Embed Size (px)

Citation preview

4

Vision “ The strategic partner in providing innovative banking solutions to customers internally and externally “

Mission

“We strive to satisfy all partners and clients through provision of prominent banking products in advanced technology by qualified cadres with dedication to sustainable excellence”

5

4Bank Directory ...............................................................................................................

7The bank strategy...........................................................................................................

8Board of Directors .........................................................................................................

9Shariah Supervisory Board ............................................................................................

10Top Management ..........................................................................................................

12Executive Management .................................................................................................

13Indicators of Global Economy during 2018...................................................................

14Indicators of Performance of National Economy during 2018 .....................................

15Classification of Omdurman National Bank in 2018 ....................................................

16Indicators of Financial Performance of the Bank ........................................................

18Report of Board of Directors on 2018 performance in thetwenty third general assembly meeting ..........................................................................................................

21Shariah Supervisory Board Report ................................................................................

22National Audit Chamber Report ..................................................................................

24Statement of Financial Position as at 31/12/2018 .........................................................

25Income Statement of the year ended at 31/12/2018 ......................................................

26Statement of cash Flow of the year ended at 31/12/2018 .............................................

27Statement of Changes in Equity as at 31/12/2018 .....................................................

28Notes to Financial Statements as at 31/12/2018 ...........................................................

ConTenTs

Item Page

6

Omdurman National Bank was founded as a public shareholders company in January 1993 and the bank resumed its activities in August 1993 by providing all types of banking and investment services that comply with the principles and norms of Shariah law. The Bank is considered as the most important and main pillar of the national economy in the field of banking, investment and external trade through a network of correspondents that spread all over the world.

The bank`s most important objectives: * Collection and mobilizing Sudanese peoples` savings inside and outside Sudan.* Financing the internal and foreign trade operations and activation of cross relationships with the international banks and financial institutions.* Financing of private sector needs.* Contribution to financing the different economic sectors and investment portfolios.* Contributing effectively to the social responsibility and support of the state efforts in broadening the microfinance base and social-oriented finance as well as supporting artisans and small producers.* Deepening and development of Islamic financing formulas.* Financing projects of the economic development in the fields of mining, agriculture, industry , transportation and different infrastructural projects. The Bank Memberships in Institutions and Unions: The bank is prominent for its memberships in many local, regional and international institutions and unions.

The most important of these institutions and unions are: * Membership in Sudanese Banks Union ( SBU)* Membership in the Union of Arab Banks ( UABS)* Membership in Accounting and Auditing Organization for Islamic Financial Institutions ( AAOIFI).* Membership in Sudanese Banking Deposits and Savings Fund (BDSF).* Membership in SWIFT network.* Membership in Association of Development Financing Institutions (ADFIMI)* Membership in the Council of Islamic Banks and Financial Institutions (CIBAFI).* Membership in International Islamic Center for Resolution and Arbitration (IICRA)* Many other regional and international institutions

Bank DireCTory

7

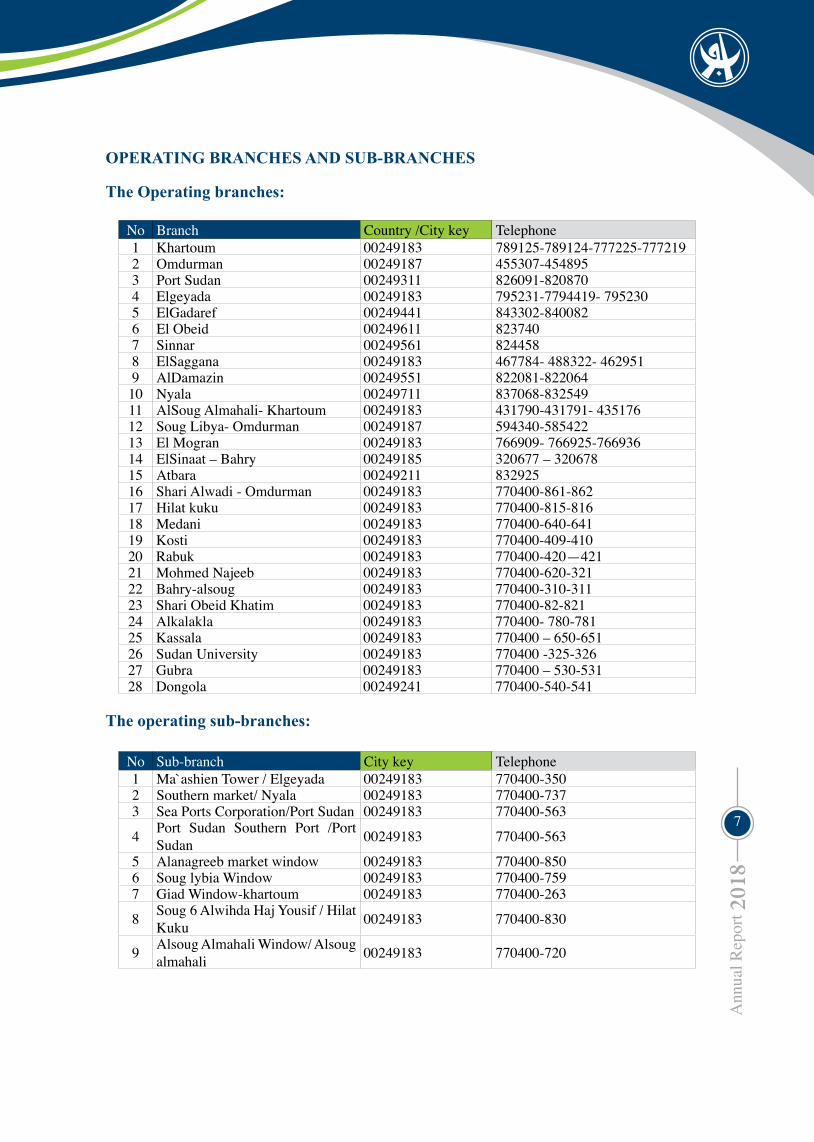

operaTing BranChes anD suB-BranChes

The operating branches:

No Branch Country /City key Telephone 1 Khartoum 00249183 789125-789124-777225-7772192 Omdurman 00249187 455307-4548953 Port Sudan 00249311 826091-8208704 Elgeyada 00249183 795231-7794419- 795230 5 ElGadaref 00249441 843302-8400826 El Obeid 00249611 8237407 Sinnar 00249561 8244588 ElSaggana 00249183 467784- 488322- 4629519 AlDamazin 00249551 822081-822064

10 Nyala 00249711 837068-83254911 AlSoug Almahali- Khartoum 00249183 431790-431791- 43517612 Soug Libya- Omdurman 00249187 594340-58542213 El Mogran 00249183 766909- 766925-76693614 ElSinaat – Bahry 00249185 320677 – 32067815 Atbara 00249211 83292516 Shari Alwadi - Omdurman 00249183 770400-861-86217 Hilat kuku 00249183 770400-815-81618 Medani 00249183 770400-640-64119 Kosti 00249183 770400-409-41020 Rabuk 00249183 770400-420—42121 Mohmed Najeeb 00249183 770400-620-32122 Bahry-alsoug 00249183 770400-310-31123 Shari Obeid Khatim 00249183 770400-82-82124 Alkalakla 00249183 770400- 780-78125 Kassala 00249183 770400 – 650-65126 Sudan University 00249183 770400 -325-32627 Gubra 00249183 770400 – 530-53128 Dongola 00249241 770400-540-541

The operating sub-branches:

No Sub-branch City key Telephone 1 Ma`ashien Tower / Elgeyada 00249183 770400-3502 Southern market/ Nyala 00249183 770400-7373 Sea Ports Corporation/Port Sudan 00249183 770400-563

4 Port Sudan Southern Port /Port Sudan 00249183 770400-563

5 Alanagreeb market window 00249183 770400-8506 Soug lybia Window 00249183 770400-7597 Giad Window-khartoum 00249183 770400-263

8 Soug 6 Alwihda Haj Yousif / Hilat Kuku 00249183 770400-830

9 Alsoug Almahali Window/ Alsoug almahali 00249183 770400-720

8

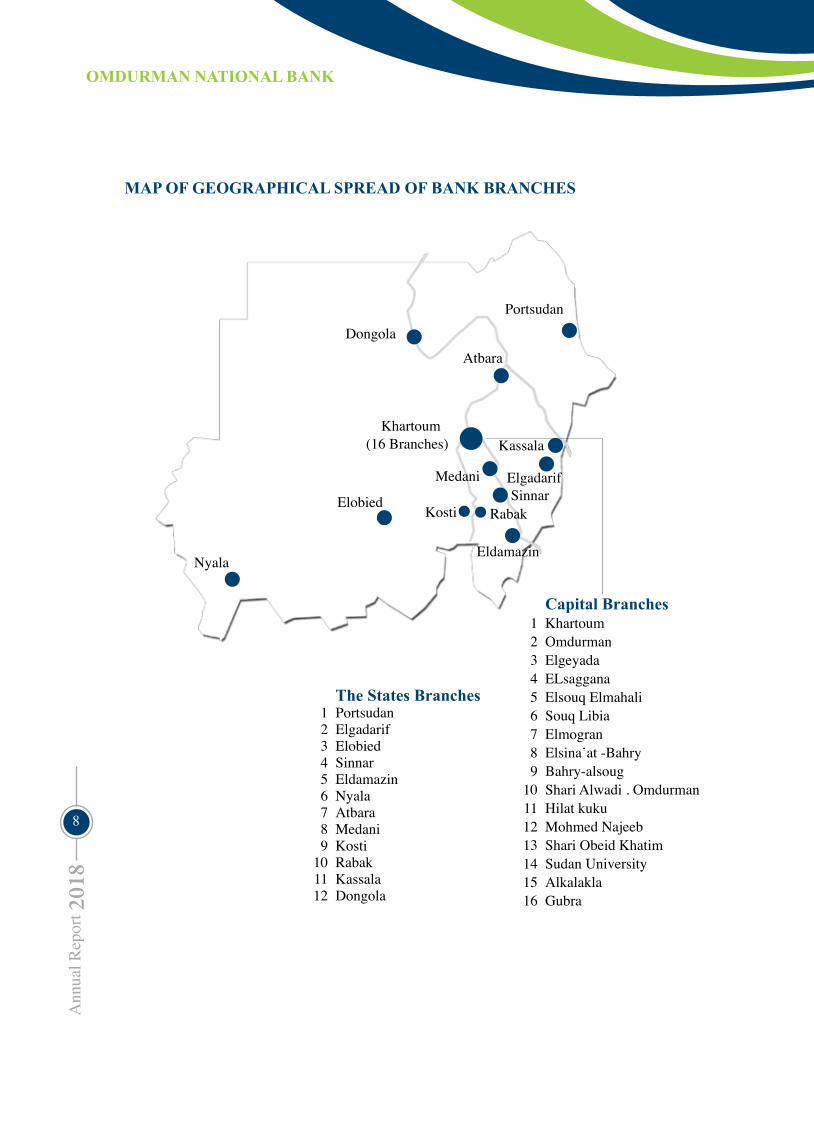

Map of geographiCal spreaD of Bank BranChes

Khartoum

Portsudan

Elgadarif

Elobied Sinnar

EldamazinNyala

Capital BranchesKhartoum1Omdurman2Elgeyada3ELsaggana4Elsouq Elmahali5Souq Libia6Elmogran7Elsina’at -Bahry8Bahry-alsoug9Shari Alwadi . Omdurman10Hilat kuku11Mohmed Najeeb12Shari Obeid Khatim13Sudan University14Alkalakla15Gubra16

The states BranchesPortsudan1Elgadarif2Elobied3Sinnar4Eldamazin5Nyala6Atbara7Medani8Kosti9Rabak10Kassala11Dongola12

(16 Branches)

Atbara

Dongola

Kassala

Medani

Kosti Rabak

9

The bank`s strategy aims to realize its mission in contributing strongly in building its country based on its people`s inherited civilization and values to realize its objectives for the good of its all relevant partners. Also, the strategy aims to achieve the vision of

the bank for providing its client with distinct banking services in order to meet the ambitions of depositors, investors as well as shareholders. In this course, the bank will use the best banking technologies and instruments that will be offered through qualified cadres foreseeing brighter future for Sudan. The most important features of the bank strategy are as follows: 1. Commitment to adjust the bank various activities by the principles and provisions of Islamic Shariah .2. Using the latest available banking technological systems to improve and promote the quality level of the provided banking services and satisfy its clients.3. Developing the skills and the experiences of the human capital through continuous training and capacity building.4. Optimizing the use of resources to increase the income, maximizing revenues and maintain low cost rate.5. strengthening and expanding the bank`s external relationships.

1. The bank looks forward to continue focusing on developing the banking technology through completing the phases of introducing the new electronic banking system so as to cope with the modern banking industry.2. The bank strives to incur sustainable improvement in the banking services quality and the levels of clients satisfaction

3. The bank is working to maintain its pioneering position in the Sudanese Banking sector in terms of capturing the lion`s share of assets , deposits and finance.

The Bank sTraTegy:

The Bank`s fuTure plans:

10

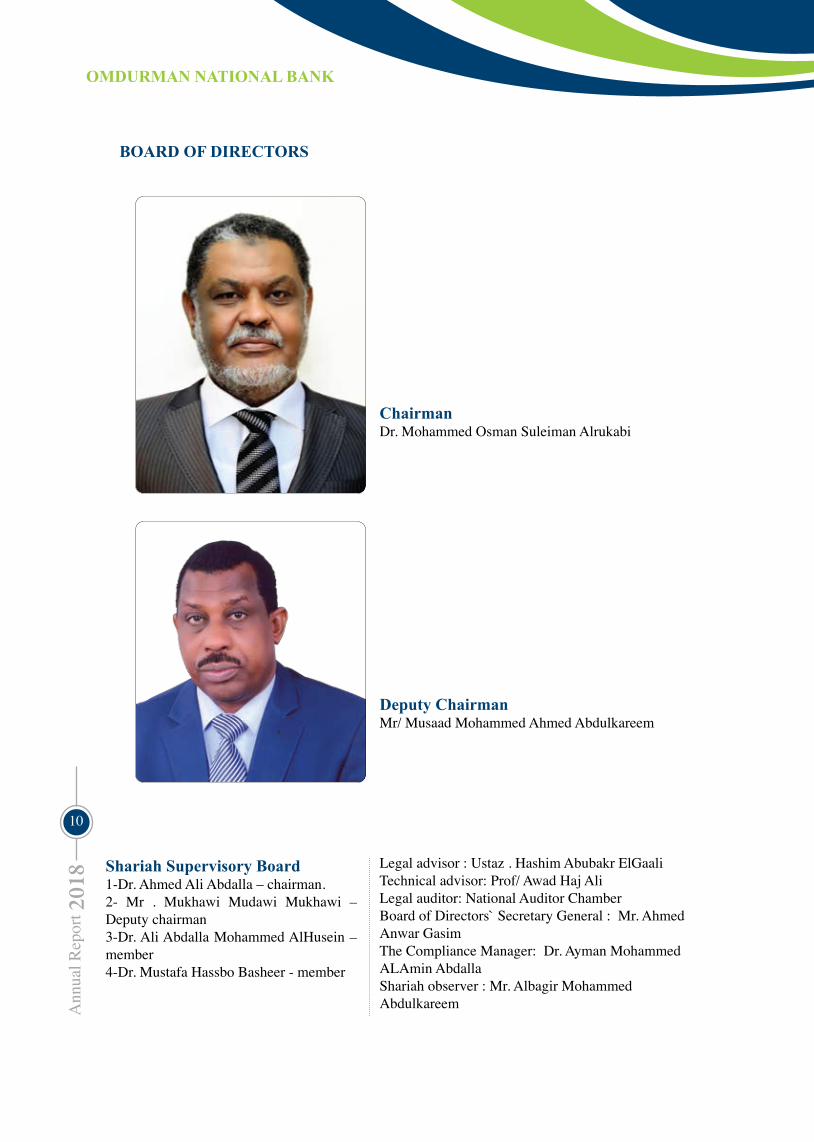

BoarD of DireCTors

ChairmanDr. Mohammed Osman Suleiman Alrukabi

Deputy ChairmanMr/ Musaad Mohammed Ahmed Abdulkareem

shariah supervisory Board 1- Dr. Ahmed Ali Abdalla – chairman.2- Mr . Mukhawi Mudawi Mukhawi – Deputy chairman3- Dr. Ali Abdalla Mohammed AlHusein – member4- Dr. Mustafa Hassbo Basheer - member

