Embed Size (px)

Citation preview

Open Economy Macroeconomics Lecture NotesOpen Economy Macroeconomics

Ozan Hatipoglu

Department of Economics, Bogazici University

Spring 2014

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 1 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and sold

Transfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign tradeFacilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.

Provides credit for foreign tradeFacilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign trade

Facilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign tradeFacilitates hedging against currency shocks

Largest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign tradeFacilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)

24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign tradeFacilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limit

No commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

Foreign Exchange (FX) Markets -Definition, Functions andFeatures

Definition: A market where national currencies are bought and soldTransfers purchasing power from one currency to another and allowsfor international transactions.Provides credit for foreign tradeFacilitates hedging against currency shocksLargest market in the world in terms of trade volume (over $6 trilliondaily in spot, forward and swaps)24 hours trading and no trading limitNo commissions by brokers but bid-ask spread required by dealers

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 2 / 93

International Transactions

Occur between individuals, firms, governments, international agencies.

Trade : Turkish firm sells a good to a US firm. Either the US firm paysin TL by converting $ into TL or pays in $ and the Turkish firmconverts it to TL. Trade practice of exporting Turkish firms: get paid inforeign currency if it is Euro or $ otherwise TL.Foreign Direct Investment(FDI). Example : US definition: ForeignDirect Investment is defined as whenever a US citizen, organization, oraffiliated group takes an interest of 10 percent or more in a foreignbusiness entity. It includes setting up a business, buying an office blocketc.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 3 / 93

International Transactions

Occur between individuals, firms, governments, international agencies.Trade : Turkish firm sells a good to a US firm. Either the US firm paysin TL by converting $ into TL or pays in $ and the Turkish firmconverts it to TL. Trade practice of exporting Turkish firms: get paid inforeign currency if it is Euro or $ otherwise TL.

Foreign Direct Investment(FDI). Example : US definition: ForeignDirect Investment is defined as whenever a US citizen, organization, oraffiliated group takes an interest of 10 percent or more in a foreignbusiness entity. It includes setting up a business, buying an office blocketc.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 3 / 93

International Transactions

Occur between individuals, firms, governments, international agencies.Trade : Turkish firm sells a good to a US firm. Either the US firm paysin TL by converting $ into TL or pays in $ and the Turkish firmconverts it to TL. Trade practice of exporting Turkish firms: get paid inforeign currency if it is Euro or $ otherwise TL.Foreign Direct Investment(FDI). Example : US definition: ForeignDirect Investment is defined as whenever a US citizen, organization, oraffiliated group takes an interest of 10 percent or more in a foreignbusiness entity. It includes setting up a business, buying an office blocketc.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 3 / 93

International Transactions

Portfolio Investments:This is an investment by individuals, firms orpublic bodies (ex. national and local governments) in foreign financialinstruments. Foreign financial instruments include government bondsand foreign stock.

The biggest difference between FDI and Foreign Portfolio Investment isthat Foreign Portfolio Investment is not associated with a significantequity stake or in other words management privileges.Aid : Humanitarian, Goods and Services, Infrastructure Aid , DebtRelief, Education AidRemittances : Ex: Workers Remittances”Foreign” in this context means foreign national or entity established inanother country. Ex: Garanti Bank International is a foreign firm.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 4 / 93

International Transactions

Portfolio Investments:This is an investment by individuals, firms orpublic bodies (ex. national and local governments) in foreign financialinstruments. Foreign financial instruments include government bondsand foreign stock.The biggest difference between FDI and Foreign Portfolio Investment isthat Foreign Portfolio Investment is not associated with a significantequity stake or in other words management privileges.

Aid : Humanitarian, Goods and Services, Infrastructure Aid , DebtRelief, Education AidRemittances : Ex: Workers Remittances”Foreign” in this context means foreign national or entity established inanother country. Ex: Garanti Bank International is a foreign firm.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 4 / 93

International Transactions

Portfolio Investments:This is an investment by individuals, firms orpublic bodies (ex. national and local governments) in foreign financialinstruments. Foreign financial instruments include government bondsand foreign stock.The biggest difference between FDI and Foreign Portfolio Investment isthat Foreign Portfolio Investment is not associated with a significantequity stake or in other words management privileges.Aid : Humanitarian, Goods and Services, Infrastructure Aid , DebtRelief, Education Aid

Remittances : Ex: Workers Remittances”Foreign” in this context means foreign national or entity established inanother country. Ex: Garanti Bank International is a foreign firm.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 4 / 93

International Transactions

Portfolio Investments:This is an investment by individuals, firms orpublic bodies (ex. national and local governments) in foreign financialinstruments. Foreign financial instruments include government bondsand foreign stock.The biggest difference between FDI and Foreign Portfolio Investment isthat Foreign Portfolio Investment is not associated with a significantequity stake or in other words management privileges.Aid : Humanitarian, Goods and Services, Infrastructure Aid , DebtRelief, Education AidRemittances : Ex: Workers Remittances

”Foreign” in this context means foreign national or entity established inanother country. Ex: Garanti Bank International is a foreign firm.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 4 / 93

International Transactions

Portfolio Investments:This is an investment by individuals, firms orpublic bodies (ex. national and local governments) in foreign financialinstruments. Foreign financial instruments include government bondsand foreign stock.The biggest difference between FDI and Foreign Portfolio Investment isthat Foreign Portfolio Investment is not associated with a significantequity stake or in other words management privileges.Aid : Humanitarian, Goods and Services, Infrastructure Aid , DebtRelief, Education AidRemittances : Ex: Workers Remittances”Foreign” in this context means foreign national or entity established inanother country. Ex: Garanti Bank International is a foreign firm.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 4 / 93

Types of FX Rate

Bilateral: Between two countries

Effective or trade-weighted (Multilateral): Weighted by the proportionof each country’s trade volume in total trade volume.

Nominal FX Rates: Actual Rates

Real FX rates: Adjusted by price differentials in two countries

Real Effective FX rates: Adjusted by price differentials in the set oftrade partners. TCMB reports two types of Real Effective FX rate (vs. Developed and vs. Developing Countries)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 5 / 93

Types of FX Rate

Bilateral: Between two countries

Effective or trade-weighted (Multilateral): Weighted by the proportionof each country’s trade volume in total trade volume.

Nominal FX Rates: Actual Rates

Real FX rates: Adjusted by price differentials in two countries

Real Effective FX rates: Adjusted by price differentials in the set oftrade partners. TCMB reports two types of Real Effective FX rate (vs. Developed and vs. Developing Countries)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 5 / 93

Types of FX Rate

Bilateral: Between two countries

Effective or trade-weighted (Multilateral): Weighted by the proportionof each country’s trade volume in total trade volume.

Nominal FX Rates: Actual Rates

Real FX rates: Adjusted by price differentials in two countries

Real Effective FX rates: Adjusted by price differentials in the set oftrade partners. TCMB reports two types of Real Effective FX rate (vs. Developed and vs. Developing Countries)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 5 / 93

Types of FX Rate

Bilateral: Between two countries

Effective or trade-weighted (Multilateral): Weighted by the proportionof each country’s trade volume in total trade volume.

Nominal FX Rates: Actual Rates

Real FX rates: Adjusted by price differentials in two countries

Real Effective FX rates: Adjusted by price differentials in the set oftrade partners. TCMB reports two types of Real Effective FX rate (vs. Developed and vs. Developing Countries)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 5 / 93

Types of FX Rate

Bilateral: Between two countries

Effective or trade-weighted (Multilateral): Weighted by the proportionof each country’s trade volume in total trade volume.

