Embed Size (px)

Citation preview

Motivational profiling of store brand shoppers:Differences across quality tiers

Mercedes Martos-Partal & Oscar González-Benito &

Mariana Fustinoni-Venturini

# Springer Science+Business Media New York 2013

Abstract A recent trend characterizing the retail industry is the rapid growth of storebrands; many retailers now manage a store brand portfolio that incorporates multiplevalue propositions, such as a generic, a standard, and a premium brand. Yet currentliterature has not investigated whether the motivations and benefits sought differ amongconsumers of national brands and those of different types of store brand. This studyanalyses the shopping expenditures and motivational characteristics of customers oftwo major chains in the Spanish retail industry. The positioning of store brandsmoderates the benefits sought by store brand shoppers, such that each brand attractsdifferent customer segments. Moreover, the overlap between these segments tends to belower than their overlap with segments of national brand buyers. Therefore, anyreference to store brands as a whole appears overly simplistic; an adequately selectedportfolio of store brands instead may help retailers steal purchases from national brands,without cannibalizing their own brands' sales.

Keywords Store brand portfolio . Generic and premium store brands . Benefits sought .

Motivational profile

The growth of store brands represents one of the most notable trends in marketing inrecent decades (Szymanowski and Gijsbrechts 2012). Store brands first emerged ascheap alternatives to national brands, an initial positioning reinforced over time by lowprices, which led consumers to associate store brands with a low-quality levels(Richardson et al. 1994). This trend has been changing. Many retailers are moving

Mark LettDOI 10.1007/s11002-013-9274-x

M. Martos-Partal (*) : O. González-Benito :M. Fustinoni-VenturiniDepartamento de Administración y Economía de la Empresa, Universidad de Salamanca, Campus Miguelde Unamuno, 37007 Salamanca, Spaine-mail: [email protected]

O. González-Benitoe-mail: [email protected]

M. Fustinoni-Venturinie-mail: [email protected]

toward higher-quality store brands, which offer benefits for retailer profitability(Corstjens and Lal 2000), and these moves have been noticed by consumers.Manufacturers can no longer assume that store brands are just cheap alternatives boughtby people who cannot afford national brands. Thus, it is instructive to keep in mind aremarkable change in quality perceptions of store brands, with the recognition that storebrands today are attractive alternatives to national brand products (ACNielsen 2011).

Many retailers have developed store brand portfolios that incorporate multiple valuepropositions (Geyskens et al. 2010). A portfolio of store brands enables the retailer topenetrate several different customer segments simultaneously (Kumar and Steenkamp2007). The newest trend is the offer of premium store brands, together with generic andstandard store brands that thus far have been the most common types. Considering thisnew competitive scenario, store brands cannot be analyzed in aggregate; as Palmeiraand Thomas (2011) suggest, it seems surprising that the multitier reality has notreceived more marketing attention.

In this evolving context, store brand shopper profiling, despite being one of the earliestresearch topics related to store brands, remains highly interesting. The extraordinarygrowth of store brand sales and their markedly increasing heterogeneity makes it neces-sary to return to this theme and explore it in more depth. The tasks of delimiting thecommon characteristics shared by potential customers of modern store brands, as well asthose that distinguish them as identifiable, accessible, and actionable, remain a priority forretailers. Therefore, the main goal of this article is to analyze the motivational determi-nants of consumers' choices among national brands and different types of store brands.

Our research contributes to previous literature in two interrelated aspects. First, wefocus on the heterogeneity of store brands, according to the distinctions of their valuepropositions. Specifically, we consider a three-tiered classification that distinguishesgeneric, standard, and premium store brands (Geyskens et al. 2010). Presumably, thesetypes of store brands seek to reach a wider consumer base, such that they should attractdifferent kinds of consumers. Second, we investigate the motivational and benefits-sought characterization of store brand buyers. Despite a large body of research intostore-brand consumers, we still lack sufficient empirical generalizations (Ailawadi andKeller 2004). Previous studies have focused on sociodemographic variables to explainthe choice of store brands as alternatives to national brands, and just a few soughtbenefits, such as price sensitivity and quality sensitivity, have received real researchattention (Sethuraman 2006). With some notable exceptions (e.g., Ailawadi et al. 2001),the other benefits sought have been scantly researched. Because segmentation by benefitsought deepens the motivational rationale and causal factors of consumption, andtherefore should determine shopping behavior more accurately than descriptive factors(Haley 1968), its potential to distinguish store brand buyers seems deserving of moretimely attention. Furthermore, previous research has obviated an explicit comparison ofdifferent types of store brands, particularly the upper level of quality positioning(premium). In this context, we focus on the relationship between consumers' motiva-tional traits and the purchase of different types of store brands as substitutes for nationalbrands. Distinguishing store brands' positions might offer an underlying reason for someinconclusive or even contradictory previous evidence in this regard.

