Embed Size (px)

Citation preview

Notas de Aula (Gibbons, 1992) - Teoria dos Jogos

J. Bertolai

September 26, 2017

Contents

Teoria dos Jogos: Panorama geral 2

Um exemplo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

A Teoria Economica e a Teoria dos Jogos . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Cap. 1 - Static Games of Complete Information 15

1.1 Normal form games and Nash equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

1.2 Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

1.3 Mixed strategies and existence of equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Cap. 2 - Dynamic Games of Complete Information 49

2.1 Dynamic games of complete and perfect information . . . . . . . . . . . . . . . . . . . . . . . 49

2.2 Two-stage games of complete but imperfect information . . . . . . . . . . . . . . . . . . . . . 61

2.3 Repeated games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

2.4 Dynamic games of complete but imperfect information . . . . . . . . . . . . . . . . . . . . . . 96

Cap. 3 - Static Games of Incomplete Information 107

3.1 Static Bayesian games and Bayesian Nash equilibrium . . . . . . . . . . . . . . . . . . . . . . 107

3.2 Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

3.3 The Revelation Principle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Cap. 4 - Dynamic games of incomplete information 132

4.1 Introduction to Perfect Bayesian equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

4.2 Signaling Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

4.3 Other applications of Signaling Games . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

4.4 Refinements of Perfect Bayesian Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . 188

Topicos Especiais 199

Instabilidade Financeira (Bank runs) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 199

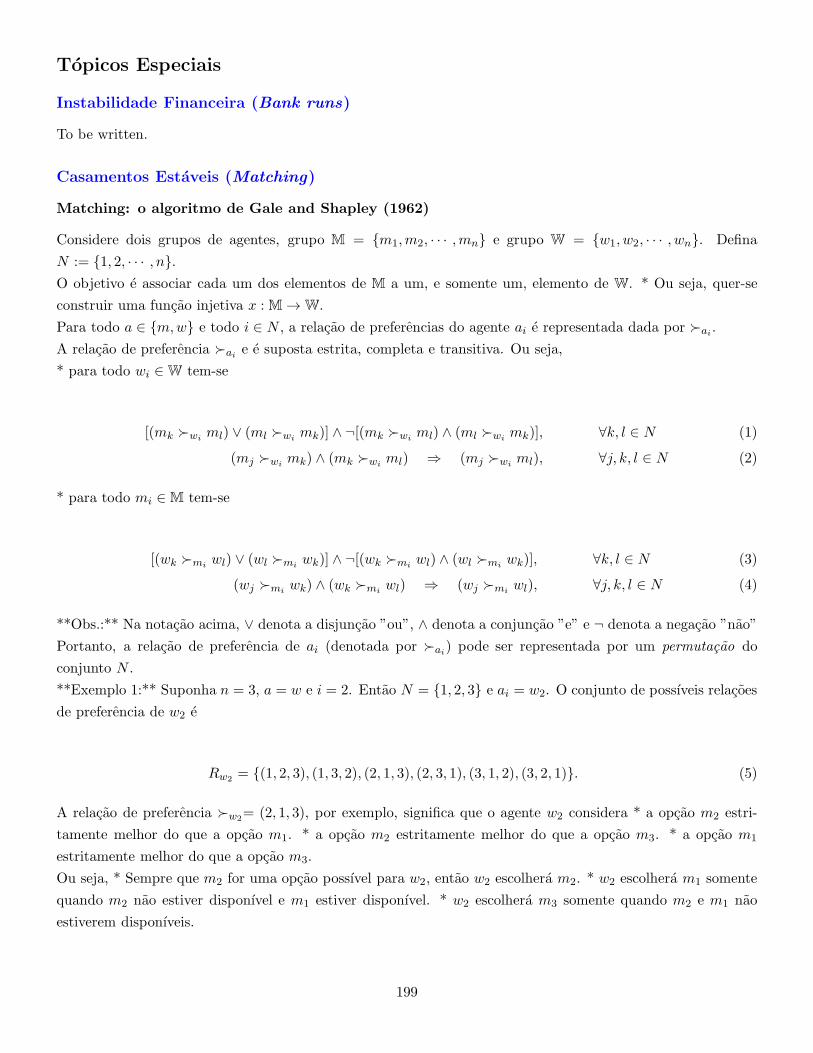

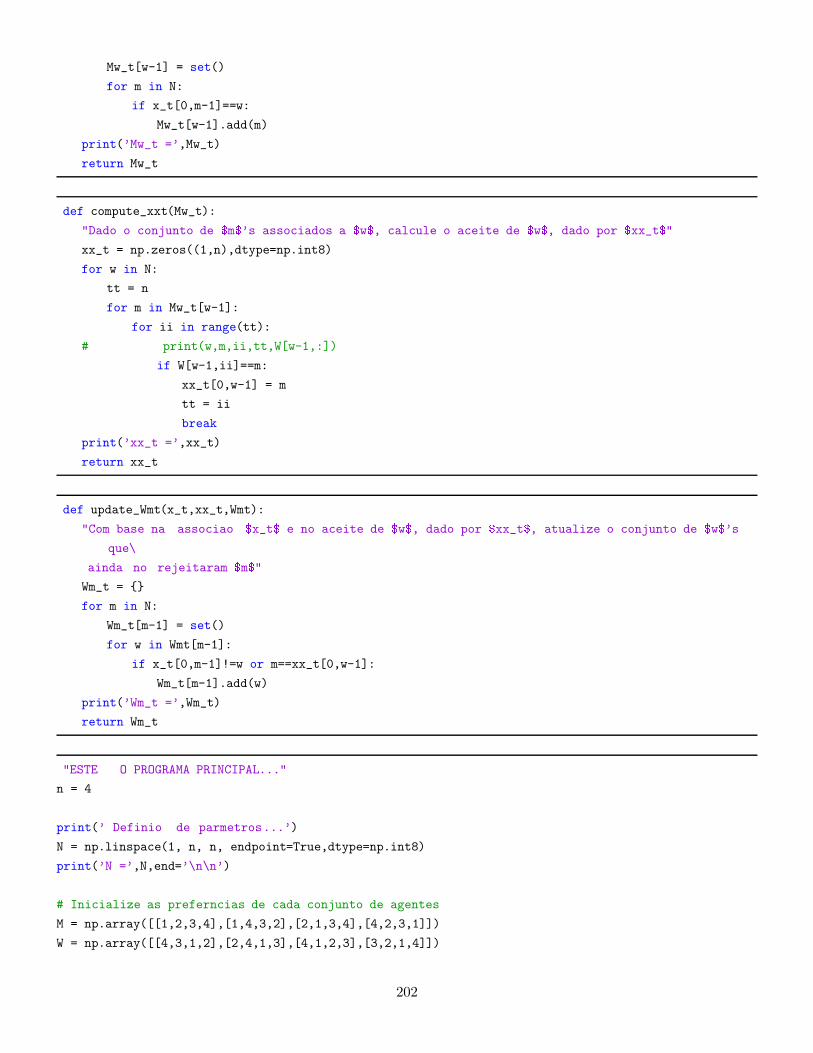

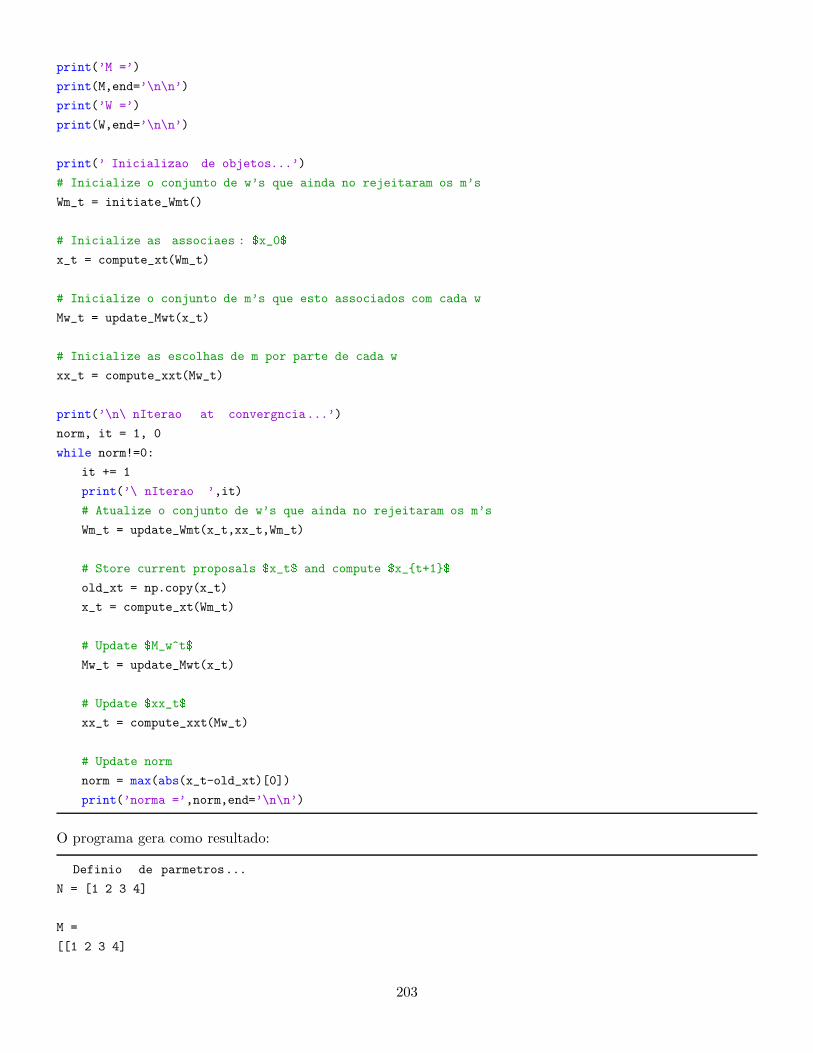

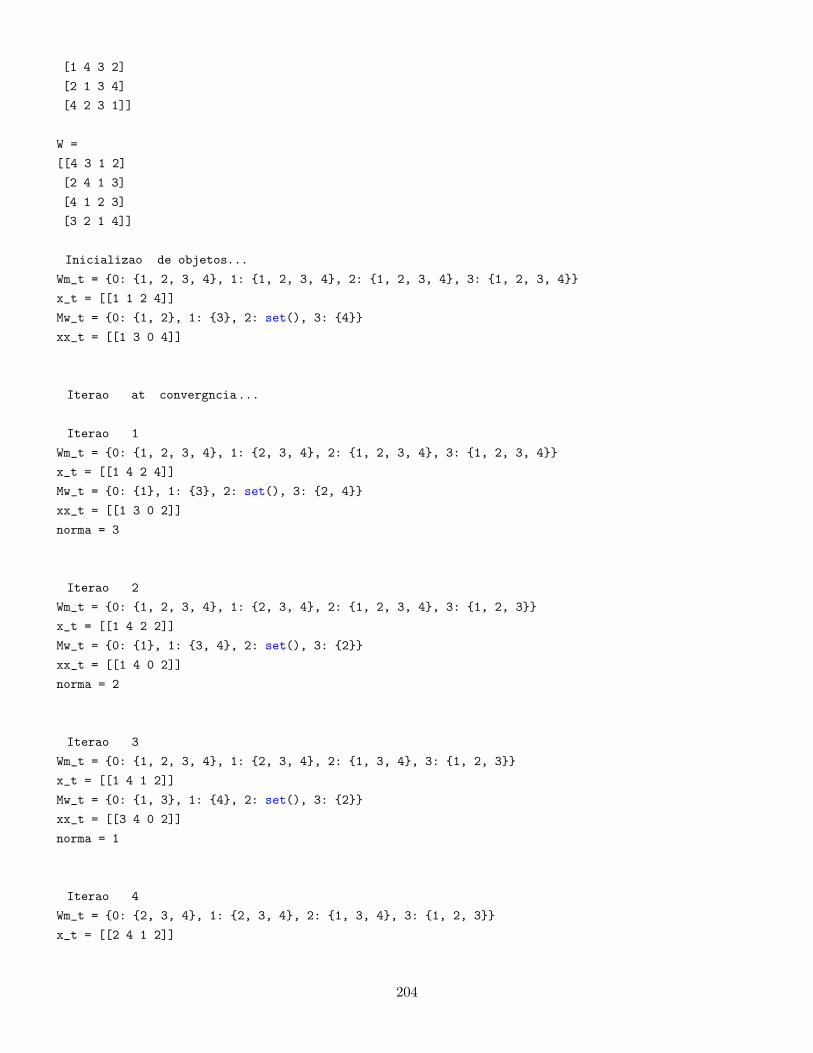

Casamentos Estaveis (Matching) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 199

References 206

1

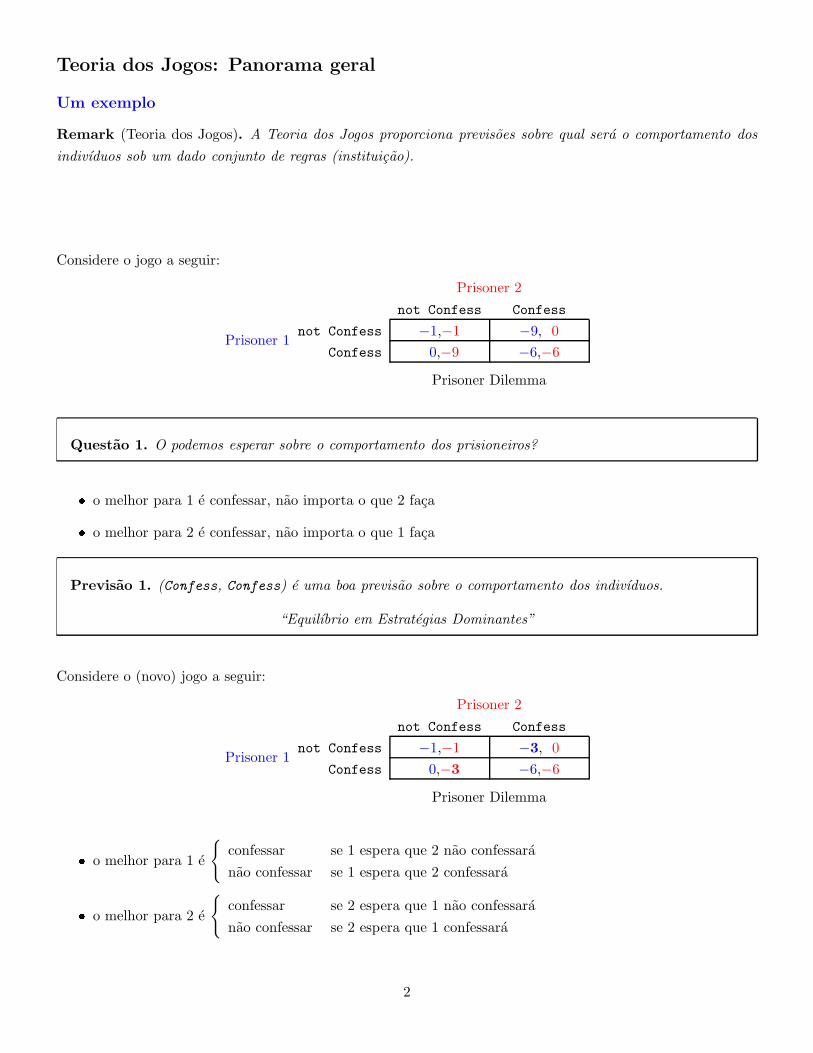

Teoria dos Jogos: Panorama geral

Um exemplo

Remark (Teoria dos Jogos). A Teoria dos Jogos proporciona previsoes sobre qual sera o comportamento dos

indivıduos sob um dado conjunto de regras (instituicao).

Considere o jogo a seguir:

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −9, 0

Confess 0,−9 −6,−6

Prisoner Dilemma

Questao 1. O podemos esperar sobre o comportamento dos prisioneiros?

� o melhor para 1 e confessar, nao importa o que 2 faca

� o melhor para 2 e confessar, nao importa o que 1 faca

Previsao 1. (Confess, Confess) e uma boa previsao sobre o comportamento dos indivıduos.

“Equilıbrio em Estrategias Dominantes”

Considere o (novo) jogo a seguir:

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −3, 0

Confess 0,−3 −6,−6

Prisoner Dilemma

� o melhor para 1 e

{

confessar se 1 espera que 2 nao confessara

nao confessar se 1 espera que 2 confessara

� o melhor para 2 e

{

confessar se 2 espera que 1 nao confessara

nao confessar se 2 espera que 1 confessara

2

Previsao 2. Ha duas boas previsoes para o comportamento dos indivıduos: (not Confess, Confess) e

(Confess, not Confess)

“Equilıbrios de Nash”

Considere o (novo) jogo a seguir:

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −3,−3

Confess −3,−3 −6,−6

Prisoner Dilemma

� o melhor para 1 e

{

nao confessar se 1 espera que 2 nao confessara

nao confessar se 1 espera que 2 confessara

� o melhor para 2 e

{

nao confessar se 2 espera que 1 nao confessara

nao confessar se 2 espera que 1 confessara

Previsao 3. Ha somente uma boa previsao para o comportamento dos indivıduos:

“Equilıbrios de Nash”: (not Confess, not Confess)

Considere o (caso geral de) jogo a seguir:

Prisoner 1

Prisoner 2

not Confess Confess

not Confess a,a b,c

Confess c,b d,d

Prisoner Dilemma

3

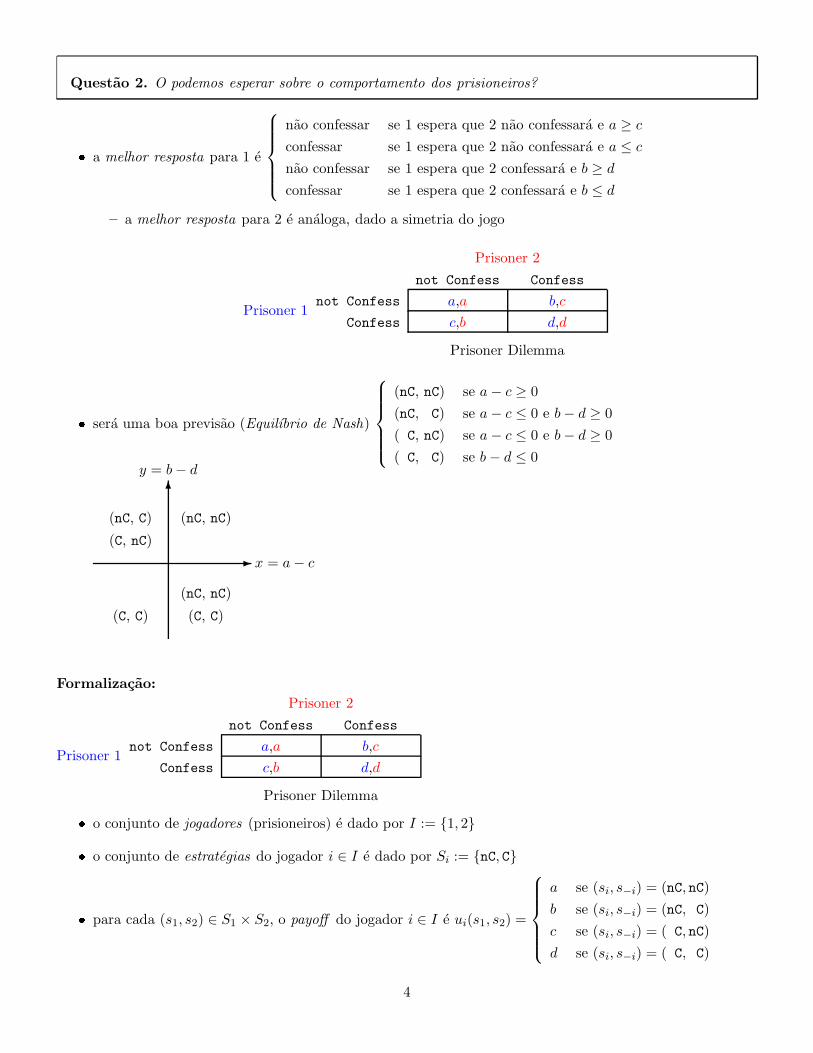

Questao 2. O podemos esperar sobre o comportamento dos prisioneiros?

