Embed Size (px)

Citation preview

Medium-Term Expenditure Frameworks (MTEF):

Logic, Benefits, Limitations

Ronnie Downes, OECD Results-Based Planning, Budgeting, Monitoring & Evaluation

Chengdu City, China 12-16 August 2013

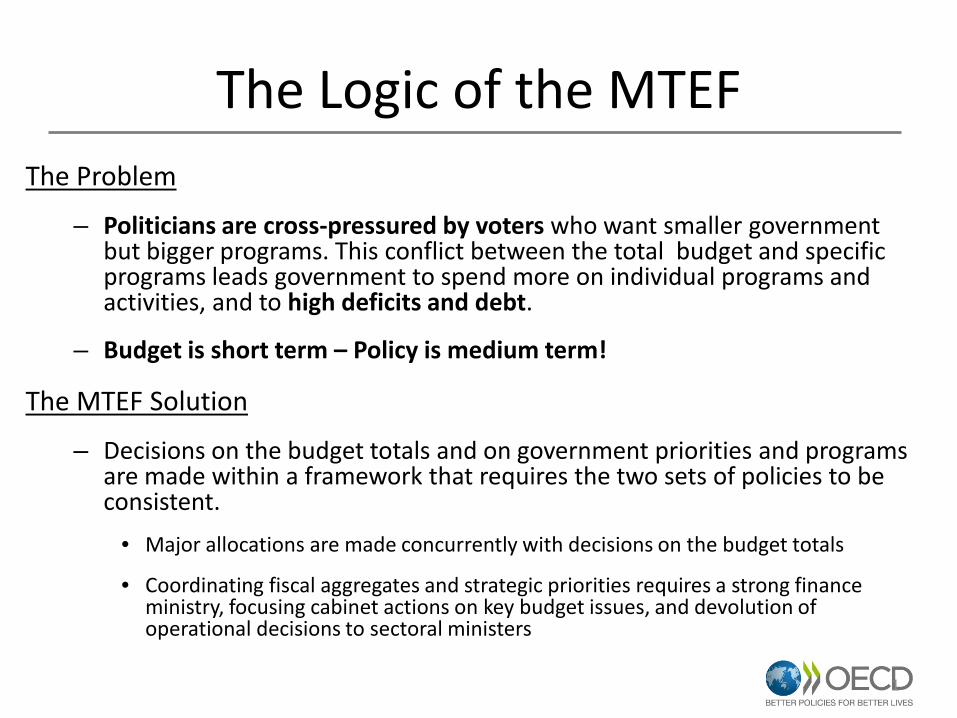

The Logic of the MTEF The Problem

– Politicians are cross-pressured by voters who want smaller government but bigger programs. This conflict between the total budget and specific programs leads government to spend more on individual programs and activities, and to high deficits and debt.

– Budget is short term – Policy is medium term!

The MTEF Solution

– Decisions on the budget totals and on government priorities and programs are made within a framework that requires the two sets of policies to be consistent.

• Major allocations are made concurrently with decisions on the budget totals

• Coordinating fiscal aggregates and strategic priorities requires a strong finance ministry, focusing cabinet actions on key budget issues, and devolution of operational decisions to sectoral ministers

