Embed Size (px)

Citation preview

www.elsevier.com/locate/wasman

Waste Management 26 (2006) 110–122

On the effect of demographic characteristics on the formulationof solid waste charging policy

A. Karagiannidis *, A. Xirogiannopoulou, N. Moussiopoulos

Laboratory of Heat Transfer and Environmental Engineering, Department of Mechanical Engineering, Box 483,

Aristotle University, 54124 Thessaloniki, Greece

Accepted 6 January 2005

Available online 11 March 2005

Abstract

This paper presents the results from an analysis of municipal charges in Greece, as the fees paid by municipal waste producers to

the municipal authorities are included in these charges and constitute a major part of them. The aim is to determine whether and

how some of the demographic characteristics of a municipality influence the formulation of municipal waste charges and specifically

the level of the charge. The study included 339 Hellenic municipalities, which comprised approximately 62% of the overall popula-

tion in the country.

� 2005 Elsevier Ltd. All rights reserved.

1. Trends in municipal solid waste charging policies

Municipal waste services constitute a very important

component in the waste management chain. The contin-

uously growing waste production – and the increasedhazardousness of waste fractions as well – renders waste

management among the larger industries in the world.

The increasing waste production which raises the waste

management cost to high levels, as well as the (a) Pol-

luter-Pays Principle (PPP) (Commission of the Euro-

pean Communities, 2003; Official Journal of the

European Communities, 2001); Organization of Eco-

nomic Co-operation and Development (OECD,2001a), (b) Precautionary Principle (Commission of

the European Communities, 2000) and (c) Producer

0956-053X/$ - see front matter � 2005 Elsevier Ltd. All rights reserved.

doi:10.1016/j.wasman.2005.01.013

Abbreviations: HD, Household Density; HOG, Hellenic Official

Gazette; LCL, Lower Control Limit; OECD, Organisation for Eco-

nomic Co-Operation and Development; PAYT, Pay As You Throw;

PD, Population Density; PPC, Public Power Corporation of Greece;

PPP, Polluter Pays Principles; UCL, Upper Control Limit; WM,

Waste Management.* Corresponding author. Tel.: +30 231 099 4165; fax: +30 231 099

6012.

E-mail address: [email protected] (A. Karagiannidis).

Responsibility Principle (OECD, 2001b) are leading

the current management towards incorporating in its

procedures and pricing, mechanisms for reducing the

impact to the environment and for establishing equity

and fairness towards citizens as well.The aforementioned three principles constitute a sig-

nificant part of the global policy for environmental

protection. In particular, the PPP is the basis for the

Pay-As-You-Throw (PAYT) – system for variable waste

charging, according to the amount produced by each

household (Skumatz et al., 1997; Canterbury, 1997,

1998; Miranda and Aldy, 1996; Karagiannidis et al.,

2002; Aravossis, 2002; Intecus, 1998; www.payt.net,2004). These principles impose that related systems

should be adopted in both waste management levels,

i.e., collection and disposal (treatment and final dis-

posal). It should be noted that the incorporation of

PPP in the last stage of waste management (tipping fees

at landfills) is more feasible to be implemented because

of the available weighing system at the entrance of the

landfills, which facilitates the cost accounting of thewastes disposed.

Until recently, causing pollution either remained

‘‘unpunished’’ or the charging of the related activities

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 111

was not proportional to the damage caused. PPP allo-

cates the economic obligations concerning environmen-

tal pollution. PAYT, as a representative of PPP in the

waste management chain, aims at the identification of

the polluter and his/her enforcement to pay the cost of

waste collection and treatment according to the amountof the pollution that he/she produces (OECD, 1992;

www.payt.net, 2004). In this way, the financial return

of waste services is becoming an instrument for stimulat-

ing polluters (waste producers) towards reduction of

pollution (waste).

Another trend in waste management is the evaluation

of the performance either of each waste service sepa-

rately or of the overall procedure. Benchmarking iswidely spread in the evaluation of business performance

and recently appears to be promoted also in the evalua-

tion of public/municipal services (Her Majesty�s Gov-

ernment, 2003; Bolli and Tarcq, 2001; Accounts

Commission, 2000; Department for Environment, Food

and Rural Affairs Defra, 2000; Nilsson et al., 2001; Sme-

ets and Weterings, 1999). Benchmarking of waste ser-

vices is a tool for evaluating and comparing wasteservices of a specific municipality over time, as well as

comparing different municipalities for the same refer-

ence year. Waste charges and the resulting waste reduc-

tion can be a measure for the performance evaluation of

waste services, especially in a PAYT scheme.

2. Waste charges in Greece

Traditionally in Greece, waste collection and disposal

are the responsibility of the Local self-Government

Organizations (Hellenic Official Gazette HOG, 1958).

The involvement of the private sector in this field, espe-

cially in waste treatment, disposal and recycling services,

is increasing. This fact affects also the Hellenic waste

management process towards the global policy for sus-tainable development (OECD, 2000, 2001a,b), since

the involvement of the private sector expands the mar-

ket-based environmental policy, thus providing incen-

tives for developing and disseminating technologies, as

well as promoting local, national or/and international

collaboration.

The pricing model for waste services applied in

Greece is a flat-rate system (estimation of waste chargesaccording to the surface-area of the served property)

and waste charges are collected through the electricity

bill (HOG, 1975, 1976, 1980 and HOG, 1989). This bill-

ing and collection method of waste charges induces crit-

icism about its fairness towards citizens and certainly

does not introduce incentives for waste prevention

and/or reduction. This billing method remains in force

in Greece, due to the Hellenic Legislation which pre-determines this method, allowing only one more alterna-

tive solution-through the water bill (HOG, 1976).

Furthermore, concerning recycling, the recent financ-

ing of a cooperation scheme between industry (67%) and

Local Authorities (33%) (approved by the Ministry for

the Environment, Physical Planning and Public Works

– based on the Law 2939/2001 (HOG, 2001), harmoniza-

tion of the EC Directive 94/62/EC) constitutes a meansfor the recovery of the cost of recycling, which will addi-

tionally burden citizens through the raising of prices of

consumer goods. Concerning treatment and final dis-

posal of wastes, the responsible authority for these ac-

tions relieves the municipal authority from the waste

collected, in the same way that the municipal authority

relieves citizens from the wastes produced by them.

The financial return for treatment and final disposal iscalculated under the same concept with the correspond-

ing charging against the waste producers, in this case the

municipalities.

Waste charges in Greece are part of the municipal

charges, which also include street lighting (HOG,

1980). These municipal charges are calculated for each

real-estate property through the multiplication of the

real estates surface area by a certain coefficient (flat-ratesystem). This coefficient is the final result of an account-

ing procedure, which begins from the division of the

waste-management and street-lighting cost (forecast

each year for the following year by the municipal coun-

cil) by the total surface area of the served real estate par-

cels. This coefficient is finally specified for each property

after adjustments according to the charging policy of

each municipality (e.g., different charge among resi-dences, stores, etc.). Specifically, each municipality is

authorized to classify its real estate parcels into catego-

ries and to determine and attribute a different coefficient

to each category. The municipal charge (M) for each real

estate is calculated on an annual basis by the formula:

M ¼ C � A;

where C is the calculation coefficient (€/m2year), appli-

cable to the particular real estate, A is the surface of

the real estate (m2).

