Embed Size (px)

Citation preview

Managing the Sales Factor: Sourcing Services & Intangibles

Jamie Fenwick, Time Warner Cable, Charlotte, [email protected]

Maria Eberle, Baker & McKenzie, New York, [email protected]

Raymond J. Freda, Andersen Tax, New York, NY [email protected]

March 14, 2016

2

AGENDA• Background on Sourcing Methodologies

• Emerging Issues with Multiple Sourcing Regimes

• Update on Cost of Performance Sourcing (“COP”)

• Market Based Sourcing (“MBS”)• Services• Intangibles

• Conformity/Non-Conformity Issues

• MTC Provisions

Background• Cost of Performance Sourcing

• Approximately 24 states still retain some form of a cost of performance methodology for sourcing services or intangibles.

• Costs of Performance or Income Producing Activity is generally a cost or expense analysis.

• All or Nothing (greater than 50%).

• Relative Cost of performance (“RCOP”).

Background• Approximately 21 Jurisdictions have formally

transitioned or in the process of transitioning to a MBS regime.

• AZ - 4 Year Phase-in MBS (2014 – 2017)• Mixed MBS and Income Producing

Sourcing (85/15, 90/10 etc…).

• This includes a number of major (by population and contribution to GDP) jurisdictions including: AZ, CA, GA, IL, MA, NYS/C, PA, WA.

5

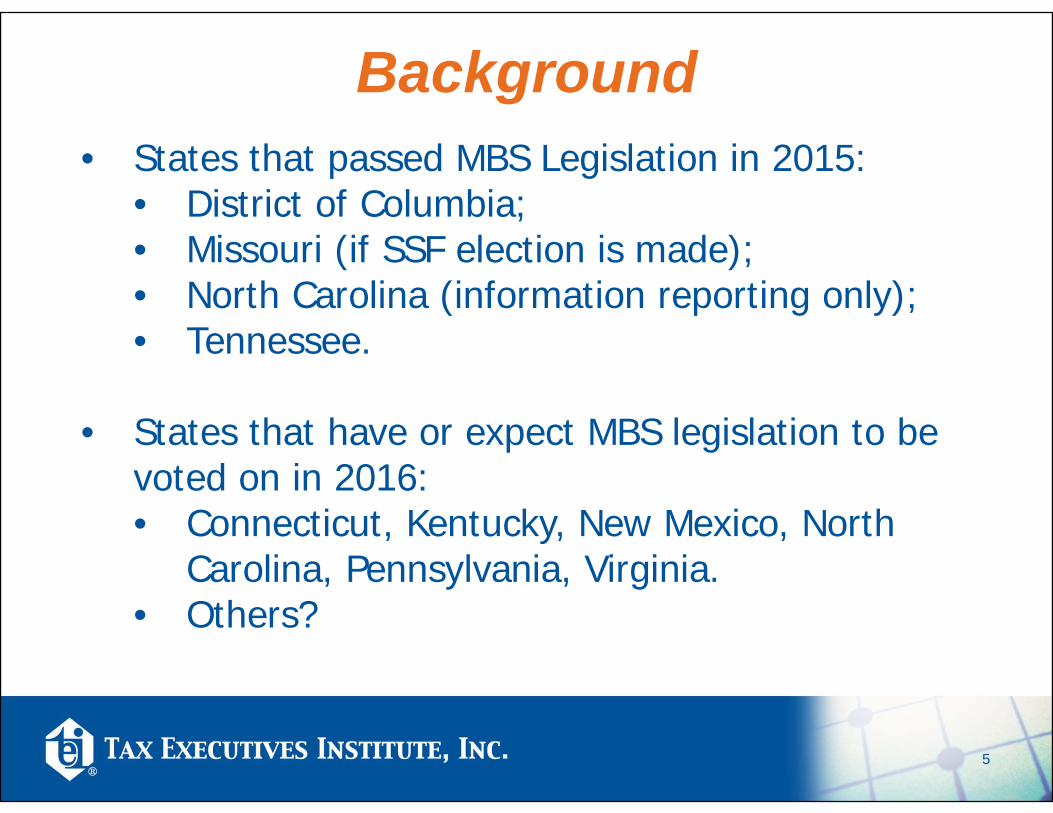

Background• States that passed MBS Legislation in 2015:

• District of Columbia;• Missouri (if SSF election is made);• North Carolina (information reporting only);• Tennessee.

• States that have or expect MBS legislation to be voted on in 2016:• Connecticut, Kentucky, New Mexico, North

Carolina, Pennsylvania, Virginia.• Others?

6

Background

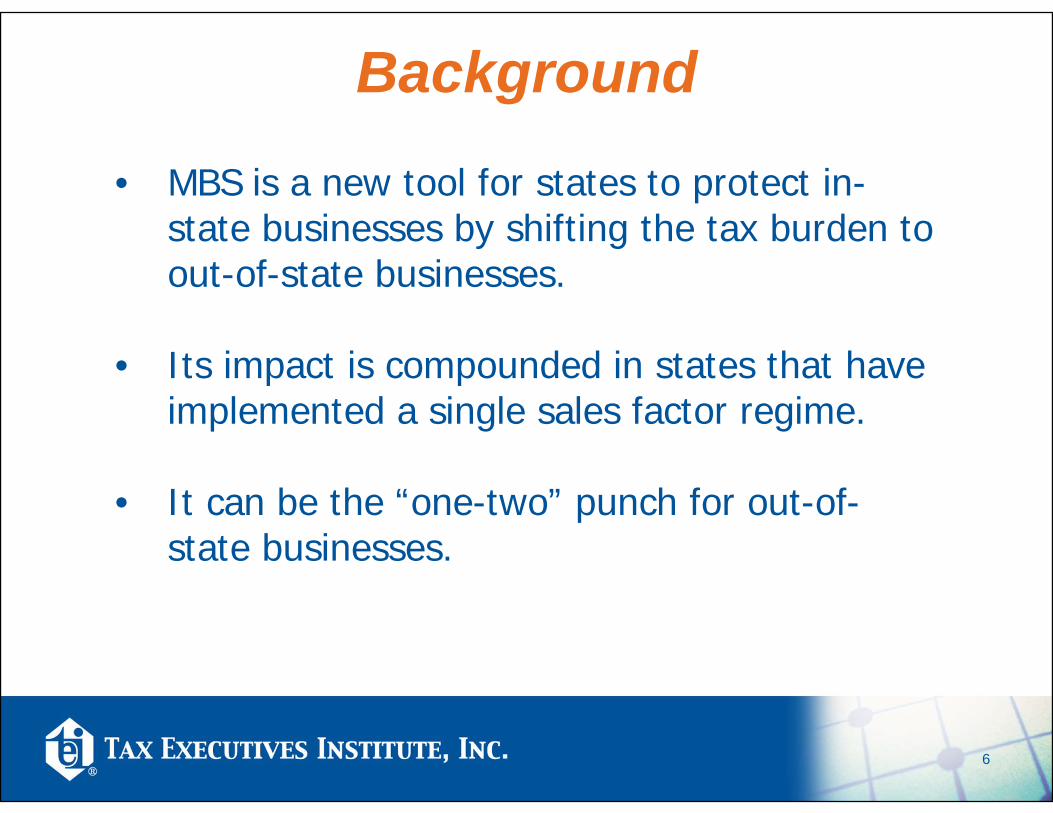

• MBS is a new tool for states to protect in-state businesses by shifting the tax burden to out-of-state businesses.

• Its impact is compounded in states that have implemented a single sales factor regime.

• It can be the “one-two” punch for out-of-state businesses.

7

Emerging Issues with Multiple Sourcing Regimes

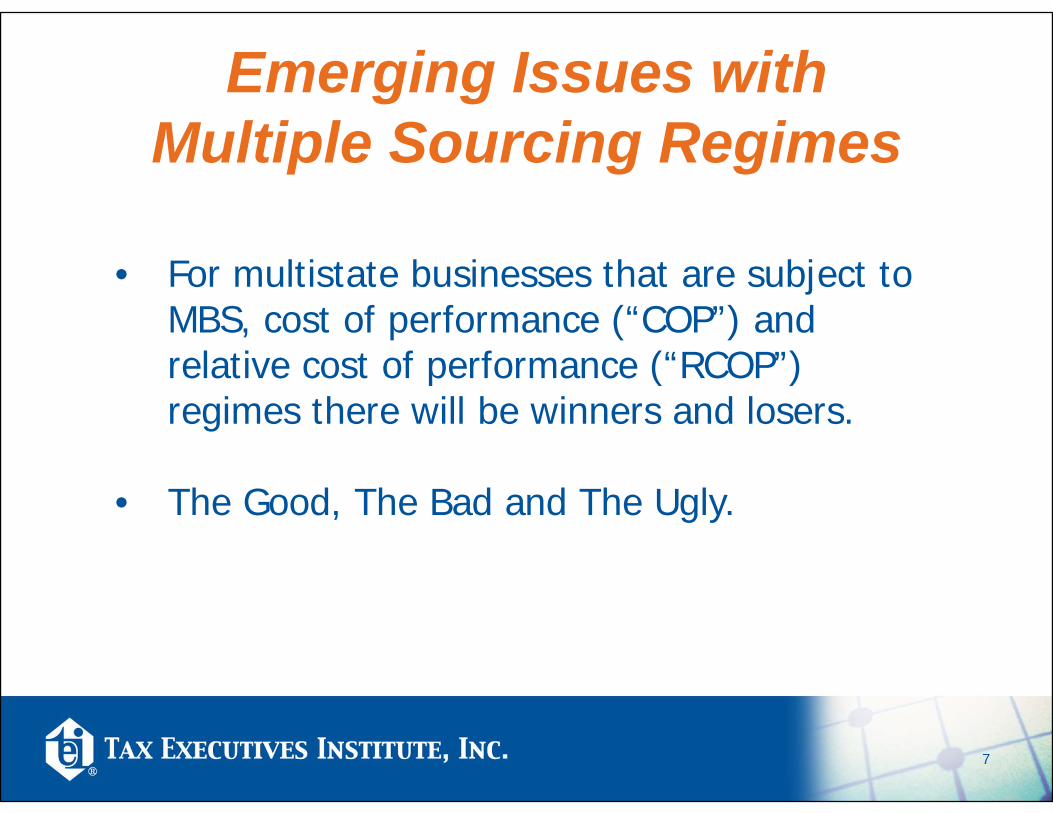

• For multistate businesses that are subject to MBS, cost of performance (“COP”) and relative cost of performance (“RCOP”) regimes there will be winners and losers.

• The Good, The Bad and The Ugly.