1

Year 0 Year 1 Year 2 Year 3

Savings on existing programmes

Fiscal space for new programmes

Expenditure ceilings

MTEF Projections Policy and Contingency reserve

Cost of existing programs and new initiatives

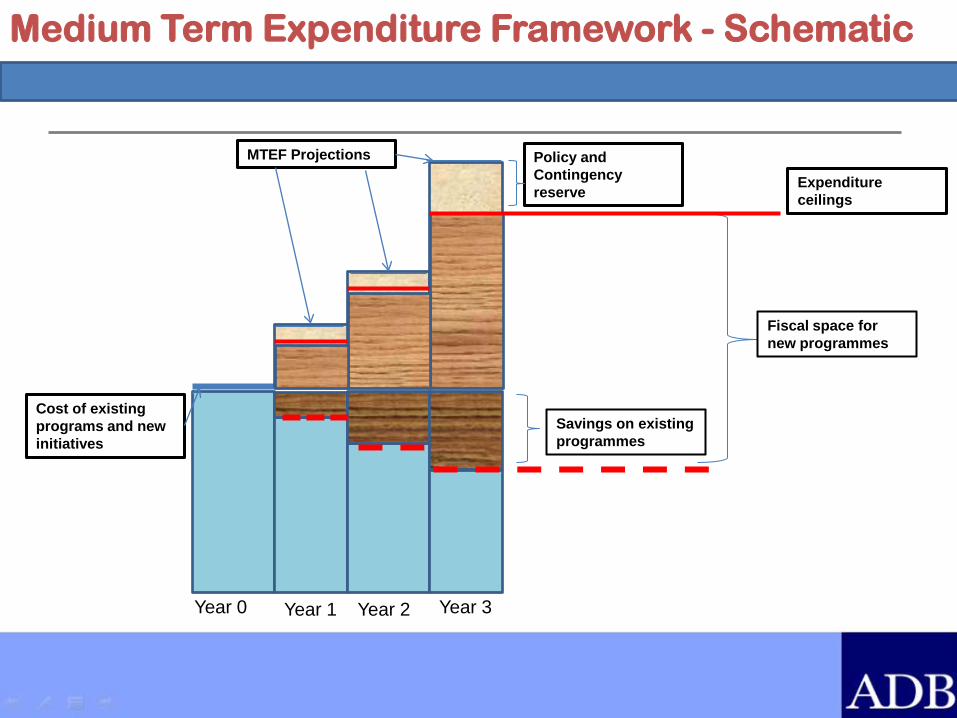

Medium Term Expenditure Framework - Schematic

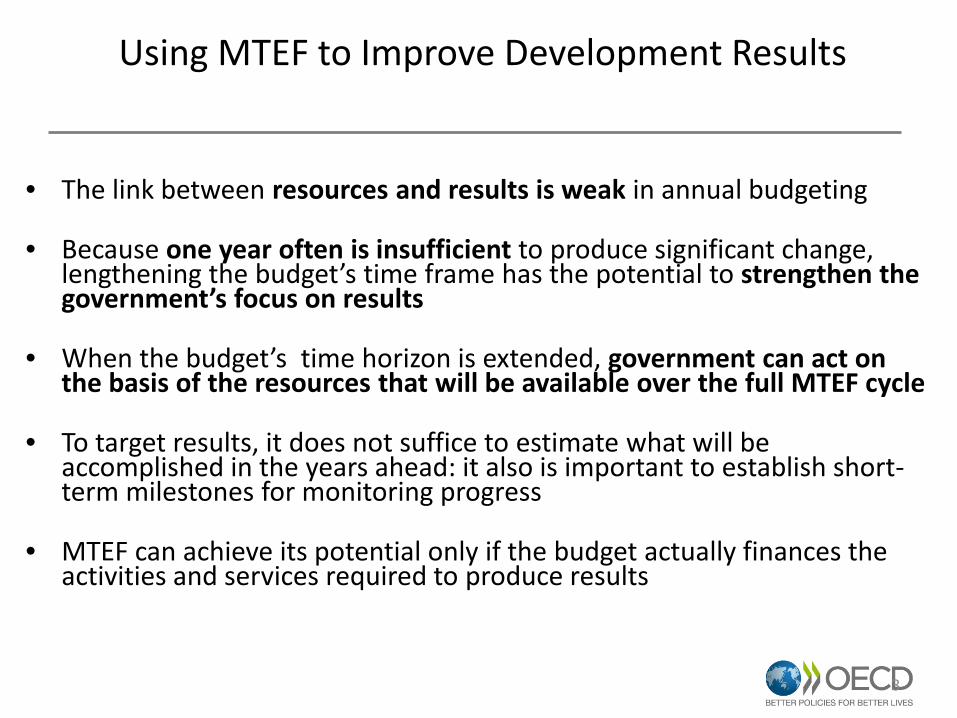

Using MTEF to Improve Development Results

• The link between resources and results is weak in annual budgeting

• Because one year often is insufficient to produce significant change, lengthening the budget’s time frame has the potential to strengthen the government’s focus on results

• When the budget’s time horizon is extended, government can act on the basis of the resources that will be available over the full MTEF cycle

• To target results, it does not suffice to estimate what will be accomplished in the years ahead: it also is important to establish short-term milestones for monitoring progress

• MTEF can achieve its potential only if the budget actually finances the activities and services required to produce results

