Embed Size (px)

Citation preview

1

Name And title

TITLE LINE 1 TITLE LINE 2

Date • Place

3

Confidentiality, Safe Harbor and Non-GAAP Results

This presentation contains confidential information regarding Tenneco Inc. By reviewing this information, the participants agree to treat the information confidentially, not to distribute it and not to use it for any purpose other than evaluating Tenneco Inc. as a potential supplier.

Please see the safe harbor statement and the tables that reconcile GAAP results with non-GAAP results in Tenneco’s corresponding financial results press release, which is incorporated herein by reference.

4

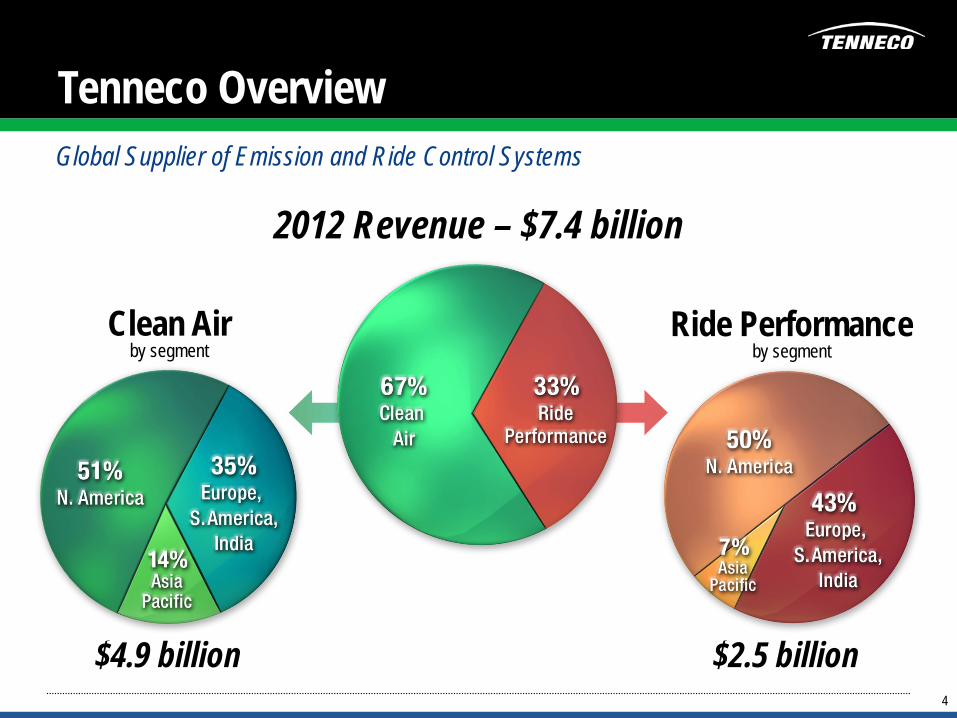

Tenneco Overview

Clean Air by segment

Global Supplier of Emission and Ride Control Systems

2012 Revenue – $7.4 billion

Ride Performance by segment

$4.9 billion $2.5 billion

5

Tenneco Strengths

- Customers - Markets - Geographies - Products

- Solutions to meet emissions regulations - Vehicle ride & handling performance

- Executing with discipline

- Strong alignment globally - Strength at all levels - Talented and dedicated - Passion for winning

• Balance

• Product Technology

• Operational Excellence

• Our People

6

Tenneco Global Operations

6

Headquarters Clean Air Manufacturing Ride Performance Manufacturing Clean Air Engineering Performance Engineering

Nearly 25,000 employees serving customers globally from 89 manufacturing facilities and 14 engineering and technical centers

6

7

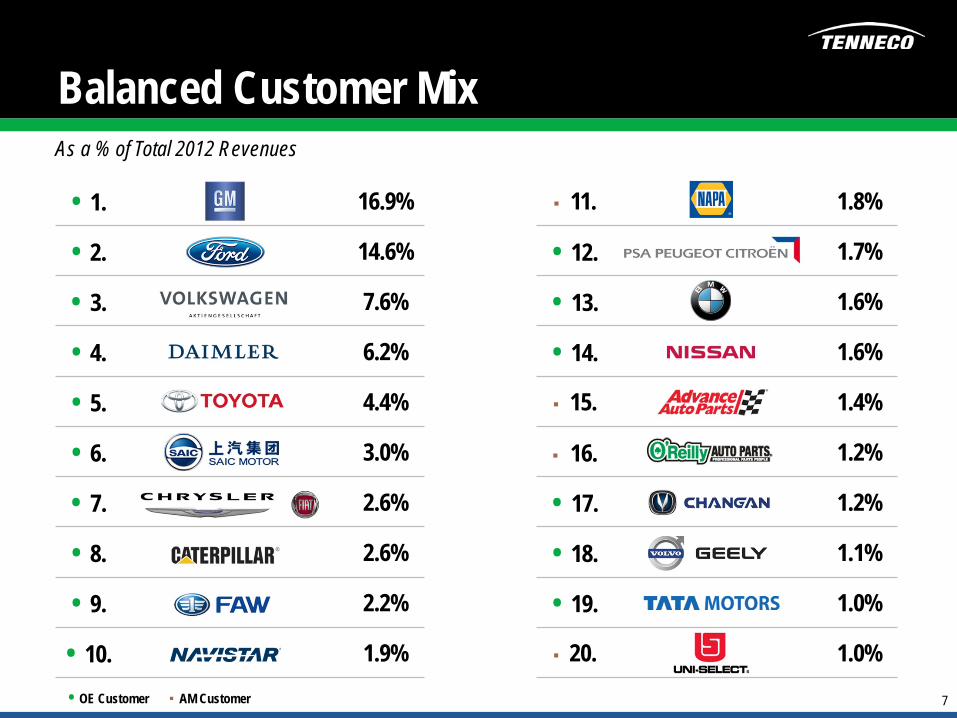

Balanced Customer Mix

• 1. 16.9% ■ 11. 1.8%

• 2. 14.6% • 12. 1.7%

• 3. 7.6% • 13. 1.6%

• 4. 6.2% • 14. 1.6%

• 5. 4.4% ■ 15. 1.4%

• 6. 3.0% ■ 16. 1.2%

• 7. 2.6% • 17. 1.2%

• 8. 2.6% • 18. 1.1%

• 9. 2.2% • 19. 1.0%

• 10. 1.9% ■ 20. 1.0%

As a % of Total 2012 Revenues

• OE Customer ■ AM Customer

8

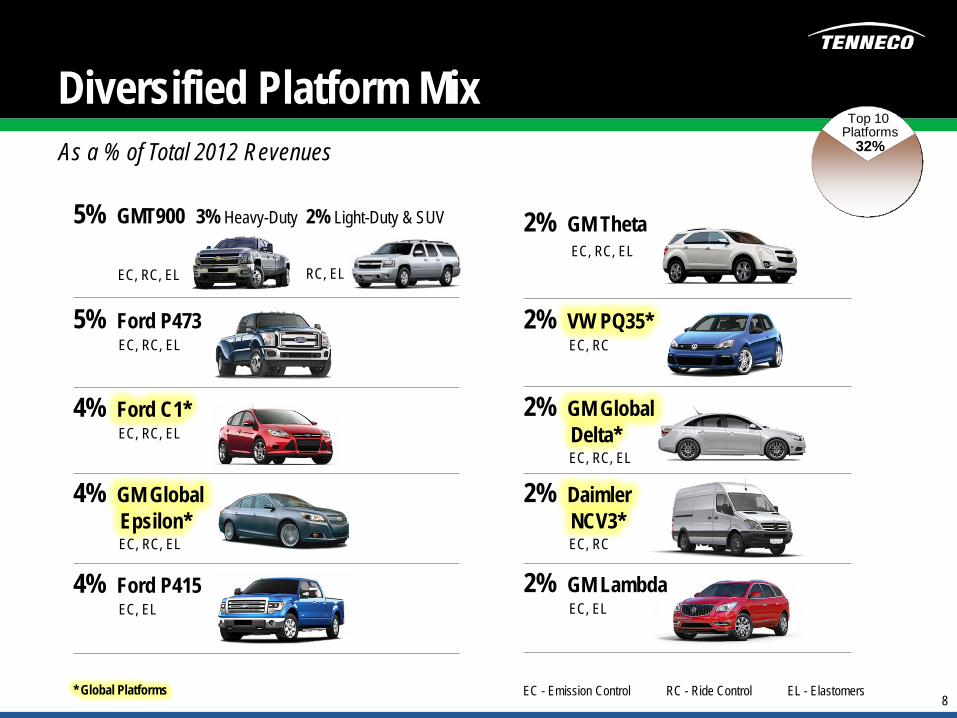

Diversified Platform Mix

2% GM Theta EC, RC, EL

2% VW PQ35* EC, RC

2% GM Global Delta* EC, RC, EL

2% Daimler NCV3* EC, RC

2% GM Lambda EC, EL

5% GMT900

EC, RC, EL

3% Heavy-Duty 2% Light-Duty & SUV

RC, EL

5% Ford P473 EC, RC, EL

4% Ford C1* EC, RC, EL

4% GM Global Epsilon* EC, RC, EL

4% Ford P415 EC, EL

As a % of Total 2012 Revenues

EC - Emission Control RC - Ride Control EL - Elastomers

Top 10 Platforms

32%

* Global Platforms

9

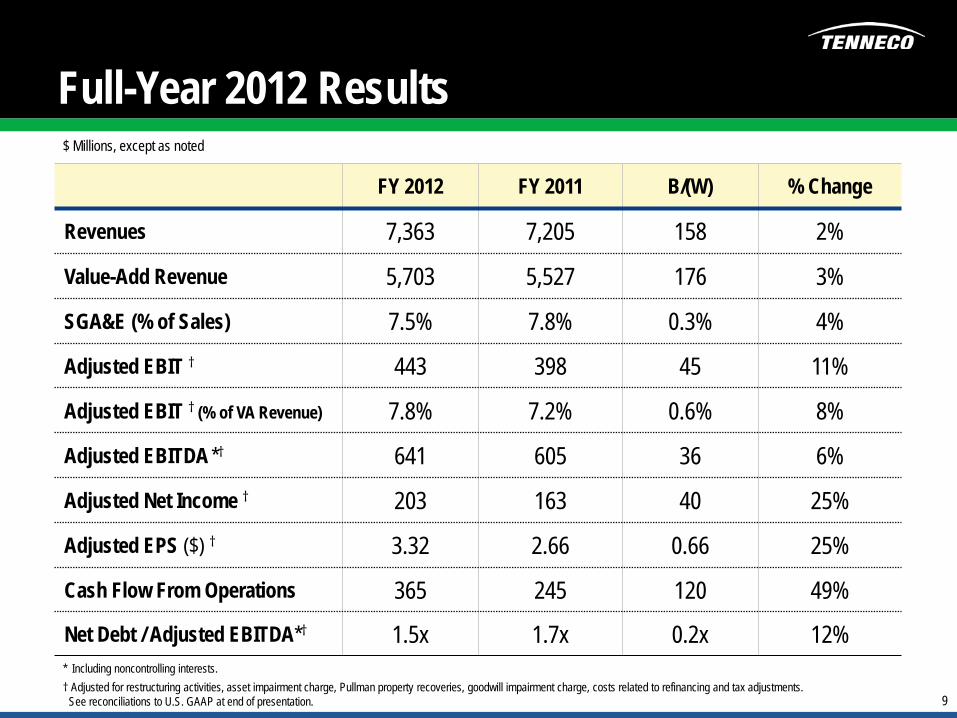

Full-Year 2012 Results

FY 2012 FY 2011 B/(W) % Change

Revenues 7,363 7,205 158 2%

Value-Add Revenue 5,703 5,527 176 3%

SGA&E (% of Sales) 7.5% 7.8% 0.3% 4%

Adjusted EBIT † 443 398 45 11%

Adjusted EBIT † (% of VA Revenue) 7.8% 7.2% 0.6% 8%

Adjusted EBITDA *† 641 605 36 6%

Adjusted Net Income † 203 163 40 25%

Adjusted EPS ($) † 3.32 2.66 0.66 25%

Cash Flow From Operations 365 245 120 49%

Net Debt / Adjusted EBITDA*† 1.5x 1.7x 0.2x 12% * Including noncontrolling interests. † Adjusted for restructuring activities, asset impairment charge, Pullman property recoveries, goodwill impairment charge, costs related to refinancing and tax adjustments. See reconciliations to U.S. GAAP at end of presentation.