Legal advisor : Ustaz . Hashim Abubakr ElGaaliTechnical advisor: Prof/ Awad Haj AliLegal auditor: National Auditor ChamberBoard of Directors` Secretary General : Mr. Ahmed Anwar GasimThe Compliance Manager: Dr. Ayman Mohammed ALAmin Abdalla Shariah observer : Mr. Albagir Mohammed Abdulkareem

11

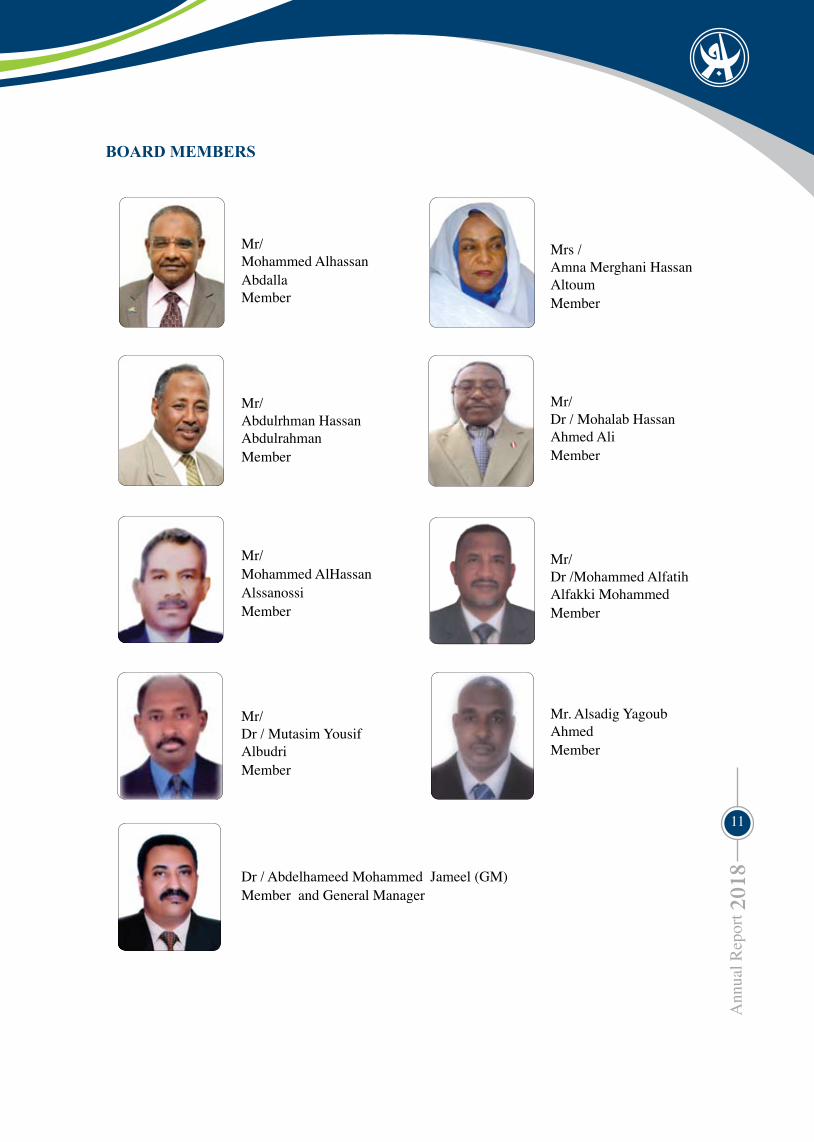

Mr/ Mohammed AlHassan Alssanossi Member

Mr/Dr /Mohammed Alfatih Alfakki MohammedMember

Mr/Dr / Mohalab Hassan Ahmed AliMember

Mr/ Dr / Mutasim Yousif AlbudriMember

Mr. Alsadig Yagoub Ahmed Member

Dr / Abdelhameed Mohammed Jameel (GM)Member and General Manager

Mrs /Amna Merghani Hassan AltoumMember

Mr/Mohammed Alhassan AbdallaMember

BoarD MeMBers

Mr/Abdulrhman Hassan Abdulrahman Member

12

Dr. abdelhameed Mohammed Jameel

general Manager

Top ManageMenT

13

Mr. Yahia Mohamed Mukhtar

Deputy general Manager

assistants general Manager

Mr. Ahmed Albasheer Moh. AhmedAssistant G.M for Operations

Mr. Mohammed Alamin Alhaj AlhusseinAssistant G.M for Policies &

Administration

14

exeCuTiVe ManageMenT

DireCTors of DeparTMenTs: No Director Department 1 Mr. Abdalla Khogali Mohammed Elfaki Technology Projects Unit2 Dr. Omer Hassan Ahmed Hassan Alhareef Internal Audit3 Mr. Hussein Mohammed Ali Omer Human Resources Development4 Mr. Nuraldeen Ahmed Mohammed Abdelmajeed Risk Management5 Mr. Mohammed Abdalla Ali Alshier Information technology 6 Mr. Faisal Mahmoud Abdalla Ahmed Managerial Services7 Mr. Isamedin Abdelrahim Ibrahim Finance and Credit8 Dr. Atif Alsheikh Ali Mohammed Marketing 9 Mr. Isamedin Abuazeib Abu Central Operations 10 Mr. Abdulaziz Hassan Mohammed Ahmed Kareiri Systems and Development11 Mr. Khalfalla Saeed Mohammed Ahmed Financial Affairs12 Mr. Osama Mohammed AlKheir Okasha Legal affairs 13 Mr. Siddig Mohammed Farajalla External Relations and treasury 14 Dr. Mohammed Hussein Abdulrahman Hashim Planning and Quality(Acting)15 Mr. Ihab Mohammed Osman Executive Office

The BranChes Managers: first: khartoum state Branches:No Manager Branch 1 Mr. Osama Abdulrahman Mohammed Ali Khartoum 2 Mr. Moawia Ahmed Hussein Soug Almahali-Khartoum3 Mr. Amir Hassan AlBasheer AlHassan Elgeyada4 Dr. Anas Osman Hassan Malik El Mogran5 Mr. Yousif Hashim Ahmed Alfaki Omdurman6 Dr. Mohammed AlHassan Abdelghani Soug Libya- Omdurman7 Mr. Ibrahim Mahmoud Yasin Krar ElSinaat – Bahry8 Mr. Osman Mohammed Alazrag Ahmed ElSaggana 9 Mr. Abdulrhman Babiker Ali Osman Shari Alwadi- Omdurman10 Mr. Ammar Abdalla Mohammed Abdalla Hilat kuku11 Mr. Imadeldin Merghani Alnier Mohammed Najeeb12 Mr. Salih Mohammed Abdalla Bahry-alsoug13 Mr. AlZubeir Idriss Mohammed Ali Shari Obeid Khatim14 Mr. Mohammed Alhassan Mohammed Ali Alkalakla15 Mr. Khalid Ahmed Mohammed Abd Alhafeez Sudan University16 Mr. Abdulfatah Alawad Alhassan Gubra

second: other states Branches:No Manager Branch 17 Mr. Ali Abdulateef Abdulrahim Port Sudan18 Mr. Faris Hassan Albnna Kuku AlDamazin19 Mr. Omer Mohammed Ahmed Abdalla Atbara20 Mr. Hassan Almusaad Lili Ahmed Nyala21 Mr. Izzeldeen Ali Mohammed Elhaj El Obeid22 Mr. Tajeldeen Ibrahim ElSheikh ElGadaref23 Mr. Hamza Aldaw Basheer Aldaw Sinnar (acting)24 Mr. Omran Abdalla Abdelrahim Medani25 Mr. Mohammed Ahmed Musa Hamdtalla Kosti26 Mr. Sami Izzeldeen Mohammed Elhadi Rubak27 Mr. Mohammed Onour Mohammed Ismaeel Kassala28 Mr. Abdulhafeez Mohammed Mohammed Kheir Dongola

15

inDiCaTors of gloBal eConoMyDuring 2018

The growth rates of the global economy during 2018 reached 3.7% compared with 3.8% in

2017, as the economic activity in the advanced economies witnessed a remarkable decrease with - 0.1 % in 2018 compared with growth of 2.3 % in 2017. Whereas the developing countries’ economies witnessed growth with 4.6% , as the Brazilian scored growth rate of

1.3% in 2018 compared with (1.1%) in 2017, also, the Russian registered growth rate of 1.7%

in 2018 compared to decrease with (1.5%) in 2017 whereas China scored growth rate of (6.6%) and India

(7.3%) to be regarded as the biggest expected growth rates in 2018. For the economies of Middle East , North Africa, Afghanistan and Pakistan, the growth rates registered an increase with 2.4% in 2018 compared to 2.2% in 2017. The international Trade: The international trade grew in 2018 by 4% compared to 5.3 % in 2017. The advanced economies witnessed decrease as they decreased by 3.2% in 2018 compared with 4.3% in 2017 . Also, the economies of the emerging markets and developing economies increased by 5.4% in 2018 compared to 7.1% in 2017. Prices of Oil and Raw Materials: The oil barrel prices in US Dollar for Brent crude oil of the United Kingdom, Fatih.Dubai and Western Texas Intermediate reached $ 68.58 US Dollar for a barrel in 2018 , compared to $ 52.7 US Dollar in 2017. Whereas the consumer goods in the advanced economies registered change rate of 2% in 2018 compared to 1.7% in 2017. For the economies of emerging markets and developing economies the change rate registered is 4.9% in 2018 compared with 4.3% in 2017

Sources : * world Bank * International Monetary Fund

16

Sources : * world Bank * International Monetary Fund

The year 2018 witnessed a number of economic changes at the local and

regional levels that had a major effect on the Sudanese economic indicators. The most important indicators1 are as follows: gross Domestic product (gDp):

According to the data estimates, Sudan economy incurred growth with 2.3% in

2018, compared to growth rate of 1.4% in 2017 this is due to decrease oil exports and revenues of gold exports. Inflation Rate: The average inflation rate reached 72.9% in 2018 compared with 32.6% in 2017 foreign Trade:The Sudanese exports reached $ 3.5 billion US Dollars in 2018 compared to $ 4 billion in 2017. And the imports reached $ 7.9 billion in 2018 compared to $ 9.2 billion in 2017.The Monetary indicators and exchange rate: The money supply at the end of 2018 reached SDG 431 billion compared to SDG 203 billion at the end of 2017The average exchange rate of the European currency (Euro) in December 2018 was SDG 54.03 compared to SDG 8.43 in December 2017. Deposits and finance:The deposits in the Sudanese commercial banks increased to SDG 303 billion at the end of 2018 compared to SDG 140 billion in 2017. The volume of the banking finance reached SDG 147 billion by the end of 2018 compared to SDG 103 billion of finance in 2017.

inDiCaTors of perforManCe of naTional eConoMy During 2018

17

The bank was rated in 2018 , according to the regional and international institutions, in a leading position at the top of the sudanese banks. This rating included the following:a) Omdurman National Bank was rated in 2018 by the Islamic International Rating Agency in terms of financial performance, governance and institutional and Shariah

control.The total credit score of the bank is in the range of 71-75, reflecting adequate credit standards, where the

rights of Different interests are adequately protected .b ) Omdurman National bank has been awarded the prize of the

First Bank in Sudan in 2018 ,for the fourth consecutive year and the tenth since establishment of the so-called prize , by “ The Banker Awards “ magazine that issued by the British Financial Times institution, for possessing the largest assets volume , beside the highest rates of return on ownership equity and net profits as well as the bank`s ability to absorb the crises and overcome the difficulties which may obstruct its march forward.c ) Omdurman National Bank has been awarded the prize of the compliant financial institutions in line of the social responsibility of 2017 for the Islamic Banks. This is among 12 Sudanese banks through sessions of Conference and prize of the social responsibility for Islamic Banks in 2017 which held in the Kingdom of Bahrain d ) Omdurman National bank has been awarded the Arab prize of the productive families of 2016 as the best Bank that supports and nurtures the productive families for 2016. This competition is organized by Bahrain Kingdom every two years through the Ministry of Labor and Social Development in Bahrain.e ) The Omdurman National bank has been awarded the national prize of the productive families for 2016 that is provided annually by Ministry of Social Care and Insurance in Sudan.f ) The Omdurman National bank has maintained its pioneer position among the Sudanese banks, occupying the rank no (81) in the list of the biggest Islamic institutions and the rank no (73) in the list of the Islamic banks in the world, and the rank no (1) in the list of the Sudanese Financial institutions according to the rating of (The Banker) of the British Financial Times issue of 2013.g ) The Omdurman National bank has maintained its leading position among the Sudanese banks in the list of the Biggest 150 Arab banks according to the rating of the Journal of Arab banks Union for the years 2007, 2008, 2009 , 2010 and 2011. h ) The Omdurman National bank has occupied the rank no (81) in the list of the Biggest 100 African banks according to the rating of “ the Banker “ magazine issue of January 2014.i ) The Omdurman National bank has occupied the rank no (117) in the list of the first 150 Arab banks in terms of shareholders rights according to the rating of “ Economics and Business “ magazine – Bruit in the issue no 418 of October 2014.

The raTing of oMDurMan naTional Bank up To 2018

18Assets Demand deposits

inDiCaTors of finanCial perforManCe of The Bank(2012 -2018)

The following table shows the most significant financial indicators:

(in 1000 SDG)Description 2012 2013 2014 2015 2016 2017 2018Assets 9,165,359 10,561,174 12,607,097 13,992,164 15,574,165 28.358,964 75,530,186Demand deposits

2,115,397 2,413,425 2,864,531 4,787,312 5,741,962 10,494,701 25,568,458

Investment deposits

4,489,368 5,275,374 5,657,779 6,552,219 7,009,359 13,872,458 42,460,574

Paid up capital

800,000 800,000 800,000 800,000 800,000 1,000,000 1,340,055

Equity 1,121,817 1,217,670 1,306,296 1,469,842 1,615,911 2,143,895 3,333,115Revenues 707,706 714,943 887,073 1,196,336 1,651,733 2,383,067 4,397,672Operating Expenses

118,444 141,016 165,977 212,635 298,006 362,434 591,782

Provisions 110,580 30,569 75,281 66,303 60,975 120,800 126,187Net profits 102,331 166,594 258,944 396,806 479,348 703,485 1,478,782

19

Investment deposits Paid up capital

Equity Revenues

Net profits

20

reporT of ChairMan of BoarD of DireCTors on 2018 perforManCe in The 23nD general asseMBly

