Embed Size (px)

Citation preview

2002 Annual Report on German Cooperation with Developing Countries.

For Development with a Future.

New Energy

F O R E I G N O F F I C E S O F T H E K F W G R O U P

Afghanistan: KfW Office KabulDirector: Martin Jenner

Egypt: KfW/DEG Office CairoDirector: Jan Blum

Belgium: Liaison Office to the EU, BrusselsDirector: Stephan Sellen

Bolivia: KfW Office La PazDirector: Stefan Zeeb

Bosnia and Herzegovina: KfW Office SarajevoDirector: Frank Bellon

Brazil: KfW Office BrasíliaDirector: Dietmar Wenz

Brazil: DEG/KfW Office São PauloDirector (KfW): Volker WiederholdDirector (DEG): Thomas Kessler

China: KfW/DEG Office BeijingDirector (KfW): Dr. Karl-Joachim TredeDirector (DEG): Markus tho Pesch

Côte d’Ivoire: KfW Office Abidjan (relocatedto Dakar, Senegal, in 8/2003, currently inAccra, Ghana)Director: Bruno Schoen

Guatemala: KfW Office Guatemala CityDirector: Helge Jahn

India: KfW/DEG Office New DelhiDirector (KfW): Andrea JohnstonDirector (DEG): Hans-Georg Hansmann

Indonesia: KfW/DEG Office JakartaDirector (KfW): Jens ClausenDirector (DEG): Wilhelm Icke

Jordan: KfW Office AmmanDirector: Reinhard Schmidt

Cambodia: KfW Office Phnom PenhDirector: Dr. Klaus Müller

Kenya: KfW/DEG Office NairobiDirector: Oskar von Maltzan

Kosovo: KfW Office PristinaDirector: Dr. Johannes Feist

Macedonia: KfW Office SkopjeDirector: Dr. Christian Lütke-Wöstmann

Mexico: DEG Office MexicoDirector: Armin Albert (from 8/2003)

Montenegro: KfW Office PodgoricaDirector: Frank Bellon

Nicaragua: KfW Office ManaguaDirector: Helge Jahn

Palestinian Territories: KfW Office Al BirehDirector: Reinhard Schmidt

Peru: KfW Office LimaDirector: Stefan Zeeb

Serbia: KfW/DEG Office BelgradeDirector: Dr. Johannes Feist

South Africa: DEG/KfW Office JohannesburgDirector: Beate Baethke

Tanzania: KfW Office Dar es SalaamDirector: Oskar von Maltzan

Thailand: KfW/DEG Office BangkokDirector (KfW): Andreas Klocke Director (DEG): Herbert Jäger

Turkey: KfW Office AnkaraDirector: Burkhard Hinz

Vietnam: KfW Office HanoiDirector: Dr. Klaus Müller

Addresses, phone numbers and e-mail addresses of our foreign offices are available at:

www.deginvest.de/german/home/Service//Kontakt/Aussenbueros/index.htmlwww.kfw.de/DE/Entwicklungszusammenarbeit/Kontakt3/Auslandsbr.jsp

x Nairobi

x Dar Es Salaamx

Jakarta

x Phnom Penh

x Hanoi

x Bangkok

xNew Delhi

Beijing x

Cairo x

xJohannesburg

x La Paz

x São Paulo

xBrasilia

Lima x

Ankarax

x xx

Sarajevo Belgrade

PristinaPodgorica

x

x

Skopje

x Main locations (25)

xAbidjan

Managua x

Guatemala City x

Kabul x

x

Al Bireh

Amman

Pristina

x

Situation as per May 2003

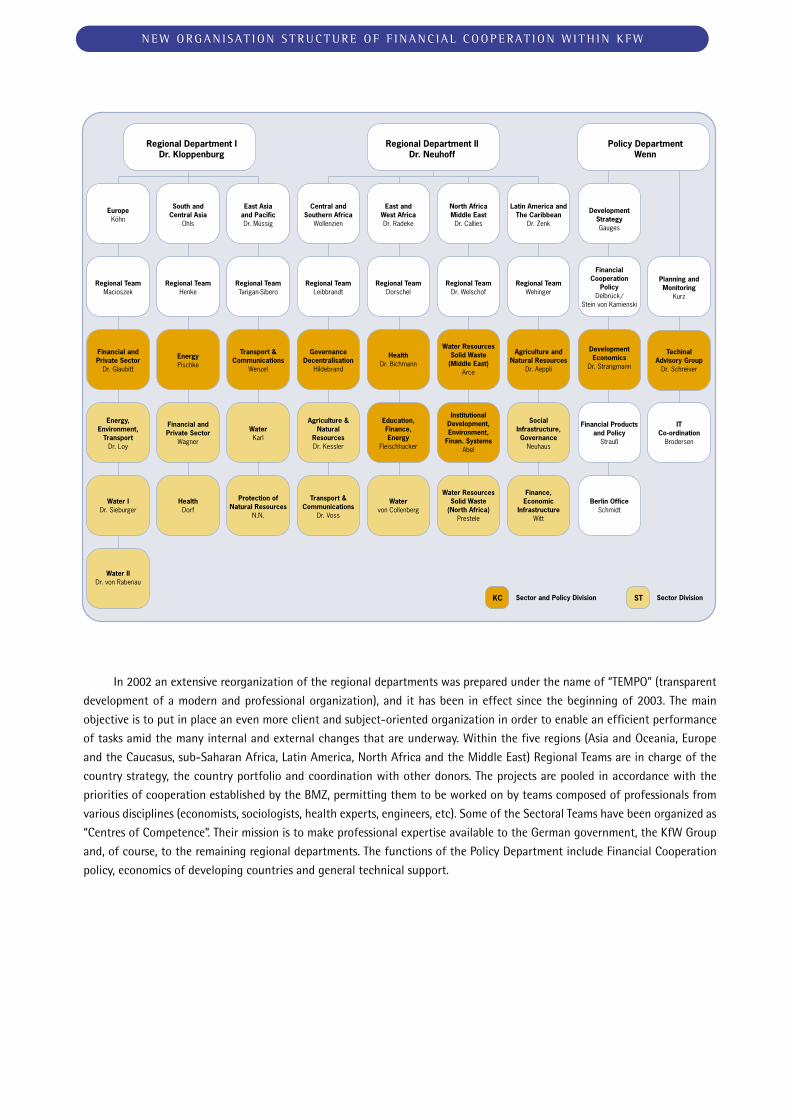

In 2002 an extensive reorganization of the regional departments was prepared under the name of “TEMPO” (transparent

development of a modern and professional organization), and it has been in effect since the beginning of 2003. The main

objective is to put in place an even more client and subject-oriented organization in order to enable an efficient performance

of tasks amid the many internal and external changes that are underway. Within the five regions (Asia and Oceania, Europe

and the Caucasus, sub-Saharan Africa, Latin America, North Africa and the Middle East) Regional Teams are in charge of the

country strategy, the country portfolio and coordination with other donors. The projects are pooled in accordance with the

priorities of cooperation established by the BMZ, permitting them to be worked on by teams composed of professionals from

various disciplines (economists, sociologists, health experts, engineers, etc). Some of the Sectoral Teams have been organized as

“Centres of Competence”. Their mission is to make professional expertise available to the German government, the KfW Group

and, of course, to the remaining regional departments. The functions of the Policy Department include Financial Cooperation

policy, economics of developing countries and general technical support.

N E W O R G A N I S AT I O N S T R U C T U R E O F F I N A N C I A L C O O P E R AT I O N W I T H I N K F W

Regional TeamHenke

Regional TeamTarigan-Sibero

Regional TeamLeibbrandt

Regional TeamDorschel

Regional TeamDr. Welschof

Regional TeamWehinger

FinancialCooperation

PolicyDelbrück/

Stein von Kamienski

EnergyPischke

Transport &Communications

Wenzel

HealthDr. Bichmann

Water ResourcesSolid Waste

(Middle East)Arce

Agriculture andNatural Resources

Dr. Aeppli

DevelopmentEconomics

Dr. Strangmann

GovernanceDecentralisation

Hildebrand

Financial andPrivate Sector

Wagner

WaterKarl

Agriculture &Natural

ResourcesDr. Kessler

Education,Finance,Energy

Fleischhacker

InstitutionalDevelopment,Environment,

Finan. SystemsAbel

SocialInfrastructure,Governance

Neuhaus

Financial Productsand Policy

Strauß

HealthDorf

Protection ofNatural Resources

N.N.

