Embed Size (px)

Citation preview

Monetary Policy Spillovers & Leaning Against the Wind

Karl Habermeier International Monetary Fund

Presentation at the Federal Reserve Bank of New York

2015 Central Banking Seminar

October 6, 2015

Agenda

Spillovers from Divergent Monetary Policies

Monetary Policy and Financial Stability

IMF staff papers

Spillover Report

July 2015

www.imf.org/external/np/pp/eng/2015/082815a.pdf

See also:

Carolina Buitron and Esteban Vesperoni, Spillover Implications of Differences in Monetary Conditions in the United States and the Euro Area, IMF, July 2015

Julian Chow, Florence Jaumotte, et al., Spillovers from Dollar Appreciation, IMF July 2015

Easy monetary policies in systemic advanced economies (U.S., U.K., euro area, Japan) are …

… good for them—they will raise output toward potential and inflation toward target.

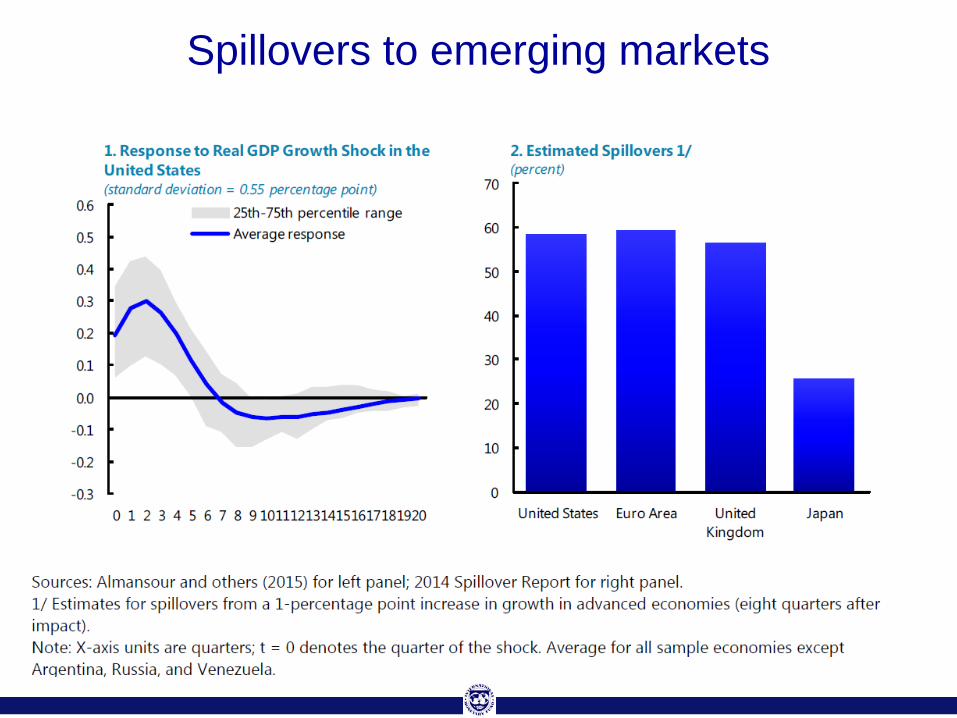

… good for other countries—an improvement in growth prospects in major advanced economies generates positive spillovers for emerging markets (and for other advanced economies), partly as their exports pick up. A recovery in major advanced economies also boosts confidence and capital flows increase.

Spillovers generally positive …

Spillovers to emerging markets

Volatility to be expected—Interest rate normalization in the U.S. can create volatility in markets. Clear communication with an eye to market expectations is a must.

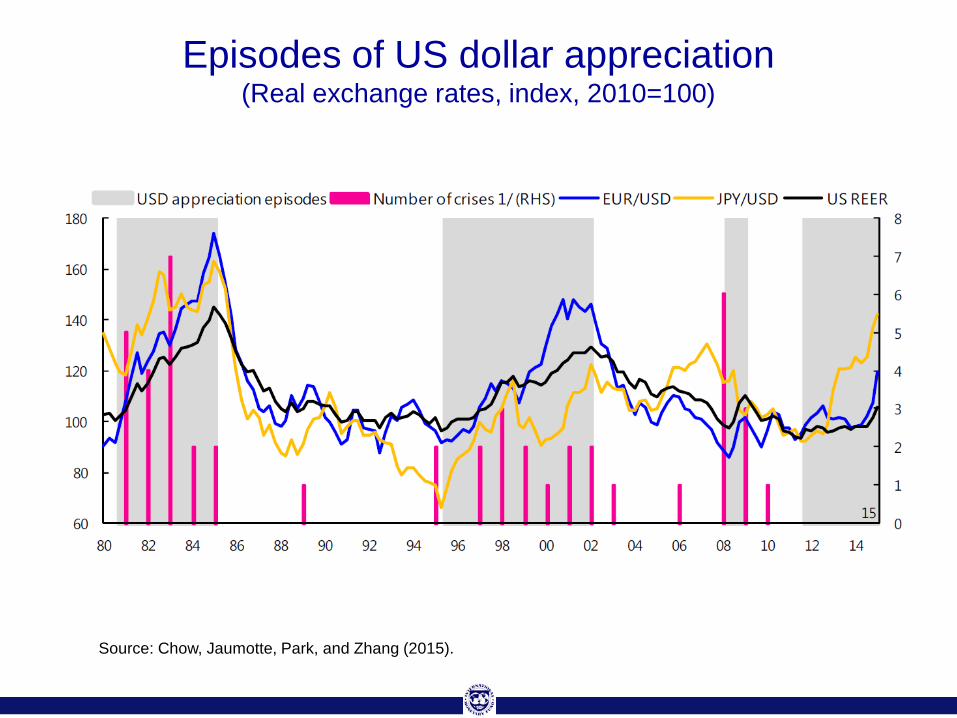

Spillovers from dollar appreciation • Source of past crises—In the past, episodes of U.S. dollar appreciation have

often been associated with crises in emerging markets. • Improved resilience—Emerging markets have over the past two decades

become less dependent than in the past on debt denominated in foreign currencies, have a larger FX reserves buffer of foreign exchange reserves, and many have moved to more flexible exchange rates.