� a melhor resposta para 1 e

nao confessar se 1 espera que 2 nao confessara e a ≥ c

confessar se 1 espera que 2 nao confessara e a ≤ c

nao confessar se 1 espera que 2 confessara e b ≥ d

confessar se 1 espera que 2 confessara e b ≤ d

– a melhor resposta para 2 e analoga, dado a simetria do jogo

Prisoner 1

Prisoner 2

not Confess Confess

not Confess a,a b,c

Confess c,b d,d

Prisoner Dilemma

� sera uma boa previsao (Equilıbrio de Nash)

(nC, nC) se a− c ≥ 0

(nC, C) se a− c ≤ 0 e b− d ≥ 0

( C, nC) se a− c ≤ 0 e b− d ≥ 0

( C, C) se b− d ≤ 0

✲

✻

x = a− c

y = b− d

(nC, nC)

(nC, nC)

(C, C)(C, C)

(nC, C)

(C, nC)

Formalizacao:

Prisoner 1

Prisoner 2

not Confess Confess

not Confess a,a b,c

Confess c,b d,d

Prisoner Dilemma

� o conjunto de jogadores (prisioneiros) e dado por I := {1, 2}

� o conjunto de estrategias do jogador i ∈ I e dado por Si := {nC, C}

� para cada (s1, s2) ∈ S1 × S2, o payoff do jogador i ∈ I e ui(s1, s2) =

a se (si, s−i) = (nC, nC)

b se (si, s−i) = (nC, C)

c se (si, s−i) = ( C, nC)

d se (si, s−i) = ( C, C)

4

� o conjunto de melhores respostas de i para a conjectura s−i e dado por

Ri(s−i) := argmaxσ∈Si

ui(σ, s−i)

Definicao 1. O perfil de estrategias (s1, s2) e um equilıbrio de Nash se s1 ∈ R1(s2) e s2 ∈ R2(s1). Ou

seja, se si e ponto fixo de Ri ◦R−i:

s1 ∈ R1(R2(s1)) e s2 ∈ R2(R1(s2))

Teorema 1 (Nash et al. (1950)). In the n-player normal-form game

G = {S1, S2, · · · , Sn;u1, u2, · · · , un},

� if n is finite and Si is finite for every i

then there is at least one Nash Equilibrium (possibly involving mixed strategies).

Desenho de Mecanismos

Questao 3. Quais devem ser as possıveis sentencas dos prisioneiros (a, b, c e d) quando a sociedade deseja

que eles revelem a verdade (C,C) e

� nao se pode prender alguem sem alguma confissao por mais do que 1 ano (a ≥ −1);

� nao se pode prender alguem usando testemunha por mais do que 2 anos (b ≥ −2);

� nao se pode prender alguem usando confissao por mais do que 10 anos (c ≥ −10 e d ≥ −10); e

� a sociedade deseja maximizar −a− b− c− d?

P1

P2

nC C

nC a,a b,c

C c,b d,d

Prisoner Dilemma

5

Ou seja, como desenhar o mecanismo otimo para revelar a verdade?

� se houvesse evidencia de culpa dos 2 prisioneiros, a sociedade escolheria (a, b, c, d) = (−1,−2,−10,−10)

� como nao ha evidencia da culpa, ninguem confessara o crime se (a, b, c, d) = (−1,−2,−10,−10)

P1

P2

nC C

nC a,a b,c

C c,b d,d

Prisoner Dilemma

✲

✻

x = a− c

y = b− d

(nC, nC)

(nC, nC)

(C, C)(C, C)

(nC, C)

(C, nC)

Questao 4. Como convencer os prisioneiros a confessar?

� os 2 indivıduos confessam somente quando y = b− d ≤ 0

– esta restricao e chamada de restricao de incentivos

� as penas sao limitadas (a ≥ −1, b ≥ −2 e c, d ≥ −10)

– esta restricao e chamada de restricao de factibilidade

� O mecanismo (a, b, c, d) otimo resolve:

max(a,b,c,d)

−(a+ b+ c+ d) s.t.

a ≥ −1

b ≥ −2

c, d ≥ −10

b ≤ d

,

ou seja, ele e dado por m∗ := (a∗, b∗, c∗, d∗) = (−1,−2,−10,−2)

Observacao 1. “A sociedade desenha o mecanismo para induzir a confissao (C,C), mas pode acabar em

uma situacao (nC,nC) pior do que a esperada.”

Proof. Sob o mecanismo otimo m∗ = (−1,−2,−10,−2) tem-se

x = a∗ − c∗ = 9 > 0 e y = b∗ − d∗ = 0 ≥ 0

6

e, portanto, ha dois equilıbrios de Nash: (nC, nC) e (C, C).

✲

✻

x = a− c

y = b− d

(nC, nC)

(nC, nC)

(C, C)(C, C)

(nC, C)

(C, nC)

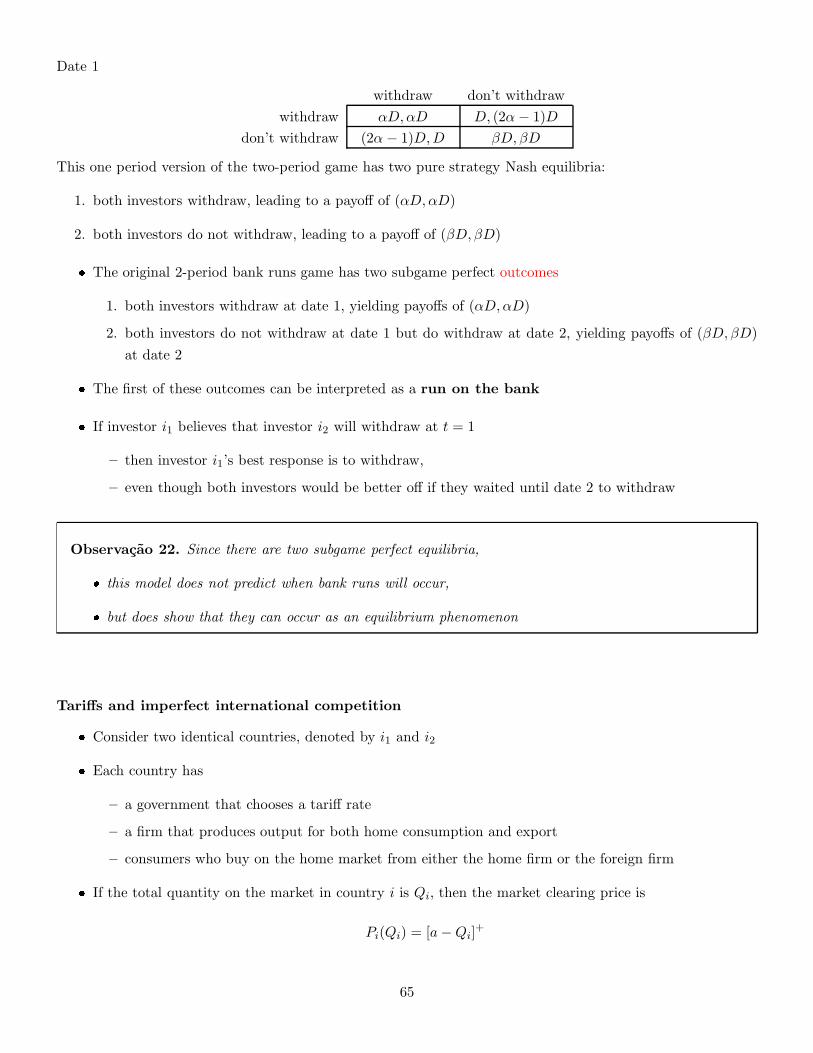

Aplicacao: Corrida Bancaria em equilıbrio

� Ha dois indivıduos na economia, chamados depositantes.

� Os depositantes vivem por 3 perıodos: t = 0, 1, 2

– perıodo inicial (data 0)

– curto prazo (data 1)

– longo prazo (data 2)

e auferem utilidade u(c1 + c2) = c1 + c2

– c1 consumo no perıodo t = 1

– c2 consumo no perıodo t = 2

e possuem dotacao inicial (em t = 0) individual de D unidades de recursos

� Os indivıduos participam de um arranjo bancario de tres perıodos:

– decisao de investimento (data 0)

– curto prazo (data 1)

– longo prazo (data 2)

� Na data zero ambos depositam D unidades de recurso no banco.

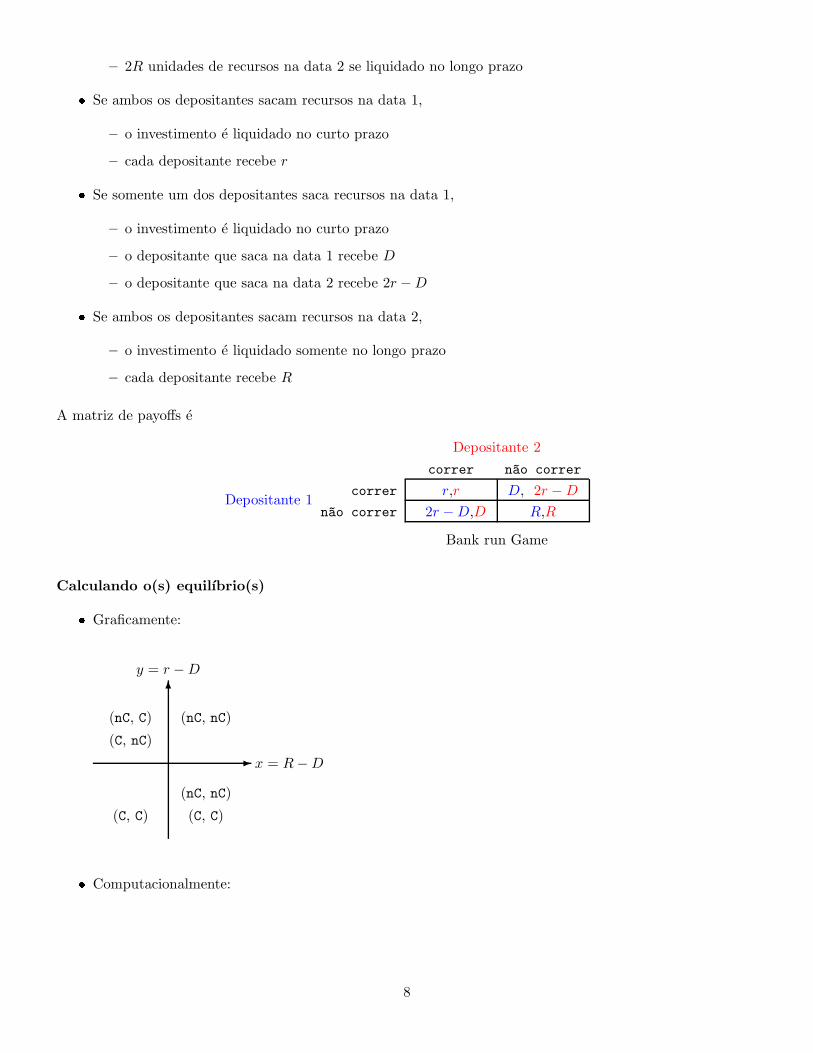

� O banco recebe 2D unidades de recurso e as aplica em um investimento que rende:

– 2r unidades de recursos na data 1 se liquidado no curto prazo

7

– 2R unidades de recursos na data 2 se liquidado no longo prazo

� Se ambos os depositantes sacam recursos na data 1,

– o investimento e liquidado no curto prazo

– cada depositante recebe r

� Se somente um dos depositantes saca recursos na data 1,

– o investimento e liquidado no curto prazo

– o depositante que saca na data 1 recebe D

– o depositante que saca na data 2 recebe 2r −D

� Se ambos os depositantes sacam recursos na data 2,

– o investimento e liquidado somente no longo prazo

– cada depositante recebe R

A matriz de payoffs e

Depositante 1

Depositante 2

correr n~ao correr

correr r,r D, 2r −D

n~ao correr 2r −D,D R,R

Bank run Game

Calculando o(s) equilıbrio(s)

� Graficamente:

✲

✻

x = R−D

y = r −D

(nC, nC)

(nC, nC)

(C, C)(C, C)

(nC, C)

(C, nC)

� Computacionalmente:

8

def payoffs(x,y):

"""Para cada par de estrat\’egias s1=x e s2=y,

esta fun\c{c}\~aoo retorna o payoff do jogador 1 e o payoff do jogador 2"""

if x==’correr’:

if y==’correr’:

z = [r,r]

else:

z = [D,2*r-D]

else:

if y== ’correr’:

z = [2*r-D,D]

else:

z = [R,R]

return z

def NE( S = (’correr’,’no correr’) ):

equilibrios = []

# Para cada perfil de estratgias s = (s1,s2)

for s1 in S:

for s2 in S:

# verifique se ’s’ equilbrio

v = payoffs(s1,s2)

eq = True

for t in S:

if payoffs(t,s2)[0]>v[0] or payoffs(s1,t)[1]>v[1]:

eq = False

break

if eq:

equilibrios.append(’({},{})’.format(s1,s2))

return equilibrios

– O programa a seguir usa as funcoes payoffs() e NE() para calcular o conjunto de equilıbrios de

Nash.

* dois casos serao estudados

* em ambos os casos, a dotacao inicial e D = 1 e o retorno de longo prazo e de 20%, ou seja,

R = 1.2

* no primeiro caso, o retorno de curto prazo e 10%, ou seja, r = 1.1

* no segundo caso, o retorno de curto prazo e −10%, ou seja, r = 0.9

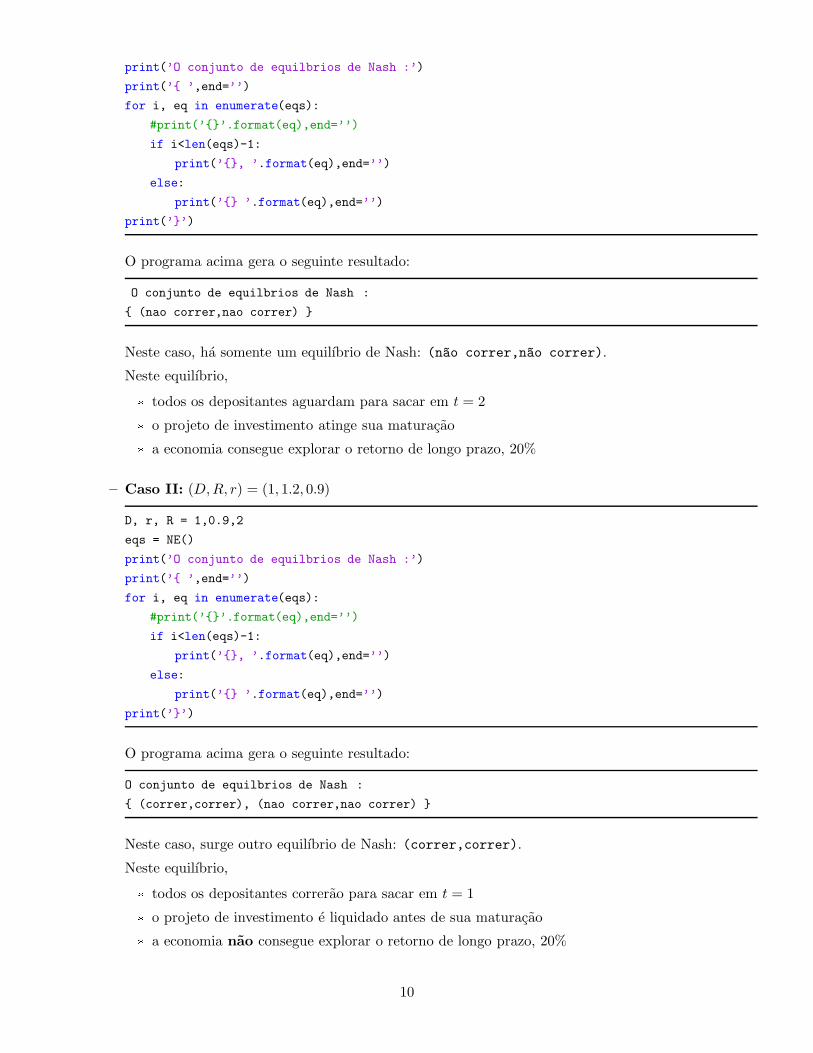

– Caso I: (D,R, r) = (1, 1.2, 1.1)

D, r, R = 1,1.1,1.2

eqs = NE()

9

print(’O conjunto de equilbrios de Nash :’)

print(’{ ’,end=’’)

for i, eq in enumerate(eqs):

#print(’{}’.format(eq),end=’’)

if i<len(eqs)-1:

print(’{}, ’.format(eq),end=’’)

else:

print(’{} ’.format(eq),end=’’)

print(’}’)

O programa acima gera o seguinte resultado:

O conjunto de equilbrios de Nash :

{ (nao correr,nao correr) }

Neste caso, ha somente um equilıbrio de Nash: (n~ao correr,n~ao correr).

Neste equilıbrio,

* todos os depositantes aguardam para sacar em t = 2

* o projeto de investimento atinge sua maturacao

* a economia consegue explorar o retorno de longo prazo, 20%

– Caso II: (D,R, r) = (1, 1.2, 0.9)

D, r, R = 1,0.9,2

eqs = NE()

print(’O conjunto de equilbrios de Nash :’)

print(’{ ’,end=’’)

for i, eq in enumerate(eqs):

#print(’{}’.format(eq),end=’’)

if i<len(eqs)-1:

print(’{}, ’.format(eq),end=’’)

else:

print(’{} ’.format(eq),end=’’)

print(’}’)

O programa acima gera o seguinte resultado:

O conjunto de equilbrios de Nash :

{ (correr,correr), (nao correr,nao correr) }

Neste caso, surge outro equilıbrio de Nash: (correr,correr).

Neste equilıbrio,

* todos os depositantes correrao para sacar em t = 1

* o projeto de investimento e liquidado antes de sua maturacao

* a economia nao consegue explorar o retorno de longo prazo, 20%

10

Observacao 2. A previsao do modelo neste caso e:

– ou a economia beneficiara do retorno de longo prazo (Estabilidade bancaria)

– ou a economia estara em situacao pior do que sem o arranjo bancario (Instabilidade bancaria)

mas nao ha certeza sobre qual equilıbrio emergira.

A Teoria Economica e a Teoria dos Jogos

Teoria Economica: estudo das formas alternativas de se alocar recursos escassos.

Economics is a science which studies human behavior as a relationship between ends and scarce means which

have alternative uses

� fim ultimo da Ciencia Economica e o indivıduo e seu bem estar

Exemplo: como escassez determina alocacao otima

Considere uma economia habitada por I indivıduos

� com somente J = 2 bens, cuja dotacao e ωj ≥ 0, e sem producao

Definicao 2. Uma alocacao e um vetor

x =((x11, x

21), (x

12, x

22), . . . , (x

1I , x

2I))∈ R

2I+

que especifica uma cesta de consumo (x1i , x2i ) ∈ R

2+ para cada indivıduo i ∈ {1, 2, . . . , I}. A alocacao e dita

factıvel seI∑

i=1

xji ≤ ωj, ∀j ∈ {1, 2}.

11

� distribuicao de recursos entre os indivıduos

� Caixa de Edgeworth (I = 2)

Eficiencia vs Equidade: o que e uma alocacao socialmente otima?

Definicao 3. Uma alocacao factıvel x ∈ R2I+ e Pareto otima se nao existe outra alocacao x′ ∈ R

2I+ factıvel

tal que

ui(x′i) ≥ ui(xi) para todo i ∈ {1, 2, . . . , I}

e ui(x′i) > ui(xi) para algum i.

� propriedade mınima e consensual

– mınima: toda alocacao otima precisa ser Pareto otima

– consensual: nao pode haver desperdıcio sob a alocacao otima

� Caixa de Edgeworth e a Curva de Contrato

Economics and Efficiency

Eficiencia como criterio de previsao: Eficiencia de Pareto e a regra, nao a excecao

� Certo consenso entre economistas

� Melhorias de Pareto: por que esperar que elas nao sao exploradas?