To achieve our objective, we analyze the customers of two retailers, both of whichpursue multiple-tier store brand strategies and offer several store brands with differentprice–quality positions, then compare the various store brands offered by the same

Mark Lett

retailer. This approach minimizes the potentially biasing effect of any one retailer'spositioning. We further use objective behavior data (panel data), in combination withsubjective data (survey), to describe people's shopping motivations and relate them totheir choices of store and national brands. Finally, our dependent variable is consumers'budget allocation to national brands and different types of store brands, so our analysisrelies on a fractional multinomial logit model.

Our results provide interesting insights about the role of consumers' price sensitivity,promotion propensity, service sensitivity, shopping enjoyment, innovativeness, andbrand sensitivity for the choice of national brands and generic, standard, and premiumstore brands. When the positioning prioritizes price (i.e., generic brands), it attractsconsumers who are price sensitive but not service sensitive. When a brand's positioningprioritizes quality (i.e., premium brands), it attracts store brand shoppers who are moreconcerned about service but less concerned with price. It also seems to attract shopperswho are more concerned about shopping enjoyment, less brand sensitive, and lessinnovative. Our findings thus suggest that general references to store brands and storebrand buyers can be incomplete and ambiguous. The positioning of store brands has astrong effect on the profile of potential buyers. Each store brand tier attracts differentprofiles of customers. The motivations to substitute national brands with recent valuepropositions by store brands differ from the motivations that prompted the purchase ofmore traditional store brands. Therefore, our findings show that the expansion of storebrand portfolios has enabled retailers to attract very different profiles of consumers andcompete with national brands from different flanks.

1 Conceptual framework

1.1 Store brand portfolio

Store brands traditionally have been perceived as inferior quality alternatives, whichcompensated for their lack of quality with lower prices (Richardson et al. 1994). Todaythough, the price effect on perceived quality has decreased (Völckner and Hofmann2007), and even when store brands offer better prices, consumers perceive that theirquality levels are comparable to those of manufacturers' brands. Recent literature alsohas noted store brands' positive developments in terms of perceived quality (Sobermanand Parker 2006; Steenkamp et al. 2010). Store brand offers have developed to such anextent that major distributors rarely commercialize just one store brand and insteaddevise store brand portfolios to appeal simultaneously to different markets of con-sumers (Geyskens et al. 2010; Kumar and Steenkamp 2007). A common brandportfolio strategy features three tiers that suggest a “good, better, best” approach, withan economic and a premium store brand line, as well as the standard brand that has longbeen available (Ailawadi and Keller 2004).

Standard store brands usually adopt a balanced position in terms of quality and priceand follow an imitation strategy toward national brands, which enables them to offersimilar quality at a lower price. In contrast, generic brands emphasize basic uses of theproduct, positioning themselves as the cheaper alternative and engaging in limitedpromotional activities, simpler packaging, and economized ingredients. Perhaps themost notable development in the store brand market though is upmarket expansion.

Mark Lett

Premium store brands are the top end of the market and deliver quality equal to that ofpremium quality national brands. By using this premium brand, distributors hope todifferentiate themselves and improve their image.

1.2 Motivational profile of store brand shoppers

To determine the underlying determinants of store brand shopping, an emphasis onmotivations and benefits sought emerges as appealing because these elements consti-tute the true reason for consumption (Haley 1968). Because of the evolution of storebrands across the price–quality continuum, we consider it insufficient to propose asingle store brand consumer profile. Rather, we expect that motivational aspects differfor the choice of generic, standard, and premium store brands as alternatives to nationalbrands. However, the few studies that compare consumers' motivations across price–quality positions (Bellizi et al. 1981; Cunningham et al. 1982) have focused exclusivelyon a comparison of generic and standard versions.

Price sensitivity The price differential between store brands and national brands is stillan important selling proposition for store brands. On average, store brands are lessexpensive than national brands in grocery product classes; they gain sales by offering aprice lower than that of the national brands, and price sensitivity should be an importantcriterion among store brand buyers (Cunningham et al. 1982; Sinha and Batra 1999).However, in the store brand portfolio, brands take very different positions along theprice–quality continuum. Whereas generic brands are the cheapest alternatives andstandard brands offer lower prices than average prices for national brands, premiumbrands' strategy is not based on price differentials (Burt 2000). Moreover, prices forpremium store brands are usually higher than average prices for national brands.Therefore, price–quality positions of store brands should affect price-sensitive con-sumers' choices.

H1. Price sensitivity is associated with higher probabilities of purchasing genericstore brands relative to standard store brands, standard store brands relative tonational brands, and national brands relative to premium store brands.

Promotion propensity As store brands gain footholds, national brand manufacturerslikely turn to promotions to prevent consumer switching, and promotion-prone con-sumers may buy national instead of store brands (Garretson et al. 2002). In general,research has treated people who purchase national brands on promotion as differentfrom typical store brand consumers (Ailawadi et al. 2001); it appears that this motiva-tional aspect relates negatively to store brand shopping (Burton et al. 1998). However,the growing heterogeneity of store brand strategies challenges this behavioral pattern.Although generic store brands are virtually never promoted, marketing decisions forpremium or standard store brands tend to be more similar to those of manufacturerbrands (Kumar and Steenkamp 2007). These store brands often use promotions, thoughstill perhaps less intensively than national brands (Sethuraman and Raju 2011). Thus,only store brands positioned on the lower price, lower quality end of the continuumshould be less attractive to shoppers looking for promotions, whereas the value

Mark Lett

proposition of store brands should affect promotion-prone consumers' choices asfollows:

H2. Promotion propensity is associated with lower probabilities of purchasinggeneric store brands relative to standard store brands and standard store brandsrelative to national brands and premium store brands.

