Embed Size (px)

Citation preview

AFRICAN DEVELOPMENT FUND

MOZAMBIQUE

ECONOMIC GOVERNANCE AND INCLUSIVE GROWTH

PROGRAM (EGIGP) – PHASE II

APPRAISAL REPORT

OSGE/SARC

November 2015

Publi

c D

iscl

osu

re A

uth

ori

zed

P

ubli

c D

iscl

osu

re A

uth

ori

zed

TABLE OF CONTENTS

CURRENCY EQUIVALENTS i

ACRONYMS AND ABBREVIATIONS ii

PROGRAM INFORMATION iii

EXECUTIVE SUMMARY FOR 2015 PROGRAM iv

RESULTS-BASED LOGICAL FRAMEWORK v

I. THE PROPOSAL .......................................................................................................... 1

II. UPDATE ON COUNTRY ELIGIBILITY .................................................................. 2

III. YEAR 2015 PROGRAM .............................................................................................. 4

3.1 Program Goal and Purpose ................................................................................................................. 4 3.2 Program Components ...................................................................................................... 4

3.3 Program Outputs and Expected Results .......................................................................... 5 3.4 Progress on Prior Actions Outlined in the Previous Operation ....................................... 6

3.5 Policy Dialogue ............................................................................................................... 7 3.6 Loan or Grant Conditions ................................................................................................ 7

3.7 Application of Good Practice Principles on Conditionality ............................................ 9

3.8 Financing Needs ............................................................................................................ 10

IV. OPERATION IMPLEMENTATION ....................................................................... 10

4.1 Beneficiaries of the Program ......................................................................................... 10

4.2 Implementation Arrangements ...................................................................................... 11 4.3 Financial Management and Disbursement and Reporting Arrangements ..................... 11

4.4 Procurement .................................................................................................................. 11

V. LEGAL DOCUMENTATION AND AUTHORITY ................................................ 12

5.1 Legal Documentation .................................................................................................... 12 5.2 Conditions Associated with Bank’s Intervention .......................................................... 12

5.3 Compliance with Bank Group Policies ......................................................................... 12

VI. RISK MANAGEMENT .............................................................................................. 12

VII. RECOMMENDATION .............................................................................................. 13

Tables

Table 1: Key Macroeconomic Indicators

Table 2: Progress on Targets from Result Based Logical Framework (RLF)

Table 3: Prior Actions for 2015 Program

Table 4: Proposed Indicative Triggers for 2016

Table 5: Financing Requirements and Sources, 2014-2016 and Bank Group Financing

Annexes

Annex I: Letter of Development Policy

Annex II: IMF Country Relations Note

i

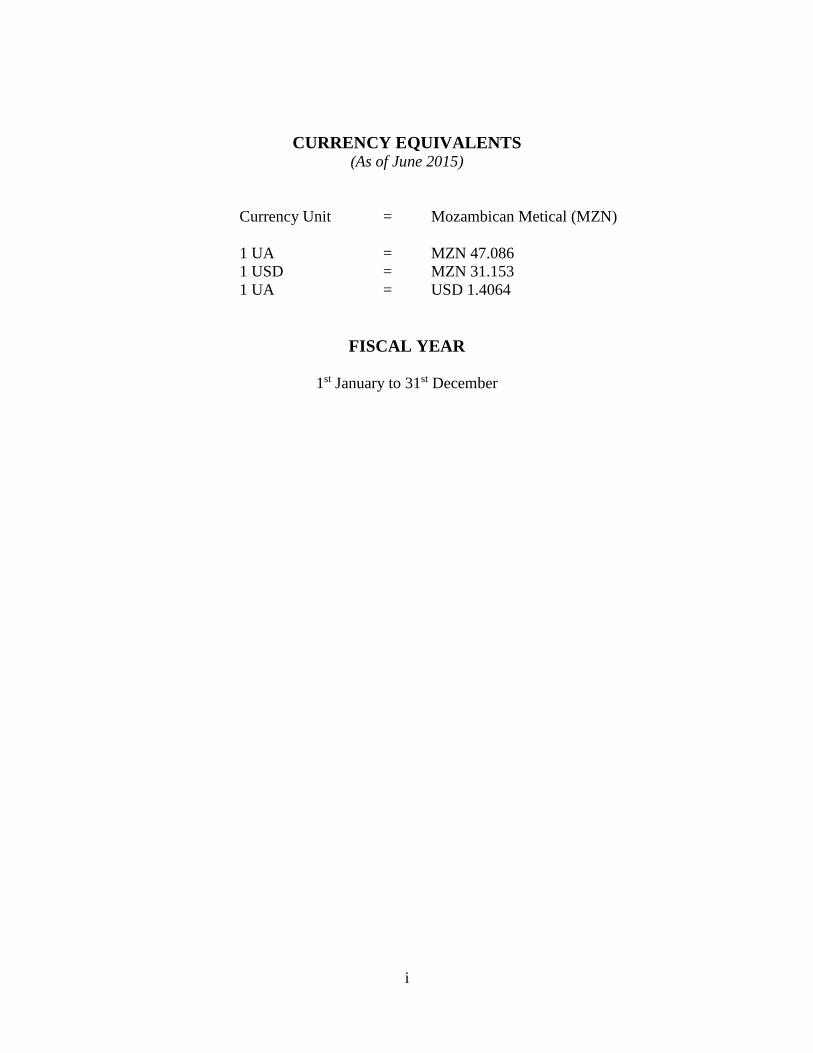

CURRENCY EQUIVALENTS (As of June 2015)

Currency Unit = Mozambican Metical (MZN)

1 UA = MZN 47.086

1 USD = MZN 31.153

1 UA = USD 1.4064

FISCAL YEAR

1st January to 31st December

ii

ACRONYMS AND ABBREVIATIONS

AfDB African Development Bank

BAU Balcão de Atendimento Único

BoM Bank of Mozambique

CPIA Country Policy and Institutional Assessment

CSO Civil society organization

CSP Country Strategy Paper

DP Development partner

DSA Debt Sustainability Analysis

DfID UK Department for International Development

EGIGP Economic Governance and Inclusive Growth Program

EITI Extractive Industries Transparency Initiative

EMAN II Private Sector Development Strategy II

EMATUM

e-SISTAFE

FDI

Empresa Moçambicana de Atum

Sistema de Administração financeira do Estado

Foreign Direct Investment

FRA Fiduciary Risk Assessment

FRELIMO

FSDS

Frente de Libertação de Moçambique

Financial Sector Development Strategy

GBS General Budget Support

GDP Gross Domestic Product

GoM Government of Mozambique

HDI Human Development Index

IGEPE

IGF

Instituto de Gestão das Participações do Estado

General Inspectorate of Finance

IIAG Ibrahim Index of African Governance

IIP Integrated Investment Program

IMF International Monetary Fund

IPSAS International Public Sector Accounting Standards

MDGs Millennium Development Goals

MIC Ministry of Industry and Commerce

MoEF Ministry of Economy and Finance

MoU Memorandum of Understanding

MSME Micro-, small and medium enterprise

MTFF Medium-Term Fiscal Framework

M&E Monitoring and evaluation

PAF Performance Assessment Framework

PARP Poverty Reduction Action Plan

PBO Program Based Operation

PEFA Public Expenditure and Financial Accountability

PFM Public Financial Management

PSD Private sector development

RBLF Results-based logical framework

RENAMO Resistência Nacional Moçambicana

SME

SAR

Small and Micro Enterprises

Streamlined Appraisal Report

SOE State-owned enterprise

TA Tribunal Administrativo (Administrative Court)

TSA Treasury Single Account

TYS

UGEA

Ten-Year Strategy

Executive Management Procurement Units

iii

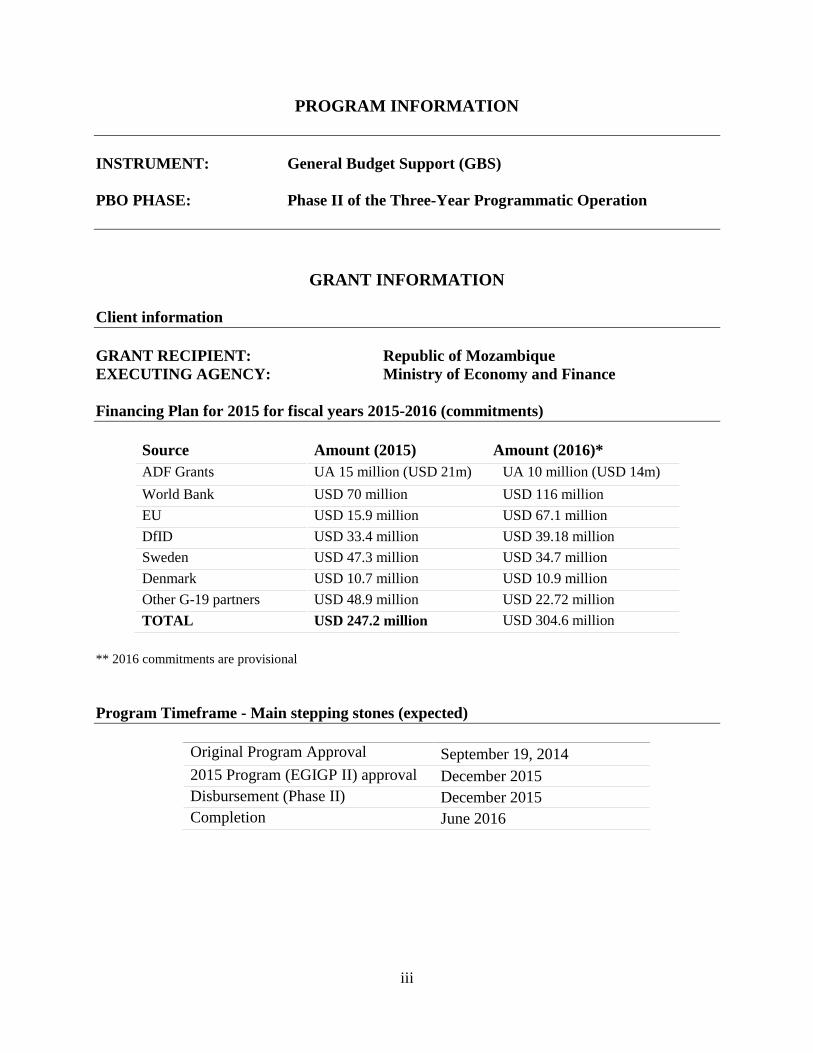

PROGRAM INFORMATION

INSTRUMENT: General Budget Support (GBS)

PBO PHASE: Phase II of the Three-Year Programmatic Operation

GRANT INFORMATION

Client information

GRANT RECIPIENT: Republic of Mozambique

EXECUTING AGENCY: Ministry of Economy and Finance

Financing Plan for 2015 for fiscal years 2015-2016 (commitments)

Source Amount (2015) Amount (2016)*

ADF Grants UA 15 million (USD 21m) UA 10 million (USD 14m)

World Bank USD 70 million USD 116 million

EU USD 15.9 million USD 67.1 million

DfID USD 33.4 million USD 39.18 million

Sweden USD 47.3 million USD 34.7 million

Denmark USD 10.7 million USD 10.9 million

Other G-19 partners USD 48.9 million USD 22.72 million

TOTAL USD 247.2 million USD 304.6 million

** 2016 commitments are provisional

Program Timeframe - Main stepping stones (expected)