$ Millions, except as noted

10

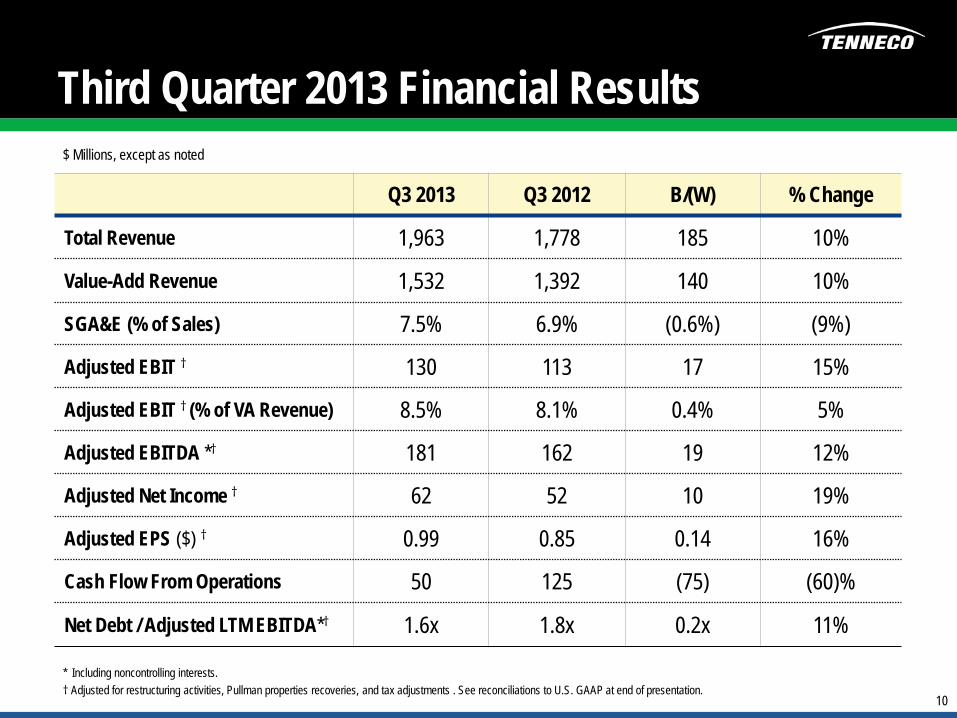

Third Quarter 2013 Financial Results $ Millions, except as noted

Q3 2013 Q3 2012 B/(W) % Change

Total Revenue 1,963 1,778 185 10%

Value-Add Revenue 1,532 1,392 140 10%

SGA&E (% of Sales) 7.5% 6.9% (0.6%) (9%)

Adjusted EBIT † 130 113 17 15%

Adjusted EBIT † (% of VA Revenue) 8.5% 8.1% 0.4% 5%

Adjusted EBITDA *† 181 162 19 12%

Adjusted Net Income † 62 52 10 19%

Adjusted EPS ($) † 0.99 0.85 0.14 16%

Cash Flow From Operations 50 125 (75) (60)%

Net Debt / Adjusted LTM EBITDA*† 1.6x 1.8x 0.2x 11%

* Including noncontrolling interests. † Adjusted for restructuring activities, Pullman properties recoveries, and tax adjustments . See reconciliations to U.S. GAAP at end of presentation.

11

Product Line Focused Strategic Imperatives STRATEGIC IMPERATIVES

A COMMON FOUNDATION

PROFITABLE GROWTH

CLEAN AIR • Global regulatory expertise • Foundation in core sciences • Total systems integration • Cost-effective global market

solutions – Light vehicle – Commercial vehicle – Large engines • China specific solutions • Large platform lifecycle services

RIDE PERFORMANCE • Product cost leadership • Superior functionality • Advanced technology • Vehicle dynamics / integrated

systems expertise • NVH solutions provider • Leading aftermarket brands

Healthier Lives Superior Driving Experience

Operational Excellence

Financial Strength

• Safety and quality • Tenneco Manufacturing System • Global business processes / capabilities • Optimized global footprint • Strategic supplier partnerships

• Earnings growth • Cash flow • EVA • Balance sheet strength

12

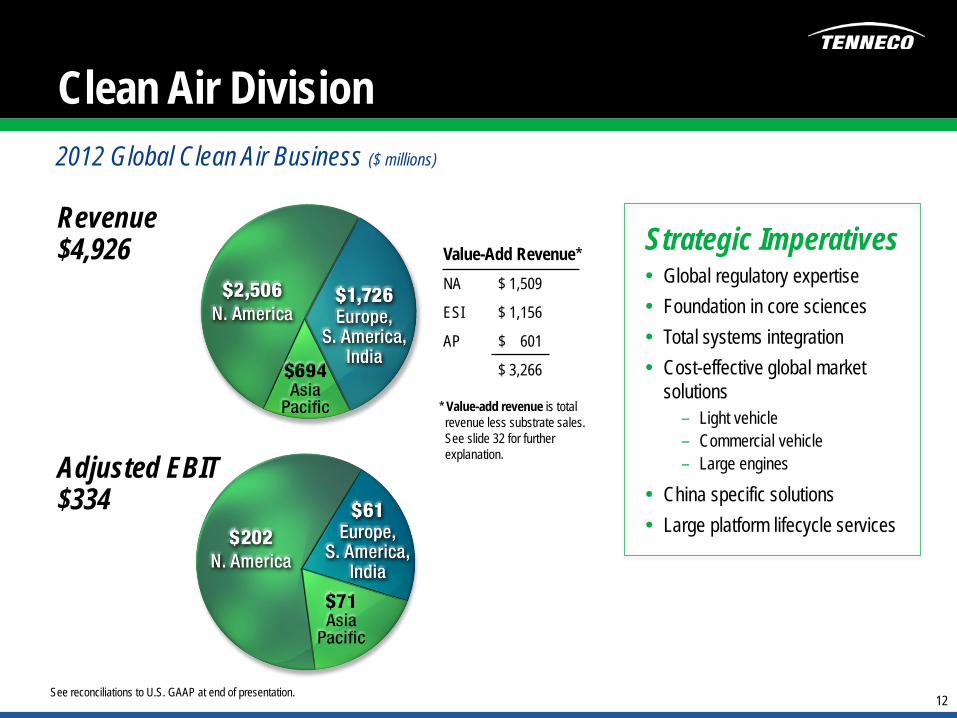

Clean Air Division 2012 Global Clean Air Business ($ millions)

Revenue $4,926

Adjusted EBIT $334

Value-Add Revenue* NA $ 1,509

ESI $ 1,156

AP $ 601

$ 3,266

Strategic Imperatives • Global regulatory expertise • Foundation in core sciences • Total systems integration • Cost-effective global market

solutions – Light vehicle – Commercial vehicle – Large engines

• China specific solutions • Large platform lifecycle services

See reconciliations to U.S. GAAP at end of presentation.

* Value-add revenue is total revenue less substrate sales. See slide 32 for further explanation.

13

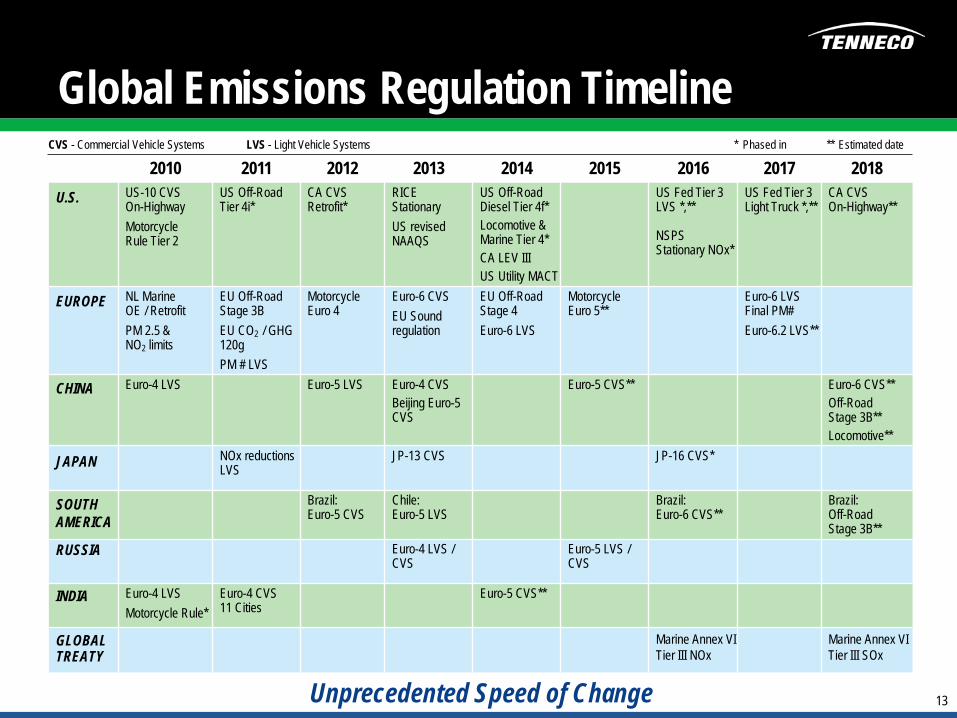

Global Emissions Regulation Timeline 2010 2011 2012 2013 2014 2015 2016 2017 2018

U.S. US-10 CVS On-Highway Motorcycle Rule Tier 2

US Off-Road Tier 4i*

CA CVS Retrofit*

RICE Stationary US revised NAAQS

US Off-Road Diesel Tier 4f* Locomotive & Marine Tier 4* CA LEV III US Utility MACT

US Fed Tier 3 LVS *,**

NSPS Stationary NOx*

US Fed Tier 3 Light Truck *,**

CA CVS On-Highway**

EUROPE NL Marine OE / Retrofit PM 2.5 & NO2 limits

EU Off-Road Stage 3B EU CO2 / GHG 120g PM # LVS

Motorcycle Euro 4

Euro-6 CVS EU Sound regulation

EU Off-Road Stage 4 Euro-6 LVS

Motorcycle Euro 5**

Euro-6 LVS Final PM# Euro-6.2 LVS**

CHINA Euro-4 LVS Euro-5 LVS Euro-4 CVS Beijing Euro-5 CVS

Euro-5 CVS** Euro-6 CVS** Off-Road Stage 3B** Locomotive**

JAPAN NOx reductions LVS

JP-13 CVS JP-16 CVS*

SOUTH AMERICA

Brazil: Euro-5 CVS

Chile: Euro-5 LVS

Brazil: Euro-6 CVS**

Brazil: Off-Road Stage 3B**

RUSSIA Euro-4 LVS / CVS

Euro-5 LVS / CVS

INDIA Euro-4 LVS Motorcycle Rule*

Euro-4 CVS 11 Cities

Euro-5 CVS**

GLOBAL TREATY

Marine Annex VI Tier III NOx

Marine Annex VI Tier III SOx

CVS - Commercial Vehicle Systems LVS - Light Vehicle Systems * Phased in ** Estimated date