Transport &Communications

Dr. Voss

Watervon Collenberg

Water ResourcesSolid Waste

(North Africa)Prestele

Finance,Economic

InfrastructureWitt

Berlin OfficeSchmidt

ST Sector DivisionKC Sector and Policy Division

Regional Department IDr. Kloppenburg

East Asiaand PacificDr. Müssig

Central andSouthern Africa

Wollenzien

East andWest AfricaDr. Radeke

North AfricaMiddle East

Dr. Callies

Latin America andThe Caribbean

Dr. Zenk

DevelopmentStrategyGauges

EuropeKöhn

South andCentral Asia

Ohls

Regional Department IIDr. Neuhoff

Policy DepartmentWenn

Planning andMonitoring

Kurz

TechinalAdvisory Group

Dr. Schreiver

ITCo-ordination

Brodersen

Water IIDr. von Rabenau

Regional TeamMacioszek

Financial andPrivate Sector

Dr. Glaubitt

Energy,Environment,

TransportDr. Loy

Water IDr. Sieburger

CONTENT

1. Overview 2

2. Activites of KfW and DEG in Development Cooperation 4Guided by the Goals of the Millennium Declaration 4

Activities in Figures 5

National and international Cooperation 8

Message of Greeting on the Cooperation with AFD 9

Main Themes of the Year 2002 10

3. Promotion Energy Efficiency, Renewable Energies and Climate Protection 12Energy and Sustainable Development 12

Strategies for a Sustainable Energy Supply 16

Guest Contribution to AREED Initiative, Senegal 16

Project Examples:Serbia: District Heating in Cold Winter 23

Bangladesh: Clean and Efficient Power Generation by the Private Sector 24

China I: Modernized Coal-Fired Power Plants for Cleaner Air and More Energy 25

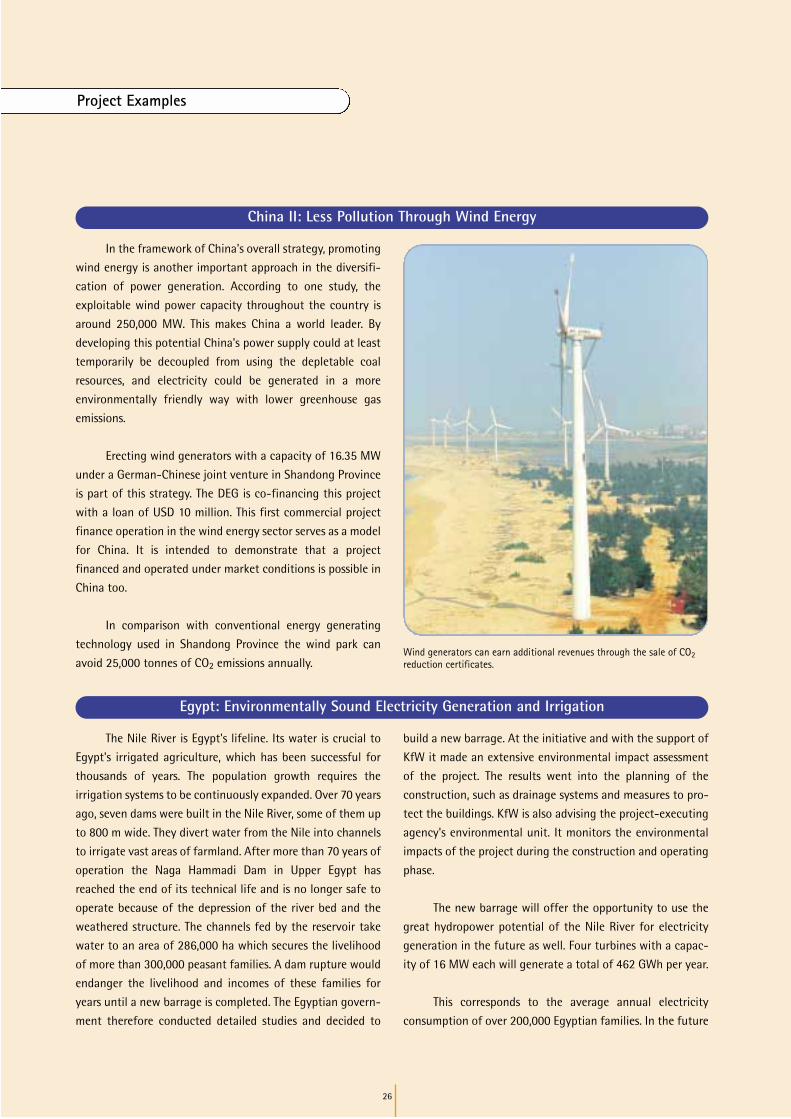

China II: Less Pollution Through Wind Energy 26

Egypt: Environmentally Sound Electricity Generation and Irrigation 26

Kenya: Geothermal Energy – Heat from the Earth for a Clean Environment 27

Morocco: Energy from the Sun and the Wind 28

South Africa: Electricity from Solar Home Systems for Remote Regions 28

India: Renewable Energies are Making Headway 29

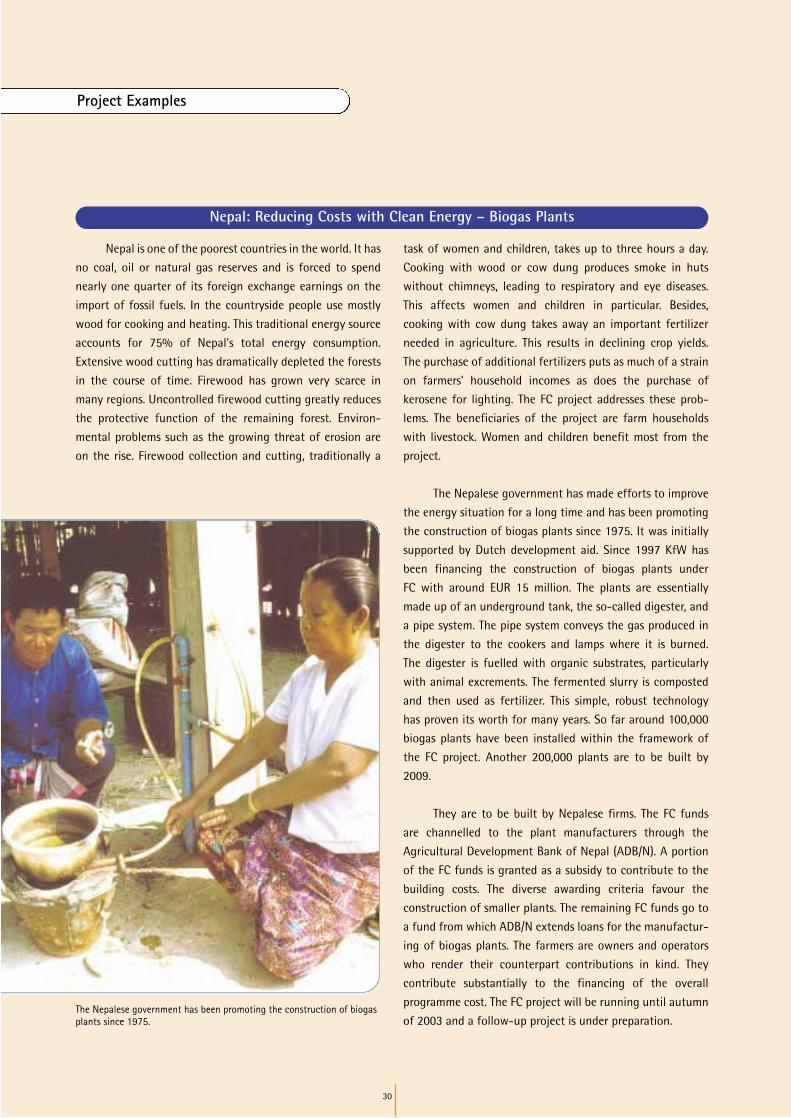

Nepal: Reducing Costs with Clean Energy – Biogas Plants 30

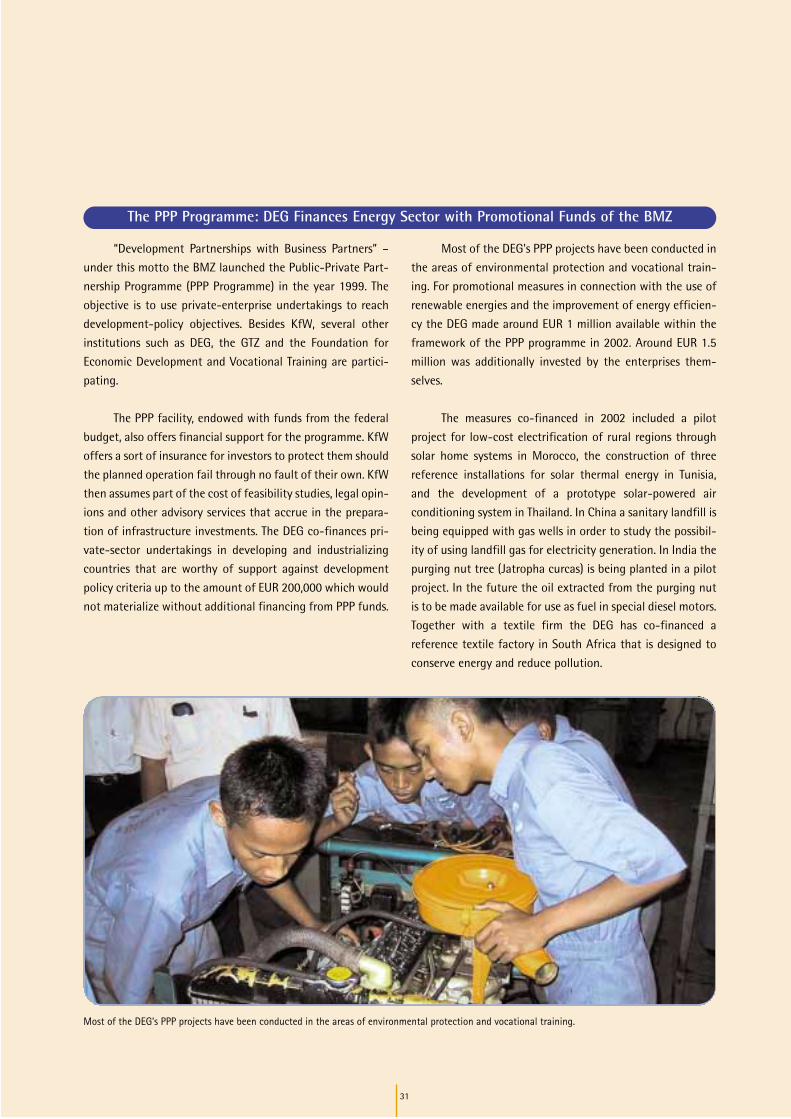

The PPP Programme: DEG Finances Energy Sector with Promotional Funds of the BMZ 31

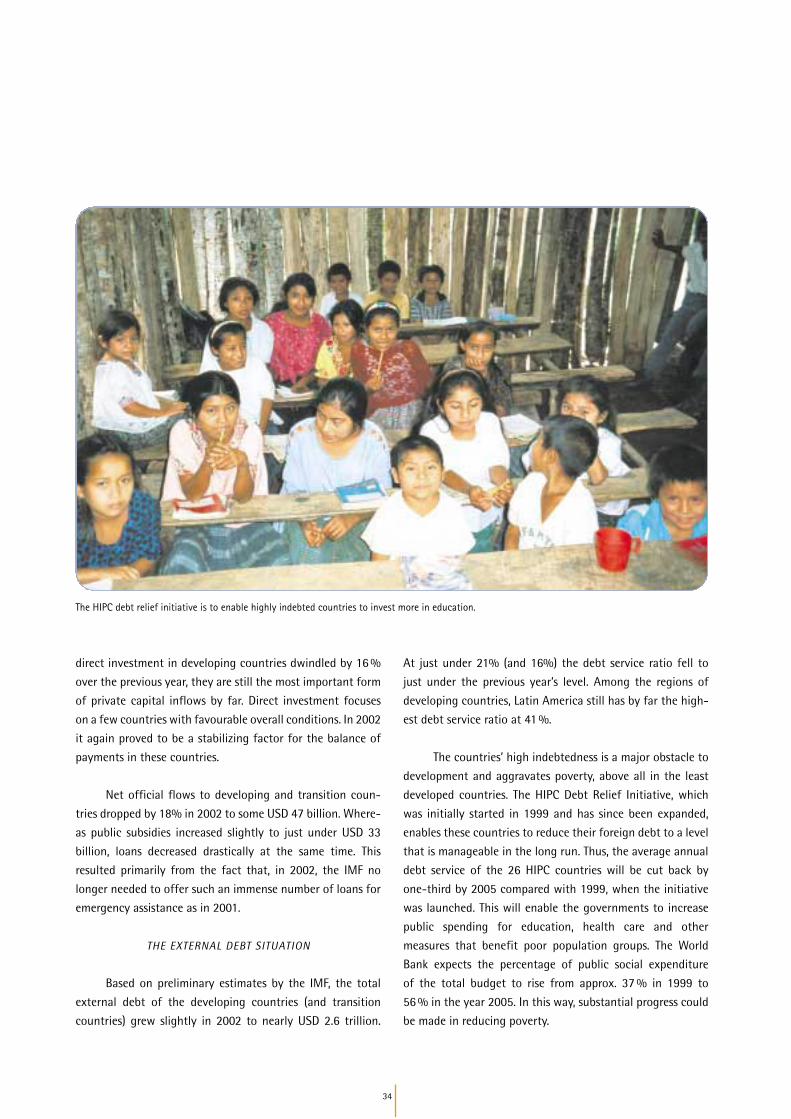

4. Regional Perspectives 32The Situation of the Developing Countries and the Transition Countries 32

Regional Development in Sub-Saharan Africa 35

Project Example Mozambique 42

Regional Development in North Africa and the Middle East 45

Regional Development in Asia 47

Regional Development in Latin America 50

Regional Development of the European Transition Countries 52

Statistical Appendix 54

Preface 1

“One World – German Development Cooperation: shaping

globalization, fighting poverty, securing peace” was formulated as the

new guiding message by the German Ministry for Economic Coope-

ration and Development (BMZ). KfW and the DEG are working jointly

on this task with all their financing instruments under the umbrella

of the KfW Group. We understand the guiding message of the BMZ

at once as a mission and a high standard which we can fulfil only

in concert with the people and the governments of the partner

countries.

Under politically and economically difficult global conditions

we continued to pursue the overriding objective of reducing poverty

in the year under review as well. The Millennium Goals with their

concrete indicators provide the necessary orientation also for the

future. The global fight against poverty eases social and economic

tension and reduces ecological risks. Without closing the gap between

rich and poor it will not be possible to bring about lasting peace.

The focal themes of the present 2002 Annual Report address

important issues of globalization and poverty reduction:

• Chapter 3 presents strategies and opportunities for sustainable

energy supplies in developing countries. As the world’s leading

bilateral financier of renewable energies the KfW Group offers

comprehensive expertise and innovative approaches.

• Chapter 4 focuses on the development in sub-Saharan Africa and

presents hopeful trends and adapted cooperation strategies.

These topics make it particularly clear that bilateral develop-

ment cooperation makes a significant contribution to shaping global

development policy.

Wolfgang Kroh

(Member of the Board of

Managing Directors of KfW)

Dr. Winfried Polte

(Chairman of the Board of

Management of DEG)

1

PREFACE

Wolfgang Kroh

Dr. Winfried Polte

2

GOALS

For development cooperation (DC), poverty reduction

continues to be the main objective. The global fight against

poverty reduces social and economic tension, secures peace

and durably mitigates risks to the environment. To achieve

this the German government supports the so-called

“Millennium Development Goals” (MDG), which were adopt-

ed in a declaration of 189 states at the Millennium Summit

of the United Nations in September 2000.

FOREIGN REPRESENTATIONS

The foreign representations of KfW and DEG were

further expanded in 2002. The KfW Group is currently

represented in 25 developing countries. Having a local

presence makes it easier to participate intensively in the

sector dialogue and to coordinate projects and programmes

with other bilateral and multilateral DC institutions.