• Corporate debt a concern—build-up of foreign-denominated corporate debt in emerging markets. Risks are moderate but bear watching.

… but also some risks

Episodes of US dollar appreciation (Real exchange rates, index, 2010=100)

Source: Chow, Jaumotte, Park, and Zhang (2015).

Corporate debt in percent of GDP

Three interrelated sources of risk • Weakness of commodities prices • China rebalancing • US monetary normalization / divergence

EME growth slowdown continues, partly structural

Market pressures and reversal of capital flows

Growing importance of negative spillovers from large EMEs to rest of world

Monetary and fiscal space is limited in an increasing number of countries

Monetary policy divergence only one risk to EMEs

Agenda

Spillovers from Divergent Monetary Policies

Monetary Policy and Financial Stability

IMF staff paper

Monetary Policy and Financial Stability

August 2015

www.imf.org/external/np/pp/eng/2015/082815a.pdf

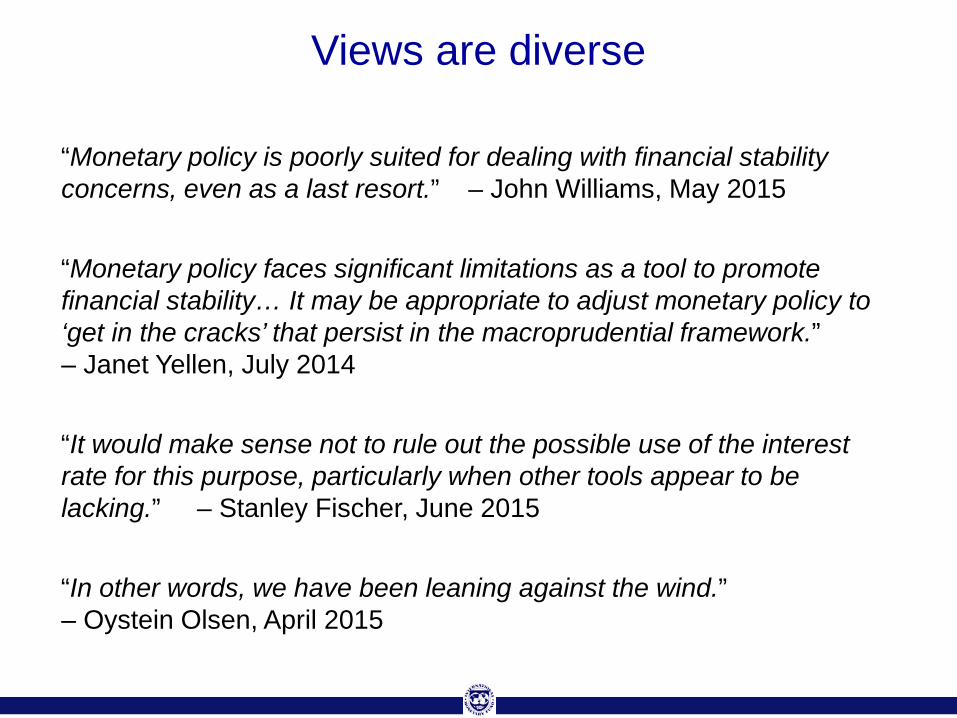

“Monetary policy is poorly suited for dealing with financial stability concerns, even as a last resort.” – John Williams, May 2015

“Monetary policy faces significant limitations as a tool to promote financial stability… It may be appropriate to adjust monetary policy to ‘get in the cracks’ that persist in the macroprudential framework.” – Janet Yellen, July 2014

“It would make sense not to rule out the possible use of the interest rate for this purpose, particularly when other tools appear to be lacking.” – Stanley Fischer, June 2015

“In other words, we have been leaning against the wind.” – Oystein Olsen, April 2015

Views are diverse

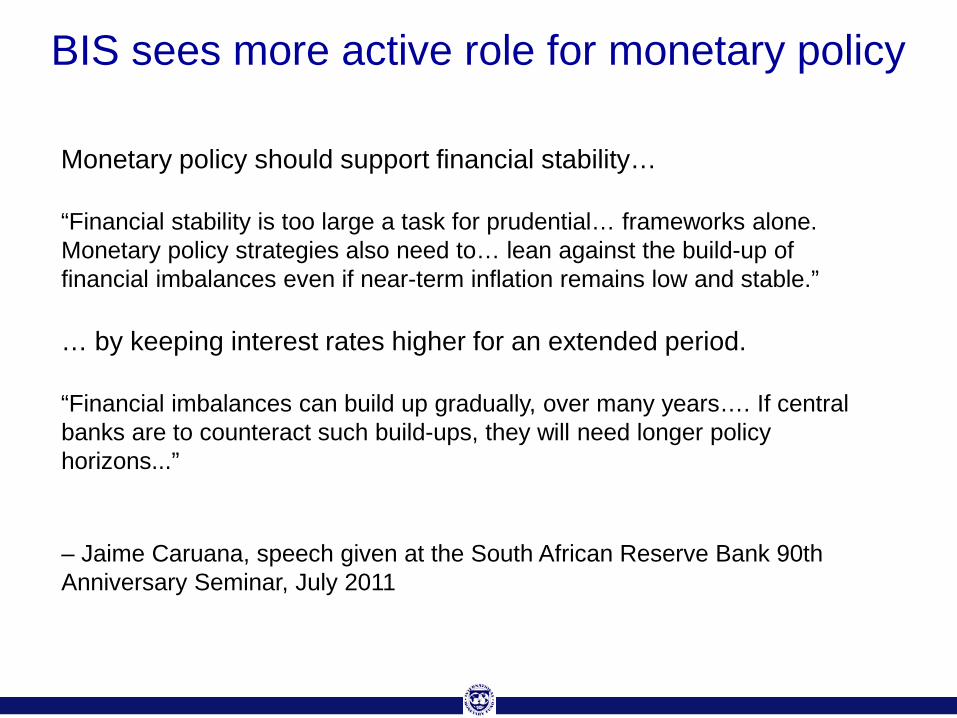

Monetary policy should support financial stability…

“Financial stability is too large a task for prudential… frameworks alone. Monetary policy strategies also need to… lean against the build-up of financial imbalances even if near-term inflation remains low and stable.”