Unprecedented Speed of Change

14

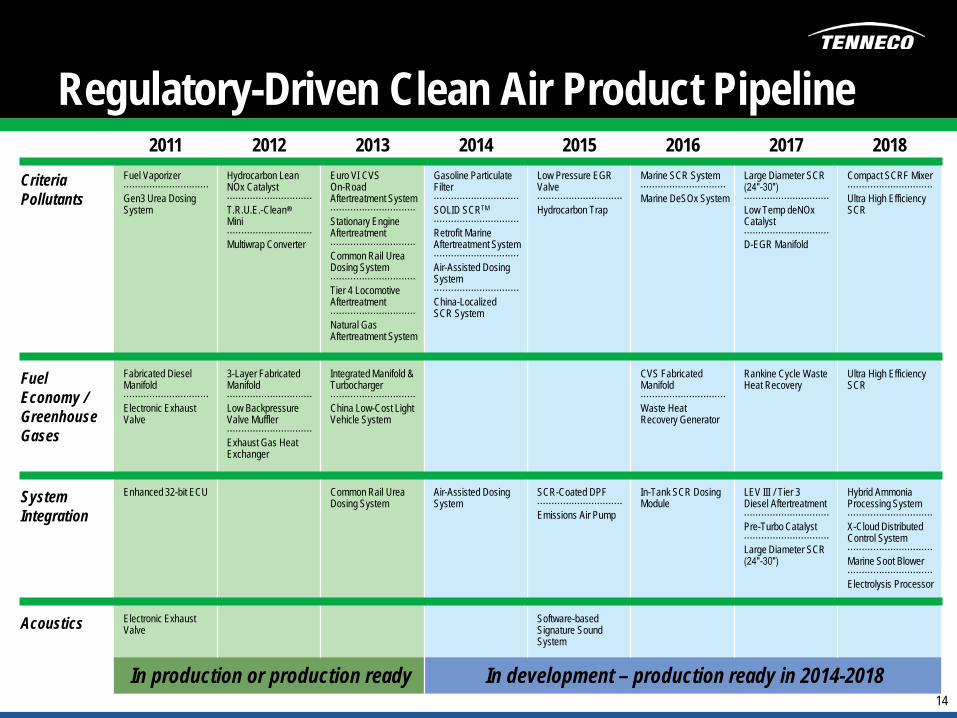

2011 2012 2013 2014 2015 2016 2017 2018

Criteria Pollutants

Fuel Vaporizer ······························ Gen3 Urea Dosing System

Hydrocarbon Lean NOx Catalyst ······························ T.R.U.E.-Clean®

Mini ······························ Multiwrap Converter

Euro VI CVS On-Road Aftertreatment System ······························ Stationary Engine Aftertreatment ······························ Common Rail Urea Dosing System ······························ Tier 4 Locomotive Aftertreatment ······························ Natural Gas Aftertreatment System

Gasoline Particulate Filter ······························ SOLID SCRTM

······························ Retrofit Marine Aftertreatment System ······························ Air-Assisted Dosing System ······························ China-Localized SCR System

Low Pressure EGR Valve ······························ Hydrocarbon Trap

Marine SCR System ······························ Marine DeSOx System

Large Diameter SCR (24″-30″) ······························ Low Temp deNOx Catalyst ······························ D-EGR Manifold

Compact SCRF Mixer ······························ Ultra High Efficiency SCR

Fuel Economy / Greenhouse Gases

Fabricated Diesel Manifold ······························ Electronic Exhaust Valve

3-Layer Fabricated Manifold ······························ Low Backpressure Valve Muffler ······························ Exhaust Gas Heat Exchanger

Integrated Manifold & Turbocharger ······························ China Low-Cost Light Vehicle System

CVS Fabricated Manifold ······························ Waste Heat Recovery Generator

Rankine Cycle Waste Heat Recovery

Ultra High Efficiency SCR

System Integration

Enhanced 32-bit ECU Common Rail Urea Dosing System

Air-Assisted Dosing System

SCR-Coated DPF ······························ Emissions Air Pump

In-Tank SCR Dosing Module

LEV III / Tier 3 Diesel Aftertreatment ······························ Pre-Turbo Catalyst ······························ Large Diameter SCR (24″-30″)

Hybrid Ammonia Processing System ······························ X-Cloud Distributed Control System ······························ Marine Soot Blower ······························ Electrolysis Processor

Acoustics Electronic Exhaust Valve

Software-based Signature Sound System

In production or production ready In development – production ready in 2014-2018

Regulatory-Driven Clean Air Product Pipeline

15

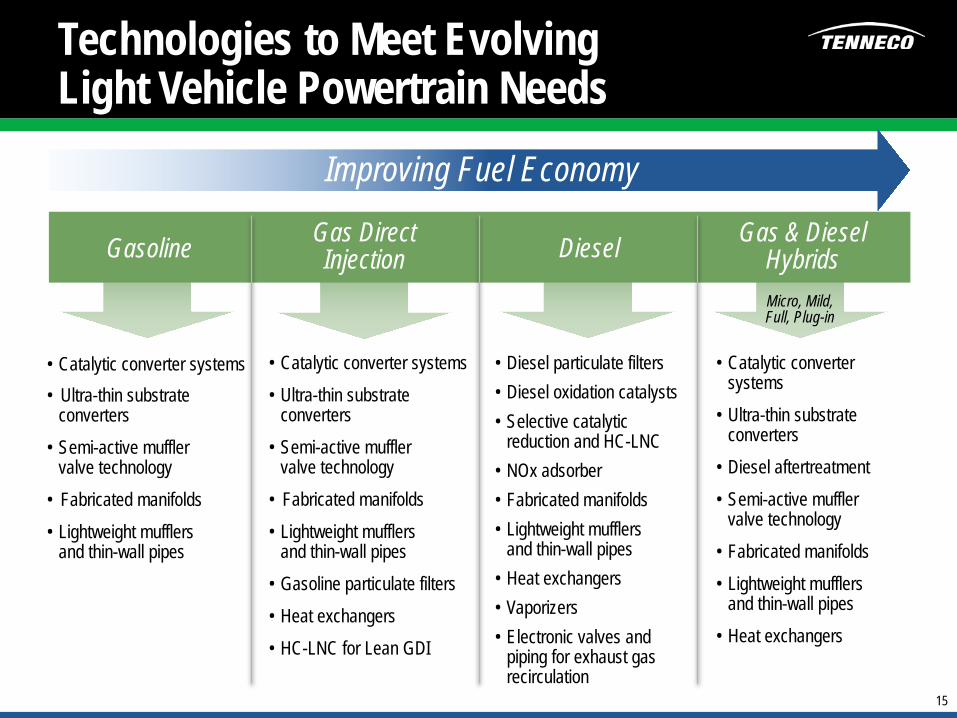

Technologies to Meet Evolving Light Vehicle Powertrain Needs

Improving Fuel Economy

Micro, Mild, Full, Plug-in

• Catalytic converter systems • Ultra-thin substrate

converters • Semi-active muffler

valve technology • Fabricated manifolds • Lightweight mufflers

and thin-wall pipes

• Catalytic converter systems • Ultra-thin substrate

converters • Semi-active muffler

valve technology • Fabricated manifolds • Lightweight mufflers

and thin-wall pipes • Gasoline particulate filters • Heat exchangers • HC-LNC for Lean GDI

• Catalytic converter systems

• Ultra-thin substrate converters

• Diesel aftertreatment • Semi-active muffler

valve technology • Fabricated manifolds • Lightweight mufflers

and thin-wall pipes • Heat exchangers

Gasoline Gas Direct Injection Diesel Gas & Diesel

Hybrids

• Diesel particulate filters • Diesel oxidation catalysts • Selective catalytic

reduction and HC-LNC • NOx adsorber • Fabricated manifolds • Lightweight mufflers

and thin-wall pipes • Heat exchangers • Vaporizers • Electronic valves and

piping for exhaust gas recirculation

16

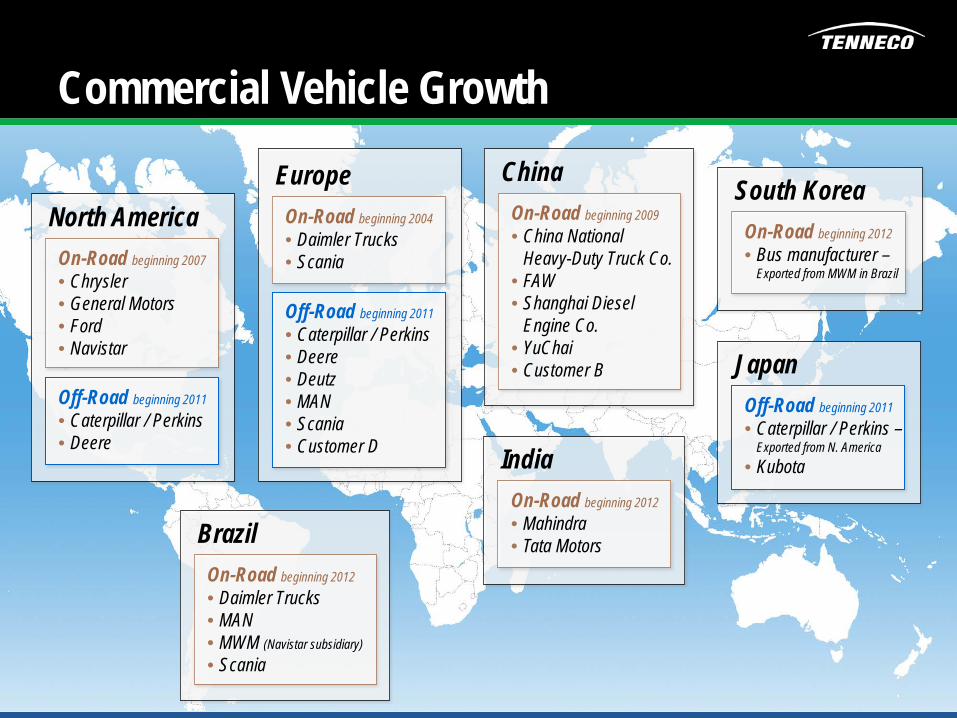

Commercial Vehicle Growth

North America On-Road beginning 2007

• Chrysler • General Motors • Ford • Navistar

Off-Road beginning 2011

• Caterpillar / Perkins • Deere

Europe On-Road beginning 2004

• Daimler Trucks • Scania

Off-Road beginning 2011

• Caterpillar / Perkins • Deere • Deutz • MAN • Scania • Customer D

Brazil On-Road beginning 2012

• Daimler Trucks • MAN • MWM (Navistar subsidiary) • Scania

India On-Road beginning 2012

• Mahindra • Tata Motors

China On-Road beginning 2009

• China National Heavy-Duty Truck Co.

• FAW • Shanghai Diesel

Engine Co. • YuChai • Customer B

South Korea On-Road beginning 2012

• Bus manufacturer –Exported from MWM in Brazil

Japan Off-Road beginning 2011

• Caterpillar / Perkins – Exported from N. America

• Kubota

17

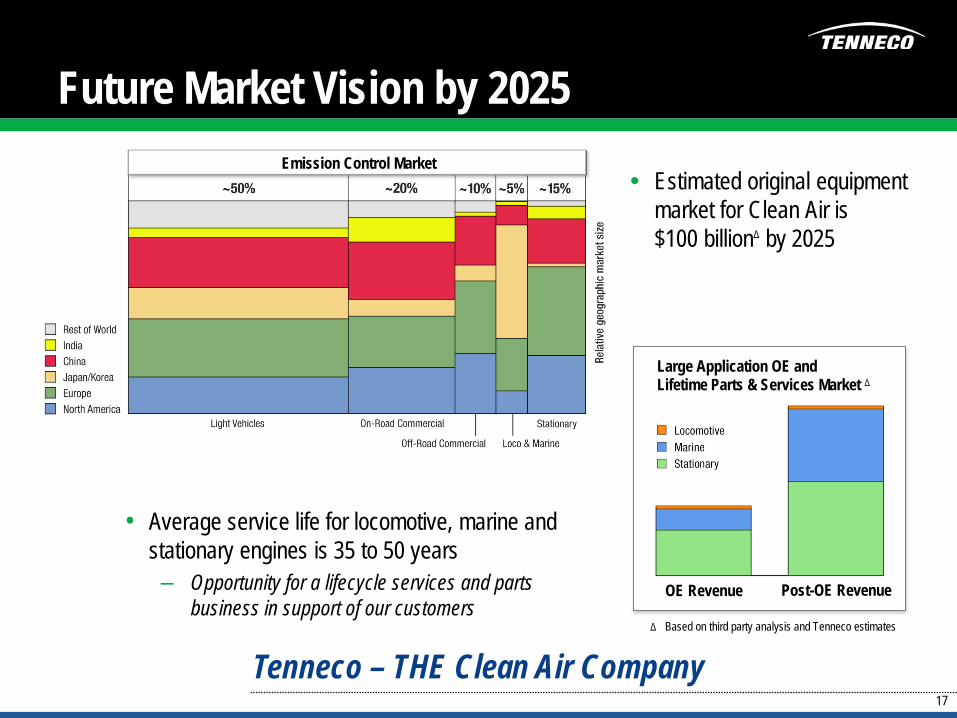

Future Market Vision by 2025

Tenneco – THE Clean Air Company

• Estimated original equipment market for Clean Air is $100 billionΔ by 2025

Δ Based on third party analysis and Tenneco estimates

Large Application OE and Lifetime Parts & Services Market Δ

OE Revenue Post-OE Revenue

Emission Control Market

• Average service life for locomotive, marine and stationary engines is 35 to 50 years – Opportunity for a lifecycle services and parts

