ 953

AUDITOR'S REPORT............................................................................................................ 966Report of Independent Accountants .............................................................................. 967

SUPPLEMENTARY FINANCIAL INFORMATION....................................................... 967APPENDIX BAPPENDIX C

NATURE OF INTEREST....................................................................................................... 977SIMPLE INTEREST............................................................................................................ 978COMPOUND INTEREST................................................................................................. 978

SECTION 1 FUTURE VALUE CONCEPTS....................................................................... 979FUTURE VALUE OF A SINGLE AMOUNT..................................................................... 979FUTURE VALUE OF AN ANNUITY.................................................................................. 982SECTION 2 PRESENT VALUE CONCEPTS..................................................................... 985

Managerial AccountingTable of Contents

x

PRESENT VALUE VARIABLES.......................................................................................... 985PRESENT VALUE OF A SINGLE AMOUNT................................................................... 985PRESENT VALUE OF AN ANNUITY................................................................................ 988TIME PERIODS AND DISCOUNTING............................................................................ 991COMPUTING THE PRESENT VALUES IN A CAPITAL BUDGETINGDECISIONū 991GLOSSARY............................................................................................................................ 1000

APPENDIX DETHICAL BEHAVIOR FOR PRACTITIONERS OF MANAGEMENT ACCOUNTINGAND FINANCIAL MANAGEMENT............................................................................... 1001STANDARDS OF ETHICAL CONDUCT FOR PRACTITIONERS OF MANAGEMENTACCOUNTING AND FINANCIAL MANAGEMENT................................................. 1002

COMPETENCE................................................................................................................ 1002CONFIDENTIALITY....................................................................................................... 1002INTEGRITY....................................................................................................................... 1003OBJECTIVITY................................................................................................................... 1003RESOLUTION OF ETHICAL CONFLICT................................................................... 1003

AFTERWORDCASE‐1....ū 1007CARD‐MART SWIMS IN THE DOT‐COM SEA: JOB ORDER COSTING............. 1007

THE BUSINESS SITUATION......................................................................................... 1007CASE‐2....ū 1010CARD‐MART SWIMS IN THE DOT‐COM SEA: ACTIVITY‐BASED COSTING.. 1010

THE BUSINESS SITUATION......................................................................................... 1011CASE‐3....ū 1016CARD‐MART SWIMS IN THE DOT‐COM SEA: CAPITAL BUDGETING............ 1016

THE BUSINESS SITUATION......................................................................................... 1016CASE‐4....ū 1019CARD‐MART SWIMS IN THE DOT‐COM SEA: TRANSFER PRICING ISSUES. 1019

THE BUSINESS SITUATION......................................................................................... 1019CASE‐5....ū 1022RICHLAND CIRCULAR CLUB PRO RODEO ROUNDUP......................................... 1022

THE BUSINESS SITUATION......................................................................................... 1022

Managerial AccountingTable of Contents

xi

Managerial AccountingTable of Contents

xii

Chapter 8

Performance Evaluation Through Standard Costs

Navigator

• Scan Study Objectives

• Read Feature Story

• Read Preview

• Read text and answer Before You Go On

p. 327 □ p. 332 □ p. 341 □

• Work Using the Decision Toolkit

• Review Summary of Study Objectives

• Work Demonstration Problem

• Answer Self‐Study Questions

• Complete Assignments

Managerial AccountingChapter 8

Page 487

STUDY OBJECTIVES

After studying this chapter, you should be able to:

1. Distinguish between a standard and a budget.

2. Identify the advantages of standard costs.

3. Describe how standards are set.

4. State the formulas for determining direct materials and direct labor variances.

5. State the formulas for determining manufacturing overhead variances.

6. Discuss the reporting of variances.

7. Prepare an income statement for management under a standard costing system.

Managerial AccountingChapter 8

Page 488

Feature Story

HIGHLIGHTING PERFORMANCE EFFICIENCY

There's a very good chance that the highlighter you're holding in your hand was made bySanford, a maker of permanent markers and other writing instruments. Sanford,headquartered in Illinois, annually sells hundreds of millions of dollars' worth of ACCENThighlighters, fine‐point pens, Sharpie permanent markers, Expo dry‐erase markers foroverhead projectors, and other writing instruments.

Since Sanford makes literally billions of writing utensils per year, the company must keeptight control over manufacturing costs. A very important part of Sanford's manufacturingprocess is determining how much direct materials, labor, and overhead should cost. Thesecosts are then compared to actual costs to assess performance efficiency. Raw materials forSanford's markers include a barrel, plug, cap, ink reservoir, and a nib (tip). These parts areassembled by machine to produce thousands of units per hour. A major component ofmanufacturing overhead is machine maintenance—some fixed, some variable.

“Labor costs are associated with material handling and equipment maintenance functions.Although the assembly process is highly automated, labor is still required to move raw

Managerial AccountingChapter 8

Page 489

materials to the machine and to package the finished product. In addition, highly skilledtechnicians are required to service and maintain each piece of equipment,” says Mike Orr,vice president, operations.

Labor rates are predictable because the hourly workers are covered by a union contract. Thestory is the same with the fringe benefits and some supervisory salaries. Even volume levelsare fairly predictable—demand for the product is high—so fixed overhead is efficientlyabsorbed. Raw material standard costs are based on the previous year's actual prices plusany anticipated inflation. Lately, though, inflation has been so low that the company isconsidering any price increase in raw material to be unfavorable because its standards willremain unchanged.

PREVIEW OF CHAPTER 8

Standards are a fact of life. You met the admission standards for the school you are attending.The vehicle that you drive had to meet certain governmental emissions standards. Thehamburgers and salads you eat in a restaurant have to meet certain health and nutritionalstandards before they can be sold. And, as described in our Feature Story, Sanford Corp.develops standards for the costs of its materials, labor, and overhead which it compares withits actual costs. The reason for standards in these cases is very simple: They help to ensurethat overall product quality is high. Without standards, quality control is lost.

In this chapter we continue the study of controlling costs. You will learn how to developstandard costs that permit the evaluation of performance.

The content and organization of Chapter 8 are as follows.

THE NEED FOR STANDARDS

Standards are common in business. Those imposed by government agencies are often calledregulations. They include the Fair Labor Standards Act, the Equal Employment Opportunity

Managerial AccountingChapter 8

Page 490

Act, and a multitude of environmental standards. Standards established internally by a companymay extend to personnel matters, such as employee absenteeism and ethical codes of conduct,quality control standards for products, and standard costs for goods and services. In managerialaccounting, standard costs are predetermined unit costs, which are used as measures ofperformance.

We will focus on manufacturing operations in the remainder of this chapter. But you should alsorecognize that standard costs also apply to many types of service businesses as well. For example,a fast‐food restaurant such as McDonald's knows the price it should pay for pickles, beef, buns,and other ingredients. It also knows how much time it should take an employee to flip hamburgers.If too much is paid for pickles or too much time is taken to prepare Big Macs, the deviations arenoticed and corrective action is taken. Standard costs also may be used in not‐for‐profit enterprisessuch as universities, charitable organizations, and governmental agencies.

DISTINGUISHING BETWEEN STANDARDS AND BUDGETS

In concept, standards and budgets are essentially the same. Both are predetermined costs, andboth contribute to management planning and control. There is a difference, however, in the waythe terms are expressed. A standard is a unit amount. A budget is a total amount. Thus, it iscustomary to state that the standard cost of direct labor for a unit of product is $10. If 5,000 unitsof the product are produced, the $50,000 of direct labor is the budgeted labor cost. A standardis the budgeted cost per unit of product. A standard is therefore concerned with each individualcost component that makes up the entire budget.

There are important accounting differences between budgets and standards. Except in theapplication of manufacturing overhead to jobs and processes, budget data are not journalizedin cost accounting systems. In contrast, as will be illustrated in the appendix to this chapter,standard costs may be incorporated into cost accounting systems. Also, a company may reportits inventories at standard cost in its financial statements, but it would not report inventories atbudgeted costs.

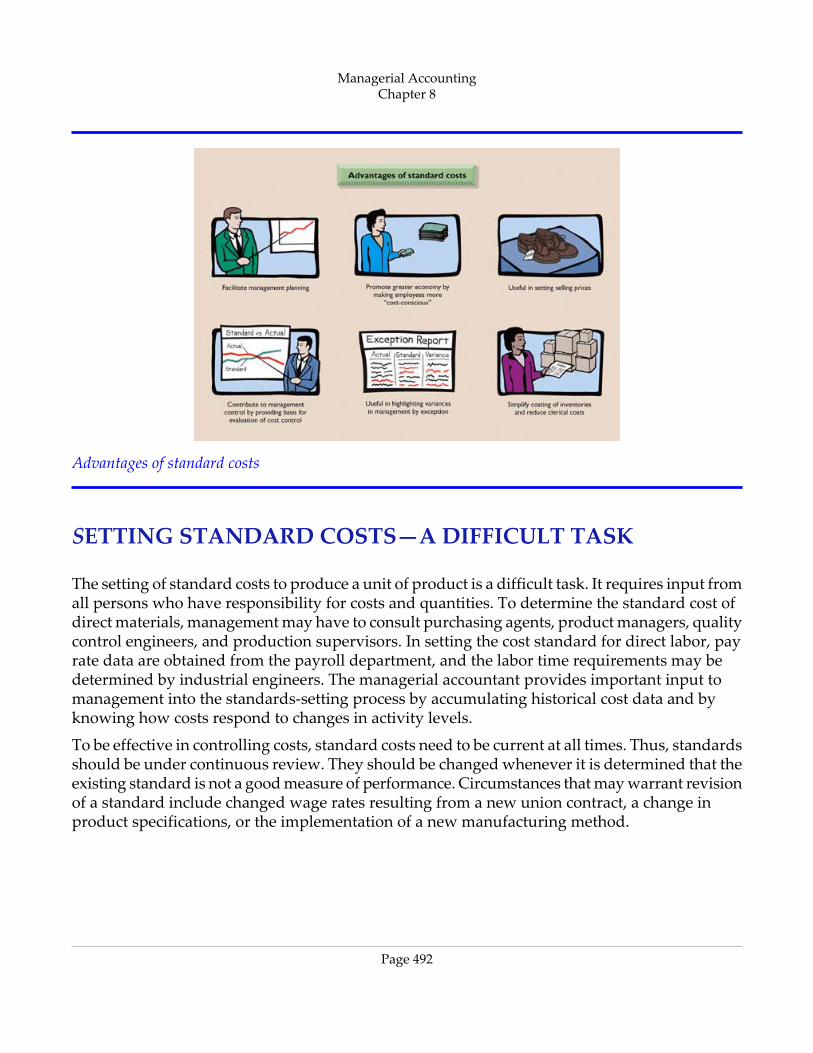

WHY STANDARD COSTS?

Standard costs offer a number of advantages to an organization, as shown in Illustration 1. Theseadvantages will be realized only when standard costs are carefully established and prudentlyused. Using standards solely as a means of placing blame can have a negative effect on managersand employees. In an effort to minimize this effect, many companies offer wage incentives tothose who meet their standards.

Managerial AccountingChapter 8

Page 491

Advantages of standard costs

SETTING STANDARD COSTS—A DIFFICULT TASK

The setting of standard costs to produce a unit of product is a difficult task. It requires input fromall persons who have responsibility for costs and quantities. To determine the standard cost ofdirect materials, management may have to consult purchasing agents, product managers, qualitycontrol engineers, and production supervisors. In setting the cost standard for direct labor, payrate data are obtained from the payroll department, and the labor time requirements may bedetermined by industrial engineers. The managerial accountant provides important input tomanagement into the standards‐setting process by accumulating historical cost data and byknowing how costs respond to changes in activity levels.

To be effective in controlling costs, standard costs need to be current at all times. Thus, standardsshould be under continuous review. They should be changed whenever it is determined that theexisting standard is not a good measure of performance. Circumstances that may warrant revisionof a standard include changed wage rates resulting from a new union contract, a change inproduct specifications, or the implementation of a new manufacturing method.

Managerial AccountingChapter 8

Page 492

IDEAL VERSUS NORMAL STANDARDS

Standards may be set at one of two levels: ideal or normal. Ideal standards represent optimumlevels of performance under perfect operating conditions. Normal standards represent efficientlevels of performance that are attainable under expected operating conditions.

Some managers believe ideal standards will stimulate workers to ever‐increasing improvement.However, most managers believe that ideal standards lower the morale of the entire workforcebecause they are so difficult, if not impossible, to meet. Very few companies use ideal standards.

Most companies that use standards set them at a normal level. Properly set, normal standardsshould be rigorous but attainable. Normal standards allow for rest periods, machine breakdowns,and other “normal” contingencies in the production process. It will be assumed in the remainderof this chapter that standard costs are set at a normal level.

A CASE STUDY

To establish the standard cost of producing a product, it is necessary to establish standards foreach manufacturing cost element—direct materials, direct labor, and manufacturing overhead.The standard for each element is derived from the standard price to be paid and the standardquantity to be used. To illustrate, we will look at a case study of how standard costs are set. Inthis extended example, we will assume that Xonic, Inc. wishes to use standard costs to measureperformance in filling an order for 1,000 gallons of Weed‐O, a liquid weed killer.