… by keeping interest rates higher for an extended period.

“Financial imbalances can build up gradually, over many years…. If central banks are to counteract such build-ups, they will need longer policy horizons...”

– Jaime Caruana, speech given at the South African Reserve Bank 90th Anniversary Seminar, July 2011

BIS sees more active role for monetary policy

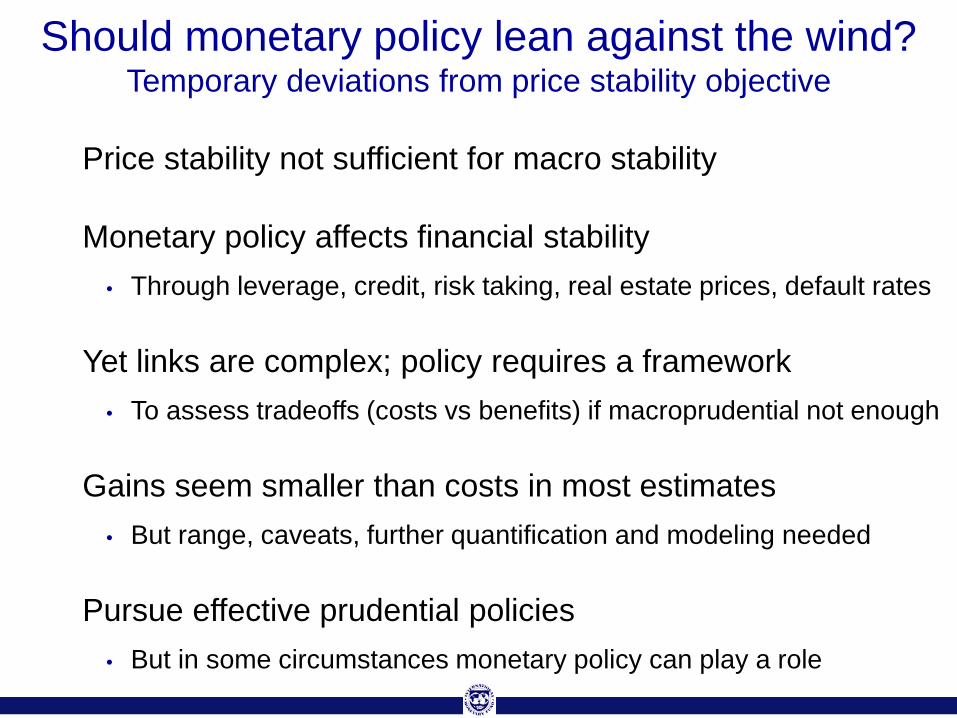

Price stability not sufficient for macro stability

Monetary policy affects financial stability • Through leverage, credit, risk taking, real estate prices, default rates

Yet links are complex; policy requires a framework • To assess tradeoffs (costs vs benefits) if macroprudential not enough

Gains seem smaller than costs in most estimates • But range, caveats, further quantification and modeling needed

Pursue effective prudential policies • But in some circumstances monetary policy can play a role

Should monetary policy lean against the wind? Temporary deviations from price stability objective

Three objectives

Help policy-makers consider tradeoffs • Develop a framework for a cost-benefit analysis, consistent approach

Help policy-makers act • Provide initial calibrations and policy recommendations

• Based on research frontier

• Reduce policy uncertainty

Guide future work • Identify knowledge gaps

• Establish Fund as key voice in live policy debate

Great Moderation • Monetary policy to focus on inflation (& unemployment/ output gaps)

Asset prices and credit aggregates a concern • Only through their impact on welfare: GDP and inflation • RBA, Riksbank, Norges Bank, some EMs have different views

Benign neglect approach to boom/busts • Bubbles difficult to identify • Costs of clean up limited and policy effective • Better to clean up ex post than prevent ex ante

Financial stability important, but job of regulators

Pre-crisis consensus

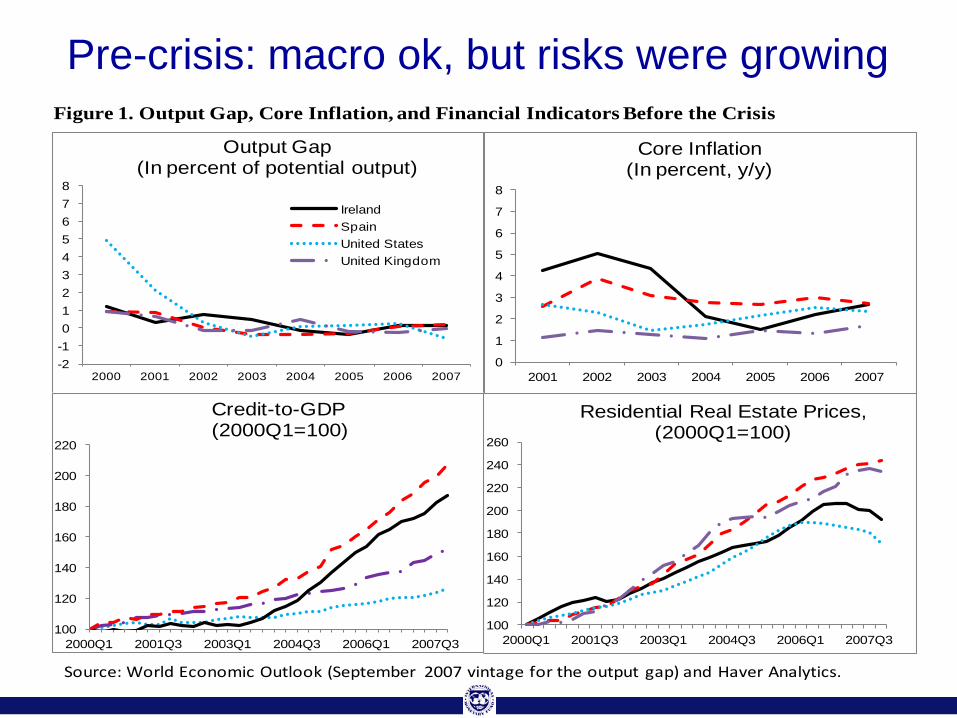

Pre-crisis: macro ok, but risks were growing

-2-1012345678

2000 2001 2002 2003 2004 2005 2006 2007

Output Gap(In percent of potential output)