In the Name of Allah the Most Gracious the Most Merciful

Dear Brothers..Allah`s peace , mercy and blessing be upon you Praise is to Allah with Whose grace the righteous are done, and utmost peace and blessings be upon the most honourable creature – our messenger, Mohammed and to his family and followers.honorable Brothers..Today , I am fully proud to meet you in our regular 23nd meeting of the bank general assembly to evaluate the performance during the past year 2018, as that year (2018) witnessed the bank celebration about its silver jubilee on August 14th 2018 under the theme “ 25 years of prominence and accomplishment” then the celebrations continued to the end of the year and the bank silver jubilee has come as gratitude conveyed to the founders ; as documentation for accomplishments and striving for future as we look forward to realizing a new vision with modern concepts “ by the Will of Allah” serving the Islamic banking and improving the national economy and the welfare of the dignified Sudanese people.In the year 2018 , we , with praise to Allah and By His Support, managed to realize all our strategic goals and upgrade the institution through the intent and dedicated work and joined cooperation and collaboration among the board of directors, its different committees, the executive management and the bank staff despite all these adverse economic situations. Dear Brothers ..We meet to day to go through the most important accomplishments made by the bank during 2018 and specify the pros and cons, to enhance the pros avoid the cons stressing our sustainable commitment towards our new mission and vision for being the most perfect partner in submitting innovative banking solutions to its customers inside and outside Sudan and to continue in the leading position for Sudanese banking system as well as being a model for national institutions in supporting the national economy. honorable Brothers..The bank witnessed remarkable progress in its business size and results, continuing its leadership of the Sudanese banks in 2018 as a result of the adoption of an ambitious strategy which took into consideration all the external and internal effects, depending on the same pattern of previous performance with professionalism, institutional control and transparency. In the beginning, please excuse me to summarize the most important financial results achieved by the bank in 2018 which reflects , in all its indicators , a positive growth in all data . And it is the thing that assisted the

bank to maintain its pioneer position in the banking system. It is important to mention that the bank managed to realize the objectives of the plan and budget for 2018 with higher performance and praise is to Allah. These indicators are as follows: firstly: assets: The Total Assets reached SDG 75.53 billion in 2018 compared to SDG 28.36 billion in 2017, registering a growth rate of 166%. secondly: liabilities and investment Deposits: The liabilities in 2018 reached SDG 72.20 billion compared to SDG 26.22 billion in 2017 with growth rate of 175%.The most important liabilities and investment deposits are as follows: 1) Total deposits: The total deposits in local and foreign currencies reached SDG 68.03 billion in 2018 compared to SDG 24.43 billion in 2017 with growth rate of 180%. And this is apparently displayed in the following: 1- current deposits: The total current deposits in 2018 reached SDG 20.13 billion compared to SDG 7.85 billion in 2017 with growth rate of 156%.2- Saving deposits:The saving deposits increased in 2018 to reach SDG 3.1 billion compared to SDG 1.6 billion in 2017 with growth rate of 90%.3- Insurances and margins :The insurances reached SDG 2.62 billion in 2018 compared to SDG 1.04 billion in 2017 with growth rate of 153%. 4- Investment deposits ( investors accounts):The investment deposits reached SDG 42.5 billion in 2018 compared to SDG 13.9 billion in 2017 with growth rate of 206%.Thirdly: equity:The equity increased in 2018 with 55% in comparison to 2017 as it reached SDG 3.33 billion in 2018 compared to SDG 2.14 billion in 2017. This increase is greatly attributable to increase of the paid-up capital , profits and the reserve.fourthly: the bank investment activities:The bank has continued playing its leading role of supporting the national economy, as the size of finance and investment for the various sectors has reached SDG 22.7 billion by the end of 2018 compared to SDG 15.3 billion in 2017 registering a growth rate of 48%.The bank continued its special strategy of financing

21

public and private sector companies operating in line of infra-structure and development projects. Also, the bank contributed to all financing portfolios executed by the banking system covering the fields of industry , agriculture , mining , energy , oil , and infra-structure.. Also, during 2018, many roads was financed such as the national exports road ( Omdurman – Gabrat Elsheikh – Bara ) with the length of 105 klm and fund size of SDG 250 million. Besides , Alseleim – Nawa road in Shimalia state with fund size exceeding SDG 247 million.With regard to the finance of the small sectors and productive families, the bank continued its policy of supporting this sector believing that, supporting these segments and helping them to enter the production cycle is the best way for alleviating poverty as well as broadening the base of economic activities to increase the Gross Domestic Production (GDP). In this scope the bank has adopted the expansion of the micro-finance umbrella and activities through focusing on the training of the targeted groups before offering the finance in a shape of consecutive classes in coordination with organizers. Accordingly the bank has held more than (30) training courses during the last five years training more than 3200 persons from the targeted groups of : martyrs` families , military pensioners , widows and groups coordinated with Sudanese Women Union and all were offered the finance. This experience proved to be successful as it is clearly apparent in the improvement of the living standards of the beneficiary families and nearly no default registered.The bank also always uses a notable portion of its finance portfolio in financing other sectors those have social dimension.fifthly: foreign trade: The bank role , as a financial firm supporting the Sudanese economy especially in the field of foreign trade, has appeared to be the best strategic partner bank in line of exports and imports despite the economic difficulties. As the bank managed to succeed in executing the export and import operations for its customers and this is greatly attributed to the bank meticulous internal policies of foreign currency management that helped a lot in strengthening the relationships of the bank with correspondents through meeting the commitments towards those correspondents. And after the resolution of alleviating the economic sanctions from Sudan , the network of correspondents expanded all over the world especially in Europe and Asia. sixthly: Gross Income and Net profits (income statement): The bank net profits reached SDG 1479 million as at

the end of 2018 compared to SDG 703 million in 2017 with growth rate of 110%. These profits were realized as a result of the high revenues accomplished this year reaching SDG 4.4 billion before the deduction of the profits of investment deposits at an operating cost rate not exceeding 13% of revenues. Knowing that the international standard of operating cost rate is 35% and this is clearly refers to the effectiveness of the bank in generating revenues and the good management of expenses. And the total cost rate approximately reached 27% in 2018 compared to the international standard rate of 55%. Seventhly : Investment Deposits Profits: The Investment Deposits Profits reached SDG 1638 million at the end of 2018 compared to SDG 980 million in 2017. The profits were distributed at the rate of 15% for the long-term deposits and 13.5% for absolute and restricted deposits in local currency compared to 15% , 14.5% consecutively in 2017. Also, profits were distributed at the rate of 6% distributed for the deposits in foreign currency in 2018 , the same as in 2017 , referring to that the investment deposits size reached SDG 42.5 billion with the rate 42% of the investment deposits in the banking system at the end of 2018.eighthly: the technical services:In 2018, the bank continued applying and activating its technical strategy that targets upgrading the banking technical services through the e-payment tools in the bank (sale points, ATMs , SMS, ONB application , e- portfolio and banking internet)for they are alternatives that support the gradual transformation from using cash banknotes to to cashless society. As the bank expanded its services to the customers covering all commercial transactions and activities such as power purchase , mobile balance , registration to universities and bill payment to custom corporation ..etcWithin the context of the bank coping with the electronic government project , the bank signed many contracts during the year 2018 with specialized bodies in line of e-payment technology resulting in provision of e-portfolio service to all citizens , as the year 2018 witnessed inauguration of the electronic ONB portfolio card in the people civil record service complexes ( Alsaggana , Omdurman and Bahry). Ninthly: Early warning indicators:The year 2018 witnessed a remarkable stability in the bank rating according to the preventive supervisory standard (CAEL) and the quarterly reports of Central Bank of Sudan. As the bank rank remain stable at “ Satisfactory” level. Dear honorable Brothers The human resource development is the main base and the key of success and accomplishments. So, the board

22

of directors and executive management concentrate on providing an excellent working environment for the staff and on improvement of their performance through the continuous training program inside and outside Sudan. The training opportunities in 2018 reached 16800 ones inside and outside Sudan at the rate of more than one training course for an individual.Also, the management has been keen in its policy of granting incentives to the staff, and continuously improving their living and financial standards, as the year 2018 witnessed an increase in the number of promoted employees and increased loans allowed to employees in order to achieve the job satisfaction , urging them to exert more efforts as well as the activation of the programs of strengthening the social ties among the staff.All these above has had positive reflection on the staff performance in the bankand realization of the bank different goals as well as 3nabling the bank to maintain its human capabilities boosting the staff loyalty towards the bank Dear honorable Brothers.. The bank financing and banking services have been reflected on the variable local and national mass media. The thing that assist a lot in intensifying the image of the bank on the people conscious and that has led to creation of new dimension of marketing activity. In the context of the bank strife for amplifying its market share, the financial comprehensiveness strategy was executed, as the period of 2016 to 2018 witnessed opening of 17 branches such as two branches of Kosti and Rubak in White Nile state; Medani in Gezira state ; AlThora bewadi branch in Krare locality ; Hilat Kuku branch in Sharg ekneel locality ; Mohammed najeeb ; Bahry alsoug ; Obeid Khatim ; Alkalkla ; Sudan University ; Kassala branch in Kassala state and Gubrabranch in Khartoum state. This is in addition to two windows of soug alangreeb and sough lybia in Omdurman beside Giad tower , soug almahli, Khartoum , Soug 6 Haj Yousif Alwihda windows. In this year Dongola branch was opened in Shimalia state. More bank branches will be opened in Khartoum state and other states. Dear honorable brothers.. Praise and gratitude to Allah for that the project of ONB Tower has been inaugurated through purchase of land with total size of 14 thousand meter square facing the While Nile river in Sunut city in the Nile Confluence commercial area. The tower design was selected by consultant engineering committee. During this year we will start the work to get the iconic accomplishment to be high architectural minaret in the capital Khartoum to suit the first bank in Sudan. Dear attendees In regard to social responsibility, the bank has continued its usual role of the direct support to the

needs of the community (individuals and institutions) such as the rehabilitation of education , health , religious institutions. Also, the year 2018 witnessed the continuation of the orphan joy project which includes distribution of Eid dress and wears among the orphan children besides, the bank released in 2018 many financing packages targetibg corporations , unions and woman association as the bank inaugurated the product of “ Your Ommra is Our Responsibility” to finance the ceremony of the Holly lands Visit. Believing in the importance of the youth role in all lines , the bank organized sport sessions for youth and youngsters in a number of states in Sudan. Also, the bank has continued its remarkable activity in the Holly Month Ramadan of daily providing food and beverages to 3000 person during the month in the grand mosques of Khartoum, Khartoum North and Omdurman. Besides, it provides food and beverages to the passerby in the main streets of the capital. Dear honorable Brothers As culmination to the bank`s accomplishments during 2018, the bank has occupied many advanced positions and ranks in the classifications conducted by the specialized regional and international financial and banking institutions at the regional and global levels.. As the bank managed to maintain its leading position in the Sudanese banking system in 2018 obtaining the rank no (1) in Sudan of 2018, according to the classification of “ The Banker” the British magazine for the four consecutive year and tenth times since its establishment. Also, the bank has occupied its pioneering position among the giants group in the world as many of banking and financial institutions from 149 countries have won this prize Dear Brothers:Praise be to Allah for these remarkable accomplishments which have been achieved by Allah`s Divine support, and as the result of the joint efforts exerted by shareholders, board of directors, its committees, the top executive management and the staff.Also, we assure that the march of accomplishments will never cease to this limit deeply believing that Omdurman National Bank will continue to be the first choice for clients in Sudan and for outside correspondents banks as well. Finally, we submit our recommendations for your honorable assembly for approval of the Financial statements, the Reports of Board of Directors, National Audit Chamber , Shariah Supervisory Board and legal advisor. Also, we submit our proposal for profits distribution for the year 2018.

On Allah we rely and He leads the righteous wayPeace be upon you

Dr. Mohammed osman suleiman alrukabi Chairman of board of directors

23

In the Name of Allah the Most Gracious the Most Merciful

shariah superVisory BoarDRamadan 16th 1440May 21st 2019

shariah superVisory BoarD reporT of 2018

Praise is to Allah – the Generous Patron and pray be to our master, Mohammed peace be up on him and his family Dear shareholders of Omdurman National BankPeace and Allah`s blessings be upon youReferring to the foundation order of Shariah supervisory board, the standard of Islamic financial institutions governance and Central Bank of Sudan mandate about appointment of Shariah supervisory board with its responsibilities and reports.The Shariah supervisory board present to Omdurman National Bank general assembly the following report:The responsibility of commitment to the articles of Islamic Shariah and its principles beside doing of all bank daily transactions in accordance with the above is borne by the bank management to be regarded as routine work and executive activity and the board in collaboration with training administration offer the training programs as well as issuance of Islamic consultation “Fatwa”, resolutions and directives that lay the basics of the banking activity and elaborations of its rules. Also, the board issues an independent opinion reflecting its supervision of the bank activities and direct its remarks to realize the goal of serious work to comply with Shariah principles .The board and Shariah superintendent visited all of the bank branches and went over the audit administration report about the correctness of the bank transactions audited by it and the legal affairs about their reviewing remarks result in addition to the certificate of financial administration about spending of illegal earnings ;to charitable activities.Also, the board went over the national auditor chamber report about distribution of profits among the owners of absolute investment deposits and owners` equity beside what appears about the bank Zakat for the fiscal year 2018.So, Shariah supervisory board has come out with the following: 1/ the bank transactions revised by the board in the terminating year on 31/12/2018 were performed according to the Islamic laws and principles. 2/ the realized gains obtained from illegal sources and means were retained as an illegal gains and spent in charitable activities as mandated to. 3/ the Zakat was allocated according to Shariah principles , Zakat law and Zakat Chamber mandate.The board hereby offers its due thanks to the bank administration for its cooperation and commitment to Shariah law and principles. Besides , the due attention of the bank administration paid to encourage te staff to promote their faith and conscience spontaneously. We ask Allah success and welfare to all.

Mr . Mukhawi Mudawi Mukhawi Dr. Ali Abdalla MohmedAlhusain Deputy chairman member Dr. Mustafa Hassbo Basheer Member

24

naTional auDiT ChaMBer reporTauDiTor’s reporT To shareholDers of oMDurMan naTional Bank

In the Name of Allah the Most Gracious the Most Merciful

The opinion: We have audited the accompanying Consolidat-ed financial statements of Omdurman National Bank which consist of Consolidated statement of financial position as at December 31st 2018, income, changes in owners` equity and cash flow Consolidated statements for the year then ended and summary of significant accounting policies and other explanatory notes.

In our opinion that the enclosed Consolidat-ed financial statement are authentic and fair representation of the bank financial position as at December 31st 2018, beside its Consolidated financial performance and cash flow for the year then ended in accordance with international financial reporting standards and accounting standards issued by Auditing Organization for Islamic Financial Institution and in compliance to laws and by-laws.

The basis of opinion: We conducted our audit in accordance with International Standards on Auditing. Our responsibility in light of these standards will lately be mentioned under the article of Auditors` Responsibility about Consolidated financial statements audition. Our independence required us to be restricted to the professionalism principles according to standards and international auditing profession ethics as well as the ethical prerequisites relevant to financial statement audition.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

governance body and Management`s responsibility for the Consolidated financial statement: Management is responsible for the preparation and fair presentation of these Consolidated financial statements in accordance with international financial reporting standards and accounting standards issued by Auditing Organization for

Islamic Financial Institutions. This responsibility also includes maintaining appropriate internal control and monitoring system, in accordance with what is determined by management relevant to the preparation and fair presentation of Unified financial statements that are free from material misstatement , whether due to fraud or error.

In preparing those statements , the management will be responsible for evaluating the extent of the bank capability to proceed sustainably and reveal , if it is possible, the relevant items of sustainability. This is in addition to use the sustainability principle otherwise , the management intends to liquefy the bank or cease working or in absence of actual alternative for the management to adopt.

The responsibility of the governance body is supervising the process of the the bank financial report preparation.

auditors` responsibility about auditing the unified Consolidated financial statements : Our objectives are acquiring reasonable assurance about whether the Consolidated financial statements as whole are free from material misstatement , whether due to fraud or error. And issuing a report that reflects our opinion.

The reasonable assurance represents high degree of assurance but not enough guarantee that auditing was performed in accordance with International Standards on Auditing, as material misstatements may often be discovered when found. Errors can happen as a result of fraud or mistake and they are considered material if they are individual or collective and expected to impact the user economic decision made arising from these Consolidated financial statements.

As a part of auditing and according to those international standards, we perform the professional judgment maintaining the professional skepticism attitude throughout the

25

commercial activities inside the bank , in order to formulate our judgment about them in the Con-solidated financial statements. We are responsible for directing and supervising and performing auditing processes for the bank and we remain just responsible for our opinion in auditing.

We notify the governance body about , among other issues, the scope and time of auditing plans and its important results including any defects in the internal monitoring system that were discovered during our auditing.

One of notices reached with the governance body that we determined the most important notices during auditing the current Consolidated financial statements. And depending on that , we consider them as important notices about auditing processes. We describe these notices in our report. Except in case there is a law or by-laws preventing publicly disclosing these notices or in case that , in rare exceptional conditions, disclosing notice must not mentioned in our report for the impacts from that may harm the goals of public interest of disclosing.

