Embed Size (px)

Citation preview

1Øresund Trends 2012

English www.tendensoresund.org

Øresund Trends 2012

2 Øresund Trends 2012

Project ManagerBirgitte Steenstrup, [email protected]

Data collection, analysis and text Thomas Behrens The Swedish Employment ServiceMai Lundemark Copenhagen Municipality, Interreg-projektet Job og UddannelseGert Jørgensen Employment Region Copenhagen & ZealandEivor Johansson Malmö MunicipalityAnders Axelsson Region SkåneChristian Lindell Region SkåneChristina Ripa Region SkåneDaniel Svärd Region SkåneLova Wigvall Region SkåneLene Wittek-Holmberg Wonderful CopenhagenBritt Andresen The Öresund CommitteePeter Krygell The Öresund Committee

Editing and translation into Danish Marianne WormEtcetera Communicationswww.etcetera.dk

Translation into English Katie Schwarck, [email protected]

For more information, visitwww.tendensoresund.org

Graphic designMikael Forthwww.forth.dk

PrintingCS-Grafisk A/S

Print run500

3Øresund Trends 2012

ContEnts

A region in development . . . . . . . . . . . . . . . . . . . . . . . 4 Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Facts about the Øresund Region . . . . . . . . . . . . . . . . . 6 Geography. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Map of the Øresund Region. . . . . . . . . . . . . . . . . . . . . . . . 7 Demographics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Knowledge and innovation . . . . . . . . . . . . . . . . . . . . 12 Economic development. . . . . . . . . . . . . . . . . . . . . . . . . . .12 Business structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16 Research and development . . . . . . . . . . . . . . . . . . . . . . . .28 Education . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

Culture and Experience . . . . . . . . . . . . . . . . . . . . . . 40 Culture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40 Identity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .45 tourism . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .46 Health. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48 Welfare. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .54

A coherent and diverse labour market . . . . . . . . . . . 56 the labour market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56 Commuting across Øresund . . . . . . . . . . . . . . . . . . . . . . .62

Accessibility and mobility . . . . . . . . . . . . . . . . . . . . 70 Migration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .70 Housing and construction . . . . . . . . . . . . . . . . . . . . . . . . .78 House prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .84 traffic across Øresund. . . . . . . . . . . . . . . . . . . . . . . . . . . .90 Copenhagen Airport . . . . . . . . . . . . . . . . . . . . . . . . . . . . .94

About the analysis . . . . . . . . . . . . . . . . . . . . . . . . . 100Dark figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100 About Ørestat. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101 About Øresund trends . . . . . . . . . . . . . . . . . . . . . . . . . .102

Contact list . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

4 Øresund Trends 2012A REGIon In DEvEloPMEnt | PREFACE

A REGIon In DEvEloPMEnt Preface

The Øresund Region is home to 3.8 million people. Over the next 20 years, the population is projected to grow by a further 10 per cent.

The region is an important factor for both the Danish and Swedish national economy since 27 per cent of their com-bined GDP is created in the Øresund Region.

Within an economic context, Øresund integration is an important element on both sides of Øresund. In 2010, Øresund commuters contributed 751 million EUR in added value to the Danish economy. Since the opening of the Øresund Bridge in 2000 and as a re-sult of Øresund commuting, the Dan-ish economy has received a substantial financial injection totalling 4,4 billion EUR – which in 2010 prices is equiv-alent to 1.3 Øresund Bridges. In other

words, the social gains from the Øresund Bridge far exceed what it cost to build it. At the same time, Sweden saves 178 mil-lion euro per annum in unemployment benefit because unemployed Swedes find work in Denmark.

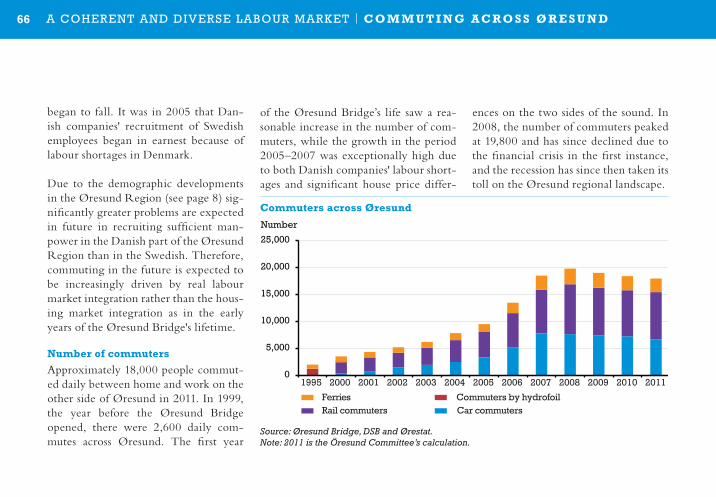

Like the rest of Europe, the Øresund Region has been affected by the finan-cial crisis. The crisis has led to a halt to the increase in relocation, commuting and traffic across the Øresund. In 2011, the number of daily commuters totalled 18,000, slightly lower than in 2008, when commuting was at its highest level with almost 20,000 commuters across Øresund. In 2011, an average of 91,500 individuals crossed Øresund (by car, coach, train and ferry) and 24,700 ve-hicles crossed Øresund every day. This is an increase of 1 per cent in passenger numbers and a decrease of 2 per cent on the year in the number of vehicles.Economic growth in the Øresund

Region (6 per cent) in the period 2000-2009 was lower than the average for the EU27 area (13 per cent). The develop-ment is significantly lower than in both the Helsinki Region (24 per cent) and Stockholm County (30 per cent).

However, gross regional product per employee during 2000-2009 was stronger in the Øresund Region (5.3 per cent) than the average for all regions in Europe (4.2 per cent). This is still lower than in Stockholm (19.2 per cent) and Helsinki (16.9 per cent) for the period 2000-2009. This is a situation that needs to be addressed if the Øresund Region is to remain an important driver for the whole of Scandinavia.

The Øresund Region has considera-ble potential, which could be exploit-ed better. 35 per cent of the population has a higher education, which is above the national level in both Denmark

5Øresund Trends 2012

and Sweden. In total, approximately 150,000 students study at the region's 11 universities and higher educational in-stitutions.

The percentage of gross regional prod-uct spent on research and development in the Øresund Region is among the highest (4.9 per cent) in Europe. At the same time, 43 per cent of industry’s total investment in research and development for the whole of Denmark and Sweden is placed in the region. Nevertheless, all signs are that it is not easy to turn these investments into innovation and commercial products, which is a general problem in Denmark and Sweden.

12 years after the opening of the Øresund Bridge, it is gratifying to note that a common Øresund regional iden-tity among the citizens of the region is growing. But identity and integration assume increased and mutual communi-

cation across Øresund within the areas of culture, the labour market, knowl-edge and innovation as well as traf-fic and infrastucture. Øresund Trends monitors and analyses this integration and we hope you will find the analysis interesting.

A REGIon In DEvEloPMEnt | PREFACE

6 Øresund Trends 2012

FACts ABout tHE ØREsunD REGIon GEoGRAPhy

Geographically, the Øresund Region consists of Zealand, Lolland, Falster, Møn and Bornholm on the Danish side and Scania on the Swedish side of Øresund – hence the name. Adminis-tratively, it consists of three regions: the Capital Region of Denmark and Region Zealand on the Danish side and Scania on the Swedish side.

The Øresund Region’s Danish and Swed-ish sides are connected in the south by the 16 km long Øresund Bridge between Co-penhagen and Malmö, which opened in 2000, and in the north, by the ferry link between Elsinore and Helsingborg.

The Øresund Region covers a total area of 21,203 square kilometres – equiva-lent to half the entire area of Denmark – with 9,834 square kilometres on the Danish side and 11,369 on the Swedish

side. Measured in square metres, Scania is the largest, but about two-thirds of the 3.8 million inhabitants in the Øresund Region live on the Danish side, which has 2.5 million inhabitants while there are 1.3 million on the Swedish side.

The Øresund Region includes the capi-tal of Denmark, Copenhagen, and Swe-den's third largest city, Malmö. Copen-hagen-Malmö is the largest urban area in Scandinavia.

The average population density is 179 inhabitants per square kilometre: high-est on the Danish side with 258 inhabit-ants per square kilometre and lowest on the Swedish side with 110 inhabitants per square kilometre. There is signifi-cant geographic variation: from dense metropolitan areas such as Copenhagen and Malmö to the relatively sparsely populated rural municipalities of Lol-land and in eastern Scania.

Administratively, the Øresund Region consists of the 33 municipalities that make up the Scania region on the Swed-ish side, while on the Danish side there are the 46 municipalities that make up the Capital Region and Region Zea-land.

Population figures in the Øresund Region’s six largest municipalities (mid-2012)

Copenhagen 552,000Frederiksberg 101,000Roskilde 83,000

Malmö 305,000helsingborg 131,000Lund 112,000

Source: Statistics Denmark and Statistics Sweden.

FACts ABout tHE ØREsunD REGIon | GEoGRAPhy

7Øresund Trends 2012

lolland Guldborg-sund

næstved

slagelse

vording-borg

Faxe

Køge

stevns

Ring-sted

sorø

Kalund-borg

Holbæk

odsherred Frederikssund

lejre Roskilde

solrød

Greve

Egedal

Frederiks-værk-Hundested

GribskovHelsingør

HillerødFredens-borg

HørsholmAllerød

RudersdalFuresø

Høje-taastrup

lyngby-taarbæk

GentofteGlad- saxeHer-

levBallerup

Copenhagen

Frederiks-bergAlbertslund Glos-

trup

Rød-ovre

Ishøjval-lens-bæk

Brønd-by Hvid-

ovretårnby

Dragør

Båstad

Ängelhom

Höganäs

Helsing-borg

Åstorp

BjuvKlippan

svalöv

lands-krona

Kävlinge

lomma

Burlöv

Malmö

staffans-torp

lund

vellinge

trelle-borg

svedalaskurup

Eslöv

Höör

Hörby

sjöbo

Ystad

tomelillasimrishamn

Kristianstad

Hässle-holmPerstorp

Örkelljunga

Bro-mölla

Östra Göinge

osby

Born-holm

Capital Region

Region Zealand

Capital Region

SCAniA

FACts ABout tHE ØREsunD REGIon | GEoGRAPhy

8 Øresund Trends 2012

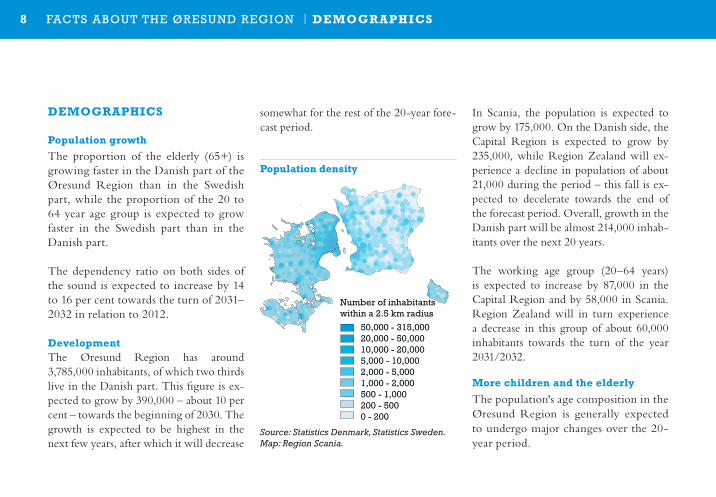

DEMoGRAPhiCS

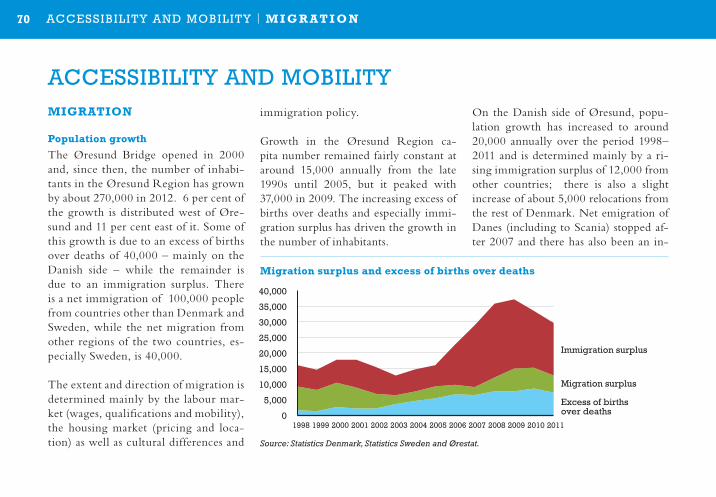

Population growth

The proportion of the elderly (65+) is growing faster in the Danish part of the Øresund Region than in the Swedish part, while the proportion of the 20 to 64 year age group is expected to grow faster in the Swedish part than in the Danish part.

