Embed Size (px)

Citation preview

OVERVIEW OF CARIBBEAN TOURISM IN THE OVERVIEW OF CARIBBEAN TOURISM IN THE CURRENT GLOBAL CRISIS – STATUS AND CURRENT GLOBAL CRISIS – STATUS AND NEED FOR BETTER TOURISM STATISTICSNEED FOR BETTER TOURISM STATISTICS

Presented by WINFIELD GRIFFITH

Caribbean Tourism Organization, July, 2009

Trends In CARICOM Tourism Trends In CARICOM Tourism

Visitor Arrivals 1989 – 2008Visitor Arrivals 1989 – 2008

CARICOM TOURISTS ARRIVALS SO FAR CARICOM TOURISTS ARRIVALS SO FAR THIS YEARTHIS YEAR

CRUISE TOURISM TRENDSCRUISE TOURISM TRENDS

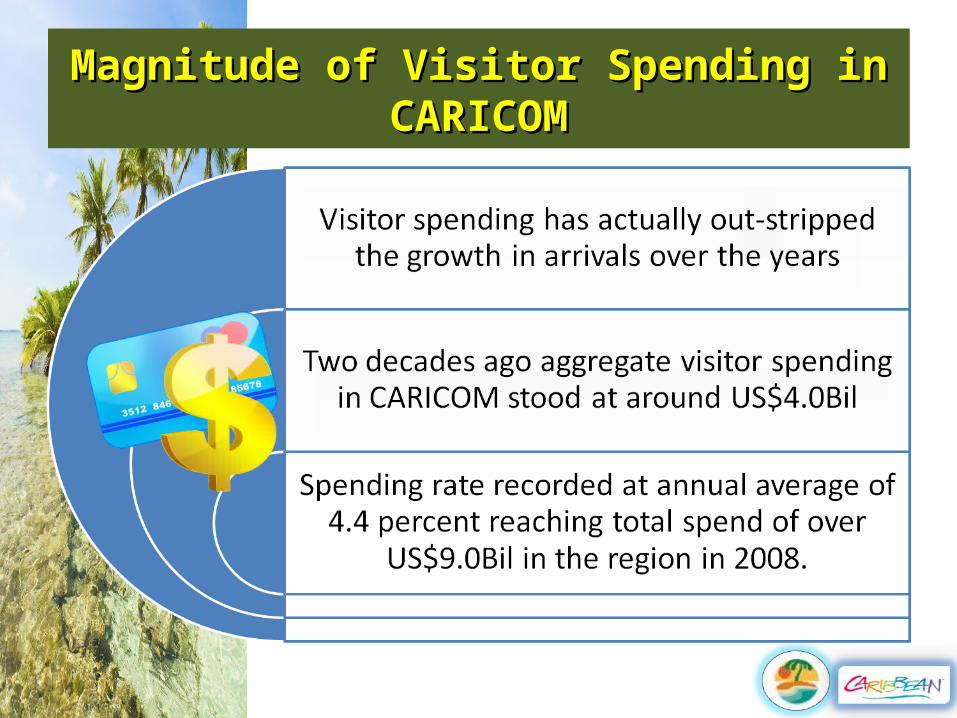

Magnitude of Visitor Spending in CARICOMMagnitude of Visitor Spending in CARICOM

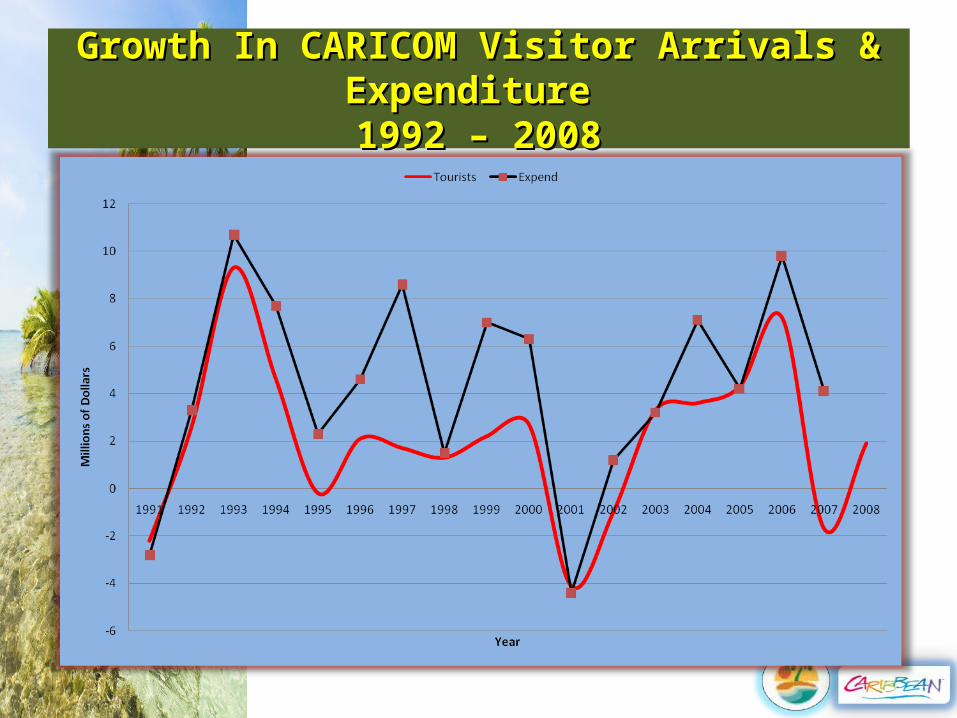

Growth In CARICOM Visitor Arrivals & Expenditure Growth In CARICOM Visitor Arrivals & Expenditure 1992 – 20081992 – 2008

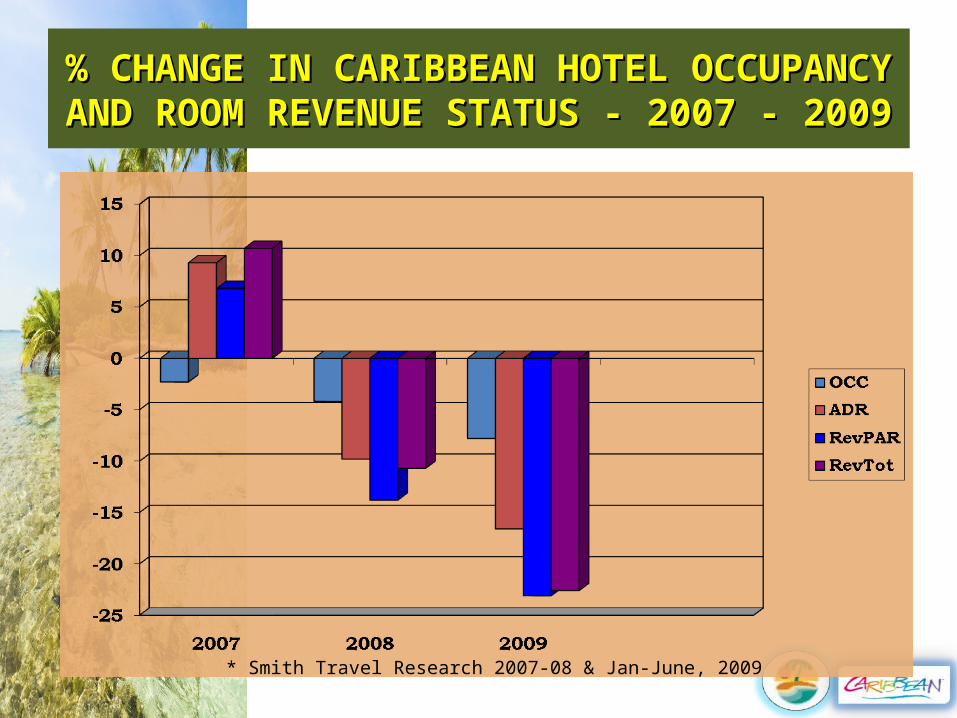

% CHANGE IN CARIBBEAN HOTEL OCCUPANCY AND % CHANGE IN CARIBBEAN HOTEL OCCUPANCY AND ROOM REVENUE STATUS - 2007 - 2009ROOM REVENUE STATUS - 2007 - 2009

