Embed Size (px)

Citation preview

1 Mobility 2030 and beyond_SHOWN.pptx

1

Campinas, October 4th, 2013

E-mobility 2030 Megatrends, technologies and implications for CPFL

Dr. Wolfgang Bernhart, Senior Partner

A Energia na Cidade do Futuro

2 Mobility 2030 and beyond_SHOWN.pptx

2

Contents

A Urban Mobility 2030

B New powertrain technologies

C Battery and fuel cell economics

D New business models in infrastructure provision and connectivity services

3 Mobility 2030 and beyond_SHOWN.pptx

A. Urban Mobility 2030

4 Mobility 2030 and beyond_SHOWN.pptx

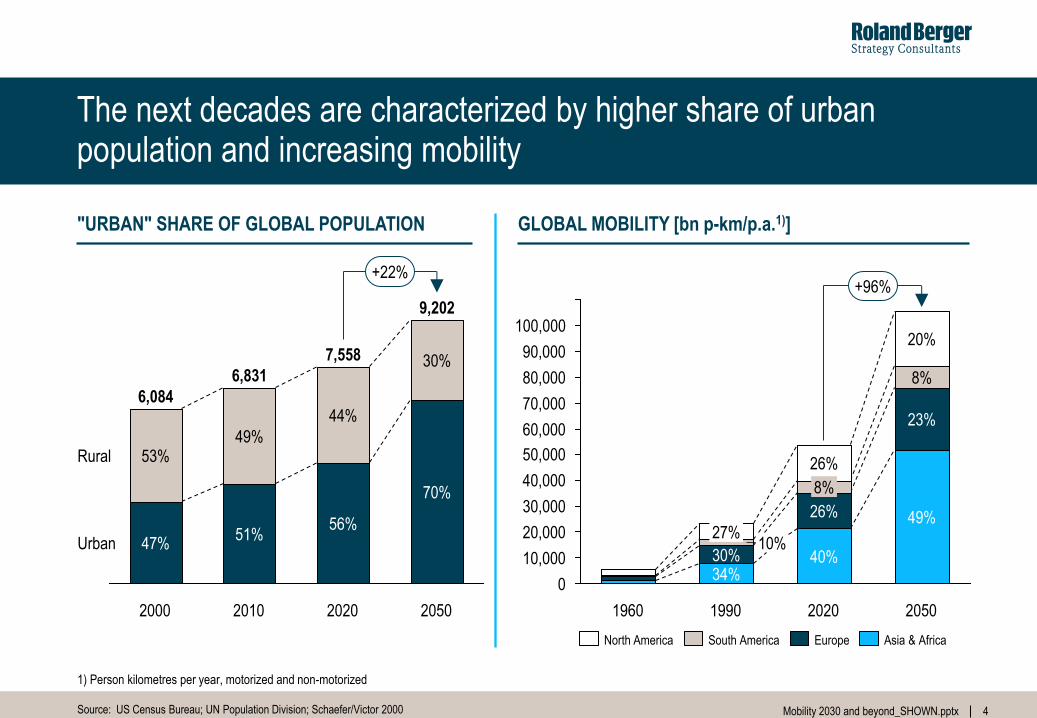

The next decades are characterized by higher share of urban population and increasing mobility

4

1) Person kilometres per year, motorized and non-motorized

Source: US Census Bureau; UN Population Division; Schaefer/Victor 2000

"URBAN" SHARE OF GLOBAL POPULATION GLOBAL MOBILITY [bn p-km/p.a.1)]

70%

30%

2020

7,558

56%

44%

2010

6,831

51%

49%

2000

6,084

+22%

Urban

Rural

2050

9,202

47%

53%

100,000

90,000

80,000

70,000

60,000

50,000

30,000 26%

40% 34%

2020

8%

23%

49%

2050

+96%

40,000

0

30% 10,000

20,000

1990

10% 27%

20%

26%

8%

1960

Asia & Africa Europe South America North America

5 Mobility 2030 and beyond_SHOWN.pptx

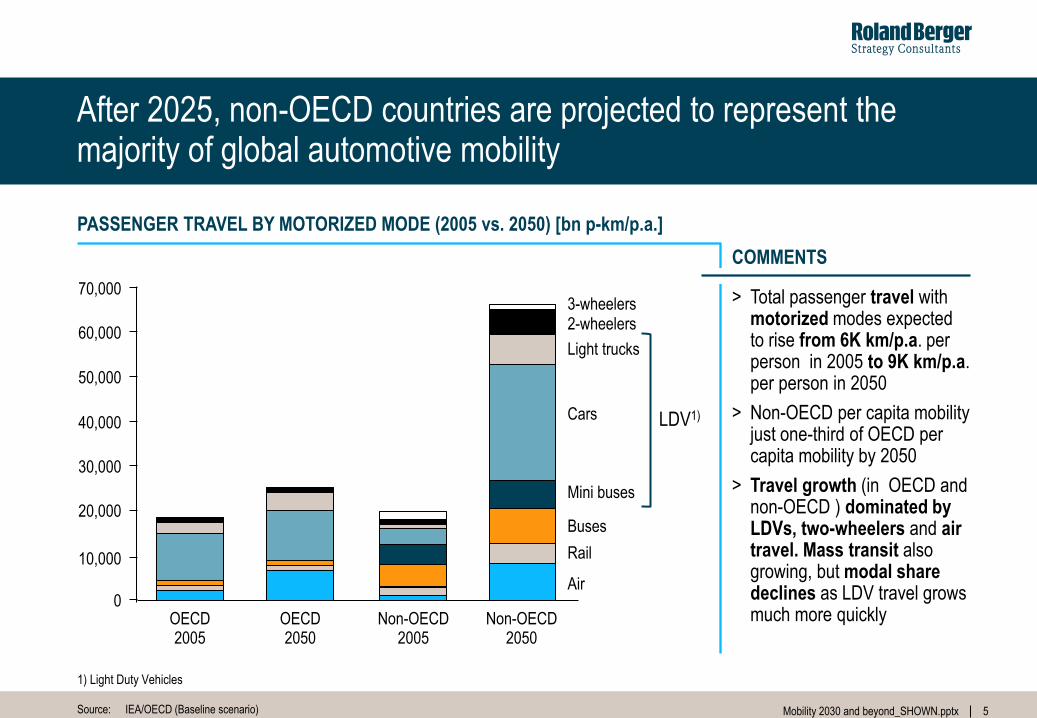

After 2025, non-OECD countries are projected to represent the majority of global automotive mobility

Source: IEA/OECD (Baseline scenario)

> Total passenger travel with motorized modes expected to rise from 6K km/p.a. per person in 2005 to 9K km/p.a. per person in 2050

> Non-OECD per capita mobility just one-third of OECD per capita mobility by 2050

> Travel growth (in OECD and non-OECD ) dominated by LDVs, two-wheelers and air travel. Mass transit also growing, but modal share declines as LDV travel grows much more quickly

COMMENTS

PASSENGER TRAVEL BY MOTORIZED MODE (2005 vs. 2050) [bn p-km/p.a.]

3-wheelers 2-wheelers

Light trucks

Cars

Mini buses

Buses

Rail

Air 0

10,000

20,000

30,000

50,000

60,000

40,000

70,000

OECD 2005

OECD 2050

Non-OECD 2005

Non-OECD 2050

LDV1)

1) Light Duty Vehicles

6 Mobility 2030 and beyond_SHOWN.pptx

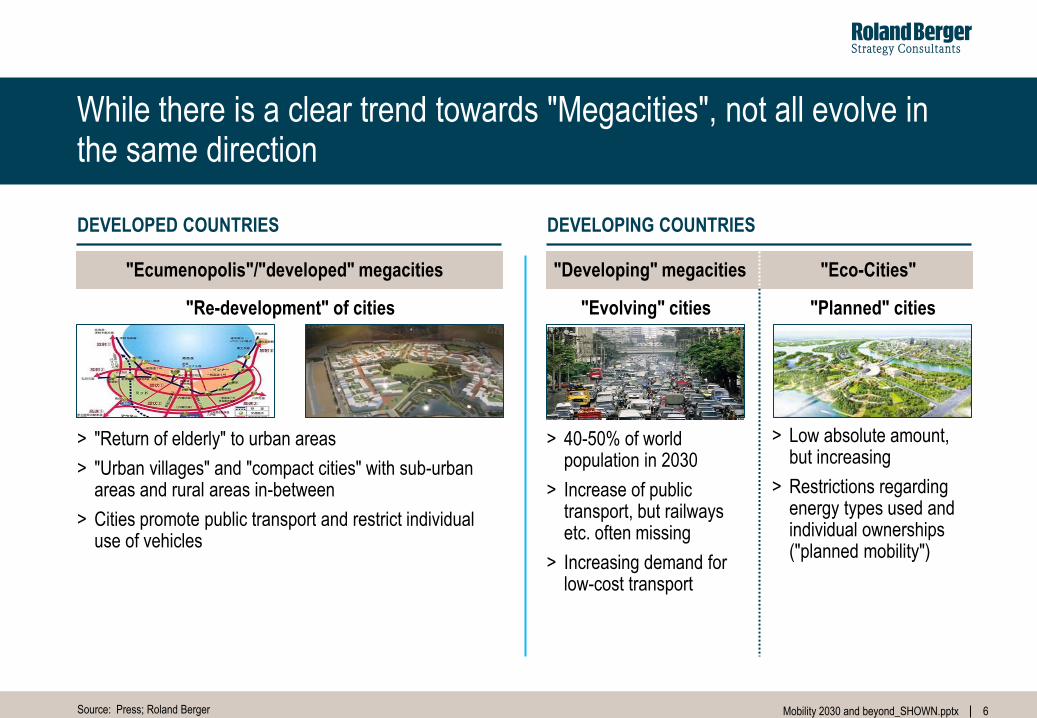

While there is a clear trend towards "Megacities", not all evolve in the same direction

6

Source: Press; Roland Berger

DEVELOPED COUNTRIES DEVELOPING COUNTRIES

"Ecumenopolis"/"developed" megacities "Developing" megacities "Eco-Cities"

"Re-development" of cities

> "Return of elderly" to urban areas

> "Urban villages" and "compact cities" with sub-urban areas and rural areas in-between

> Cities promote public transport and restrict individual use of vehicles

"Evolving" cities "Planned" cities

> 40-50% of world population in 2030

> Increase of public transport, but railways etc. often missing

> Increasing demand for low-cost transport

> Low absolute amount, but increasing

> Restrictions regarding energy types used and individual ownerships ("planned mobility")

7 Mobility 2030 and beyond_SHOWN.pptx

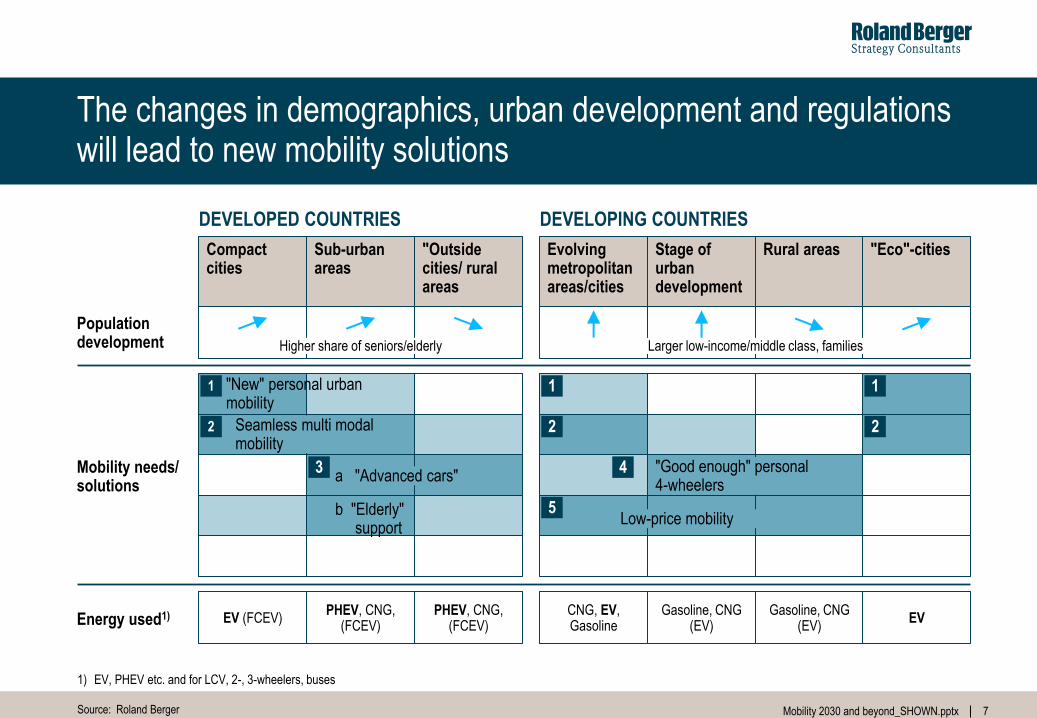

The changes in demographics, urban development and regulations will lead to new mobility solutions