The dependency ratio on both sides of the sound is expected to increase by 14 to 16 per cent towards the turn of 2031–2032 in relation to 2012.

DevelopmentThe Øresund Region has around 3,785,000 inhabitants, of which two thirds live in the Danish part. This figure is ex-pected to grow by 390,000 – about 10 per cent – towards the beginning of 2030. The growth is expected to be highest in the next few years, after which it will decrease

somewhat for the rest of the 20-year fore-cast period.

In Scania, the population is expected to grow by 175,000. On the Danish side, the Capital Region is expected to grow by 235,000, while Region Zealand will ex-perience a decline in population of about 21,000 during the period – this fall is ex-pected to decelerate towards the end of the forecast period. Overall, growth in the Danish part will be almost 214,000 inhab-itants over the next 20 years.

The working age group (20–64 years) is expected to increase by 87,000 in the Capital Region and by 58,000 in Scania. Region Zealand will in turn experience a decrease in this group of about 60,000 inhabitants towards the turn of the year 2031/2032.

More children and the elderly

The population's age composition in the Øresund Region is generally expected to undergo major changes over the 20-year period.

50,000 - 315,00020,000 - 50,00010,000 - 20,0005,000 - 10,0002,000 - 5,0001,000 - 2,000500 - 1,000200 - 5000 - 200

Number of inhabitants within a 2.5 km radius

Source: Statistics Denmark, Statistics Sweden.Map: Region Scania.

Population density

FACts ABout tHE ØREsunD REGIon | DEMoGRAPhiCS

9Øresund Trends 2012

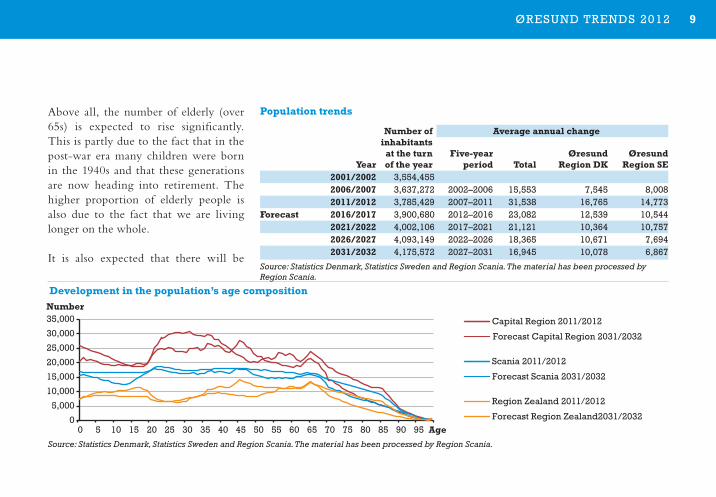

Above all, the number of elderly (over 65s) is expected to rise significantly. This is partly due to the fact that in the post-war era many children were born in the 1940s and that these generations are now heading into retirement. The higher proportion of elderly people is also due to the fact that we are living longer on the whole.

It is also expected that there will be

Population trends

number of inhabitants

at the turn of the year

Average annual change

yearFive-year

period TotalØresund

Region DKØresund

Region SE2001/2002 3,554,4552006/2007 3,637,272 2002–2006 15,553 7,545 8,0082011/2012 3,785,429 2007–2011 31,538 16,765 14,773

Forecast 2016/2017 3,900,680 2012–2016 23,082 12,539 10,5442021/2022 4,002,106 2017–2021 21,121 10,364 10,7572026/2027 4,093,149 2022–2026 18,365 10,671 7,6942031/2032 4,175,572 2027–2031 16,945 10,078 6,867

Source: Statistics Denmark, Statistics Sweden and Region Scania. The material has been processed by Region Scania.

Source: Statistics Denmark, Statistics Sweden and Region Scania. The material has been processed by Region Scania.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

Number

Age

Capital Region 2011/2012

Forecast Capital Region 2031/2032

Scania 2011/2012

Forecast Scania 2031/2032

Region Zealand 2011/2012

Forecast Region Zealand2031/2032

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Capita

l

Region

Region

Zeal

and

Scan

ia

Stock

holm

County

Denmar

k

Sweden

0 1 2 3 4 5 6 7 8 9

10

-90 -91 -92 -93 -94 -95 -96 -97 -98 -99 -00 -01 -02 -03 -04 -05 -06 -07 -08 -09 -10 -11

Million vehicles

Øresund Bridge Ferries Copenhagen-Malmö Ferries Elsinore-Helsingborg

0

5

10

15

20

25

30

35

40

-01 -02 -03 -04 -05 -06 -07 -08 -09 -10 -11

Million individuals

Car Train Ferries Hydrofoil

0102030405060708090

100

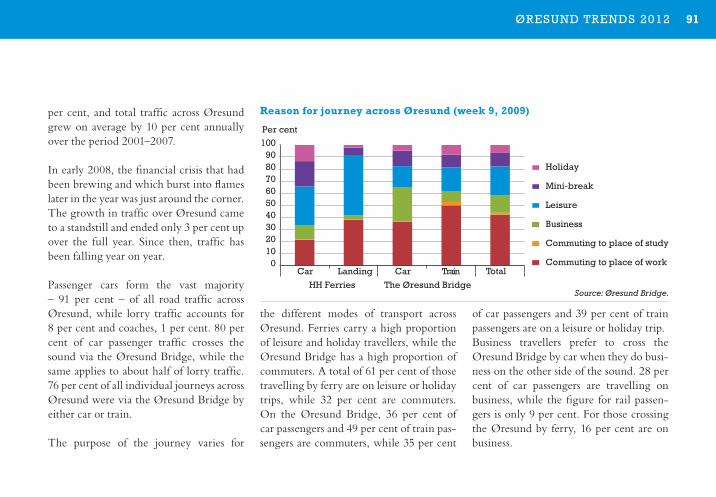

Car Landing Car TrainHH Ferries The Øresund Bridge

Total

Holiday

Mini-break

Leisure

Business

Commuting to place of study

Commuting to place of work

Per cent

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

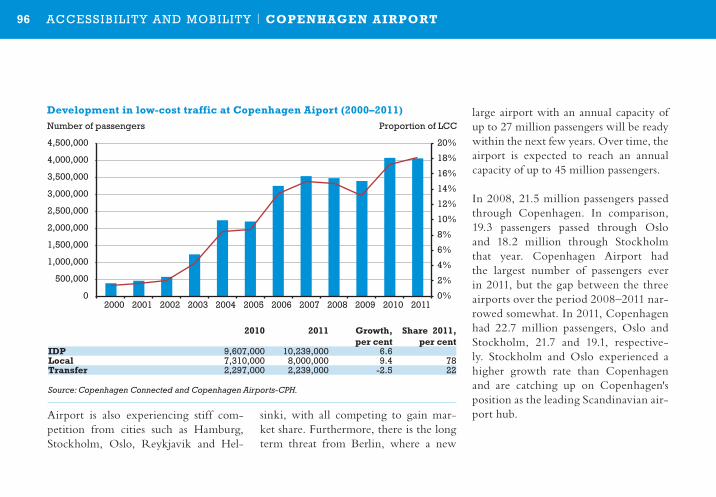

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Books, newspapers and magazines

Architectural business

Design, photography and translation

Theatre, concerts, artistic creation

Libraries and archives

Museums and cultural heritage collections

Film, video, TV, radio and press

Development in the population’s age composition

FACts ABout tHE ØREsunD REGIon | DEMoGRAPhiCS

10 Øresund Trends 2012

working age, Scanians supported three people more than the Danes.

By the turn of the year 2031–2032, it is expected that these figures will have increased to 0.79 (the Danish part) and 0.81 (the Swedish part). This will mean an increase in the dependency ratio of about 16 per cent in the Danish part and 14 per cent in the Swedish part. The gap between the two parts of the Øresund Region will then be narrowed down to a difference of about 2 per cent.

If you look at the breakdown of the dependency ratio between the two regions in the Danish part of the Øresund

FACts ABout tHE ØREsunD REGIon | DEMoGRAPhiCS

an increasing number of children and young people, especially in the Capital Region and Scania. This is due in large part to increased migration – both from peripheral areas in both countries and immigration from other countries – and that an increasing number are reaching childbearing age.

Consequences for the economy

The dependency ratio in the Øresund Region is expected to increase signif-icantly due to increasing population growth, especially in the non-active age groups, 0–19–year-olds and over 65s, which are growing faster than those aged 20–64.

The population’s changing age composi-tion will present challenges for the wel-fare state as we know it, particularly in relation to child care, schools, care of the elderly and demand for different types of housing. All types of care will come

under pressure because there will be few-er people of working age to support the overall dependency requirement, and more will demand public services.

The dependency ratio is defined as the burden of every person of working age (20–64) to provide beyond themselves. This ratio focuses purely on age, and not whether people of working age are in work or not.

In the Danish part of the Øresund Region, the dependency ratio in 2012 was 0.68 persons, while in the Swedish part it was marginally higher, at 0.71. This means that for every 100 people of

Development in dependency ratio (2012–2032)Geography 2011/2012 2012/2022 2031/2032Øresund Region DK 0.68 0.71 0.79Øresund Region SE 0.71 0.77 0.81Capital Region 0.64 0.65 0.72Region Zealand 0.77 0.86 0.98Source: Statistics Denmark, Statistics Sweden and Region Scania. The material has been processed by Region Scania.

11Øresund Trends 2012

Region, the difference between the two is significantly higher than the differ-ence between the Danish and Swedish parts. In 2012, the dependency ratio in the Capital Region was 0.64 while in Region Zealand it was 0.77 – a differ-ence of 0.13. At the turn of 2031–2032, the Capital Region's dependency ratio is expected to be 0.72, and Region Zealand will have a dependency ratio of 0.98 – these are significant increases of 27 per cent for Region Zealand and 13 per cent for the Capital Region, compared to 2012.

Although the dependency ratio is rising across the Øresund Region, the increase will be significantly greater in Region Zealand and Scania in comparison with the Capital Region. Scania and Region Zea-land will, at the turn of 2031–2032, have a dependency ratio of 0.81 and 0.98 respec-tively, while the Capital Region is expect-ed to have a dependency ratio of 0.72.

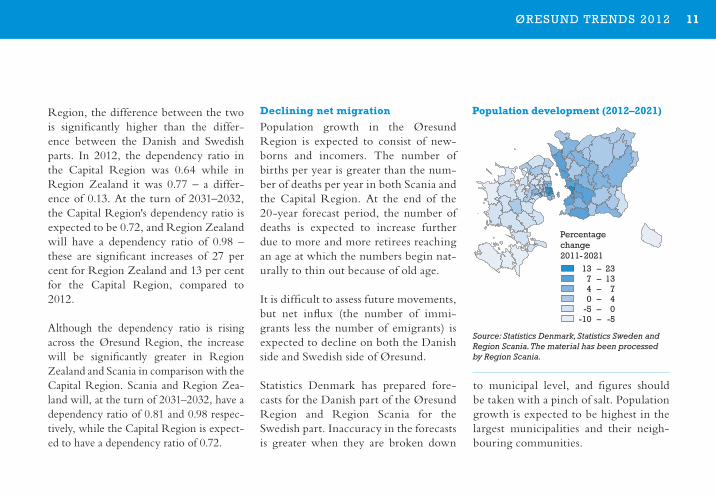

Declining net migration

Population growth in the Øresund Region is expected to consist of new-borns and incomers. The number of births per year is greater than the num-ber of deaths per year in both Scania and the Capital Region. At the end of the 20-year forecast period, the number of deaths is expected to increase further due to more and more retirees reaching an age at which the numbers begin nat-urally to thin out because of old age.

It is difficult to assess future movements, but net influx (the number of immi-grants less the number of emigrants) is expected to decline on both the Danish side and Swedish side of Øresund.

Statistics Denmark has prepared fore-casts for the Danish part of the Øresund Region and Region Scania for the Swedish part. Inaccuracy in the forecasts is greater when they are broken down

to municipal level, and figures should be taken with a pinch of salt. Population growth is expected to be highest in the largest municipalities and their neigh-bouring communities.