3

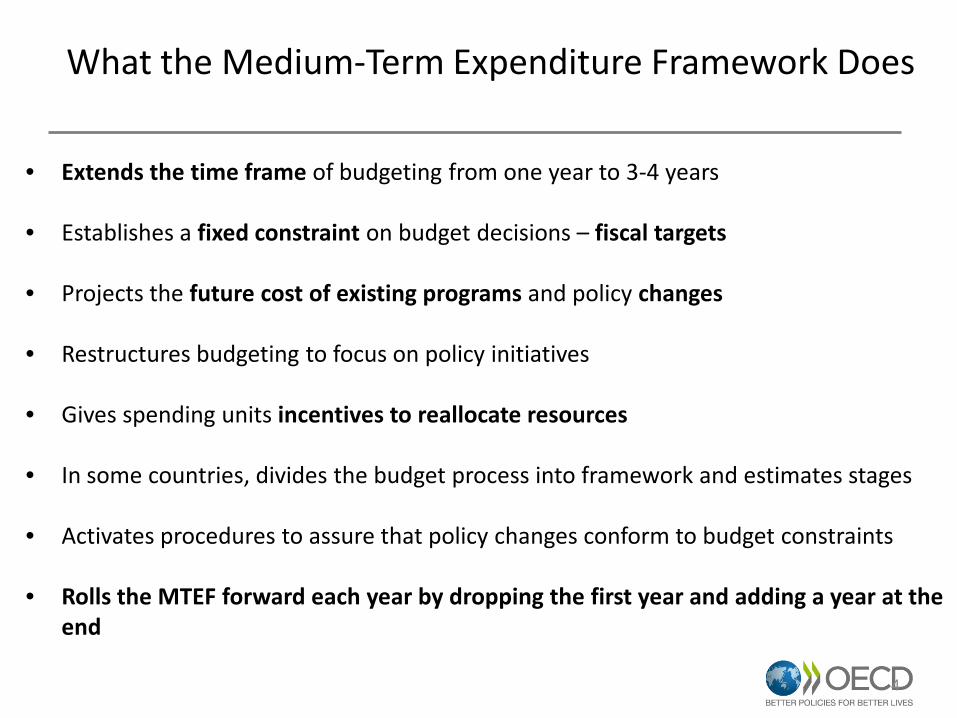

What the Medium-Term Expenditure Framework Does

• Extends the time frame of budgeting from one year to 3-4 years

• Establishes a fixed constraint on budget decisions – fiscal targets

• Projects the future cost of existing programs and policy changes

• Restructures budgeting to focus on policy initiatives

• Gives spending units incentives to reallocate resources

• In some countries, divides the budget process into framework and estimates stages

• Activates procedures to assure that policy changes conform to budget constraints

• Rolls the MTEF forward each year by dropping the first year and adding a year at the end

4

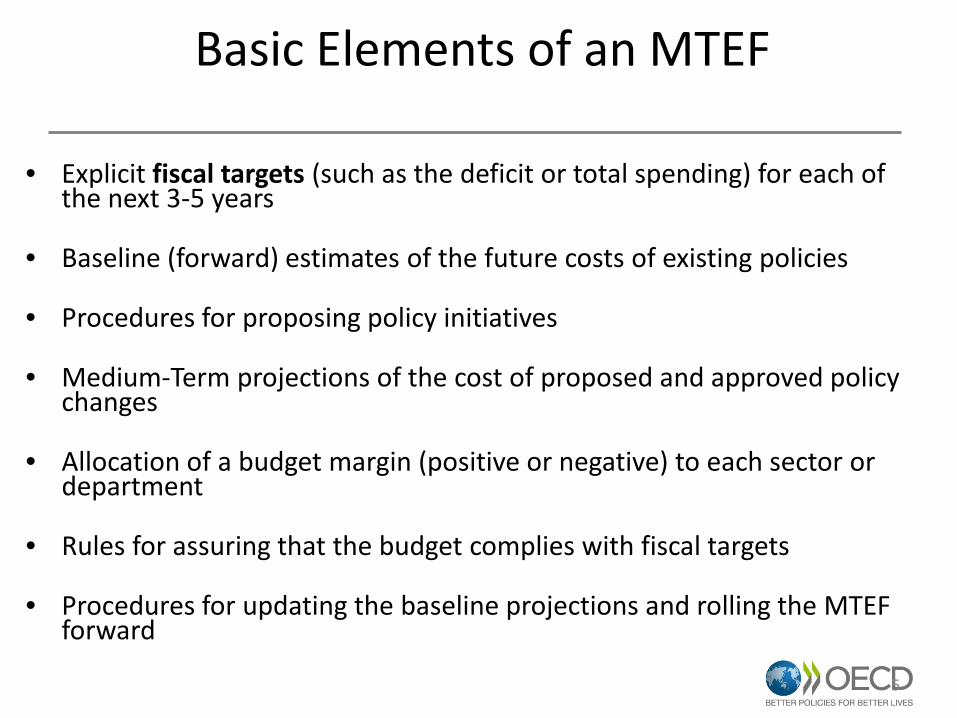

Basic Elements of an MTEF

• Explicit fiscal targets (such as the deficit or total spending) for each of the next 3-5 years

