Embed Size (px)

Citation preview

COST SHARING, SUBCONTRACTS

& MORE…….

PAD Seminar – October, 2012

Gail L. Ryan, Assistant Vice President

Sponsored Program Administration

COURSE OBJECTIVES High level understanding of the following:

Cost-sharing on sponsored projectsSub-contracts on sponsored projectsOMB Circular A-21 BasicsUses of Indirect Cost Recovery

WHAT IS COST-SHARING? Definition (reference OMB

Circular A-110):

Project costs not borne by the sponsor but supported by contributions from the recipient and/or third parties, both cash and in-kind.

COST-SHARING DEFINED

Portion of research costs that are not borne by the sponsorPrimarily required by federal sponsorsPledge can be a % of total project costs or a

fixed amountObligation must come from non federal

fundsObligation must not come from federal flow

through

TYPES OF COST-SHARING Mandatory – explicit in award document

and/or explicit in program announcement or guidelines.

Voluntary Committed – defined and quantified in either dollars or narrative in proposal.

Voluntary Uncommitted – occurs in course of project, was not planned or anticipated.Cost overruns fall into this category

COMMITTED VS. UNCOMMITTED Committed cost-sharing

Regardless of mandatory or voluntary, once committed becomes true obligation to the institution.

Must be documented in financial system Proposal commitments = Award

requirements Voluntary Uncommitted cost-sharing

Treated differently than committed cost-sharing. Not included in organized research base for F&A

rate purposes. Excluded from effort reporting requirements of A-

21, Section J-8. Does NOT need to be documented

COMMON FORMS OF COST SHARING Personnel – time/effort of PI or other staff

Per OMB A-110, rates for volunteer services shall be consistent with those paid for similar work in the recipient’s organization.

Equipment – sometimes a required match for a new piece of equipment to be provided by the University. Use of existing equipment is usually not allowable as

cost-sharing. Operational costs – supplies, travel, etc. “In-kind” cost sharing – donations by third parties.

Quantifiable Certification/documentation of actual

F&A – reduction in recovery can often be claimed

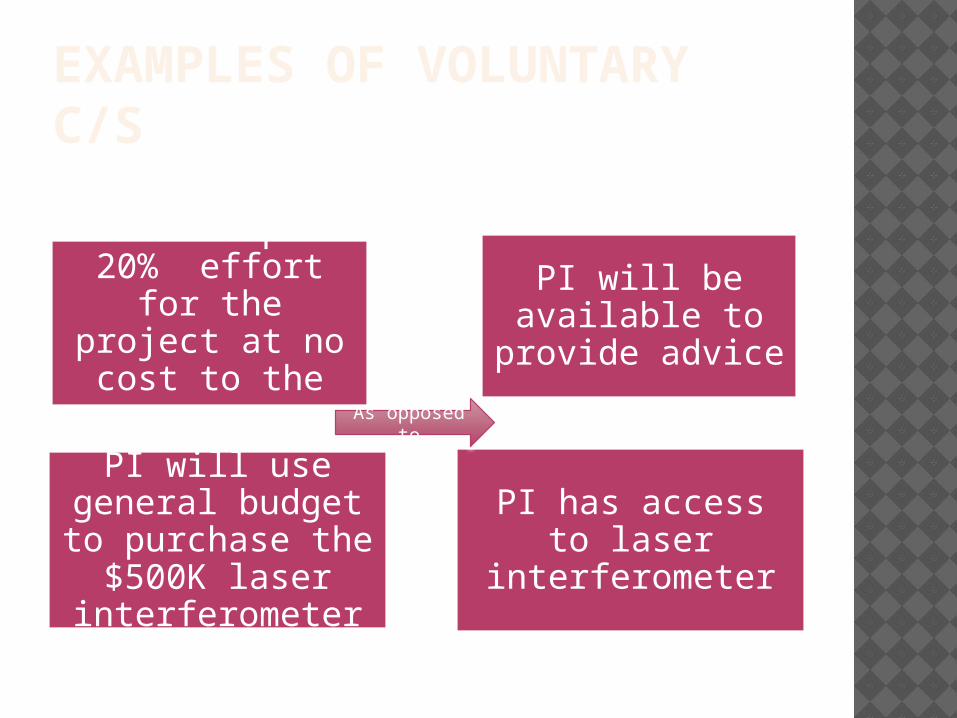

EXAMPLES OF VOLUNTARY C/S

PI will spend 20% effort for

the project at no cost to the

agency

PI will be available to

provide advice

PI will use general budget to

purchase the $500K laser

interferometer

PI has access to laser

interferometer

As opposed to

WHAT ABOUT SALARY CAP?