� Principal criterio de previsao da Teoria economica

An equilibrium concept: competitive equilibrium – markets and prices

Definicao 4. Uma alocacao x∗ ∈ R2I+ e um preco p∗ = (p∗1, p

∗2) ∈ R

2+ constituem um equilıbrio competitivo

se

� Utility maximization: para cada consumidor i, x∗i resolve

maxx∈R2

+

{ui(xi) : s.t. p∗1x

1 + p∗2x2 ≤ p∗1ω

1i + p∗ω2

i

}

12

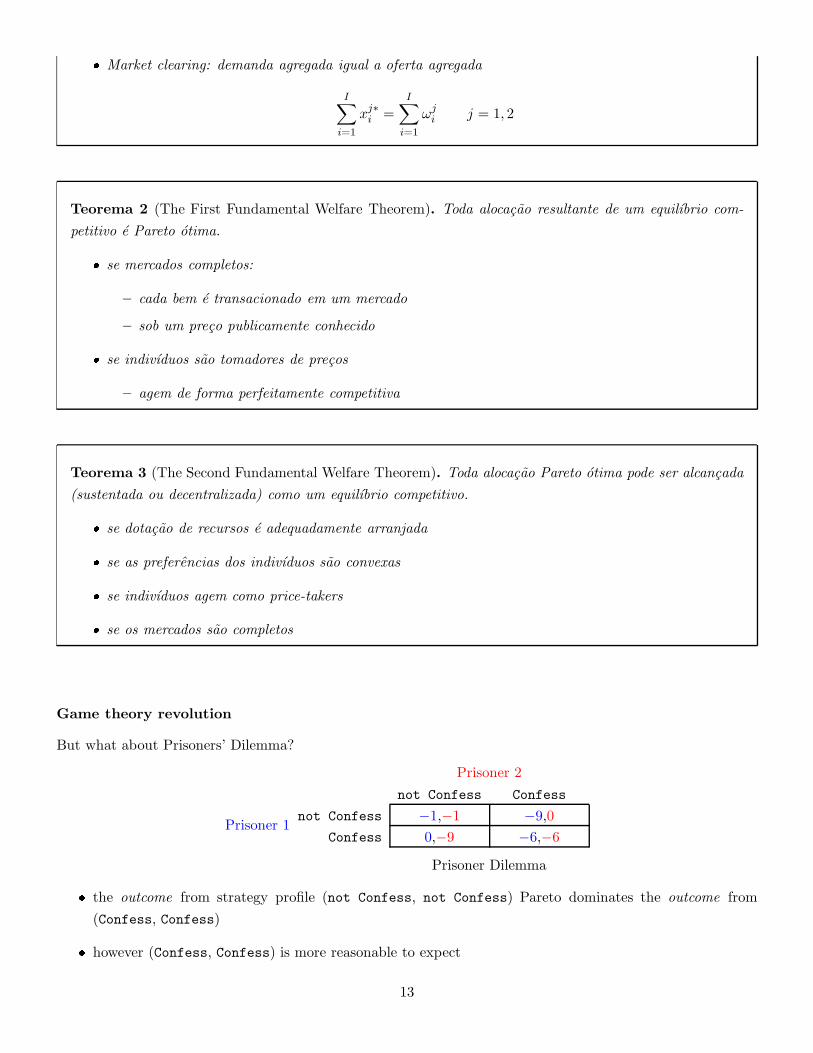

� Market clearing: demanda agregada igual a oferta agregada

I∑

i=1

xj∗i =I∑

i=1

ωji j = 1, 2

Teorema 2 (The First Fundamental Welfare Theorem). Toda alocacao resultante de um equilıbrio com-

petitivo e Pareto otima.

� se mercados completos:

– cada bem e transacionado em um mercado

– sob um preco publicamente conhecido

� se indivıduos sao tomadores de precos

– agem de forma perfeitamente competitiva

Teorema 3 (The Second Fundamental Welfare Theorem). Toda alocacao Pareto otima pode ser alcancada

(sustentada ou decentralizada) como um equilıbrio competitivo.

� se dotacao de recursos e adequadamente arranjada

� se as preferencias dos indivıduos sao convexas

� se indivıduos agem como price-takers

� se os mercados sao completos

Game theory revolution

But what about Prisoners’ Dilemma?

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −9,0

Confess 0,−9 −6,−6

Prisoner Dilemma

� the outcome from strategy profile (not Confess, not Confess) Pareto dominates the outcome from

(Confess, Confess)

� however (Confess, Confess) is more reasonable to expect

13

Another equilibrium concept: Nash equilibrium

Strategic interdependence:

� Each individual’s welfare depends not only on his own actions but also on the actions of the other

individuals

� The actions that are best for an individual to take may depend on what he expects the other players to

do

Even more equilibrium concepts and some refinements:

� Equilibrium in Dominant strategies

� Nash equilibrium

� subgame-Perfect Nash equilibrium

� Bayesian Nash equilibrium

� Perfect Bayesian Nash equilibrium

� The Intuitive Criterion (Cho and Kreps (1987))

Mechanism Design

Questao 5 (Choosing among games:). How to design games in order to implement optimal allocations?

� Principal-Agent problems

– moral hazard

– adverse selection

� The Social Planner problems (social optimum)

– fiscal policy

– monetary policy

– regulation

� The Revelation Principle

14

Cap. 1 - Static Games of Complete Information

Static Games of Complete Information:

� Static:

– players simultaneously choose actions

– payoffs players receive depend on the combination of actions just chosen

� Complete information:

– each player’s payoff function is common knowledge among all players

– exemplo: leiloes

Questao 6. What is a game?

Definicao 5. A game is a formal representation of a situation in which a number of individuals interact

in a setting of strategic interdependence.

� Each individual’s welfare depends not only on his own actions but also on the actions of the other

individuals

� The actions that are best for an individual to take may depend on what he expects the other players to

do

1.1 Normal form games and Nash equilibrium

Normal-form representation of games

In the normal-form representation of the game

� each player simultaneously chooses a strategy.

� the combination of strategies chosen by players determines a payoff for each player

Exemplo 1 (The prisoners’ dilemma).

The environment

� Two suspects are arrested and charged with a crime

� The police lack sufficient evidence to convict the suspects, unless at least one confesses

� The suspects are in separate cells

� The police explain the consequences that will follow from the actions they could take

15

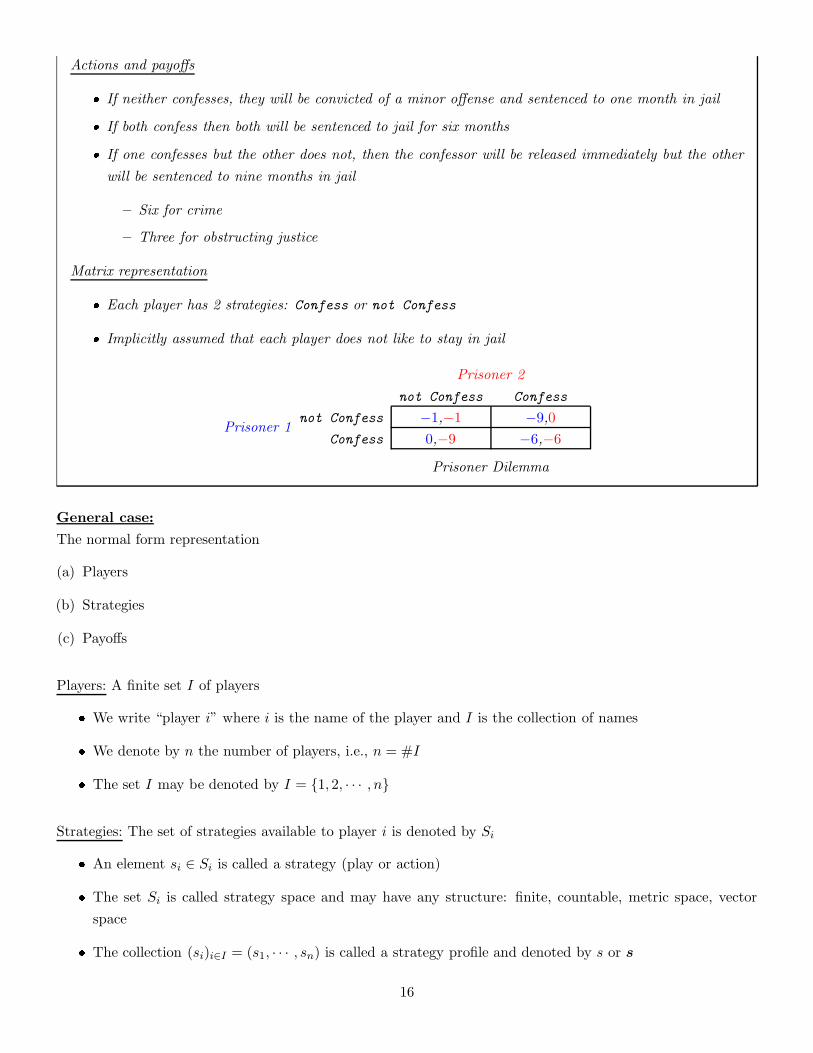

Actions and payoffs

� If neither confesses, they will be convicted of a minor offense and sentenced to one month in jail

� If both confess then both will be sentenced to jail for six months

� If one confesses but the other does not, then the confessor will be released immediately but the other

will be sentenced to nine months in jail

– Six for crime

– Three for obstructing justice

Matrix representation

� Each player has 2 strategies: Confess or not Confess

� Implicitly assumed that each player does not like to stay in jail

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −9,0

Confess 0,−9 −6,−6

Prisoner Dilemma

General case:

The normal form representation

(a) Players

(b) Strategies

(c) Payoffs

Players: A finite set I of players

� We write “player i” where i is the name of the player and I is the collection of names

� We denote by n the number of players, i.e., n = #I

� The set I may be denoted by I = {1, 2, · · · , n}

Strategies: The set of strategies available to player i is denoted by Si

� An element si ∈ Si is called a strategy (play or action)

� The set Si is called strategy space and may have any structure: finite, countable, metric space, vector

space

� The collection (si)i∈I = (s1, · · · , sn) is called a strategy profile and denoted by s or s

16

� Given an agent j and a profile s, we denote by (s−j ; s′j) the new profile σ = (σi)i∈I defined by

σi =

{

s′j if i = j

si if i 6= j

1 < j < n ⇒ (s−j; s′j) = (s1, . . . , sj−1, s

′j , sj+1, . . . , sn)

Payoffs:

� The payoff of player i is a function

ui :

∏

j∈I Sj → [−∞,+∞]

s 7→ ui(s)

where ui(s) is the payoff of player i when

– he plays strategy si

– and any other player j plays strategy sj

� We use alternatively the following notation

ui(s) = ui ((sj)j∈I) = ui(s−i; si) = ui(s1, s2, . . . , sn)

Definicao 6. A game in normal form is a family

G = (Si, ui)i∈I

where for each i ∈ I

� Si is a set

� ui is a function from S =∏

j∈I Sj to [−∞,+∞]

Observacao 3. We should know describe how to solve a game-theoretic problem

Questao 7. Can we anticipate how a game will be played?

� What should we expect to observe in a game played by

– rational players

17

– who are fully knowledgeable about

* the structure of the game

* and each others’ rationality?

Simultaneous moves: In a normal form game the players choose their strategies simultaneously

� This does not imply that they act simultaneously

� It suffices that each choose his or her action without knowledge of the others’ choices

– Prisoners’ dilemma: the prisoners may reach decisions at arbitrary times but it must be in separate

cells

– Bidders in an sealed-bid auction

Iterated elimination of strictly dominated strategies

Definicao 7 (Strictly dominated strategies). Consider a normal form game (Si, ui)i∈I .

� Let s′i and s′′i be two strategies in Si.

Strategy s′i is strictly dominated by strategy s′′i if,

� for each possible combination of the other players’ strategies,

the player i’s payoff from playing s′i is strictly less than the payoff playing s′′i .

� Formally,

ui(s′i, s−i) < ui(s′′i , s−i) ∀s−i ∈∏

k 6=i

Sk,

Rationality: Rational players do not play strictly dominated strategies

Observacao 4 (The prisoners’ dilemma). For a prisoner, playing not Confess is strictly dominated by

playing Confess

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −9,0

Confess 0,−9 −6,−6

Prisoner Dilemma

18

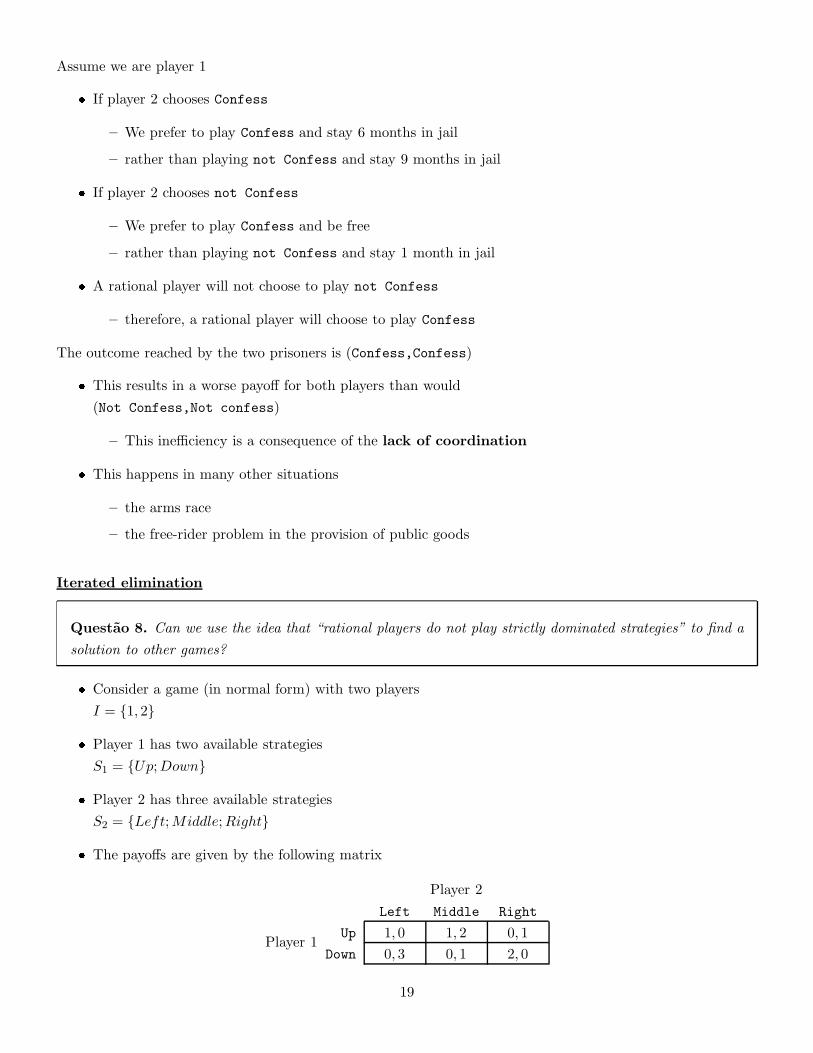

Assume we are player 1

� If player 2 chooses Confess

– We prefer to play Confess and stay 6 months in jail

– rather than playing not Confess and stay 9 months in jail

� If player 2 chooses not Confess

– We prefer to play Confess and be free

– rather than playing not Confess and stay 1 month in jail

� A rational player will not choose to play not Confess

– therefore, a rational player will choose to play Confess

The outcome reached by the two prisoners is (Confess,Confess)

� This results in a worse payoff for both players than would

(Not Confess,Not confess)

– This inefficiency is a consequence of the lack of coordination

� This happens in many other situations

– the arms race

– the free-rider problem in the provision of public goods

Iterated elimination

Questao 8. Can we use the idea that “rational players do not play strictly dominated strategies” to find a

solution to other games?

� Consider a game (in normal form) with two players

I = {1, 2}

� Player 1 has two available strategies

S1 = {Up;Down}

� Player 2 has three available strategies

S2 = {Left;Middle;Right}

� The payoffs are given by the following matrix

Player 1

Player 2

Left Middle Right

Up 1, 0 1, 2 0, 1

Down 0, 3 0, 1 2, 0

19

� for Player 1

– Up is not strictly dominated by Down

– Down is not strictly dominated by Up

� for Player 2

– Right is strictly dominated by Middle

– player 2 will never play Right

� if Player 1 knows that Player 2 is rational

– then Player 1 can eliminate Right from Player 2’s strategy set

� then both players can play the game as if it were the following game

Player 1

Player 2

Left Middle

Up 1, 0 1, 2

Down 0, 3 0, 1

� For Player 1 the strategy Down is strictly dominated by Up

� If Player 2 knows that

– Player 1 is rational; and

– Player 1 knows that Player 2 is rational

then Player 2 can eliminate Down from S1

� Now the game is as follows

Player 1

Player 2

Left Middle

Up 1, 0 1, 2

� For Player 2 the strategy Left is strictly dominated by Middle

Observacao 5. By iterated elimination of strictly dominated strategies

� the outcome of the game is (Up,Middle)

Definicao 8 (Iterated elimination of strictly dominated strategies). This process is called iterated elimi-

nation of strictly dominated strategies.

20

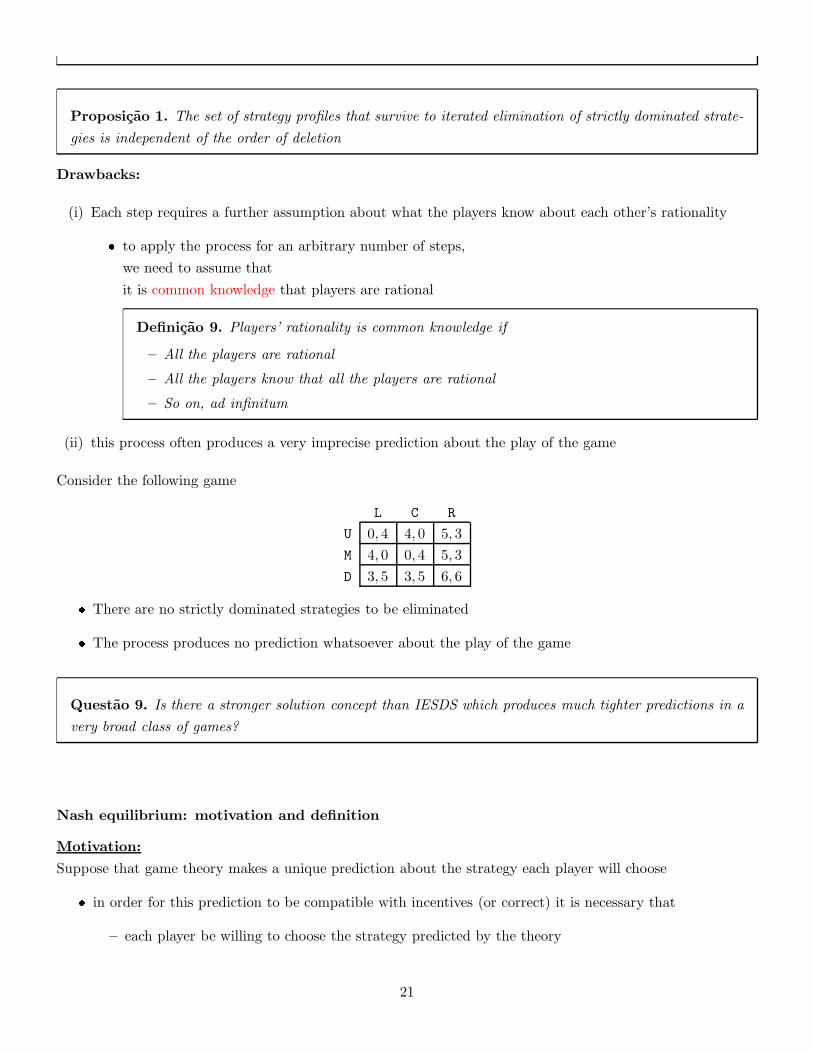

Proposicao 1. The set of strategy profiles that survive to iterated elimination of strictly dominated strate-

gies is independent of the order of deletion

Drawbacks:

(i) Each step requires a further assumption about what the players know about each other’s rationality

� to apply the process for an arbitrary number of steps,

we need to assume that

it is common knowledge that players are rational

Definicao 9. Players’ rationality is common knowledge if

– All the players are rational

– All the players know that all the players are rational

– So on, ad infinitum

(ii) this process often produces a very imprecise prediction about the play of the game

Consider the following game

L C R

U 0, 4 4, 0 5, 3

M 4, 0 0, 4 5, 3

D 3, 5 3, 5 6, 6

� There are no strictly dominated strategies to be eliminated

� The process produces no prediction whatsoever about the play of the game

Questao 9. Is there a stronger solution concept than IESDS which produces much tighter predictions in a

very broad class of games?