AlTahir Abdulgaioom Ibrahim FCCAGeneral AuditorThe Republic of SudanKhartoum Date: 21 Ragab 1440March 28th 2019

auditing process. Also, we have performed the following:

Determining and evaluating risks and material misstatements found in the Consolidated financial statements, whether resulted from fraud or error. And design and executing auditing procedures to deal with such risks and obtaining sufficient and appropriate evidences to provide the basis for stating our opinion. The danger of not discovering the material misstatements resulted from fraud is higher than error misstatement. For fraud misstatements can entails fraudulence, intended deletion, conspiring, misleading notifications or surpassing the internal audition procedures.

Understanding the relevant internal audition so as to design appropriate auditing procedures for current conditions.

Assessing the extent of accounting policies appropriateness and the reasonability of accounting estimates and relevant disclosures performed by the management.

Judging the extent of appropriateness in management using of accountancy sustainability principle. That is raised from the auditing evidence we obtained. Whether there is material non-assurance related to events or circumstances that may raise material skepticism about the bank capability to proceed sustainably in its activity according to sustainability principle. If we deduced that there is material non-assurance, we ought to remark ,on our report, to the relevant disclosures stated on the bank financial statements. If these disclosures are not sufficient, we ought Unified to amend our opinion. Our judgments depend on the auditing evidence obtained up to our report date. Moreover, the future events and circumstances may lead to cessation of bank to proceed sustainably in its activity according to the sustainability principle.

Evaluating the general objective , structure and content of the Consolidated financial statements including the financial notes, whether they exhibit transactions and events in a fair manner.

Obtaining sufficient auditing evidences for the

26

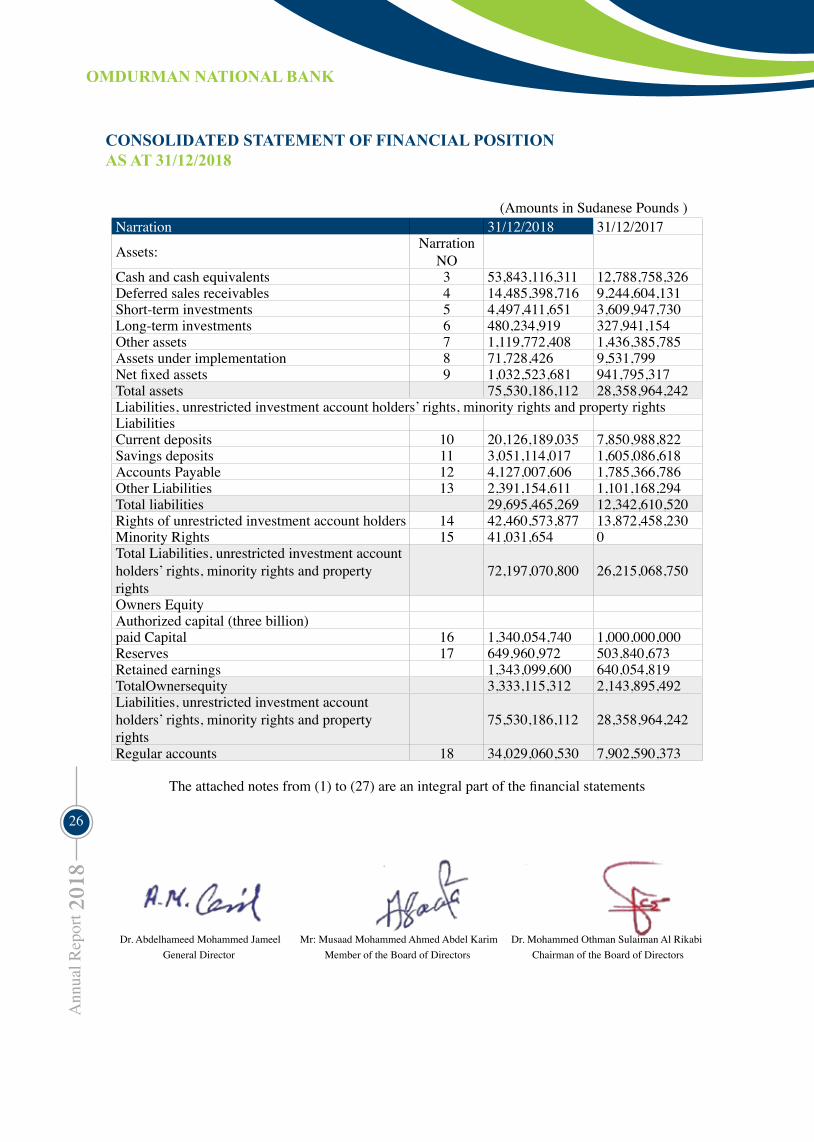

ConsoliDaTeD sTaTeMenT of finanCial posiTion as aT 31/12/2018

Dr. Mohammed Othman Sulaiman Al Rikabi Mr: Musaad Mohammed Ahmed Abdel Karim Dr. Abdelhameed Mohammed Jameel Chairman of the Board of Directors Member of the Board of DirectorsGeneral Director

(Amounts in Sudanese Pounds )Narration 31/12/2018 31/12/2017

Assets: Narration NO

Cash and cash equivalents 3 53,843,116,311 12,788,758,326Deferred sales receivables 4 14,485,398,716 9,244,604,131Short-term investments 5 4,497,411,651 3,609,947,730Long-term investments 6 480,234,919 327,941,154Other assets 7 1,119,772,408 1,436,385,785Assets under implementation 8 71,728,426 9,531,799Net fixed assets 9 1,032,523,681 941,795,317Total assets 75,530,186,112 28,358,964,242Liabilities, unrestricted investment account holders’ rights, minority rights and property rightsLiabilities Current deposits 10 20,126,189,035 7,850,988,822Savings deposits 11 3,051,114,017 1,605,086,618Accounts Payable 12 4,127,007,606 1,785,366,786Other Liabilities 13 2,391,154,611 1,101,168,294Total liabilities 29,695,465,269 12,342,610,520Rights of unrestricted investment account holders 14 42,460,573,877 13,872,458,230Minority Rights 15 41,031,654 0Total Liabilities, unrestricted investment account holders’ rights, minority rights and property rights

72,197,070,800 26,215,068,750

Owners Equity Authorized capital (three billion)paid Capital 16 1,340,054,740 1,000,000,000Reserves 17 649,960,972 503,840,673Retained earnings 1,343,099,600 640,054,819TotalOwnersequity 3,333,115,312 2,143,895,492Liabilities, unrestricted investment account holders’ rights, minority rights and property rights

75,530,186,112 28,358,964,242

Regular accounts 18 34,029,060,530 7,902,590,373

The attached notes from (1) to (27) are an integral part of the financial statements

27

Dr. Mohammed Othman Sulaiman Al Rikabi Mr: Musaad Mohammed Ahmed Abdel Karim Dr. Abdelhameed Mohammed Jameel Chairman of the Board of Directors Member of the Board of DirectorsGeneral Director

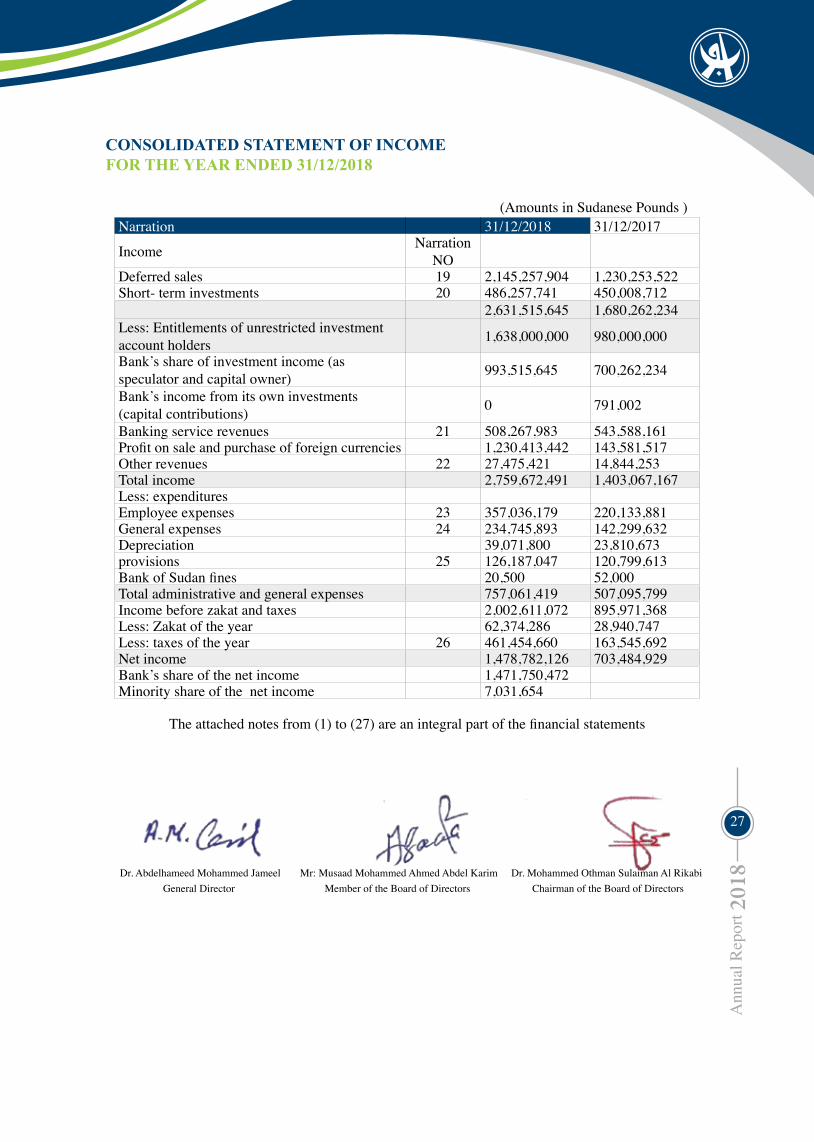

ConsoliDaTeD sTaTeMenT of inCoMe for The year enDeD 31/12/2018

(Amounts in Sudanese Pounds )Narration 31/12/2018 31/12/2017

Income Narration NO

Deferred sales 19 2,145,257,904 1,230,253,522Short- term investments 20 486,257,741 450,008,712

2,631,515,645 1,680,262,234Less: Entitlements of unrestricted investment account holders 1,638,000,000 980,000,000

Bank’s share of investment income (as speculator and capital owner) 993,515,645 700,262,234

Bank’s income from its own investments (capital contributions) 0 791,002

Banking service revenues 21 508,267,983 543,588,161Profit on sale and purchase of foreign currencies 1,230,413,442 143,581,517Other revenues 22 27,475,421 14,844,253Total income 2,759,672,491 1,403,067,167Less: expenditures Employee expenses 23 357,036,179 220,133,881General expenses 24 234,745,893 142,299,632Depreciation 39,071,800 23,810,673provisions 25 126,187,047 120,799,613Bank of Sudan fines 20,500 52,000Total administrative and general expenses 757,061,419 507,095,799Income before zakat and taxes 2,002,611,072 895,971,368Less: Zakat of the year 62,374,286 28,940,747Less: taxes of the year 26 461,454,660 163,545,692Net income 1,478,782,126 703,484,929Bank’s share of the net income 1,471,750,472Minority share of the net income 7,031,654

The attached notes from (1) to (27) are an integral part of the financial statements

28

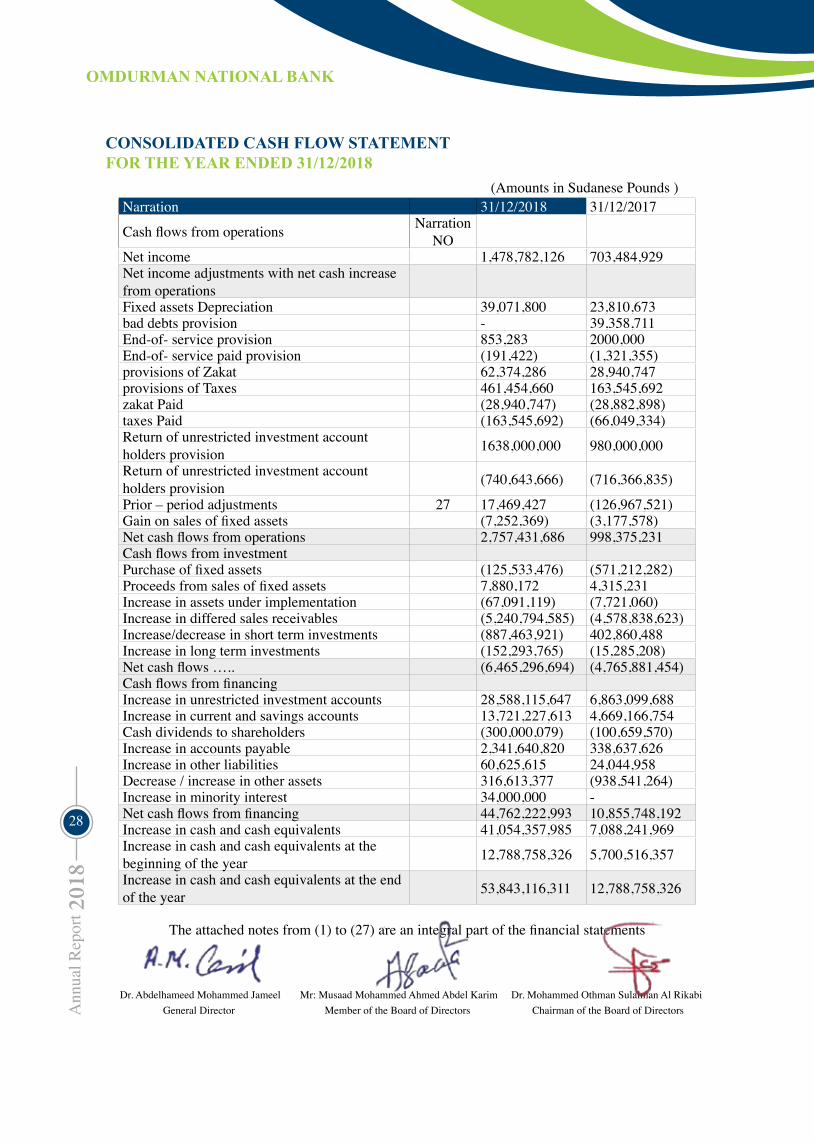

ConsoliDaTeD Cash floW sTaTeMenTfor The year enDeD 31/12/2018

(Amounts in Sudanese Pounds )Narration 31/12/2018 31/12/2017

Cash flows from operations Narration NO

Net income 1,478,782,126 703,484,929Net income adjustments with net cash increase from operationsFixed assets Depreciation 39,071,800 23,810,673bad debts provision - 39,358,711End-of- service provision 853,283 2000,000End-of- service paid provision (191,422) (1,321,355)provisions of Zakat 62,374,286 28,940,747provisions of Taxes 461,454,660 163,545,692zakat Paid (28,940,747) (28,882,898)taxes Paid (163,545,692) (66,049,334)Return of unrestricted investment account holders provision 1638,000,000 980,000,000

Return of unrestricted investment account holders provision (740,643,666) (716,366,835)

Prior – period adjustments 27 17,469,427 (126,967,521)Gain on sales of fixed assets (7,252,369) (3,177,578)Net cash flows from operations 2,757,431,686 998,375,231Cash flows from investmentPurchase of fixed assets (125,533,476) (571,212,282)Proceeds from sales of fixed assets 7,880,172 4,315,231Increase in assets under implementation (67,091,119) (7,721,060)Increase in differed sales receivables (5,240,794,585) (4,578,838,623)Increase/decrease in short term investments (887,463,921) 402,860,488Increase in long term investments (152,293,765) (15,285,208)Net cash flows ….. (6,465,296,694) (4,765,881,454)Cash flows from financingIncrease in unrestricted investment accounts 28,588,115,647 6,863,099,688Increase in current and savings accounts 13,721,227,613 4,669,166,754Cash dividends to shareholders (300,000,079) (100,659,570)Increase in accounts payable 2,341,640,820 338,637,626Increase in other liabilities 60,625,615 24,044,958Decrease / increase in other assets 316,613,377 (938,541,264)Increase in minority interest 34,000,000 -Net cash flows from financing 44,762,222,993 10,855,748,192Increase in cash and cash equivalents 41,054,357,985 7,088,241,969Increase in cash and cash equivalents at the beginning of the year 12,788,758,326 5,700,516,357

