Embed Size (px)

DESCRIPTION

InMobi's Mobile World Congress Thought Leadership Whitepaper Series: Defining the next phase of mobile adverting.

Citation preview

www.inmobi.com

THOUGHTSERIES

LEADERSHIP

MOBILE WORLD CONGRESS

DEVELOPERS AS INNOVATORS

14 - 17 FEB, 2011

© 2011 InMobi. Developers as Innovators Page 1 www.inmobi.com

13 February, 2011

As 2010 came to a close, it was clear that the debate over if “this will be the year of mobile advertising” ended with it. Good riddance! Mobile advertising is clearly here to stay and it’s absolutely huge. Ad spending figures aside, consumers have announced their intentions by flocking to mobile, and advertisers have no choice but to follow.

While the journalists and bloggers busily draft lists and make predictions, at InMobi, we decided to take a slightly different approach. Rather than simply add to the noise, we took a step back and asked ourselves “what will define the next phase of mobile advertising?”

We chose to develop a series of whitepapers and offer in depth analysis, for a select number of topics. For the series we discuss three concepts that we think will define the next phase of mobile advertising. We invited partners in the industry to collaborate with us, and invite you to join the conversation on twitter@inmobi or on our blog at www.inmobi.com/inmobiblog.

James LambertiVP, Global Marketing and ResearchInMobi,

THOUGHT LEADERSHIP SERIES:DEFINING THE NEXT PHASE OF MOBILE ADVERTISING

InMobi is the world’s largest independent mobile advertising network. With offices on four continents we provide advertisers, publishers and developers with a uniquely global solution for advertising. Our network is growing fast and we now deliver the unprecedented ability to reach 194 Million consumers, in over 115 countries, through more than U.S. $31.5 Billion mobile ad impressions monthly. We recently were selected as a 2010 AlwaysOn Global 250 Company to Watch in Silicon Valley.

InMobi is venture-backed with marquee investors including: Kleiner, Perkins, Caufield & Byers and Sherpalo Ventures. The company has offices in London, San Francisco, Bangalore, Tokyo, and Singapore.

ABOUT INMOBI

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators Page 1 www.inmobi.com

13 February, 2011

As 2010 came to a close, it was clear that the debate over if “this will be the year of mobile advertising” ended with it. Good riddance! Mobile advertising is clearly here to stay and it’s absolutely huge. Ad spending figures aside, consumers have announced their intentions by flocking to mobile, and advertisers have no choice but to follow.

While the journalists and bloggers busily draft lists and make predictions, at InMobi, we decided to take a slightly different approach. Rather than simply add to the noise, we took a step back and asked ourselves “what will define the next phase of mobile advertising?”

We chose to develop a series of whitepapers and offer in depth analysis, for a select number of topics. For the series we discuss three concepts that we think will define the next phase of mobile advertising. We invited partners in the industry to collaborate with us, and invite you to join the conversation on twitter@inmobi or on our blog at www.inmobi.com/inmobiblog.

James LambertiVP, Global Marketing and ResearchInMobi,

THOUGHT LEADERSHIP SERIES:DEFINING THE NEXT PHASE OF MOBILE ADVERTISING

InMobi is the world’s largest independent mobile advertising network. With offices on four continents we provide advertisers, publishers and developers with a uniquely global solution for advertising. Our network is growing fast and we now deliver the unprecedented ability to reach 194 Million consumers, in over 115 countries, through more than U.S. $31.5 Billion mobile ad impressions monthly. We recently were selected as a 2010 AlwaysOn Global 250 Company to Watch in Silicon Valley.

InMobi is venture-backed with marquee investors including: Kleiner, Perkins, Caufield & Byers and Sherpalo Ventures. The company has offices in London, San Francisco, Bangalore, Tokyo, and Singapore.

ABOUT INMOBI

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators www.inmobi.com

The outcome is that developers will drive innovation in mobile advertising. They have billions to gain, nothing to hold them back, and are in control of their own destiny. This last point leads to our next trend.