• Baseline (forward) estimates of the future costs of existing policies

• Procedures for proposing policy initiatives

• Medium-Term projections of the cost of proposed and approved policy changes

• Allocation of a budget margin (positive or negative) to each sector or department

• Rules for assuring that the budget complies with fiscal targets

• Procedures for updating the baseline projections and rolling the MTEF forward

5

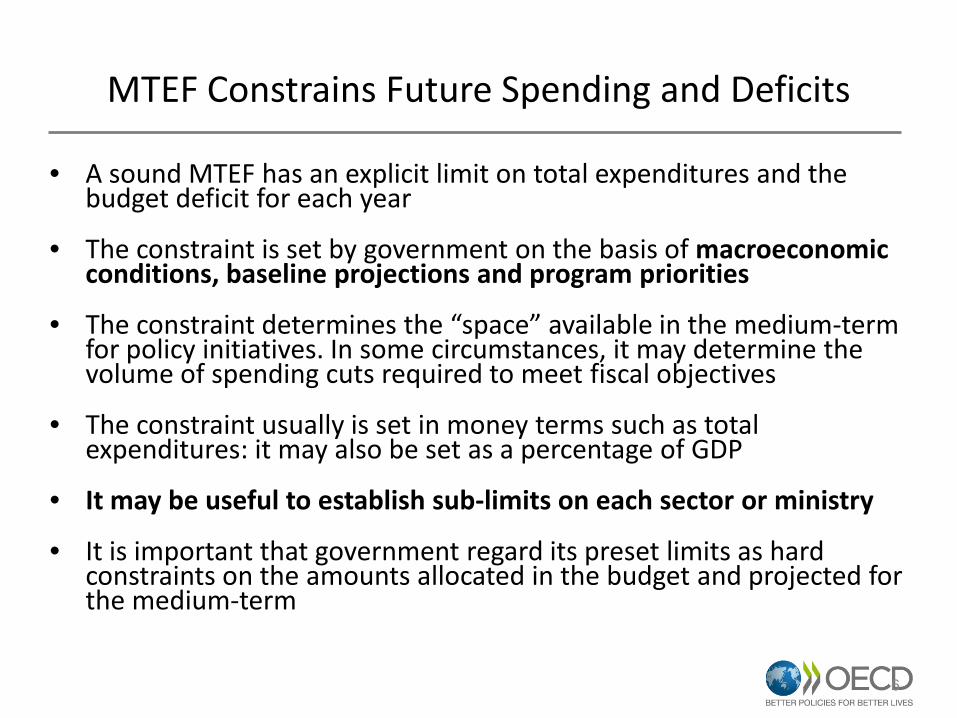

MTEF Constrains Future Spending and Deficits

• A sound MTEF has an explicit limit on total expenditures and the budget deficit for each year

• The constraint is set by government on the basis of macroeconomic conditions, baseline projections and program priorities

• The constraint determines the “space” available in the medium-term for policy initiatives. In some circumstances, it may determine the volume of spending cuts required to meet fiscal objectives

• The constraint usually is set in money terms such as total expenditures: it may also be set as a percentage of GDP

• It may be useful to establish sub-limits on each sector or ministry

• It is important that government regard its preset limits as hard constraints on the amounts allocated in the budget and projected for the medium-term