Direct Materials

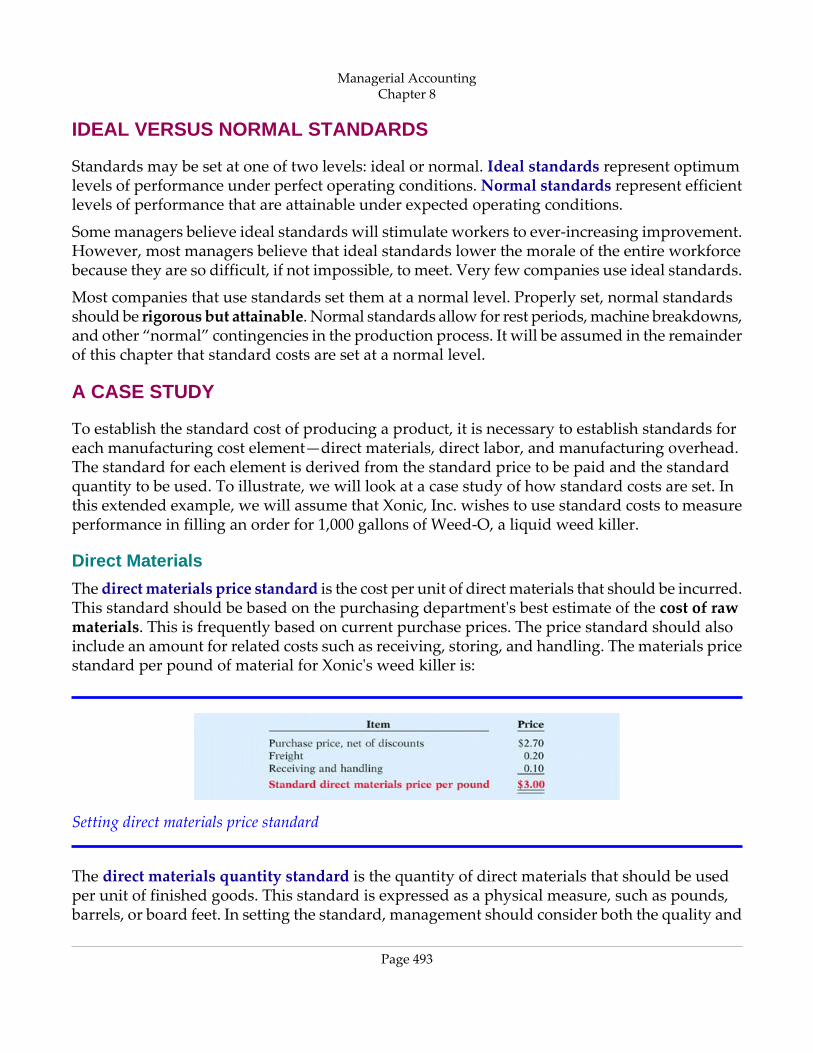

The direct materials price standard is the cost per unit of direct materials that should be incurred.This standard should be based on the purchasing department's best estimate of the cost of rawmaterials. This is frequently based on current purchase prices. The price standard should alsoinclude an amount for related costs such as receiving, storing, and handling. The materials pricestandard per pound of material for Xonic's weed killer is:

Setting direct materials price standard

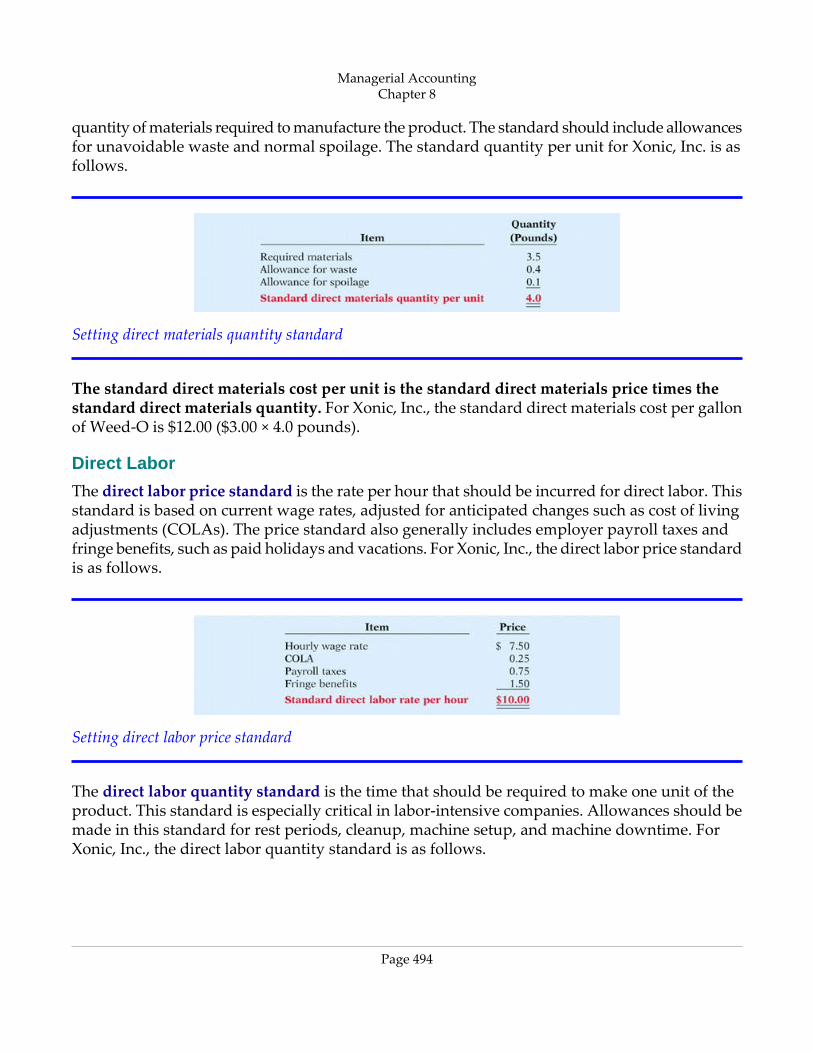

The direct materials quantity standard is the quantity of direct materials that should be usedper unit of finished goods. This standard is expressed as a physical measure, such as pounds,barrels, or board feet. In setting the standard, management should consider both the quality and

Managerial AccountingChapter 8

Page 493

quantity of materials required to manufacture the product. The standard should include allowancesfor unavoidable waste and normal spoilage. The standard quantity per unit for Xonic, Inc. is asfollows.

Setting direct materials quantity standard

The standard direct materials cost per unit is the standard direct materials price times thestandard direct materials quantity. For Xonic, Inc., the standard direct materials cost per gallonof Weed‐O is $12.00 ($3.00 × 4.0 pounds).

Direct Labor

The direct labor price standard is the rate per hour that should be incurred for direct labor. Thisstandard is based on current wage rates, adjusted for anticipated changes such as cost of livingadjustments (COLAs). The price standard also generally includes employer payroll taxes andfringe benefits, such as paid holidays and vacations. For Xonic, Inc., the direct labor price standardis as follows.

Setting direct labor price standard

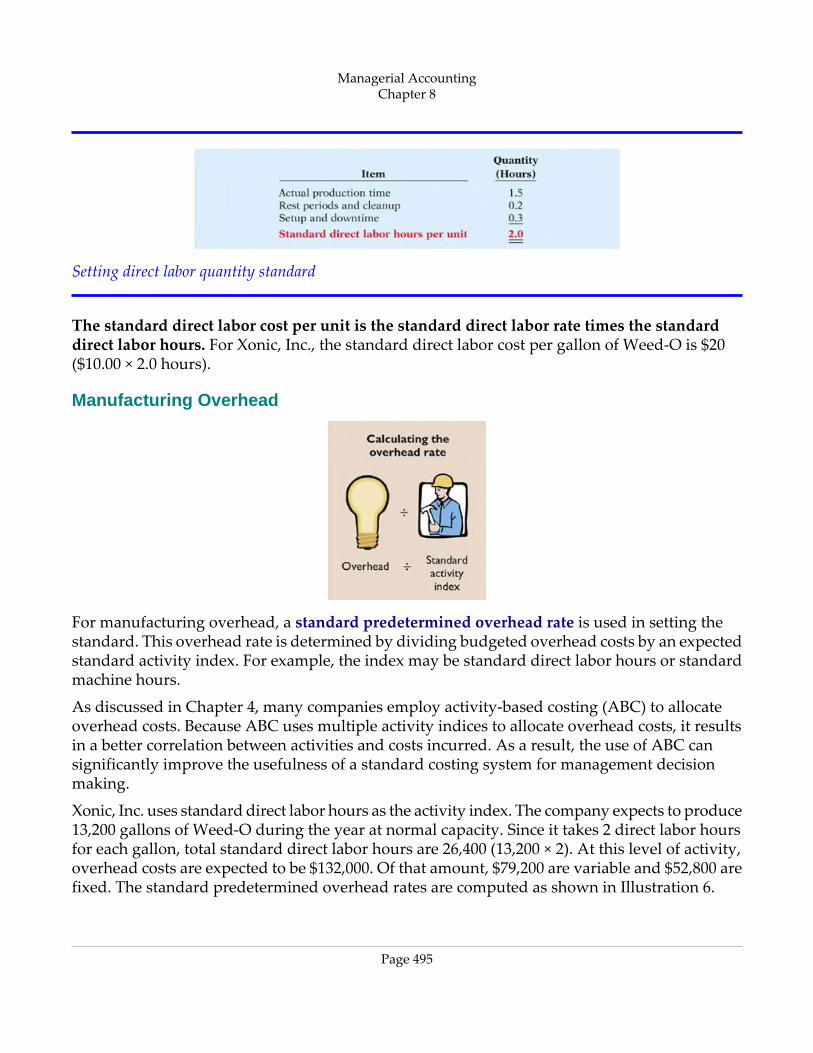

The direct labor quantity standard is the time that should be required to make one unit of theproduct. This standard is especially critical in labor‐intensive companies. Allowances should bemade in this standard for rest periods, cleanup, machine setup, and machine downtime. ForXonic, Inc., the direct labor quantity standard is as follows.

Managerial AccountingChapter 8

Page 494

Setting direct labor quantity standard

The standard direct labor cost per unit is the standard direct labor rate times the standarddirect labor hours. For Xonic, Inc., the standard direct labor cost per gallon of Weed‐O is $20($10.00 × 2.0 hours).

Manufacturing Overhead

For manufacturing overhead, a standard predetermined overhead rate is used in setting thestandard. This overhead rate is determined by dividing budgeted overhead costs by an expectedstandard activity index. For example, the index may be standard direct labor hours or standardmachine hours.

As discussed in Chapter 4, many companies employ activity‐based costing (ABC) to allocateoverhead costs. Because ABC uses multiple activity indices to allocate overhead costs, it resultsin a better correlation between activities and costs incurred. As a result, the use of ABC cansignificantly improve the usefulness of a standard costing system for management decisionmaking.

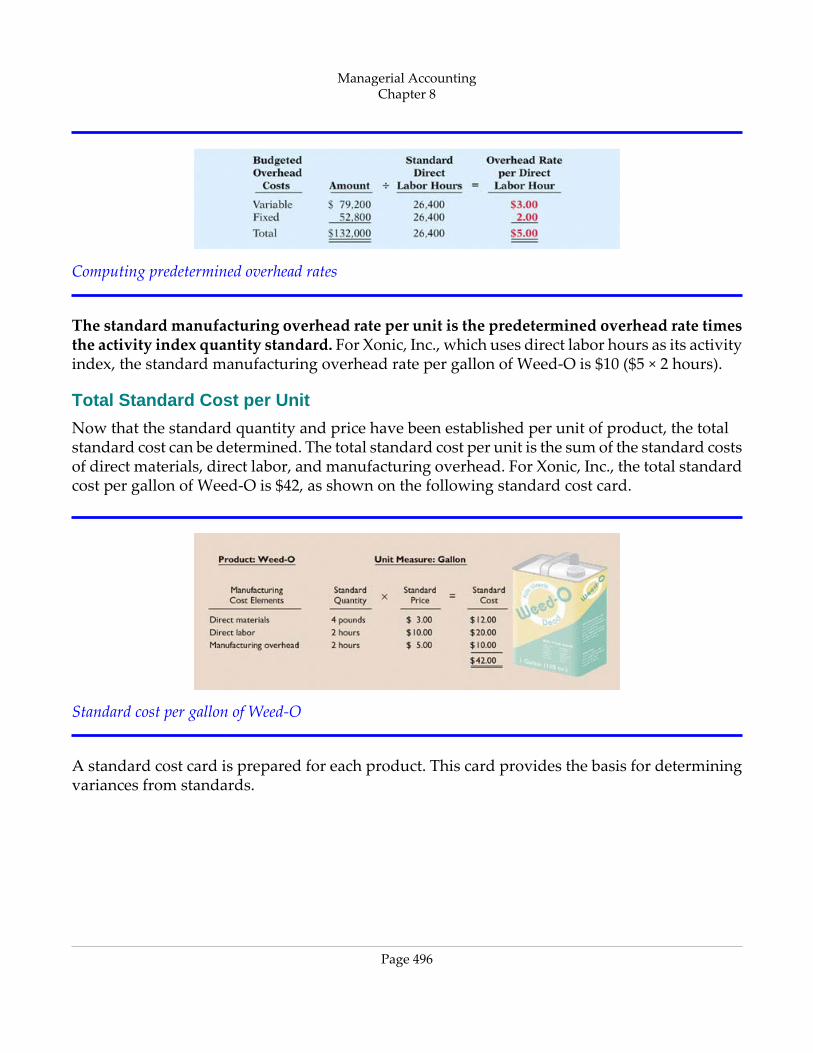

Xonic, Inc. uses standard direct labor hours as the activity index. The company expects to produce13,200 gallons of Weed‐O during the year at normal capacity. Since it takes 2 direct labor hoursfor each gallon, total standard direct labor hours are 26,400 (13,200 × 2). At this level of activity,overhead costs are expected to be $132,000. Of that amount, $79,200 are variable and $52,800 arefixed. The standard predetermined overhead rates are computed as shown in Illustration 6.

