Embed Size (px)

Citation preview

130

CHAPTER - 6

PA – NPA ANALYSIS AND INTERPRETATION OF DATA OF

SELECTED UCBS TEKAN TOGETHER 6.1 Introduction 131

6.2 Concept Of NPA And Its Importance In Banking Sector 131

6.3 Common - Size Analysis Of The Selected UCBs 132

6.4 Common – Size Analysis Of PA And NPAs Of The

Selected UCBs Taken Together

132

6.5 Ratio Analysis Of The Selected UCBs Taken Together

6.5.1 Gross NPA ratio

6.5.2 Net NPA ratio

6.5.3 Problem Assets ratio

6.5.4 Depositors‟ Safety ratio

6.5.5 Share Holders Risk ratio

6.5.6 Provisions ratio

6.5.7 Sub – standard Assets ratio

6.5.8 Doubtful Assets ratio

6.5.9 Loss Assets ratio

134

6.6 General Causes Of Non Performing Assets

153

131

CHAPTER - 6 PA – NPA ANALYSIS AND INTERPRETATION OF DATA OF

SELECTED UCBS TEKAN TOGETHER

6.1 INTRODUCTION:

In today‟s world of healthy competition where all business units and industries

are trying to survive in the market, the banking sector too can not be aloof from

competition in market. As liberalization and globalization has opened door for free

entry in any business, the co-operative sector of banking has to face competition from

not only nationalized or commercial banks but also from private financial instructions

and foreign banks. Two or three decades back, profit had a back seat and came as an

end product. They never consciously planned their business of banking from the profit

point of view. But today profit is a sign of vitality and success in a competitive

scenario. It ensures survival and growth and can eventually become the only parameter

for performance evaluation. Profit depends upon NPA provisions. Hence, for a banker,

NPA has become very significant.

In this chapter an attempt has been made to find out the importance of PA and

NPA in banking sector and to measure the level of NPA of banking sector using

accounting techniques of NPA analysis and statistical tools along with graphs and

charts.

6.2 CONCEPT OF NPA AND ITS IMPORTANCE IN BANKING SECTOR:

Guidelines issued by Reserve Bank of India regarding recognition, asset

classification and provisioning norms have compelled banks in India not to show true

financial picture in the balance sheet but also to take corrective steps for improving

their loan portfolio. With the adoption of these guidelines, banks are now fully vigilant

about quality of their loan assets and various steps are being taken by them to reduce

the NPAs. It is always better to follow the proper policy for appraisal, supervision and

follow – up of advances to avoid NPAs. However, risks attached to lending cannot be

completely eliminated. If certain advances are converted into NPAs, it is necessary to

take corrective steps to reduce them. Reduction in NPAs is necessary to improve

profitability.

132

6.3 COMMON - SIZE ANALYSIS OF THE SELECTED UCBs:

The entire picture of the PA and NPA of the selected UCBs under study has

been presented in the form of common – size statement for the period spreading from

2001-02 to 2008-09. An attempt to analyze PA and NPA of the selected UCBs with

the help of their common - size PA and NPA statement is made at this stage. Here the

figures of total advances have been taken as equal to 100 and the percentage of

individual items of PA and NPAs has been calculated. Common - size PA and NPA

statement has been presented in appendices 7.2 to 7.11

6.4 COMMON – SIZE ANALYSIS OF PA AND NPAs OF THE SELECTED

UCBs TAKEN TOGETHER:

Consolidated PA and NPAs of all the selected UCBs under study has been

presented in appendix 7.1. The appendix clearly indicates the ratio of PA and NPAs of

all the selected UCBs during the period of study. The proportion of each component of

the PA and NPAs statement has also been found out considering the total Advances as

100.