6

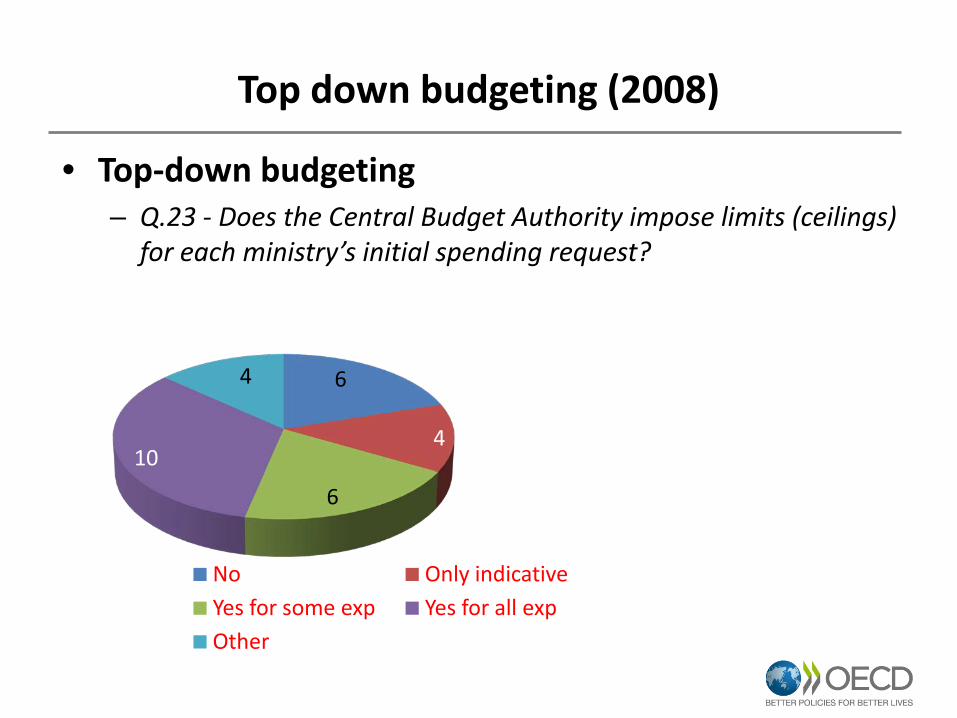

Top down budgeting (2008)

• Top-down budgeting – Q.23 - Does the Central Budget Authority impose limits (ceilings)

for each ministry’s initial spending request?

7

6

4

6

10

4

No Only indicative Yes for some exp Yes for all exp Other

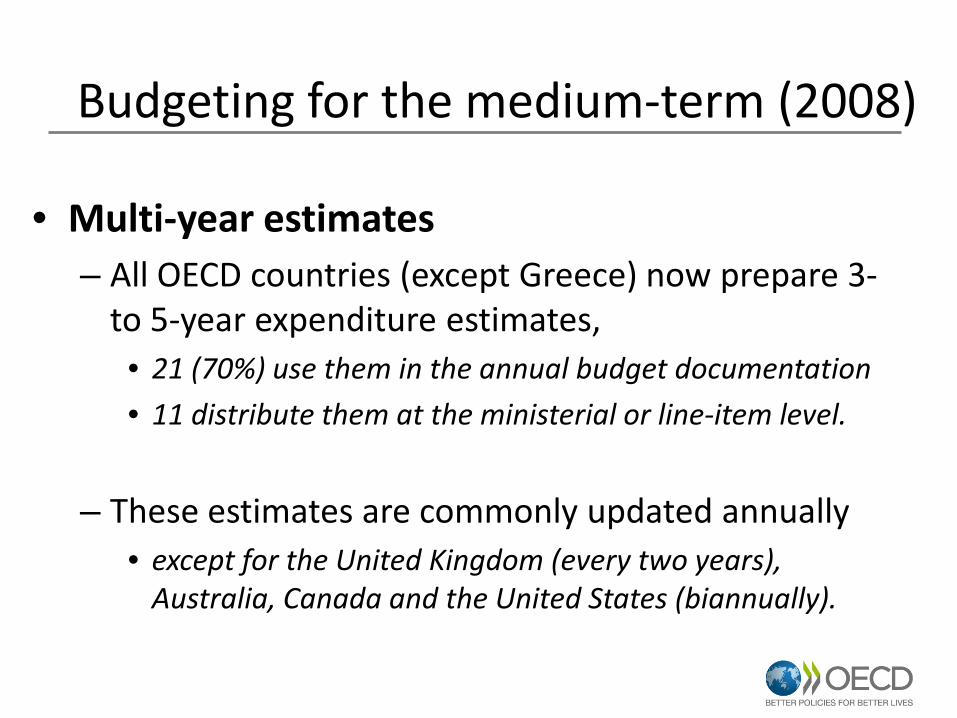

Budgeting for the medium-term (2008)

• Multi-year estimates – All OECD countries (except Greece) now prepare 3-

to 5-year expenditure estimates, • 21 (70%) use them in the annual budget documentation

• 11 distribute them at the ministerial or line-item level.

– These estimates are commonly updated annually • except for the United Kingdom (every two years),

Australia, Canada and the United States (biannually).