Nash equilibrium: motivation and definition

Motivation:

Suppose that game theory makes a unique prediction about the strategy each player will choose

� in order for this prediction to be compatible with incentives (or correct) it is necessary that

– each player be willing to choose the strategy predicted by the theory

21

– each player’s predicted strategies must be that player’s best response to the predicted strategies of

other players

� such a prediction could be called

strategically stable or self-enforcing

– no single player wants to deviate from his or her predicted strategy

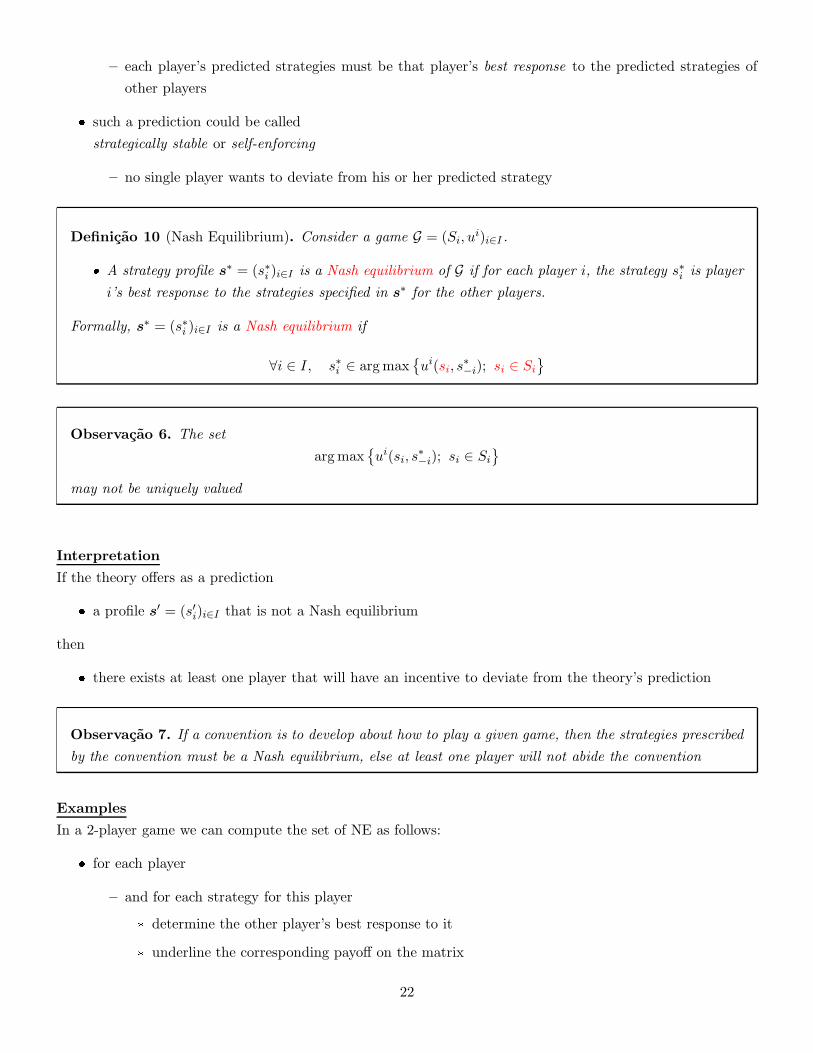

Definicao 10 (Nash Equilibrium). Consider a game G = (Si, ui)i∈I .

� A strategy profile s∗ = (s∗i )i∈I is a Nash equilibrium of G if for each player i, the strategy s∗i is player

i’s best response to the strategies specified in s∗ for the other players.

Formally, s∗ = (s∗i )i∈I is a Nash equilibrium if

∀i ∈ I, s∗i ∈ argmax{ui(si, s

∗−i); si ∈ Si

}

Observacao 6. The set

argmax{ui(si, s

∗−i); si ∈ Si

}

may not be uniquely valued

Interpretation

If the theory offers as a prediction

� a profile s′ = (s′i)i∈I that is not a Nash equilibrium

then

� there exists at least one player that will have an incentive to deviate from the theory’s prediction

Observacao 7. If a convention is to develop about how to play a given game, then the strategies prescribed

by the convention must be a Nash equilibrium, else at least one player will not abide the convention

Examples

In a 2-player game we can compute the set of NE as follows:

� for each player

– and for each strategy for this player

* determine the other player’s best response to it

* underline the corresponding payoff on the matrix

22

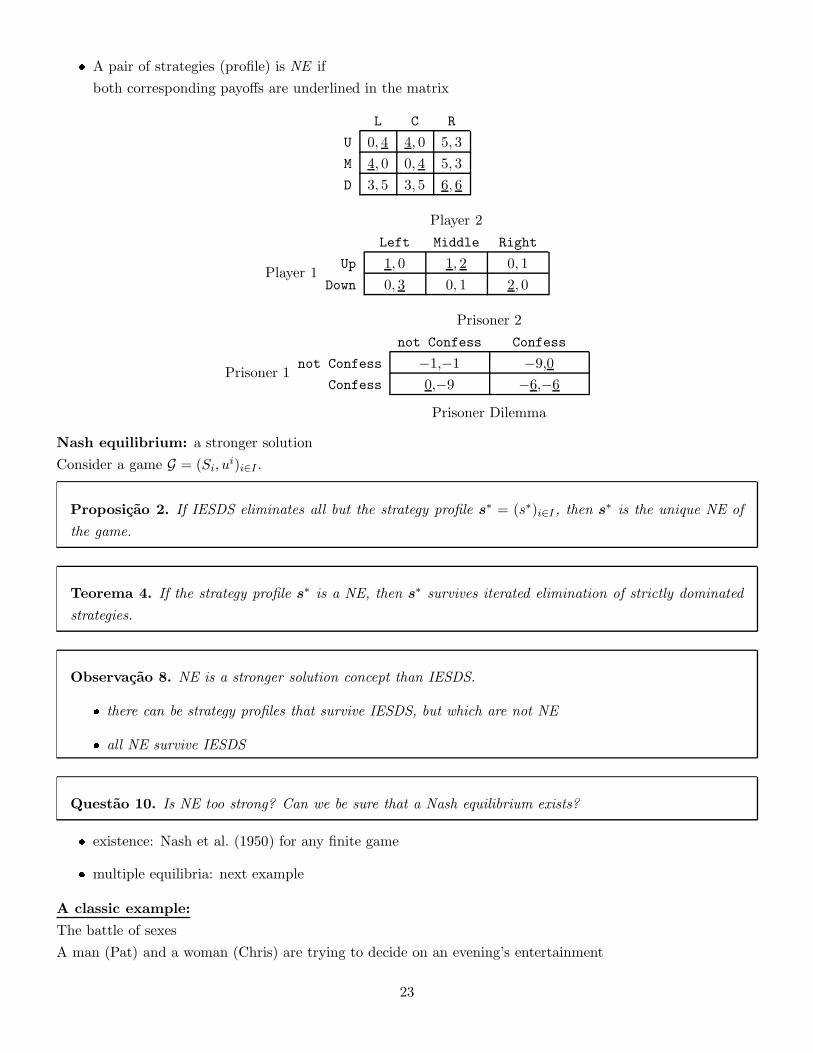

� A pair of strategies (profile) is NE if

both corresponding payoffs are underlined in the matrix

L C R

U 0, 4 4, 0 5, 3

M 4, 0 0, 4 5, 3

D 3, 5 3, 5 6, 6

Player 1

Player 2

Left Middle Right

Up 1, 0 1, 2 0, 1

Down 0, 3 0, 1 2, 0

Prisoner 1

Prisoner 2

not Confess Confess

not Confess −1,−1 −9,0

Confess 0,−9 −6,−6

Prisoner Dilemma

Nash equilibrium: a stronger solution

Consider a game G = (Si, ui)i∈I .

Proposicao 2. If IESDS eliminates all but the strategy profile s∗ = (s∗)i∈I , then s∗ is the unique NE of

the game.

Teorema 4. If the strategy profile s∗ is a NE, then s∗ survives iterated elimination of strictly dominated

strategies.

Observacao 8. NE is a stronger solution concept than IESDS.

� there can be strategy profiles that survive IESDS, but which are not NE

� all NE survive IESDS

Questao 10. Is NE too strong? Can we be sure that a Nash equilibrium exists?

� existence: Nash et al. (1950) for any finite game

� multiple equilibria: next example

A classic example:

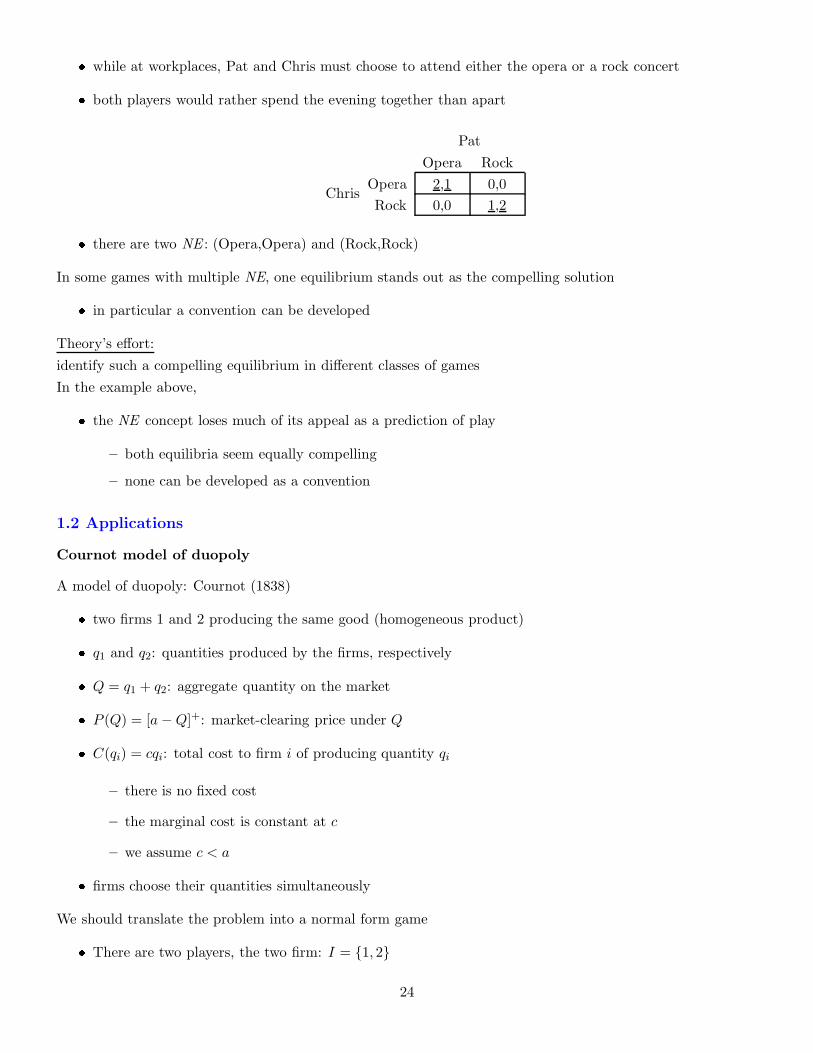

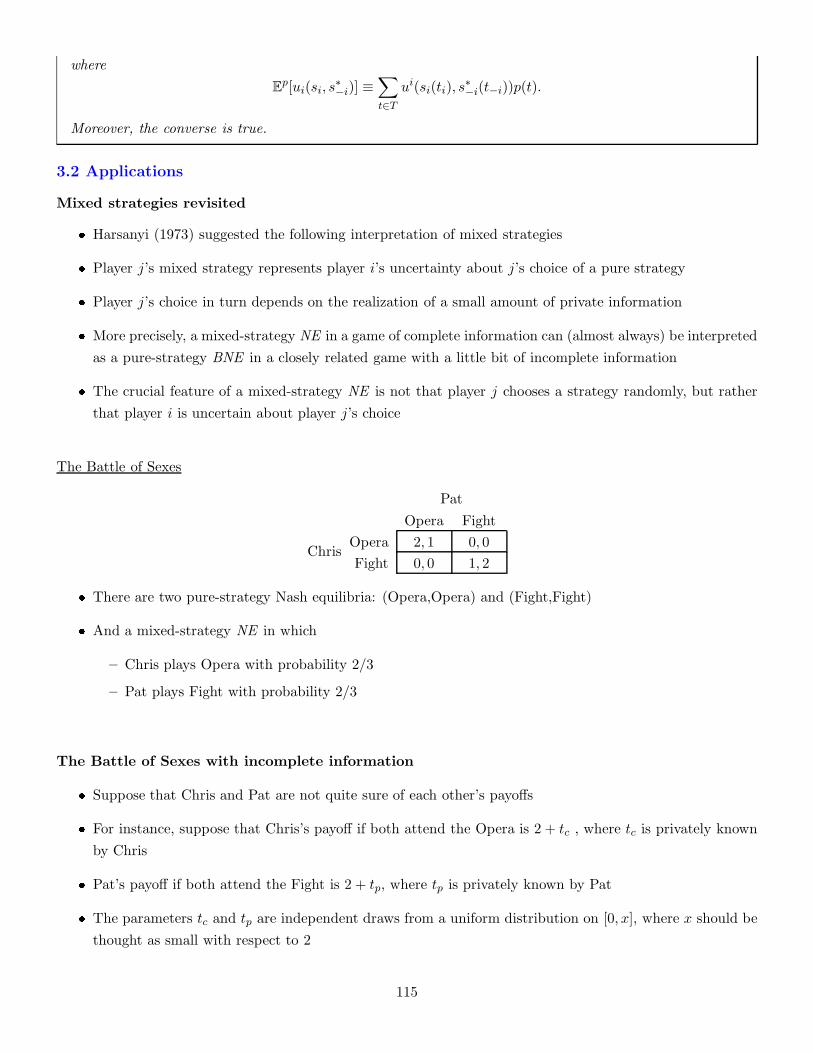

The battle of sexes

A man (Pat) and a woman (Chris) are trying to decide on an evening’s entertainment

23

� while at workplaces, Pat and Chris must choose to attend either the opera or a rock concert

� both players would rather spend the evening together than apart

Chris

Pat

Opera Rock

Opera 2,1 0,0

Rock 0,0 1,2

� there are two NE : (Opera,Opera) and (Rock,Rock)

In some games with multiple NE, one equilibrium stands out as the compelling solution

� in particular a convention can be developed

Theory’s effort:

identify such a compelling equilibrium in different classes of games

In the example above,

� the NE concept loses much of its appeal as a prediction of play

– both equilibria seem equally compelling

– none can be developed as a convention

1.2 Applications

Cournot model of duopoly

A model of duopoly: Cournot (1838)

� two firms 1 and 2 producing the same good (homogeneous product)

� q1 and q2: quantities produced by the firms, respectively

� Q = q1 + q2: aggregate quantity on the market

� P (Q) = [a−Q]+: market-clearing price under Q

� C(qi) = cqi: total cost to firm i of producing quantity qi

– there is no fixed cost

– the marginal cost is constant at c

– we assume c < a

� firms choose their quantities simultaneously

We should translate the problem into a normal form game

� There are two players, the two firm: I = {1, 2}

24

� The strategies available to each firm are the different quantities Qi = [0,∞)

� An element of Qi is denoted qi

– One could reduce the set Qi to [0, a] since P (Q) = 0 for Q ≥ a

� The payoff of firm i for a profile (qi, qj) is its profit defined by

πi(qi, qj) = qi[P (qi + qj)− c] = qi([a− (qi + qj)]

+ − c)

The game is then G = (Qi, πi)i∈I

Nash equilibrium (NE)

A strategy to find a NE is to look for necessary condition (and then to check that it is sufficient)

� if (q∗1 , q∗2) is a Nash equilibrium, then

∀i ∈ I, q∗i ∈ argmax{πi(qi; q∗j ) : qi ≥ 0}

� we have

πi(qi; q∗j ) =

{

qi[(a− c− q∗j )− qi] if qi < a− q∗j−qic if qi ≥ a− q∗j

� all strategies qi ≥ a− q∗j are SD by qi = 0. Therefore,

q∗i ∈ argmax{πi(qi; q∗j ) : 0 ≤ qi < a− q∗j}

and the first order condition is necessary and sufficient

� objective function’s derivative is∂πi∂qi

(qi, q∗j ) = a− c− q∗j − 2qi

� assuming that q∗i ∈ (0, a− c) for each firm i, we have

q∗i =1

2(a− q∗j − c)

which yields

q∗i =a− c

3, ∀i ∈ I

obs.: this is consistent with the assumption q∗i ∈ (0, a − c)

Observacao 9. There is a unique Nash equilibrium, called Cournot equilibrium

Interpretation

Each firm would like to be a monopolist in this market

25

� it would choose qi to maximize πi(qi, 0). The solution is

qm =a− c

2

and the associated profit is

πi(qm; 0) =(a− c)2

4

With the two firms

� aggregate profits would be maximized by setting

q1 + q2 = qm

this would occur with qi = qm/2

Problem with the strategy profile (qm/2, qm/2):

� the market price P (qm) is too high

– at this price, each firm has an incentive to deviate by increasing the production

– in spite of the fact that such a deviation drives down the market price, the profit obtained still

increases

In the Cournot equilibrium,

� the aggregate quantity is higher

� so the associated price is lower

the temptation to increase output is reduced,

� just enough that each firm i is just deterred from increasing qi

Graphical solution

� if q1 < a− c, then firm 2’s best response is

R2(q1) =1

2(a− q1 − c)

Likewise,

� if q2 < a− c then firm 1’s best response is

R1(q2) =1

2(a− q2 − c)

26

� The two best response functions intersect only once,

at the equilibrium profile (q∗1 , q∗2)

Cournot duopoly and iterated elimination

A third proof: iterated elimination of strictly dominated strategies

� if there is a unique solution then it is a Nash equilibrium

Proposicao 3. The monopoly quantity qm = a−c2 strictly dominates any higher quantity.

We can then consider the game G(3) = (Q(3)i , πi)i∈I with

Q(3)i = [0, qm]

Proof. Step 1: Assume qm + qj < a. Then

πi(qm; qj) = qm

[a− c

2− qj

]

while

πi(qm + x, qj) = [qm + x]

[a− c

2− x− qj

]

= πi(qm, qj)− x(x+ qj)

Step 2: Assume qm + qj > a. Then,

πi(qm + x; qj) = −c[qm + x]

27

Proposicao 4. Given that quantities exceeding qm = (a − c)/2 have been eliminated, the quantity qm/2

strictly dominates any lower quantity.

Formally,

� for any x ∈ (0, qm/2] we have

πi[qm/2, qj ] > πi[qm/2 − x, qj ]; ∀qj ∈ [0, (a − c)/2]

Proof.

πi(qm/2, qj) = qm/2

[3

4(a− c)− qj

]

and

πi(qm/2− x, qj) = [qm/2− x]

[3

4(a− c) + x− qj

]

= πi(qm/2, qj)− x

[a− c

2+ x− qj

]

After these two steps, the quantities remaining in each firm’s strategy space are those in the interval

[a− c

4,a− c

2

]

� repeating these arguments leads to ever smaller intervals of remaining quantities

� in the limit (we need countably many steps), these intervals converge to the single point q∗i = a−c3

Cournot duopoly and iterated elimination

If we add one or more firms in Cournot’s model

� then the first step of elimination continues to hold

� but that’s it

Observacao 10. IESDS yields only the imprecise prediction that each firm’s quantity will not exceed the

monopoly quantity

Example: Three firms

28

� Q−i: sum of the quantities chosen by the firms other than i

πi(qi;Q−i) =

{

qi(a− qi −Q−i − c) if qi +Q−i < a

−cqi if qi +Q−i > a

� it is again true that qm strictly dominates any higher quantity

∀x > 0; πi(qm;Q−i) > πi(qm + x;Q−i); ∀Q−i > 0

Each firm reduces its strategy set to [0, qm], but

� no further strategies can be eliminated

Proposicao 5. No quantity qi ∈ [0, qm] is strictly dominated

Proof. For each qi ∈ [0, qm] there is a Q−i such that

qi ∈ argmax{πi(q′i, Q−i) : q′i ∈ [0, qm]}

In effect, we know that Q−i ∈ [0, 2qm] = [0, a− c]. Fix qi ∈ [0, qm] and recall that

πi(qi;Q−i) =

{

qi(a− qi −Q−i − c) if qi +Q−i < a

−cqi if qi +Q−i > a.