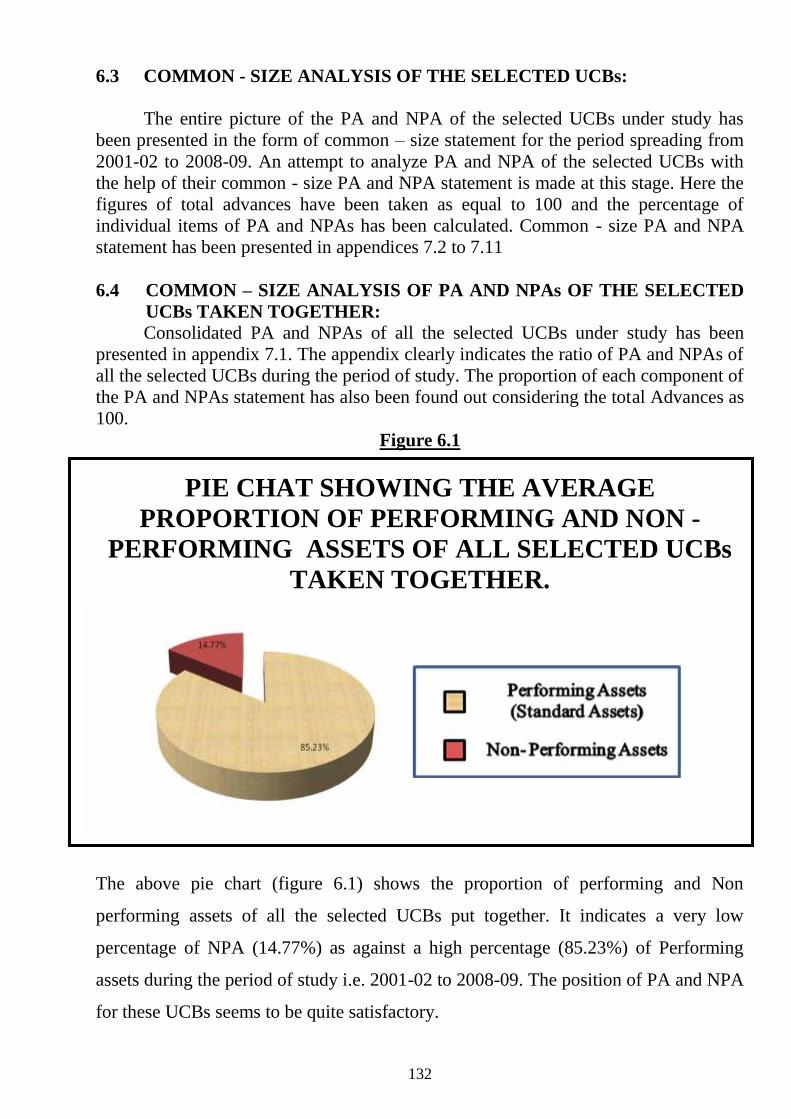

Figure 6.1

PIE CHAT SHOWING THE AVERAGE

PROPORTION OF PERFORMING AND NON -

PERFORMING ASSETS OF ALL SELECTED UCBs

TAKEN TOGETHER.

The above pie chart (figure 6.1) shows the proportion of performing and Non

performing assets of all the selected UCBs put together. It indicates a very low

percentage of NPA (14.77%) as against a high percentage (85.23%) of Performing

assets during the period of study i.e. 2001-02 to 2008-09. The position of PA and NPA

for these UCBs seems to be quite satisfactory.

