Embed Size (px)

Citation preview

1 of 13

NAIC 2015 Spring Meeting Newsletter

“Working It Out” April 2015

Under the hot Arizona sun, the commissioners and participants certainly got their workout, both literally and figuratively, during the NAIC 2015 Spring Meeting. Amid the physical workout of walking two or three blocks in 90 degree heat between meeting locations, the commissioners were working out a common ground on the issues on their 2015 agenda. Overall, there were no significant changes or debates, primarily further clarification and implementation of adopted or exposed items from 2014.

As noted below, the NAIC certainly has a lot on their plate to handle between now and the Summer Meeting in Chicago in August. Therefore, we expect a lot of significant changes being implemented after the upcoming meeting.

Captive Insurance Update

XXX/AXXX Supplemental Reinsurance Exhibit

The 2015 XXX/AXXX supplemental reinsurance exhibit was adopted by the Principles Based Reserving (PBR) (EX) Task Force. The exhibit is intended to capture the reporting of XXX/AXXX reinsurance contemplated by the XXX/AXXX Reinsurance Transactions Framework (AG 48). The exhibit is similar to the 2014 XXX/AXXX exhibit, however, revisions are being considered. The Blanks (E) Working is considering having different disclosures for “grandfathered” transactions and the transactions that must comply with AG 48.

RBC Cushion

The determination of the RBC cushion described in AG 48 is still in process. The Life Risk-Based Capital (RBC) (E) Working Group has two primary tasks:

1. Identify an appropriate consequence for transactions that do not comply with the requirements of AG 48 and;

2. Develop a methodology to ensure that there are sufficient good assets backing the reserves in the covered transactions.

The second task addresses the fact that PBR approximates the 85th percentile of the distribution of the present value of future cash flows while RBC plus statutory reserves approximate the 95th percentile.

On its February 27, 2015 conference call, the Life RBC Working Group exposed for comment a proposal that removes the impact of a qualified actuarial opinion based solely on AG 48 and a proposal which increases the authorized control level RBC by the cumulative amount of all primary security shortfalls. The second proposal addresses the task to identify an effective incentive to encourage company compliance with AG 48. On its March 9, 2015 conference call, the Life RBC Working Group exposed for comment a consolidated RBC shortfall proposal which addresses bridging the percentile gap in the second task given to the Life RBC Working Group. This proposal creates a new RBC exhibit showing the RBC calculation and total adjusted capital for each captive reinsurer along with the ceding company. Any

Contents

Captive Insurance Update ....... 1

Principles-Based Reserving Implementation Update ............ 2

Private Equity Issues ............... 3

Capital Adequacy and Risk Based Capital ............................ 3

Terrorism Risk Update ............. 5

Executive Committee ............... 6

P&C Insurance Committee ...... 6

Other Committee and Working Group Highlights ...................... 6

NAIC 2015 Spring Meeting Newsletter

April 2015

2 of 13

cumulative RBC shortfall results in a reduction to the ceding company’s total adjusted capital. These three proposals were exposed for additional comment on a conference call held on April 8, 2015.

Amendments to Credit for Reinsurance Model Law

The Reinsurance (E) Task Force re-formed the XXX/AXXX Captive Reinsurance Regulation Drafting Group to present a draft regulation to the Task Force to establish requirements regarding the reinsurance of XXX/AXXX policies. A draft is planned to be presented at the 2015 NAIC Summer Meeting in August 2015.

“Primary Security” Definition

The Statutory Accounting Principles (E) Working Group (SAPWG) will be providing input during 2015 on the definition of a “primary security” in the development of the XXX/AXXX Reinsurance Model Regulation.

SAPWG also exposed revisions to the audited disclosures of SSAP 61R, Life, Deposit-Type Contracts and Accident and Health Reinsurance, to illustrate whether the securities backing ceded reserves are in compliance with AG48 or the proposed XXX/AXXX Reinsurance Model Regulation.

Captive Accreditation

The Financial Regulation Standards and Accreditation (F) Committee discussed the proposed Preamble that would include in the scope of the Accreditation Program captive insurers and special purpose vehicles that assume business written in accordance with Regulation XXX, Regulation AXXX, variable annuities valued under Actuarial Guidelines XLIII—CARVM for Variable Annuities (AG 43) and long-term care insurance valued under the Health Insurance Reserves Model Regulation (#10). The Committee discussed comments received and instructed NAIC staff to revise the Preamble to clarify that these are the only type of captives (other than risk retention groups) to be included in the scope of the Accreditation Program. A captive included in the Accreditation Program is treated the same as a multi-state insurer. The Committee is considering holding an interim meeting prior to the Summer National Meeting to discuss this issue further.

Principles-Based Reserving Implementation Update

Adoption Update

The PBR Task Force announced that approximately 23 states have adopted PBR legislation. During 2015, it is expected that 15 states will introduce legislation to adopt PBR. During 2016, it is expected that 4 states will adopt PBR legislation. If these 42 states adopt, approximately 80% of the premium will be represented. For PBR to become effective, 42 states representing 75% of premium most adopt. The PBR Task Force commented that it appears the industry is on track to have PBR become effective starting January 1, 2017, at the earliest.

Small Company Exemption

On a February 11, 2015 conference call, the PBR Task Force voted to adopt a small company exemption provision that was proposed by American Council of Life Insurers (ACLI). The following summarizes the regulatory criteria agreed by the PBR Task Force in regards a small company exemption:

Companywide Exemption: Unlike the existing product line exclusions, this small company exemption would apply to the entire company.

Exempt from Performing PBR Exclusion Tests: Rather than being exempted from the Valuation Manual entirely (and thus not subject to reporting requirements, etc.), the company would be exempted from performing PBR exclusion tests.

NAIC 2015 Spring Meeting Newsletter

April 2015

3 of 13

Premium threshold: A company’s ordinary life premiums must be less than $300 million for the legal entity and less than $600 million for the associated group.

RBC threshold: A company’s RBC must be at least 450%.

Universal Life with Secondary Guarantees (ULSGs): There can be no material ULSG business in-force.

Reserve methodology that applies for exempted companies: Commissioners Reserve Valuation Methodology (CRVM).

Location of Small Company Exemption: The exemption language will be included in the Valuation Manual as opposed to being added to the model Standard Valuation Law.