Nominal FX Rates: Actual Rates

Real FX rates: Adjusted by price differentials in two countries

Real Effective FX rates: Adjusted by price differentials in the set oftrade partners. TCMB reports two types of Real Effective FX rate (vs. Developed and vs. Developing Countries)

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 5 / 93

Types of FX Rate

Real FX Rate is a sign of the degree of competitiveness.

Spot vs. forward rates.

Buying vs. Selling ( Bid vs. Ask). Spread=Bid-Ask¿0 Spreadincreases during weekends, holidays, turbulent times.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 6 / 93

Types of FX Rate

Real FX Rate is a sign of the degree of competitiveness.

Spot vs. forward rates.

Buying vs. Selling ( Bid vs. Ask). Spread=Bid-Ask¿0 Spreadincreases during weekends, holidays, turbulent times.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 6 / 93

Types of FX Rate

Real FX Rate is a sign of the degree of competitiveness.

Spot vs. forward rates.

Buying vs. Selling ( Bid vs. Ask). Spread=Bid-Ask¿0 Spreadincreases during weekends, holidays, turbulent times.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 6 / 93

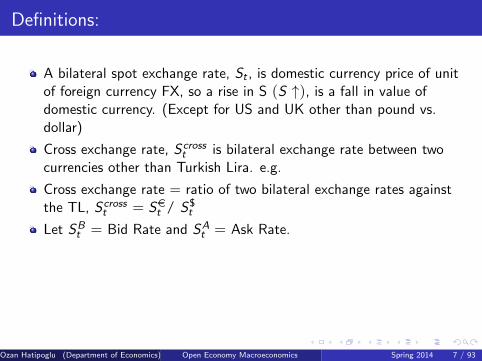

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Definitions:

A bilateral spot exchange rate, St , is domestic currency price of unitof foreign currency FX, so a rise in S (S ↑), is a fall in value ofdomestic currency. (Except for US and UK other than pound vs.dollar)

Cross exchange rate, Scrosst is bilateral exchange rate between two

currencies other than Turkish Lira. e.g.

Cross exchange rate = ratio of two bilateral exchange rates againstthe TL, Scross

t = Set / S$t

Let SBt = Bid Rate and SA

t = Ask Rate.

Suppose the buyer wants to buy $. Dealer asks SAt for 1 $ and Buyer

asks 1/SAt for 1TL.

Suppose the buyer wants to buy TL. Dealer asks 1/SBt for 1 TL and

Buyer asks SBt for 1$.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 7 / 93

Demand for FX

Turkish establishments demand $ in exchange for TL in order toimport from or invest in USA (and all other international transactionsmentioned above)

US establishments demand TL in exchange for $ in order to importfrom or invest in Turkey(and all other international transactionsmentioned above)

Speculators buy or sell TL (sell or buy $)

Total excess demand/supply eliminated instantaneously by exchange ratemovement

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 8 / 93

Demand for FX

Turkish establishments demand $ in exchange for TL in order toimport from or invest in USA (and all other international transactionsmentioned above)

US establishments demand TL in exchange for $ in order to importfrom or invest in Turkey(and all other international transactionsmentioned above)

Speculators buy or sell TL (sell or buy $)

Total excess demand/supply eliminated instantaneously by exchange ratemovement

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 8 / 93

Demand for FX

Turkish establishments demand $ in exchange for TL in order toimport from or invest in USA (and all other international transactionsmentioned above)

US establishments demand TL in exchange for $ in order to importfrom or invest in Turkey(and all other international transactionsmentioned above)

Speculators buy or sell TL (sell or buy $)

Total excess demand/supply eliminated instantaneously by exchange ratemovement

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 8 / 93

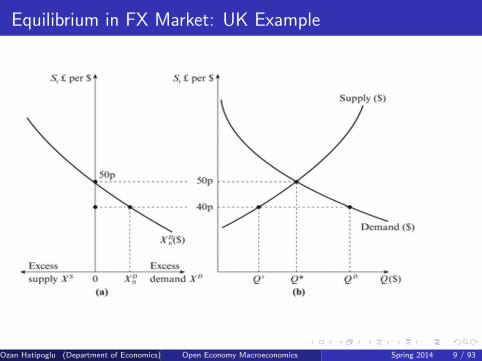

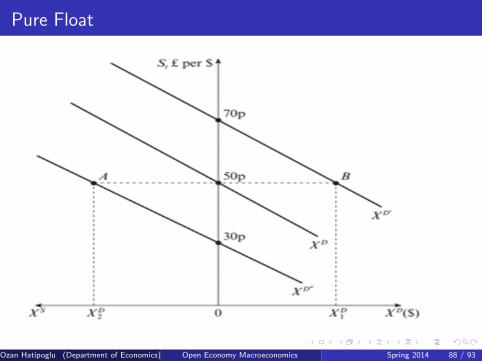

Equilibrium in FX Market: UK Example

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 9 / 93

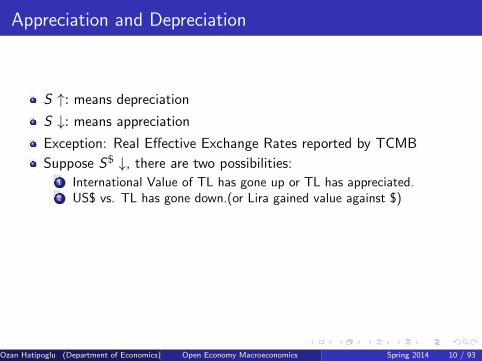

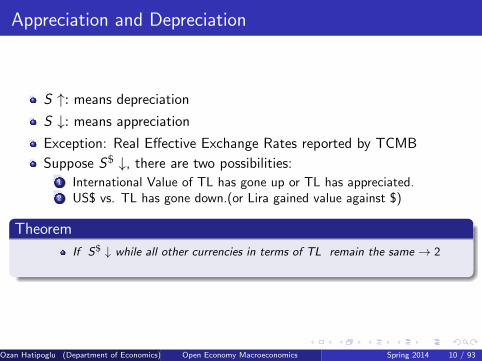

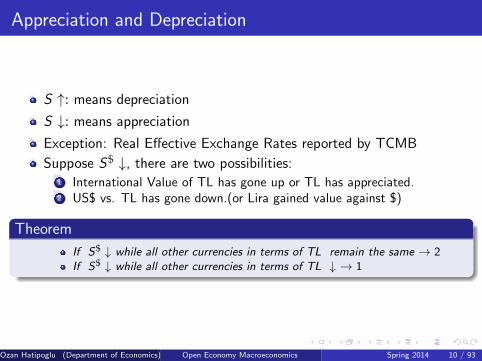

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:

1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:

1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:

1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:

1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:1 International Value of TL has gone up or TL has appreciated.

2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2

If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Appreciation and Depreciation

S ↑: means depreciation

S ↓: means appreciation

Exception: Real Effective Exchange Rates reported by TCMB

Suppose S$ ↓, there are two possibilities:1 International Value of TL has gone up or TL has appreciated.2 US$ vs. TL has gone down.(or Lira gained value against $)

Theorem

If S$ ↓ while all other currencies in terms of TL remain the same → 2If S$ ↓ while all other currencies in terms of TL ↓ → 1

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 10 / 93

Balance of Payments (BOP)

Definition

All transactions between Turkey and the rest of the world(ROW) in agiven year. It serves as flow of demand and supply for TL.

It consists of

1 Current Account,

2 Capital and/or Financial Account

3 Balancing Item.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 11 / 93

Balance of Payments (BOP)

Definition

All transactions between Turkey and the rest of the world(ROW) in agiven year. It serves as flow of demand and supply for TL.

It consists of

1 Current Account,

2 Capital and/or Financial Account

3 Balancing Item.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 11 / 93

Balance of Payments (BOP)

Definition

All transactions between Turkey and the rest of the world(ROW) in agiven year. It serves as flow of demand and supply for TL.