8

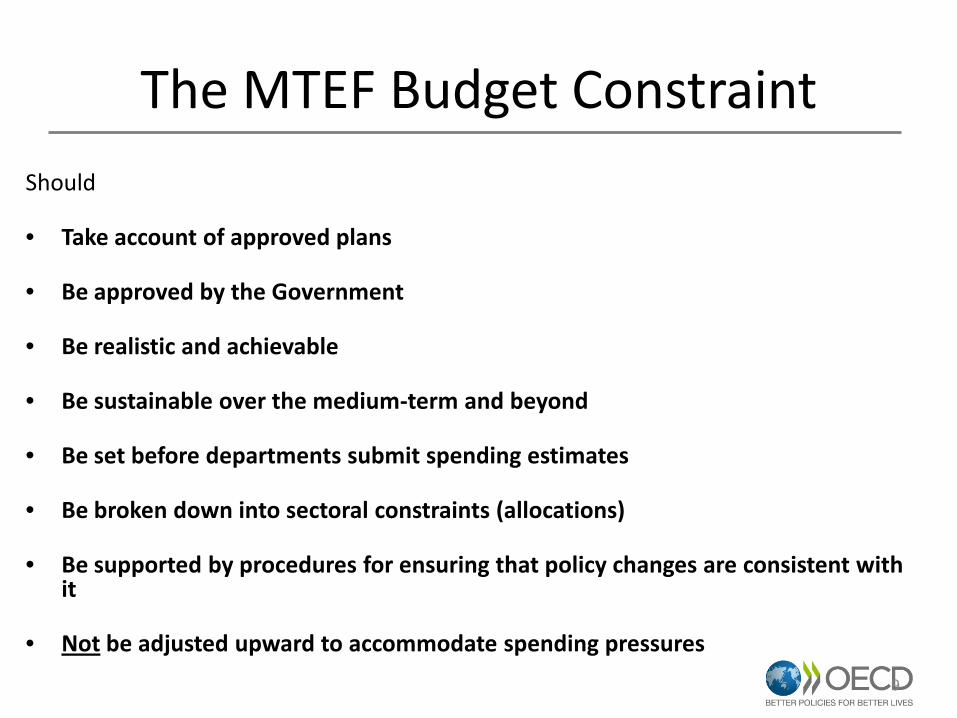

The MTEF Budget Constraint Should

• Take account of approved plans

• Be approved by the Government

• Be realistic and achievable

• Be sustainable over the medium-term and beyond

• Be set before departments submit spending estimates

• Be broken down into sectoral constraints (allocations)

• Be supported by procedures for ensuring that policy changes are consistent with it

• Not be adjusted upward to accommodate spending pressures

9

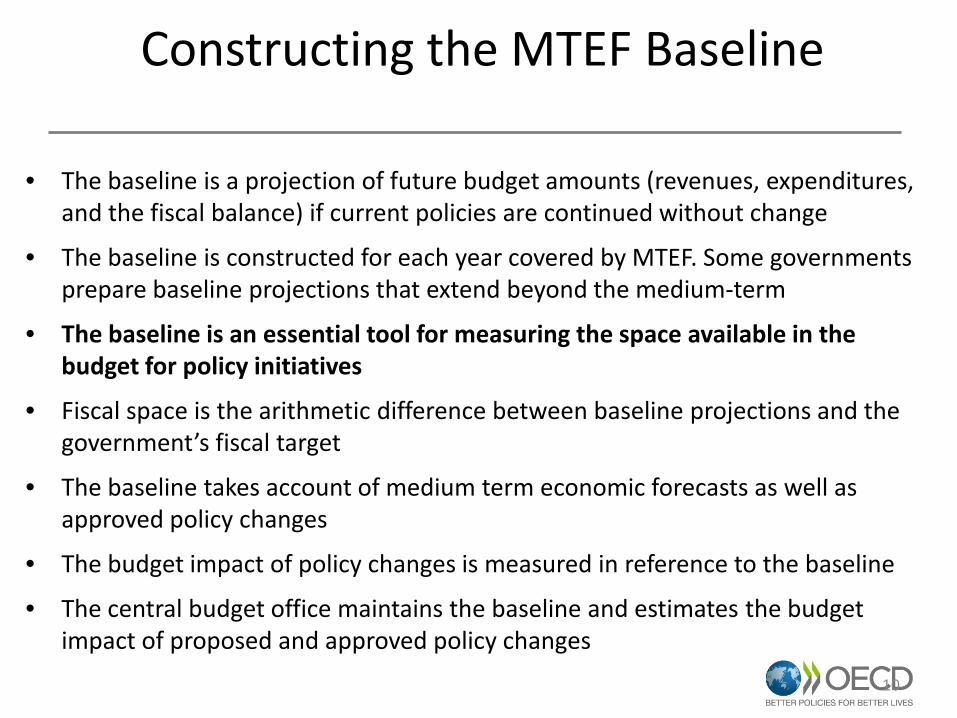

Constructing the MTEF Baseline

• The baseline is a projection of future budget amounts (revenues, expenditures, and the fiscal balance) if current policies are continued without change

• The baseline is constructed for each year covered by MTEF. Some governments prepare baseline projections that extend beyond the medium-term