Original Program Approval September 19, 2014

2015 Program (EGIGP II) approval December 2015

Disbursement (Phase II) December 2015

Completion June 2016

iv

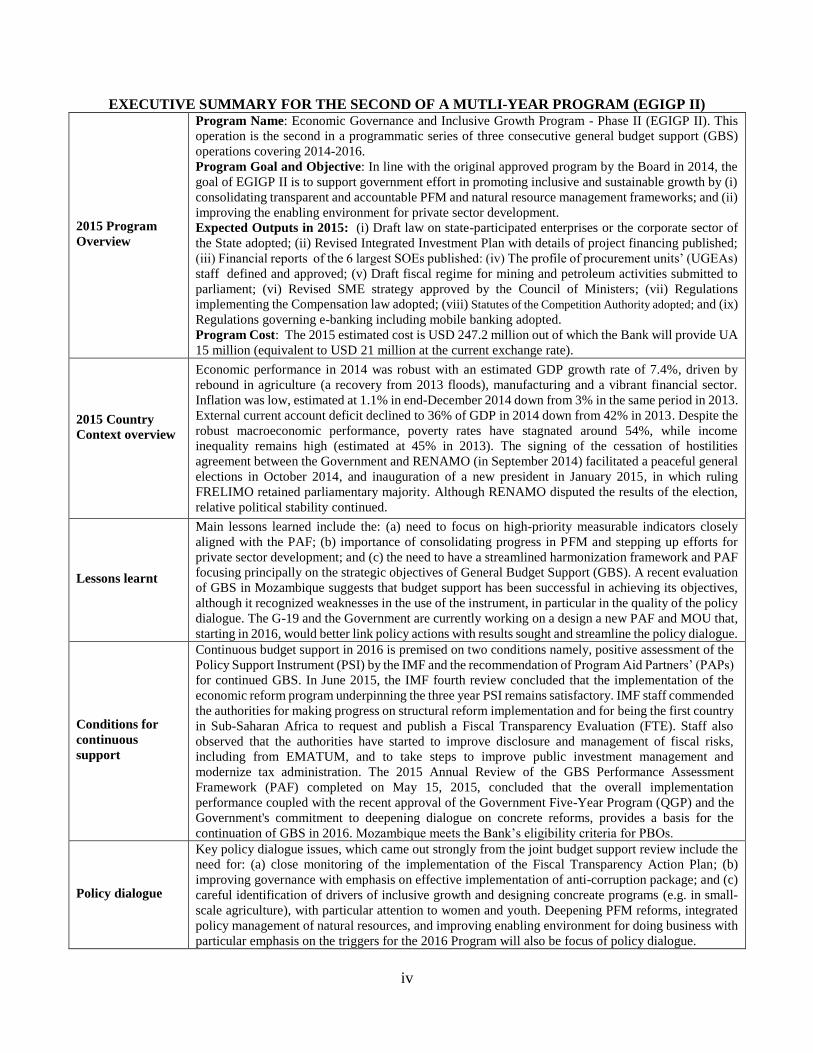

EXECUTIVE SUMMARY FOR THE SECOND OF A MUTLI-YEAR PROGRAM (EGIGP II)

2015 Program

Overview

Program Name: Economic Governance and Inclusive Growth Program - Phase II (EGIGP II). This

operation is the second in a programmatic series of three consecutive general budget support (GBS)

operations covering 2014-2016.

Program Goal and Objective: In line with the original approved program by the Board in 2014, the

goal of EGIGP II is to support government effort in promoting inclusive and sustainable growth by (i)

consolidating transparent and accountable PFM and natural resource management frameworks; and (ii)

improving the enabling environment for private sector development.

Expected Outputs in 2015: (i) Draft law on state-participated enterprises or the corporate sector of

the State adopted; (ii) Revised Integrated Investment Plan with details of project financing published;

(iii) Financial reports of the 6 largest SOEs published: (iv) The profile of procurement units’ (UGEAs)

staff defined and approved; (v) Draft fiscal regime for mining and petroleum activities submitted to

parliament; (vi) Revised SME strategy approved by the Council of Ministers; (vii) Regulations

implementing the Compensation law adopted; (viii) Statutes of the Competition Authority adopted; and (ix)

Regulations governing e-banking including mobile banking adopted.

Program Cost: The 2015 estimated cost is USD 247.2 million out of which the Bank will provide UA

15 million (equivalent to USD 21 million at the current exchange rate).

2015 Country

Context overview

Economic performance in 2014 was robust with an estimated GDP growth rate of 7.4%, driven by

rebound in agriculture (a recovery from 2013 floods), manufacturing and a vibrant financial sector.

Inflation was low, estimated at 1.1% in end-December 2014 down from 3% in the same period in 2013.

External current account deficit declined to 36% of GDP in 2014 down from 42% in 2013. Despite the

robust macroeconomic performance, poverty rates have stagnated around 54%, while income

inequality remains high (estimated at 45% in 2013). The signing of the cessation of hostilities

agreement between the Government and RENAMO (in September 2014) facilitated a peaceful general

elections in October 2014, and inauguration of a new president in January 2015, in which ruling

FRELIMO retained parliamentary majority. Although RENAMO disputed the results of the election,

relative political stability continued.

Lessons learnt

Main lessons learned include the: (a) need to focus on high-priority measurable indicators closely

aligned with the PAF; (b) importance of consolidating progress in PFM and stepping up efforts for

private sector development; and (c) the need to have a streamlined harmonization framework and PAF

focusing principally on the strategic objectives of General Budget Support (GBS). A recent evaluation

of GBS in Mozambique suggests that budget support has been successful in achieving its objectives,

although it recognized weaknesses in the use of the instrument, in particular in the quality of the policy

dialogue. The G-19 and the Government are currently working on a design a new PAF and MOU that,

starting in 2016, would better link policy actions with results sought and streamline the policy dialogue.

Conditions for

continuous

support

Continuous budget support in 2016 is premised on two conditions namely, positive assessment of the

Policy Support Instrument (PSI) by the IMF and the recommendation of Program Aid Partners’ (PAPs)

for continued GBS. In June 2015, the IMF fourth review concluded that the implementation of the

economic reform program underpinning the three year PSI remains satisfactory. IMF staff commended

the authorities for making progress on structural reform implementation and for being the first country

in Sub-Saharan Africa to request and publish a Fiscal Transparency Evaluation (FTE). Staff also

observed that the authorities have started to improve disclosure and management of fiscal risks,

including from EMATUM, and to take steps to improve public investment management and

modernize tax administration. The 2015 Annual Review of the GBS Performance Assessment

Framework (PAF) completed on May 15, 2015, concluded that the overall implementation

performance coupled with the recent approval of the Government Five-Year Program (QGP) and the

Government's commitment to deepening dialogue on concrete reforms, provides a basis for the

continuation of GBS in 2016. Mozambique meets the Bank’s eligibility criteria for PBOs.

Policy dialogue

Key policy dialogue issues, which came out strongly from the joint budget support review include the

need for: (a) close monitoring of the implementation of the Fiscal Transparency Action Plan; (b)

improving governance with emphasis on effective implementation of anti-corruption package; and (c)

careful identification of drivers of inclusive growth and designing concreate programs (e.g. in small-

scale agriculture), with particular attention to women and youth. Deepening PFM reforms, integrated

policy management of natural resources, and improving enabling environment for doing business with

particular emphasis on the triggers for the 2016 Program will also be focus of policy dialogue.

v

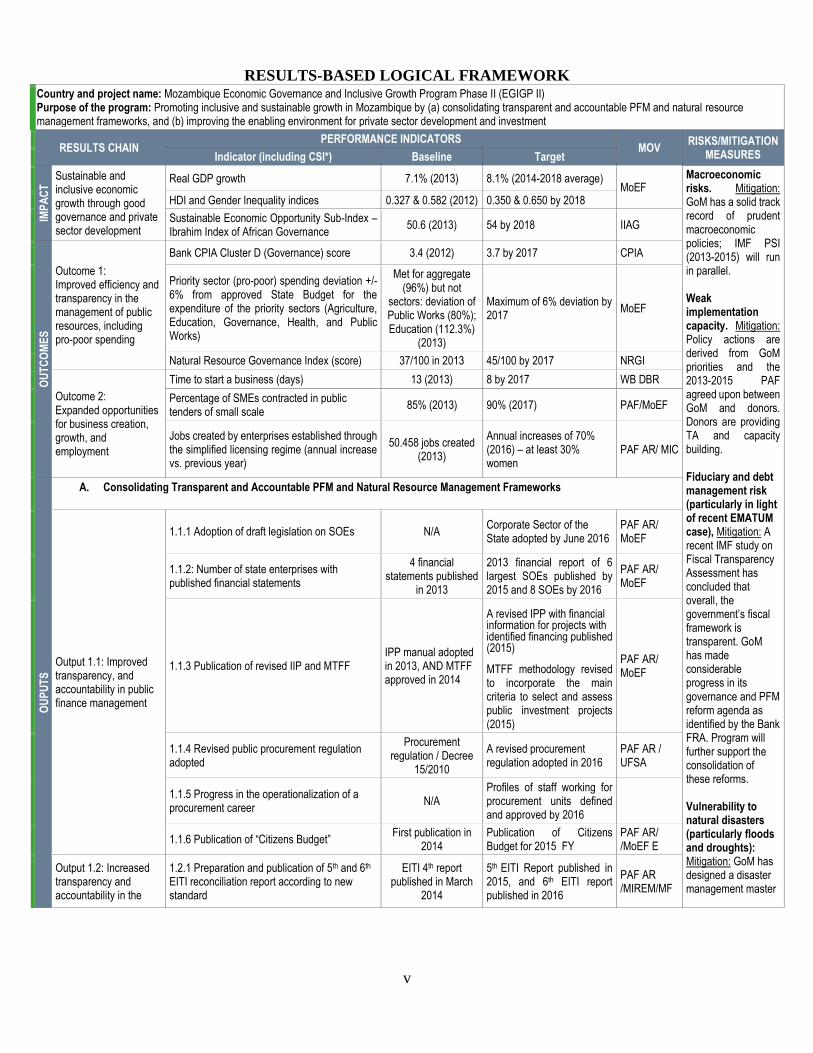

RESULTS-BASED LOGICAL FRAMEWORK Country and project name: Mozambique Economic Governance and Inclusive Growth Program Phase II (EGIGP II) Purpose of the program: Promoting inclusive and sustainable growth in Mozambique by (a) consolidating transparent and accountable PFM and natural resource management frameworks, and (b) improving the enabling environment for private sector development and investment

RESULTS CHAIN PERFORMANCE INDICATORS

MOV RISKS/MITIGATION

MEASURES Indicator (including CSI*) Baseline Target

IMP

AC

T Sustainable and

inclusive economic growth through good governance and private sector development

Real GDP growth 7.1% (2013) 8.1% (2014-2018 average) MoEF

Macroeconomic risks. Mitigation: GoM has a solid track record of prudent macroeconomic policies; IMF PSI (2013-2015) will run in parallel. Weak implementation capacity. Mitigation: Policy actions are derived from GoM priorities and the 2013-2015 PAF agreed upon between GoM and donors. Donors are providing TA and capacity building. Fiduciary and debt management risk (particularly in light of recent EMATUM case), Mitigation: A recent IMF study on Fiscal Transparency Assessment has concluded that overall, the government’s fiscal framework is transparent. GoM has made considerable progress in its governance and PFM reform agenda as identified by the Bank FRA. Program will further support the consolidation of these reforms. Vulnerability to natural disasters (particularly floods and droughts): Mitigation: GoM has designed a disaster management master