133

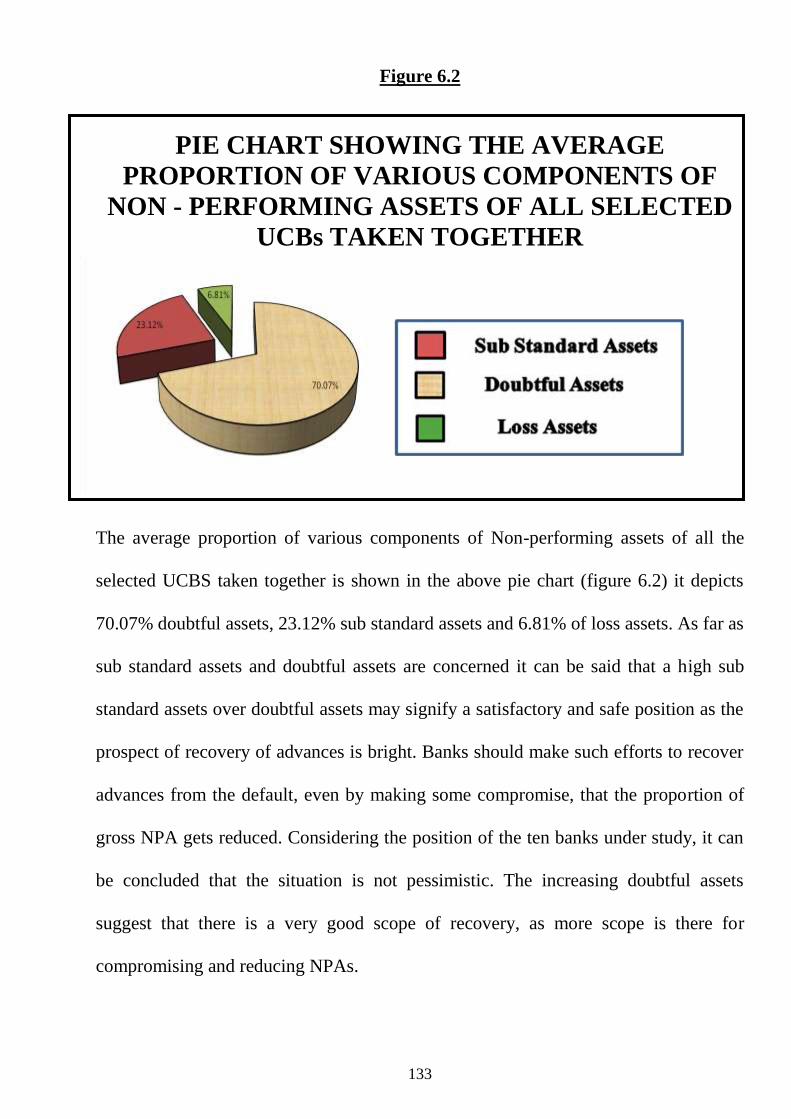

Figure 6.2

PIE CHART SHOWING THE AVERAGE

PROPORTION OF VARIOUS COMPONENTS OF

NON - PERFORMING ASSETS OF ALL SELECTED

UCBs TAKEN TOGETHER

The average proportion of various components of Non-performing assets of all the

selected UCBS taken together is shown in the above pie chart (figure 6.2) it depicts

70.07% doubtful assets, 23.12% sub standard assets and 6.81% of loss assets. As far as

sub standard assets and doubtful assets are concerned it can be said that a high sub

standard assets over doubtful assets may signify a satisfactory and safe position as the

prospect of recovery of advances is bright. Banks should make such efforts to recover

advances from the default, even by making some compromise, that the proportion of

gross NPA gets reduced. Considering the position of the ten banks under study, it can

be concluded that the situation is not pessimistic. The increasing doubtful assets

suggest that there is a very good scope of recovery, as more scope is there for

compromising and reducing NPAs.

134

6.5 RATIO ANALYSIS OF THE SELECTED UCBs:

An attempt has also been made to judge the position of NPAs of the UCBs

through ratio analysis using important ratios as follows:

6.5.10 Gross NPA ratio.

6.5.11 Net NPA ratio.

6.5.12 Problem Assets ratio.

6.5.13 Depositors‟ Safety ratio.

6.5.14 Share Holders Risk ratio.

6.5.15 Provisions ratio.

6.5.16 Sub – standard Assets ratio.

6.5.17 Doubtful Assets ratio.

6.5.18 Loss Assets ratio.

135

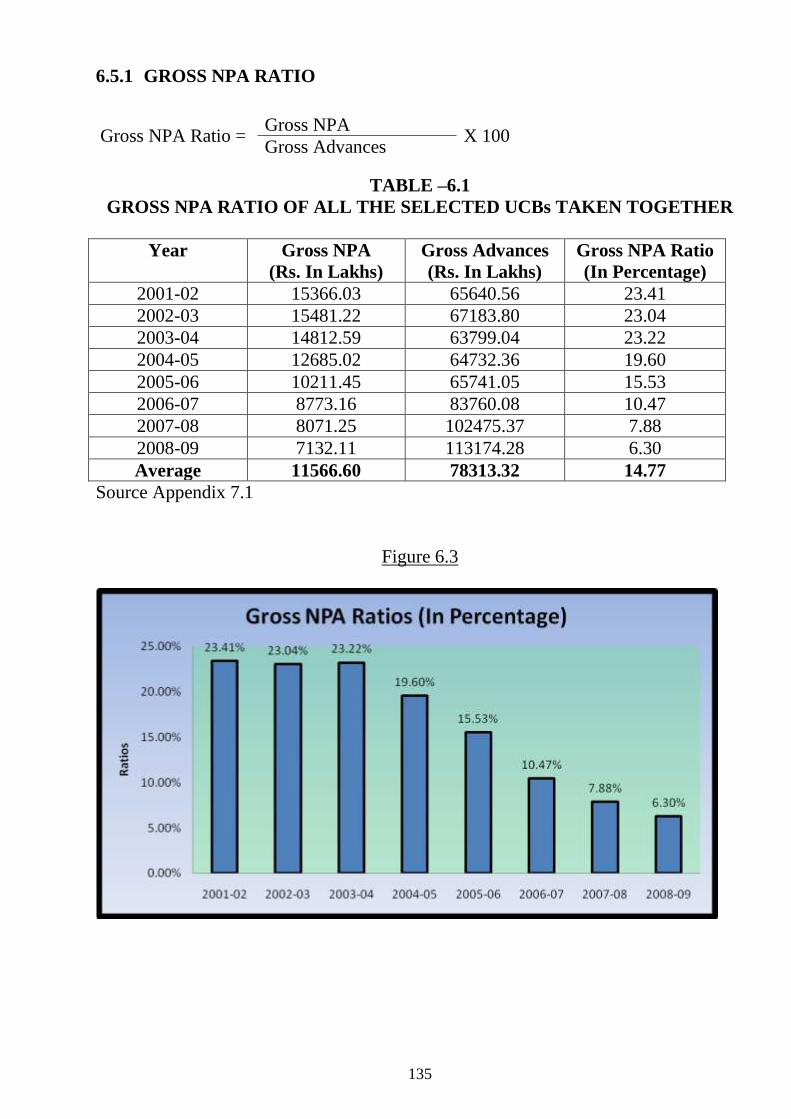

6.5.1 GROSS NPA RATIO

Gross NPA Ratio = Gross NPA

X 100 Gross Advances

TABLE –6.1

GROSS NPA RATIO OF ALL THE SELECTED UCBs TAKEN TOGETHER

Year Gross NPA

(Rs. In Lakhs)

Gross Advances

(Rs. In Lakhs)

Gross NPA Ratio

(In Percentage)

2001-02 15366.03 65640.56 23.41

2002-03 15481.22 67183.80 23.04

2003-04 14812.59 63799.04 23.22

2004-05 12685.02 64732.36 19.60

2005-06 10211.45 65741.05 15.53

2006-07 8773.16 83760.08 10.47

2007-08 8071.25 102475.37 7.88

2008-09 7132.11 113174.28 6.30

Average 11566.60 78313.32 14.77

Source Appendix 7.1

Figure 6.3

136

The above table and graph makes it very clear that the average

gross NPA of all the UCBs under study is very satisfactory. It is seen

that the gross NPA which was 23.41% in 2001-02 reduced marginally

every year and finally reached 6.30% in 2008-09 which is much lower

than the average gross NPA (14.77%). It goes without saying that the

UCBs are taking good care and following ideal norms of granting

advances, so that the recovery is satisfactory leading to lower gross

NPA. It is very encouraging that the gross NPA ratio in the last three

years is very much lower than the average 14.77%.