8

Emerging Issues – The Good

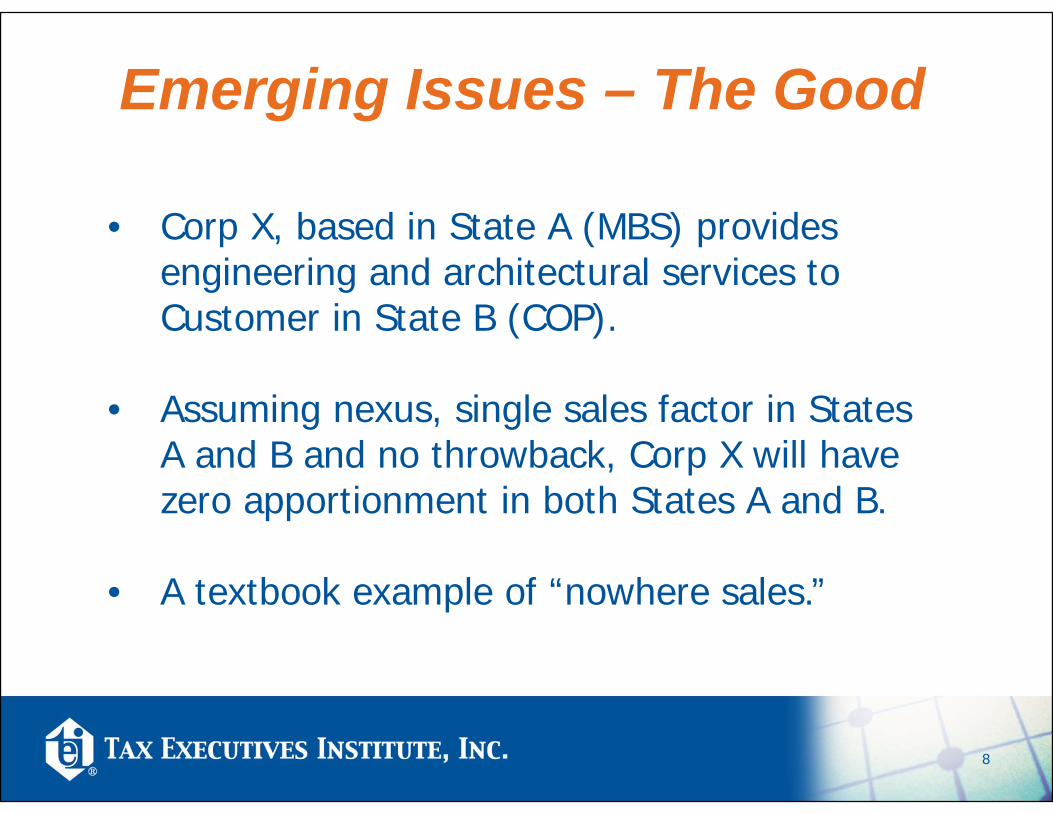

• Corp X, based in State A (MBS) provides engineering and architectural services to Customer in State B (COP).

• Assuming nexus, single sales factor in States A and B and no throwback, Corp X will have zero apportionment in both States A and B.

• A textbook example of “nowhere sales.”

9

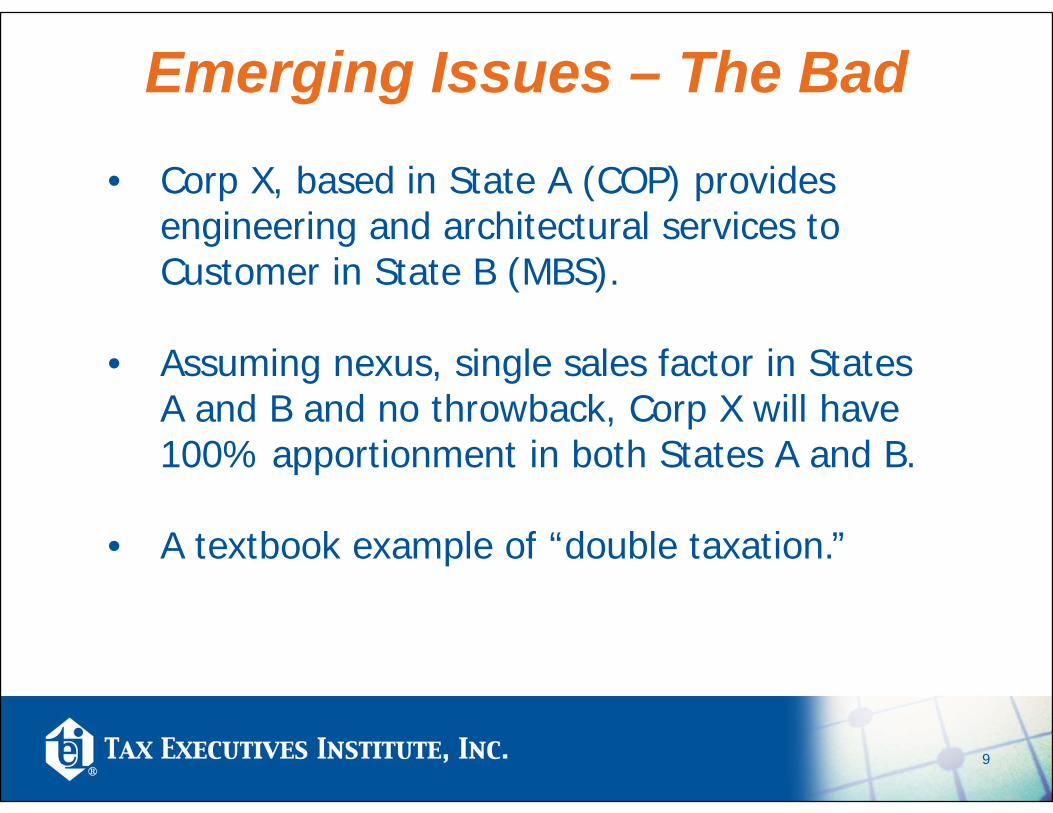

Emerging Issues – The Bad• Corp X, based in State A (COP) provides

engineering and architectural services to Customer in State B (MBS).

• Assuming nexus, single sales factor in States A and B and no throwback, Corp X will have 100% apportionment in both States A and B.

• A textbook example of “double taxation.”

10

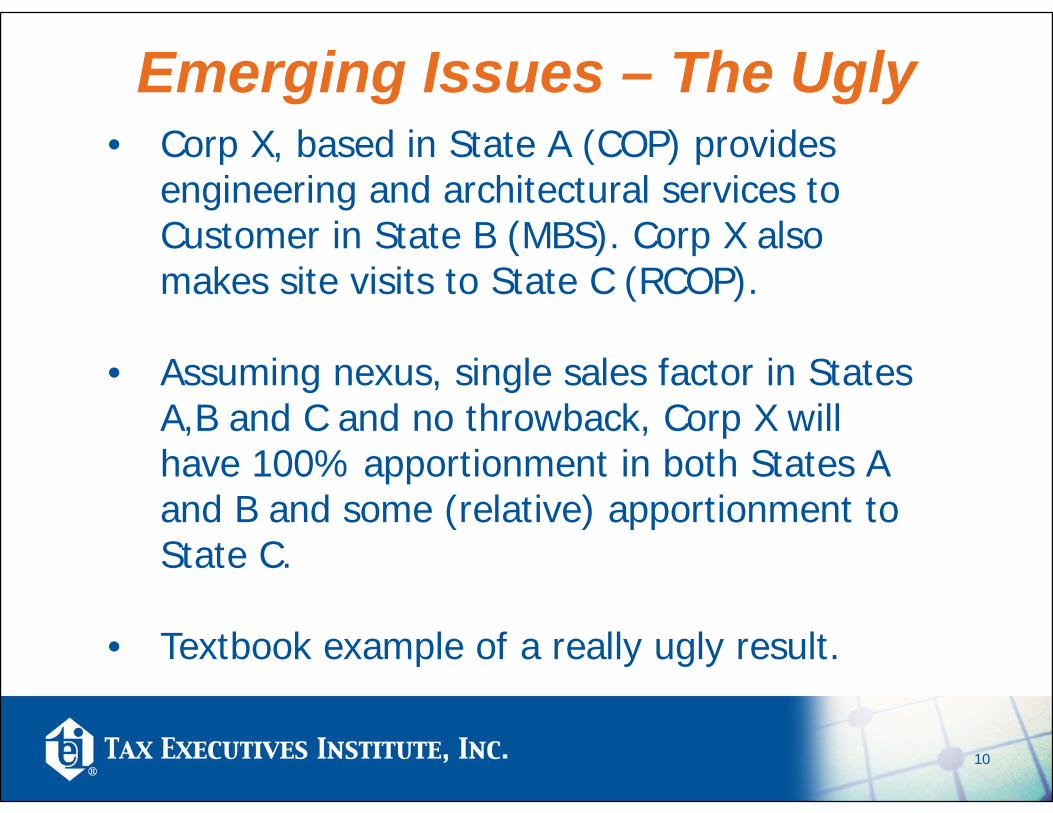

Emerging Issues – The Ugly• Corp X, based in State A (COP) provides

engineering and architectural services to Customer in State B (MBS). Corp X also makes site visits to State C (RCOP).

• Assuming nexus, single sales factor in States A,B and C and no throwback, Corp X will have 100% apportionment in both States A and B and some (relative) apportionment to State C.

• Textbook example of a really ugly result.

11

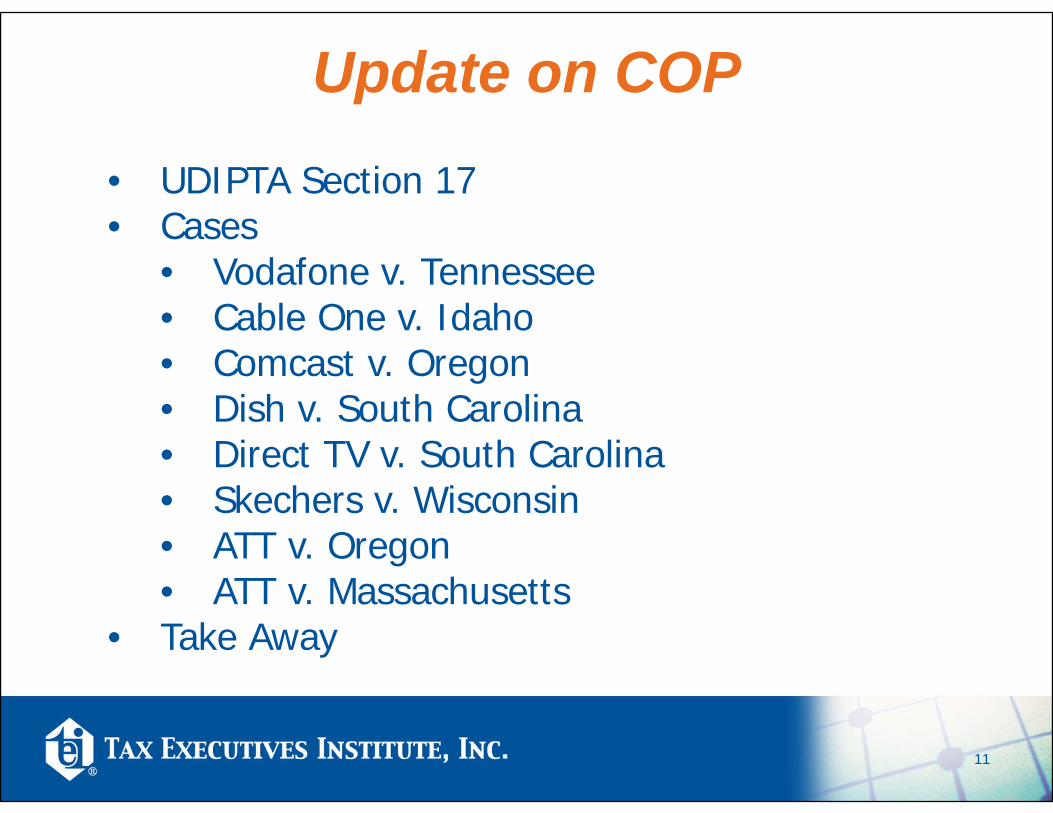

Update on COP• UDIPTA Section 17• Cases

• Vodafone v. Tennessee• Cable One v. Idaho• Comcast v. Oregon• Dish v. South Carolina• Direct TV v. South Carolina• Skechers v. Wisconsin• ATT v. Oregon• ATT v. Massachusetts