* Smith Travel Research 2007-08 & Jan-June, 2009

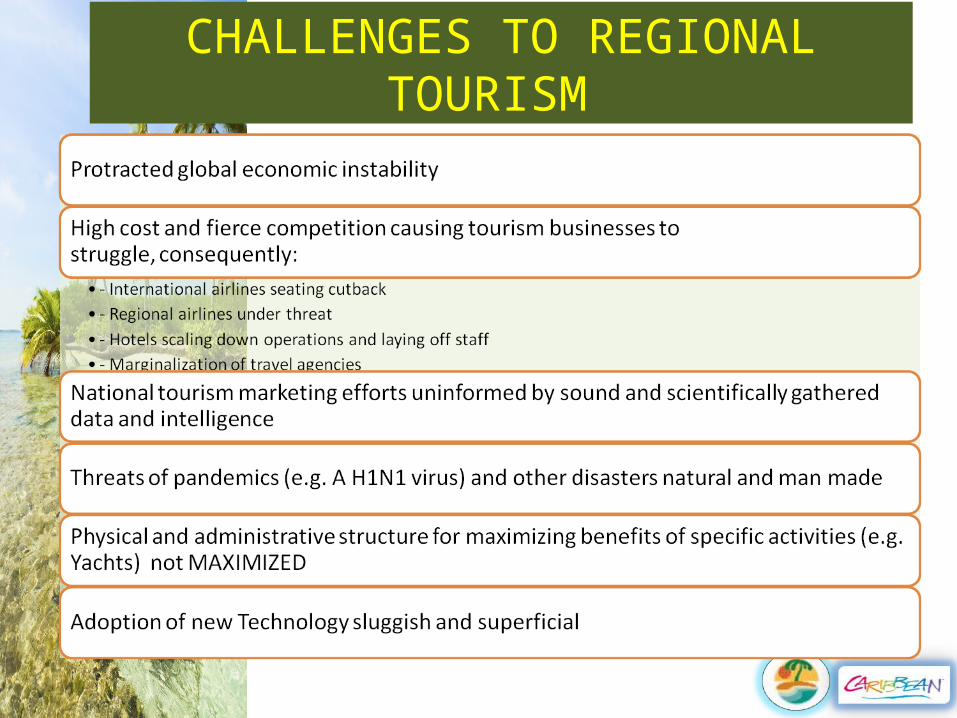

CHALLENGES TO REGIONAL TOURISM

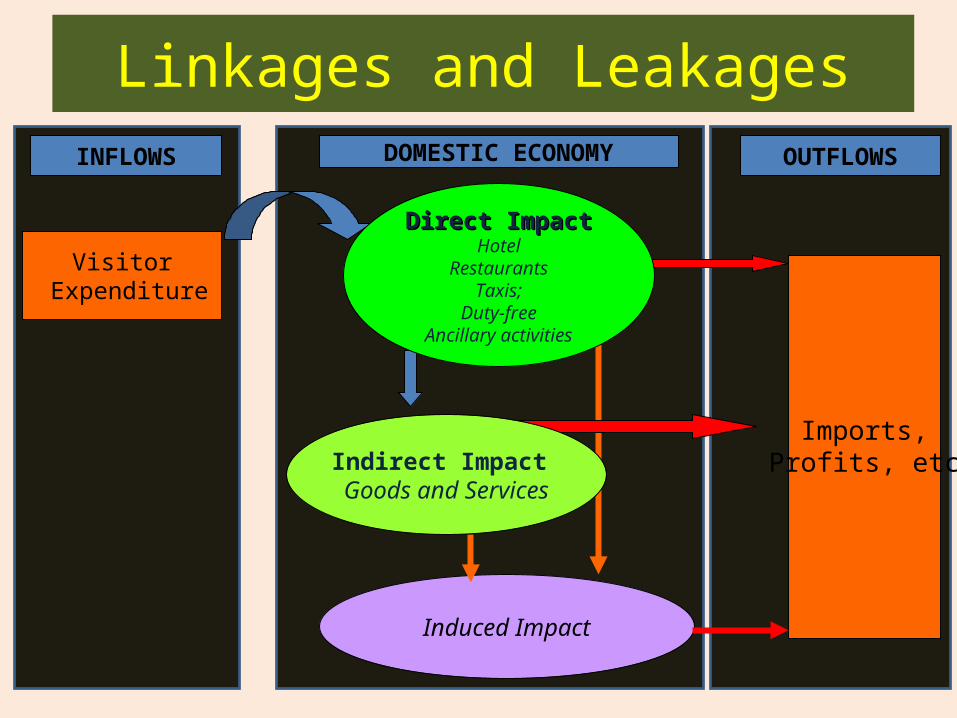

Linkages and Leakages

Visitor Expenditure

INFLOWS DOMESTIC ECONOMY OUTFLOWS

Imports,Profits, etc

Induced Impact

Indirect Impact Goods and Services

Direct ImpactDirect ImpactHotel

RestaurantsTaxis;