Service sensitivity The search for service relates to the search for the best shoppingexperience, the best shopping basket, and, in particular, the highest product quality. Onthe contrary, non-service sensitive consumers mainly focus on price. For example, outletmalls attract price-sensitive non-service sensitive consumers (Coughlan and Soberhan2005). Since quality-sensitive consumers avoid store brands because they worry abouttheir traditionally assumed inferior quality (Ailawadi et al. 2001, 2008), service sensi-tivity should relate inversely to store brand purchases. However, this line of reasoningdoes not make sense if we take the heterogeneity of store brands into account. Theflagship store brands of most retailers tend to present a standard or premium profile.These brands are part of the retailer's image, with simultaneous transference betweenstore brand images and store images (Nies and Natter 2012). These store brands arepositioned in higher levels of quality and should affect, or even reverse, the role ofservice sensitivity in consumers' choice between store and national brands.

H3. Service sensitivity is associated with lower probabilities of purchasinggeneric store brands relative to standard store brands, standard store brandsrelative to national brands, and national brands relative to premium store brands.

Shopping enjoyment Some consumers enjoy shopping and consider it not a means toan end but rather a recreational end to itself (Williams et al. 1985). However, previousresearch offers inconclusive results related to shopping enjoyment; some studies show anegative relation (Ailawadi et al. 2008) and others offer no significant relation(Ailawadi et al. 2001) between shopping enjoyment and store brand purchases.Considering the store brands located at different positions on the price–quality contin-uum may help clarify these findings. Williams et al. (1985) show that consumers whoseek fun while shopping prefer products and services associated with higher prices,such as national brands and well-known department stores. In general, they are notdiscount consumers. They may be less attracted to generic brands and more attracted topremium brands as alternatives to national brands. Even if all distributors make someefforts to develop hedonic attributes and improve their own brands with nicer packagesand publicity investments (Kumar and Steenkamp 2007), this effort may be especiallysalient for premium brands.

H4. Shopping enjoyment is associated with lower probabilities of purchasinggeneric store brands relative to standard store brands, standard store brandsrelative to national brands, and national brands relative to premium store brands.

Innovativeness A consumer's innovativeness reflects his or her proneness to try andbuy new and different products (Xie 2008). Product innovation traditionally has been

Mark Lett

credited with providing one of the most effective weapons manufacturers may useagainst store brands (Kumar and Steenkamp 2007). However, store brand strategiestend to be minimally innovative, in that they represent a “me-too” approach (Sinapuelasand Robinson 2009). Innovativeness should relate inversely to consumers' choice ofstore rather than national brands. Yet premium store brands also represent a recentphenomenon that involves more newness and uniqueness. Considering this sense ofnovelty, innovative consumers may be more attracted to these brands than to theirtraditional standard and generic counterparts. Moreover, store brand positioning reflectsnot only the degree of innovativeness but also the competitive effect of these innova-tions. In this regard, Gielens (2012) cites the need to assess the multiple tiers of themodern store brands context to determine the effect of new product developments. Inparticular, she notes that innovations by leading national brands take sales from all storebrand tiers; standard store brands behave increasingly like leading national brands; andonly innovations launched by economy store brands fail to affect rival shares.

H5. Innovativeness is associated with lower probabilities of purchasing genericstore brands relative to standard store brands and standard store brands relative tonational brands and premium store brands.

Brand sensitivity Park et al. (2010) define brand-sensitive consumers as those orientedtoward more expensive, well-known brands, who do not conduct careful investigationsof branded products' quality or attributes. Brand sensitivity and store brand purchaseshave been scarcely researched though. Customers with more positive attitudes towardstore brands and with more store brands in their shopping baskets appear less orientedtoward branded products (Baltas and Argouslidis 2007). That is, brand sensitivityappears inversely related to the choice of store brands. However, standard and premiumstore brands are getting wider recognition among consumers. Retailers tend to use anumbrella branding strategy for these brands, relate them to the retail name, and evenposition them as flagship store brands. Therefore, brand-sensitive consumers mayprefer premium store brands, with their improved quality positioning, higher prices,and extended marketing (Kumar and Steenkamp 2007). In contrast, generic storebrands are commonly viewed as “category killers”—cheap, me-too products (Dunneand Narasimhan 1999)—that should have little appeal for brand-sensitive consumers.

H6. Brand sensitivity is associated with lower probabilities of purchasing genericstore brands relative to standard store brands and standard store brands relative tonational brands and premium store brands.