• Take Away

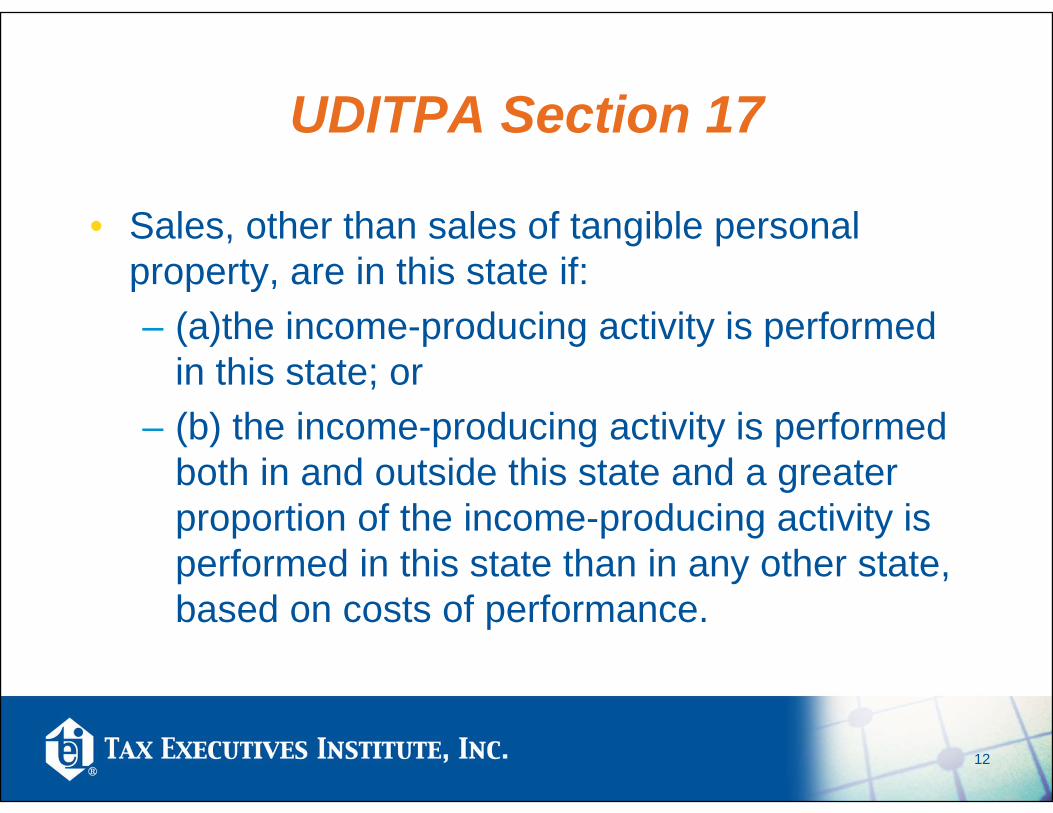

UDITPA Section 17

• Sales, other than sales of tangible personal property, are in this state if: – (a)the income-producing activity is performed

in this state; or – (b) the income-producing activity is performed

both in and outside this state and a greater proportion of the income-producing activity is performed in this state than in any other state, based on costs of performance.

12

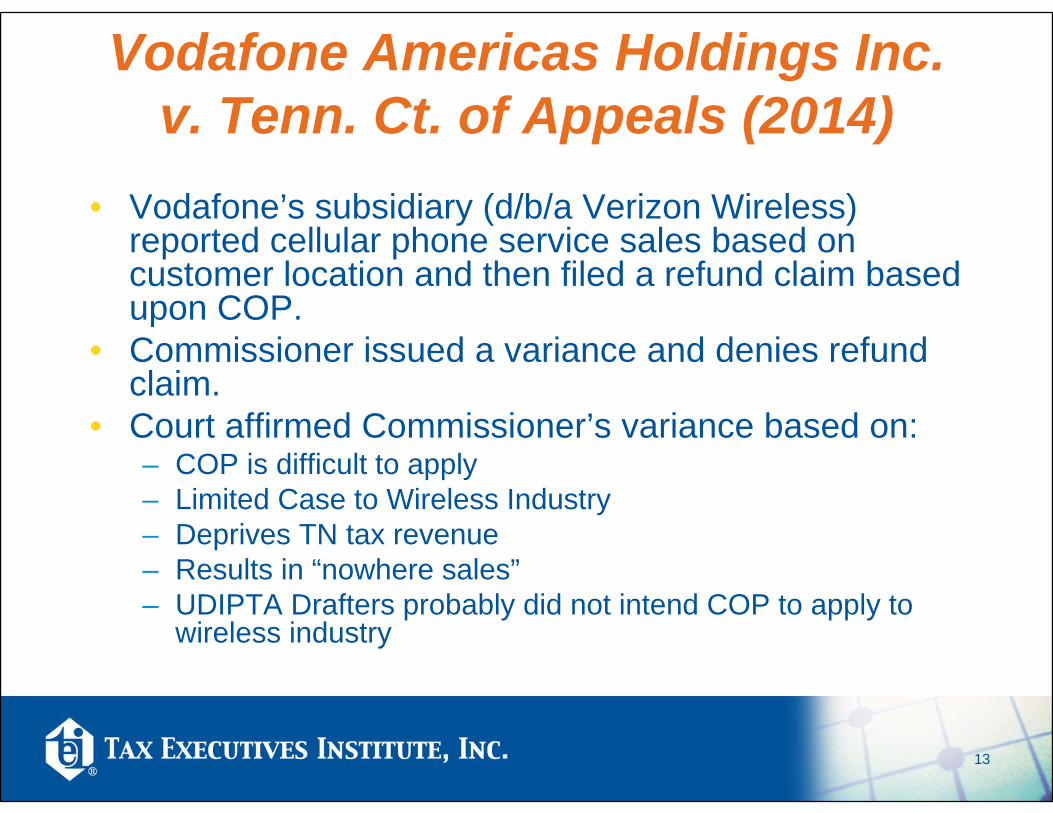

Vodafone Americas Holdings Inc. v. Tenn. Ct. of Appeals (2014)

• Vodafone’s subsidiary (d/b/a Verizon Wireless) reported cellular phone service sales based on customer location and then filed a refund claim based upon COP.

• Commissioner issued a variance and denies refund claim.

• Court affirmed Commissioner’s variance based on:– COP is difficult to apply– Limited Case to Wireless Industry– Deprives TN tax revenue– Results in “nowhere sales”– UDIPTA Drafters probably did not intend COP to apply to

wireless industry

13

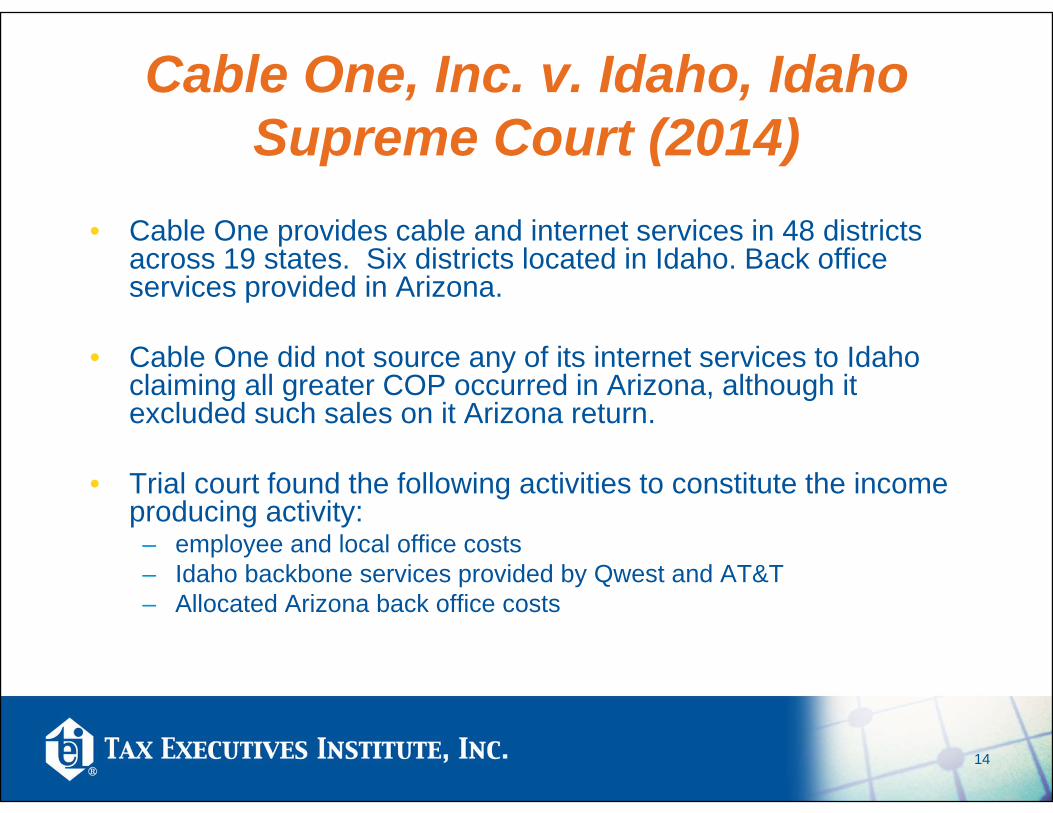

Cable One, Inc. v. Idaho, Idaho Supreme Court (2014)

• Cable One provides cable and internet services in 48 districts across 19 states. Six districts located in Idaho. Back office services provided in Arizona.