Percentage change 2011- 2021

13 – 23 7 – 13 4 – 7 0 – 4 -5 – 0 -10 – -5

Source: Statistics Denmark, Statistics Sweden and Region Scania. The material has been processed by Region Scania.

Population development (2012–2021)

FACts ABout tHE ØREsunD REGIon | DEMoGRAPhiCS

12 Øresund Trends 2012

EConoMiC DEvELoPMEnT

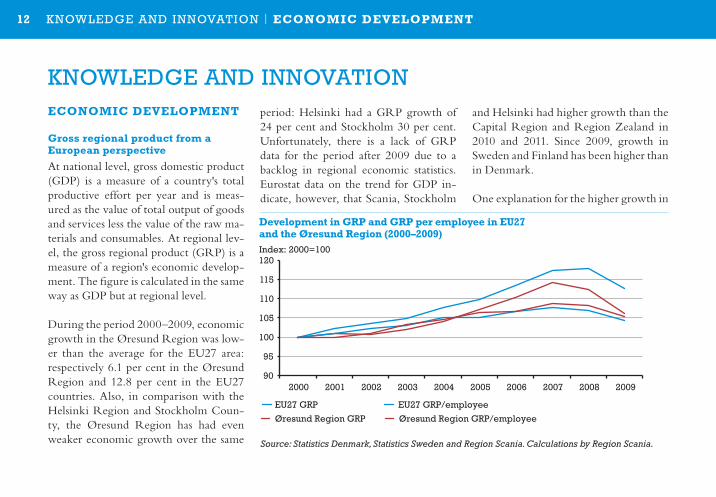

Gross regional product from a European perspective

At national level, gross domestic product (GDP) is a measure of a country's total productive effort per year and is meas-ured as the value of total output of goods and services less the value of the raw ma-terials and consumables. At regional lev-el, the gross regional product (GRP) is a measure of a region's economic develop-ment. The figure is calculated in the same way as GDP but at regional level.

During the period 2000–2009, economic growth in the Øresund Region was low-er than the average for the EU27 area: respectively 6.1 per cent in the Øresund Region and 12.8 per cent in the EU27 countries. Also, in comparison with the Helsinki Region and Stockholm Coun-ty, the Øresund Region has had even weaker economic growth over the same

period: Helsinki had a GRP growth of 24 per cent and Stockholm 30 per cent. Unfortunately, there is a lack of GRP data for the period after 2009 due to a backlog in regional economic statistics. Eurostat data on the trend for GDP in-dicate, however, that Scania, Stockholm

and Helsinki had higher growth than the Capital Region and Region Zealand in 2010 and 2011. Since 2009, growth in Sweden and Finland has been higher than in Denmark.

One explanation for the higher growth in

90

95

100

105

110

115

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Index: 2000=100

EU27 GRP

Øresund Region GRP

EU27 GRP/employee

Øresund Region GRP/employee

90

95

100

105

110

115

120

125

130

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Øresund Region DK

Region Zealand

Capital Region

Øresund Region SE (Scania)

Development in GRP and GRP per employee in EU27 and the Øresund Region (2000–2009)

Source: Statistics Denmark, Statistics Sweden and Region Scania. Calculations by Region Scania.

KnoWlEDGE AnD InnovAtIon | EConoMiC DEvELoPMEnT

KnoWlEDGE AnD InnovAtIon

13Øresund Trends 2012

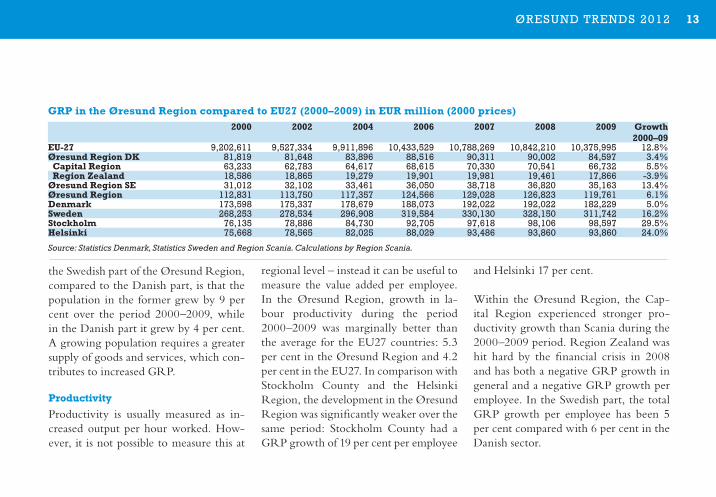

GRP in the Øresund Region compared to EU27 (2000–2009) in EUR million (2000 prices)2000 2002 2004 2006 2007 2008 2009 Growth

2000–09EU-27 9,202,611 9,527,334 9,911,896 10,433,529 10,788,269 10,842,210 10,375,995 12.8%Øresund Region DK 81,819 81,648 83,896 88,516 90,311 90,002 84,597 3.4% Capital Region 63,233 62,783 64,617 68,615 70,330 70,541 66,732 5.5% Region Zealand 18,586 18,865 19,279 19,901 19,981 19,461 17,866 -3.9%Øresund Region SE 31,012 32,102 33,461 36,050 38,718 36,820 35,163 13.4%Øresund Region 112,831 113,750 117,357 124,566 129,028 126,823 119,761 6.1%Denmark 173,598 175,337 178,679 188,073 192,022 192,022 182,229 5.0%Sweden 268,253 278,534 296,908 319,584 330,130 328,150 311,742 16.2%Stockholm 76,135 78,886 84,730 92,705 97,618 98,106 98,597 29.5%helsinki 75,668 78,565 82,025 88,029 93,486 93,860 93,860 24.0%

Source: Statistics Denmark, Statistics Sweden and Region Scania. Calculations by Region Scania.

the Swedish part of the Øresund Region, compared to the Danish part, is that the population in the former grew by 9 per cent over the period 2000–2009, while in the Danish part it grew by 4 per cent. A growing population requires a greater supply of goods and services, which con-tributes to increased GRP.

Productivity

Productivity is usually measured as in-creased output per hour worked. How-ever, it is not possible to measure this at

regional level – instead it can be useful to measure the value added per employee. In the Øresund Region, growth in la-bour productivity during the period 2000–2009 was marginally better than the average for the EU27 countries: 5.3 per cent in the Øresund Region and 4.2 per cent in the EU27. In comparison with Stockholm County and the Helsinki Region, the development in the Øresund Region was significantly weaker over the same period: Stockholm County had a GRP growth of 19 per cent per employee

and Helsinki 17 per cent.

Within the Øresund Region, the Cap-ital Region experienced stronger pro-ductivity growth than Scania during the 2000–2009 period. Region Zealand was hit hard by the financial crisis in 2008 and has both a negative GRP growth in general and a negative GRP growth per employee. In the Swedish part, the total GRP growth per employee has been 5 per cent compared with 6 per cent in the Danish sector.

KnoWlEDGE AnD InnovAtIon | EConoMiC DEvELoPMEnT

14 Øresund Trends 201290

95

100

105

110

115

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Index: 2000=100

EU27 GRP

Øresund Region GRP

EU27 GRP/employee

Øresund Region GRP/employee

90

95

100

105

110

115

120

125

130

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Øresund Region DK

Region Zealand

Capital Region

Øresund Region SE (Scania)

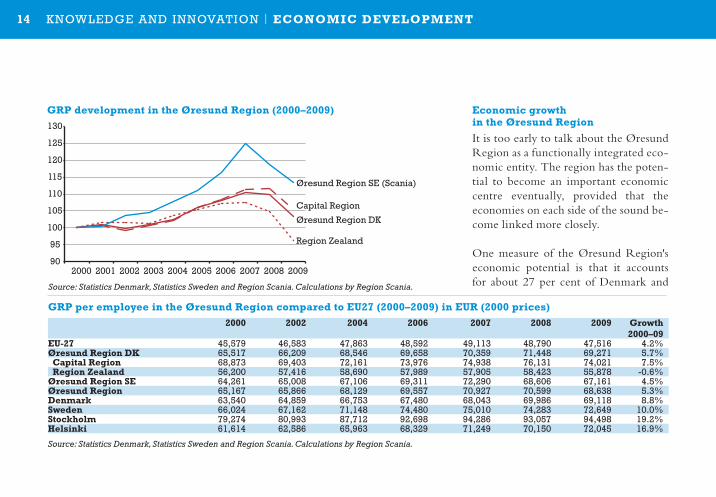

GRP development in the Øresund Region (2000–2009)

Source: Statistics Denmark, Statistics Sweden and Region Scania. Calculations by Region Scania.

GRP per employee in the Øresund Region compared to EU27 (2000–2009) in EUR (2000 prices) 2000 2002 2004 2006 2007 2008 2009 Growth

2000–09EU-27 45,579 46,583 47,863 48,592 49,113 48,790 47,516 4.2%Øresund Region DK 65,517 66,209 68,546 69,658 70,359 71,448 69,271 5.7% Capital Region 68,873 69,403 72,161 73,976 74,938 76,131 74,021 7.5% Region Zealand 56,200 57,416 58,690 57,989 57,905 58,423 55,878 -0.6%Øresund Region SE 64,261 65,008 67,106 69,311 72,290 68,606 67,161 4.5%Øresund Region 65,167 65,866 68,129 69,557 70,927 70,599 68,638 5.3%Denmark 63,540 64,859 66,753 67,480 68,043 69,986 69,118 8.8%Sweden 66,024 67,162 71,148 74,480 75,010 74,283 72,649 10.0%Stockholm 79,274 80,993 87,712 92,698 94,286 93,057 94,498 19.2%helsinki 61,614 62,586 65,963 68,329 71,249 70,150 72,045 16.9%

Source: Statistics Denmark, Statistics Sweden and Region Scania. Calculations by Region Scania.

Economic growth in the Øresund Region

It is too early to talk about the Øresund Region as a functionally integrated eco-nomic entity. The region has the poten-tial to become an important economic centre eventually, provided that the economies on each side of the sound be-come linked more closely.

One measure of the Øresund Region's economic potential is that it accounts for about 27 per cent of Denmark and

KnoWlEDGE AnD InnovAtIon | EConoMiC DEvELoPMEnT

15Øresund Trends 2012

Sweden's total GDP. In 2009, the Danish part of the Øresund Region accounted for 49 per cent of Denmark’s total GDP. The Capital Region alone accounted for 38 per cent and Region Zealand for 11 per cent. The Swedish part of the Øresund Region accounted for 11 per cent of Sweden's total GDP, which has remained unchanged since 2000.

The Danish part of the Øresund Region accounts for two-thirds of the Øresund Region's total GRP. GRP growth has been higher in Scania than in the Dan-ish part of the Øresund Region, partly due to the fact that the financial cri-sis hit Denmark harder than Sweden. While Scania’s GRP increased by 13 per cent during the period, the corre-sponding increase in the Danish part of the Øresund Region was just 3 per cent.

KnoWlEDGE AnD InnovAtIon | EConoMiC DEvELoPMEnT

16 Øresund Trends 2012

BUSinESS STRUCTURE

As with the rest of the Western world, the Øresund Region is undergoing structural changes: the proportion of persons employed in the private service sector is increasing, while the propor-tion of persons employed in production and agriculture is decreasing.

Because of a break in the statistics in 2007, it is not possible to set out the region's long-term structural chang-es, but it is certain that there are major structural differences between individu-al areas in the region.

In 2010, approximately 11 per cent of the total employment in the Capital Region was engaged in manufacturing, including the construction industry. By comparison, the figures for Region Zea-land and Scania were 18 and 20 per cent respectively. Although manufacturing is

falling in all three parts of the Øresund Region, the Capital Region is experi-encing the biggest drop.

On the other hand, the Capital Region has a high proportion of employees – 52 per cent – in the private service sector. In Region Zealand and Scania, the pri-vate service sector accounts for 43 and 44 per cent of total employment. The most prominent sectors in all three regions are business services, transport along with wholesale and retail trading.

The high-tech sector in Europe

Globalisation means that the 'old' econ-omies are facing increased competition from countries with lower costs and to counter the increased competition, it is necessary to think along new lines. One strategy could be to compete better on knowledge rather than price for goods and services. In order to analyse which countries/regions have knowledge-

intensive production, the OECD has identified a number of sectors of particu-lar interest under the classification 'high-tech'.