IrelandSpainUnited StatesUnited Kingdom

100

120

140

160

180

200

220

240

260

2000Q1 2001Q3 2003Q1 2004Q3 2006Q1 2007Q3

Residential Real Estate Prices, (2000Q1=100)

100

120

140

160

180

200

220

2000Q1 2001Q3 2003Q1 2004Q3 2006Q1 2007Q3

Credit-to-GDP (2000Q1=100)

0

1

2

3

4

5

6

7

8

2001 2002 2003 2004 2005 2006 2007

Core Inflation(In percent, y/y)

Source: World Economic Outlook (September 2007 vintage for the output gap) and Haver Analytics.

Figure 1. Output Gap, Core Inflation, and Financial Indicators Before the Crisis

LVA

EST

LTU

IRL

UKR

JPN

RUS

DNK

HKG

SWE

SVN

GBRNLD

SVK

ESP

BGR

MYS

BOL

THAPHL

AUS

IND

KAZ

PAN

URY

DOM

NPL

VNM

BGD

MOZCHLMAR

SURIDN

CHN

y = -1.2852x + 12.969R² = 0.14

-50

-25

0

25

50

75

100

-30 -20 -10 0 10 20 30

Cha

nge

in c

redi

t-to-

GD

P ra

tio fr

om 2

000

to 2

006

Change in GDP from 2007 to 2009

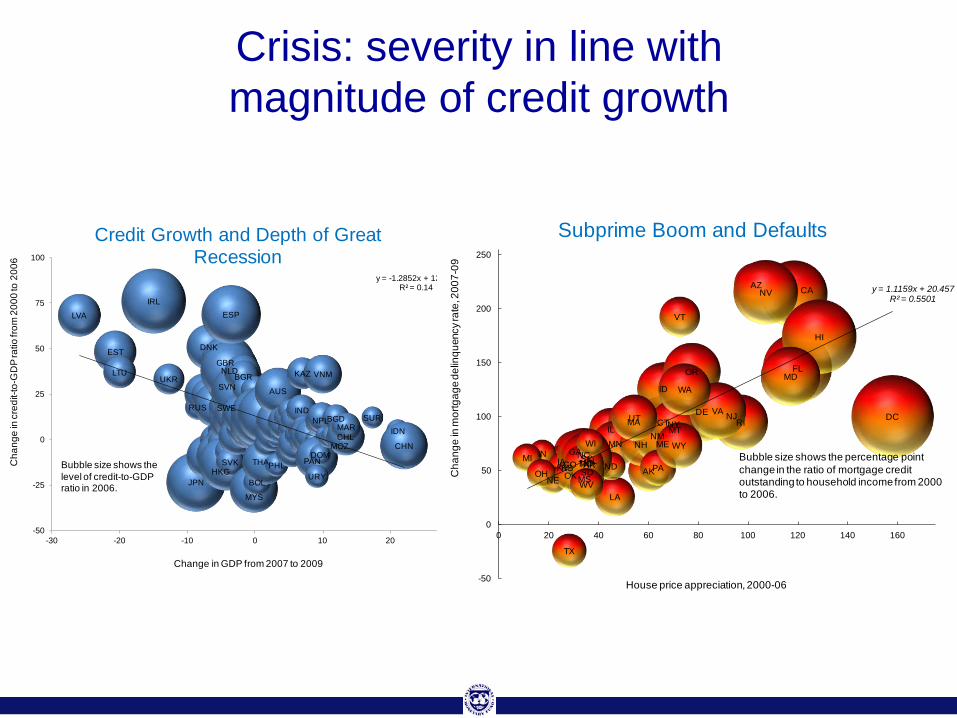

Credit Growth and Depth of Great Recession

Bubble size shows the level of credit-to-GDP ratio in 2006.

AKALAR

AZ CA

CO

CT DCDE

FL

GA

HI

IA

ID

IL

INKSKY

LA

MA

MD

MEMI

MN

MO

MS

MT

NCND

NE

NH

NJ

NM

NV

NY

OH OK

OR

PA

RI

SCSDTN

TX

UTVA

VT

WA

WI

WV

WY

y = 1.1159x + 20.457R² = 0.5501

-50

0

50

100

150

200

250

0 20 40 60 80 100 120 140 160

Cha

nge

in m

ortg

age

delin

quen

cy ra

te, 2

007-

09

House price appreciation, 2000-06

Subprime Boom and Defaults

Bubble size shows the percentage point change in the ratio of mortgage credit outstanding to household income from 2000 to 2006.

