Embed Size (px)

Citation preview

HIROSHIMA BANK ANNUAL REPORT 201324

THE HIROSHIMA BANK, LTD. AND CONSOLIDATED SUBSIDIARIESMarch 31, 2012 and 2013

Notes to Consolidated Financial Statements

1 Basis of presenting consolidated financial statements

The accompanying consolidated financial statements of the Hiroshima Bank, Ltd. (the “Bank”) and its consolidated subsidiaries have been prepared in accordance with the provisions set forth in the Japanese Financial Instruments and Exchange Law and its related accounting regulations, and in conformity with accounting principles generally accepted in Japan (“Japanese GAAP”), which are different in certain respects as to application and disclosure requirements of International Financial Reporting Standards.

The accompanying consolidated financial statements have been restructured and translated into English (with some expanded descriptions) from the consolidated financial statements of the Bank prepared in accordance with Japanese GAAP and filed with the appropriate Local Finance Bureau of the Ministry of Finance as required by the Financial Instruments and Exchange Law. Some supplementary information included in the statutory Japanese language consolidated financial statements, but not required for fair presentation, is not presented in the accompanying consolidated financial statements.

The Bank maintains its accounting records in Japanese yen, the currency in which the Bank is incorporated and operates. In preparing the accompanying consolidated financial statements and notes thereto, Japanese yen figures less than one million yen have been rounded down to the nearest million yen, except for per share data, in accordance with the Financial Instruments and Exchange Law and Enforcement Regulation concerning Banking Law of Japan. Therefore, total or subtotal amounts shown in the accompanying consolidated financial statements and notes thereto do not necessarily agree with the sums of individual amounts. The translations of the Japanese yen amounts into U.S. dollars are included solely for the convenience of readers, using the prevailing exchange rate at March 31, 2013, which was ¥94.05 to U.S.$1.00. The convenience translations should not be construed as representations that the Japanese yen amounts have been, could have been, or could in the future be, converted into U.S. dollars at this or any other rate of exchange.

2 Principles of consolidation

The consolidated financial statements include the accounts of the Bank and all of its majority-owned subsidiaries. The Bank includes the accounts of several companies which are less than 50% owned in the accompanying consolidated financial statements in case that the Bank has control over these companies through cross-shareholdings, transfer of management, and provision of debt guarantees and loans. All significant intercompany balances and transactions have been eliminated.

Investments in 20% to 50% owned companies are carried at cost adjusted for equity in undistributed earnings or losses since acquisition (the equity method). The Bank also applies the equity method for investments in certain companies which are less than 20% owned in case that the Bank is able to exercise significant influence over these companies.

Consequently, the consolidated financial statements include the account of the Bank and its subsidiaries and affiliated companies (six subsidiaries and five affiliated companies).

As of March 31, 2013, the fiscal year ending dates are March 31 for 5 subsidiaries and January 24 for 1 subsidiary. 1 subsidiary whose fiscal year ends at the date other than March 31 is consolidated using its fiscal year end financial statements.

3 Significant accounting policies

Trading assets and trading liabilitiesThe Bank adopted mark-to-market accounting for trading assets and trading liabilities including securities, financial receivables and financial derivatives for trading purpose. Trading assets and trading liabilities are recorded on a trade date basis, and revenues and expenses related to trading securities transactions are also recorded on a trade date basis. Securities and financial receivables for trading purpose are stated at market or fair value at the balance sheet date. Financial derivatives such as futures and option transactions are stated at a deemed settlement amount at the balance sheet date. Unrealized gains or losses incurred by the mark-to-market method are charged to income.

HIROSHIMA BANK ANNUAL REPORT 2013 25

SecuritiesAll companies are required to examine the intent of holding each security and classify those securities as (a) securities held for trading purposes (hereafter, “trading securities”), (b) debt securities intended to be held to maturity (hereafter, “held-to-maturity debt securities”), (c) equity securities issued by subsidiaries and affiliated companies, and (d) for all other securities that are not classified in any of the above categories (hereafter, “available-for-sale securities”).

Trading securities are stated at fair market value. Gains and losses realized on disposal and unrealized gains and losses from market value fluctuations are recognized as gains or losses in the period of the change. Held-to-maturity debt securities are stated at amortized cost. Equity securities issued by subsidiaries and affiliated companies which are not consolidated or accounted for using the equity method are stated at moving-average cost. Available-for-sale securities with available fair market values are stated at fair market value. Unrealized gains and unrealized losses on these securities are reported, net of applicable income taxes, as a separate component of net assets. Realized gains and losses on sale of such securities are computed using moving-average cost.

Securities available-for-sale for which fair value cannot be reliably determined are carried at cost determined by the moving average method.

Debt securities with no available fair market value are stated at amortized cost, net of the amount considered not collectible. Other securities with no available fair market value are stated at moving-average cost.

If the market value of held-to-maturity debt securities, equity securities issued by subsidiaries and affiliated companies not consolidated or accounted for by the equity method, and available-for-sale securities, declines significantly, such securities are stated at fair market value and the difference between fair market value and the carrying amount is recognized as loss in the period of the decline. If the fair market value of equity securities issued by unconsolidated subsidiaries and affiliated companies not on the equity method is not readily available, such securities should be written down to net asset value with a corresponding charge in the income statement in the event net asset value declines significantly. In these cases, such fair market value or the net asset value will be the carrying amount of the securities at the beginning of the next year.

When market values of available-for-sale securities with fair market values decline by 50% or more of the acquisition

cost at the balance sheet date, the Bank writes down such securities to the fair market values and records the related write-downs as loss in its consolidated statement of income. When market values of available-for-sale securities with fair market value decline by 30% or more but less than 50% of the acquisition cost, write-downs to the fair market values may be recognized for certain issuers based on evaluation of issuers’ debtor classification. The Bank devaluated the securities other than securities held for trading purposes and recognized a loss of ¥2,842 million (¥1,931 million for equity securities and ¥234 million for bonds and ¥675 million for financial receivables purchased) and ¥1,280 million ($14 million) (¥867 million ($9 million) for equity securities and ¥292 million ($3 million) for bonds and ¥120 million ($1 million) for financial receivables purchased) as for the years ended March 31, 2012 and 2013, respectively.

Derivatives and hedge accountingCompanies are required to state derivative financial instruments at fair value and to recognize changes in the fair value as gains or losses unless derivative financial instruments are used for hedging purposes.

(1) Hedging against interest rate fluctuationsThe Bank applies deferred hedge accounting pursuant to the treatment regulated by “Treatment for Accounting and Auditing of Application of Accounting Standard for Financial Instruments in Banking Industry (JICPA Industry Audit Committee Report No.24)” to hedge transactions such as interest rate swaps entered into to mitigate interest rate risk arising from financial assets and liabilities. The Bank assessed the hedge’s effectiveness by considering the adequacy of offsetting movement of the fair value by the changes in interest rates through classifying the hedged items such as loans and borrowed money and the hedging transactions such as interest rate swaps by their maturity.

(2) Hedging against foreign currency fluctuationsThe Bank applies deferred hedge accounting to hedge transactions such as currency swaps and foreign exchange swaps entered into to mitigate foreign exchange risk arising from foreign-currency-denominated financial assets and liabilities.

The Bank applies the hedge accounting pursuant to “Treatment of Accounting and Auditing Concerning Accounting for Foreign Currency Transactions in Banking Industry (JICPA Industry Audit Committee Report No.25)” to currency swap transactions and foreign exchange swap transactions for the purpose of funds lending and borrowing in different currencies. The Bank assesses the hedge’s

HIROSHIMA BANK ANNUAL REPORT 201326

effectiveness by confirming that the positions of hedge instruments (currency swap and foreign exchange swap transactions) do not exceed the corresponding foreign-currency-denominated financial receivables and debts as hedged items.

(3) Exceptional treatmentFor some assets and liabilities, the Bank defers recognition of gains or losses resulting from changes in fair value of derivative financial instruments until the related losses or gains on the hedged items are recognized. Also, if interest rate swap contracts are used as hedge and meet certain hedging criteria, the net amount to be paid or received under the interest rate swap contract is added to or deducted from the interest on the assets or liabilities for which the swap contract was executed.

Tangible fixed assets (except for lease assets)Tangible fixed assets except for land utilized for business operations are stated at cost less accumulated depreciation. Accumulated impairment losses are deducted from acquisition costs.

The Bank and its consolidated subsidiaries depreciate their tangible fixed assets under the declining-balance method over their estimated useful lives. Estimated useful lives of major items are as follows: Buildings: 22 – 50 years Others: 3 – 20 years

(Changes in accounting policies which are difficult to distinguish from changes in accounting estimates)In accordance with the amendment of the Corporation Tax Act, effective from the fiscal year ended March 31, 2013 the Bank and its consolidated subsidiaries have changed depreciation method for those tangible fixed assets acquired on or after April 1, 2012. The effect of this change was to increase income before income taxes and minority interests by ¥30 million ($319 thousand).

Pursuant to the Law concerning Revaluation of Land (the “Law”), land for business operations as of March 31, 1998 was revalued at fair value. Due to the revaluation, the carrying value of the land was increased by ¥53,429 million to ¥71,380 million as of March 31, 1998, and the related net unrealized gain was reported in liabilities as “Land revaluation reserve.” Effective March 31, 1999, the Law has been revised for presentation of the unrealized gain. According to the revised Law, net unrealized gain reported in liabilities shall be reclassified in a separate component of stockholders’ equity net of applicable income taxes as “Land revaluation reserve, net of tax” as of March 31, 1999.

According to the revised Law, the Bank is not permitted to revalue the land at any time even in case that the fair value of the land declines. Such unrecorded revaluation loss as of March 31, 2012 and 2013 was ¥31,251 million and ¥32,034 million ($341 million), respectively.

Accumulated depreciation for tangible assets, recognized as for the fiscal year ended March 31, 2012 and 2013, amounted to ¥43,519 million and ¥44,588 million ($474 million), respectively.

Intangible fixed assets (except for lease assets)Intangible fixed assets are amortized using the straight-line method. Software utilized by the Bank is amortized over the period in which it is expected to be utilized (mainly five or ten years in 2012 and 2013).

Lease assetsLease assets in “Tangible fixed assets” or “Intangible fixed assets” of the finance leases other than those that transfer the ownership of leased property to the lessees is computed under the straight-line method over the lease term with zero residual value unless residual value is guaranteed by the corresponding lease contracts.

Reserve for possible loan lossesFor loans to insolvent customers who are undergoing bankruptcy or other collection proceedings or in a similar financial condition, the reserve for possible loan losses is provided in the full amount of such loans, excluding the portion that is estimated to be recoverable due to available security interests or guarantees.

For the unsecured and unguaranteed portions of loans to customers not presently in the above circumstances, but for which there is a high probability of so becoming, the reserve for possible loan losses is provided for estimated unrecoverable amounts determined after evaluating the customer’s overall financial conditions.

Effective April 1, 2003, in order to estimate a reserve for possible loan losses in cases where the Bank is able to rationally evaluate cash flows from collection of principals and interests of the relevant loans, the Bank introduced the Discounted Cash Flow method (“the DCF method”) for claims on borrowers whose loans are classified as “Restructured loans, including loans to supported companies” as referred in Note 6 and whose total loans outstanding exceeds a certain threshold. Under the DCF method, the difference between the cash flows discounted by the original interest rate and the book value of the loan is provided as a reserve for possible loan losses.

HIROSHIMA BANK ANNUAL REPORT 2013 27

From the fiscal year ended March 31, 2013, the Bank uses the DCF method for claims on borrowers whose loans are classified as Potentially Bankrupt Borrowers when the cash flow from the repayment of the principal and interest received can be reasonably estimated, and whose total loans outstanding exceed a certain credit threshold. As a result, income before income taxes decreased ¥2,152 million ($23 million).

For other loans, the reserve for possible loan losses is provided based on the Bank’s actual rate of loan losses in the past.

Consolidated subsidiaries provide the reserve for possible loan losses mainly based on the actual rate of loan losses in the past.

All branches and the credit supervision department evaluate all loans in accordance with the self-assessment rule, and their evaluations are audited by the asset audit section, which is independent from branches and credit supervision department, and the evaluations are revised as required based on the audits.

Secured and guaranteed loans which are for insolvent borrowers or in a similar financial condition are disclosed based on the amount of loans net of amounts estimated not to be collected through disposition of collateral or through execution of guarantees. Such amounts directly set off against those loans at March 31, 2012 and 2013 were ¥30,017 million and ¥29,589 million ($315 million), respectively.

Employees’ severance and retirement benefitsThe liabilities and expenses for severance and retirement benefits were determined based on the amounts actuarially calculated using certain assumptions.

The Bank and its consolidated subsidiaries provided allowance for employees’ severance and retirement benefits at March 31, 2012 and 2013 based on the estimated amounts of projected benefit obligation and the fair value of the plan assets at those dates. Actuarial gains and losses were recognized in expenses using the straight-line method over 14 years, which was not longer than the average of the estimated remaining service lives, commencing with the following period. Prior service costs were recognized in the consolidated statements of income as incurred.