The statistical analysis of municipal charges that is

presented next in this paper focused on the calculation

coefficients and their correlations with the population

and the number of households in the correspondingmunicipality. Data on the calculation coefficients re-

ferred to the year 2002 and were provided by the Public

Power Corporation of Greece (PPC), which manages the

collection of municipal charges through the electricity

bill. Data on the number of citizens and households orig-

inated from the National Statistical Service of Greece

(1991, 2001). Each municipality informs the PPC on an

annual basis, on two charging coefficients that will beused by the PPC for the billing of the municipal charges

to its customers. These coefficients are determined every

year by the municipal council (as discussed above) and

refer to residences (Cr) and stores (Cs).

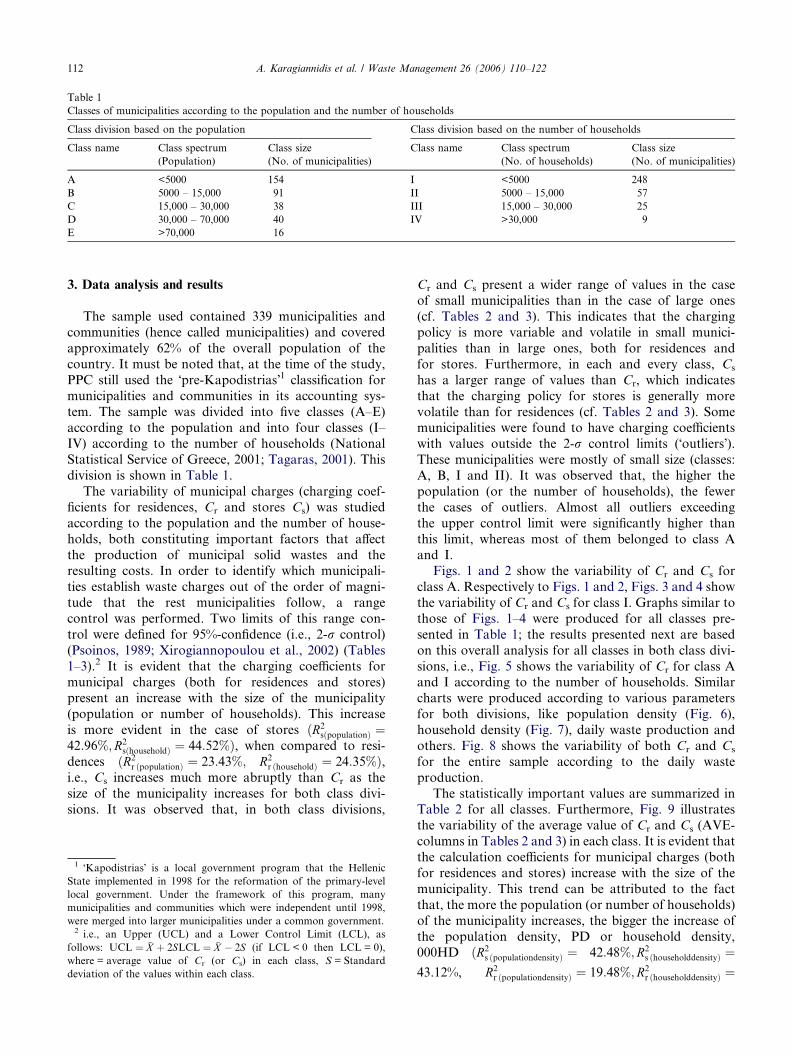

Table 1

Classes of municipalities according to the population and the number of households

Class division based on the population Class division based on the number of households

Class name Class spectrum

(Population)

Class size

(No. of municipalities)

Class name Class spectrum

(No. of households)

Class size

(No. of municipalities)

A <5000 154 I <5000 248

B 5000 – 15,000 91 II 5000 – 15,000 57

C 15,000 – 30,000 38 III 15,000 – 30,000 25

D 30,000 – 70,000 40 IV >30,000 9

E >70,000 16

112 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

3. Data analysis and results

The sample used contained 339 municipalities and

communities (hence called municipalities) and covered

approximately 62% of the overall population of the

country. It must be noted that, at the time of the study,

PPC still used the �pre-Kapodistrias�1 classification for

municipalities and communities in its accounting sys-

tem. The sample was divided into five classes (A–E)

according to the population and into four classes (I–IV) according to the number of households (National

Statistical Service of Greece, 2001; Tagaras, 2001). This

division is shown in Table 1.

The variability of municipal charges (charging coef-

ficients for residences, Cr and stores Cs) was studied

according to the population and the number of house-

holds, both constituting important factors that affect

the production of municipal solid wastes and theresulting costs. In order to identify which municipali-

ties establish waste charges out of the order of magni-

tude that the rest municipalities follow, a range

control was performed. Two limits of this range con-

trol were defined for 95%-confidence (i.e., 2-r control)

(Psoinos, 1989; Xirogiannopoulou et al., 2002) (Tables

1–3).2 It is evident that the charging coefficients for

municipal charges (both for residences and stores)present an increase with the size of the municipality

(population or number of households). This increase

is more evident in the case of stores ðR2sðpopulationÞ ¼

42:96%;R2sðhouseholdÞ ¼ 44:52%Þ, when compared to resi-

dences ðR2r ðpopulationÞ ¼ 23:43%; R2

r ðhouseholdÞ ¼ 24:35%Þ,i.e., Cs increases much more abruptly than Cr as the

size of the municipality increases for both class divi-

sions. It was observed that, in both class divisions,

1 �Kapodistrias� is a local government program that the Hellenic

State implemented in 1998 for the reformation of the primary-level

local government. Under the framework of this program, many

municipalities and communities which were independent until 1998,

were merged into larger municipalities under a common government.2 i.e., an Upper (UCL) and a Lower Control Limit (LCL), as

follows: UCL ¼ �X þ 2SLCL ¼ �X � 2S (if LCL < 0 then LCL = 0),

where = average value of Cr (or Cs) in each class, S = Standard

deviation of the values within each class.

Cr and Cs present a wider range of values in the caseof small municipalities than in the case of large ones

(cf. Tables 2 and 3). This indicates that the charging

policy is more variable and volatile in small munici-

palities than in large ones, both for residences and

for stores. Furthermore, in each and every class, Cs

has a larger range of values than Cr, which indicates

that the charging policy for stores is generally more

volatile than for residences (cf. Tables 2 and 3). Somemunicipalities were found to have charging coefficients

with values outside the 2-r control limits (�outliers�).These municipalities were mostly of small size (classes:

A, B, I and II). It was observed that, the higher the

population (or the number of households), the fewer

the cases of outliers. Almost all outliers exceeding

the upper control limit were significantly higher than

this limit, whereas most of them belonged to class Aand I.