It consists of

1 Current Account,

2 Capital and/or Financial Account

3 Balancing Item.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 11 / 93

BOP Items: Current Account

Current account (CRA): Here and now. Export receipts (X) ascredits, import payments (M) as debits, net = current accountbalance (goods, services including financial services, interest anddividends, rent, tourism)

1 Visibles (merchandise account): traded goods, processed goods,repairs on goods, gold, purchase of capital goods such as machinery,aircrafts

2 Invisibles (service account): rights, licenses, insurance, tourism andother intangibles

3 Interests, Profits and Dividends: rents from capital services, e.g.rental income, interest on deposit accounts, dividend payments onstocks, other profits transfers.

4 Transfers: worker’s remittances, aid.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 12 / 93

BOP Items: Current Account

Current account (CRA): Here and now. Export receipts (X) ascredits, import payments (M) as debits, net = current accountbalance (goods, services including financial services, interest anddividends, rent, tourism)

1 Visibles (merchandise account): traded goods, processed goods,repairs on goods, gold, purchase of capital goods such as machinery,aircrafts

2 Invisibles (service account): rights, licenses, insurance, tourism andother intangibles

3 Interests, Profits and Dividends: rents from capital services, e.g.rental income, interest on deposit accounts, dividend payments onstocks, other profits transfers.

4 Transfers: worker’s remittances, aid.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 12 / 93

BOP Items: Current Account

Current account (CRA): Here and now. Export receipts (X) ascredits, import payments (M) as debits, net = current accountbalance (goods, services including financial services, interest anddividends, rent, tourism)

1 Visibles (merchandise account): traded goods, processed goods,repairs on goods, gold, purchase of capital goods such as machinery,aircrafts

2 Invisibles (service account): rights, licenses, insurance, tourism andother intangibles

3 Interests, Profits and Dividends: rents from capital services, e.g.rental income, interest on deposit accounts, dividend payments onstocks, other profits transfers.

4 Transfers: worker’s remittances, aid.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 12 / 93

BOP Items: Current Account

Current account (CRA): Here and now. Export receipts (X) ascredits, import payments (M) as debits, net = current accountbalance (goods, services including financial services, interest anddividends, rent, tourism)

1 Visibles (merchandise account): traded goods, processed goods,repairs on goods, gold, purchase of capital goods such as machinery,aircrafts

2 Invisibles (service account): rights, licenses, insurance, tourism andother intangibles

3 Interests, Profits and Dividends: rents from capital services, e.g.rental income, interest on deposit accounts, dividend payments onstocks, other profits transfers.

4 Transfers: worker’s remittances, aid.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 12 / 93

BOP Items: Current Account

Current account (CRA): Here and now. Export receipts (X) ascredits, import payments (M) as debits, net = current accountbalance (goods, services including financial services, interest anddividends, rent, tourism)

1 Visibles (merchandise account): traded goods, processed goods,repairs on goods, gold, purchase of capital goods such as machinery,aircrafts

2 Invisibles (service account): rights, licenses, insurance, tourism andother intangibles

3 Interests, Profits and Dividends: rents from capital services, e.g.rental income, interest on deposit accounts, dividend payments onstocks, other profits transfers.

4 Transfers: worker’s remittances, aid.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 12 / 93

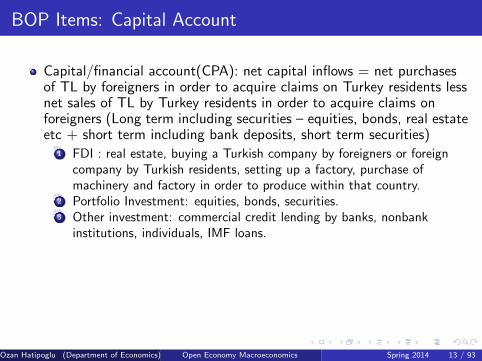

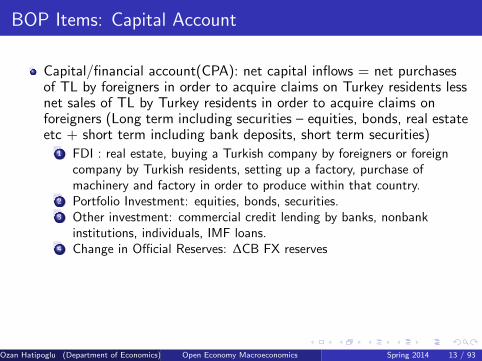

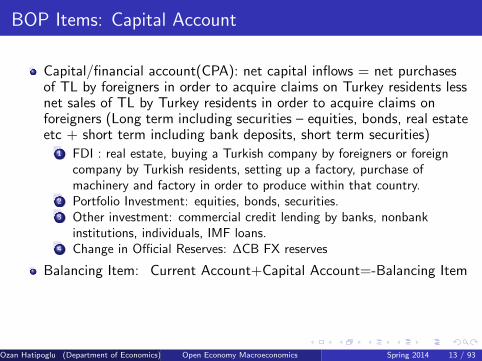

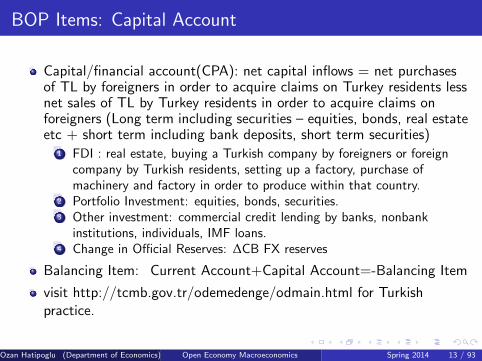

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.

3 Other investment: commercial credit lending by banks, nonbankinstitutions, individuals, IMF loans.

4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.

4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

BOP Items: Capital Account

Capital/financial account(CPA): net capital inflows = net purchasesof TL by foreigners in order to acquire claims on Turkey residents lessnet sales of TL by Turkey residents in order to acquire claims onforeigners (Long term including securities – equities, bonds, real estateetc + short term including bank deposits, short term securities)

1 FDI : real estate, buying a Turkish company by foreigners or foreigncompany by Turkish residents, setting up a factory, purchase ofmachinery and factory in order to produce within that country.

2 Portfolio Investment: equities, bonds, securities.3 Other investment: commercial credit lending by banks, nonbank

institutions, individuals, IMF loans.4 Change in Official Reserves: ∆CB FX reserves

Balancing Item: Current Account+Capital Account=-Balancing Item

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 13 / 93

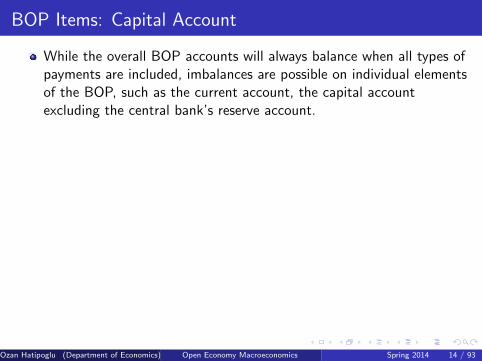

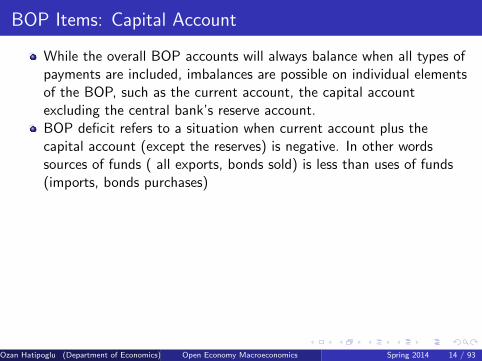

BOP Items: Capital Account

While the overall BOP accounts will always balance when all types ofpayments are included, imbalances are possible on individual elementsof the BOP, such as the current account, the capital accountexcluding the central bank’s reserve account.