Reserve for executive retirement benefitsReserve for executive retirement benefits is provided for payment of retirement benefits to directors, corporate auditors and other executive officers, in the amount

deemed accrued at the fiscal year-end based on our internal regulations.

Reserve for reimbursement of dormant depositsReserve for reimbursement of dormant deposits which were derecognized as liabilities under certain conditions is provided for the possible losses on the future claims of withdrawal.

Reserve for point loyalty programsReserve for point loyalty program is provided for the estimated expenses based on an estimate of the future usage of points. Points are granted to credit card holders through card usage under the point loyalty program which is designed to promote card usage.

Foreign currency translationThe consolidated financial statements of the Bank are maintained in Japanese yen. Assets and liabilities denominated in foreign currencies are translated into Japanese yen at the exchange rates prevailing at the balance sheet dates.

Income taxesIncome taxes consist of corporation, enterprise and inhabitants taxes. The provision for income taxes is computed based on the pretax income of the Bank and each of its consolidated subsidiaries with certain adjustments required for consolidation and tax purposes. The asset and liability approach is used to recognize deferred tax assets and liabilities for loss carryforwards and the expected future tax consequences of temporary differences between the carrying amounts and the tax bases of assets and liabilities.

Valuation allowances are recorded to reduce deferred tax assets based on the assessment of the realizability of the tax benefits.

Consumption tax National and local consumption taxes of the Bank and its consolidated domestic subsidiaries are accounted for using the tax-excluded method.

Consolidated statements of cash flows and cash equivalentsIn preparing the consolidated statements of cash flows, cash and due from the BANK OF JAPAN are considered to be cash and cash equivalents.

Amounts per share Net assets per share is calculated by dividing net assets by the number of common stocks outstanding at the year end (excluding “treasury stock”).

HIROSHIMA BANK ANNUAL REPORT 201328

Net income per share is calculated by dividing net income attributable to the stockholders by the average number of common stocks outstanding during the year (excluding “treasury stock”).

Cash dividends per share represent the actual amounts declared as applicable to the respective years.

ReclassificationsCertain amounts in the 2012 consolidated financial statements have been reclassified to conform with the 2013 presentation.

Accounting standard issued but not yet effectiveAccounting Standard for Retirement Benefit (ASBJ Statement No.26, May 17, 2012) and Guidance for Accounting Standard for Retirement Benefit (ASBJ Guidance No.25, May 17, 2012)

(1) OutlineThe accounting standard has been revised in light of improving financial reporting and trend toward international convergence, mainly on ( i ) changes in accounting methods for unrecognized actuarial differences and unrecognized prior service costs, and enhancement of disclosure items; ( ii ) changes of calculation methods for projected benefit obligations and service cost.

(2) Date of applicationThe Bank intends to adopt ( i ) to consolidated financial statements as of the end of the fiscal year beginning on April 1, 2013, and to adopt ( ii ) from the fiscal year beginning on April 1, 2014.

(3) Effects of adoption of the revised accounting standardEffects of adoption of the revised accounting standard are currently examined.

ESOP Trust Utilizing Employee Stock Ownership AssociationThe board of directors of the Bank, at the meeting held on May 13, 2011, approved a resolution to introduce and “ESOP Trust” utilizing employee stock ownership association as an incentive plan for employees.

In line with the economic substance of the plan, the Bank accounts for the transactions involving the trust account as its own given that the Bank guarantees the ESOP Trust’s liabilities. Therefore, the Bank’s shares owned by the ESOP Trust are accounted for as treasury stock in the consolidated balance sheets and consolidated statements of changes in net assets and dividends paid to the shares are balances

out by the dividends earned by the ESOP Trust. The assets, liabilities, income and expenses of the ESOP are included in the consolidated balance sheets, consolidated statements of income, consolidated statement of comprehensive income, consolidated statements of changes in net assets and consolidated statements of cash flows.

4 Securities

(1) Trading account securities included in “Trading assets,” certificate of deposits with banks included in “Cash and due from banks,” and trust beneficiary rights included in “Financial receivables purchased,” which are separately reported from “Securities” in the consolidated balance sheets, are included in this section.

(2) The following tables summarize acquisition costs, book values and fair values of securities with available fair values as of March 31, 2012 and 2013:

a) Trading securities:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Amount of net unrealized gains included in the consolidated statements of income ¥0 ¥1 $0

b) Available-for-sale securities:At March 31, 2012

Millions of yen

Fair value exceeding cost: Book valueAcquisition

cost

Gross unrealized

gain

Equity Securities ¥ 37,483 ¥ 22,945 ¥ 14,537Bonds: 1,324,264 1,311,316 12,947

National government bonds 1,044,990 1,037,251 7,738Local government bonds 146,745 143,205 3,540Bonds 132,527 130,859 1,668

Others 143,704 140,342 3,362Sub Total ¥1,505,452 ¥1,474,605 ¥ 30,846

Fair value not exceeding cost:

Equity Securities ¥ 42,069 ¥ 54,684 ¥(12,615)Bonds: 133,415 134,842 (1,426)

National government bonds 98,984 99,364 (379)Local government bonds 4,844 4,847 (3)Bonds 29,586 30,630 (1,044)

Others 122,980 137,358 (14,377)Sub Total ¥ 298,465 ¥ 326,885 ¥(28,419)Total ¥1,803,918 ¥1,801,491 ¥ 2,427

HIROSHIMA BANK ANNUAL REPORT 2013 29

At March 31, 2013Millions of yen

Fair value exceeding cost: Book valueAcquisition

cost

Gross unrealized

gain

Equity Securities ¥ 51,582 ¥ 31,838 ¥19,744Bonds: 1,363,613 1,342,944 20,669

National government bonds 1,057,108 1,044,683 12,425Local government bonds 154,908 149,683 5,225Bonds 151,596 148,577 3,018

Others 253,223 239,491 13,732Sub Total ¥1,668,419 ¥1,614,273 ¥54,145

Fair value not exceeding cost:

Equity Securities ¥ 36,186 ¥ 43,320 ¥ (7,133)Bonds: 214,936 215,473 (537)

National government bonds 199,718 199,787 (69)Local government bonds — — —Bonds 15,218 15,686 (467)

Others 133,079 139,253 (6,174)Sub Total 384,201 398,047 (13,845)Total ¥2,052,621 ¥2,012,321 ¥40,300

Millions of U.S. dollars

Fair value exceeding cost: Book valueAcquisition

cost

Gross unrealized

gain

Equity Securities $ 549 $ 339 $210Bonds: 14,499 14,279 220

National government bonds 11,240 11,108 132Local government bonds 1,647 1,591 56Bonds 1,612 1,580 32

Others 2,692 2,546 146Sub Total $17,740 $17,164 $576

Fair value not exceeding cost:

Equity Securities $ 385 $ 460 $ (75)Bonds: 2,285 2,291 (6)

National government bonds 2,123 2,124 (1)Local government bonds — — —Bonds 162 167 (5)

Others 1,415 1,481 (66)Sub Total 4,085 4,232 (147)Total $21,825 $21,396 $429

(3) Total sales of available-for-sale securities sold at March 31, 2012 and 2013 were as follows:

At March 31, 2012Millions of yen

TypeProceeds

from sales

Total amount of gains on

sales

Total amount of losses on

sales

Equity Securities ¥ 13,124 ¥ 1,790 ¥3,909Bonds: 1,838,478 6,948 2,204

National government bonds 1,816,701 6,918 1,881Local government bonds 8,138 9 —Bonds 13,638 20 323

Others 114,158 2,118 2,225Total ¥1,965,761 ¥10,857 ¥8,339

At March 31, 2013Millions of yen

TypeProceeds

from sales

Total amount of gains on

sales

Total amount of losses on

sales

Equity Securities ¥ 17,572 ¥ 4,883 ¥3,533Bonds: 2,191,283 8,071 2,321

National government bonds 2,176,232 8,039 2,321Local government bonds 4,147 4 —Bonds 10,902 27 —

Others 200,786 2,243 3,329Total ¥2,409,642 ¥15,198 ¥9,184

Millions of U.S. dollars

TypeProceeds

from sales

Total amount of gains on

sales

Total amount of losses on

sales

Equity Securities $ 187 $ 52 $38Bonds: 23,299 86 25

National government bonds 23,139 86 25Local government bonds 44 0 —Bonds 116 0 —

Others 2,135 24 35Total $25,621 $162 $98

HIROSHIMA BANK ANNUAL REPORT 201330

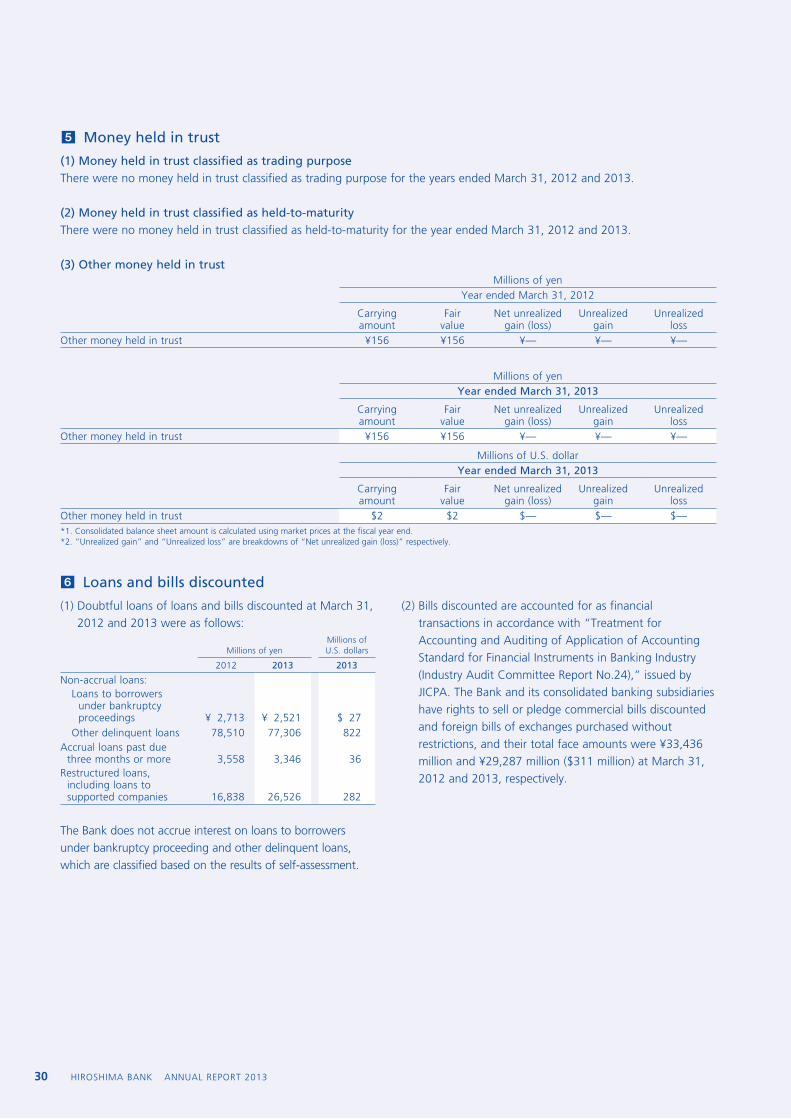

6 Loans and bills discounted

(1) Doubtful loans of loans and bills discounted at March 31, 2012 and 2013 were as follows:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Non-accrual loans:Loans to borrowers under bankruptcy proceedings ¥ 2,713 ¥ 2,521 $ 27Other delinquent loans 78,510 77,306 822

Accrual loans past due three months or more 3,558 3,346 36Restructured loans, including loans to supported companies 16,838 26,526 282

The Bank does not accrue interest on loans to borrowers under bankruptcy proceeding and other delinquent loans, which are classified based on the results of self-assessment.

(2) Bills discounted are accounted for as financial transactions in accordance with “Treatment for Accounting and Auditing of Application of Accounting Standard for Financial Instruments in Banking Industry (Industry Audit Committee Report No.24),” issued by JICPA. The Bank and its consolidated banking subsidiaries have rights to sell or pledge commercial bills discounted and foreign bills of exchanges purchased without restrictions, and their total face amounts were ¥33,436 million and ¥29,287 million ($311 million) at March 31, 2012 and 2013, respectively.

5 Money held in trust

(1) Money held in trust classified as trading purposeThere were no money held in trust classified as trading purpose for the years ended March 31, 2012 and 2013.

(2) Money held in trust classified as held-to-maturityThere were no money held in trust classified as held-to-maturity for the year ended March 31, 2012 and 2013.

(3) Other money held in trust Millions of yen

Year ended March 31, 2012

Carrying amount

Fair value

Net unrealized gain (loss)

Unrealized gain

Unrealized loss

Other money held in trust ¥156 ¥156 ¥— ¥— ¥—

Millions of yenYear ended March 31, 2013

Carrying amount

Fair value

Net unrealized gain (loss)

Unrealized gain

Unrealized loss

Other money held in trust ¥156 ¥156 ¥— ¥— ¥—

Millions of U.S. dollarYear ended March 31, 2013

Carrying amount

Fair value

Net unrealized gain (loss)

Unrealized gain

Unrealized loss

Other money held in trust $2 $2 $— $— $—*1. Consolidated balance sheet amount is calculated using market prices at the fiscal year end.*2. “Unrealized gain” and “Unrealized loss” are breakdowns of “Net unrealized gain (loss)” respectively.