HDI and Gender Inequality indices 0.327 & 0.582 (2012) 0.350 & 0.650 by 2018

Sustainable Economic Opportunity Sub-Index – Ibrahim Index of African Governance

50.6 (2013) 54 by 2018 IIAG

OU

TC

OM

ES

Outcome 1: Improved efficiency and transparency in the management of public resources, including pro-poor spending

Bank CPIA Cluster D (Governance) score 3.4 (2012) 3.7 by 2017 CPIA

Priority sector (pro-poor) spending deviation +/- 6% from approved State Budget for the expenditure of the priority sectors (Agriculture, Education, Governance, Health, and Public Works)

Met for aggregate (96%) but not

sectors: deviation of Public Works (80%); Education (112.3%)

(2013)

Maximum of 6% deviation by 2017

MoEF

Natural Resource Governance Index (score) 37/100 in 2013 45/100 by 2017 NRGI

Outcome 2: Expanded opportunities for business creation, growth, and employment

Time to start a business (days) 13 (2013) 8 by 2017 WB DBR

Percentage of SMEs contracted in public tenders of small scale

85% (2013) 90% (2017) PAF/MoEF

Jobs created by enterprises established through the simplified licensing regime (annual increase vs. previous year)

50.458 jobs created (2013)

Annual increases of 70% (2016) – at least 30% women

PAF AR/ MIC

OU

PU

TS

A. Consolidating Transparent and Accountable PFM and Natural Resource Management Frameworks

Output 1.1: Improved transparency, and accountability in public finance management

1.1.1 Adoption of draft legislation on SOEs N/A Corporate Sector of the State adopted by June 2016

PAF AR/ MoEF

1.1.2: Number of state enterprises with published financial statements

4 financial statements published

in 2013

2013 financial report of 6 largest SOEs published by 2015 and 8 SOEs by 2016

PAF AR/ MoEF

1.1.3 Publication of revised IIP and MTFF IPP manual adopted in 2013, AND MTFF approved in 2014

A revised IPP with financial information for projects with identified financing published (2015)

MTFF methodology revised to incorporate the main criteria to select and assess public investment projects (2015)

PAF AR/ MoEF

1.1.4 Revised public procurement regulation adopted

Procurement regulation / Decree

15/2010

A revised procurement regulation adopted in 2016

PAF AR / UFSA

1.1.5 Progress in the operationalization of a procurement career

N/A Profiles of staff working for procurement units defined and approved by 2016

1.1.6 Publication of “Citizens Budget” First publication in

2014 Publication of Citizens Budget for 2015 FY

PAF AR/ /MoEF E

Output 1.2: Increased transparency and accountability in the

1.2.1 Preparation and publication of 5th and 6th EITI reconciliation report according to new standard

EITI 4th report published in March

2014

5th EITI Report published in 2015, and 6th EITI report published in 2016

PAF AR /MIREM/MF

vi

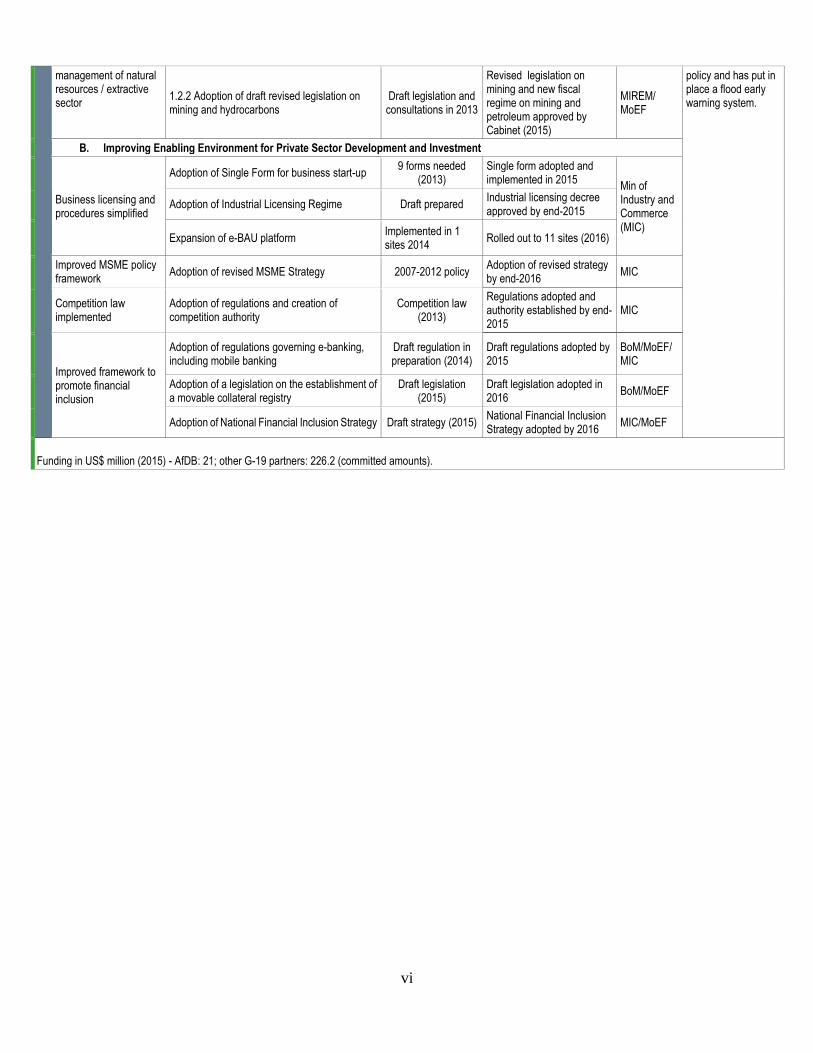

management of natural resources / extractive sector

1.2.2 Adoption of draft revised legislation on mining and hydrocarbons

Draft legislation and consultations in 2013

Revised legislation on mining and new fiscal regime on mining and petroleum approved by Cabinet (2015)

MIREM/ MoEF

policy and has put in place a flood early warning system.

B. Improving Enabling Environment for Private Sector Development and Investment

Business licensing and procedures simplified

Adoption of Single Form for business start-up 9 forms needed

(2013) Single form adopted and implemented in 2015

Min of Industry and Commerce (MIC)

Adoption of Industrial Licensing Regime Draft prepared Industrial licensing decree approved by end-2015

Expansion of e-BAU platform Implemented in 1 sites 2014

Rolled out to 11 sites (2016)

Improved MSME policy framework

Adoption of revised MSME Strategy 2007-2012 policy Adoption of revised strategy by end-2016

MIC

Competition law implemented

Adoption of regulations and creation of competition authority

Competition law (2013)

Regulations adopted and authority established by end-2015

MIC

Improved framework to promote financial inclusion

Adoption of regulations governing e-banking, including mobile banking

Draft regulation in preparation (2014)

Draft regulations adopted by 2015

BoM/MoEF/ MIC

Adoption of a legislation on the establishment of a movable collateral registry

Draft legislation (2015)

Draft legislation adopted in 2016

BoM/MoEF

Adoption of National Financial Inclusion Strategy Draft strategy (2015) National Financial Inclusion Strategy adopted by 2016

MIC/MoEF

Funding in US$ million (2015) - AfDB: 21; other G-19 partners: 226.2 (committed amounts).

1

REPORT AND RECOMMENDATION BY MANAGEMENT TO THE BOARD OF

DIRECTORS ON A PROPOSED GRANT TO MOZAMBIQUE FOR THE ECONOMIC

GOVERNANCE AND INCLUSIVE GROWTH PROGRAM PHASE II (EGIGP II)

I. INTRODUCTION: THE PROPOSAL

1.1 Management submits this report and recommendation for a proposed ADF grant of

UA 15 million to finance the second phase of the Mozambique Economic Governance and

Inclusive Growth Program (EGIGP II). The EGIGP was designed as a programmatic series of

three consecutive general budget support (GBS) operations covering fiscal years 2014, 2015, and

2016. All the operations in the series are single tranche. Consistent with the Bank’s Policy on

Program-Based Operations (PBOs), the disbursement of the proceeds of the first phase1 in the

programmatic series (UA19.335 million) was approved and disbursed against the achievement of a

set of prior actions for 2014. In addition, the EGIGP anticipated indicative triggers for the second

and third phases (EGIGP II and III) in 2015 and 2016, thereby providing predictable financing for

the Government of Mozambique (GoM) and creating a medium-term platform for policy dialogue.

EGIGP II is the second in a series of three annual single-tranche operations to be delivered in 2015.

1.2 The proposed EGIGP II is aligned with the Government’s development plan and multi-

donor budget support program. The EGIGP II is harmonized with the G19 joint-donor mechanism

for provision of GBS, and reforms supported under EGIGP II are in line with the Poverty Reduction

Action Plan (PARP, Programa de Ação para a Redução da Pobreza 2011-2014), the Medium-Term

Fiscal Framework (MTFF) 2015-2017 and the objectives laid out in the Five-Year Program. In

February 2015, Government approved a new Five-Year Program (2015-2019), outlining the main

priorities and strategic actions for the medium term, with emphasis on employment creation, and

greater competitiveness through higher productivity.

1.3 In line with the original approved program by the Board in 2014, the development

objective of EGIGP II is to promote inclusive and sustainable growth in Mozambique. Strong

economic growth (average 7%) over the past two decades has not translated into significant poverty

reduction2. This is due to a growth pattern, driven by large capital intensive projects in mining and

hydrocarbon sectors, with limited links to the rest of the economy. Consistent with the Bank’s

operational objectives and new institutional priorities3, the reforms supported by this operation

will contribute to inclusive growth and support Mozambique in achieving the Bank’s objective

of improving the quality of life and well-being of all Mozambican. Reforms to simplify business

regulations and start up procedures to obtain a license will lead to higher investment, increase

productivity of the private sector and increase job creation for youth and women. These reforms are

focused more to benefit smaller and medium enterprises that have fewer resources at their disposal

to deal with an excessively onerous business environment. The development of the extractive

industry brings significant opportunity to the country but much will depend on whether Government

is able to capture a fair share of the rents and how these are used. Reforms supported under the

operation will improve regulatory environment, transparency and management of public finance and

the extractive industries. These changes will contribute to a more judicious use of resources and

sharing benefits.

1 ADF/BD/WP/2014/93 2 Strong economic growth led to a decline in the national poverty headcount by 14 percentage points between 1997 and

2003 to 56 percent, implying a growth elasticity of poverty reduction of 0.3. Poverty fell between 2003 and 2009 to 52

percent, implying a growth elasticity of poverty reduction of only 0.14. 3 The new High-5 recently announced by the President of the Bank Group that will drive the Bank’s work as it

implements its current ten year strategy are: (a) Light up and Power Africa; (b) Feed Africa; (c) Integrate Africa; (d)

Industrialize Africa, and (e) Improve quality of life for the people of Africa

2

II. UPDATE OF COUNTRY ELIGIBILITY

2.1 Country’s continued commitment to poverty reduction: The GoM’s continued

commitment to poverty reduction and inclusive growth is encapsulated in the new Five Year Program

(Plano Quinquenal do Governo, PQG 2015-2019), whose major emphasis is on employment creation,

poverty reduction and greater competitiveness through higher productivity. The five guiding pillars

of the national development strategy are (i) consolidation of national unity, peace and sovereignty,

(ii) development of human and social capital, (iii) promotion of employment, productivity and

competitiveness, (iv) development of economic and social infrastructure, and (v) sustainable and

transparent management of natural resources. It has also three supporting pillars: (a) consolidate the

democratic rule of law, good governance and decentralization, (b) promote a balanced and stable

macroeconomic environment, and (c) reinforce international cooperation. The PQG represents

significant continuity in the focus of the government program, and has elevated the transparent and

sustainable management of its natural resources to one of the top priorities. The 2015 program is

fully consistent with these strategic pillars.