Crisis: severity in line with magnitude of credit growth

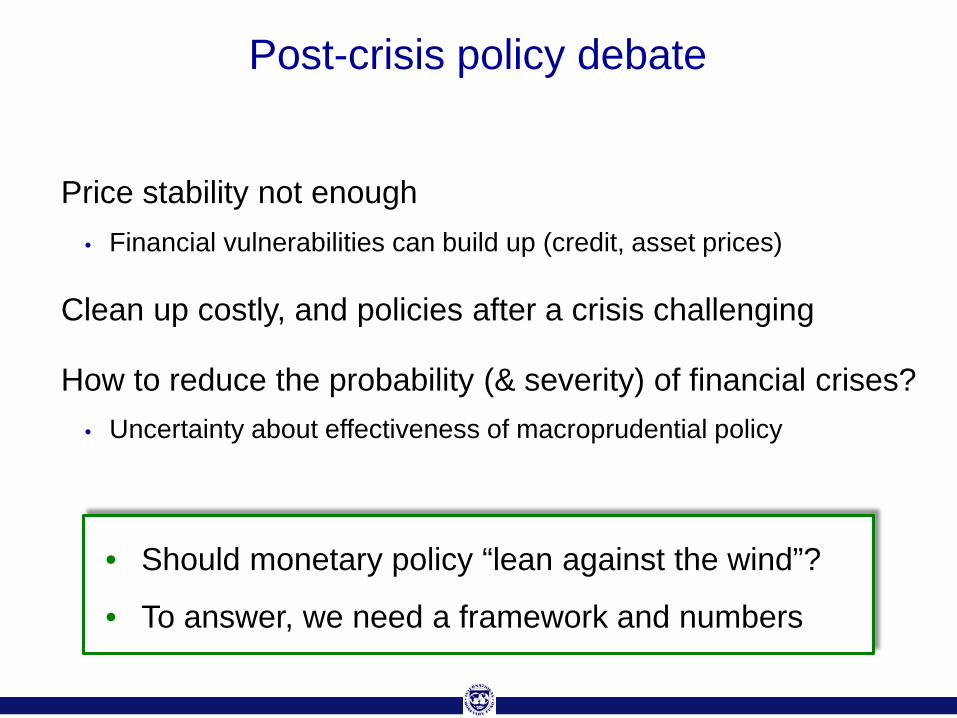

Post-crisis policy debate

Price stability not enough • Financial vulnerabilities can build up (credit, asset prices)

Clean up costly, and policies after a crisis challenging

How to reduce the probability (& severity) of financial crises? • Uncertainty about effectiveness of macroprudential policy

• Should monetary policy “lean against the wind”?

• To answer, we need a framework and numbers

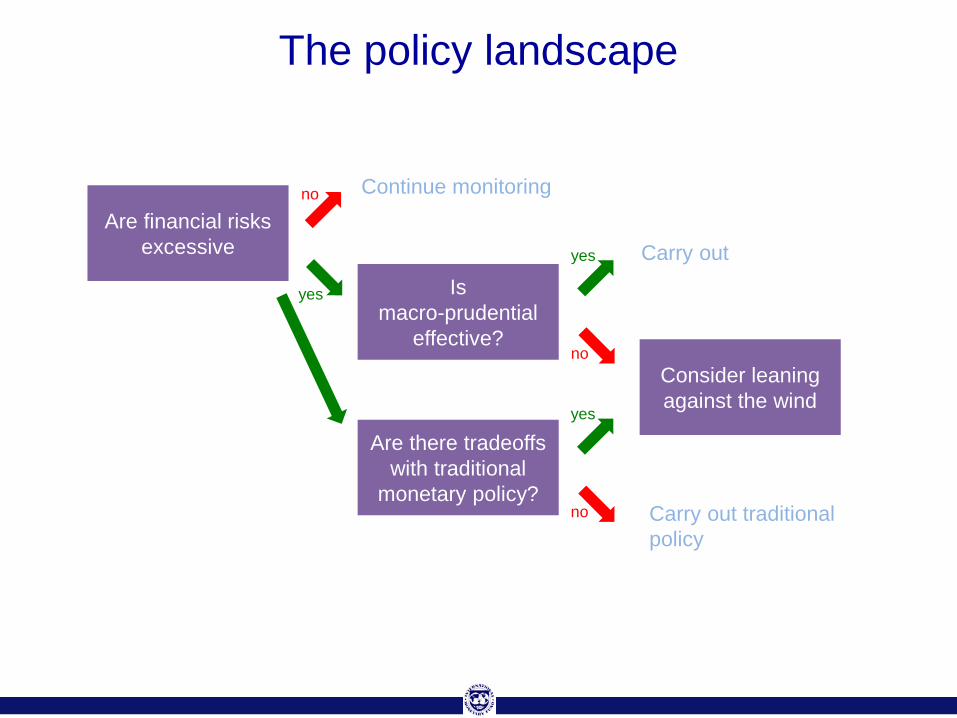

The policy landscape

Are financial risks excessive

Is macro-prudential

effective?

Are there tradeoffs with traditional

monetary policy?