Then, the FOC is satisfied for qi and Q−i = a− c− 2qi.

Bertrand model of duopoly

We consider a different model of how two duopolists might interact

� Bertrand (1883) suggested that firms actually choose prices, rather than quantities as in Cournot’s model

We consider the case of differentiated products

� firms 1 and 2 choose prices p1 and p2, respectively

� the quantity that consumers demand from firm i’s product is

qi(pi, pj) = [a− pi + bpj]+ 0 < b < 2

� b reflects the extent to which

firm i’s product is a substitute for firm j’s product

29

Observacao 11. This is an unrealistic demand function

� demand for firm i’s product is positive

� even when firm i charges an arbitrarily high price,

provided firm j also charges a high enough price.

� there are no fixed costs of production

� marginal cost of production is constant at a value c ∈ (0, a)

The normal form game:

� the set of players is I = {1, 2}

� the strategy set Pi of player i is Pi = [0,∞)

� the payoff function corresponds to profits:

πi(pi, pj) = qi(pi, pj)[pi − c] = [a− pi + bpj ]+(pi − c)

The game is G = (Pi, πi)i∈I

Nash equilibrium:

the price pair (p∗1, p∗2) is a Nash equilibrium if,

� for each firm i the price p∗i solves

max0≤pi<∞

πi(pi, p∗j) = max

c<pi<a+bp∗j

[a− pi + bp∗j ][pi − c]

� objective function’s derivative is∂πi∂pi

(pi, p∗j) = a+ c+ bp∗j − 2pi

and, therefore, the solution to firm i’s optimization problem is

p∗i =1

2(a+ bp∗j + c)

If (p∗1, p∗2) is a Nash equilibrium, one must have

p∗1 =1

2(a+ bp∗2 + c) and p∗2 =

1

2(a+ bp∗1 + c)

30

� if b < 2 then the unique Nash equilibrium is

p∗1 = p∗2 =a+ c

2− b

Final-offer arbritation

Consider a firm and a union which dispute wages

(i) the firm and the union simultaneously make offers

� the firm offers the wage wf

� the union offers the wage wu

(ii) an arbitrator chooses one of the two offers as the settlement

� x: ideal settlement arbitrator would like to impose

The decision rule is as follows:

� after observing the parties’ offers, wf and wu,

the arbitrator simply chooses the offer that is closer to x

Provided that wf < wu

� the arbitrator chooses wf if x < (wf + wu)/2

� the arbitrator chooses wu if x > (wf + wu)/2

� the arbitrator flips a coin if x = (wf + wu)/2

The arbitrator knows x but the parties do not

� the parties believe that x is randomly distributed according to a probability measure µ on the Borelian

sets of [0, 1)

� the cumulative probability distribution is denoted by F

F (x) ≡ Pr{x ≤ x} = µ[0, x]

31

� F : [0, 1) → [0, 1] is differentiable, with derivative f

� f represents the density function, i.e.,

∫

[0,∞)h(x)µ(dx) =

∫

[0,∞)h(x)f(x)dx

for every Borel measurable function h : [0,∞) → R+

Given the offers wf and wu, the parties believe that

� wf is chosen under probability

Pr{wf chosen} = µ

[

0,wf + wu

2

)

= F

(wf + wu

2

)

� wu is chosen under probability

Pr{wu chosen} = µ

[wf + wu

2,∞

)

= 1− F

(wf + wu

2

)

and, therefore, expected wage settlement is given by

E(w) = wf × Pr{wf chosen}+ wu × Pr{wu chosen}

= wfF

(wf +wu

2

)

+ wu

[

1− F

(wf + wu

2

)]

We assume that

� the firm wants to minimize E(w)

� the union wants to maximize E(w)

If (w∗f , w

∗u) is a Nash equilibrium, then

� w∗f must solve

min0≤wf<∞

{

wfF

(wf + w∗

u

2

)

+ w∗u

[

1− F

(wf + w∗

u

2

)]}

� w∗u must solve

max0≤wu<∞

{

w∗fF

(w∗f + wu

2

)

+ wu

[

1− F

(w∗f + wu

2

)]}

Suppose that (w∗f , w

∗u) is strictly positive

� FOC for the firm’s problem

(w∗u − w∗

f )×1

2f

(w∗u + w∗

f

2

)

= F

(w∗u + w∗

f

2

)

32

� FOC for the union’s problem

(w∗u − w∗

f )×1

2f

(w∗u +w∗

f

2

)

= 1− F

(w∗u + w∗

f

2

)

Therefore,

F

(w∗u + w∗

f

2

)

=1

2

The average of the offers must equal

� the median of the arbitrator’s preferred settlement

F

(w∗u + w∗

f

2

)

=1

2

The gap between the offers must equal

� the inverse of the value of the density function

� at the median of the arbitrator’s preferred settlement

w∗u − w∗

f =1

f(w∗

u+w∗

f

2

)

An example:

Suppose the arbitrator’s preferred settlement is normally distributed with mean m and variance σ2, i.e.,

f(x) =1√2πσ2

exp

{

− 1

2σ(x−m)2

}

� the median of the distribution equals the mean m

– the normal distribution is symmetric around its mean,

The necessary conditions are then translated into

w∗u + w∗

f

2= m and w∗

u − w∗f =

1

f(m)=

√2πσ2

The Nash equilibrium offers are

w∗u = m+

√

πσ2

2and w∗

f = m−√

πσ2

2

In equilibrium,

33

� the parties’ offers are centered around m

– m: expectation of the arbitrator’s preferred settlement

� the gap between the offers increases with σ2

– σ2: parties’ uncertainty about the arbitrator’s preferred settlement

A more aggressive offer

� lower offer by the firm

� higher offer by the union

yields a better payoff if it is chosen by the arbitrator

� but is less likely to be chosen

When there is more uncertainty (i.e., σ2 higher)

� the parties can afford to be more aggressive

When there is hardly any uncertainty, in contrast,

� neither party can afford to make an offer far from the mean

The problem of the Commons

� consider the n farmers in a village: I = {1, · · · , n}

� each summer, all the farmers graze their goats on the village green

� during the spring, the farmers simultaneously choose how many goats to own

Let

� gi: number of goats owned by farmer i

� G = g1 + · · ·+ gn: total number of goats in the village

� c > 0: the cost of buying and caring for a goat

� v(G): the value (per goats) to a farmer of grazing a goat on the green

� goats are continuously divisible

34

� v : [0, Gmax] → R+ is

– twice continuously differentiable

– v′ < 0 and v′′ < 0

The normal-form representation:

� a strategy for farmer i is gi

� the strategy space is Gi = [0,∞) (we could have chosen Gi = [0, Gmax])

� the payoff to farmer i

– from grazing gi goats

– when the numbers of goats of the other farmers are g−i

is

πi(gi, g−i) = giv(gi + σ[g−i])− cgi

where σ[g−i] =∑

k 6=i gk

If (g∗i )i∈I is a Nash equilibrium

� then g∗i is a solution to

maxgi≥0

{giv(gi + σ[g∗−i])− cgi

}

� if g∗i > 0, then the FOC is

v(g∗i + σ[g∗−i]) + g∗i v′(g∗i + σ[g−i])− c = 0

Summing over all farmers and dividing by n, we get

v(G∗) +1

nG∗v′(G∗)− c = 0

where G∗ denotes∑

i∈I g∗i

Social optimum

A social planner decides how many goats the “society” should graze on the village green

35

� the planner should solve

maxG≥0

{Gv(G) −Gc}

independent on the way the social profit should be divided

� the FOC is

v(Gs) +Gsv′(Gs)− c = 0

Lema 1. One must have G∗ > Gs.

Observacao 12. Too many goats are grazed in the Nash equilibrium, compared to the social equilibrium

� The common resource is overutilized

When a farmer considers the effect of adding one more goat, he focuses on

� the cost of production: c

� the additional benefit: v(gi + σ[g−i∗])

� the harm to his other goats: giv′(gi + σ[g−i∗])

He does not care about the effect of his action on the other farmers

� this is the reason we have G∗v′(G∗)/n and not GSv′(GS)

1.3 Mixed strategies and existence of equilibrium

Non-existence: Matching pennies

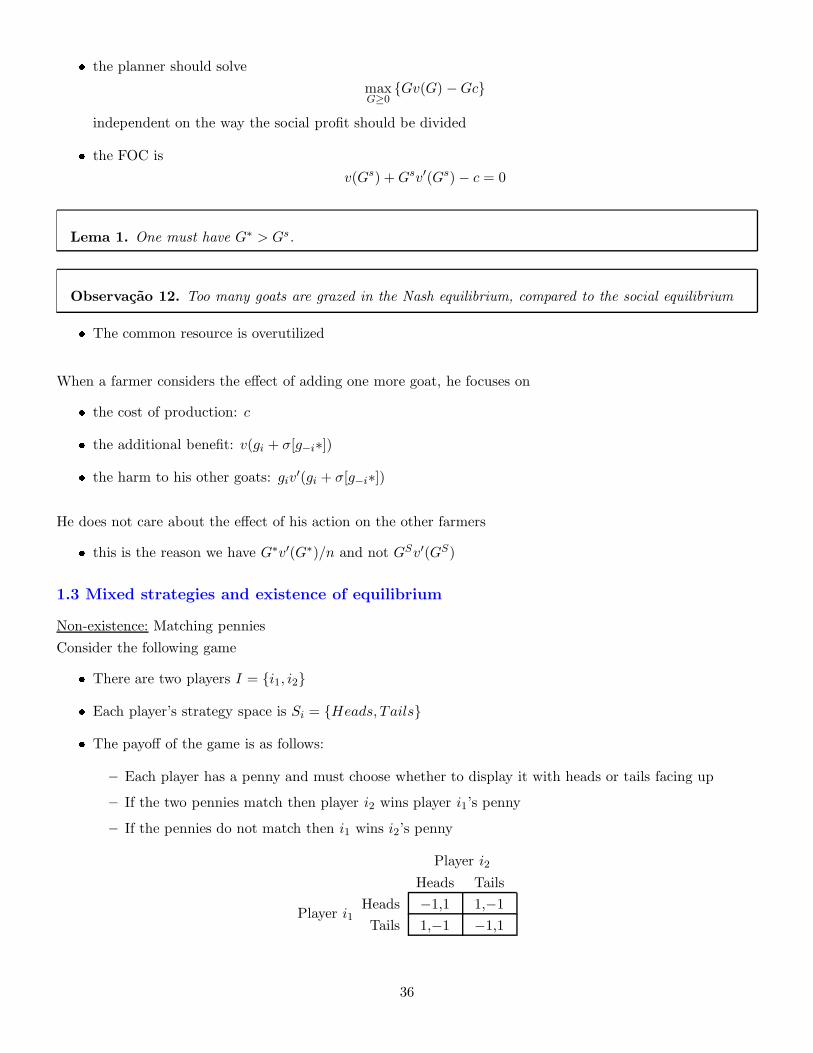

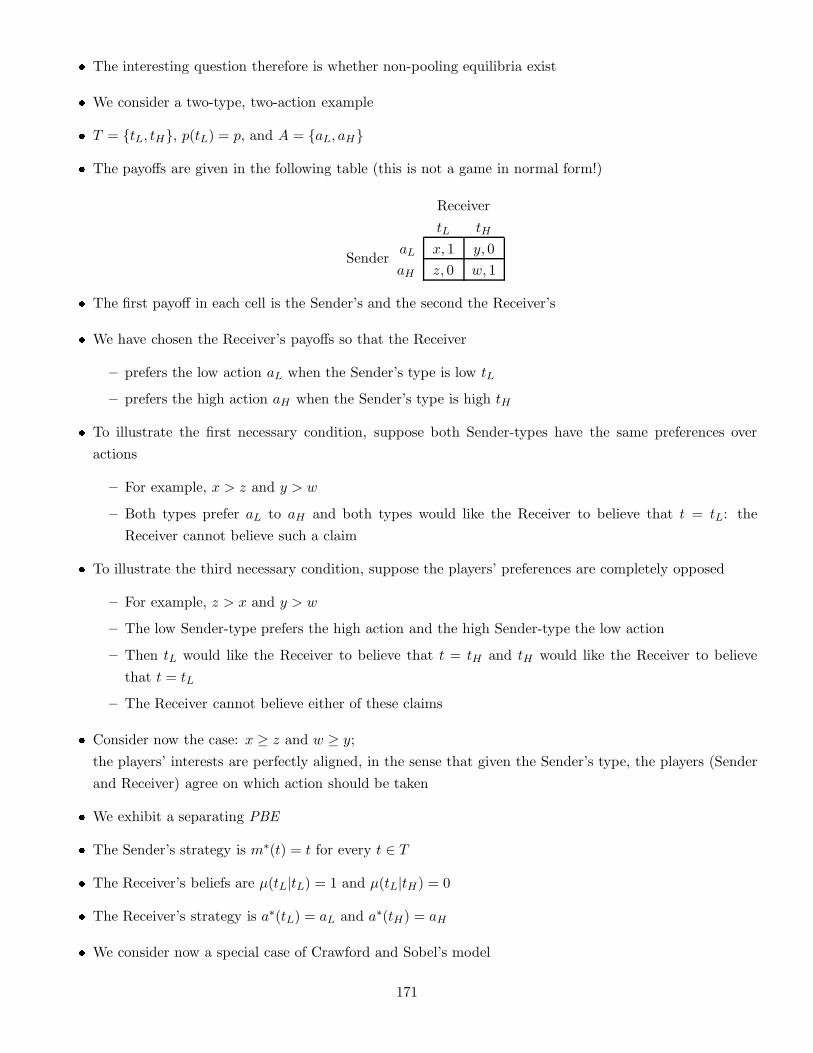

Consider the following game

� There are two players I = {i1, i2}

� Each player’s strategy space is Si = {Heads, Tails}

� The payoff of the game is as follows:

– Each player has a penny and must choose whether to display it with heads or tails facing up

– If the two pennies match then player i2 wins player i1’s penny

– If the pennies do not match then i1 wins i2’s penny

Player i1

Player i2

Heads Tails

Heads −1,1 1,−1

Tails 1,−1 −1,1

36

Proposicao 6. There is no Nash equilibrium.

Player i1

Player i2

Heads Tails

Heads −1,1 1,−1

Tails 1,−1 −1,1

If the players’ strategies

� match then player i1 prefers to switch strategies

� do not match then i2 prefers to switch

This situation occurs in many games

� Poker, battle

To overcome this difficulty, we introduce the notion of a mixed strategy

Mixed strategies

A mixed strategy is a probability measure (distribution) over the strategies in Si

� A strategy in Si is called a pure strategy

� The set of mixed strategies is denoted by Prob(Si) or ∆Si

Definicao 11. A mixed strategy p = (p(si))si∈Siof player i is a vector in R

Si satisfying

∀si ∈ Si, psi = p(si) ≥ 0 and∑

si∈Si

p(si) = 1

� if the mixed strategy p is such that there exists si ∈ Si satisfying

∀si ∈ Si, p(si) =

{

0 if si 6= si

1 ifsi = si

then p is denoted Dirac(si) or 1si and (abusing notations) is assimilated with the pure strategy si

Interpretation

A family p−i = (pj)j 6=i of mixed strategies pj ∈ ∆(Sj) can represent

� agent i’s uncertainty about

� which strategy each other agent j will play

37

Notation 5. The expected value of agent i’s payoff if he plays si believing that the other players will play

according to p−i is denoted by

ui(si, p−i)

and is defined by

ui(si, p−i) ≡ Ep−i [ui(si)] =

∑

s−i∈S−i

∏

j 6=i

pj(sj)

︸ ︷︷ ︸

p−i(s−i)

ui(si, s−i)

Notation 6. If pi is a mixed strategy in ∆(Si) we let p = (pj)j∈I and the expected value

Ep[ui] =

∑

s∈S

∏

j∈J

pj(sj)

ui(si1 , . . . , sin)

=∑

s∈S

pi1(si1) . . . pin(sin)ui(si1 , . . . , sin)

is denoted by

ui(p)

Observe that

ui(p) =∑

si∈Si

pi(si)ui(si, p−i)

Definicao 12. We say that

� there is no belief that player i could hold about the strategies the other players will choose

� such that it would be optimal to play si

when

∀p−i ∈∏

j 6=i

∆(Sj), si /∈ argmax{Ep−i [ui(si)] : si ∈ Si}

In other words,

� for every belief p−i that agent i could hold about the others,

� there exists a pure strategy si ∈ Si such that

Ep−i [ui(si)] < E

p−i [ui(si)]

� be careful, the strategy si may depend on the belief p−i.

38

Proposicao 7. Assume that the pure strategy si is strictly dominated by the pure strategy σi

∀s−i ∈ S−i, ui(si, s−i) < ui(σi, s−i)

Then

� there is no belief that player i could hold about the strategies the other players will choose such that

it would be optimal to play si.

More precisely, for every family p−i = (pj)j 6=i of mixed strategies pj ∈ ∆(Sj), we have

Ep−i [ui(si)] < E

p−i [ui(σi)]

In this case, the strategy σi improves the expected payoff independently of the belief p−i agent i holds about

the other players’ actions

Observacao 13. The converse may not be true

Consider the following game

Player i1

Player i2

L R

T 3,− 0,−M 0,− 3,−B 1,− 1,−

For any belief pi2 agent i1 may have about i2’s strategies, the strategy B is never a best response

� if pi2(L) > 1/2 then i1’s best response is T

� if pi2(L) < 1/2 then i1’s best response is M

� if pi2(L) = 1/2 then i1’s best response is either T or M

However, the strategy B is not strictly dominated by another pure strategy

Consider the mixed strategy pi1 defined by

pi1(T ) = 1/2, pi1(M) = 1/2 and pi1(B) = 0

Such a probability will be denoted by1

pi1 = (1/2, 1/2, 0)

For any belief pi2 agent i1 may have about i2’s strategies,

ui1(B, pi2) = ui1(1B , pi2) = 1 < 3/2 = ui1(pi1 , pi2)

1Sometimes one my find the notations: pi1 = 1

2Dirac(T ) + 1

2Dirac(M) or pi1 = 1

21T + 1

21M .

39

Observacao 14. The strategy B is strictly dominated by the mixed strategy pi1 = (1/2, 1/2, 0)

Observacao 15. A given pure strategy can be a best response to a mixed strategy

� even if the pure strategy is not a best response to any other pure strategy

Player i1

Player i2

L R

T 3,− 0,−M 0,− 3,−B 2,− 2,−

� The pure strategy B is not a best response for player i1 to either L or R by player i2

� but B is the best response for player i1 to the mixed strategy pi2 by player i2 provided that

1

3< pi2(L) <

2

3

Existence of Nash equilibrium

Nash equilibrium with mixed strategies

We fix a game G = (Si, ui)i∈I

Definicao 13. A profile of mixed strategies p∗ = (p∗i )i∈I is a Nash equilibrium of the game G if

� each player’s mixed strategy is a best response to the other players’ mixed strategies,

∀i ∈ I, p∗i ∈ argmax{ui(pi, p

∗−i) : pi ∈ ∆(Si)

}.

The family p−i = (pj)j 6=i represents player i’s uncertainty about which strategy each player j will choose

Observacao 16. Fix three players i, j and k.