business in support of our customers

18

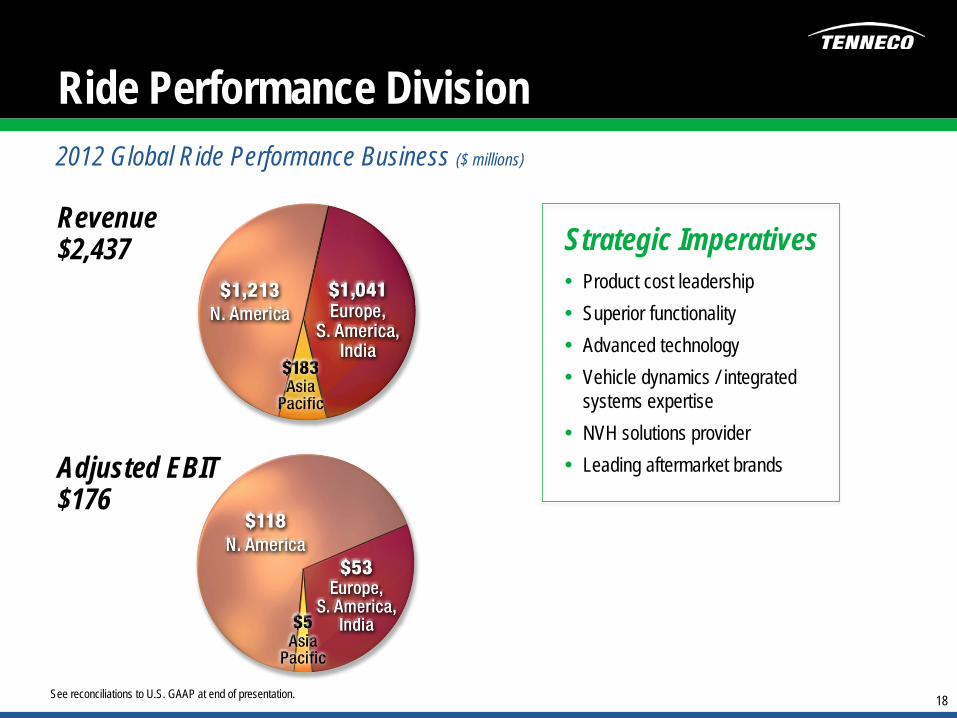

Ride Performance Division 2012 Global Ride Performance Business ($ millions)

Revenue $2,437

Adjusted EBIT $176

Strategic Imperatives • Product cost leadership • Superior functionality • Advanced technology • Vehicle dynamics / integrated

systems expertise • NVH solutions provider • Leading aftermarket brands

See reconciliations to U.S. GAAP at end of presentation.

19

Product Cost Leadership

• Customers demand highly engineered shocks and struts – Specific to platform ride and handling targets – Often more than one variant per platform

• Challenging pricing environment for highly engineered product

• Tenneco manufactures more than 80 million conventional shocks and struts annually

• Strategic focus on product cost innovation will drive significant opportunity for shareholder value creation

Strategic focus on product cost innovation

20

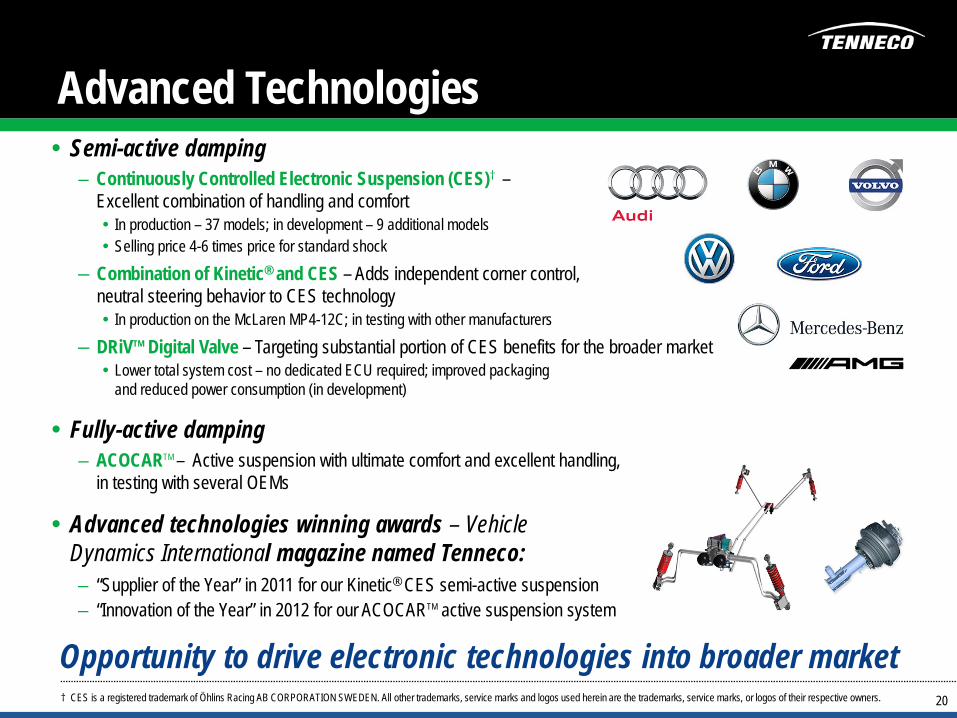

Advanced Technologies

† CES is a registered trademark of Öhlins Racing AB CORPORATION SWEDEN. All other trademarks, service marks and logos used herein are the trademarks, service marks, or logos of their respective owners.

• Semi-active damping – Continuously Controlled Electronic Suspension (CES)† –

Excellent combination of handling and comfort • In production – 37 models; in development – 9 additional models • Selling price 4-6 times price for standard shock

– Combination of Kinetic® and CES – Adds independent corner control, neutral steering behavior to CES technology • In production on the McLaren MP4-12C; in testing with other manufacturers

– DRiVTM Digital Valve – Targeting substantial portion of CES benefits for the broader market • Lower total system cost – no dedicated ECU required; improved packaging

and reduced power consumption (in development)

• Fully-active damping – ACOCARTM – Active suspension with ultimate comfort and excellent handling,

in testing with several OEMs

• Advanced technologies winning awards – Vehicle Dynamics International magazine named Tenneco: – “Supplier of the Year” in 2011 for our Kinetic® CES semi-active suspension – “Innovation of the Year” in 2012 for our ACOCARTM active suspension system

Opportunity to drive electronic technologies into broader market

21 † CES is a registered trademark of Öhlins Racing AB CORPORATION SWEDEN. All other trademarks, service marks and logos used herein are the trademarks, service marks, or logos of their respective owners.

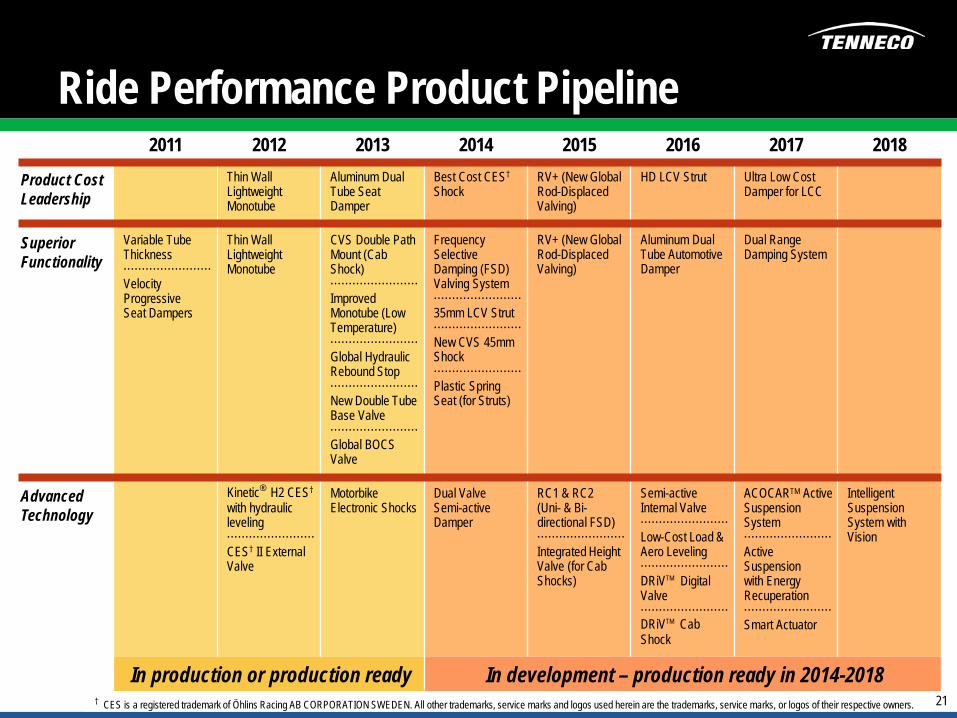

2011 2012 2013 2014 2015 2016 2017 2018

Product Cost Leadership

Thin Wall Lightweight Monotube

Aluminum Dual Tube Seat Damper

Best Cost CES† Shock

RV+ (New Global Rod-Displaced Valving)

HD LCV Strut Ultra Low Cost Damper for LCC

Superior Functionality

Variable Tube Thickness ························ Velocity Progressive Seat Dampers

Thin Wall Lightweight Monotube

CVS Double Path Mount (Cab Shock) ························ Improved Monotube (Low Temperature) ························ Global Hydraulic Rebound Stop ························ New Double Tube Base Valve ························ Global BOCS Valve

Frequency Selective Damping (FSD) Valving System ························ 35mm LCV Strut ························ New CVS 45mm Shock ························ Plastic Spring Seat (for Struts)

RV+ (New Global Rod-Displaced Valving)

Aluminum Dual Tube Automotive Damper

Dual Range Damping System

Advanced Technology

Kinetic® H2 CES† with hydraulic leveling ························ CES† II External Valve

Motorbike Electronic Shocks

Dual Valve Semi-active Damper

RC1 & RC2 (Uni- & Bi-directional FSD) ························ Integrated Height Valve (for Cab Shocks)

Semi-active Internal Valve ························ Low-Cost Load & Aero Leveling ························ DRiVTM Digital Valve ························ DRiVTM Cab Shock

ACOCARTM Active Suspension System ························ Active Suspension with Energy Recuperation ························ Smart Actuator

Intelligent Suspension System with Vision

In production or production ready In development – production ready in 2014-2018

Ride Performance Product Pipeline

22

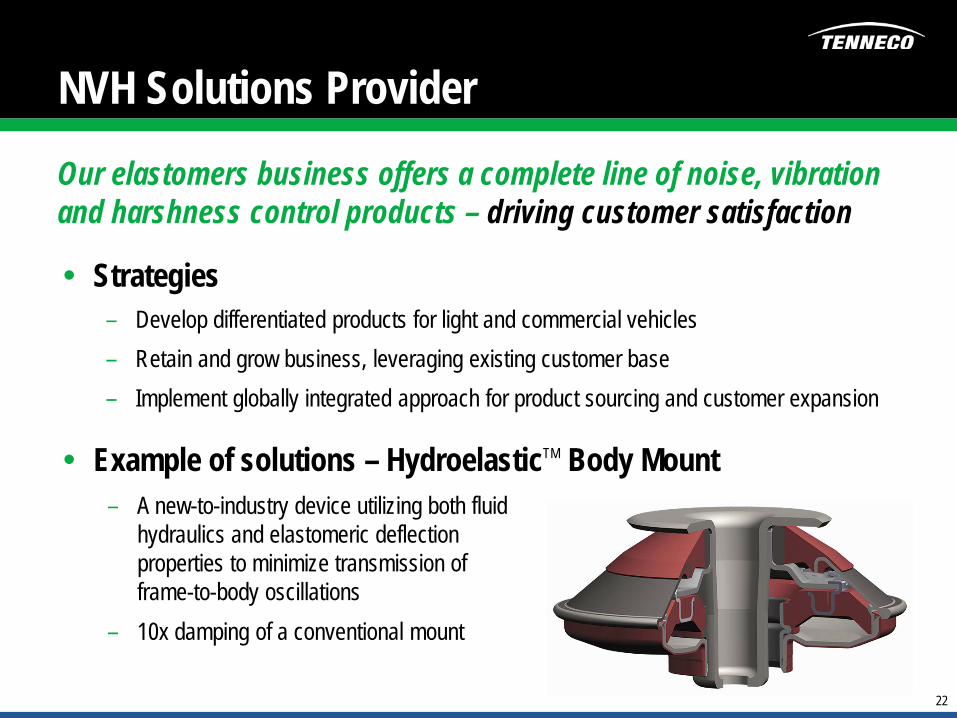

NVH Solutions Provider

Our elastomers business offers a complete line of noise, vibration and harshness control products – driving customer satisfaction