Private Equity Issues

The Private Equity Issues (E) Working Group (PEIWG) was appointed as part of the Financial Analysis (E) Working Group (FAWG), charged to develop procedures that regulators can use when considering ways to mitigate and monitor risk associated with private equity/hedge fund ownership and control of insurance company assets, including the development of best practices and consideration of possible changes in NAIC policy positions as deemed appropriate. During the 2015 Spring Meeting, PEIWG adopted amendments to the Financial Analysis Handbook, to guide examiners in evaluating the appropriate risks of an acquisition of an insurance company, including unique risks that would be relevant for the acquisition of an insurance company by a private equity firm.

Capital Adequacy and Risk Based Capital

The Capital Adequacy (E) Task Force had productive meetings in evaluating emerging risk, of which many changes were adopted upon the referral from the RBC Working Groups. These meetings included the evolving discussions of evaluating operational risk for RBC to be in line with international oversight; the impact of on-going discussions of the 2013-36 Investment Classification Project which may redefine investment definitions and ultimately redefine RBC charges in the future; and further the SAPWG charging the Capital Adequacy (E) Task Force to consider the need for a separate RBC charge for assets held on deposit with state departments for the benefit of all policyholders. Below is a summary of the motions from these meetings:

All Lines of Business

Under the direction of the Capital Adequacy (E) Task Force, the task force has exposed a 30-day comment period in regards to changes to the instructions for the RBC Jurat Page for all lines of business which would clarify RBC Jurat Page instructions and require RBC Jurat Page signatures to be in accordance with the requirements of Company’s domiciliary state.

Under the direction of the Capital Adequacy (E) Task Force, the task force has exposed a 30-day comment period in regards to changes to the instructions for the amounts reported in Total Adjusted Capital Less ACA fees as the amounts should equal those amounts disclosed in Note 22E in the Notes to the Annual Statement. The Statutory Accounting Principles (E) Working Group and the Blanks (E) Working Group are simultaneously exposing proposals to the disclosure in SSAP No. 106 and the annual statement Notes to Financial Statement, Note 22—Events Subsequent for the Federal Affordable Care Act 9010 Fee. The Blanks (E) Working Group will consider for adoption the proposal to the Notes to Financial Statement—Note 22 Events Subsequent on the 9010 Fee in June 2015. Capital Adequacy will consider the proposal for adoption if it is adopted by the Blanks Working Group.

Under the direction of the Capital Adequacy (E) Task Force, the task force has adopted changes to the instructions for the Management Discussion and Analysis RBC Instructions, indicating that the RBC Requirement, Total Adjusted Capital and RBC factors cannot be modified for the calculation of authorized control level. During the review of annual statement and RBC reporting, the staff noted that some companies were modifying the RBC requirement amount for the Calculation of Authorized Control Level

NAIC 2015 Spring Meeting Newsletter

April 2015

4 of 13

at the request of the domiciliary state. The NAIC staff reiterated permitted practices are not allowed for the Risk-Based Capital.

Life and Fraternal Entities

Under the direction of the Capital Adequacy (E) Task Force, the task force has adopted the Affordable Care Act Underwriting Risk and Risk Adjustment and Risk Corridor Sensitivity Test for Life entities RBC blanks. The adoption adds a new blanks page and instructions to the Life and Fraternal Risk-Based Capital Formulas for reporting year 2015. This breaks out premiums, claims and the loss ratio (LR) by individual, small group and large group plans as well as a break out of claims and the LR for Medicare, Medicaid and Other Health. These changes will provide regulators with a more granular view of a health entity’s overall writings as a result of the Federal Affordable Care Act (ACA). This page would be for informational purposes only for Life and Fraternal entities to complete beginning in reporting year 2015 and will allow regulators to analyze the potential impact that the ACA may have on health business written by the entity. Further, the adoption also adds a sensitivity test to reduce the total adjusted capital by either the receivable or payable for the risk adjustment and risk corridor in the ACA based on a 25% adjustment. The adoption allows regulators to identify the impact of the risk adjustment and risk corridor receivables and payables from the ACA on Total Adjusted Capital.

The Investment Risk-Based Capital (E) Working Group referred their March 28, 2015 report to the Capital Adequacy (E) Task Force in regards to Life Insurer RBC for Derivatives. Their report recommends (1) a change to the potential exposure formula for written credit default swaps, and (2) changes to RBC and AVR calculations to bring them into alignment with the associated risk and transactional changes mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act, specifically derivative collateral for over-the-counter, centrally-cleared derivatives.

The Life Risk-Based (E) Working Group continued discussions regarding the proposal to change RBC formulas for posted collateral on derivatives. The proposed change would exclude cash collateral pledged for derivative transactions from line (6.3) – Write-ins for Invested Assets in LR012 and add line (7.2) for derivative collateral pledged in LR017. It would also add line (17) in LR012, line (20) in LR017, and line 33 in the AVR blanks for centrally cleared derivatives. The proposed change would result in consistent reporting of cash pledged as collateral for derivative transactions and would eliminate the over-charging of risk for cash collateral. No adoption have made at this time.

Health Entities

Under the direction of the Capital Adequacy (E) Task Force, the task force has adopted changes to the Health RBC blanks to simplify the RBC charge for the ownership of Investment Affiliates (affiliate Type 5) to be a fixed factor times the carrying value of the common stock and preferred stock. The reason for this change is because the RBC charge for the ownership of the Investment Affiliate under the current Health RBC Instructions cannot be validated / verified.

The Health Risk-Based Capital (E) Working Group continued to discuss the excessive growth RBC charges for start-up companies for clarifying language to the instructions.

The group further set for exposure the instructions for clarification to the definition of Other Health Coverages on page XR012 & XR012A to address where companies should report life and property and casualty premiums in the Health RBC formulas.

Property & Casualty Entities

Under the direction of the Capital Adequacy (E) Task Force, the task force has adopted changes to the Property /Casualty RBC blanks. The adoption reflects (1) a new Underwriting Risk-Experience Fluctuation Risk PR020A and Risk Adjustment and Risk Corridor Sensitivity Test; (2) R6 and R7 Contingent Credit Risk Factors; (3) PR012A for Credit Risk for Informational purposes only; (4) Exemption Criteria to PR026 Interrogatory; 2015-04CR for Curve Sorting; and (5) Aggregate Exceedance Probability

NAIC 2015 Spring Meeting Newsletter

April 2015

5 of 13

(AEP) vs. Occurrence Exceedance Probability (OEP) for the Property/Casualty Risk-Based Capital (E) Working Group.