137

6.5.2 NET NPA RATIO

Net NPA Ratio = Gross NPA – Provisions

X 100 Gross Advances - Provisions

TABLE –6.2

NET NPA RATIO OF ALL THE SELECTED UCBs TAKEN TOGETHER

Year Net NPA

(Rs. In

Lakhs)

Gross

Advances

(Rs. In

Lakhs)

Provisions

by banks

(Rs. In

Lakhs)

Net

Advances

(Rs. In

Lakhs)

NET NPA

Ratio

(In

Percentage)

2001-02 4982.88 65640.56 10660.25 54980.31 9.06

2002-03 4942.84 67183.80 12389.64 54794.16 9.02

2003-04 3378.26 63799.04 15292.62 48506.42 6.96

2004-05 1733.94 64732.36 16915.86 47816.50 3.63

2005-06 411.64 65741.05 18282.75 47458.30 0.87

2006-07 0.00 83760.08 18611.99 65148.09 0.00

2007-08 0.00 102475.37 19009.99 83465.38 0.00

2008-09 0.00 113174.28 17969.65 95204.63 0.00

Average 1931.20 78313.32 16141.59 62171.20 3.11

Source: Appendices 7.1 & 8.1

Figure 6.4

138

The above graph presents the Net NPA Ratio of all the selected UCBs

taken together. It can be noticed that Net NPA ratio has resulted in the first

five years of study i.e. from 2001-02 to 2005-06, though reducing in effect.

The Net NPA ratio during these years can be ascribed to the high Net NPA

position of The Sardar Bhiladwala Pardi People‟s Co.Op. Bank Ltd. The

bank had failed to make sufficient provisions against NPA in these years.

However, they succeeded in making provisions and thus they could bring

the Net NPA down to zero. The Net NPA Ratio of the bank in the year

2006-07,2007-08 and 2008-09 is zero after the improvement of the above

bank. It is to be seen that the position of all other banks has been very good

and they had zero net NPA ratio. It is therefore, evident that nine of the

above ten banks have been able to make enough provisions against their

gross NPA which is a very satisfactory position. The management of all

these banks have taken enough care in granting advances and they have

been very meticulous in recovering from defaulters. Another observation is

that the above banks have strictly followed the RBI guidelines by making

provisions against NPAs.