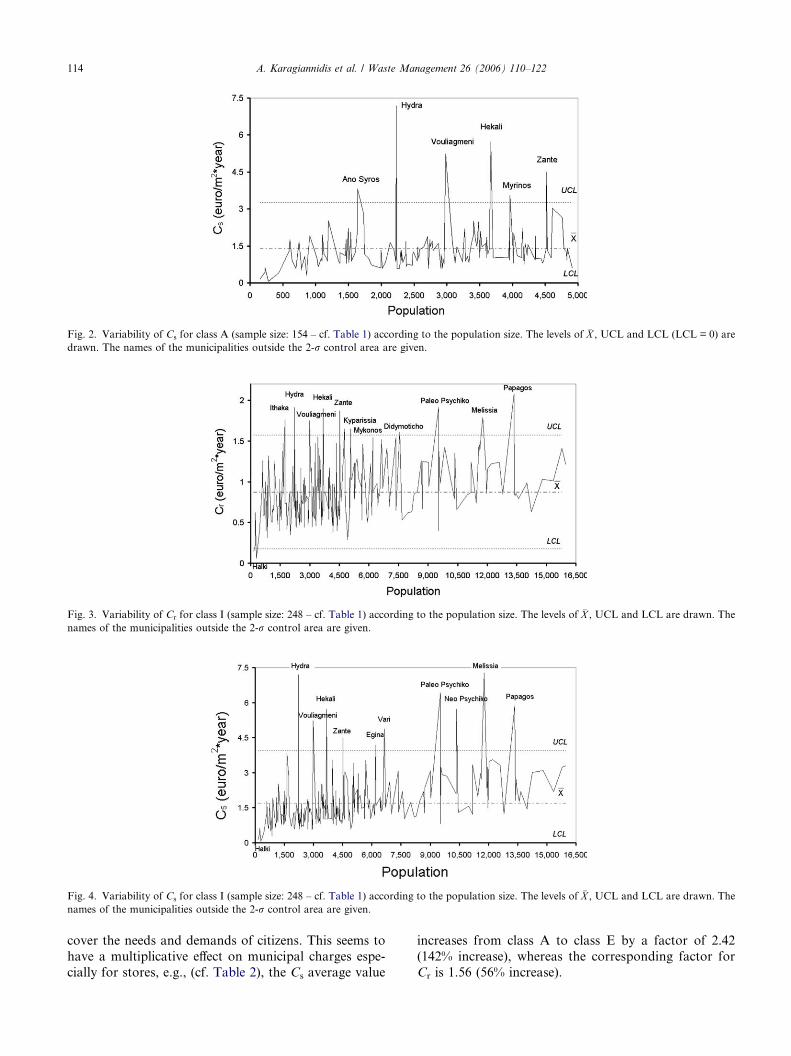

Figs. 1 and 2 show the variability of Cr and Cs for

class A. Respectively to Figs. 1 and 2, Figs. 3 and 4 show

the variability of Cr and Cs for class I. Graphs similar to

those of Figs. 1–4 were produced for all classes pre-

sented in Table 1; the results presented next are based

on this overall analysis for all classes in both class divi-

sions, i.e., Fig. 5 shows the variability of Cr for class Aand I according to the number of households. Similar

charts were produced according to various parameters

for both divisions, like population density (Fig. 6),

household density (Fig. 7), daily waste production and

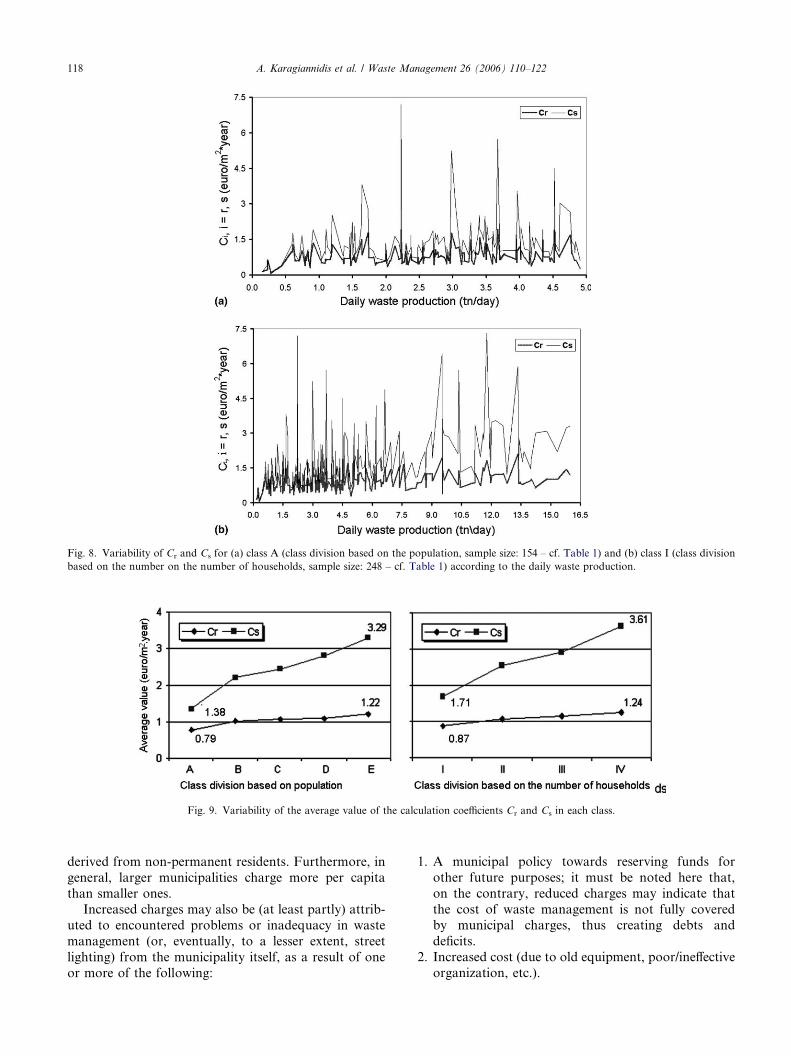

others. Fig. 8 shows the variability of both Cr and Cs

for the entire sample according to the daily waste

production.

The statistically important values are summarized inTable 2 for all classes. Furthermore, Fig. 9 illustrates

the variability of the average value of Cr and Cs (AVE-

columns in Tables 2 and 3) in each class. It is evident that

the calculation coefficients for municipal charges (both

for residences and stores) increase with the size of the

municipality. This trend can be attributed to the fact

that, the more the population (or number of households)

of the municipality increases, the bigger the increase ofthe population density, PD or household density,

000HD ðR2s ðpopulationdensityÞ ¼ 42:48%;R2

s ðhouseholddensityÞ ¼43.12%, R2

r ðpopulationdensityÞ ¼ 19:48%;R2r ðhouseholddensityÞ ¼

Table 3

Statistical indices in each class for Cs

Cs (€/m2year)

AVE �X MAX MIN MAX–MIN Standard deviation S

Class division based on the population A 1.38 7.19 0.06 7.13 0.94

B 2.21 7.31 0.82 6.49 1.21

C 2.46 4.2 1.57 2.63 0.59

D 2.81 4.75 1.11 3.64 0.82

E 3.29 5.12 2.02 3.1 0.87

Class division based on the number of households I 1.71 7.31 0.06 7.25 1.12

II 2.54 4.75 1.11 3.64 0.77

III 2.92 3.83 1.74 2.09 0.52

IV 3.61 5.12 2.02 3.1 1.08

Table 2

Statistical indices in each class for Cr

Class Cr (€/m2year)