COMMITMENTS IN A DIFFICULT

ENVIRONMENT

Last year KfW provided around EUR 1.3 billion in new

commitments for the promotion of developing countries

(EUR 3.0 billion in the previous year). Adjusted for a special

loan to the IMF totalling around EUR 1.4 billion last year,

commitments in 2002 were around EUR 300 million lower

than the year before. Commitments from budget funds of the

BMZ were around 7 % below the previous year’s level, at

EUR 971 million (EUR 1,040 million), mostly as a result of

project-related reallocations. Despite the difficult global

economic environment the DEG achieved its highest commit-

ment volume so far, at EUR 464 million (EUR 412 million). The

biggest share of total commitments made by KfW and DEG

went to partner countries in Asia, followed by Europe/the

Caucasus and sub-Saharan Africa.

PRIORITY SECTOR:

SOCIAL INFRASTRUCTURE

The sectoral distribution of KfW’s commitments in 2002

was characterized by the very high volume of commitments

for social infrastructure in the areas of water supply, sanita-

tion, education and health care. DEG financed mainly the

producing sector, followed by the financial sector.

With a share of 49 % (46 %) almost half of the FC

financing volume was invested in the cross-cutting area

“poverty reduction”. Around 37 % of the funds were applied

with the explicit or secondary goal of protecting the environ-

ment and natural resources.

MORE PARTNERSHIPS AND DELEGATION OF

ACTIVITIES

In a number of cooperative projects, cofinancings and

partnerships, the KfW Group is combining its competence

with the specific strengths of other financing institutions.

Chief among these partnerships is the close cooperation with

the GTZ (Deutsche Gesellschaft für Technische Zusammen-

arbeit – German Agency for Technical Cooperation). Both

institutions are supporting the BMZ through an intensive

cooperation above and beyond the project level. For over

30 years KfW has maintained good relations with the French

development bank AFD which in the meantime have lead to

a number of joint projects and mandates exchanged between

both agencies. The subsidiaries of the two agencies in charge

of private sector finance, DEG and PROPARCO, have joined

similar institutions to form the Association of European

Development Finance Institutions (EDFI). Partnerships enable

more efficient and effective work in developing countries.

Eradicating poverty is the most important objective of developmentcooperation.

1. OVERVIEW

PREVENTING CRISES BY MAKING POVERTY

REDUCTION A DEVELOPMENT GOAL

A development policy that seeks to eradicate poverty

can offer new perspectives to many people, improve their

living conditions noticeably and thereby contribute towards

securing peace. This is necessary particularly in crisis situa-

tions – even if development policy cannot solve the intri-

cately connected problems and causes by itself and, most

importantly, without the active participation of the local

population. In addition to our commitment to securing the

peace in Central America, the Palestinian Territories and in the

framework of the Stability Pact for Southeastern Europe, this

is illustrated very strongly by the example of Afghanistan.

Here KfW and the GTZ have a local office since January 2002.

The first projects have already been implemented successfully.

ENERGY EFFICIENCY, RENEWABLE ENERGIES

AND CLIMATE PROTECTION

Sustainable and efficient use of energy is one of the

great challenges for developing countries as well. Climate

protection concerns all of us. Because of their geography

and economic structure, developing countries in particular

have greater difficulty in adapting to the possible effects of

climate change than the industrialized countries. As energy

sources dwindle and energy prices rise, these countries are

seizing the opportunity of applying new technologies to make

rational and efficient use of environmentally friendly and

efficient forms of energy. The main focus of this report lies

on the discussion of problems and possible solutions for a

sustainable energy supply. It has to be achieved with energy

sources of the future – promoting them is an important task

of development cooperation.

IN FOCUS: DEVELOPMENT COOPERATION

WITH SUB-SAHARAN AFRICA

Public opinion literally perceives sub-Saharan Africa as

the "black continent": marginalized from the world economy,

disrupted by violent conflicts, with no hope for an end to

poverty. But hopeful developments are taking place, even

though this region has not remained unscathed by the

consequences of the downswing of the world economy. The

differences in the development of the countries of this region

have become even greater than in the past years. The coun-

tries that have achieved the highest growth rates are those

with reforms firmly in place and above-average political

stability. Sub-Saharan Africa is the main focus area in the

regional section of this report.

3

Climate protection concerns all of us – droughts have devastating consequences for people and the environment.

4

The German federal government has committed itself in

the context of development cooperation (DC) to pursue the

overriding goal of poverty reduction. The global fight against

poverty reduces social and economic tension and durably

mitigates risks to the environment. Securing peace in the long

run is not possible without reducing the gap between rich and

poor. To achieve this the German government supports the

goals of the Millennium Declaration, which was adopted by

189 states at the Millennium Summit of the United Nations

in September 2000. The “Millennium Development Goals”

(MDG) formulated on the basis of this declaration were tak-

en up in the German federal government’s action programme

to reduce poverty by 2015. The MDGs (see box) and the pover-

ty reduction strategies of our partner countries, which are of-

ten laid down in “poverty reduction strategy papers” (PRSP),

constitute the reference framework for all protagonists in DC.

In the context of enhanced donor coordination the

MDGs are also an important yardstick for the orientation of

the work of KfW, which implements Financial Cooperation

(FC) on behalf of the German government. KfW participates

in expert discussions on developmental priorities, checks

whether strategies, programmes and projects are eligible for

promotion from a development-policy perspective, finances

and supports their implementation and, finally, evaluates

every project for its developmental effectiveness and its

contribution to reducing poverty.

INTEGRATION OF DEG IS BEING

CONTINUED

Since the integration of DEG into the KfW Group in

2001 both companies have closely coordinated their pro-

motional instruments and the products they offer to the

developing countries. In the framework of FC KfW concen-

trates on projects in the public sector and finances mainly

projects in the field of social and economic infrastructure.

DEG continues its development-policy mission and finances

investments in the private sector in developing countries. In

their activities there are a variety of synergies ranging from

joint projects and a uniform appearance before customers to

a coordinated handling of customer inquiries.

The network of foreign representations of KfW and DEG

was further expanded in 2002 with the opening of two new

offices in Kabul and Ankara. The KfW Group is currently

represented in 25 developing countries. The experts in the

foreign representations help to intensify cooperation with the

local project partners. Also, having a local presence makes it

easier to participate intensively in the sector dialogue and to

coordinate projects and programmes with other bilateral and

multilateral DC institutions.

2. ACTIVITIES OF KFW AND DEG IN DEVELOPMENT COOPERATION

THE „MILLENNIUM DEVELOPMENT GOALS“ (TO BE ACHIEVED BY 2015):

• Halving the proportion of extremely poor people and people who suffer from hunger, measured by the world pop-

ulation of 1990 and by the proportion of people whose income is less than USD 1 a day

• Achieving universal primary education for all children, girls and boys alike, up to the age of 14

• Promoting gender equality and empowerment of women

• Reducing child and infant mortality to two-thirds of the level of 1990

• Reducing maternal mortality to three-quarters of the level of 1990

• Combating HIV/AIDS, malaria and other epidemics

• Ensuring environmental sustainability, halving the proportion of people without access to safe drinking water, cli-

mate protection, protection of biodiversity and forests

• Building up a global partnership for development by implementing fair trading and financial systems (including

debt reduction) and responsible good governance, both nationally and internationally

Guided by the Goals of the Millennium Declaration

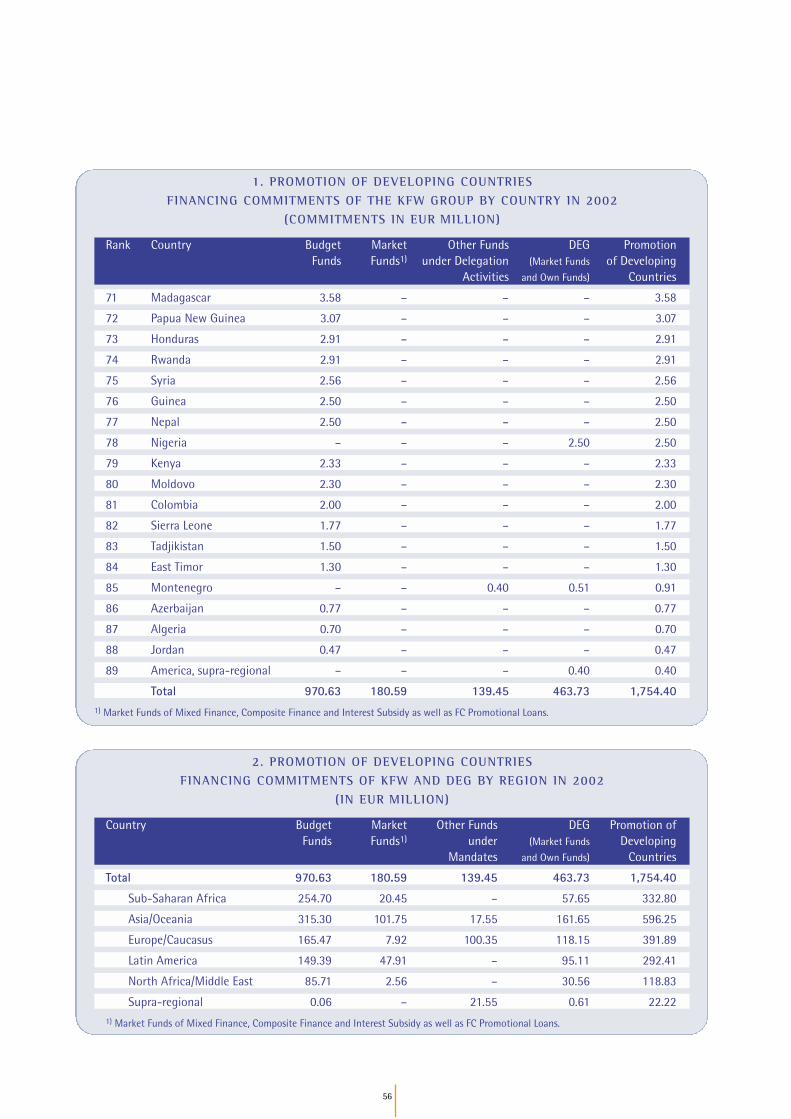

DEVELOPMENT OF COMMITMENTS OF

KFW AND DEG

In the year 2002 KfW and DEG committed a total

of EUR 1.8 billion to support the developing countries

(see table 1).

Commitments for the promotion of developing coun-

tries comprise federal budget funds, especially from the

German Ministry for Economic Cooperation and Development

(BMZ), funds from other donors in the context of mandates

as well as KfW’s and DEG’s own funds. The biggest share of

total commitments made by KfW and DEG went to Asia,

followed by Europe/the Caucasus and sub-Saharan Africa

(see chart 1).