Managerial AccountingChapter 8

Page 495

Computing predetermined overhead rates

The standard manufacturing overhead rate per unit is the predetermined overhead rate timesthe activity index quantity standard. For Xonic, Inc., which uses direct labor hours as its activityindex, the standard manufacturing overhead rate per gallon of Weed‐O is $10 ($5 × 2 hours).

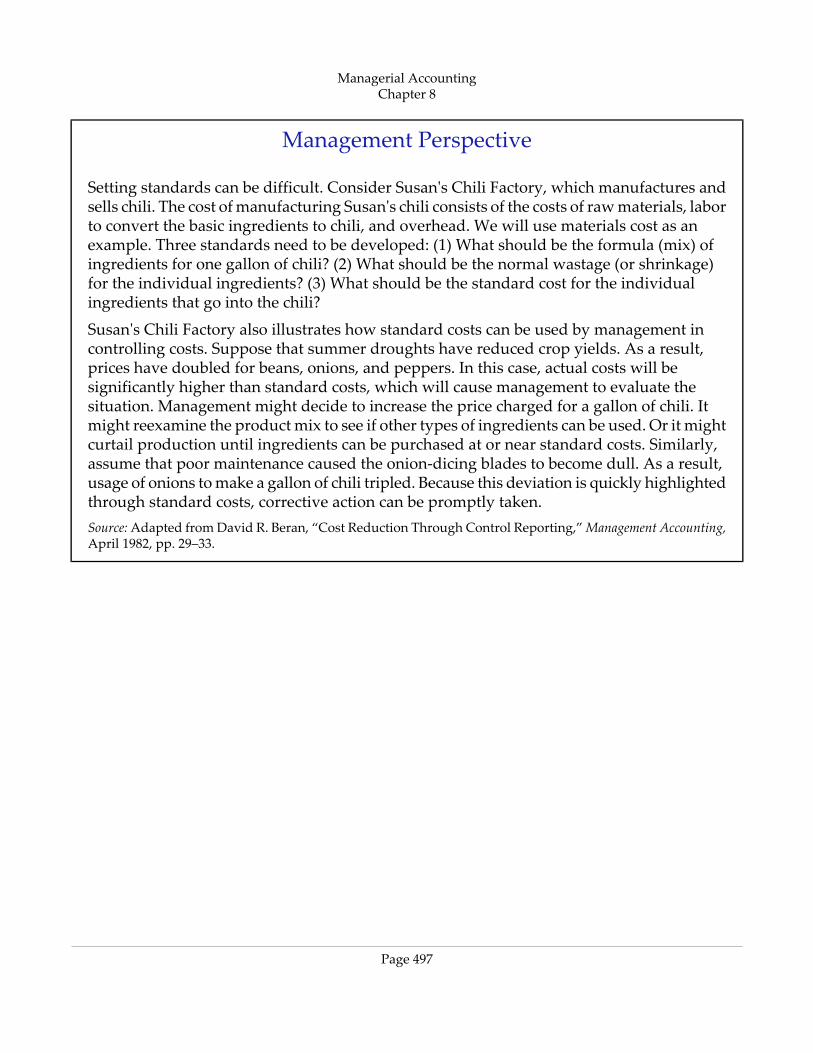

Total Standard Cost per Unit

Now that the standard quantity and price have been established per unit of product, the totalstandard cost can be determined. The total standard cost per unit is the sum of the standard costsof direct materials, direct labor, and manufacturing overhead. For Xonic, Inc., the total standardcost per gallon of Weed‐O is $42, as shown on the following standard cost card.

Standard cost per gallon of Weed‐O

A standard cost card is prepared for each product. This card provides the basis for determiningvariances from standards.

Managerial AccountingChapter 8

Page 496

Management Perspective

Setting standards can be difficult. Consider Susan's Chili Factory, which manufactures andsells chili. The cost of manufacturing Susan's chili consists of the costs of raw materials, laborto convert the basic ingredients to chili, and overhead. We will use materials cost as anexample. Three standards need to be developed: (1) What should be the formula (mix) ofingredients for one gallon of chili? (2) What should be the normal wastage (or shrinkage)for the individual ingredients? (3) What should be the standard cost for the individualingredients that go into the chili?

Susan's Chili Factory also illustrates how standard costs can be used by management incontrolling costs. Suppose that summer droughts have reduced crop yields. As a result,prices have doubled for beans, onions, and peppers. In this case, actual costs will besignificantly higher than standard costs, which will cause management to evaluate thesituation. Management might decide to increase the price charged for a gallon of chili. Itmight reexamine the product mix to see if other types of ingredients can be used. Or it mightcurtail production until ingredients can be purchased at or near standard costs. Similarly,assume that poor maintenance caused the onion‐dicing blades to become dull. As a result,usage of onions to make a gallon of chili tripled. Because this deviation is quickly highlightedthrough standard costs, corrective action can be promptly taken.Source: Adapted from David R. Beran, “Cost Reduction Through Control Reporting,” Management Accounting,April 1982, pp. 29–33.

Managerial AccountingChapter 8

Page 497

Before You Go On...

Review It

1. How do standards differ from budgets?

2. What are the advantages of standard costs to an organization?

3. Distinguish between normal standards and ideal standards. Which standard is morewidely used? Why?

Do It

1. The management of Arapahoe Company has decided to use standard costs.Management asks you to explain the components used in setting the standard costper unit for direct materials, direct labor, and manufacturing overhead.

Action Plan

• Differentiate between the two components of each standard: price and quantity.

Related exercise material: BE8‐2, BE8‐3, and E8‐1.

VARIANCES FROM STANDARDS

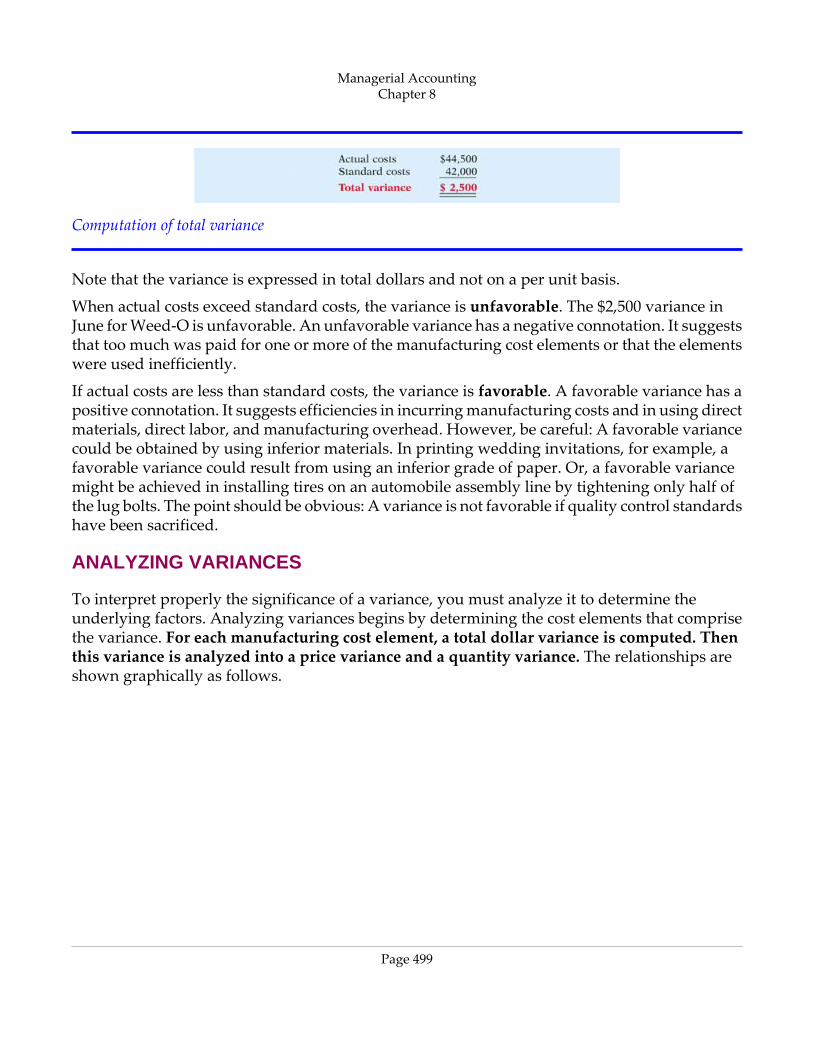

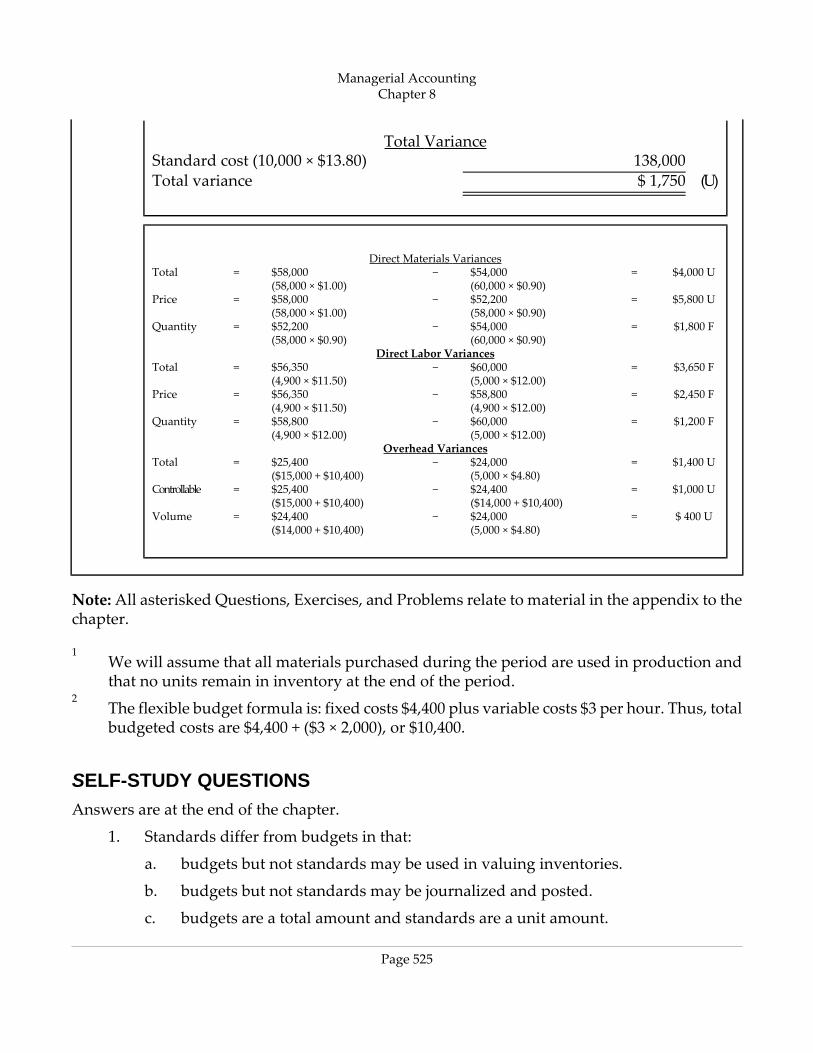

One of the major management uses of standard costs is to identify variances from standards.Variances are the differences between total actual costs and total standard costs. To illustrate,we will assume that in producing 1,000 gallons of Weed‐O in the month of June, Xonic, Inc.incurred the following costs.

Actual production costs

Total standard costs are determined by multiplying the units produced by the standard cost perunit. The total standard cost of Weed‐O is $42,000 (1,000 gallons × $42). Thus, the total varianceis $2,500, as shown below.

Managerial AccountingChapter 8

Page 498

Computation of total variance

Note that the variance is expressed in total dollars and not on a per unit basis.

When actual costs exceed standard costs, the variance is unfavorable. The $2,500 variance inJune for Weed‐O is unfavorable. An unfavorable variance has a negative connotation. It suggeststhat too much was paid for one or more of the manufacturing cost elements or that the elementswere used inefficiently.

If actual costs are less than standard costs, the variance is favorable. A favorable variance has apositive connotation. It suggests efficiencies in incurring manufacturing costs and in using directmaterials, direct labor, and manufacturing overhead. However, be careful: A favorable variancecould be obtained by using inferior materials. In printing wedding invitations, for example, afavorable variance could result from using an inferior grade of paper. Or, a favorable variancemight be achieved in installing tires on an automobile assembly line by tightening only half ofthe lug bolts. The point should be obvious: A variance is not favorable if quality control standardshave been sacrificed.

