Embed Size (px)

Citation preview

H E A L T H W E A L T H C A R E E R

M E R C E R ’ S 2 0 1 6C O M P E N S AT I O N P L A N N I N GS E M I N ARD O I N G M O R E W I T H L E S S

Vancouver

SEPTEMBER 2015

© MERCER 2015 1

T O D AY ’ S P R E S E N T E R S

H E L M U TP A S T R I C K

A I L S AF O R S G R E N

G R A H A MD O D D

T O D AY ’ S P R E S E N T E R S

© MERCER 2015 2

T O D AY ’ S D I S C U S S I O N

ECONOMICOUTLOOK

01HIGHLIGHTSFROM THE

SURVEY

02INSIDE

EMPLOYEES’MINDS

03

Economic Outlook

Mercer 2016 CompensationPlanning Seminar – Vancouver

September 15, 2015

Helmut PastrickChief EconomistCentral 1 Credit Union

|

Economics

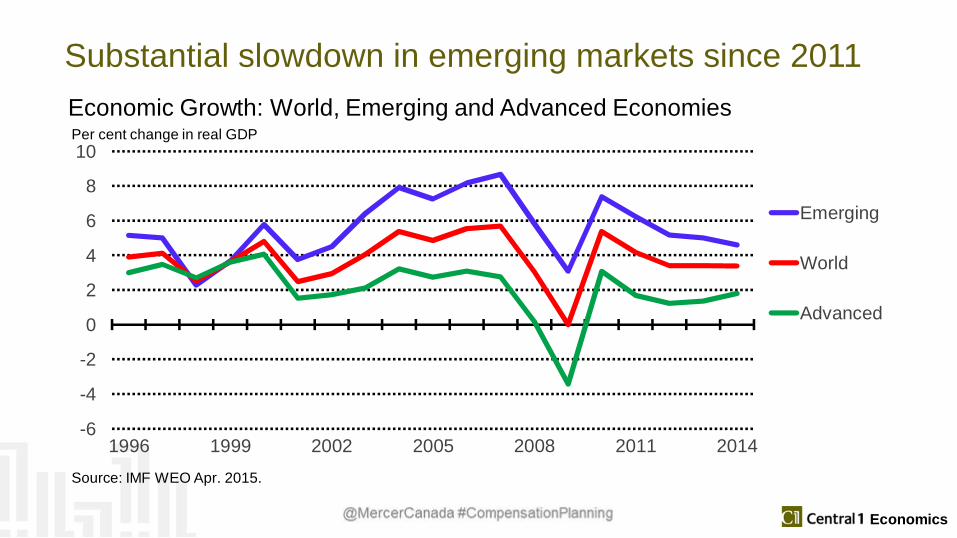

Substantial slowdown in emerging markets since 2011

-6

-4

-2

0

2

4

6

8

10

1996 1999 2002 2005 2008 2011 2014

Emerging

World

Advanced

Per cent change in real GDP

Source: IMF WEO Apr. 2015.

Economic Growth: World, Emerging and Advanced Economies

|

Economics

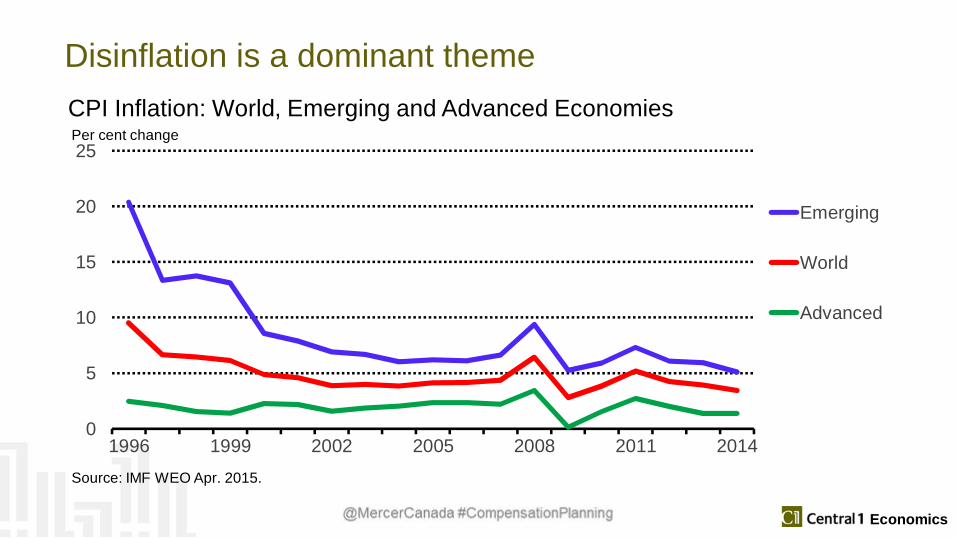

Disinflation is a dominant theme

0

5

10

15

20

25

1996 1999 2002 2005 2008 2011 2014

Emerging

World

Advanced

Per cent change

Source: IMF WEO Apr. 2015.

CPI Inflation: World, Emerging and Advanced Economies

|

Economics

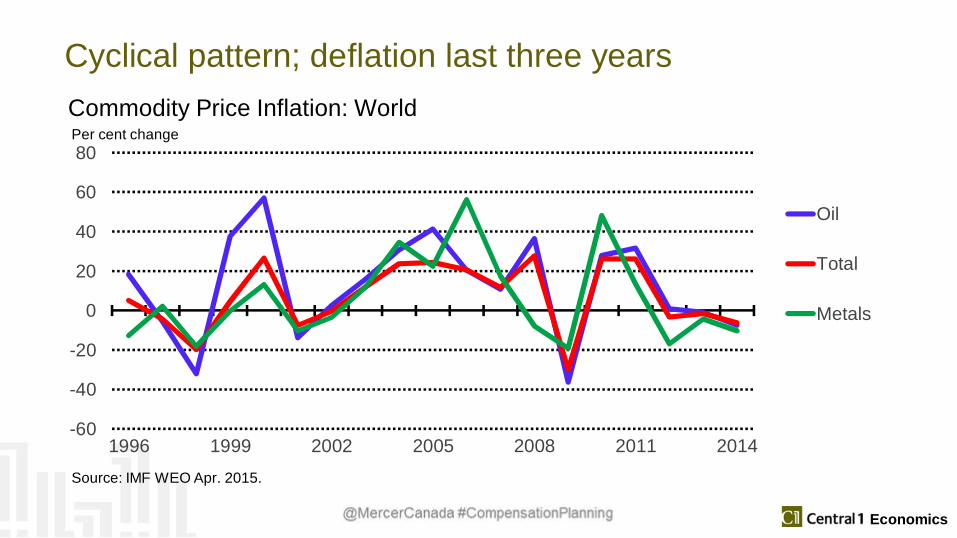

Cyclical pattern; deflation last three years

-60

-40

-20

0

20

40

60

80

1996 1999 2002 2005 2008 2011 2014

Oil

Total

Metals

Per cent change

Source: IMF WEO Apr. 2015.

Commodity Price Inflation: World

|

Economics

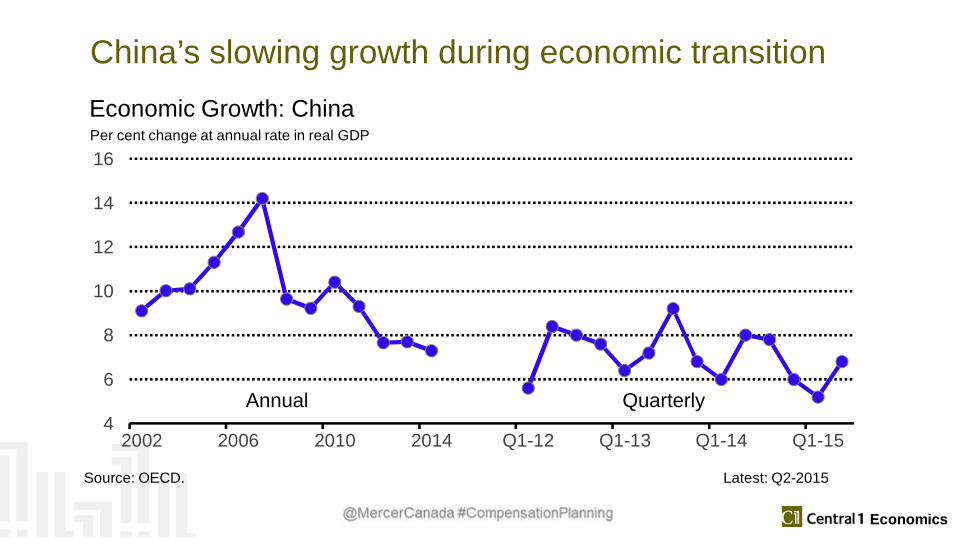

China’s slowing growth during economic transition

4

6

8

10

12

14

16

2002 2006 2010 2014 Q1-12 Q1-13 Q1-14 Q1-15

Per cent change at annual rate in real GDP

Source: OECD. Latest: Q2-2015

Economic Growth: China

Annual Quarterly

|

Economics

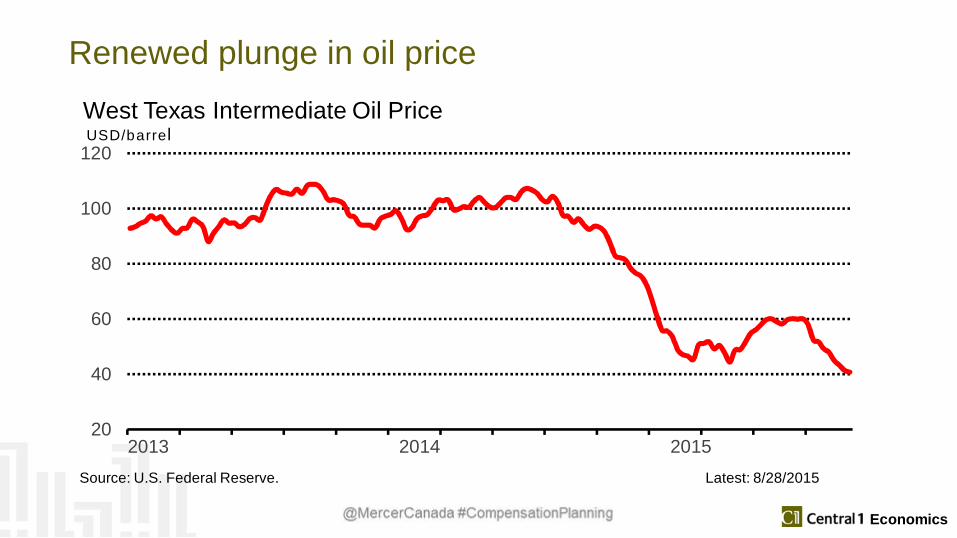

Renewed plunge in oil price

20

40

60

80

100

120

2013 2014 2015

West Texas Intermediate Oil PriceUSD/barrel

Source: U.S. Federal Reserve. Latest: 8/28/2015

|

Economics

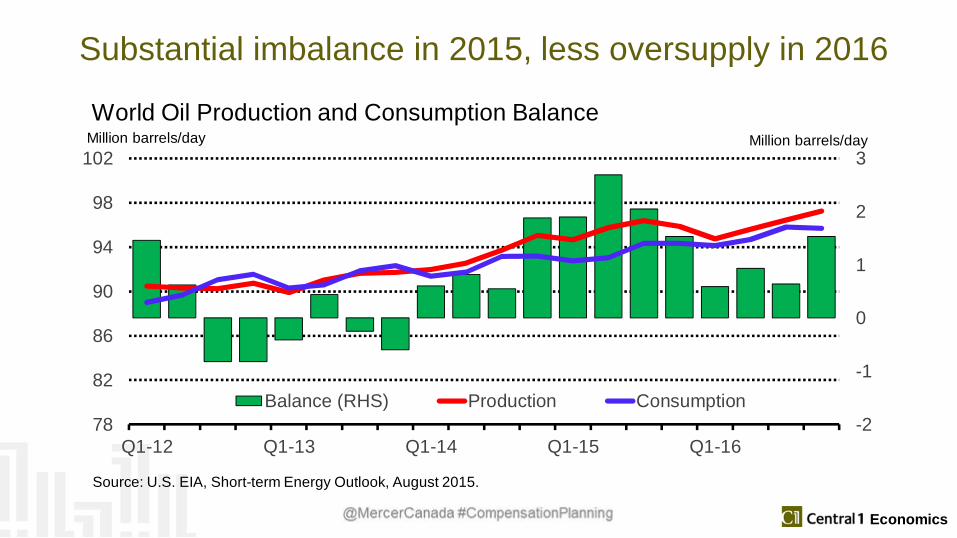

Substantial imbalance in 2015, less oversupply in 2016

-2

-1

0

1

2

3

78

82

86

90

94

98

102

Q1-12 Q1-13 Q1-14 Q1-15 Q1-16

Balance (RHS) Production Consumption

Million barrels/dayWorld Oil Production and Consumption Balance

Million barrels/day

Source: U.S. EIA, Short-term Energy Outlook, August 2015.

|

Economics

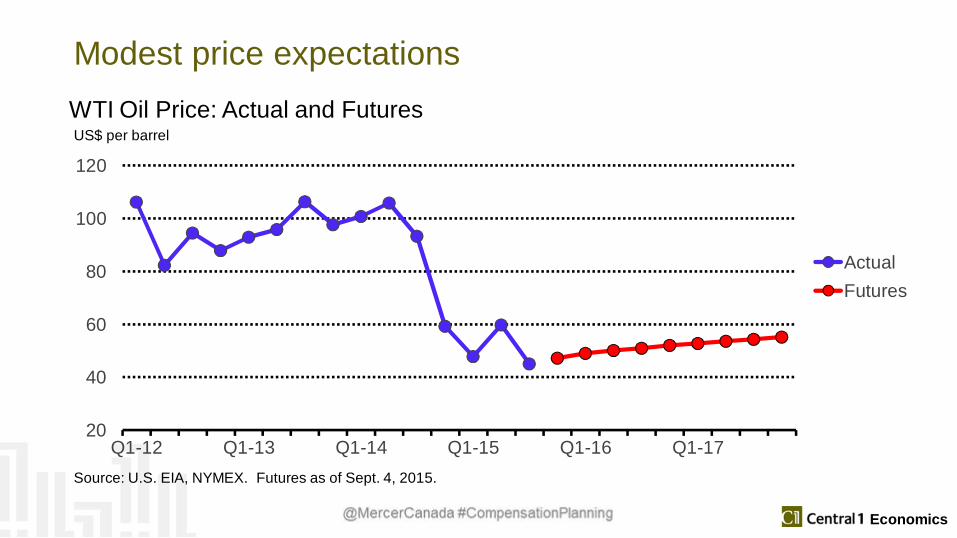

Modest price expectations

20

40

60

80

100

120

Q1-12 Q1-13 Q1-14 Q1-15 Q1-16 Q1-17

ActualFutures

US$ per barrel

Source: U.S. EIA, NYMEX. Futures as of Sept. 4, 2015.