HIROSHIMA BANK ANNUAL REPORT 2013 31

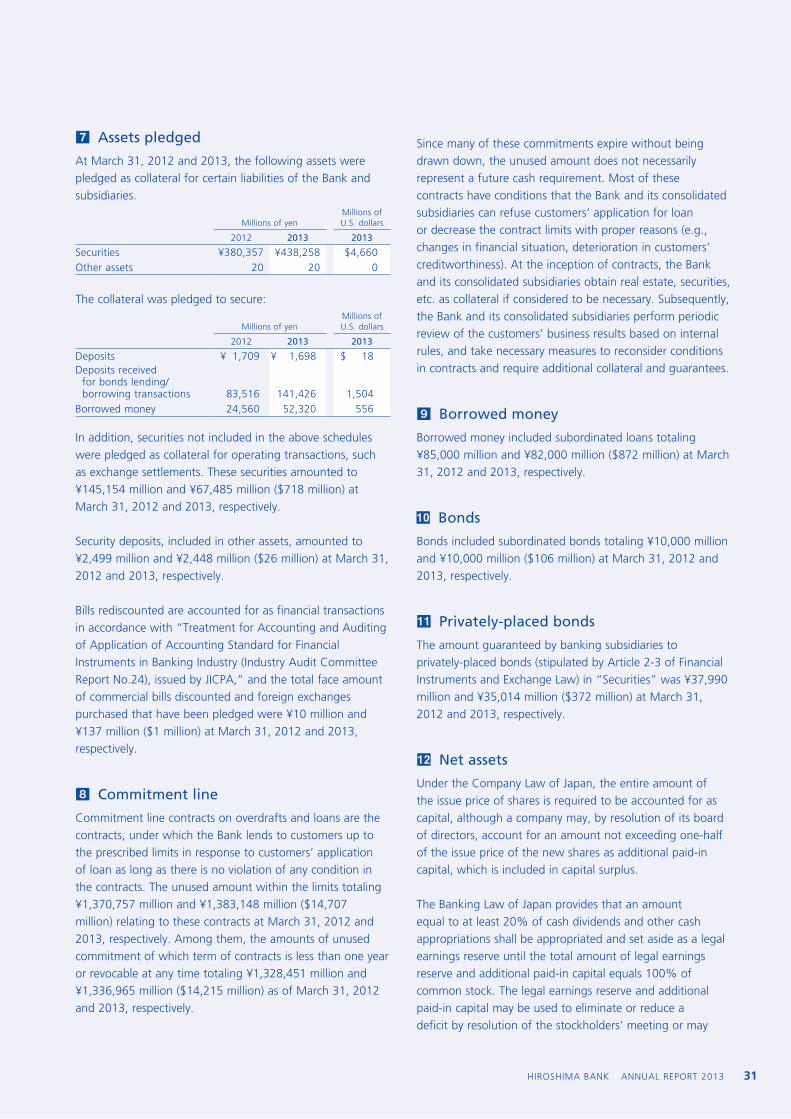

7 Assets pledged

At March 31, 2012 and 2013, the following assets were pledged as collateral for certain liabilities of the Bank and subsidiaries.

Millions of yenMillions of U.S. dollars

2012 2013 2013

Securities ¥380,357 ¥438,258 $4,660Other assets 20 20 0

The collateral was pledged to secure:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Deposits ¥ 1,709 ¥ 1,698 $ 18Deposits received for bonds lending/ borrowing transactions 83,516 141,426 1,504Borrowed money 24,560 52,320 556

In addition, securities not included in the above schedules were pledged as collateral for operating transactions, such as exchange settlements. These securities amounted to ¥145,154 million and ¥67,485 million ($718 million) at March 31, 2012 and 2013, respectively.

Security deposits, included in other assets, amounted to ¥2,499 million and ¥2,448 million ($26 million) at March 31, 2012 and 2013, respectively.

Bills rediscounted are accounted for as financial transactions in accordance with “Treatment for Accounting and Auditing of Application of Accounting Standard for Financial Instruments in Banking Industry (Industry Audit Committee Report No.24), issued by JICPA,” and the total face amount of commercial bills discounted and foreign exchanges purchased that have been pledged were ¥10 million and ¥137 million ($1 million) at March 31, 2012 and 2013, respectively.

8 Commitment line

Commitment line contracts on overdrafts and loans are the contracts, under which the Bank lends to customers up to the prescribed limits in response to customers’ application of loan as long as there is no violation of any condition in the contracts. The unused amount within the limits totaling ¥1,370,757 million and ¥1,383,148 million ($14,707 million) relating to these contracts at March 31, 2012 and 2013, respectively. Among them, the amounts of unused commitment of which term of contracts is less than one year or revocable at any time totaling ¥1,328,451 million and ¥1,336,965 million ($14,215 million) as of March 31, 2012 and 2013, respectively.

Since many of these commitments expire without being drawn down, the unused amount does not necessarily represent a future cash requirement. Most of these contracts have conditions that the Bank and its consolidated subsidiaries can refuse customers’ application for loan or decrease the contract limits with proper reasons (e.g., changes in financial situation, deterioration in customers’ creditworthiness). At the inception of contracts, the Bank and its consolidated subsidiaries obtain real estate, securities, etc. as collateral if considered to be necessary. Subsequently, the Bank and its consolidated subsidiaries perform periodic review of the customers’ business results based on internal rules, and take necessary measures to reconsider conditions in contracts and require additional collateral and guarantees.

9 Borrowed money

Borrowed money included subordinated loans totaling ¥85,000 million and ¥82,000 million ($872 million) at March 31, 2012 and 2013, respectively.

10 Bonds

Bonds included subordinated bonds totaling ¥10,000 million and ¥10,000 million ($106 million) at March 31, 2012 and 2013, respectively.

11 Privately-placed bonds

The amount guaranteed by banking subsidiaries to privately-placed bonds (stipulated by Article 2-3 of Financial Instruments and Exchange Law) in “Securities” was ¥37,990 million and ¥35,014 million ($372 million) at March 31, 2012 and 2013, respectively.

12 Net assets

Under the Company Law of Japan, the entire amount of the issue price of shares is required to be accounted for as capital, although a company may, by resolution of its board of directors, account for an amount not exceeding one-half of the issue price of the new shares as additional paid-in capital, which is included in capital surplus.

The Banking Law of Japan provides that an amount equal to at least 20% of cash dividends and other cash appropriations shall be appropriated and set aside as a legal earnings reserve until the total amount of legal earnings reserve and additional paid-in capital equals 100% of common stock. The legal earnings reserve and additional paid-in capital may be used to eliminate or reduce a deficit by resolution of the stockholders’ meeting or may

HIROSHIMA BANK ANNUAL REPORT 201332

be capitalized by resolution of the Board of Directors. On condition that the total amount of legal earnings reserve and additional paid-in capital remains being equal to or exceeding 100% of common stock, they are available for distributions or certain other purposes by the resolution of stockholders’ meeting. Legal earnings reserve is included in retained earnings in the accompanying financial statements.

The maximum amount that the Bank can distribute as dividends is calculated based on the unconsolidated financial statements of the Bank in accordance with the Company Law of Japan.

In accordance with the customary practice in Japan, the appropriations are not accrued in the financial statements for the period to which they relate, but are recorded in the subsequent accounting period in which the stockholders’ approval has been obtained. Retained earnings at March 31, 2013 include the amount representing the year-end cash dividend of ¥1,859 million ($20 million), ¥3.00 ($0.03) per share, which was approved at the stockholders’ meeting held on June 26, 2013.

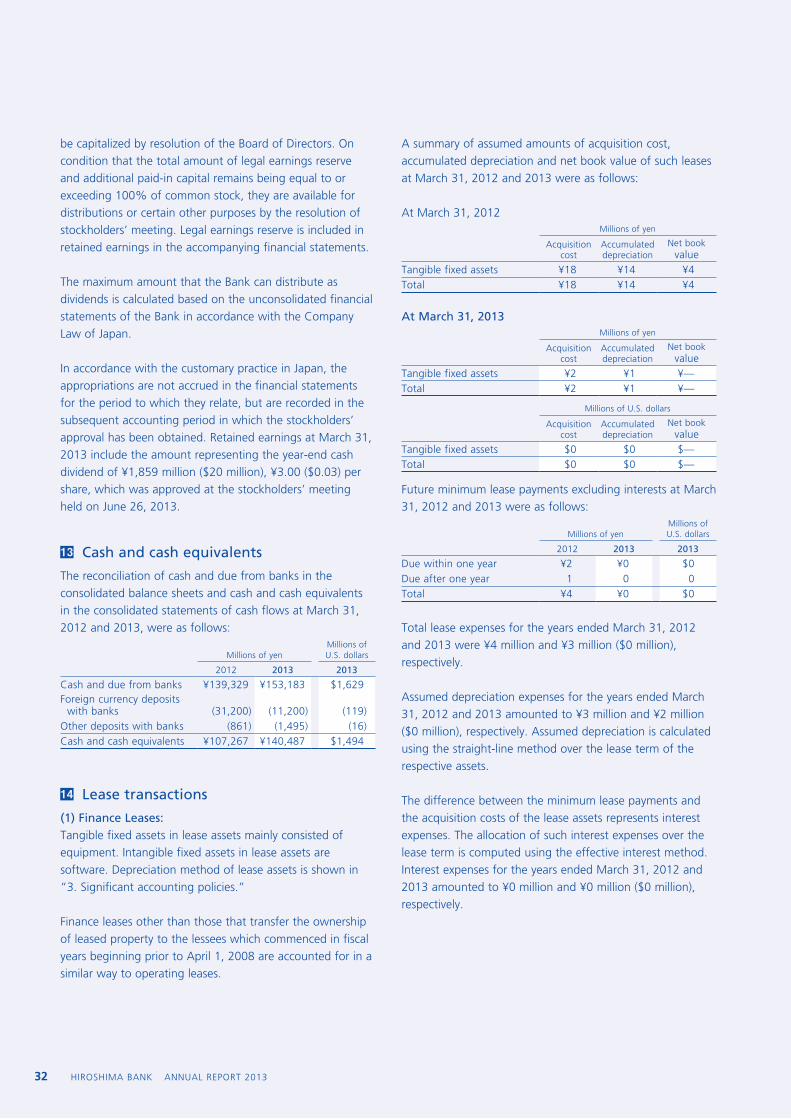

13 Cash and cash equivalents

The reconciliation of cash and due from banks in the consolidated balance sheets and cash and cash equivalents in the consolidated statements of cash flows at March 31, 2012 and 2013, were as follows:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Cash and due from banks ¥139,329 ¥153,183 $1,629Foreign currency deposits with banks (31,200) (11,200) (119)Other deposits with banks (861) (1,495) (16)Cash and cash equivalents ¥107,267 ¥140,487 $1,494

14 Lease transactions

(1) Finance Leases:Tangible fixed assets in lease assets mainly consisted of equipment. Intangible fixed assets in lease assets are software. Depreciation method of lease assets is shown in “3. Significant accounting policies.”

Finance leases other than those that transfer the ownership of leased property to the lessees which commenced in fiscal years beginning prior to April 1, 2008 are accounted for in a similar way to operating leases.

A summary of assumed amounts of acquisition cost, accumulated depreciation and net book value of such leases at March 31, 2012 and 2013 were as follows:

At March 31, 2012Millions of yen

Acquisition cost

Accumulated depreciation

Net book value

Tangible fixed assets ¥18 ¥14 ¥4Total ¥18 ¥14 ¥4

At March 31, 2013Millions of yen

Acquisition cost

Accumulated depreciation

Net book value

Tangible fixed assets ¥2 ¥1 ¥—Total ¥2 ¥1 ¥—

Millions of U.S. dollars

Acquisition cost

Accumulated depreciation

Net book value

Tangible fixed assets $0 $0 $—Total $0 $0 $—

Future minimum lease payments excluding interests at March 31, 2012 and 2013 were as follows:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Due within one year ¥2 ¥0 $0Due after one year 1 0 0Total ¥4 ¥0 $0

Total lease expenses for the years ended March 31, 2012 and 2013 were ¥4 million and ¥3 million ($0 million), respectively.

Assumed depreciation expenses for the years ended March 31, 2012 and 2013 amounted to ¥3 million and ¥2 million ($0 million), respectively. Assumed depreciation is calculated using the straight-line method over the lease term of the respective assets.

The difference between the minimum lease payments and the acquisition costs of the lease assets represents interest expenses. The allocation of such interest expenses over the lease term is computed using the effective interest method. Interest expenses for the years ended March 31, 2012 and 2013 amounted to ¥0 million and ¥0 million ($0 million), respectively.