ANALYZING VARIANCES

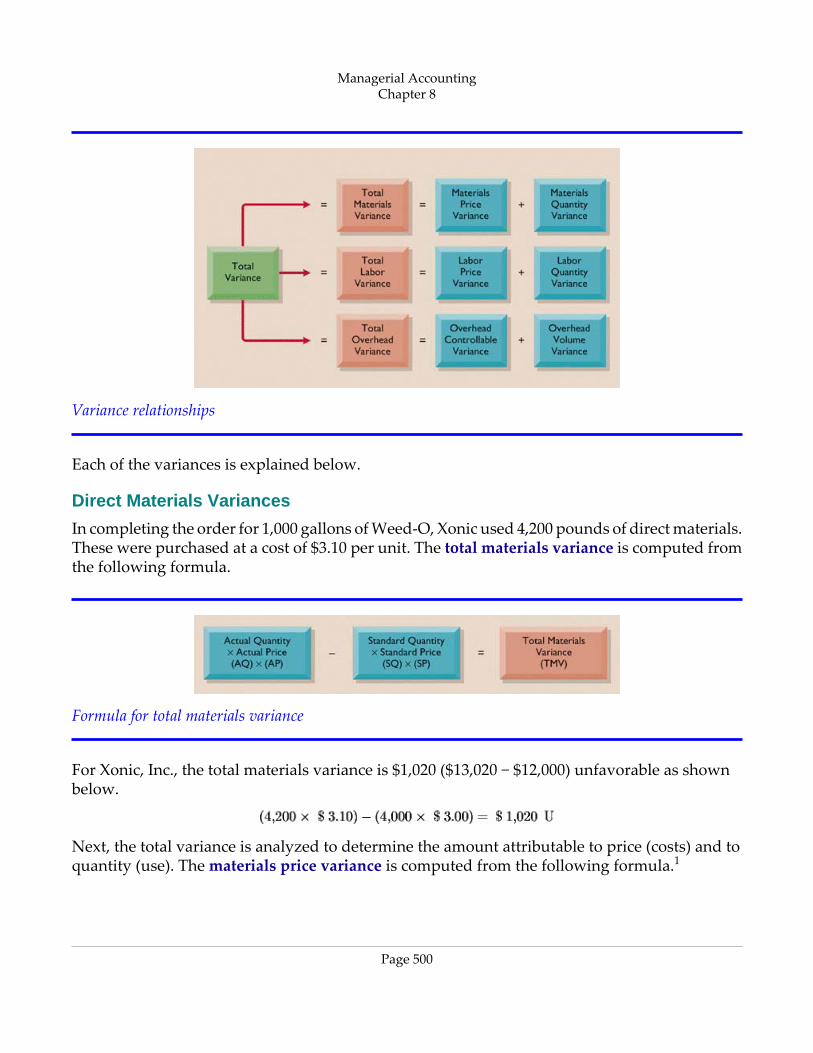

To interpret properly the significance of a variance, you must analyze it to determine theunderlying factors. Analyzing variances begins by determining the cost elements that comprisethe variance. For each manufacturing cost element, a total dollar variance is computed. Thenthis variance is analyzed into a price variance and a quantity variance. The relationships areshown graphically as follows.

Managerial AccountingChapter 8

Page 499

Variance relationships

Each of the variances is explained below.

Direct Materials Variances

In completing the order for 1,000 gallons of Weed‐O, Xonic used 4,200 pounds of direct materials.These were purchased at a cost of $3.10 per unit. The total materials variance is computed fromthe following formula.

Formula for total materials variance

For Xonic, Inc., the total materials variance is $1,020 ($13,020 − $12,000) unfavorable as shownbelow.

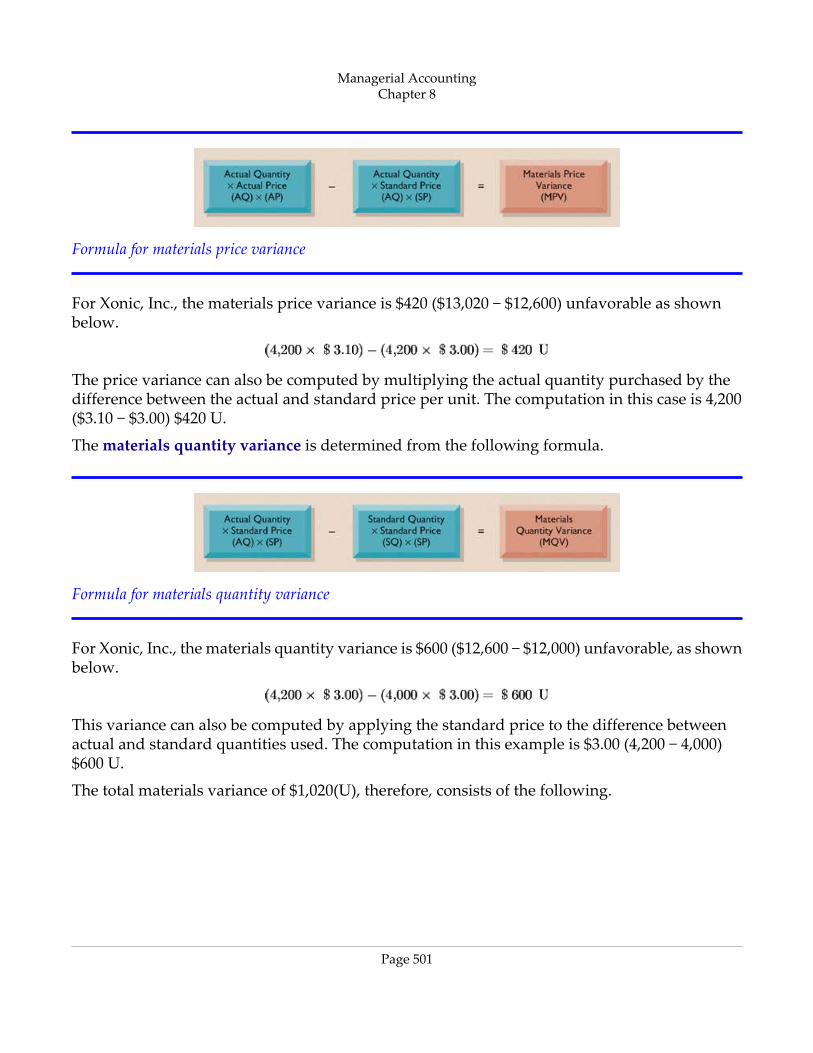

Next, the total variance is analyzed to determine the amount attributable to price (costs) and toquantity (use). The materials price variance is computed from the following formula.1

Managerial AccountingChapter 8

Page 500

Formula for materials price variance

For Xonic, Inc., the materials price variance is $420 ($13,020 − $12,600) unfavorable as shownbelow.

The price variance can also be computed by multiplying the actual quantity purchased by thedifference between the actual and standard price per unit. The computation in this case is 4,200($3.10 − $3.00) $420 U.

The materials quantity variance is determined from the following formula.

Formula for materials quantity variance

For Xonic, Inc., the materials quantity variance is $600 ($12,600 − $12,000) unfavorable, as shownbelow.

This variance can also be computed by applying the standard price to the difference betweenactual and standard quantities used. The computation in this example is $3.00 (4,200 − 4,000)$600 U.

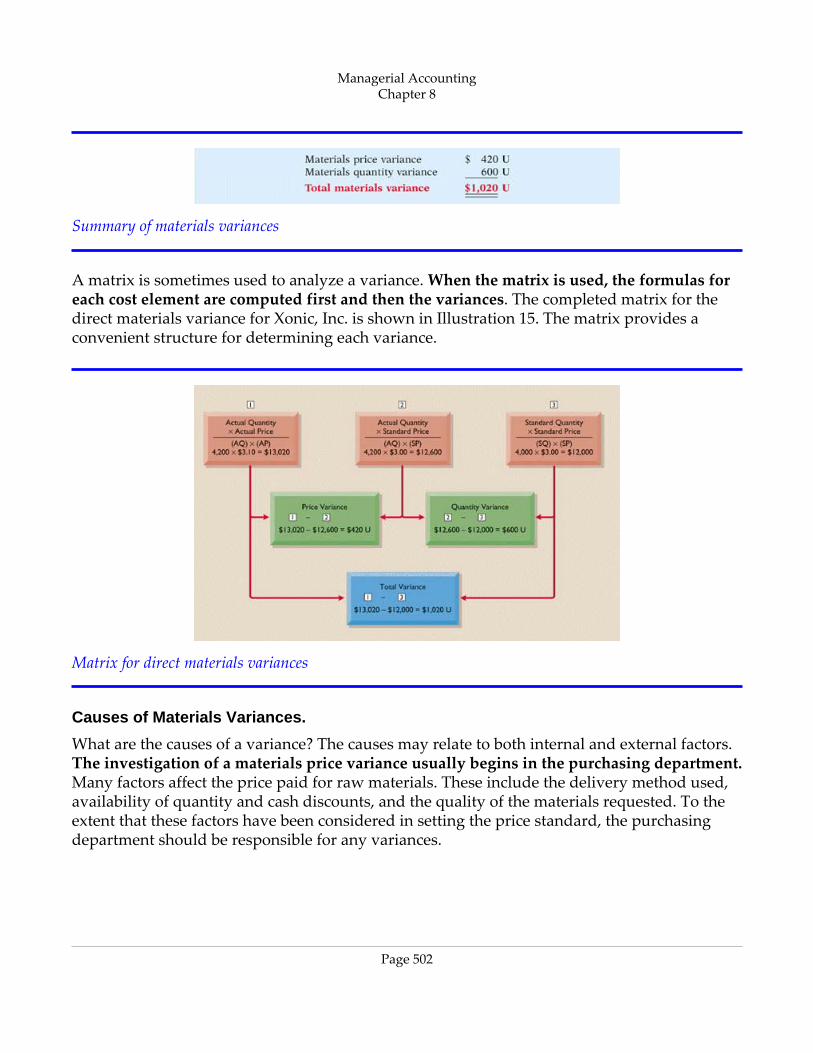

The total materials variance of $1,020(U), therefore, consists of the following.

Managerial AccountingChapter 8

Page 501

Summary of materials variances

A matrix is sometimes used to analyze a variance. When the matrix is used, the formulas foreach cost element are computed first and then the variances. The completed matrix for thedirect materials variance for Xonic, Inc. is shown in Illustration 15. The matrix provides aconvenient structure for determining each variance.

Matrix for direct materials variances

Causes of Materials Variances.

What are the causes of a variance? The causes may relate to both internal and external factors.The investigation of a materials price variance usually begins in the purchasing department.Many factors affect the price paid for raw materials. These include the delivery method used,availability of quantity and cash discounts, and the quality of the materials requested. To theextent that these factors have been considered in setting the price standard, the purchasingdepartment should be responsible for any variances.

Managerial AccountingChapter 8

Page 502

However, a variance may be beyond the control of the purchasing department. Sometimes, forexample, prices may rise faster than expected. Moreover, actions by groups over which thecompany has no control, such as the OPEC nations' oil price increases, may cause an unfavorablevariance. There are also times when a production department may be responsible for the pricevariance. This may occur when a rush order forces the company to pay a higher price for thematerials.

The starting point for determining the cause(s) of an unfavorable materials quantity variance isin the production department. If the variances are due to inexperienced workers, faulty machinery,or carelessness, the production department would be responsible. However, if the materialsobtained by the purchasing department were of inferior quality, then the purchasing departmentshould be responsible.

Management Perspective

If purchase price variances are used as a basis for measuring performance, purchasingdepartments often will continually search for the lowest‐cost item. However, this basis canbecome counterproductive if it leads to late deliveries of the goods or the purchase ofinferior‐quality goods.

Managerial AccountingChapter 8

Page 503

Before You Go On...

Review It

1. What are the three main components of the total variance from standard cost?

2. What are the formulas for computing the total, price, and quantity variances fordirect materials?

Do It

1. The standard cost of Product XX includes two units of direct materials at $8.00 perunit. During July, 22,000 units of direct materials are purchased at $7.50 and usedto produce 10,000 units. Compute the total, price, and quantity variances for materials.

Action Plan

Use the formulas for computing each of the materials variances:

•

•

•

Related exercise material: BE8‐4, BE8‐5, BE8‐6, BE8‐7, BE8‐8, E8‐2, E8‐3, E8‐4, E8‐6, E8‐7, E8‐8,E8‐9, and E8‐12.