7

Source: Roland Berger

DEVELOPED COUNTRIES DEVELOPING COUNTRIES

Compact cities

Sub-urban areas

"Outside cities/ rural areas

Evolving metropolitan areas/cities

Stage of urban development

Rural areas "Eco"-cities

EV (FCEV) PHEV, CNG,

(FCEV) PHEV, CNG,

(FCEV) CNG, EV, Gasoline

Gasoline, CNG (EV)

Gasoline, CNG (EV)

EV

Population development

Mobility needs/ solutions

Energy used1)

1) EV, PHEV etc. and for LCV, 2-, 3-wheelers, buses

Higher share of seniors/elderly Larger low-income/middle class, families

1

2

3

1

2

5

4

1

2

"New" personal urban mobility

Seamless multi modal mobility

a "Advanced cars"

b "Elderly" support

Low-price mobility

"Good enough" personal 4-wheelers

8 Mobility 2030 and beyond_SHOWN.pptx

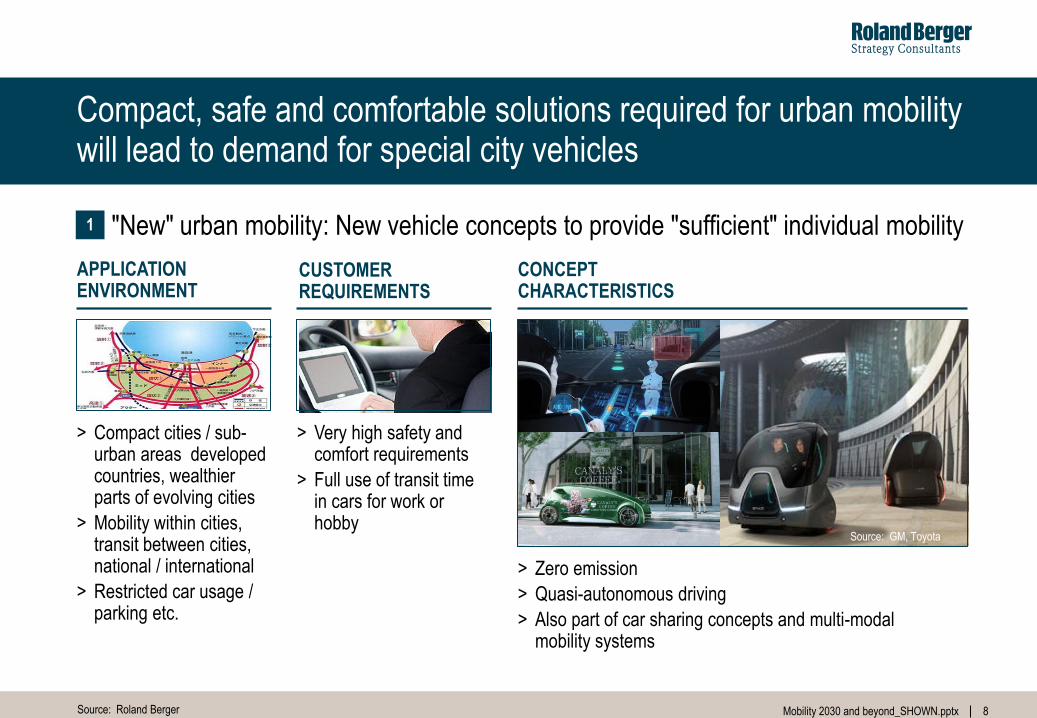

Compact, safe and comfortable solutions required for urban mobility will lead to demand for special city vehicles

8

Source: Roland Berger

"New" urban mobility: New vehicle concepts to provide "sufficient" individual mobility

> Compact cities / sub-urban areas developed countries, wealthier parts of evolving cities

> Mobility within cities, transit between cities, national / international

> Restricted car usage / parking etc.

APPLICATION ENVIRONMENT

CUSTOMER REQUIREMENTS

> Very high safety and comfort requirements

> Full use of transit time in cars for work or hobby

> Zero emission

> Quasi-autonomous driving

> Also part of car sharing concepts and multi-modal mobility systems

CONCEPT CHARACTERISTICS

1

Source: GM, Toyota

9 Mobility 2030 and beyond_SHOWN.pptx

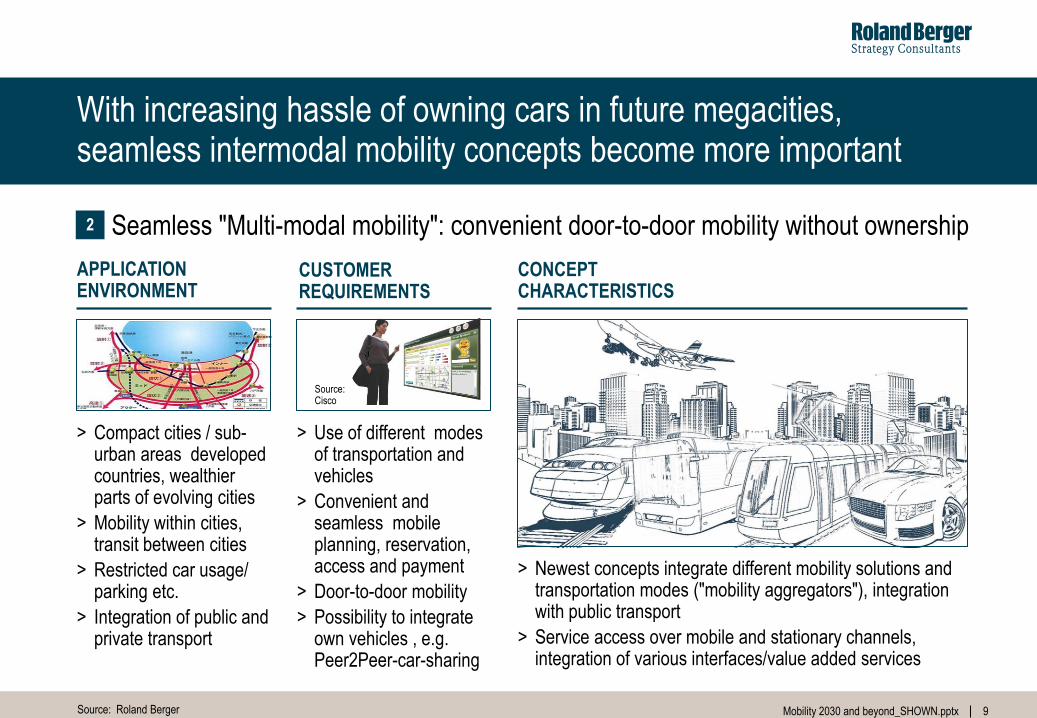

Source: Cisco

With increasing hassle of owning cars in future megacities, seamless intermodal mobility concepts become more important

9

Source: Roland Berger

Seamless "Multi-modal mobility": convenient door-to-door mobility without ownership

> Compact cities / sub-urban areas developed countries, wealthier parts of evolving cities

> Mobility within cities, transit between cities

> Restricted car usage/ parking etc.

> Integration of public and private transport

> Use of different modes of transportation and vehicles

> Convenient and seamless mobile planning, reservation, access and payment

> Door-to-door mobility

> Possibility to integrate own vehicles , e.g. Peer2Peer-car-sharing

> Newest concepts integrate different mobility solutions and transportation modes ("mobility aggregators"), integration with public transport

> Service access over mobile and stationary channels, integration of various interfaces/value added services

2

APPLICATION ENVIRONMENT

CUSTOMER REQUIREMENTS

CONCEPT CHARACTERISTICS

10 Mobility 2030 and beyond_SHOWN.pptx

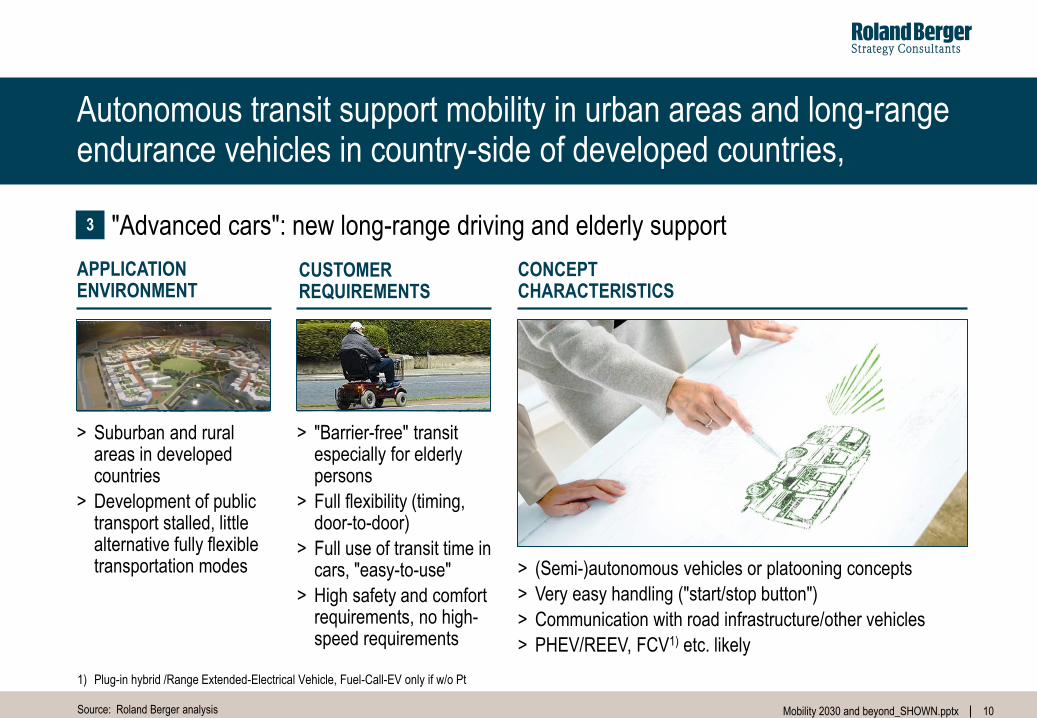

Autonomous transit support mobility in urban areas and long-range endurance vehicles in country-side of developed countries,

10

Source: Roland Berger analysis

"Advanced cars": new long-range driving and elderly support 3

> Suburban and rural areas in developed countries

> Development of public transport stalled, little alternative fully flexible transportation modes

> "Barrier-free" transit especially for elderly persons

> Full flexibility (timing, door-to-door)

> Full use of transit time in cars, "easy-to-use"

> High safety and comfort requirements, no high-speed requirements

> (Semi-)autonomous vehicles or platooning concepts

> Very easy handling ("start/stop button")

> Communication with road infrastructure/other vehicles

> PHEV/REEV, FCV1) etc. likely

APPLICATION ENVIRONMENT

CUSTOMER REQUIREMENTS

CONCEPT CHARACTERISTICS

1) Plug-in hybrid /Range Extended-Electrical Vehicle, Fuel-Call-EV only if w/o Pt

11 Mobility 2030 and beyond_SHOWN.pptx

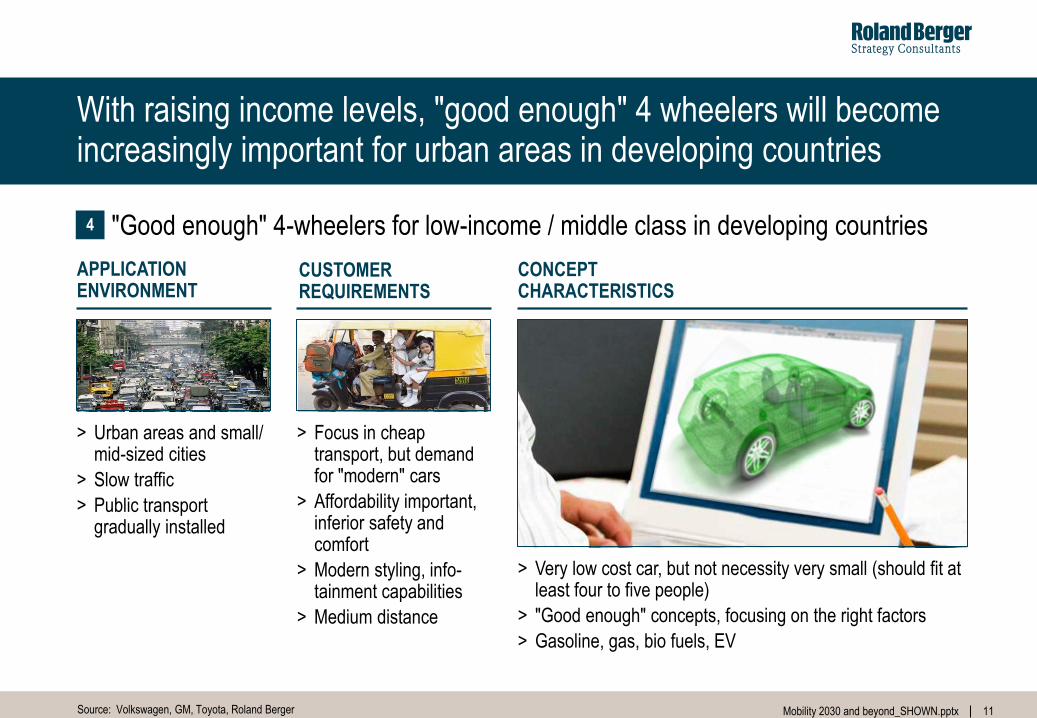

With raising income levels, "good enough" 4 wheelers will become increasingly important for urban areas in developing countries