The high-tech classification includes in-dustries with high-tech service and goods production; for example, specialisation in the production of pharmaceuticals, com-munications and aircraft and, in the ser-vice sector, research and development as well as IT and telecommunications. It is slightly misleading to call some of these industries ‘high-tech’, since it is more about knowledge industries, which are both value-creating in themselves while also providing services that strengthen the business community. However, since the high-tech concept is standard in the OECD, we will also use this term in this report. A high proportion of employment in the high-tech sector is considered to be an important competitive parameter to achieve the EU 2020 targets.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

17Øresund Trends 2012

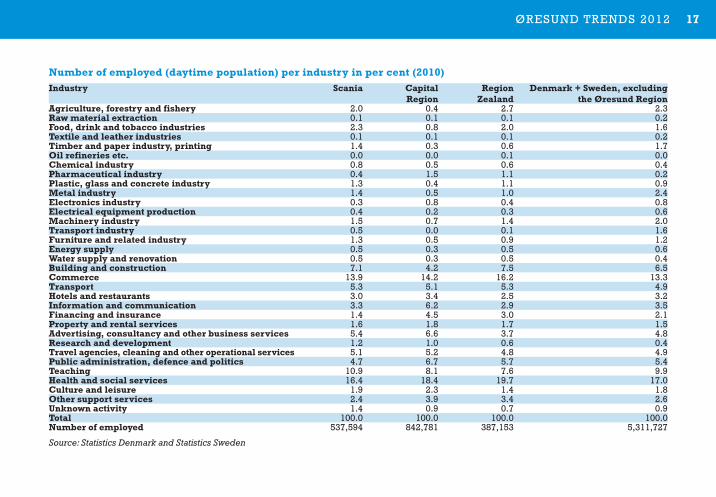

number of employed (daytime population) per industry in per cent (2010)industry Scania Capital

RegionRegion

ZealandDenmark + Sweden, excluding

the Øresund RegionAgriculture, forestry and fishery 2.0 0.4 2.7 2.3Raw material extraction 0.1 0.1 0.1 0.2Food, drink and tobacco industries 2.3 0.8 2.0 1.6Textile and leather industries 0.1 0.1 0.1 0.2Timber and paper industry, printing 1.4 0.3 0.6 1.7oil refineries etc . 0.0 0.0 0.1 0.0Chemical industry 0.8 0.5 0.6 0.4Pharmaceutical industry 0.4 1.5 1.1 0.2Plastic, glass and concrete industry 1.3 0.4 1.1 0.9Metal industry 1.4 0.5 1.0 2.4Electronics industry 0.3 0.8 0.4 0.8Electrical equipment production 0.4 0.2 0.3 0.6Machinery industry 1.5 0.7 1.4 2.0Transport industry 0.5 0.0 0.1 1.6Furniture and related industry 1.3 0.5 0.9 1.2Energy supply 0.5 0.3 0.5 0.6Water supply and renovation 0.5 0.3 0.5 0.4Building and construction 7.1 4.2 7.5 6.5Commerce 13.9 14.2 16.2 13.3Transport 5.3 5.1 5.3 4.9hotels and restaurants 3.0 3.4 2.5 3.2information and communication 3.3 6.2 2.9 3.5Financing and insurance 1.4 4.5 3.0 2.1Property and rental services 1.6 1.8 1.7 1.5Advertising, consultancy and other business services 5.4 6.6 3.7 4.8Research and development 1.2 1.0 0.6 0.4Travel agencies, cleaning and other operational services 5.1 5.2 4.8 4.9Public administration, defence and politics 4.7 6.7 5.7 5.4Teaching 10.9 8.1 7.6 9.9health and social services 16.4 18.4 19.7 17.0Culture and leisure 1.9 2.3 1.4 1.8other support services 2.4 3.9 3.4 2.6Unknown activity 1.4 0.9 0.7 0.9Total 100.0 100.0 100.0 100.0number of employed 537,594 842,781 387,153 5,311,727

Source: Statistics Denmark and Statistics Sweden

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

18 Øresund Trends 2012

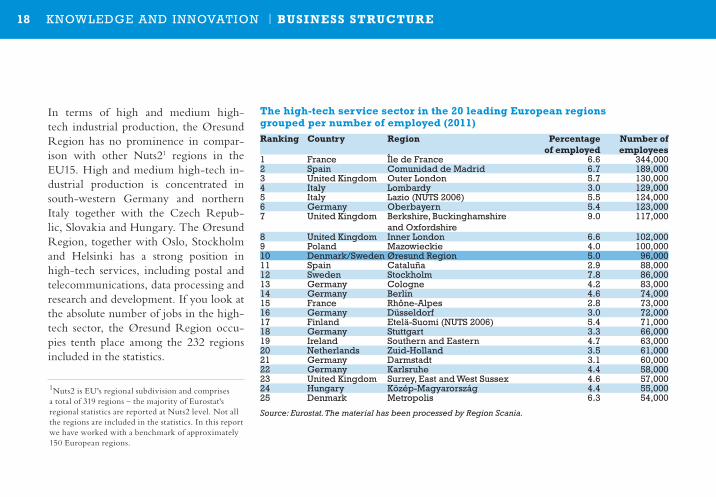

1Nuts2 is EU's regional subdivision and comprises a total of 319 regions – the majority of Eurostat's regional statistics are reported at Nuts2 level. Not all the regions are included in the statistics. In this report we have worked with a benchmark of approximately 150 European regions.

In terms of high and medium high-tech industrial production, the Øresund Region has no prominence in compar-ison with other Nuts21 regions in the EU15. High and medium high-tech in-dustrial production is concentrated in south-western Germany and northern Italy together with the Czech Repub-lic, Slovakia and Hungary. The Øresund Region, together with Oslo, Stockholm and Helsinki has a strong position in high-tech services, including postal and telecommunications, data processing and research and development. If you look at the absolute number of jobs in the high-tech sector, the Øresund Region occu-pies tenth place among the 232 regions included in the statistics.

The high-tech service sector in the 20 leading European regions grouped per number of employed (2011)Ranking Country Region Percentage

of employednumber of employees

1 France Île de France 6.6 344,0002 spain Comunidad de Madrid 6.7 189,0003 united Kingdom outer london 5.7 130,0004 Italy lombardy 3.0 129,0005 Italy lazio (nuts 2006) 5.5 124,0006 Germany oberbayern 5.4 123,0007 united Kingdom Berkshire, Buckinghamshire

and oxfordshire9.0 117,000

8 united Kingdom Inner london 6.6 102,0009 Poland Mazowieckie 4.0 100,00010 Denmark/sweden Øresund Region 5.0 96,00011 spain Cataluña 2.9 88,00012 sweden stockholm 7.8 86,00013 Germany Cologne 4.2 83,00014 Germany Berlin 4.6 74,00015 France Rhône-Alpes 2.8 73,00016 Germany Düsseldorf 3.0 72,00017 Finland Etelä-suomi (nuts 2006) 5.4 71,00018 Germany stuttgart 3.3 66,00019 Ireland southern and Eastern 4.7 63,00020 netherlands Zuid-Holland 3.5 61,00021 Germany Darmstadt 3.1 60,00022 Germany Karlsruhe 4.4 58,00023 united Kingdom surrey, East and West sussex 4.6 57,00024 Hungary Közép-Magyarország 4.4 55,00025 Denmark Metropolis 6.3 54,000

Source: Eurostat. The material has been processed by Region Scania.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

19Øresund Trends 2012

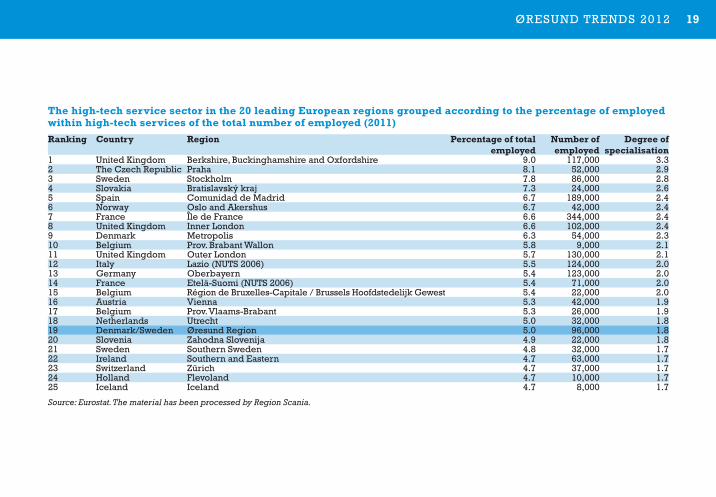

The high-tech service sector in the 20 leading European regions grouped according to the percentage of employed within high-tech services of the total number of employed (2011)Ranking Country Region Percentage of total

employednumber of employed

Degree of specialisation

1 united Kingdom Berkshire, Buckinghamshire and oxfordshire 9.0 117,000 3.32 the Czech Republic Praha 8.1 52,000 2.93 sweden stockholm 7.8 86,000 2.84 slovakia Bratislavský kraj 7.3 24,000 2.65 spain Comunidad de Madrid 6.7 189,000 2.46 norway oslo and Akershus 6.7 42,000 2.47 France Île de France 6.6 344,000 2.48 united Kingdom Inner london 6.6 102,000 2.49 Denmark Metropolis 6.3 54,000 2.310 Belgium Prov. Brabant Wallon 5.8 9,000 2.111 united Kingdom outer london 5.7 130,000 2.112 Italy lazio (nuts 2006) 5.5 124,000 2.013 Germany oberbayern 5.4 123,000 2.014 France Etelä-suomi (nuts 2006) 5.4 71,000 2.015 Belgium Région de Bruxelles-Capitale / Brussels Hoofdstedelijk Gewest 5.4 22,000 2.016 Austria vienna 5.3 42,000 1.917 Belgium Prov. vlaams-Brabant 5.3 26,000 1.918 netherlands utrecht 5.0 32,000 1.819 Denmark/sweden Øresund Region 5.0 96,000 1.820 slovenia Zahodna slovenija 4.9 22,000 1.821 sweden southern sweden 4.8 32,000 1.722 Ireland southern and Eastern 4.7 63,000 1.723 switzerland Zürich 4.7 37,000 1.724 Holland Flevoland 4.7 10,000 1.725 Iceland Iceland 4.7 8,000 1.7

Source: Eurostat. The material has been processed by Region Scania.

The high-tech service sector in the 20 leading European regions grouped per number of employed (2011)Ranking Country Region Percentage

of employednumber of employees

1 France Île de France 6.6 344,0002 spain Comunidad de Madrid 6.7 189,0003 united Kingdom outer london 5.7 130,0004 Italy lombardy 3.0 129,0005 Italy lazio (nuts 2006) 5.5 124,0006 Germany oberbayern 5.4 123,0007 united Kingdom Berkshire, Buckinghamshire

and oxfordshire9.0 117,000

8 united Kingdom Inner london 6.6 102,0009 Poland Mazowieckie 4.0 100,00010 Denmark/sweden Øresund Region 5.0 96,00011 spain Cataluña 2.9 88,00012 sweden stockholm 7.8 86,00013 Germany Cologne 4.2 83,00014 Germany Berlin 4.6 74,00015 France Rhône-Alpes 2.8 73,00016 Germany Düsseldorf 3.0 72,00017 Finland Etelä-suomi (nuts 2006) 5.4 71,00018 Germany stuttgart 3.3 66,00019 Ireland southern and Eastern 4.7 63,00020 netherlands Zuid-Holland 3.5 61,00021 Germany Darmstadt 3.1 60,00022 Germany Karlsruhe 4.4 58,00023 united Kingdom surrey, East and West sussex 4.6 57,00024 Hungary Közép-Magyarország 4.4 55,00025 Denmark Metropolis 6.3 54,000

Source: Eurostat. The material has been processed by Region Scania.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