HIROSHIMA BANK ANNUAL REPORT 2013 33

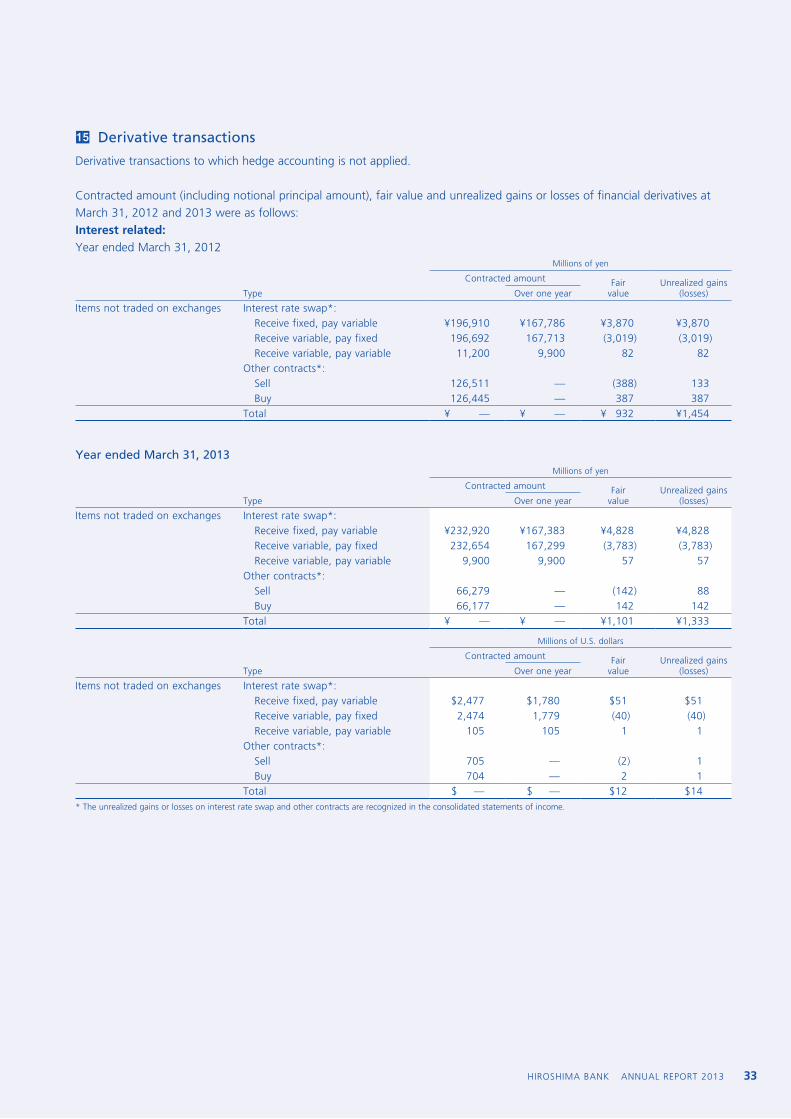

15 Derivative transactions

Derivative transactions to which hedge accounting is not applied.

Contracted amount (including notional principal amount), fair value and unrealized gains or losses of financial derivatives at March 31, 2012 and 2013 were as follows:Interest related: Year ended March 31, 2012

Millions of yen

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Interest rate swap*:Receive fixed, pay variable ¥196,910 ¥167,786 ¥3,870 ¥3,870Receive variable, pay fixed 196,692 167,713 (3,019) (3,019)Receive variable, pay variable 11,200 9,900 82 82

Other contracts*:Sell 126,511 — (388) 133Buy 126,445 — 387 387

Total ¥ — ¥ — ¥ 932 ¥1,454

Year ended March 31, 2013Millions of yen

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Interest rate swap*:Receive fixed, pay variable ¥232,920 ¥167,383 ¥4,828 ¥4,828Receive variable, pay fixed 232,654 167,299 (3,783) (3,783)Receive variable, pay variable 9,900 9,900 57 57

Other contracts*:Sell 66,279 — (142) 88Buy 66,177 — 142 142

Total ¥ — ¥ — ¥1,101 ¥1,333

Millions of U.S. dollars

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Interest rate swap*: Receive fixed, pay variable $2,477 $1,780 $51 $51

Receive variable, pay fixed 2,474 1,779 (40) (40)Receive variable, pay variable 105 105 1 1

Other contracts*:Sell 705 — (2) 1Buy 704 — 2 1

Total $ — $ — $12 $14* The unrealized gains or losses on interest rate swap and other contracts are recognized in the consolidated statements of income.

HIROSHIMA BANK ANNUAL REPORT 201334

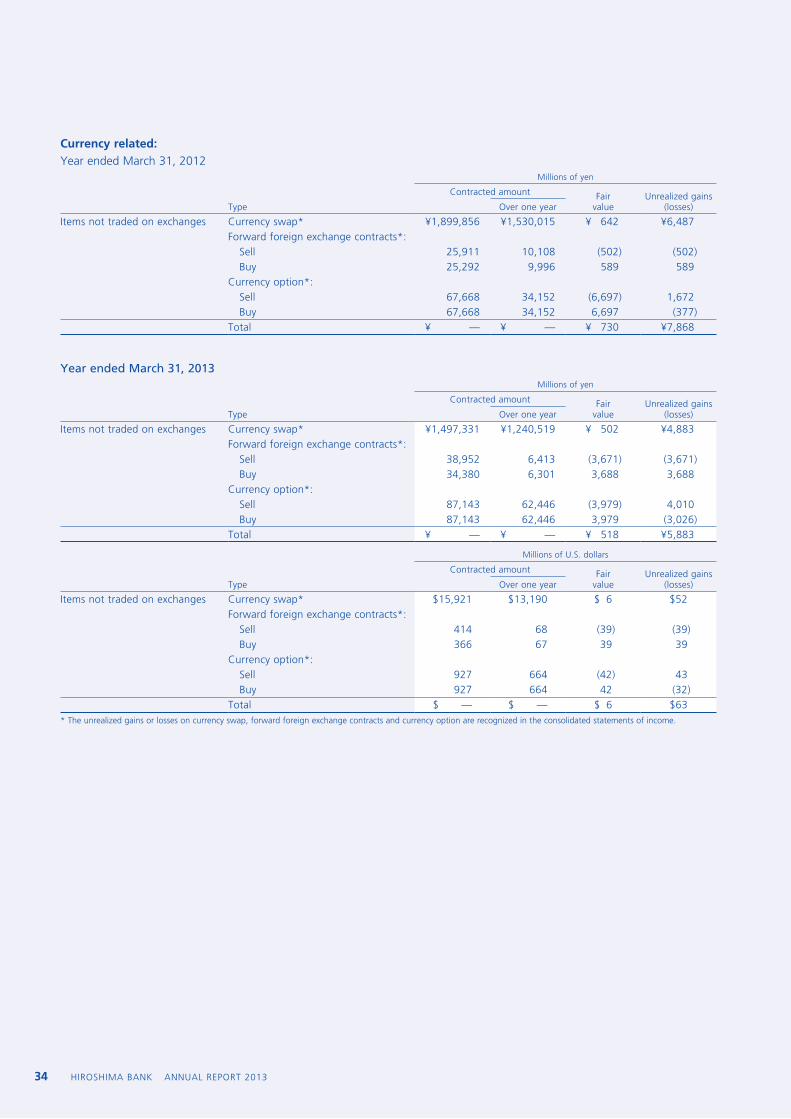

Currency related:Year ended March 31, 2012

Millions of yen

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Currency swap* ¥1,899,856 ¥1,530,015 ¥ 642 ¥6,487Forward foreign exchange contracts*:

Sell 25,911 10,108 (502) (502)Buy 25,292 9,996 589 589

Currency option*:Sell 67,668 34,152 (6,697) 1,672Buy 67,668 34,152 6,697 (377)

Total ¥ — ¥ — ¥ 730 ¥7,868

Year ended March 31, 2013Millions of yen

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Currency swap* ¥1,497,331 ¥1,240,519 ¥ 502 ¥4,883Forward foreign exchange contracts*:

Sell 38,952 6,413 (3,671) (3,671)Buy 34,380 6,301 3,688 3,688

Currency option*:Sell 87,143 62,446 (3,979) 4,010Buy 87,143 62,446 3,979 (3,026)

Total ¥ — ¥ — ¥ 518 ¥5,883

Millions of U.S. dollars

Contracted amount Fair value

Unrealized gains (losses)Type Over one year

Items not traded on exchanges Currency swap* $15,921 $13,190 $ 6 $52Forward foreign exchange contracts*:

Sell 414 68 (39) (39)Buy 366 67 39 39

Currency option*:Sell 927 664 (42) 43Buy 927 664 42 (32)

Total $ — $ — $ 6 $63* The unrealized gains or losses on currency swap, forward foreign exchange contracts and currency option are recognized in the consolidated statements of income.

HIROSHIMA BANK ANNUAL REPORT 2013 35

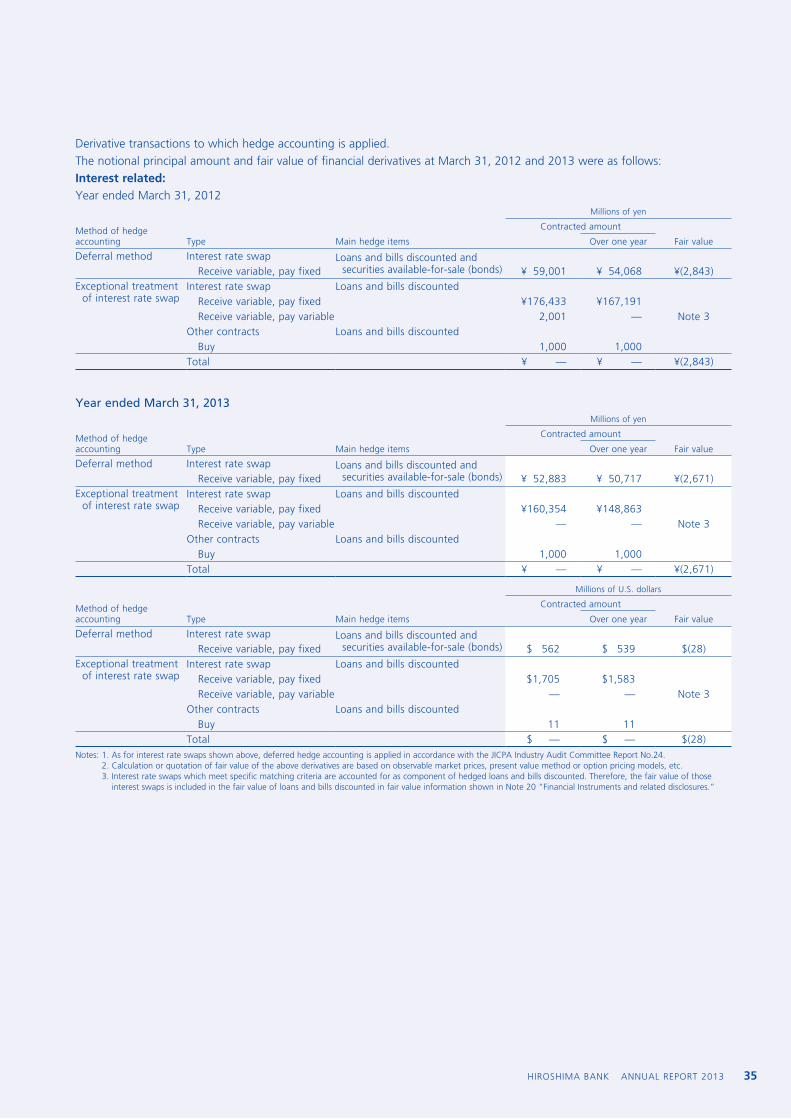

Derivative transactions to which hedge accounting is applied.The notional principal amount and fair value of financial derivatives at March 31, 2012 and 2013 were as follows:Interest related:Year ended March 31, 2012

Millions of yen

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Interest rate swap Loans and bills discounted and securities available-for-sale (bonds)Receive variable, pay fixed ¥ 59,001 ¥ 54,068 ¥(2,843)

Exceptional treatment of interest rate swap

Interest rate swap Loans and bills discountedReceive variable, pay fixed ¥176,433 ¥167,191Receive variable, pay variable 2,001 — Note 3

Other contracts Loans and bills discountedBuy 1,000 1,000

Total ¥ — ¥ — ¥(2,843)

Year ended March 31, 2013Millions of yen

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Interest rate swap Loans and bills discounted and securities available-for-sale (bonds)Receive variable, pay fixed ¥ 52,883 ¥ 50,717 ¥(2,671)

Exceptional treatment of interest rate swap

Interest rate swap Loans and bills discountedReceive variable, pay fixed ¥160,354 ¥148,863Receive variable, pay variable — — Note 3

Other contracts Loans and bills discountedBuy 1,000 1,000

Total ¥ — ¥ — ¥(2,671)

Millions of U.S. dollars

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Interest rate swap Loans and bills discounted and securities available-for-sale (bonds)Receive variable, pay fixed $ 562 $ 539 $(28)

Exceptional treatment of interest rate swap

Interest rate swap Loans and bills discountedReceive variable, pay fixed $1,705 $1,583Receive variable, pay variable — — Note 3

Other contracts Loans and bills discountedBuy 11 11

Total $ — $ — $(28)Notes: 1. As for interest rate swaps shown above, deferred hedge accounting is applied in accordance with the JICPA Industry Audit Committee Report No.24. 2. Calculation or quotation of fair value of the above derivatives are based on observable market prices, present value method or option pricing models, etc. 3. Interest rate swaps which meet specific matching criteria are accounted for as component of hedged loans and bills discounted. Therefore, the fair value of those

interest swaps is included in the fair value of loans and bills discounted in fair value information shown in Note 20 “Financial Instruments and related disclosures.”