WTI Oil Price: Actual and Futures

|

Economics

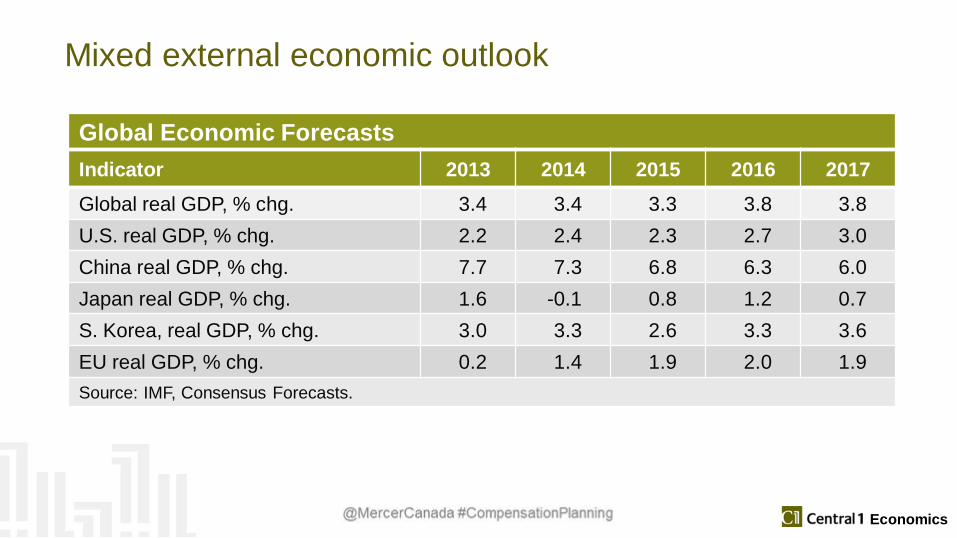

Global Economic ForecastsIndicator 2013 2014 2015 2016 2017Global real GDP, % chg. 3.4 3.4 3.3 3.8 3.8U.S. real GDP, % chg. 2.2 2.4 2.3 2.7 3.0China real GDP, % chg. 7.7 7.3 6.8 6.3 6.0Japan real GDP, % chg. 1.6 -0.1 0.8 1.2 0.7S. Korea, real GDP, % chg. 3.0 3.3 2.6 3.3 3.6EU real GDP, % chg. 0.2 1.4 1.9 2.0 1.9Source: IMF, Consensus Forecasts.

Mixed external economic outlook

|

Economics

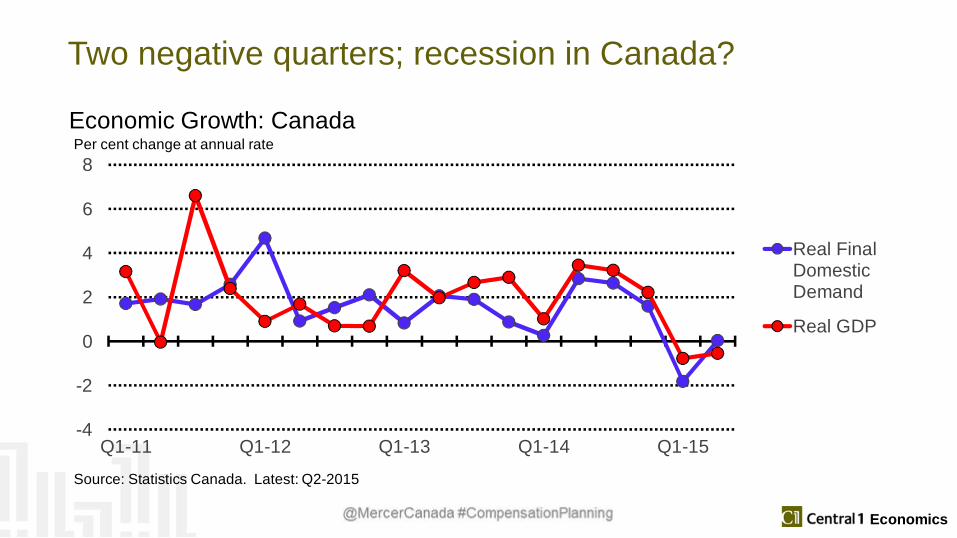

Two negative quarters; recession in Canada?

-4

-2

0

2

4

6

8

Q1-11 Q1-12 Q1-13 Q1-14 Q1-15

Real FinalDomesticDemand

Real GDP

Per cent change at annual rate

Source: Statistics Canada. Latest: Q2-2015

Economic Growth: Canada

|

Economics

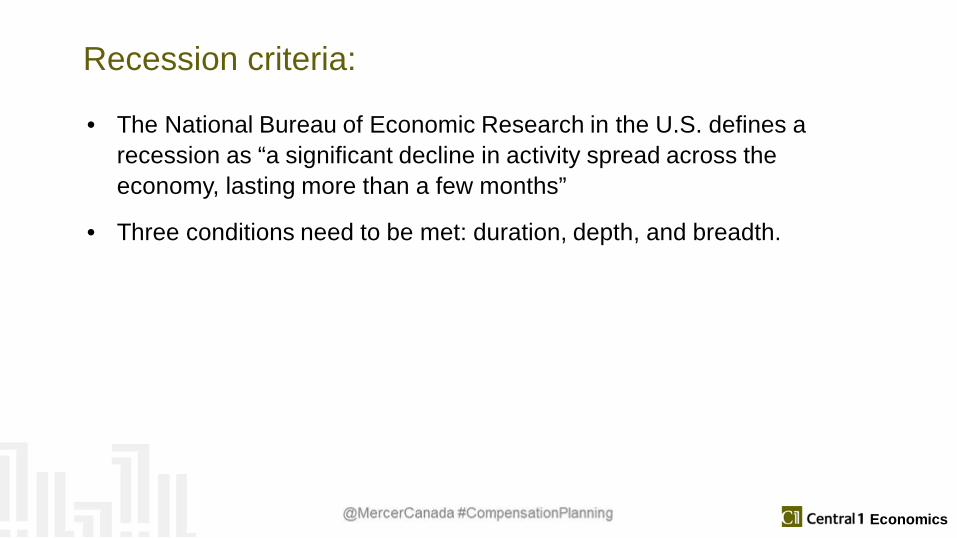

Recession criteria:

• The National Bureau of Economic Research in the U.S. defines arecession as “a significant decline in activity spread across theeconomy, lasting more than a few months”

• Three conditions need to be met: duration, depth, and breadth.

|

Economics

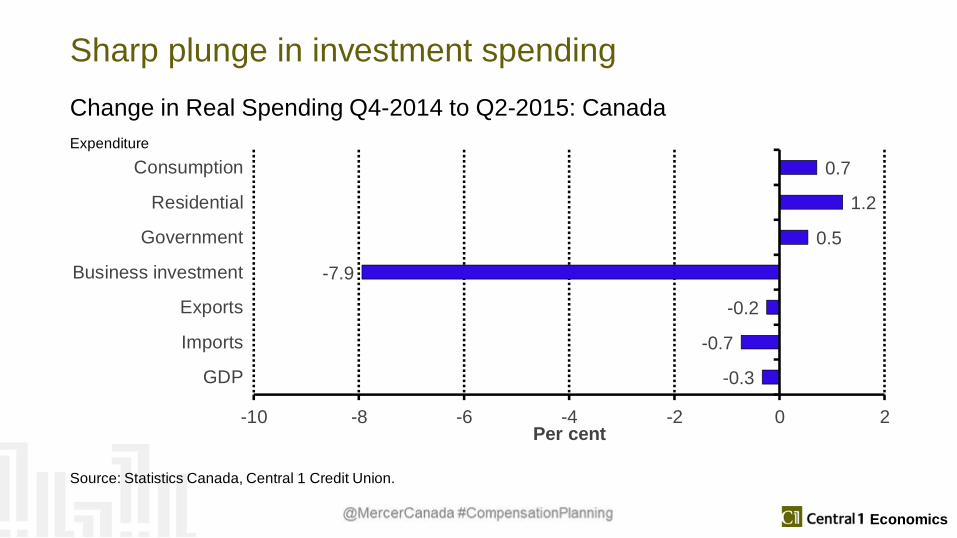

Sharp plunge in investment spending

-0.3

-0.7

-0.2

-7.9

0.5

1.2

0.7

-10 -8 -6 -4 -2 0 2

GDP

Imports

Exports

Business investment

Government

Residential

Consumption

Per cent

Expenditure

Source: Statistics Canada, Central 1 Credit Union.