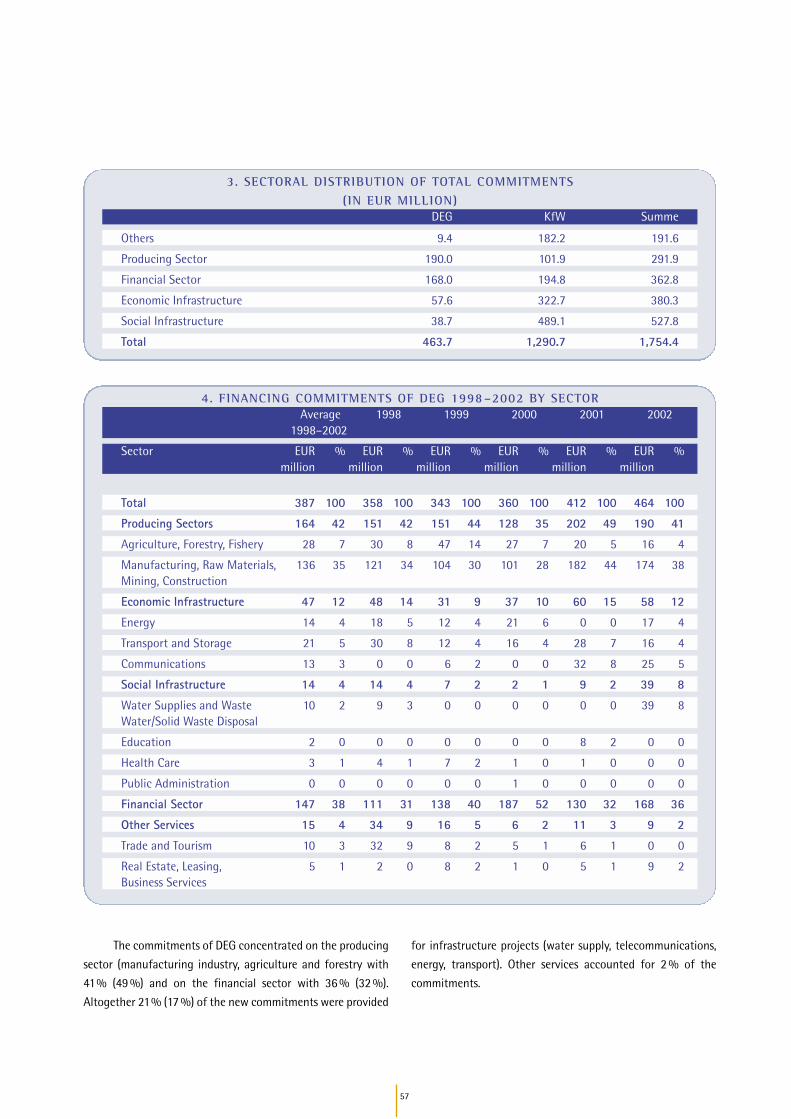

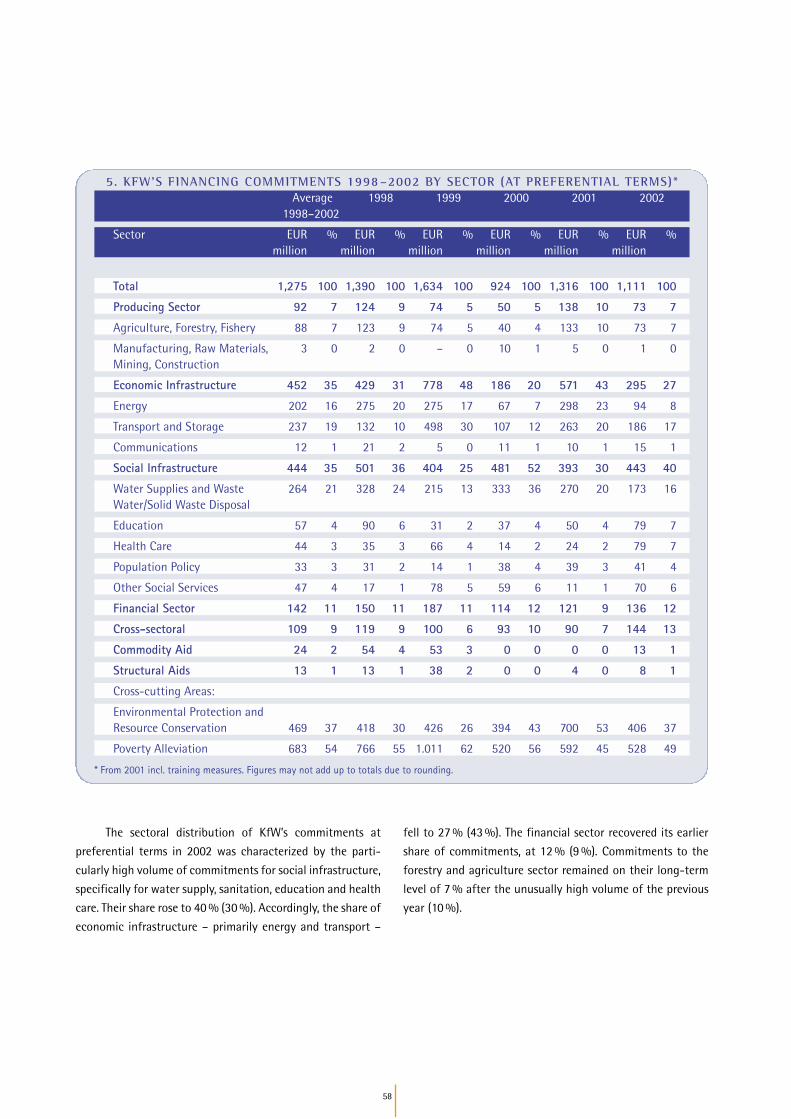

The sectoral distribution of KfW’s commitments in 2002

was characterized by the very high volume of commitments

for social infrastructure in the areas of water supply,

sanitation, education and health care. DEG financed mainly

the producing sector, followed by the financial sector

(see chart 2). More detailed commitment figures are given

in the Statistical Appendix.

5

COMMITMENTS OF KFW AND DEG FOR THE PROMOTION OF DEVELOPING COUNTRIES 1998–2002

(COMMITMENTS IN EUR MILLION)

1998 1999 2000 2001 2002

Federal budget funds 1,357 1,278 851 1,040 971

Market funds of composite finance/mixed finance/interest reduction 33 356 76 276 140

Commitments under FC on preferential terms 1,390 1,634 927 1,316 1,111

Commitments for FC promotional loans – – 30 116 41

Mandates/TRANSFORM Programme 35 38 62 162 139

Loans to the Poverty Reduction and Growth Facility of the IMF – – 495 1,430 –

Total KfW Commitments: 1,425 1,672 1,514 3,024 1,291

Total DEG Commitments 358 343 360 412 464

Total Commitments for the Promotion of Developing Countries (KfW and DEG) 1,783 2,015 1,874 3,436 1,755

Activities in Figures

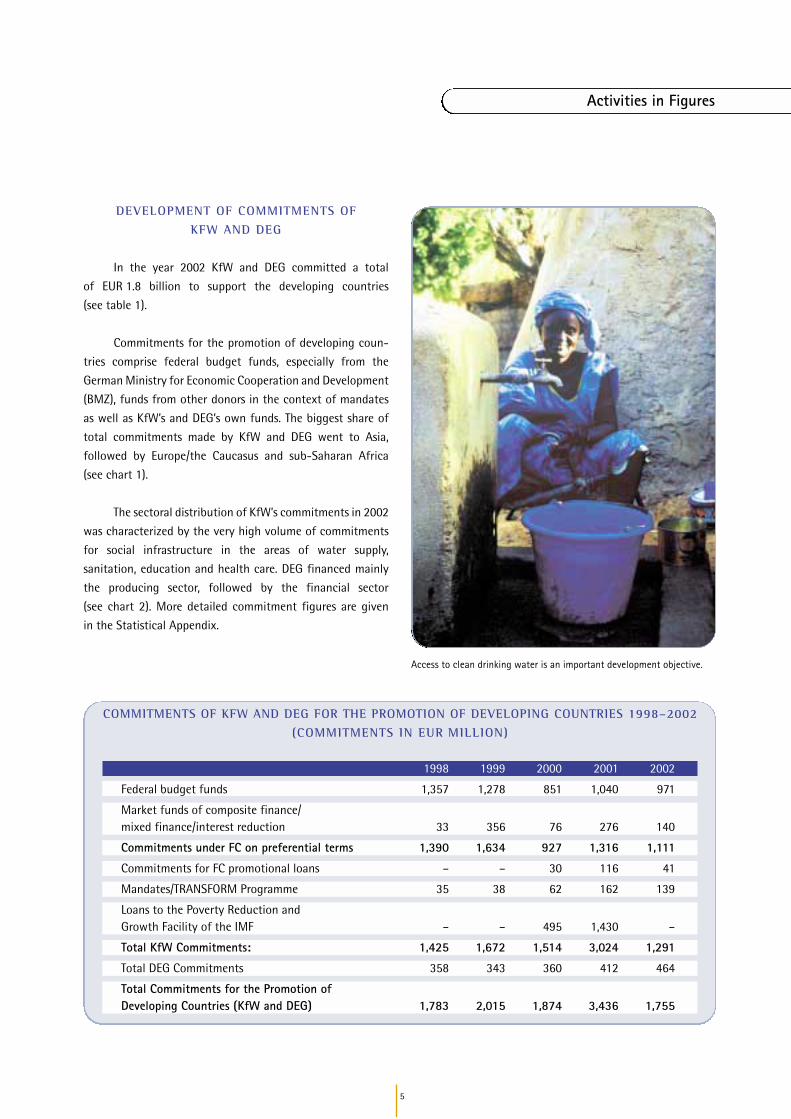

Access to clean drinking water is an important development objective.

6

COMMITMENTS OF KFW

KfW is currently financing a total of 1,408 projects in

109 partner countries. Last year KfW provided around EUR 1.3

billion (EUR 3.0 billion) in new commitments for the pro-

motion of developing countries. Adjusted for a special loan

of approx. EUR 1.4 billion granted to the IMF in 2001,

commitments in 2002 were around EUR 300 million lower

than the year before. Commitments from budget funds of the

BMZ were around 7% below the previous year’s level, at

EUR 971 million (EUR 1,040 million). This is mostly the result

of project-related reallocations. Of the commitments from

budget funds 70 % were extended as non-repayable grants

and 30 % as low-interest loans with terms of 30 to 40 years.

The weighted average interest rate of FC loans newly

committed in 2002 on preferential terms was 1.19 % p.a.

(1.05 % p.a.)

With a share of 49 % (46 %) almost half of the FC

financing volume in 2002 went to the cross-cutting area of

“poverty reduction”. Around 22 % of the funds were com-

mitted explicitly for the protection of the environment and

natural resources and another 15 % for projects which have

the protection of the environment and natural resources as

an important secondary objective.

The weak cyclical development worldwide has lead to

a stretching of and shift in investments in the developing

countries as well. This had a direct impact on the volume

of market funds (composite and mixed finance, interest

reductions), and on FC promotional loans committed by KfW.

In these loans, funds are provided at market conditions to

promote projects that are developmentally justified. In the

year under review, despite a difficult world economic

environment, KfW was able to mobilize a total of EUR 181

million (EUR 392 million) for such projects.

Moreover in 2002, KfW was assigned new mandates

for EUR 139 million (EUR 161 million), among others for

measures in Southeastern Europe, Afghanistan, Georgia and

Turkey. After the above-average amount committed under

mandates in 2001, this is again a particularly good result.

The most important mandates assigned to KfW were from the

EU Commission, the EIB, the UN and the Agence Française de

Développement (AFD), but also from the German Ministry of

Foreign Affairs and the German Ministry of Finance.

Activities in Figures

After the war in Afghanistan reconstruction began immediately.

COMMITMENTS OF DEG

For DEG, too, the business climate in 2002 was marked

by the persistent weakness of the world economy and the

difficult environment for investment that prevailed in nume-

rous partner countries. Nevertheless, DEG was able to further

expand its financing business, and with commitments to-

talling EUR 464 million in 2002 (EUR 412 million) it recorded

its highest volume of new commitments ever. DEG’s total

portfolio of loans and equity holdings of EUR 2.3 billion

comprises investments in 453 companies in 84 countries.

In the year under review DEG provided EUR 49 million

for equity financing and EUR 398 million for loans, of which

EUR 31 million was for mezzanine loans. Thus, total venture

capital provided in the form of equity investments and mez-

zanine financings added up to EUR 80 million, which is a share

of 17 % in the total commitment volume. More than EUR 16

million was committed for guarantees. Co-financing was

provided for investments in 66 projects in 31 countries.

Under the Public-Private Partnership (PPP) Programme

initiated by the BMZ for development partnerships by German

7

Chart 1:Regional Distribution of Commitments of KfW and DEG in 2002(in EUR million)

0 100 200 300 400 500 600 700

DEG KfW

Europe andCaucasus

Asia andOceania

Sub-SaharanAfrica

Latin America

North Africa/Middle East

Supra-regional

Chart 2:Sectoral Distribution of Commitments of KfW and DEG in 2002(in EUR million)

SocialInfrastructure

0 100 200 300 400 500 600

DEG KfW

EconomicInfrastructure

Financial Sector

ProducingSector

Other

companies DEG promoted another 51 projects in the year

under review. For this purpose the German government

provided grants in the amount of EUR 8 million. On behalf of

the Federal Ministry for Economic Cooperation and Develop-

ment (BMZ) the DEG offers a special Business Start-up

Programme for qualified experts from developing countries

who return to their home countries.