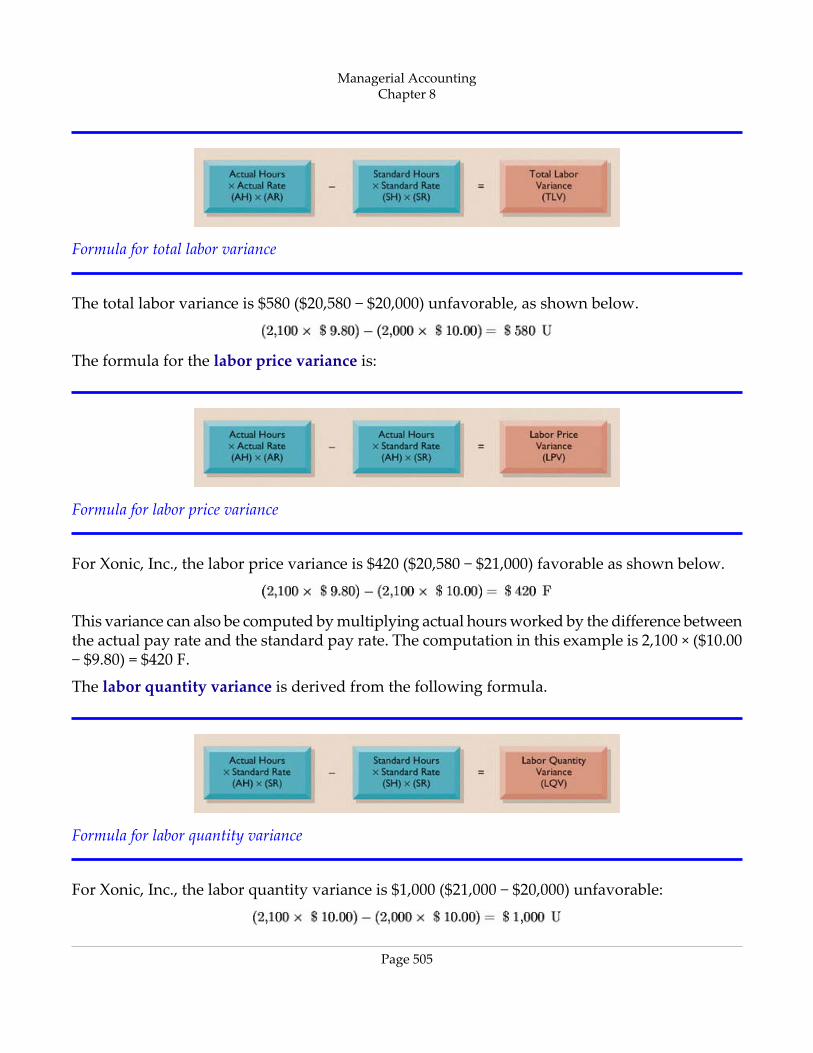

Direct Labor Variances

The process of determining direct labor variances is the same as for determining the directmaterials variances. In completing the Weed‐O order, Xonic, Inc. incurred 2,100 direct labor hoursat an average hourly rate of $9.80. The standard hours allowed for the units produced were 2,000hours (1,000 units × 2 hours). The standard labor rate was $10 per hour. The total labor varianceis obtained from the following formula.

Managerial AccountingChapter 8

Page 504

Formula for total labor variance

The total labor variance is $580 ($20,580 − $20,000) unfavorable, as shown below.

The formula for the labor price variance is:

Formula for labor price variance

For Xonic, Inc., the labor price variance is $420 ($20,580 − $21,000) favorable as shown below.

This variance can also be computed by multiplying actual hours worked by the difference betweenthe actual pay rate and the standard pay rate. The computation in this example is 2,100 × ($10.00− $9.80) = $420 F.

The labor quantity variance is derived from the following formula.

Formula for labor quantity variance

For Xonic, Inc., the labor quantity variance is $1,000 ($21,000 − $20,000) unfavorable:

Managerial AccountingChapter 8

Page 505

The same result can be obtained by multiplying the standard rate by the difference betweenactual hours worked and standard hours allowed. In this case the computation is $10.00 × (2,100− 2,000) = $1,000 U.

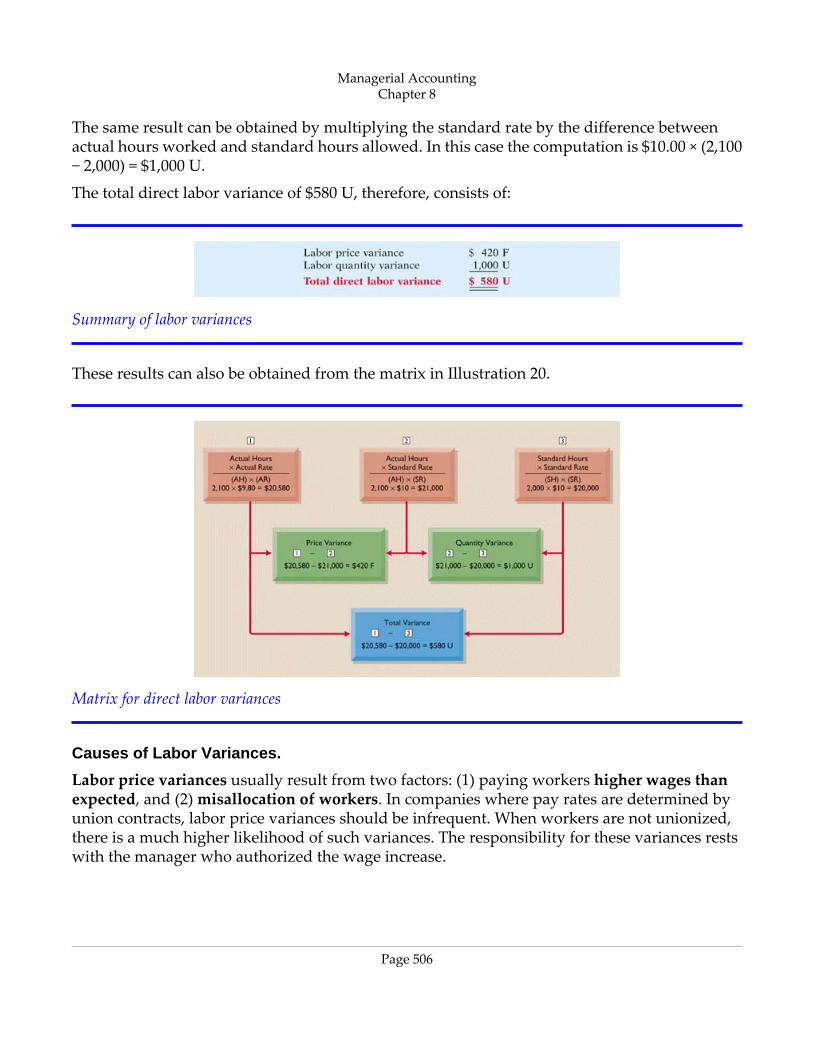

The total direct labor variance of $580 U, therefore, consists of:

Summary of labor variances

These results can also be obtained from the matrix in Illustration 20.

Matrix for direct labor variances

Causes of Labor Variances.

Labor price variances usually result from two factors: (1) paying workers higher wages thanexpected, and (2) misallocation of workers. In companies where pay rates are determined byunion contracts, labor price variances should be infrequent. When workers are not unionized,there is a much higher likelihood of such variances. The responsibility for these variances restswith the manager who authorized the wage increase.

Managerial AccountingChapter 8

Page 506

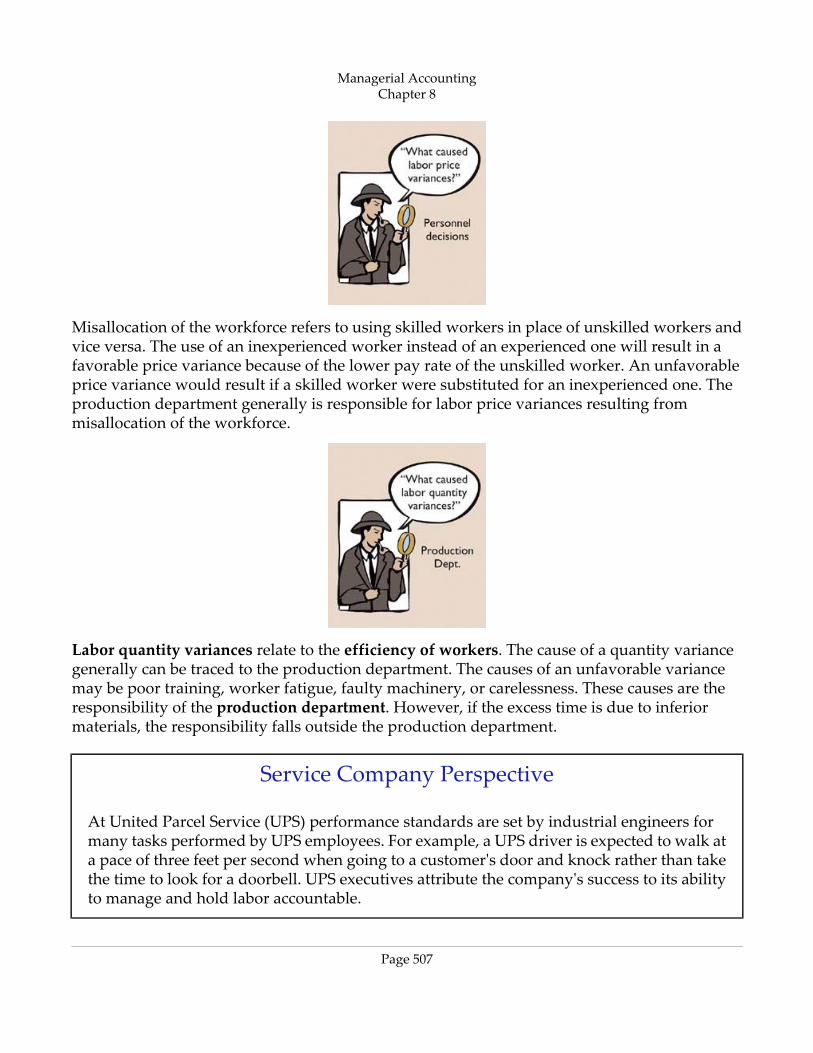

Misallocation of the workforce refers to using skilled workers in place of unskilled workers andvice versa. The use of an inexperienced worker instead of an experienced one will result in afavorable price variance because of the lower pay rate of the unskilled worker. An unfavorableprice variance would result if a skilled worker were substituted for an inexperienced one. Theproduction department generally is responsible for labor price variances resulting frommisallocation of the workforce.

Labor quantity variances relate to the efficiency of workers. The cause of a quantity variancegenerally can be traced to the production department. The causes of an unfavorable variancemay be poor training, worker fatigue, faulty machinery, or carelessness. These causes are theresponsibility of the production department. However, if the excess time is due to inferiormaterials, the responsibility falls outside the production department.

Service Company Perspective

At United Parcel Service (UPS) performance standards are set by industrial engineers formany tasks performed by UPS employees. For example, a UPS driver is expected to walk ata pace of three feet per second when going to a customer's door and knock rather than takethe time to look for a doorbell. UPS executives attribute the company's success to its abilityto manage and hold labor accountable.

Managerial AccountingChapter 8

Page 507

Manufacturing Overhead Variances

The computation of the manufacturing overhead variances is conceptually the same as thecomputation of the materials and labor variances. However, the task is more challenging formanufacturing overhead because both variable and fixed overhead costs must be considered.

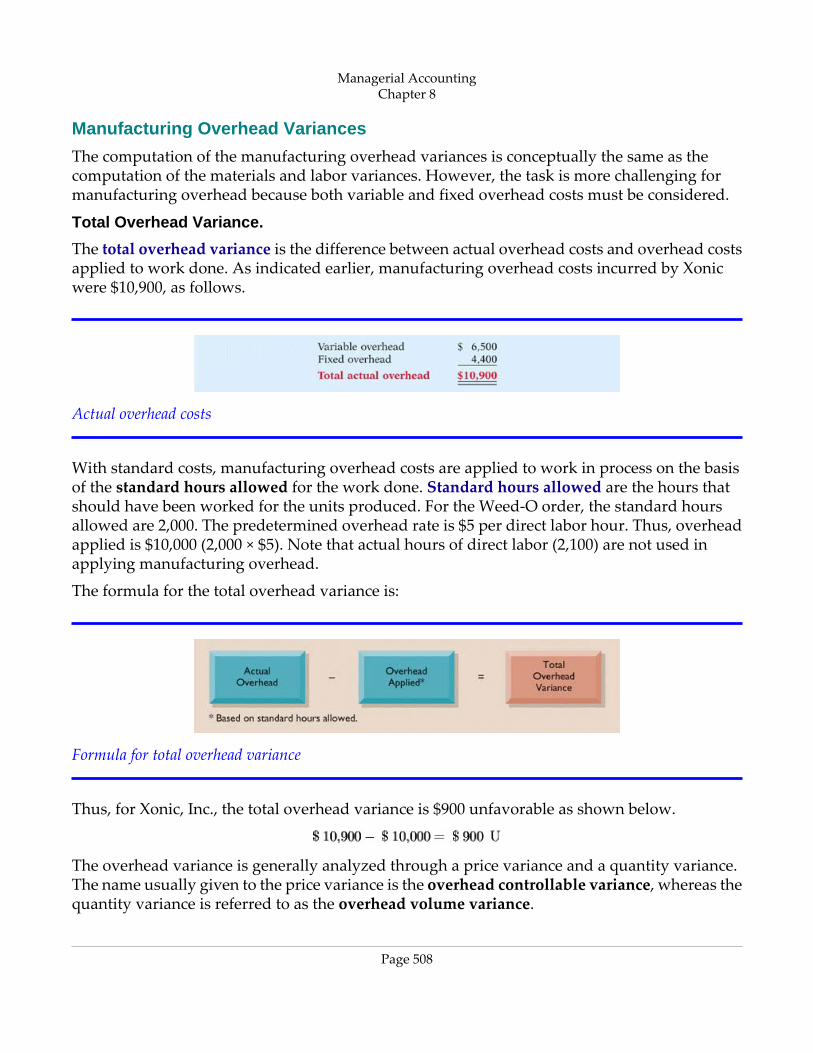

Total Overhead Variance.

