Embed Size (px)

DESCRIPTION

On 9 May 2005, a group of experts from a wide variety of backgrounds assembled to discuss the impact of the new mandatory operating and financial review (OFR) on companies’ sustainability practices and reporting. The specific issue of sustainability was chosen because many companies will find collecting and reporting information about sustainability–related issues a challenge. Please read this report to find out more.

Citation preview

OFR and Sustainability RoundtableExamining the impact of the OFR on sustainable

development and corporate reporting

Technical Report

supported by

Writers:Danka Starovic CIMADr Arlo Brady Mott MacDonald Group and Judge Institute of Management

Contact:[email protected]

Copyright © CIMA 2005First published in 2005 by:The Chartered Institute of Management Accountants26 Chapter StreetLondon SW1P 4NP

The publishers of this document consider that it is a worthwhile contribution to discussion,without necessarily sharing the views expressed.

No responsibility for loss occasioned to any person acting or refraining fromaction as a result of any material in this publication can be accepted by the authorsor the publishers.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system,or transmitted, in any form or by any means method or device, electronic (whether now orhereafter known or developed), mechanical, photocopying, recorded or otherwise, withoutthe prior permission of the publishers.

Translation requests should be submitted to CIMA.

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

● The OFR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

● The Roundtable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

● Aims of the report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

List of participants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

OFR content and key performance indicators . . . . . . . . . . . . . . . . . . . 8

● Quantitative and qualitative information . . . . . . . . . . . . . . . . . . . . . . . 8

Investors and investor pressure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

● Investor engagement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

● Do equity analysts care about the OFR? . . . . . . . . . . . . . . . . . . . . . . . . 10

● Evolving measures of performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

● Are all investors the same? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

CSR reports and the OFR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

● OFR, CSR or both? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

● What belongs where? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

● Shareholders vs stakeholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

● Stakeholder engagement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Suggested reading . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Contents 1

Contents

Introduction

On 9 May 2005, a group of experts from a wide variety of backgrounds assembled todiscuss the impact of the new mandatory Operating and Financial Review (OFR) oncompanies’ sustainability practices and reporting.

The specific issue of sustainability was chosen because many companies will findcollecting and reporting information about sustainability–related issues a challenge.

In addition, although the OFR is addressed to the members of the company, theinformation will also be of relevance to other stakeholders. It is therefore an area wherethere could be conflict between the directors’ judgement of what is material andstakeholders’ demands for transparency.

There is also the problem of how the OFR will relate to existing sustainability orCorporate Social Responsibility (CSR) reports which are produced by a number ofcompanies, particularly in the FTSE100.

The debate highlighted the following issues:

Quantitative and qualitative informationThe OFR should contain both types of information but it would be futile to prescribe thebalance between the two. In some cases, it may prove particularly difficult to developquantitative indicators.

There is a danger that greater weight is given to quantitative information on the basisthat it is perceived to convey a greater degree of accuracy than a narrative report.Weshould get used to the idea that qualitative information, though potentially imprecise,can be very useful when assessing strategic performance.

Investors and investor pressureOne of the main drivers for the evolution of the OFR will be investor involvement.Theextent to which information in existing CSR reports will appear in the OFR will depend onthe level of interest shown by investors.

There was concern that equity analysts would ignore the OFR because of timing issues.By the time the annual report appears, the information it contains is largely old news foranalysts who have had the benefit of face-to-face meetings with companies at an earlierstage.This may need to be addressed in future, perhaps by including the OFR with thepreliminary statements. Nevertheless, even if the OFR is not widely read by analysts, theprocess of preparation will help to generate a better flow of information betweencompanies and investors.

Executive summary 2

Executive summary

In addition, it should be remembered that different types of investors have different kindsof mandates and there is a growing number of specialist governance and sociallyresponsible investment (SRI) analysts. Companies will have to give considerable thoughtas to the specific audience for the report.

In terms of selection of key performance indicators (KPIs), a balance has to be struckbetween consistency and comparability on the one hand and the need to develop newKPIs to reflect the dynamic nature of business.This is where the narrative sections of theOFR can be useful in explaining KPI choices and any changes from previous years.

CSR reports and the OFRCompanies that already produce a CSR report are likely to continue to do so.Althoughsome overlap is inevitable, the reports are aimed at different audiences and thereforerequire different approaches for preparation and assurance.The main issue is theinterrelation of the two reports, both in terms of content and the process of preparation.

For the OFR, boards should select the two or three sustainability issues that are trulyrelevant for overall strategy and report on those. In some cases, it might be appropriateto select long-term issues that could have a serious impact on the company’s futurestrategy.

A key difference between the CSR report and the OFR is that the former is anunregulated communications format which permits exploration of various issues.Thesemight be inappropriate for the OFR which requires consistency and comparability.