Duty-freeAncillary activities

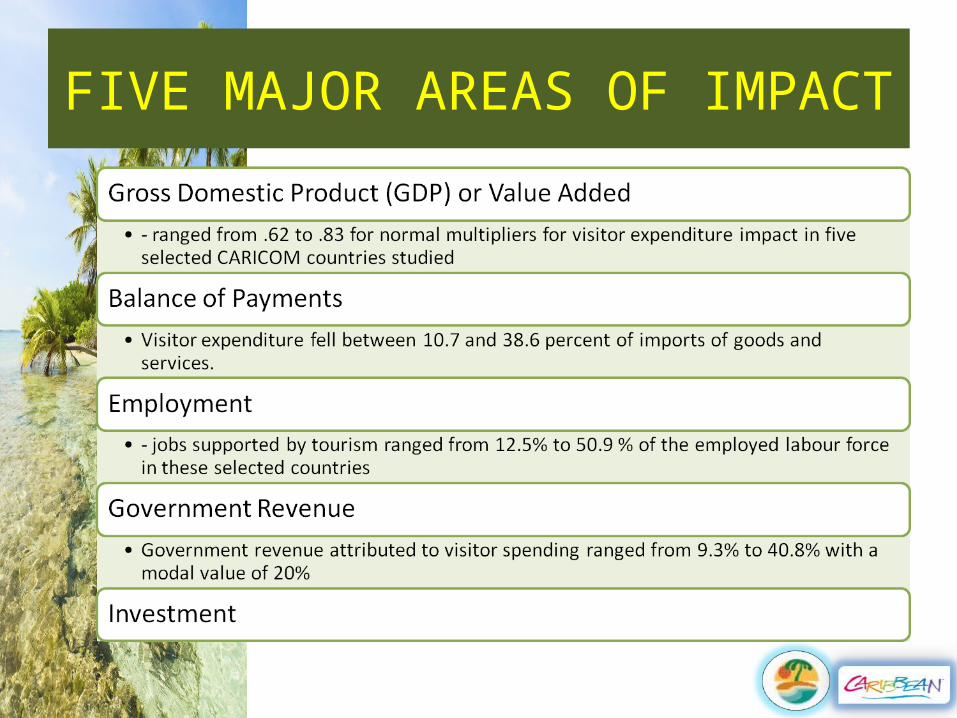

FIVE MAJOR AREAS OF IMPACT

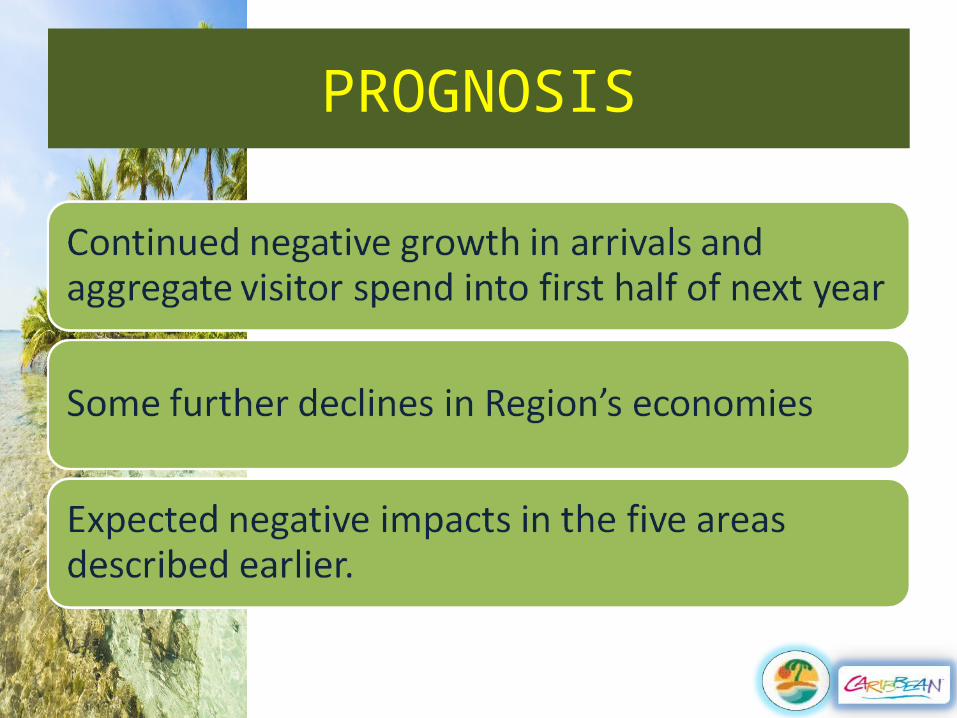