Increase in cash and cash equivalents at the end of the year 53,843,116,311 12,788,758,326

The attached notes from (1) to (27) are an integral part of the financial statements

Dr. Mohammed Othman Sulaiman Al Rikabi Mr: Musaad Mohammed Ahmed Abdel Karim Dr. Abdelhameed Mohammed Jameel Chairman of the Board of Directors Member of the Board of DirectorsGeneral Director

29

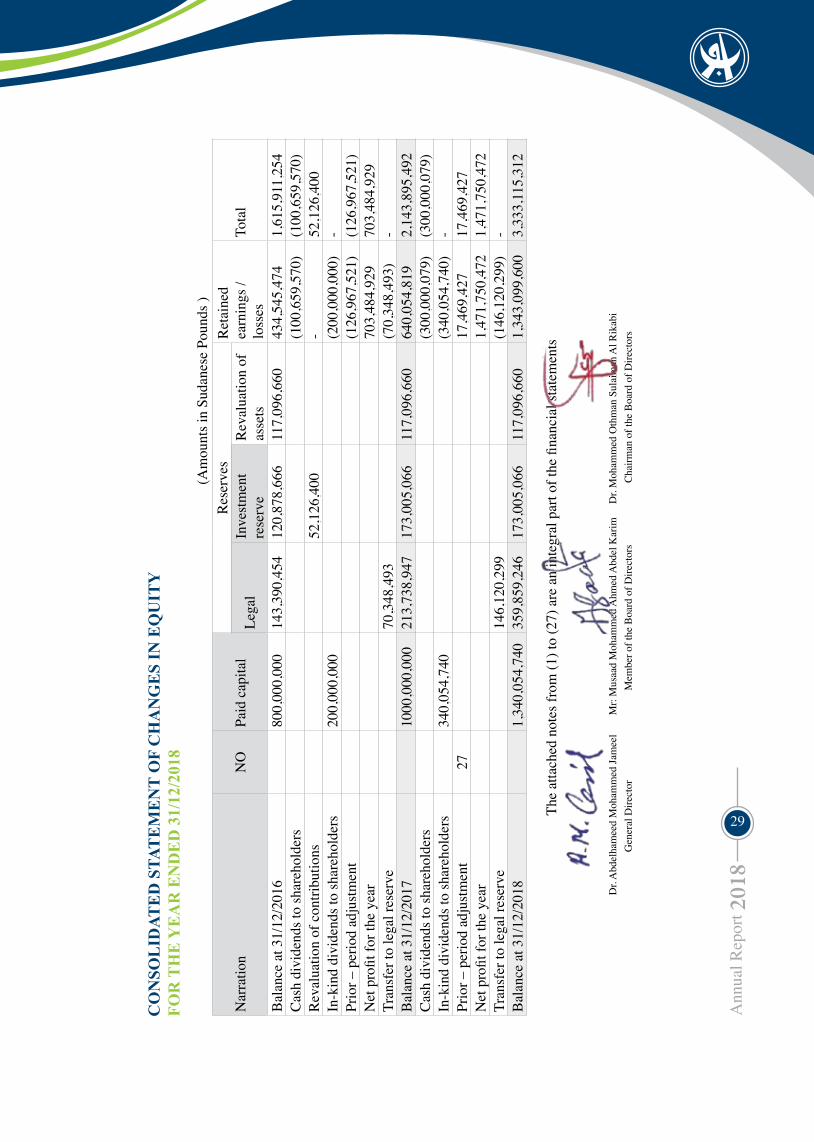

Co

nso

liD

aTe

D s

TaT

eM

en

T o

f C

ha

ng

es

in e

qu

iTy

fo

r T

he

ye

ar

en

De

D 3

1/12

/201

8

(Am

ount

s in

Suda

nese

Pou

nds )

Tota

l R

etai

ned

earn

ings

/ lo

sses

Res

erve

sPa

id c

apita

l N

O

Nar

ratio

n R

eval

uatio

n of

as

sets

Inve

stm

ent

rese

rve

Lega

l

1,61

5,91

1,25

443

4,54

5,47

411

7,09

6,66

012

0,87

8,66

614

3,39

0,45

480

0,00

0,00

0B

alan

ce a

t 31/

12/2

016

(100

,659

,570

)(1

00,6

59,5

70)

Cas

h di

vide

nds t

o sh

areh

olde

rs52

,126

,400

-52

,126

,400

Rev

alua

tion

of c

ontri

butio

ns-

(200

,000

,000

)20

0,00

0,00

0In

-kin

d di

vide

nds t

o sh

areh

olde

rs(1

26,9

67,5

21)

(126

,967

,521

)Pr

ior –

per

iod

adju

stm

ent

703,

484,

929

703,

484,

929

Net

pro

fit fo

r the

yea

r-

(70,

348,

493)

70,3

48,4

93Tr

ansf

er to

lega

l res

erve

2,14

3,89

5,49

264

0,05

4,81

911

7,09

6,66

017

3,00

5,06

621

3,73

8,94

710

00,0

00,0

00B

alan

ce a

t 31/

12/2

017

(300

,000

,079

)(3

00,0

00,0

79)

Cas

h di

vide

nds t

o sh

areh

olde

rs-

(340

,054

,740

)34

0,05

4,74

0In

-kin

d di

vide

nds t

o sh

areh

olde

rs17

,469

,427

17,4

69,4

2727

Prio

r – p

erio

d ad

just

men

t1,

471,

750,

472

1,47

1,75

0,47

2N

et p

rofit

for t

he y

ear

-(1

46,1

20,2

99)

146,

120,

299

Tran

sfer

to le

gal r

eser

ve3,

333,

115,

312

1,34

3,09

9,60

011

7,09

6,66

017

3,00

5,06

635

9,85

9,24

61,

340,

054,

740

Bal

ance

at 3

1/12

/201

8

The

atta

ched

not

es fr

om (1

) to

(27)

are

an

inte

gral

par

t of t

he fi

nanc

ial s

tate

men

ts

Dr.

Moh

amm

ed O

thm

an S

ulai

man

Al R

ikab

i M

r: M

usaa

d M

oham

med

Ahm

ed A

bdel

Kar

im D

r. A

bdel

ham

eed

Moh

amm

ed Ja

mee

l C

hairm

an o

f the

Boa

rd o

f Dire

ctor

s

Mem

ber o

f the

Boa

rd o

f Dire

ctor

sG

ener

al D

irect

or

30

noTes To finanCial sTaTeMenTs as aT 31/12/ 2018

note no (1)incorporation and activityOmdurman National Bank was established in January 1993 as a public shareholding company with limited liability under (Companies Act of 1925, amended 2015). The bank has practiced its actual banking activity in August 1993, offering all banking and investment services in accordance with Islamic Sharia. Omdurman National Bank is considered one of the leading national institutions. It represents an important pillar of the national economy in the field of banking, investment, development and foreign trade. It has a wide network of many correspondents which is spread across the world. The bank operates its banking activities through the presidency and its branches in Sudan, including 16 branches in Khartoum state, 11 branches in other states, and 10 mandates. The authorized capital is three billion Sudanese pounds. The paid-up capital is one billion three hundred and forty million and fifty-four thousand and seven hundred and forty pounds. The main objectives of the bank* Mobilizing and attracting public savings all over Sudan as well as collecting and accepting the savings of Sudanese working abroad.* Financing of economic development projects, mining sector, productive sectors and foreign trade in general. * Support and finance the microfinance sector, finance with a social dimension, the cooperative sector, and the sectors of craftsmen and professionals. * Provide social and cooperative support to serve state employees and pensioners.* Work towards achieving social justice and balanced development by establishing branches in all states of Sudan. * Establishing the bank’s private companies and contributing to the establishment of companies with others to serve the Bank’s objectives. note no (2) accounting policiesa. Basis of preparation of financial statementsThe financial statements are prepared in accordance with the standards of the Islamic Financial Accounting and Auditing Organization, international accounting standards and policies and publications of the Central Bank of Sudan. The financial statements are prepared in accordance with the external cost principle.

b. Transactions in foreign currenciesThe bank accounts are held in Sudanese pounds while other foreign currencies are recorded on the basis of the prevailing exchange rate at the date of maturity. Assets and liabilities denominated in foreign currencies were assessed in the financial statements as at 31/12/2018 at 47.6188 pounds against the dollar, at 54.4149 pounds against the euro and at 12.6947 pounds against the Saudi riyal. c. revenues and expensesIncome and expenses are recorded in the books in accordance with the accrual accounting principle. Income from deferred sales (Murabaha, contracting, installment sales ... etc.) and securities is also recorded accordingly. Income from short-term financing (participation, speculation, etc.) is recorded after actual cash collection and liquidation according to the standards of the Accounting and Auditing Organization for Islamic Financial Institutions. Income and expenses are recorded in foreign exchange at the local rate prevailing at the date of maturity. d. Depreciation of fixed assetsFixed assets are depreciated using the fixed installment method. Depreciation is calculated for the assets added during the year on a monthly basis from the date of their operation at the annual depreciation rate determined for the different fixed assets. e. Stock assessmentEnding inventory isevaluate depend on the cost price.f. financial statements classificationThe financial statements for 2017 have been amended to conform to the financial statements for 2018 according to the standards of the Accounting and Auditing Organization for Islamic Financial Institutions and International Accounting Standards. g. Basis of dividing the profits of investment accountsThe investment accounts’ profits are determined based on the weight of its contribution to the finance portfolio by balance rate method. A percentage of profits is deducted to the shareholders as management margins as the Bank manages the financing operations as a speculator.

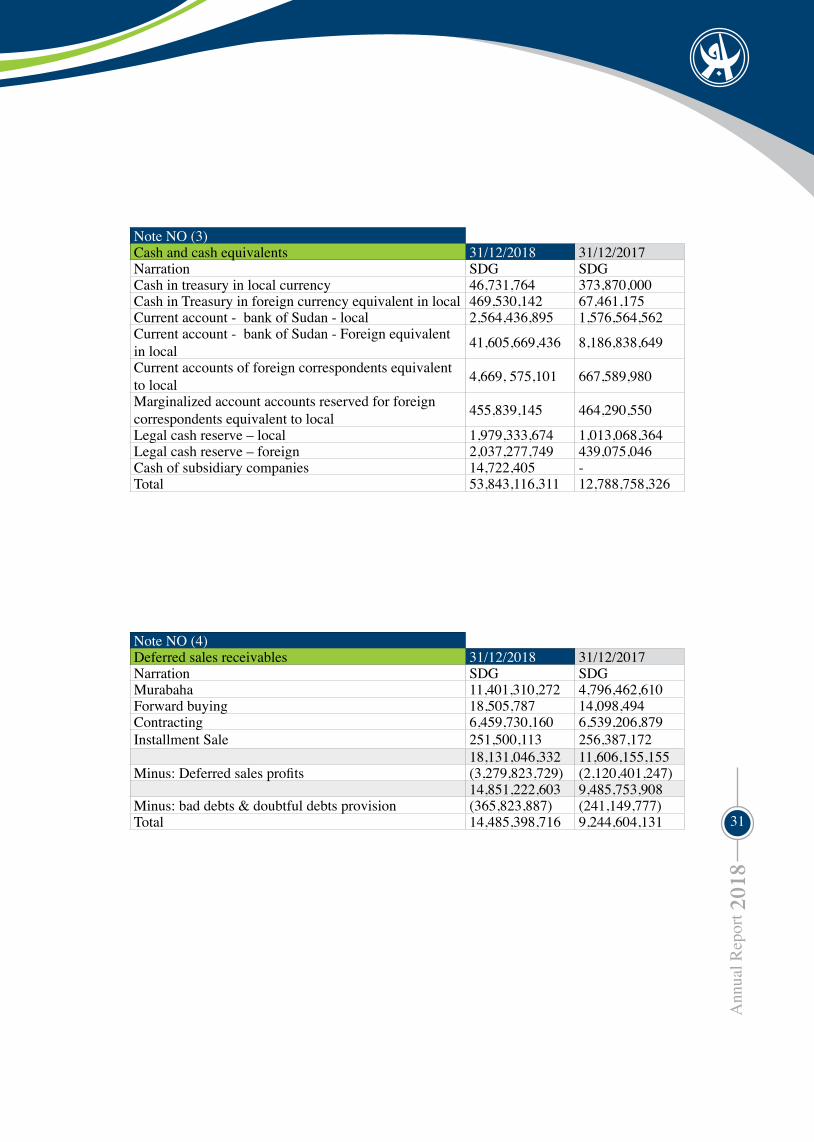

31

Note NO (3) Cash and cash equivalents 31/12/2018 31/12/2017Narration SDG SDGCash in treasury in local currency 46,731,764 373,870,000Cash in Treasury in foreign currency equivalent in local 469,530,142 67,461,175Current account - bank of Sudan - local 2,564,436,895 1,576,564,562Current account - bank of Sudan - Foreign equivalent in local 41,605,669,436 8,186,838,649

Current accounts of foreign correspondents equivalent to local 4,669, 575,101 667,589,980

Marginalized account accounts reserved for foreign correspondents equivalent to local 455,839,145 464,290,550

Legal cash reserve – local 1,979,333,674 1,013,068,364Legal cash reserve – foreign 2,037,277,749 439,075,046Cash of subsidiary companies 14,722,405 - Total 53,843,116,311 12,788,758,326

Note NO (4) Deferred sales receivables 31/12/2018 31/12/2017Narration SDG SDGMurabaha 11,401,310,272 4,796,462,610Forward buying 18,505,787 14,098,494Contracting 6,459,730,160 6,539,206,879Installment Sale 251,500,113 256,387,172

18,131,046,332 11,606,155,155Minus: Deferred sales profits (3,279,823,729) (2,120,401,247)

14,851,222,603 9,485,753,908Minus: bad debts & doubtful debts provision (365,823,887) (241,149,777)Total 14,485,398,716 9,244,604,131

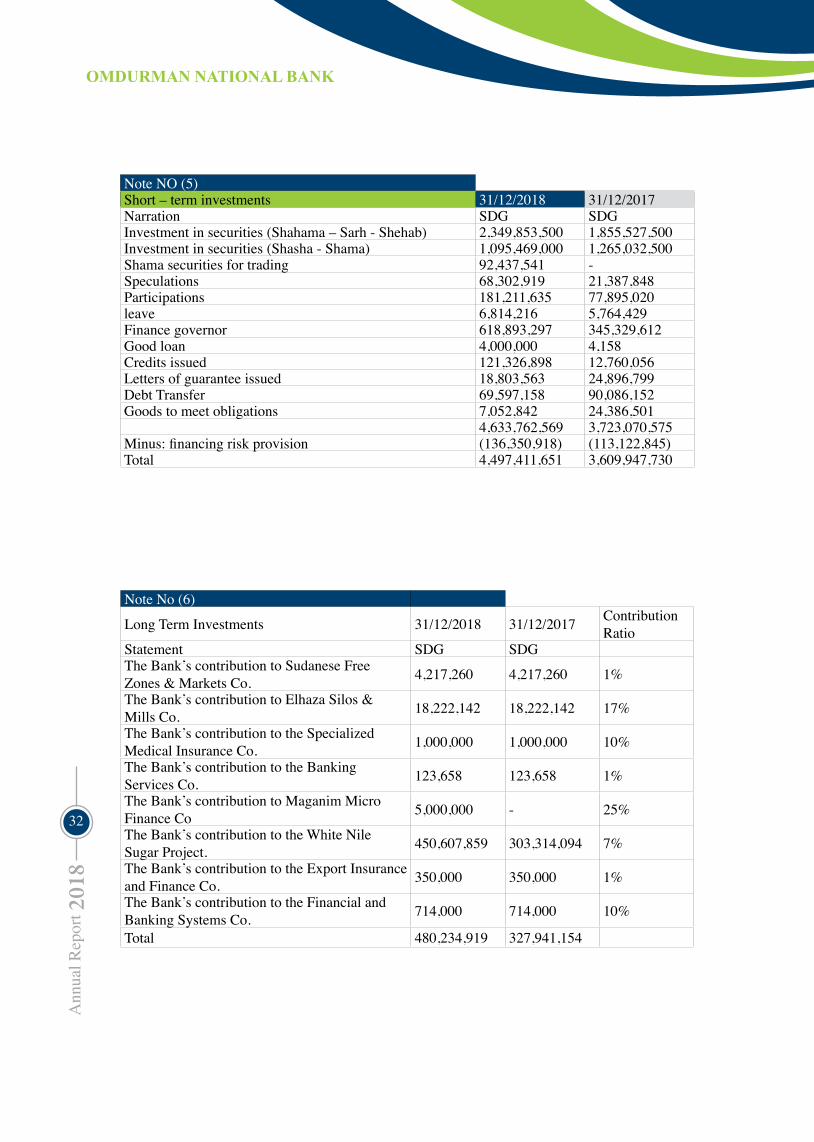

32

Note NO (5)Short – term investments 31/12/2018 31/12/2017Narration SDG SDGInvestment in securities (Shahama – Sarh - Shehab) 2,349,853,500 1,855,527,500Investment in securities (Shasha - Shama) 1,095,469,000 1,265,032,500Shama securities for trading 92,437,541 -Speculations 68,302,919 21,387,848Participations 181,211,635 77,895,020leave 6,814,216 5,764,429Finance governor 618,893,297 345,329,612Good loan 4,000,000 4,158Credits issued 121,326,898 12,760,056Letters of guarantee issued 18,803,563 24,896,799Debt Transfer 69,597,158 90,086,152Goods to meet obligations 7,052,842 24,386,501