Shareholders vs stakeholdersTo a degree, the shareholder/stakeholder dichotomy is misleading in that companiesproduce CSR reports for a reason – they believe that they will ultimately createshareholder value.

Although not aimed directly at investors, the CSR report may be a useful source ofinformation for them.An issue that may at first sight appear irrelevant to shareholdersand of concern only to a narrow stakeholder group, may in fact turn out to be an earlyindicator of something that will impact long-term shareholder value.

Companies might need to conduct stakeholder engagement work to determine whatkinds of KPIs should be included in OFRs.The costs and benefits of this need to beconsidered carefully. Ultimately, the OFR is aimed at members of the company andshould focus on information that is strategically relevant.

Executive summary 3

Conclusions

● The OFR needs to be a part of mainstream corporate reporting. Both companies andinvestors need to ensure that it fulfils its mandatory remit and potential to improvethe transparency of corporate reporting.

● In time, we should hopefully see convergence of good practice which will allowcomparability and consistency.

● Business needs to pay attention to stakeholder opinion for reputational reasons aswell as to meet the needs of its customers. However, the OFR is aimed at membersof the company and should not be cluttered with information that is notstrategically relevant. ‘Taking account of’ is not the same as‘being held accountable to’.

● The publication of the OFR may be an opportune time for companies to stand backand review the entirety of their corporate communications package in order toensure overall coherence. As the length of various reports increases, it becomes evenmore important to have ‘read across’ between different sections.

Once the first round of OFRs is published, companies may also find it useful to seekfeedback from users in order to make sure the report is meeting their needs.

Executive summary 4

The OFR

There is no shortage of opinions about the Operating and Financial Review (OFR). Acresof newspaper print and a glut of seminars, conferences and presentations have beendevoted to it in recent years.The Conservative Party even made it a part of their electionmanifesto in 2005, vowing to scrap the mandatory requirement as part of itsderegulation package for business. One Labour victory later, the mandatory OFR is still inplace and all listed companies now have to comply for financial years that began on orafter 1 April 2005.

At the heart of the OFR is a desire to improve transparency in corporate reporting. It ismeant to provide information to ‘assist members of the company to assess the strategiesadopted by the entity and the potential for those strategies to succeed’.This includes thenature, development and performance of the business, as well as the resources, principalrisks and uncertainties that may affect it. (ASB, 2005).

Although the OFR is not new – many large companies have been producing theirs for awhile – it seems that the UK business leaders remain split over its benefits. Researchconducted by MORI in May this year shows that some 43 per cent support it and 48 percent oppose it.

Part of the reason the OFR is proving to be so contentious is undoubtedly therequirement to report – ‘to the extent necessary’ – on environmental, employee,community and social issues.

Up until now, if a company felt the need to report on its environmental or socialperformance, it did so on a voluntary basis, mainly through so-called CSR/sustainabilityreports.There has been little legislative pressure (in the UK) and, as a result, there are stillrelatively few British companies who do report. In the main, sustainability reporting isrestricted to the ‘usual suspects’, and the quality, coverage and size of their reports ishighly variable.

One can therefore assume that the majority of some 1400 listed UK companies may nothave mechanisms in place for collecting and reporting relevant information and maytherefore struggle with OFR preparation.

Introduction 5

Introduction

The Roundtable

Some 24 hours before the Accounting Standards Board (ASB) issued the final OFRStandard, a group of experts from a wide variety of backgrounds – financial controllers,investment managers, risk experts and CSR specialists – assembled to discuss the impactof the OFR on companies’ sustainability practices and reporting.The event was chairedby Dr Arlo Brady, a research associate at the Judge Institute of Management.

Why did we choose sustainability in particular?In many ways, sustainability or corporate social responsibility has been the most visiblepart of companies’ attempts at non-financial reporting.There might not be many CSRreports, especially not outside the FTSE100, but the fact that they exist at all is atestament to the growing importance of the subject matter.

Some companies have been forced to publish their reports as a result of public scrutinyand pressure from NGOs or single-issue campaigners. Others, such as Co-operativeFinancial Services (CFS), have used CSR strategically, thereby creating uniquecompetitive advantage.

But for the majority, collecting and reporting information about sustainability-relatedissues will undoubtedly be a challenge.They will have to start from scratch and considerthe processes they need to put into place to make it happen – from how to collect therelevant information to who within the company is responsible for its accuracy.

In addition, although the OFR is addressed to the members of the company, the ASBstandard states that the information disclosed in it will be of relevance to otherstakeholders. It also states that the OFR ‘should not, however, be seen as a replacementfor other forms of reporting addressed to a wider stakeholder group.’