The task force adoption changes page PR026 to add a sensitivity test to reduce the total adjusted capital by either the receivable or payable for the risk adjustment and risk corridor in the ACA based on a 25% adjustment. The change allows regulators to identify the impact of the risk adjustment and risk corridor receivables and payables from the ACA on Total Adjusted Capital. Further, the change adds a new blanks page and instructions to the P/C Risk-Based Capital Formula for reporting year 2015. The new page is PR020A Underwriting Risk – Experience Fluctuation Risk. The change breaks out premiums, claims and the medical loss ratio (MLR) by individual, small group and large group plans as well as a break out of claims and the MLR for Medicare, Medicaid and Other Health. These changes provide regulators with a more granular view of a health entity’s overall writings as a result of the ACA. This page is for informational purposes only for P/C entities to complete beginning in reporting year 2015 and allows regulators to analyze the potential impact that the ACA has had on health business written by the entity.

The adoption revised the catastrophe contingent credit risk charge for modeled reinsurance recoverable in R6 and R7 from 0.100 to 0.048. This change applies a more appropriate factor for modeled reinsurance recoverables that reflects the underlying credit risk associated with highly rated reinsurers plus a margin for other than credit risk. This adoption is consistent with the methodology utilized to derive the R3 credit risk charge proposed in 2014-21P.

Next, the adopted changes would add a new page PR012A and R3A and R4A components in pages PR031 and 032 respectively for informational purposes only. This structure will allow regulators to analyze the potential impact to the RBC ratio based on the Reinsurance Association of America (RAA) new credit risk proposal.

Further, Instructions and Interrogatories have been added to the PR026 of the P/C Risk-Based Capital Formula and Instruction for reporting year 2015. These changes provide an exemption from completing PR026 by providing interrogatories to determine whether there is “substantive earthquake and hurricane risk exposure” based on minimum coverage exposure and surplus percentages of Insured Value - Property in Catastrophe-Prone Areas. In general, if a company uses an intercompany pooling arrangement or quota share arrangement with affiliates covering 100% of its earthquake and hurricane risks such that there is no exposure for these risks, then this page may be left blank. Further, the changes to the form and instructions for PR026 clarify issues related to EP curve sorting, calculation of the catastrophe contingent credit risk charge for reinsurance recoverables, and use of AEP and OEP model output. These revisions provide needed flexibility to companies by allowing them to employ catastrophe models for RBC in a manner that is consistent with the way the company internally evaluates and manages its modeled net catastrophe risk.

Further discussions from the Property and Casualty Risk-Based Capital (E) Working group included discussion to simplify the RBC charge for the ownership of Investment Affiliates (affiliate Type 7) to be a fixed factor times the carrying value of the common stock, preferred stock and bonds, as the current P&C RBC charge cannot be validated/verified. No adoptions were made at this time.

Terrorism Risk Update

In January 2015, the federal government passed the Terrorism Risk Insurance Reauthorization Act of 2015 (the “Act”). The Act extends the federal government’s terrorism risk coverage through December 31, 2020. In addition to extending the coverage, the Federal government added data reporting requirements in Section 111 of the Act. These additional data reporting requirements are meant to allow the Federal government and the Secretary of Treasury to perform studies on the effectiveness of the terrorism risk program for future extension considerations.

The requested data includes:

lines of insurance with exposure to such losses;

NAIC 2015 Spring Meeting Newsletter

April 2015

6 of 13

premiums earned on such coverage;

geographical location of exposures;

pricing of such coverage;

the take-up rate for such coverage;

the amount of private reinsurance for acts of terrorism purchased; and

such other matters as the Secretary considers appropriate

This data is required to be submitted annually starting in 2016, for 2015 data. The deadline for this data submission is June 30, 2016, and each year thereafter.

The Terrorism Insurance Implementation (C) Working Group is considering including this information as a data supplement to the Annual Statement blank. Further deliberations will occur over the next few months to develop a proposal for the 2015 Summer Meeting.

Executive Committee

During the Executive Committee meeting Commissioner McPeak of Tennessee reported that the Principle-Based Reserving Implementation (EX) Task Force met Feb. 11 and adopted the regulatory criteria for the PBR small company exemption. The current PBR exemptions are by product line. The main difference between the current exemptions and the small company exemption are discussed above under the Principle Based Reserving Implementation Update. The executive committee passed a motion to adopt the regulatory criteria for a small company exemption. In addition the Committee approved a model law development request to draft a new NAIC model to address the issue of unclaimed life insurance death benefits.

P&C Insurance Committee

The Property & Casualty Insurance (C) Committee adopted the Model Bulletin, Filing Procedures for Compliance with the Provisions of the Terrorism Risk Insurance Program Reauthorization Act of 2015

which requires filing updates for all property and casualty entities writing commercial line products.

Other Committee and Working Group Highlights

STATUTORY ACCOUNTING PRINCIPLES (E) WORKING GROUP AND EMERGING ACCOUNTING ISSUES (E) WORKING GROUP

This section summarizes the actions of the Statutory Accounting Working Group (SAPWG) and Emerging Accounting Issues Working Group (EAIWG) relating to the adoption or exposure of the Statements of Statutory Accounting Principles.