HIROSHIMA BANK ANNUAL REPORT 201336

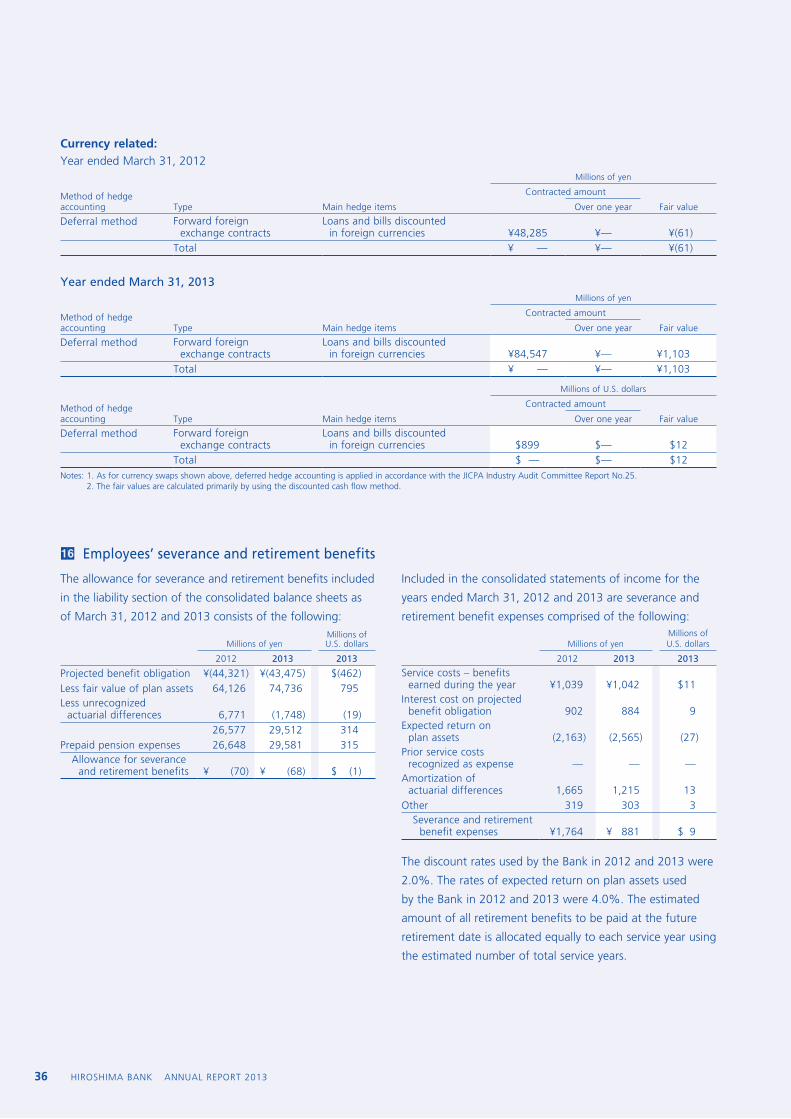

Currency related:Year ended March 31, 2012

Millions of yen

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Forward foreign exchange contracts

Loans and bills discounted in foreign currencies ¥48,285 ¥— ¥(61)

Total ¥ — ¥— ¥(61)

Year ended March 31, 2013Millions of yen

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Forward foreign exchange contracts

Loans and bills discounted in foreign currencies ¥84,547 ¥— ¥1,103

Total ¥ — ¥— ¥1,103

Millions of U.S. dollars

Method of hedge accounting

Contracted amount

Type Main hedge items Over one year Fair value

Deferral method Forward foreign exchange contracts

Loans and bills discounted in foreign currencies $899 $— $12

Total $ — $— $12Notes: 1. As for currency swaps shown above, deferred hedge accounting is applied in accordance with the JICPA Industry Audit Committee Report No.25. 2. The fair values are calculated primarily by using the discounted cash flow method.

16 Employees’ severance and retirement benefits

The allowance for severance and retirement benefits included

in the liability section of the consolidated balance sheets as

of March 31, 2012 and 2013 consists of the following:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Projected benefit obligation ¥(44,321) ¥(43,475) $(462)Less fair value of plan assets 64,126 74,736 795Less unrecognized actuarial differences 6,771 (1,748) (19)

26,577 29,512 314Prepaid pension expenses 26,648 29,581 315

Allowance for severance and retirement benefits ¥ (70) ¥ (68) $ (1)

Included in the consolidated statements of income for the

years ended March 31, 2012 and 2013 are severance and

retirement benefit expenses comprised of the following:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Service costs – benefits earned during the year ¥1,039 ¥1,042 $11Interest cost on projected benefit obligation 902 884 9Expected return on plan assets (2,163) (2,565) (27)Prior service costs recognized as expense — — —Amortization of actuarial differences 1,665 1,215 13Other 319 303 3

Severance and retirement benefit expenses ¥1,764 ¥ 881 $ 9

The discount rates used by the Bank in 2012 and 2013 were

2.0%. The rates of expected return on plan assets used

by the Bank in 2012 and 2013 were 4.0%. The estimated

amount of all retirement benefits to be paid at the future

retirement date is allocated equally to each service year using

the estimated number of total service years.

HIROSHIMA BANK ANNUAL REPORT 2013 37

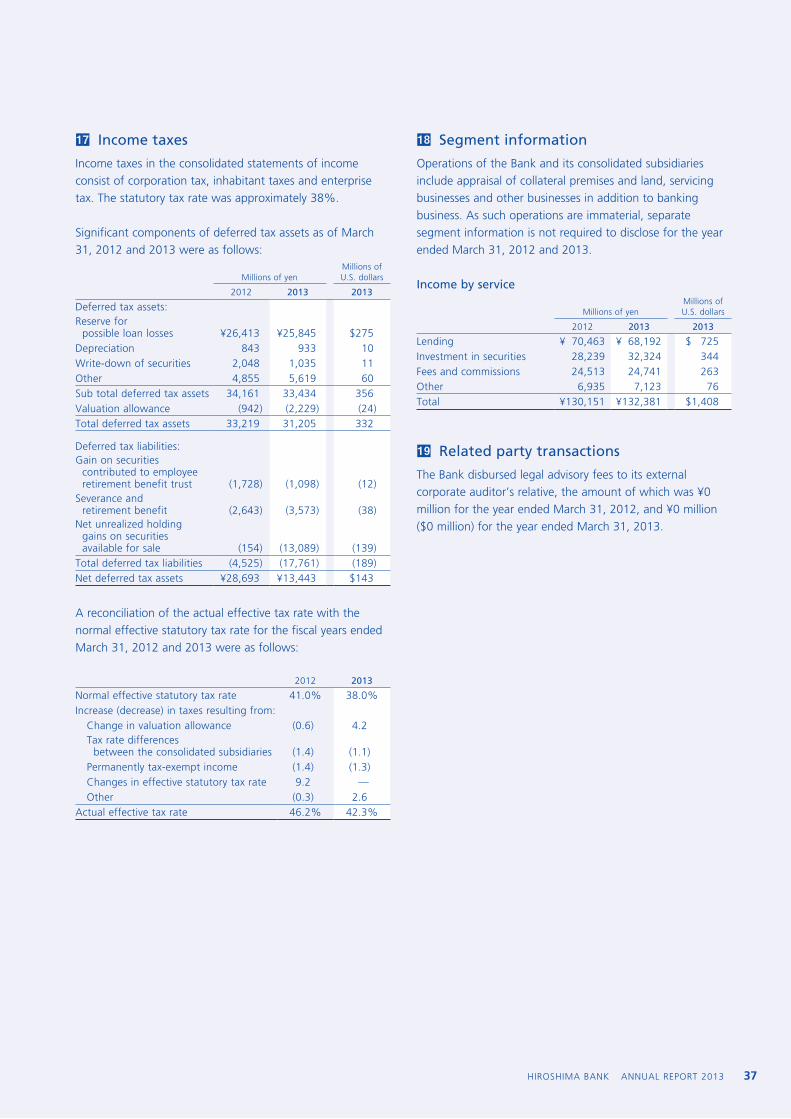

17 Income taxes

Income taxes in the consolidated statements of income consist of corporation tax, inhabitant taxes and enterprise tax. The statutory tax rate was approximately 38%.

Significant components of deferred tax assets as of March 31, 2012 and 2013 were as follows:

Millions of yenMillions of U.S. dollars

2012 2013 2013

Deferred tax assets:Reserve for possible loan losses ¥26,413 ¥25,845 $275Depreciation 843 933 10Write-down of securities 2,048 1,035 11Other 4,855 5,619 60Sub total deferred tax assets 34,161 33,434 356Valuation allowance (942) (2,229) (24)Total deferred tax assets 33,219 31,205 332

Deferred tax liabilities:Gain on securities contributed to employee retirement benefit trust (1,728) (1,098) (12)Severance and retirement benefit (2,643) (3,573) (38)Net unrealized holding gains on securities available for sale (154) (13,089) (139)Total deferred tax liabilities (4,525) (17,761) (189)Net deferred tax assets ¥28,693 ¥13,443 $143

A reconciliation of the actual effective tax rate with the normal effective statutory tax rate for the fiscal years ended March 31, 2012 and 2013 were as follows:

2012 2013

Normal effective statutory tax rate 41.0% 38.0%Increase (decrease) in taxes resulting from:

Change in valuation allowance (0.6) 4.2Tax rate differences between the consolidated subsidiaries (1.4) (1.1)Permanently tax-exempt income (1.4) (1.3)Changes in effective statutory tax rate 9.2 —Other (0.3) 2.6

Actual effective tax rate 46.2% 42.3%

18 Segment information

Operations of the Bank and its consolidated subsidiaries include appraisal of collateral premises and land, servicing businesses and other businesses in addition to banking business. As such operations are immaterial, separate segment information is not required to disclose for the year ended March 31, 2012 and 2013.

Income by service

Millions of yenMillions of U.S. dollars

2012 2013 2013

Lending ¥ 70,463 ¥ 68,192 $ 725Investment in securities 28,239 32,324 344Fees and commissions 24,513 24,741 263Other 6,935 7,123 76Total ¥130,151 ¥132,381 $1,408

19 Related party transactions

The Bank disbursed legal advisory fees to its external corporate auditor’s relative, the amount of which was ¥0 million for the year ended March 31, 2012, and ¥0 million ($0 million) for the year ended March 31, 2013.

HIROSHIMA BANK ANNUAL REPORT 201338

20 Financial instruments and related disclosures

(1) Policy for financial instrumentsThe Bank and its consolidated subsidiaries conduct financial service such as financial instruments transaction, credit guarantee, leasing and credit card services, with banking as their core activity. Among these businesses, core banking operations include fund procurement through deposit-taking and fund management through loans and investment security portfolios. The financial assets and liabilities of the Bank are subject to Asset Liability Management (“ALM,” comprehensive management of assets and liabilities) in such a way as to prevent adverse impact from interest-rate, foreign-exchange and market-value fluctuation.

(2) Nature and extent of risk arising from financial instruments

Loans and bills discounted are primarily provided to domestic institutional and individual customers, in which the Bank is exposed to customer’s credit risk. Securities primarily consist of stocks, bonds and investment trusts held by the Bank for the purposes of building and maintaining good relationships with customers, sole investment objective and held-to-maturity investment objective.

They are exposed to risk of fluctuation in interest rates and prices in the bond/stock markets and in addition, credit risk arising from downgrading of issuer’s credit rating. Borrowed money, Bonds and Commercial papers are exposed to liquidity risk, the risk that the Bank is unable to meet its obligations as they fall due.

The Bank enters into the following derivative transactions, such as currency swaps and forward foreign exchange contracts to meet the financial needs of customers and interest rate swaps for the purpose of optimizing ALM. As part of optimizing ALM, the Bank uses hedge accounting, specifying derivatives such as interest rate swaps as hedging instruments, and loan as hedged items.

(3) Risk management for financial instrumentsCredit risk managementCredit risk is the risk of sustaining losses due to reduction or loss of value of assets due to deteriorating credit circumstances at a borrower.

(Credit screening system)For all major loans made by branches, the Bank has in place a system of rigorous credit-screening carried out by a credit-screening department, which is independent of the sales departments. In addition to establishing teams for each sector, the credit-screening department has established dedicated team to ensure sounder borrower finances and

effective corporate rehabilitation, and also offers support to managements trying to improve operational management.

In evaluating a customer application for a loan, the Bank will give a considered response, in line with “the basic principles prescribed credit” set up by the Board of Directors, turning down any application that runs counter to the law or public morality and taking careful account of profitability and public benefit, in addition to fund use, repayment source, and guarantee and collateral arrangements.