• Strategies – Develop differentiated products for light and commercial vehicles – Retain and grow business, leveraging existing customer base – Implement globally integrated approach for product sourcing and customer expansion

• Example of solutions – HydroelasticTM Body Mount – A new-to-industry device utilizing both fluid

hydraulics and elastomeric deflection properties to minimize transmission of frame-to-body oscillations

– 10x damping of a conventional mount

23

Leading Aftermarket Brands • Tenneco’s brand management, marketing and distribution expertise have

resulted in leading aftermarket Clean Air and Ride Performance market shares

• Leveraging knowledge and capability as car parc grows in new regions

#1 Clean Air #1 Ride Performance

#1 Clean Air #1 Ride Performance

#1 Ride Performance

24

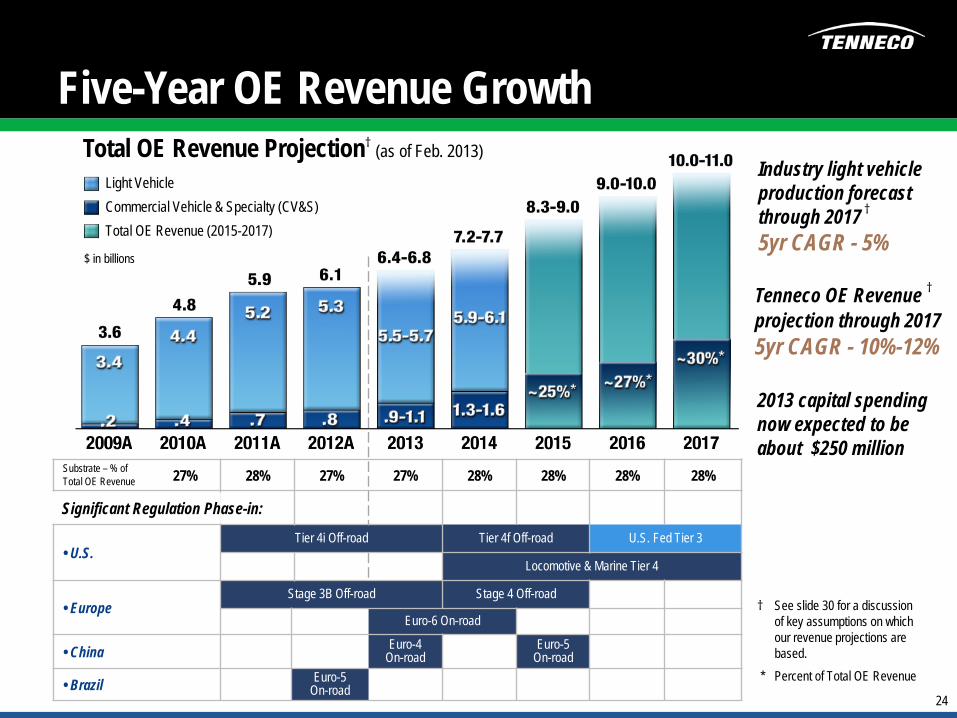

Five-Year OE Revenue Growth Total OE Revenue Projection† (as of Feb. 2013)

Light Vehicle Commercial Vehicle & Specialty (CV&S) Total OE Revenue (2015-2017)

† See slide 30 for a discussion of key assumptions on which our revenue projections are based.

* Percent of Total OE Revenue

Substrate – % of Total OE Revenue 27% 28% 27% 27% 28% 28% 28% 28%

• U.S. Tier 4i Off-road Tier 4f Off-road U.S. Fed Tier 3

Locomotive & Marine Tier 4

• Europe Stage 3B Off-road Stage 4 Off-road

Euro-6 On-road

• China Euro-4 On-road

Euro-5 On-road

• Brazil Euro-5 On-road

Significant Regulation Phase-in:

$ in billions

Industry light vehicle production forecast through 2017 † 5yr CAGR - 5%

Tenneco OE Revenue †

projection through 2017 5yr CAGR - 10%-12%

2013 capital spending now expected to be about $250 million

25

Tenneco Manufacturing System (T.M.S.) • Highly focused on global manufacturing performance

– Safety – Process driven quality – Process efficiency – Inventory management

• T.M.S. University Plants in all operating regions – Structured to drive focused development of core competencies and standardization – Leverage operational leadership and best practices

• Standardization of global processes are key to our success

– Global platform management – Industrialization of new technologies – Supplier management – Total capital efficiency

Driving Consistency Across Global Operations

Over $50 million – Process Excellence

savings in 2011 (Lean and Six Sigma)

TM

26

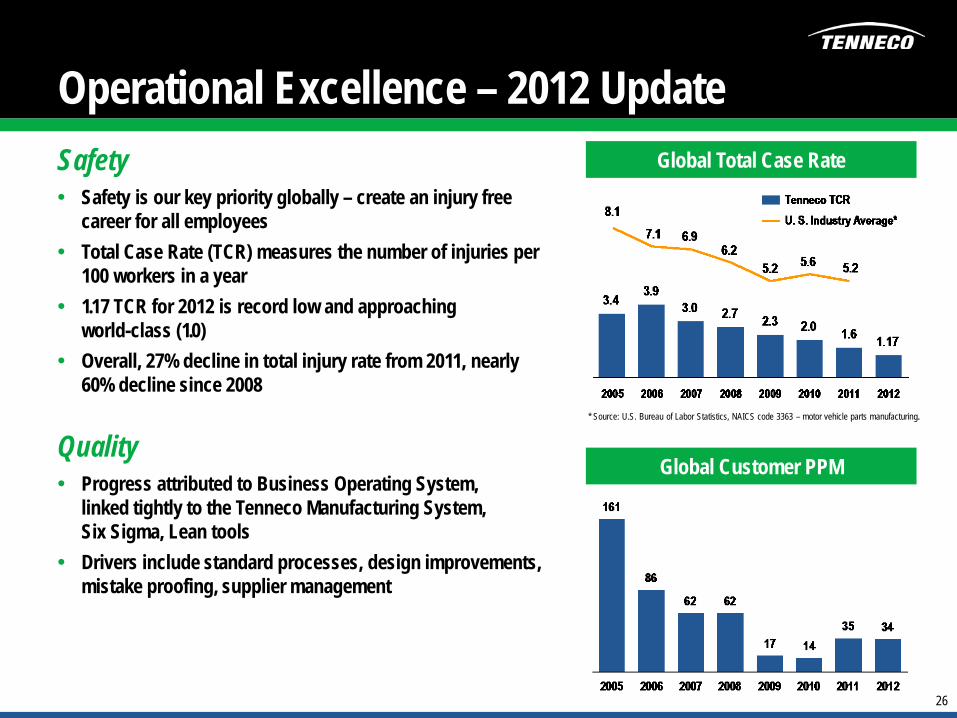

Operational Excellence – 2012 Update Safety • Safety is our key priority globally – create an injury free

career for all employees • Total Case Rate (TCR) measures the number of injuries per

100 workers in a year • 1.17 TCR for 2012 is record low and approaching

world-class (1.0) • Overall, 27% decline in total injury rate from 2011, nearly

60% decline since 2008

Quality • Progress attributed to Business Operating System,

linked tightly to the Tenneco Manufacturing System, Six Sigma, Lean tools

• Drivers include standard processes, design improvements, mistake proofing, supplier management

* Source: U.S. Bureau of Labor Statistics, NAICS code 3363 – motor vehicle parts manufacturing.

Global Total Case Rate

Global Customer PPM

27

Summary • History of growth, profitability and deleveraging • Clean Air regulations and technology drive growth opportunities

– Light vehicle content and market share growth – Content and market share growth in on-road and off-road commercial vehicles, and locomotive,

marine and stationary engines – Content and volume growth in emerging markets

• Market leading Ride Performance business – Product cost leadership leveraging scale of business – Semi-active and active damping technologies

• Sound business model with geographic, customer, end-market, product and platform balance

– Leading supplier of Clean Air and Ride Performance products and systems – No. 1 aftermarket supplier driven by leading brands

• Strong operational capabilities and manufacturing footprint • Demonstrated commitment to balance sheet strength and financial stability • Experienced management team

28

29

Tenneco’s OE Revenue Projections Tenneco’s revenue projections are as of February 2013, and the company does not otherwise intend to update these projections until February 2014. Revenue assumptions are based on projected customer production schedules, IHS Automotive January 2013 forecasts and Power Systems Research January 2013 forecasts. Our currency assumption is $1.27/€ for all years in our projection.

In addition to the information set forth on this slide and slide 25, Tenneco’s OE revenue projections are based on the type of information set forth under “Outlook” in Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as set forth in Tenneco’s Annual Report on Form 10-K for the year ended December 31, 2012. Please see that disclosure for further information. Key additional assumptions and limitations described in that disclosure include:

• Revenue projections are based on original equipment manufacturers’ programs that have been formally awarded to the company; programs where the company is highly confident that it will be awarded business based on informal customer indications consistent with past practices; Tenneco’s status as supplier for the existing program and its relationship with the customer; and the actual original equipment revenues achieved by the company for each of the last several years compared to the amount of those revenues that the company estimated it would generate at the beginning of each year.

• Revenue projections are based on the anticipated pricing of each program over its life.

• Revenue projections assume a fixed foreign currency value. This value is used to translate foreign business to the U.S. dollar.

• Revenue projections are subject to increase or decrease due to changes in customer requirements, customer and consumer preferences, the number of vehicles actually produced by our customers, pricing and foreign currency.

30

Financial Results Disclaimer • Use of Non-GAAP Financial Information In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”) included in this presentation, the company has provided information regarding certain non-GAAP financial measures. These measures include Earnings Before Interest Expense, Income Taxes, Noncontrolling Interests and Depreciation and Amortization (“EBITDA*”), Net Debt, Value-Add Revenue, Adjusted EBITDA*, Adjusted Earnings Before Interest Expense, Income Taxes and Noncontrolling Interests (“Adjusted EBIT”), Adjusted Net Income and Adjusted Earnings Per Share.

Reconciliations of these non-GAAP financial measures to the comparable GAAP measure are included in this presentation. * Including noncontrolling interests.

31

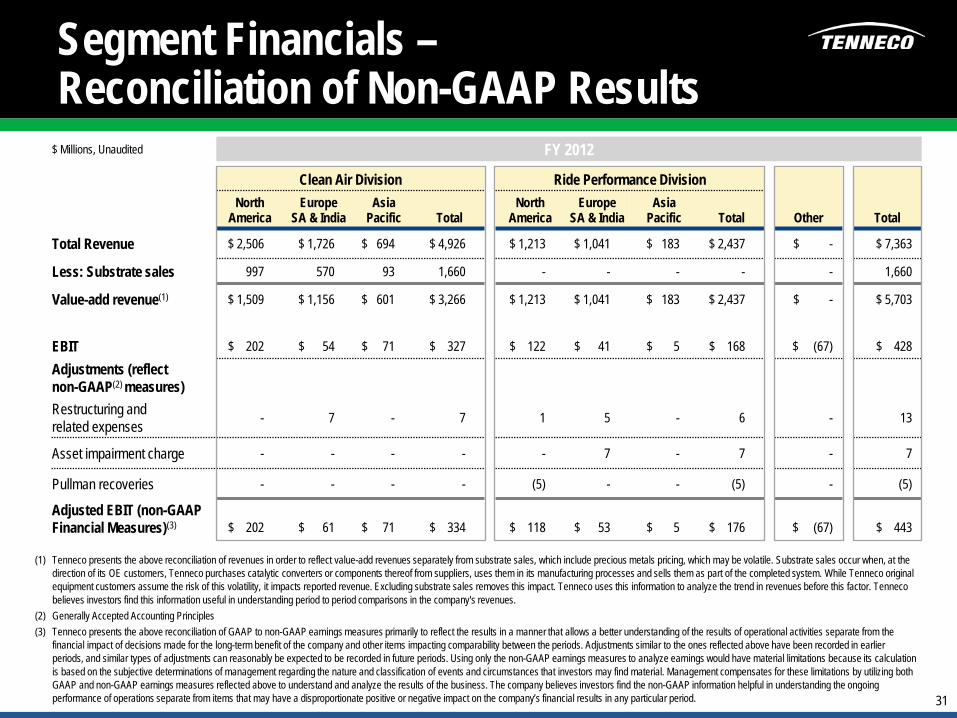

Segment Financials – Reconciliation of Non-GAAP Results

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenues separately from substrate sales, which include precious metals pricing, which may be volatile. Substrate sales occur when, at the direction of its OE customers, Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and sells them as part of the completed system. While Tenneco original equipment customers assume the risk of this volatility, it impacts reported revenue. Excluding substrate sales removes this impact. Tenneco uses this information to analyze the trend in revenues before this factor. Tenneco believes investors find this information useful in understanding period to period comparisons in the company's revenues.