AVE �X MAX MIN MAX–MIN Standard deviation S

Class division based on the population A 0.79 1.91 0.06 1.85 0.36

B 1.01 2.08 0.4 1.68 0.33

C 1.06 1.74 0.7 1.04 0.22

D 1.09 2.2 0.37 1.83 0.30

E 1.22 1.76 0.66 1.1 0.28

Class division based on the number of households I 0.87 2.08 0.06 2.02 0.35

II 1.06 1.74 0.37 1.37 0.25

III 1.15 2.2 0.7 1.5 0.28

IV 1.24 1.76 0.66 1.1 0.35

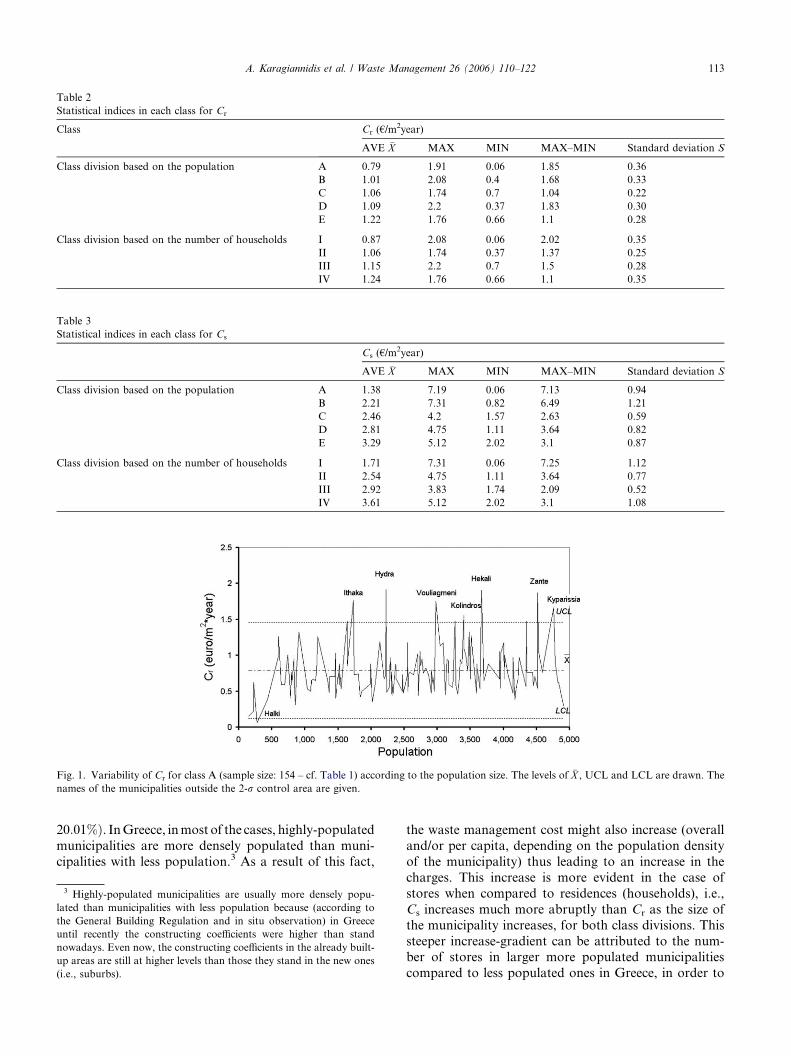

Fig. 1. Variability of Cr for class A (sample size: 154 – cf. Table 1) according to the population size. The levels of �X , UCL and LCL are drawn. The

names of the municipalities outside the 2-r control area are given.

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 113

20:01%Þ. InGreece, inmost of the cases, highly-populated

municipalities are more densely populated than muni-

cipalities with less population.3 As a result of this fact,

3 Highly-populated municipalities are usually more densely popu-

lated than municipalities with less population because (according to

the General Building Regulation and in situ observation) in Greece

until recently the constructing coefficients were higher than stand

nowadays. Even now, the constructing coefficients in the already built-

up areas are still at higher levels than those they stand in the new ones

(i.e., suburbs).

the waste management cost might also increase (overall

and/or per capita, depending on the population density

of the municipality) thus leading to an increase in the

charges. This increase is more evident in the case of

stores when compared to residences (households), i.e.,

Cs increases much more abruptly than Cr as the size of

the municipality increases, for both class divisions. This

steeper increase-gradient can be attributed to the num-ber of stores in larger more populated municipalities

compared to less populated ones in Greece, in order to

Fig. 2. Variability of Cs for class A (sample size: 154 – cf. Table 1) according to the population size. The levels of �X , UCL and LCL (LCL = 0) are

drawn. The names of the municipalities outside the 2-r control area are given.

Fig. 3. Variability of Cr for class I (sample size: 248 – cf. Table 1) according to the population size. The levels of �X , UCL and LCL are drawn. The

names of the municipalities outside the 2-r control area are given.

Fig. 4. Variability of Cs for class I (sample size: 248 – cf. Table 1) according to the population size. The levels of �X , UCL and LCL are drawn. The

names of the municipalities outside the 2-r control area are given.

114 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

cover the needs and demands of citizens. This seems to

have a multiplicative effect on municipal charges espe-

cially for stores, e.g., (cf. Table 2), the Cs average value

increases from class A to class E by a factor of 2.42

(142% increase), whereas the corresponding factor for

Cr is 1.56 (56% increase).