139

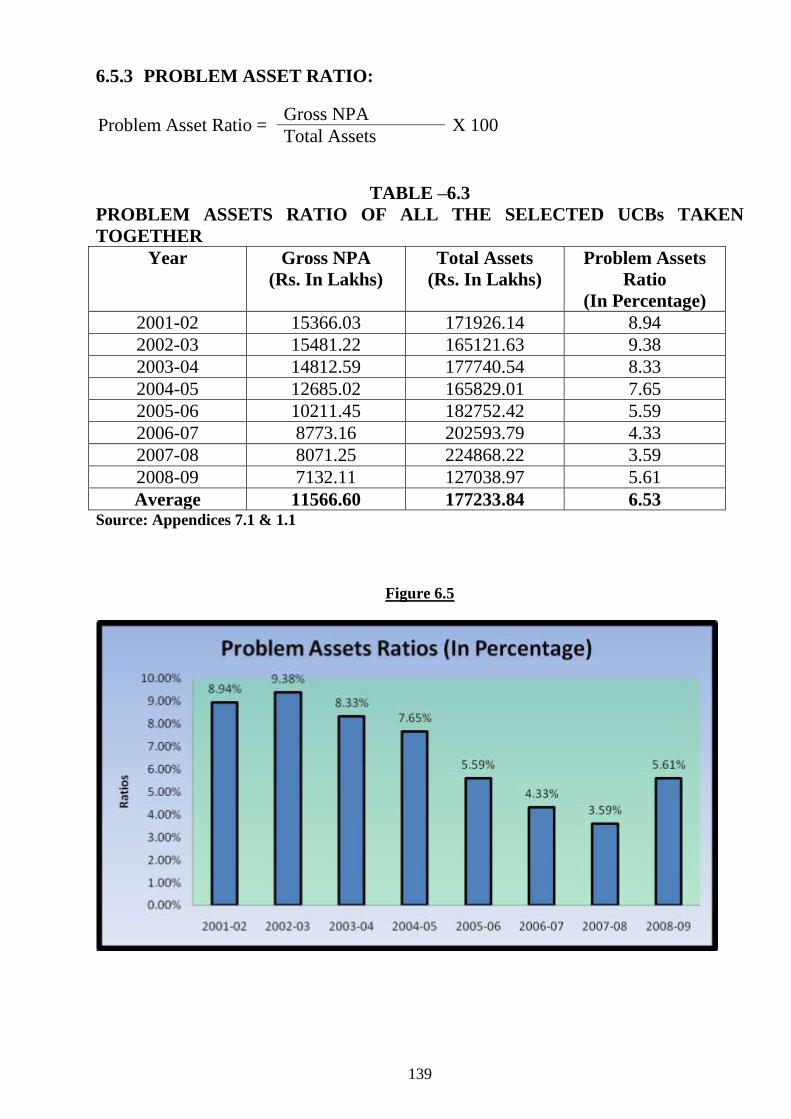

6.5.3 PROBLEM ASSET RATIO:

Problem Asset Ratio = Gross NPA

X 100 Total Assets

TABLE –6.3

PROBLEM ASSETS RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER

Year Gross NPA

(Rs. In Lakhs)

Total Assets

(Rs. In Lakhs)

Problem Assets

Ratio

(In Percentage)

2001-02 15366.03 171926.14 8.94

2002-03 15481.22 165121.63 9.38

2003-04 14812.59 177740.54 8.33

2004-05 12685.02 165829.01 7.65

2005-06 10211.45 182752.42 5.59

2006-07 8773.16 202593.79 4.33

2007-08 8071.25 224868.22 3.59

2008-09 7132.11 127038.97 5.61

Average 11566.60 177233.84 6.53 Source: Appendices 7.1 & 1.1

Figure 6.5

140

The Problem assets ratio shows the proportion of Gross NPA to total

assets and the table & graph given above shows that the percentage of all

selected UCBs is 6.53% on an average for the last 8 years. The percentage

shown is, however not stable. It was reducing from 2002-03 to 2007-08 but

it went slightly up in the year 2008-09. It seems that much attention has

been given by the management to the proportion of Gross NPA and total

assets of the bank. The gross NPA is on the rise due to the increase in

advances.