NAIC 2015 Spring Meeting Newsletter

April 2015

7 of 13

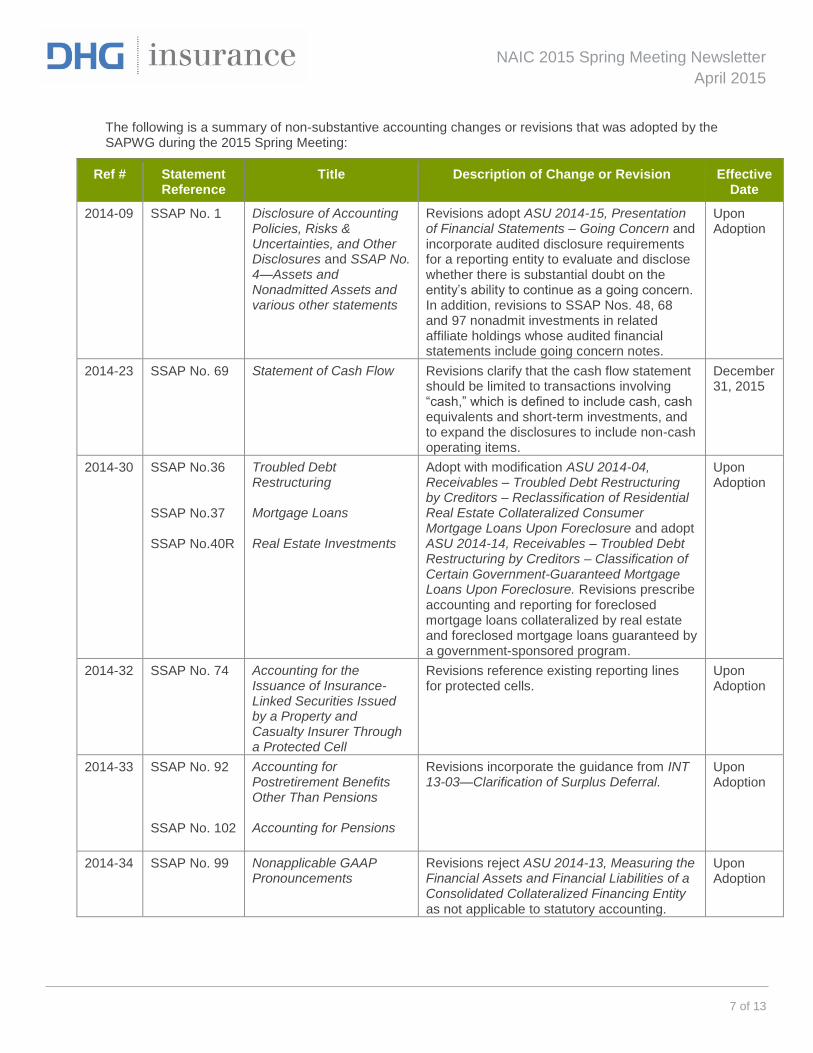

The following is a summary of non-substantive accounting changes or revisions that was adopted by the SAPWG during the 2015 Spring Meeting:

Ref # Statement Reference

Title Description of Change or Revision Effective Date

2014-09 SSAP No. 1 Disclosure of Accounting Policies, Risks & Uncertainties, and Other Disclosures and SSAP No. 4—Assets and Nonadmitted Assets and various other statements

Revisions adopt ASU 2014-15, Presentation of Financial Statements – Going Concern and incorporate audited disclosure requirements for a reporting entity to evaluate and disclose whether there is substantial doubt on the entity’s ability to continue as a going concern. In addition, revisions to SSAP Nos. 48, 68 and 97 nonadmit investments in related affiliate holdings whose audited financial statements include going concern notes.

Upon Adoption

2014-23 SSAP No. 69 Statement of Cash Flow Revisions clarify that the cash flow statement should be limited to transactions involving “cash,” which is defined to include cash, cash equivalents and short-term investments, and to expand the disclosures to include non-cash operating items.

December 31, 2015

2014-30 SSAP No.36 SSAP No.37 SSAP No.40R

Troubled Debt Restructuring Mortgage Loans Real Estate Investments

Adopt with modification ASU 2014-04, Receivables – Troubled Debt Restructuring by Creditors – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans Upon Foreclosure and adopt ASU 2014-14, Receivables – Troubled Debt Restructuring by Creditors – Classification of Certain Government-Guaranteed Mortgage Loans Upon Foreclosure. Revisions prescribe accounting and reporting for foreclosed mortgage loans collateralized by real estate and foreclosed mortgage loans guaranteed by a government-sponsored program.

Upon Adoption

2014-32 SSAP No. 74 Accounting for the Issuance of Insurance-Linked Securities Issued by a Property and Casualty Insurer Through a Protected Cell

Revisions reference existing reporting lines for protected cells.

Upon Adoption

2014-33 SSAP No. 92 SSAP No. 102

Accounting for Postretirement Benefits Other Than Pensions

Accounting for Pensions

Revisions incorporate the guidance from INT 13-03—Clarification of Surplus Deferral.

Upon Adoption

2014-34 SSAP No. 99 Nonapplicable GAAP Pronouncements

Revisions reject ASU 2014-13, Measuring the Financial Assets and Financial Liabilities of a Consolidated Collateralized Financing Entity as not applicable to statutory accounting.

Upon Adoption

NAIC 2015 Spring Meeting Newsletter

April 2015

8 of 13

2014-35 SSAP No. 11 Postemployment Benefits and Compensated Absences

Revisions delete disclosures that pertain to defined benefit and defined contribution plans, with a reference to complete the disclosures in SSAP No. 92 if the entity is providing special or contractual termination benefits.

Upon Adoption

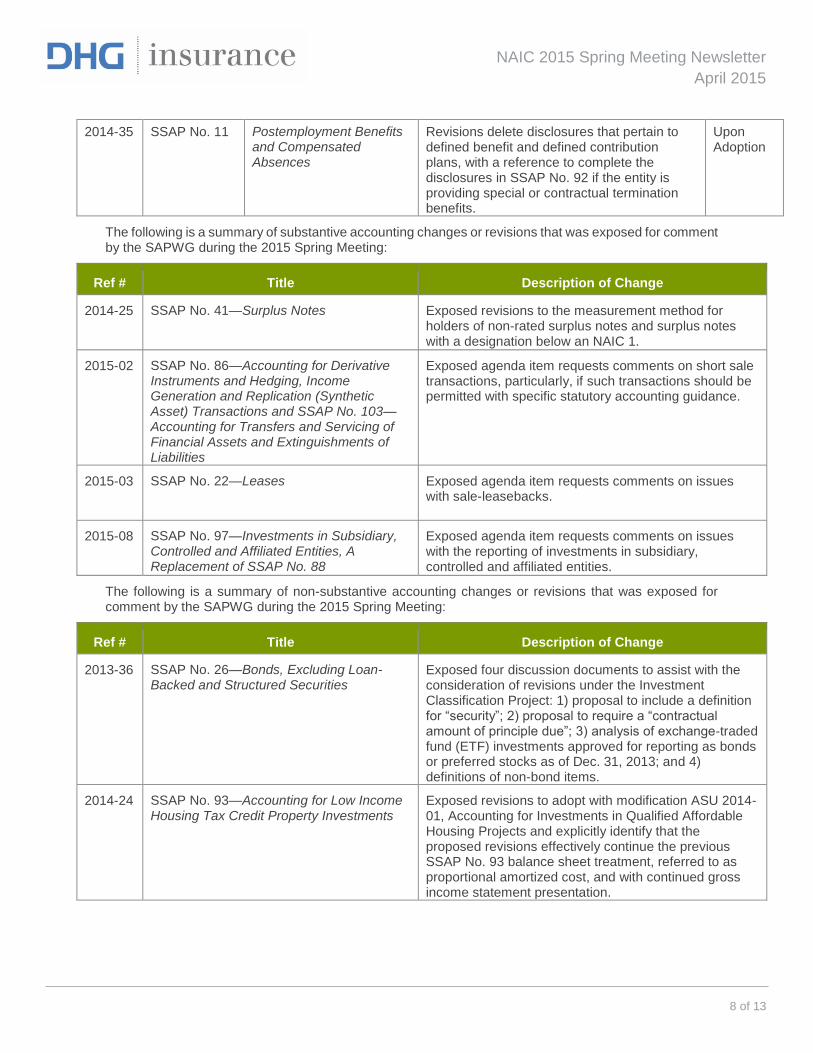

The following is a summary of substantive accounting changes or revisions that was exposed for comment by the SAPWG during the 2015 Spring Meeting:

Ref # Title Description of Change

2014-25 SSAP No. 41—Surplus Notes Exposed revisions to the measurement method for holders of non-rated surplus notes and surplus notes with a designation below an NAIC 1.