• Cable One did not source any of its internet services to Idaho claiming all greater COP occurred in Arizona, although it excluded such sales on it Arizona return.

• Trial court found the following activities to constitute the income producing activity: – employee and local office costs– Idaho backbone services provided by Qwest and AT&T– Allocated Arizona back office costs

14

Cable One (Continued)

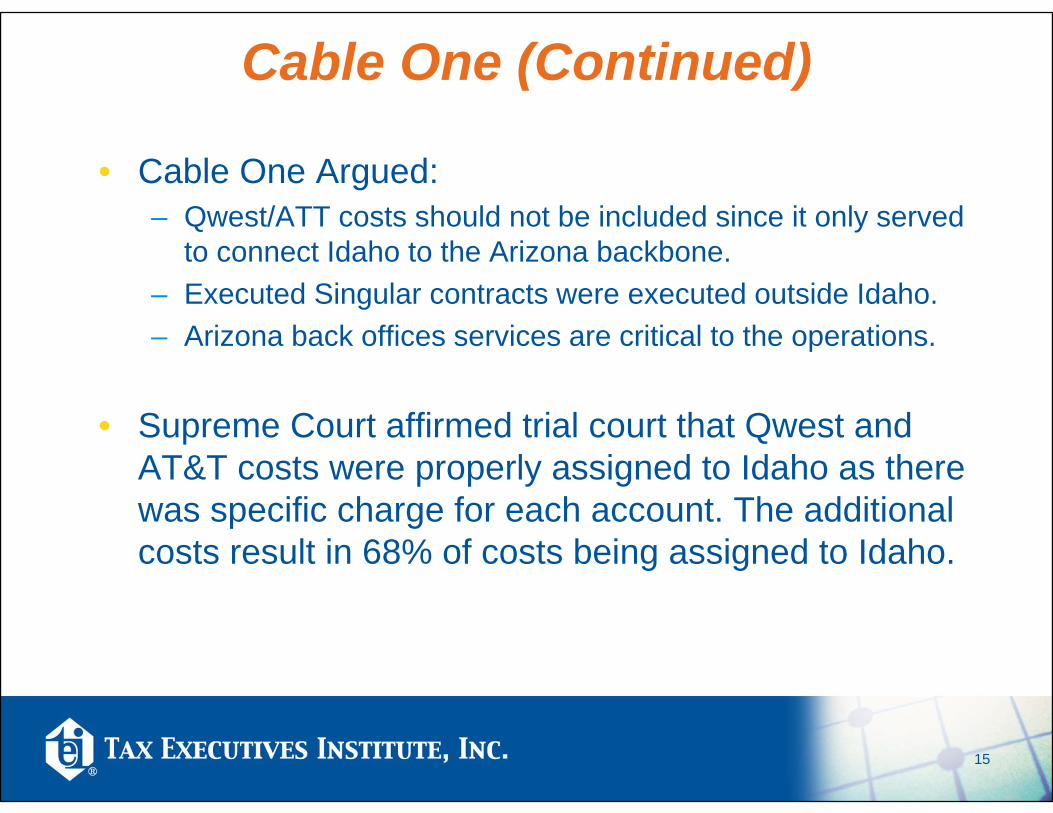

• Cable One Argued:– Qwest/ATT costs should not be included since it only served

to connect Idaho to the Arizona backbone.– Executed Singular contracts were executed outside Idaho.– Arizona back offices services are critical to the operations.

• Supreme Court affirmed trial court that Qwest and AT&T costs were properly assigned to Idaho as there was specific charge for each account. The additional costs result in 68% of costs being assigned to Idaho.

15

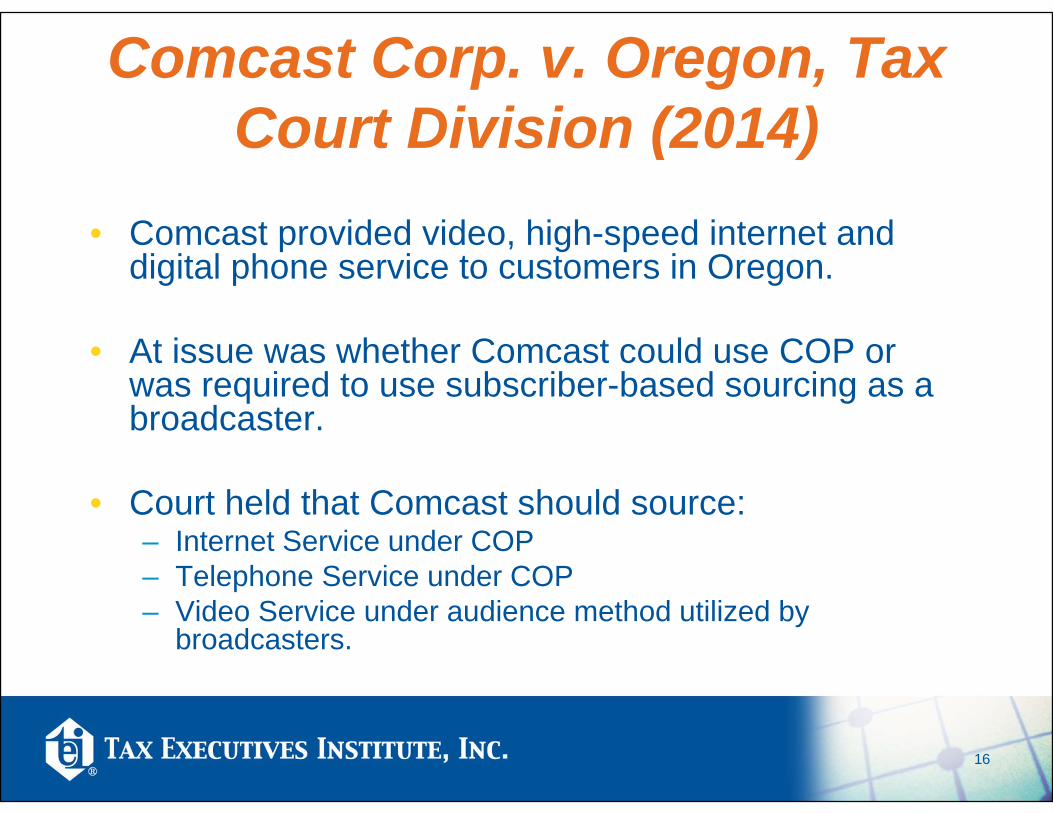

Comcast Corp. v. Oregon, Tax Court Division (2014)

• Comcast provided video, high-speed internet and digital phone service to customers in Oregon.

• At issue was whether Comcast could use COP or was required to use subscriber-based sourcing as a broadcaster.

• Court held that Comcast should source:– Internet Service under COP– Telephone Service under COP– Video Service under audience method utilized by

broadcasters.

16

Dish DBS Corporation v. South Carolina (2015)

• Echostar provides satellite television in SC. Five components to service: 1) programming; 2) uplink; 3) satellite; 4) roof top dish; and 5) set top box.

• Echostar used alternating sourcing methods over audit period including cost of performance.

• South Carolina argued that it Echostar should source based on subscribers.

17

Dish DBS (Continued)• Commission decided South Carolina is not a

strict cost of performance state and that the statute could be interpreted to apply a flexible standard that may vary amongst industries.

• Denied summary judgment as there were insufficient facts in the record to determine where Echostar’s income producing activity occurred (e.g., subscriber, uplink, broadcast centers, etc…).

18

DirectTV v. South Carolina (2015)

• DirectTV provided satellite television service to South Carolinas Subscribers and was denied refund claim by South Carolina Dept. of Revenue which argued that it should source its receipts based on subscribers.

• Department supported that result with the position that the income-producing activity was the delivery of the signal into the homes. Taxpayer argued that such activities were identified using “value drivers”: content and programming, acquisition and distribution of content to customers, marketing and sale of the service, and customer services.

19

DirectTV (Continued)

• Commission decided that:– DirectTV “failed to sufficiently identify its outside

income-producing activities.” “While DirectTV may rely heavily upon ‘value drivers’ in determining the value of certain components within its company, DirectTV has, as aforementioned, failed to sufficiently demonstrate whether and to what extent those value drivers are income producing activities. . . . “Furthermore, even if it had identified those activities, DirectTV failed to sufficiently establish that those activities should be sourced elsewhere.”

20

Skechers USA v. Wisconsin,Tax Appeals Comm. (2015)

• In Wisconsin, if income producing activity is performed in more than one state, the sales are divided based upon the proportion of direct costs incurred in each state.

• SKII was an intangible holding company, licensing the use of intangibles in Wisconsin and elsewhere to its affiliate.

• SKII had no offices, employees, or representatives in Wisconsin. The licensing agreements were negotiated and executed outside Wisconsin.

21

Skechers (Continued)• SKII designed and developed the brand from

outside the state and Skechers and not SKII controlled how and where the IP was used.

• Wisconsin adopted market sourcing only in 2009.

• Because SKII engaged in no activities in Wisconsin and its affiliates activities cannot be attributed to it, SKII had no income producing activities in Wisconsin.

22

AT&T V. Massachusetts Appeals Court of Mass. (2012)

• AT&T filed refund claim and argued that its interstate telephone service should be sourced using a income producing methodology.

• Income producing activity is “a transaction, procedure, or operation directly engaged in by ta taxpayer which results in a separately identifiable item of income.”

• AT&T argued that the income producing activity for its interstate calls includes the global telecommunications network based in NJ.

23

AT&T V. Massachusetts (Continued)

• Board agreed with AT&T as to use of the operational approach. The Board also did not include cost/activities of local exchanges and

• Operational v. Transactional Analysis at issue.

• Court affirms use of operation test in part because of the difficulty of administering the transactional.

24

AT&T V. OregonOregon Supreme CT. (2015)

• AT&T filed refund claim and argued that is should be able to use an “operational/network” approach for purposes of determining where its income producing activity occurs.

• Oregon challenges and argues for application of the transactional test.

25

AT&T v. Oregon (Continued)

• Court agrees with Department of Revenue’s interpretation of statute such that income producing activity is something associated with individual items and of income and that equates to individual sales.

• Court holds that AT&T did not meet its burden of proving that greater amount of costs related to interstate calls were incurred outside Oregon.

26

Cost of Performance –Take Away

• Cost of Performance analysis is dynamic. • “Items of Income” and “Income Producing

Activity” are determinative.• Variations may exist for different industries.• Potential “all or nothing” result is problematic –

see Sec. 18.• State’s concerned about revenue and “nowhere

sales.”

27

28

MBS - Overview

• Given the states’ relatively recent legislative transition to MBS there is a lack of judicial guidance.

• Currently, primary focus is on statutory language, regulatory promulgations and other guidance issued by the taxing authorities.

• Presents both challenges and opportunities to taxpayers.