Change in Real Spending Q4-2014 to Q2-2015: Canada

|

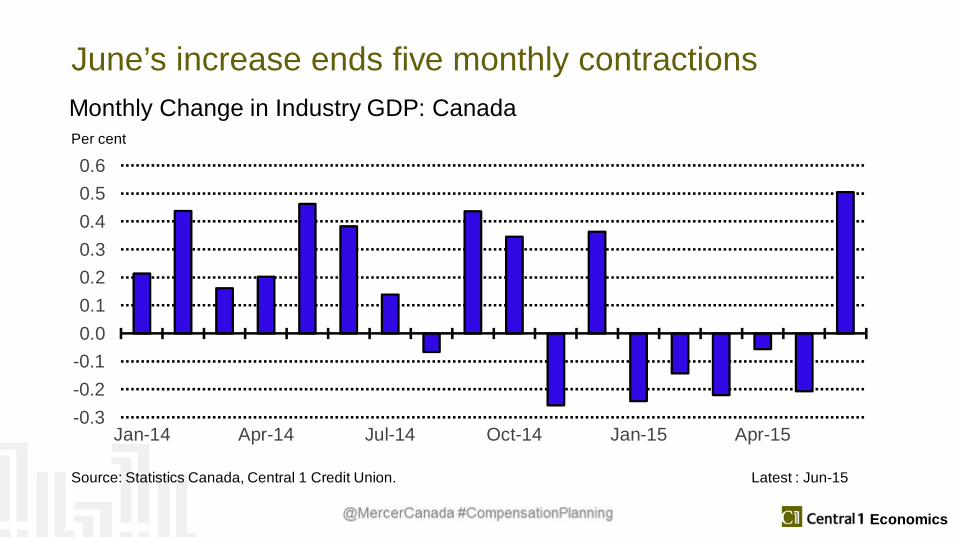

Economics

June’s increase ends five monthly contractions

-0.3-0.2-0.10.00.10.20.30.40.50.6

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

Per cent

Source: Statistics Canada, Central 1 Credit Union. Latest : Jun-15

Monthly Change in Industry GDP: Canada

|

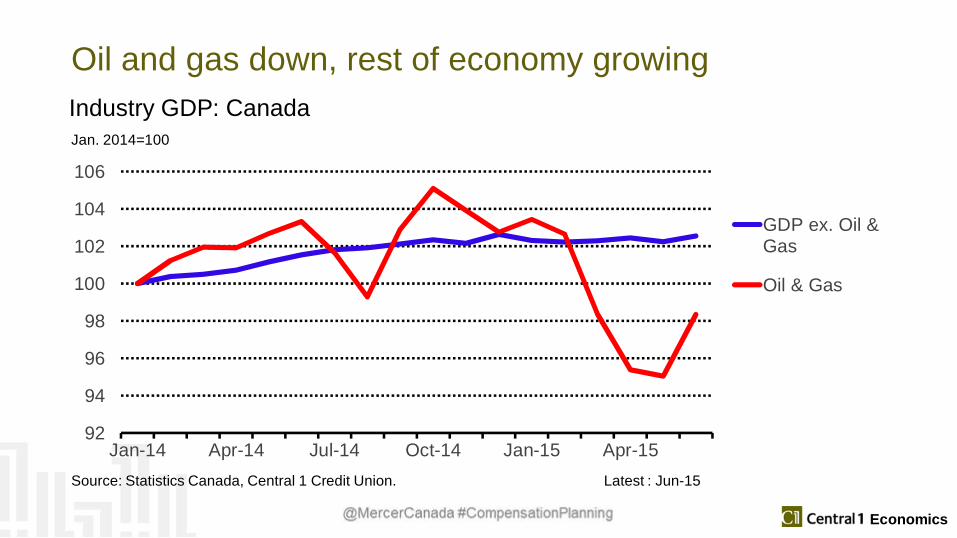

Economics

Oil and gas down, rest of economy growing

92

94

96

98

100

102

104

106

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

GDP ex. Oil &Gas

Oil & Gas

Jan. 2014=100

Source: Statistics Canada, Central 1 Credit Union. Latest : Jun-15

Industry GDP: Canada

|

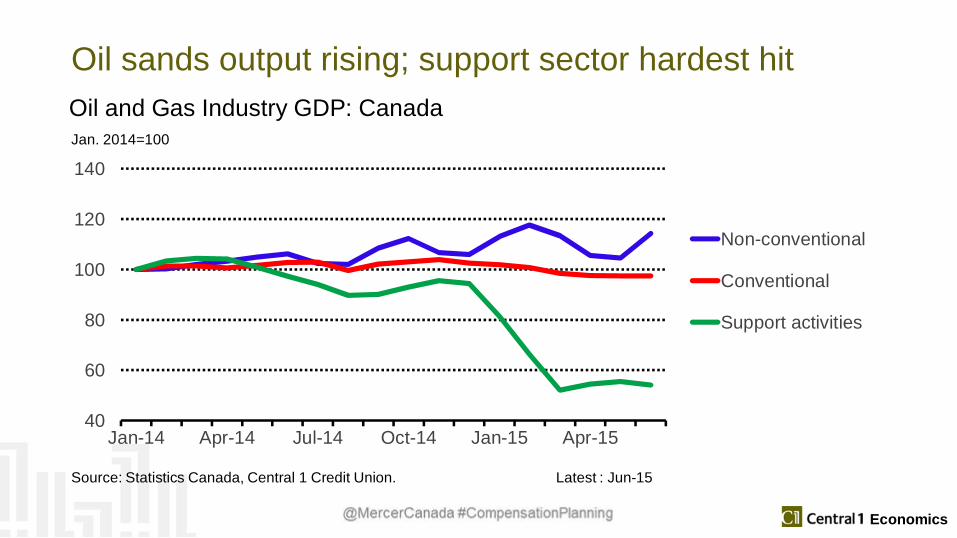

Economics

Oil sands output rising; support sector hardest hit

40

60

80

100

120

140

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

Non-conventional

Conventional

Support activities

Jan. 2014=100

Source: Statistics Canada, Central 1 Credit Union. Latest : Jun-15

Oil and Gas Industry GDP: Canada

|

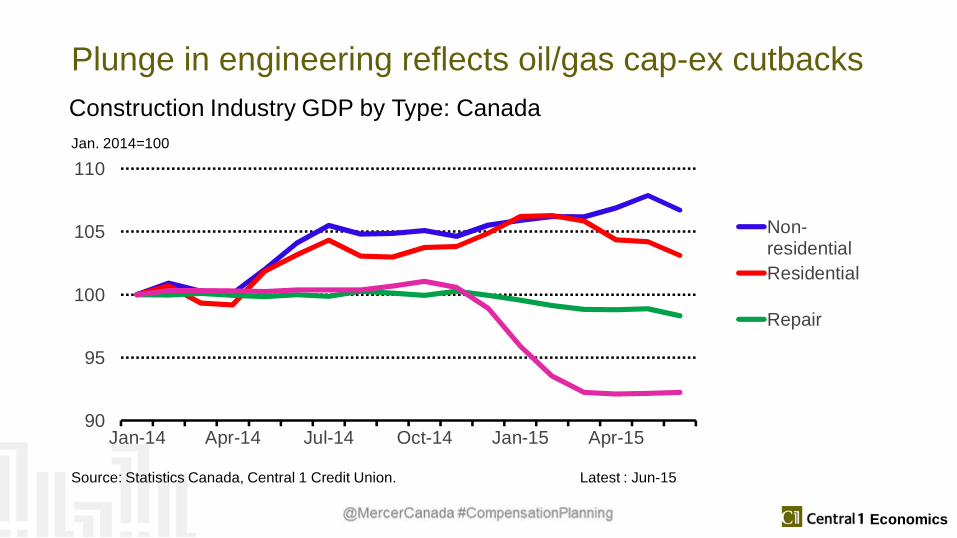

Economics

Plunge in engineering reflects oil/gas cap-ex cutbacks

90

95

100

105

110

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

Non-residentialResidential

Repair

Jan. 2014=100

Source: Statistics Canada, Central 1 Credit Union. Latest : Jun-15

Construction Industry GDP by Type: Canada

|

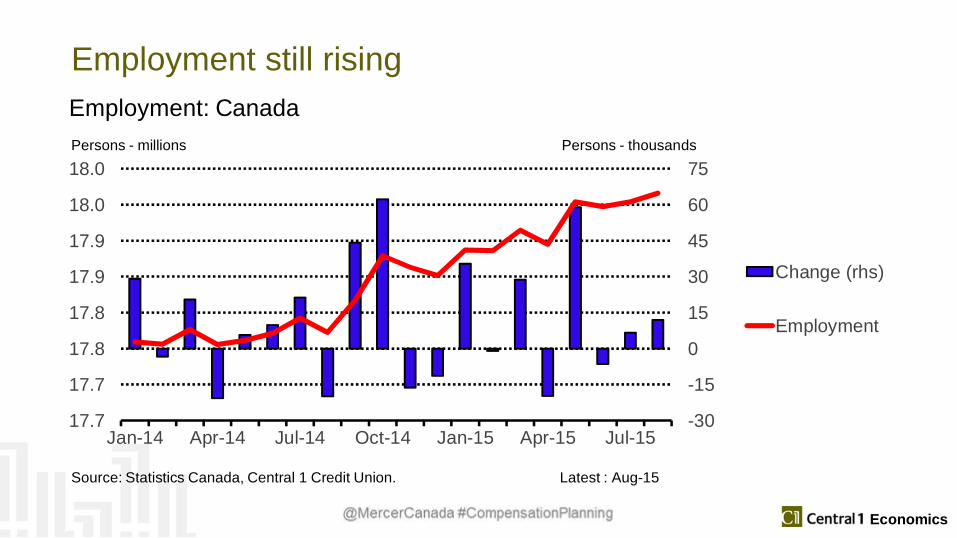

Economics

Employment still rising

-30

-15

0

15

30

45

60

75

17.7

17.7

17.8

17.8

17.9

17.9

18.0

18.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15

Change (rhs)

Employment

Persons - millions Persons - thousands

Source: Statistics Canada, Central 1 Credit Union. Latest : Aug-15

Employment: Canada

|

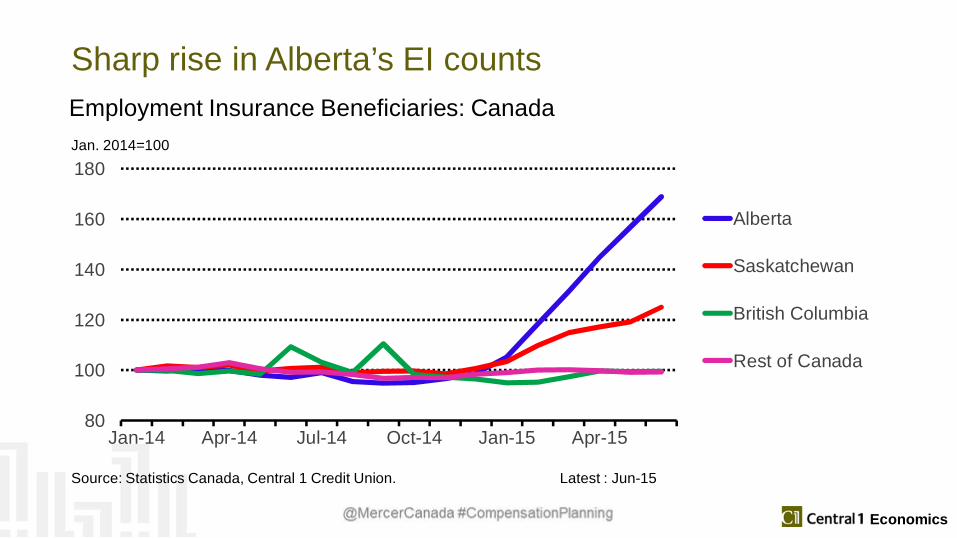

Economics

Sharp rise in Alberta’s EI counts

80

100

120

140

160

180

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15

Alberta

Saskatchewan

British Columbia

Rest of Canada

Jan. 2014=100

Source: Statistics Canada, Central 1 Credit Union. Latest : Jun-15

Employment Insurance Beneficiaries: Canada

|

Economics

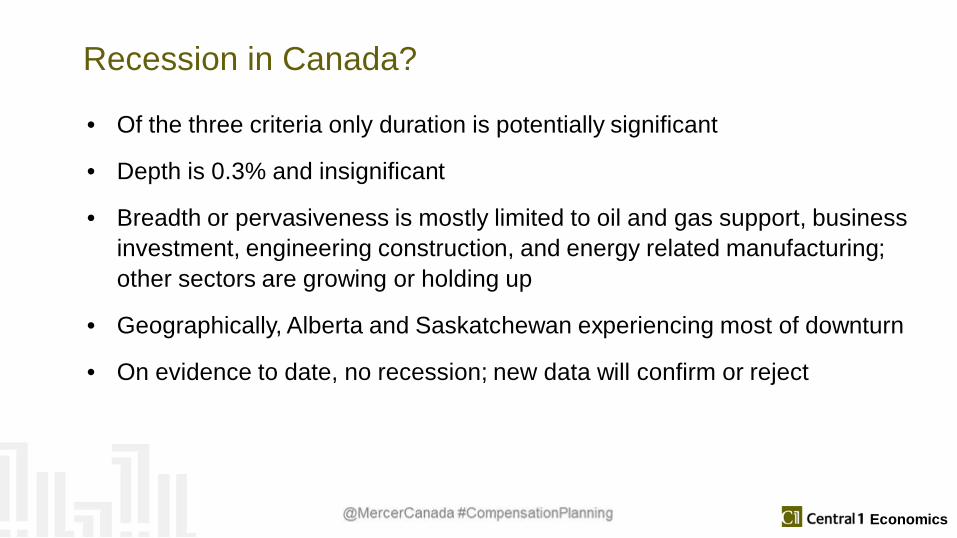

Recession in Canada?

• Of the three criteria only duration is potentially significant

• Depth is 0.3% and insignificant

• Breadth or pervasiveness is mostly limited to oil and gas support, businessinvestment, engineering construction, and energy related manufacturing;other sectors are growing or holding up

• Geographically, Alberta and Saskatchewan experiencing most of downturn

• On evidence to date, no recession; new data will confirm or reject

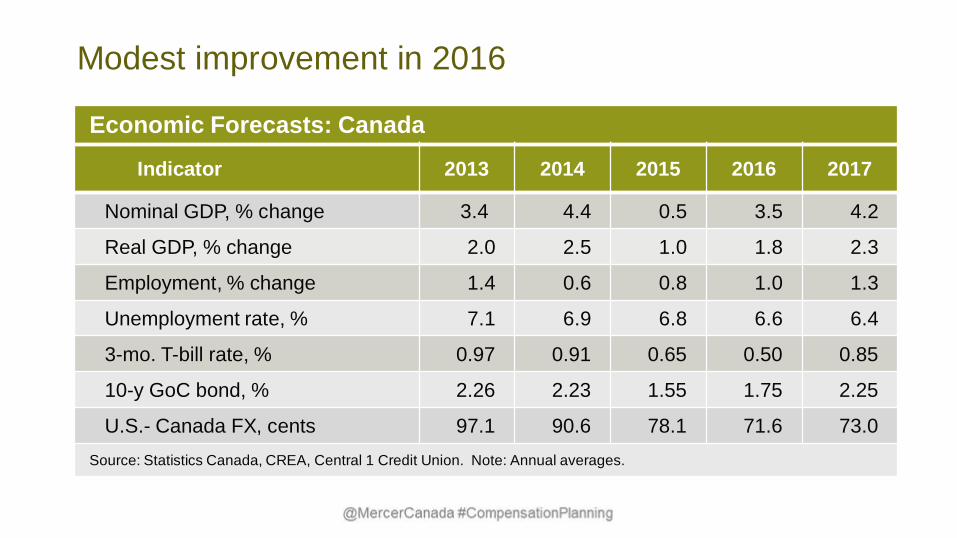

Modest improvement in 2016

Economic Forecasts: Canada

Indicator 2013 2014 2015 2016 2017

Nominal GDP, % change 3.4 4.4 0.5 3.5 4.2

Real GDP, % change 2.0 2.5 1.0 1.8 2.3

Employment, % change 1.4 0.6 0.8 1.0 1.3

Unemployment rate, % 7.1 6.9 6.8 6.6 6.4

3-mo. T-bill rate, % 0.97 0.91 0.65 0.50 0.85

10-y GoC bond, % 2.26 2.23 1.55 1.75 2.25

U.S.- Canada FX, cents 97.1 90.6 78.1 71.6 73.0Source: Statistics Canada, CREA, Central 1 Credit Union. Note: Annual averages.

|

Economics

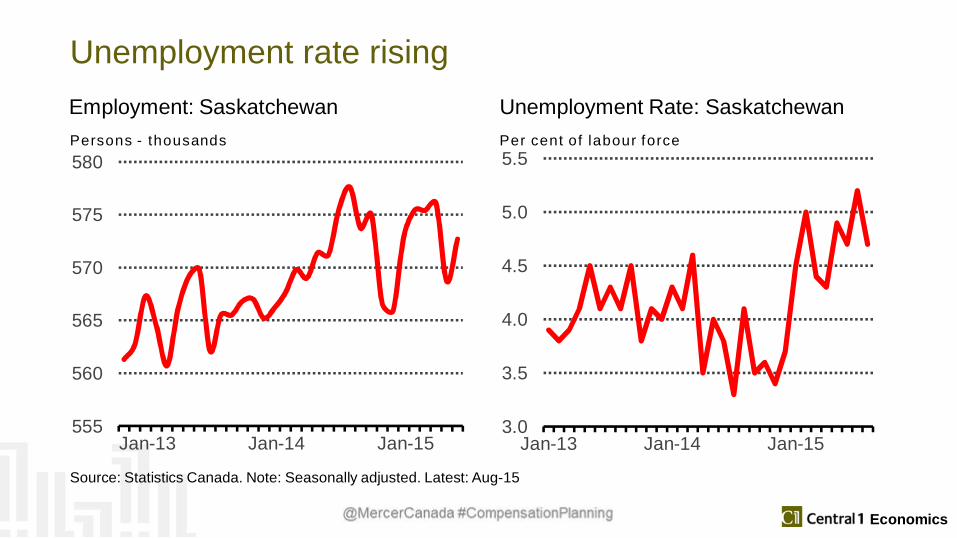

Unemployment rate rising

555

560

565

570

575

580

Jan-13 Jan-14 Jan-15

Persons - thousands

Employment: Saskatchewan

3.0

3.5

4.0

4.5

5.0

5.5

Jan-13 Jan-14 Jan-15

Per cent of labour force

Unemployment Rate: Saskatchewan

Source: Statistics Canada. Note: Seasonally adjusted. Latest: Aug-15

|

Economics

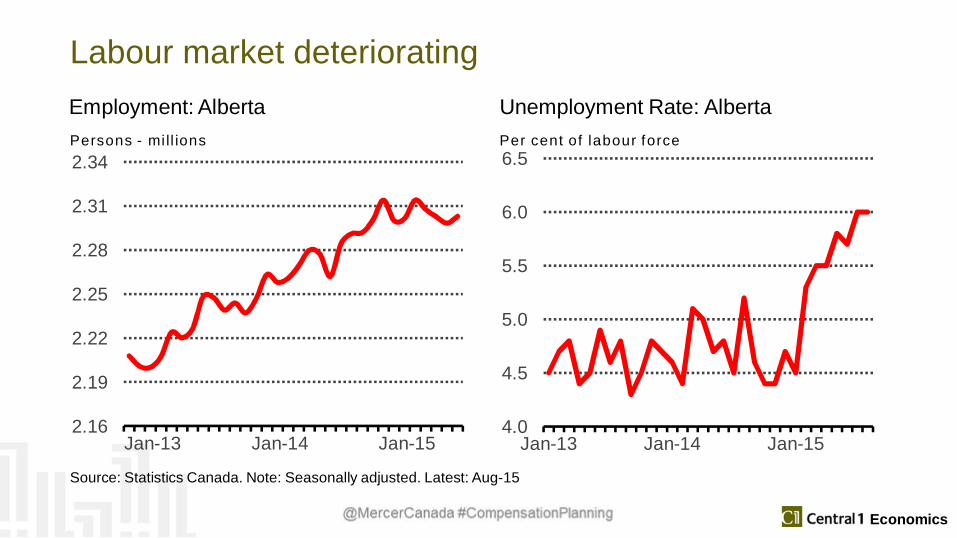

Labour market deteriorating

2.16

2.19

2.22

2.25

2.28

2.31

2.34

Jan-13 Jan-14 Jan-15

Persons - mi ll ions

Employment: Alberta

4.0

4.5

5.0

5.5

6.0

6.5

Jan-13 Jan-14 Jan-15

Per cent of labour force

Unemployment Rate: Alberta

Source: Statistics Canada. Note: Seasonally adjusted. Latest: Aug-15

|

Economics

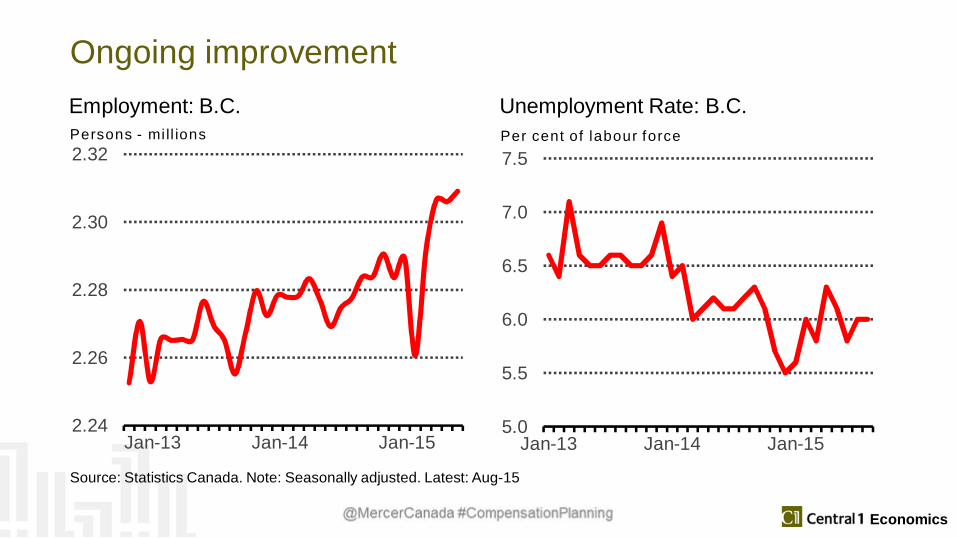

Ongoing improvement

2.24

2.26

2.28

2.30

2.32

Jan-13 Jan-14 Jan-15

Persons - mi ll ions

Employment: B.C.