2015-02 SSAP No. 86—Accounting for Derivative Instruments and Hedging, Income Generation and Replication (Synthetic Asset) Transactions and SSAP No. 103—Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities

Exposed agenda item requests comments on short sale transactions, particularly, if such transactions should be permitted with specific statutory accounting guidance.

2015-03 SSAP No. 22—Leases Exposed agenda item requests comments on issues with sale-leasebacks.

2015-08 SSAP No. 97—Investments in Subsidiary, Controlled and Affiliated Entities, A Replacement of SSAP No. 88

Exposed agenda item requests comments on issues with the reporting of investments in subsidiary, controlled and affiliated entities.

The following is a summary of non-substantive accounting changes or revisions that was exposed for comment by the SAPWG during the 2015 Spring Meeting:

Ref # Title Description of Change

2013-36 SSAP No. 26—Bonds, Excluding Loan-Backed and Structured Securities

Exposed four discussion documents to assist with the consideration of revisions under the Investment Classification Project: 1) proposal to include a definition for “security”; 2) proposal to require a “contractual amount of principle due”; 3) analysis of exchange-traded fund (ETF) investments approved for reporting as bonds or preferred stocks as of Dec. 31, 2013; and 4) definitions of non-bond items.

2014-24 SSAP No. 93—Accounting for Low Income Housing Tax Credit Property Investments

Exposed revisions to adopt with modification ASU 2014-01, Accounting for Investments in Qualified Affordable Housing Projects and explicitly identify that the proposed revisions effectively continue the previous SSAP No. 93 balance sheet treatment, referred to as proportional amortized cost, and with continued gross income statement presentation.

NAIC 2015 Spring Meeting Newsletter

April 2015

9 of 13

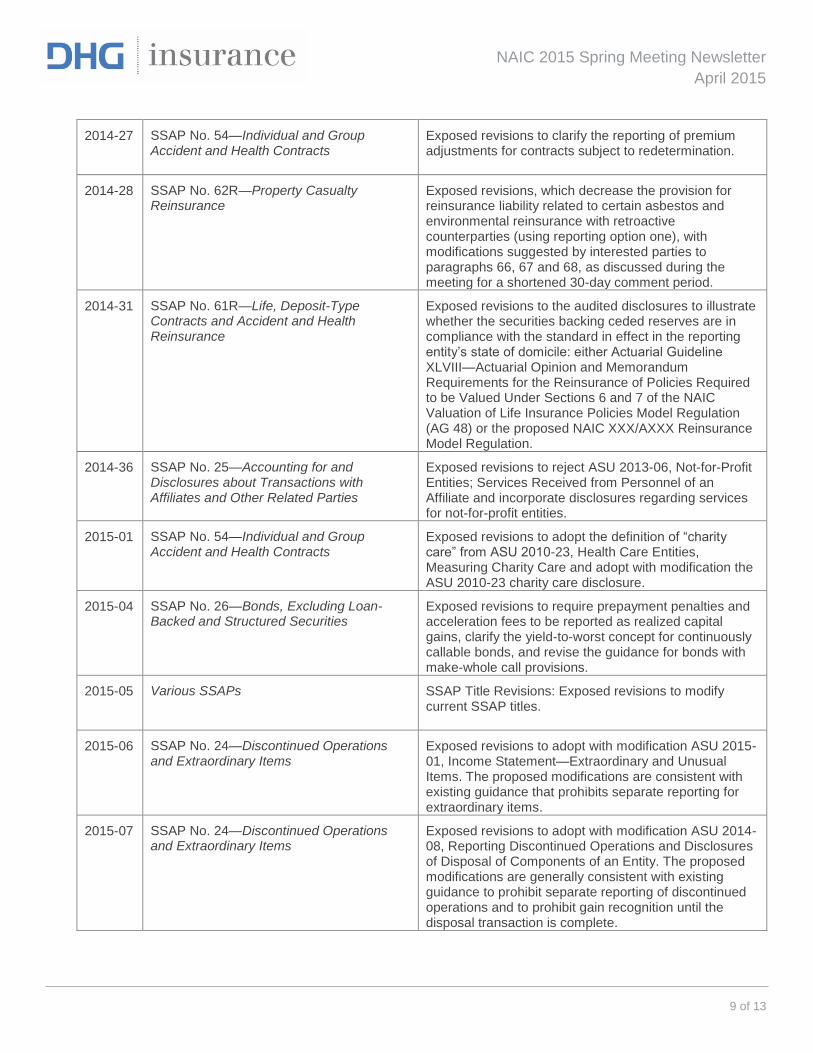

2014-27 SSAP No. 54—Individual and Group Accident and Health Contracts

Exposed revisions to clarify the reporting of premium adjustments for contracts subject to redetermination.

2014-28 SSAP No. 62R—Property Casualty Reinsurance

Exposed revisions, which decrease the provision for reinsurance liability related to certain asbestos and environmental reinsurance with retroactive counterparties (using reporting option one), with modifications suggested by interested parties to paragraphs 66, 67 and 68, as discussed during the meeting for a shortened 30-day comment period.

2014-31 SSAP No. 61R—Life, Deposit-Type Contracts and Accident and Health Reinsurance

Exposed revisions to the audited disclosures to illustrate whether the securities backing ceded reserves are in compliance with the standard in effect in the reporting entity’s state of domicile: either Actuarial Guideline XLVIII—Actuarial Opinion and Memorandum Requirements for the Reinsurance of Policies Required to be Valued Under Sections 6 and 7 of the NAIC Valuation of Life Insurance Policies Model Regulation (AG 48) or the proposed NAIC XXX/AXXX Reinsurance Model Regulation.

2014-36 SSAP No. 25—Accounting for and Disclosures about Transactions with Affiliates and Other Related Parties

Exposed revisions to reject ASU 2013-06, Not-for-Profit Entities; Services Received from Personnel of an Affiliate and incorporate disclosures regarding services for not-for-profit entities.

2015-01 SSAP No. 54—Individual and Group Accident and Health Contracts

Exposed revisions to adopt the definition of “charity care” from ASU 2010-23, Health Care Entities, Measuring Charity Care and adopt with modification the ASU 2010-23 charity care disclosure.