No one knows how those stakeholders will react to the first round of OFRs but it is anarea where we could potentially see conflict between directors’ judgement of what ismaterial and stakeholders’ demands for transparency. More clarity about expectationsmay be needed on both sides.

Aims of the report

The aim of this brief report is to provide some basic background on the OFRrequirements – detailed information is available elsewhere and we list some of the mainsources on page 17 – and to summarise the discussions that took place on 9 May.

We hope the reported dialogue highlights some of the issues that companies, investorsand CSR specialists may face after OFRs are published. In particular, we hope it alerts allthe participants to particular areas of importance or those that may be ripe formisunderstandings or conflict.

Introduction 6

List of participants 7

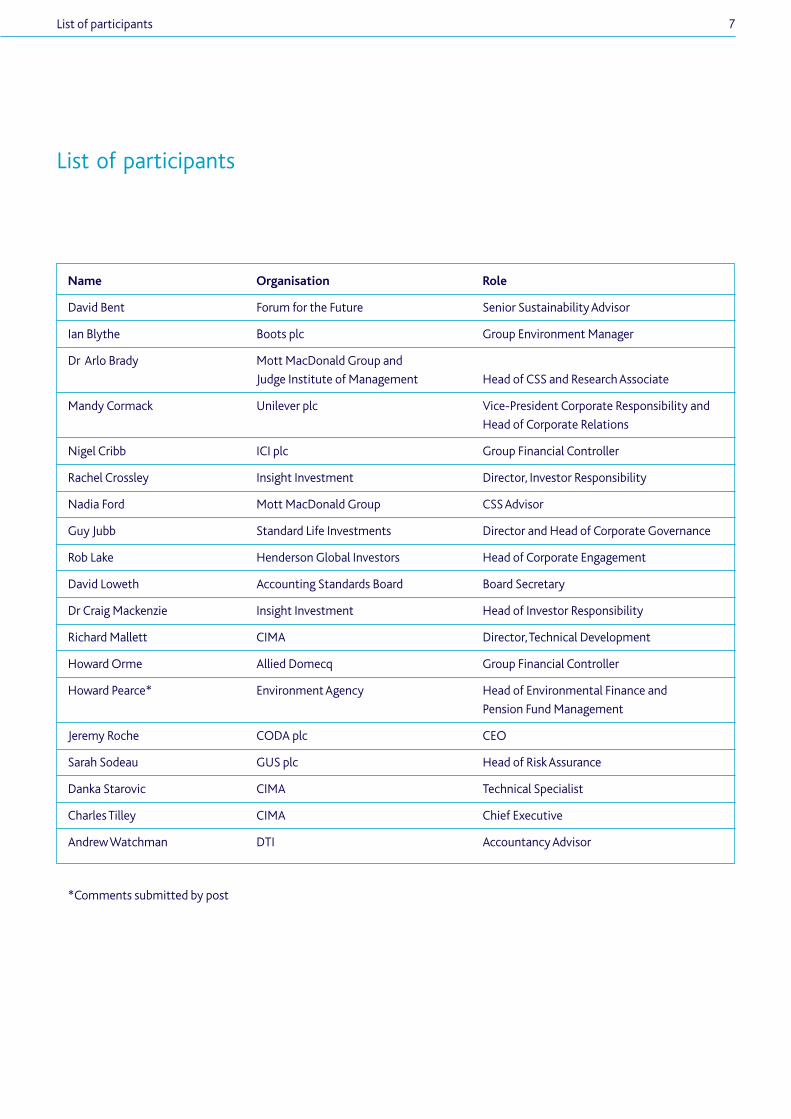

Name Organisation Role

David Bent Forum for the Future Senior Sustainability Advisor

Ian Blythe Boots plc Group Environment Manager

Dr Arlo Brady Mott MacDonald Group and

Judge Institute of Management Head of CSS and Research Associate

Mandy Cormack Unilever plc Vice-President Corporate Responsibility and

Head of Corporate Relations

Nigel Cribb ICI plc Group Financial Controller

Rachel Crossley Insight Investment Director, Investor Responsibility

Nadia Ford Mott MacDonald Group CSS Advisor

Guy Jubb Standard Life Investments Director and Head of Corporate Governance

Rob Lake Henderson Global Investors Head of Corporate Engagement

David Loweth Accounting Standards Board Board Secretary

Dr Craig Mackenzie Insight Investment Head of Investor Responsibility

Richard Mallett CIMA Director,Technical Development

Howard Orme Allied Domecq Group Financial Controller

Howard Pearce* Environment Agency Head of Environmental Finance and

Pension Fund Management

Jeremy Roche CODA plc CEO

Sarah Sodeau GUS plc Head of Risk Assurance

Danka Starovic CIMA Technical Specialist

Charles Tilley CIMA Chief Executive

Andrew Watchman DTI Accountancy Advisor

*Comments submitted by post

List of participants

Because the participants came from such a wide variety of backgrounds, the debate

about the OFR content focused on fairly general themes rather than the specifics of

individual companies’ performance.