2 Methodology

To analyze how store brand positioning aligns with the different motivational charac-teristics of store brand shoppers, we focus on retail chains whose store brand portfoliosinclude brands that reflect various positioning strategies. Our comparison of storebrands offered by the same retailer, thus, isolates the role of store brand positioning,

Mark Lett

distinct from the positioning of the chain. This study centers on two major retail chainsthat operate in the Spanish market: Carrefour and Eroski. Among Carrefour's storebrands, three stand out as follows: “Número 1,” “Carrefour,” and “Carrefour de nuestratierra” (recently renamed Carrefour Discount, Carrefour, and Carrefour Selección,respectively). These store brands correspond to its generic, standard, and premiumofferings. For Eroski, we similarly find three options in its brand portfolio: “Eroski,”“Eroski Selección,” and “Eroski Deleitte” (the latter two now are commercialized asEroski SeleQtia and Eroski Natur Selección). These three brands correspond to stan-dard (Eroski) and premium (Eroski Selección and Eroski Deleitte) positions. For bothretailers, we study pure store brands, in the sense that the name of the brands includesthe name of the retailer.

To conduct the empirical analysis, we collected historical data about expen-ditures in the food category for a sample of 2,577 households from the KantarWorldPanel Household Panel. Data correspond to a 1-year period (second halfof 2007 to the first half of 2008). These data enable us to compute the share ofwallet of each household devoted to each retail chain; we define customers of aretailer as households with shares greater than or equal to 1 % for that retailerduring the studied period (we obtained similar results with other cutoff points,such as 2 and 5 %). The purpose was to obviate casual customers, who are probablyless familiar with the retailer's store brand portfolio. This definition identified a sampleof 1,199 customers for Carrefour and 914 for Eroski. Furthermore, with these data, wecalculated the share of wallet of each store brand that the retailer sells. This version ofshare of wallet is the dependent variable.

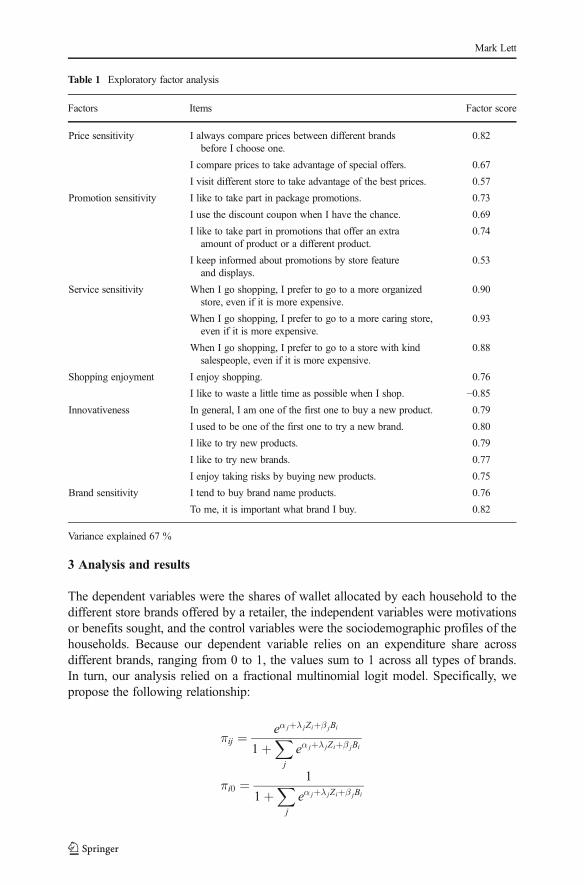

Next, we gathered information from an “opinions and attitude” survey conducted byKantar WorldPanel with more than 4,000 panelists in July 2008. This informationhelped quantify the motivations and benefits sought by consumers. Of the 160 ques-tions in the survey, we considered those that corresponded to the benefits sought in ourtheoretical framework; these items used five-point Likert-type scales (1=“stronglydisagree,” 5=“strongly agree”). With these selected items, we then conducted aprincipal components factorial analysis to identify the specific dimensions of benefitssought. Six factors were consistent with the motivations we have proposed in ourconceptual framework, as we detail in Table 1. Moreover, our service sensitivitymeasure was positively correlated (p<0.0) with the item “I do not mind paying morefor quality,” which supports our claim that the desire for service relates to the desire forproduct quality. For our factor analysis, we used the factor resulting from this analysisto measure benefits sought in shopping.

The panel data also provided sociodemographic information for the households,which we included as control variables. We considered household size (1–8, whereeight represents households with eight or more members), the presence of childrenunder 6 years of age, and social class (four levels: low, low–medium, medium, andmedium–high to high).

We combined the motivational data from the survey with expenditure data and thesociodemographic profile of clients for each chain, obtained from the panel, using onlythose households present in both samples. As a consequence, our final samples featured838 clients of Carrefour and 596 customers of Eroski (285 households were customersof both retailers).