• The baseline is an essential tool for measuring the space available in the budget for policy initiatives

• Fiscal space is the arithmetic difference between baseline projections and the government’s fiscal target

• The baseline takes account of medium term economic forecasts as well as approved policy changes

• The budget impact of policy changes is measured in reference to the baseline

• The central budget office maintains the baseline and estimates the budget impact of proposed and approved policy changes

10

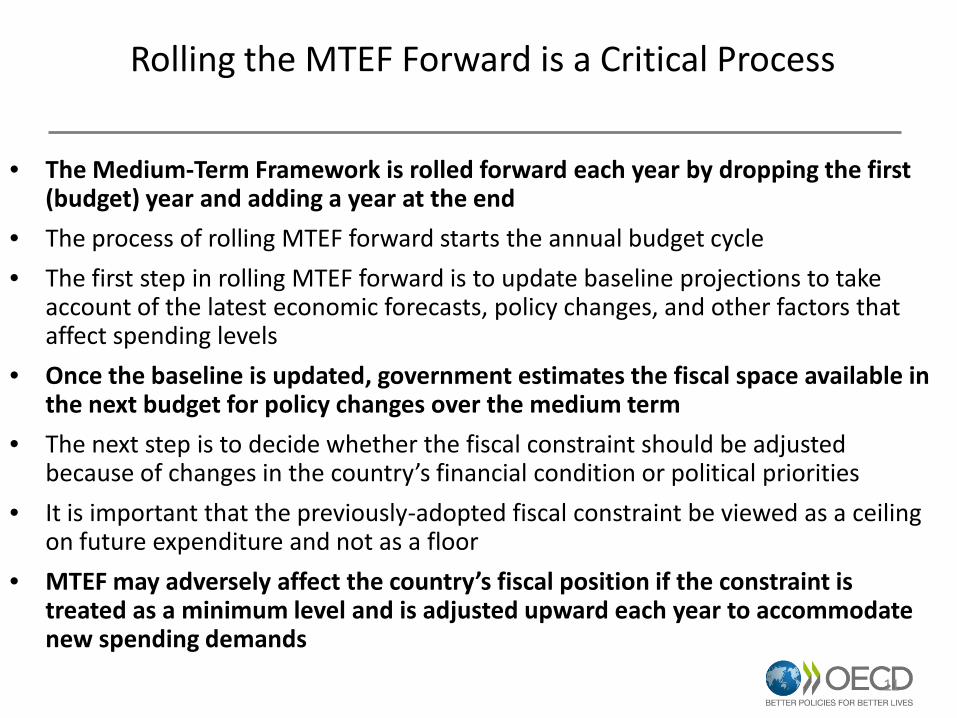

Rolling the MTEF Forward is a Critical Process

• The Medium-Term Framework is rolled forward each year by dropping the first (budget) year and adding a year at the end

• The process of rolling MTEF forward starts the annual budget cycle

• The first step in rolling MTEF forward is to update baseline projections to take account of the latest economic forecasts, policy changes, and other factors that affect spending levels

• Once the baseline is updated, government estimates the fiscal space available in the next budget for policy changes over the medium term

• The next step is to decide whether the fiscal constraint should be adjusted because of changes in the country’s financial condition or political priorities

• It is important that the previously-adopted fiscal constraint be viewed as a ceiling on future expenditure and not as a floor

• MTEF may adversely affect the country’s fiscal position if the constraint is treated as a minimum level and is adjusted upward each year to accommodate new spending demands

11

The Annual Budget Is Linked to MTEF

• Government continues to prepare an annual budget when it adopts MTEF

• The budget becomes the first year of the medium-term framework • When it is approved, the budget authorizes expenditure for the next

year, in contrast to MTEF which only indicates expenditure for future years

• The annual budget should not be a separate process: it should be fully integrated into the MTEF

• When it budgets for the next year, government projects the medium-term implications of current decisions, determines whether these projections are consistent with the medium-term fiscal constraint, and specifies expected medium-term program results

• Government uses the annual budget to allocate money for policy initiatives over the next 3-4 years

12

Using MTEF to Improve Development Results

• The link between resources and results is weak in annual budgeting

• One year usually is insufficient to produce significant change, lengthening the budget’s time frame has the potential to strengthen the government’s focus on results

• When the budget’s time horizon is extended, government can act on the basis of the resources that will be available over the full MTEF cycle

• To target results, it does not suffice to estimate what will be accomplished in the years ahead: it also is important to establish short-term targets for monitoring progress

• MTEF can achieve its potential only if the budget actually finances the activities and services required to produce results

13

Issues in Designing an MTEF

• How many years does it cover? – Usual practice is 3-5 years

• Is it based on current or constant prices?