2.2 Continued political stability: In 2012, Mozambique celebrated 20 years of peace during

which elections were held regularly and peacefully. Political stability was jeopardized in 2013 when

tension between the Government and RENAMO, the former rebel group turned political opposition,

degenerated into fighting in the interior of the country. The resumption of dialogue and signing of

the cessation of hostilities agreement in September 2014 facilitated general elections conducted in

October 2014, and inauguration of a new president and a new government in January 2015, in which

ruling FRELIMO retained parliamentary majority. Although RENAMO disputed the results of the

election, relative political stability continued. The new government has expressed commitment to

political decentralization and the existing framework for political dialogue, which with support from

development partners, has contributed to ensuring stability.

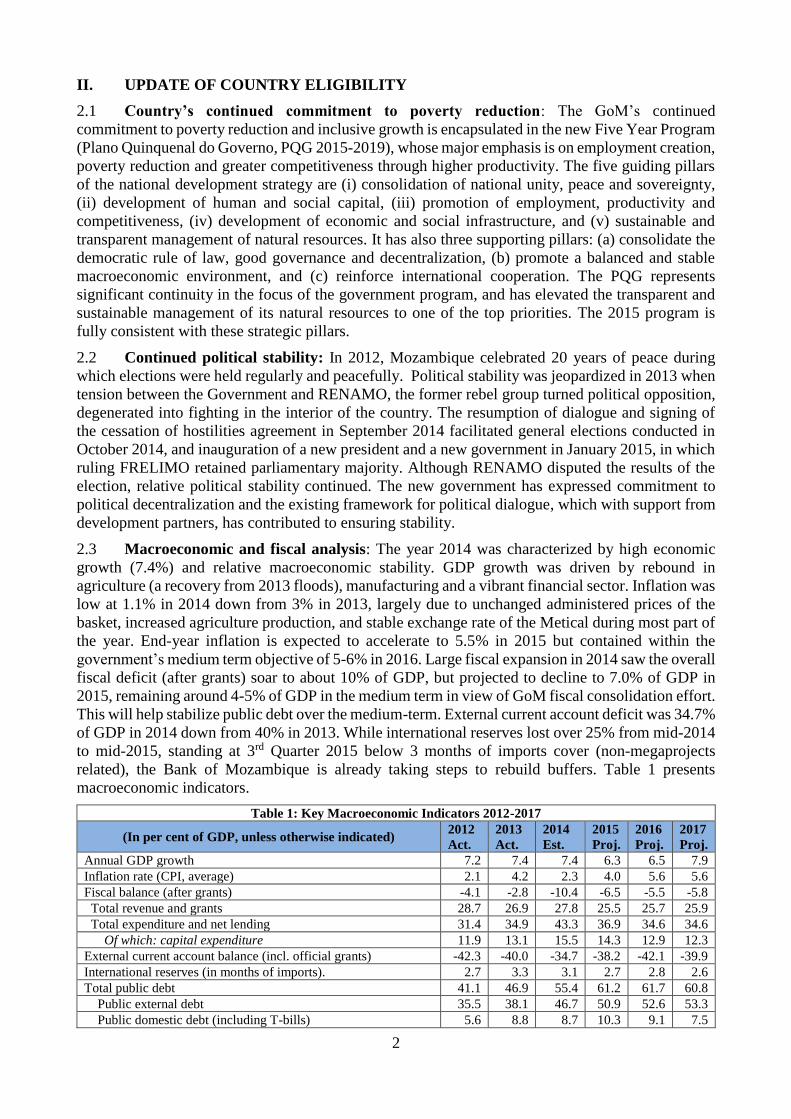

2.3 Macroeconomic and fiscal analysis: The year 2014 was characterized by high economic

growth (7.4%) and relative macroeconomic stability. GDP growth was driven by rebound in

agriculture (a recovery from 2013 floods), manufacturing and a vibrant financial sector. Inflation was

low at 1.1% in 2014 down from 3% in 2013, largely due to unchanged administered prices of the

basket, increased agriculture production, and stable exchange rate of the Metical during most part of

the year. End-year inflation is expected to accelerate to 5.5% in 2015 but contained within the

government’s medium term objective of 5-6% in 2016. Large fiscal expansion in 2014 saw the overall

fiscal deficit (after grants) soar to about 10% of GDP, but projected to decline to 7.0% of GDP in

2015, remaining around 4-5% of GDP in the medium term in view of GoM fiscal consolidation effort.

This will help stabilize public debt over the medium-term. External current account deficit was 34.7%

of GDP in 2014 down from 40% in 2013. While international reserves lost over 25% from mid-2014

to mid-2015, standing at 3rd Quarter 2015 below 3 months of imports cover (non-megaprojects

related), the Bank of Mozambique is already taking steps to rebuild buffers. Table 1 presents

macroeconomic indicators.

Table 1: Key Macroeconomic Indicators 2012-2017

(In per cent of GDP, unless otherwise indicated) 2012

Act.

2013

Act.

2014

Est.

2015

Proj.

2016

Proj.

2017

Proj.

Annual GDP growth 7.2 7.4 7.4 6.3 6.5 7.9

Inflation rate (CPI, average) 2.1 4.2 2.3 4.0 5.6 5.6

Fiscal balance (after grants) -4.1 -2.8 -10.4 -6.5 -5.5 -5.8

Total revenue and grants 28.7 26.9 27.8 25.5 25.7 25.9

Total expenditure and net lending 31.4 34.9 43.3 36.9 34.6 34.6

Of which: capital expenditure 11.9 13.1 15.5 14.3 12.9 12.3

External current account balance (incl. official grants) -42.3 -40.0 -34.7 -38.2 -42.1 -39.9

International reserves (in months of imports). 2.7 3.3 3.1 2.7 2.8 2.6

Total public debt 41.1 46.9 55.4 61.2 61.7 60.8

Public external debt 35.5 38.1 46.7 50.9 52.6 53.3

Public domestic debt (including T-bills) 5.6 8.8 8.7 10.3 9.1 7.5

3

2.4 Government is committed to a prudent fiscal stance. The 2015 budget approved by

parliament reflects an effort to tighten fiscal policy and commitment to implement fiscal

consolidation. Authorities plan to continue reducing public spending to below 34.6% of GDP by

2017 and the overall deficit (after grants) from over 10.4% in 2014 to 5.8% in 2017 and later to 5%

in 2019. One-off factor explain about half of the fiscal loosening, with electoral spending accounting

for 0.9% of GDP, and the inclusion in the budget of the non-commercial spending of EMATUM

representing 2.8% of GDP. Economic activity in 2015 has remain solid, though new challenges have

emerged with the drop in commodity prices and require decisive policy action. Mozambique’s

medium-term macroeconomic outlook is positive. Annual growth is expected 6.3% in 2015 and is

projected to accelerate slightly to 6.5% in 2016 and in 2017 to around 8% as agriculture recovers

from the 2015 floods and growth continues strongly in the extractive sector, construction,

transportation and communications. In the short run, resource-related FDI, and infrastructure

investments, both public and private, are expected to be major contributors to growth. Weaker

commodity prices, particularly if prolonged, could have an adverse impact on Mozambique’s

economic prospects. The external position has deteriorated considerably, with continued pressure

over the balance of payments since mid-2014. The widening of the trade balance deficit reduced

foreign currency liquidity. The Metical is on freefall against the US dollar accumulating a 45.4% loss

year-on-year. The devaluation negatively affects debt sustainability, as 80% of public debt is

denominated in US dollars. The Central Bank has already start to increase reference rates to tighten

monetary policy in order to contain inflationary pressures and assist the Metical exchange rate. Inflation is projected to stay between 5-6% through 2017. The IMF concluded its 4th PSI review in

July 2015 and acknowledged Mozambique’s strong economic growth record, but the increasing

challenging environment requires stepping up the progress in implementing structural reforms,

including fiscal risks management, public investment management and tax administration. In

addition, Government agreed for an 18-month Stand-by Credit Facility of SDR 204.48 million to

support the Balance of Payments. The overall macroeconomic framework provides adequate basis

for this operation.

2.5 Fiduciary risk assessment: Several satisfactory fiduciary risk assessments (FRAs) have been

undertaken in Mozambique, including three PEFA assessments in 2006, 2008 and 2010. In particular,

the 2010 PEFA assessment identified substantial progress in areas such as budget credibility (with

the roll-out of the e-SISTAFE system, improvement in budget transparency and a reduction in the

deviation of budget execution from budgeted amounts) and, to a lesser, extent, comprehensiveness

and transparency of the budget. In particular, the country’s performance in budget transparency is

strong, with all eight major budget documents being regularly published and a major improvement

in terms of the Open Budget Index, from a score of 28 out of 100 in 2010 to 47 in 2012. Reforms

have continued unabated since 2010 in all areas, and a new PEFA assessment has been launched in

May 2015 and expected to be completed before end-December 2015. The Bank’s Fiduciary Risk

Assessment (FRA) undertaken in 2015 as part of the CSP issue paper concluded that the fiduciary

risk is substantial, although declining (see annex III).

2.6 Harmonization: Coordination amongst development partners (DPs) in Mozambique is

highly harmonized under the G-19 budget support donor group4and is governed by the new

Memorandum of Understanding (MoU) signed in September 2015. The core GBS partners and

the Ministry of Economy and Finance (MoEF) have been working on the reform of the harmonization

framework for GBS. Consequently, a streamlined MoU focusing only on GBS has been adopted in

2015 to underpin a more focused PAF and a more effective policy dialogue. A common Performance

Assessment Framework (PAF) which is aligned with the Government’s PQG 2015-2019, will inform

individual DPs’ GBS programs. In addition, DPs and GoM jointly monitor “areas of special

4 Out of the G-19 Group, otherwise known as Program Aid Partners, only 14 currently provide budget support. The G-19

includes: Austria, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Norway, Portugal, Sweden, Switzerland,

UK, EU, AfDB and World Bank, two associate members (USA and UN) and IMF (ex-officio member).

4

attention” linked to specific reforms. Policy dialogue takes place at the political (Head of Mission)

and technical (Head of Corporations and working groups) levels. The Bank is involved at both levels

and plays an active role in the Head of Corporation as well as in the Economist Working Group,

Private Sector Group, and Budget Analysis Group. The PAF cycle is based on a planning exercise in

September/October (when PAF indicators are defined for the following year) and a review exercise

in April/May (when performance in the previous year is assessed). The review of the 2014 program

was concluded on 15 May 2015 and a joint aide-memoire detailing progress in program

implementation has informed the design of EGIGP II. Budget support partners are currently working

with the Government to design a new PAF that will better link policy actions with results sought and

to form the basis for providing budget support from 2016 onwards.

III. YEAR 2015 PROGRAM

3.1 Program Goal and Purpose

3.1.1 As earlier indicated, the goal of EGIGP is to support the government effort in promoting

inclusive and sustainable growth through good governance by (i) consolidating transparent and

accountable PFM and natural resource management frameworks; and (ii) improving the enabling

environment for private sector development. Consistent with this goal, the operational objective of

the 2015 program is strengthening policy, legal and regulatory frameworks for transparency and

accountability in pubic financial management (public investment management, fiscal risk

management, and natural resource management) and business enabling environment.