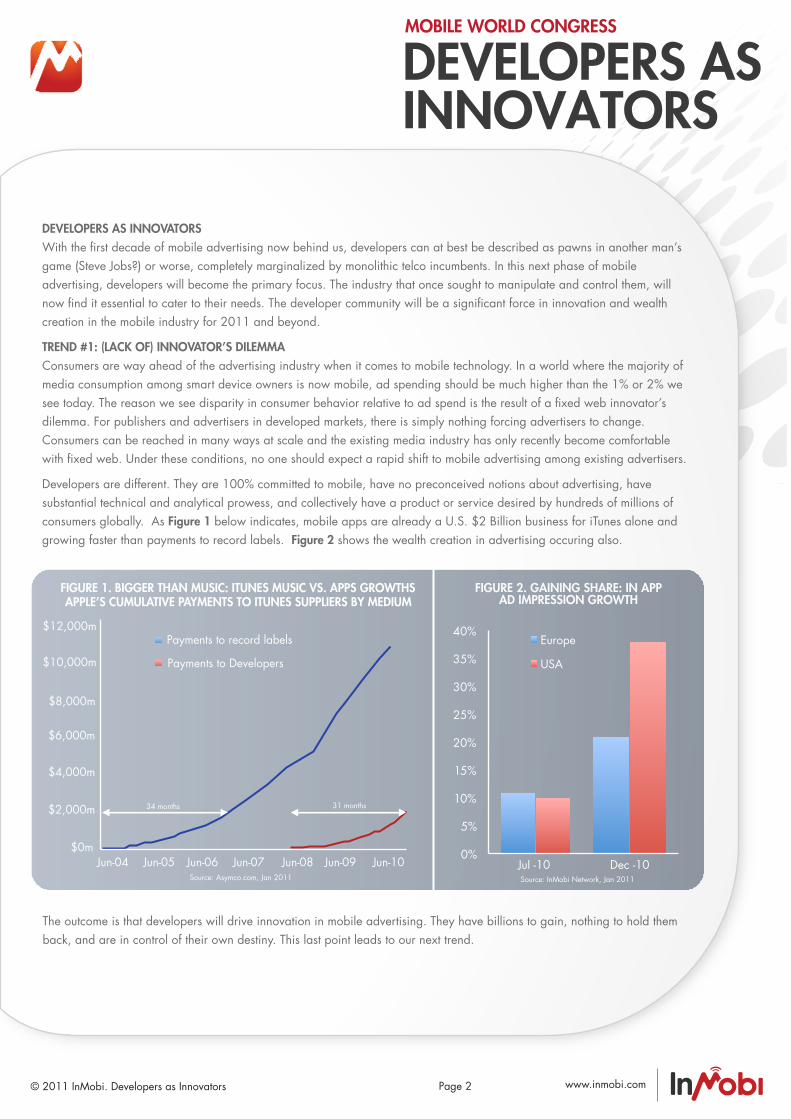

FIGURE 1. BIGGER THAN MUSIC: ITUNES MUSIC VS. APPS GROWTHSAPPLE’S CUMULATIVE PAYMENTS TO ITUNES SUPPLIERS BY MEDIUM

Payments to record labels

Source: Asymco.com, Jan 2011

34 months 31 months

Payments to Developers

$12,000m

$10,000m

$8,000m

$6,000m

$4,000m

$2,000m

$0mJun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 Jun-10

DEVELOPERS AS INNOVATORSWith the first decade of mobile advertising now behind us, developers can at best be described as pawns in another man’s game (Steve Jobs?) or worse, completely marginalized by monolithic telco incumbents. In this next phase of mobile advertising, developers will become the primary focus. The industry that once sought to manipulate and control them, will now find it essential to cater to their needs. The developer community will be a significant force in innovation and wealth creation in the mobile industry for 2011 and beyond.

TREND #1: (LACK OF) INNOVATOR’S DILEMMAConsumers are way ahead of the advertising industry when it comes to mobile technology. In a world where the majority of media consumption among smart device owners is now mobile, ad spending should be much higher than the 1% or 2% we see today. The reason we see disparity in consumer behavior relative to ad spend is the result of a fixed web innovator’s dilemma. For publishers and advertisers in developed markets, there is simply nothing forcing advertisers to change. Consumers can be reached in many ways at scale and the existing media industry has only recently become comfortable with fixed web. Under these conditions, no one should expect a rapid shift to mobile advertising among existing advertisers.

Developers are different. They are 100% committed to mobile, have no preconceived notions about advertising, have substantial technical and analytical prowess, and collectively have a product or service desired by hundreds of millions of consumers globally. As Figure 1 below indicates, mobile apps are already a U.S. $2 Billion business for iTunes alone and growing faster than payments to record labels. Figure 2 shows the wealth creation in advertising occuring also.