BOP deficit refers to a situation when current account plus thecapital account (except the reserves) is negative. In other wordssources of funds ( all exports, bonds sold) is less than uses of funds(imports, bonds purchases)BOP Deficit 6= Current Account Deficit 6= Capital Account DeficitBOP imbalances are due to: the exchange rate, the government’sfiscal deficit, business competitiveness, and private behaviour such asthe willingness of consumers to go into debt to finance extraconsumption. Ben Bernanke argues that the primary driver is thecapital account, where a global savings glut caused by savers insurplus countries, runs ahead of the available investmentopportunities, and is pushed into the US resulting in excessconsumption and asset price inflationvisit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 14 / 93

BOP Items: Capital Account

While the overall BOP accounts will always balance when all types ofpayments are included, imbalances are possible on individual elementsof the BOP, such as the current account, the capital accountexcluding the central bank’s reserve account.BOP deficit refers to a situation when current account plus thecapital account (except the reserves) is negative. In other wordssources of funds ( all exports, bonds sold) is less than uses of funds(imports, bonds purchases)

BOP Deficit 6= Current Account Deficit 6= Capital Account DeficitBOP imbalances are due to: the exchange rate, the government’sfiscal deficit, business competitiveness, and private behaviour such asthe willingness of consumers to go into debt to finance extraconsumption. Ben Bernanke argues that the primary driver is thecapital account, where a global savings glut caused by savers insurplus countries, runs ahead of the available investmentopportunities, and is pushed into the US resulting in excessconsumption and asset price inflationvisit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 14 / 93

BOP Items: Capital Account

While the overall BOP accounts will always balance when all types ofpayments are included, imbalances are possible on individual elementsof the BOP, such as the current account, the capital accountexcluding the central bank’s reserve account.BOP deficit refers to a situation when current account plus thecapital account (except the reserves) is negative. In other wordssources of funds ( all exports, bonds sold) is less than uses of funds(imports, bonds purchases)BOP Deficit 6= Current Account Deficit 6= Capital Account Deficit

BOP imbalances are due to: the exchange rate, the government’sfiscal deficit, business competitiveness, and private behaviour such asthe willingness of consumers to go into debt to finance extraconsumption. Ben Bernanke argues that the primary driver is thecapital account, where a global savings glut caused by savers insurplus countries, runs ahead of the available investmentopportunities, and is pushed into the US resulting in excessconsumption and asset price inflationvisit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 14 / 93

BOP Items: Capital Account

While the overall BOP accounts will always balance when all types ofpayments are included, imbalances are possible on individual elementsof the BOP, such as the current account, the capital accountexcluding the central bank’s reserve account.BOP deficit refers to a situation when current account plus thecapital account (except the reserves) is negative. In other wordssources of funds ( all exports, bonds sold) is less than uses of funds(imports, bonds purchases)BOP Deficit 6= Current Account Deficit 6= Capital Account DeficitBOP imbalances are due to: the exchange rate, the government’sfiscal deficit, business competitiveness, and private behaviour such asthe willingness of consumers to go into debt to finance extraconsumption. Ben Bernanke argues that the primary driver is thecapital account, where a global savings glut caused by savers insurplus countries, runs ahead of the available investmentopportunities, and is pushed into the US resulting in excessconsumption and asset price inflation

visit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 14 / 93

BOP Items: Capital Account

While the overall BOP accounts will always balance when all types ofpayments are included, imbalances are possible on individual elementsof the BOP, such as the current account, the capital accountexcluding the central bank’s reserve account.BOP deficit refers to a situation when current account plus thecapital account (except the reserves) is negative. In other wordssources of funds ( all exports, bonds sold) is less than uses of funds(imports, bonds purchases)BOP Deficit 6= Current Account Deficit 6= Capital Account DeficitBOP imbalances are due to: the exchange rate, the government’sfiscal deficit, business competitiveness, and private behaviour such asthe willingness of consumers to go into debt to finance extraconsumption. Ben Bernanke argues that the primary driver is thecapital account, where a global savings glut caused by savers insurplus countries, runs ahead of the available investmentopportunities, and is pushed into the US resulting in excessconsumption and asset price inflationvisit http://tcmb.gov.tr/odemedenge/odmain.html for Turkishpractice.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 14 / 93

Relationship Between BOP and FX rate regime

Under pure float: Total net underlying demand for TL = CRAsurplus+CPA surplus =Basic balance is equated to zero by exchangerate movement, unless

Under fixed rates: Government intervenes to fix exchange rate, inwhich case. Item for 4 in CPA :∆CB FX reserves= CRA+CPA toprevent basic balance causing exchange rate to move

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 15 / 93

Relationship Between BOP and FX rate regime

Under pure float: Total net underlying demand for TL = CRAsurplus+CPA surplus =Basic balance is equated to zero by exchangerate movement, unless

Under fixed rates: Government intervenes to fix exchange rate, inwhich case. Item for 4 in CPA :∆CB FX reserves= CRA+CPA toprevent basic balance causing exchange rate to move

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 15 / 93

Balance of Payments: Crisis and Balancing Mechanisms

A BOP crisis (currency crisis) occurs when a nation is unable toservice its debt repayments and/or to pay for essential imports. Itgenerally is coupled with a fast depreciation of home currency.

General Mechanism: Large Capital Inflows over Time (either due tofinance high economic growth, in this case to finance investment / ordue to excessive consumption, in this case to finance consumption (and lower savings)) → unsustainable levels of debt creates a chain ofevents: → investors pull out their funds by selling domestic currencydenominated assets causing rapid depreciation of home currency →Local banks and firms run in to sudden debt problems because theirrevenues are in local currency but their existing debt is in foreigncurrency → the central bank can support the currency as long as ithas enough FXreserves, but once reserves fall below a certain levelchooses to increase interest rates to prevent outflows → preventscurrency depreciation and reduces the value of debt in domesticcurrency→ however, the domestic economy is depressed → recessionfollows.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 16 / 93

Balance of Payments: Crisis and Balancing Mechanisms

A BOP crisis (currency crisis) occurs when a nation is unable toservice its debt repayments and/or to pay for essential imports. Itgenerally is coupled with a fast depreciation of home currency.General Mechanism: Large Capital Inflows over Time (either due tofinance high economic growth, in this case to finance investment / ordue to excessive consumption, in this case to finance consumption (and lower savings)) → unsustainable levels of debt creates a chain ofevents: → investors pull out their funds by selling domestic currencydenominated assets causing rapid depreciation of home currency →Local banks and firms run in to sudden debt problems because theirrevenues are in local currency but their existing debt is in foreigncurrency → the central bank can support the currency as long as ithas enough FXreserves, but once reserves fall below a certain levelchooses to increase interest rates to prevent outflows → preventscurrency depreciation and reduces the value of debt in domesticcurrency→ however, the domestic economy is depressed → recessionfollows.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 16 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)

1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price

2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson

2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model

3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

Theories about Exchange Rate Determination

Purchasing Power Parity (PPP)1 Law of One Price2 PPP Extensions

1 Harrod-Balassa-Samuelson2 Trade Costs(Iceberg) Model3 Incomplete Pass-Through

Uncovered Interest Rate Parity

Covered Interest Rate Parity

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 17 / 93

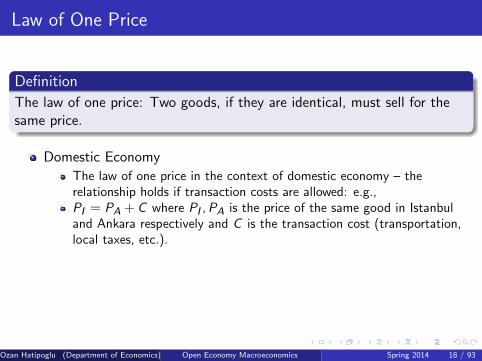

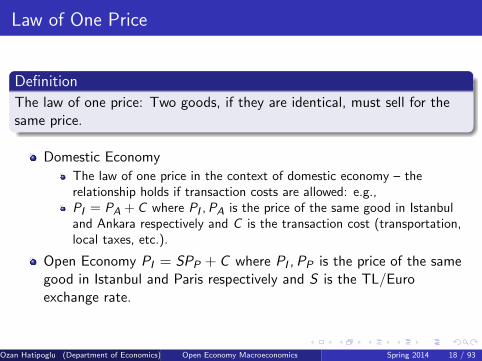

Law of One Price

Definition

The law of one price: Two goods, if they are identical, must sell for thesame price.