3.2 Program Components

3.2.1 The EGIGP II components remain the same as specified in the original Program

Appraisal Report (PAR) namely (1) Consolidating transparent and accountable PFM and natural

resource management frameworks; and (2) Improving the enabling environment for private sector

development. These two components are complementary and mutually reinforcing.

Component 1: Consolidating Transparent and Accountable PFM and Natural Resource

Management Frameworks

3.2.2 Mozambique has made important progress in PFM and natural resource management,

but further efforts are needed to strengthen efficiency and governance. Furthermore, EMATUM

sovereign guarantee calls for a strengthening of investment planning and monitoring of fiscal risks.

In this regard, the Government is undertaking major reforms in the areas of: (i) budget credibility and

predictability; (ii) management of fiscal risks; (iii) expenditure controls; (iv) value for money in

spending; and (v) the extractive sector transparency.

3.2.3 EGIGP I supported (as prior action) the adoption of a Fiscal Transparency Action Plan

(FTAP) in March 2014, in coordination with the IMF, to strengthen governance of fiscal resource

flows and monitoring fiscal risks. Government has registered progress in rolling out the integrated

financial management system (e-SISTAFE) across government ministries and expanding its

functionality over time. The program has supported (as prior action) the operationalisation of the

procurement functionality in e-SISTAFE, as the first step to allow the creation of a database on

procurement processes at all levels. Government has also taken measures to improve transparency in

the management of the extractive sector. EGIGP I supported (as prior action) the adoption of a revised

legislations for the mining and petroleum sectors in mid-2014. This legislation increases transparency

in contract disclosure, but further reform and implementing regulations will be required to concretise

many aspects of the legislations.

3.2.4 EGIGP II would support government efforts and plans to strengthening the fiduciary

systems and governance in extractives. This include measures to enhance linkages and streamline

the investment planning instruments, further fiscal transparency in SOEs, broadening and deepening

of Mozambique’s EITI engagement, and operationalization of the revised legal framework on mining

and petroleum.

5

Component 2: Improving the Enabling Environment for Private Sector Development

3.2.5 The Government is implementing reforms to improve the business enabling

environment for private sector development. The Bank continued to support Government to

implement two strategies shaping the private sector development agenda, namely: (a) EMAN II

(2013-2017), focusing on simplifying business regulations and strengthening competitiveness

through concrete legal and regulatory reforms; and (b) the FSDS 2013-2022, aimed at fostering

stability, access and long-term development with an emphasis on MSMEs to promote inclusive

growth and job creation, particularly for women and youth.

3.2.6 EGIGP I supported (as prior action) the adoption of a decree for introducing a single form for

business start-up procedures, adoption of a revised industrial licensing decree, and the creation of

private credit bureaus and register of borrowers. These reform measures are encapsulated in the

above strategies and aimed at promoting a friendlier investment climate and expanded access to

finance, as well as address information gaps allowing financial institutions to better assess clients’

creditworthiness.

3.2.7 EGIGP II will support government to deepen reforms supported under EGIGP I

including: (a) measures to expand the integrated one-stop-shop network (e-BAUs, which are already

being piloted to support streamlined business procedures); (b) implementation of the 2013

Competition Law, through the adoption of the regulations and establishment of a new competition

authority aimed at facilitating market entry and ensuring a level playing field; and (c) adoption of

regulations for e-banking and mobile banking services in order to promote inclusion in rural areas.

3.3 Program Outputs and Expected Results

3.3.1 Implementation progress of the program of reforms supported under the previous operation

(EGIGP I) has contributed to improve the business climate and to enhance transparency in the PFM

system and the management of extractive industries. The Government has implemented regulatory

reform to improve the business environment including revision and simplification of licensing

requirement and streamlining procedures for starting a business. There has been considerable

progress in rolling out e-SISTAFE across multiple public agencies, as well as expanding its

functionality over time. E-SISTAFE now covers budget preparation as well as budget execution and

the reporting of expenditures. Public finance review show the trajectory of improvement, as the PFM

reform program produced substantial improvements in fiscal policy and budget execution.

Nevertheless, there is need to strengthen the public investment management systems and greater

transparency and oversight in the management of stated owned enterprises. Progress made on the

outputs targets established in the original PAR approved by the Board in 2014, as envisaged in the

results logical framework (RLF) is summarized in Table 2 below.

Table 2: Progress on Targets from the RLF

Output Achievements

A. Consolidating Transparent and Accountable PFM and Natural Resource Management Frameworks

Improved fiscal transparency A Fiscal Transparency Action Plan is being considered. Six of the largest state

enterprises have published financial statements

Strengthened procurement

systems

Progress is made in the operationalization of the procurement functionality in e-

SISTAFE, allowing for the creation of a database on procurement processes at all

levels

Increased oversight by service

users and CSOs in budget

process and public service

delivery

The 2014 and 2015 citizens budget have been published

6

Improved efficiency,

transparency and inclusion in

the management of mineral

resources

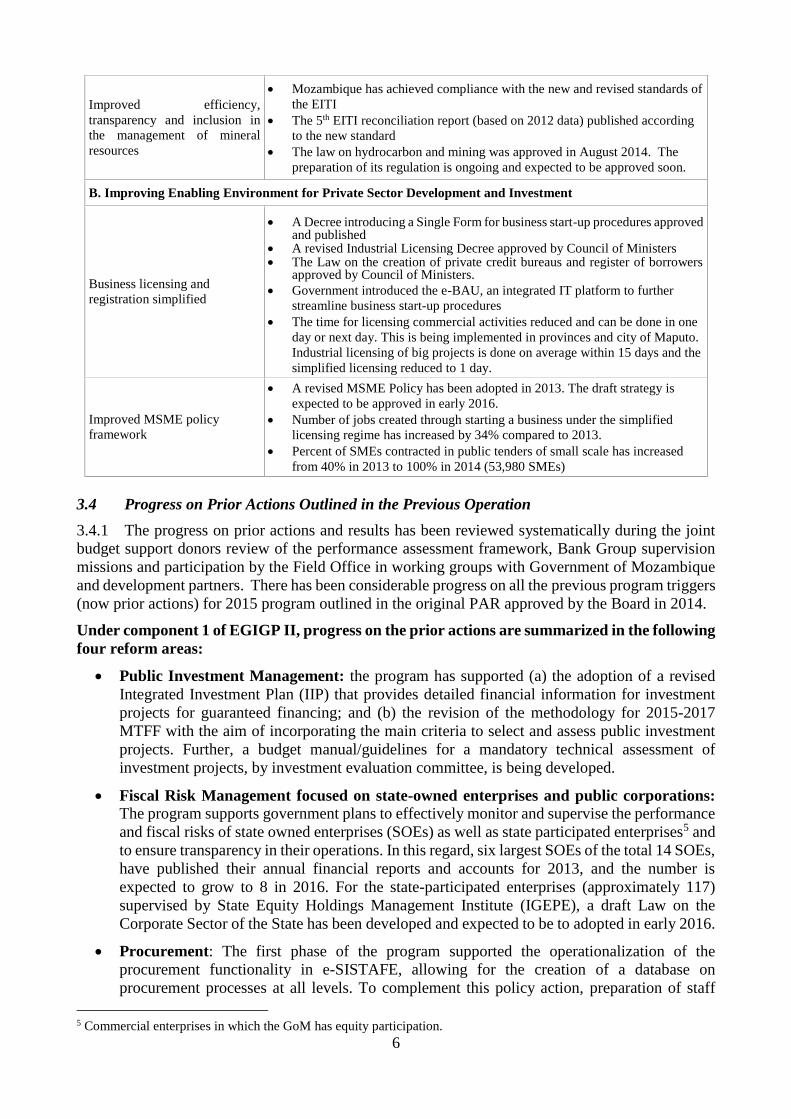

Mozambique has achieved compliance with the new and revised standards of

the EITI

The 5th EITI reconciliation report (based on 2012 data) published according

to the new standard

The law on hydrocarbon and mining was approved in August 2014. The

preparation of its regulation is ongoing and expected to be approved soon.

B. Improving Enabling Environment for Private Sector Development and Investment

Business licensing and

registration simplified

A Decree introducing a Single Form for business start-up procedures approved and published

A revised Industrial Licensing Decree approved by Council of Ministers The Law on the creation of private credit bureaus and register of borrowers

approved by Council of Ministers.

Government introduced the e-BAU, an integrated IT platform to further

streamline business start-up procedures

The time for licensing commercial activities reduced and can be done in one

day or next day. This is being implemented in provinces and city of Maputo.

Industrial licensing of big projects is done on average within 15 days and the

simplified licensing reduced to 1 day.

Improved MSME policy

framework

A revised MSME Policy has been adopted in 2013. The draft strategy is

expected to be approved in early 2016.

Number of jobs created through starting a business under the simplified

licensing regime has increased by 34% compared to 2013.

Percent of SMEs contracted in public tenders of small scale has increased

from 40% in 2013 to 100% in 2014 (53,980 SMEs)

3.4 Progress on Prior Actions Outlined in the Previous Operation

3.4.1 The progress on prior actions and results has been reviewed systematically during the joint

budget support donors review of the performance assessment framework, Bank Group supervision

missions and participation by the Field Office in working groups with Government of Mozambique

and development partners. There has been considerable progress on all the previous program triggers

(now prior actions) for 2015 program outlined in the original PAR approved by the Board in 2014.

Under component 1 of EGIGP II, progress on the prior actions are summarized in the following

four reform areas:

Public Investment Management: the program has supported (a) the adoption of a revised

Integrated Investment Plan (IIP) that provides detailed financial information for investment

projects for guaranteed financing; and (b) the revision of the methodology for 2015-2017

MTFF with the aim of incorporating the main criteria to select and assess public investment

projects. Further, a budget manual/guidelines for a mandatory technical assessment of

investment projects, by investment evaluation committee, is being developed.

Fiscal Risk Management focused on state-owned enterprises and public corporations:

The program supports government plans to effectively monitor and supervise the performance

and fiscal risks of state owned enterprises (SOEs) as well as state participated enterprises5 and

to ensure transparency in their operations. In this regard, six largest SOEs of the total 14 SOEs,

have published their annual financial reports and accounts for 2013, and the number is

expected to grow to 8 in 2016. For the state-participated enterprises (approximately 117)

supervised by State Equity Holdings Management Institute (IGEPE), a draft Law on the

Corporate Sector of the State has been developed and expected to be to adopted in early 2016.

Procurement: The first phase of the program supported the operationalization of the

procurement functionality in e-SISTAFE, allowing for the creation of a database on

procurement processes at all levels. To complement this policy action, preparation of staff

5 Commercial enterprises in which the GoM has equity participation.

7

profile of the Procurement Units’ (UGEAs) is being developed with the aim of strengthening

the capacity and skills mix of professional staff. However, the approval of the procurement

staff profile has delayed until the revision of the procurement law is completed in early 2016.

Natural Resource Management: The program supported the adoption of the legislation for

mining and hydrocarbon fiscal regime as well as the implementing regulation for the mining

law. Mozambique has also shown serious commitment to the new EITI standards. The

preparation of the 6th EITI report covering 2013 and 2014 based on the new standards has

started, and is expected to be published by March 2016.