20 Øresund Trends 2012

2FA: Functional labour market region

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

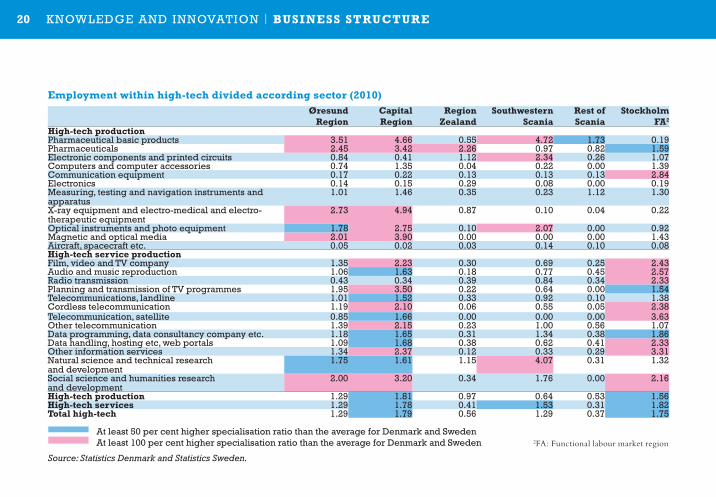

Employment within high-tech divided according sector (2010)Øresund

RegionCapital Region

Region Zealand

Southwestern Scania

Rest of Scania

Stockholm FA2

high-tech productionPharmaceutical basic products 3.51 4.66 0.55 4.72 1.73 0.19Pharmaceuticals 2.45 3.42 2.26 0.97 0.82 1.59Electronic components and printed circuits 0.84 0.41 1.12 2.34 0.26 1.07Computers and computer accessories 0.74 1.35 0.04 0.22 0.00 1.39Communication equipment 0.17 0.22 0.13 0.13 0.13 2.84Electronics 0.14 0.15 0.29 0.08 0.00 0.19Measuring, testing and navigation instruments and apparatus

1.01 1.46 0.35 0.23 1.12 1.30

X-ray equipment and electro-medical and electro-therapeutic equipment

2.73 4.94 0.87 0.10 0.04 0.22

optical instruments and photo equipment 1.78 2.75 0.10 2.07 0.00 0.92Magnetic and optical media 2.01 3.90 0.00 0.00 0.00 1.43Aircraft, spacecraft etc. 0.05 0.02 0.03 0.14 0.10 0.08high-tech service productionFilm, video and tv company 1.35 2.23 0.30 0.69 0.25 2.43Audio and music reproduction 1.06 1.63 0.18 0.77 0.45 2.57Radio transmission 0.43 0.34 0.39 0.84 0.34 2.33Planning and transmission of tv programmes 1.95 3.50 0.22 0.64 0.00 1.54telecommunications, landline 1.01 1.52 0.33 0.92 0.10 1.38Cordless telecommunication 1.19 2.10 0.06 0.55 0.05 2.38telecommunication, satellite 0.85 1.66 0.00 0.00 0.00 3.63other telecommunication 1.39 2.15 0.23 1.00 0.56 1.07Data programming, data consultancy company etc. 1.18 1.65 0.31 1.34 0.38 1.86Data handling, hosting etc, web portals 1.09 1.68 0.38 0.62 0.41 2.33other information services 1.34 2.37 0.12 0.33 0.29 3.31natural science and technical research and development

1.75 1.61 1.15 4.07 0.31 1.32

social science and humanities research and development

2.00 3.20 0.34 1.76 0.00 2.16

high-tech production 1.29 1.81 0.97 0.64 0.53 1.56high-tech services 1.29 1.78 0.41 1.53 0.31 1.82Total high-tech 1.29 1.79 0.56 1.29 0.37 1.75

At least 50 per cent higher specialisation ratio than the average for Denmark and sweden At least 100 per cent higher specialisation ratio than the average for Denmark and sweden

Source: Statistics Denmark and Statistics Sweden.

21Øresund Trends 2012

“Specialisation ratio” measures the share of employment in the high-tech sector in a region divided by the average em-ployment share in all regions.

Berkshire, Buckinghamshire and Ox-fordshire are the regions with the high-est proportion employed in high-tech services (9 per cent of total employ-ment), which gives a specialisation ratio of 3.3. Stockholm occupies third place with 7.8 per cent of employment and a specialisation ratio of 2.9. The Capital Region is in ninth place with 6.3 per cent of employment in high-tech serv- ices and a specialisation ratio of 2.3, while the Øresund Region is in nine-teenth place with 5 per cent employed in high-tech services, which corresponds to a specialisation ratio of 1.8.

The high-tech sectors in Denmark and Sweden

From a Danish-Swedish perspective, the Øresund Region's high-tech profile is not as strong as it is from a European perspective. By calculating a regional specialisation index for the high-tech sector, where 1 is equal to the average for Denmark and Sweden combined, it becomes possible to describe the tech-nological profile for each region. The Stockholm Region has a high-tech spe-cialisation index of some 60 per cent above the average for Denmark and Sweden. By comparison, the Øresund Region has a specialisation index of only 29 per cent of the Danish-Swedish average. Within the Øresund Region, the Capital Region has the highest spe-cialisation ratio with 57 per cent above the Danish-Swedish average, while southwestern Scania has 51 per cent.

Stockholm has a significantly higher

specialisation ratio within high-tech than the Øresund Region. If you look at industries in the high-tech sector indi-vidually, the picture changes somewhat. For example, the Øresund Region has a competitive position in pharmaceutical production compared to Stockholm.

Within the Øresund Region, Scania specialises not only in manufacturing, but also in natural science and technical research and development; for example, there are several research and develop-ment-intensive enterprises in both bio-technology and telecommunications.

The Capital Region occupies a prom-inent position, primarily in the phar-maceutical industry, other advanced technological production and other data related industries.

Region Zealand specialises particularly in medical technology. Of all employ-

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

22 Øresund Trends 2012

Jobs according to sector in percentage (2010)Øresund

RegionØresund

Region DKØresund

Region SEDenmark Sweden Denmark

and SwedenAgriculture, hunting, forestry and fishery 6.6 5.4 9.0 11.3 9.4 8.9Raw material extraction 0.1 0.1 0.1 0.1 0.1 0.1Manufacturing companies 5.0 4.5 6.1 5.5 6.4 5.7Electricity, gas and district heating 0.2 0.2 0.2 0.3 0.2 0.2Water supply, sewerage, waste handling and purifica-tion of soil and groundwater

0.3 0.4 0.3 0.4 0.3 0.3

Building and construction companies 10.2 9.8 10.9 9.3 11.5 10.5Wholesale and retail trading, repair of motor vehicles and motorcycles

17.9 18.0 17.6 18.1 15.8 17.1

Transport and freight handling 4.3 4.2 4.6 4.2 4.6 4.4overnight facilities and catering 4.5 4.6 4.1 4.4 4.1 4.3information and communication 5.3 6.2 3.7 4.3 4.3 4.6Banking and finance, insurance 1.4 1.6 1.0 1.6 1.1 1.3Property 4.3 4.8 3.3 5.3 3.0 4.0Liberal, scientific and technical services 13.2 13.2 13.2 10.1 13.2 12.4Administrative services and helplines 4.8 5.4 3.6 4.7 3.6 4.3Public administration and defence; social security 0.6 0.6 0.7 0.6 0.7 0.7Teaching 3.2 2.7 4.0 2.7 4.1 3.4health service and social services 8.6 10.2 5.5 9.5 5.7 7.6Culture, entertainment and sport 3.1 2.6 4.1 2.3 4.2 3.3other services 6.1 5.3 7.6 5.3 7.1 6.3Private households with homehelps; household produ-ction of goods and services for own use

0.1 0.1 0.0 0.1 0.0 0.0

Extra territorial organisations and bodies 0.0 0.0 0.0 0.0 0.0 0.0Unknown 0.3 0.2 0.6 0.2 0.5 0.4Percentage total 100.0 100.0 100.0 100.0 100.0 100.0Total number 208,009 138,116 69,893 305,565 527,427 1,249,010

Source: Ørestat.Note: Only businesses that account for the main revenue source for the owner or others are included. Ancillary companies with no employees are thus not included.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

23Øresund Trends 2012

ees in the pharmaceutical industry in Denmark and Sweden, 62 per cent were found in the Øresund Region in 2010.

It should be remembered, however, that the above information is from 2010. Since then there has been a major re-structuring of the telecommunications and medical technology industries in the Øresund Region: Nokia in Copen-hagen and AstraZeneca in Lund have closed while Sony has announced cuts.

The Øresund Region had well over 44,000 employees (2010) in technical research and high-tech manufacturing – which accounts for 35 per cent of Den-mark's and Sweden's total employment in this sector – and is the largest know-ledge centre, followed by Stockholm FA in second place with 32,800 people em-

ployed within this sector. It is important, however, to remember that the Øresund Region cannot yet be described as an economically homogeneous region in the same way as other metropolitan regions like Stockholm, for example. In the longer term, increased integra-tion between business in Zealand and in Scania will be encouraged through scale effects3, which can also help to strength-en the Øresund Region's position in terms of competition and in cooperation

with other metropolitan regions across the rest of Scandinavia and Europe.

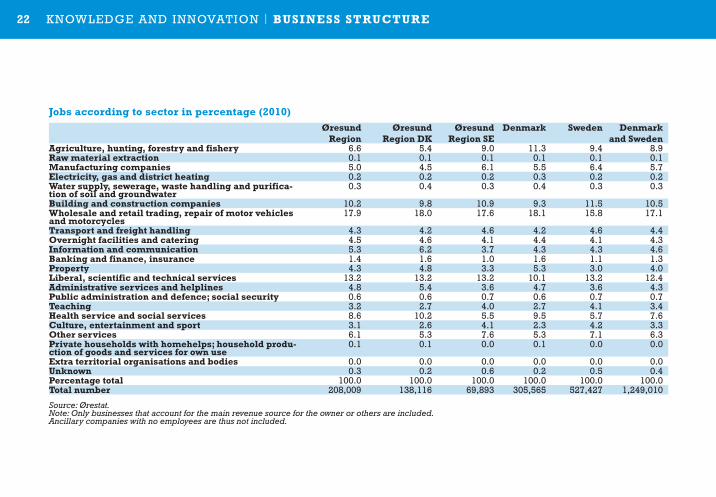

Jobs in the Øresund Region

In 2010, a total of 208,000 jobs were in the Øresund Region, of which 78 per cent were in the service sector, which in turn was 4 percentage points higher than the average for Denmark and Swe-den.

The highest proportion of jobs was

Jobs according to the number of employees (2010)number of employees

Øresund Region

Øresund Region DK

Øresund Region SE

Denmark Sweden

1 52.9 51.9 55.0 49.2 52.72–4 22.0 22.4 21.2 23.3 21.85–9 10.9 11.2 10.3 12.1 11.110–19 7.1 7.3 6.7 7.9 7.220–49 4.5 4.6 4.4 4.9 4.650–99 1.5 1.5 1.6 1.6 1.6100+ 1.1 1.1 0.9 1.0 1.0Percentage total 100.0 100.0 100.0 100.0 100.0Total number 208,552 138,659 69,893 306,837 527,427

Source: Ørestat. Note: Only businesses that account for the main revenue source for the owner or others are included. Ancillary companies with no employees are thus not included.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

3Scale effect or economy of scale effects: large regions tend to have higher growth and to be more innovative than small regions.

24 Øresund Trends 2012

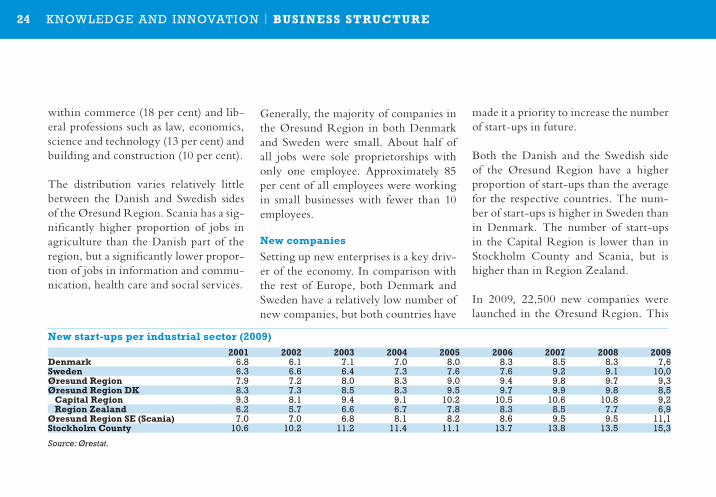

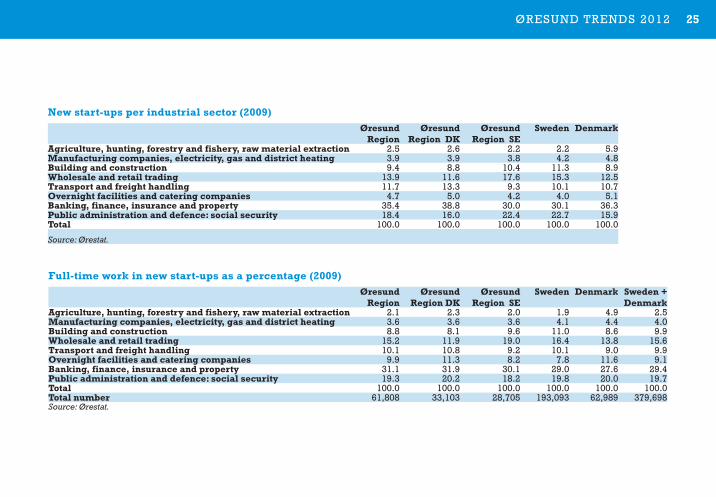

made it a priority to increase the number of start-ups in future.