Domestic Economy

The law of one price in the context of domestic economy – therelationship holds if transaction costs are allowed: e.g.,PI = PA + C where PI , PA is the price of the same good in Istanbuland Ankara respectively and C is the transaction cost (transportation,local taxes, etc.).

Open Economy PI = SPP + C where PI , PP is the price of the samegood in Istanbul and Paris respectively and S is the TL/Euroexchange rate.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 18 / 93

Law of One Price

Definition

The law of one price: Two goods, if they are identical, must sell for thesame price.

Domestic Economy

The law of one price in the context of domestic economy – therelationship holds if transaction costs are allowed: e.g.,

PI = PA + C where PI , PA is the price of the same good in Istanbuland Ankara respectively and C is the transaction cost (transportation,local taxes, etc.).

Open Economy PI = SPP + C where PI , PP is the price of the samegood in Istanbul and Paris respectively and S is the TL/Euroexchange rate.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 18 / 93

Law of One Price

Definition

The law of one price: Two goods, if they are identical, must sell for thesame price.

Domestic Economy

The law of one price in the context of domestic economy – therelationship holds if transaction costs are allowed: e.g.,PI = PA + C where PI , PA is the price of the same good in Istanbuland Ankara respectively and C is the transaction cost (transportation,local taxes, etc.).

Open Economy PI = SPP + C where PI , PP is the price of the samegood in Istanbul and Paris respectively and S is the TL/Euroexchange rate.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 18 / 93

Law of One Price

Definition

The law of one price: Two goods, if they are identical, must sell for thesame price.

Domestic Economy

The law of one price in the context of domestic economy – therelationship holds if transaction costs are allowed: e.g.,PI = PA + C where PI , PA is the price of the same good in Istanbuland Ankara respectively and C is the transaction cost (transportation,local taxes, etc.).

Open Economy PI = SPP + C where PI , PP is the price of the samegood in Istanbul and Paris respectively and S is the TL/Euroexchange rate.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 18 / 93

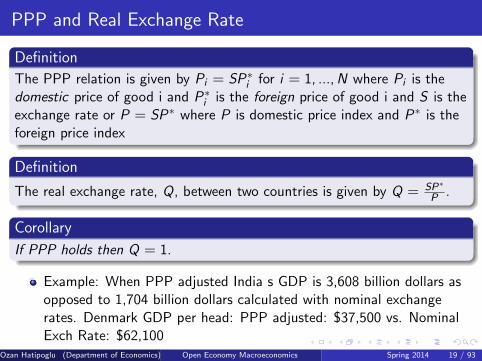

PPP and Real Exchange Rate

Definition

The PPP relation is given by Pi = SP∗i for i = 1, ..., N where Pi is thedomestic price of good i and P∗i is the foreign price of good i and S is theexchange rate or P = SP∗ where P is domestic price index and P∗ is theforeign price index

Definition

The real exchange rate, Q, between two countries is given by Q = SP∗

P .

Corollary

If PPP holds then Q = 1.

Example: When PPP adjusted India s GDP is 3,608 billion dollars asopposed to 1,704 billion dollars calculated with nominal exchangerates. Denmark GDP per head: PPP adjusted: $37,500 vs. NominalExch Rate: $62,100

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 19 / 93

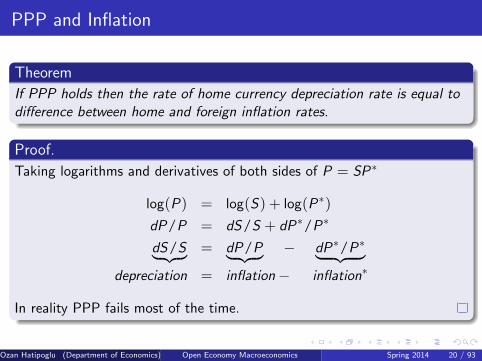

PPP and Inflation

Theorem

If PPP holds then the rate of home currency depreciation rate is equal todifference between home and foreign inflation rates.

Proof.

Taking logarithms and derivatives of both sides of P = SP∗

log(P) = log(S) + log(P∗)

dP/P = dS/S + dP∗/P∗

dS/S︸ ︷︷ ︸ = dP/P︸ ︷︷ ︸ − dP∗/P∗︸ ︷︷ ︸depreciation = inflation− inflation∗

In reality PPP fails most of the time.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 20 / 93

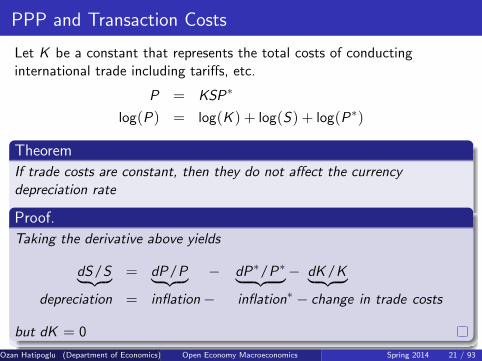

PPP and Transaction Costs

Let K be a constant that represents the total costs of conductinginternational trade including tariffs, etc.

P = KSP∗

log(P) = log(K ) + log(S) + log(P∗)

Theorem

If trade costs are constant, then they do not affect the currencydepreciation rate

Proof.

Taking the derivative above yields

dS/S︸ ︷︷ ︸ = dP/P︸ ︷︷ ︸ − dP∗/P∗︸ ︷︷ ︸− dK /K︸ ︷︷ ︸depreciation = inflation− inflation∗ − change in trade costs

but dK = 0

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 21 / 93

Harrod, Balassa and Samuelson Effect

Definition

The observation that consumer price levels in wealthier countries aresystematically higher than in poorer ones (the ”Penn effect”).

Definition

An economic model predicting the above, based on the assumption thatproductivity or productivity growth-rates vary more by country in thetraded goods’ sectors than in other sectors (the Balassa–Samuelsonhypothesis)

Workers in some countries have higher productivity than in others.

Certain labour-intensive jobs such as those in services are lessresponsive to productivity innovations than others.

Some of the fixed-productivity sectors are also the ones producingnon-transportable goods (for instance haircuts) - this must be thecase or the labour intensive work would have been off-shored.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 22 / 93

Harrod, Balassa and Samuelson Effect

Definition

The observation that consumer price levels in wealthier countries aresystematically higher than in poorer ones (the ”Penn effect”).

Definition

An economic model predicting the above, based on the assumption thatproductivity or productivity growth-rates vary more by country in thetraded goods’ sectors than in other sectors (the Balassa–Samuelsonhypothesis)

Workers in some countries have higher productivity than in others.

Certain labour-intensive jobs such as those in services are lessresponsive to productivity innovations than others.