What player j believes about the possible strategies played by player i coincides with what player k believes

Consider an abstract game G = (Si, ui)i∈I

� fix a family pi−i = (pij)j 6=i of mixed strategies representing player i’s beliefs about player j’s strategies

� denote by S∗i (p

i−i) the set of pure strategies best response of player i defined by

S∗i (p

i−i) ≡ argmax{ui(si, pi−i) : si ∈ Si}

– assume that Si is finite, then S∗i (p

i−i) is non-empty

40

� if pi is a mixed strategy in ∆(Si), we denote by supp pi its support defined by

supp pi = {pi > 0} = {si ∈ Si : pi(si) > 0}

Proposicao 8. A mixed strategy p∗i is a best response to pi−i, i.e.,

p∗i ∈ argmax{ui(pi, pi−i) : pi ∈ ∆(Si)}

if and only if the support of p∗i is a subset of all pure strategies that are best response to pi−i, i.e.,

{si ∈ Si : p∗i (si) > 0} ≡ supp p∗i ⊂ S∗

i (pi−i)

In other words the set

argmax{ui(pi, pi−i) : pi ∈ ∆(Si)}

of best responses to pi−i coincides with

Prob(S∗i (p

i−i)) = ∆(S∗

i (pi−i))

NE with mixed strategies: An equivalent definition

Teorema 7. A profile of mixed strategies p∗ = (p∗i )i∈I is a Nash equilibrium of the game G if and only if

� for every player i every pure strategy in the support of p∗i is a best response to the other players’ mixed

strategies

∀i ∈ I, supp p∗i ⊂ argmax{ui(si, p∗−i) : si ∈ Si}

Interpretation 8. Players

� have identical beliefs about other players’ possible actions or strategies

� choose best response strategies consistent with these beliefs

Matching pennies

Player i1

Player i2

Heads Tails

Heads −1,1 1,−1

Tails 1,−1 −1,1

� suppose that player i1 believes that player i2 will play

– Heads with probability q and

– Tails with probability 1− q

41

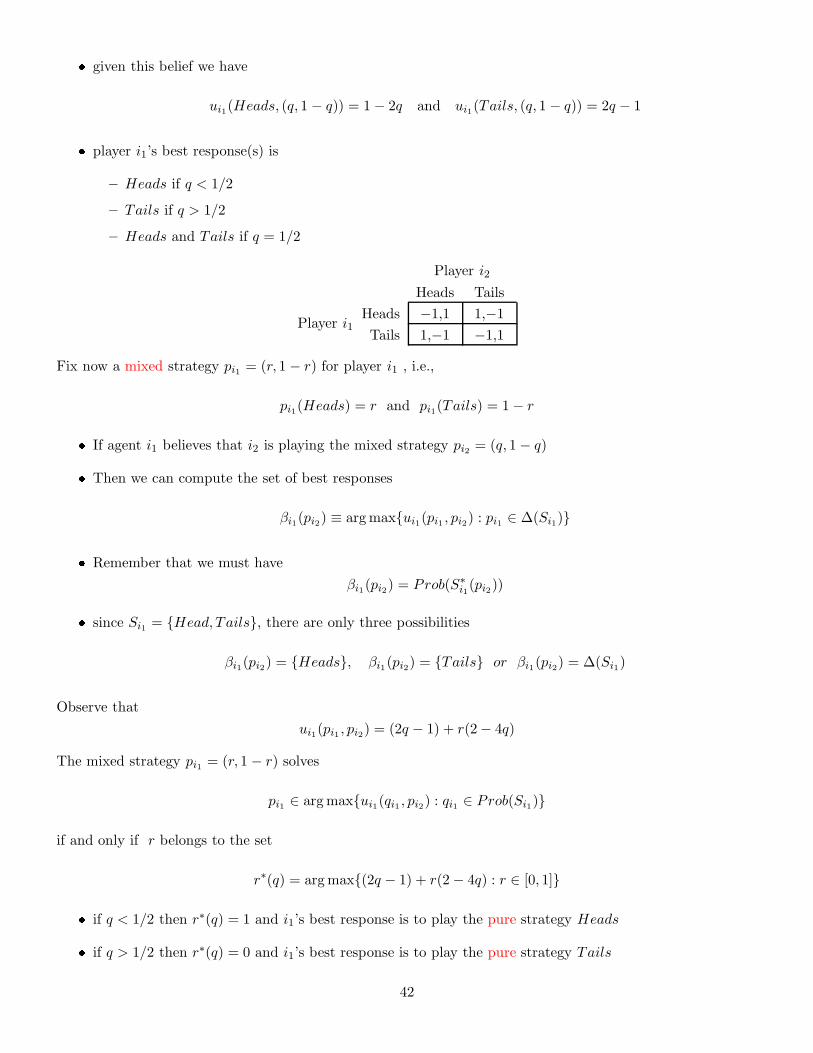

� given this belief we have

ui1(Heads, (q, 1 − q)) = 1− 2q and ui1(Tails, (q, 1 − q)) = 2q − 1

� player i1’s best response(s) is

– Heads if q < 1/2

– Tails if q > 1/2

– Heads and Tails if q = 1/2

Player i1

Player i2

Heads Tails

Heads −1,1 1,−1

Tails 1,−1 −1,1

Fix now a mixed strategy pi1 = (r, 1 − r) for player i1 , i.e.,

pi1(Heads) = r and pi1(Tails) = 1− r

� If agent i1 believes that i2 is playing the mixed strategy pi2 = (q, 1− q)

� Then we can compute the set of best responses

βi1(pi2) ≡ argmax{ui1(pi1 , pi2) : pi1 ∈ ∆(Si1)}

� Remember that we must have

βi1(pi2) = Prob(S∗i1(pi2))

� since Si1 = {Head, Tails}, there are only three possibilities

βi1(pi2) = {Heads}, βi1(pi2) = {Tails} or βi1(pi2) = ∆(Si1)

Observe that

ui1(pi1 , pi2) = (2q − 1) + r(2− 4q)

The mixed strategy pi1 = (r, 1 − r) solves

pi1 ∈ argmax{ui1(qi1 , pi2) : qi1 ∈ Prob(Si1)}

if and only if r belongs to the set

r∗(q) = argmax{(2q − 1) + r(2− 4q) : r ∈ [0, 1]}

� if q < 1/2 then r∗(q) = 1 and i1’s best response is to play the pure strategy Heads

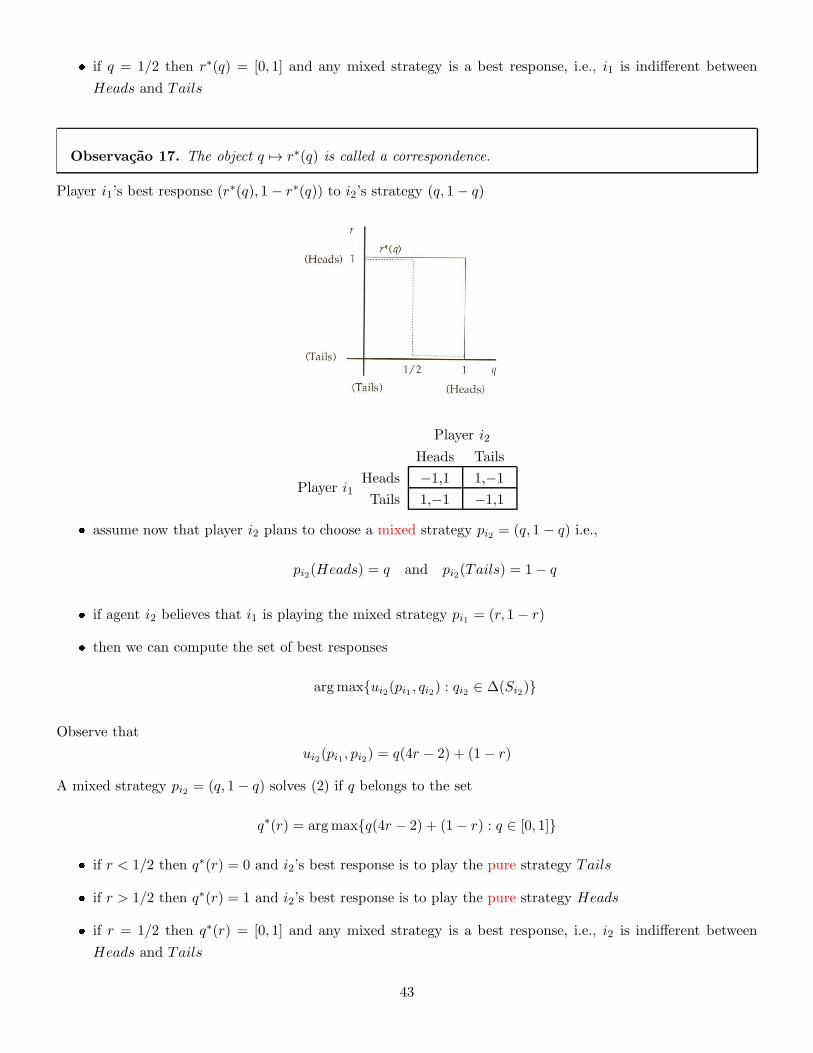

� if q > 1/2 then r∗(q) = 0 and i1’s best response is to play the pure strategy Tails

42

� if q = 1/2 then r∗(q) = [0, 1] and any mixed strategy is a best response, i.e., i1 is indifferent between

Heads and Tails

Observacao 17. The object q 7→ r∗(q) is called a correspondence.

Player i1’s best response (r∗(q), 1 − r∗(q)) to i2’s strategy (q, 1− q)

Player i1

Player i2

Heads Tails

Heads −1,1 1,−1

Tails 1,−1 −1,1

� assume now that player i2 plans to choose a mixed strategy pi2 = (q, 1 − q) i.e.,

pi2(Heads) = q and pi2(Tails) = 1− q

� if agent i2 believes that i1 is playing the mixed strategy pi1 = (r, 1 − r)

� then we can compute the set of best responses

argmax{ui2(pi1 , qi2) : qi2 ∈ ∆(Si2)}

Observe that

ui2(pi1 , pi2) = q(4r − 2) + (1− r)

A mixed strategy pi2 = (q, 1− q) solves (2) if q belongs to the set

q∗(r) = argmax{q(4r − 2) + (1− r) : q ∈ [0, 1]}

� if r < 1/2 then q∗(r) = 0 and i2’s best response is to play the pure strategy Tails

� if r > 1/2 then q∗(r) = 1 and i2’s best response is to play the pure strategy Heads

� if r = 1/2 then q∗(r) = [0, 1] and any mixed strategy is a best response, i.e., i2 is indifferent between

Heads and Tails

43

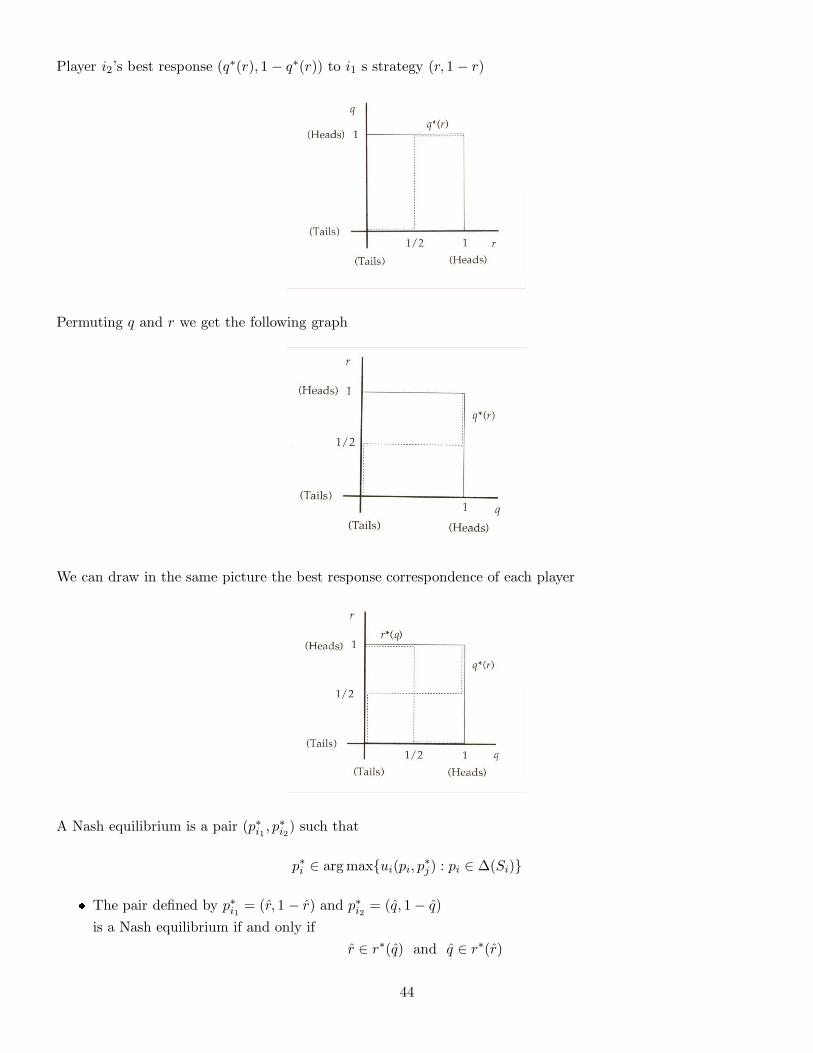

Player i2’s best response (q∗(r), 1 − q∗(r)) to i1 s strategy (r, 1 − r)

Permuting q and r we get the following graph

We can draw in the same picture the best response correspondence of each player

A Nash equilibrium is a pair (p∗i1 , p∗i2) such that

p∗i ∈ argmax{ui(pi, p∗j) : pi ∈ ∆(Si)}

� The pair defined by p∗i1 = (r, 1 − r) and p∗i2 = (q, 1− q)

is a Nash equilibrium if and only if

r ∈ r∗(q) and q ∈ r∗(r)

44

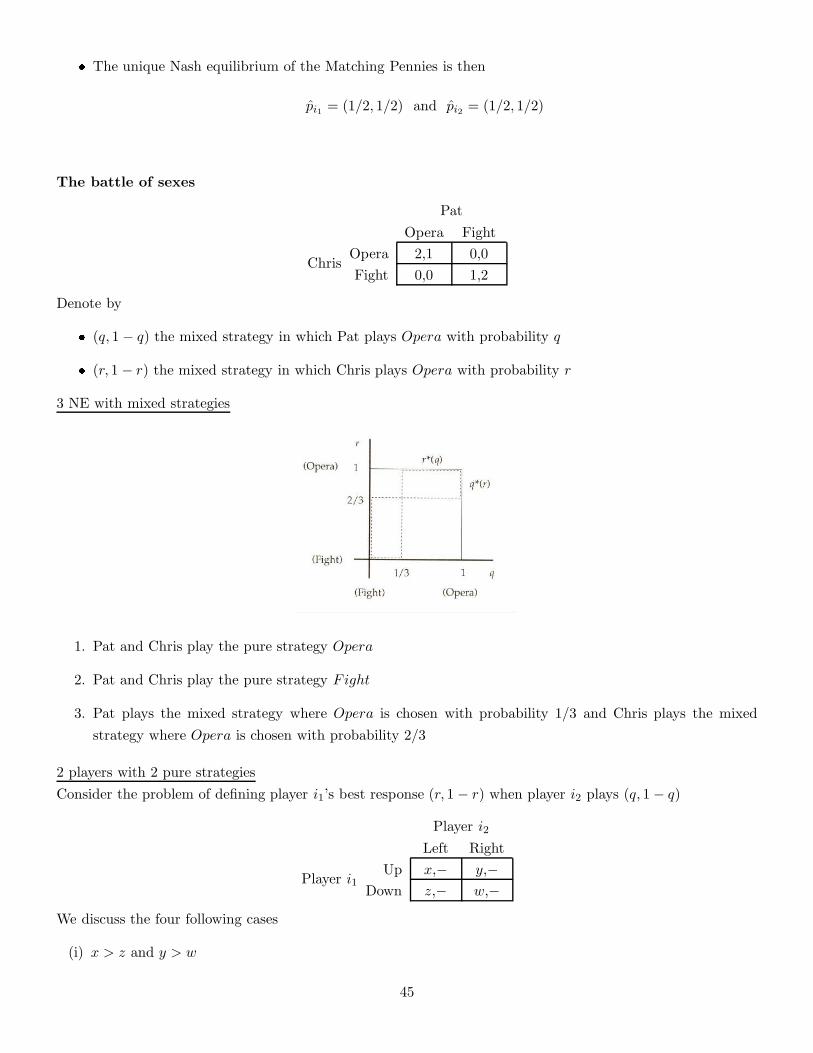

� The unique Nash equilibrium of the Matching Pennies is then

pi1 = (1/2, 1/2) and pi2 = (1/2, 1/2)

The battle of sexes

Chris

Pat

Opera Fight

Opera 2,1 0,0

Fight 0,0 1,2

Denote by

� (q, 1− q) the mixed strategy in which Pat plays Opera with probability q

� (r, 1 − r) the mixed strategy in which Chris plays Opera with probability r

3 NE with mixed strategies

1. Pat and Chris play the pure strategy Opera

2. Pat and Chris play the pure strategy Fight

3. Pat plays the mixed strategy where Opera is chosen with probability 1/3 and Chris plays the mixed

strategy where Opera is chosen with probability 2/3

2 players with 2 pure strategies

Consider the problem of defining player i1’s best response (r, 1 − r) when player i2 plays (q, 1− q)

Player i1

Player i2

Left Right

Up x,− y,−Down z,− w,−

We discuss the four following cases

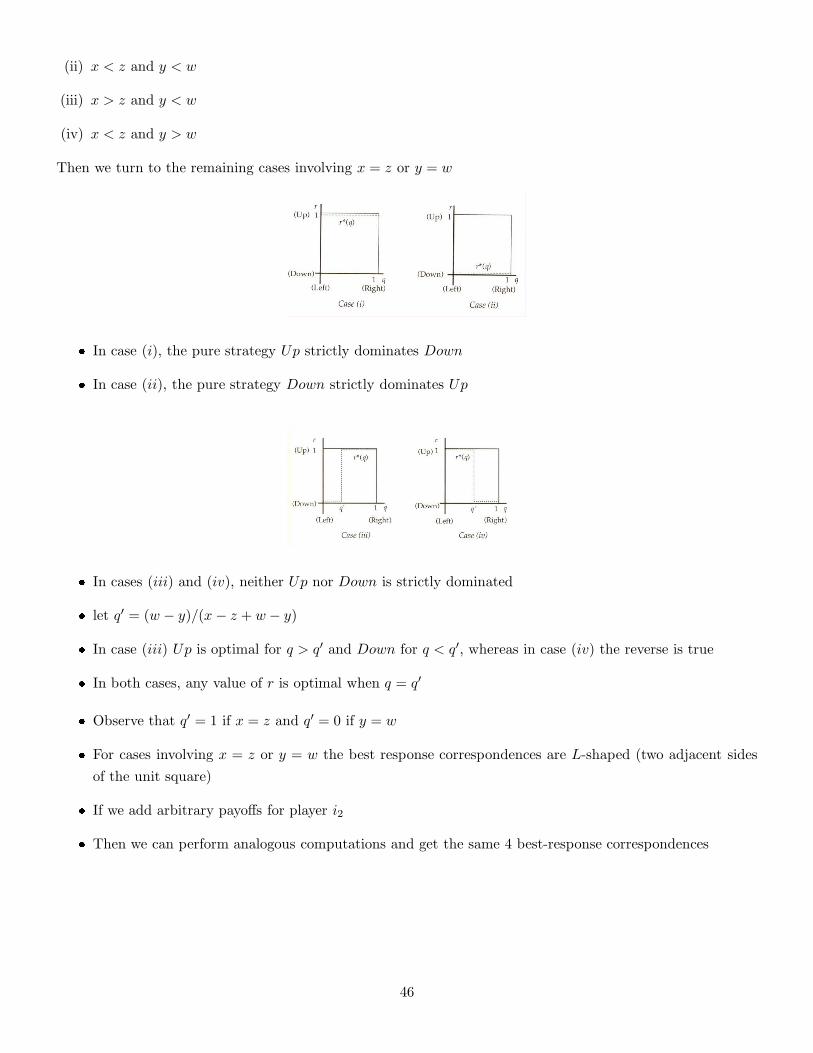

(i) x > z and y > w

45

(ii) x < z and y < w

(iii) x > z and y < w

(iv) x < z and y > w

Then we turn to the remaining cases involving x = z or y = w

� In case (i), the pure strategy Up strictly dominates Down

� In case (ii), the pure strategy Down strictly dominates Up

� In cases (iii) and (iv), neither Up nor Down is strictly dominated

� let q′ = (w − y)/(x− z + w − y)

� In case (iii) Up is optimal for q > q′ and Down for q < q′, whereas in case (iv) the reverse is true

� In both cases, any value of r is optimal when q = q′

� Observe that q′ = 1 if x = z and q′ = 0 if y = w

� For cases involving x = z or y = w the best response correspondences are L-shaped (two adjacent sides

of the unit square)

� If we add arbitrary payoffs for player i2

� Then we can perform analogous computations and get the same 4 best-response correspondences