0%

5%

10%

15%

20%

25%

30%

35%

40%

Jul -10 Dec -10

Europe

USA

FIGURE 2. GAINING SHARE: IN APPAD IMPRESSION GROWTH

Source: InMobi Network, Jan 2011

Page 2

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators www.inmobi.com

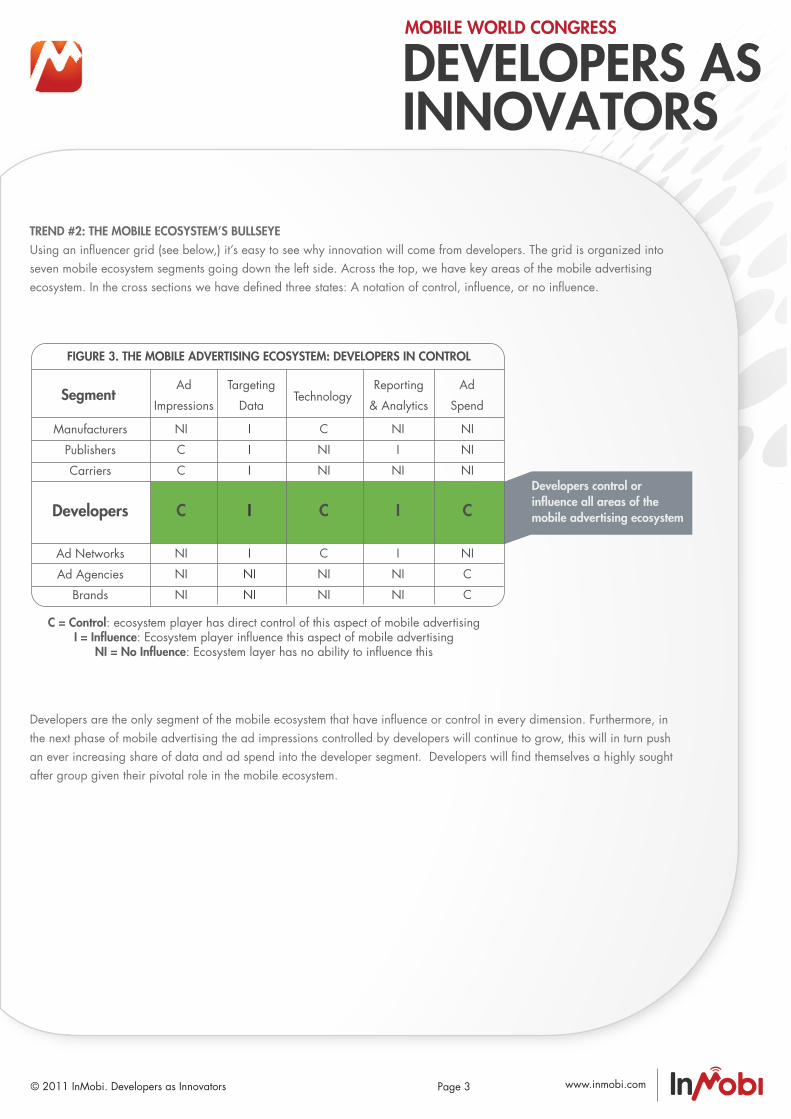

TREND #2: THE MOBILE ECOSYSTEM’S BULLSEYEUsing an influencer grid (see below,) it’s easy to see why innovation will come from developers. The grid is organized into seven mobile ecosystem segments going down the left side. Across the top, we have key areas of the mobile advertising ecosystem. In the cross sections we have defined three states: A notation of control, influence, or no influence.

Developers are the only segment of the mobile ecosystem that have influence or control in every dimension. Furthermore, in the next phase of mobile advertising the ad impressions controlled by developers will continue to grow, this will in turn push an ever increasing share of data and ad spend into the developer segment. Developers will find themselves a highly sought after group given their pivotal role in the mobile ecosystem.