Some of the fixed-productivity sectors are also the ones producingnon-transportable goods (for instance haircuts) - this must be thecase or the labour intensive work would have been off-shored.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 22 / 93

Harrod, Balassa and Samuelson Effect

Definition

The observation that consumer price levels in wealthier countries aresystematically higher than in poorer ones (the ”Penn effect”).

Definition

An economic model predicting the above, based on the assumption thatproductivity or productivity growth-rates vary more by country in thetraded goods’ sectors than in other sectors (the Balassa–Samuelsonhypothesis)

Workers in some countries have higher productivity than in others.

Certain labour-intensive jobs such as those in services are lessresponsive to productivity innovations than others.

Some of the fixed-productivity sectors are also the ones producingnon-transportable goods (for instance haircuts) - this must be thecase or the labour intensive work would have been off-shored.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 22 / 93

Harrod, Balassa and Samuelson Effect(cont’d)

To equalize local wage levels with the (highly productive) Zurichengineers, McDonalds Zurich employees must be paid more thanMcDonalds Moscow employees, even though the burger productionrate per employee is an international constant.

The CPI is made up of:local goods/services (which are expensive relative to tradables in richcountries)Tradables, which have the same price everywhereThe (real) exchange rate is pegged (by the law of one price) so thattradable goods follow PPP (purchasing power parity) but not localgoods.. PPP holds only for tradable goods. Entirely tradable goodscannot vary greatly in price by location (because buyers can sourcefrom the lowest cost location). But most services must be deliveredlocally (e.g. hairdressing) which makes PPP-deviations sustainable.The Penn effect is that PPP-deviations usually occur in the samedirection: where incomes are high, average price levels are typicallyhigh.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 23 / 93

Harrod, Balassa and Samuelson Effect(cont’d)

To equalize local wage levels with the (highly productive) Zurichengineers, McDonalds Zurich employees must be paid more thanMcDonalds Moscow employees, even though the burger productionrate per employee is an international constant.The CPI is made up of:

local goods/services (which are expensive relative to tradables in richcountries)Tradables, which have the same price everywhereThe (real) exchange rate is pegged (by the law of one price) so thattradable goods follow PPP (purchasing power parity) but not localgoods.. PPP holds only for tradable goods. Entirely tradable goodscannot vary greatly in price by location (because buyers can sourcefrom the lowest cost location). But most services must be deliveredlocally (e.g. hairdressing) which makes PPP-deviations sustainable.The Penn effect is that PPP-deviations usually occur in the samedirection: where incomes are high, average price levels are typicallyhigh.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 23 / 93

Harrod, Balassa and Samuelson Effect(cont’d)

To equalize local wage levels with the (highly productive) Zurichengineers, McDonalds Zurich employees must be paid more thanMcDonalds Moscow employees, even though the burger productionrate per employee is an international constant.The CPI is made up of:local goods/services (which are expensive relative to tradables in richcountries)

Tradables, which have the same price everywhereThe (real) exchange rate is pegged (by the law of one price) so thattradable goods follow PPP (purchasing power parity) but not localgoods.. PPP holds only for tradable goods. Entirely tradable goodscannot vary greatly in price by location (because buyers can sourcefrom the lowest cost location). But most services must be deliveredlocally (e.g. hairdressing) which makes PPP-deviations sustainable.The Penn effect is that PPP-deviations usually occur in the samedirection: where incomes are high, average price levels are typicallyhigh.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 23 / 93

Harrod, Balassa and Samuelson Effect(cont’d)

To equalize local wage levels with the (highly productive) Zurichengineers, McDonalds Zurich employees must be paid more thanMcDonalds Moscow employees, even though the burger productionrate per employee is an international constant.The CPI is made up of:local goods/services (which are expensive relative to tradables in richcountries)Tradables, which have the same price everywhere

The (real) exchange rate is pegged (by the law of one price) so thattradable goods follow PPP (purchasing power parity) but not localgoods.. PPP holds only for tradable goods. Entirely tradable goodscannot vary greatly in price by location (because buyers can sourcefrom the lowest cost location). But most services must be deliveredlocally (e.g. hairdressing) which makes PPP-deviations sustainable.The Penn effect is that PPP-deviations usually occur in the samedirection: where incomes are high, average price levels are typicallyhigh.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 23 / 93

Harrod, Balassa and Samuelson Effect(cont’d)

To equalize local wage levels with the (highly productive) Zurichengineers, McDonalds Zurich employees must be paid more thanMcDonalds Moscow employees, even though the burger productionrate per employee is an international constant.The CPI is made up of:local goods/services (which are expensive relative to tradables in richcountries)Tradables, which have the same price everywhereThe (real) exchange rate is pegged (by the law of one price) so thattradable goods follow PPP (purchasing power parity) but not localgoods.. PPP holds only for tradable goods. Entirely tradable goodscannot vary greatly in price by location (because buyers can sourcefrom the lowest cost location). But most services must be deliveredlocally (e.g. hairdressing) which makes PPP-deviations sustainable.The Penn effect is that PPP-deviations usually occur in the samedirection: where incomes are high, average price levels are typicallyhigh.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 23 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

PPP Extensions- Arbitrage in goods.

Goods arbitrage only profitable when price deviation exceedstransactions costs, C , so:

If price deviation P − P∗ < C , no trade

If price deviation P − P∗ > C , trade.

But C different for each trader and each type of good

When price deviation large (small), arbitrage (not) profitable for mosttraders/goods

In general, larger the price deviation, greater volume of arbitrage andmore rapid is real exchange rate adjustment