11

Source: Volkswagen, GM, Toyota, Roland Berger

"Good enough" 4-wheelers for low-income / middle class in developing countries 4

> Urban areas and small/ mid-sized cities

> Slow traffic

> Public transport gradually installed

> Focus in cheap transport, but demand for "modern" cars

> Affordability important, inferior safety and comfort

> Modern styling, info-tainment capabilities

> Medium distance

> Very low cost car, but not necessity very small (should fit at least four to five people)

> "Good enough" concepts, focusing on the right factors

> Gasoline, gas, bio fuels, EV

APPLICATION ENVIRONMENT

CUSTOMER REQUIREMENTS

CONCEPT CHARACTERISTICS

12 Mobility 2030 and beyond_SHOWN.pptx

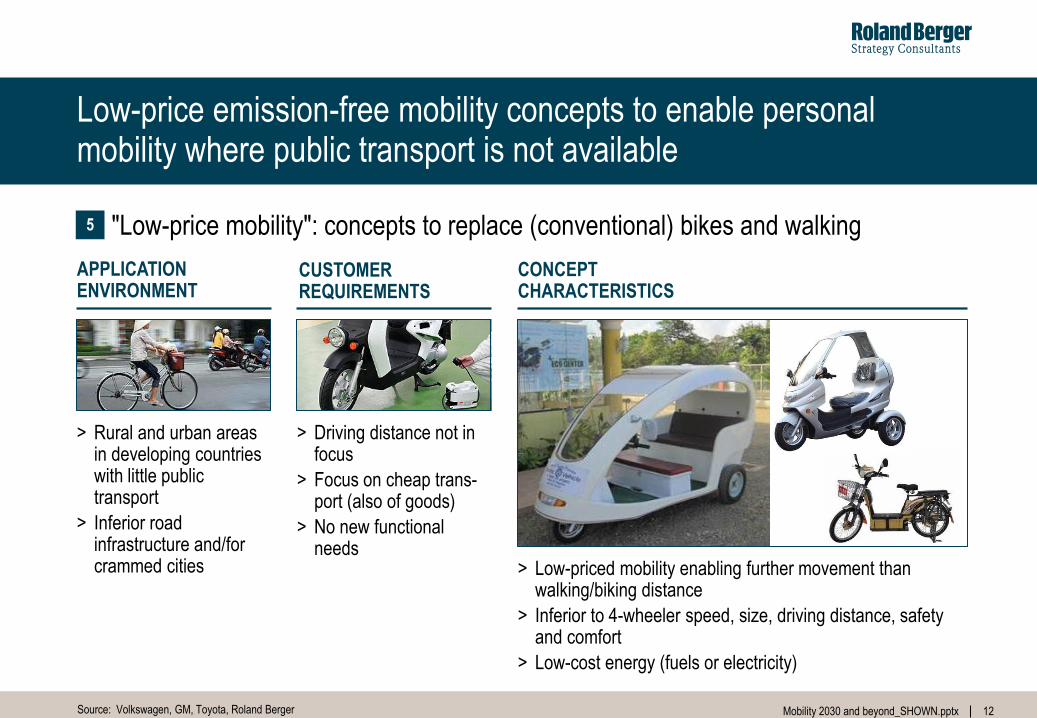

Low-price emission-free mobility concepts to enable personal mobility where public transport is not available

12

Source: Volkswagen, GM, Toyota, Roland Berger

"Low-price mobility": concepts to replace (conventional) bikes and walking 5

> Rural and urban areas in developing countries with little public transport

> Inferior road infrastructure and/for crammed cities

> Driving distance not in focus

> Focus on cheap trans-port (also of goods)

> No new functional needs

> Low-priced mobility enabling further movement than walking/biking distance

> Inferior to 4-wheeler speed, size, driving distance, safety and comfort

> Low-cost energy (fuels or electricity)

APPLICATION ENVIRONMENT

CUSTOMER REQUIREMENTS

CONCEPT CHARACTERISTICS

13 Mobility 2030 and beyond_SHOWN.pptx

B. New powertrain technologies

14 Mobility 2030 and beyond_SHOWN.pptx

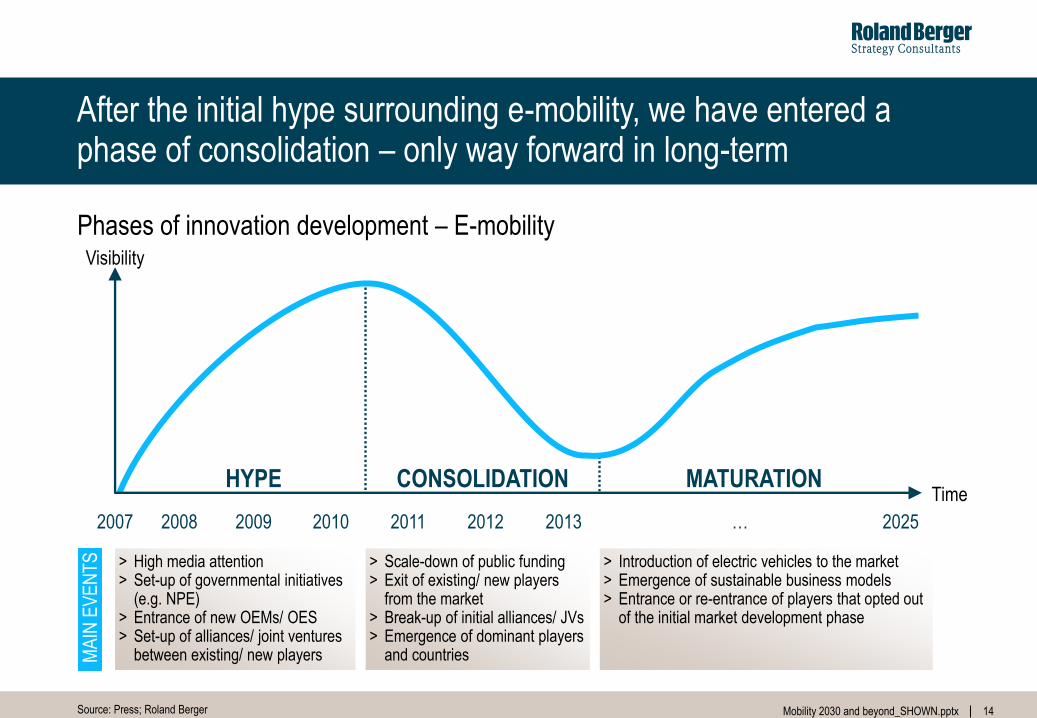

After the initial hype surrounding e-mobility, we have entered a phase of consolidation – only way forward in long-term

14

Phases of innovation development – E-mobility

> High media attention > Set-up of governmental initiatives

(e.g. NPE) > Entrance of new OEMs/ OES > Set-up of alliances/ joint ventures

between existing/ new players

> Scale-down of public funding > Exit of existing/ new players

from the market > Break-up of initial alliances/ JVs > Emergence of dominant players

and countries

> Introduction of electric vehicles to the market > Emergence of sustainable business models > Entrance or re-entrance of players that opted out

of the initial market development phase

MA

IN E

VE

NT

S

Source: Press; Roland Berger

2007 2008 2009 2010 2011 2012 2013 … 2025

HYPE CONSOLIDATION MATURATION Time

Visibility

15 Mobility 2030 and beyond_SHOWN.pptx

15

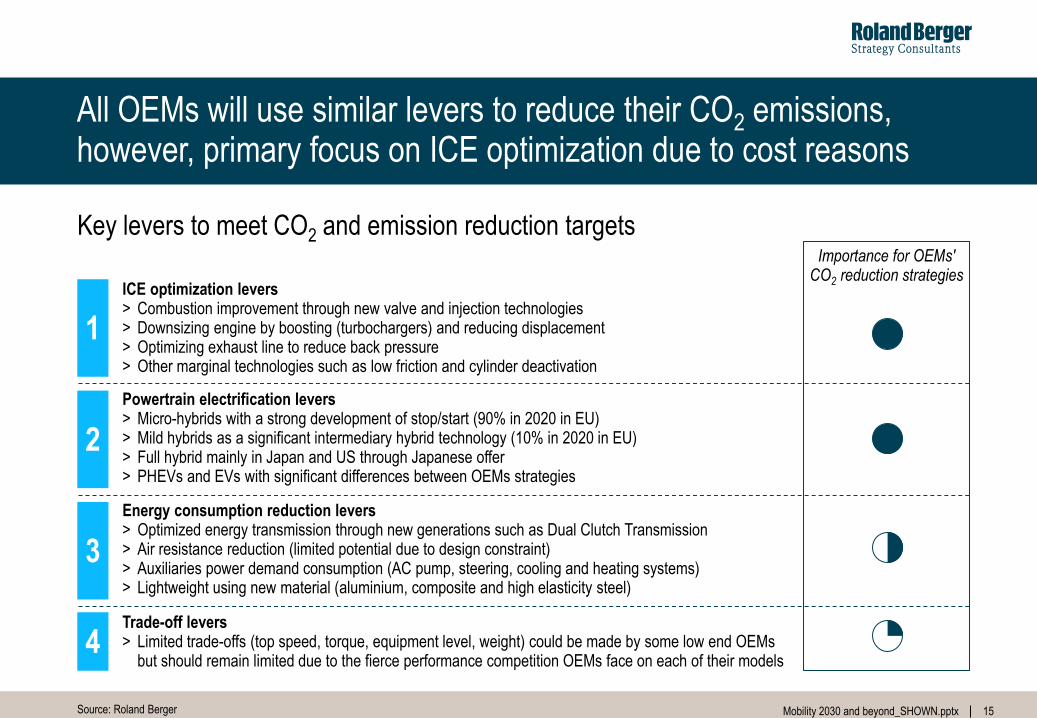

All OEMs will use similar levers to reduce their CO2 emissions, however, primary focus on ICE optimization due to cost reasons

1

2

3

4

Importance for OEMs' CO2 reduction strategies

Key levers to meet CO2 and emission reduction targets

Source: Roland Berger

ICE optimization levers > Combustion improvement through new valve and injection technologies > Downsizing engine by boosting (turbochargers) and reducing displacement > Optimizing exhaust line to reduce back pressure > Other marginal technologies such as low friction and cylinder deactivation

Powertrain electrification levers > Micro-hybrids with a strong development of stop/start (90% in 2020 in EU) > Mild hybrids as a significant intermediary hybrid technology (10% in 2020 in EU) > Full hybrid mainly in Japan and US through Japanese offer > PHEVs and EVs with significant differences between OEMs strategies

Energy consumption reduction levers > Optimized energy transmission through new generations such as Dual Clutch Transmission > Air resistance reduction (limited potential due to design constraint) > Auxiliaries power demand consumption (AC pump, steering, cooling and heating systems) > Lightweight using new material (aluminium, composite and high elasticity steel)

Trade-off levers > Limited trade-offs (top speed, torque, equipment level, weight) could be made by some low end OEMs

but should remain limited due to the fierce performance competition OEMs face on each of their models