In cases where customers apply for a review of borrowing terms, the Bank will give a considered response taking account of actual circumstances faced by the customer, in line with “the basic principles for facilitation of finance” set up by the Board of Directors. Appropriate and prompt credit screening is carried out after joint appraisal of a customer’s needs and concerns — and not just based on a mechanical, uniform judgment informed only by financial statements and other superficial statistics and industry-specific guidelines.

To strengthen and expand the credit-screening system, the Bank seeks to duly appraise the creditworthiness of a given company through case-by-case credit management and takes continuous measures to improve the credit-screening skills of employees by various kinds of training program.

(Risk management using the credit rating system)The Bank has introduced the credit rating system to give an objective overview of credit risk on loans. Based on financial and other data indicating the level of creditworthiness of the borrower, the Bank has divided borrowers into 12 grades, and continuously monitors changes in credit risk. The Bank then carries out credit risk quantification based on these grades, to assess credit risk on loan assets and set baseline interest rates on loans.

The Bank also accumulates and organizes the data necessary for quantification of credit risks, such as the default rate within each grade and extent of asset recovery from customers in default, and uses highly sophisticated quantification technique to obtain a still more detailed picture of risk-monitored assets.

(Self-assessment of assets)In parallel with the credit rating system, the Bank conducts strict checks into the soundness of loan and other assets through annual assessment. Screening is carried out by particular Bank branches in light of the financial situation faced by the borrower, and the results are checked by the credit-screening department of the Head Office. In addition, the Risk Management Division extracts important

HIROSHIMA BANK ANNUAL REPORT 2013 39

information and conducts a rigorous review of screening due process and accuracy, and the Audit Division carries out the process audit. Based on this self-assessment of assets, in cases where there is no realistic prospect of asset recovery, provisions are made to reserve for possible loan losses to cover the entire value of the sum at risk. This provision is then recorded as a loss for the fiscal year under review. In this way the Bank ensures asset soundness on a continuous basis.

Market risk management( i ) Market risk management systemMarket risk which is associated with change in the value of financial instruments from fluctuations in interest rates, securities prices, foreign exchange rates, and other market-related indices, have an effect on our financial performance. The Bank controls market risk to stabilize earnings by endeavoring to improve and strengthen ALM.

Management of trading account riskWith regard to the trading accounts (for securities and off-balance sheet transactions that target short-term gains on sales or purchases, and trading at the behest of customers), the Bank has special management mechanisms in place to guard against risk, since these transactions differ qualitatively from banking account transactions (involving deposits and loans, investment securities, and related transactions). The Bank has set up designated trading accounts, and is strengthening their management using transparent accounting procedures based on fair value.

For proprietary position dealing, the Bank limits the position by complying with strict rules in terms of position limits and loss-cutting measures. For positions and transactions on behalf of customers, the Bank follows a policy of square positions by fully covering them through the interbank market.

(ii) Quantitative information relating to market risk(a) Financial products for trading purposesThe Bank holds securities and derivative transactions including interest-rate and currency swaps as trading-purpose.

To measure the amount of market risk, the Bank adopts VaR (Value at Risk) using the variance-covariance method (observation period: one year; confidence interval: 99.9%; holding period: one day).

As of March 31, 2013, the entire VaR of the Bank was ¥2 million ($0 million).

(b) Financial products held for other than trading-purposeThe Bank holds various products such as loans, securities, deposits, corporate bonds, and derivatives for other than trading-purpose.

To measure the amount of market risk associated with these products, the Bank uses the VaR method using the variance-covariance method (observation period: one year; confidence interval: 99.9%; holding period: six months for strategic equity investments, three months for securities other than strategic equity investments, and one year for others).

The total VaR as of March 31, 2013 was ¥57,925 million ($616 million). Within liquid deposits, the Bank recognizes interest risks related to deposits left in the Bank for long periods without withdrawal, which are allocated each fiscal period as core deposits. From the fiscal year ended March 31, 2013, the Bank has revised its allocation method for core deposits allocated in each fiscal period.

(c) VaR adequacyThe relationship between the VaR calculated with the model and actual gains and losses data is back-tested. The Bank has confirmed that the calculating model used for these measurements captures market risk with the necessary degree of accuracy.

However, because VaR is a method of measuring the amount of market risk in terms of the probability of a certain event happening based on past statistical variation, it cannot be used for assessing risk in a market environment characterized by abnormal change.

Liquidity risk management The Bank has a structure to conduct liquidity measurements and to secure available reserves over the net cumulative outflow forecasted in an emergency situation.

(4) Fair values of financial instrumentsFair values of financial instruments are based on quoted price in active markets. If quoted price is not available, other rational valuation techniques are used.

Since the calculations of the reasonably calculated prices are implemented under certain conditions and assumptions, the result of calculations would differ if such calculations are made under different conditions and assumptions.

HIROSHIMA BANK ANNUAL REPORT 201340

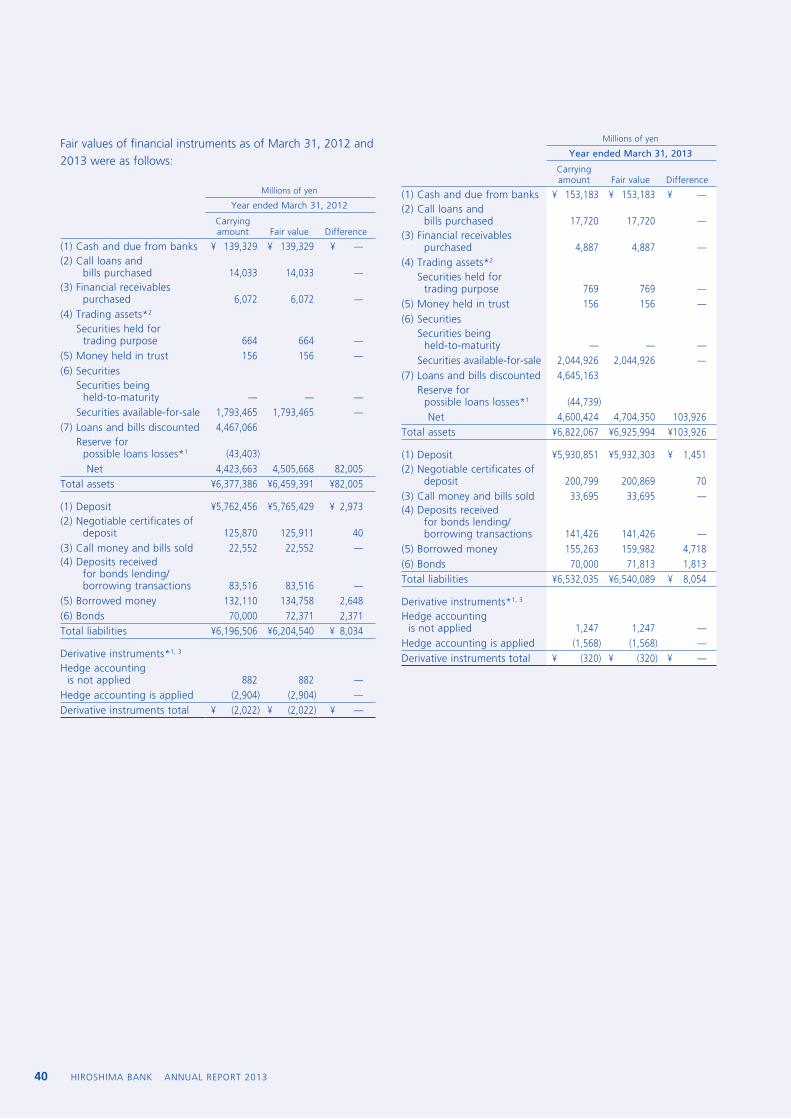

Fair values of financial instruments as of March 31, 2012 and 2013 were as follows:

Millions of yen

Year ended March 31, 2012

Carrying amount Fair value Difference

(1) Cash and due from banks ¥ 139,329 ¥ 139,329 ¥ —(2) Call loans and

bills purchased 14,033 14,033 —(3) Financial receivables

purchased 6,072 6,072 —(4) Trading assets*2

Securities held for trading purpose 664 664 —

(5) Money held in trust 156 156 —(6) Securities

Securities being held-to-maturity — — —Securities available-for-sale 1,793,465 1,793,465 —

(7) Loans and bills discounted 4,467,066Reserve for possible loans losses*1 (43,403)

Net 4,423,663 4,505,668 82,005Total assets ¥6,377,386 ¥6,459,391 ¥82,005

(1) Deposit ¥5,762,456 ¥5,765,429 ¥ 2,973(2) Negotiable certificates of

deposit 125,870 125,911 40(3) Call money and bills sold 22,552 22,552 —(4) Deposits received

for bonds lending/ borrowing transactions 83,516 83,516 —

(5) Borrowed money 132,110 134,758 2,648(6) Bonds 70,000 72,371 2,371Total liabilities ¥6,196,506 ¥6,204,540 ¥ 8,034

Derivative instruments*1, 3

Hedge accounting is not applied 882 882 —Hedge accounting is applied (2,904) (2,904) —Derivative instruments total ¥ (2,022) ¥ (2,022) ¥ —

Millions of yen

Year ended March 31, 2013

Carrying amount Fair value Difference

(1) Cash and due from banks ¥ 153,183 ¥ 153,183 ¥ —(2) Call loans and

bills purchased 17,720 17,720 —(3) Financial receivables

purchased 4,887 4,887 —(4) Trading assets*2

Securities held for trading purpose 769 769 —

(5) Money held in trust 156 156 —(6) Securities

Securities being held-to-maturity — — —Securities available-for-sale 2,044,926 2,044,926 —

(7) Loans and bills discounted 4,645,163Reserve for possible loans losses*1 (44,739)

Net 4,600,424 4,704,350 103,926Total assets ¥6,822,067 ¥6,925,994 ¥103,926

(1) Deposit ¥5,930,851 ¥5,932,303 ¥ 1,451(2) Negotiable certificates of

deposit 200,799 200,869 70(3) Call money and bills sold 33,695 33,695 —(4) Deposits received

for bonds lending/ borrowing transactions 141,426 141,426 —

(5) Borrowed money 155,263 159,982 4,718(6) Bonds 70,000 71,813 1,813Total liabilities ¥6,532,035 ¥6,540,089 ¥ 8,054

Derivative instruments*1, 3

Hedge accounting is not applied 1,247 1,247 —Hedge accounting is applied (1,568) (1,568) —Derivative instruments total ¥ (320) ¥ (320) ¥ —

HIROSHIMA BANK ANNUAL REPORT 2013 41

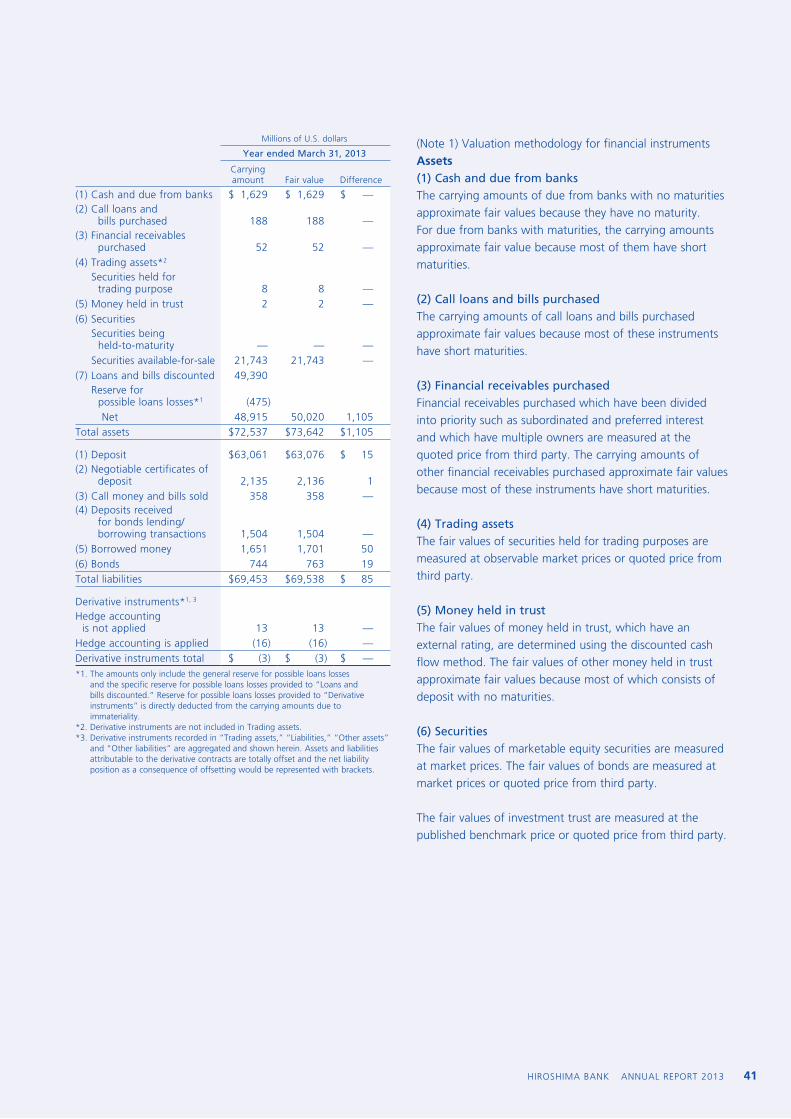

Millions of U.S. dollars

Year ended March 31, 2013

Carrying amount Fair value Difference

(1) Cash and due from banks $ 1,629 $ 1,629 $ —(2) Call loans and

bills purchased 188 188 —(3) Financial receivables

purchased 52 52 —(4) Trading assets*2

Securities held for trading purpose 8 8 —

(5) Money held in trust 2 2 —(6) Securities

Securities being held-to-maturity — — —Securities available-for-sale 21,743 21,743 —

(7) Loans and bills discounted 49,390Reserve for possible loans losses*1 (475)

Net 48,915 50,020 1,105Total assets $72,537 $73,642 $1,105

(1) Deposit $63,061 $63,076 $ 15(2) Negotiable certificates of

deposit 2,135 2,136 1(3) Call money and bills sold 358 358 —(4) Deposits received

for bonds lending/ borrowing transactions 1,504 1,504 —

(5) Borrowed money 1,651 1,701 50(6) Bonds 744 763 19Total liabilities $69,453 $69,538 $ 85

Derivative instruments*1, 3

Hedge accounting is not applied 13 13 —Hedge accounting is applied (16) (16) —Derivative instruments total $ (3) $ (3) $ —*1. The amounts only include the general reserve for possible loans losses

and the specific reserve for possible loans losses provided to “Loans and bills discounted.” Reserve for possible loans losses provided to “Derivative instruments” is directly deducted from the carrying amounts due to immateriality.