DISBURSEMENTS OF KFW AND DEG

In the year 2002 KfW and DEG altogether disbursed a

total of EUR 1.7 billion to support developing countries (EUR

1.8 billion). DEG’s share of this amount was EUR 357 billion

(EUR 244 billion) and KfW’s share amounted to EUR 1.3 mil-

lion (EUR 1.6 million).

Of KfW’s FC disbursements (not including market funds)

in the total amount of EUR 998 million (EUR 1,157 million)

35 % (38 %) were for services rendered at the local level in the

partner countries and had direct income and employment

effects in these countries. The German industry accounted

for 40 % (45 %) of disbursements for supplies and services

subject to international public invitations to tender. The

8

disbursements in foreign currency benefited in particular

the following sectors: advisory and consulting services (27 %),

the construction industry (22 %), electrical engineering

(19 %) and mechanical engineering (14 %).

DEBT CONSOLIDATION AND

DEBT CONVERSION

Under specific circumstances the German government

is prepared to ease, or to grant partial release from, the

repayment of development assistance loans of highly

indebted partner countries willing to implement reforms.

KfW participates in the negotiations on the German side. In

2002, for instance, KfW concluded debt consolidation

agreements with Côte d’Ivoire, Ghana, Indonesia, Jordan,

Yugoslavia, Cameroon, Kyrgyzstan, Nigeria and Pakistan for

altogether EUR 3.7 billion. In addition, Bolivia was the first

country whose debt was completely cancelled under the HIPC

Initiative (for Heavily Indebted Poor Countries). The amount

released was EUR 335 million.

In 2002 the federal government committed a volume of

EUR 49 million for debt conversions. In exchange for the

release from repayment these funds can be utilized in the

debtor country for poverty reduction and environmental

conservation projects. Including commitments made in 2001

KfW concluded debt conversion agreements for EUR 97

million in 2002. In total, EUR 244 million was already waived

for this purpose.

National and International Cooperation

In a number of cooperative projects, co-financings and

partnerships, the KfW Group is combining its competence

with the specific strengths of other financing institutions.

Chief among these partnerships is the GTZ (Deutsche

Gesellschaft für Technische Zusammenarbeit – German

Agency for Technical Cooperation). GTZ’s primary goal is to

strengthen the performance of local partner organizations

in order to improve the living conditions and perspectives of

the people in the developing and transition countries. The

competences of GTZ and KfW complement one another and

together both institutions support the BMZ. In many partner

countries KfW and GTZ are already operating joint offices. GTZ

and KfW have formed a strategic alliance with regard to the

development and implementation of country strategies and

priority strategies. In this context national measures are being

embedded in the activities of the international donor

community. Moreover, KfW and GTZ have established an

intensive cross-project cooperation and carry out a number

of cooperative projects. At the end of 2002 there were 229

ongoing cooperative projects with GTZ in 68 countries.

At the international level KfW is currently implement-

ing 260 projects in co-financing with other donor organiza-

tions. The joint financing contributes actively to a better

In 2002 Bolivia was the first country to have all its foreign debtcancelled under the HIPC initiative.

Leistungen in Zahlen

interaction between bilateral and multilateral development

cooperation. The different donors coordinate their procedures

and requirements, thus increasing the developmental effec-

tiveness of the individual contributions and enabling the

partners to coordinate and administer the assistance more

efficiently.

KfW can look back on a very close and long-standing

cooperation with the French development bank AFD. This

partnership is much more than a joint financing of projects.

It also comprises learning from one another, supported by

the exchange of staff, and the joint appearance at the inter-

national level. This also includes jointly implementing

projects for other contractors (see message of greeting from

H. Severino).

9

MESSAGE OF GREETING ON THE COOPERATION WITH AFD

FROM JEAN-MICHEL SEVERINO, DIRECTOR GENERAL OF AFD

This year we have celebrated the 40th anniversary of the Elysée Treaty, which is

a sign of the friendship between our two countries. Is there a better opportuni-

ty for KfW and AFD to celebrate their cooperation? This cooperation has a long

history. In 1973 the two institutions together set up an association of European

development finance institutions. Since then the Financial Cooperation segment

of the KfW Group has proved to be a remarkable partner of AFD. Our mutual

understanding is also illustrated by the exchange of staff. This exchange of

competence, experience and views, which was started roughly 10 years ago,

has helped to bring our two "professional families” closer together. Our mutual

confidence has grown and recently expressed itself again by the reciprocal

assignment of mandates by KfW to AFD (e.g. in Mali) and by AFD to KfW (e.g. in

Kenya). In fact, our close relationship reflects a subtle but fundamental truth:

We share a common mission. Was not each of our institutions entrusted with the

task of taking up the challenges of the post-war era? Today we are also engaged

in reforms that pursue common objectives: efficiency of our assistance, sectoral

and geographic concentration, and donor coordination. Finally, and as a matter

of fact also beyond this, we are united by a common vision of the future, in

particular the future relations between Europe and the industrializing and

developing countries.

At the European and international levels the DEG also

cooperates closely with other development finance institu-

tions. Under the organizational umbrella of the association

of European Development Finance Institutions (EDFI) a lively

exchange of experience is taking place on all investment-

related areas. Comparably intensive contacts exist also with

the International Finance Corporation (IFC), which is part

of the World Bank Group. The result of such cooperations are

co-financings with one or more of these partners in

altogether 147 projects. This includes, in particular, joint

project financings with the Dutch FMO and the AFD sub-

sidiary PROPARCO.

Jean-Michel Severino

Reopening a reconstructed school in Afghanistan.

10

PREVENTING CRISES BY MAKING POVERTY

REDUCTION A DEVELOPMENT GOAL

Given the imminent dangers of terrorism and war all

over the world the contribution of development policy

to poverty reduction has taken on new significance. It is

undisputed that the trend towards radicalization is nourished

by poverty and the resulting lack of perspective of large

sections of the population. A development policy that seeks

to reduce poverty can offer new perspectives to many people,

noticeably improve their living conditions and thereby

contribute to securing peace. This is necessary particularly

in crisis situations, even if development policy cannot solve

the intricately connected problems and causes alone and,

above all, without the active participation of the local

population.

In addition to our commitment to securing the peace in

Central America, the Palestinian Territories and in the frame-

work of the Stability Pact for Southeastern Europe, this is

illustrated very strongly by the example of Afghanistan:

Since January 2002 KfW and GTZ have been present in Kabul

with a joint office in order to coordinate the emergency aid

for the reconstruction on site in Afghanistan. FC and EU funds

have been provided, among others, to rehabilitate education

and health care facilities and to co-finance the reconstruc-

tion of the water and power supply. Now power is again being

supplied for street lighting, hospitals and schools. Despite

difficult starting conditions 13 projects were launched in

2002. Of these, five projects have already been concluded.

In addition, on behalf of the BMZ, DEG provides equity

assistance to start-up businesses in Afghanistan with

non-repayable grants. Overall, more than two million people

in Afghanistan benefit directly or indirectly from our

activities. Despite considerable efforts and a good donor

coordination the conditions for DC in the country are expect-

ed to remain extremely difficult for many years to come.

Sustainable results can by achieved only through a longer-

term involvement.

WATER AS A BASIS FOR

SUSTAINABLE DEVELOPMENT

In line with its importance for poverty reduction the

water sector is one major focus of KfW’s promotional

activities. Several sub-goals of the Millennium Declaration

are directly supported through projects in the water sector

(access to safe drinking water, promotion of health care

and the protection of natural resources). In the last five years

KfW committed roughly EUR 260 million annually for the

water sector. A sustained development success can be

achieved only if the projects are demand-oriented, i.e. if the

users are involved in the planning and implementation of

the projects. For instance, in rural water supply projects

the future users are involved in many stages – from the

Main Themes of the Year 2002

consideration of alternative solutions to the organizational

design of the operation of facilities. In the field of urban

infrastructure public relations work conducted at an early

stage plays an important role to meet the demand. Financial

sustainability is ensured through tariff systems that take

account of the income situation of poorer sections of the

population.

Moreover, environmental impacts spreading across

regional boundaries from unregulated water use are becom-

ing ever more important, since conflicts over the use of

water are increasing with growing regional water scarcity.

Often there is competition within the country between the

drinking water needs of the population and agriculture as

a large-scale consumer but also between neighbouring

states for the use of cross-border watercourses. FC also

promotes regional cooperation between different countries

sharing the same international waters for the joint manage-

ment of the water resources. FC projects in the water sector

support the efficient use of the water reserves. Protecting

the water resources can mitigate impending conflicts over

their use.

SOCIAL STANDARDS

IN DEVELOPMENT COOPERATION

The social standards, which we have taken for granted

in our working environment for a long time, have not

been adequately implemented in many countries yet. These

so-called core labour standards include the ILO Conventions

concerning the ban on child labour and forced labour, free

collective bargaining and the non-discrimination of women

on the job. An important concern of German development

policy is to improve the working and living conditions in the

partner countries by promoting the core labour standards.

For this purpose KfW has supplemented its guidelines for

the award of contracts under Financial Cooperation, which

bindingly stipulate that all core labour standards applicable

in the respective country have to be adhered to also in the

event of contracts being awarded to local contractors in the

developing country.

DEG has laid down these goals particularly in its guide-

lines for the social compatibility of its project business. Thus,

when appraising and structuring a project it agrees on specific

criteria for social aspects in its contracts with the customer.

Key elements are mandatory reporting on the part of the

project partner and the right of DEG to inspect the project

during the operating phase.

11

The number of people who have no access to clean drinking water is tobe halved by the year 2015 (Millennium Declaration, September 2000).

3. PROMOTING ENERGY EFFICIENCY, RENEWABLE ENERGIES AND CLIMATE PROTECTION

ENERGY AND ECONOMIC

DEVELOPMENT

Poverty eradication, the main objective formulated in

the Millennium Declaration, also means supplying all people

with adequate energy services. How do we have to manage

our energy resources if we want to make development

sustainable for all the world’s people? How can the dilemma

between protecting the Earth’s climate and economic

development be mitigated for our partner countries? The

subject of energy was very fervently debated at the World

Summit on Sustainable Development in Johannesburg in

2002 (see box).

Life in our world is unthinkable without energy. There is

still a very close connection between economic growth and

energy consumption. Use of energy makes an economy grow,

creates jobs and income. All convenience goods are produced

with energy. It keeps the entire physical and social infra-

structure going. Railways, buses and cars need electricity and

fuels. Most staple foods and often drinking water must be

heated or boiled. People inhabiting the Earth’s cold zones

cannot survive without heating. Electrical pumps provide

clean drinking water from pipe networks or wells. All this

requires a reliable and efficient energy supply.

ENERGY AND POVERTY ERADICATION

Around 1.6 billion people have no access to “modern”,

usually commercially traded forms of energy. Without

corrective measures this will hardly change even in the next

30 years. About 2.4 billion people, primarily in the rural

regions of Africa and Asia, still use traditional biomass for

cooking and heating, that is, firewood, agri residues and dung.

According to estimates of the International Energy Agency in

Paris (IEA) the absolute number of people who will continue

12

WORLD SUMMIT ON SUSTAINABLE DEVELOPMENT IN JOHANNESBURG IN 2002:

THE ROLE OF THE TOPIC OF ENERGY

At the World Summit in Johannesburg the international community of states adopted measures at the national and

global level designed to achieve the objective of sustainable development. Where consensus was possible, concrete

milestones were agreed for these measures.

The summit participants had a very controversial debate on the subject of energy. The debate centred on the desire

of the EU and several developing countries to increase the proportion of renewable energies in the coming years.

They wanted an agreement to raise the share of renewable energies in worldwide energy consumption to 15% by the

year 2010. This initiative was blocked particularly by the USA, the OPEC countries and the Group of 77. Therefore,

instead of agreeing on specific time-bound targets and percentages the states only settled for the political intent

to substantially increase the share of energy to be obtained from renewable sources. They also emphasized the need

for diversifying energy supplies and improving energy efficiency.

Responding to this outcome of the negotiations and encouraged by the German government, the EU started an

initiative to expand the use of renewable energies. Germany will take the following measures in support of this initia-

tive, which many other states have already joined:

• Conduct an international energy conference in Germany, presumably in June 2004, focusing on sustainable energy

systems and the role of energy in the fight against poverty.