(2) Generally Accepted Accounting Principles (3) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results in a manner that allows a better understanding of the results of operational activities separate from the

financial impact of decisions made for the long-term benefit of the company and other items impacting comparability between the periods. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business. The company believes investors find the non-GAAP information helpful in understanding the ongoing performance of operations separate from items that may have a disproportionate positive or negative impact on the company’s financial results in any particular period.

$ Millions, Unaudited FY 2012

Clean Air Division Ride Performance Division North

America Europe

SA & India Asia

Pacific Total North

America Europe

SA & India Asia

Pacific Total Other Total

Total Revenue $ 2,506 $ 1,726 $ 694 $ 4,926 $ 1,213 $ 1,041 $ 183 $ 2,437 $ - $ 7,363

Less: Substrate sales 997 570 93 1,660 - - - - - 1,660

Value-add revenue(1) $ 1,509 $ 1,156 $ 601 $ 3,266 $ 1,213 $ 1,041 $ 183 $ 2,437 $ - $ 5,703

EBIT $ 202 $ 54 $ 71 $ 327 $ 122 $ 41 $ 5 $ 168 $ (67) $ 428

Adjustments (reflect non-GAAP(2) measures) Restructuring and related expenses - 7 - 7 1 5 - 6 - 13

Asset impairment charge - - - - - 7 - 7 - 7

Pullman recoveries - - - - (5) - - (5) - (5)

Adjusted EBIT (non-GAAP Financial Measures)(3) $ 202 $ 61 $ 71 $ 334 $ 118 $ 53 $ 5 $ 176 $ (67) $ 443

32

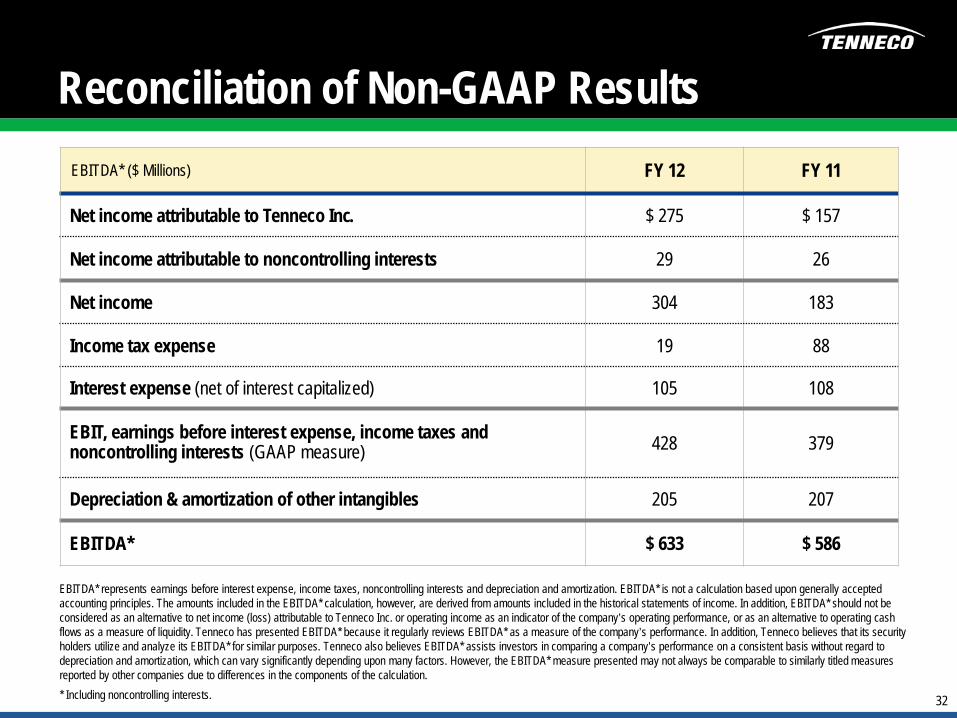

Reconciliation of Non-GAAP Results

FY 12 FY 11

Net income attributable to Tenneco Inc. $ 275 $ 157

Net income attributable to noncontrolling interests 29 26

Net income 304 183

Income tax expense 19 88

Interest expense (net of interest capitalized) 105 108

EBIT, earnings before interest expense, income taxes and noncontrolling interests (GAAP measure) 428 379

Depreciation & amortization of other intangibles 205 207

EBITDA* $ 633 $ 586

EBITDA* ($ Millions)

EBITDA* represents earnings before interest expense, income taxes, noncontrolling interests and depreciation and amortization. EBITDA* is not a calculation based upon generally accepted accounting principles. The amounts included in the EBITDA* calculation, however, are derived from amounts included in the historical statements of income. In addition, EBITDA* should not be considered as an alternative to net income (loss) attributable to Tenneco Inc. or operating income as an indicator of the company’s operating performance, or as an alternative to operating cash flows as a measure of liquidity. Tenneco has presented EBITDA* because it regularly reviews EBITDA* as a measure of the company’s performance. In addition, Tenneco believes that its security holders utilize and analyze its EBITDA* for similar purposes. Tenneco also believes EBITDA* assists investors in comparing a company’s performance on a consistent basis without regard to depreciation and amortization, which can vary significantly depending upon many factors. However, the EBITDA* measure presented may not always be comparable to similarly titled measures reported by other companies due to differences in the components of the calculation. * Including noncontrolling interests.

33

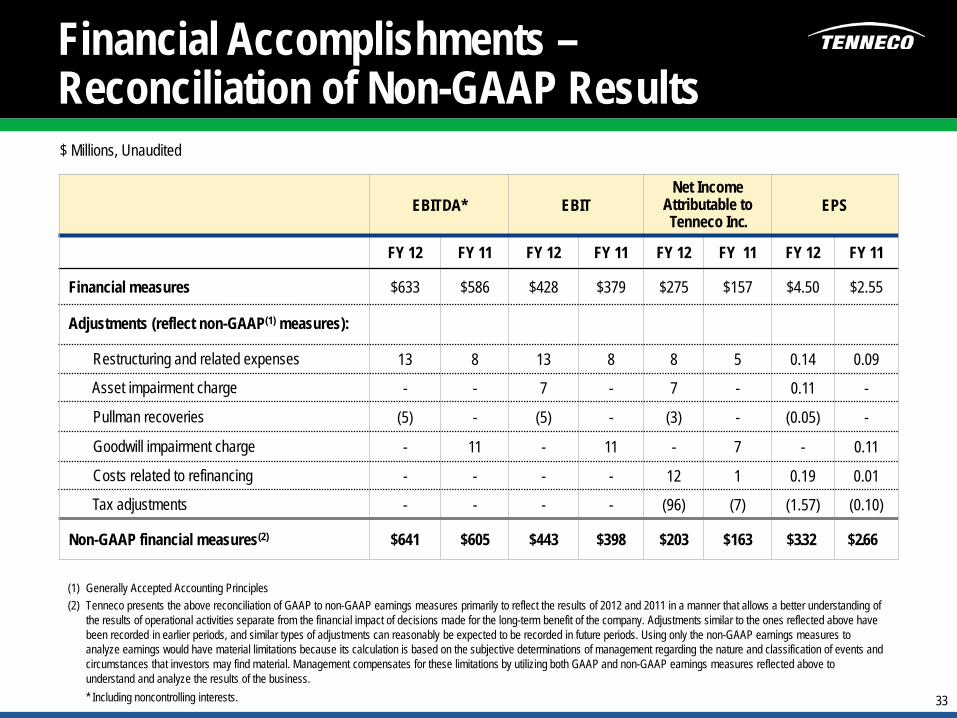

Financial Accomplishments – Reconciliation of Non-GAAP Results

EBITDA* EBIT Net Income

Attributable to Tenneco Inc.

EPS

FY 12 FY 11 FY 12 FY 11 FY 12 FY 11 FY 12 FY 11

Financial measures $633 $586 $428 $379 $275 $157 $4.50 $2.55

Adjustments (reflect non-GAAP(1) measures):

Restructuring and related expenses 13 8 13 8 8 5 0.14 0.09

Asset impairment charge - - 7 - 7 - 0.11 -

Pullman recoveries (5) - (5) - (3) - (0.05) -

Goodwill impairment charge - 11 - 11 - 7 - 0.11

Costs related to refinancing - - - - 12 1 0.19 0.01

Tax adjustments - - - - (96) (7) (1.57) (0.10)

Non-GAAP financial measures(2) $641 $605 $443 $398 $203 $163 $3.32 $2.66

(1) Generally Accepted Accounting Principles (2) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results of 2012 and 2011 in a manner that allows a better understanding of

the results of operational activities separate from the financial impact of decisions made for the long-term benefit of the company. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business.

* Including noncontrolling interests.

$ Millions, Unaudited

34

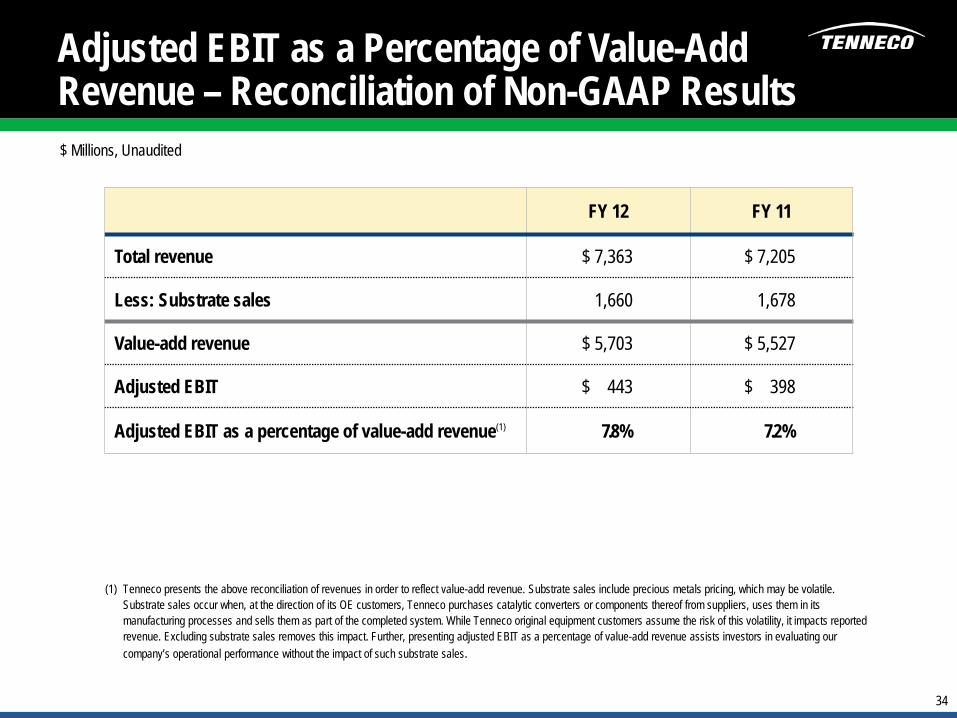

Adjusted EBIT as a Percentage of Value-Add Revenue – Reconciliation of Non-GAAP Results

FY 12 FY 11

Total revenue $ 7,363 $ 7,205

Less: Substrate sales 1,660 1,678

Value-add revenue $ 5,703 $ 5,527

Adjusted EBIT $ 443 $ 398

Adjusted EBIT as a percentage of value-add revenue(1) 7.8% 7.2%

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenue. Substrate sales include precious metals pricing, which may be volatile. Substrate sales occur when, at the direction of its OE customers, Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and sells them as part of the completed system. While Tenneco original equipment customers assume the risk of this volatility, it impacts reported revenue. Excluding substrate sales removes this impact. Further, presenting adjusted EBIT as a percentage of value-add revenue assists investors in evaluating our company’s operational performance without the impact of such substrate sales.