The total overhead variance is the difference between actual overhead costs and overhead costsapplied to work done. As indicated earlier, manufacturing overhead costs incurred by Xonicwere $10,900, as follows.

Actual overhead costs

With standard costs, manufacturing overhead costs are applied to work in process on the basisof the standard hours allowed for the work done. Standard hours allowed are the hours thatshould have been worked for the units produced. For the Weed‐O order, the standard hoursallowed are 2,000. The predetermined overhead rate is $5 per direct labor hour. Thus, overheadapplied is $10,000 (2,000 × $5). Note that actual hours of direct labor (2,100) are not used inapplying manufacturing overhead.

The formula for the total overhead variance is:

Formula for total overhead variance

Thus, for Xonic, Inc., the total overhead variance is $900 unfavorable as shown below.

The overhead variance is generally analyzed through a price variance and a quantity variance.The name usually given to the price variance is the overhead controllable variance, whereas thequantity variance is referred to as the overhead volume variance.

Managerial AccountingChapter 8

Page 508

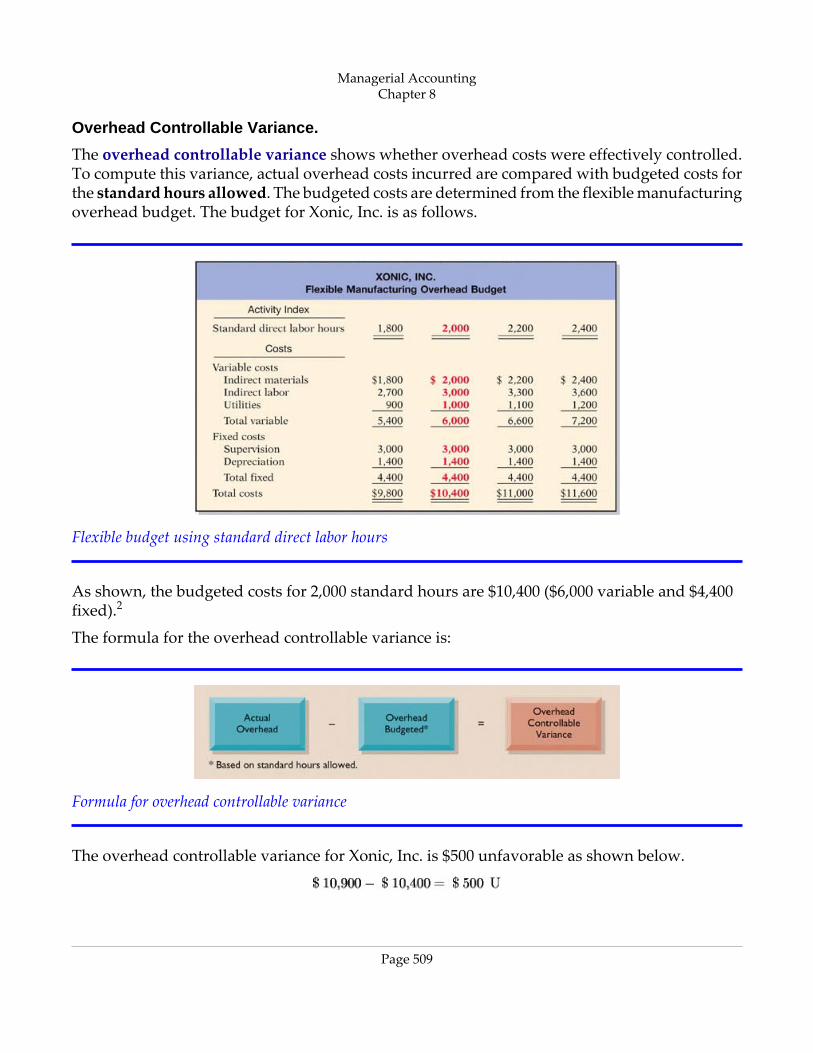

Overhead Controllable Variance.

The overhead controllable variance shows whether overhead costs were effectively controlled.To compute this variance, actual overhead costs incurred are compared with budgeted costs forthe standard hours allowed. The budgeted costs are determined from the flexible manufacturingoverhead budget. The budget for Xonic, Inc. is as follows.

Flexible budget using standard direct labor hours

As shown, the budgeted costs for 2,000 standard hours are $10,400 ($6,000 variable and $4,400fixed).2

The formula for the overhead controllable variance is:

Formula for overhead controllable variance

The overhead controllable variance for Xonic, Inc. is $500 unfavorable as shown below.

Managerial AccountingChapter 8

Page 509

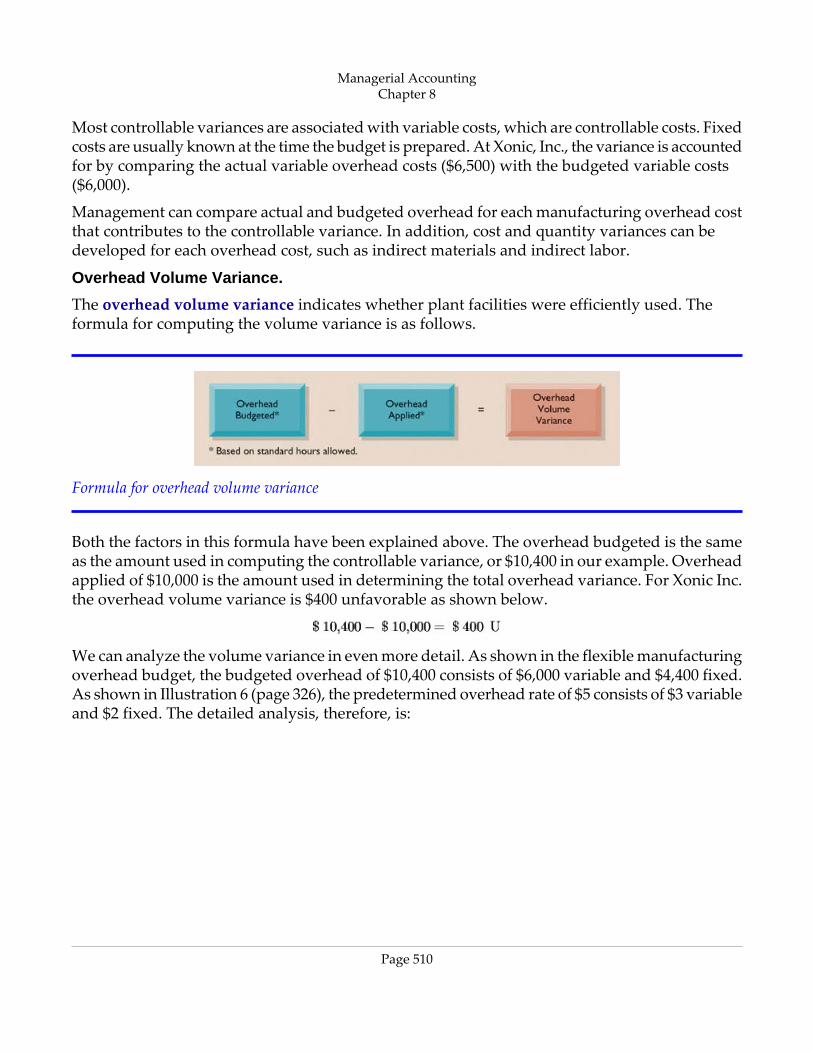

Most controllable variances are associated with variable costs, which are controllable costs. Fixedcosts are usually known at the time the budget is prepared. At Xonic, Inc., the variance is accountedfor by comparing the actual variable overhead costs ($6,500) with the budgeted variable costs($6,000).

Management can compare actual and budgeted overhead for each manufacturing overhead costthat contributes to the controllable variance. In addition, cost and quantity variances can bedeveloped for each overhead cost, such as indirect materials and indirect labor.

Overhead Volume Variance.

The overhead volume variance indicates whether plant facilities were efficiently used. Theformula for computing the volume variance is as follows.

Formula for overhead volume variance

Both the factors in this formula have been explained above. The overhead budgeted is the sameas the amount used in computing the controllable variance, or $10,400 in our example. Overheadapplied of $10,000 is the amount used in determining the total overhead variance. For Xonic Inc.the overhead volume variance is $400 unfavorable as shown below.

We can analyze the volume variance in even more detail. As shown in the flexible manufacturingoverhead budget, the budgeted overhead of $10,400 consists of $6,000 variable and $4,400 fixed.As shown in Illustration 6 (page 326), the predetermined overhead rate of $5 consists of $3 variableand $2 fixed. The detailed analysis, therefore, is:

Managerial AccountingChapter 8

Page 510

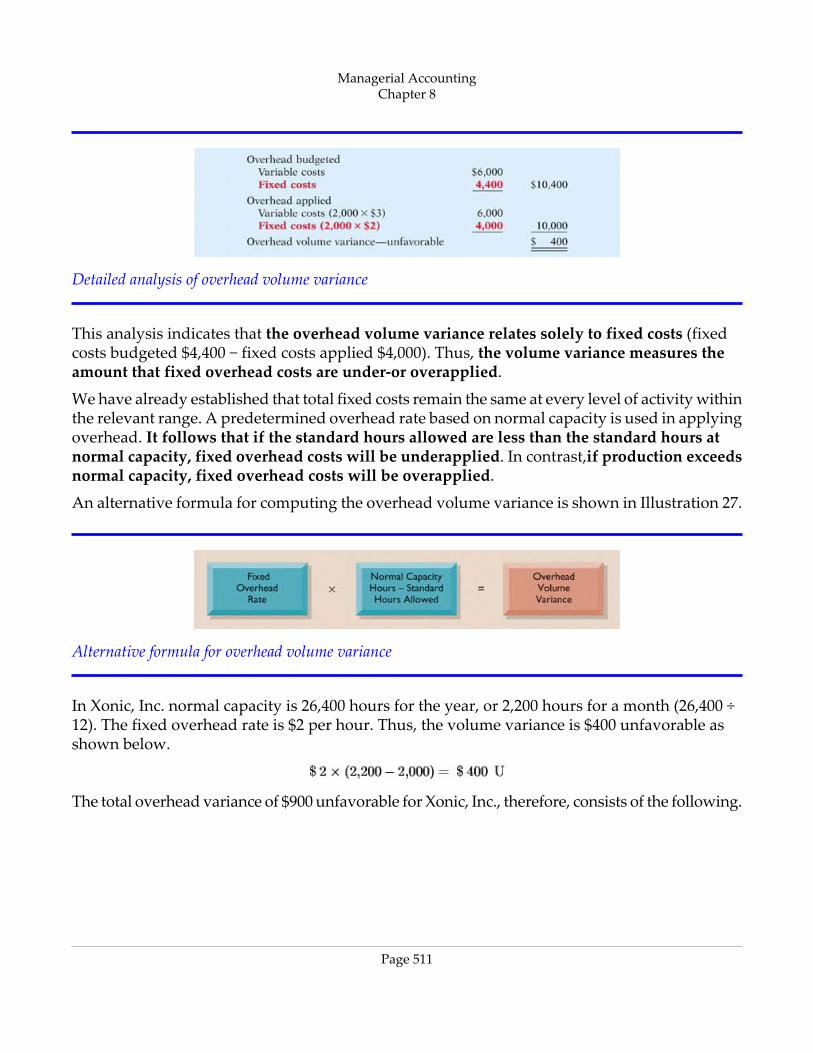

Detailed analysis of overhead volume variance

This analysis indicates that the overhead volume variance relates solely to fixed costs (fixedcosts budgeted $4,400 − fixed costs applied $4,000). Thus, the volume variance measures theamount that fixed overhead costs are under‐or overapplied.

We have already established that total fixed costs remain the same at every level of activity withinthe relevant range. A predetermined overhead rate based on normal capacity is used in applyingoverhead. It follows that if the standard hours allowed are less than the standard hours atnormal capacity, fixed overhead costs will be underapplied. In contrast,if production exceedsnormal capacity, fixed overhead costs will be overapplied.

An alternative formula for computing the overhead volume variance is shown in Illustration 27.

Alternative formula for overhead volume variance

In Xonic, Inc. normal capacity is 26,400 hours for the year, or 2,200 hours for a month (26,400 ÷12). The fixed overhead rate is $2 per hour. Thus, the volume variance is $400 unfavorable asshown below.

The total overhead variance of $900 unfavorable for Xonic, Inc., therefore, consists of the following.