• Support developing countries by stepping up the promotion of sustainable energy systems. Over the next five years

EUR 1 billion will be made available for renewable energies and increasing energy efficiency from the budget of

the BMZ.

Energy and Sustainable development

13

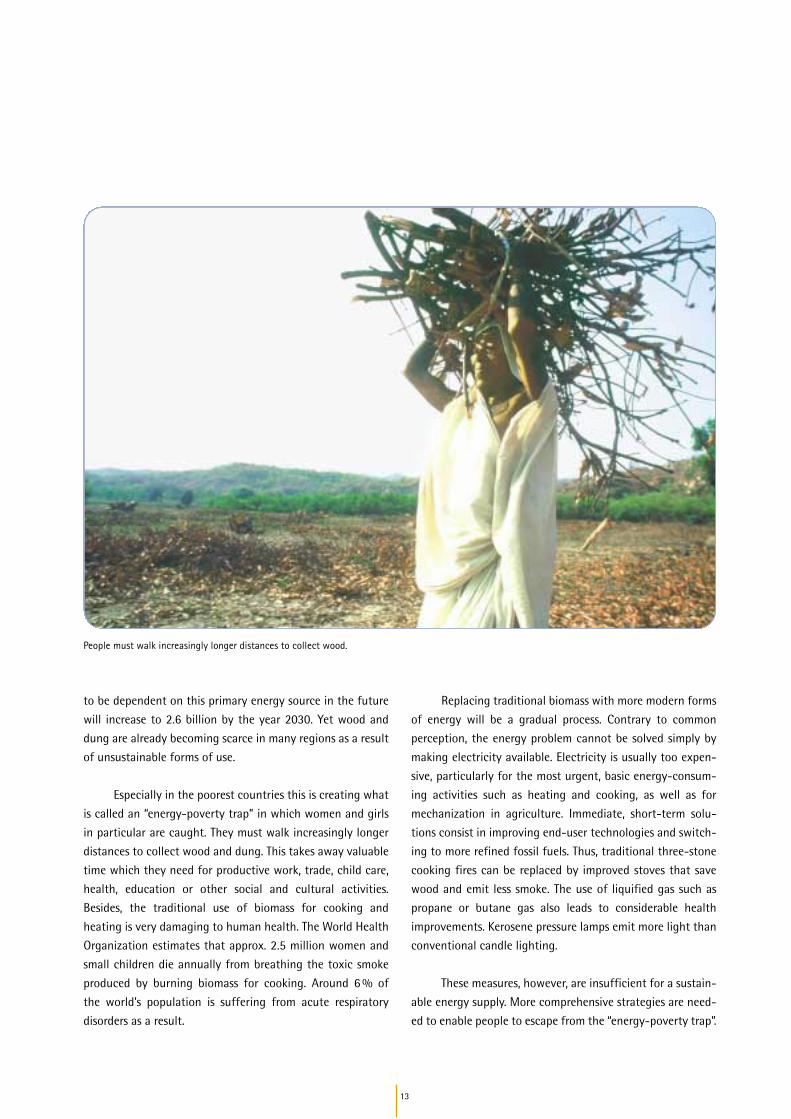

to be dependent on this primary energy source in the future

will increase to 2.6 billion by the year 2030. Yet wood and

dung are already becoming scarce in many regions as a result

of unsustainable forms of use.

Especially in the poorest countries this is creating what

is called an “energy-poverty trap” in which women and girls

in particular are caught. They must walk increasingly longer

distances to collect wood and dung. This takes away valuable

time which they need for productive work, trade, child care,

health, education or other social and cultural activities.

Besides, the traditional use of biomass for cooking and

heating is very damaging to human health. The World Health

Organization estimates that approx. 2.5 million women and

small children die annually from breathing the toxic smoke

produced by burning biomass for cooking. Around 6 % of

the world’s population is suffering from acute respiratory

disorders as a result.

Replacing traditional biomass with more modern forms

of energy will be a gradual process. Contrary to common

perception, the energy problem cannot be solved simply by

making electricity available. Electricity is usually too expen-

sive, particularly for the most urgent, basic energy-consum-

ing activities such as heating and cooking, as well as for

mechanization in agriculture. Immediate, short-term solu-

tions consist in improving end-user technologies and switch-

ing to more refined fossil fuels. Thus, traditional three-stone

cooking fires can be replaced by improved stoves that save

wood and emit less smoke. The use of liquified gas such as

propane or butane gas also leads to considerable health

improvements. Kerosene pressure lamps emit more light than

conventional candle lighting.

These measures, however, are insufficient for a sustain-

able energy supply. More comprehensive strategies are need-

ed to enable people to escape from the “energy-poverty trap”.

People must walk increasingly longer distances to collect wood.

ENERGY AND ENVIRONMENT

The conversion of energy always has environmental

consequences. Burning fossil fuels impacts the environment

by releasing hazardous substances (particulates, sulphur and

nitrogen) and greenhouse gases that damage the Earth’s

climate. Oil spills and leakages during transport, as in the

case of tanker accidents, cause severe damage to the environ-

ment. The unsustainable use of traditional renewable energies

such as wood and other biomass can cause deforestation,

desertification and soil erosion. At the same time, the burning

of cow dung for heating and cooking purposes deprives

agricultural soils of important organic material. Even the

generation of electricity from hydropower can produce

negative social and ecological consequences through the

construction of dams and reservoirs, as the “World Commis-

sion on Dams” (WCD) has prominently established. If the WCD

recommendations are followed, however, hydropower will

continue to be an important element in energy supply in the

future as well.

The greatest challenge from a global perspective is to

limit the anthropogenic greenhouse gas emissions (GHG

emissions, the main GHG is CO2). The IEA estimates that the

demand for primary energy in the developing countries will

more than double by the year 2030. The burning of fossil fuels

14

Energy and Sustainable development

Obsolete technology in coal-fired power plants and industrial enterprises pollutes the environment in China.

like oil, coal and natural gas will account for more than 75 %

of additional GHG emissions in the next 30 years. The World

Energy Council estimates the resulting CO2 emissions to be

around 70 % above today’s level around the year 2030 if all

other conditions remain the same. The developing countries

will have the highest growth rates. In the year 2030 their

share in worldwide CO2 emissions will already be at 47 %,

exceeding the 42 % share of the OECD countries. By com-

parison, in the year 2000 the OECD share was 55 % and that

of the developing countries 34 %. On the other hand, per

capita emissions in the OECD countries will still be around five

times as high as in the developing countries, at 13 tonnes per

year against 2.4 tonnes per year.

Given the long time it takes to develop and implement

new energy technologies it is all the more important to set the

course for CO2 avoidance in due time. The industrialized

countries need to act first. Because of their high primary

energy consumption they are today the biggest emitters

of CO2. However, greenhouse gas emissions in the atmosphere

can be limited in the long term only if the developing coun-

tries are involved in this process.

For them it is particularly difficult to adapt to climate

change because of their geography and economic structure.

Therefore they will be particularly hard hit by expected

15

impacts such as global warming, rising water levels, hurri-

canes and cyclones, and droughts. So it must also be in the

developing countries’ immediate interest to contribute to

global climate protection.

PRECONDITIONS FOR A

SUSTAINABLE ENERGY SUPPLY

Worldwide demand for energy will continue to rise,

particularly in developing countries. According to the current

state of knowledge, the main problem does not consist in

making additional energy resources available in the future.

Fossil fuel reserves are sufficient to meet growing energy

needs until far beyond the year 2050. Technically, renewable

energies, especially solar energy, can be used almost without

limitations. However, the utilization of renewable energies

on a broader scale is currently more costly than the use of

conventional energy technologies. If market conditions and

prices remain unchanged, conventional energies will be given

preference.

For this reason the IEA estimates that the share of

renewable energies in primary energy consumption will

even decline in the next three decades. Given that the mix of

energy sources will then consist mostly of fossil fuels there

will be an overproportionate increase in air pollution and

greenhouse gas emissions. Expanding nuclear power gene-

ration – itself without impact on atmospheric CO2 – is no

solution because of the high risks and unnecessary given

the vast renewable energy potential in developing countries.

The main challenges for sustainable energy supply in

developing countries are threefold:

• Energy must be safe. Consumers must be able to count

on reliable energy services. This presupposes an adequate

energy supply that can be maintained and expanded

only by continuously investing in the entire energy

infrastructure. Maintenance and repairs on energy

installations must be ensured. Not least, the growth of

energy demand must be contained through the efficient

use of energy and by prices that adequately reflect costs.

Thus, it will be necessary to decouple economic growth

from the growth of energy consumption.

• Energy must be cost-effective. Necessary energy services

should be delivered at reasonable and affordable prices

and, at least over the medium term, without subsidies.

This is a prerequisite for economic growth and pro-

ductivity increases in which the poor groups of the

population participate as well. Energy must be gener-

ated, distributed and utilized efficiently.

• Energy must be “clean”. This implies the requirement of

ecological sustainability of the energy supply system.

Negative environmental and health impacts of energy

consumption must be reduced. This means that clean

sources of energy and environmentally benign energy

technologies should be applied wherever possible. In this

connection the promotion of renewable energies is of

particular importance.

Promoting renewable energy is of particular importance.

REFORMING AND LIBERALIZING

ENERGY MARKETS

In many developing and transition countries the ener-

gy sector is dominated by state monopolies. Governments in-

fluence energy utilities’ day-to-day business. Widespread

clientelism leads to inefficient management which disregards

commercial criteria. Energy prices are kept at an excessively

low level for political considerations so that the revenue

collected is insufficient for maintenance and upkeep and

investments cannot be financed without help from outside.

Since state coffers are notoriously empty the funds required

for new investment and reinvestment can no longer be

mobilized in such a situation.

Several developing countries, particularly in Asia and

Latin America, have reacted by starting to liberalize their

energy sector in the past years. The purpose of opening the

market is to involve the private sector more strongly in

investment and operation. This is expected to raise produc-

tivity and lower the cost of energy supply.

But in order to encourage private investors to invest in

developing countries it is necessary to create a trustworthy

regulatory framework. Potential investors must regard it as

transparent and stable enough for a long-term capital

investment. In addition to market-based regulatory mecha-

nisms and incentive structures, appropriate monitoring

instruments must be created to prevent market abuse.

The hope for a greater role of the private sector and, in

particular, of small and medium-sized enterprises, is appro-

priately expressed in a guest contribution on the “AREED”

Initiative in Senegal (see box).

16

PROSPECTS FOR WIDENING MODERN ENERGY SERVICES IN AFRICA

Guest contribution by Youba Sokona, Director of Environmental Development Action in the Third World (ENDA),

Head of Energy Programme “African Rural Energy Enterprise Development” (AREED) in Senegal:

The vast majority of Africans have no access to modern energy services. Improvements in the standard of living for the

growing population and economic development for the continent cannot be achieved, however, without access to

affordable and appropriate energy services.

Great efforts are necessary to unleash the great potential of Africa’s rich energy and natural resources. Policy reform,

social development and institutional development must be advanced. But in undertaking these tasks it will be essen-

tial to develop models, new types of institutional arrangements, policies and approaches that really work under the

conditions currently prevailing in Africa. Critical actions to meet human needs in the area of energy must take the

following elements into account:

• more sustainable use of biomass for energy,

• access to affordable, modern energy services must be extended to those who lack them,

• the efficiency of energy production, distribution and use must be improved,

• indigenous energy resources must be expanded to promote self-reliance and reduce net import costs.

The aim of the AREED initiative is to show that a significant portion of the energy services needed in Africa’s rural areas

and urban peripheries can be reliably provided by small and medium-sized enterprises. The ongoing negotiations on

climate change present an opportunity for African countries to revisit sustainable energy options with renewed

urgency. The negotiations should result in new forms and approaches of north-south cooperation that will contribute

to promoting the private sector approach followed by AREED.

Strategies for a Sustainable Energy Supply

17

Flue gas desulphurisation plants in coal-fired power plants reducehazardous emissions.