Both the Danish and the Swedish side of the Øresund Region have a higher proportion of start-ups than the average for the respective countries. The num-ber of start-ups is higher in Sweden than in Denmark. The number of start-ups in the Capital Region is lower than in Stockholm County and Scania, but is higher than in Region Zealand.

In 2009, 22,500 new companies were launched in the Øresund Region. This

within commerce (18 per cent) and lib-eral professions such as law, economics, science and technology (13 per cent) and building and construction (10 per cent).

The distribution varies relatively little between the Danish and Swedish sides of the Øresund Region. Scania has a sig-nificantly higher proportion of jobs in agriculture than the Danish part of the region, but a significantly lower propor-tion of jobs in information and commu-nication, health care and social services.

Generally, the majority of companies in the Øresund Region in both Denmark and Sweden were small. About half of all jobs were sole proprietorships with only one employee. Approximately 85 per cent of all employees were working in small businesses with fewer than 10 employees.

new companies

Setting up new enterprises is a key driv-er of the economy. In comparison with the rest of Europe, both Denmark and Sweden have a relatively low number of new companies, but both countries have

new start-ups per industrial sector (2009)2001 2002 2003 2004 2005 2006 2007 2008 2009

Denmark 6.8 6.1 7.1 7.0 8.0 8.3 8.5 8.3 7,6Sweden 6.3 6.6 6.4 7.3 7.6 7.6 9.2 9.1 10,0Øresund Region 7.9 7.2 8.0 8.3 9.0 9.4 9.8 9.7 9,3Øresund Region DK 8.3 7.3 8.5 8.3 9.5 9.7 9.9 9.8 8,5 Capital Region 9.3 8.1 9.4 9.1 10.2 10.5 10.6 10.8 9,2 Region Zealand 6.2 5.7 6.6 6.7 7.8 8.3 8.5 7.7 6,9Øresund Region SE (Scania) 7.0 7.0 6.8 8.1 8.2 8.6 9.5 9.5 11,1Stockholm County 10.6 10.2 11.2 11.4 11.1 13.7 13.8 13.5 15,3

Source: Ørestat.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

25Øresund Trends 2012KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

Full-time work in new start-ups as a percentage (2009)Øresund

Region Øresund

Region DKØresund

Region SESweden Denmark Sweden +

DenmarkAgriculture, hunting, forestry and fishery, raw material extraction 2.1 2.3 2.0 1.9 4.9 2.5Manufacturing companies, electricity, gas and district heating 3.6 3.6 3.6 4.1 4.4 4.0Building and construction 8.8 8.1 9.6 11.0 8.6 9.9Wholesale and retail trading 15.2 11.9 19.0 16.4 13.8 15.6Transport and freight handling 10.1 10.8 9.2 10.1 9.0 9.9overnight facilities and catering companies 9.9 11.3 8.2 7.8 11.6 9.1Banking, finance, insurance and property 31.1 31.9 30.1 29.0 27.6 29.4Public administration and defence: social security 19.3 20.2 18.2 19.8 20.0 19.7Total 100.0 100.0 100.0 100.0 100.0 100.0Total number 61,808 33,103 28,705 193,093 62,989 379,698Source: Ørestat.

new start-ups per industrial sector (2009)Øresund

Region Øresund

Region DKØresund

Region SESweden Denmark

Agriculture, hunting, forestry and fishery, raw material extraction 2.5 2.6 2.2 2.2 5.9Manufacturing companies, electricity, gas and district heating 3.9 3.9 3.8 4.2 4.8Building and construction 9.4 8.8 10.4 11.3 8.9Wholesale and retail trading 13.9 11.6 17.6 15.3 12.5Transport and freight handling 11.7 13.3 9.3 10.1 10.7overnight facilities and catering companies 4.7 5.0 4.2 4.0 5.1Banking, finance, insurance and property 35.4 38.8 30.0 30.1 36.3Public administration and defence: social security 18.4 16.0 22.4 22.7 15.9Total 100.0 100.0 100.0 100.0 100.0

Source: Ørestat.

26 Øresund Trends 2012

figure represents 26 per cent of all new businesses in Denmark and Sweden. 61 per cent of the new businesses were established on the Danish side of the Øresund.

The majority of new companies in the Øresund Region were set up in the financial and business services sectors (35 per cent), commerce (14 per cent), build-ing and construction (9 per cent) and hotels and restaurants (5 per cent). The industry breakdown of start-ups in Sca-nia roughly corresponds to the distribu-tion in Sweden as a whole, but with some over-representation in terms of wholesale and retail businesses. The Danish part of the Øresund Region differs primarily from Denmark as a whole in that it has a larger share in the financial sector and business services together with a smaller share of start-up companies in the whole-sale and retail trade. Industry structural differences are greater between the Dan-

ish and the Swedish parts of the Øresund Region than they are in proportion to the respective countries as a whole.

In 2009, 31 per cent of man years in the Øresund Region's new businesses were established in the financial sector and business services. This was followed by commerce (15 per cent) and transport and communications (10 per cent). This pattern is consistent regardless of geog-raphy.

KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

27Øresund Trends 2012KnoWlEDGE AnD InnovAtIon | BUSinESS STRUCTURE

28 Øresund Trends 2012

RESEARCh AnD DEvELoPMEnT

The first phase of the innovation process is usually founded upon research and development (R&D). The knowledge base that underlies high tech and quali-tative products, goods and services arises from this.

However, it is far from certain wheth-er the results of R&D are always com-mercialised in the same region in which the research takes place. This can affect economic growth1.

The regional return on R&D invest-ment depends on several factors, such as conducting R&D projects in rela-

tion to other economic activities in the value chain: R&D activity focus (basic research, applied research or experi-mental development), the regional mar-ket size and access to capital. The time factor also plays an important role in the innovation process, which can frequent-ly have a time frame of several decades. A specialised R&D sector of appropriate size and quality is the first step towards financial success in the modern knowl-edge economy.

In this context, the Øresund Region occupies a prominent place at the Nor-dic and European level (see page 16 on business structure). This is also reflected in access to capital – especially foreign capital – to finance R&D. In addition,

the Nordic countries are generally char-acterised by a good business climate2.

R&D investments

Investment in R&D is a key objective of regional capacity and willingness to optimise the knowledge base. It does not, however, necessarily mean that all investments in R&D are transformed into commercial products. The EU2020 plan, which aims to make the EU the world's most competitive knowledge economy, uses R&D investments as one of 14 indicators to measure progress. The goal is an investment level of at least 3 per cent of GDP.

The Nordic countries – apart from Nor-way and Iceland – are world leaders in

1This is supported by empirical studies. Further evidence to support it is demonstrated in a 2006 study, which included Nuts2 regions that compared R&D intensity and number of patents on the one hand against economic development (measured in GDP per capita) on the other. The study showed that the region that invested the most in R&D – Braunschweig in Germany – was simultaneously the fourth weakest region in terms of economic growth. Conversely, none of the league's top 10 growth regions has an R&D intensity of more than 2 per cent (Hanell, T & Neubauer, J: Geographies of Knowledge Production in Europe. Nordregio WP 2006: 3).

2Forbes Best Countries for Business 2011. The Nordic countries' position in the world (in parentheses): Denmark (5), Sweden (7), Norway (8), Finland (13) and Iceland (23).

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

29Øresund Trends 2012

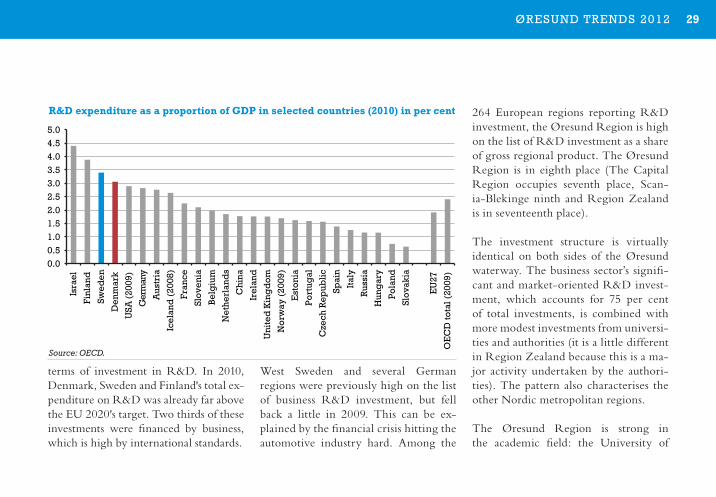

terms of investment in R&D. In 2010, Denmark, Sweden and Finland's total ex-penditure on R&D was already far above the EU 2020's target. Two thirds of these investments were financed by business, which is high by international standards.

West Sweden and several German regions were previously high on the list of business R&D investment, but fell back a little in 2009. This can be ex-plained by the financial crisis hitting the automotive industry hard. Among the

264 European regions reporting R&D investment, the Øresund Region is high on the list of R&D investment as a share of gross regional product. The Øresund Region is in eighth place (The Capital Region occupies seventh place, Scan-ia-Blekinge ninth and Region Zealand is in seventeenth place).

The investment structure is virtually identical on both sides of the Øresund waterway. The business sector’s signifi-cant and market-oriented R&D invest-ment, which accounts for 75 per cent of total investments, is combined with more modest investments from universi-ties and authorities (it is a little different in Region Zealand because this is a ma-jor activity undertaken by the authori-ties). The pattern also characterises the other Nordic metropolitan regions.

The Øresund Region is strong in the academic field: the University of

90

95

100

105

110

115

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Index: 2000=100

EU27 BRP

Öresundsregionen BRP

EU27 BRP/sysselsatt

Öresundsregionen BRP/sysselsatt

90

95

100

105

110

115

120

125

130

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Öresund DK

Region Sjælland

Region Hovedstaden

Skåne

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Isra

el

Finl

and

Swed

en

Den

mar

k

USA

(20

09)

Ger

man

y

Aus

tria

Icel

and

(20

08)

Fran

ce

Slov

enia

Belg

ium

Net

herl

and

s

Chi

na

Irel

and

Uni

ted

Kin

gd

om

Nor

way

(20

09)

Est

onia

Port

ugal

Cze

ch R

epub

lic

Spai

n

Ital

y

Rus

sia

Hun

gar

y

Pola

nd

Slov

akia

EU

27

OE

CD

tota

l (20

09)

R&D expenditure as a proportion of GDP in selected countries (2010) in per cent

Source: OECD.

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

30 Øresund Trends 2012

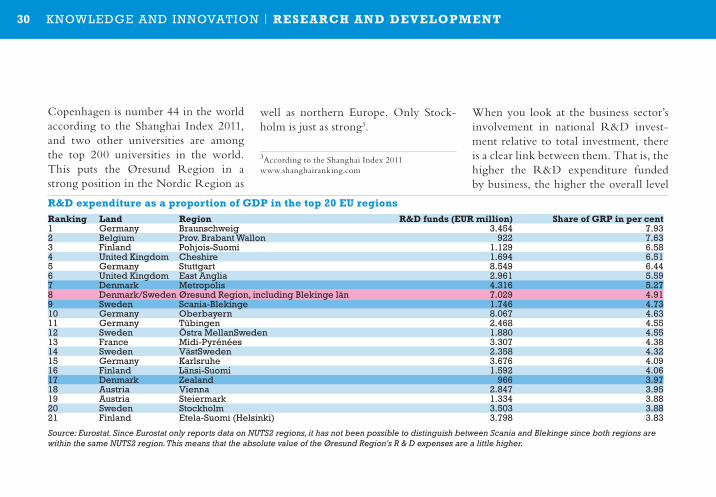

Copenhagen is number 44 in the world according to the Shanghai Index 2011, and two other universities are among the top 200 universities in the world. This puts the Øresund Region in a strong position in the Nordic Region as

well as northern Europe. Only Stock-holm is just as strong3.