– Usual practice is to update the baseline for price changes

• Does it have a contingency reserve? – The reserve accommodates unforeseen events or policy changes

• How much spending detail does it include?

– Typically, allocations by major organization units or sectors

• Are allocations for future years guaranteed? – No. Government prepares an annual budget in each future year

covered by MTEF 14

Country example: Netherlands

• Expenditure limits agreed by each incoming government

• Objectives, Performance targets, Resources: all agreed at the same time

• Expenditure ceilings remain unchanged over the lifetime of the government – Completely separate from revenues – “fixed” rather than “rolling” expenditure ceilings – Good for fiscal discipline, planning – Bad for flexibility, reallocation of resources

15

Country example: UK

• “Spending Review” usually every 2 or 3 years • Fixed ceilings

– Originally linked to “Public Service Agreements” (performance targets)

• Process is internal / bureaucratic • Weakness: 3-year ceilings “locked in” upward

spending (2007 Spending Review) • Strength: new agreements help to “lock in” and

secure the savings required under the austerity programme

16

Country example: Austria

• 3-year rolling expenditure ceilings

• New year (year 4) agreed every year

• Unspent funds can be “carried over” until the following year – Removes the “end year rush” to spend money

– Risk? Build-up of large, unspent reserves

• Part of overall reformed fiscal framework – MTEF; Performance; Accruals budgeting

17

MTEF Changes the Role of the Central Budget Office

• In most developing countries, the primary role of the budget office is to control public expenditures

• It performs this role by preparing the annual budget, monitoring expenditures during the year, and controlling actions by spending units

• Line-item budgeting, which focuses on inputs, is well suited for control-based management

• MTEF continues these roles, but subordinates them to the policy-making functions of budgeting

• In MTEF, the principal role of the budget office is to manage policy changes by measuring their impacts on current and future budgets, and assessing whether they are in accord with government priorities, and can be accommodated within MTEF fiscal limits

18

MTEF Changes the Role of the Central Budget Office, continued

• The budget office manages the baseline process by updating projections and by estimating the cost of proposed or approved policy initiatives

• To perform these tasks, the budget office has to curtail – but not eliminate – its control function; it can do this by consolidating line items into broad categories, and by giving spending units greater flexibility

• The extent to which the budget office can prudently shift from control to policymaking depends on the country’s financial condition and the reliability of its financial management systems

19

The Legislature’s Role In MTEF?

• There is no uniform pattern: each country has to define the legislature’s role in ways that are consistent with its governmental system and political traditions

• In some countries, parliament does not take any action on the MTEF prepared by government; in others, the legislature debates MTEF, and in some, it formally approves the Medium-Term Framework

• Parliament has a bigger voice on MTEF in countries that permit it to amend the government’s budget than in countries that don’t

• The legislature is likely to have a more active MTEF role when it has its own budget experts and is not dependent on the government for data and analysis

• MTEF can promote fiscal discipline when the legislature’s budget work is fragmented, and sectoral committees have a strong voice in budget decisions

20

Is Your Country Ready for MTEF?

• Many countries claim to have MTEF, but few have effective systems

• Some countries that have MTEF lack the political and administrative capacity to operate a Medium-Term Framework

• Several characteristics of its budget process indicate whether a government is ready for MTEF – First, does the country have a reliable budget system? If there is significant variance

between budgeted and actual expenditures, MTEF will probably be ineffective

– Second, does the government have capacity to produce reliable economic data and forecasts? Implementation of MTEF depends on these forecasts

– Third, does the government produce timely and accurate financial reports? Without these reports, MTEF will lack credibility

– Fourth, does government have the capacity to measure the future budgetary impacts of its policy decisions? These measurements are a vital feature of successful MTEFs

– Finally, is the country’s fiscal condition highly volatile and uncertain? If it is, it will be difficult to make firm medium-term decisions

21

How to make MTEF effective?

• If MTEF is not used for budgeting, it is useless – Many countries have an MTEF but do not base budget decisions on it

• MTEF must become the government’s budget process – Some countries have an annual budget and a separate MTEF

• MTEF should be used by political leaders to set fiscal policy and spending priorities – If MTEF is treated as a technical exercise, politicians will not pay attention to it

• MTEF should focus budgeting on policy choices – If budgeting is used to control the details of spending, MTEF will not be of much value

• MTEF should be a rolling process: Last year’s decisions should be the starting point – If the budget disregards medium-term decisions, MTEF will not be effective

22