4,633,762,569 3,723,070,575Minus: financing risk provision (136,350,918) (113,122,845)Total 4,497,411,651 3,609,947,730

Note No (6)

Long Term Investments 31/12/2018 31/12/2017 Contribution Ratio

Statement SDG SDGThe Bank’s contribution to Sudanese Free Zones & Markets Co. 4,217,260 4,217,260 1%

The Bank’s contribution to Elhaza Silos & Mills Co. 18,222,142 18,222,142 17%

The Bank’s contribution to the Specialized Medical Insurance Co. 1,000,000 1,000,000 10%

The Bank’s contribution to the Banking Services Co. 123,658 123,658 1%

The Bank’s contribution to Maganim Micro Finance Co 5,000,000 - 25%

The Bank’s contribution to the White Nile Sugar Project. 450,607,859 303,314,094 7%

The Bank’s contribution to the Export Insurance and Finance Co. 350,000 350,000 1%

The Bank’s contribution to the Financial and Banking Systems Co. 714,000 714,000 10%

Total 480,234,919 327,941,154

33

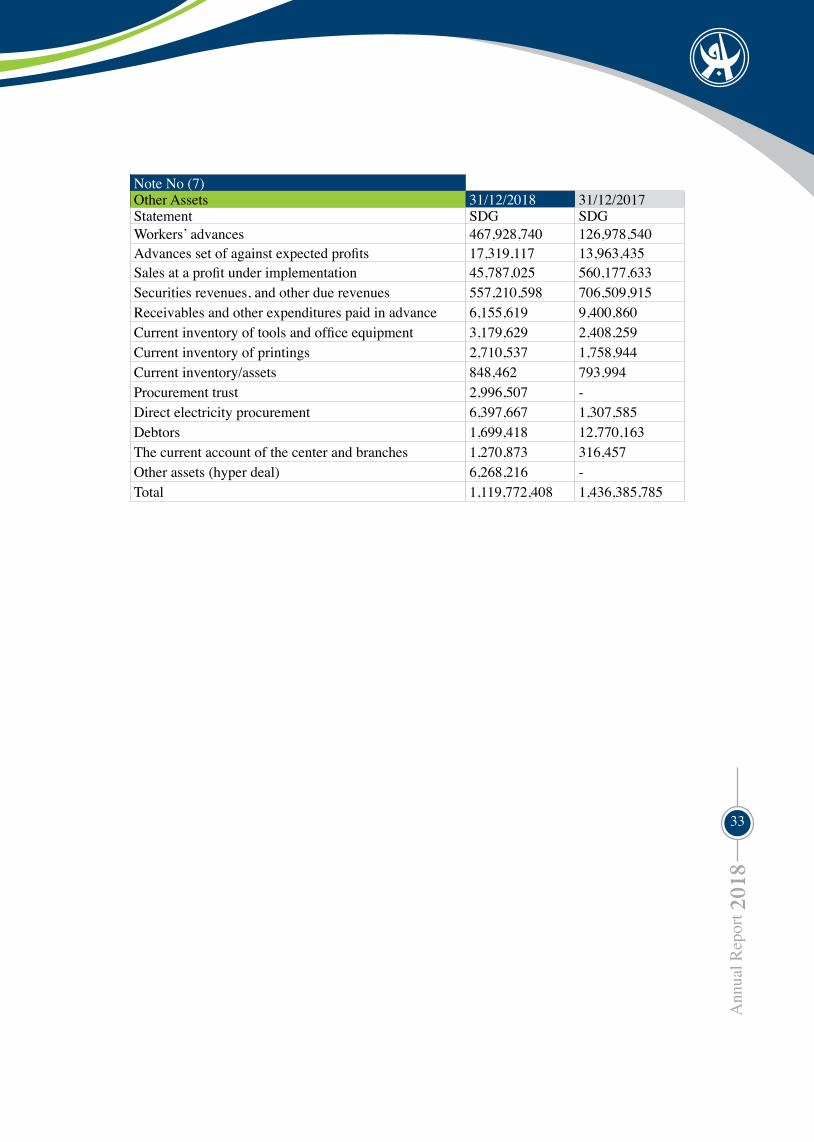

Note No (7)Other Assets 31/12/2018 31/12/2017Statement SDG SDGWorkers’ advances 467,928,740 126,978,540Advances set of against expected profits 17,319,117 13,963,435Sales at a profit under implementation 45,787,025 560,177,633Securities revenues, and other due revenues 557,210,598 706,509,915Receivables and other expenditures paid in advance 6,155,619 9,400,860Current inventory of tools and office equipment 3,179,629 2,408,259Current inventory of printings 2,710,537 1,758,944Current inventory/assets 848,462 793,994Procurement trust 2,996,507 -Direct electricity procurement 6,397,667 1,307,585Debtors 1,699,418 12,770,163The current account of the center and branches 1,270,873 316,457Other assets (hyper deal) 6,268,216 -Total 1,119,772,408 1,436,385,785

34

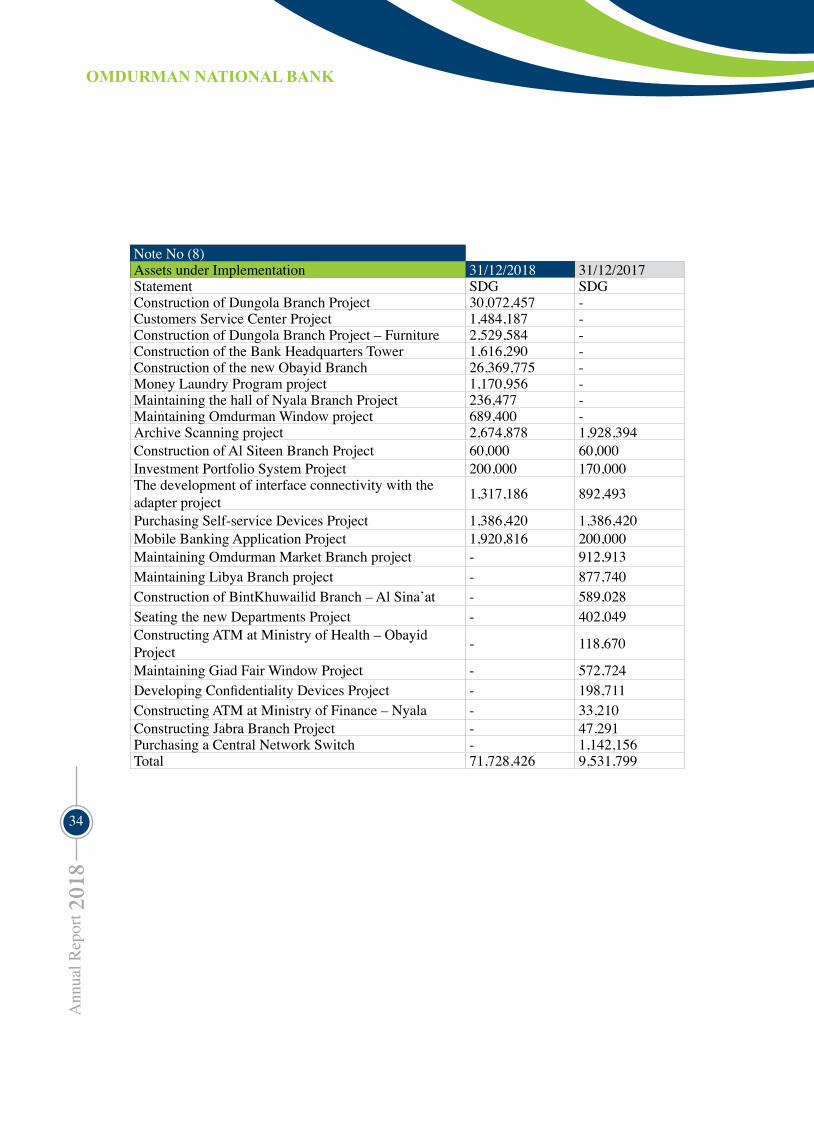

Note No (8)Assets under Implementation 31/12/2018 31/12/2017Statement SDG SDGConstruction of Dungola Branch Project 30,072,457 -Customers Service Center Project 1,484,187 -Construction of Dungola Branch Project – Furniture 2,529,584 -Construction of the Bank Headquarters Tower 1,616,290 -Construction of the new Obayid Branch 26,369,775 -Money Laundry Program project 1,170,956 -Maintaining the hall of Nyala Branch Project 236,477 -Maintaining Omdurman Window project 689,400 -Archive Scanning project 2,674,878 1,928,394Construction of Al Siteen Branch Project 60,000 60,000Investment Portfolio System Project 200,000 170,000The development of interface connectivity with the adapter project 1,317,186 892,493

Purchasing Self-service Devices Project 1,386,420 1,386,420Mobile Banking Application Project 1,920,816 200,000Maintaining Omdurman Market Branch project - 912,913Maintaining Libya Branch project - 877,740Construction of BintKhuwailid Branch – Al Sina’at - 589,028Seating the new Departments Project - 402,049Constructing ATM at Ministry of Health – Obayid Project - 118,670

Maintaining Giad Fair Window Project - 572,724Developing Confidentiality Devices Project - 198,711Constructing ATM at Ministry of Finance – Nyala - 33,210Constructing Jabra Branch Project - 47,291Purchasing a Central Network Switch - 1,142,156Total 71,728,426 9,531,799

35

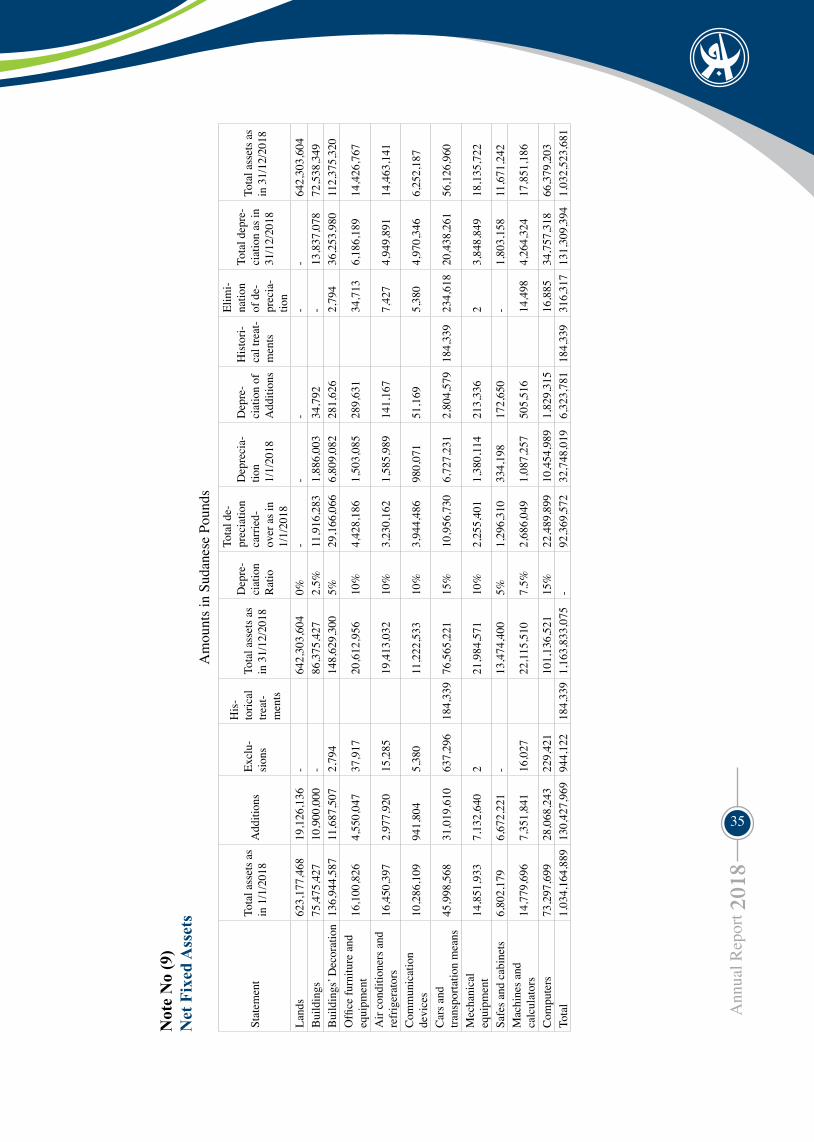

not

e n

o (9

)n

et f

ixed

ass

ets

Am

ount

s in

Suda

nese

Pou

nds

Stat

emen

tTo

tal a

sset

s as

in 1

/1/2

018

Add

ition

sEx

clu-

sion

s

His

-to

rical

tre

at-

men

ts

Tota

l ass

ets a

s in

31/

12/2

018

Dep

re-

ciat

ion

Rat

io

Tota

l de-

prec

iatio

n ca

rrie

d-ov

er a

s in

1/1/

2018

Dep

reci

a-tio

n1/

1/20

18

Dep

re-

ciat

ion

of

Add

ition

s

His

tori-

cal t

reat

-m

ents

Elim

i-na

tion

of d

e-pr

ecia

-tio

n

Tota

l dep

re-

ciat

ion

as in

31

/12/

2018

Tota

l ass

ets a

s in

31/

12/2

018

Land

s62

3,17

7,46

819

,126

,136

-64

2,30

3,60

40%

--

--

-64

2,30

3,60

4B

uild

ings

75,4

75,4

2710

,900

,000

-86

,375

,427

2.5%

11,9

16,2

831,

886,

003

34,7

92-

13,8

37,0

7872

,538

,349

Bui

ldin

gs’ D

ecor

atio

n13

6,94

4,58

711

,687

,507

2,79

414

8,62

9,30

05%

29,1

66,0

666,

809,

082

281,

626

2,79

436

,253

,980

112,

375,

320

Offi

ce fu

rnitu

re a

nd

equi

pmen

t16

,100

,826

4,55

0,04

737

,917

20,6

12,9

5610

%4,

428,

186

1,50

3,08

528

9,63

134

,713

6,18

6,18

914

,426

,767

Air

cond

ition

ers a

nd

refr

iger

ator

s16

,450

,397

2,97

7,92

015

,285

19,4

13,0

3210

%3,

230,

162

1,58

5,98

914

1,16

77,

427

4,94

9,89

114

,463

,141

Com

mun

icat

ion

devi

ces

10,2

86,1

0994

1,80

45,

380

11,2

22,5

3310

%3,

944,

486

980,

071

51,1

695,

380

4,97

0,34

66,

252,

187

Car

s and

tra

nspo

rtatio

n m

eans

45,9

98,5

6831

,019

,610

637,

296

184,

339

76,5

65,2

2115

%10

,956

,730

6,72

7,23

12,

804,

579

184,

339

234,

618

20,4

38,2

6156

,126

,960

Mec

hani

cal

equi

pmen

t14

,851

,933

7,13

2,64

02

21,9

84,5

7110

%2,

255,

401

1,38

0,11

421

3,33

62

3,84

8,84

918

,135

,722

Safe

s and

cab

inet

s6,

802,

179

6,67

2,22

1-

13,4

74,4

005%

1,29

6,31

033

4,19

817

2,65

0-

1,80

3,15

811

,671

,242

Mac

hine

s and

ca

lcul

ator

s14

,779

,696

7,35

1,84

116

,027

22,1

15,5

107.