29

MBS - Overview

• MBS primarily impacts the sourcing of revenue derived from services and intangibles as most states have retained their rules regarding the sourcing of sales of tangible and real property and/or the leases thereof.

• Destination still reigns supreme for sales of tangible personal property.

• Situs of or use of real or tangible property still forms basis for sourcing lease revenue.

30

MBS - Overview

• Service providers have to navigate each state’s rules in determining the “market” to appropriately source their revenue.• OH has 50 separate sourcing regimes for

enumerated services.• Issues include determining:

• Where the service is received;• Where the benefit of the service is

received;• Where the customer is located; • Where the service is delivered.

31

MBS - Overview • Sourcing revenue from intangible property

(patents, trademarks, other intellectual property) presents as many issues as sourcing revenue from services. • License v. sales of intangibles (see CA

below)

• Issues include determining:• Where employed to produce another

product;• Where are royalties exploited;• Where is the property located.

32

MBS - Other Issues• Other issues to contemplate when employing

MBS:• Proportional MBS (e.g. IL, PA);• Hierarchy of Sourcing Rules (e.g., NYS/C, MA);

• Good faith standard• Due Diligence• Conformity/Consistency• Business or Individual Customer

• “Reasonable” Approximation (e.g., CA, MA);• Throw-out Rule(e.g. IL, MA).

33

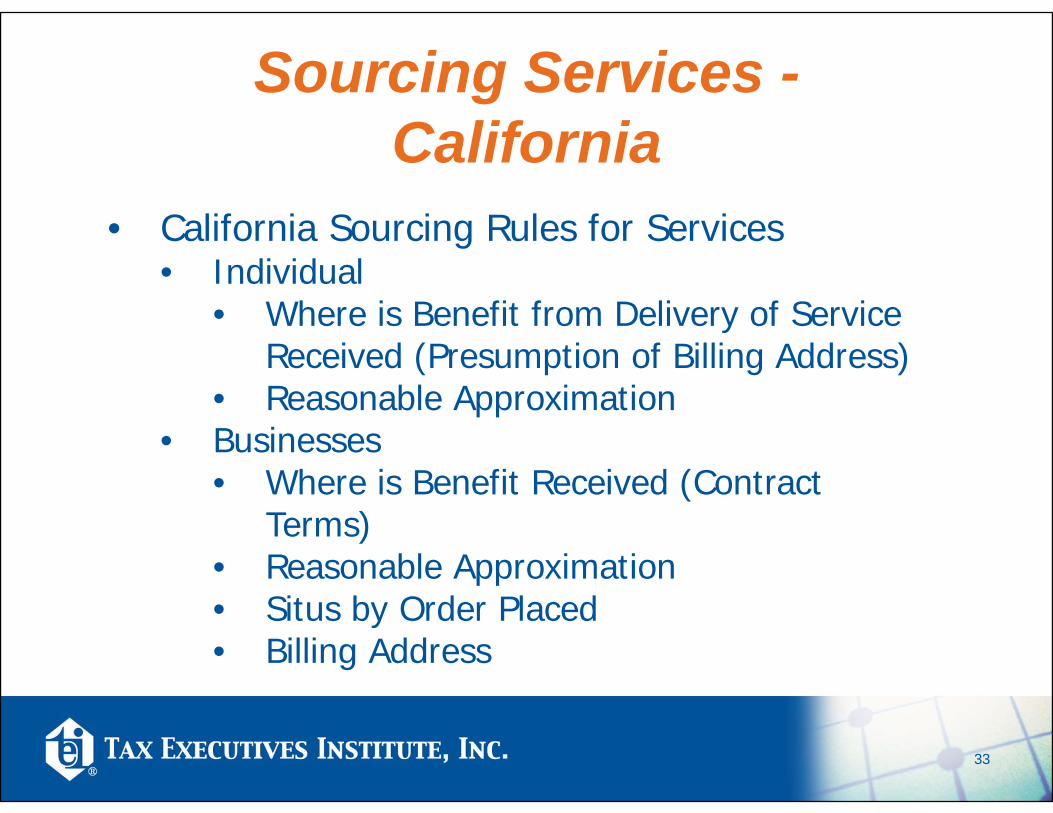

Sourcing Services -California

• California Sourcing Rules for Services• Individual

• Where is Benefit from Delivery of Service Received (Presumption of Billing Address)

• Reasonable Approximation• Businesses

• Where is Benefit Received (Contract Terms)

• Reasonable Approximation• Situs by Order Placed• Billing Address

34

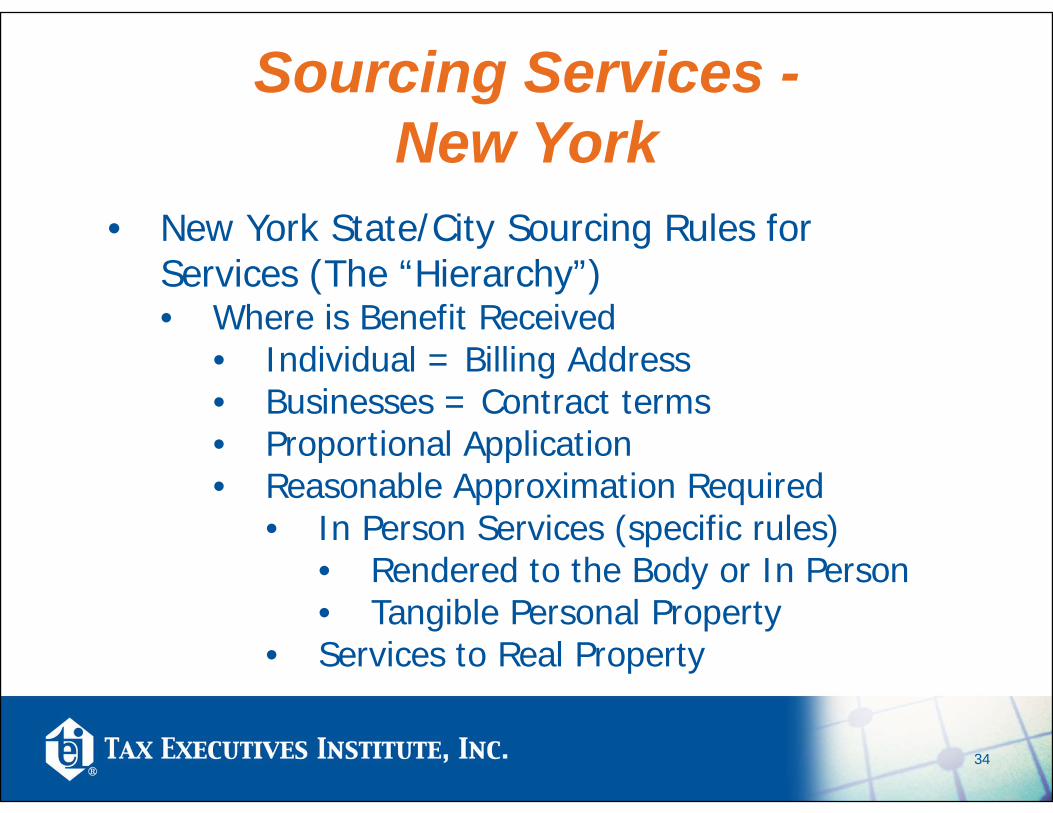

Sourcing Services -New York

• New York State/City Sourcing Rules for Services (The “Hierarchy”)• Where is Benefit Received

• Individual = Billing Address• Businesses = Contract terms• Proportional Application • Reasonable Approximation Required

• In Person Services (specific rules)• Rendered to the Body or In Person • Tangible Personal Property

• Services to Real Property

35

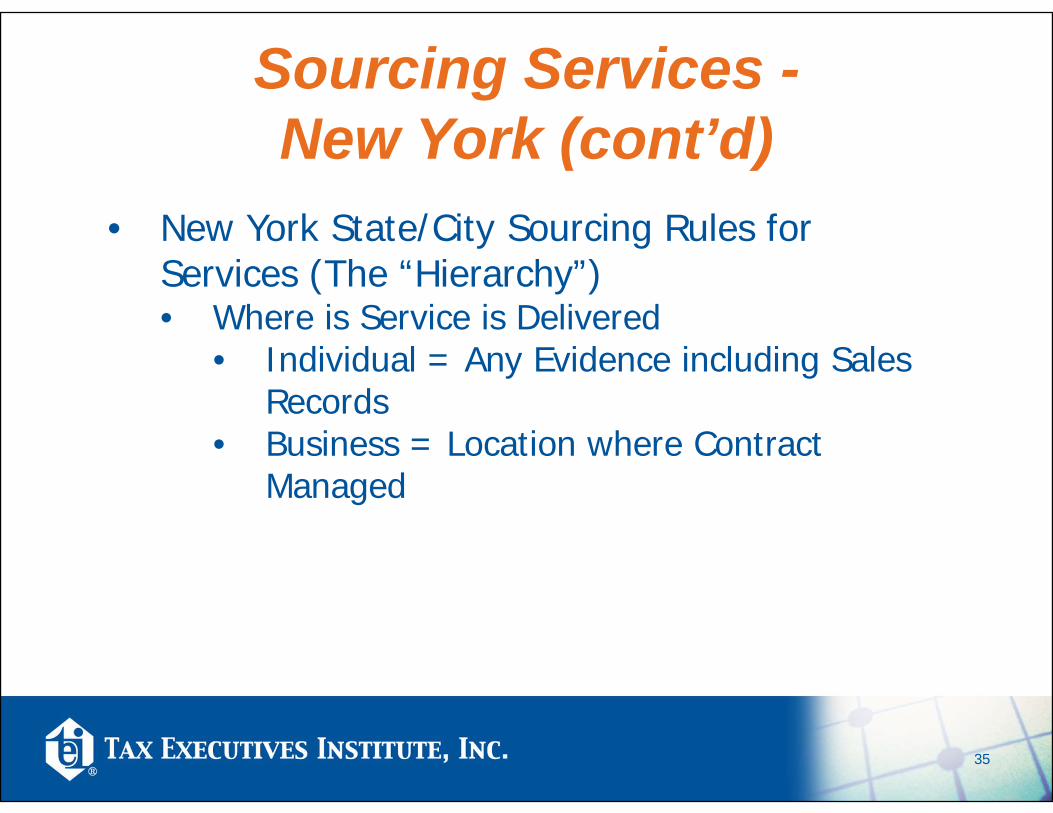

Sourcing Services -New York (cont’d)

• New York State/City Sourcing Rules for Services (The “Hierarchy”)• Where is Service is Delivered