Quantitative and qualitative information

One of the first issues to be discussed was whether the OFR should contain

predominantly quantitative or qualitative information. Unsurprisingly, the answer was

both – whichever is chosen depends on the issue in question.

In some cases, according to Rob Lake from Henderson Global Investors, when reporting

environmental performance in an area such as greenhouse gas emissions, most of the

data will be quantitative and historical by definition. But the discussion about the main

environmental trends or factors likely to affect the company’s future development and

the board’s view about the future significance of emissions may well be purely

qualitative. For example, a company may choose to outline the steps it intends to take to

reduce its gas emissions; that is likely to be a narrative report rather than another set of

numbers.

Similarly, methodologies for capturing and reporting data may already be relatively well

established for some issues, such as reporting on waste emissions.They may simply need

a bit of tweaking to make them suitable for inclusion in the OFR.

But with others, such as the ‘softer’ issues around human capital, it could be difficult, or

even impossible, to develop quantitative indicators, at least not for the first cycle of the

OFR. It is therefore futile trying to predict in advance what the OFR may look like or

prescribe that a certain percentage of it should be quantitative or qualitative.

There was a warning, however, not to give greater weight to quantitative reports on the

basis that they convey a greater degree of accuracy than a narrative.According to David

Bent from Forum for the Future, this could lead companies to downgrade all future

information and rely purely on historical, quantitative data.And that is exactly what the

OFR is trying to avoid.

‘I think we should not tripourselves up right at thestart by saying thatquantitative is much betterthan qualitative.’

David Bent,

Forum for the Future

OFR content and KPIs

OFR content and KPIs 8

OFR content and KPIs 9

Instead, we should get used to the idea that qualitative information, though potentially

imprecise, can be useful when assessing strategic performance.

Dr Craig Mackenzie from Insight Investment added that he understood the OFR to be

about telling a convincing story to shareholders. If that is the case, then the story needs

to be illustrated with evidence which will undoubtedly include numbers. Put simply, it is

one thing to claim to have high levels of customer satisfaction but quite another to have

data to prove it.

In reality, very few issues are likely to be separable into clearly quantitative or clearly

qualitative information.While producing a report that is predominantly one or the other

is not in any way illegal, eventually shareholders will voice their opinion about the nature

of the information provided.

Investor engagement

The ASB Reporting Standard for the OFR spells out a principle that the ‘OFR shall focus onmatters that are relevant to the interests of the members’. It also states that ‘Members’needs are paramount when directors consider what information shall be contained in theOFR’. (ASB, 2005).

According to Andrew Watchman from the DTI, one of the main drivers for the evolutionof the OFR should be investor involvement. Indeed, the extent to which the informationthat now sits in CSR reports will find its way into the mainstream OFR will in largemeasure depend on the amount of interest shown by investors.

Notwithstanding the different perspectives of different types of investor – a subject thedebate touched upon later – companies will need to put themselves in the shoes of areasonable and diligent investor and try to figure out what the notional person actuallywants.And if it is thought that they really want the added comprehensiveness of a CSRreport, then companies will have to respond accordingly.

Do equity analysts care about the OFR?

There was some concern, however, that equity analysts will ignore the OFR altogether.This runs the risk of making the document itself superfluous and the cost of producing ita regulatory burden.

The importance of analysts lies in their role as the first link in the corporate reportingsupply chain. In a sense, they are almost proxy investors as they publishrecommendations and valuations of companies’ shares that may affect their trade andtherefore price.

Their recommendations are based on various sources of information, including thecompanies’ preliminary results as well as broker reports which in effect ‘pre-digest’anything likely to be new and/or interesting in the annual report.

In addition, during their face-to-face meetings with companies, analysts receive muchmore than just the update on financial results.They obtain information about thecompany’s future strategy and an opportunity to form their own perceptions about thequality of management thinking and the competence of executives.They are also likelyto see some of the KPIs that may later appear in the OFR. Research (Holland, 2002) hasconfirmed that for analysts, these private meetings are an opportunity to ‘look into thewhites of managers’ eyes’ and challenge them on different issues, sometimes quiterobustly.

However, this also means that by time the annual report comes out, it is largely old news.Most of the information it contains has already been circulated and reflected in thecompany’s share price. Both Rob Lake and Craig Mackenzie insisted that the OFRpublication is therefore unlikely to greatly – if at all – improve the quality of analysts’access to information or their resulting perception of the business.