Mark Lett

3 Analysis and results

The dependent variables were the shares of wallet allocated by each household to thedifferent store brands offered by a retailer, the independent variables were motivationsor benefits sought, and the control variables were the sociodemographic profiles of thehouseholds. Because our dependent variable relies on an expenditure share acrossdifferent brands, ranging from 0 to 1, the values sum to 1 across all types of brands.In turn, our analysis relied on a fractional multinomial logit model. Specifically, wepropose the following relationship:

πij ¼ eα jþλ jZiþβ jBi

1þX

j

eα jþλ jZiþβ jBi

πi0 ¼ 1

1þX

j

eα jþλ jZiþβ jBi

Table 1 Exploratory factor analysis

Factors Items Factor score

Price sensitivity I always compare prices between different brandsbefore I choose one.

0.82

I compare prices to take advantage of special offers. 0.67

I visit different store to take advantage of the best prices. 0.57

Promotion sensitivity I like to take part in package promotions. 0.73

I use the discount coupon when I have the chance. 0.69

I like to take part in promotions that offer an extraamount of product or a different product.

0.74

I keep informed about promotions by store featureand displays.

0.53

Service sensitivity When I go shopping, I prefer to go to a more organizedstore, even if it is more expensive.

0.90

When I go shopping, I prefer to go to a more caring store,even if it is more expensive.

0.93

When I go shopping, I prefer to go to a store with kindsalespeople, even if it is more expensive.

0.88

Shopping enjoyment I enjoy shopping. 0.76

I like to waste a little time as possible when I shop. −0.85Innovativeness In general, I am one of the first one to buy a new product. 0.79

I used to be one of the first one to try a new brand. 0.80

I like to try new products. 0.79

I like to try new brands. 0.77

I enjoy taking risks by buying new products. 0.75

Brand sensitivity I tend to buy brand name products. 0.76

To me, it is important what brand I buy. 0.82

Variance explained 67 %

Mark Lett

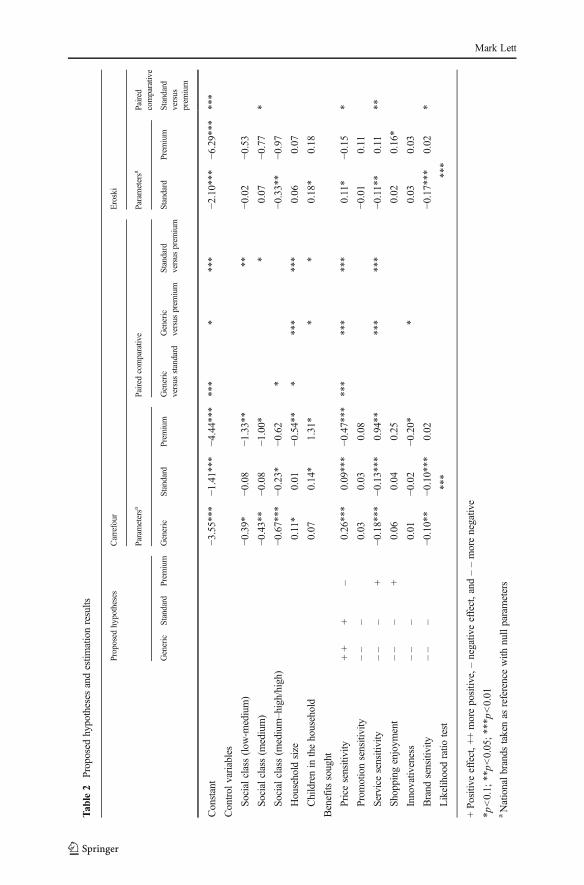

Where πij indicates the share of wallet of household i with store brand j, and πi0

denotes the share of wallet of household i in national brands; αj denotes a parameterthat quantifies expenditure tendencies for store brand j, Zi is the vector ofsociodemographic variables to household i, λj denotes a vector of parameters thatrecognizes the effect of sociodemographic variables (one social class must be takenas a reference), Bi is the vector of benefits sought by household i, and βj denotes avector of parameters, corresponding to the effects of benefits sought. Note that we usenational brands as a reference, and we thus quantify the effect of household character-istics for different types of store brand shopping with respect to national brands. Toestimate the model, we used the Stata fmlogit routine (Maarten 2008). Table 2 containsthe results.