2015-04 SSAP No. 26—Bonds, Excluding Loan-Backed and Structured Securities

Exposed revisions to require prepayment penalties and acceleration fees to be reported as realized capital gains, clarify the yield-to-worst concept for continuously callable bonds, and revise the guidance for bonds with make-whole call provisions.

2015-05 Various SSAPs SSAP Title Revisions: Exposed revisions to modify current SSAP titles.

2015-06 SSAP No. 24—Discontinued Operations and Extraordinary Items

Exposed revisions to adopt with modification ASU 2015-01, Income Statement—Extraordinary and Unusual Items. The proposed modifications are consistent with existing guidance that prohibits separate reporting for extraordinary items.

2015-07 SSAP No. 24—Discontinued Operations and Extraordinary Items

Exposed revisions to adopt with modification ASU 2014-08, Reporting Discontinued Operations and Disclosures of Disposal of Components of an Entity. The proposed modifications are generally consistent with existing guidance to prohibit separate reporting of discontinued operations and to prohibit gain recognition until the disposal transaction is complete.

NAIC 2015 Spring Meeting Newsletter

April 2015

10 of 13

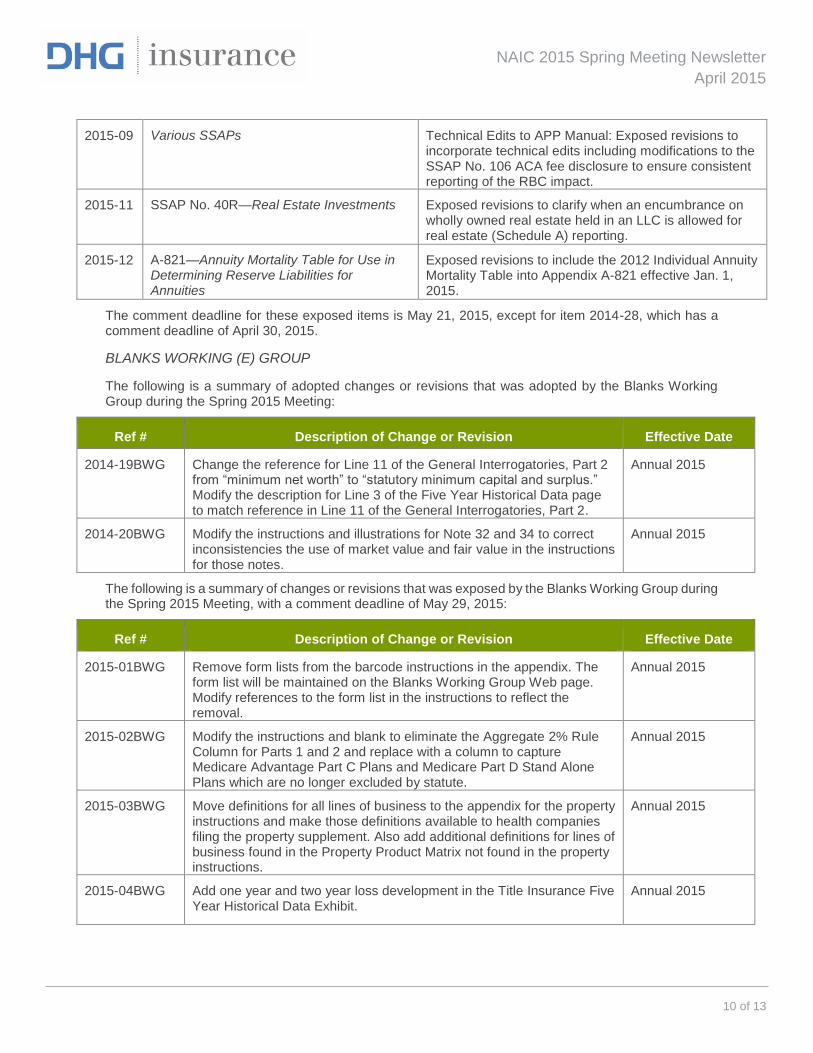

2015-09 Various SSAPs Technical Edits to APP Manual: Exposed revisions to incorporate technical edits including modifications to the SSAP No. 106 ACA fee disclosure to ensure consistent reporting of the RBC impact.

2015-11 SSAP No. 40R—Real Estate Investments Exposed revisions to clarify when an encumbrance on wholly owned real estate held in an LLC is allowed for real estate (Schedule A) reporting.

2015-12 A-821—Annuity Mortality Table for Use in Determining Reserve Liabilities for Annuities

Exposed revisions to include the 2012 Individual Annuity Mortality Table into Appendix A-821 effective Jan. 1, 2015.

The comment deadline for these exposed items is May 21, 2015, except for item 2014-28, which has a comment deadline of April 30, 2015.

BLANKS WORKING (E) GROUP

The following is a summary of adopted changes or revisions that was adopted by the Blanks Working Group during the Spring 2015 Meeting:

Ref # Description of Change or Revision Effective Date

2014-19BWG Change the reference for Line 11 of the General Interrogatories, Part 2 from “minimum net worth” to “statutory minimum capital and surplus.” Modify the description for Line 3 of the Five Year Historical Data page to match reference in Line 11 of the General Interrogatories, Part 2.

Annual 2015

2014-20BWG Modify the instructions and illustrations for Note 32 and 34 to correct inconsistencies the use of market value and fair value in the instructions for those notes.

Annual 2015

The following is a summary of changes or revisions that was exposed by the Blanks Working Group during the Spring 2015 Meeting, with a comment deadline of May 29, 2015:

Ref # Description of Change or Revision Effective Date

2015-01BWG Remove form lists from the barcode instructions in the appendix. The form list will be maintained on the Blanks Working Group Web page. Modify references to the form list in the instructions to reflect the removal.

Annual 2015

2015-02BWG Modify the instructions and blank to eliminate the Aggregate 2% Rule Column for Parts 1 and 2 and replace with a column to capture Medicare Advantage Part C Plans and Medicare Part D Stand Alone Plans which are no longer excluded by statute.

Annual 2015

2015-03BWG Move definitions for all lines of business to the appendix for the property instructions and make those definitions available to health companies filing the property supplement. Also add additional definitions for lines of business found in the Property Product Matrix not found in the property instructions.

Annual 2015

2015-04BWG Add one year and two year loss development in the Title Insurance Five Year Historical Data Exhibit.