‘Hopefully, one of the maindrivers for a positiveevolution in the qualitativefactors will be engagementwith investors.The extent towhich information – the vastpart of which is in CSRreports already – will find itsway into the mainstreamOFR will in large measurecome down to how muchinterest investors really showin this type of information.’

Andrew Watchman,

DTI

‘Frankly, the vast majority ofanalysts who do the numbercrunching will completelyignore the OFR.’

Dr Craig Mackenzie,

Insight Investment

Investors and investor pressure

Investors and investor pressure 10

Investors and investor pressure 11

Charles Tilley, an advocate of the OFR’s potential to improve the quality andtransparency of corporate reporting, thought that this was a ‘terrifying’ prospect. Headded that, considering the annual report and the OFR come at the end of a process bywhich the relevant information gets disseminated to key users, then perhaps the issue oftiming needs to be addressed in the future.The OFR might need to be attached topreliminary statements so that analysts receive all the relevant information togetherwith the financial update.

Dr Mackenzie pointed out that, even if the report itself is not widely read by analysts, theprocess of preparation will help to generate a better flow of information betweencompanies and investors.

First and foremost, the OFR will help with what he calls ‘story-making’ because it willcreate a more structured context for corporate communication.

Companies will be forced to organise their thinking about strategy in a way that makessense to shareholders by considering what they choose to communicate and when, andhow they can improve their story to make it more convincing.With the OFR as abackdrop, there is an opportunity to make all investor communication consistent.

Evolving measures of performance

As Andrew Watchman from the DTI pointed out, there is currently nothing to stop acompany reporting one set of KPIs in a presentation to, say, analysts, but a completelydifferent set to a different audience at a different time.With the OFR as the frameworkfor investor scrutiny, it is going to become much harder to get away with selective andinconsistent reporting.

However, there was some concern amongst the rountable companies that reporting astatic set of KPIs implies the business never changes – which is clearly not the case intoday’s dynamic competitive environment. Mandy Cormack said that, for example,Unilever’s health and safety performance indicators keep evolving.Although this makescomparisons difficult, Unilever’s rationale for doing it is that it is committed to safety ofits employees and contractors. If it can implement a better way of monitoring it, it willnot hesitate to do so even if it runs the risk of inconsistency.

Clearly, this is one area where quantitative information such as historical indicators hasto be put in a wider context.A narrative can be used to explain and justify KPI choices andany changes from previous years.

Howard Orme reminded the panel that the market will not let you ‘chop and change’KPIs willy-nilly and that doing so would constitute ‘investor relations suicide’. In otherwords, there is a certain amount of market rather than legislative pressure againstinconsistency.

Howard Pearce from the Environment Agency suggested that companies select KPIs fromthe forthcoming DEFRA publication on environmental KPIs which is out for consultationover summer 2005.The data should be collected from the companies’ existing control,procurement, financial accounting and CSR reporting systems as companies shouldalready be managing the risks involved.

‘Not many sell-side orindeed buy-side financialanalysts will get up in themorning and say – I must goand read the OFR. But thatdoes not mean that there isnot going to be a veryinterested audience in theinvestment community.’

Rob Lake,

Henderson Global Investors

‘The OFR will put disciplineand structure intocommunication processes.’

Andrew Watchman,

DTI

Both companies and investors should work together to ensure that the OFR becomes asignificant part of mainstream reporting rather than a ‘specialist subject’, according toGuy Jubb from Standard Life Investments. Investors agreed on the need for engagementand follow up.

Equally, companies ought to be responsive to investor concerns and make sure the OFRmeets their needs. If the issues mentioned in the OFR are deemed to be strategicallyimportant, there ought to be a ‘read across’ with other segments of the companies’reporting ‘package’ such as, for example, the remuneration report.

Are all investors the same?

Investors are often portrayed as being a uniform entity but in reality, they are a verydiverse group.The fact that City analysts may not read the actual document does not initself spell the death of the OFR. Rob Lake pointed out that this is already the case withother sections of the annual report which, though unread by analysts, are neverthelessseen as vitally important for transparency and good governance. It is therefore more aquestion of who within the financial community will make use of the OFR information.

There are investors with a different kind of mandate, such as the growing number ofspecialist governance and socially responsible investment (SRI) analysts.Their approachtends to be long-term stewardship so, in Mintzberg’s words, they are owners rather thanpunters.While they may not manage money directly, they do vote at AGMs and theirviews are influential, not least because they often get reported in the press.

Although specialised, they are increasingly interacting with the traditional ‘numbercrunching’ analysts.This ensures cross-fertilisation and a better ‘fit’ between financialand non-financial information.