$ Millions, Unaudited

35

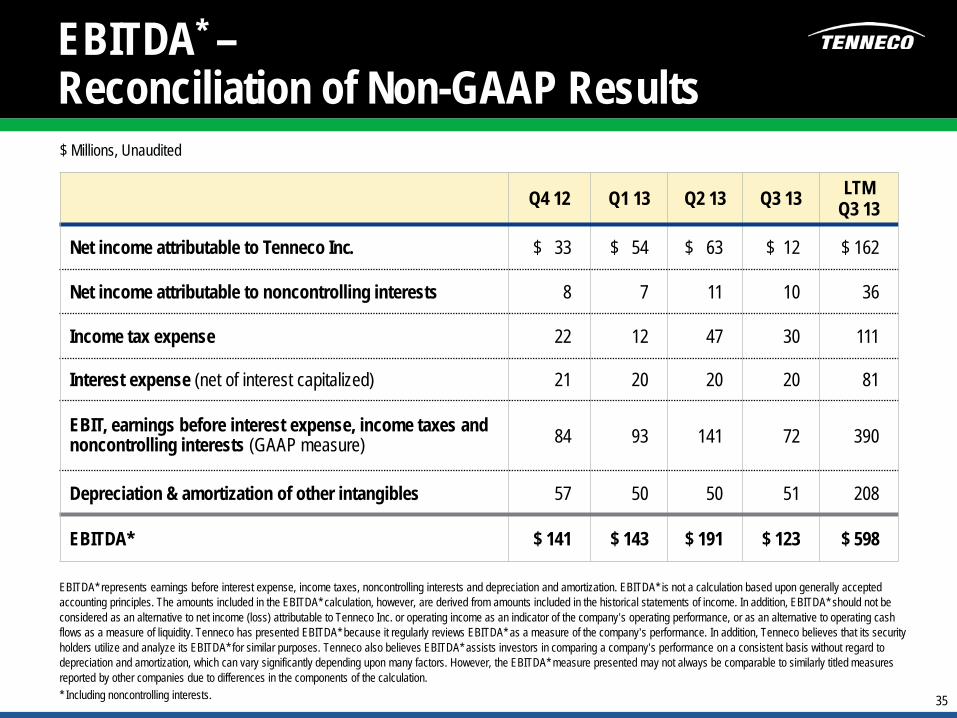

EBITDA* – Reconciliation of Non-GAAP Results

Q4 12 Q1 13 Q2 13 Q3 13 LTM Q3 13

Net income attributable to Tenneco Inc. $ 33 $ 54 $ 63 $ 12 $ 162

Net income attributable to noncontrolling interests 8 7 11 10 36

Income tax expense 22 12 47 30 111

Interest expense (net of interest capitalized) 21 20 20 20 81

EBIT, earnings before interest expense, income taxes and noncontrolling interests (GAAP measure) 84 93 141 72 390

Depreciation & amortization of other intangibles 57 50 50 51 208

EBITDA* $ 141 $ 143 $ 191 $ 123 $ 598

EBITDA* represents earnings before interest expense, income taxes, noncontrolling interests and depreciation and amortization. EBITDA* is not a calculation based upon generally accepted accounting principles. The amounts included in the EBITDA* calculation, however, are derived from amounts included in the historical statements of income. In addition, EBITDA* should not be considered as an alternative to net income (loss) attributable to Tenneco Inc. or operating income as an indicator of the company’s operating performance, or as an alternative to operating cash flows as a measure of liquidity. Tenneco has presented EBITDA* because it regularly reviews EBITDA* as a measure of the company’s performance. In addition, Tenneco believes that its security holders utilize and analyze its EBITDA* for similar purposes. Tenneco also believes EBITDA* assists investors in comparing a company’s performance on a consistent basis without regard to depreciation and amortization, which can vary significantly depending upon many factors. However, the EBITDA* measure presented may not always be comparable to similarly titled measures reported by other companies due to differences in the components of the calculation. * Including noncontrolling interests.

$ Millions, Unaudited

36

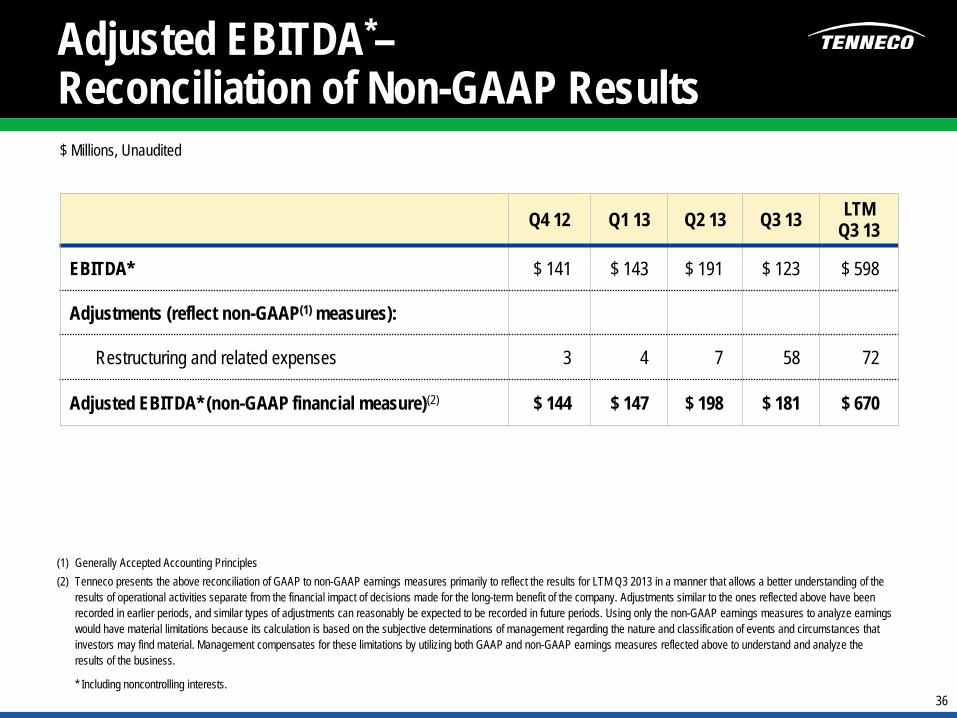

Adjusted EBITDA*– Reconciliation of Non-GAAP Results

(1) Generally Accepted Accounting Principles (2) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results for LTM Q3 2013 in a manner that allows a better understanding of the

results of operational activities separate from the financial impact of decisions made for the long-term benefit of the company. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business.

* Including noncontrolling interests.

$ Millions, Unaudited

Q4 12 Q1 13 Q2 13 Q3 13 LTM Q3 13

EBITDA* $ 141 $ 143 $ 191 $ 123 $ 598

Adjustments (reflect non-GAAP(1) measures):

Restructuring and related expenses 3 4 7 58 72

Adjusted EBITDA* (non-GAAP financial measure)(2) $ 144 $ 147 $ 198 $ 181 $ 670

37

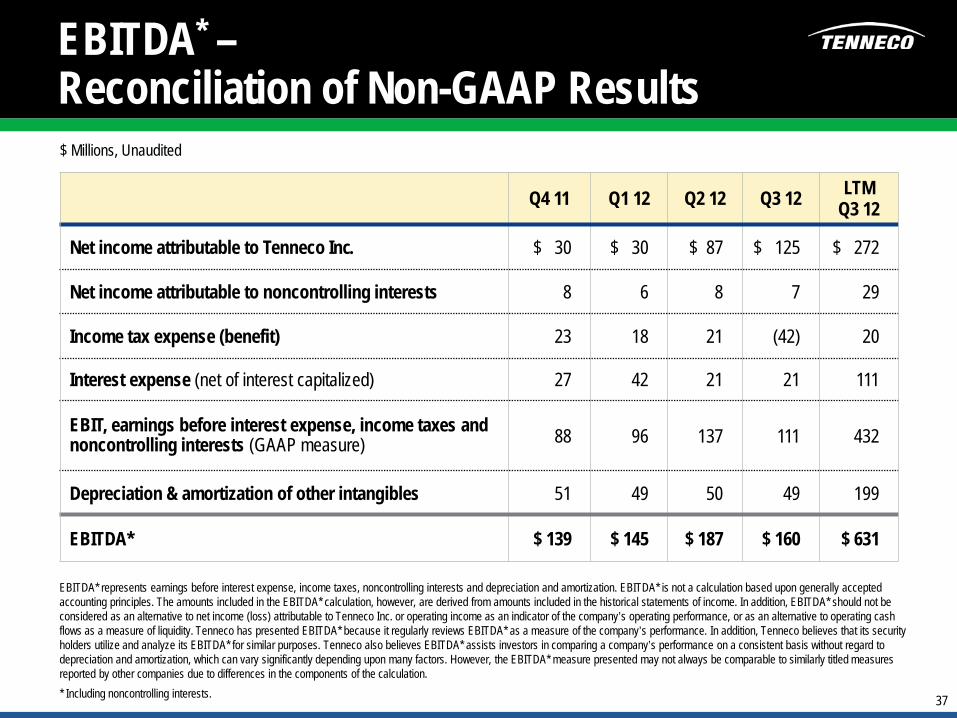

EBITDA* – Reconciliation of Non-GAAP Results

Q4 11 Q1 12 Q2 12 Q3 12 LTM Q3 12

Net income attributable to Tenneco Inc. $ 30 $ 30 $ 87 $ 125 $ 272

Net income attributable to noncontrolling interests 8 6 8 7 29

Income tax expense (benefit) 23 18 21 (42) 20

Interest expense (net of interest capitalized) 27 42 21 21 111

EBIT, earnings before interest expense, income taxes and noncontrolling interests (GAAP measure) 88 96 137 111 432

Depreciation & amortization of other intangibles 51 49 50 49 199

EBITDA* $ 139 $ 145 $ 187 $ 160 $ 631

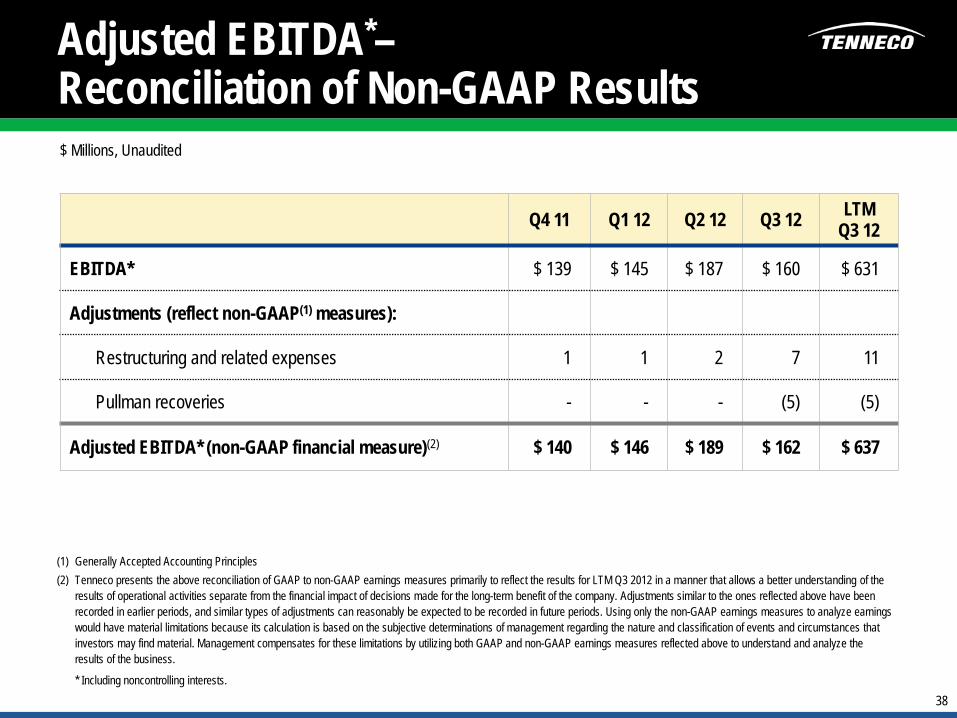

EBITDA* represents earnings before interest expense, income taxes, noncontrolling interests and depreciation and amortization. EBITDA* is not a calculation based upon generally accepted accounting principles. The amounts included in the EBITDA* calculation, however, are derived from amounts included in the historical statements of income. In addition, EBITDA* should not be considered as an alternative to net income (loss) attributable to Tenneco Inc. or operating income as an indicator of the company’s operating performance, or as an alternative to operating cash flows as a measure of liquidity. Tenneco has presented EBITDA* because it regularly reviews EBITDA* as a measure of the company’s performance. In addition, Tenneco believes that its security holders utilize and analyze its EBITDA* for similar purposes. Tenneco also believes EBITDA* assists investors in comparing a company’s performance on a consistent basis without regard to depreciation and amortization, which can vary significantly depending upon many factors. However, the EBITDA* measure presented may not always be comparable to similarly titled measures reported by other companies due to differences in the components of the calculation. * Including noncontrolling interests.