16 Mobility 2030 and beyond_SHOWN.pptx

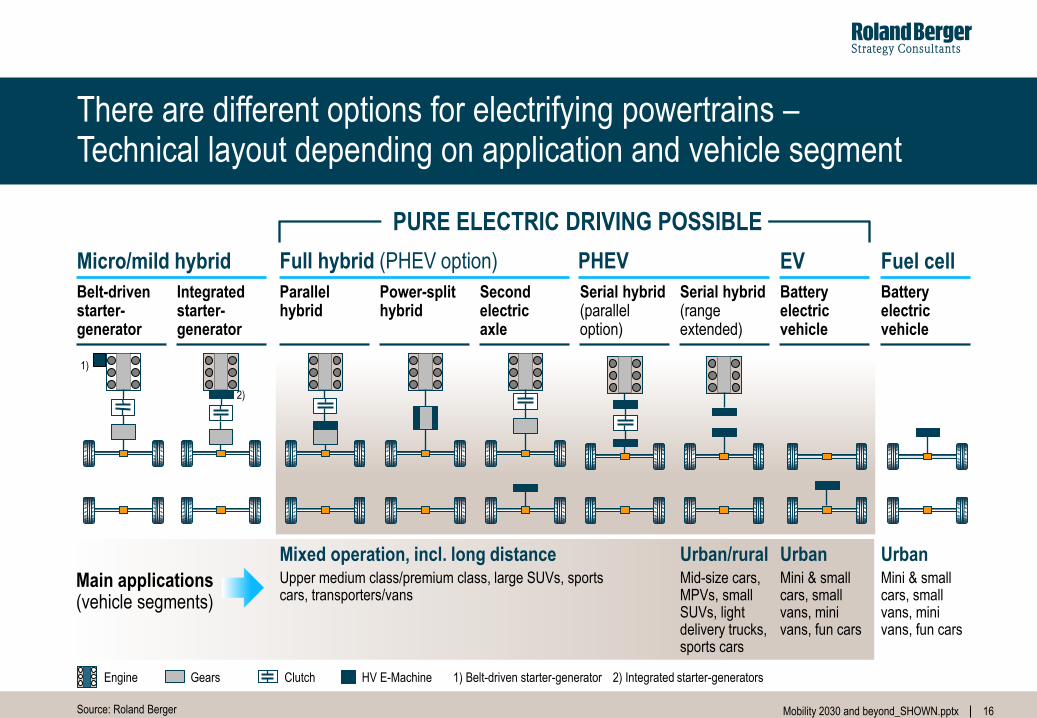

There are different options for electrifying powertrains – Technical layout depending on application and vehicle segment

Engine Gears Clutch HV E-Machine 1) Belt-driven starter-generator 2) Integrated starter-generators

Source: Roland Berger

Micro/mild hybrid

Belt-driven starter-generator

Integrated starter- generator

Full hybrid (PHEV option)

Second electric axle

Serial hybrid (range extended)

Parallel hybrid

Power-split hybrid

Battery electric vehicle

EV

Serial hybrid (parallel option)

PHEV

PURE ELECTRIC DRIVING POSSIBLE

Battery electric vehicle

Fuel cell

1)

2)

Mixed operation, incl. long distance Urban/rural Urban Mini & small cars, small vans, mini vans, fun cars

Mid-size cars, MPVs, small SUVs, light delivery trucks, sports cars

Upper medium class/premium class, large SUVs, sports cars, transporters/vans

Main applications (vehicle segments)

Urban Mini & small cars, small vans, mini vans, fun cars

17 Mobility 2030 and beyond_SHOWN.pptx

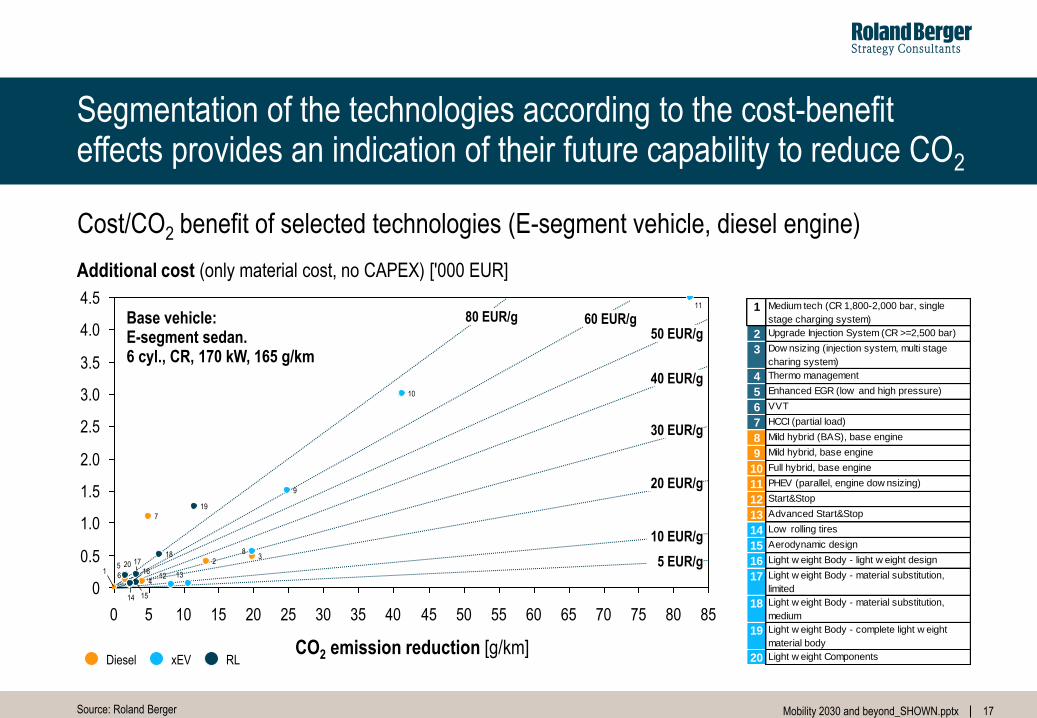

Segmentation of the technologies according to the cost-benefit effects provides an indication of their future capability to reduce CO2

Source: Roland Berger

Additional cost (only material cost, no CAPEX) ['000 EUR]

CO2 emission reduction [g/km]

Base vehicle: E-segment sedan. 6 cyl., CR, 170 kW, 165 g/km

RL xEV Diesel

40 EUR/g

30 EUR/g

20 EUR/g

10 EUR/g

5 EUR/g

50 EUR/g 80 EUR/g 60 EUR/g

60 0 40 75 70 65

3.5

55 50 45

4.5

4.0

3.0

2.5

2.0

1.5

1.0

0.5

0

85 80 35 30 25 20 15 10 5

19

18 17

16

15 14

13 12

20

10

9

8

7

6

11

4

3 2

1 5

1 Medium tech (CR 1,800-2,000 bar, single

stage charging system)

2 Upgrade Injection System (CR >=2,500 bar)

3 Dow nsizing (injection system, multi stage

charing system)

4 Thermo management

5 Enhanced EGR (low and high pressure)

6 VVT

7 HCCI (partial load)

8 Mild hybrid (BAS), base engine

9 Mild hybrid, base engine

10 Full hybrid, base engine

11 PHEV (parallel, engine dow nsizing)

12 Start&Stop

13 Advanced Start&Stop

14 Low rolling tires

15 Aerodynamic design

16 Light w eight Body - light w eight design

17 Light w eight Body - material substitution,

limited

18 Light w eight Body - material substitution,

medium

19 Light w eight Body - complete light w eight

material body

20 Light w eight Components

Cost/CO2 benefit of selected technologies (E-segment vehicle, diesel engine)

18 Mobility 2030 and beyond_SHOWN.pptx

18

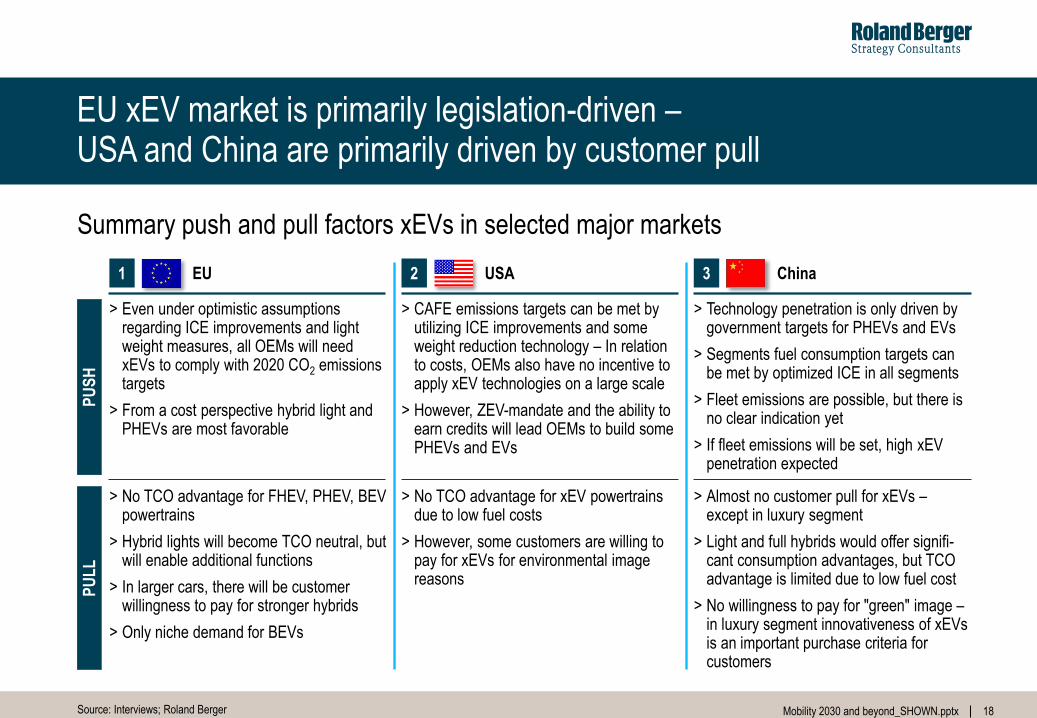

EU xEV market is primarily legislation-driven – USA and China are primarily driven by customer pull

EU 1 USA 2

PU

SH

> Even under optimistic assumptions regarding ICE improvements and light weight measures, all OEMs will need xEVs to comply with 2020 CO2 emissions targets

> From a cost perspective hybrid light and PHEVs are most favorable

> CAFE emissions targets can be met by utilizing ICE improvements and some weight reduction technology – In relation to costs, OEMs also have no incentive to apply xEV technologies on a large scale

> However, ZEV-mandate and the ability to earn credits will lead OEMs to build some PHEVs and EVs

> Technology penetration is only driven by government targets for PHEVs and EVs

> Segments fuel consumption targets can be met by optimized ICE in all segments

> Fleet emissions are possible, but there is no clear indication yet

> If fleet emissions will be set, high xEV penetration expected

China 3

PU

LL

> No TCO advantage for FHEV, PHEV, BEV powertrains

> Hybrid lights will become TCO neutral, but will enable additional functions

> In larger cars, there will be customer willingness to pay for stronger hybrids

> Only niche demand for BEVs

> No TCO advantage for xEV powertrains due to low fuel costs

> However, some customers are willing to pay for xEVs for environmental image reasons

> Almost no customer pull for xEVs – except in luxury segment

> Light and full hybrids would offer signifi-cant consumption advantages, but TCO advantage is limited due to low fuel cost

> No willingness to pay for "green" image – in luxury segment innovativeness of xEVs is an important purchase criteria for customers

Source: Interviews; Roland Berger

Summary push and pull factors xEVs in selected major markets

19 Mobility 2030 and beyond_SHOWN.pptx

Short

<40 km

Medium

40-120 km

Long

>120 km

19

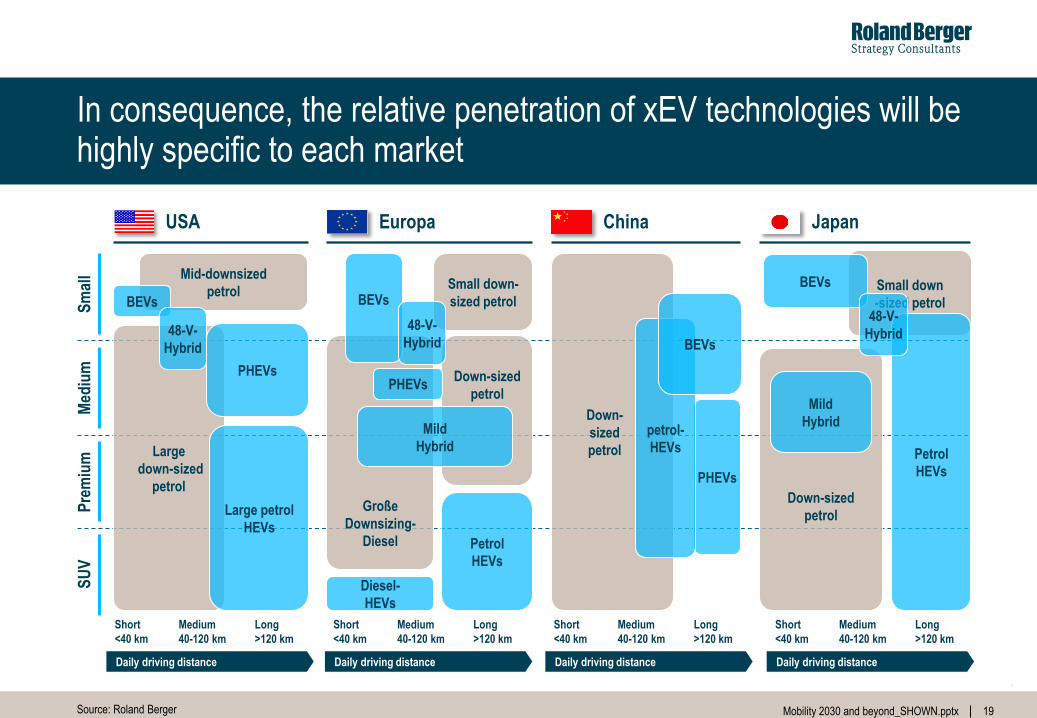

In consequence, the relative penetration of xEV technologies will be highly specific to each market