Finally, there was a warning that when deciding what information to report, companiesand boards will also have to consider who their shareholders actually are.As Rob Lakesaid, the investment world is already very diverse and is becoming increasingly so. Hedgefunds or proprietary desks, both of which have been under heavy criticism recently, arealso shareholders.Their time horizons and therefore their priorities may be entirelydifferent from those of traditional investors.As a result, their approach to sustainability –for example, their views on environment-related investments with longer payoffs, arelikely to be different.

For companies, this should mean a general awareness that it is not only the single issuepressure groups or NGOs that may try to influence the reporting agenda. Someshareholders may try to do the same, especially if there is a vacuum where legitimateinvestor engagement should be.

‘The OFR is clearly going toevolve.The DTI allows ayear’s grace so thatcompanies could perhapsstill be experimenting a littlebit in the first year before theregulatory regime kicks infully.’

Andrew Watchman,

DTI

‘There is a relatively smallgroup of people ininvestment houses who takean interest in the OFR andthey tend to be the samepeople who are busy runningaround voting and doing lotsof other things. So there is abit of a problem, I think, interms of using the consumerof the report to drive bestpractice.’

Rob Lake,

Henderson Global Investors

‘Sustainability is veryimportant for certainshareholders and investors –but for others, it does notcome into their particularequation or remit. I thinkwhen boards set out on thisjourney they will have togive some consideredthought at the outset as tojust who this report is in factdesigned for.’

Guy Jubb,

Standard Life Investments

Investors and investor pressure 12

OFR, CSR or both?

Most of the companies represented at the roundtable already produce a standalone CSRreport and all of them said they would continue to do so.There was no question aboutthe OFR superseding it in any way.Although some overlap was inevitable, it was stressedthat the reports are aimed at different audiences and will therefore require differentstrategies for preparation and assurance.

The issue for companies was more around how the two reports are likely to relate to eachother, both in terms of content and the process of preparation.

Although the OFR is written for the benefit of members of the company, there was somedebate about whether it is feasible to produce a document that would satisfy bothshareholders and stakeholders. Guy Jubb reminded the participants that though this ispossible, it is worth bearing in mind that the directors’ ultimate accountability is toshareholders alone.

David Bent pointed out that a CSR report should set the scene for the OFR. Companiesthat already take time to prepare a good CSR report may find it a lot easier when itcomes to preparing the OFR as they will already have considered what is strategicallyimportant.

What belongs where?

Nigel Cribb from ICI said that this type of relationship between reports may sound logicalin theory, as the OFR could be seen as a high-level summary of the more comprehensiveCSR report. But in practice, it may be difficult to narrow the focus of reporting evenfurther. For companies that have already been through the process of selecting thestrategically relevant issues and KPIs, cutting their number down further will be achallenge.

Craig Mackenzie contested this by saying that however important many CSR issues maybe in themselves, many of them are simply not material to shareholders. In other words,the process of preparing an OFR should not be about trying to cherry-pick, say, five mostimportant KPIs out of the whole CSR report. Instead, it should be about the boardselecting two or three issues – perhaps a few more in companies with obvious social orenvironmental impacts – that are truly relevant for its strategy.

The KPIs selected do not necessarily have to have an immediate impact. It may beappropriate to select more long-term issues. For a company like Unilever, Dr Mackenziesaid, it could be something like obesity or access to unsustainable fisheries or indeedunsustainable sourcing in general – all of which are likely to have a serious and long-termimpact on its ability to keep producing its goods and supplying its customers.

He added that it is, on the other hand, entirely appropriate for a CSR report to cover allthe issues that a company thinks are relevant from a social or environmental point ofview. Considering such a report is aimed at a wide group of stakeholders, it will by defaultbe far-reaching in its approach.

‘All of your communicationfrom the packaging, theadvertising, the marketingmessages, investor relations,your analyst briefings, yourCSR report, your OFR – thisis telling the world aboutwhat your company is like,what its values are, what isunderlying it – so they haveto be a coherent piece. Butthey are also all addressed todifferent people for differentpurposes.’

David Bent,

Forum for the Future

CSR reports and the OFR 13

CSR reports and the OFR

Mandy Cormack agreed, citing the example of advertising and the social debate that hasbuilt up around it as something that the Unilever CSR report would discuss in terms of,for example, the company’s approach to self-regulation.Although that is notimmediately relevant in terms of explaining the company’s performance to the City, it isnevertheless an important area for Unilever to be involved.

Mandy Cormack felt that the CSR report offered a unique and legitimate place forreporting issues such as these.This was precisely because it is an unregulatedcommunication format which allows the exploration of issues that have a ‘wave pattern’and come in and out of focus of attention.They may be inappropriate for the OFR –which she referred to as a ‘hard’ statement, meaning it requires consistency andcomparability.