141

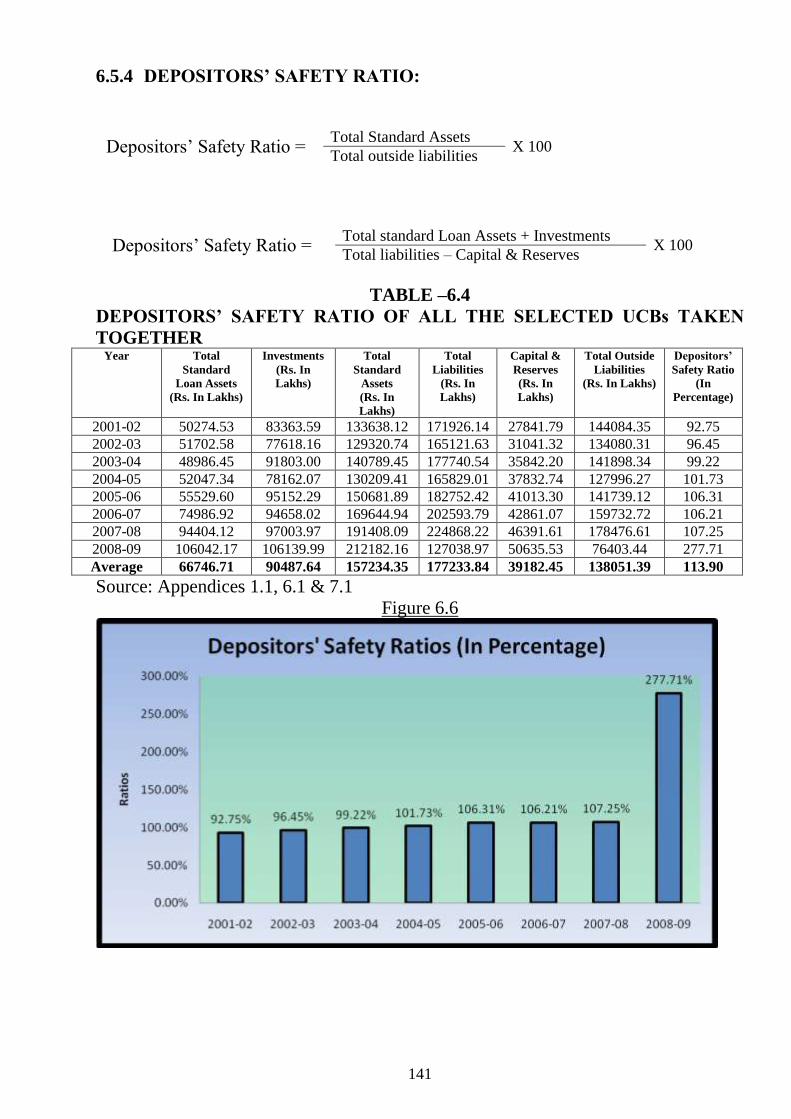

6.5.4 DEPOSITORS‟ SAFETY RATIO:

Depositors‟ Safety Ratio = Total Standard Assets

X 100 Total outside liabilities

Depositors‟ Safety Ratio = Total standard Loan Assets + Investments

X 100 Total liabilities – Capital & Reserves

TABLE –6.4

DEPOSITORS‟ SAFETY RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER Year Total

Standard

Loan Assets

(Rs. In Lakhs)

Investments

(Rs. In

Lakhs)

Total

Standard

Assets

(Rs. In

Lakhs)

Total

Liabilities

(Rs. In

Lakhs)

Capital &

Reserves

(Rs. In

Lakhs)

Total Outside

Liabilities

(Rs. In Lakhs)

Depositors‟

Safety Ratio

(In

Percentage)

2001-02 50274.53 83363.59 133638.12 171926.14 27841.79 144084.35 92.75

2002-03 51702.58 77618.16 129320.74 165121.63 31041.32 134080.31 96.45

2003-04 48986.45 91803.00 140789.45 177740.54 35842.20 141898.34 99.22

2004-05 52047.34 78162.07 130209.41 165829.01 37832.74 127996.27 101.73

2005-06 55529.60 95152.29 150681.89 182752.42 41013.30 141739.12 106.31

2006-07 74986.92 94658.02 169644.94 202593.79 42861.07 159732.72 106.21

2007-08 94404.12 97003.97 191408.09 224868.22 46391.61 178476.61 107.25

2008-09 106042.17 106139.99 212182.16 127038.97 50635.53 76403.44 277.71

Average 66746.71 90487.64 157234.35 177233.84 39182.45 138051.39 113.90

Source: Appendices 1.1, 6.1 & 7.1

Figure 6.6

142

Due to awareness of depositors towards safety of their money deposited in

a bank they are forced to study the proportion of standard assets of the bank

to the outside liabilities, mostly consisting of their deposits. The above

table and graph proves that the ratio of all the UCBs under study is very

satisfactory in the last eight years, especially in the year 2008-09. The

percentage shot up from 107.25% in 2007-08 to 277.71% in 2008-09. The

eight year average of more than 100% is highly comfortable. To the credit

of all the UCBs it must be stated that the ratio during 2008-09 is very high

i.e. 277.71% and it can be safely stated that the depositors‟ money is safe in

these UCBs.