*2. Derivative instruments are not included in Trading assets.*3. Derivative instruments recorded in “Trading assets,” “Liabilities,” “Other assets”

and “Other liabilities” are aggregated and shown herein. Assets and liabilities attributable to the derivative contracts are totally offset and the net liability position as a consequence of offsetting would be represented with brackets.

(Note 1) Valuation methodology for financial instrumentsAssets(1) Cash and due from banksThe carrying amounts of due from banks with no maturities approximate fair values because they have no maturity. For due from banks with maturities, the carrying amounts approximate fair value because most of them have short maturities.

(2) Call loans and bills purchasedThe carrying amounts of call loans and bills purchased approximate fair values because most of these instruments have short maturities.

(3) Financial receivables purchasedFinancial receivables purchased which have been divided into priority such as subordinated and preferred interest and which have multiple owners are measured at the quoted price from third party. The carrying amounts of other financial receivables purchased approximate fair values because most of these instruments have short maturities.

(4) Trading assetsThe fair values of securities held for trading purposes are measured at observable market prices or quoted price from third party.

(5) Money held in trustThe fair values of money held in trust, which have an external rating, are determined using the discounted cash flow method. The fair values of other money held in trust approximate fair values because most of which consists of deposit with no maturities.

(6) SecuritiesThe fair values of marketable equity securities are measured at market prices. The fair values of bonds are measured at market prices or quoted price from third party.

The fair values of investment trust are measured at the published benchmark price or quoted price from third party.

HIROSHIMA BANK ANNUAL REPORT 201342

The value reasonably estimated for the such bonds was calculated by the discounting the estimated future cash flows at the rate derived from yields of Japanese government bonds. The yields of Japanese government bonds and volatility are major variables in pricing.

(7) Loans and bills discountedThe fair values of loans and bills discounted are determined by discounting expected cash flows at the rates that would be applied for the new same contract for each type of loan product, interest, period of time and internal ratings-based classification.

For loans to obligors “legally bankrupt,” “virtually bankrupt” and “possibly bankrupt,” since the reserve is provided based on amounts expected to be collected through the disposal of collateral or execution of guarantees, the net carrying amount as of the consolidated balance sheet date is the reasonable estimate of the fair value of those loans.

Loans with no maturities approximate fair values because most of which are without concern of collectability.

Liabilities(1) Deposit, (2) Negotiable certificates of depositThe fair values of demand deposits are recognized as the payment at the date of the consolidated balance sheets. The fair values of time deposit are determined by discounting the contractual cash flows at the rates that would be applied for new same contract.

(3) Call money and bills sold, (4) Deposits received for bonds lending/borrowing transactionsThe carrying amounts of call money and bills sold, deposits received for bonds lending/borrowing transactions approximate fair values, because these instruments are with short maturities.

(5) Borrowed moneyThe fair values of borrowed money are determined by discounting the contractual cash flows at the rate that would be applied for new same contract. The carrying amounts of borrowed money with short maturities approximate fair values.

(6) BondsThe fair values of bonds are measured at quoted price from third party.

Derivative instrumentsThe fair values of derivative instrument are measured at the market prices or determined using the discounted cash flow method or option pricing models.

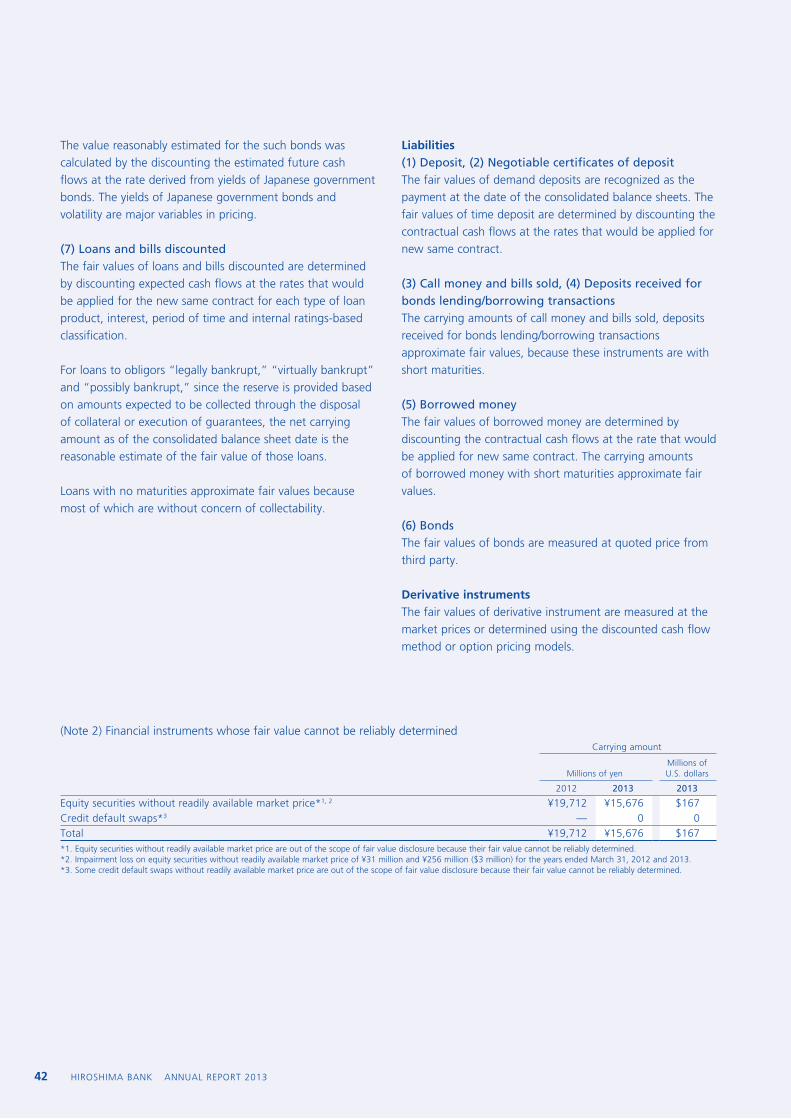

(Note 2) Financial instruments whose fair value cannot be reliably determinedCarrying amount

Millions of yenMillions of U.S. dollars

2012 2013 2013

Equity securities without readily available market price*1, 2 ¥19,712 ¥15,676 $167Credit default swaps*3 — 0 0Total ¥19,712 ¥15,676 $167*1. Equity securities without readily available market price are out of the scope of fair value disclosure because their fair value cannot be reliably determined.*2. Impairment loss on equity securities without readily available market price of ¥31 million and ¥256 million ($3 million) for the years ended March 31, 2012 and 2013.*3. Some credit default swaps without readily available market price are out of the scope of fair value disclosure because their fair value cannot be reliably determined.

HIROSHIMA BANK ANNUAL REPORT 2013 43

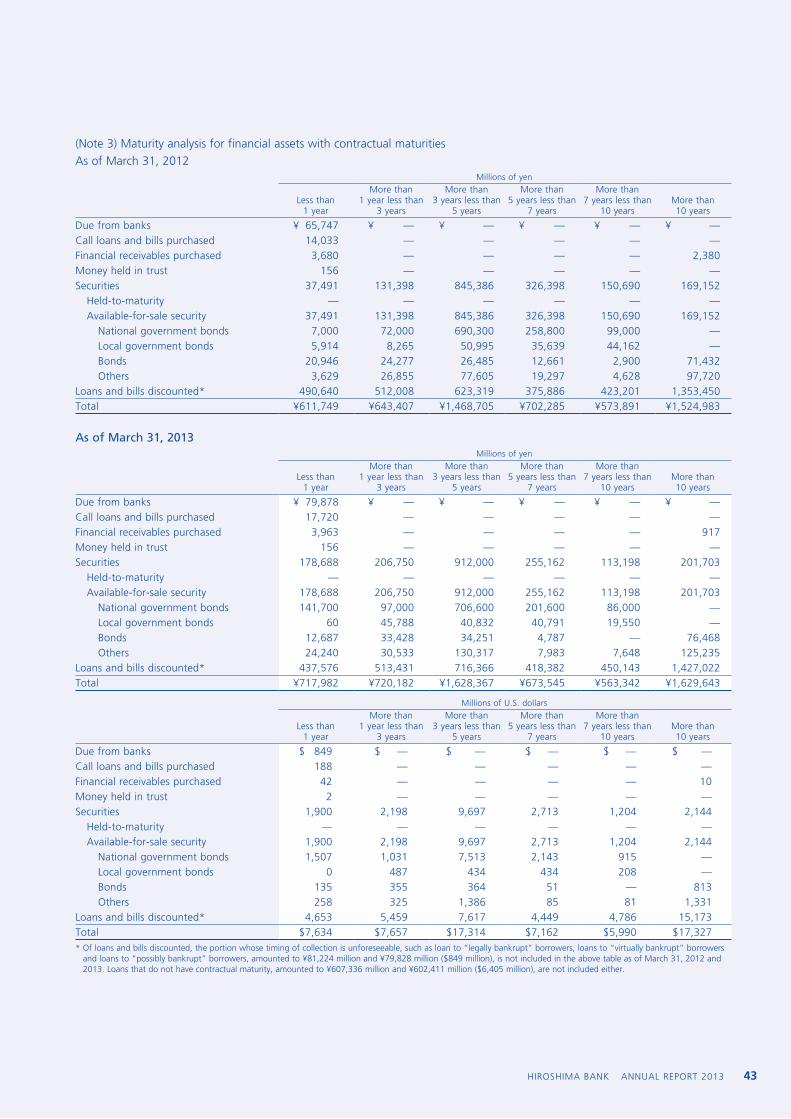

(Note 3) Maturity analysis for financial assets with contractual maturities As of March 31, 2012

Millions of yen

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Due from banks ¥ 65,747 ¥ — ¥ — ¥ — ¥ — ¥ —Call loans and bills purchased 14,033 — — — — —Financial receivables purchased 3,680 — — — — 2,380Money held in trust 156 — — — — —Securities 37,491 131,398 845,386 326,398 150,690 169,152

Held-to-maturity — — — — — —Available-for-sale security 37,491 131,398 845,386 326,398 150,690 169,152

National government bonds 7,000 72,000 690,300 258,800 99,000 —Local government bonds 5,914 8,265 50,995 35,639 44,162 —Bonds 20,946 24,277 26,485 12,661 2,900 71,432Others 3,629 26,855 77,605 19,297 4,628 97,720

Loans and bills discounted* 490,640 512,008 623,319 375,886 423,201 1,353,450Total ¥611,749 ¥643,407 ¥1,468,705 ¥702,285 ¥573,891 ¥1,524,983

As of March 31, 2013Millions of yen

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Due from banks ¥ 79,878 ¥ — ¥ — ¥ — ¥ — ¥ —Call loans and bills purchased 17,720 — — — — —Financial receivables purchased 3,963 — — — — 917Money held in trust 156 — — — — —Securities 178,688 206,750 912,000 255,162 113,198 201,703

Held-to-maturity — — — — — —Available-for-sale security 178,688 206,750 912,000 255,162 113,198 201,703

National government bonds 141,700 97,000 706,600 201,600 86,000 —Local government bonds 60 45,788 40,832 40,791 19,550 —Bonds 12,687 33,428 34,251 4,787 — 76,468Others 24,240 30,533 130,317 7,983 7,648 125,235

Loans and bills discounted* 437,576 513,431 716,366 418,382 450,143 1,427,022Total ¥717,982 ¥720,182 ¥1,628,367 ¥673,545 ¥563,342 ¥1,629,643

Millions of U.S. dollars

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Due from banks $ 849 $ — $ — $ — $ — $ —Call loans and bills purchased 188 — — — — —Financial receivables purchased 42 — — — — 10Money held in trust 2 — — — — —Securities 1,900 2,198 9,697 2,713 1,204 2,144

Held-to-maturity — — — — — —Available-for-sale security 1,900 2,198 9,697 2,713 1,204 2,144

National government bonds 1,507 1,031 7,513 2,143 915 —Local government bonds 0 487 434 434 208 —Bonds 135 355 364 51 — 813Others 258 325 1,386 85 81 1,331

Loans and bills discounted* 4,653 5,459 7,617 4,449 4,786 15,173Total $7,634 $7,657 $17,314 $7,162 $5,990 $17,327* Of loans and bills discounted, the portion whose timing of collection is unforeseeable, such as loan to “legally bankrupt” borrowers, loans to “virtually bankrupt” borrowers

and loans to “possibly bankrupt” borrowers, amounted to ¥81,224 million and ¥79,828 million ($849 million), is not included in the above table as of March 31, 2012 and 2013. Loans that do not have contractual maturity, amounted to ¥607,336 million and ¥602,411 million ($6,405 million), are not included either.