5.0

5.5

6.0

6.5

7.0

7.5

Jan-13 Jan-14 Jan-15

Per cent of labour force

Unemployment Rate: B.C.

Source: Statistics Canada. Note: Seasonally adjusted. Latest: Aug-15

|

Economics

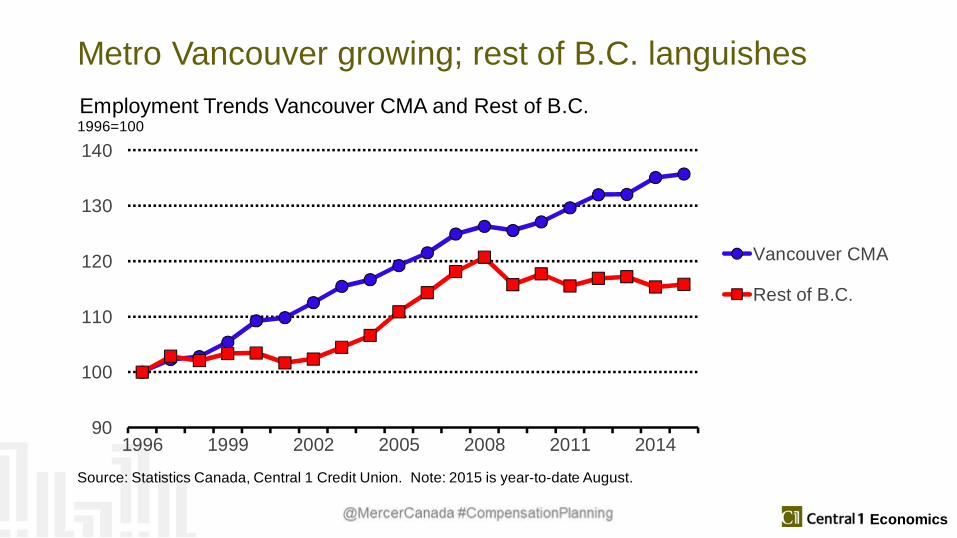

Metro Vancouver growing; rest of B.C. languishes

90

100

110

120

130

140

1996 1999 2002 2005 2008 2011 2014

Vancouver CMA

Rest of B.C.

1996=100

Source: Statistics Canada, Central 1 Credit Union. Note: 2015 is year-to-date August.

Employment Trends Vancouver CMA and Rest of B.C.

|

Economics

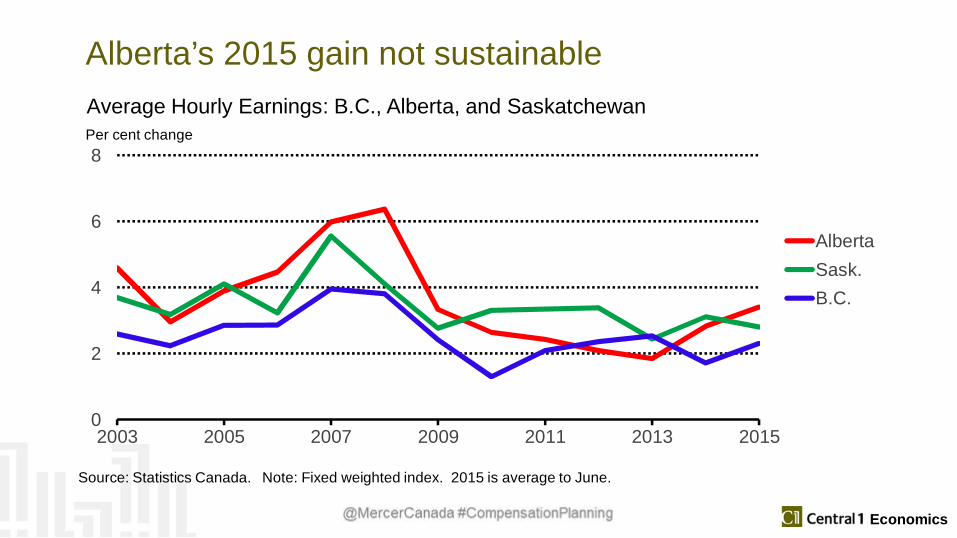

Alberta’s 2015 gain not sustainable

0

2

4

6

8

2003 2005 2007 2009 2011 2013 2015

AlbertaSask.B.C.

Per cent change

Source: Statistics Canada. Note: Fixed weighted index. 2015 is average to June.

Average Hourly Earnings: B.C., Alberta, and Saskatchewan

|

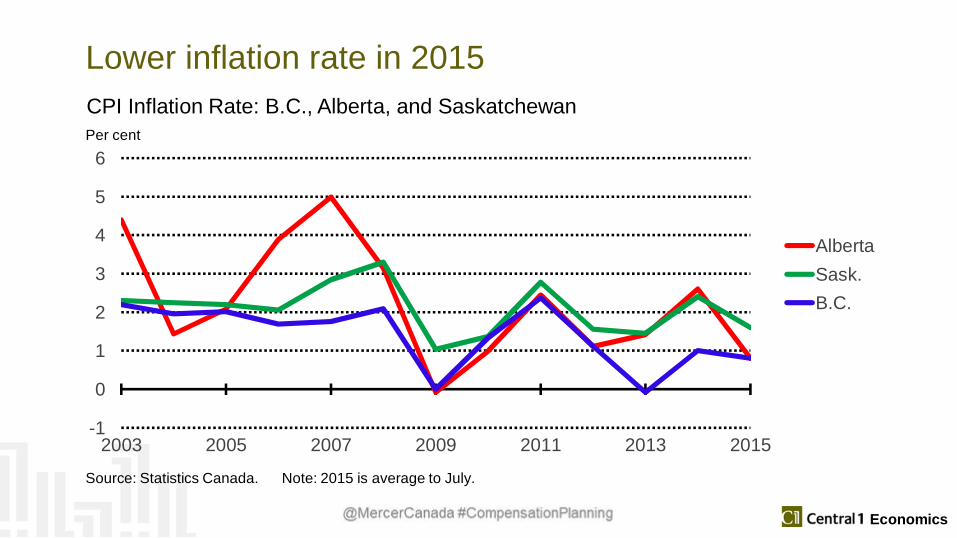

Economics

Lower inflation rate in 2015

-1

0

1

2

3

4

5

6

2003 2005 2007 2009 2011 2013 2015

AlbertaSask.B.C.

Per cent

Source: Statistics Canada. Note: 2015 is average to July.

CPI Inflation Rate: B.C., Alberta, and Saskatchewan

|

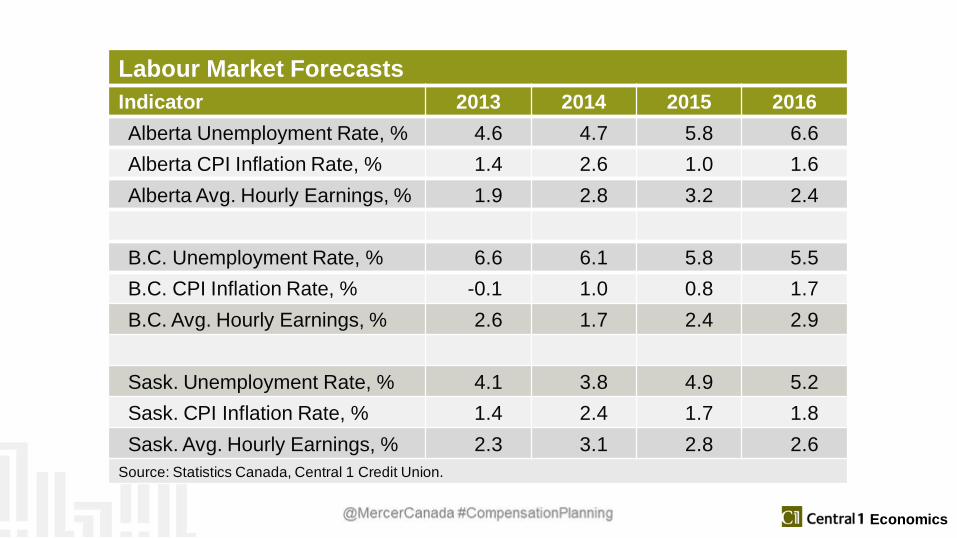

Economics

Labour Market ForecastsIndicator 2013 2014 2015 2016Alberta Unemployment Rate, % 4.6 4.7 5.8 6.6Alberta CPI Inflation Rate, % 1.4 2.6 1.0 1.6Alberta Avg. Hourly Earnings, % 1.9 2.8 3.2 2.4

B.C. Unemployment Rate, % 6.6 6.1 5.8 5.5B.C. CPI Inflation Rate, % -0.1 1.0 0.8 1.7B.C. Avg. Hourly Earnings, % 2.6 1.7 2.4 2.9

Sask. Unemployment Rate, % 4.1 3.8 4.9 5.2Sask. CPI Inflation Rate, % 1.4 2.4 1.7 1.8Sask. Avg. Hourly Earnings, % 2.3 3.1 2.8 2.6

Source: Statistics Canada, Central 1 Credit Union.

Thank you

© MERCER 2015 31© MERCER 2015 31

HIGHLIGHTSFROM THE SURVEY

© MERCER 2015 32

M E R C E R R E S E A R C H

© MERCER 2015 33

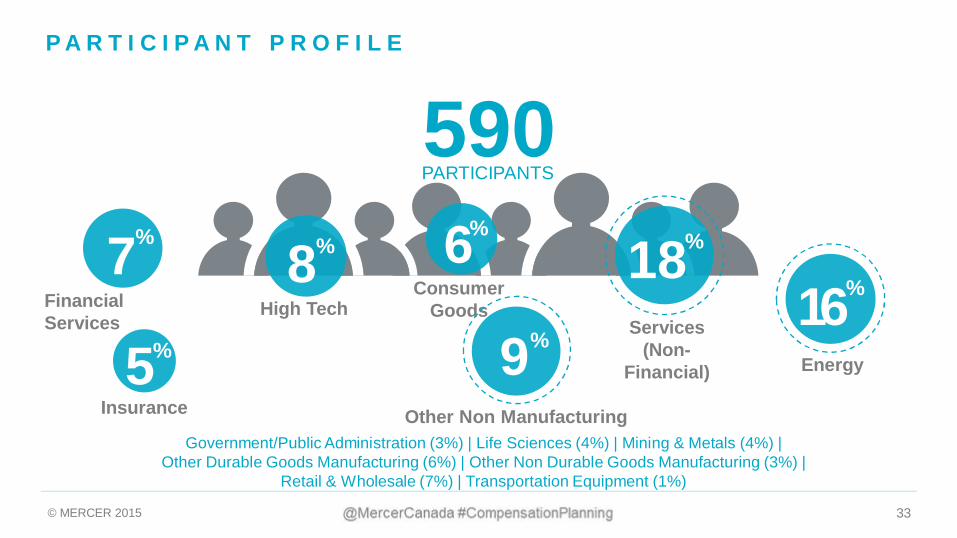

P A R T I C I P A N T P R O F I L E

590PARTICIPANTS

18%

Services(Non-

Financial)

1 %6Energy

%7FinancialServices

%8High Tech

%6Consumer

Goods

%5Insurance

%9Other Non Manufacturing

Government/Public Administration (3%) | Life Sciences (4%) | Mining & Metals (4%) |Other Durable Goods Manufacturing (6%) | Other Non Durable Goods Manufacturing (3%) |

Retail & Wholesale (7%) | Transportation Equipment (1%)

© MERCER 2015 34

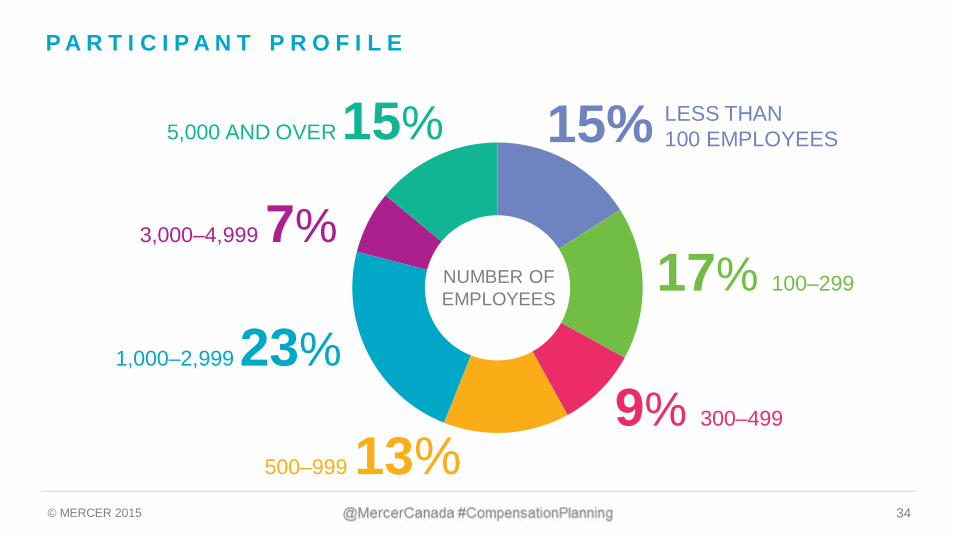

P A R T I C I P A N T P R O F I L E

5,000 AND OVER 15%

3,000–4,999 7%

1,000–2,999 23%

500–999 13%

17% 100–299

9% 300–499

NUMBER OFEMPLOYEES

LESS THAN100 EMPLOYEES15%

© MERCER 2015 35

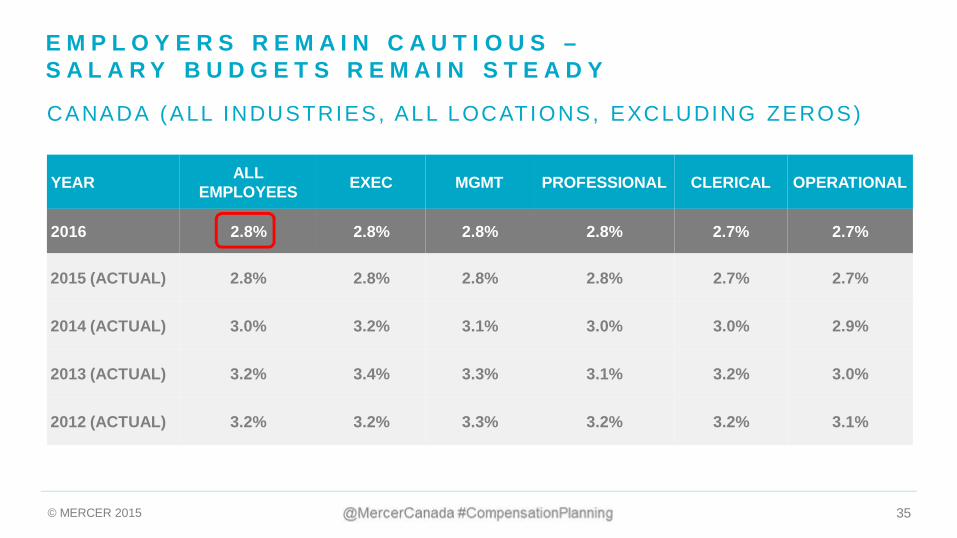

E M P L O Y E R S R E M A I N C A U T I O U S –S A L A R Y B U D G E T S R E M A I N S T E A D Y

YEAR ALLEMPLOYEES EXEC MGMT PROFESSIONAL CLERICAL OPERATIONAL

2016 2.8% 2.8% 2.8% 2.8% 2.7% 2.7%

CANADA (ALL INDUSTRIES, ALL LOCATIONS, EXCLUDING ZEROS)