Manufacturers

Publishers

Carriers

Developers

Ad Networks

Ad Agencies

Brands

SegmentAd

Impressions

Targeting

DataTechnology

Reporting

& Analytics

Ad

Spend

NI

C

C

C

NI

NI

NI

I

I

I

I

I

NI

NI

C

NI

NI

C

C

NI

NI

NI

I

NI

I

I

NI

NI

NI

NI

NI

C

NI

C

C

FIGURE 3. THE MOBILE ADVERTISING ECOSYSTEM: DEVELOPERS IN CONTROL

C = Control: ecosystem player has direct control of this aspect of mobile advertisingI = Influence: Ecosystem player influence this aspect of mobile advertising

NI = No Influence: Ecosystem layer has no ability to influence this

Page 3

Developers control or influence all areas of the mobile advertising ecosystem

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators www.inmobi.com

TREND #2: THE MOBILE ECOSYSTEM’S BULLSEYEUsing an influencer grid (see below,) it’s easy to see why innovation will come from developers. The grid is organized into seven mobile ecosystem segments going down the left side. Across the top, we have key areas of the mobile advertising ecosystem. In the cross sections we have defined three states: A notation of control, influence, or no influence.

Developers are the only segment of the mobile ecosystem that have influence or control in every dimension. Furthermore, in the next phase of mobile advertising the ad impressions controlled by developers will continue to grow, this will in turn push an ever increasing share of data and ad spend into the developer segment. Developers will find themselves a highly sought after group given their pivotal role in the mobile ecosystem.

Manufacturers

Publishers

Carriers

Developers

Ad Networks

Ad Agencies

Brands

SegmentAd

Impressions

Targeting

DataTechnology

Reporting

& Analytics

Ad

Spend

NI

C

C

C

NI

NI

NI

I

I

I

I

I

NI

NI

C

NI

NI

C

C

NI

NI

NI

I

NI

I

I

NI

NI

NI

NI

NI

C

NI

C

C

FIGURE 3. THE MOBILE ADVERTISING ECOSYSTEM: DEVELOPERS IN CONTROL

C = Control: ecosystem player has direct control of this aspect of mobile advertisingI = Influence: Ecosystem player influence this aspect of mobile advertising