Managerial AccountingChapter 8

Page 511

Summary of overhead variances

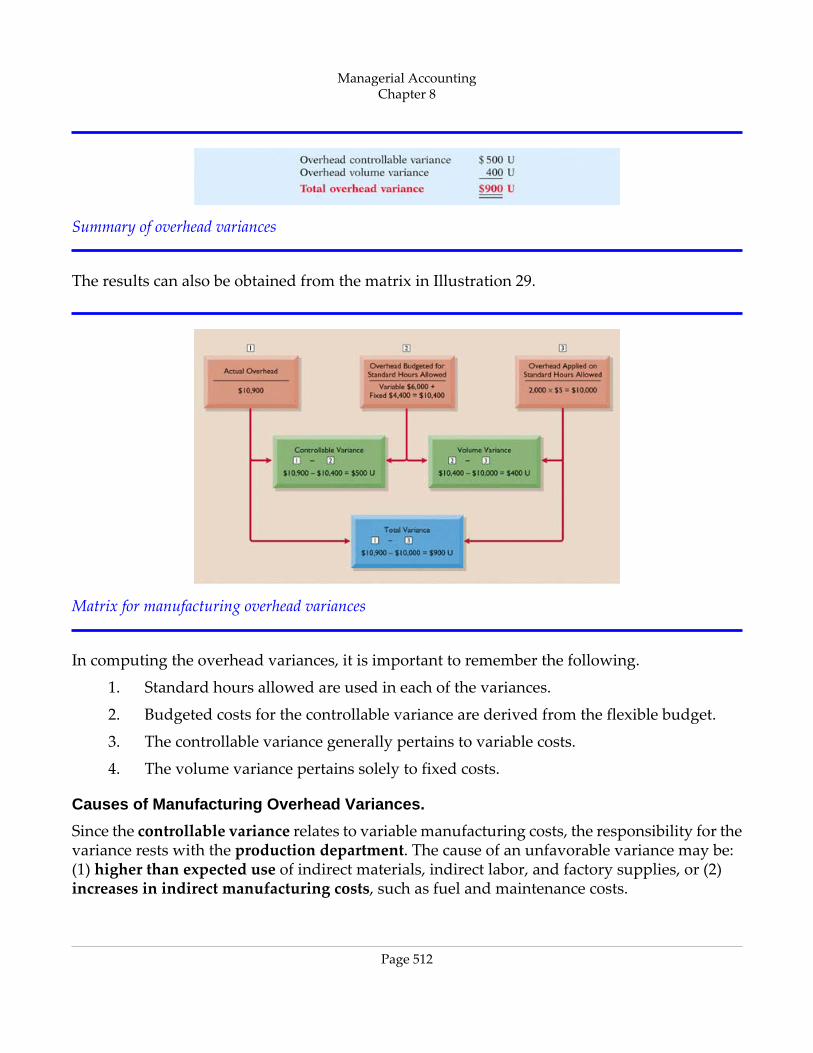

The results can also be obtained from the matrix in Illustration 29.

Matrix for manufacturing overhead variances

In computing the overhead variances, it is important to remember the following.

1. Standard hours allowed are used in each of the variances.

2. Budgeted costs for the controllable variance are derived from the flexible budget.

3. The controllable variance generally pertains to variable costs.

4. The volume variance pertains solely to fixed costs.

Causes of Manufacturing Overhead Variances.

Since the controllable variance relates to variable manufacturing costs, the responsibility for thevariance rests with the production department. The cause of an unfavorable variance may be:(1) higher than expected use of indirect materials, indirect labor, and factory supplies, or (2)increases in indirect manufacturing costs, such as fuel and maintenance costs.

Managerial AccountingChapter 8

Page 512

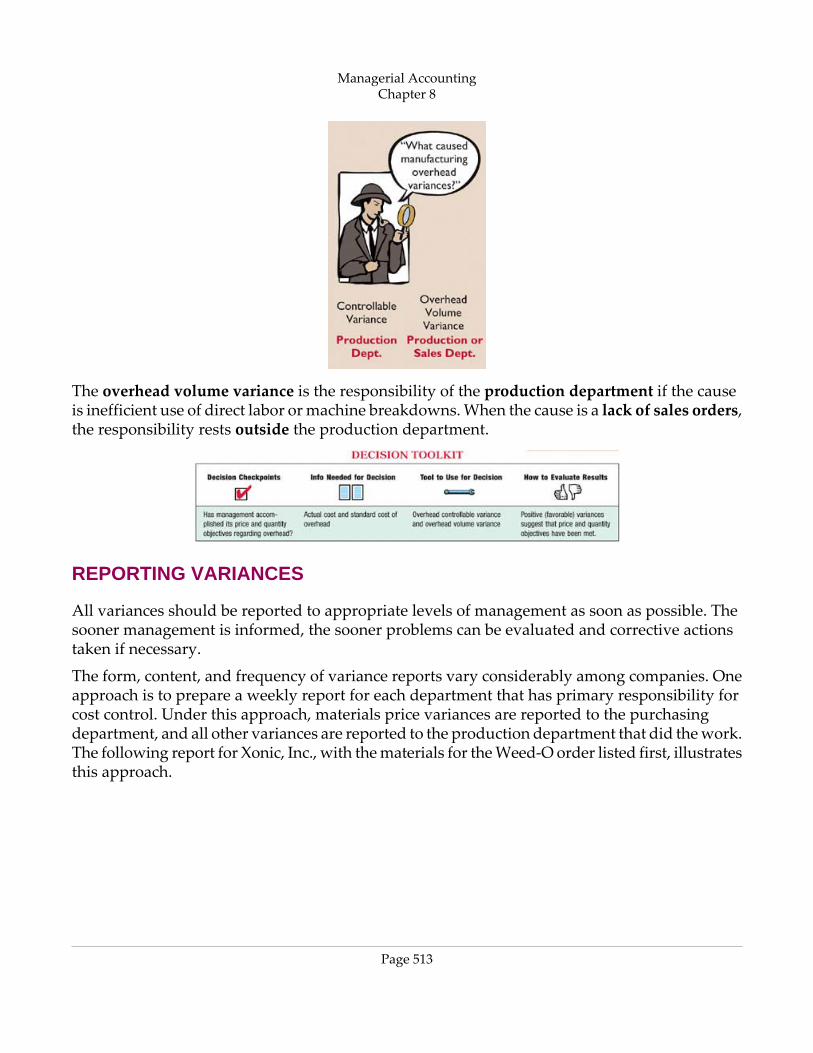

The overhead volume variance is the responsibility of the production department if the causeis inefficient use of direct labor or machine breakdowns. When the cause is a lack of sales orders,the responsibility rests outside the production department.

REPORTING VARIANCES

All variances should be reported to appropriate levels of management as soon as possible. Thesooner management is informed, the sooner problems can be evaluated and corrective actionstaken if necessary.

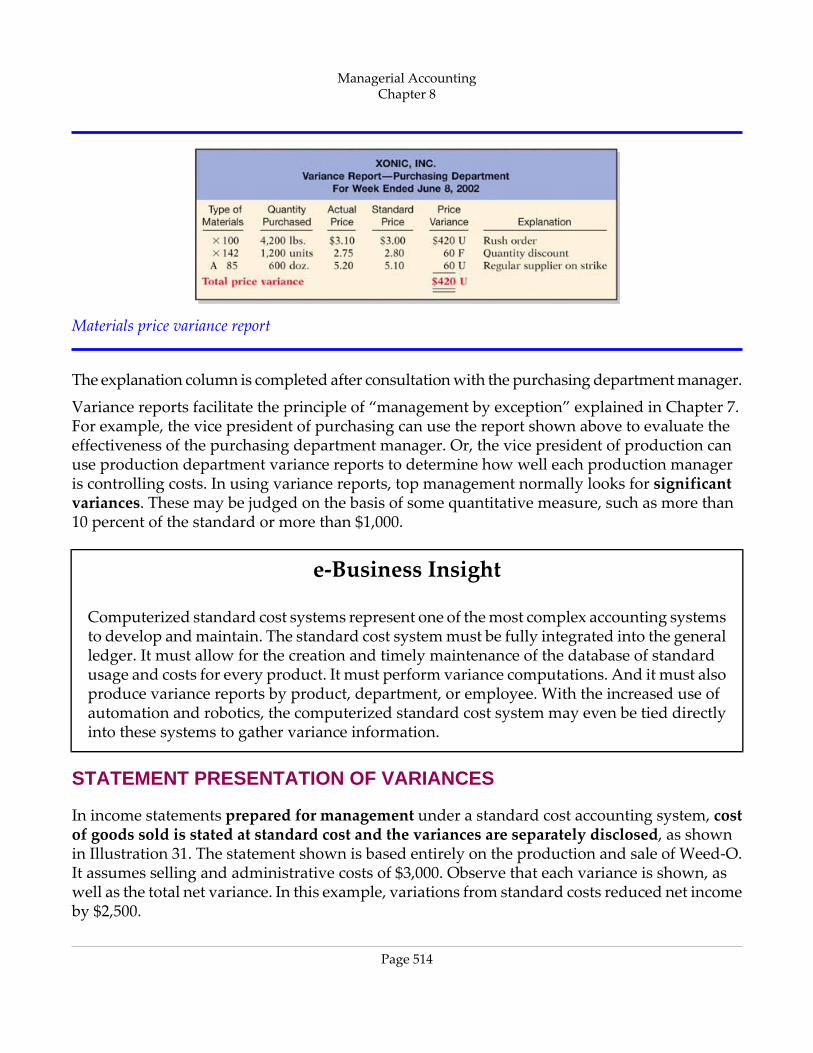

The form, content, and frequency of variance reports vary considerably among companies. Oneapproach is to prepare a weekly report for each department that has primary responsibility forcost control. Under this approach, materials price variances are reported to the purchasingdepartment, and all other variances are reported to the production department that did the work.The following report for Xonic, Inc., with the materials for the Weed‐O order listed first, illustratesthis approach.

Managerial AccountingChapter 8

Page 513

Materials price variance report

The explanation column is completed after consultation with the purchasing department manager.

Variance reports facilitate the principle of “management by exception” explained in Chapter 7.For example, the vice president of purchasing can use the report shown above to evaluate theeffectiveness of the purchasing department manager. Or, the vice president of production canuse production department variance reports to determine how well each production manageris controlling costs. In using variance reports, top management normally looks for significantvariances. These may be judged on the basis of some quantitative measure, such as more than10 percent of the standard or more than $1,000.

e‐Business Insight

Computerized standard cost systems represent one of the most complex accounting systemsto develop and maintain. The standard cost system must be fully integrated into the generalledger. It must allow for the creation and timely maintenance of the database of standardusage and costs for every product. It must perform variance computations. And it must alsoproduce variance reports by product, department, or employee. With the increased use ofautomation and robotics, the computerized standard cost system may even be tied directlyinto these systems to gather variance information.

STATEMENT PRESENTATION OF VARIANCES

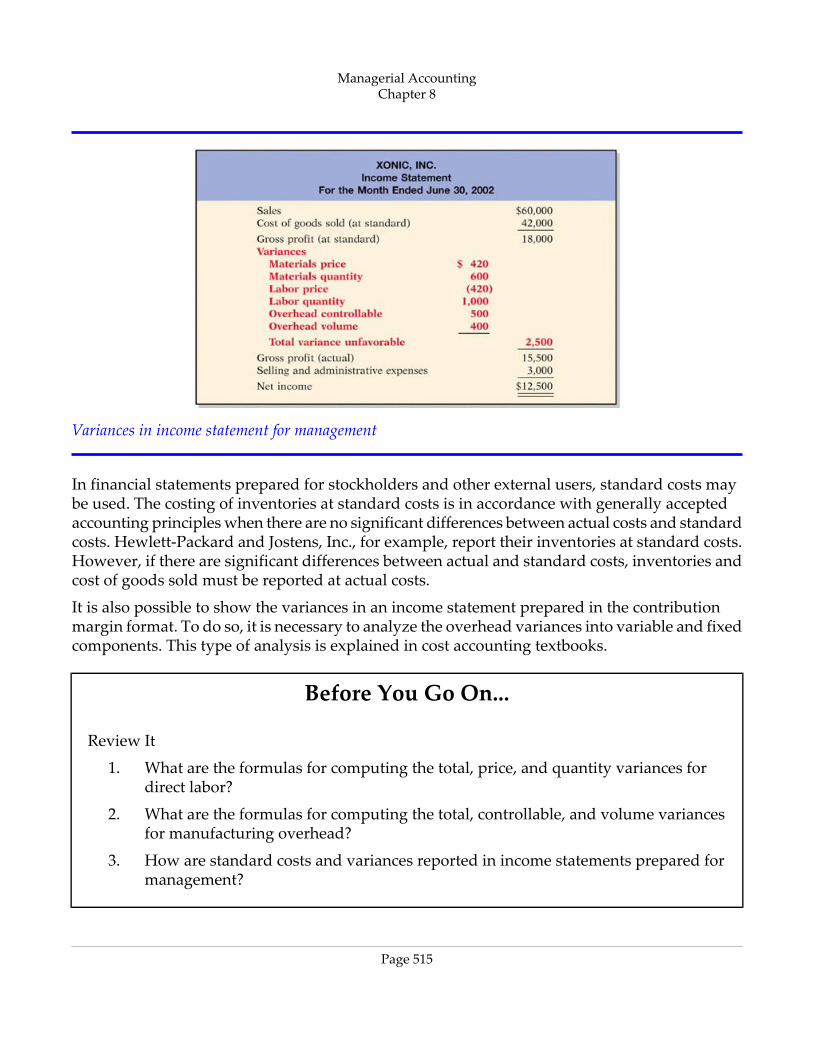

In income statements prepared for management under a standard cost accounting system, costof goods sold is stated at standard cost and the variances are separately disclosed, as shownin Illustration 31. The statement shown is based entirely on the production and sale of Weed‐O.It assumes selling and administrative costs of $3,000. Observe that each variance is shown, aswell as the total net variance. In this example, variations from standard costs reduced net incomeby $2,500.