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 24 / 93

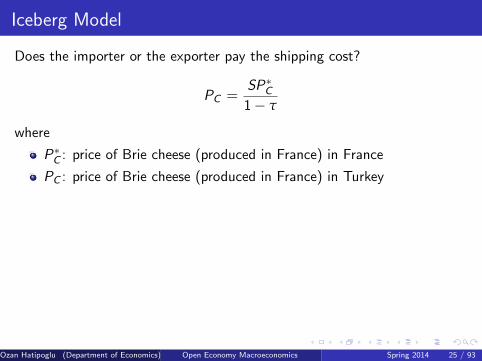

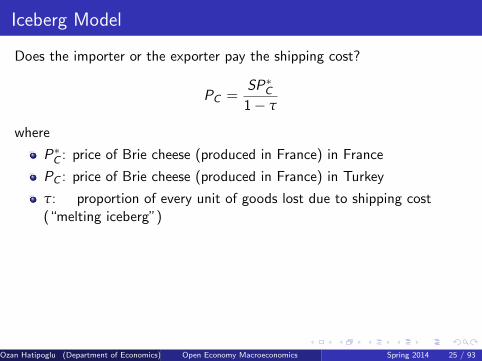

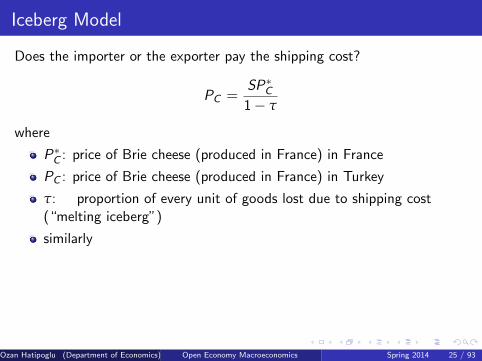

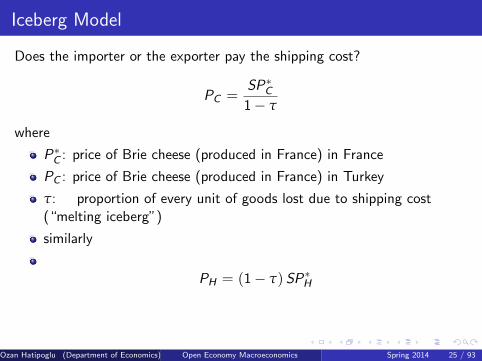

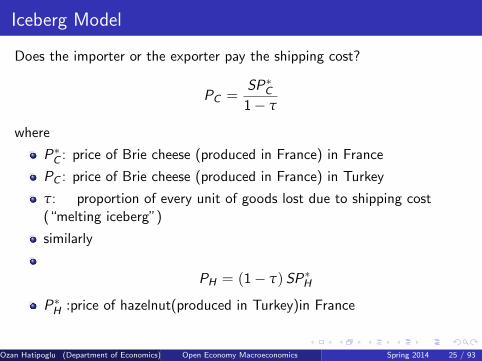

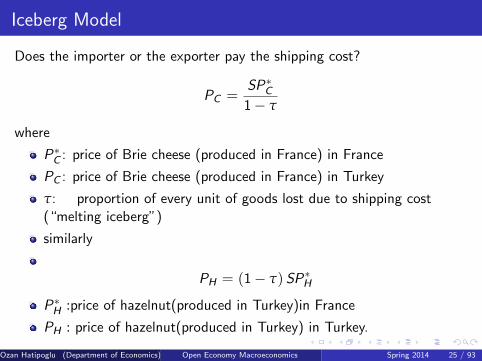

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

Iceberg Model

Does the importer or the exporter pay the shipping cost?

PC =SP∗C1− τ

where

P∗C : price of Brie cheese (produced in France) in France

PC : price of Brie cheese (produced in France) in Turkey

τ: proportion of every unit of goods lost due to shipping cost(“melting iceberg”)

similarly

PH = (1− τ) SP∗H

P∗H :price of hazelnut(produced in Turkey)in France

PH : price of hazelnut(produced in Turkey) in Turkey.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 25 / 93

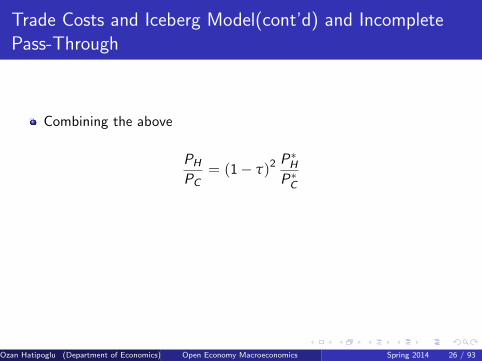

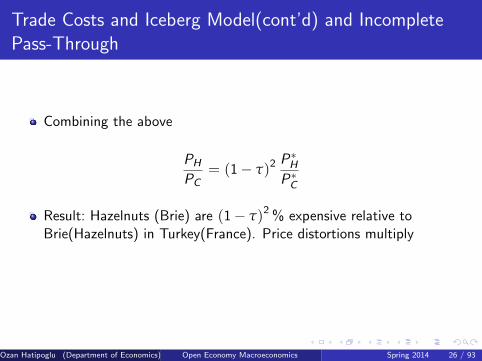

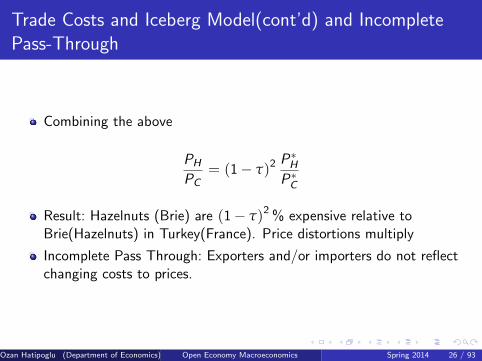

Trade Costs and Iceberg Model(cont’d) and IncompletePass-Through

Combining the above

PH

PC= (1− τ)2

P∗HP∗C

Result: Hazelnuts (Brie) are (1− τ)2 % expensive relative toBrie(Hazelnuts) in Turkey(France). Price distortions multiply

Incomplete Pass Through: Exporters and/or importers do not reflectchanging costs to prices.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 26 / 93

Trade Costs and Iceberg Model(cont’d) and IncompletePass-Through

Combining the above

PH

PC= (1− τ)2

P∗HP∗C

Result: Hazelnuts (Brie) are (1− τ)2 % expensive relative toBrie(Hazelnuts) in Turkey(France). Price distortions multiply

Incomplete Pass Through: Exporters and/or importers do not reflectchanging costs to prices.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 26 / 93

Trade Costs and Iceberg Model(cont’d) and IncompletePass-Through

Combining the above

PH

PC= (1− τ)2

P∗HP∗C

Result: Hazelnuts (Brie) are (1− τ)2 % expensive relative toBrie(Hazelnuts) in Turkey(France). Price distortions multiply

Incomplete Pass Through: Exporters and/or importers do not reflectchanging costs to prices.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 26 / 93

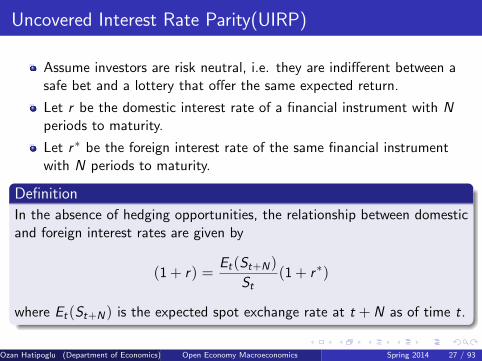

Uncovered Interest Rate Parity(UIRP)

Assume investors are risk neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return.

Let r be the domestic interest rate of a financial instrument with Nperiods to maturity.

Let r ∗ be the foreign interest rate of the same financial instrumentwith N periods to maturity.

Definition

In the absence of hedging opportunities, the relationship between domesticand foreign interest rates are given by

(1 + r) =Et(St+N)

St(1 + r ∗)

where Et(St+N) is the expected spot exchange rate at t + N as of time t.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 27 / 93

Uncovered Interest Rate Parity(UIRP)

Assume investors are risk neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return.

Let r be the domestic interest rate of a financial instrument with Nperiods to maturity.

Let r ∗ be the foreign interest rate of the same financial instrumentwith N periods to maturity.

Definition

In the absence of hedging opportunities, the relationship between domesticand foreign interest rates are given by

(1 + r) =Et(St+N)

St(1 + r ∗)

where Et(St+N) is the expected spot exchange rate at t + N as of time t.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 27 / 93

Uncovered Interest Rate Parity(UIRP)

Assume investors are risk neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return.

Let r be the domestic interest rate of a financial instrument with Nperiods to maturity.

Let r ∗ be the foreign interest rate of the same financial instrumentwith N periods to maturity.

Definition

In the absence of hedging opportunities, the relationship between domesticand foreign interest rates are given by

(1 + r) =Et(St+N)

St(1 + r ∗)

where Et(St+N) is the expected spot exchange rate at t + N as of time t.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 27 / 93

Uncovered Interest Rate Parity(UIRP)

Assume investors are risk neutral, i.e. they are indifferent between asafe bet and a lottery that offer the same expected return.

Let r be the domestic interest rate of a financial instrument with Nperiods to maturity.

Let r ∗ be the foreign interest rate of the same financial instrumentwith N periods to maturity.

Definition

In the absence of hedging opportunities, the relationship between domesticand foreign interest rates are given by

(1 + r) =Et(St+N)

St(1 + r ∗)

where Et(St+N) is the expected spot exchange rate at t + N as of time t.