Regarding the effect of benefits sought, the positioning of the store brand moderatesthe relation between store brand consumption and price sensitivity. For Carrefour, theparameter for price sensitivity decreases as quality positioning increases: highest forgeneric brands, followed by standard brands, and then lowest and negative for premiumones. Similarly, Eroski's standard brand buyers are more price sensitive than premiumbrand buyers, in support of H1. Whereas more price-sensitive customers prefer genericsand standard store brands to national brands, less price-sensitive customers preferpremium store brands to national brands. The hypothesized moderation of store brandpositioning on the relationship between promotion sensitivity and store brand con-sumption (H2) cannot be confirmed though because the effects of these variables arenot significant. For service sensitivity, we find a negative effect on store brandconsumption for generic and standard brands (Carrefour) and for standard brands(Eroski). This negative effect disappears for premium brands and even grows positivefor Carrefour, in support of H3—at least for the difference between premium and othertypes of store brands. As observed for price sensitivity, the effect of service sensitivityon the purchase of premium store brands instead of national brands is directly oppositethe effect on the purchase of generic and standard store brands, as substitutes fornational brands. Regarding the effect of shopping enjoyment, our findings suggestfew significant effects. The consumption of premium brands seems positively related tothe search for enjoyment in Eroski. However, we do not find significant differencesacross different types of stores brands and thus cannot confirm H4. The innovativenessresults are somewhat unexpected. We proposed that innovativeness would be morerelated to premium store brand consumption, but our findings for Carrefour suggest theopposite, so we must reject H5. We recommend some caution with regard to thisfinding though, considering the low confidence level (90 %). Perhaps it reflectsCarrefour's emphasis on positioning its premium store brand as providing traditionalproducts from selected origins, which may increase customers' quality perceptions butdecrease their innovativeness perceptions. Finally, we find a significant negativerelationship between brand sensitivity and generic and standard brands in Carrefourand standard brands in Eroski. These effects are not significant for premium brands, inline with H6. However, the differences across store brands' positions are not significant.

These results further imply some differences between retailers. The results for Eroskiseem less strong than for Carrefour, which may result from several effects. From astatistical point of view, the sample of Eroski customers is smaller than that forCarrefour, so the power of the tests is lower. In addition, we noted some signs of biasin the sample selection when we combined the panel and survey data to obtain the

Mark Lett

Tab

le2

Proposed

hypotheses

andestim

ationresults

Proposed

hypotheses

Carrefour

Eroski

Parametersa

Paired

comparative

Parametersa

Paired

comparative

Generic

Standard

Prem

ium

Generic

Standard

Prem

ium

Generic

versus

standard

Generic

versus

prem

ium

Standard

versus

prem

ium

Standard

Prem

ium

Standard

versus

prem

ium

Constant

−3.55***

−1.41***

−4.44***

***

****

−2.10***

−6.29***

***

Control

variables

Socialclass(low

-medium)

−0.39*

−0.08

−1.33**

**−0

.02

−0.53

Socialclass(m

edium)

−0.43**

−0.08

−1.00*

*0.07

−0.77

*

Socialclass(m

edium–high/high)

−0.67***

−0.23*

−0.62

*−0

.33**

−0.97

Household

size

0.11*

0.01

−0.54**

****

***

0.06

0.07

Childrenin

thehousehold

0.07

0.14*

1.31*

**

0.18*

0.18

Benefits

sought

Pricesensitivity

++

+–

0.26***

0.09***

−0.47***

***

***

***

0.11*

−0.15

*

Prom

otionsensitivity

––

–0.03

0.03

0.08

−0.01

0.11

Servicesensitivity

––

–+

−0.18***

−0.13***

0.94**

***

***

−0.11**

0.11

**

Shopping

enjoym

ent

––

–+

0.06

0.04

0.25

0.02

0.16*

Innovativ

eness

––

–0.01

−0.02

−0.20*

*0.03

0.03

Brand

sensitivity

––

–−0

.10**

−0.10***

0.02

−0.17***

0.02

*

Likelihoodratio

test

***

***

+Po

sitiv

eeffect,+

+morepositiv

e,–negativ

eeffect,and

––morenegativ

e

*p<0.1;

**p<0.05;***p

<0.01

aNationalbrands

takenas

referencewith

nullparameters

Mark Lett

Eroski sample. The final sample (adding survey data) differed from the sample ofcustomers (from panel data) on some sociodemographic characteristics. Finally, from amarketing perspective, the maturity of the two chains' store brand portfolios differs asfollows: Carrefour was the first retailer in Spain to launch store brands in 1982, whereasEroski completed the migration to Eroski brands only in 1994. Perceptual changessimply may take more time.

4 Conclusions

A recent trend in retail markets is to manage multiple store brands in a portfolio,positioning each brand differently on the price–quality spectrum. This emergingscenario demands a reconsideration of an early research topic, namely store brandversus national brand shopper profiling. Our research focuses on the impacts of storebrand positioning for the motivational characterization of store brand shoppers.

Our empirical results, obtained with samples of customers of two grocery retail chains,contributes to existing literature by specifying the clear differences among the store brandshopper profiles for generic, standard, and premium brands. Thus, the positioning of storebrands moderates the motivational characterization of store brand shoppers. When thepositioning prioritizes price (i.e., generic brands), it attracts consumers who are pricesensitive but not service sensitive. When a brand's positioning prioritizes quality (i.e.,premium brands), it attracts store brand shoppers who are more concerned about servicebut less concerned with price. It also seems to attract shoppers who are more concernedabout shopping enjoyment, less brand sensitive, and, surprisingly, less innovative—though this last claim requires some caution and further investigation.