USA Japan China Europa

Down-

sized

petrol

Große

Downsizing-

Diesel

Small down-

sized petrol

Down-sized

petrol

Petrol

HEVs

Mild

Hybrid

Diesel-

HEVs

PHEVs

Pre

miu

m

Med

ium

S

UV

S

mal

l

Small down

-sized petrol

Petrol

HEVs

Large

down-sized

petrol

Large petrol

HEVs

PHEVs

Mid-downsized

petrol

Down-sized

petrol

BEVs

Mild

Hybrid

48-V-

Hybrid

Daily driving distance Daily driving distance Daily driving distance Daily driving distance

Short

<40 km

Medium

40-120 km

Long

>120 km

Source: Roland Berger

PHEVs

BEVs

48-V-

Hybrid

petrol-

HEVs

BEVs

BEVs

48-V-

Hybrid

Short

<40 km

Medium

40-120 km

Long

>120 km

Short

<40 km

Medium

40-120 km

Long

>120 km

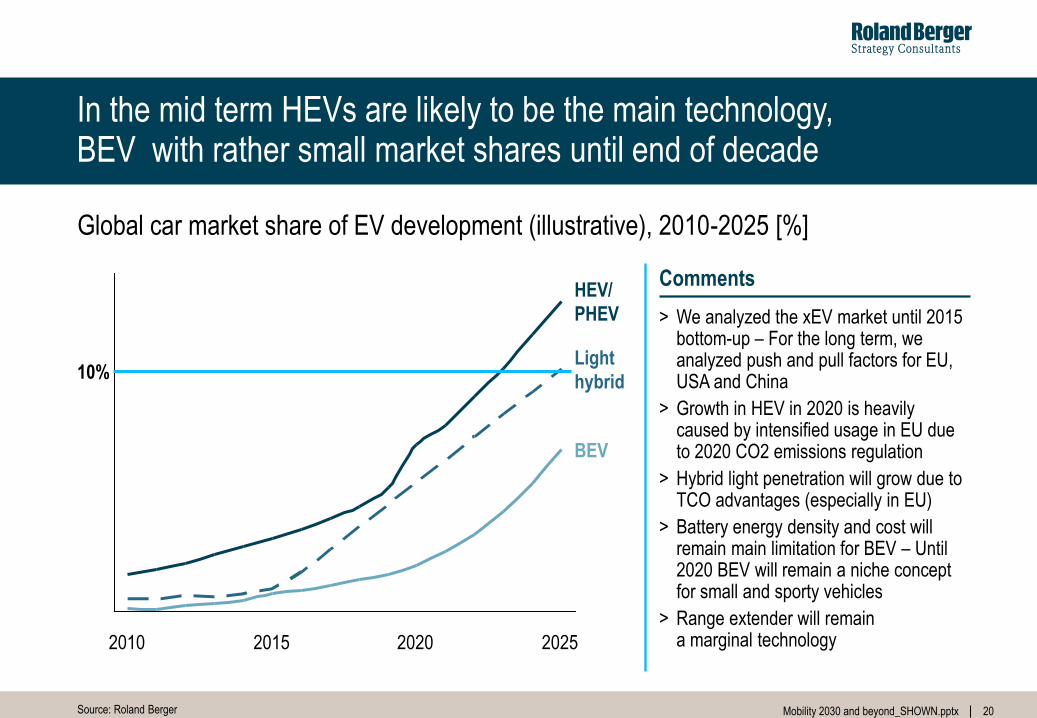

20 Mobility 2030 and beyond_SHOWN.pptx

Light

hybrid

BEV

HEV/

PHEV

2025 2020 2015 2010

Source: Roland Berger

Global car market share of EV development (illustrative), 2010-2025 [%]

In the mid term HEVs are likely to be the main technology, BEV with rather small market shares until end of decade

> We analyzed the xEV market until 2015 bottom-up – For the long term, we analyzed push and pull factors for EU, USA and China

> Growth in HEV in 2020 is heavily caused by intensified usage in EU due to 2020 CO2 emissions regulation

> Hybrid light penetration will grow due to TCO advantages (especially in EU)

> Battery energy density and cost will remain main limitation for BEV – Until 2020 BEV will remain a niche concept for small and sporty vehicles

> Range extender will remain a marginal technology

Comments

10%

21 Mobility 2030 and beyond_SHOWN.pptx

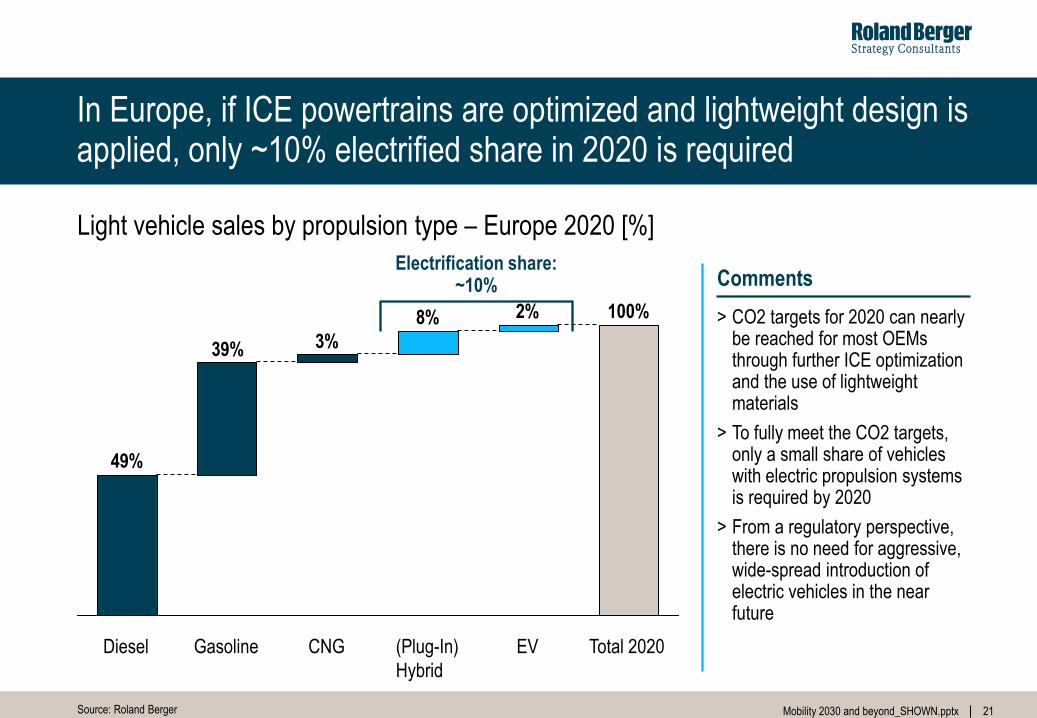

In Europe, if ICE powertrains are optimized and lightweight design is applied, only ~10% electrified share in 2020 is required

21

Light vehicle sales by propulsion type – Europe 2020 [%]

Source: Roland Berger

> CO2 targets for 2020 can nearly be reached for most OEMs through further ICE optimization and the use of lightweight materials

> To fully meet the CO2 targets, only a small share of vehicles with electric propulsion systems is required by 2020

> From a regulatory perspective, there is no need for aggressive, wide-spread introduction of electric vehicles in the near future

Comments

2%8%

3%39%

49%

Diesel CNG EV (Plug-In)

Hybrid

100%

Total 2020 Gasoline

Electrification share: ~10%

22 Mobility 2030 and beyond_SHOWN.pptx

C. Battery and fuel cell economics

23 Mobility 2030 and beyond_SHOWN.pptx

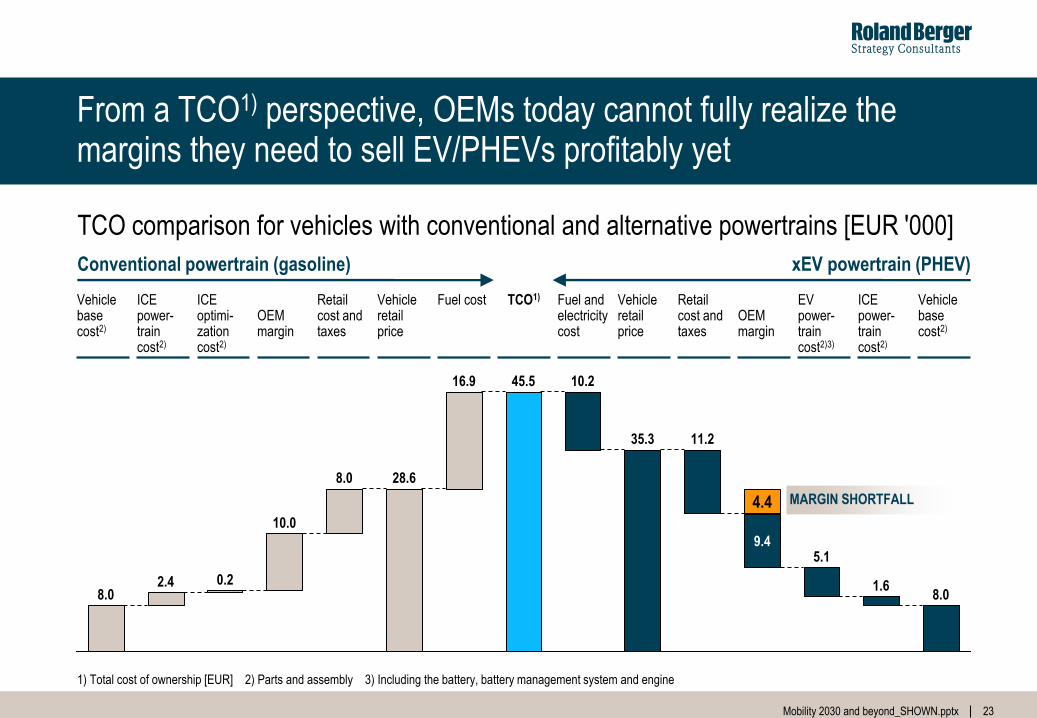

28.6 8.0

10.0

0.2 2.4 8.0

11.2 35.3

10.2 45.5 16.9

8.0 1.6

5.1

4.4

9.4

From a TCO1) perspective, OEMs today cannot fully realize the margins they need to sell EV/PHEVs profitably yet

23

TCO comparison for vehicles with conventional and alternative powertrains [EUR '000]

1) Total cost of ownership [EUR] 2) Parts and assembly 3) Including the battery, battery management system and engine

MARGIN SHORTFALL

Conventional powertrain (gasoline) xEV powertrain (PHEV)

Retail cost and taxes

Vehicle retail price

ICE power-train cost2)

OEM margin

ICE optimi-zation cost2)

TCO1) Fuel and electricity cost

Vehicle base cost2)

Retail cost and taxes

Vehicle retail price

Fuel cost OEM margin

EV power-train cost2)3)

ICE power-train cost2)

Vehicle base cost2)