When you look at the business sector’s involvement in national R&D invest-ment relative to total investment, there is a clear link between them. That is, the higher the R&D expenditure funded by business, the higher the overall level

3According to the Shanghai Index 2011www.shanghairanking.com

R&D expenditure as a proportion of GDP in the top 20 EU regionsRanking Land Region R&D funds (EUR million) Share of GRP in per cent1 Germany Braunschweig 3.454 7.932 Belgium Prov. Brabant Wallon 922 7.633 Finland Pohjois-suomi 1.129 6.584 united Kingdom Cheshire 1.694 6.515 Germany stuttgart 8.549 6.446 united Kingdom East Anglia 2.961 5.597 Denmark Metropolis 4.316 5.278 Denmark/sweden Øresund Region, including Blekinge län 7.029 4.919 sweden scania-Blekinge 1.746 4.7310 Germany oberbayern 8.067 4.6311 Germany tübingen 2.468 4.5512 sweden Östra Mellansweden 1.880 4.5513 France Midi-Pyrénées 3.307 4.3814 sweden västsweden 2.358 4.3215 Germany Karlsruhe 3.676 4.0916 Finland länsi-suomi 1.592 4.0617 Denmark Zealand 966 3.9718 Austria vienna 2.847 3.9519 Austria steiermark 1.334 3.8820 sweden stockholm 3.503 3.8821 Finland Etela-suomi (Helsinki) 3.798 3.83

Source: Eurostat. Since Eurostat only reports data on NUTS2 regions, it has not been possible to distinguish between Scania and Blekinge since both regions are within the same NUTS2 region. This means that the absolute value of the Øresund Region's R & D expenses are a little higher.

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

31Øresund Trends 2012

of investment in the country4. This re-lationship is apparent for most Nordic regions.

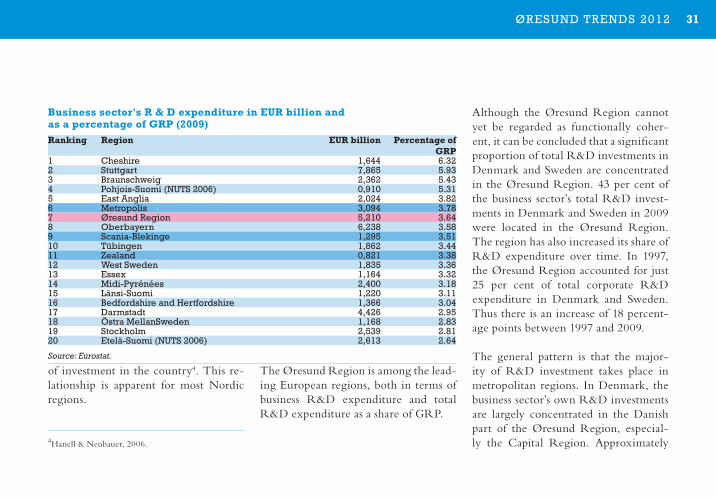

The Øresund Region is among the lead-ing European regions, both in terms of business R&D expenditure and total R&D expenditure as a share of GRP.

Although the Øresund Region cannot yet be regarded as functionally coher-ent, it can be concluded that a significant proportion of total R&D investments in Denmark and Sweden are concentrated in the Øresund Region. 43 per cent of the business sector’s total R&D invest-ments in Denmark and Sweden in 2009 were located in the Øresund Region. The region has also increased its share of R&D expenditure over time. In 1997, the Øresund Region accounted for just 25 per cent of total corporate R&D expenditure in Denmark and Sweden. Thus there is an increase of 18 percent-age points between 1997 and 2009.

The general pattern is that the major-ity of R&D investment takes place in metropolitan regions. In Denmark, the business sector’s own R&D investments are largely concentrated in the Danish part of the Øresund Region, especial-ly the Capital Region. Approximately

Business sector's R & D expenditure in EUR billion and as a percentage of GRP (2009)Ranking Region EUR billion Percentage of

GRP1 Cheshire 1,644 6.322 stuttgart 7,865 5.933 Braunschweig 2,362 5.434 Pohjois-suomi (nuts 2006) 0,910 5.315 East Anglia 2,024 3.826 Metropolis 3,094 3.787 Øresund Region 5,210 3.648 oberbayern 6,238 3.589 scania-Blekinge 1,295 3.5110 tübingen 1,862 3.4411 Zealand 0,821 3.3812 West sweden 1,835 3.3613 Essex 1,164 3.3214 Midi-Pyrénées 2,400 3.1815 länsi-suomi 1,220 3.1116 Bedfordshire and Hertfordshire 1,366 3.0417 Darmstadt 4,426 2.9518 Östra Mellansweden 1,168 2.8319 stockholm 2,539 2.8120 Etelä-suomi (nuts 2006) 2,613 2.64

Source: Eurostat.

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

4Hanell & Neubauer, 2006.

32 Øresund Trends 2012

84 per cent of Danish business R&D investment takes place in the Danish part of the Øresund Region: the Capital Region accounts for the majority, 66 per cent, and Region Zealand for 18 per cent.

In Sweden, the greater part of business R&D investment is also in the Capital Region, but Stockholm's role is not as dominant in Sweden as Copenhagen is in Denmark. Approximately 34 per cent of business R&D investments are made in Stockholm County, followed by 25 per cent in the Västra Götaland Region and 17 per cent in Scania and Blekinge (figures from 2009).

If we measure business R&D expend-iture as a share of GRP, the Øresund Region is also high. The Capital Region has the highest with 3.78 per cent, fol-lowed by Scania-Blekinge and Region Zealand with 3.51 per cent and 3.38 per

cent, respectively. The proportion for the total Øresund Region amounts to 3.64 per cent.

When comparing investments inter-nationally in nominal terms, it is not obvious that the same sums can finance an equal amount of R&D in different countries and regions. It depends, of course, on the different structures in terms of business, research and costs.

Another part of the explanation is the wage gap between countries and re-gions as well as between sectors. Differ- ences in purchasing power are usually adjusted to different price indices. This is not possible for R&D. As with so many other services, R&D is personnel heavy, and so the majority of R&D ex-penditure goes in salaries5.

Around two-thirds of R&D expend-iture is accounted for by salaries in the

Øresund Region. Although it is not currently possible to analyse the conse-quences in detail, it is reasonable to as-sume that investment in R&D on the Danish side probably has a lower pur-chasing power and thus finances a smaller amount of R&D than is the case in Swe-den. This becomes more important when comparing regions in western and east-ern Europe. The difference in purchas-ing power can influence the investment patterns in R&D in Europe significantly in the longer term; this is because lower costs outside western Europe may attract a much larger share of R&D investment in the future.

5Denmark and Sweden have no statistics on R&D investments, but in Germany, R&D studies include questions of this nature. The German studies show that in most industries, around two thirds of R&D ex-penditure goes to fund salaries, especially in dedicated R&D environments (Stifterverband für die Deutsche Wissenschaft: FuF-Datenreport 2007. Tabellen und Daten, s. 38 Tabelle 14).

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

33Øresund Trends 2012

Since 2000, wage costs in Denmark have increased by 35 per cent, while Sweden has experienced a growth of 18 per cent. In comparison, labour costs in Germany rose by just 6 per cent over the same pe-riod. In other words, it has become rela-tively expensive to conduct R&D in the Øresund Region and in the Danish part in particular.

innovative capacity

The ability to translate research, know-ledge and ideas into new commercial products and processes is essential to increasing a region's global competitive-ness. Innovative capacity is difficult to measure, in part because the concept is difficult to define, in part because there is a lack of standardised data at regional level.

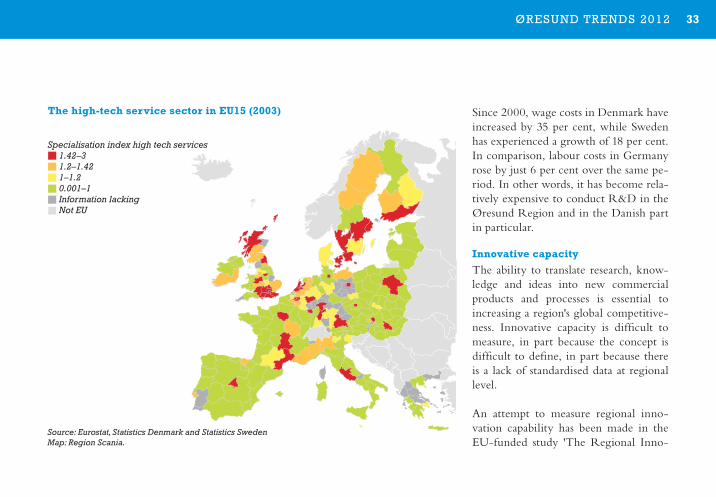

An attempt to measure regional inno-vation capability has been made in the EU-funded study 'The Regional Inno-

Source: Eurostat, Statistics Denmark and Statistics SwedenMap: Region Scania.

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

The high-tech service sector in EU15 (2003)

Specialisation index high tech services1.42–3 1.2–1.42 1–1.2 0.001–1 Information lackingNot EU

34 Øresund Trends 2012

vation Scoreboard'. According to the study, regions in Denmark and Sweden are among the most innovative regions in Europe. The study is based on a weighted index of 17 different indicators, which are divided into three main groups: innova-tion promoting background factors (pub-lic R&D expenditure, higher education, access to broadband, etc.) innovation activities in enterprises (R&D expendi-ture, patents, etc.) and performance fac-tors (employees in high-tech companies, sales of new products, new innovation companies, etc.). The latest survey from December 2009 contains data from 2006.

Unfortunately, the statistics in Den-mark are at national level, not regional. Denmark as a whole is considered to be among the regions with the highest capacity for innovation, while Scania is

in the next highest group, which includes much of the central and western regions (half of EEA6 countries' regions).

KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

6EEA countries consists of 27 EU member states plus Iceland, Norway and Liechtenstein.

35Øresund Trends 2012KnoWlEDGE AnD InnovAtIon | RESEARCh AnD DEvELoPMEnT

36 Øresund Trends 2012KnoWlEDGE AnD InnovAtIon | E D U C AT i o n

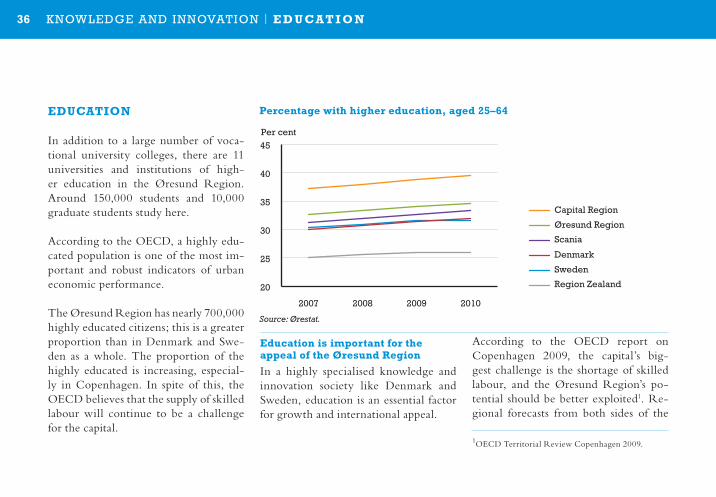

EDUCATion

In addition to a large number of voca-tional university colleges, there are 11 universities and institutions of high-er education in the Øresund Region. Around 150,000 students and 10,000 graduate students study here.

According to the OECD, a highly edu-cated population is one of the most im-portant and robust indicators of urban economic performance.

The Øresund Region has nearly 700,000 highly educated citizens; this is a greater proportion than in Denmark and Swe-den as a whole. The proportion of the highly educated is increasing, especial-ly in Copenhagen. In spite of this, the OECD believes that the supply of skilled labour will continue to be a challenge for the capital.

Education is important for the appeal of the Øresund Region

In a highly specialised knowledge and innovation society like Denmark and Sweden, education is an essential factor for growth and international appeal.

According to the OECD report on Copenhagen 2009, the capital’s big-gest challenge is the shortage of skilled labour, and the Øresund Region’s po-tential should be better exploited1. Re-gional forecasts from both sides of the

20

25

30

35

40

45

2007 2008 2009 2010

Per cent

Denmark

Capital Region

Region Zealand

Sweden

Scania

Øresund Region

0

500

1,000

1,500

2,000

2,500

1999/2000

2000/2001

2001/2002

2002/2003

2003/2004

2004/2005

2005/2006

2006/2007

2007/2008

2008/2009

2009/2010

2010/2011

Swedish students in Denmark

Danish students in Sweden

Percentage with higher education, aged 25–64

Source: Ørestat.