Shareholders vs stakeholders

Rob Lake took the debate one step further by saying that the shareholder/stakeholderdichotomy is to a certain extent false anyway.When companies produce CSR reportscovering a whole range of issues from greenhouse gas emissions to ‘how many babies theCEO has kissed in the previous year’, they do it for a reason.

They perceive that there is some benefit in doing so which will eventually – and perhapsin a roundabout way – translate into shareholder value.There would be little point indoing it at all otherwise. Investors – including his own company – do not assume thatboards of directors are so naive as to invest a lot of time and money into good CSRreporting if the result has no value whatsoever to shareholders.

He added that although not aimed at them, the CSR report may in fact be a useful sourceof information for investors. For example, it would reveal the importance a companyattaches to its reputation and standing in the local community and how much it isprepared to invest in developing them.

In addition, an issue that may at first sight appear irrelevant to shareholders and ofconcern only to a narrow stakeholder group, may in fact turn out to be an early indicatorof something that will impact long-term shareholder value.This does not mean that it issuitable for the OFR – at least not on its own. It might find its way in as a part of anaggregated issue.

Guy Jubb added that companies should use this as an opportunity to stand back andexamine their corporate reporting practices. Rather than simply publishing the reportsand forgetting about them, they should go the extra mile and seek feedback from usersas to whether or not they are meeting their need.And if they are not, then they need totake action to address it.

‘We are talking about thereally big strategic business-relevant risks and anythingthat is not in that big hairycategory would have to goon the web or in some otherform of communication.’

Mandy Cormack,

Unilever

CSR reports and the OFR 14

Stakeholder engagement

The Chairman raised a question about whether companies need to conduct stakeholderengagement work in order to help them decide what kinds of KPIs may need to beincluded in their OFRs.

Both Sarah Sodeau and Mandy Cormack thought that, although companies may findengaging with stakeholders useful, they need to state at the outset that their finalchoices might not be based on the outcomes of this process.The results might notnecessarily be helpful so the costs and benefits of such an exercise need to be weighed upcarefully.

Howard Pearce said it was not necessary to go through the engagement or consultationprocess if the company is using a set of standard KPIs derived, for example, from DEFRAor ASB guidelines. However, if using company-specific, non-standard KPIs, then theremay be need to consult more widely.

David Bent mentioned the two kinds of regulatory regime with which companies need tocomply. On the one hand, there is the formal, regulatory regime but on the other, there isthe civil regime, consisting of civil society groups (NGOs, pressure groups, etc) that, in hiswords, ‘go around causing bother’.

This civil regime, through its public agenda, is trying to mark out the territory withinwhich they feel companies are allowed to operate.The boundaries and the relationshipbetween business and society are therefore constantly shifting.

The ‘business of business may be business’ but corporate communication is part ofcontinuous renegotiating of the ‘licence to operate’ between companies and society.ACSR report is therefore not only a way of justifying company’s strategic choices but alsoa way of marking out the territory in which it feels it can legitimately do business and asignal it is trying to play a legitimate role in society.

‘If it is the board of directorsthat is accountable for thechoice of KPIs, then theboard of directors has tomake that decision. If theydo not agree with theirstakeholder requirements,then they have to beprepared to say so.’

Sarah Sodeau,

GUS plc

CSR reports and the OFR 15

16

Despite having a potentially controversial mix of participants, the OFR and SustainabilityRoundtable turned out to be a constructive dialogue between different interest groups.Hopefully, the publication of the first round of OFRs will not turn out to be too dissimilar.

If there was a consensus about anything during the meeting, it was about the need tomake the OFR a part of mainstream corporate reporting. It makes the effort put intoproducing it worthwhile and it gives investors valuable information about the company’sstrategy and potential. In other words, both companies and investors need to ensure thatthe OFR fulfils its legal remit as well as its potential to improve transparency of corporatereporting. In time, there will hopefully be a convergence of best – or at least good –practice which will allow more comparability and consistency.

The publication of the OFR may be an opportune time for companies to stand back andreview the entirety of their corporate communications package in order to ensure overallcoherence.As the length of various reports increases, it becomes even more important tohave ‘read across’ between different sections.

Once the first round of OFRs is published, companies may also find it useful to seekfeedback from users in order to make sure the report is meeting their needs.