5%2,

686,

049

1,08

7,25

750

5,51

614

,498

4,26

4,32

417

,851

,186

Com

pute

rs73

,297

,699

28,0

68,2

4322

9,42

110

1,13

6,52

115

%22

,489

,899

10,4

54,9

891,

829,

315

16,8

8534

,757

,318

66,3

79,2

03To

tal

1,03

4,16

4,88

913

0,42

7,96

994

4,12

218

4,33

91,

163,

833,

075

-92

,369

,572

32,7

48,0

196,

323,

781

184,

339

316,

317

131,

309,

394

1,03

2,52

3,68

1

36

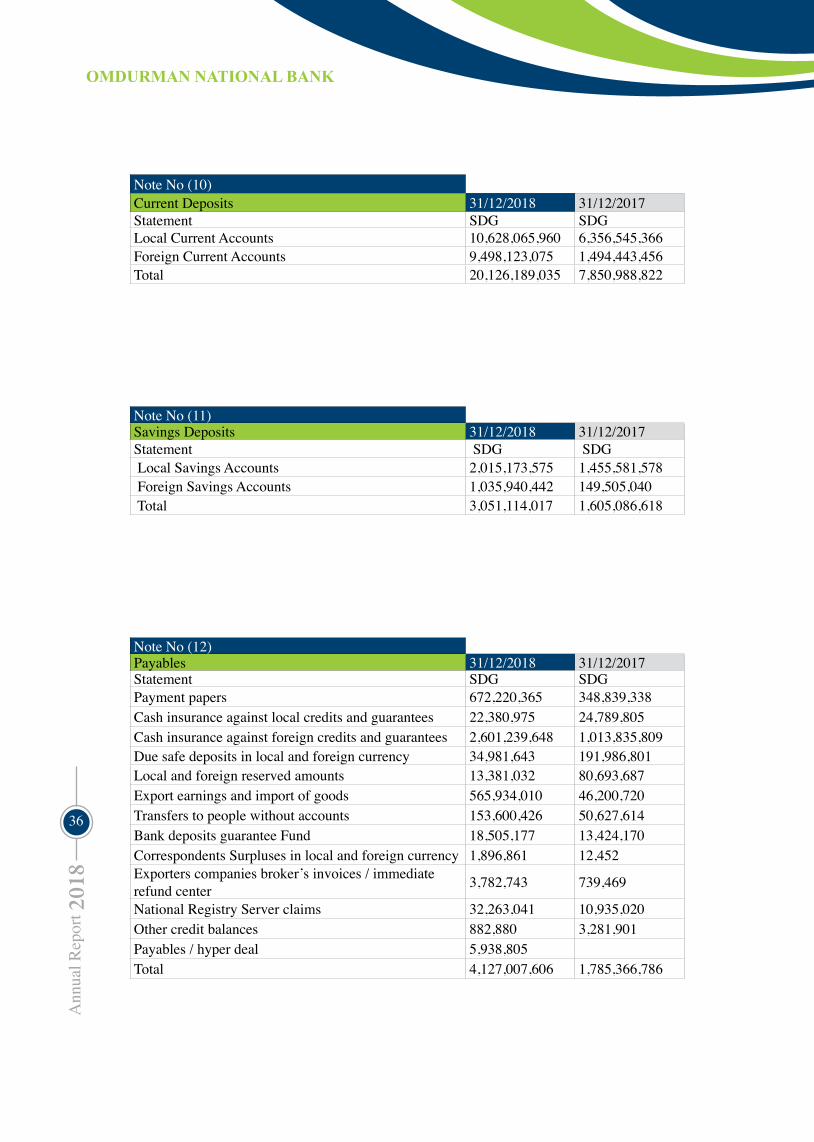

Note No (10)Current Deposits 31/12/2018 31/12/2017Statement SDG SDGLocal Current Accounts 10,628,065,960 6,356,545,366Foreign Current Accounts 9,498,123,075 1,494,443,456Total 20,126,189,035 7,850,988,822

Note No (11)Savings Deposits 31/12/2018 31/12/2017Statement SDG SDG Local Savings Accounts 2,015,173,575 1,455,581,578 Foreign Savings Accounts 1,035,940,442 149,505,040 Total 3,051,114,017 1,605,086,618

Note No (12)Payables 31/12/2018 31/12/2017Statement SDG SDGPayment papers 672,220,365 348,839,338Cash insurance against local credits and guarantees 22,380,975 24,789,805Cash insurance against foreign credits and guarantees 2,601,239,648 1,013,835,809Due safe deposits in local and foreign currency 34,981,643 191,986,801Local and foreign reserved amounts 13,381,032 80,693,687Export earnings and import of goods 565,934,010 46,200,720Transfers to people without accounts 153,600,426 50,627,614Bank deposits guarantee Fund 18,505,177 13,424,170Correspondents Surpluses in local and foreign currency 1,896,861 12,452Exporters companies broker’s invoices / immediate refund center 3,782,743 739,469

National Registry Server claims 32,263,041 10,935,020Other credit balances 882,880 3,281,901Payables / hyper deal 5,938,805Total 4,127,007,606 1,785,366,786

37

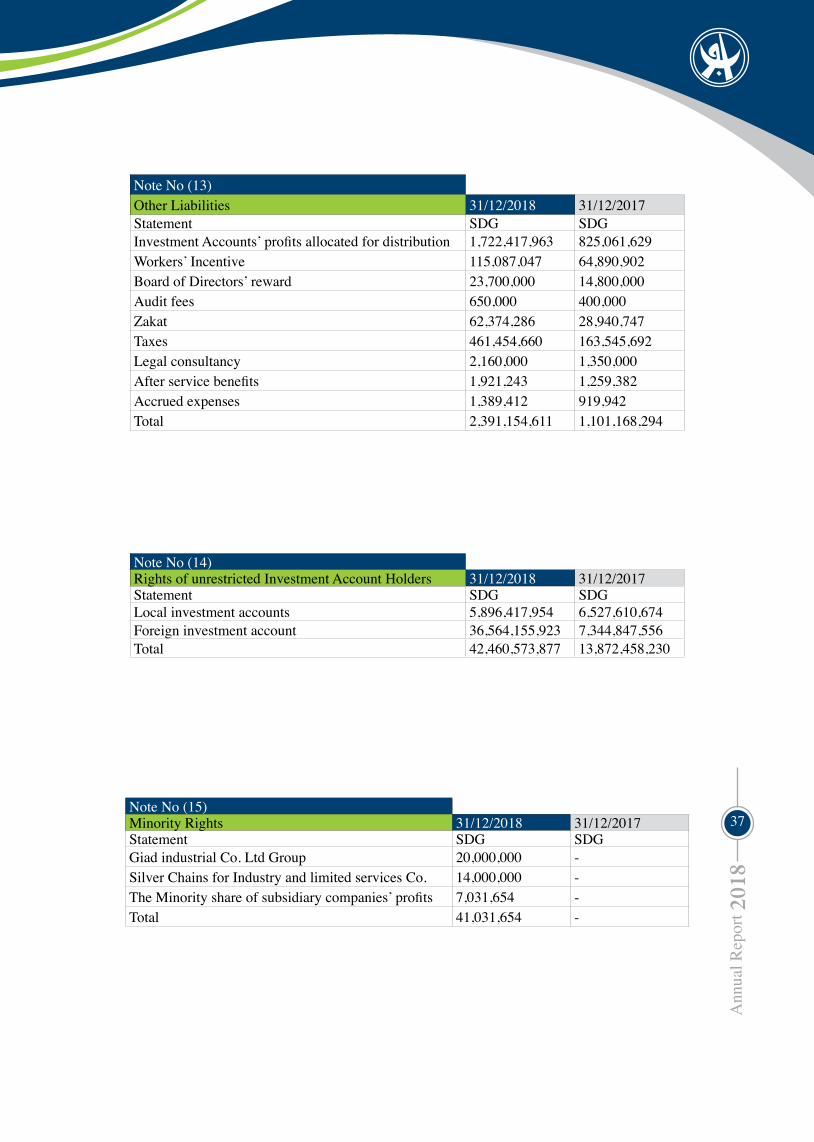

Note No (13)Other Liabilities 31/12/2018 31/12/2017Statement SDG SDGInvestment Accounts’ profits allocated for distribution 1,722,417,963 825,061,629Workers’ Incentive 115,087,047 64,890,902Board of Directors’ reward 23,700,000 14,800,000Audit fees 650,000 400,000Zakat 62,374,286 28,940,747Taxes 461,454,660 163,545,692Legal consultancy 2,160,000 1,350,000After service benefits 1,921,243 1,259,382Accrued expenses 1,389,412 919,942Total 2,391,154,611 1,101,168,294

Note No (14)Rights of unrestricted Investment Account Holders 31/12/2018 31/12/2017Statement SDG SDGLocal investment accounts 5,896,417,954 6,527,610,674Foreign investment account 36,564,155,923 7,344,847,556Total 42,460,573,877 13,872,458,230

Note No (15)Minority Rights 31/12/2018 31/12/2017Statement SDG SDGGiad industrial Co. Ltd Group 20,000,000 -Silver Chains for Industry and limited services Co. 14,000,000 -The Minority share of subsidiary companies’ profits 7,031,654 -Total 41,031,654 -

38

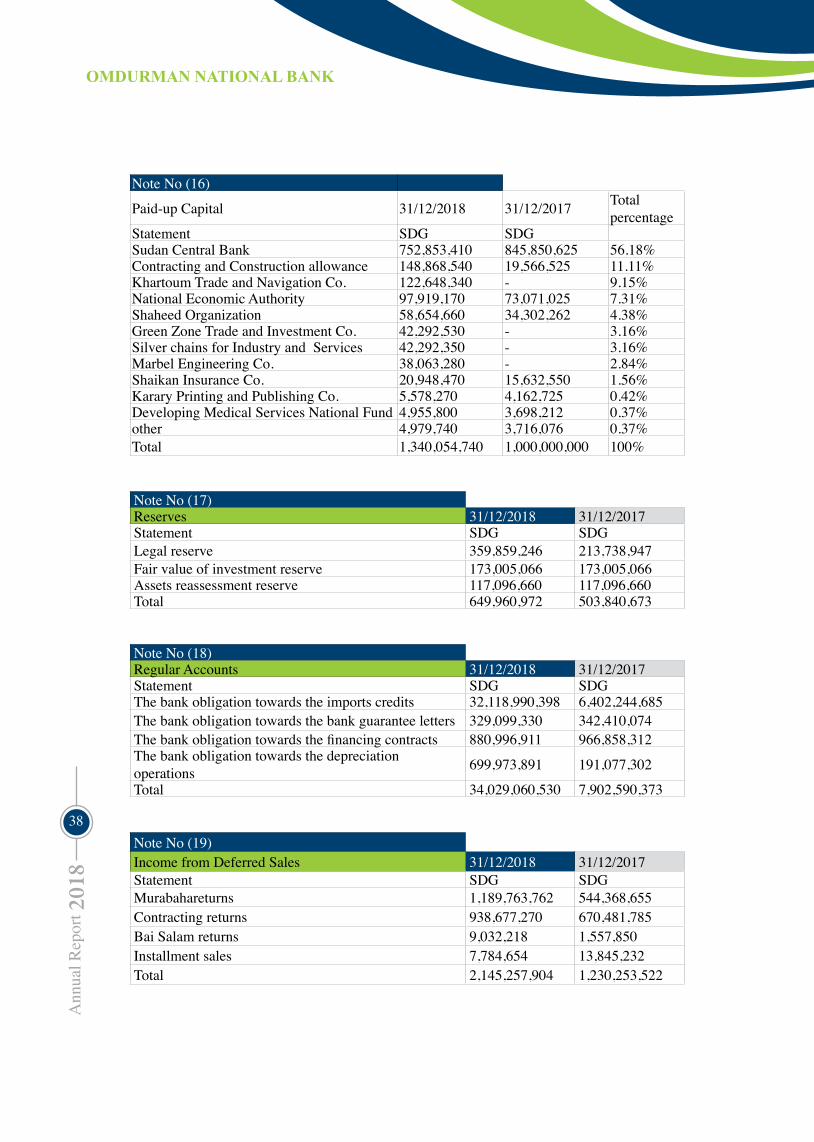

Note No (16)

Paid-up Capital 31/12/2018 31/12/2017 Total percentage

Statement SDG SDGSudan Central Bank 752,853,410 845,850,625 56.18%Contracting and Construction allowance 148,868,540 19,566,525 11.11%Khartoum Trade and Navigation Co. 122,648,340 - 9.15%National Economic Authority 97,919,170 73,071,025 7.31%Shaheed Organization 58,654,660 34,302,262 4.38%Green Zone Trade and Investment Co. 42,292,530 - 3.16%Silver chains for Industry and Services 42,292,350 - 3.16%Marbel Engineering Co. 38,063,280 - 2.84%Shaikan Insurance Co. 20,948,470 15,632,550 1.56%Karary Printing and Publishing Co. 5,578,270 4,162,725 0.42%Developing Medical Services National Fund 4,955,800 3,698,212 0.37%other 4,979,740 3,716,076 0.37%Total 1,340,054,740 1,000,000,000 100%

Note No (17)Reserves 31/12/2018 31/12/2017Statement SDG SDGLegal reserve 359,859,246 213,738,947Fair value of investment reserve 173,005,066 173,005,066Assets reassessment reserve 117,096,660 117,096,660Total 649,960,972 503,840,673

Note No (18)Regular Accounts 31/12/2018 31/12/2017Statement SDG SDGThe bank obligation towards the imports credits 32,118,990,398 6,402,244,685The bank obligation towards the bank guarantee letters 329,099,330 342,410,074The bank obligation towards the financing contracts 880,996,911 966,858,312The bank obligation towards the depreciation operations 699,973,891 191,077,302

Total 34,029,060,530 7,902,590,373

Note No (19)Income from Deferred Sales 31/12/2018 31/12/2017Statement SDG SDGMurabahareturns 1,189,763,762 544,368,655Contracting returns 938,677,270 670,481,785Bai Salam returns 9,032,218 1,557,850Installment sales 7,784,654 13,845,232Total 2,145,257,904 1,230,253,522