1OECD Territorial Review Copenhagen 2009.

37Øresund Trends 2012

sound also show a growing need for highly educated labour2. Education is a major factor in the individual’s hold on the labour market because people with low or no education are at a high risk of ending up outside it.

A highly educated population

690,500 (or 35 per cent) of the Øresund Region’s population of working age (25–64 years)3 have a higher education. With 35 per cent being highly educated, the Øresund Region has a greater share of the highly educated than Denmark and Swe-den have nationwide (32 per cent each). The Capital Region has the highest pro-portion of highly educated, followed by Scania and Region Zealand.

2Source: Region Scania (2012) Utbildnings- och ar-betsmarknadsprognos för Scania – med sikte på 2020; det tværregionale analysesamarbejde i Østdanmark (2012) Østdanmark 2010–2024 – fremskrivninger med Sam/K-Line.3 Source: Ørestat.

A growing proportion of highly educated youth

The education level among young people between the ages of 25–34 in the Øresund Region shows that more and more of the younger generation are taking up higher education. This trend is stronger in the Øresund Region than in Denmark and Sweden as a whole. Approximately 40 per cent of young people in the region now have a higher education, which is about 5 per cent more than the region’s popula-tion (up to 65) as a whole.

The highly educated are concentrated in cities

In the Øresund Region, the proportion of young people with a higher education is not developing at a uniform pace. The proportion of young people with a high-er education is growing in the Capital Region and in Scania, while it has de-clined slightly in Region Zealand.

Percentage of university graduates between the ages of 25 and 34

2007 2010Capital Region 40.3 41.9Region Zealand 24.9 24.1Scania 39.0 39.8

Source: Ørestat

In the Swedish part of the Øresund Region, over 40 per cent are highly ed-ucated in Lund, while the proportion among municipalities in the northern part of Scania is less than 25 per cent.

The tendency to concentrate in met-ropolitan areas and within commuting distance of them is a common pattern. Students and people with a higher ed-ucation move to the areas with the best education and job opportunities.

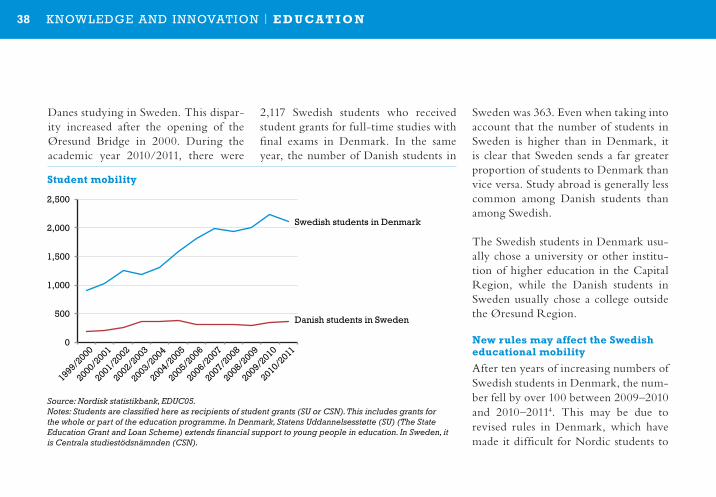

Swedish students are more mobile than Danish

There have always been many more Swedes going to Denmark to study than

KnoWlEDGE AnD InnovAtIon | E D U C AT i o n

38 Øresund Trends 2012

Danes studying in Sweden. This dispar-ity increased after the opening of the Øresund Bridge in 2000. During the academic year 2010/2011, there were 20

25

30

35

40

45

2007 2008 2009 2010

Per cent

Denmark

Capital Region

Region Zealand

Sweden

Scania

Øresund Region

0

500

1,000

1,500

2,000

2,500

1999/2000

2000/2001

2001/2002

2002/2003

2003/2004

2004/2005

2005/2006

2006/2007

2007/2008

2008/2009

2009/2010

2010/2011

Swedish students in Denmark

Danish students in Sweden

Student mobility

Source: Nordisk statistikbank, EDUC05.Notes: Students are classified here as recipients of student grants (SU or CSN). This includes grants for the whole or part of the education programme. In Denmark, Statens Uddannelsesstøtte (SU) (The State Education Grant and Loan Scheme) extends financial support to young people in education. In Sweden, it is Centrala studiestödsnämnden (CSN).

2,117 Swedish students who received student grants for full-time studies with final exams in Denmark. In the same year, the number of Danish students in

Sweden was 363. Even when taking into account that the number of students in Sweden is higher than in Denmark, it is clear that Sweden sends a far greater proportion of students to Denmark than vice versa. Study abroad is generally less common among Danish students than among Swedish.

The Swedish students in Denmark usu-ally chose a university or other institu-tion of higher education in the Capital Region, while the Danish students in Sweden usually chose a college outside the Øresund Region.

new rules may affect the Swedish educational mobility

After ten years of increasing numbers of Swedish students in Denmark, the num-ber fell by over 100 between 2009–2010 and 2010–20114. This may be due to revised rules in Denmark, which have made it difficult for Nordic students to

KnoWlEDGE AnD InnovAtIon | E D U C AT i o n

39Øresund Trends 2012

achieve high marks when their grades from their home country have to be val-idated in Denmark. This makes it more difficult to be admitted to the most pop-ular education programmes. At the same time, the requirement for tuition fees in 2011 was made more rigorous for single subjects in Denmark.

Mobility highest at university level5

The vast majority of those studying on the other side of the sound are studying at universities or other higher educa-tion institutions. 90 per cent of Swedish students in Denmark and 75 per cent of Danish students in Sweden studied at university or other higher education institutions in 2010–2011. This is partly due to the international grading scale of colleges and universities, ECTS (Euro-

pean Credit Transfer and Accumulation System), which makes it easy to com-pare grades and transfer credits between European college and university pro-grammes. It can be rather more difficult to validate grades between international commercial and secondary education.

Popular fields of study 2010/2011

Looking at the subjects that are popu-lar, medicine tops the list in Denmark as in previous studies among Swedes: 687 were enrolled in medical school in Denmark. This is followed by econom-ics (270) and veterinary studies (218). Training as an architect was also a very popular education among Swedes (130).

About a third of the Danish students in Sweden prefer psychology, sport and so-cial studies. This is followed by arts and crafts, journalism and media, and then the humanities and economics.

About the statisticsA number of statistics databases under-lie the figures on education in Denmark and sweden. these include: oECD, nordic statistics Bank and Ørestat. De-spite the international IsCED standard (International standard Classification of Education) for categorising levels of ed-ucation in an internationally comparable way, there are still some difficulties in making comparisons, for example, the definition of tertiary education IsCED 5a) differs in Denmark and sweden. In Denmark it includes full-time study for a minimum of three years with a final examination. In sweden it does not re-quire a degree, but at least three years of full-time study.

4The figures vary depending on the time of the sur-vey. New figures from CSN indicate 200.5DTS: KELA Students Abroad 2010–2011.

KnoWlEDGE AnD InnovAtIon | E D U C AT i o n

40 Øresund Trends 2012

1Nätverksbaserad urban innovation, Öresunds- regionen version 3.0, Underlag till IBU:s projekt om Öresundsregionens kvalitet, identitet och framtid, Oxford Research, 2009.

CULTURE

Culture and creativity are important factors for individual development, social cohesion and economic growth.

José Manuel Barroso, President of the European Commission

The Øresund Region is the largest met-ropolitan area in the Nordic countries and it also links Denmark and Sweden together. This gives a special cultural strength and diversity in the meeting between two countries’ related but dif-ferent customs and languages. It also involves a number of challenges and opportunities for culture to work across the Øresund and to create a common identity for the whole region.

Culture is identity, habits and expres-sion, and culture is part of creating and consuming activities and affects business

life and the labour market. An exciting cultural life is essential not only for cit-izens' well-being, but is also an impor-tant factor when companies choose their base, as well as when foreign knowledge workers seeking jobs abroad choose a new country in which to settle with family and children.

The Øresund Region is characterised by a rich cultural life, both in terms of the diversity that extends from the ethnicity of its urban areas to theatre, music and museums internationally, and in terms of the identity that goes right across the Øresund, and which challenges and en-riches due to differences in culture and language.

Over 50,000 – or nearly a third of all those employed in the cultural sector in Denmark and Sweden – work in the Øresund Region. Business sectors with TV, film and visual media and archi-

tecture as a focal point are strong in the Øresund Region and, unlike the general trend over the last few years, the cultural sector is currently experiencing modest progress.

Awareness of the region and the feeling of cohesion are greater on the Swed-ish side than on the Danish side of the Øresund. As many as 79 per cent of Swedes identify themselves wholly or partly with the Øresund Region, while the same applies to just 44 per cent of Danes1. However, the common identi-ty is reinforced through many differ-ent cultural collaborations across the Øresund, such as the common platform for the Øresund Region's cultural play-ers: Culture Øresund.

CultuRE AnD EXPERIEnCE | CULTURE

CultuRE AnD EXPERIEnCE

41Øresund Trends 2012

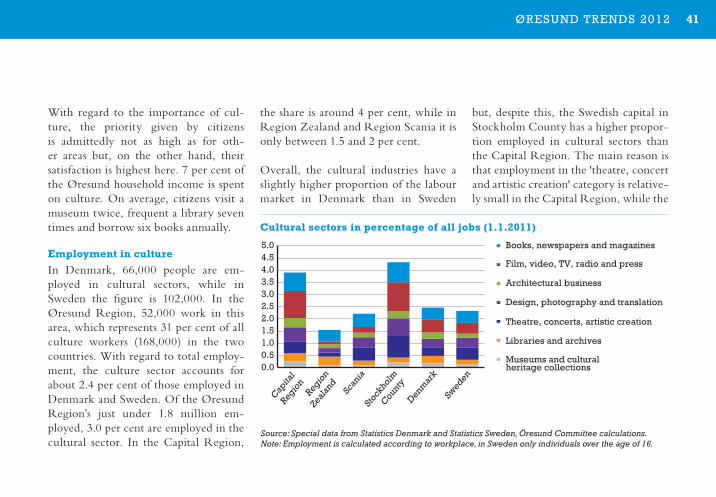

With regard to the importance of cul-ture, the priority given by citizens is admittedly not as high as for oth-er areas but, on the other hand, their satisfaction is highest here. 7 per cent of the Øresund household income is spent on culture. On average, citizens visit a museum twice, frequent a library seven times and borrow six books annually.

Employment in culture

In Denmark, 66,000 people are em-ployed in cultural sectors, while in Sweden the figure is 102,000. In the Øresund Region, 52,000 work in this area, which represents 31 per cent of all culture workers (168,000) in the two countries. With regard to total employ-ment, the culture sector accounts for about 2.4 per cent of those employed in Denmark and Sweden. Of the Øresund Region’s just under 1.8 million em-ployed, 3.0 per cent are employed in the cultural sector. In the Capital Region,

the share is around 4 per cent, while in Region Zealand and Region Scania it is only between 1.5 and 2 per cent.

Overall, the cultural industries have a slightly higher proportion of the labour market in Denmark than in Sweden

but, despite this, the Swedish capital in Stockholm County has a higher propor-tion employed in cultural sectors than the Capital Region. The main reason is that employment in the 'theatre, concert and artistic creation' category is relative-ly small in the Capital Region, while the

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

Number

Age

Capital Region 2011/2012

Forecast Capital Region 2031/2032

Scania 2011/2012

Forecast Scania 2031/2032

Region Zealand 2011/2012

Forecast Region Zealand2031/2032

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Capita

l

Region

Region

Zeal

and

Scan

ia

Stock

holm

County

Denmar

k

Sweden

0 1 2 3 4 5 6 7 8 9

10

-90 -91 -92 -93 -94 -95 -96 -97 -98 -99 -00 -01 -02 -03 -04 -05 -06 -07 -08 -09 -10 -11

Million vehicles

Øresund Bridge Ferries Copenhagen-Malmö Ferries Elsinore-Helsingborg

0

5

10

15

20

25

30

35

40

-01 -02 -03 -04 -05 -06 -07 -08 -09 -10 -11

Million individuals

Car Train Ferries Hydrofoil

0102030405060708090

100

Car Landing Car TrainHH Ferries The Øresund Bridge

Total

Holiday

Mini-break