$ Millions, Unaudited

38

Adjusted EBITDA*– Reconciliation of Non-GAAP Results

(1) Generally Accepted Accounting Principles (2) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results for LTM Q3 2012 in a manner that allows a better understanding of the

results of operational activities separate from the financial impact of decisions made for the long-term benefit of the company. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business.

* Including noncontrolling interests.

$ Millions, Unaudited

Q4 11 Q1 12 Q2 12 Q3 12 LTM Q3 12

EBITDA* $ 139 $ 145 $ 187 $ 160 $ 631

Adjustments (reflect non-GAAP(1) measures):

Restructuring and related expenses 1 1 2 7 11

Pullman recoveries - - - (5) (5)

Adjusted EBITDA* (non-GAAP financial measure)(2) $ 140 $ 146 $ 189 $ 162 $ 637

39

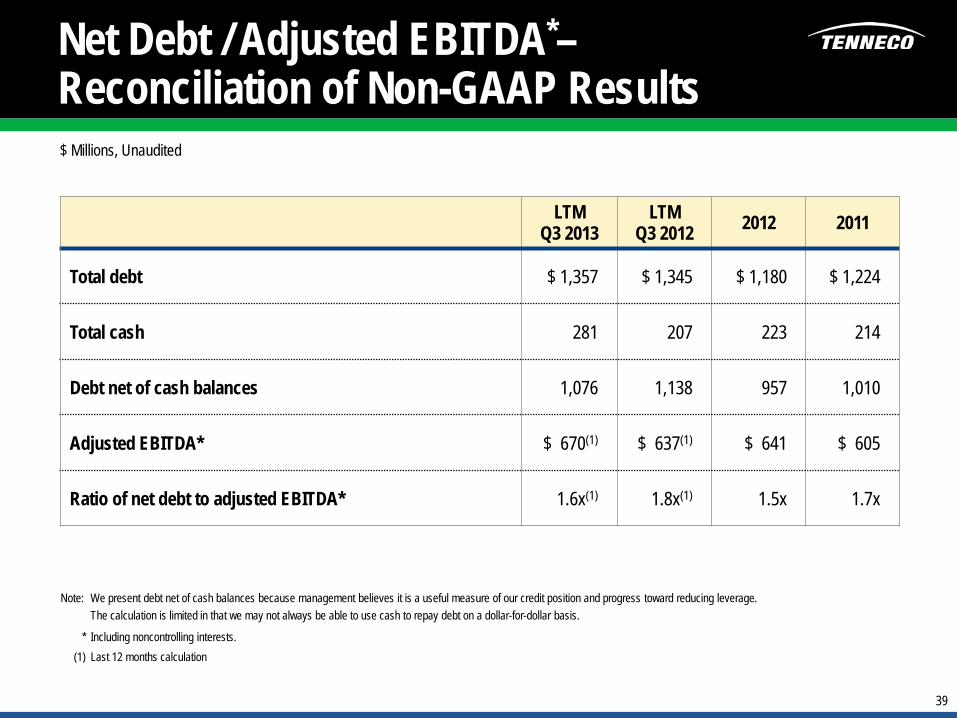

Net Debt / Adjusted EBITDA*– Reconciliation of Non-GAAP Results

Note: We present debt net of cash balances because management believes it is a useful measure of our credit position and progress toward reducing leverage. The calculation is limited in that we may not always be able to use cash to repay debt on a dollar-for-dollar basis.

* Including noncontrolling interests. (1) Last 12 months calculation

$ Millions, Unaudited

LTM Q3 2013

LTM Q3 2012 2012 2011

Total debt $ 1,357 $ 1,345 $ 1,180 $ 1,224

Total cash 281 207 223 214

Debt net of cash balances 1,076 1,138 957 1,010

Adjusted EBITDA* $ 670(1) $ 637(1) $ 641 $ 605

Ratio of net debt to adjusted EBITDA* 1.6x(1) 1.8x(1) 1.5x 1.7x

40

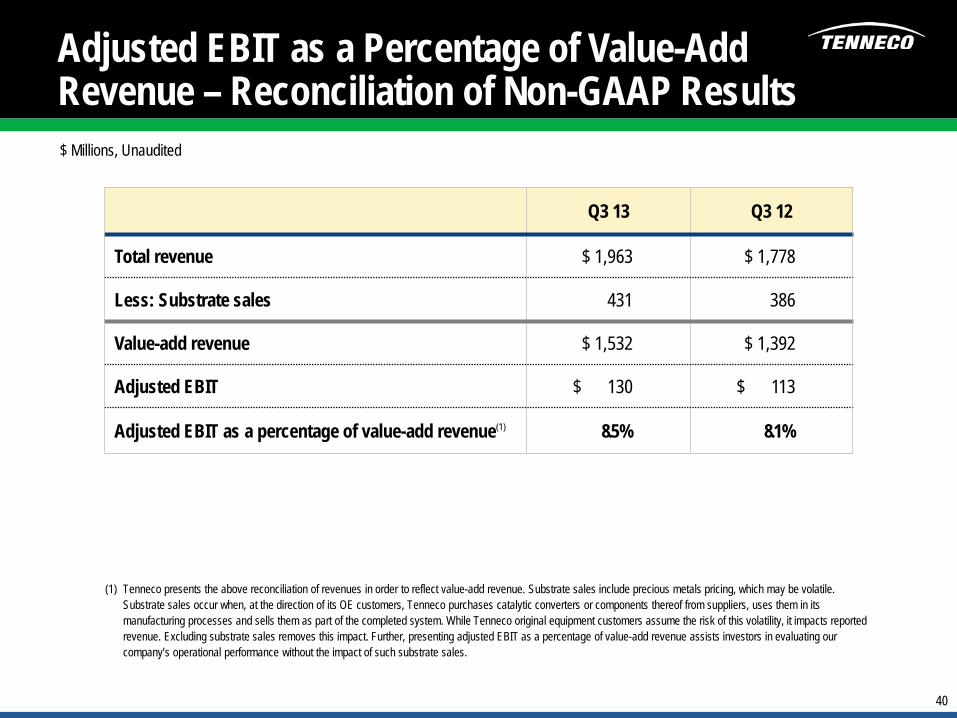

Adjusted EBIT as a Percentage of Value-Add Revenue – Reconciliation of Non-GAAP Results

Q3 13 Q3 12

Total revenue $ 1,963 $ 1,778

Less: Substrate sales 431 386

Value-add revenue $ 1,532 $ 1,392

Adjusted EBIT $ 130 $ 113

Adjusted EBIT as a percentage of value-add revenue(1) 8.5% 8.1%

(1) Tenneco presents the above reconciliation of revenues in order to reflect value-add revenue. Substrate sales include precious metals pricing, which may be volatile. Substrate sales occur when, at the direction of its OE customers, Tenneco purchases catalytic converters or components thereof from suppliers, uses them in its manufacturing processes and sells them as part of the completed system. While Tenneco original equipment customers assume the risk of this volatility, it impacts reported revenue. Excluding substrate sales removes this impact. Further, presenting adjusted EBIT as a percentage of value-add revenue assists investors in evaluating our company’s operational performance without the impact of such substrate sales.

$ Millions, Unaudited

41

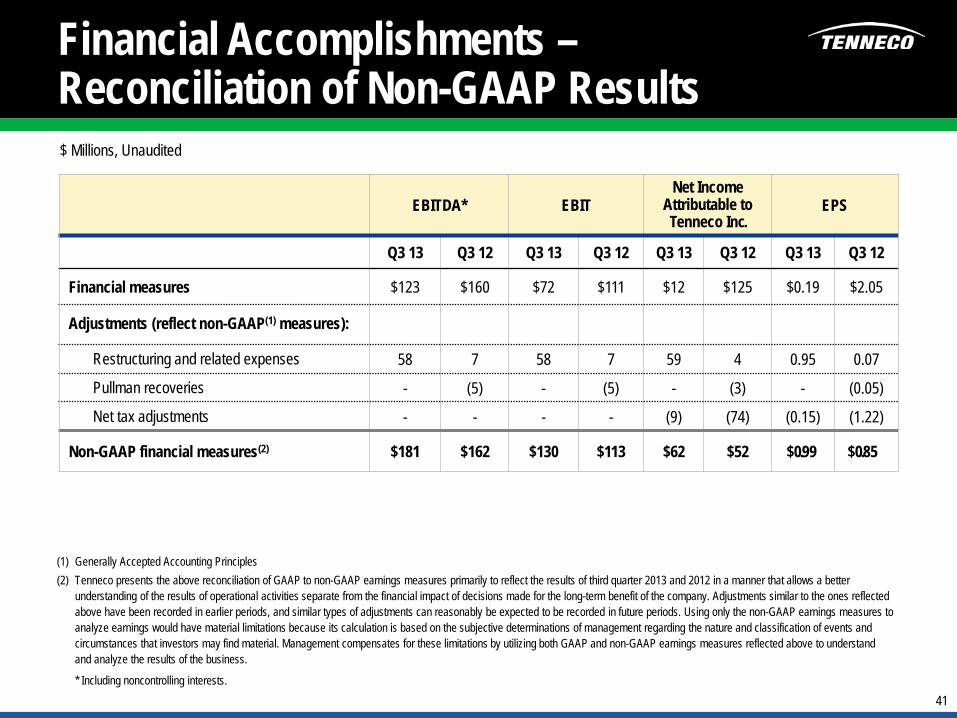

Financial Accomplishments – Reconciliation of Non-GAAP Results

EBITDA* EBIT Net Income

Attributable to Tenneco Inc.

EPS

Q3 13 Q3 12 Q3 13 Q3 12 Q3 13 Q3 12 Q3 13 Q3 12

Financial measures $123 $160 $72 $111 $12 $125 $0.19 $2.05

Adjustments (reflect non-GAAP(1) measures):

Restructuring and related expenses 58 7 58 7 59 4 0.95 0.07

Pullman recoveries - (5) - (5) - (3) - (0.05)

Net tax adjustments - - - - (9) (74) (0.15) (1.22)

Non-GAAP financial measures(2) $181 $162 $130 $113 $62 $52 $0.99 $0.85

(1) Generally Accepted Accounting Principles (2) Tenneco presents the above reconciliation of GAAP to non-GAAP earnings measures primarily to reflect the results of third quarter 2013 and 2012 in a manner that allows a better

understanding of the results of operational activities separate from the financial impact of decisions made for the long-term benefit of the company. Adjustments similar to the ones reflected above have been recorded in earlier periods, and similar types of adjustments can reasonably be expected to be recorded in future periods. Using only the non-GAAP earnings measures to analyze earnings would have material limitations because its calculation is based on the subjective determinations of management regarding the nature and classification of events and circumstances that investors may find material. Management compensates for these limitations by utilizing both GAAP and non-GAAP earnings measures reflected above to understand and analyze the results of the business.

* Including noncontrolling interests.

$ Millions, Unaudited