2015 (ACTUAL) 2.8% 2.8% 2.8% 2.8% 2.7% 2.7%

2014 (ACTUAL) 3.0% 3.2% 3.1% 3.0% 3.0% 2.9%

2013 (ACTUAL) 3.2% 3.4% 3.3% 3.1% 3.2% 3.0%

2012 (ACTUAL) 3.2% 3.2% 3.3% 3.2% 3.2% 3.1%

© MERCER 2015 36

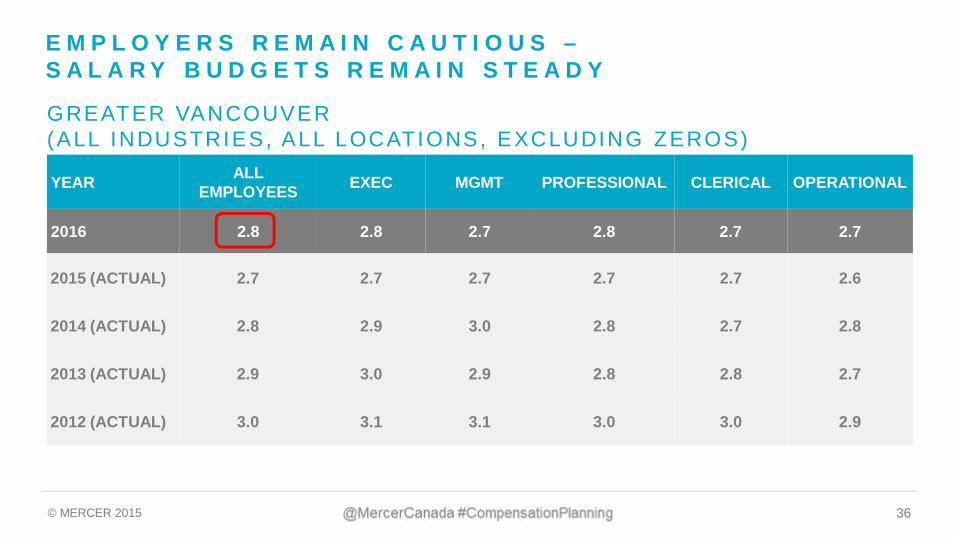

E M P L O Y E R S R E M A I N C A U T I O U S –S A L A R Y B U D G E T S R E M A I N S T E A D Y

YEAR ALLEMPLOYEES EXEC MGMT PROFESSIONAL CLERICAL OPERATIONAL

2016 2.8 2.8 2.7 2.8 2.7 2.7

GREATER VANCOUVER(ALL INDUSTRIES, ALL LOCATIONS, EXCLUDING ZEROS)

2015 (ACTUAL) 2.7 2.7 2.7 2.7 2.7 2.6

2014 (ACTUAL) 2.8 2.9 3.0 2.8 2.7 2.8

2013 (ACTUAL) 2.9 3.0 2.9 2.8 2.8 2.7

2012 (ACTUAL) 3.0 3.1 3.1 3.0 3.0 2.9

© MERCER 2015 37

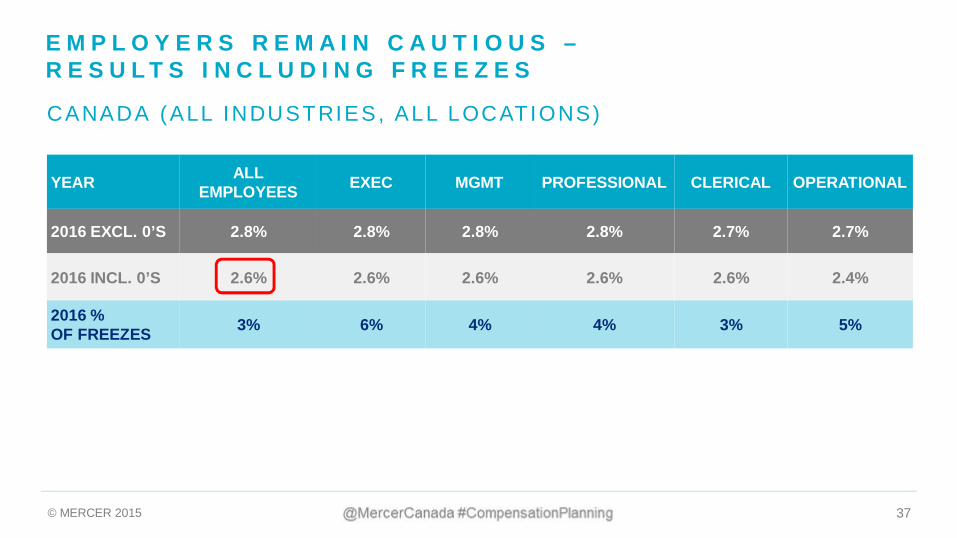

E M P L O Y E R S R E M A I N C A U T I O U S –R E S U L T S I N C L U D I N G F R E E Z E S

YEAR ALLEMPLOYEES EXEC MGMT PROFESSIONAL CLERICAL OPERATIONAL

2016 EXCL. 0’S 2.8% 2.8% 2.8% 2.8% 2.7% 2.7%

2016 INCL. 0’S 2.6% 2.6% 2.6% 2.6% 2.6% 2.4%

2016 %OF FREEZES 3% 6% 4% 4% 3% 5%

CANADA (ALL INDUSTRIES, ALL LOCATIONS)

© MERCER 2015 38

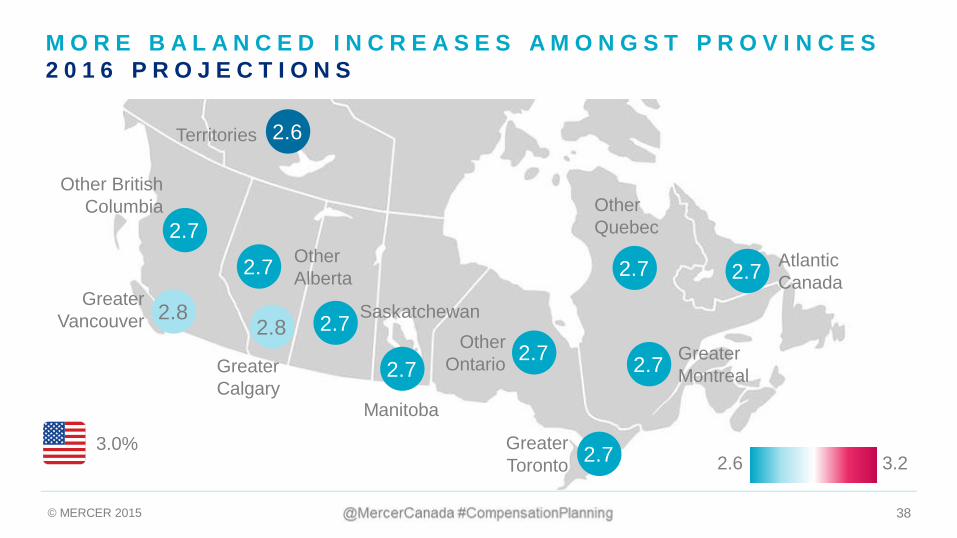

M O R E B A L A N C E D I N C R E A S E S A M O N G S T P R O V I N C E S2 0 1 6 P R O J E C T I O N S

OtherAlberta

GreaterCalgary

SaskatchewanGreater

Vancouver

Manitoba

GreaterMontreal

OtherQuebec

OtherOntario

Other BritishColumbia

GreaterToronto

AtlanticCanada

Territories

2.8

2.7

2.72.8

2.7 2.7

2.7

2.7

2.6

2.7

2.7

2.7

3.22.63.0%

© MERCER 2015 39

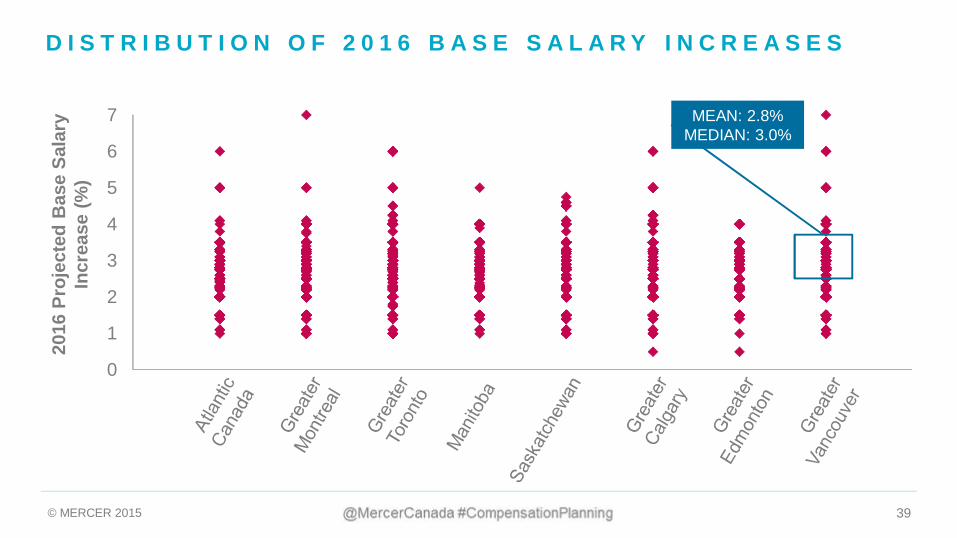

0

1

2

3

4

5

6

7

D I S T R I B U T I O N O F 2 0 1 6 B A S E S A L A R Y I N C R E A S E S20

16Pr

ojec

ted

Bas

eSa

lary

Incr

ease

(%)

MEAN: 2.8%MEDIAN: 3.0%

© MERCER 2015 40

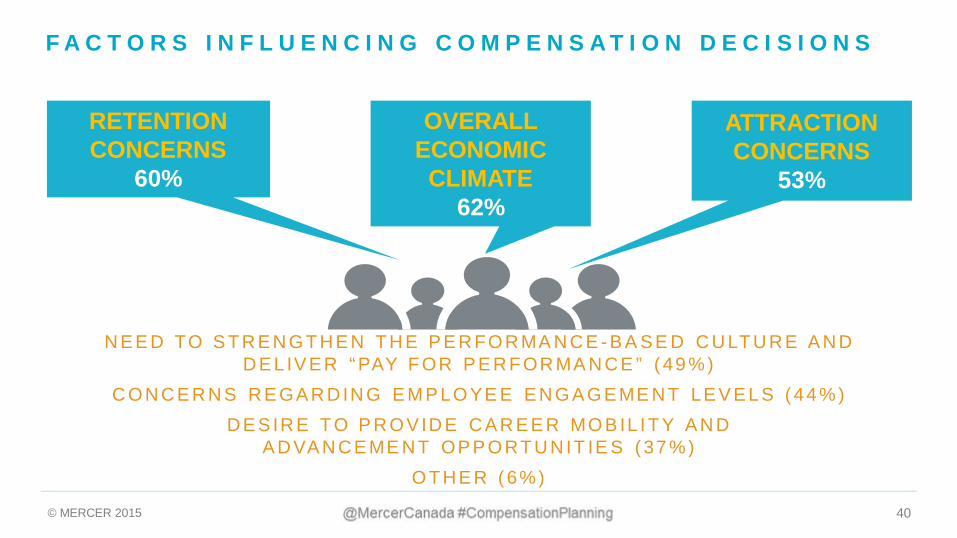

F A C T O R S I N F L U E N C I N G C O M P E N S A T I O N D E C I S I O N S

RETENTIONCONCERNS

60%

OVERALLECONOMIC

CLIMATE62%

ATTRACTIONCONCERNS

53%

N E E D TO S T R E N G T H E N T H E P E R FO R MA N C E - B A S E D C U LT U R E A N DD E L IV E R “ PAY F OR P E R F OR MA N C E ” ( 49 % )

C O N C E R N S R E GA R D IN G E M P LO YE E E N G A G E ME N T LE V E L S ( 44 % )D E S IR E T O P R O V ID E C A R E E R MO B IL I T Y A N D

A D VA N C E ME N T OP P O RT U N IT IE S ( 37 % )O T H E R ( 6% )

© MERCER 2015 41

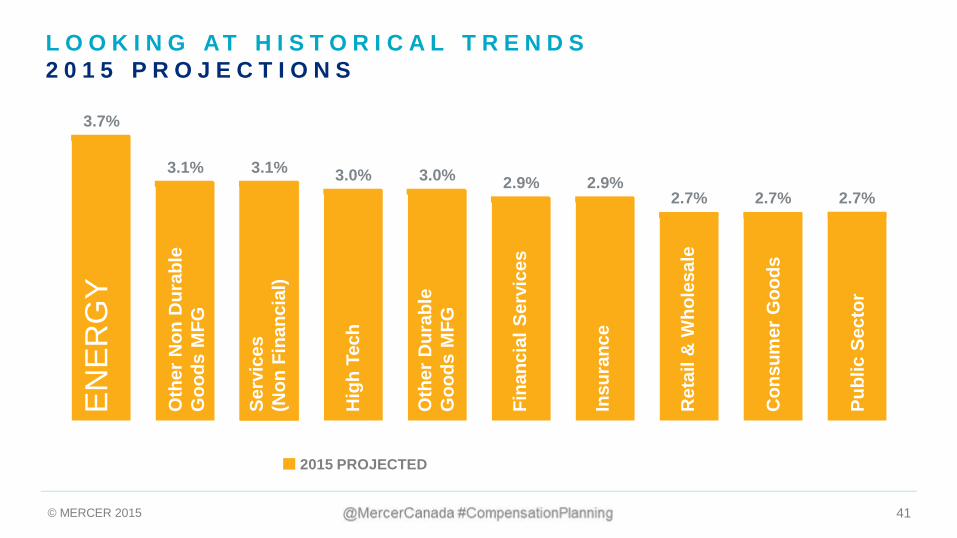

3.7%

3.1% 3.1% 3.0% 3.0% 2.9% 2.9%2.7% 2.7% 2.7%

L O O K I N G AT H I S T O R I C A L T R E N D S2 0 1 5 P R O J E C T I O N S

EN

ER

GY

Oth

erN

onD

urab

leG

oods

MFG

Serv

ices

(Non

Fina

ncia

l)