• Individual = Any Evidence including Sales Records

• Business = Location where Contract Managed

36

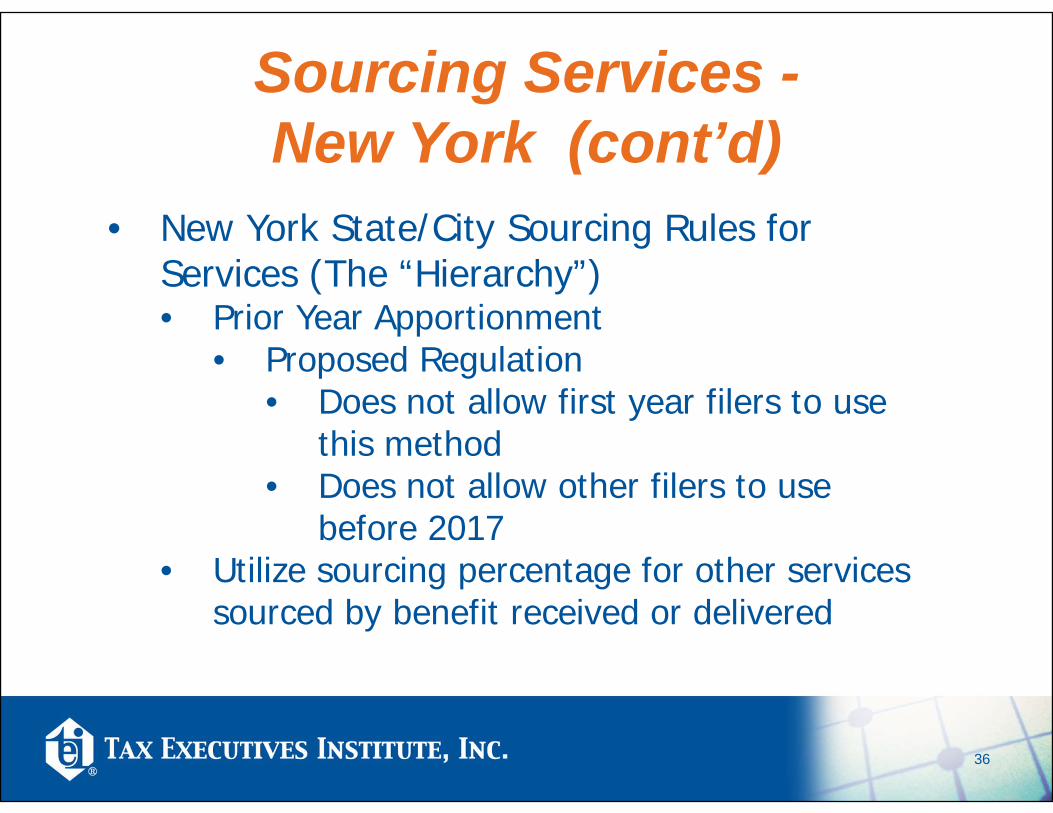

Sourcing Services -New York (cont’d)

• New York State/City Sourcing Rules for Services (The “Hierarchy”)• Prior Year Apportionment

• Proposed Regulation• Does not allow first year filers to use

this method• Does not allow other filers to use

before 2017• Utilize sourcing percentage for other services

sourced by benefit received or delivered

37

Sourcing Services -New York (cont’d)

• New York State/City Sourcing Rules for Services• Intermediary Services

• Services “on behalf of” an intermediary is a service that is provided on directly to a consumer at the direction of an intermediary:• Benefit Received or Delivered to Consumer.• Benefit Delivered to Intermediary.• Prior Year Sourcing Rule.• Utilize sourcing percentage for other services

sourced by benefit received or delivered.

38

Sourcing Other Services -New York (cont’d)

• New York State/City Sourcing Rules for Services• Intermediary Services

• Services provided “ through” an intermediary is a service that is sold to an intermediary who then passes on the service to the consumer:• Benefit Received or Delivered to Consumer.• Benefit Received to Intermediary.• Prior Year Sourcing.• Utilize sourcing percentage for other services

sourced by benefit received or delivered.

39

Sourcing Services -Pennsylvania

• Pennsylvania Sourcing Rules for Services• Services are sourced to PA if the service is

delivered to a location in Pennsylvania.• Proportional sourcing if service is delivered

within and without the State.• If cannot determine where delivered

• Individual = Billing address• Business = Situs of where Service is

ordered

40

Sourcing Intangibles Income - Illinois

• Illinois• Patents

• Good Produced in IL• Utilization of Patent in IL /

Everywhere• Copyrights

• Printing Occurs in IL• Utilization in IL / Everywhere

• Trademarks• Source to Commercial Dom of

Licensee

41

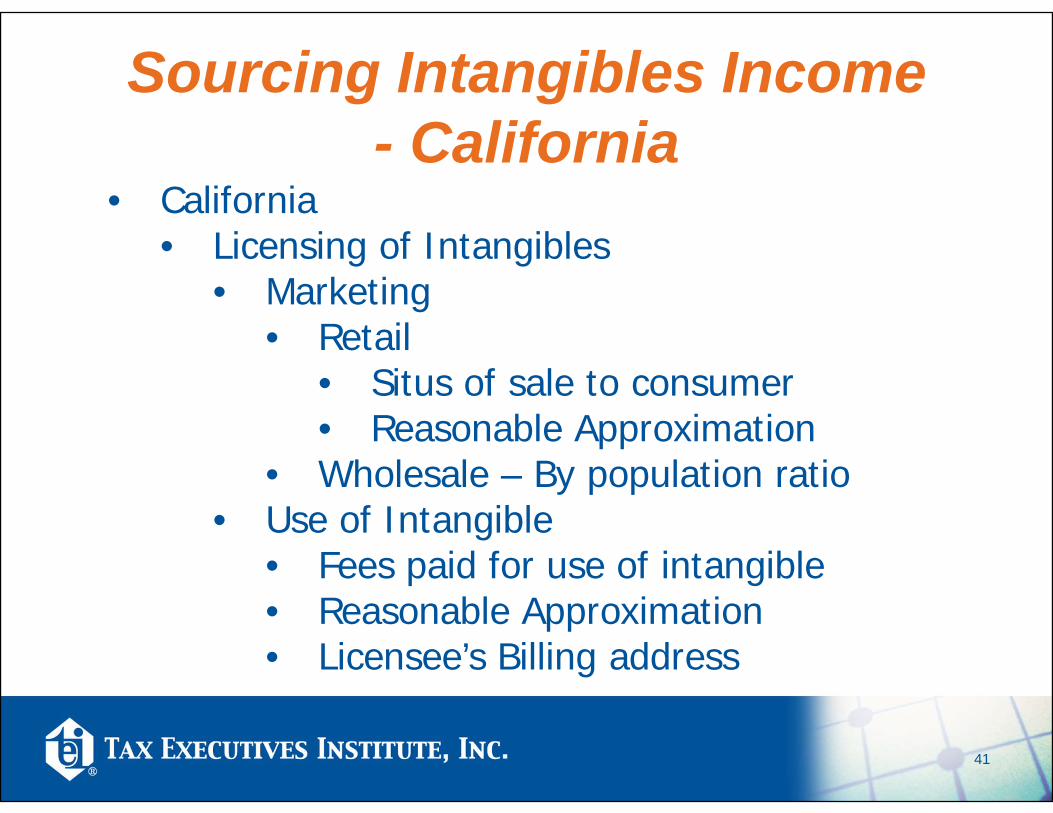

Sourcing Intangibles Income - California

• California• Licensing of Intangibles

• Marketing • Retail

• Situs of sale to consumer• Reasonable Approximation

• Wholesale – By population ratio• Use of Intangible

• Fees paid for use of intangible• Reasonable Approximation• Licensee’s Billing address

42

Sourcing Intangibles Income - California (cont’d)

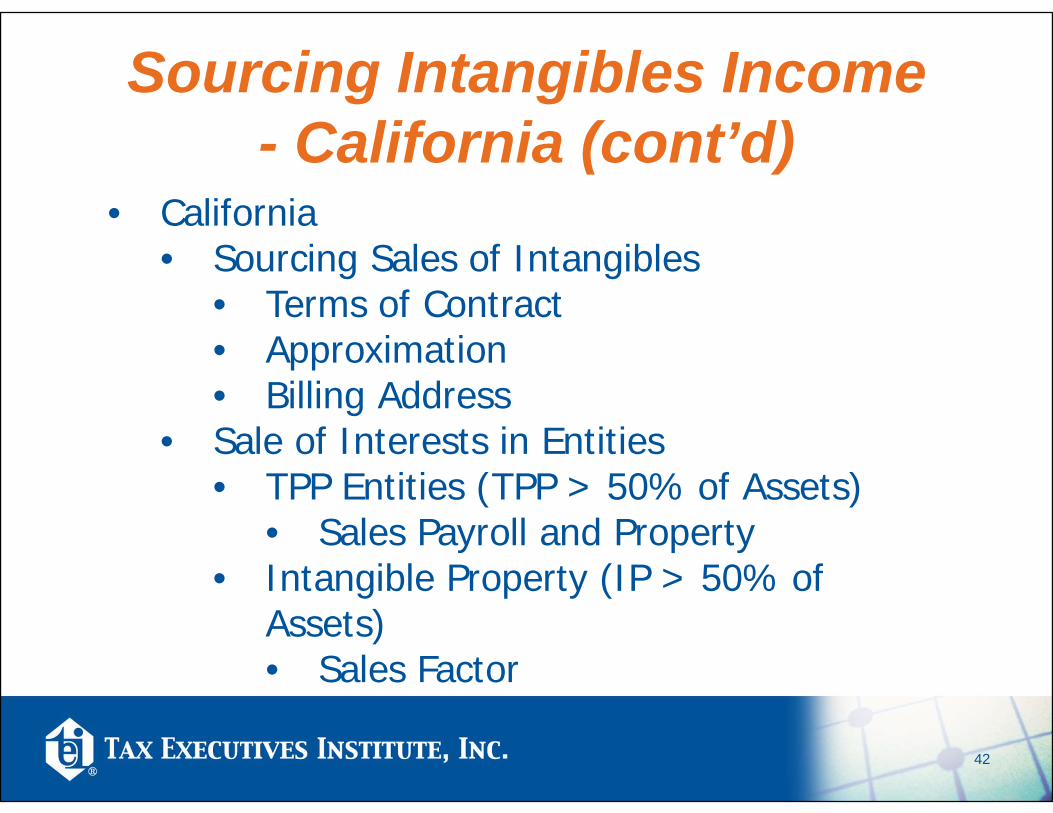

• California• Sourcing Sales of Intangibles

• Terms of Contract• Approximation• Billing Address

• Sale of Interests in Entities• TPP Entities (TPP > 50% of Assets)