yes

no

no

yes

Consider leaning against the wind

no

yes

Continue monitoring

Carry out

Carry out traditional policy

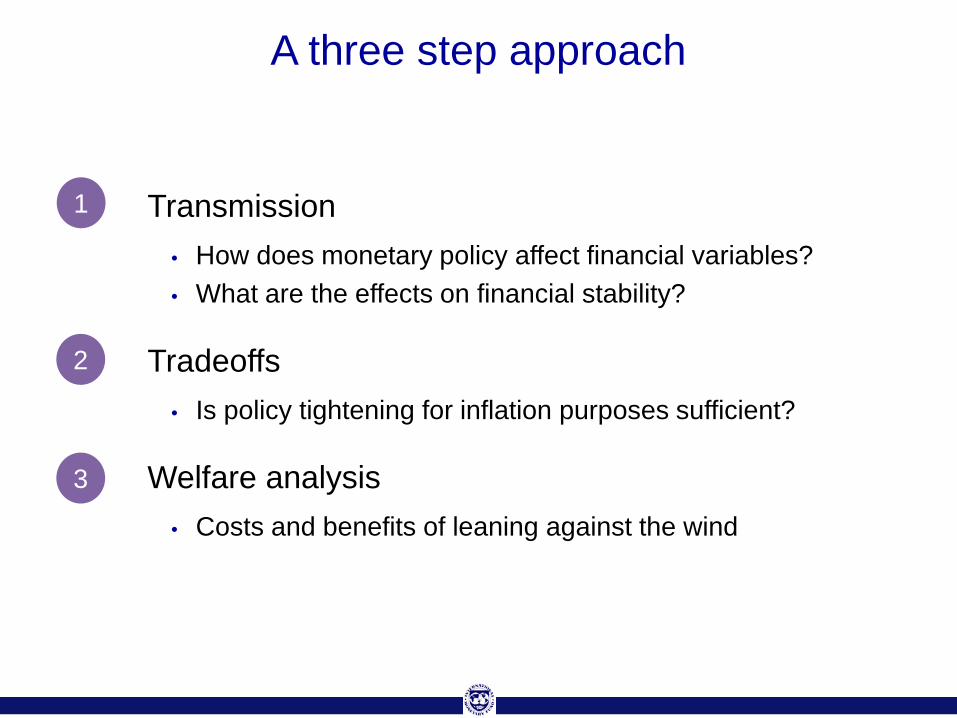

A three step approach

Transmission • How does monetary policy affect financial variables? • What are the effects on financial stability?

Tradeoffs • Is policy tightening for inflation purposes sufficient?

Welfare analysis • Costs and benefits of leaning against the wind

1

3

2

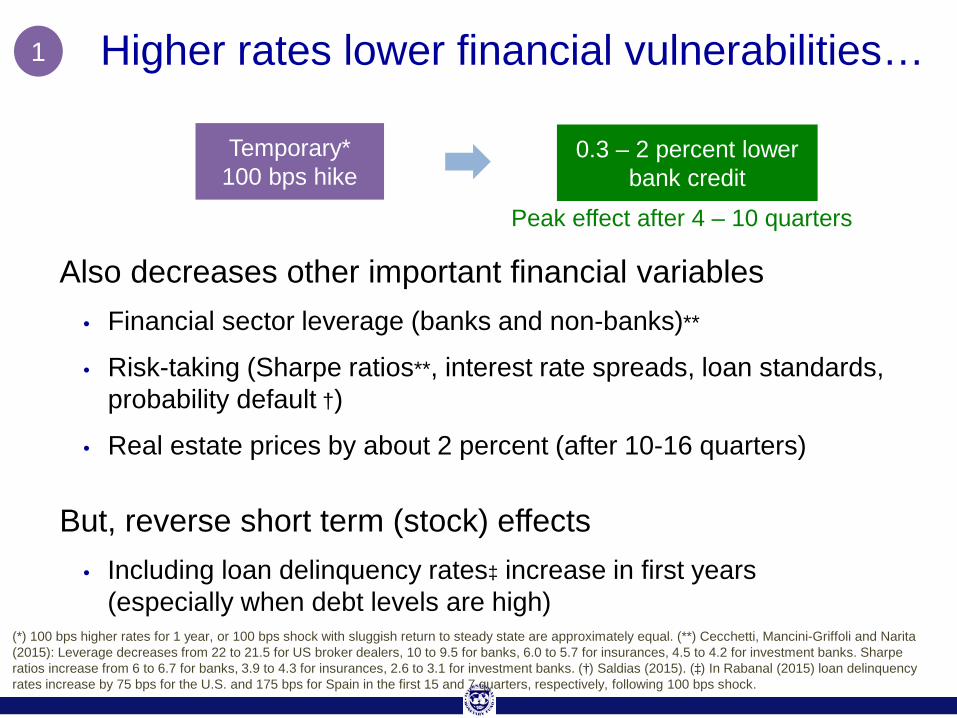

Also decreases other important financial variables • Financial sector leverage (banks and non-banks)**

• Risk-taking (Sharpe ratios**, interest rate spreads, loan standards, probability default †)

• Real estate prices by about 2 percent (after 10-16 quarters)

But, reverse short term (stock) effects • Including loan delinquency rates‡ increase in first years

(especially when debt levels are high)

Higher rates lower financial vulnerabilities… 1

0.3 – 2 percent lower bank credit

Temporary* 100 bps hike

Peak effect after 4 – 10 quarters

(*) 100 bps higher rates for 1 year, or 100 bps shock with sluggish return to steady state are approximately equal. (**) Cecchetti, Mancini-Griffoli and Narita (2015): Leverage decreases from 22 to 21.5 for US broker dealers, 10 to 9.5 for banks, 6.0 to 5.7 for insurances, 4.5 to 4.2 for investment banks. Sharpe ratios increase from 6 to 6.7 for banks, 3.9 to 4.3 for insurances, 2.6 to 3.1 for investment banks. (†) Saldias (2015). (‡) In Rabanal (2015) loan delinquency rates increase by 75 bps for the U.S. and 175 bps for Spain in the first 15 and 7 quarters, respectively, following 100 bps shock.