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 27 / 93

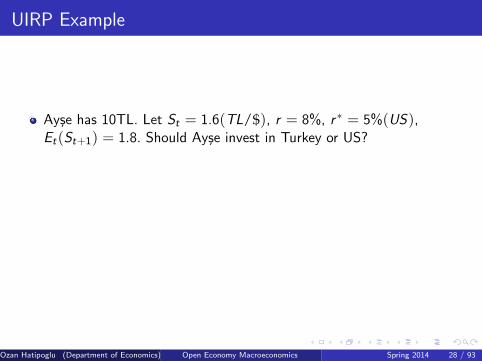

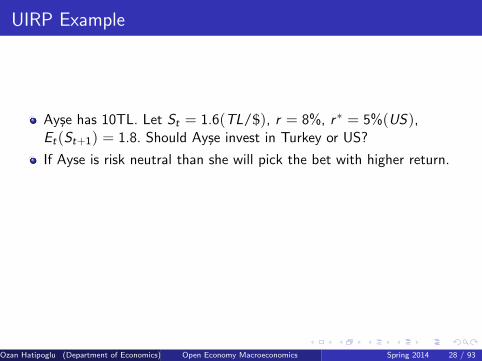

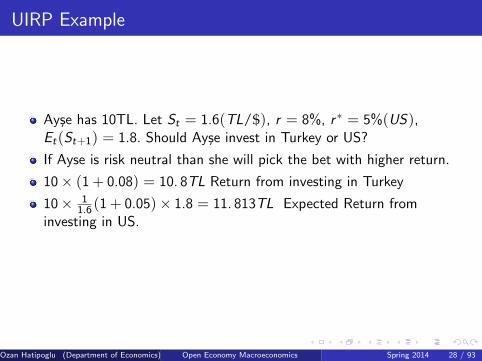

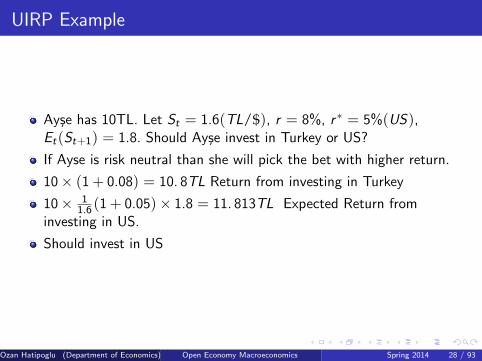

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r ∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will pick the bet with higher return.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 28 / 93

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r ∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will pick the bet with higher return.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 28 / 93

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r ∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will pick the bet with higher return.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 28 / 93

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r ∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will pick the bet with higher return.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 28 / 93

UIRP Example

Ayse has 10TL. Let St = 1.6(TL/$), r = 8%, r ∗ = 5%(US),Et(St+1) = 1.8. Should Ayse invest in Turkey or US?

If Ayse is risk neutral than she will pick the bet with higher return.

10× (1 + 0.08) = 10. 8TL Return from investing in Turkey

10× 11.6 (1 + 0.05)× 1.8 = 11. 813TL Expected Return from

investing in US.

Should invest in US

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 28 / 93

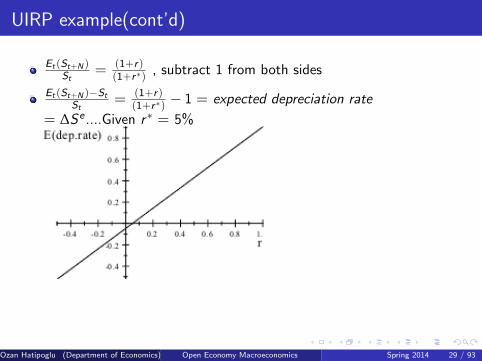

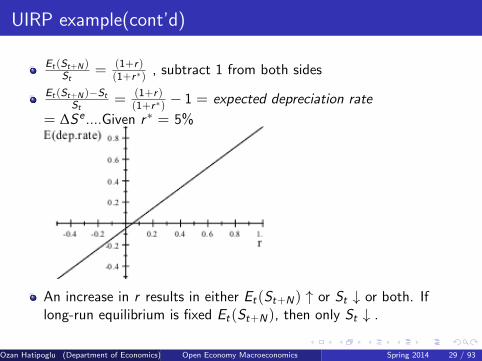

UIRP example(cont’d)

Et (St+N )St

= (1+r )(1+r ∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r )(1+r ∗) − 1 = expected depreciation rate

= ∆Se ....Given r ∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 29 / 93

UIRP example(cont’d)

Et (St+N )St

= (1+r )(1+r ∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r )(1+r ∗) − 1 = expected depreciation rate

= ∆Se ....Given r ∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 29 / 93

UIRP example(cont’d)

Et (St+N )St

= (1+r )(1+r ∗) , subtract 1 from both sides

Et (St+N )−StSt

= (1+r )(1+r ∗) − 1 = expected depreciation rate

= ∆Se ....Given r ∗ = 5%

An increase in r results in either Et(St+N) ↑ or St ↓ or both. Iflong-run equilibrium is fixed Et(St+N), then only St ↓ .

Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics Spring 2014 29 / 93

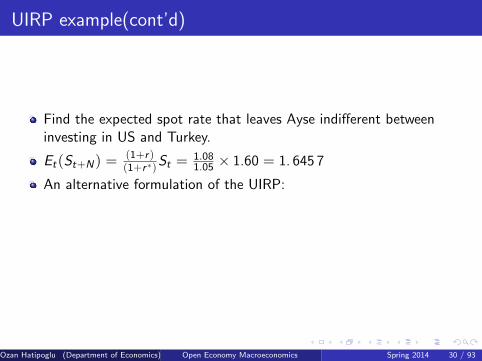

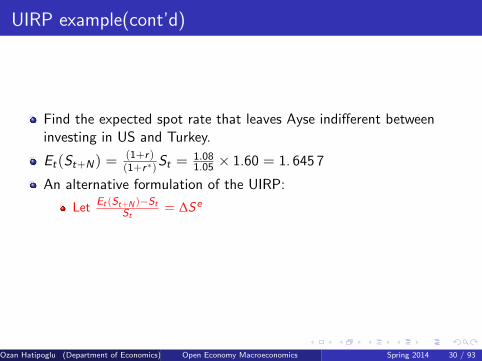

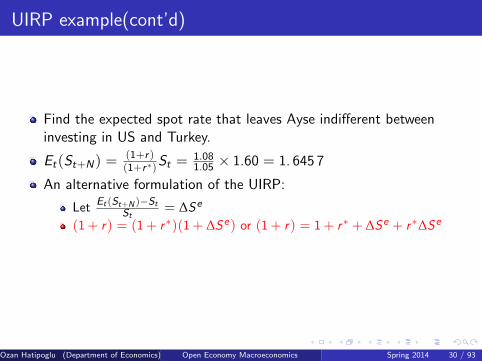

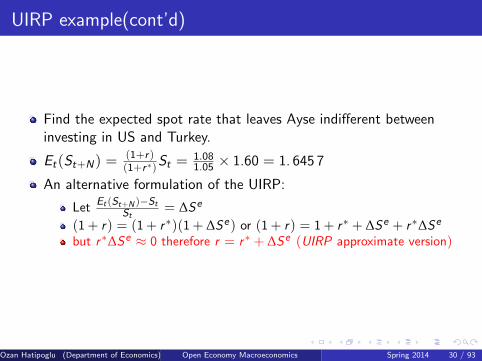

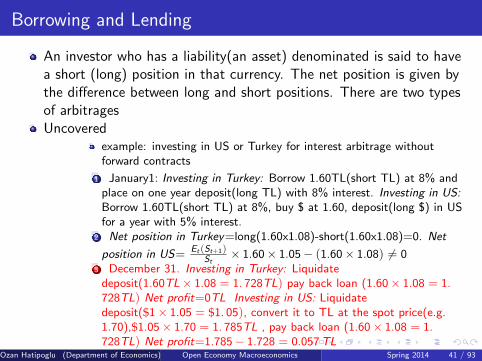

UIRP example(cont’d)