We also contribute to extant literature by showing empirically that store brand shop-pers' motivational traits are affected by store brand positioning; store brands cannot beanalyzed in aggregate. The store brand phenomenon has grown highly heterogeneous,and consumers' responses depend on the peculiarities that characterize each store brand.Motivations to purchase store instead of national brands may differ or even contrast acrossthe different value propositions of various store brands. Therefore, our findings suggestthat references to store brands as a whole are likely overly simplistic; different kinds ofstore brands need to be considered explicitly. Previous evidence suggests that a storebrand is not just another brand but rather a singular brand, whose concept prevails acrossretailers, because many consumers fail to distinguish the store brands of different chains(Szymanowski and Gilbrechts 2012). Our findings suggest further that each type of storebrand should be treated as a singular brand. In this regard, our results support the growinginterest in investigating store brand portfolios and their varied competitive positions, inresponse to recent calls to clarify the implications of this phenomenon (Geyskens et al.2010; Martos-Partal and González-Benito 2011; Palmeira and Thomas 2011).

For practitioners, our results also offer key insights. First, store brands are not the same;each type of brand attracts a different consumer segment. As a consequence, overlapbetween segments may be lower than the overlap they exhibit with segments of nationalbrand buyers. Retailers thus can manage a store brand portfolio. In that different storebrands tiers attract different consumer segments, cannibalization is lower. Second, thepositioning of store brands along the quality–price continuum has been effective andlargely accepted by consumers. Retailers' efforts to improve consumers' perceptions of

Mark Lett

their brands, by developing high quality, higher priced brands, thus seems worthwhile.Dissociating store brands from their traditional, price-oriented image has allowed retailersto attract very different profiles of consumers. Moreover, different types of store brandsalong the price–quality continuum compete with national brands from different flanks;national brands appear surrounded. Retailers should maintain this approach, using theirhigher quality store brands to establish differentiation and build image and loyalty, even astheir generic brands support their price battles against discount retailers by attracting price-oriented segments. Third, other benefits sought, such as promotion sensitivity, shoppingenjoyment, and innovativeness, appear less differentiated across store brand types. Thisfinding suggests a positioning opportunity for retailers, which they could exploit todifferentiate themselves from both national brands and other retailers' store brands.However, such an approach would require substantial marketing investments to distin-guish brand types by motivational traits.

Finally, this study is not exempt from limitations, which suggest some furtherresearch directions. First, Spain is one of the most developed markets for store brands,with a 49 % market share, so results for other countries may differ. Second, we onlyprovide evidence for two leading retailers. The generalization of these results couldsuffer from the risk of selection bias; our focus on the customers of specific retailersalso might condition the determinants of SB choice. Third, the measures we used couldbe improved. For example, the benefits sought measures were quantified in a generalway, not for each store brand. In addition, we excluded other benefits that shoppersmight seek, such as product quality sensitivity or a desire to meet budgetary constraints(Ailawadi et al. 2001), smart shopper self-perceptions (Garretson et al. 2002), andvariety or uniformity seeking (Ailawadi et al. 2001; Yoon et al. 2011). Fourth, ourresearch classifies store brands according to their emphasis on price versus quality, butretailers have vast portfolios of store brands and offer other classification methods, suchas category- or benefit-based segmentation (Kumar and Steenkamp 2007). Furtherresearch should explore the differential effects of these categories on motivationalcharacterizations of store brand shoppers. Fifth, our study focuses on different tiersof store brands but obviates different types of national brands. Considering differentprofiles of national brands, such as premium or luxury national brands, could provideadditional insights into the comparison between store and national brand shoppers.Finally, our study has focused on private label portfolios developed under the retailer'sbrand umbrella, i.e., store brands include the name of the retailer. Other types of privatelabels should also be analyzed.

Acknowledgments We thank the editors and reviewers for their insightful comments and suggestions onprevious versions of this article. We also thank Kantar WorldPanel Spain for providing the study data. Thisresearch was supported by Ministerio de Educación y Ciencia, Grant ECO2011-23381 (Spain).

References

ACNielsen (2011). “The rise of the value-conscious shopper” http://au.nielsen.com/site/documents/PrivateLabelGlobalReportMar2011.pdf (accessed 30 May 2011).

Ailawadi, K. L., & Keller, K. L. (2004). Understanding retail branding: Conceptual insights and researchpriorities. Journal of Retailing, 80, 331–342.

Mark Lett

Ailawadi, K. L., Neslin, S. A., & Gedenk, K. (2001). Pursuing the value-conscious consumer: Store brandsversus national brand promotions. Journal of Marketing, 65, 71–89.

Ailawadi, K. L., Pauwels, K., & Steenkamp, J.-B. E. M. (2008). Private label use and store loyalty. Journal ofMarketing, 72(6), 19–30.

Baltas, G., & Argouslidis, P. C. (2007). Consumer characteristics and demand for store brands. InternationalJournal of Retail & Distribution Management, 35(5), 328–341.

Bellizi, J. A., Kruckeberg, H. F., Hamilton, J. R., & Martin, W. S. (1981). Consumer perceptions of national,private, and generic brands. Journal of Retailing, 57(Winter), 56–70.