24 Mobility 2030 and beyond_SHOWN.pptx

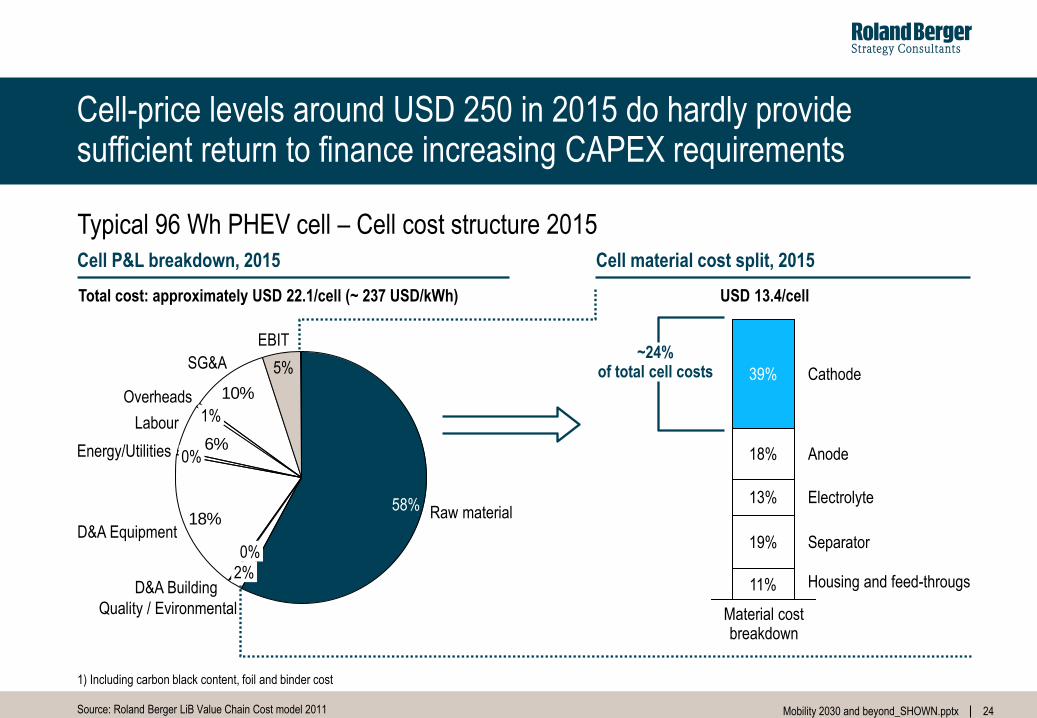

Cell-price levels around USD 250 in 2015 do hardly provide sufficient return to finance increasing CAPEX requirements

Source: Roland Berger LiB Value Chain Cost model 2011

Cell P&L breakdown, 2015 Cell material cost split, 2015

6%

10%

18%

EBIT

5% SG&A

Overheads 1% Labour

Energy/Utilities 0%

D&A Equipment

D&A Building

0%

Quality / Evironmental

2%

Raw material 58%

Total cost: approximately USD 22.1/cell (~ 237 USD/kWh)

18%

39%

Separator

Housing and feed-througs

Anode

Electrolyte

11%

Cathode

13%

19%

Material cost breakdown

USD 13.4/cell

~24% of total cell costs

1) Including carbon black content, foil and binder cost

Typical 96 Wh PHEV cell – Cell cost structure 2015

25 Mobility 2030 and beyond_SHOWN.pptx

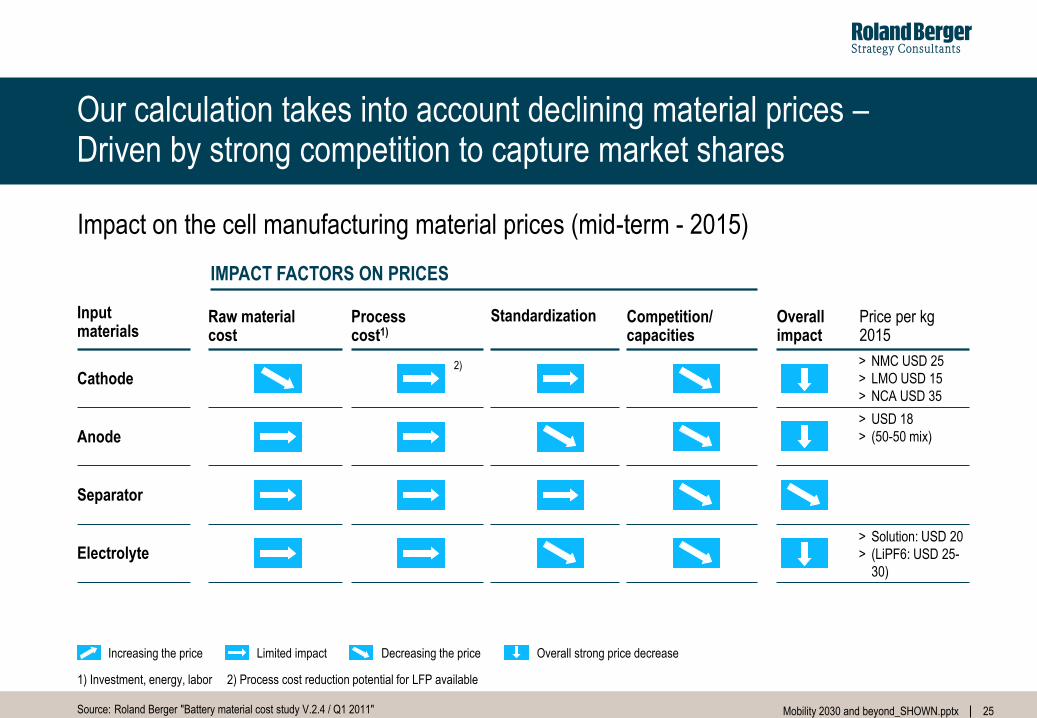

Our calculation takes into account declining material prices – Driven by strong competition to capture market shares

Increasing the price Limited impact Decreasing the price

Input materials

Raw material cost

Process cost1)

Standardization Competition/ capacities

IMPACT FACTORS ON PRICES

Separator

Anode

Electrolyte

Cathode 2)

Overall strong price decrease

Source: Roland Berger "Battery material cost study V.2.4 / Q1 2011"

Overall impact

> NMC USD 25

> LMO USD 15

> NCA USD 35

Price per kg 2015

> USD 18

> (50-50 mix)

> Solution: USD 20

> (LiPF6: USD 25-

30)

Impact on the cell manufacturing material prices (mid-term - 2015)

1) Investment, energy, labor 2) Process cost reduction potential for LFP available

26 Mobility 2030 and beyond_SHOWN.pptx

26

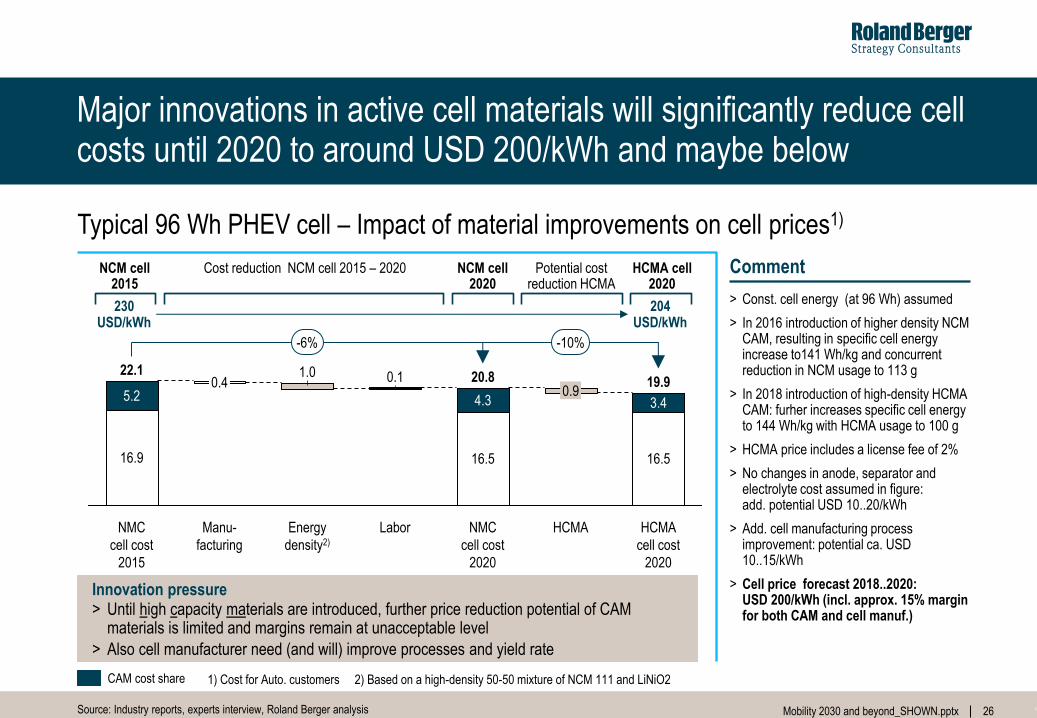

Major innovations in active cell materials will significantly reduce cell costs until 2020 to around USD 200/kWh and maybe below

26

> Const. cell energy (at 96 Wh) assumed

> In 2016 introduction of higher density NCM CAM, resulting in specific cell energy increase to141 Wh/kg and concurrent reduction in NCM usage to 113 g

> In 2018 introduction of high-density HCMA CAM: furher increases specific cell energy to 144 Wh/kg with HCMA usage to 100 g

> HCMA price includes a license fee of 2%

> No changes in anode, separator and electrolyte cost assumed in figure: add. potential USD 10..20/kWh

> Add. cell manufacturing process improvement: potential ca. USD 10..15/kWh

> Cell price forecast 2018..2020: USD 200/kWh (incl. approx. 15% margin for both CAM and cell manuf.)

CAM cost share

-10% -6%

HCMA

cell cost

2020

19.9

16.5

4.3

Labor

0.1

Energy

density2)

1.0

Manu-

facturing

0.4

NMC

cell cost

2015

22.1

16.9

5.2 3.4

HCMA

0.9

NMC

cell cost

2020

20.8

16.5

Cost reduction NCM cell 2015 – 2020 NCM cell 2015

NCM cell 2020

HCMA cell 2020

Potential cost reduction HCMA

230 USD/kWh

204 USD/kWh

Comment

Source: Roland Berger LiB Value Chain Cost model 2011

Source: Industry reports, experts interview, Roland Berger analysis

> Until high capacity materials are introduced, further price reduction potential of CAM materials is limited and margins remain at unacceptable level

> Also cell manufacturer need (and will) improve processes and yield rate

Innovation pressure

1) Cost for Auto. customers 2) Based on a high-density 50-50 mixture of NCM 111 and LiNiO2

Typical 96 Wh PHEV cell – Impact of material improvements on cell prices1)

27 Mobility 2030 and beyond_SHOWN.pptx

27

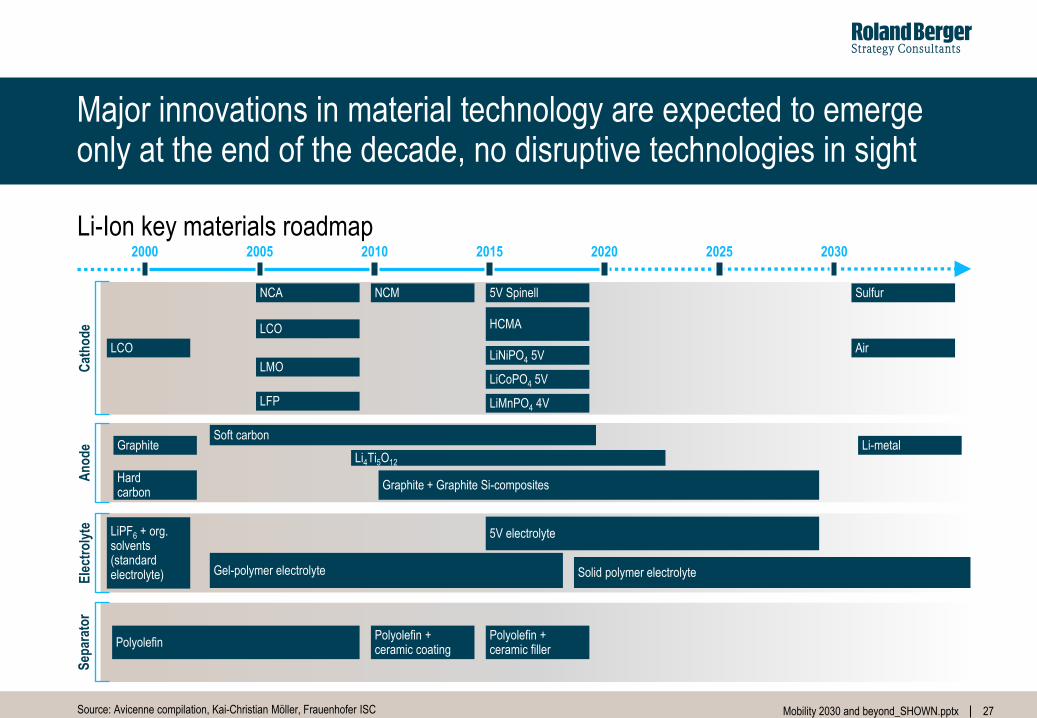

Major innovations in material technology are expected to emerge only at the end of the decade, no disruptive technologies in sight

2000 2015 2010 2005

Cat

ho

de

2020 2030 2025

An

od

e E

lect

roly

te

Sep

arat

or

Li-Ion key materials roadmap

Source: Avicenne compilation, Kai-Christian Möller, Frauenhofer ISC

LCO

LiPF6 + org. solvents (standard electrolyte)

