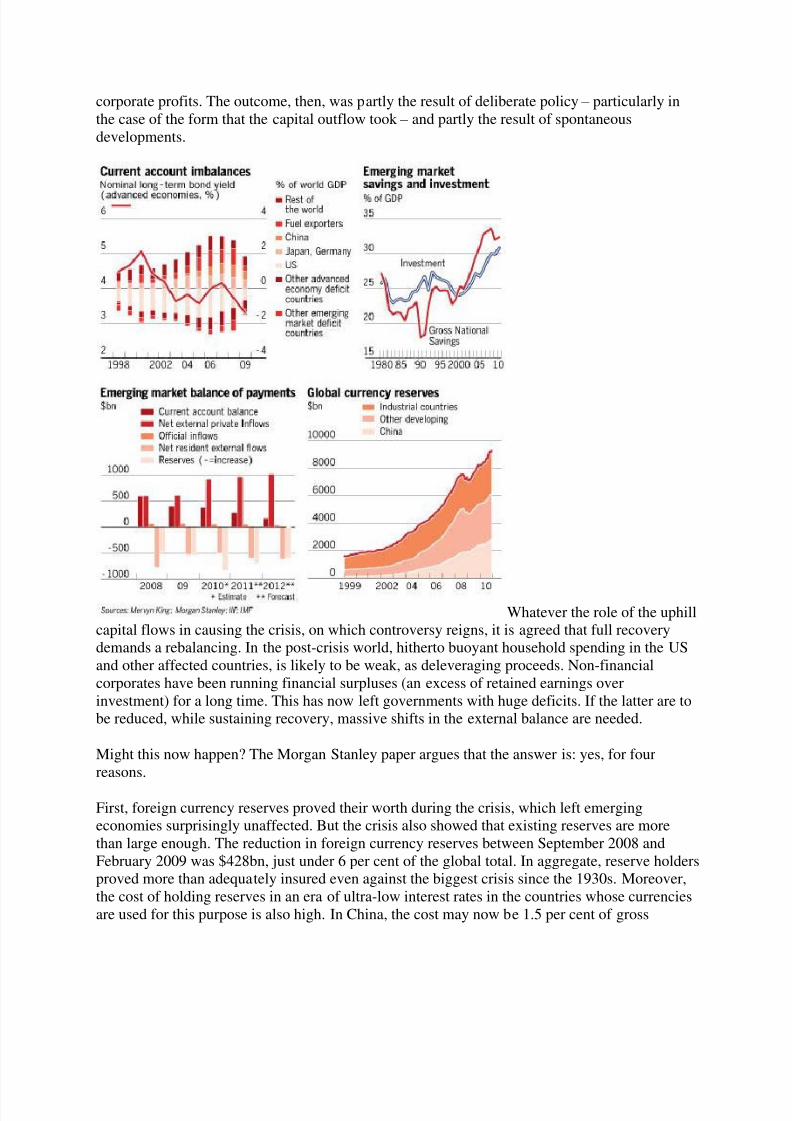

Waiting for the great rebalancing By Martin WolfPublished: April 5 2011 21:19 | Last updated: April 5 2011 21:19 Pressures are building up for a rebalancing o f the world economy. The p rivate sector has long been trying to send a large net flow of capital from the world’s relatively sluggish rich countries to its dynamic emerging ones. But the governments of the latter have resisted, by intervening in currency markets and sending the capital back as official currency reserves. But forces now at work in the world economy seem likely to bring this recycling to a natural end. If so, that would be very helpful, though it would also create new challenges. Mervyn King, governor of the Bank of England, has given an account of the role of the so-called global imbalances in February’s Financial Stability Review of the Banque de France. This “uphill” flow of capital from poor to rich countries, predominantly into supposedly safe assets, had important consequences: a reduction in the real rate of interest; a rise in asset prices, particularly of housing in several countries, not least the US; a reach for yield; a wave offinancial innovation, to create higher yielding, but supposedly safe assets; a boom in residential construction; and ultimately a huge financial crisis. The follies of finance and failures ofregulation bear the blame. But global developments –not just the so-called “savings glut, but the form that those flows took–helped create the conditions for the disaster. Indeed, a clear correlation exists between the rise in non-performing loans during the crisis and countries’ initial current account positions. As Mr King also notes, the underlying determinant was a surge in savings in already surplus regions even greater than their rise in investment. In another recent paper, for Morgan Stanley, entitledThe Great Rebalancing, Alan Taylor of the University of California at Davis and Manoj Pradhan, show the same thing, this time for emerging countries specifically (see chart). Why then did the surge in savings take place? Mr King suggests three explanations: a shift towards export-promotion, which created the need for highly competitive real exchange rates; a decision to accumulate foreign currency reserves, in the aftermath of the financial crises of the 1990s; and the combination of low levels of financial development with inadequate social safety nets, which encouraged higher savings. In China, one would also have to add the surge in