HARMONIZING ENERGY PRICES WITH

ENERGY COSTS

In developing countries consumers often pay much less

for energy services than it costs to make them available. Fossil

fuels in particular are often heavily subsidized. This leads to

excessive demand and, in consequence, causes damage to the

environment and climate that would be avoidable. If prices

are made to reflect costs and subsidies that distort the market

are dismantled, consumer behaviour can be positively

influenced. Consumers would be encouraged to use energy

responsibly and economically, thereby protecting the envi-

ronment. KfW therefore makes its support of energy projects

conditional on the existence of a tariff system that reflects

the actual cost of providing energy services. In countries

where these conditions are not yet fulfilled German DC and

other donors jointly conduct a dialogue with the govern-

ments to improve the overall framework. A level playing

field in the market improves not only the prospects of

renewable energies but also the chances for increasing energy

efficiency.

Access to modern energy supply systems brings developmentopportunities to rural regions.

18

SPREADING THE USE OF RENEWABLE

ENERGIES

Renewable energies include hydropower and biomass,

the “traditional” renewable energies, as well as solar energy,

wind, geothermal energy and modern biomass energy systems

– the “new” renewable energy sources. The great advantage

of renewable energies is that they can be used without

affecting the Earth’s climate, meaning that they emit few or

no additional greenhouse gases during operation. In general,

they also emit fewer hazardous, polluting substances than

fossil fuels. Another advantage is that their operation is

usually relatively cost-effective because the energy sources

(sun, wind, water, geothermal energy) are freely obtainable.

On the other hand, there are also many reasons that still

limit the economic potential required for a purely commercial

financing of renewable energies in developing countries.

The risks are being perceived as too high, and the projects

using “new” technologies, which are typically smaller, incur

relatively high transaction costs (particularly in the case of

solar energy).

Even in countries where the macro-economic environ-

ment and the energy sector conditions favour renewable en-

ergies it is easier to mobilize private capital for conventional

and technically proven technologies. This trend can even

be observed in investments aimed at increasing energy

efficiency, which would amortize the costs incurred by the

enterprise through energy savings even in a short time. The

problem is more serious for renewable energies.

Particularly in remote rural areas, where consumers

can be equipped with decentralized generating systems,

renewable energies have cost advantages over conventional

technologies. Electricity demand there is low and the central

power grid is far away, so that it would be too costly for the

utility to expand its interconnected grid, as it would other-

wise do under a “classic” electrification strategy. Moreover,

renewable energy sources – mostly photovoltaic systems – are

increasingly being used in the promotion of other sectors such

as health care, primary education, water supply and tele-

communications.

Strategies for a Sustainable Energy Supply

Hydropower will play an important role as a classic renewable energy in the future as well.

USING ENERGY MORE EFFICIENTLY

A concrete approach towards making energy supply

sustainable consists in making energy utilization more effi-

cient in all stages of the energy cycle – from extraction

through distribution to end use. This is where ecological and

economic concerns can usually be harmonized at a reasonable

cost. Through efficiency improvements the same energy

output, such as heating and electricity, can be made available

with less energy input. In many developing countries there are

ways to achieve a considerable economic potential at rela-

tively low cost. With these approaches, pollutant emissions

can usually be reduced in a cost-effective way.

ASSISTANCE MECHANISMS

The vicious circle has not been broken yet: because of

low production numbers, the risks and costs of the new re-

newable energy technologies in particular are still very

high and the high costs, in turn, keep demand low as well.

Renewable energies can be made much more competitive

by bundling the demand of potential users. Equipment price

reductions that are expected to result from rising production

numbers will also benefit low-income buyers. Increased risks

can be mitigated by suitable guarantee instruments.

In the medium term, however, additional incentives will

be necessary in most projects. Favourable financing condi-

tions, grants and tax relief can contribute to reducing the

costs from a business perspective. On the earnings side cost

disadvantages can be offset by administratively increased

sales prices. Output-based “smart subsidies”, which are based

on performance and reward the sustainable operation of a

photovoltaic system, for instance, are increasingly being

considered. It is important to limit subsidies to a minimum

while at the same time applying public funds in a targeted

and cost-effective way in order to limit free-rider effects.

Subsidies should also be restricted to the phase of market

introduction, be reduced over time and contain an explicit

exit clause. The volume of subsidies should generally be

limited to the extent required to compensate for market

distortions.

Such considerations require a more differentiated

approach in defining strategies of cooperation and in select-

ing financing instruments to spread the use of renewable

energies. Essential criteria include the state of competitive-

ness of the technology to be used for the energy service

required (heating, power, lighting, etc) and the supply and

income situation of the end user. Where various alternatives

are available the economic and ecological cost-effectiveness

will be the decisive selection criterion.

19

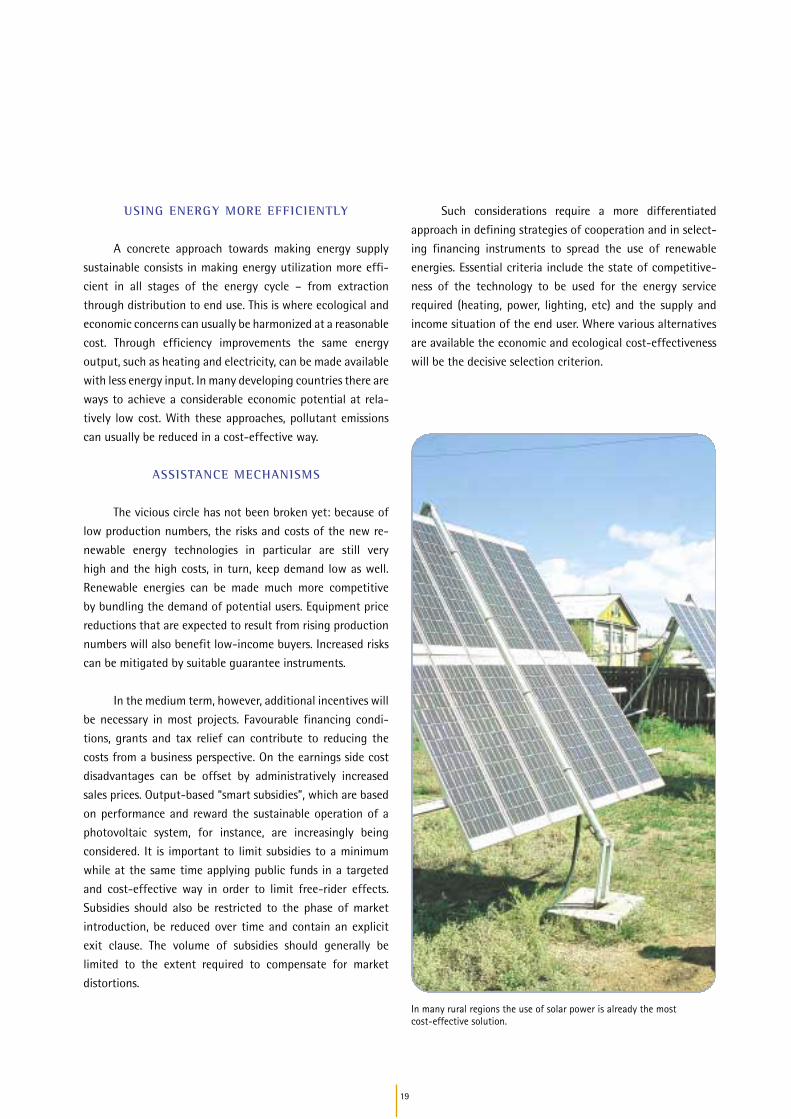

In many rural regions the use of solar power is already the most cost-effective solution.

20

CO2 CERTIFICATES – AN INNOVATIVE

FINANCING INSTRUMENT

The “flexible Kyoto Mechanisms” and the trade in CO2

Certificates constitute innovative instruments for the financ-

ing and dissemination of renewable energies and efficiency-

enhancing technologies.

KfW intends to set up a Carbon Fund for Climate

Protection to promote emissions trading (see box p. 21).

PROMOTING SUSTAINABLE ENERGY SUPPLY

IN DEVELOPING COUNTRIES

FINANCING OF ENERGY PROJECTS BY KFW AND DEG

Promoting environmentally benign and sustainable

energy supplies in developing countries has a particularly

high priority for KfW and the DEG. KfW is today the world’s

leading bilateral financier of renewable energies. The follow-

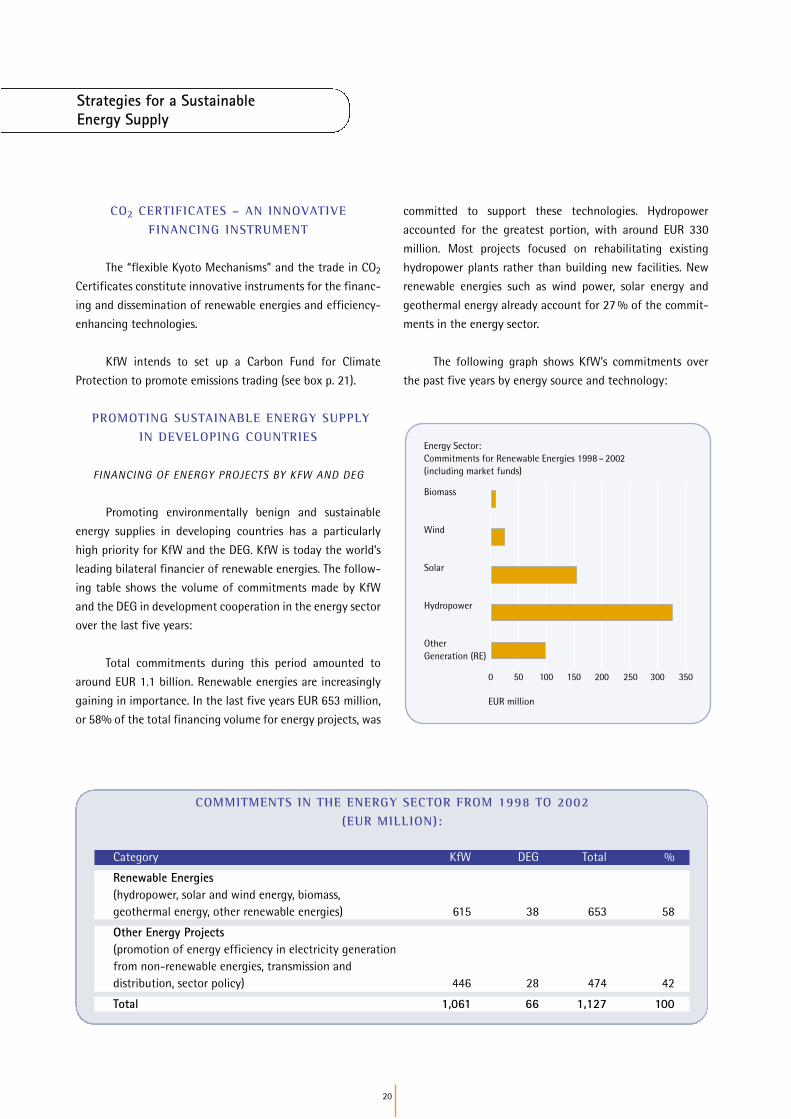

ing table shows the volume of commitments made by KfW

and the DEG in development cooperation in the energy sector

over the last five years:

Total commitments during this period amounted to

around EUR 1.1 billion. Renewable energies are increasingly

gaining in importance. In the last five years EUR 653 million,

or 58% of the total financing volume for energy projects, was

Strategies for a Sustainable Energy Supply

committed to support these technologies. Hydropower

accounted for the greatest portion, with around EUR 330

million. Most projects focused on rehabilitating existing

hydropower plants rather than building new facilities. New

renewable energies such as wind power, solar energy and

geothermal energy already account for 27 % of the commit-

ments in the energy sector.

The following graph shows KfW’s commitments over

the past five years by energy source and technology:

COMMITMENTS IN THE ENERGY SECTOR FROM 1998 TO 2002

(EUR MILLION):

Category KfW DEG Total %

Renewable Energies(hydropower, solar and wind energy, biomass, geothermal energy, other renewable energies) 615 38 653 58

Other Energy Projects(promotion of energy efficiency in electricity generation from non-renewable energies, transmission and distribution, sector policy) 446 28 474 42

Total 1,061 66 1,127 100

Energy Sector:Commitments for Renewable Energies 1998 – 2002(including market funds)

Biomass

Wind

Solar

Hydropower

OtherGeneration (RE)

0

EUR million

50 100 150 200 250 300 350

21

In the face of the looming global climate catastrophe

a framework convention on climate protection was signed

in the Japanese city of Kyoto in 1997. In this convention,

known as the Kyoto Protocol, the industrialized countries

took responsibility as the main originators of the greenhouse

effect and for the first time entered into a legally binding

commitment to limit or reduce their emissions: they under-

took to reduce their emissions of the six most important

greenhouse gases in the years 2008 to 2012 by at least 5.2 %

against 1990 as their emissions base year. Different reduction

objectives were set for the individual countries. The govern-

ment of the Federal Republic of Germany adopted the

objective to lower carbon-dioxide emissions by 25 % by the

year 2005 against the base year 1990.