There is no doubt that business needs to pay attention to stakeholder opinion. It cannotsucceed otherwise, not only because it runs a significant risk to its reputation – but alsobecause it fails to meet the needs of its customers.As a recent article in The Economistput it:

‘Companies that treat social issues as either irritating distractions or simply unjustifiedvehicles for attack on business are turning a blind eye to impending forces that have thepotential fundamentally to alter their strategic future.’ (Davis, 2005)

But ultimately, the OFR is aimed at members of the company and should not becluttered with information that isn’t strategically relevant. ‘Taking account of ’ is not thesame as ‘being held accountable to’:‘Accountability refers to a much more formal anddirect set of rights and obligations’ (The Economist, 22 January 2005)

Finally, it is worth adding that there is much about sustainability reporting, whether inthe OFR or elsewhere, that is common sense. Some recommendations for companieswishing to engage in best practice include:

● Engaging stakeholders (and sometimes NGOs) in a dialogue● Establishing principles and procedures for addressing difficult issues such as labour

standards for suppliers, environmental reporting and human rights● Adjusting reward systems to reflect the company’s commitment to CSR● Having the senior leadership team and members of the board of directors engage in

an ongoing process of CSR risk evaluation● Establishing anonymous reporting and whistle-blowing policies and procedures● Educating employees and managers about CSR policies and the company’s

commitment to CSR● Having the senior leadership team communicate CSR priorities and set an example

through their own behaviour. (Donaldson, 2005)

‘One of the tricks at theoutset is going to be forcorporates and investors tomake sure that the OFRcomes into mainstreamcorporate reporting and doesnot become a specialistsubject in itself.’

Guy Jubb,

Standard Life Investments

Conclusions

Conclusions

Suggested reading

17

Accounting Standards Board, 2005.Reporting Standard 1: Operating and Financial Review. London: ASB Publications

Beattie, V and Thompson, S.J., 2005. Intangibles and the OFR. Financial Management.June 2005 pp. 29 – 30

CIMA, 2004. Response to Draft Regulations on the Operating and Financial Review andthe Directors’ Report: a Consultative Document [online]. Ausgust 2004.Available from: www.cimaglobal.com/cps/rde/xbcr/SID-0AAAC544-09520178/live/ofrdirectorsreport_consresponse_2004.pdf [Accessed 10 June 2005]

Davis, I., 2005.The biggest contract. The Economist.28 May 2005 Vol. 375 Issue 8428 pp.87-89

Deloitte & Touche LLP., 2005. The mandatory OFR: qualitative information is no longeroptional. Corporate Governance Update [online]. May 2005 pp. 3 – 17. Available from:www.deloitte.com/dtt/cda/doc/content/UK_AA_CorporateGovernance_May05.pdf[Accessed 8 June 2005]

Deloitte & Touche LLP., 2003. From Carrots to Sticks: a Survey of Narrative Reporting inAnnual Reports [online]. London: Deloitte & Touche LLP.Available from: www.deloitte.com/dtt/cda/doc/content/uk_gov_carrotssticks_1203.pdf[Accessed 8 June 2005]

Donaldson, T., 2005. Defining the value of doing good business. Financial Times.3 June 2005. Supplement: FT Mastering Corporate Governance pp. 2 – 3

Economist., 2005. The Ethics of Business. The Economist. 22 January 2005.Vol. 374 Issue 8410, special section pp. 20 – 23

Environment Agency website Available from: www.environment-agency.gov.uk/

Holland, J., 2002. Financial institutions and corporate governance. London: CIMA

Mintzberg, H., Simons, R. and Basu, K., 2002. Beyond Selfishness: Working Draft [online].Available from: www.cbsr.bc.ca/files/ReportsandPapers/mintzberg-beyondselfishness.pdf [Accessed 9 June 2005]

Suggested reading

PriceWaterhouseCoopers., 2005. The Operating and Financial Review (OFRPreparers’ Guide : Give Yourself a Head Start [online]. London: PriceWaterhouseCoopers.Available from: www.pwc.com/uk/eng/main/home/index.html (Registration required)[Accessed 8 June 2005]

Ross, L., 2005. The Operating and Financial Review. Financial Management.May 2005 pp. 28 – 30

Ross, L., 2005. CIMA Offers Solutions to Overlong OFRs. Insight [online]. March 2005.Available at: www.cimaglobal.com/cps/rde/xchg/SID-0AAAC564-417D4793/live/root.xsl/6382_7502.htm [Accessed 10 June 2005]

UK, Department of Trade & Industry., 2005. Guidance on the OFR and Changes to theDirectors’ Report [online]. London, DTI. Available from:www.dti.gov.uk/cld/OFR_Guidance.pdf [Accessed 8 June 2005]

Suggested reading 18

CIMA (The Chartered Institute of Management Accountants) represents members and supports the wider financial management

and business community. Its key activities relate to business strategy, information strategy and financial strategy. Its focus is to

qualify students, to support both members and employers and to protect the public interest.

June 2005

The Chartered Instituteof Management Accountants26 Chapter StreetLondon SW1P 4NPUnited Kingdom

T. +44 (0)20 7663 5441F. +44 (0)20 8849 2262E. [email protected]