PROGNOSIS

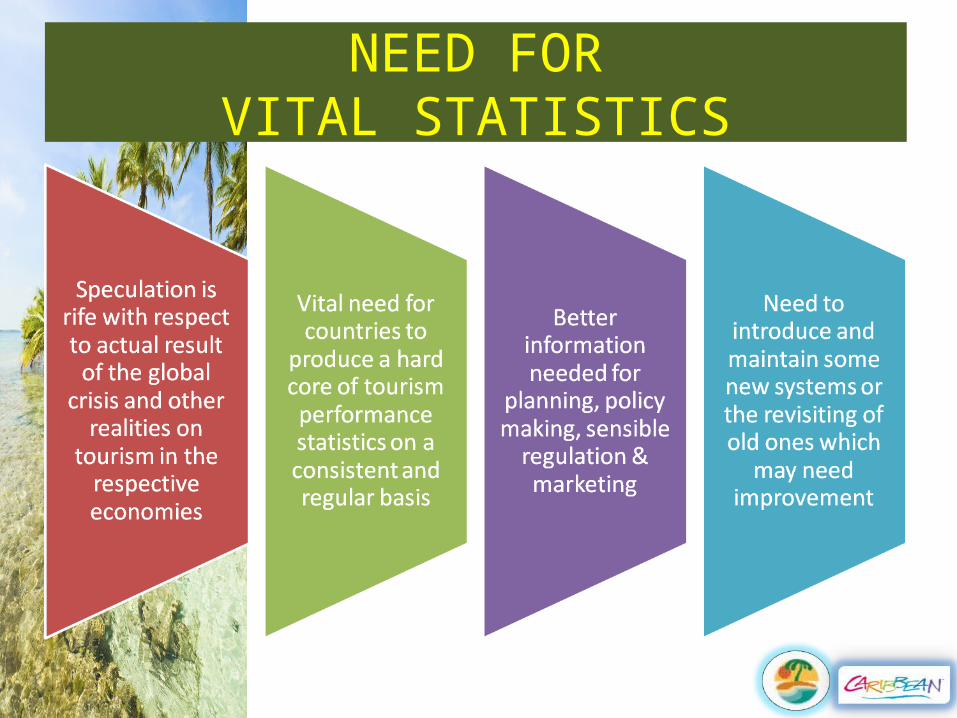

NEED FORVITAL STATISTICS

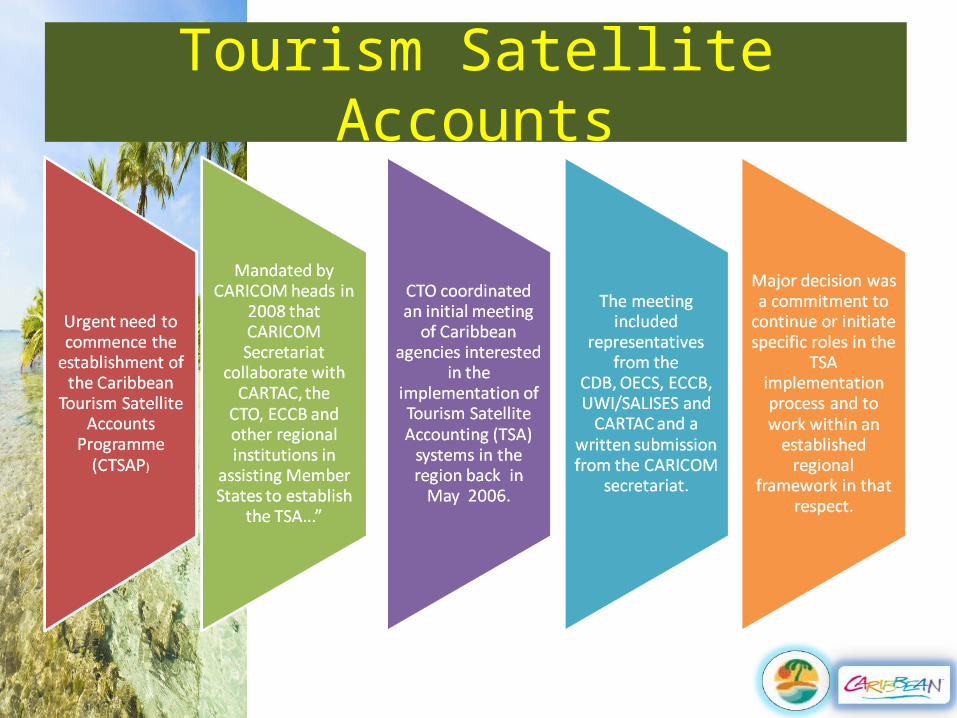

Tourism Satellite Accounts