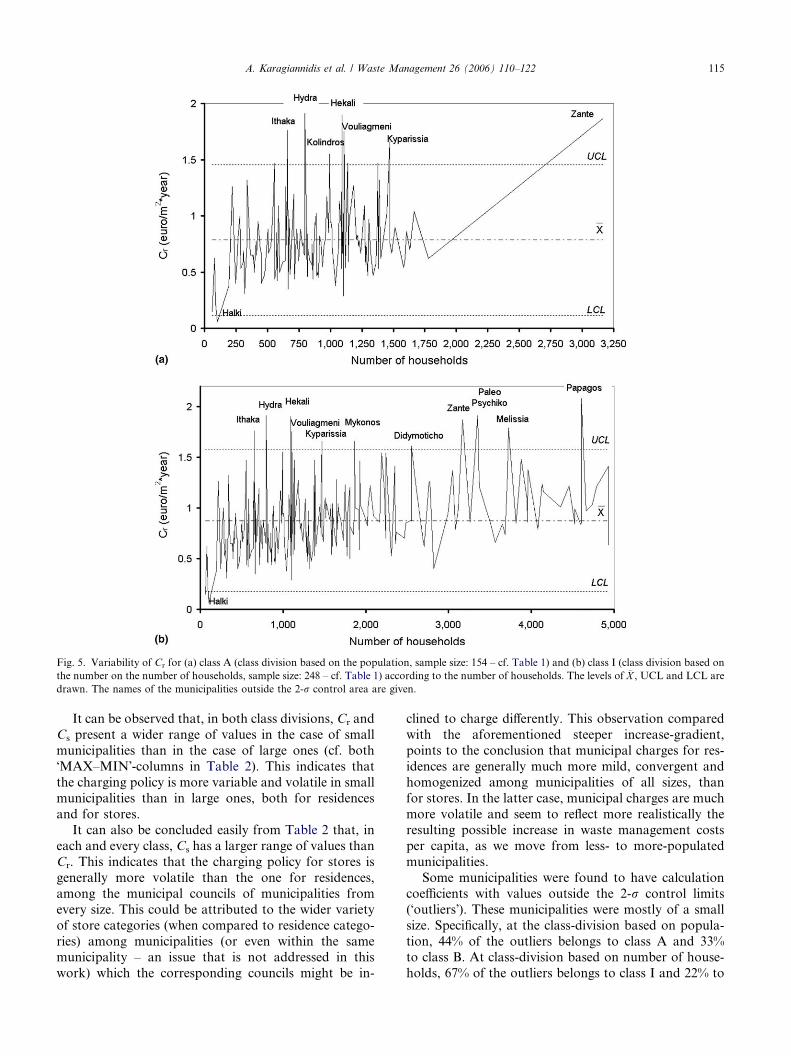

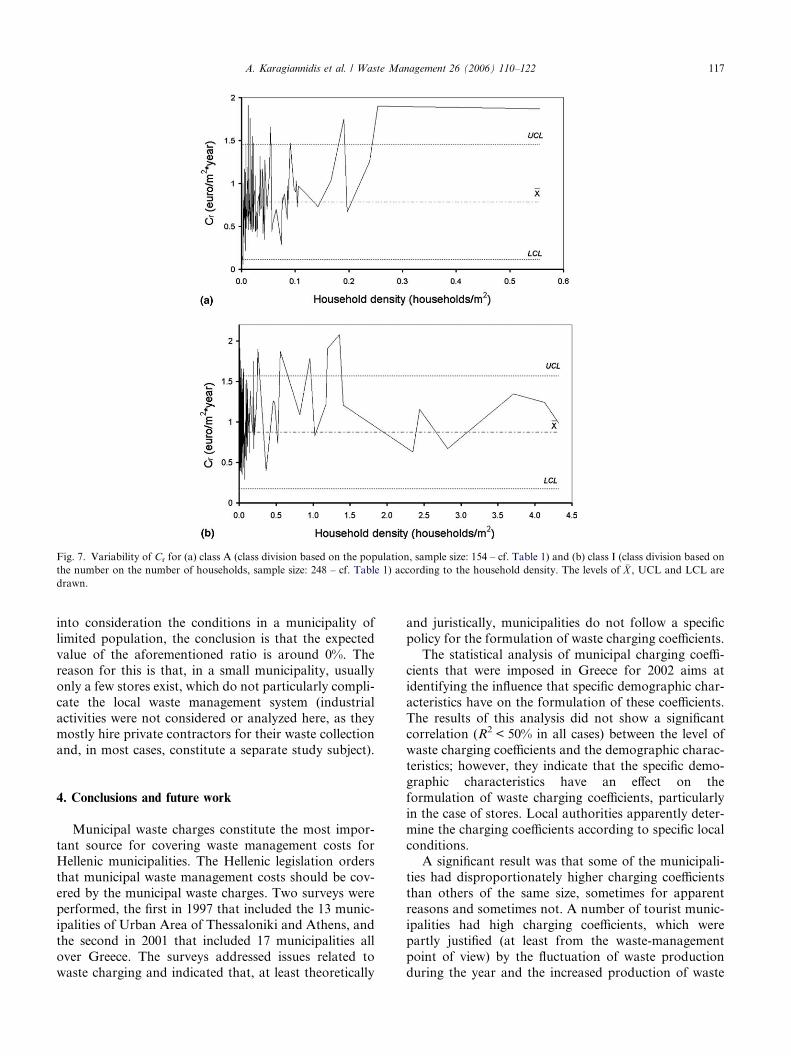

Fig. 5. Variability of Cr for (a) class A (class division based on the population, sample size: 154 – cf. Table 1) and (b) class I (class division based on

the number on the number of households, sample size: 248 – cf. Table 1) according to the number of households. The levels of �X , UCL and LCL are

drawn. The names of the municipalities outside the 2-r control area are given.

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 115

It can be observed that, in both class divisions, Cr and

Cs present a wider range of values in the case of small

municipalities than in the case of large ones (cf. both

�MAX–MIN�-columns in Table 2). This indicates that

the charging policy is more variable and volatile in small

municipalities than in large ones, both for residences

and for stores.It can also be concluded easily from Table 2 that, in

each and every class, Cs has a larger range of values than

Cr. This indicates that the charging policy for stores is

generally more volatile than the one for residences,

among the municipal councils of municipalities from

every size. This could be attributed to the wider variety

of store categories (when compared to residence catego-

ries) among municipalities (or even within the samemunicipality – an issue that is not addressed in this

work) which the corresponding councils might be in-

clined to charge differently. This observation compared

with the aforementioned steeper increase-gradient,

points to the conclusion that municipal charges for res-

idences are generally much more mild, convergent and

homogenized among municipalities of all sizes, than

for stores. In the latter case, municipal charges are much

more volatile and seem to reflect more realistically theresulting possible increase in waste management costs

per capita, as we move from less- to more-populated

municipalities.

Some municipalities were found to have calculation

coefficients with values outside the 2-r control limits

(�outliers�). These municipalities were mostly of a small

size. Specifically, at the class-division based on popula-

tion, 44% of the outliers belongs to class A and 33%to class B. At class-division based on number of house-

holds, 67% of the outliers belongs to class I and 22% to

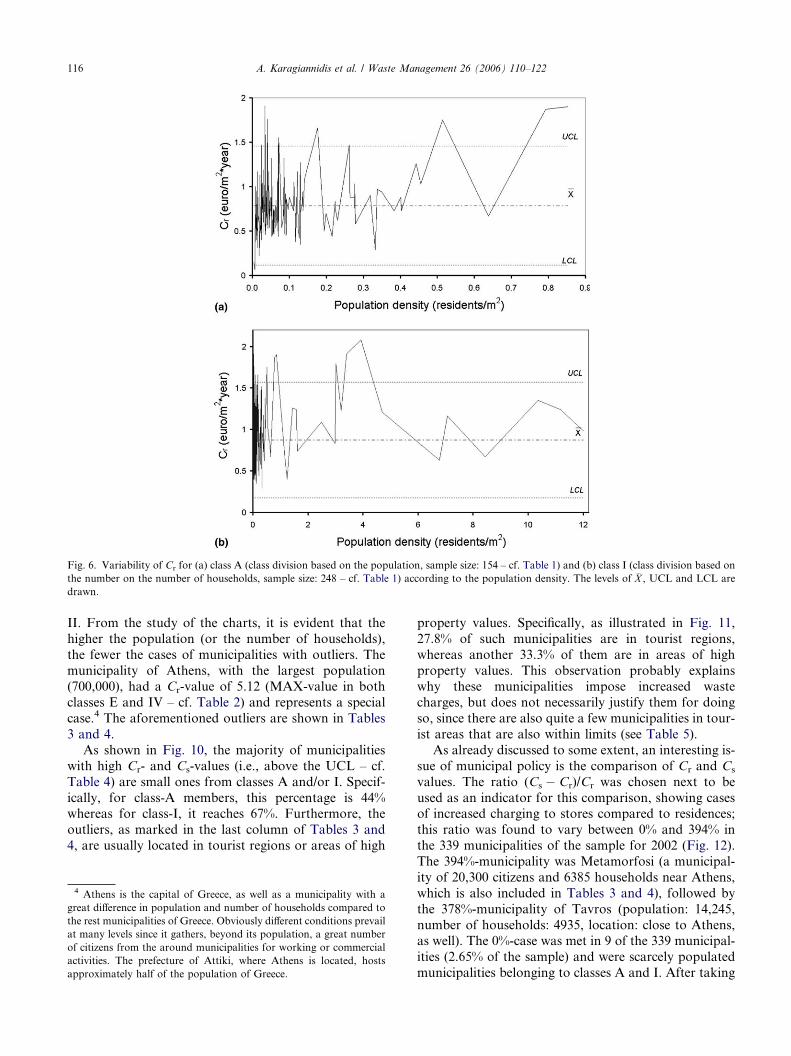

Fig. 6. Variability of Cr for (a) class A (class division based on the population, sample size: 154 – cf. Table 1) and (b) class I (class division based on