Under component 2 of the EGIGP II, progress on the prior actions are summarized as follows:

Business regulatory reforms: The Government has expanded e-BAU platform to 8 sites

allowing further streamlining through automation of business start-up procedures. The time it

takes for licensing commercial activities has significantly reduced. For example, the time it takes

for obtaining construction licence declined sharply from 377 days in 2012 to 18 days currently.

Financial Sector Development: A new regulation on electronic money (e-banking and mobile

banking) has been approved by the Board of Bank of Mozambique. The new regulation imposes

a requirement for the E-money issuers to deposit the funds received against issuing of E-money

in a custody account (termed “trust account”) as a mean of protecting the money owed to E-

money holders, should they need to redeem it. Furthermore, a draft Law on the moveable

collateral is being developed. Given the cross-cutting nature of the draft Law, a workshop was

conducted in July 2015 in order to consult with the main stakeholders. The draft law is expected

to be finalized and submitted to Council of Ministers by end-December 2015.

SME Strategy and Competition Law and Competition Authority: To further deepen inclusive

development, a national SME strategy is being developed and is expected to be submitted to

Council of Ministers for approval in early 2016. The new SME Strategy focuses on enhancing

the capacity of the MSMEs, increasing their access to financial services, and improving access to

markets. To promote competitiveness, both the regulations for implementing the Competition

Law, and the Statutes (“estatutos”) of the Competition Authority were approved in 2015.

3.5 Policy Dialogue

3.5.1 Key policy dialogue issues, which came out strongly from the joint PAPs-GoM review of the

implementation of the 2014 program include the need for close monitoring of the Fiscal Transparency

Action Plan, including identifying legal and structural reforms on the basis of IMF evaluation; good

governance with emphasis on effective implementation of anti-corruption package and strengthening

the link between the Integrated Investment Plan (IIP) with debt sustainability. Policy dialogue will

also focus on the need for careful identification of drivers of inclusive growth and designing concreate

programs especially in small-scale agriculture, informal sector, services and tourism to operationalize

it, with particular attention to women and youth. Policy dialogue with the GoM will also be

intensified on the streamlined MoU and PAF focusing principally on GBS for effective monitoring

and evaluation of budget support operations. Deepening PFM reforms and improving business

enabling environment with particular emphasis on the triggers for the 2016 Program will also be

focus of policy dialogue.

3.6 Loan and Grant Conditions

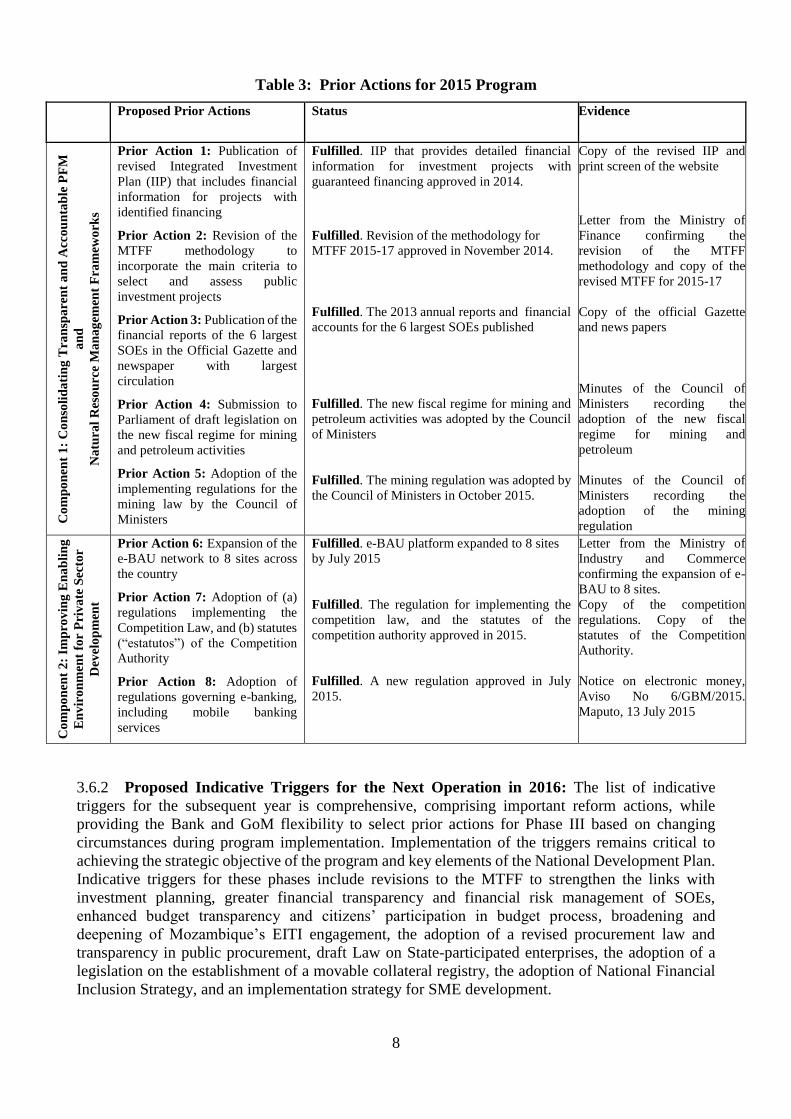

3.6.1 Prior Action for 2015 Program: Table 3 summarizes the changes between the triggers

identified for EGIGP II in EGIGP I and the proposed prior actions for this operation. All EGIGP II

prior actions have been met by the authorities and the required documentary evidences will be

submitted to the Bank before the operation is presented to the Board. Further, there is logical follow

up of reform actions linked to the previous and the next phase of the programmatic operation.

8

Table 3: Prior Actions for 2015 Program

Proposed Prior Actions Status Evidence

Co

mp

on

ent

1:

Co

nso

lid

ati

ng

Tra

nsp

are

nt

an

d A

cco

un

tab

le P

FM

an

d

Na

tura

l R

eso

urc

e M

an

ag

emen

t F

ram

ewo

rks

Prior Action 1: Publication of

revised Integrated Investment

Plan (IIP) that includes financial

information for projects with

identified financing

Prior Action 2: Revision of the

MTFF methodology to

incorporate the main criteria to

select and assess public

investment projects

Prior Action 3: Publication of the

financial reports of the 6 largest

SOEs in the Official Gazette and

newspaper with largest

circulation

Prior Action 4: Submission to

Parliament of draft legislation on

the new fiscal regime for mining

and petroleum activities

Prior Action 5: Adoption of the

implementing regulations for the

mining law by the Council of

Ministers

Fulfilled. IIP that provides detailed financial

information for investment projects with

guaranteed financing approved in 2014.

Fulfilled. Revision of the methodology for

MTFF 2015-17 approved in November 2014.

Fulfilled. The 2013 annual reports and financial

accounts for the 6 largest SOEs published

Fulfilled. The new fiscal regime for mining and

petroleum activities was adopted by the Council

of Ministers

Fulfilled. The mining regulation was adopted by

the Council of Ministers in October 2015.

Copy of the revised IIP and

print screen of the website

Letter from the Ministry of

Finance confirming the

revision of the MTFF

methodology and copy of the

revised MTFF for 2015-17

Copy of the official Gazette

and news papers

Minutes of the Council of

Ministers recording the

adoption of the new fiscal

regime for mining and

petroleum

Minutes of the Council of

Ministers recording the

adoption of the mining

regulation

Co

mp

on

ent

2:

Imp

rov

ing

En

ab

lin

g

En

vir

on

men

t fo

r P

riv

ate

Sec

tor

Dev

elo

pm

ent

Prior Action 6: Expansion of the

e-BAU network to 8 sites across

the country

Prior Action 7: Adoption of (a)

regulations implementing the

Competition Law, and (b) statutes

(“estatutos”) of the Competition

Authority

Prior Action 8: Adoption of

regulations governing e-banking,

including mobile banking

services

Fulfilled. e-BAU platform expanded to 8 sites

by July 2015

Fulfilled. The regulation for implementing the

competition law, and the statutes of the

competition authority approved in 2015.

Fulfilled. A new regulation approved in July

2015.

Letter from the Ministry of

Industry and Commerce

confirming the expansion of e-

BAU to 8 sites.

Copy of the competition

regulations. Copy of the

statutes of the Competition

Authority.

Notice on electronic money,

Aviso No 6/GBM/2015.

Maputo, 13 July 2015

3.6.2 Proposed Indicative Triggers for the Next Operation in 2016: The list of indicative

triggers for the subsequent year is comprehensive, comprising important reform actions, while

providing the Bank and GoM flexibility to select prior actions for Phase III based on changing

circumstances during program implementation. Implementation of the triggers remains critical to

achieving the strategic objective of the program and key elements of the National Development Plan.

Indicative triggers for these phases include revisions to the MTFF to strengthen the links with

investment planning, greater financial transparency and financial risk management of SOEs,

enhanced budget transparency and citizens’ participation in budget process, broadening and

deepening of Mozambique’s EITI engagement, the adoption of a revised procurement law and

transparency in public procurement, draft Law on State-participated enterprises, the adoption of a

legislation on the establishment of a movable collateral registry, the adoption of National Financial

Inclusion Strategy, and an implementation strategy for SME development.

9

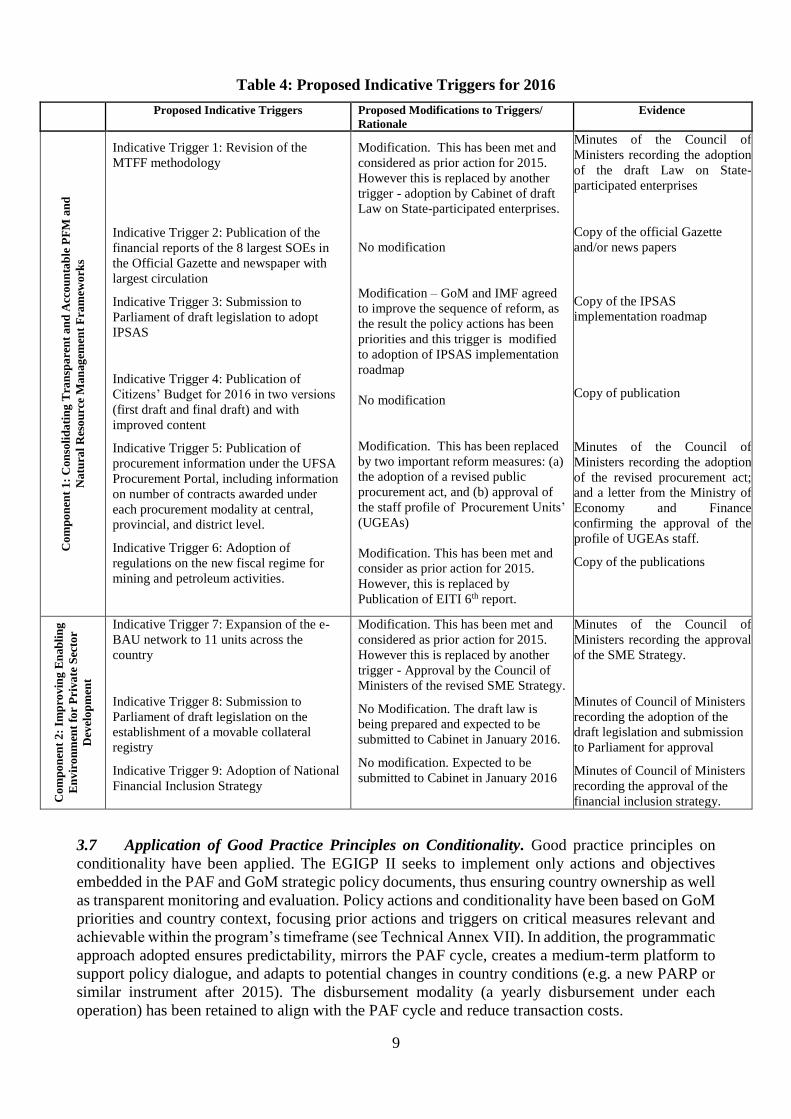

Table 4: Proposed Indicative Triggers for 2016

Proposed Indicative Triggers Proposed Modifications to Triggers/

Rationale

Evidence

Co

mp

on

ent

1:

Con

soli

da

tin

g T

ran

spa

ren

t a

nd

Acc

ou

nta

ble

PF

M a

nd

Na

tura

l R

eso

urc

e M

an

ag

emen

t F

ram

ewo

rks

Indicative Trigger 1: Revision of the

MTFF methodology

Indicative Trigger 2: Publication of the

financial reports of the 8 largest SOEs in

the Official Gazette and newspaper with

largest circulation

Indicative Trigger 3: Submission to

Parliament of draft legislation to adopt

IPSAS

Indicative Trigger 4: Publication of

Citizens’ Budget for 2016 in two versions

(first draft and final draft) and with

improved content

Indicative Trigger 5: Publication of

procurement information under the UFSA

Procurement Portal, including information

on number of contracts awarded under

each procurement modality at central,

provincial, and district level.