Annual 2015

NAIC 2015 Spring Meeting Newsletter

April 2015

11 of 13

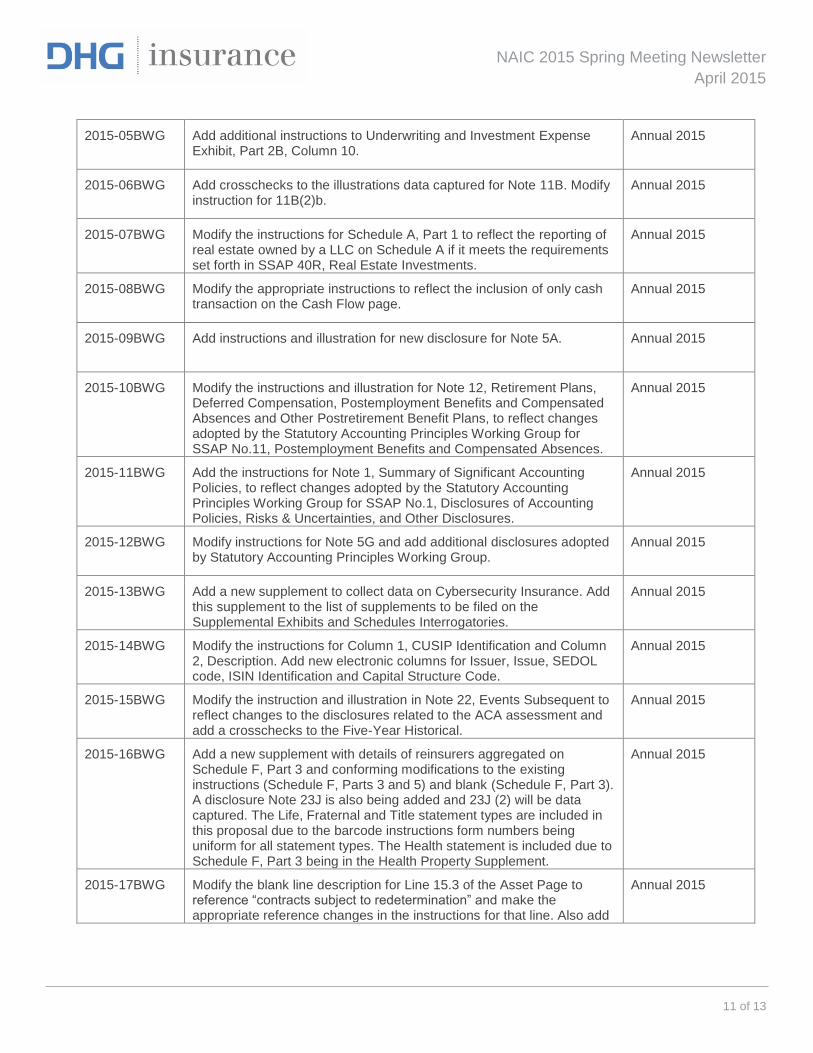

2015-05BWG Add additional instructions to Underwriting and Investment Expense Exhibit, Part 2B, Column 10.

Annual 2015

2015-06BWG Add crosschecks to the illustrations data captured for Note 11B. Modify instruction for 11B(2)b.

Annual 2015

2015-07BWG Modify the instructions for Schedule A, Part 1 to reflect the reporting of real estate owned by a LLC on Schedule A if it meets the requirements set forth in SSAP 40R, Real Estate Investments.

Annual 2015

2015-08BWG Modify the appropriate instructions to reflect the inclusion of only cash transaction on the Cash Flow page.

Annual 2015

2015-09BWG Add instructions and illustration for new disclosure for Note 5A. Annual 2015

2015-10BWG Modify the instructions and illustration for Note 12, Retirement Plans, Deferred Compensation, Postemployment Benefits and Compensated Absences and Other Postretirement Benefit Plans, to reflect changes adopted by the Statutory Accounting Principles Working Group for SSAP No.11, Postemployment Benefits and Compensated Absences.

Annual 2015

2015-11BWG Add the instructions for Note 1, Summary of Significant Accounting Policies, to reflect changes adopted by the Statutory Accounting Principles Working Group for SSAP No.1, Disclosures of Accounting Policies, Risks & Uncertainties, and Other Disclosures.

Annual 2015

2015-12BWG Modify instructions for Note 5G and add additional disclosures adopted by Statutory Accounting Principles Working Group.

Annual 2015

2015-13BWG Add a new supplement to collect data on Cybersecurity Insurance. Add this supplement to the list of supplements to be filed on the Supplemental Exhibits and Schedules Interrogatories.

Annual 2015

2015-14BWG Modify the instructions for Column 1, CUSIP Identification and Column 2, Description. Add new electronic columns for Issuer, Issue, SEDOL code, ISIN Identification and Capital Structure Code.

Annual 2015

2015-15BWG Modify the instruction and illustration in Note 22, Events Subsequent to reflect changes to the disclosures related to the ACA assessment and add a crosschecks to the Five-Year Historical.

Annual 2015

2015-16BWG Add a new supplement with details of reinsurers aggregated on Schedule F, Part 3 and conforming modifications to the existing instructions (Schedule F, Parts 3 and 5) and blank (Schedule F, Part 3). A disclosure Note 23J is also being added and 23J (2) will be data captured. The Life, Fraternal and Title statement types are included in this proposal due to the barcode instructions form numbers being uniform for all statement types. The Health statement is included due to Schedule F, Part 3 being in the Health Property Supplement.

Annual 2015

2015-17BWG Modify the blank line description for Line 15.3 of the Asset Page to reference “contracts subject to redetermination” and make the appropriate reference changes in the instructions for that line. Also add