the number on the number of households, sample size: 248 – cf. Table 1) according to the population density. The levels of �X , UCL and LCL are

drawn.

116 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

II. From the study of the charts, it is evident that the

higher the population (or the number of households),

the fewer the cases of municipalities with outliers. The

municipality of Athens, with the largest population(700,000), had a Cr-value of 5.12 (MAX-value in both

classes E and IV – cf. Table 2) and represents a special

case.4 The aforementioned outliers are shown in Tables

3 and 4.

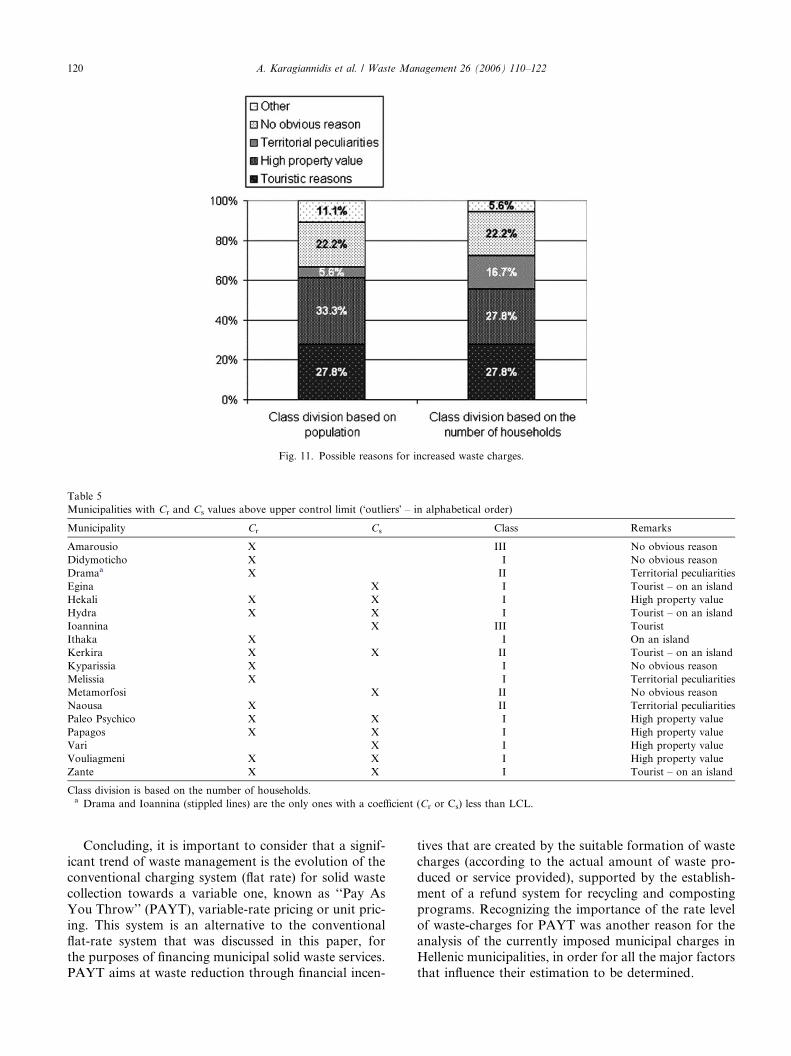

As shown in Fig. 10, the majority of municipalities

with high Cr- and Cs-values (i.e., above the UCL – cf.

Table 4) are small ones from classes A and/or I. Specif-

ically, for class-A members, this percentage is 44%whereas for class-I, it reaches 67%. Furthermore, the

outliers, as marked in the last column of Tables 3 and

4, are usually located in tourist regions or areas of high

4 Athens is the capital of Greece, as well as a municipality with a

great difference in population and number of households compared to

the rest municipalities of Greece. Obviously different conditions prevail

at many levels since it gathers, beyond its population, a great number

of citizens from the around municipalities for working or commercial

activities. The prefecture of Attiki, where Athens is located, hosts

approximately half of the population of Greece.

property values. Specifically, as illustrated in Fig. 11,

27.8% of such municipalities are in tourist regions,

whereas another 33.3% of them are in areas of high

property values. This observation probably explainswhy these municipalities impose increased waste

charges, but does not necessarily justify them for doing

so, since there are also quite a few municipalities in tour-

ist areas that are also within limits (see Table 5).

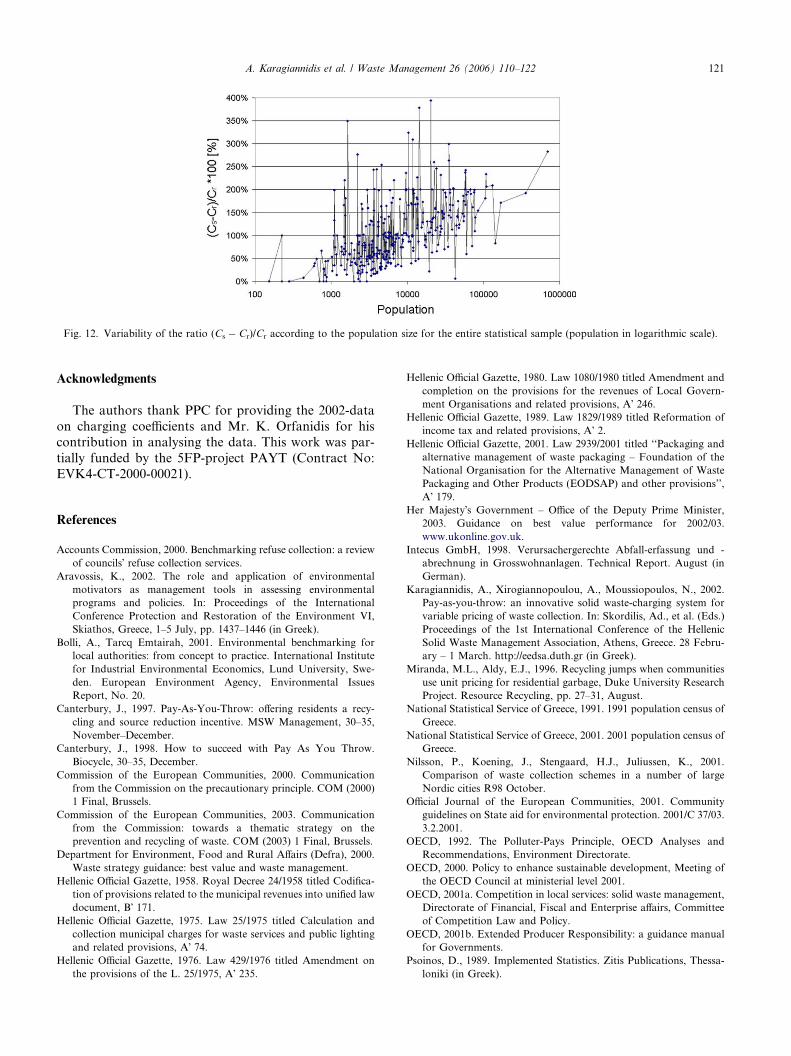

As already discussed to some extent, an interesting is-

sue of municipal policy is the comparison of Cr and Cs

values. The ratio (Cs � Cr)/Cr was chosen next to be

used as an indicator for this comparison, showing casesof increased charging to stores compared to residences;