Managerial AccountingChapter 8

Page 514

Variances in income statement for management

In financial statements prepared for stockholders and other external users, standard costs maybe used. The costing of inventories at standard costs is in accordance with generally acceptedaccounting principles when there are no significant differences between actual costs and standardcosts. Hewlett‐Packard and Jostens, Inc., for example, report their inventories at standard costs.However, if there are significant differences between actual and standard costs, inventories andcost of goods sold must be reported at actual costs.

It is also possible to show the variances in an income statement prepared in the contributionmargin format. To do so, it is necessary to analyze the overhead variances into variable and fixedcomponents. This type of analysis is explained in cost accounting textbooks.

Before You Go On...

Review It

1. What are the formulas for computing the total, price, and quantity variances fordirect labor?

2. What are the formulas for computing the total, controllable, and volume variancesfor manufacturing overhead?

3. How are standard costs and variances reported in income statements prepared formanagement?

Managerial AccountingChapter 8

Page 515

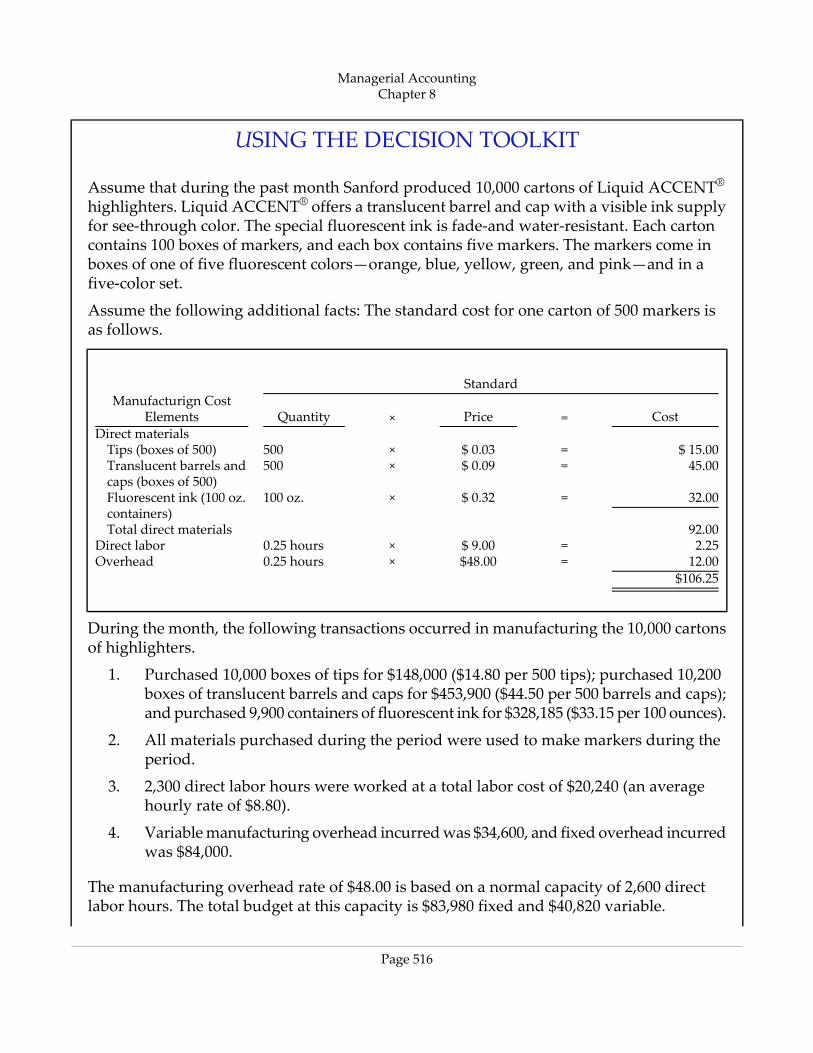

USING THE DECISION TOOLKIT

Assume that during the past month Sanford produced 10,000 cartons of Liquid ACCENT®highlighters. Liquid ACCENT® offers a translucent barrel and cap with a visible ink supplyfor see‐through color. The special fluorescent ink is fade‐and water‐resistant. Each cartoncontains 100 boxes of markers, and each box contains five markers. The markers come inboxes of one of five fluorescent colors—orange, blue, yellow, green, and pink—and in afive‐color set.

Assume the following additional facts: The standard cost for one carton of 500 markers isas follows.

Standard

Cost=Price×QuantityManufacturign Cost

ElementsDirect materials

$ 15.00=$ 0.03×500Tips (boxes of 500)45.00=$ 0.09×500Translucent barrels and

caps (boxes of 500)32.00=$ 0.32×100 oz.Fluorescent ink (100 oz.

containers)92.00Total direct materials2.25=$ 9.00×0.25 hoursDirect labor12.00=$48.00×0.25 hoursOverhead

$106.25

During the month, the following transactions occurred in manufacturing the 10,000 cartonsof highlighters.

1. Purchased 10,000 boxes of tips for $148,000 ($14.80 per 500 tips); purchased 10,200boxes of translucent barrels and caps for $453,900 ($44.50 per 500 barrels and caps);and purchased 9,900 containers of fluorescent ink for $328,185 ($33.15 per 100 ounces).

2. All materials purchased during the period were used to make markers during theperiod.

3. 2,300 direct labor hours were worked at a total labor cost of $20,240 (an averagehourly rate of $8.80).

4. Variable manufacturing overhead incurred was $34,600, and fixed overhead incurredwas $84,000.

The manufacturing overhead rate of $48.00 is based on a normal capacity of 2,600 directlabor hours. The total budget at this capacity is $83,980 fixed and $40,820 variable.

Managerial AccountingChapter 8

Page 516

Instructions

1. Determine whether Sanford met its price and quantity objectives relative to materials,labor, and overhead.

Managerial AccountingChapter 8

Page 517

Summary of Study Objectives

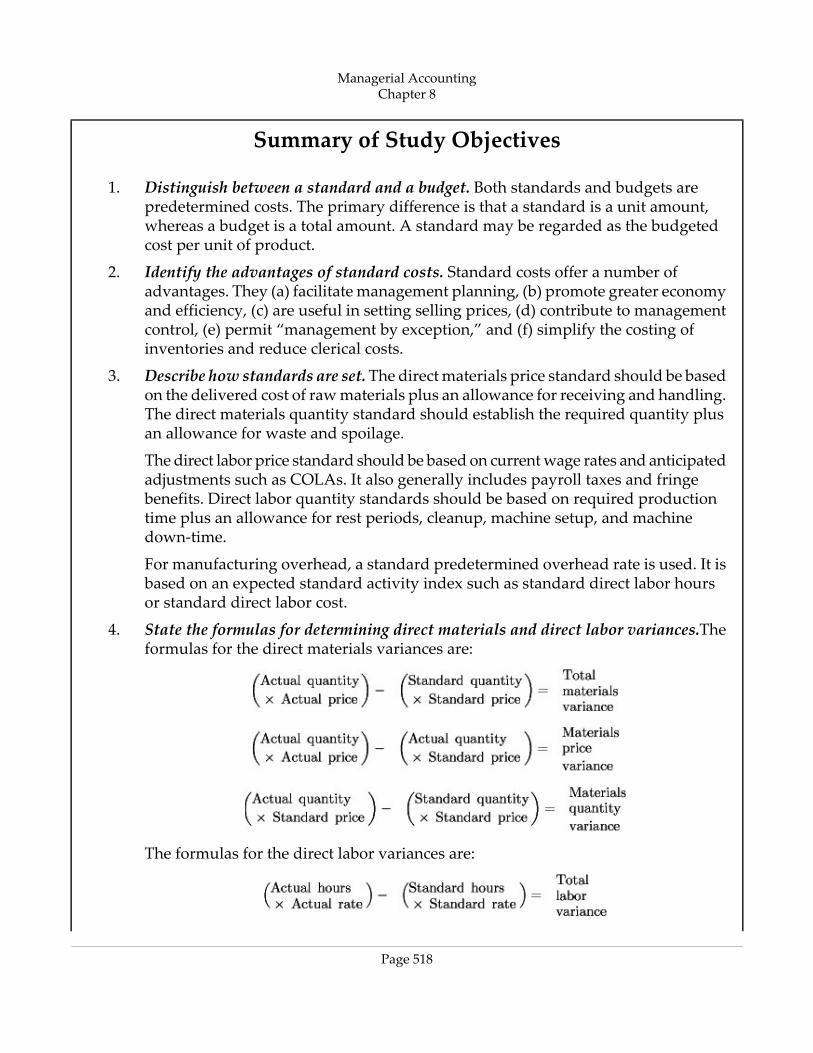

1. Distinguish between a standard and a budget. Both standards and budgets arepredetermined costs. The primary difference is that a standard is a unit amount,whereas a budget is a total amount. A standard may be regarded as the budgetedcost per unit of product.

2. Identify the advantages of standard costs. Standard costs offer a number ofadvantages. They (a) facilitate management planning, (b) promote greater economyand efficiency, (c) are useful in setting selling prices, (d) contribute to managementcontrol, (e) permit “management by exception,” and (f) simplify the costing ofinventories and reduce clerical costs.

3. Describe how standards are set.The direct materials price standard should be basedon the delivered cost of raw materials plus an allowance for receiving and handling.The direct materials quantity standard should establish the required quantity plusan allowance for waste and spoilage.

The direct labor price standard should be based on current wage rates and anticipatedadjustments such as COLAs. It also generally includes payroll taxes and fringebenefits. Direct labor quantity standards should be based on required productiontime plus an allowance for rest periods, cleanup, machine setup, and machinedown‐time.

For manufacturing overhead, a standard predetermined overhead rate is used. It isbased on an expected standard activity index such as standard direct labor hoursor standard direct labor cost.

4. State the formulas for determining direct materials and direct labor variances.Theformulas for the direct materials variances are:

The formulas for the direct labor variances are:

Managerial AccountingChapter 8

Page 518

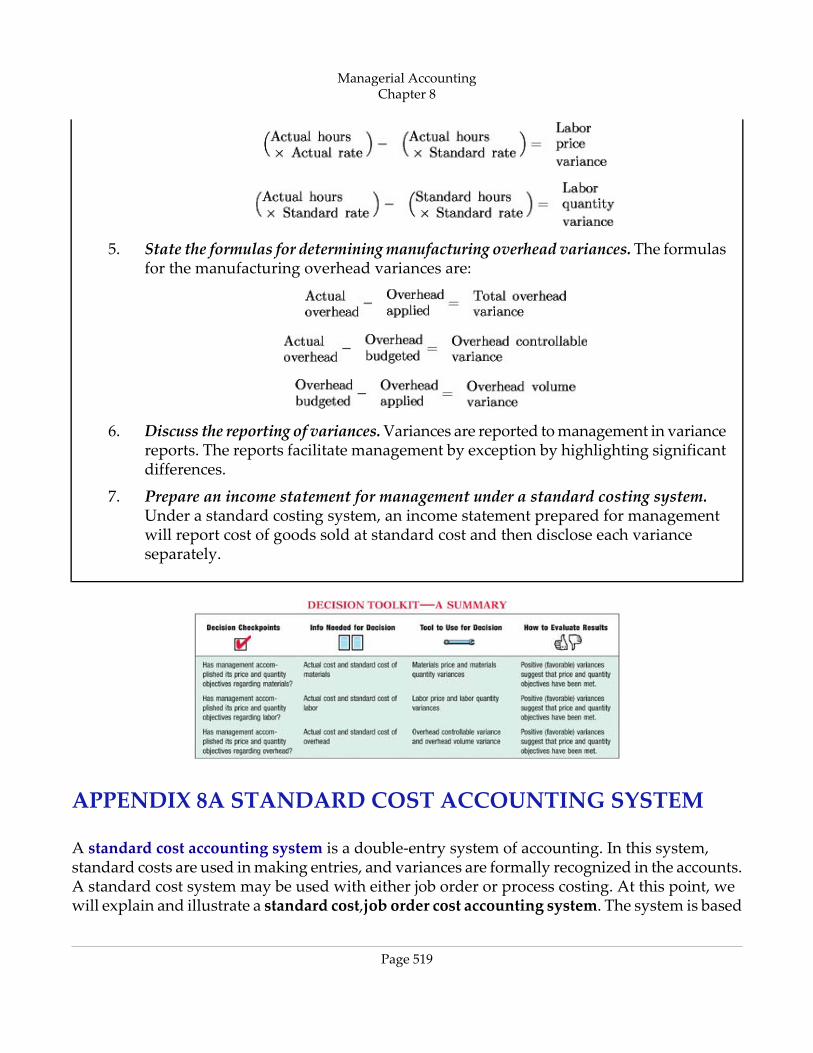

5. State the formulas for determining manufacturing overhead variances.The formulasfor the manufacturing overhead variances are:

6. Discuss the reporting of variances.Variances are reported to management in variancereports. The reports facilitate management by exception by highlighting significantdifferences.