Hig

hTe

ch

Insu

ranc

e

Con

sum

erG

oods

Ret

ail&

Who

lesa

le

Publ

icSe

ctor

Oth

erD

urab

leG

oods

MFG

Fina

ncia

lSer

vice

s

2015 PROJECTED

© MERCER 2015 42

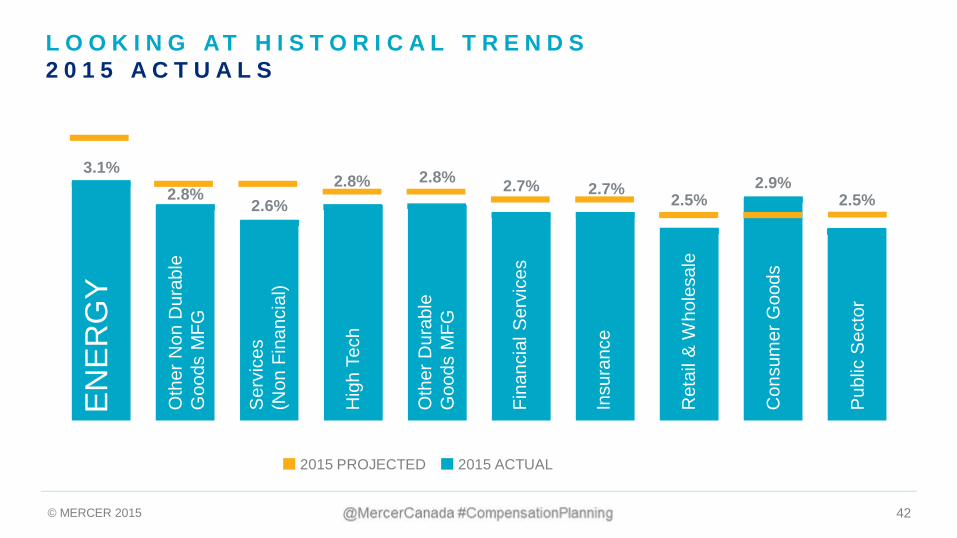

3.1%2.8%

2.6%2.8% 2.8% 2.7% 2.7%

2.5%2.9%

2.5%

L O O K I N G AT H I S T O R I C A L T R E N D S2 0 1 5 A C T U A L S

2015 PROJECTED 2015 ACTUAL

EN

ER

GY

Oth

erN

onD

urab

leG

oods

MFG

Ser

vice

s(N

onFi

nanc

ial)

Hig

hTe

ch

Insu

ranc

e

Con

sum

erG

oods

Ret

ail&

Who

lesa

le

Pub

licS

ecto

r

Oth

erD

urab

leG

oods

MFG

Fina

ncia

lSer

vice

s

© MERCER 2015 43

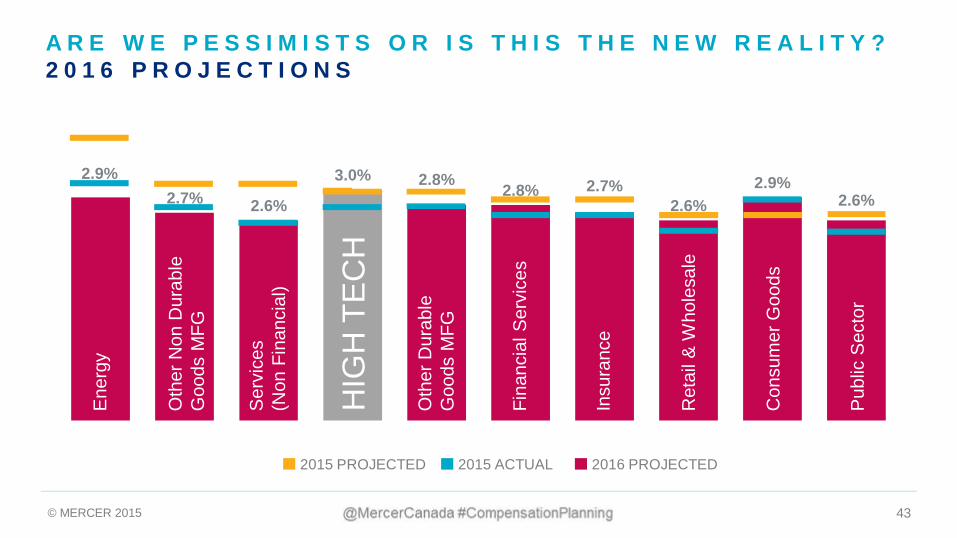

2.9%2.7% 2.6%

3.0% 2.8% 2.8% 2.7%2.6%

2.9%2.6%

A R E W E P E S S I M I S T S O R I S T H I S T H E N E W R E A L I T Y ?2 0 1 6 P R O J E C T I O N S

2015 PROJECTED 2016 PROJECTED2015 ACTUAL

Ene

rgy

Oth

erN

onD

urab

leG

oods

MFG

Ser

vice

s(N

onFi

nanc

ial)

HIG

HTE

CH

Insu

ranc

e

Con

sum

erG

oods

Ret

ail&

Who

lesa

le

Pub

licS

ecto

r

Oth

erD

urab

leG

oods

MFG

Fina

ncia

lSer

vice

s

© MERCER 2015 44

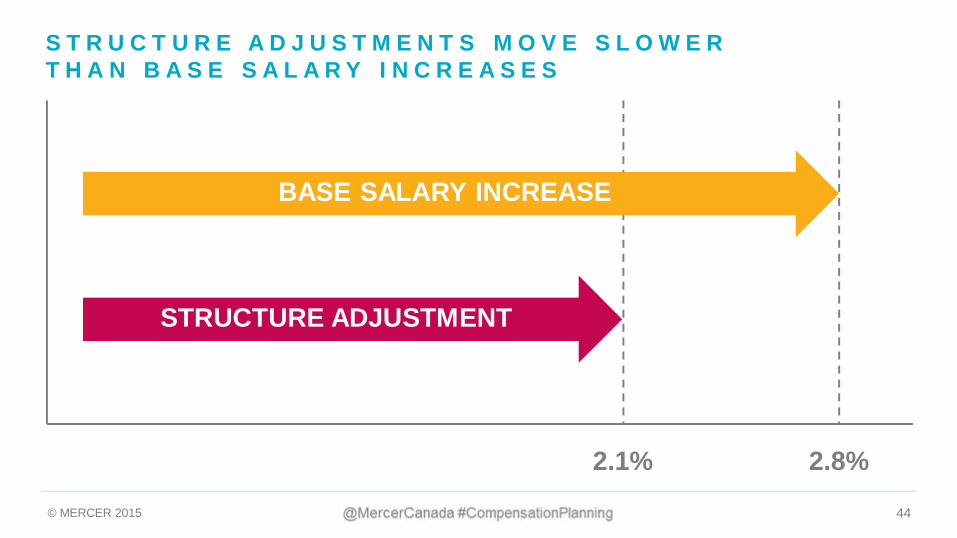

S T R U C T U R E A D J U S T M E N T S M O V E S L O W E RT H A N B A S E S A L A R Y I N C R E A S E S

BASE SALARY INCREASE

STRUCTURE ADJUSTMENT

2.1% 2.8%

© MERCER 2015 45

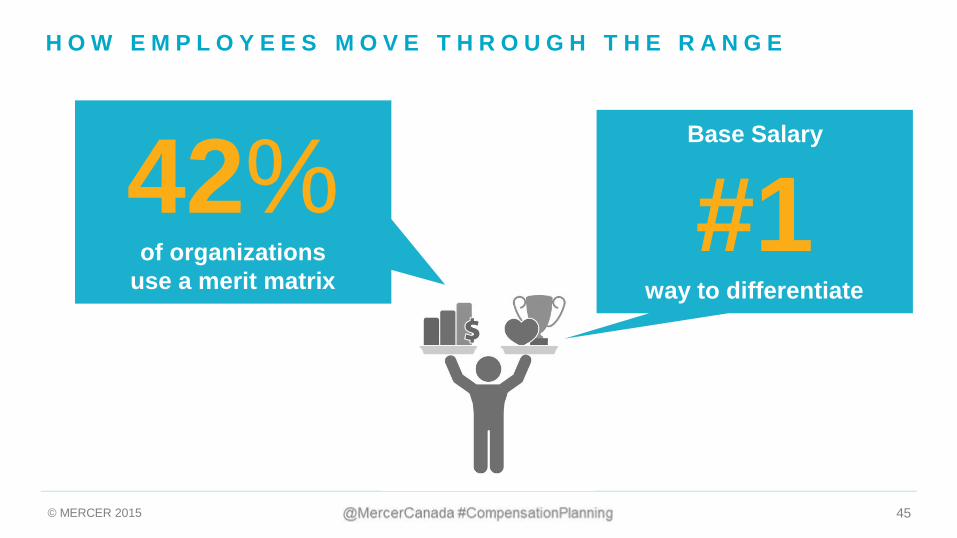

H O W E M P L O Y E E S M O V E T H R O U G H T H E R A N G E

42%of organizations

use a merit matrix

Base Salary

#1way to differentiate

© MERCER 2015 46

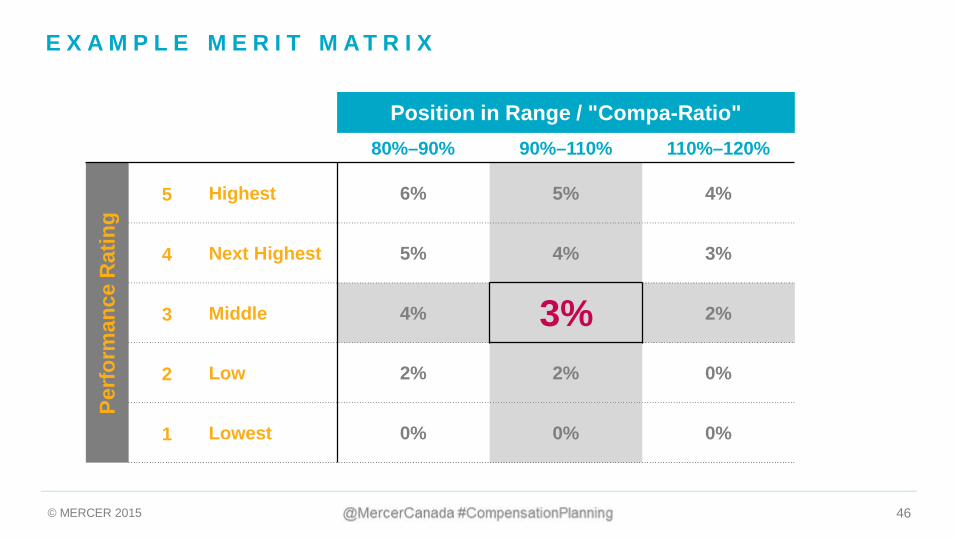

E X A M P L E M E R I T M A T R I X

Position in Range / "Compa-Ratio"80%–90% 90%–110% 110%–120%

Perf

orm

ance

Rat

ing

5 Highest 6% 5% 4%

4 Next Highest 5% 4% 3%

3 Middle 4% 3% 2%

2 Low 2% 2% 0%

1 Lowest 0% 0% 0%

© MERCER 2015 47

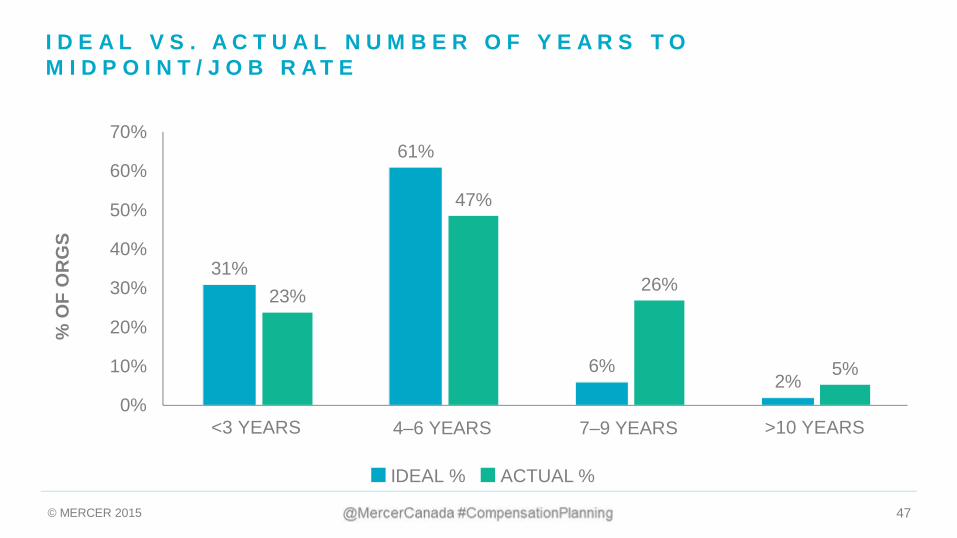

I D E A L V S . A C T U A L N U M B E R O F Y E A R S T OM I D P O I N T / J O B R A T E

31%

61%

6%2%

0%

10%

20%

30%

40%

50%

60%

70%

<3 YEARS 4–6 YEARS 7–9 YEARS >10 YEARS

%O

FO

RG

S

IDEAL %

23%

47%

26%

5%

ACTUAL %

© MERCER 2015 48

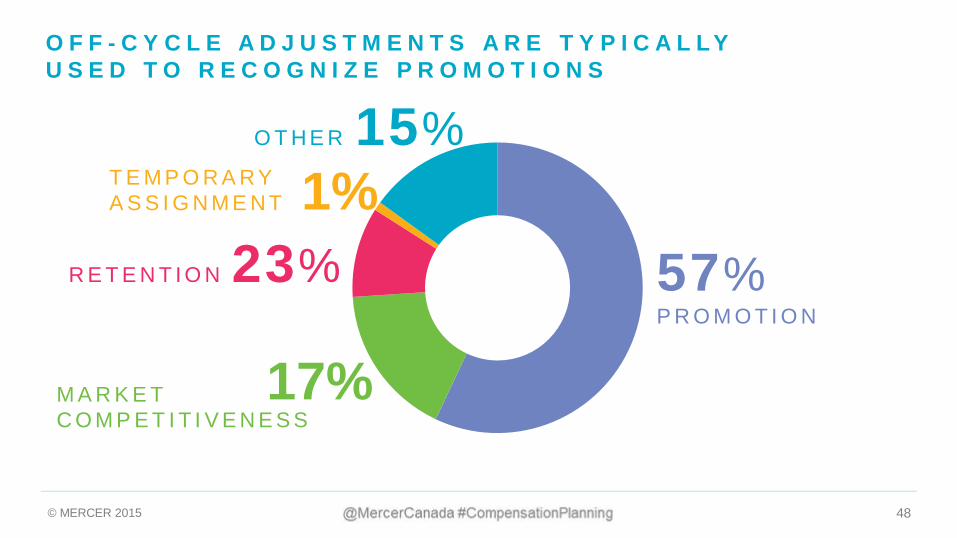

1%

17%

T E M P O R A R YA S S I G N M E N T

O F F - C Y C L E A D J U S T M E N T S A R E T Y P I C A L L YU S E D T O R E C O G N I Z E P R O M O T I O N S

O T H E R 15%

R E T E N T I O N 23%

M A R K E TC O M P E T I T I V E N E S S

57%P R O M O T I O N

© MERCER 2015 49© MERCER 2015 49

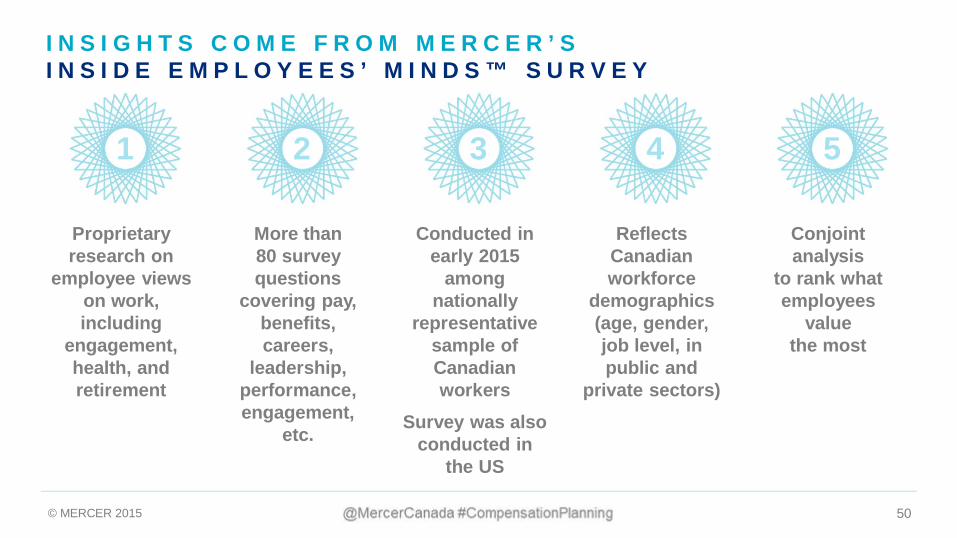

INS IDE EMPLO YEES’ MINDS

© MERCER 2015 50

Proprietaryresearch on

employee viewson work,including

engagement,health, andretirement

More than80 surveyquestions

covering pay,benefits,careers,

leadership,performance,engagement,

etc.