this ratio was found to vary between 0% and 394% in

the 339 municipalities of the sample for 2002 (Fig. 12).

The 394%-municipality was Metamorfosi (a municipal-

ity of 20,300 citizens and 6385 households near Athens,

which is also included in Tables 3 and 4), followed by

the 378%-municipality of Tavros (population: 14,245,

number of households: 4935, location: close to Athens,as well). The 0%-case was met in 9 of the 339 municipal-

ities (2.65% of the sample) and were scarcely populated

municipalities belonging to classes A and I. After taking

Fig. 7. Variability of Cr for (a) class A (class division based on the population, sample size: 154 – cf. Table 1) and (b) class I (class division based on

the number on the number of households, sample size: 248 – cf. Table 1) according to the household density. The levels of �X , UCL and LCL are

drawn.

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 117

into consideration the conditions in a municipality of

limited population, the conclusion is that the expected

value of the aforementioned ratio is around 0%. The

reason for this is that, in a small municipality, usually

only a few stores exist, which do not particularly compli-

cate the local waste management system (industrial

activities were not considered or analyzed here, as theymostly hire private contractors for their waste collection

and, in most cases, constitute a separate study subject).

4. Conclusions and future work

Municipal waste charges constitute the most impor-

tant source for covering waste management costs forHellenic municipalities. The Hellenic legislation orders

that municipal waste management costs should be cov-

ered by the municipal waste charges. Two surveys were

performed, the first in 1997 that included the 13 munic-

ipalities of Urban Area of Thessaloniki and Athens, and

the second in 2001 that included 17 municipalities all

over Greece. The surveys addressed issues related to

waste charging and indicated that, at least theoretically

and juristically, municipalities do not follow a specific

policy for the formulation of waste charging coefficients.

The statistical analysis of municipal charging coeffi-

cients that were imposed in Greece for 2002 aims at

identifying the influence that specific demographic char-

acteristics have on the formulation of these coefficients.

The results of this analysis did not show a significantcorrelation (R2 < 50% in all cases) between the level of

waste charging coefficients and the demographic charac-

teristics; however, they indicate that the specific demo-

graphic characteristics have an effect on the

formulation of waste charging coefficients, particularly

in the case of stores. Local authorities apparently deter-

mine the charging coefficients according to specific local

conditions.A significant result was that some of the municipali-

ties had disproportionately higher charging coefficients

than others of the same size, sometimes for apparent

reasons and sometimes not. A number of tourist munic-

ipalities had high charging coefficients, which were

partly justified (at least from the waste-management

point of view) by the fluctuation of waste production

during the year and the increased production of waste

Fig. 8. Variability of Cr and Cs for (a) class A (class division based on the population, sample size: 154 – cf. Table 1) and (b) class I (class division

based on the number on the number of households, sample size: 248 – cf. Table 1) according to the daily waste production.

Fig. 9. Variability of the average value of the calculation coefficients Cr and Cs in each class.

118 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

derived from non-permanent residents. Furthermore, in

general, larger municipalities charge more per capita

than smaller ones.Increased charges may also be (at least partly) attrib-

uted to encountered problems or inadequacy in waste

management (or, eventually, to a lesser extent, street

lighting) from the municipality itself, as a result of one

or more of the following:

1. A municipal policy towards reserving funds for

other future purposes; it must be noted here that,

on the contrary, reduced charges may indicate that

the cost of waste management is not fully coveredby municipal charges, thus creating debts and

deficits.

2. Increased cost (due to old equipment, poor/ineffective

organization, etc.).

Table 4

Municipalities with Cr and Cs values above upper control limit (�outliers� – in alphabetical order)

Municipality Cr Cs Class Remarks

Amarousio X D No obvious reason

Ano Syros Xa A Tourist – on an island

Athens X E Capital of Greece

Hekali X X A High property value

Hydra X X A Tourist – on an island

Ithaka X A On an island

Kerkira X D Tourist – on an island

Kolindros X A No obvious reason

Kyparissia X A No obvious reason

Melissia X X B Territorial peculiarities

Metamorfosi X X C No obvious reason

Myrinos X B Tourist – on an island

Neo Psychico X B High property value

Palio Psychico X X B High property value

Papagos X X B High property value

Vari X B High property value

Vouliagmeni X A High property value

Zante X X A Tourist – on an island

Class division is based on the population.a Symbol X indicates that this municipality has imposed at least one coefficient (either Cr or Cs) that is out of the control limits (outlier).

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 119

3. Adverse geographical and territorial conditions, and

4. Increased tipping fees.

A reason for increased charges for stores in small

municipalities is the eventual decision of the municipal

council to instigate a policy which will differentiate among

non-household waste producers according to the amount

ofwaste that they actually generate. This is fair in the casesof restaurants and taverns, but not in the case of some

other stores, e.g., small groceries, as a grocery store in

smallmunicipalities oftenproduces lesswaste than a single

household, as a result of the limited number of customers.

Concerning future work on municipal charges, it

would be interesting to separate (either with actual data

or with realistic work assumptions) the waste collection

part from the street lighting part of the charges. It wouldthen be possible to study the actual parts instead of

attempting to derive conclusions on the waste collection

part (which has been reported as being the major part of

the two, however) by studying their sum, as it was per-

formed in the present work.

Fig. 10. Distribution of municipalities with coefficients out of control limit

households (right).

The data on municipal charges that was used here

was for one year only (2002). Availability of such data

for more years would allow further work and time-

series analysis of related charging practices, as well

as possible projections into the future. The concept

of municipality benchmarking is also closely linked

to the scope of this study, as the charging coefficients

could be used as one of the criteria to form the basisfor evaluating the overall performance of the munici-

pality. It must be stressed that issues like this, which

require co-ordination among municipalities and in

close association with the Ministry of the Interior

and other state institutions, have to be undertaken

in each following case:

� at urban/rural/regional levels, by Associations ofMunicipalities and Communities;

� at prefectural level, by Local Unions of Municipali-

ties and Communities;

� at national level, by the Central Union of Municipal-

ities and Communities of Greece.

s for class division based on population (left) and on the number of

Fig. 11. Possible reasons for increased waste charges.