How should salary amount in excess of the agency (e.g. NIH) salary cap be handled?

Salary cap is considered voluntary committed, and must therefore be documented and identifiable within the financial records of the institution.

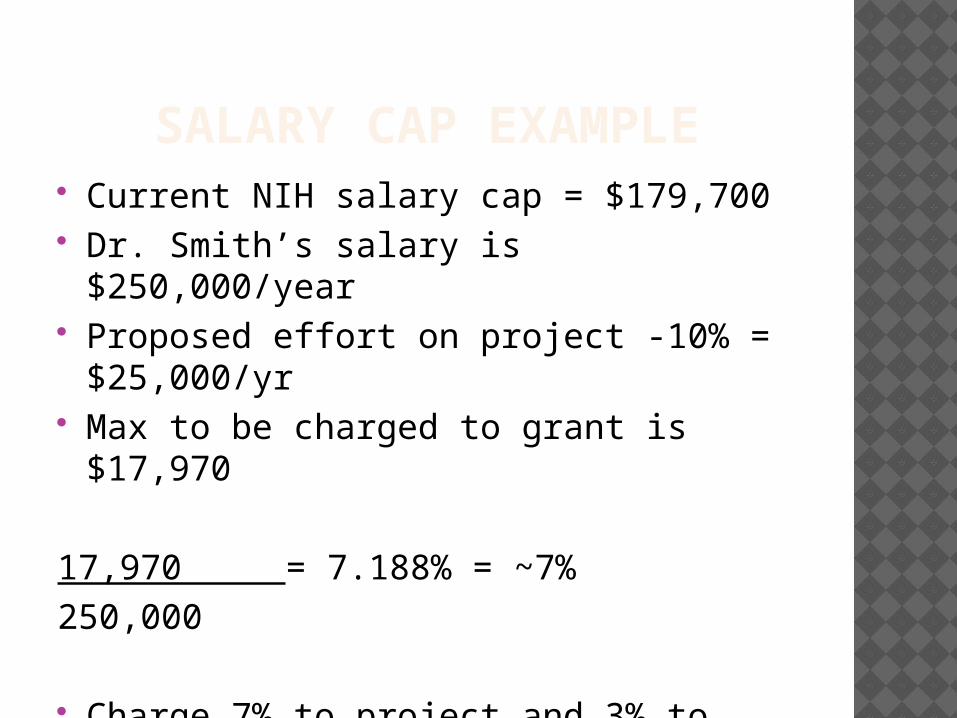

SALARY CAP EXAMPLE Current NIH salary cap = $179,700 Dr. Smith’s salary is $250,000/year Proposed effort on project -10% =

$25,000/yr Max to be charged to grant is $17,970

17,970 = 7.188% = ~7%250,000

Charge 7% to project and 3% to cost-sharing

COST-SHARING BY SUB-RECIPIENTS

Cost-sharing requirements may be passed along to sub-recipients.

Prime awardee retains ultimate responsibility for the commitment.

Therefore, if sub-recipient does not meet their match requirement, the prime awardee may need to scramble at the end of the project.

Important to monitor as part of invoicing approval process, etc.

ALLOWABILITY OF C/S EXPENSES

In order to be claimed as c/s, must meet all the same criteria to be allowable on the award:

Incurred during award periodAllowable expenditure to the projectNecessary and reasonable for

accomplishing project goals and objectivesMust be auditable

UNALLOWABLE COST-SHARING Items normally treated as indirect costs

(e.g. office supplies, clerical salaries, etc.)