Indicative Trigger 6: Adoption of

regulations on the new fiscal regime for

mining and petroleum activities.

Modification. This has been met and

considered as prior action for 2015.

However this is replaced by another

trigger - adoption by Cabinet of draft

Law on State-participated enterprises.

No modification

Modification – GoM and IMF agreed

to improve the sequence of reform, as

the result the policy actions has been

priorities and this trigger is modified

to adoption of IPSAS implementation

roadmap

No modification

Modification. This has been replaced

by two important reform measures: (a)

the adoption of a revised public

procurement act, and (b) approval of

the staff profile of Procurement Units’

(UGEAs)

Modification. This has been met and

consider as prior action for 2015.

However, this is replaced by

Publication of EITI 6th report.

Minutes of the Council of

Ministers recording the adoption

of the draft Law on State-

participated enterprises

Copy of the official Gazette

and/or news papers

Copy of the IPSAS

implementation roadmap

Copy of publication

Minutes of the Council of

Ministers recording the adoption

of the revised procurement act;

and a letter from the Ministry of

Economy and Finance

confirming the approval of the

profile of UGEAs staff.

Copy of the publications

Co

mp

on

ent

2:

Imp

rov

ing

En

ab

lin

g

En

vir

on

men

t fo

r P

riva

te S

ecto

r

Dev

elo

pm

ent

Indicative Trigger 7: Expansion of the e-

BAU network to 11 units across the

country

Indicative Trigger 8: Submission to

Parliament of draft legislation on the

establishment of a movable collateral

registry

Indicative Trigger 9: Adoption of National

Financial Inclusion Strategy

Modification. This has been met and

considered as prior action for 2015.

However this is replaced by another

trigger - Approval by the Council of

Ministers of the revised SME Strategy.

No Modification. The draft law is

being prepared and expected to be

submitted to Cabinet in January 2016.

No modification. Expected to be

submitted to Cabinet in January 2016

Minutes of the Council of

Ministers recording the approval

of the SME Strategy.

Minutes of Council of Ministers

recording the adoption of the

draft legislation and submission

to Parliament for approval

Minutes of Council of Ministers

recording the approval of the

financial inclusion strategy.

3.7 Application of Good Practice Principles on Conditionality. Good practice principles on

conditionality have been applied. The EGIGP II seeks to implement only actions and objectives

embedded in the PAF and GoM strategic policy documents, thus ensuring country ownership as well

as transparent monitoring and evaluation. Policy actions and conditionality have been based on GoM

priorities and country context, focusing prior actions and triggers on critical measures relevant and

achievable within the program’s timeframe (see Technical Annex VII). In addition, the programmatic

approach adopted ensures predictability, mirrors the PAF cycle, creates a medium-term platform to

support policy dialogue, and adapts to potential changes in country conditions (e.g. a new PARP or

similar instrument after 2015). The disbursement modality (a yearly disbursement under each

operation) has been retained to align with the PAF cycle and reduce transaction costs.

10

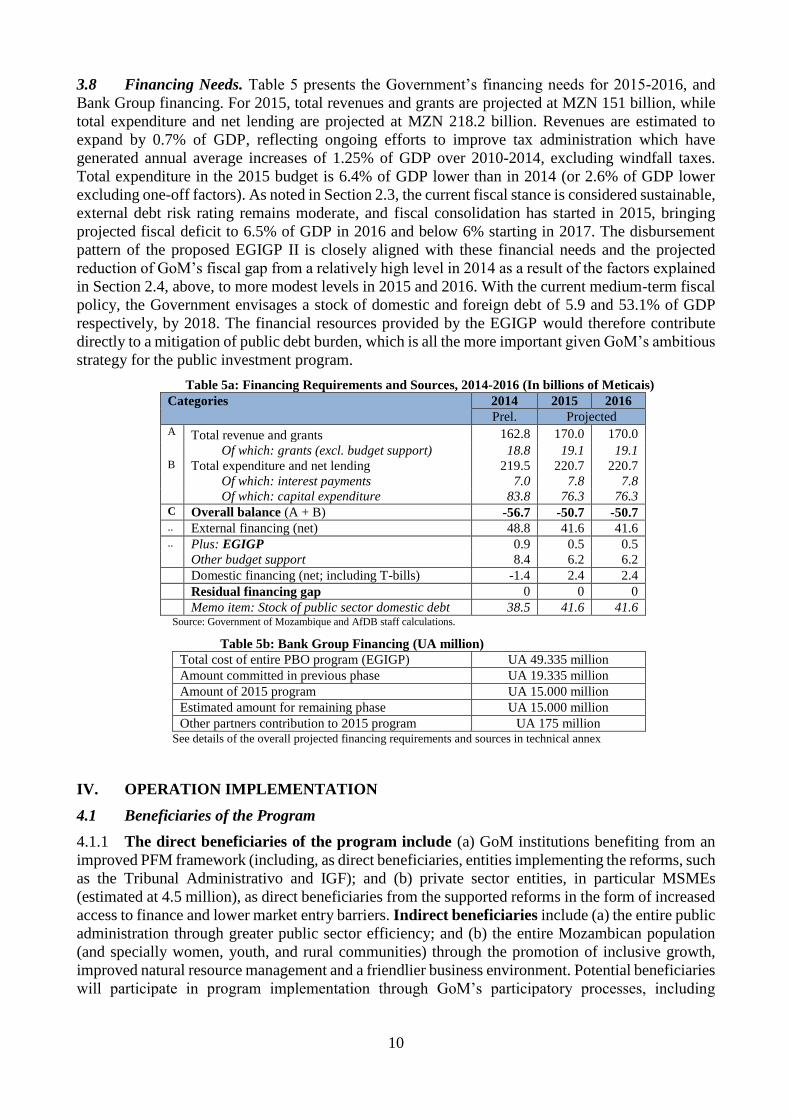

3.8 Financing Needs. Table 5 presents the Government’s financing needs for 2015-2016, and

Bank Group financing. For 2015, total revenues and grants are projected at MZN 151 billion, while

total expenditure and net lending are projected at MZN 218.2 billion. Revenues are estimated to

expand by 0.7% of GDP, reflecting ongoing efforts to improve tax administration which have

generated annual average increases of 1.25% of GDP over 2010-2014, excluding windfall taxes.

Total expenditure in the 2015 budget is 6.4% of GDP lower than in 2014 (or 2.6% of GDP lower

excluding one-off factors). As noted in Section 2.3, the current fiscal stance is considered sustainable,

external debt risk rating remains moderate, and fiscal consolidation has started in 2015, bringing

projected fiscal deficit to 6.5% of GDP in 2016 and below 6% starting in 2017. The disbursement

pattern of the proposed EGIGP II is closely aligned with these financial needs and the projected

reduction of GoM’s fiscal gap from a relatively high level in 2014 as a result of the factors explained

in Section 2.4, above, to more modest levels in 2015 and 2016. With the current medium-term fiscal

policy, the Government envisages a stock of domestic and foreign debt of 5.9 and 53.1% of GDP

respectively, by 2018. The financial resources provided by the EGIGP would therefore contribute

directly to a mitigation of public debt burden, which is all the more important given GoM’s ambitious

strategy for the public investment program.

Table 5a: Financing Requirements and Sources, 2014-2016 (In billions of Meticais)

Categories 2014 2015 2016

Prel. Projected A Total revenue and grants 162.8 170.0 170.0 Of which: grants (excl. budget support) 18.8 19.1 19.1 B Total expenditure and net lending 219.5 220.7 220.7 Of which: interest payments 7.0 7.8 7.8 Of which: capital expenditure 83.8 76.3 76.3 C Overall balance (A + B) -56.7 -50.7 -50.7 .. External financing (net) 48.8 41.6 41.6 .. Plus: EGIGP 0.9 0.5 0.5 Other budget support 8.4 6.2 6.2 Domestic financing (net; including T-bills) -1.4 2.4 2.4 Residual financing gap 0 0 0 Memo item: Stock of public sector domestic debt 38.5 41.6 41.6

Source: Government of Mozambique and AfDB staff calculations.

Table 5b: Bank Group Financing (UA million)

Total cost of entire PBO program (EGIGP) UA 49.335 million

Amount committed in previous phase UA 19.335 million

Amount of 2015 program UA 15.000 million

Estimated amount for remaining phase UA 15.000 million

Other partners contribution to 2015 program UA 175 million See details of the overall projected financing requirements and sources in technical annex

IV. OPERATION IMPLEMENTATION

4.1 Beneficiaries of the Program

4.1.1 The direct beneficiaries of the program include (a) GoM institutions benefiting from an

improved PFM framework (including, as direct beneficiaries, entities implementing the reforms, such

as the Tribunal Administrativo and IGF); and (b) private sector entities, in particular MSMEs

(estimated at 4.5 million), as direct beneficiaries from the supported reforms in the form of increased

access to finance and lower market entry barriers. Indirect beneficiaries include (a) the entire public

administration through greater public sector efficiency; and (b) the entire Mozambican population

(and specially women, youth, and rural communities) through the promotion of inclusive growth,

improved natural resource management and a friendlier business environment. Potential beneficiaries

will participate in program implementation through GoM’s participatory processes, including

11

consultations with CSOs for the preparation of the yearly Economic and Social Plans and dialogue

with private sector groups in the implementation of PSD sectoral strategies.

4.2 Implementation, Monitoring and Evaluation

4.2.1 Implementation institutional framework: The Ministry of Economy and Finance (MoEF)

will be responsible for the overall implementation of the reform program supported by the EGIGP,

in line of the harmonization framework laid down in the 2009 MoU between GoM and the G-19 DPs.

Through capacity building projects supported by the Bank and other DPs, the MoEF is being

strengthened to enhance its capacity to monitor reform implementation under the PGQ and PAF.

4.2.2 Monitoring and evaluation will take place in accordance with the MoU through (a) the joint

PAF, which is evaluated for year n outputs and outcomes in the context of the Annual Review in

April/May of year n+1, as well as (b) the regular monitoring of the PARP, both of which include

participation by civil society and other stakeholders. The program will be supervised semi-annually

in alignment with the PAF cycle, with the MZFO leading on policy dialogue through the existing G-

19 working groups and other fora. A PCR will be prepared at program completion after 2016. IMF

assessments and any other relevant analytical work will also be used to monitor progress.