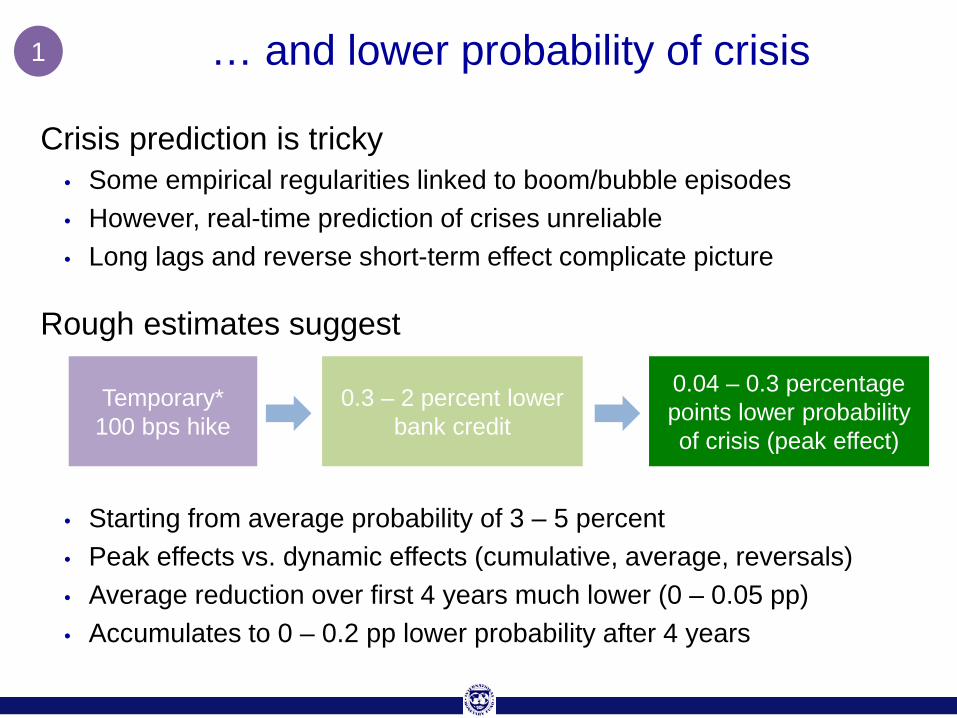

… and lower probability of crisis 1

Crisis prediction is tricky • Some empirical regularities linked to boom/bubble episodes • However, real-time prediction of crises unreliable • Long lags and reverse short-term effect complicate picture

Rough estimates suggest

• Starting from average probability of 3 – 5 percent • Peak effects vs. dynamic effects (cumulative, average, reversals) • Average reduction over first 4 years much lower (0 – 0.05 pp) • Accumulates to 0 – 0.2 pp lower probability after 4 years

0.3 – 2 percent lower bank credit

Temporary* 100 bps hike

0.04 – 0.3 percentage points lower probability of crisis (peak effect)

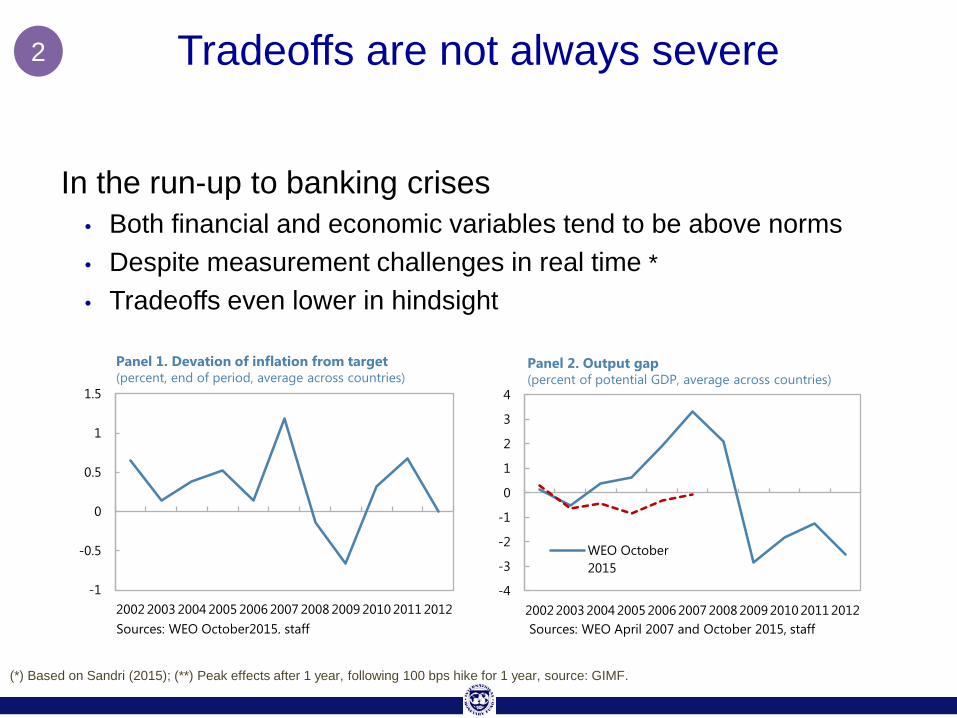

Tradeoffs are not always severe

In the run-up to banking crises • Both financial and economic variables tend to be above norms • Despite measurement challenges in real time * • Tradeoffs even lower in hindsight

2

(*) Based on Sandri (2015); (**) Peak effects after 1 year, following 100 bps hike for 1 year, source: GIMF.

-4

-3

-2

-1

0

1

2

3

4

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

WEO October2015

Panel 2. Output gap (percent of potential GDP, average across countries)

Sources: WEO April 2007 and October 2015, staff

-1

-0.5

0

0.5

1

1.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Panel 1. Devation of inflation from target (percent, end of period, average across countries)

Sources: WEO October2015, staff

Systemic leaning against the wind • May lower the buildup of vulnerabilities

Some support for leaning against the wind in DSGE models • But models remain stylized

• Effects are small and state dependent (policy mistakes possible)

• Effects of (rudimentary) macroprudential policy much larger

Welfare is best addressed with full models 3

See, for instance, Laseen, Pescatori and Turunen (2015); Quint and Rabanal (2014); Unsal (2014); Leduc and Natal (2015).