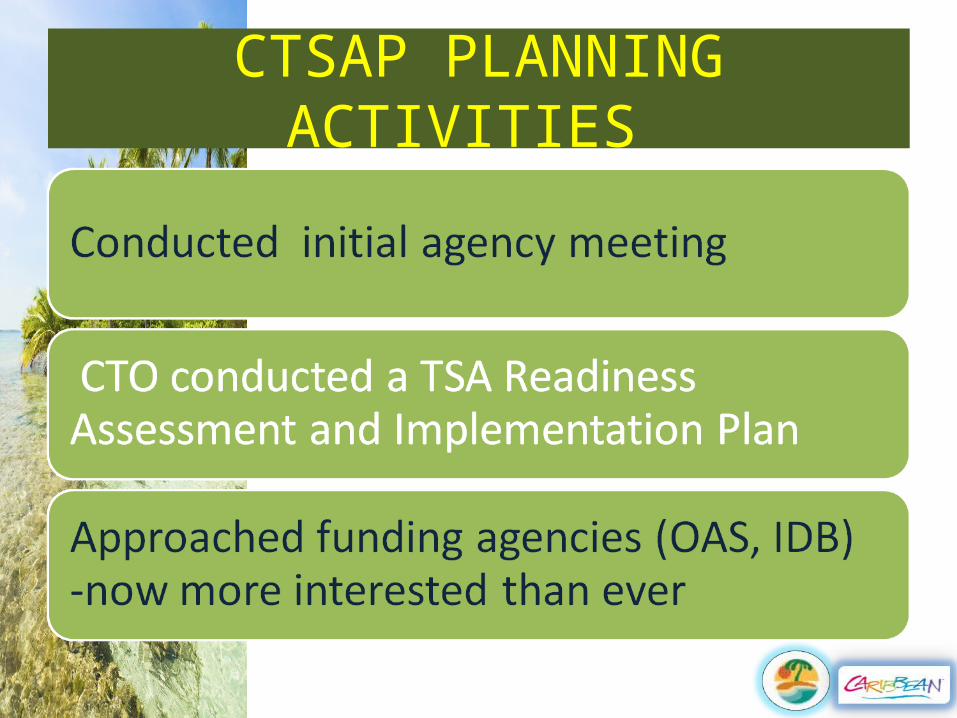

CTSAP PLANNING ACTIVITIES

Key Tourism Performance Indicators

WAY FORWARDWAY FORWARD

RESTRICTED