Burt, S. (2000). The strategic role of retail brands in British grocery retailing. European Journal of Marketing,34(8), 875–890.

Burton, S., Lichtenstein, D. R., Netemeyer, R. G., & Garretson, J. A. (1998). A scale for measuring attitudetoward private label products and an examination of its psychological and behavioral correlates. Journalof the Academy of Marketing Science, 26(4), 293–306.

Corstjens, M., & Lal, R. (2000). Building store loyalty through store brands. Journal of Marketing Research,37(3), 281–291.

Coughlan, A. T., & Soberhan, D. A. (2005). Strategic segmentation using outlet malls. International ofResearch in Marketing, 22, 61–86.

Cunningham, I. C. M., Hardy, A. P., & Imperia, G. (1982). Generic brands versus national brands and storebrands: A comparison of consumers' preferences and perceptions. Journal of Advertising Research, 22(7–8), 25–32.

Dunne, D., & Narasimhan, C. (1999). The new appeal of private label. Harvard Business Review, 77, 41–52.Garretson, J. A., Fisher, D., & Burton, S. (2002). Antecedents of private label attitude and national brand

promotion attitude: Similarities and differences. Journal of Retailing, 78(2), 91–99.Geyskens, I., Gielens, K., & Gijsbrechts, E. (2010). Proliferating private-label portfolios: How introducing

economy and premium private labels influences brand choice. Journal of Marketing Research, 47(5),791–807.

Gielens, K. (2012). New products: The antidote to private label growth? Journal of Marketing Research,49(3), 408–423.

Haley, R. I. (1968). Benefit segmentation: A decision-oriented research tool. Journal of Marketing,32(3), 30–35.

Maarten, L. B. (2008). "FMLOGIT: Stata module fitting a fractional multinomial logit model by quasimaximum likelihood," Statistical Software ComponentsS456976, Boston College Department ofEconomics.

Martos-Partal, M., & Gonzalez-Benito, O. (2011). Store brand and store loyalty: The moderating role of storebrand positioning. Marketing Letters, 22(3), 297–313.

Nies, S., & Natter, M. (2012). Does private label quality influence consumers' decision on where to shop?Psychology and Marketing, 29(49), 279–292.

Palmeira, M. M., & Thomas, D. (2011). Two-tier store brands: The benefic impact of a value brand onperceptions of premium brand. Journal of Retailing, 87(4), 540–548.

Park, J. E., Jun, Y., & Zhou, J. X. (2010). Consumer innovativeness and shopping styles. Journal of ConsumerMarketing, 27(5), 437–446.

Richardson, P., Dick, A. S., & Jain, A. K. (1994). Extrinsic and intrinsic cue effects on perceptions of storebrand quality. Journal of Marketing, 58(4), 28–36.

Sethuraman, R. (2006). “Private label marketing strategies in packaged goods: management beliefs andresearch insights”, Marketing Science Institute Working Paper, No. 06–108 (June)

Sethuraman, R., & Raju, J. S. (2011). Private label strategies: Myths and realities. In V. Shankar & G. S.Carpenter (Eds.), Handbook of Marketing Strategy. Northampton: Edward Elgar Publishing.

Sinapuelas, I. C., & Robinson, W. T. (2009). Entry for supermarket feature me-too brands: An empiricalexplanation of incidence and timing. Marketing Letters, 20(2), 183–196.

Sinha, I., & Batra, R. (1999). The effect of consumer price consciousness on private label purchase.International Journal of Research in Marketing, 16(3), 237–251.

Soberman, D. A., & Parker, P. M. (2006). The economics of quality-equivalent store brands. InternationalJournal of Research in Marketing, 23, 125–139.

Steenkamp, J.-B. E. M., & Kumar, N. (2007). Private label strategy: How to meet the store brand challenge.Boston: Harvard Business School Press.

Steenkamp, J.-B. E. M., van Heerde, H. J., & Geykens, I. (2010). What makes consumers willing to pay aprice premium for national brands over private labels? Journal of Marketing Research, 47(6), 1011–1024.

Szymanowski, M., & Gijsbrechts, E. (2012). Consumption-based cross-brand learning: Are private labelsreally private? Journal of Marketing Research, 49(2), 231–246.

Mark Lett

Völckner, F., & Hofmann, J. (2007). The price-perceived quality relationship: A meta-analytic review andassessment of its determinants. Marketing Letters, 18(3), 181–196.

Williams, T. G., Slama, M., & Rogers, J. (1985). Behavioral characteristics of the recreational shoppers andimplications for retail management. Journal of the Academy of Marketing Science, 13(3), 307–316.

Xie, Y. H. (2008). Consumer innovativeness and consumer acceptance of brand extensions. Journal ofProduct and Brand Management, 14(4), 235–243.

Yoon, S. O., Suk, K., Lee, S. M., & Park, E. Y. (2011). To seek variety or uniformity: The role of culture inconsumers' choice in a group setting. Marketing Letters, 22(1), 49–64.

Mark Lett