• Sales Payroll and Property• Intangible Property (IP > 50% of

Assets)• Sales Factor

43

Sourcing Intangibles Income - Pennsylvania

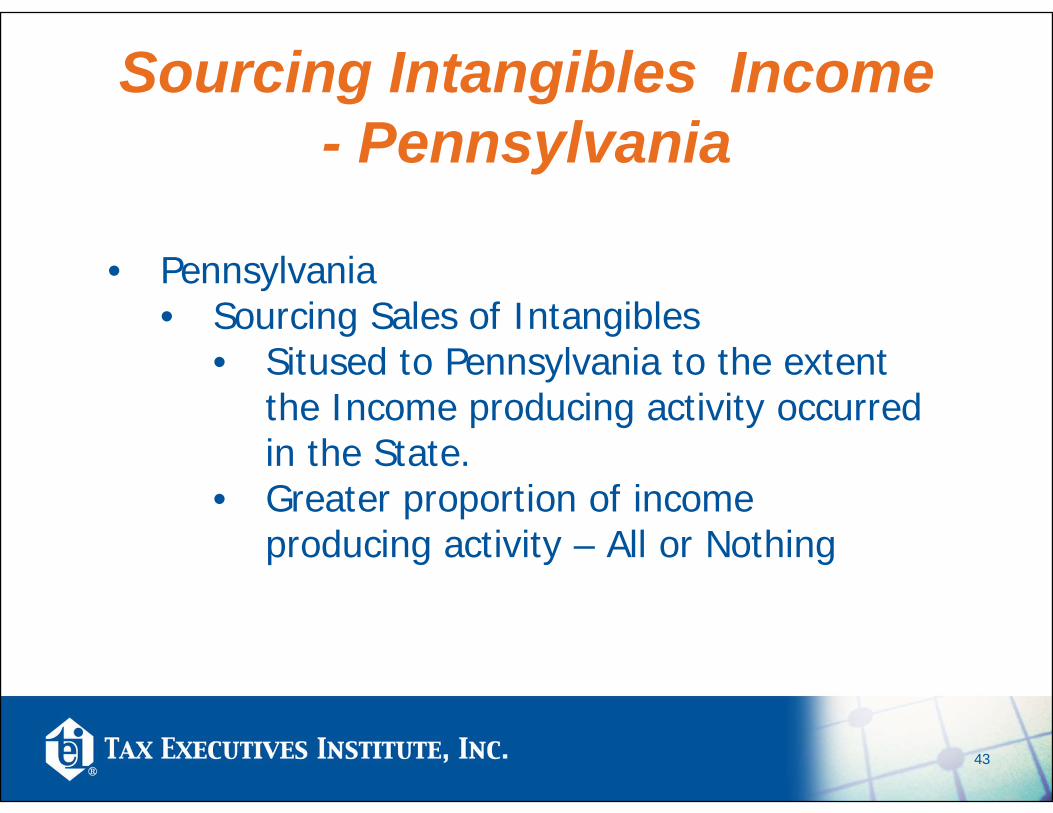

• Pennsylvania• Sourcing Sales of Intangibles

• Sitused to Pennsylvania to the extent the Income producing activity occurred in the State.

• Greater proportion of income producing activity – All or Nothing

44

Sourcing Intangibles Income -Lack of Conformity

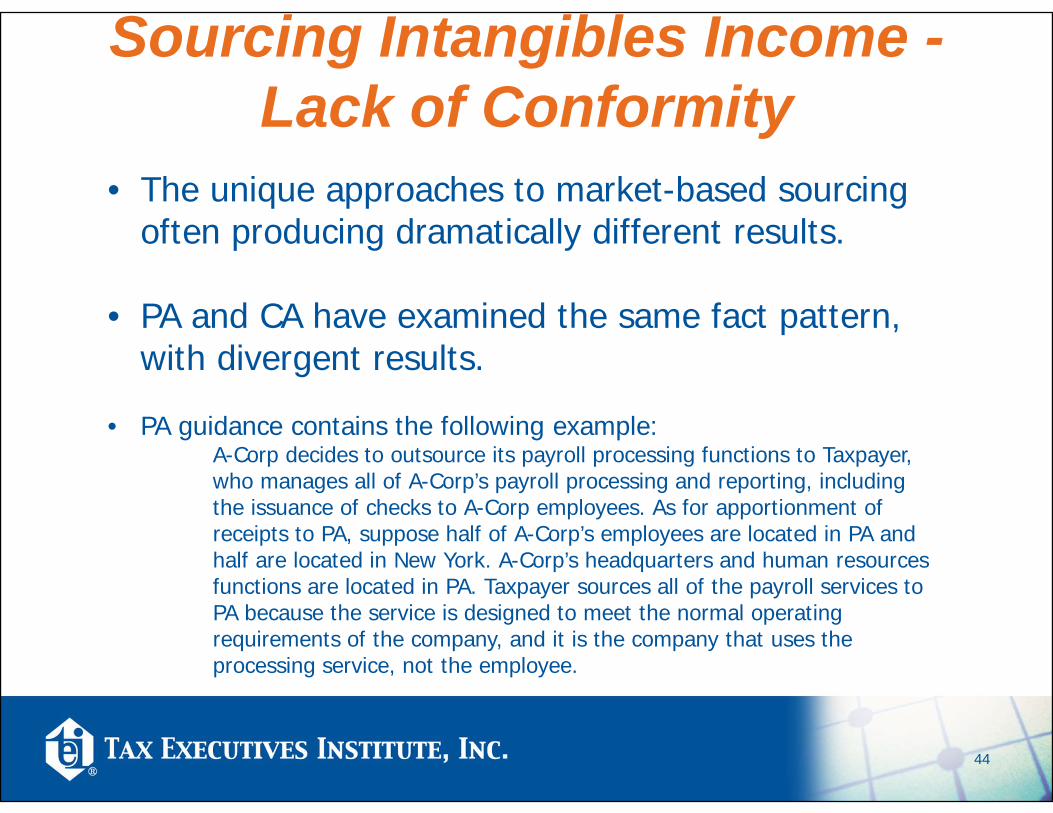

• The unique approaches to market-based sourcing often producing dramatically different results.

• PA and CA have examined the same fact pattern, with divergent results.

• PA guidance contains the following example: A-Corp decides to outsource its payroll processing functions to Taxpayer, who manages all of A-Corp’s payroll processing and reporting, including the issuance of checks to A-Corp employees. As for apportionment of receipts to PA, suppose half of A-Corp’s employees are located in PA and half are located in New York. A-Corp’s headquarters and human resources functions are located in PA. Taxpayer sources all of the payroll services to PA because the service is designed to meet the normal operating requirements of the company, and it is the company that uses the processing service, not the employee.

45

Sourcing Intangibles Income - Lack of Conformity (cont’d)

This result is directly contrary to California’s regulation, which provides that the payroll servicing company should assign its receipts by determining the ratio of employees of the customer in California compared to all employees of the customer and assign that percentage of the receipts to California. Cal. Code Regs. 25136-2(b)(1).

Multistate Tax Commission• Attempt to harmonize state MBS laws to provide

taxpayers more consistency and improve their ability to comply.

• Revisions to MTC Section 17.

• Proposed MTC Regulations.

46

MTC Revised Sec. 17• (a) Receipts, other than receipts described in Section

16, are in this State if the taxpayer’s market for the sales is in this state. The taxpayer’s market for sales is in this state: – (1) in the case of sale, rental, lease or license of

real property, if and to the extent the property is located in this state;

– (2) in the case of rental, lease or license of tangible personal property, if and to the extent the property is located in this state;

– (3) in the case of sale of a service, if and to the extent the service is delivered to a location in this state; and

47

MTC Revised Sec. 17

– (4) in the case of intangible property, • (i) that is rented, leased, or licensed, if and to the

extent the property is used in this state, provided that intangible property utilized in marketing a good or service to a consumer is “used in this state” if that good or service is purchased by a consumer who is in this state; and

48

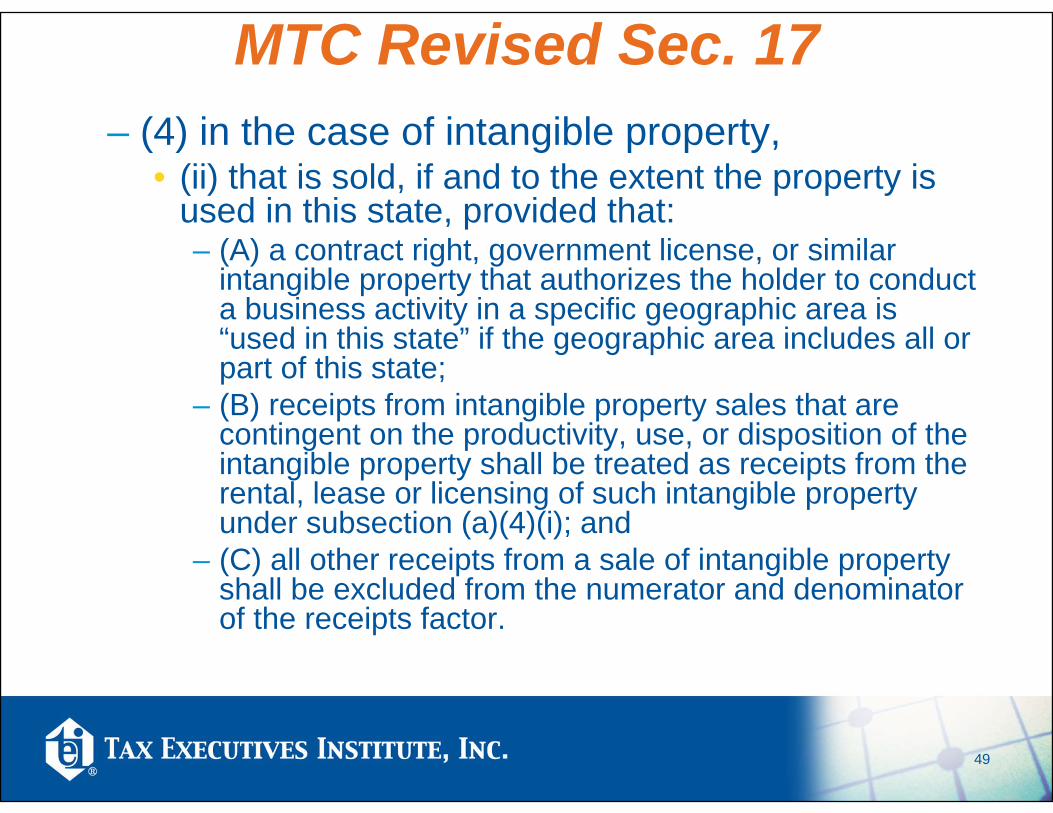

MTC Revised Sec. 17– (4) in the case of intangible property,

• (ii) that is sold, if and to the extent the property is used in this state, provided that: – (A) a contract right, government license, or similar

intangible property that authorizes the holder to conduct a business activity in a specific geographic area is “used in this state” if the geographic area includes all or part of this state;

– (B) receipts from intangible property sales that are contingent on the productivity, use, or disposition of the intangible property shall be treated as receipts from the rental, lease or licensing of such intangible property under subsection (a)(4)(i); and

– (C) all other receipts from a sale of intangible property shall be excluded from the numerator and denominator of the receipts factor.