HIROSHIMA BANK ANNUAL REPORT 201344

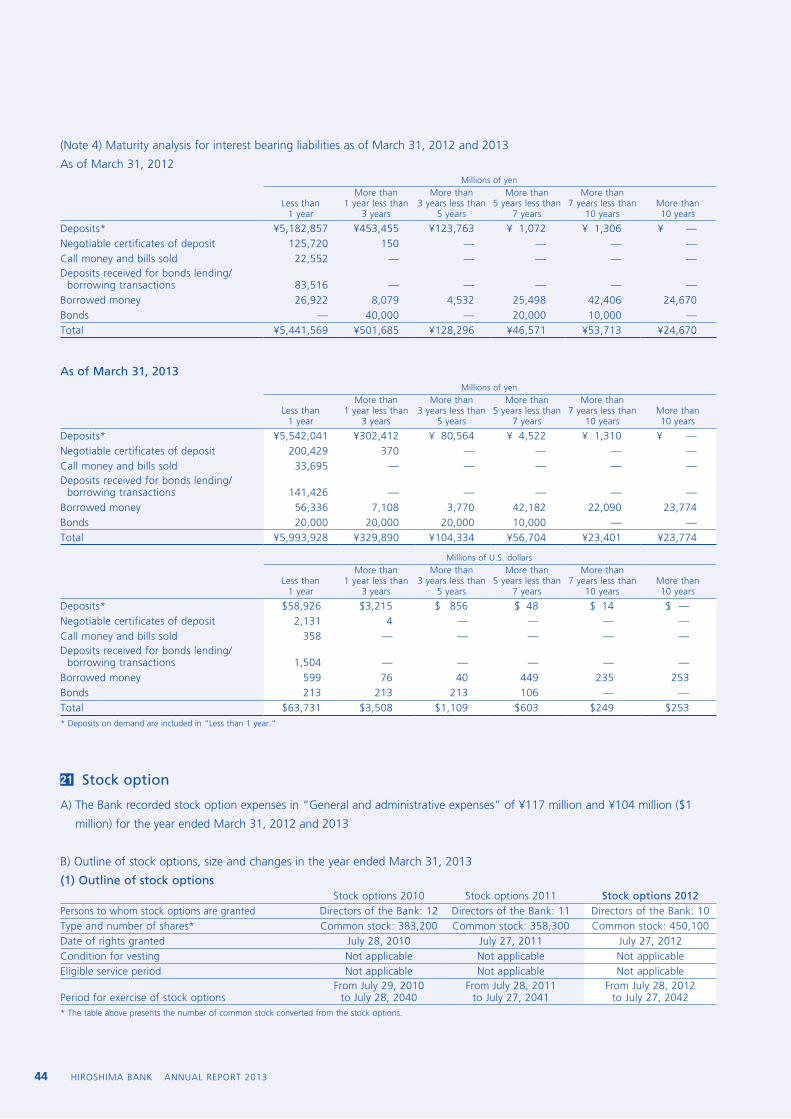

(Note 4) Maturity analysis for interest bearing liabilities as of March 31, 2012 and 2013

As of March 31, 2012Millions of yen

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Deposits* ¥5,182,857 ¥453,455 ¥123,763 ¥ 1,072 ¥ 1,306 ¥ —Negotiable certificates of deposit 125,720 150 — — — —Call money and bills sold 22,552 — — — — —Deposits received for bonds lending/ borrowing transactions 83,516 — — — — —Borrowed money 26,922 8,079 4,532 25,498 42,406 24,670Bonds — 40,000 — 20,000 10,000 —Total ¥5,441,569 ¥501,685 ¥128,296 ¥46,571 ¥53,713 ¥24,670

As of March 31, 2013Millions of yen

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Deposits* ¥5,542,041 ¥302,412 ¥ 80,564 ¥ 4,522 ¥ 1,310 ¥ —Negotiable certificates of deposit 200,429 370 — — — —Call money and bills sold 33,695 — — — — —Deposits received for bonds lending/ borrowing transactions 141,426 — — — — —Borrowed money 56,336 7,108 3,770 42,182 22,090 23,774Bonds 20,000 20,000 20,000 10,000 — —Total ¥5,993,928 ¥329,890 ¥104,334 ¥56,704 ¥23,401 ¥23,774

Millions of U.S. dollars

Less than 1 year

More than 1 year less than

3 years

More than 3 years less than

5 years

More than 5 years less than

7 years

More than 7 years less than

10 yearsMore than 10 years

Deposits* $58,926 $3,215 $ 856 $ 48 $ 14 $ —Negotiable certificates of deposit 2,131 4 — — — —Call money and bills sold 358 — — — — —Deposits received for bonds lending/ borrowing transactions 1,504 — — — — —Borrowed money 599 76 40 449 235 253Bonds 213 213 213 106 — —Total $63,731 $3,508 $1,109 $603 $249 $253* Deposits on demand are included in “Less than 1 year.”

21 Stock option

A) The Bank recorded stock option expenses in “General and administrative expenses” of ¥117 million and ¥104 million ($1

million) for the year ended March 31, 2012 and 2013

B) Outline of stock options, size and changes in the year ended March 31, 2013

(1) Outline of stock optionsStock options 2010 Stock options 2011 Stock options 2012

Persons to whom stock options are granted Directors of the Bank: 12 Directors of the Bank: 11 Directors of the Bank: 10Type and number of shares* Common stock: 383,200 Common stock: 358,300 Common stock: 450,100Date of rights granted July 28, 2010 July 27, 2011 July 27, 2012 Condition for vesting Not applicable Not applicable Not applicableEligible service period Not applicable Not applicable Not applicable

Period for exercise of stock optionsFrom July 29, 2010

to July 28, 2040From July 28, 2011

to July 27, 2041From July 28, 2012

to July 27, 2042* The table above presents the number of common stock converted from the stock options.

HIROSHIMA BANK ANNUAL REPORT 2013 45

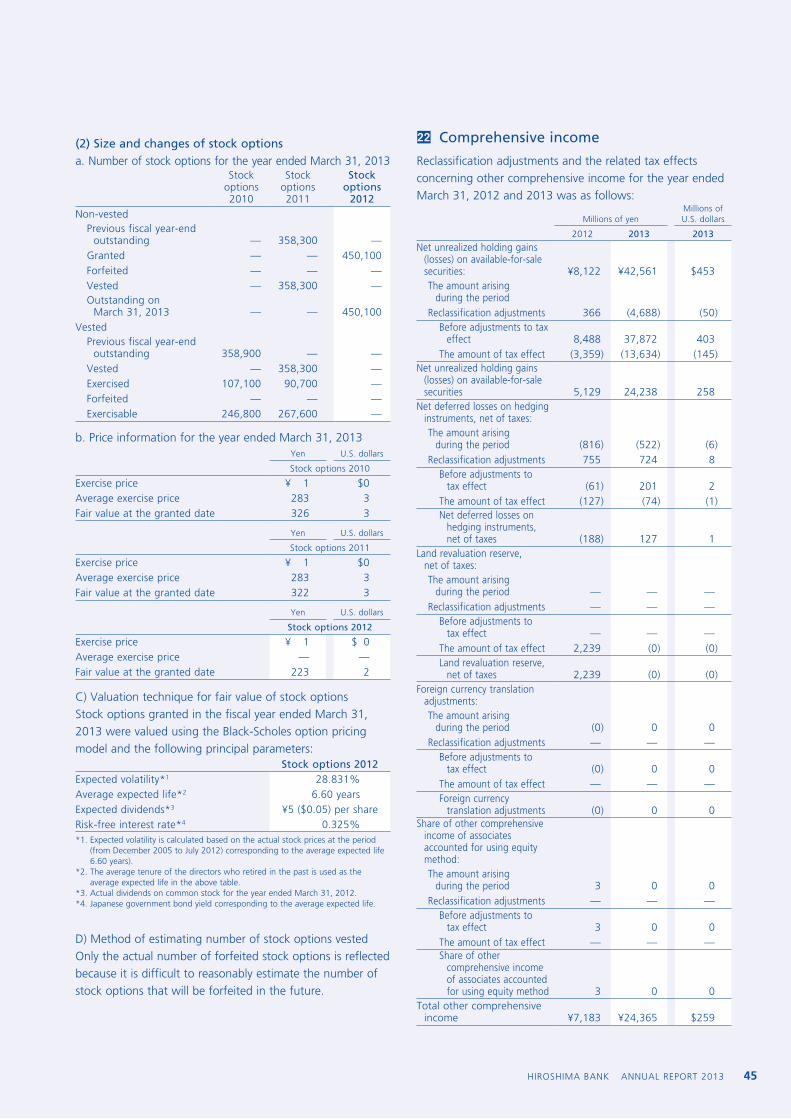

(2) Size and changes of stock optionsa. Number of stock options for the year ended March 31, 2013

Stock options 2010

Stock options 2011

Stock options

2012Non-vested

Previous fiscal year-end outstanding — 358,300 —Granted — — 450,100Forfeited — — —Vested — 358,300 —Outstanding on March 31, 2013 — — 450,100

VestedPrevious fiscal year-end outstanding 358,900 — —Vested — 358,300 —Exercised 107,100 90,700 —Forfeited — — —Exercisable 246,800 267,600 —

b. Price information for the year ended March 31, 2013Yen U.S. dollars

Stock options 2010

Exercise price ¥ 1 $0Average exercise price 283 3Fair value at the granted date 326 3

Yen U.S. dollars

Stock options 2011

Exercise price ¥ 1 $0Average exercise price 283 3Fair value at the granted date 322 3

Yen U.S. dollars

Stock options 2012

Exercise price ¥ 1 $ 0Average exercise price — —Fair value at the granted date 223 2

C) Valuation technique for fair value of stock optionsStock options granted in the fiscal year ended March 31, 2013 were valued using the Black-Scholes option pricing model and the following principal parameters:

Stock options 2012Expected volatility*1 28.831%Average expected life*2 6.60 yearsExpected dividends*3 ¥5 ($0.05) per shareRisk-free interest rate*4 0.325%*1. Expected volatility is calculated based on the actual stock prices at the period

(from December 2005 to July 2012) corresponding to the average expected life 6.60 years).

*2. The average tenure of the directors who retired in the past is used as the average expected life in the above table.

*3. Actual dividends on common stock for the year ended March 31, 2012.*4. Japanese government bond yield corresponding to the average expected life.

D) Method of estimating number of stock options vestedOnly the actual number of forfeited stock options is reflected because it is difficult to reasonably estimate the number of stock options that will be forfeited in the future.

22 Comprehensive income

Reclassification adjustments and the related tax effects concerning other comprehensive income for the year ended March 31, 2012 and 2013 was as follows:

Millions of yenMillions of U.S. dollars

2012 2013 2013Net unrealized holding gains

(losses) on available-for-sale securities: ¥8,122 ¥42,561 $453The amount arising

during the periodReclassification adjustments 366 (4,688) (50)

Before adjustments to tax effect 8,488 37,872 403

The amount of tax effect (3,359) (13,634) (145)Net unrealized holding gains

(losses) on available-for-sale securities 5,129 24,238 258

Net deferred losses on hedging instruments, net of taxes:The amount arising

during the period (816) (522) (6)Reclassification adjustments 755 724 8

Before adjustments to tax effect (61) 201 2

The amount of tax effect (127) (74) (1)Net deferred losses on

hedging instruments, net of taxes (188) 127 1

Land revaluation reserve, net of taxes:The amount arising

during the period — — —Reclassification adjustments — — —

Before adjustments to tax effect — — —

The amount of tax effect 2,239 (0) (0)Land revaluation reserve,

net of taxes 2,239 (0) (0)Foreign currency translation

adjustments:The amount arising

during the period (0) 0 0Reclassification adjustments — — —

Before adjustments to tax effect (0) 0 0

The amount of tax effect — — —Foreign currency

translation adjustments (0) 0 0Share of other comprehensive

income of associates accounted for using equity method:The amount arising

during the period 3 0 0Reclassification adjustments — — —

Before adjustments to tax effect 3 0 0

The amount of tax effect — — —Share of other

comprehensive income of associates accounted for using equity method 3 0 0

Total other comprehensive income ¥7,183 ¥24,365 $259