Annual 2015

NAIC 2015 Spring Meeting Newsletter

April 2015

12 of 13

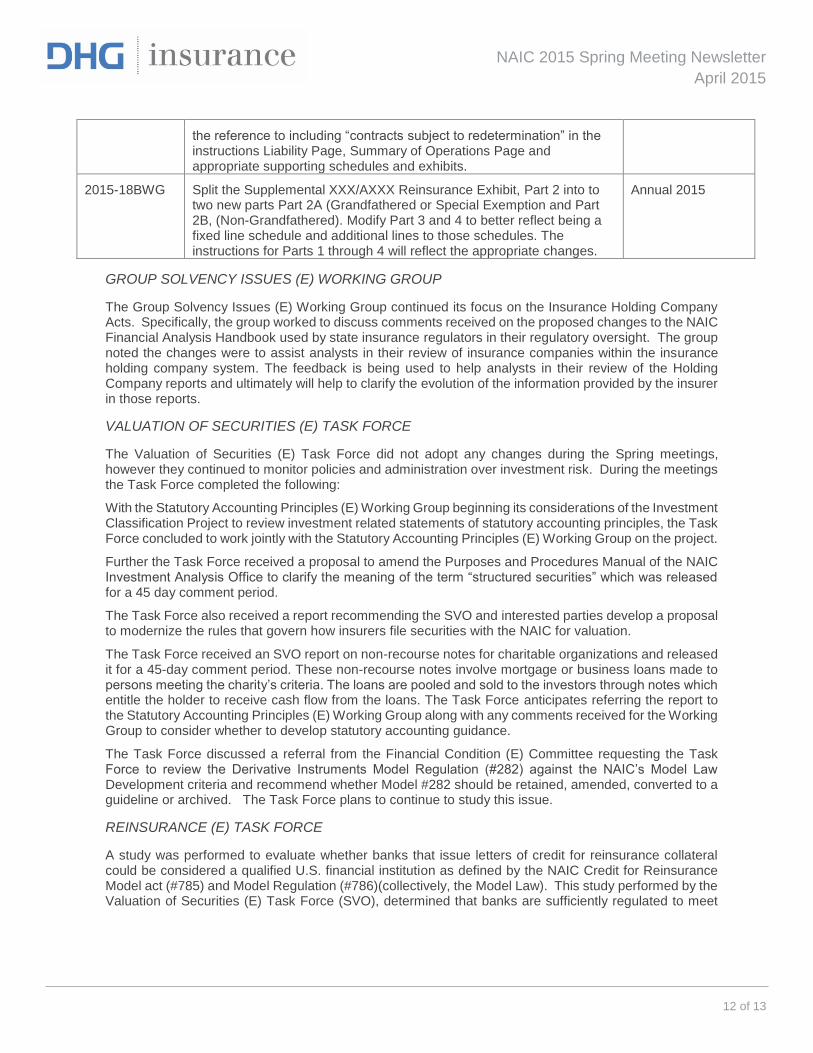

the reference to including “contracts subject to redetermination” in the instructions Liability Page, Summary of Operations Page and appropriate supporting schedules and exhibits.

2015-18BWG Split the Supplemental XXX/AXXX Reinsurance Exhibit, Part 2 into to two new parts Part 2A (Grandfathered or Special Exemption and Part 2B, (Non-Grandfathered). Modify Part 3 and 4 to better reflect being a fixed line schedule and additional lines to those schedules. The instructions for Parts 1 through 4 will reflect the appropriate changes.

Annual 2015

GROUP SOLVENCY ISSUES (E) WORKING GROUP

The Group Solvency Issues (E) Working Group continued its focus on the Insurance Holding Company Acts. Specifically, the group worked to discuss comments received on the proposed changes to the NAIC Financial Analysis Handbook used by state insurance regulators in their regulatory oversight. The group noted the changes were to assist analysts in their review of insurance companies within the insurance holding company system. The feedback is being used to help analysts in their review of the Holding Company reports and ultimately will help to clarify the evolution of the information provided by the insurer in those reports.

VALUATION OF SECURITIES (E) TASK FORCE

The Valuation of Securities (E) Task Force did not adopt any changes during the Spring meetings, however they continued to monitor policies and administration over investment risk. During the meetings the Task Force completed the following:

With the Statutory Accounting Principles (E) Working Group beginning its considerations of the Investment Classification Project to review investment related statements of statutory accounting principles, the Task Force concluded to work jointly with the Statutory Accounting Principles (E) Working Group on the project.

Further the Task Force received a proposal to amend the Purposes and Procedures Manual of the NAIC Investment Analysis Office to clarify the meaning of the term “structured securities” which was released for a 45 day comment period.

The Task Force also received a report recommending the SVO and interested parties develop a proposal to modernize the rules that govern how insurers file securities with the NAIC for valuation.

The Task Force received an SVO report on non-recourse notes for charitable organizations and released it for a 45-day comment period. These non-recourse notes involve mortgage or business loans made to persons meeting the charity’s criteria. The loans are pooled and sold to the investors through notes which entitle the holder to receive cash flow from the loans. The Task Force anticipates referring the report to the Statutory Accounting Principles (E) Working Group along with any comments received for the Working Group to consider whether to develop statutory accounting guidance.

The Task Force discussed a referral from the Financial Condition (E) Committee requesting the Task Force to review the Derivative Instruments Model Regulation (#282) against the NAIC’s Model Law Development criteria and recommend whether Model #282 should be retained, amended, converted to a guideline or archived. The Task Force plans to continue to study this issue.

REINSURANCE (E) TASK FORCE

A study was performed to evaluate whether banks that issue letters of credit for reinsurance collateral could be considered a qualified U.S. financial institution as defined by the NAIC Credit for Reinsurance Model act (#785) and Model Regulation (#786)(collectively, the Model Law). This study performed by the Valuation of Securities (E) Task Force (SVO), determined that banks are sufficiently regulated to meet

NAIC 2015 Spring Meeting Newsletter

April 2015

13 of 13

the requirements of the Model Law. Therefore, the SVO has referred to the Reinsurance (E) Task Force to discuss expanding the NAIC Bank List into a List of Qualified U.S. Financial Institutions.

CYBERSECURITY (EX) TASK FORCE

On November 19, 2014, the NAIC established the Cybersecurity (EX) Task Force under the Executive (EX) Committee which is charged with coordinating the efforts of the NAIC on cyber threats and monitoring the development in the area of cybersecurity. Issues facing the cybersecurity include the monitoring of cyber liability policies, the protection of policyholder information, and supervision of those efforts. The task force set forth its Principles for Effective Cybersecurity Insurance Regulation Guidance which is open for comments by interested parties.

Insurance Services Group Contacts and Contributors

John Roberts - Partner

1829 Eastchester Drive High Point, NC 27265 336-822-4482 [email protected]

Kevin Lee Ryals - Partner

214 N Tryon St Suite 2200 Charlotte, NC 28202 704-367-7043 [email protected]

Brian Kilbane – Sr. Manager

225 Peachtree Street NE Suite 300 Atlanta, GA 30303 404-575-8954 [email protected]

Brian Smith – Manager

1901 Ulmerton Road Suite 400 Clearwater, FL 33762 727-223-6246 [email protected]

2015 Dixon Hughes Goodman LLP

About Dixon Hughes Goodman LLP: With more than 1,800 people in 12 states, Dixon Hughes Goodman ranks among the nation’s top 20 public accounting firms. Offering comprehensive assurance, tax and advisory services, the firm focuses on major industry lines and serves clients in all 50 states as well as internationally. Visit www.dhgllp.com for additional information.