Conducted inearly 2015

amongnationally

representativesample ofCanadianworkers

Survey was alsoconducted in

the US

ReflectsCanadianworkforce

demographics(age, gender,job level, inpublic and

private sectors)

Conjointanalysis

to rank whatemployees

valuethe most

1 2 3 4 5

I N S I G H T S C O M E F R O M M E R C E R ’ SI N S I D E E M P L O Y E E S ’ M I N D S ™ S U R V E Y

© MERCER 2015 51

Two out of five privatesector workers in

Canada are seriouslyconsidering leaving

Base pay continuesto be most important

reward element,followed by

retirement, andlow-cost health care

W H A T ’ S O N E M P L O Y E E S ’ M I N D S :I ’ M S A T I S F I E D … B U T L E A V I N G

Three out of five whosay they are satisfiedwith the type of job

they do areconsidering leaving

© MERCER 2015 52

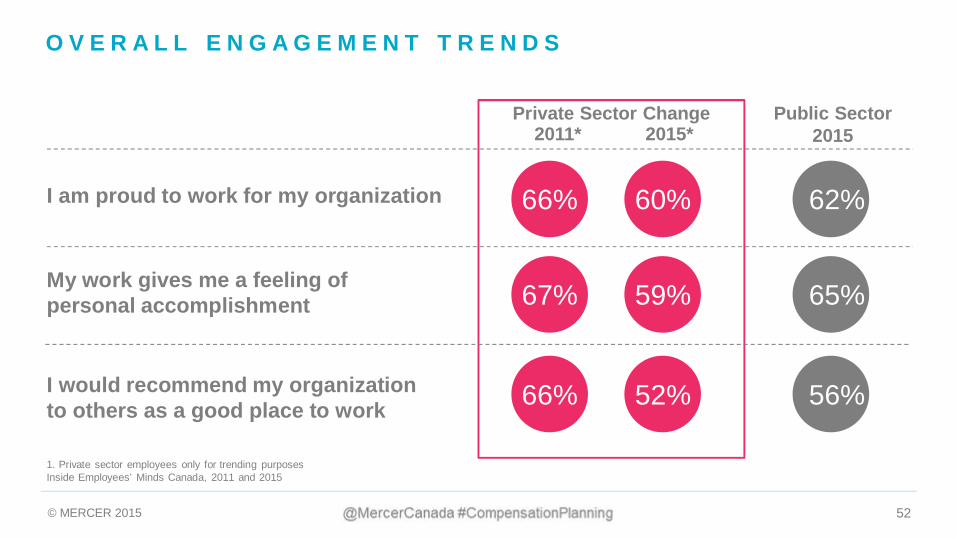

59%67% 65%My work gives me a feeling ofpersonal accomplishment

52%66% 56%I would recommend my organizationto others as a good place to work

1. Private sector employees only for trending purposesInside Employees’ Minds Canada, 2011 and 2015

2011* 2015*

I am proud to work for my organization 60%66% 62%

Private Sector Change Public Sector2015

O V E R A L L E N G A G E M E N T T R E N D S

© MERCER 2015 53

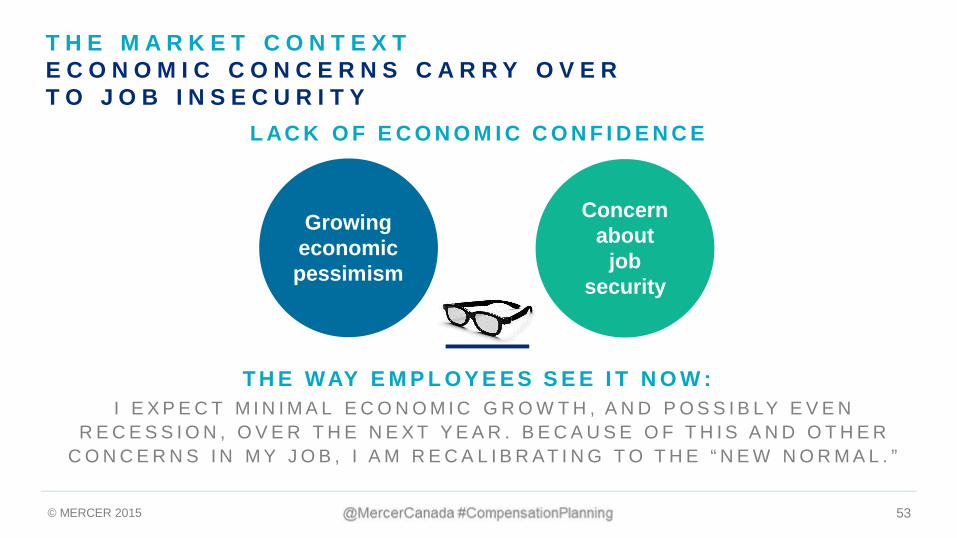

I E X P E C T M I N I M A L E C O N O M I C G R O W T H , A N D P O S S I B LY E V E NR E C E S S I O N , O V E R T H E N E X T Y E A R . B E C A U S E O F T H I S A N D O T H E R

C O N C E R N S I N M Y J O B , I A M R E C A L I B R AT I N G T O T H E “ N E W N O R M A L . ”

T H E WAY E M P L O Y E E S S E E I T N O W :

L AC K O F E C O N O M I C C O N F I D E N C E

Concernabout

jobsecurity

Growingeconomicpessimism

T H E M A R K E T C O N T E X TE C O N O M I C C O N C E R N S C A R R Y O V E RT O J O B I N S E C U R I T Y

© MERCER 2015 54

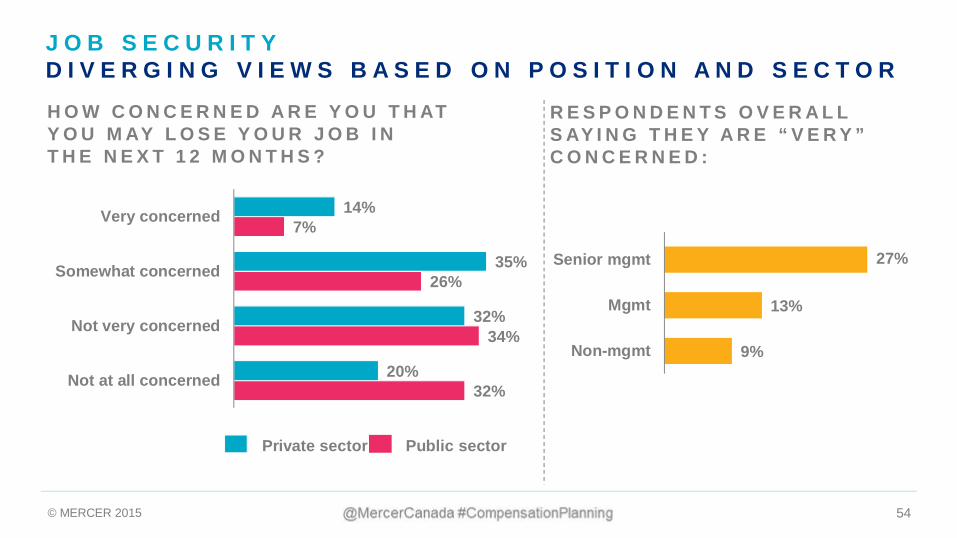

H O W C O N C E R N E D A R E Y O U T H ATY O U M AY L O S E Y O U R J O B I NT H E N E X T 1 2 M O N T H S ?

Private sector Public sector

32%

34%

26%

7%

20%

32%

35%

14%

Not at all concerned

Not very concerned

Somewhat concerned

Very concerned

R E S P O N D E N T S O V E R A L LS AY I N G T H E Y A R E “ V E R Y ”C O N C E R N E D :

9%

13%

27%

Non-mgmt

Mgmt

Senior mgmt

J O B S E C U R I T YD I V E R G I N G V I E W S B A S E D O N P O S I T I O N A N D S E C T O R

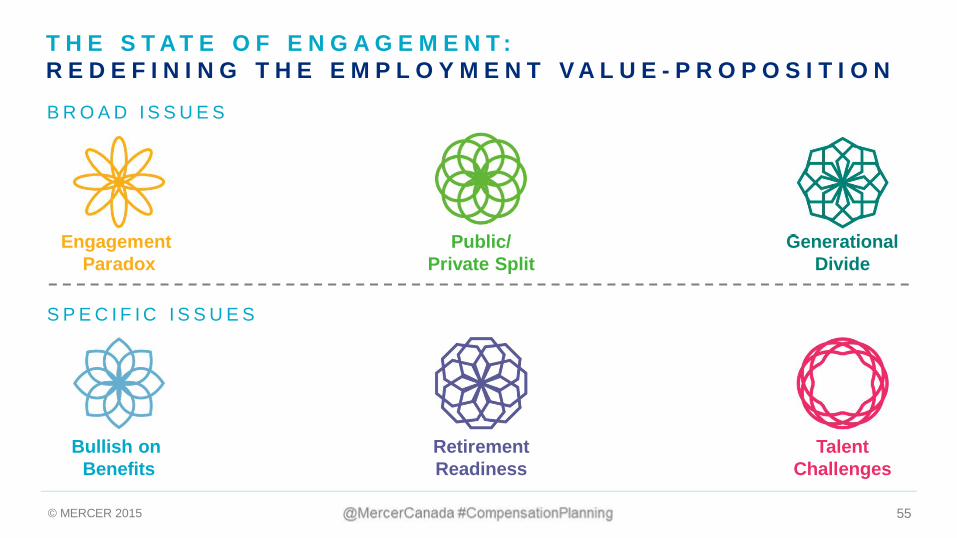

© MERCER 2015 55

B R O A D I S S U E S

S P E C I F I C I S S U E S

EngagementParadox

Public/Private Split

GenerationalDivide

Bullish onBenefits

RetirementReadiness

TalentChallenges

T H E S T A T E O F E N G A G E M E N T :R E D E F I N I N G T H E E M P L O Y M E N T V A L U E - P R O P O S I T I O N

© MERCER 2015 56

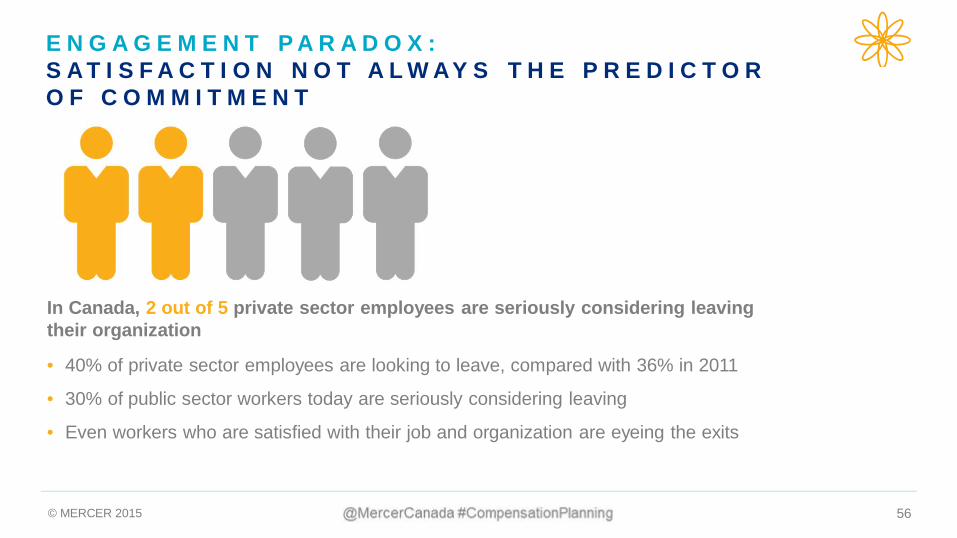

In Canada, 2 out of 5 private sector employees are seriously considering leavingtheir organization

• 40% of private sector employees are looking to leave, compared with 36% in 2011

• 30% of public sector workers today are seriously considering leaving

• Even workers who are satisfied with their job and organization are eyeing the exits

E N G A G E M E N T P A R A D O X :S A T I S F A C T I O N N O T A L W AY S T H E P R E D I C T O RO F C O M M I T M E N T

© MERCER 2015 57

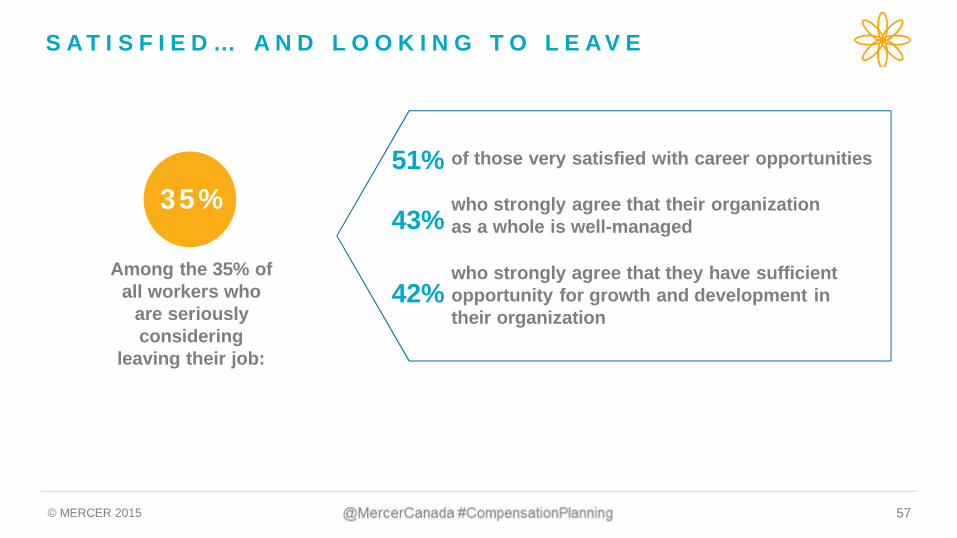

S A T I S F I E D … A N D L O O K I N G T O L E A V E

Among the 35% ofall workers who

are seriouslyconsidering

leaving their job:

35%of those very satisfied with career opportunities

who strongly agree that they have sufficientopportunity for growth and development intheir organization

who strongly agree that their organizationas a whole is well-managed

51%

43%

42%

© MERCER 2015 58

30%

45%

67%

58%

71%

85%

Non-management

Management

Senior management

Satisfaction with organization Looking to leave

S E N I O R M A N A G E R S A R E M O R E T H A N T W I C E A S L I K E LY A SN O N - M A N A G E M E N T E M P L O Y E E S T O B E S E R I O U S LY C O N S I D E R I N GL E AV I N G T H E I R O R G A N I Z AT I O N S AT T H E P R E S E N T T I M E