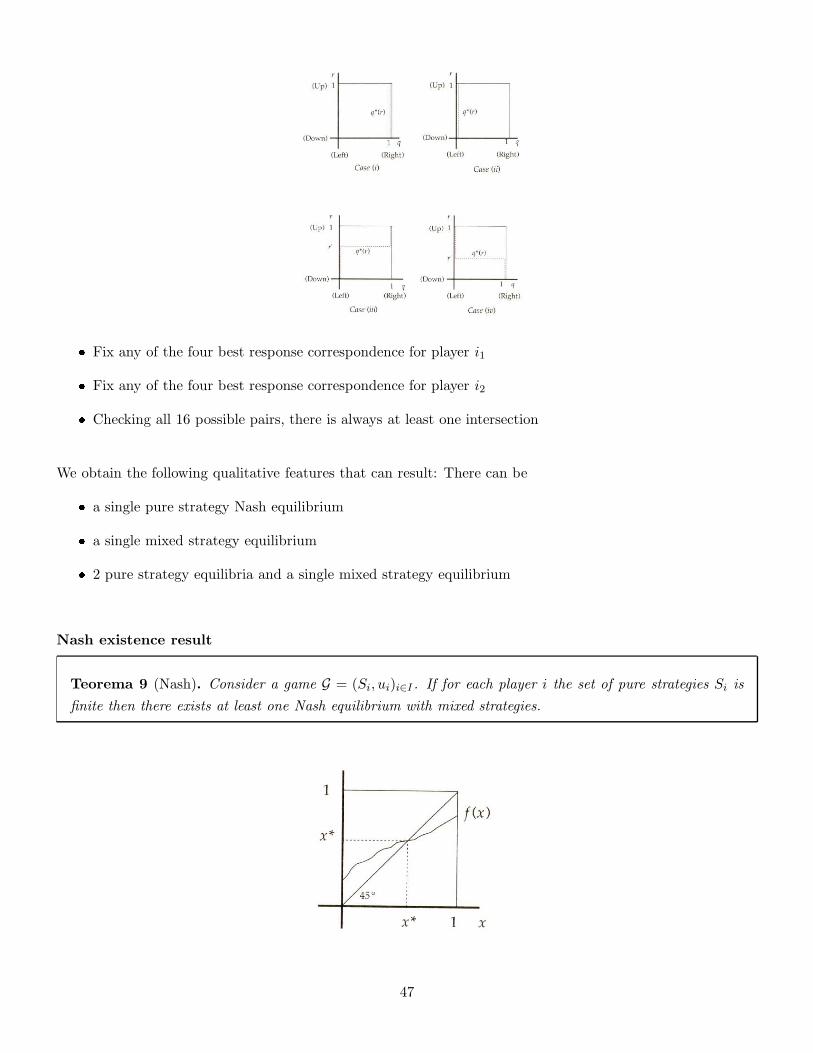

46

� Fix any of the four best response correspondence for player i1

� Fix any of the four best response correspondence for player i2

� Checking all 16 possible pairs, there is always at least one intersection

We obtain the following qualitative features that can result: There can be

� a single pure strategy Nash equilibrium

� a single mixed strategy equilibrium

� 2 pure strategy equilibria and a single mixed strategy equilibrium

Nash existence result

Teorema 9 (Nash). Consider a game G = (Si, ui)i∈I . If for each player i the set of pure strategies Si is

finite then there exists at least one Nash equilibrium with mixed strategies.

47

General existence result

Teorema 10. Consider a game G = (Si, ui)i∈I

and assume that for each player i,

(1) the set Si is a compact, convex and non-empty subset of Rni for some ni ∈ N

(2) the payoff function s → ui(s) is continuous on S =∏

i∈I Si

(3) for each s−i ∈ S−i, the function si → ui(si, s−i) is quasi-concave in the sense that

∀si ∈ Si, {s′i ∈ Si : ui(s′i, s−i) ≥ ui(si, s−i)} is convex

Then there exists at least one pure strategy Nash equilibrium

48

Cap. 2 - Dynamic games of complete information

2.1 Dynamic games of complete and perfect information

Theory: Backwards induction

Important words

� we introduce dynamic games

� restrict our attention to games with complete information

– the players’ payoff functions are common knowledge

� in this chapter we analyze dynamic games with complete but also perfect information

– at each move in the game

– the player with the move knows the full history of the play of the game thus far

� the central issue in dynamic games is credibility

An example:

Consider the following 2-move game

1. player i1 chooses between giving player i2 $1,000 and giving player i2 nothing

2. player i2 observes player i1’s move and then chooses whether or not to explode a grenade that will kill

both players

Suppose that player i2 threatens to explode the grenade unless player i1 pays the $1, 000

� if player i1 believes the threat, then

player i1’s best response is to pay the $1, 000

� but player i1 should not believe the threat, because it is not credible:

– if player i2 were given the opportunity to carry out the threat

– player i2 would choose not to carry it out

� player i1 should pay player i2 nothing

The framework

We analyze in this chapter the following class of dynamic games with complete and perfect information

� there are 2 players and 2 moves

� first, player i1 moves

49

� then player i2 observes player i1’s move

� then player i2 moves and the game ends

Description of a specific class of games

1. player i1 chooses an action ai1 from a feasible set Ai1

2. player i2 observes ai1 and then chooses an action ai2 from a feasible set Ai2

3. payoffs are ui1(ai1 , ai2) and ui2(ai1 , ai2)

Other dynamic games with complete and perfect information

The key features of a dynamic game of complete and perfect information are that

1. the moves occur in sequence

2. all previous moves are observed before the next move is chosen

3. the players’ payoffs from each feasible combination of moves are common knowledge

Backwards induction

We solve a game from this class by backwards induction as follows:

� when player i2 gets the move at the second stage of the game

� he will face the following problem

maxai2∈Ai2

{ui2(ai1 , ai2) : ai1 given}

� assume that for each ai1 ∈ Ai1 , player i2’s optimization problem has a unique solution, denoted by Ri2(ai1)

– this is player i2’s reaction (or best response) to player i1’s action

� recall that payoffs are common knowledge

– therefore player i1 can solve i2’s problem as well as i2 can

� player i1 will anticipate player i2’s reaction to each action ai1 that i1 might take

� thus player i1’s problem at the first stage amounts to

maxai1∈Ai1

{ui1(ai1 , Ri2(ai1))}

� assume that the previous optimization problem for i1 also has a unique solution, denoted by a∗i1

50

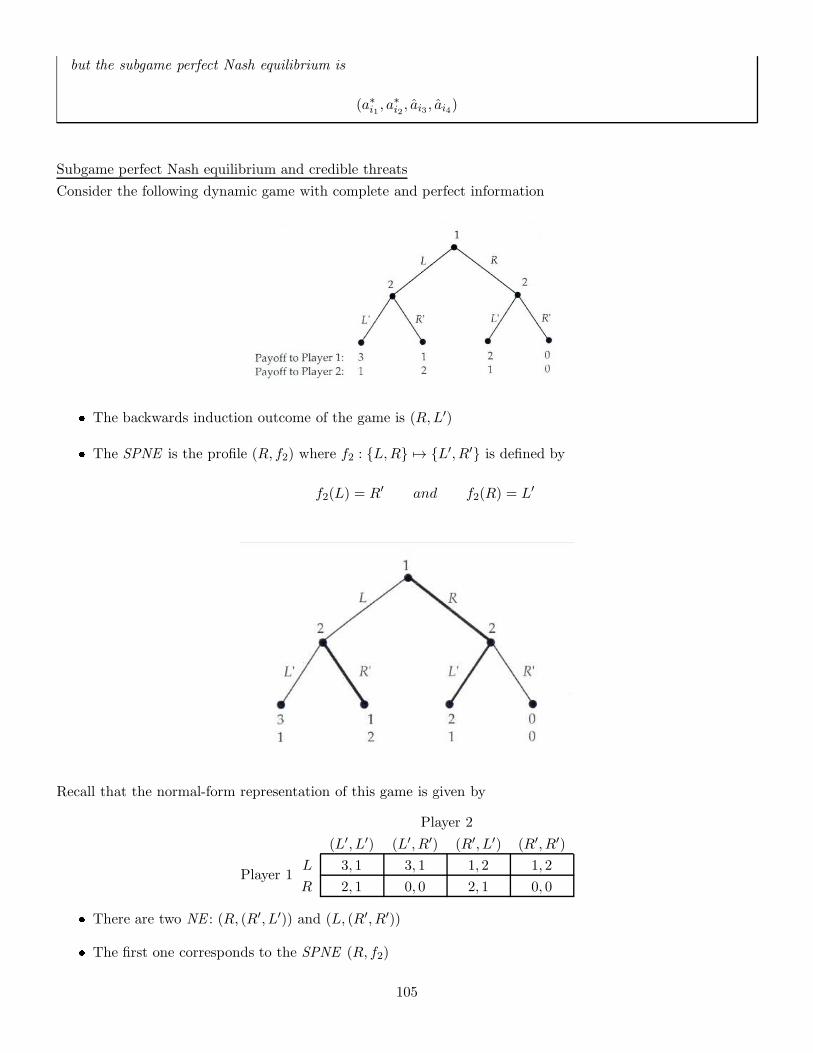

Definicao 14. The pair of actions (a∗i1 , Ri2(a∗i1)) is called the backwards induction outcome of this game

Backwards induction and credible threats

� the backwards induction outcome does not involve non-credible threats

� player i1 anticipates that player i2 will respond optimally to any action ai1 that i1 might choose, by

playing Ri2(ai1)

� player i1 gives no credence to threats by player i2 to respond in ways that will not be in i2’s self-interest

when the second stage arrives

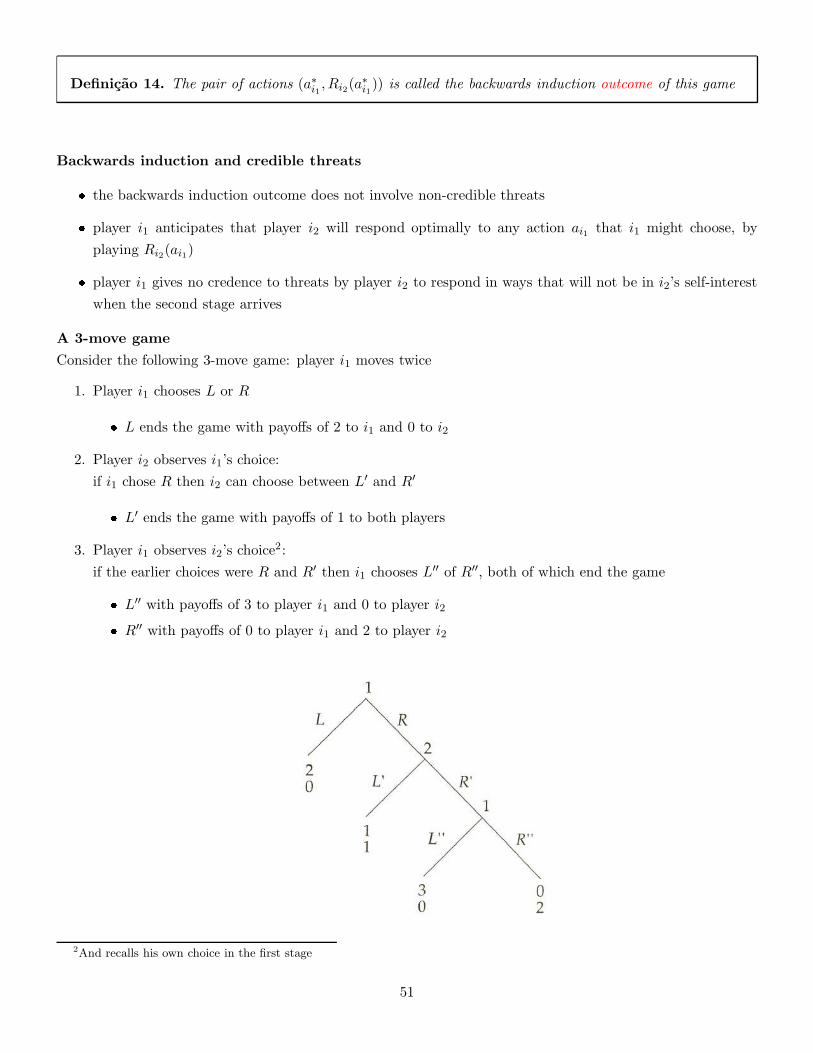

A 3-move game

Consider the following 3-move game: player i1 moves twice

1. Player i1 chooses L or R

� L ends the game with payoffs of 2 to i1 and 0 to i2

2. Player i2 observes i1’s choice:

if i1 chose R then i2 can choose between L′ and R′

� L′ ends the game with payoffs of 1 to both players

3. Player i1 observes i2’s choice2:

if the earlier choices were R and R′ then i1 chooses L′′ of R′′, both of which end the game

� L′′ with payoffs of 3 to player i1 and 0 to player i2

� R′′ with payoffs of 0 to player i1 and 2 to player i2

2And recalls his own choice in the first stage

51

Let’s compute the backwards induction outcome of this game

� we begin at the third stage, i.e., player i1’s second move

– the strategy L′′ is optimal

� at the second stage, player i2 anticipates that if the game reaches the third stage then i1 will play L′′

– payoff of 1 from action L′

– payoff of 0 from action R′

at the second stage, the optimal action for player i2 is L′

� at the first stage, player i1 anticipates that if the game reaches the second stage then i2 will play L′

– payoff of 2 from action L

– payoff of 1 from action R

the first stage choice for player i1 is L, thereby ending the game

Stackelberg model of duopoly

Von Stackelberg (1934) proposed a dynamic model of duopoly

� a dominant (leader) firm moves first

� a subordinate (follower) firm moves second

At some points in the history of the U.S. automobile history, for example, General Motors has seemed to play

such a leadership role

� as in the Cournot model, Stackelberg assumes that firms choose quantities

Timing of the game

1. firm i1 chooses the quantity qi1

2. firm i2 observes qi1 and then chooses a quantity qi2

3. the payoff to firm i is given by the profit function

πi(qi, qj) = qi[P (Q)− c]

where

52

� P (Q) = [a − Q]+ is the market-clearing price when the aggregate quantity on the market is Q =

qi1 + qi2

� c is the constant marginal cost of production (no fixed costs)

Solving by backwards induction

� we first compute i2’s reaction to an arbitrary quantity of i1

Ri2(qi1) ≡ argmax{πi2(qi1 , qi2) : qi2 ≥ 0}

which yields

Ri2(qi1) =

{a−c−qi1

2 if qi1 < a− c

0 if qi1 ≥ a− c

� second, i1 can solve i2’s problem as well as i2 can solve it

� firm i1 should anticipate that the quantity choice qi1 will be met with the reaction Ri2(qi1)

� Firm i1’s problem in the first stage of the game amounts to

argmax{πi1(qi1 , Ri2(qi1)) : qi1 ≥ 0}

� The backwards induction outcome of the Stackelberg duopoly game is (q∗i1 , q∗i2) where

q∗i1 =a− c

2and q∗i2 = Ri2(q

∗i1) =

a− c

4

Interpretation

� in the Nash equilibrium of the Cournot game (simultaneous moves) each firm produces (a− c)/3

– thus aggregate quantity in the backwards induction outcome of the Stackelberg game, 3(a− c)/4, is

greater than in the Cournot-Nash equilibrium

– so the market clearing price is lower in the Stackelberg game

� in the Stackelberg game, i1 could have chosen its Cournot quantity, (a− c)/3

– in which case i2 would have responded with its Cournot quantity

53

� in the Stackelberg game, i1 could have achieved its Cournot profit level but chose to do otherwise

� so i1’s profit in the Stackelberg game must exceed its profit in the Cournot game

� but because the market clearing price is lower in the Stackelberg game

� the aggregate profits are lower wrt. the Cournot outcome

� therefore, the fact that i1 is better off implies that i2 is worse off

Observacao 18. In game theory, having more information can make a player worse off.

� more precisely, having it known to the other players that one has more information can make a player

worse off

� in the Stackelberg game, the information in question is i1’s quantity

� firm i2 knows i1’s action qi1

� and firm i1 knows that i2 knows qi1

Wages and employment in a unionized firm

Leontief (1946) proposed the following model of the relationship between a firm and a monopoly union

� The union is the monopoly seller of labor to the firm

� The union has exclusive control over wages

� But the firm has exclusive control over employment

� The union’s utility function is U(w,L) where

– w is the wage the union demands from the firm

– L is employment

� We assume that (w,L) → U(w,L) is increasing in both w and L

� The firm’s profit function is

π(w,L) ≡ R(L)− wL

– R(L): revenue the firm can earn if it employs L workers

� We assume that L 7→ R(L) is

– twice continuously differentiable

54

– strictly increasing (i.e., R′ > 0)

– strictly concave (i.e., R′′ < 0) and

– satisfies Inada’s condition at 0 and ∞, i.e.,

limL→0+

R′(L) = ∞ and limL→∞

R(L) = 0

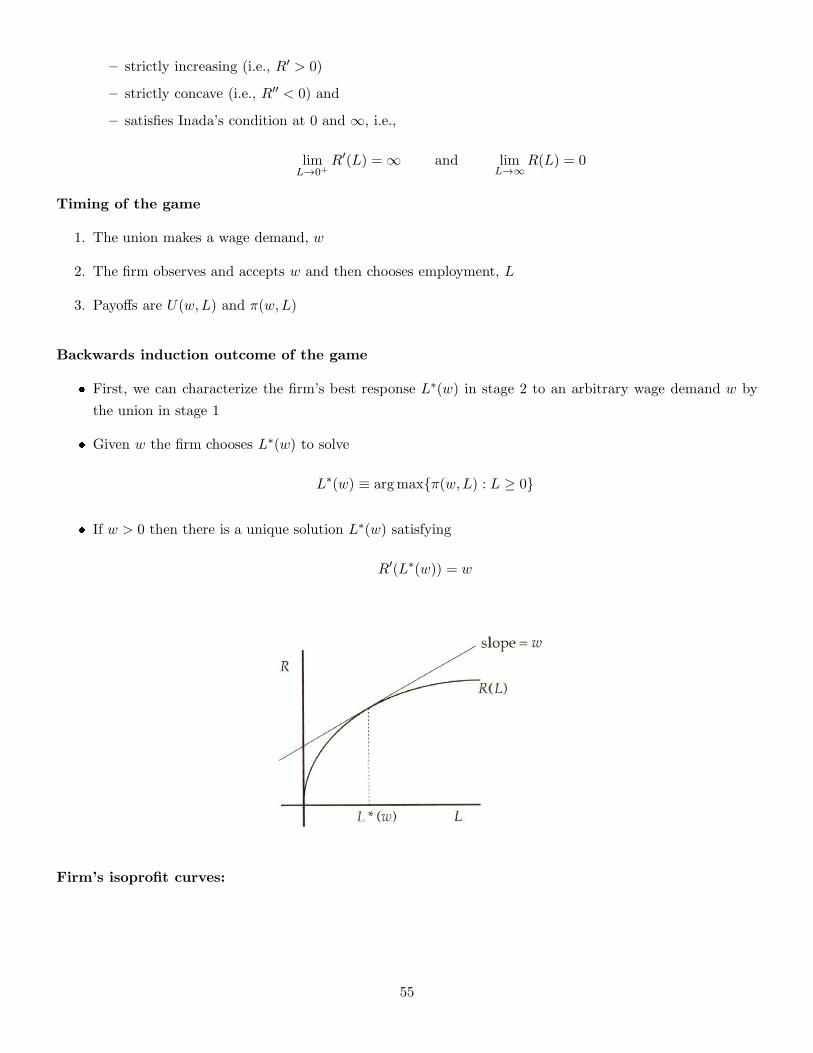

Timing of the game

1. The union makes a wage demand, w

2. The firm observes and accepts w and then chooses employment, L

3. Payoffs are U(w,L) and π(w,L)

Backwards induction outcome of the game

� First, we can characterize the firm’s best response L∗(w) in stage 2 to an arbitrary wage demand w by

the union in stage 1

� Given w the firm chooses L∗(w) to solve

L∗(w) ≡ argmax{π(w,L) : L ≥ 0}

� If w > 0 then there is a unique solution L∗(w) satisfying

R′(L∗(w)) = w

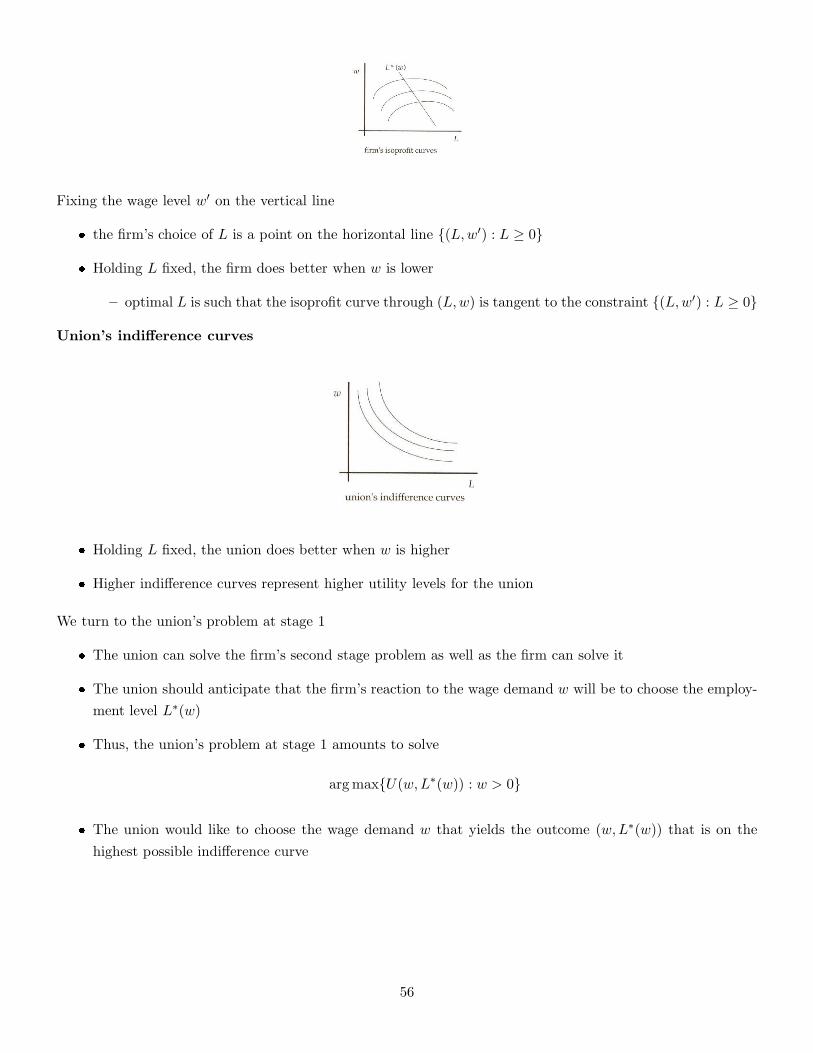

Firm’s isoprofit curves:

55

Fixing the wage level w′ on the vertical line

� the firm’s choice of L is a point on the horizontal line {(L,w′) : L ≥ 0}

� Holding L fixed, the firm does better when w is lower

– optimal L is such that the isoprofit curve through (L,w) is tangent to the constraint {(L,w′) : L ≥ 0}

Union’s indifference curves

� Holding L fixed, the union does better when w is higher

� Higher indifference curves represent higher utility levels for the union

We turn to the union’s problem at stage 1

� The union can solve the firm’s second stage problem as well as the firm can solve it

� The union should anticipate that the firm’s reaction to the wage demand w will be to choose the employ-

ment level L∗(w)

� Thus, the union’s problem at stage 1 amounts to solve

argmax{U(w,L∗(w)) : w > 0}

� The union would like to choose the wage demand w that yields the outcome (w,L∗(w)) that is on the

highest possible indifference curve

56

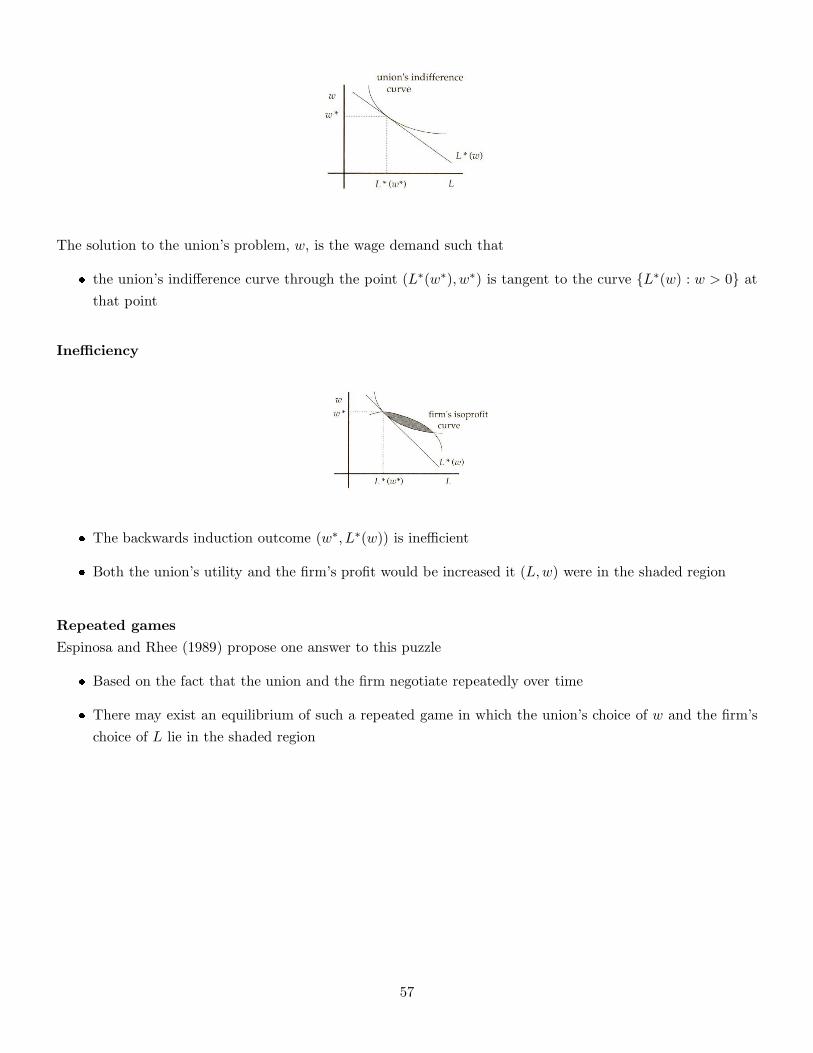

The solution to the union’s problem, w, is the wage demand such that

� the union’s indifference curve through the point (L∗(w∗), w∗) is tangent to the curve {L∗(w) : w > 0} at

that point

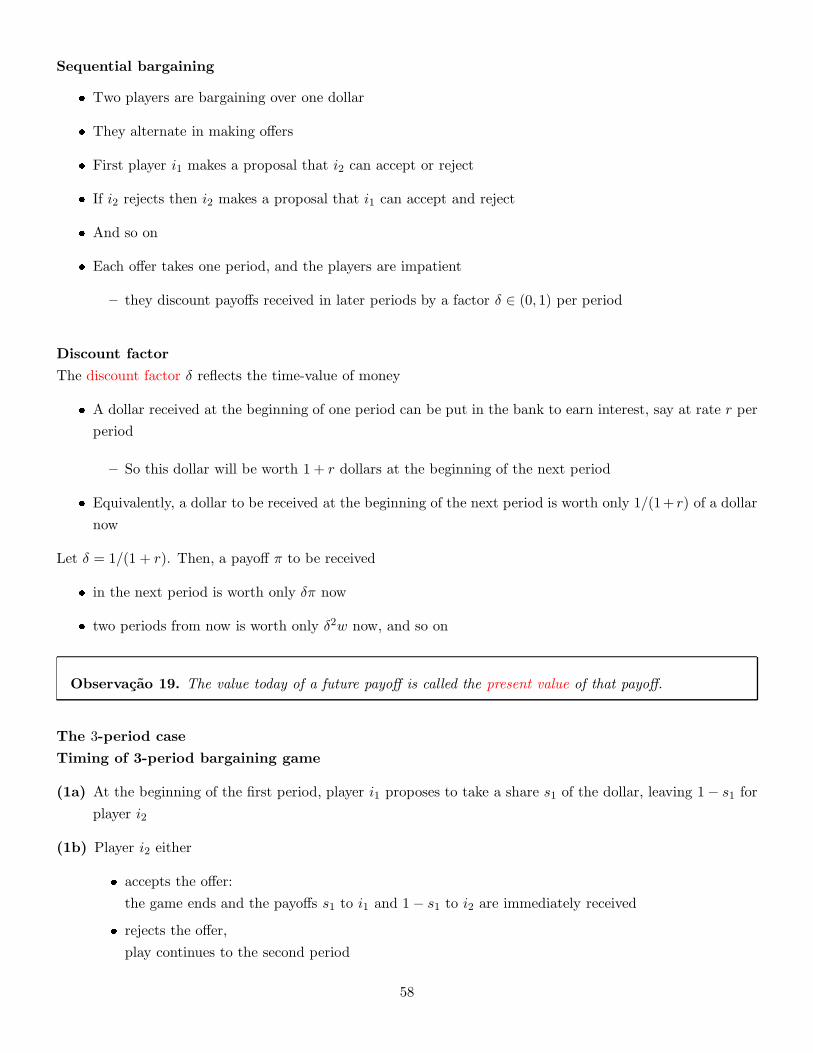

Inefficiency

� The backwards induction outcome (w∗, L∗(w)) is inefficient

� Both the union’s utility and the firm’s profit would be increased it (L,w) were in the shaded region

Repeated games

Espinosa and Rhee (1989) propose one answer to this puzzle

� Based on the fact that the union and the firm negotiate repeatedly over time

� There may exist an equilibrium of such a repeated game in which the union’s choice of w and the firm’s

choice of L lie in the shaded region

57

Sequential bargaining

� Two players are bargaining over one dollar

� They alternate in making offers

� First player i1 makes a proposal that i2 can accept or reject

� If i2 rejects then i2 makes a proposal that i1 can accept and reject

� And so on

� Each offer takes one period, and the players are impatient

– they discount payoffs received in later periods by a factor δ ∈ (0, 1) per period

Discount factor

The discount factor δ reflects the time-value of money

� A dollar received at the beginning of one period can be put in the bank to earn interest, say at rate r per

period

– So this dollar will be worth 1 + r dollars at the beginning of the next period

� Equivalently, a dollar to be received at the beginning of the next period is worth only 1/(1+ r) of a dollar

now

Let δ = 1/(1 + r). Then, a payoff π to be received

� in the next period is worth only δπ now

� two periods from now is worth only δ2w now, and so on

Observacao 19. The value today of a future payoff is called the present value of that payoff.

The 3-period case

Timing of 3-period bargaining game

(1a) At the beginning of the first period, player i1 proposes to take a share s1 of the dollar, leaving 1− s1 for

player i2

(1b) Player i2 either

� accepts the offer:

the game ends and the payoffs s1 to i1 and 1− s1 to i2 are immediately received

� rejects the offer,

play continues to the second period

58

(2a) At the beginning of the second period, i2 proposes that player i1 take a share s2 of the dollar,3 leaving

1− s2 for i2

(2b) Player i1 either

� accepts the offer:

the game ends and the payoffs s2 to i1 and 1− s2 to i2 are immediately received

� rejects the offer:

play continues to the third period

(3) At the beginning of the third period,

� i1 receives a share s of the dollar

� i2 receives a share 1− s of the dollar

where s ∈ (0, 1) is exogenously given

Backwards induction outcome

We first compute i2’s optimal offer if the second period is reached

� Player i1 can receive s in the third period by rejecting i2’s offer of s2 this period

� But the value this period of receiving s next period is only δs

� Thus, i1 will

– accept s2 if s2 ≥ δs

– reject s2 if s2 < δs

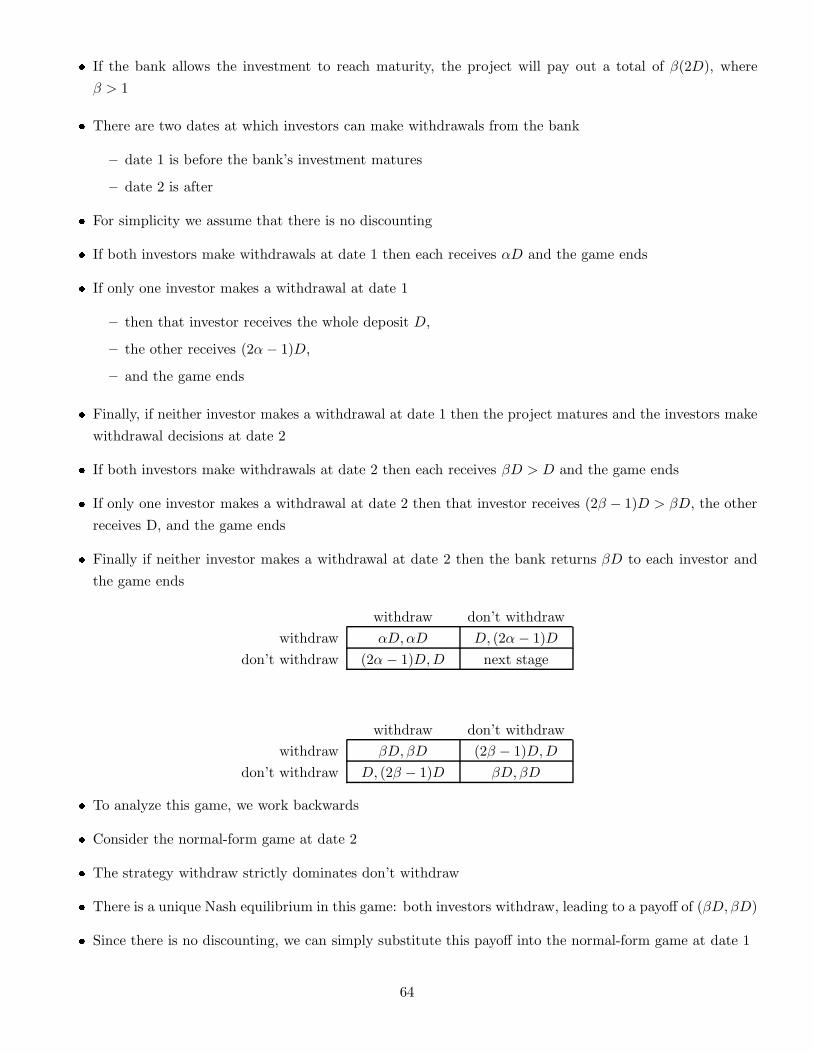

� We assume that each player will accept an offer if indifferent between accepting and rejecting

� Player i2’s decision problem in the second period amounts to choosing between

– receiving 1− δs this period by offering s2 = δs to player i1

– receiving 1− s next period by offering player i1 any s2 < δs

� The discounted value of the latter decision is δ(1 − s),

– which is less than 1− δs available from the former option

� So player i2’s optimal second-period offer is s∗2 = δs

3st always goes to player i1 regardless of who made the offer

59

Observacao 20. If play reaches the second period, player i2 will offer s∗2 and player i1 will accept.

� Since i1 can solve i2’s second-period problem as well as player i2 can

� Then i1 knows that i2 can receive 1− s∗2 in the second period by rejecting i1’s offer of s1 this period

� The value this period of receiving 1− s∗2 next period is only δ(1 − s∗2)

� Thus player i2 will accept i1’s offer of s1 this period ⇔

1− s1 ≥ δ(1− s∗2) or s1 ≤ 1− δ(1 − s∗2)

� Player i1’s first-period decision problem therefore amounts to choosing between

– receiving 1− δ(1 − s∗2) this period by offering 1− s1 = δ(1 − s∗2) to i2

– receiving s∗2 next period by offering 1− s1 < δ(1 − s∗2) to i2

� The discounted value of the latter option is δs∗2 = δ2s

– which is less than the 1− δ(1 − s∗2) = 1− δ(1 − δs) available from the former option

� Thus player i1’s optimal first-period offer is

s∗1 = 1− δ(1 − s∗2) = 1− δ(1 − δs)

Observacao 21. The backwards induction outcome of this 3-period game is

� i1 offers the settlement (s∗1, 1− s∗1) to i2, who accepts

The infinite horizon case

� The timing is as described previously

� Except that the exogenous settlement in step (3) is replaced by an infinite sequence of steps (3a), (3b),

(4a), (4b), and so on

– Player i1 makes the offer in odd-numbered period

– Player i2 in even-numbered

� Bargaining continues until one player accepts an offer

� We would like to solve backwards

� Because the game could go on infinitely, there is no last move at which to begin such an analysis

60

A solution was proposed by Shaked and Sutton (1984)

� The game beginning in the third period (should it be reached) is identical to the game as a whole (beginning

in the first period)

� In both cases (game beginning in the 3° period or as a whole)

– player i1 makes the first offer

– the players alternate in making subsequent offers

– the bargaining continues until one player accepts an offer

� Suppose that there is a backwards induction outcome of the game as a whole in which players i1 and i2

receive the payoffs s and 1− s

� We can use these payoffs in the game beginning in the third period, should it be reached

� And then work backwards to the first period, as in the 3-period model, to compute a new backwards

induction outcome for the game as a whole

� In this new backwards induction outcome, i1 will offer the settlement (f(s), 1 − f(s)) in the first period

and i2 will accept, where

f(s) = 1− δ(1− δs)

� Let sH be the highest payoff player i1 can achieve in any backwards induction outcome of the game as a

whole

� Using sH as the third-period payoff to player i1, this will produce a new backwards induction outcome in

which player i1’s first-period payoff is f(sH)

� Since s 7→ f(s) = 1− δ + δ2s is increasing, the payoff f(sH) must coincide with sH

� The only value of s that satisfies f(s) = s is 1/(1 + δ), which will be denoted by s∗

� Actually we can prove that (s∗, 1− s∗) is the unique backwards-induction outcome of the game as a whole

– In the first period, i1 offers the settlement (s∗, 1− s∗)

– Player i2 accepts

2.2 Two-stage games of complete but imperfect information

Theory: Subgame perfection

� We continue to assume that play proceeds in a sequence of stages

� The moves in all previous stages are observed before the next stage begins

� However, we now allow there be simultaneous moves within each stage

61

– The game has imperfect information

We will analyze the following simple game:

1. Players i1 and i2 simultaneously choose actions ai1 and ai2 from feasible sets Ai1 and Ai2 , respectively

2. Players i3 and i4 observe the outcome of the first stage, (ai1 , ai2), and then simultaneously choose actions

ai3 and ai4 from feasible sets Ai3 and Ai4 , respectively

3. Payoffs are ui(ai1 , ..., ai4)

� The feasible action sets of players i3 and i4 in the second stage, Ai3 and Ai4 , could be allowed to depend

on the outcome of the first stage, (ai1 , ai2)

� In particular, there may be values of (ai1 , ai2) that end the game

� One could allow for a longer sequence of stages either by allowing players to move in more than one stage

or by adding players

� In some applications, players i3 and i4 are players i1 and i2

� In other applications, either player i2 or player i4 is missing

� We solve the game by using an approach in the spirit of backwards induction

� The first step in working backwards from the end of the game involves solving a simultaneous-move game

between players i3 and i4 in stage 2, given the outcome of stage 1

� We will assume that for each feasible outcome (ai1 , ai2) of the first game, the second-stage game that

remains between players i3 and i4 has a unique Nash equilibrium denoted by (ai3(ai1 , ai2), ai4(ai1 , ai2))

62

� If i1 and i2 anticipate that the second-stage behavior of i3 and i4 will be given by the functions ai3 and

ai4

� Then the first-stage interaction between i1 and i2 amounts to the following simultaneous-move game

1. Players i1 and i2 simultaneously choose actions ai1 and ai2 from feasible sets Ai1 and Ai2 , respectively

2. Payoffs are

ui(ai1 , ai2 , ai3(ai1 , ai2), ai4(ai1 , ai2))

� Suppose (a∗i1 , a∗i2) is the unique Nash equilibrium of this simultaneous-move game

� We will call

(a∗i1 , a∗i2, a∗i3 , a

∗i4)

the subgame-perfect outcome of this two-stage game, where

a∗i3 = ai3(a∗i1, a∗i2) and a∗i4 = ai4(a

∗i1, a∗i2)

Attractive feature 11.

� Players i1 and i2 should not believe a threat by players i3 and i4 that the latter will respond with actions