49

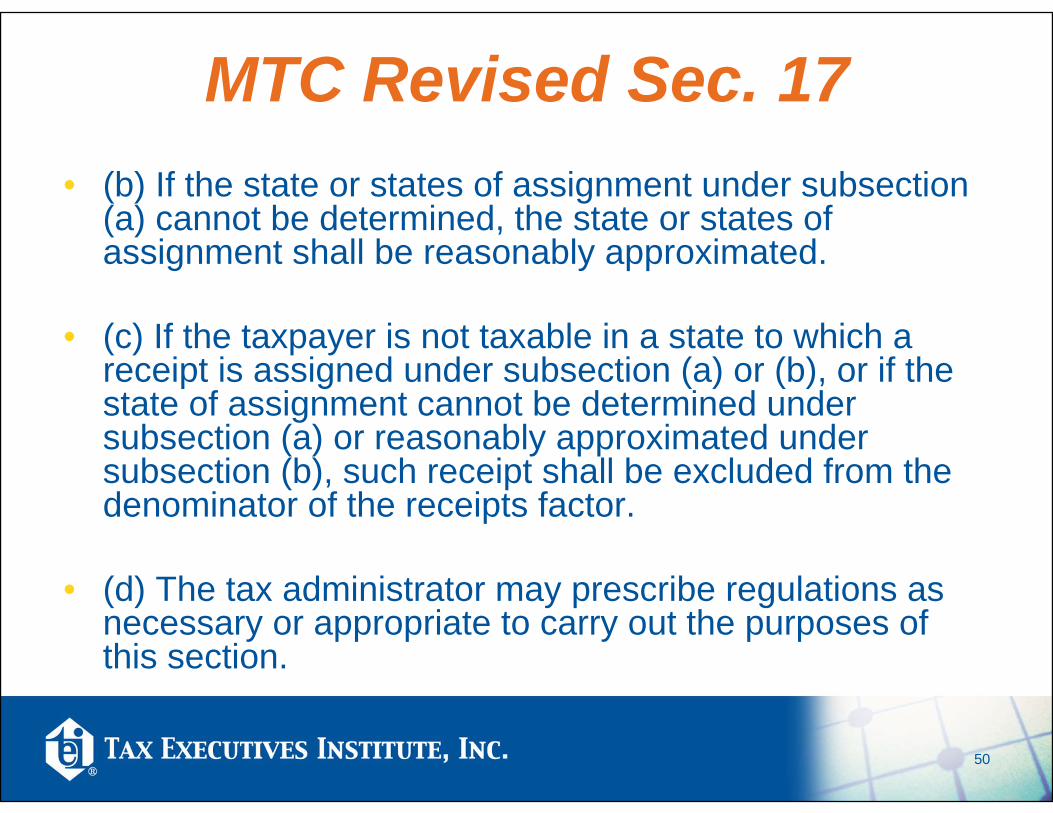

MTC Revised Sec. 17• (b) If the state or states of assignment under subsection

(a) cannot be determined, the state or states of assignment shall be reasonably approximated.

• (c) If the taxpayer is not taxable in a state to which a receipt is assigned under subsection (a) or (b), or if the state of assignment cannot be determined under subsection (a) or reasonably approximated under subsection (b), such receipt shall be excluded from the denominator of the receipts factor.

• (d) The tax administrator may prescribe regulations as necessary or appropriate to carry out the purposes of this section.

50

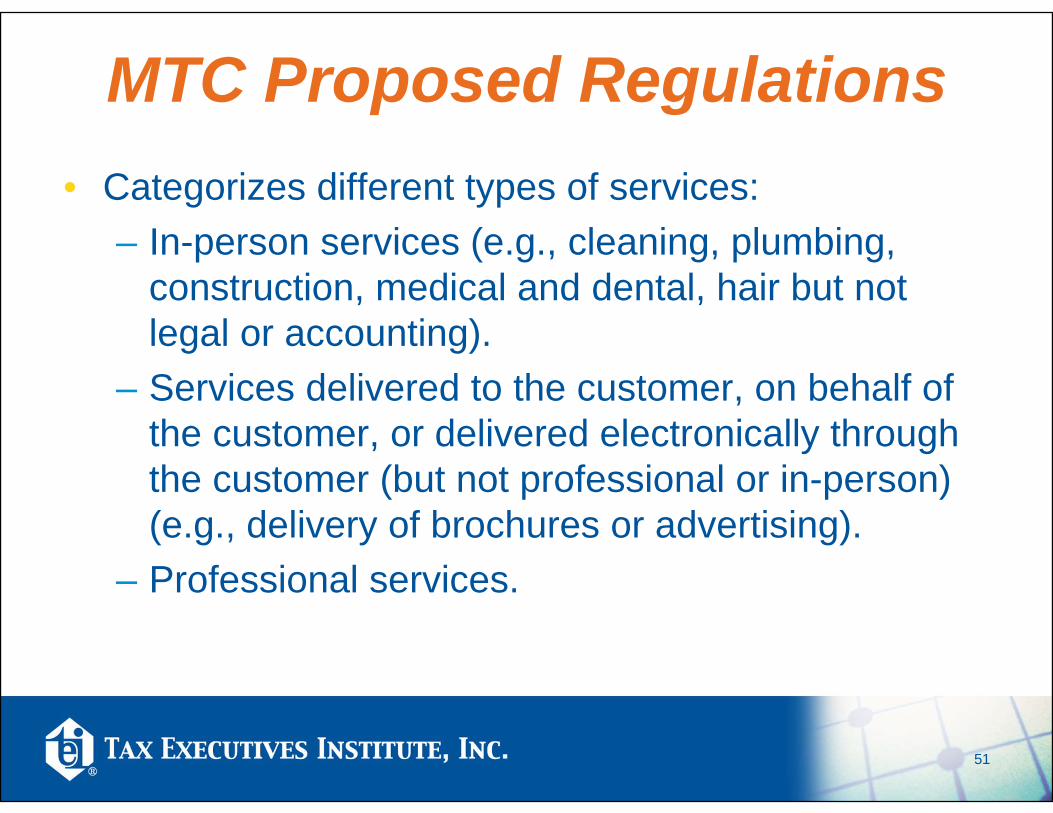

MTC Proposed Regulations• Categorizes different types of services:

– In-person services (e.g., cleaning, plumbing, construction, medical and dental, hair but not legal or accounting).

– Services delivered to the customer, on behalf of the customer, or delivered electronically through the customer (but not professional or in-person) (e.g., delivery of brochures or advertising).

– Professional services.

51

MTC Proposed Regulations• Provisions for the Sales, Rental, Lease or License of

– Real property– Tangible personal property– Intangible property

• Special Rules for– Software transactions– Sales or licenses of digital goods or services– Telecommunication companies

52

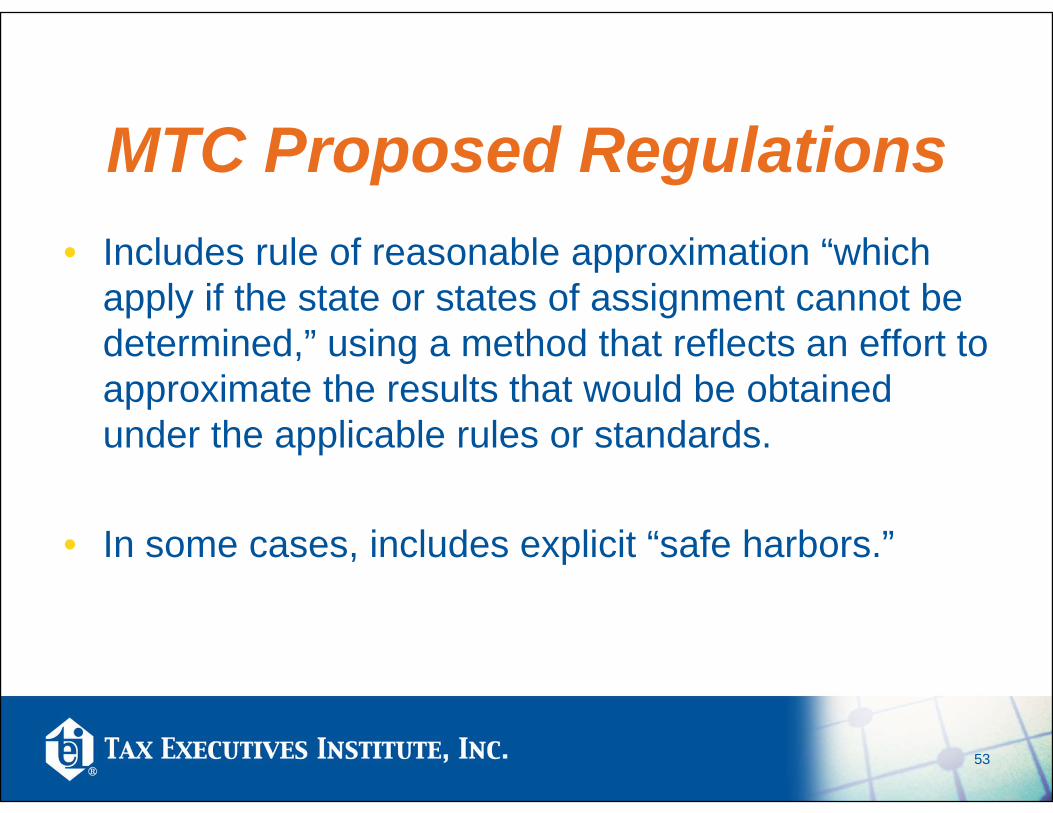

MTC Proposed Regulations• Includes rule of reasonable approximation “which

apply if the state or states of assignment cannot be determined,” using a method that reflects an effort to approximate the results that would be obtained under the applicable rules or standards.

• In some cases, includes explicit “safe harbors.”

53

MTC Proposed RegulationsWhat’s Next?

• Still at least many months away from final adoption by the MTC.

• Will states adopt the MTC revision to Sec. 17?• Will states adopt the regulations?• The MTC expects states customize their own rules.• MTC believes that even though statutes may differ

the result may often still be the same.

54

MTC Proposed RegulationsWhat’s Next?

• Others have observed, however, that the MTC’s delivery concept may conflict to some degree with benefit received states.

• MTC’s model statute and regulations also do not resolve conflict with COP states.

55

56

Potential Pitfalls• Potential Pitfalls

• No precedent on what constitutes good faith

• How much due is due diligence?• Inconsistent interpretation of the market

(e.g., Ca v. Pa on payroll sourcing).• No precedent on where the benefit is

received for services.• Throw-out Rules.• Multiple taxation.

57

Planning Opportunities• Planning Opportunities

• Review and revise various contracts and customer relationships to take advantage of place of billing address or where services are ordered.

• Leveraging default approximation rules.

• Consider shifting where services are performed to take advantage of Income Producing v. MBS rules between states.

Questions?