Table 5

Municipalities with Cr and Cs values above upper control limit (�outliers� – in alphabetical order)

Municipality Cr Cs Class Remarks

Amarousio X III No obvious reason

Didymoticho X I No obvious reason

Dramaa X II Territorial peculiarities

Egina X I Tourist – on an island

Hekali X X I High property value

Hydra X X I Tourist – on an island

Ioannina X III Tourist

Ithaka X I On an island

Kerkira X X II Tourist – on an island

Kyparissia X I No obvious reason

Melissia X I Territorial peculiarities

Metamorfosi X II No obvious reason

Naousa X II Territorial peculiarities

Paleo Psychico X X I High property value

Papagos X X I High property value

Vari X I High property value

Vouliagmeni X X I High property value

Zante X X I Tourist – on an island

Class division is based on the number of households.a Drama and Ioannina (stippled lines) are the only ones with a coefficient (Cr or Cs) less than LCL.

120 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

Concluding, it is important to consider that a signif-

icant trend of waste management is the evolution of the

conventional charging system (flat rate) for solid waste

collection towards a variable one, known as ‘‘Pay As

You Throw’’ (PAYT), variable-rate pricing or unit pric-

ing. This system is an alternative to the conventionalflat-rate system that was discussed in this paper, for

the purposes of financing municipal solid waste services.

PAYT aims at waste reduction through financial incen-

tives that are created by the suitable formation of waste

charges (according to the actual amount of waste pro-

duced or service provided), supported by the establish-

ment of a refund system for recycling and composting

programs. Recognizing the importance of the rate level

of waste-charges for PAYT was another reason for theanalysis of the currently imposed municipal charges in

Hellenic municipalities, in order for all the major factors

that influence their estimation to be determined.

Fig. 12. Variability of the ratio (Cs � Cr)/Cr according to the population size for the entire statistical sample (population in logarithmic scale).

A. Karagiannidis et al. / Waste Management 26 (2006) 110–122 121

Acknowledgments

The authors thank PPC for providing the 2002-data

on charging coefficients and Mr. K. Orfanidis for hiscontribution in analysing the data. This work was par-

tially funded by the 5FP-project PAYT (Contract No:

EVK4-CT-2000-00021).

References

Accounts Commission, 2000. Benchmarking refuse collection: a review

of councils� refuse collection services.

Aravossis, K., 2002. The role and application of environmental

motivators as management tools in assessing environmental

programs and policies. In: Proceedings of the International

Conference Protection and Restoration of the Environment VI,

Skiathos, Greece, 1–5 July, pp. 1437–1446 (in Greek).

Bolli, A., Tarcq Emtairah, 2001. Environmental benchmarking for

local authorities: from concept to practice. International Institute

for Industrial Environmental Economics, Lund University, Swe-

den. European Environment Agency, Environmental Issues

Report, No. 20.

Canterbury, J., 1997. Pay-As-You-Throw: offering residents a recy-

cling and source reduction incentive. MSW Management, 30–35,

November–December.

Canterbury, J., 1998. How to succeed with Pay As You Throw.

Biocycle, 30–35, December.

Commission of the European Communities, 2000. Communication

from the Commission on the precautionary principle. COM (2000)

1 Final, Brussels.

Commission of the European Communities, 2003. Communication

from the Commission: towards a thematic strategy on the

prevention and recycling of waste. COM (2003) 1 Final, Brussels.

Department for Environment, Food and Rural Affairs (Defra), 2000.

Waste strategy guidance: best value and waste management.

Hellenic Official Gazette, 1958. Royal Decree 24/1958 titled Codifica-

tion of provisions related to the municipal revenues into unified law

document, B� 171.Hellenic Official Gazette, 1975. Law 25/1975 titled Calculation and

collection municipal charges for waste services and public lighting

and related provisions, A� 74.Hellenic Official Gazette, 1976. Law 429/1976 titled Amendment on

the provisions of the L. 25/1975, A� 235.

Hellenic Official Gazette, 1980. Law 1080/1980 titled Amendment and

completion on the provisions for the revenues of Local Govern-

ment Organisations and related provisions, A� 246.Hellenic Official Gazette, 1989. Law 1829/1989 titled Reformation of

income tax and related provisions, A� 2.Hellenic Official Gazette, 2001. Law 2939/2001 titled ‘‘Packaging and

alternative management of waste packaging – Foundation of the

National Organisation for the Alternative Management of Waste

Packaging and Other Products (EODSAP) and other provisions’’,

A� 179.Her Majesty�s Government – Office of the Deputy Prime Minister,

2003. Guidance on best value performance for 2002/03.

www.ukonline.gov.uk.

Intecus GmbH, 1998. Verursachergerechte Abfall-erfassung und -

abrechnung in Grosswohnanlagen. Technical Report. August (in

German).

Karagiannidis, A., Xirogiannopoulou, A., Moussiopoulos, N., 2002.

Pay-as-you-throw: an innovative solid waste-charging system for

variable pricing of waste collection. In: Skordilis, Ad., et al. (Eds.)

Proceedings of the 1st International Conference of the Hellenic

Solid Waste Management Association, Athens, Greece. 28 Febru-

ary – 1 March. http://eedsa.duth.gr (in Greek).

Miranda, M.L., Aldy, E.J., 1996. Recycling jumps when communities

use unit pricing for residential garbage, Duke University Research

Project. Resource Recycling, pp. 27–31, August.

National Statistical Service of Greece, 1991. 1991 population census of

Greece.

National Statistical Service of Greece, 2001. 2001 population census of

Greece.

Nilsson, P., Koening, J., Stengaard, H.J., Juliussen, K., 2001.

Comparison of waste collection schemes in a number of large

Nordic cities R98 October.

Official Journal of the European Communities, 2001. Community

guidelines on State aid for environmental protection. 2001/C 37/03.

3.2.2001.

OECD, 1992. The Polluter-Pays Principle, OECD Analyses and

Recommendations, Environment Directorate.

OECD, 2000. Policy to enhance sustainable development, Meeting of

the OECD Council at ministerial level 2001.

OECD, 2001a. Competition in local services: solid waste management,

Directorate of Financial, Fiscal and Enterprise affairs, Committee

of Competition Law and Policy.

OECD, 2001b. Extended Producer Responsibility: a guidance manual

for Governments.

Psoinos, D., 1989. Implemented Statistics. Zitis Publications, Thessa-

loniki (in Greek).

122 A. Karagiannidis et al. / Waste Management 26 (2006) 110–122

Skumatz, L.A., Truitt, E., Green, J., 1997. The state of variable rates:

economic signals move into the mainstream. Resource Recycling,

29–35, August.

Smeets, E., Weterings, R., 1999. Environmental Indicators: typology

and overview. European Environment Agency. Technical Report,

No. 25.

Tagaras, G., 2001. Statistical Quality Control. Zitis Publications,

Thessaloniki (in Greek).

www.payt.net, Official website of the PAYT Project, A Joint

Research Project funded by the European Commission under

the environmental component Energy, Environment and Sus-

tainable Development, within the Fifth Framework

Programme.

Xirogiannopoulou, A., Karagiannidis, A., Moussiopoulos, N., 2002.

AUTh Consolidated Report. DG Research, 5FP-Project PAYT.

In: 4th Working Meeting: Dresden. 7–9 November.