S A T I S F I E D … A N D L O O K I N G T O L E A V ES E N I O R M A N A G E M E N T

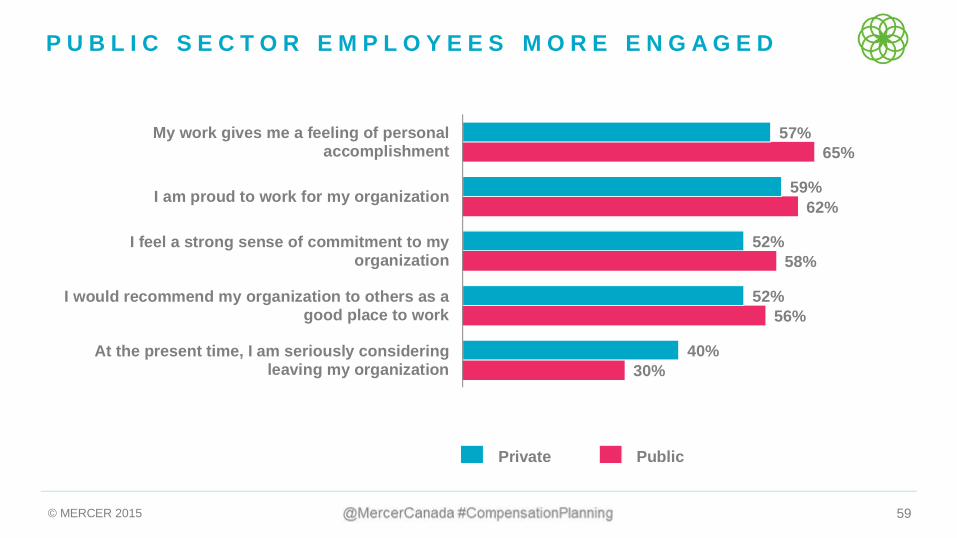

© MERCER 2015 59

30%

56%

58%

62%

65%

40%

52%

52%

59%

57%

At the present time, I am seriously consideringleaving my organization

I would recommend my organization to others as agood place to work

I feel a strong sense of commitment to myorganization

I am proud to work for my organization

My work gives me a feeling of personalaccomplishment

Private Public

P U B L I C S E C T O R E M P L O Y E E S M O R E E N G A G E D

© MERCER 2015 60

G E N E R A T I O N G A P :Y O U N G E M P L O Y E E S H A V E M I X E D V I E W S O F W O R K

In Canada, 44% under age 35 are considering leaving

• Employees age 34 and under are more positive about most aspects of work, but:

• More likely to be seriously considering leaving their job

• Employees 50 and older are much less positive about work, less likely to leave

© MERCER 2015 61

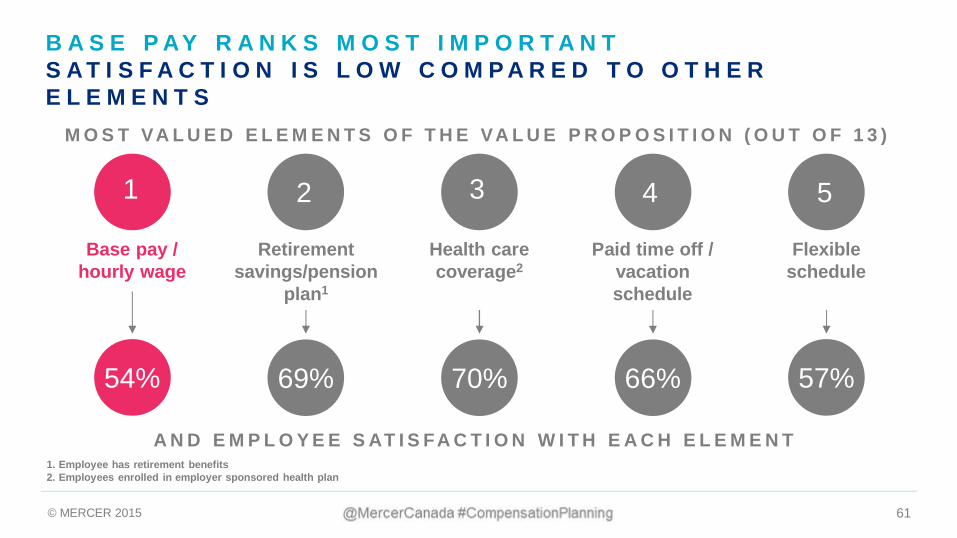

M O S T VA L U E D E L E M E N T S O F T H E VA L U E P R O P O S I T I O N ( O U T O F 1 3 )

A N D E M P L O Y E E S AT I S FA C T I O N W I T H E A C H E L E M E N T

2

Retirementsavings/pension

plan1

69%

3

Health carecoverage2

70%

4

Paid time off /vacationschedule

66%

5

Flexibleschedule

57%

1

Base pay /hourly wage

54%

B A S E P AY R A N K S M O S T I M P O R T A N TS A T I S F A C T I O N I S L O W C O M P A R E D T O O T H E RE L E M E N T S

1. Employee has retirement benefits2. Employees enrolled in employer sponsored health plan

© MERCER 2015 62

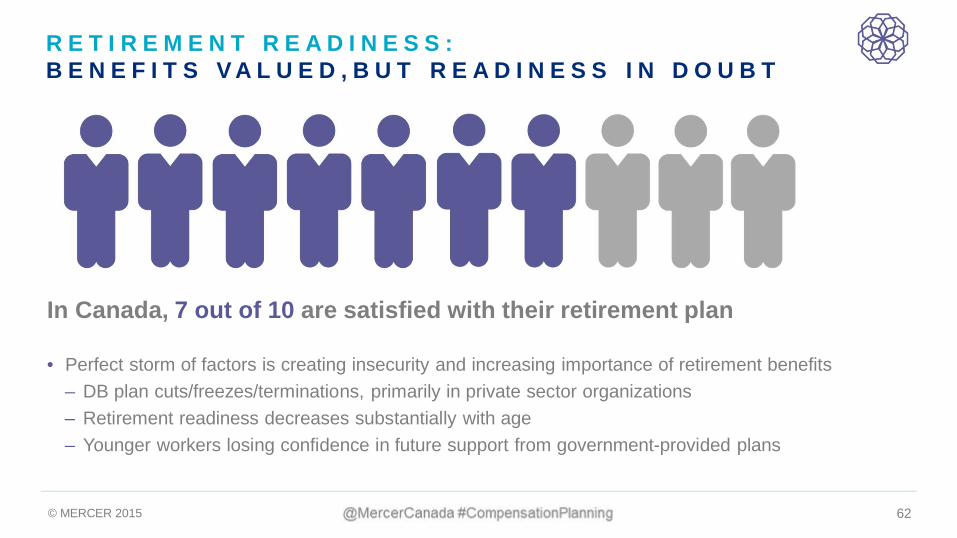

R E T I R E M E N T R E A D I N E S S :B E N E F I T S V A L U E D , B U T R E A D I N E S S I N D O U B T

In Canada, 7 out of 10 are satisfied with their retirement plan

• Perfect storm of factors is creating insecurity and increasing importance of retirement benefits– DB plan cuts/freezes/terminations, primarily in private sector organizations– Retirement readiness decreases substantially with age– Younger workers losing confidence in future support from government-provided plans

© MERCER 2015 63

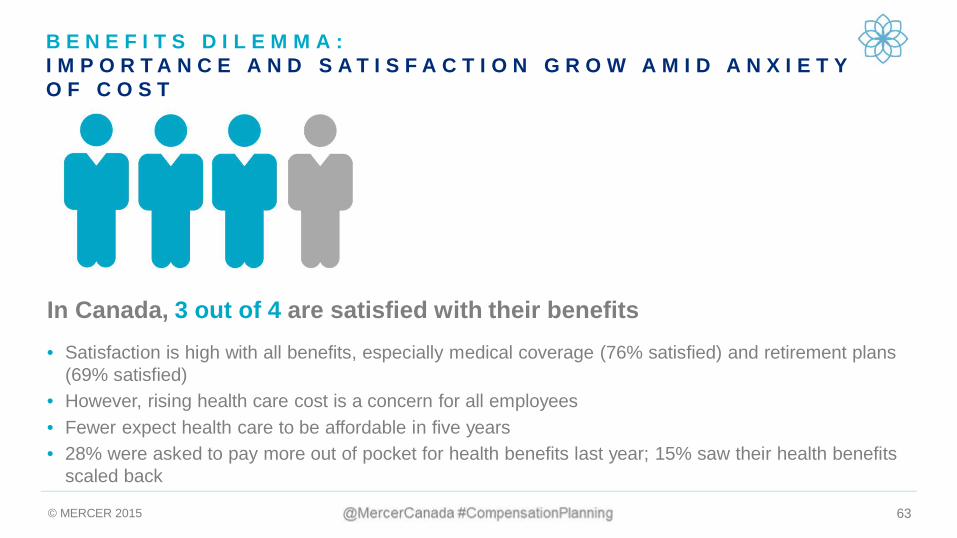

B E N E F I T S D I L E M M A :I M P O R T A N C E A N D S A T I S F A C T I O N G R O W A M I D A N X I E T YO F C O S T

In Canada, 3 out of 4 are satisfied with their benefits• Satisfaction is high with all benefits, especially medical coverage (76% satisfied) and retirement plans

(69% satisfied)• However, rising health care cost is a concern for all employees• Fewer expect health care to be affordable in five years• 28% were asked to pay more out of pocket for health benefits last year; 15% saw their health benefits

scaled back

© MERCER 2015 64

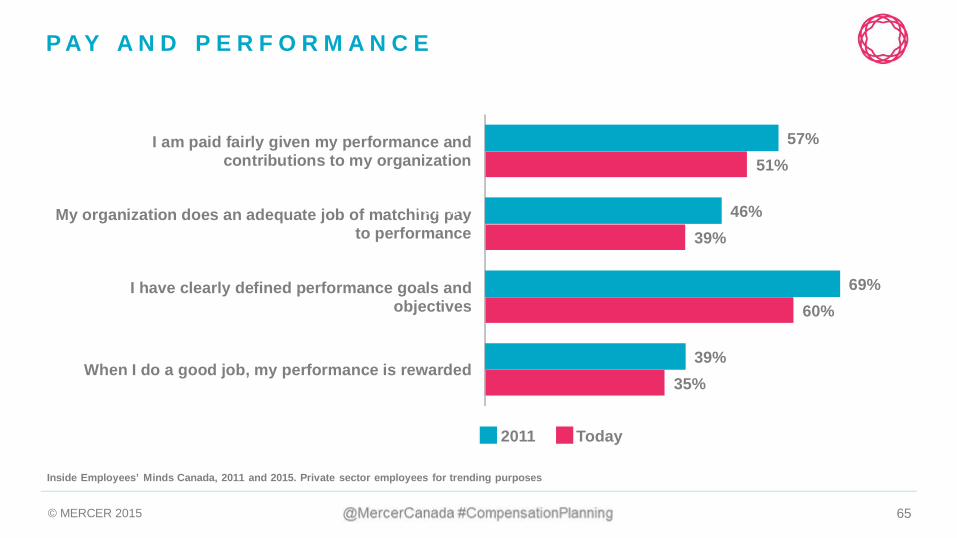

M A T C H I N G P AY A N D P E R F O R M A N C E

In Canada, about 1 out of 3 say their organization does an adequate job ofmatching pay to performance• Disconnect exists between pay and performance• Employers providing less support in careers and not retaining the best, say employees• Scores in most categories trend lower since 2011• Upbeat assessments on diversity, dignity, and respect

© MERCER 2015 65

35%

60%

39%

51%

39%

69%

46%

57%

When I do a good job, my performance is rewarded

I have clearly defined performance goals andobjectives

My organization does an adequate job of matching payto performance

I am paid fairly given my performance andcontributions to my organization

2011

TODAY

P AY A N D P E R F O R M A N C E

Inside Employees’ Minds Canada, 2011 and 2015. Private sector employees for trending purposes

2011 Today

© MERCER 2015 66

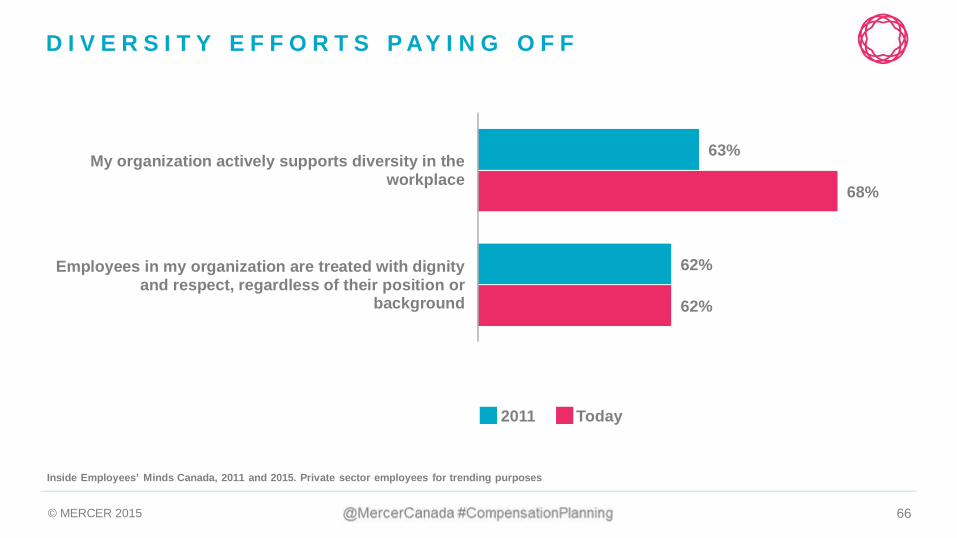

D I V E R S I T Y E F F O R T S P AY I N G O F F

62%

68%

62%

63%

Employees in my organization are treated with dignityand respect, regardless of their position or

background

My organization actively supports diversity in theworkplace

Inside Employees’ Minds Canada, 2011 and 2015. Private sector employees for trending purposes

2011 Today

© MERCER 2015 67

W H A T ’ S N E X T

STAY TUNED

© MERCER 2015 68

K E Y T A K E A W AY S

MAJORITY OFCANADIANORGANIZATIONSARE BEING MORECAUTIOUS WITHTHEIR BUDGETS IN2015 AND 2016COMPARED TOPREVIOUS YEARS

OVERALL ECONOMICCLIMATE IS THE MOSTCOMMON FACTORINFLUENCINGDECISION-MAKERSCOMPENSATIONDECISIONS FOR 2016

HAPPY DOES NOTMEAN STAYING

ARTICULATE AVALUEPROPOSITION THATSPEAKS TO ALLDEMOGRAPHICSAND EVOLVES OVERTIME

ORGANIZATIONSNEED TOUNDERSTAND THEENGAGEMENTDRIVERS FORTHEIR WORKFORCEIN ORDER TOMOTIVATE ANDRETAIN TALENT

© MERCER 2015 69

Q U E S T I O N S F R O M T H E A U D I E N C E

Ailsa ForsgrenPartner

Western Canada Talent Leader

604 609 [email protected]

Graham DoddPartner

North American Regional PracticeLeader, Talent Strategies

604 609 [email protected]