NI = No Influence: Ecosystem layer has no ability to influence this

Page 3

Developers control or influence all areas of the mobile advertising ecosystem

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators www.inmobi.com

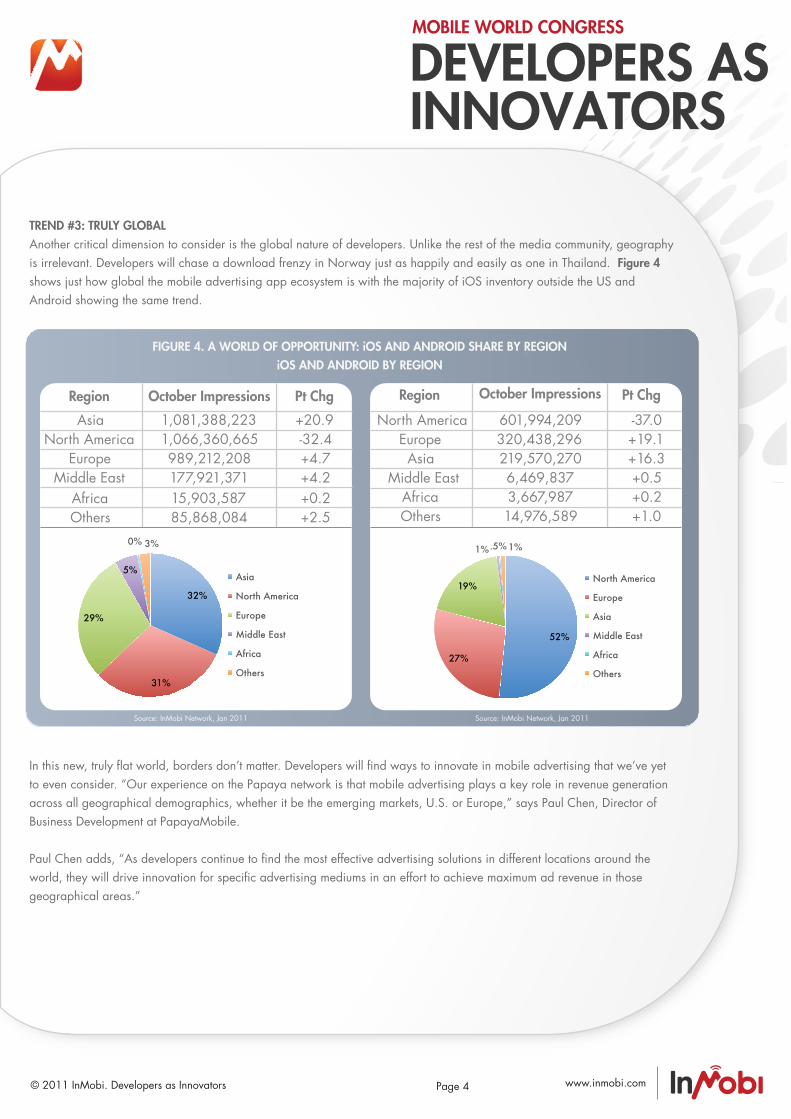

TREND #3: TRULY GLOBALAnother critical dimension to consider is the global nature of developers. Unlike the rest of the media community, geography is irrelevant. Developers will chase a download frenzy in Norway just as happily and easily as one in Thailand. Figure 4 shows just how global the mobile advertising app ecosystem is with the majority of iOS inventory outside the US and Android showing the same trend.

In this new, truly flat world, borders don’t matter. Developers will find ways to innovate in mobile advertising that we’ve yet to even consider. “Our experience on the Papaya network is that mobile advertising plays a key role in revenue generation across all geographical demographics, whether it be the emerging markets, U.S. or Europe,” says Paul Chen, Director of Business Development at PapayaMobile.

Paul Chen adds, “As developers continue to find the most effective advertising solutions in different locations around the world, they will drive innovation for specific advertising mediums in an effort to achieve maximum ad revenue in those geographical areas.”

Region October Impressions Pt Chg

Asia 1,081,388,223 +20.9North America 1,066,360,665 -32.4

Europe 989,212,208 +4.7Middle East 177,921,371 +4.2

Africa 15,903,587 +0.2Others 85,868,084 +2.5

Region Pt Chg

North America 601,994,209 -37.0Europe 320,438,296 +19.1Asia 219,570,270 +16.3

Middle East 6,469,837 +0.5Africa 3,667,987 +0.2Others 14,976,589 +1.0

October Impressions

32%

31%

29%

5%

0% 3%

Asia

North America

Europe

Middle East

Africa

Others

52%

27%

19%

1%.5% 1%

North America

Europe

Asia

Middle East

Africa

Others

FIGURE 4. A WORLD OF OPPORTUNITY: iOS AND ANDROID SHARE BY REGIONiOS AND ANDROID BY REGION

Page 4

Source: InMobi Network, Jan 2011Source: InMobi Network, Jan 2011

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS

© 2011 InMobi. Developers as Innovators www.inmobi.com

TREND #4: DEVELOPERS ARE SAVVY BUSINESS PEOPLEMobile gaming is great example of evolved business models emerging from the developer community. It is a highly competitive industry and the competition continues to increase. Given this, dynamic developers cannot expect to create a successful, well monetizable game without proper business planning. Developers have taken note. They are increasingly becoming more business savvy and understand the value in the implementation of effective monetization strategies.

As an example PapayaMobile, Android’s largest social gaming platform, has continuously evolved the monetization solutions they provide to developers. “In game banner ads used to be the status quo for monetizing freemium games. But as developers have become more attuned with other monetization and business solutions, PapayaMobile now must offer tools for wall advertisements, in-app microtransactions, support for various billing solution, and others,” says Paul Chen.

CONCLUSIONDevelopers are no longer an interesting byline of the mobile ecosystem. They are global, independent, innovative, and savvy technicians and business people. The rest of us will end up following their lead in the next phase of mobile advertising as a result.

AuthorsJames Lamberti, InMobiContributions from Paul Chen, Papaya Mobile

“Competition is tough and developers are beginning to realize that a business mentality is needed to evaluate which solutions will most effectively sustain and grow their revenue. From our perspective, we expect continued maturity of the various monetization solutions in the market, with offer, banner, and brand advertisements generating 30-40% of revenues going forward and microtransactions accounting for the rest.” Paul Chen, PapayaMobile

ABOUT PAPAYAMOBILE:PapayaMobile is an open, mobile social network for Android focused on casual gaming and virtual currency. Papaya offers developers a fast and easy way to reach more than three million users worldwide and make more money instantly. Android users love Papaya because they can play multiple games and get a complete social networking experience all in one, easy to use app. Founded in 2008 by Si Shen and Wenjie Qian, Papaya is headquartered in Beijing and has an office in Menlo Park, Calif. For more information, please visit: http://www.papayamobile.com/.

Page 5

DEVELOPERS ASINNOVATORS

MOBILE WORLD CONGRESS