Because of the global relationship of cause and effect

the Kyoto Protocol gives the signatory states flexibility in the

implementation of the reduction objectives through the

instruments of Emissions Trading, Joint Implementation,

(cooperation between industrialized countries in the imple-

mentation of projects) and the Clean Development Mecha-

nism (projects to reduce emissions in developing countries).

The basic principle behind all three flexible mechanisms is

to allow the industrialized countries to choose the most

cost-effective ways to meet their reduction obligations.

Developing countries and transition countries have clear cost

advantages in this regard.

The main purpose of the KfW Carbon Fund for Climate

Protection is that of purchasing certificates from projects that

utilize renewable energies or enhance energy efficiency. Fund

investors will be enterprises that must reduce their green-

house gas emissions but do not themselves intend to invest

abroad. They will be able to meet their reduction obligations

through the acquisition of CO2 reduction certificates. Public

funds can also be deposited in the Fund. The reduction credits

will be paid out to the depositors in proportion to their

contributions.

But not only the industrialized countries committed

to reducing emissions may benefit from emissions trading.

The additional revenues generated from the sale of certifi-

cates often allow technologies that are almost competitive to

be lifted over the threshold of profitability. This applies

particularly to the use of wind energy parks and small

hydropower plants. Another great potential exists in sewage

and landfill projects which reduce or avoid the particularly

ozone-damaging methane emissions. The implementation of

projects designed to protect the climate will direct additional

capital to developing and transition countries while serving

the transfer of technology at the same time.

CO2 reduction certificates contribute to lowering the

transfer and exchange rate risk in project financings. Earnings

from the sale of energy accrue in domestic currency but the

debt service and repayment of capital often have to be made

in foreign currency. As the revenues from the sale of CO2

certificates accrue in hard currency they offer protection

against some of these risks.

THE KYOTO PROTOCOL AND

THE PLANNED KFW CARBON FUND FOR CLIMATE PROTECTION

22

Promoting Sustainable Energy Supply in Developing Countries

CLIMATE PROTECTION BEGINS AT HOME: KFW NEUTRALIZES ITS CO2 EMISSIONS

As an enterprise KfW itself participates actively in protecting the Earth’s climate. Most of the CO2 emissions caused by

KfW result from the energy supply for its headquarters and from staff travel, particularly air travel. Total emissions are

approx. 16,000 t CO2 per year. KfW will invest EUR 1.2 million in funds of its own in a project designed to avoid the

corresponding volume of CO2 emissions through the “Clean Development Mechanism”. KfW will deactivate the result-

ing reduction certificates, that is, it will not place them in the market. This way it will neutralize its own emissions.

Energy partnerships are being constantly expanded

through the KfW Group’s long-standing cooperation and

strategic partnerships with other bilateral and multilateral

donors such as the World Bank and the EU. With this approach

we are seeking to enhance the coordination among donors,

particularly in the area of renewable energies. We are partic-

ipating primarily in the following initiatives, which were

launched alongside other initiatives around the topic of en-

ergy at the World Summit in Johannesburg: “Global Network

on Energy for Sustainable Development”, “Global Village En-

ergy Partnership” and “Global Forum for Sustainable Ener-

gies”. Apart from governments and international institutions,

members often include local initiatives and private organiza-

tions (NGOs) from donor and recipient countries. Within these

networks, members exchange their experiences concerning

strategies and approaches and identify promising projects.

The networks enable our partners in the developing countries

to access expertise, advice and financing for projects in the

energy sector.

The project examples presented on the following pages

offer an overview of the variety of approaches followed by

KfW and the DEG.

In the Kyoto Protocol which was signed in 1997 the industrialized countries committed themselves to limiting and reducing their emissions.

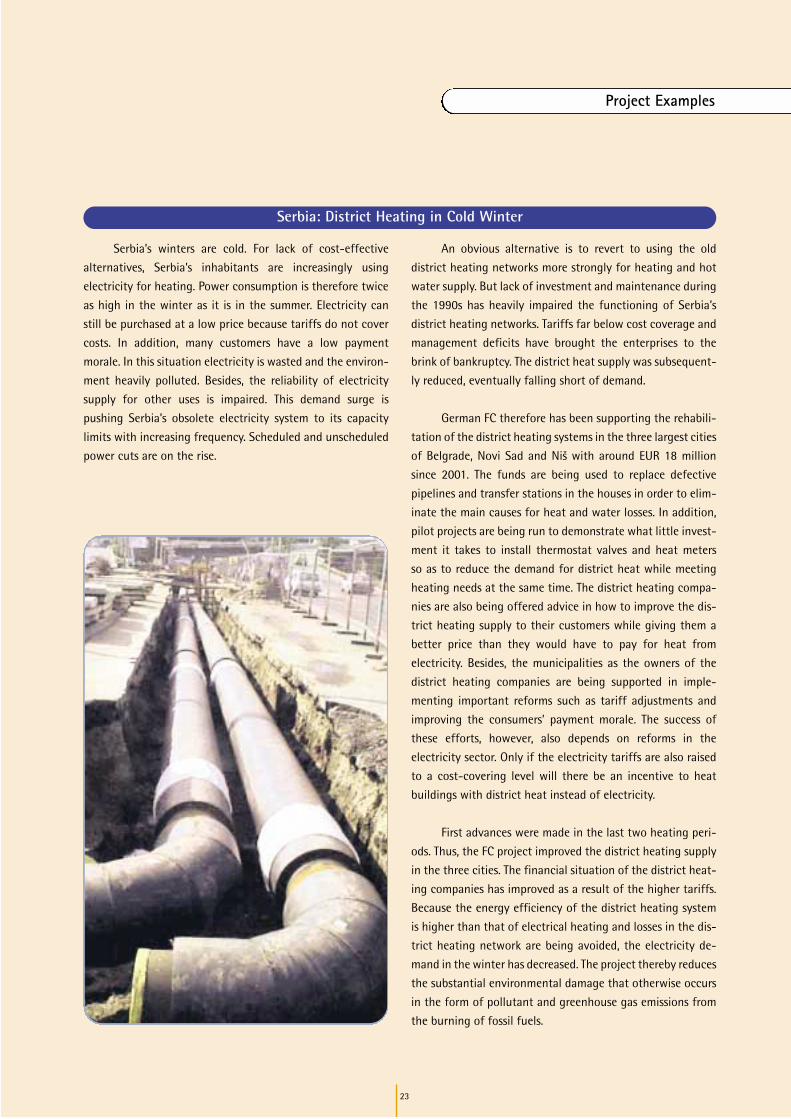

Serbia’s winters are cold. For lack of cost-effective

alternatives, Serbia’s inhabitants are increasingly using

electricity for heating. Power consumption is therefore twice

as high in the winter as it is in the summer. Electricity can

still be purchased at a low price because tariffs do not cover

costs. In addition, many customers have a low payment

morale. In this situation electricity is wasted and the environ-

ment heavily polluted. Besides, the reliability of electricity

supply for other uses is impaired. This demand surge is

pushing Serbia’s obsolete electricity system to its capacity

limits with increasing frequency. Scheduled and unscheduled

power cuts are on the rise.

An obvious alternative is to revert to using the old

district heating networks more strongly for heating and hot

water supply. But lack of investment and maintenance during

the 1990s has heavily impaired the functioning of Serbia’s

district heating networks. Tariffs far below cost coverage and

management deficits have brought the enterprises to the

brink of bankruptcy. The district heat supply was subsequent-

ly reduced, eventually falling short of demand.

German FC therefore has been supporting the rehabili-

tation of the district heating systems in the three largest cities

of Belgrade, Novi Sad and Nis with around EUR 18 million

since 2001. The funds are being used to replace defective

pipelines and transfer stations in the houses in order to elim-

inate the main causes for heat and water losses. In addition,

pilot projects are being run to demonstrate what little invest-

ment it takes to install thermostat valves and heat meters

so as to reduce the demand for district heat while meeting

heating needs at the same time. The district heating compa-

nies are also being offered advice in how to improve the dis-

trict heating supply to their customers while giving them a

better price than they would have to pay for heat from

electricity. Besides, the municipalities as the owners of the

district heating companies are being supported in imple-

menting important reforms such as tariff adjustments and

improving the consumers’ payment morale. The success of

these efforts, however, also depends on reforms in the

electricity sector. Only if the electricity tariffs are also raised

to a cost-covering level will there be an incentive to heat

buildings with district heat instead of electricity.

First advances were made in the last two heating peri-

ods. Thus, the FC project improved the district heating supply

in the three cities. The financial situation of the district heat-

ing companies has improved as a result of the higher tariffs.

Because the energy efficiency of the district heating system

is higher than that of electrical heating and losses in the dis-

trict heating network are being avoided, the electricity de-

mand in the winter has decreased. The project thereby reduces

the substantial environmental damage that otherwise occurs

in the form of pollutant and greenhouse gas emissions from

the burning of fossil fuels.

23

Serbia: District Heating in Cold Winter

Project Examples

24

Bangladesh’s electricity sector is still characterized by

two very different institutional structures. One is the

Bangladesh Power Development Board (BPDB), which has

limited financial capacity and technical efficiency. BPDB is to-

day the main player in the area of electricity generation,

transmission and distribution. The other is the rural electri-

city sector in which privately organized electricity distribu-

tion cooperatives operate under the umbrella of the Rural

Electrification Board (REB).

The REB is much more efficient than the BPDB. Indica-

tors of this include the degree of cost recovery through tariffs,

the system losses and consumers' payment morale. With the

approval of the government the REB has founded a power

plant company, the Rural Power Company (RPC). So far it is

the only domestically owned, privately organized electricity-

generating company in Bangladesh. In the 1990s the RPC

built a gas turbine power plant with a capacity of 140 MW in

Mymensingh in the north of the country. The electricity

generated by this power plant is fed into the national trans-

mission grid.

The country's entire electricity sector is suffering from

considerable bottlenecks in generation which often result in

Project Examples

A combined heat and power station can achieve a 50 % higher power output without additional fuel.

Bangladesh: Clean and Efficient Power Generation by the Private Sector

blackouts. This is why the RPC is planning to expand the

Mymensingh power plant. The existing steam power plant is

to be converted into a combined-cycle plant with a total

capacity of 216 MW. The exhaust gas from the existing gas

turbines will be harnessed to generate high-pressure steam

which will drive a steam turbine to generate electricity. This

will raise the capacity of the power plant by around 50 %

without the need for additional fuel – a particular advantage.

The plant will generate around 500 GWh additionally.

This makes the project environmentally benign as well as

economically efficient.

KfW committed FC funds of EUR 21 million to co-fi-

nance the investment cost. The plant will be constructed by

a German enterprise on a turnkey basis and the owner will

be the RPC.

The expanded power plant will be operated as a private

business under a joint venture with a German consulting firm.

An operator model of this kind could serve as a model

for other privatization projects in Bangladesh's electricity

sector. The project aims to improve energy efficiency and

promotes reforms in the electricity sector by supporting

private players in this previously state-dominated sector.

25

China I: Modernized Coal-Fired Power Plants for Cleaner Air and More Energy

In the People's Republic of China live around 1.3 billion

people who need to be supplied with electricity. With around

1,500 billion kilowatt hours annually the People's Republic of

China is the world's second largest producer of electricity

after the USA - and already the second-largest CO2 emitter

after the USA. In a few years China could move up to first

place, with 30 % of all CO2 emissions. It is estimated that

electricity consumption will grow sixfold from increasing

industrialization and rising standards of living by the year

2050. China produces 75 % of its electricity in coal-fired

power plants and mostly from coal with a high sulphur con-

tent.

As some of the existing technologies are obsolete,

power supply is associated with considerable environmental

problems. Ambient air pollution is a particularly serious prob-

lem. Particulates and sulphur dioxide, which leads to acid rain,