4.3 Financial Management and Disbursement & Reporting Arrangements

4.3.1 The overall conclusion of the PFM diagnostic reviews conducted over the last four years is

that the country’s PFM systems are improving steadily over time as systems are stabilized and

capacity and skills are developed. The 2010 PEFA report indicates that between 2008 and 2010,

eleven of the twenty-eight PEFA indicators had improved or were moving in the right direction,

fifteen indicators were unchanged; and just two indicators deteriorated. Other recent PFM diagnostic

reviews conducted indicate that the country is in the phase of consolidating the reforms underway

and exhibiting a positive trajectory of change in the overall country PFM systems. In general, the

country’s PFM system is determined to be adequate to support the Program. The Bank’s FRA

concluded that the fiduciary risk is substantial, but reducing over time (Technical Annex III).

4.3.2 Treasury Management, funds flow and disbursement method: The second phase of the

proposed operation involves a single-tranche disbursement of UA 15 million in 2015 following Board

approval. The proceeds of the grant will be deposited into an account designated by the MoEF at the

BoM that is part of the Country’s foreign exchange reserve upon fulfilment of the disbursement

conditions. The equivalent local currency will be transferred to the Treasury Single Account (TSA)

that is used to finance budgeted expenditures, and appropriately accounted for in the financial

management systems of the Government. The MoEF will provide a confirmation letter to the Bank

indicating that the amount deposited in the foreign currency account has been credited to the TSA.

4.3.3 External audit: In line with the Bank Policy on PBOs, the external audit arrangement will

follow the country’s systems. The Tribunal Administrativo, will annually audit the General State

Account including the Bank’s contribution. The annual audit report on the State Account will be

available to development partners. The 2013 General State Accounts (CGE) was published in July

2014 but the Opinion of the Administrative Court on the 2013 CGE was not published until April

2015. The 2014 CGE and Opinion of the Administrative Court is expected to be published in time

for debate in Parliament in 2015. In addition, an audit of the flow of funds of GBS will be conducted

in accordance with the GoM-G-19 MoU. The audit report and the management letter will be

submitted to the G-19, no later than six months after year end.

4.4 Procurement: The principles of the procurement regulatory framework are generally

consistent with international best practices. However, there is still need to supplement this regulatory

framework, operationalize the institutional system and build the capacity of parties in the

procurement chain. In this context, GoM has embarked on a reform process aimed at establishing a

procurement professional career path in the public administration, setting up an information system

for procurement activities and improving transparency through an efficient procurement portal. The

12

Bank’s FRA has rated procurement risk as Moderate and identified mitigating measures for the

identified risks (including EGIGP II prior actions and indicative triggers).

V. LEGAL DOCUMENTATION AND AUTHORITY

5.1 Legal Documentation

5.1.1 A protocol of agreement signed between the Republic of Mozambique and the ADF.

5.2 Conditions Associated with Bank Group Intervention

5.2.1 Prior Actions and entry into force: Before the Grant proposal is presented to the ADF Board,

GoM shall have provided evidence, satisfactory in form and substance, to the Fund that the prior

actions for EGIGP II outlined in Table 3 have been fulfilled. The Protocol of Agreement shall enter

into force upon signature by the parties.

5.2.2 Conditions precedent to the disbursement of the Grant for the EGIGP II: Disbursement

of the grant amount of UA 15 million shall be conditional upon the entry into force of the Protocol

of Agreement, and the transmission to the Bank of the details of a foreign currency account with the

Bank of Mozambique for the purpose of receiving the proceeds of the Grant.

5.3 Compliance with Bank Group Policies. This program complies with all applicable Bank

Group policies, strategies and guidelines. These include: (i) Policy on Program-Based Operations

(Revised, March 2012) and the Operational Guidelines on PBO (Revised, April 2014); (ii) Annotated

Streamlined Appraisal Report Format (2014); and (iii) revised Staff Guidance on Quality-at-Entry

Criteria and Standards for Public Sector Operations.

VI. RISK MANAGEMENT

Risk Mitigation measure

Macroeconomic stance could be

threatened by rising external debt

and unpredictable external shock

such as commodity price.

GoM has built a solid track record of prudent macroeconomic management. The 2015

budget puts the country back on sustainable path by reducing public spending and

narrowing the deficit. The IMF PSI (2013-2016) will run in parallel to the EGIGP,

thus providing a coordinated monitoring and dialogue platform for macroeconomic

management to manage shocks. This operation will contribute to minimizing risks.

Weak implementation capacity

may slow the pace and scope of

reforms.

Policy actions are derived from GoM priorities (e.g. Social and Economic Plan; 2014-

2016 MTFF) in the PAF agreed between GoM and DPs. AfDB and other DPs are

providing TA and capacity building, notably in oversight (Sweden for Tribunal

Administrativo; DfID for procurement); private and financial sector development

(World Bank on business enabling environment, DfID on financial sector, GIZ on

SMEs); and natural resource management (e.g. AfDB, World Bank, IMF, others). G-

19 commitment to budget support is still strong. Government remains engaged with

development partners to gain support for its economic reforms program.

Fiduciary risks: The EMATUM

case (issuance of a US$850m

government-backed bond), raised

transparency and debt

sustainability concerns.

A recent IMF Fiscal Transparency Assessment has concluded that overall, the

Government’s fiscal framework is transparent. An update of the DSA prepared by the

IMF shows that the debt sustainability outlook is not significantly affected by the

EMATUM transaction as long as other non-concessional debt in the pipeline for 2014

is delayed. Moreover, GoM has made good progress in its governance and PFM

reform agenda (e.g. approval of anti-corruption package; creation of a financial crimes

unit, and strengthening of audit systems). The EGIGP will further support the

consolidation of these reforms. A FRA has been carried out during appraisal

(Technical Annex III) to assess the residual fiduciary risks associated with the

program, which have been rated Substantial but reducing, and thus acceptable for

program implementation.

13

VII. RECOMMENDATION

Management recommends that the ADF Board of Directors consider and approve the proposed Grant

in an amount not exceeding UA 15.0 million to the Republic of Mozambique for phase II of the

EGIGP for the purposes, and subject to the conditions, stipulated in this report.

I

ANNEX I: Letter of Development Policy

REPÚBLICA DE MOÇAMBIQUE

MINISTÉRIO DA ECONOMIA E FINANÇAS

GABINETE DO MINISTRO

Letter nº 365/GM/MEF/2015

Maputo, November 18, 2015

Subject: Letter of Development Policy for the Economic Governance and Inclusive Growth

Program Phase II (EGIGP II)

1. I am writing on behalf of the Government of the Republic of Mozambique to request the budget

support operation – Economic Governance and Inclusive Growth Program phase II (EGIGP II) in

the amount of UA 15 million to support the implementation of the country’s Action Plan for Poverty

Reduction (PARP 2011-2015).

2. After successful democratic elections conducted in October 2014, His Excellency Filipe Jacinto

Nyusi was sworn in as a new President, and a new Government was inaugurated in January 2015.

A Five Year Government Plan 2015 - 2019 (Plano Quinquenal do Governo 2015-19) was approved

by the Parliament in April 2015.

3. We would like to commend the African Development Bank’s commitment to support our efforts to

reduce poverty over the years and the active participation in the budget support partners to

Mozambique, and signatory of the new Memorandum of Understanding between the Government

of Mozambique and the budget support development partners signed in 2015.

4. The Five Year Government Plan 2015 - 2019 (PQG 2015-19) HAS employment promotion,

productivity and competitiveness an overarching theme to achieve a more inclusive growth. The

PQG 2015-19 has five priorities: (i) consolidate national unity, peace and sovereignty, (ii) human

and social capital development, (iii) promote employment, and improve productivity and

competitiveness, (iv) economic and social infrastructure development and (v) ensure sustainable

and transparent management of natural and environmental resources. It has also three supporting

pillars which are: (a) consolidate the democratic rule of law, good governance and decentralization,

(b) promote a balanced and sustainable macroeconomic environment, and (c) reinforce international

cooperation. We are working with budget support development partners to develop a results

framework for budget support that is aligned with the PQG 2015-19 so that budget support is in

line with the country’s priorities. Departing from past experience, and in agreement with

development partners, we will not be preparing a poverty reduction strategy paper. This is in line

with the objectives of this operation, which is to support government efforts to improve the business

environment for private sector development, and strengthen transparency and accountability in the

management of public finance and natural resource management.

Macroeconomic context and outlook

5. Mozambique’s economy remains robust, with growth estimated at 7.2 percent in 2014, supported

by growth in the financial sector, agriculture and trade. Extractive industries continue to be a very

dynamic sector, but growth has slowed down as a result of low commodity prices and infrastructure

constraints. We expect developments in the mining and petroleum sectors to transform

II

Mozambique’s economy in the medium term, resulting in strong growth in coal production and

exports, the implementation of large infrastructure investments, including in LNG plants and

greater dynamism in the construction and transport sectors.

6. In line with developments around the world, growth in 2015 has decelerated in the first half of 2015

reaching 6.3 percent compared to 6.9 percent in the first half of 2014. The most dynamic sectors in

the second quarter of 2015 were extractive industries, construction, fisheries and electricity, gas and

water. We expect growth in 2015 to decelerate to 6.3 percent and to accelerate to around 8 percent

in the medium term, as investments in the extractive industries and related sectors (construction,

trade, transport) pick up and growth in some of the traditional sectors such as agriculture recovers.

7. Year on year inflation at the end of 2014 was 1.1 percent, well below BdM’s target of 5-6 percent.

Inflation remains low but has accelerated, reaching 2.41 (year-on-year) by September 2015. Low

inflation was supported by low commodity prices and relative stability against the South African

Rand, while the Metical has depreciated significantly against the US$ over the past year. After

several years of monetary easing, the central bank increased policy rates by 25 bps to 7.75 in

October 2015. We expect inflation between 5 and 6 percent over the next few years and we will

continue to monitor inflation and proactively coordinate fiscal and monetary policies. Monetary

policy will remain oriented toward achieving the objectives of keeping inflation low and stable,

safeguarding the financial system and encouraging lending. We will continue reforms to improve

operations in the financial system and broaden access to financial services.

8. In 2015 we have started a process of fiscal consolidation. Spending as a share of GDP will decline

by almost 7 percentage points of GDP to around 35 percent of GDP, narrowing the (after grants)

deficit from 10.1 percent of GDP to a projected 6 percent of GDP. We will continue to implement

a prudent fiscal policy in the medium term, with further declines in expenditure levels that, together

with increased revenue, will contribute to a narrowing of the fiscal deficit. These efforts will ensure

that the country maintains fiscal and macroeconomic stability.

9. Over the past few years we have seen a widening of the current account deficit, caused by significant

FDI inflows for the extractive industries, which by nature are capital- and import intensive. The

current account deficit widened to US$5.8 billion in 2014 or 34 percent of GDP. We expect the

deficit to narrow in 2015 on account of a reduction in investment in the coal and gas sectors.

Investments will pick up again in the second half of 2016 and onwards, with the current account

deficit widening again as the construction phase of the LNG development in the north of the country

starts. We expect the current account deficit to quickly narrow toward the end of the decade when

gas exports will start. Low commodity prices and lower than expected FDI inflows have put