Polyolefin

LCO

LMO

LFP

Air

NCA NCM 5V Spinell

HCMA

LiNiPO4 5V

LiCoPO4 5V

LiMnPO4 4V

Sulfur

Graphite

Hard carbon

Soft carbon

Li4Ti5O12

Graphite + Graphite Si-composites

Li-metal

Gel-polymer electrolyte

5V electrolyte

Solid polymer electrolyte

Polyolefin + ceramic coating

Polyolefin + ceramic filler

28 Mobility 2030 and beyond_SHOWN.pptx

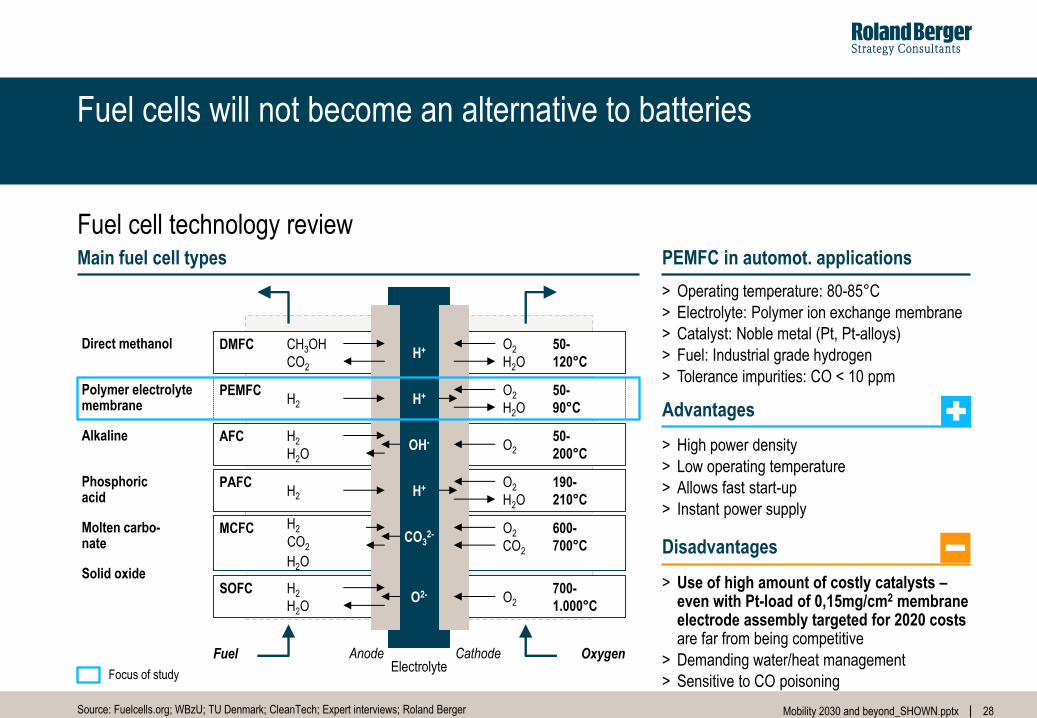

> Operating temperature: 80-85°C

> Electrolyte: Polymer ion exchange membrane

> Catalyst: Noble metal (Pt, Pt-alloys)

> Fuel: Industrial grade hydrogen

> Tolerance impurities: CO < 10 ppm

PEMFC in automot. applications

28

Fuel cells will not become an alternative to batteries

Source: Fuelcells.org; WBzU; TU Denmark; CleanTech; Expert interviews; Roland Berger

Main fuel cell types

Direct methanol

Polymer electrolyte membrane

Alkaline

Phosphoric acid

Molten carbo- nate

Solid oxide

Cathode Anode

DMFC CH3OH

CO2

50-

120°C

O2

H2O

PEMFC H2

50-

90°C

O2

H2O

AFC H2

H2O

50-

200°C O2

PAFC 190-

210°C

O2

H2O

MCFC H2

H2O

600-

700°C

O2

CO2

SOFC H2

H2O

700-

1.000°C O2

Electrolyte

H+

H+

OH-

H+

CO32-

O2-

H2

Fuel Oxygen

Advantages

> High power density

> Low operating temperature

> Allows fast start-up

> Instant power supply

> Use of high amount of costly catalysts – even with Pt-load of 0,15mg/cm2 membrane electrode assembly targeted for 2020 costs are far from being competitive

> Demanding water/heat management

> Sensitive to CO poisoning

Disadvantages

Focus of study

CO2

Fuel cell technology review

29 Mobility 2030 and beyond_SHOWN.pptx

29

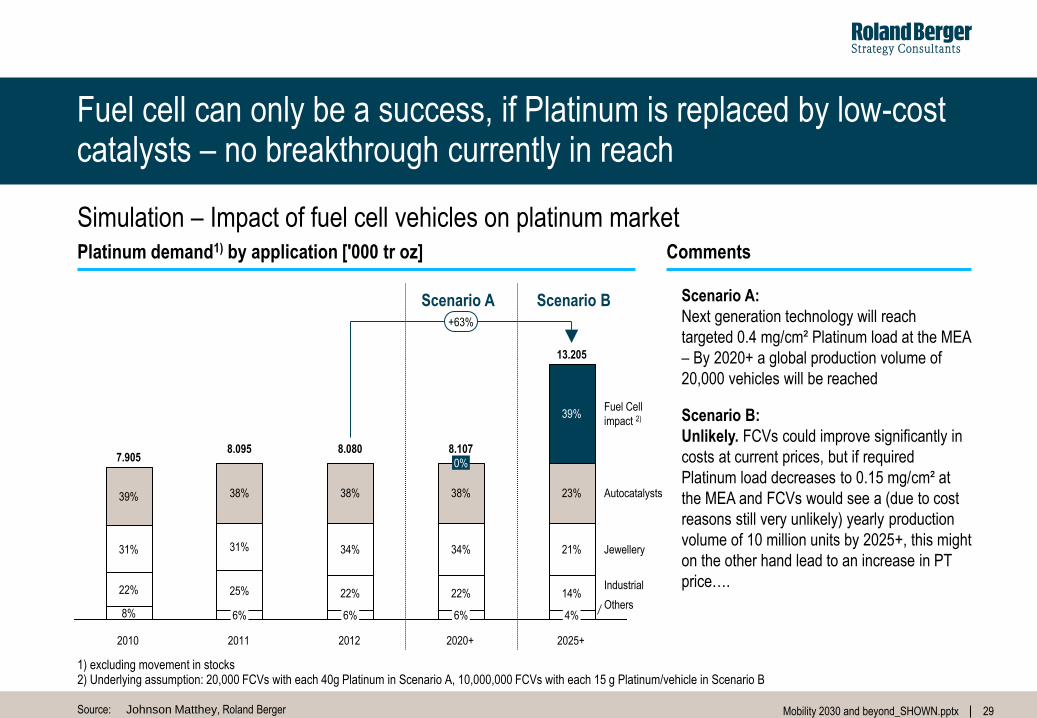

Fuel cell can only be a success, if Platinum is replaced by low-cost catalysts – no breakthrough currently in reach

Simulation – Impact of fuel cell vehicles on platinum market

Source: Johnson Matthey, Roland Berger

Platinum demand1) by application ['000 tr oz] Comments

Scenario A:

Next generation technology will reach

targeted 0.4 mg/cm² Platinum load at the MEA

– By 2020+ a global production volume of

20,000 vehicles will be reached

Scenario B:

Unlikely. FCVs could improve significantly in

costs at current prices, but if required

Platinum load decreases to 0.15 mg/cm² at

the MEA and FCVs would see a (due to cost

reasons still very unlikely) yearly production

volume of 10 million units by 2025+, this might

on the other hand lead to an increase in PT

price….

+63%

Others

Industrial

Jewellery

Autocatalysts

Fuel Cell

impact 2)

2025+

13.205

4%

14%

21%

23%

39%

2020+

8.107

6%

22%

34%

38%

0%

2012

8.080

6%

22%

34%

38%

2011

8.095

6%

25%

31%

38%

2010

7.905

8%

22%

31%

39%

Scenario A

1) excluding movement in stocks 2) Underlying assumption: 20,000 FCVs with each 40g Platinum in Scenario A, 10,000,000 FCVs with each 15 g Platinum/vehicle in Scenario B

Scenario B

30 Mobility 2030 and beyond_SHOWN.pptx

D. New business models in infrastructure provision and connectivity services

31 Mobility 2030 and beyond_SHOWN.pptx

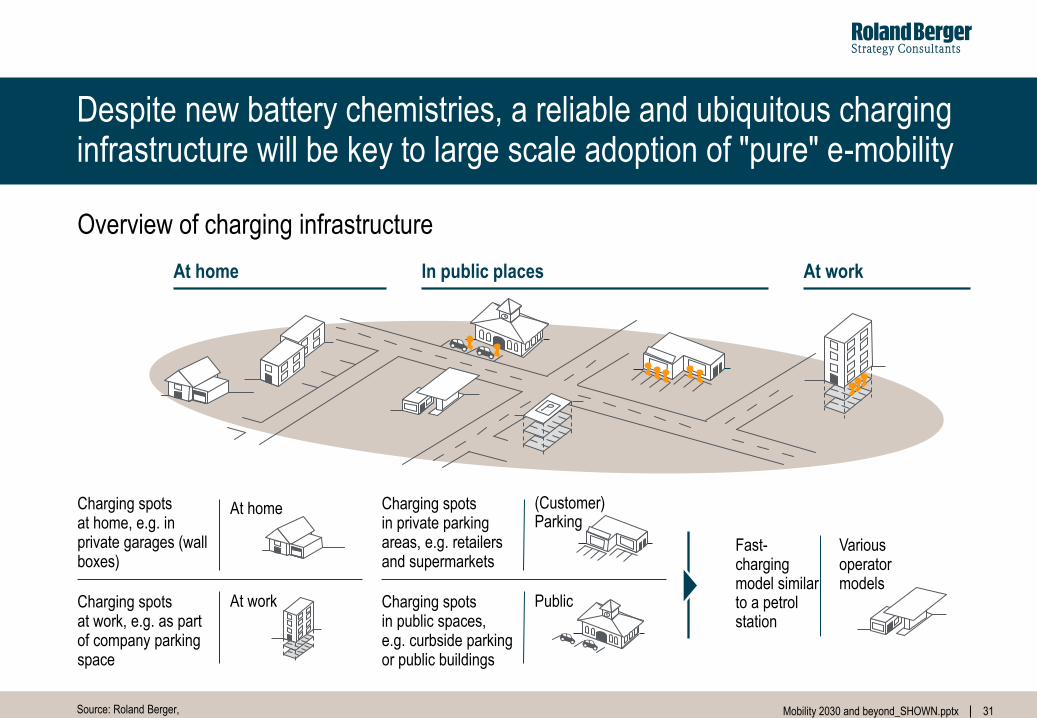

Despite new battery chemistries, a reliable and ubiquitous charging infrastructure will be key to large scale adoption of "pure" e-mobility

At home In public places At work

Charging spots at work, e.g. as part of company parking space

Charging spots at home, e.g. in private garages (wall boxes)

At home

At work Charging spots in public spaces, e.g. curbside parking or public buildings

Charging spots in private parking areas, e.g. retailers and supermarkets

(Customer) Parking

Public

Various operator models

Fast- charging model similar to a petrol station

Overview of charging infrastructure

Source: Roland Berger,

32 Mobility 2030 and beyond_SHOWN.pptx

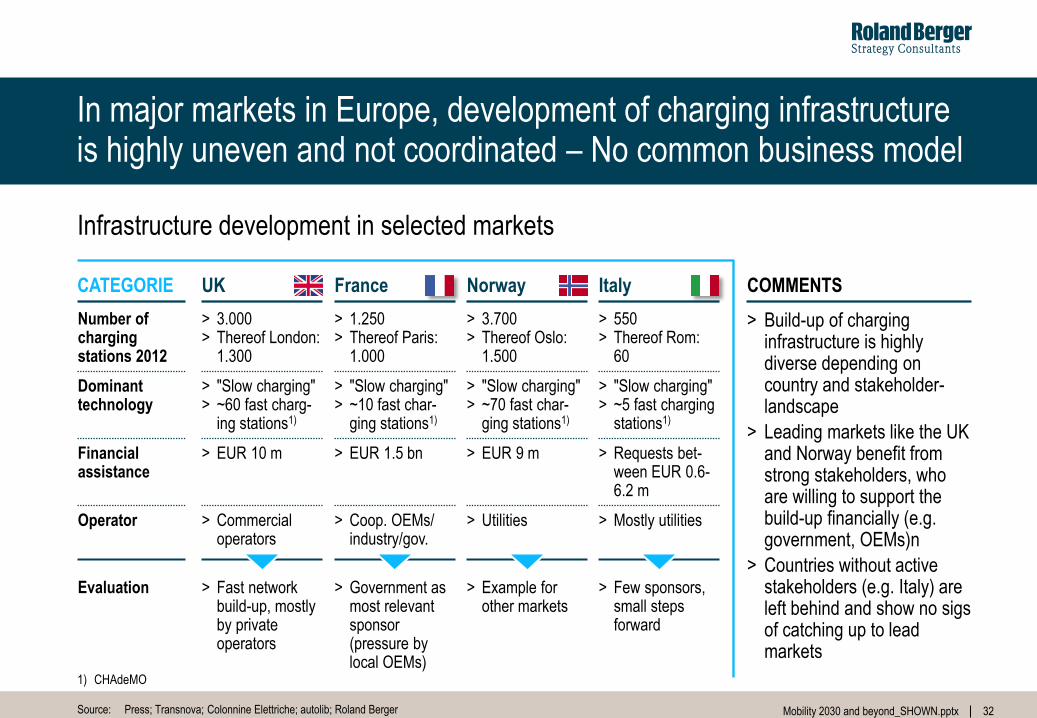

In major markets in Europe, development of charging infrastructure is highly uneven and not coordinated – No common business model