No welfare lost in forecast period

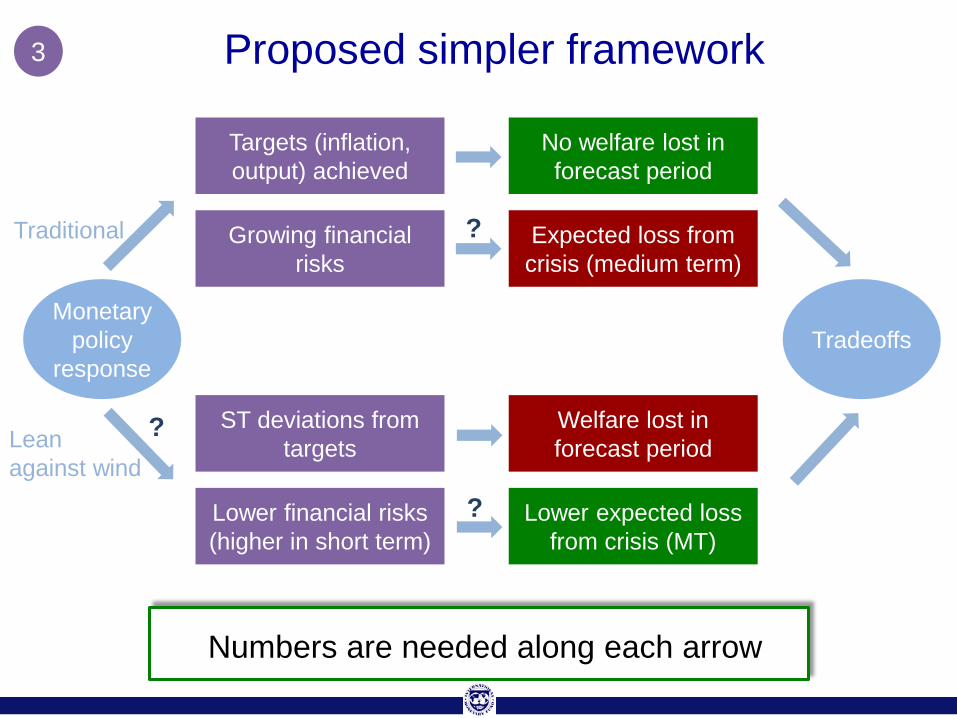

Proposed simpler framework

Targets (inflation, output) achieved

Growing financial risks

Expected loss from crisis (medium term)

Welfare lost in forecast period

ST deviations from targets

Lower financial risks (higher in short term)

Lower expected loss from crisis (MT)

Monetary policy

response Tradeoffs

Numbers are needed along each arrow

Traditional

Lean against wind

?

3

?

?

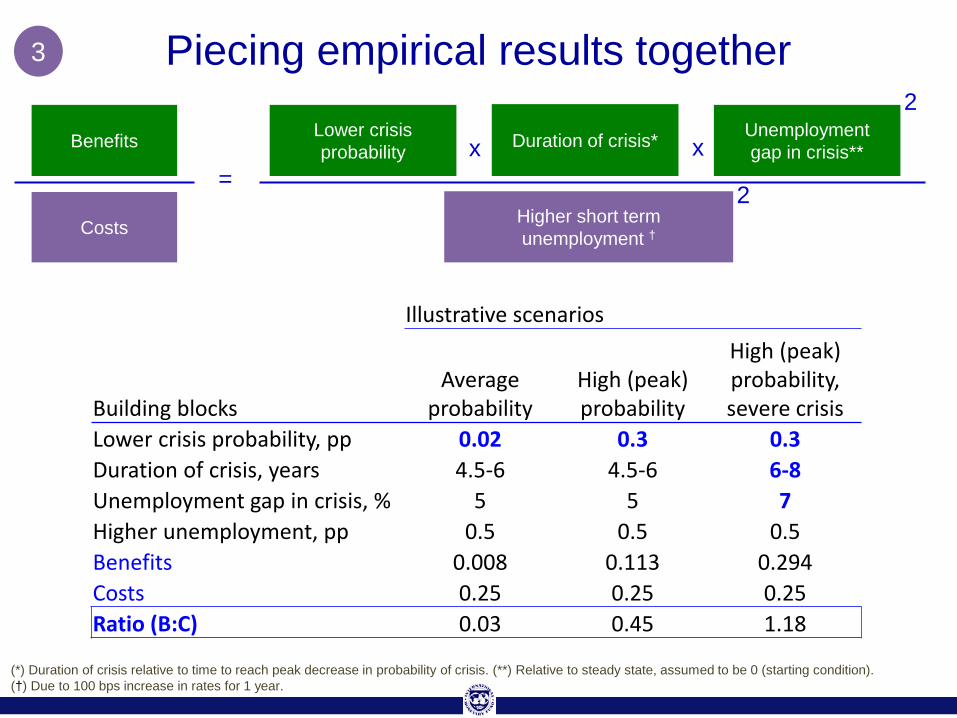

Piecing empirical results together

Costs

Benefits

=

Lower crisis probability Duration of crisis* Unemployment

gap in crisis**

Higher short term unemployment †

x x

(*) Duration of crisis relative to time to reach peak decrease in probability of crisis. (**) Relative to steady state, assumed to be 0 (starting condition). (†) Due to 100 bps increase in rates for 1 year.

Illustrative scenarios

Building blocks Average

probability High (peak) probability

High (peak) probability, severe crisis

Lower crisis probability, pp 0.02 0.3 0.3 Duration of crisis, years 4.5-6 4.5-6 6-8 Unemployment gap in crisis, % 5 5 7 Higher unemployment, pp 0.5 0.5 0.5 Benefits 0.008 0.113 0.294 Costs 0.25 0.25 0.25 Ratio (B:C) 0.03 0.45 1.18

2

2

3

Higher rates may also reduce set-backs • But findings remain inconclusive

Credibility and communication issues • Arising from multiple mandates, inflation undershooting objective,

and crises happening nonetheless

Implementation issues • Timing essential; real-time forecasting of crises an issue

Other considerations

Spillovers and small open economies

Spillovers from LATW in a large country • Higher benefits via financial linkages, but also higher costs via trade

linkages

• Requires model or other framework to assess benefits and costs across countries

• Or appreciate currency (reinforce balance sheet effects)

Constraints on LATW in small open economies • Raising rates might attract additional capital inflows, with risk of

subsequent reversal

• Special risks from FX borrowing

• Could also exacerbate exchange rate appreciation(e.g. carry trades)

• All this can reinforce balance sheet effects, financial stability risks

Should monetary policy lean against the wind?

In general, no • But the door should remain open … • … as our knowledge evolves • … and in certain circumstances (case by case)

Benefits grow relative to costs • Conjuncture: rapid credit growth, low unemployment, strong balance

sheets, high probability of crisis

• Structure: large, interconnected economy

Prudential policies should be the first policy considered • More targeted, probably less costly, more permanent