Specifically unallowable costs

Cost sharing used on another project

IMPORTANT CONSIDERATIONS

Funding sources should be identified at the time of proposal submission to ensure that commitments are in place.

In other words, “don’t put it in the proposal if you aren’t willing and able to cover the cost!”

IMPORTANT CONSIDERATIONS

Some agencies may require c/s expenditures to occur at same pace as sponsored award.

Consider total cost to the institution – hidden costs of c/s include:Loss of fringe benefits and indirect cost

recovery Increase in research base for F&A

calculationsStaff time at both departmental and central

level for accounting and reporting of c/s

CASH VS. IN-KIND C/S Cash – those outlays that involve an

actual outlay of cash by the institution (personnel, supplies, equipment, etc.)

In-kind – non-cash contributions provided by non-federal third parties, e.g.Volunteer servicesDonated supplies/equipment – must use

current fair market value

Either type must be identifiable and able to be documented.

IMPACT OF C/S There are several “not so obvious”

negative impacts of voluntary cost-sharing.

Negative impacts:Lowers F&A rateComplicates effort reporting system Increases administrative costs for

tracking/reporting cost-share

IMPORTANT CONSIDERATIONS

If there is no documentation (i.e. in the payroll distribution system) of the time devoted to research, an agency may factor in additional dollars into the research base.

This may hurt your rate negotiation process!

Better to be able to bury them in documentation.

C/S IMPACT ON F&A-SIMPLIFIED

Basics of the F&A rate: Pooled expenditures – those that cannot

be allocated to a particular project (i.e. indirect costs)

Base expenditures – those direct expenses that make up an institution’s MTDC base

Rate = Pool Base

Goal is to keep the pool high and the base low.

Where does cost-sharing fit in?

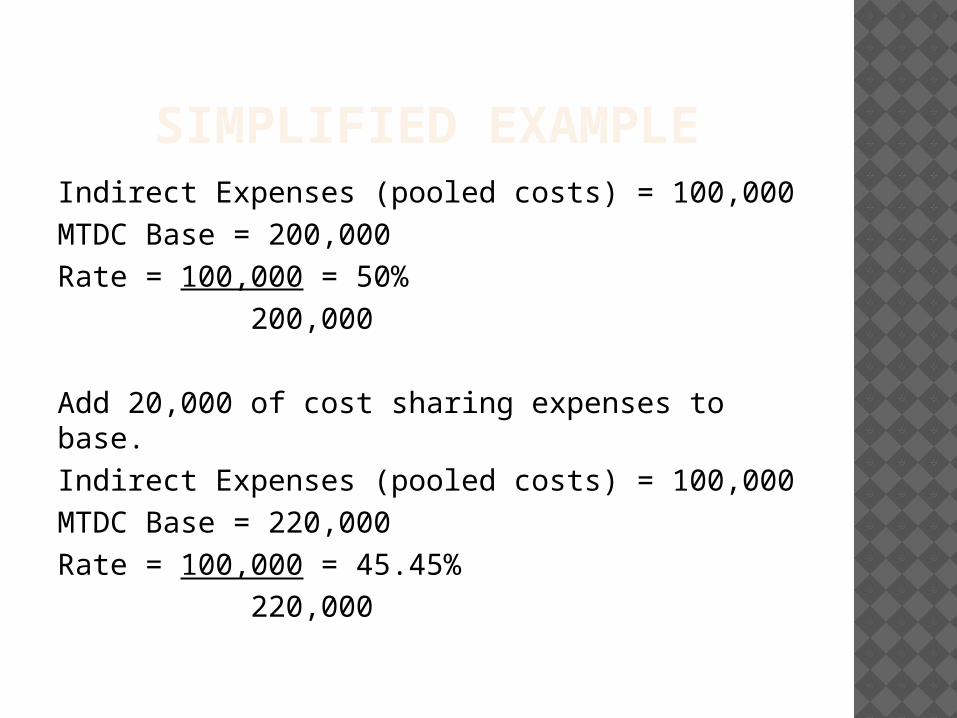

SIMPLIFIED EXAMPLEIndirect Expenses (pooled costs) = 100,000MTDC Base = 200,000Rate = 100,000 = 50% 200,000

Add 20,000 of cost sharing expenses to base.Indirect Expenses (pooled costs) = 100,000MTDC Base = 220,000Rate = 100,000 = 45.45% 220,000

FINAL ADVICE Only commit to cost-sharing when

required.