32

Source: Press; Transnova; Colonnine Elettriche; autolib; Roland Berger

> Build-up of charging infrastructure is highly diverse depending on country and stakeholder-landscape

> Leading markets like the UK and Norway benefit from strong stakeholders, who are willing to support the build-up financially (e.g. government, OEMs)n

> Countries without active stakeholders (e.g. Italy) are left behind and show no sigs of catching up to lead markets

COMMENTS CATEGORIE UK France Norway Italy

Number of charging stations 2012

> 3.000 > Thereof London:

1.300

> 1.250 > Thereof Paris:

1.000

> 3.700 > Thereof Oslo:

1.500

> 550 > Thereof Rom:

60

Dominant technology

> "Slow charging" > ~60 fast charg-

ing stations1)

> "Slow charging" > ~10 fast char-

ging stations1)

> "Slow charging" > ~70 fast char-

ging stations1)

> "Slow charging" > ~5 fast charging

stations1)

Financial assistance

> EUR 10 m > EUR 1.5 bn > EUR 9 m > Requests bet-ween EUR 0.6-6.2 m

Operator > Commercial operators

> Coop. OEMs/ industry/gov.

> Utilities > Mostly utilities

Evaluation > Fast network build-up, mostly by private operators

> Government as most relevant sponsor (pressure by local OEMs)

> Example for other markets

> Few sponsors, small steps forward

1) CHAdeMO

Infrastructure development in selected markets

33 Mobility 2030 and beyond_SHOWN.pptx

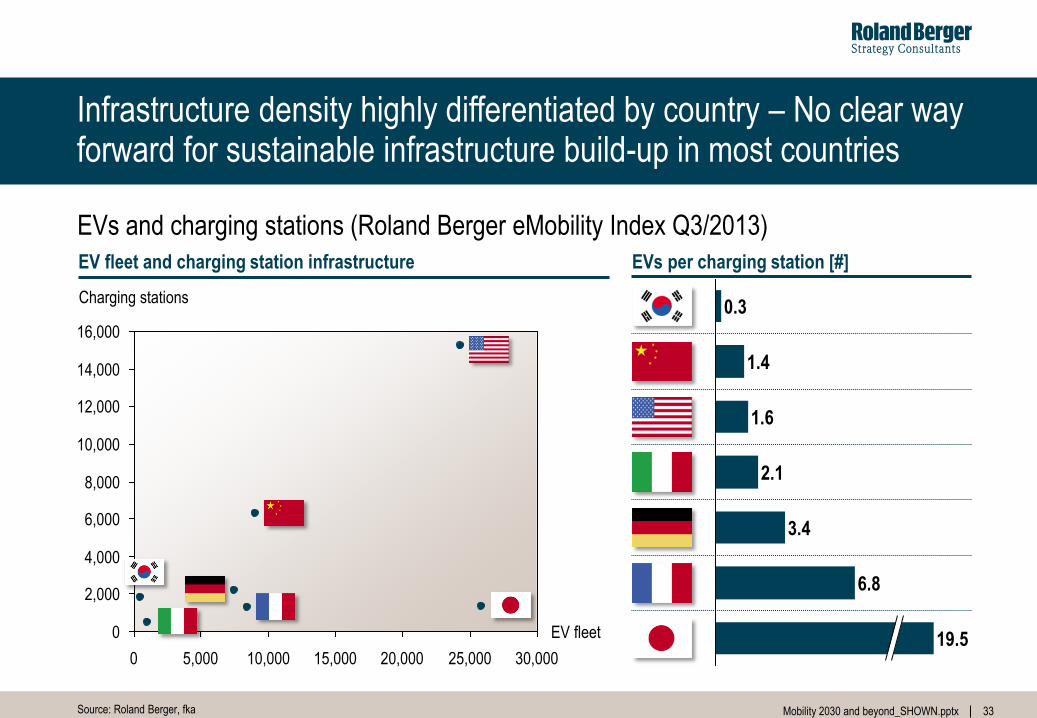

Infrastructure density highly differentiated by country – No clear way forward for sustainable infrastructure build-up in most countries

33

Source: Roland Berger, fka

EV fleet and charging station infrastructure

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

30,000 25,000 20,000 15,000 10,000 5,000 0

Charging stations

EV fleet

FR GER

CN

J

US

EVs per charging station [#]

19.5

6.8

3.4

2.1

1.6

1.4

0.3

EVs and charging stations (Roland Berger eMobility Index Q3/2013)

34 Mobility 2030 and beyond_SHOWN.pptx

34

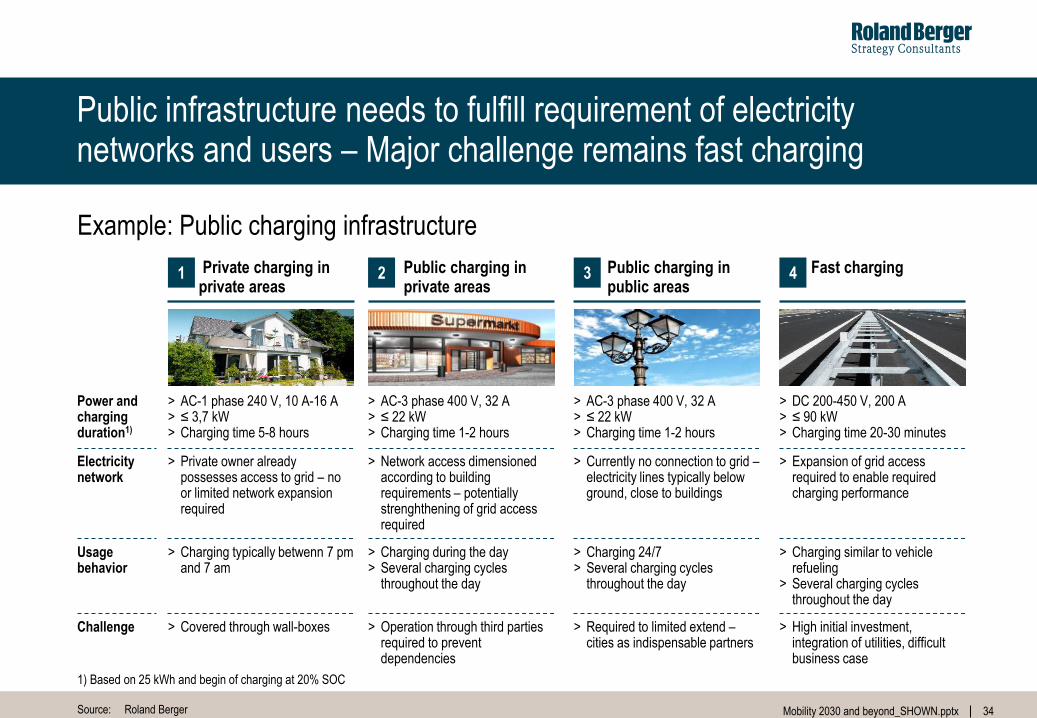

Public infrastructure needs to fulfill requirement of electricity networks and users – Major challenge remains fast charging

Private charging in private areas

1 Public charging in private areas

2 Fast charging 4 Public charging in public areas

3

> AC-1 phase 240 V, 10 A-16 A > ≤ 3,7 kW > Charging time 5-8 hours

> AC-3 phase 400 V, 32 A > ≤ 22 kW > Charging time 1-2 hours

> AC-3 phase 400 V, 32 A > ≤ 22 kW > Charging time 1-2 hours

> DC 200-450 V, 200 A > ≤ 90 kW > Charging time 20-30 minutes

Power and charging duration1)

> Charging typically betwenn 7 pm and 7 am

> Charging during the day > Several charging cycles

throughout the day

> Charging 24/7 > Several charging cycles

throughout the day

> Charging similar to vehicle refueling

> Several charging cycles throughout the day

Usage behavior

> Private owner already possesses access to grid – no or limited network expansion required

> Network access dimensioned according to building requirements – potentially strenghthening of grid access required

> Currently no connection to grid – electricity lines typically below ground, close to buildings

> Expansion of grid access required to enable required charging performance

Electricity network

1) Based on 25 kWh and begin of charging at 20% SOC

> Covered through wall-boxes > Operation through third parties required to prevent dependencies

> Required to limited extend – cities as indispensable partners

> High initial investment, integration of utilities, difficult business case

Challenge

Source: Roland Berger

Example: Public charging infrastructure

35 Mobility 2030 and beyond_SHOWN.pptx

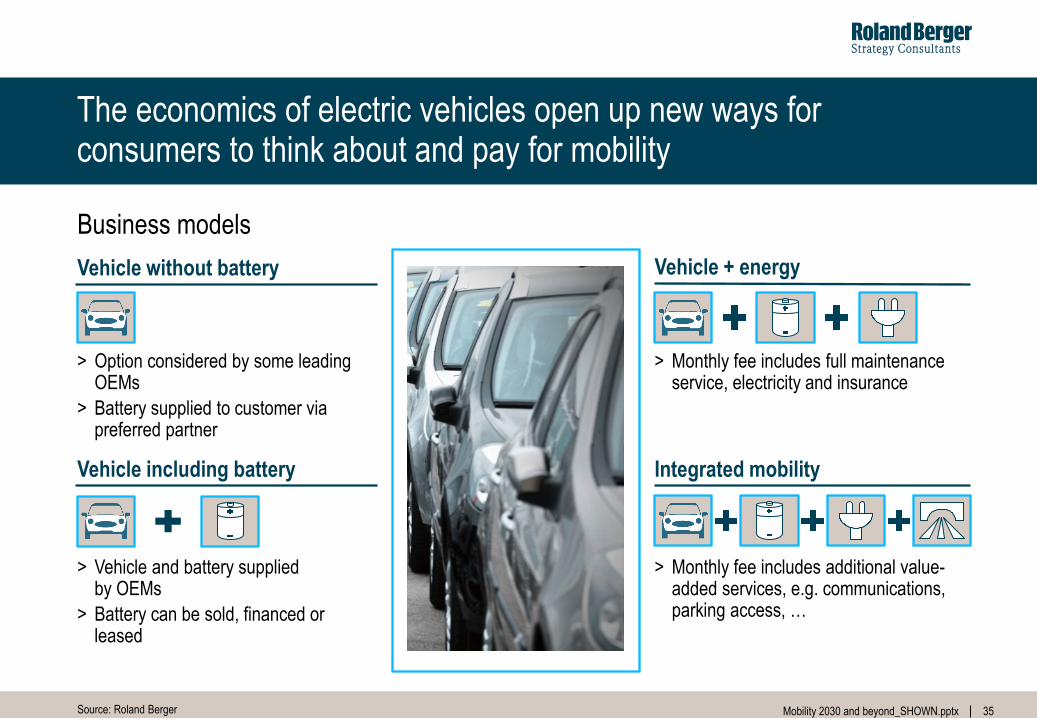

The economics of electric vehicles open up new ways for consumers to think about and pay for mobility

Vehicle + energy

> Monthly fee includes full maintenance service, electricity and insurance

Integrated mobility

> Monthly fee includes additional value-added services, e.g. communications, parking access, …

> Vehicle and battery supplied by OEMs

> Battery can be sold, financed or leased

> Option considered by some leading OEMs

> Battery supplied to customer via preferred partner

Vehicle including battery

Vehicle without battery

Business models

Source: Roland Berger

36 Mobility 2030 and beyond_SHOWN.pptx

36