39

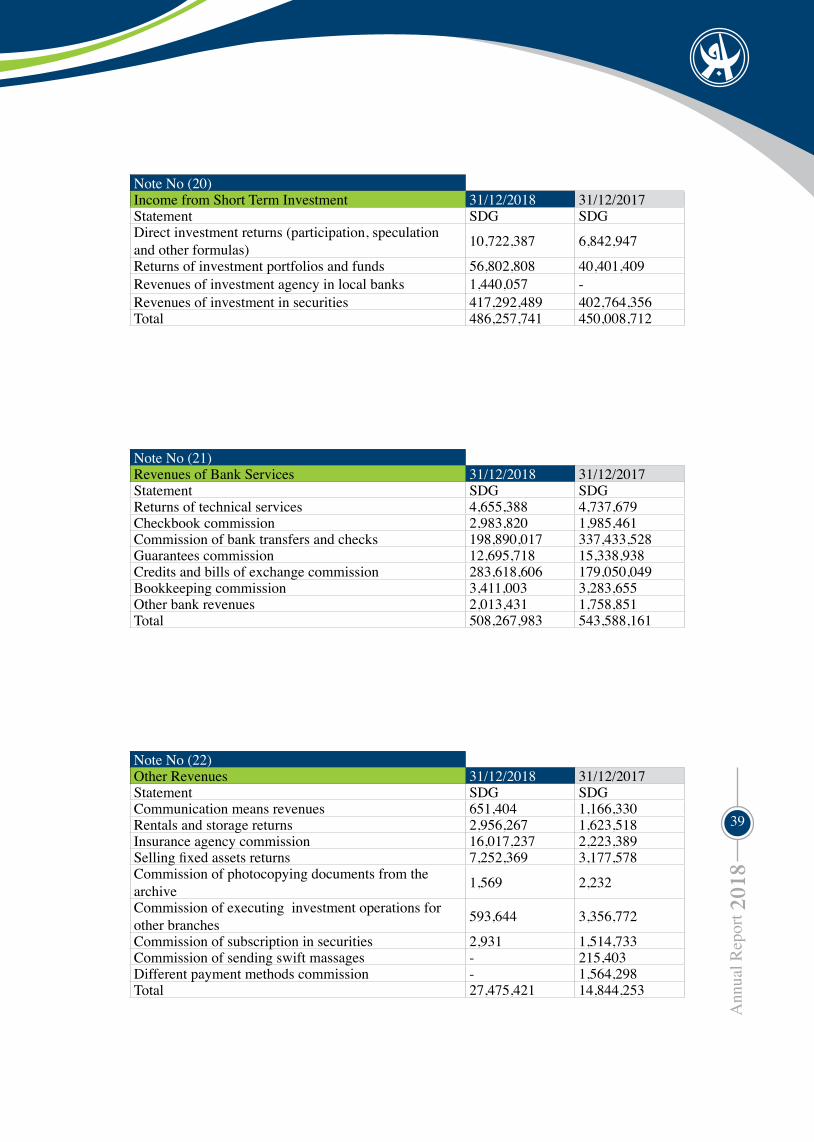

Note No (20)Income from Short Term Investment 31/12/2018 31/12/2017Statement SDG SDGDirect investment returns (participation, speculation and other formulas) 10,722,387 6,842,947

Returns of investment portfolios and funds 56,802,808 40,401,409Revenues of investment agency in local banks 1,440,057 -Revenues of investment in securities 417,292,489 402,764,356Total 486,257,741 450,008,712

Note No (21)Revenues of Bank Services 31/12/2018 31/12/2017Statement SDG SDGReturns of technical services 4,655,388 4,737,679Checkbook commission 2,983,820 1,985,461Commission of bank transfers and checks 198,890,017 337,433,528Guarantees commission 12,695,718 15,338,938Credits and bills of exchange commission 283,618,606 179,050,049Bookkeeping commission 3,411,003 3,283,655Other bank revenues 2,013,431 1,758,851Total 508,267,983 543,588,161

Note No (22)Other Revenues 31/12/2018 31/12/2017Statement SDG SDGCommunication means revenues 651,404 1,166,330Rentals and storage returns 2,956,267 1,623,518Insurance agency commission 16,017,237 2,223,389Selling fixed assets returns 7,252,369 3,177,578Commission of photocopying documents from the archive 1,569 2,232

Commission of executing investment operations for other branches 593,644 3,356,772

Commission of subscription in securities 2,931 1,514,733Commission of sending swift massages - 215,403Different payment methods commission - 1,564,298Total 27,475,421 14,844,253

40

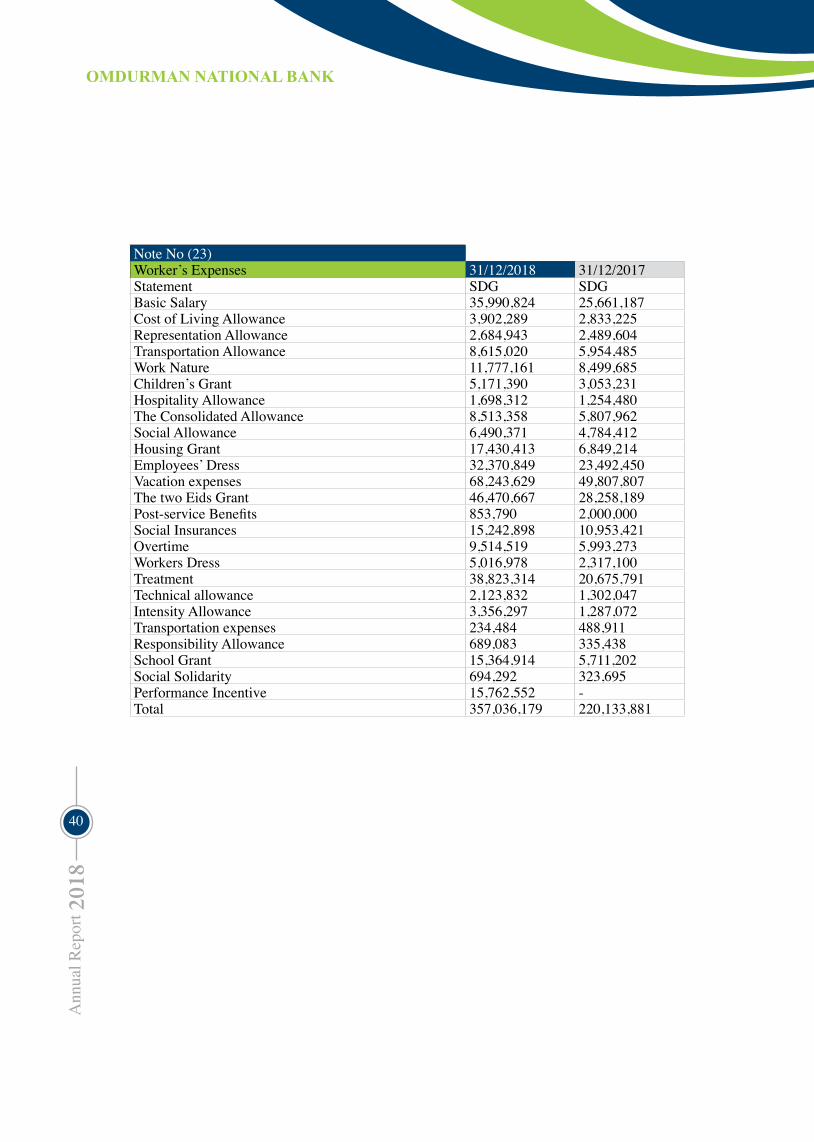

Note No (23)Worker’s Expenses 31/12/2018 31/12/2017Statement SDG SDGBasic Salary 35,990,824 25,661,187Cost of Living Allowance 3,902,289 2,833,225Representation Allowance 2,684,943 2,489,604Transportation Allowance 8,615,020 5,954,485Work Nature 11,777,161 8,499,685Children’s Grant 5,171,390 3,053,231Hospitality Allowance 1,698,312 1,254,480The Consolidated Allowance 8,513,358 5,807,962Social Allowance 6,490,371 4,784,412Housing Grant 17,430,413 6,849,214Employees’ Dress 32,370,849 23,492,450Vacation expenses 68,243,629 49,807,807The two Eids Grant 46,470,667 28,258,189Post-service Benefits 853,790 2,000,000Social Insurances 15,242,898 10,953,421Overtime 9,514,519 5,993,273Workers Dress 5,016,978 2,317,100Treatment 38,823,314 20,675,791Technical allowance 2,123,832 1,302,047Intensity Allowance 3,356,297 1,287,072Transportation expenses 234,484 488,911Responsibility Allowance 689,083 335,438School Grant 15,364,914 5,711,202Social Solidarity 694,292 323,695Performance Incentive 15,762,552 -Total 357,036,179 220,133,881

41

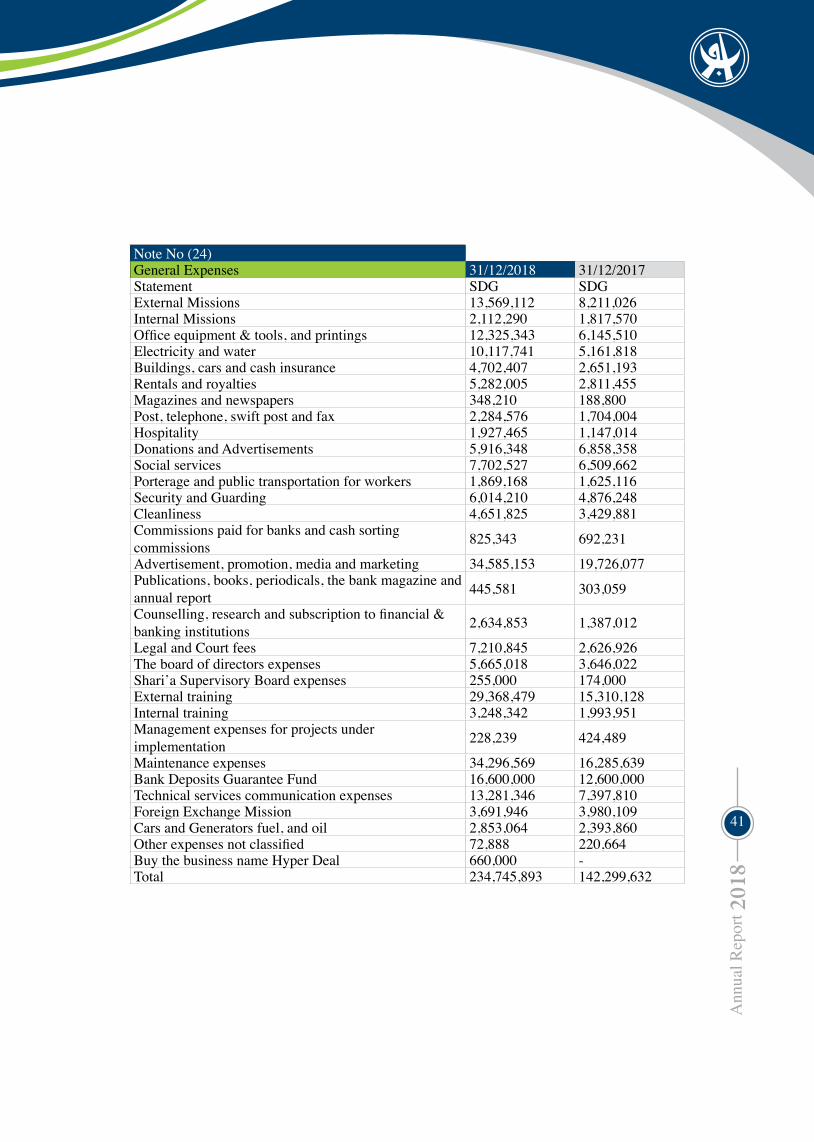

Note No (24)General Expenses 31/12/2018 31/12/2017Statement SDG SDGExternal Missions 13,569,112 8,211,026Internal Missions 2,112,290 1,817,570Office equipment & tools, and printings 12,325,343 6,145,510Electricity and water 10,117,741 5,161,818Buildings, cars and cash insurance 4,702,407 2,651,193Rentals and royalties 5,282,005 2,811,455Magazines and newspapers 348,210 188,800Post, telephone, swift post and fax 2,284,576 1,704,004Hospitality 1,927,465 1,147,014Donations and Advertisements 5,916,348 6,858,358Social services 7,702,527 6,509,662Porterage and public transportation for workers 1,869,168 1,625,116Security and Guarding 6,014,210 4,876,248Cleanliness 4,651,825 3,429,881Commissions paid for banks and cash sorting commissions 825,343 692,231

Advertisement, promotion, media and marketing 34,585,153 19,726,077Publications, books, periodicals, the bank magazine and annual report 445,581 303,059

Counselling, research and subscription to financial & banking institutions 2,634,853 1,387,012

Legal and Court fees 7,210,845 2,626,926The board of directors expenses 5,665,018 3,646,022Shari’a Supervisory Board expenses 255,000 174,000External training 29,368,479 15,310,128Internal training 3,248,342 1,993,951Management expenses for projects under implementation 228,239 424,489

Maintenance expenses 34,296,569 16,285,639Bank Deposits Guarantee Fund 16,600,000 12,600,000Technical services communication expenses 13,281,346 7,397,810Foreign Exchange Mission 3,691,946 3,980,109Cars and Generators fuel, and oil 2,853,064 2,393,860Other expenses not classified 72,888 220,664Buy the business name Hyper Deal 660,000 -Total 234,745,893 142,299,632

42

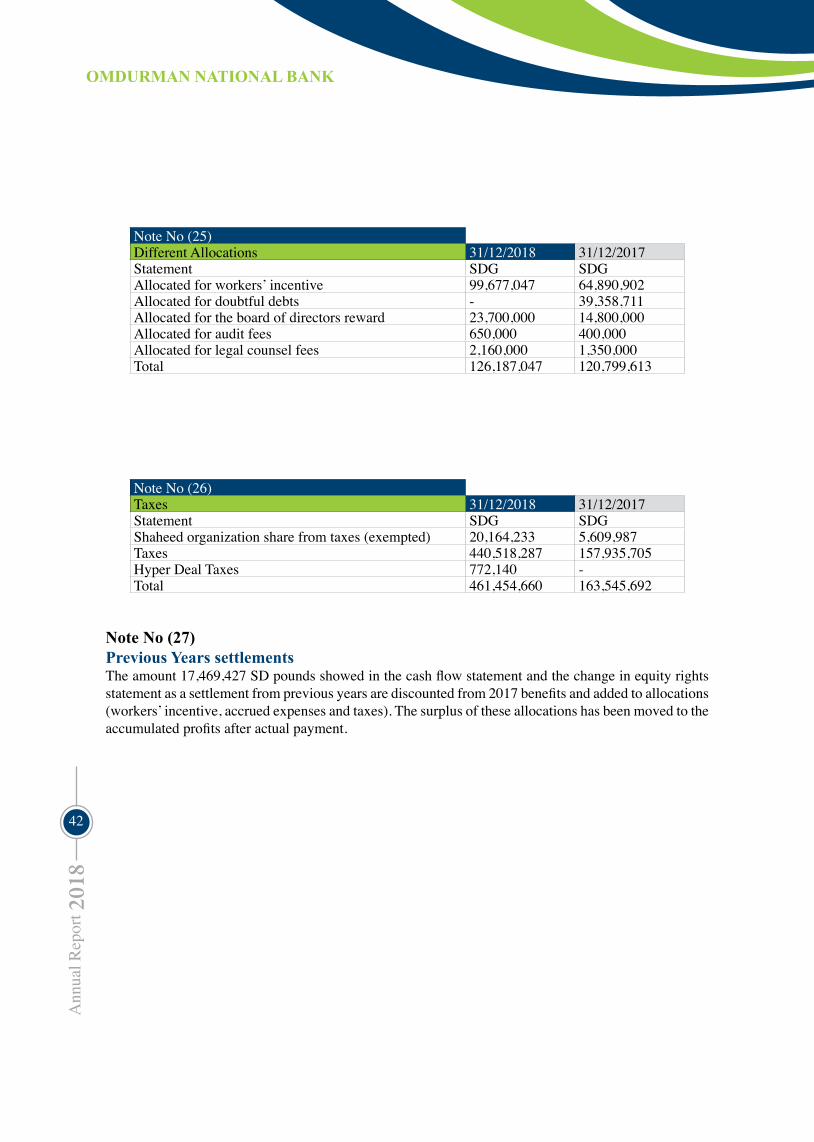

Note No (25)Different Allocations 31/12/2018 31/12/2017Statement SDG SDGAllocated for workers’ incentive 99,677,047 64,890,902Allocated for doubtful debts - 39,358,711Allocated for the board of directors reward 23,700,000 14,800,000Allocated for audit fees 650,000 400,000Allocated for legal counsel fees 2,160,000 1,350,000Total 126,187,047 120,799,613

Note No (26)Taxes 31/12/2018 31/12/2017Statement SDG SDGShaheed organization share from taxes (exempted) 20,164,233 5,609,987Taxes 440,518,287 157,935,705Hyper Deal Taxes 772,140 -Total 461,454,660 163,545,692

note no (27)previous years settlementsThe amount 17,469,427 SD pounds showed in the cash flow statement and the change in equity rights statement as a settlement from previous years are discounted from 2017 benefits and added to allocations (workers’ incentive, accrued expenses and taxes). The surplus of these allocations has been moved to the accumulated profits after actual payment.