Only commit to the level of the amount required.

Only commit what you are prepared to deliver.

DOCUMENT, DOCUMENT, DOCUMENT!

WHAT IS A SUBCONTRACT?

Differentiation between a subcontractor and a vendor is the first step:

Subcontract: An agreement written under the authority of and consistent with the terms of the Prime Award (grant or contract) that transfers a portion of the research or substantive effort to another organization.

A subcontract is normally signed by both parties.

COMPARISON TO OTHER MECHANISMS

Personal Services Contract: A written agreement that transfers a specialized service not available through a routine service provider.

The contractor requires a specialized knowledge in a particular field and often requires originality, creativity, and decision-making abilities.

The agreement is intellectual and professional in nature, and is normally signed by both parties.

COMPARISON TO OTHER MECHANISMS

Purchased Services: Are orders to procure goods and services that are normally routine in nature.

They are normally signed only by the Purchasing party.

WHEN TO ISSUE A SUBCONTRACT

A subcontract is an appropriate procurement mechanism when:

1. The collaboration is substantive programmatic work which is beyond mere analytical work-for-hire normally conducted by a routine service provider.

2. The collaboration is substantial enough that the collaborating individual or organization will participate in preparation of results, publication, presentation or other collaborative participation beyond routine analytical work.

3. The collaborator will maintain control of the work to be performed under the subcontract.

SUBCONTRACTING PROCESS

Subcontracts are typically identified in the proposal and/or approved by the sponsor.

SPA has a team dedicated to preparation and administration of subcontracts.

Approval of invoices from subrecipients is a shared responsibility: PI responsible for verifying work proceeding at

an expected pace, and expenses are reasonable based on work completed.

SPA responsible for verifying budget, allowability of expenses, etc.

SUBCONTRACTING – PI RESPONSIBILITIES

Approve scope of work and related budget

Ensure receipt of required deliverables and/or progress reports and review for appropriateness

Align deliverables/progress reports with invoices submitted for payment

Coordinate any modifications with the SPA contracts team (e.g. change in scope, rebudget request, etc.)

EXPENDITURE ALLOWABILITY

Federal awards – OMB Circular A21 outlines allowability for certain types of expenditures.

A21 = “Cost Principles for Educational Institutions”

Guidance on what should be direct charged to projects vs. what we recover via our indirect cost rate

Specifically, costs of a clerical or administrative nature are considered “sensitive” and care must be taken if direct charged (typically recovered via indirects)

A-21ALLOWABILITY The following items are considered

sensitive, and require extra justification to directly charge to federal projects:

Clerical and administrative salariesOffice supplies (includes computers by

definition of equipment threshold) Telephone line costs (local)PostageOther

A-21 ALLOWABILITY Certain criteria need to be met in order

to allow these types of expenses as direct charges:Must be able to identify the costs

specifically to the project with a high degree of accuracy

Costs must be incurred for a different purpose or circumstance (how the item is used, not “what it is”) OR part of a “major project” as defined in the circular.

Costs must have been explicitly budgeted, with justification, and awarded.

SPENDING INDIRECT COST RECOVERY ICR funds are set up in the general fund

range, and must follow the “rules” for the general fund.

Typical expenditures include items necessary to the research, but which might be considered questionable, or unallowable, if charged directly to a sponsored project.

SPENDING INDIRECT COST RECOVERY Examples of expenditures include:

Office supplies, toner, computers, etc. (those items which we discussed as being A21 sensitive)

TravelMemberships, duesBooks, journalsMiscellaneous items which are not easily

identifiable to a particular project (e.g. shared by multiple projects)

QUESTIONS???