143

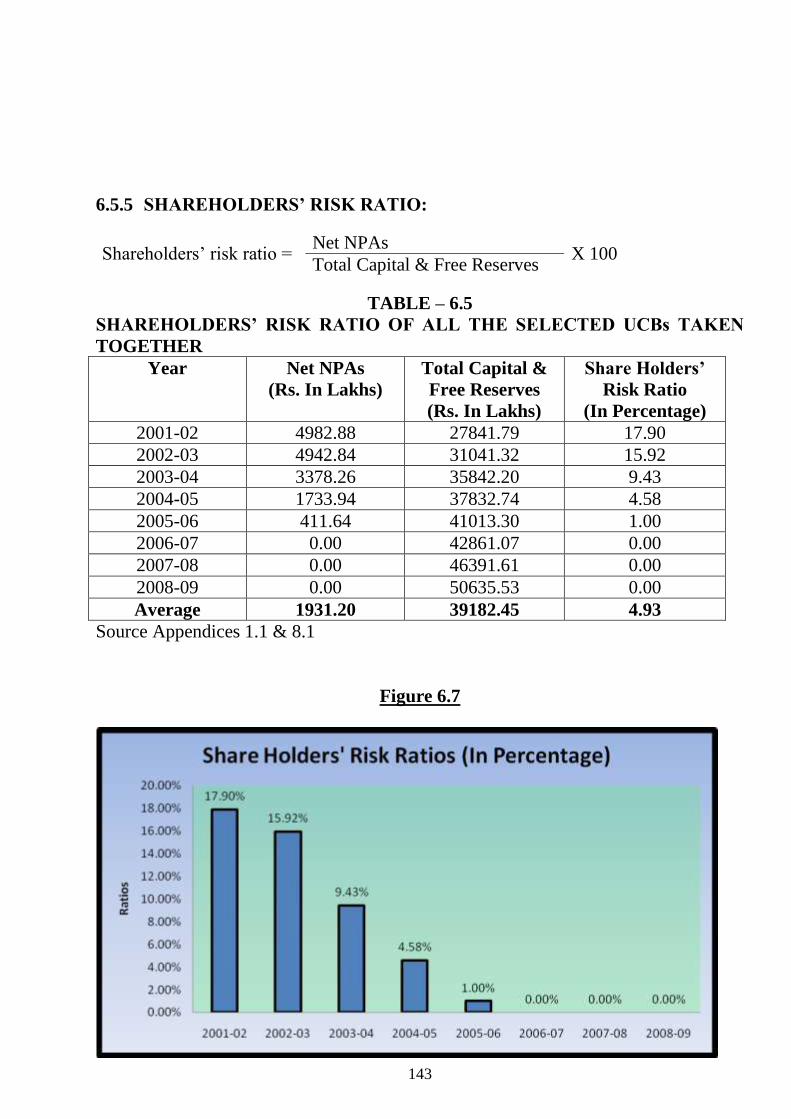

6.5.5 SHAREHOLDERS‟ RISK RATIO:

Shareholders‟ risk ratio = Net NPAs

X 100 Total Capital & Free Reserves

TABLE – 6.5

SHAREHOLDERS‟ RISK RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER

Year Net NPAs

(Rs. In Lakhs)

Total Capital &

Free Reserves

(Rs. In Lakhs)

Share Holders‟

Risk Ratio

(In Percentage)

2001-02 4982.88 27841.79 17.90

2002-03 4942.84 31041.32 15.92

2003-04 3378.26 35842.20 9.43

2004-05 1733.94 37832.74 4.58

2005-06 411.64 41013.30 1.00

2006-07 0.00 42861.07 0.00

2007-08 0.00 46391.61 0.00

2008-09 0.00 50635.53 0.00

Average 1931.20 39182.45 4.93

Source Appendices 1.1 & 8.1

Figure 6.7

144

Like depositors, the shareholders are also exposed to great risk if the

Net NPA is positive or more than zero. Hence it is necessary to see that the

shareholders‟ funds are safe in view of the NPA. So, this ratio becomes

important from the view point of the shareholders. From the table and graph

given above, we can see the position of the selected UCBs. A risk ratio is

resulted in the first five year and it is only due to The Sardar Bhiladwala

Pardi People‟s Co.Op. Bank Ltd. Which had failed in making provisions

against NPAs. However, it is a happy sign that the risk ratio in the last three

years is zero. As the Net NPA of all the banks taken together is zero in the

last three years, it is natural that the shareholders‟ risk ratio is also zero.

This signifies that the shareholders‟ funds in these banks are clearly safe.

145

6.5.6 TOTAL PROVISIONS RATIO:

Total Provisions Ratio = Total Provision

X 100 Gross NPAs

TABLE –6.6

TOTAL PROVISIONS RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER

Year Total Provisions

(Rs. In Lakhs)

Gross NPA

(Rs. In Lakhs)

Provision Ratio

(In Percentage)

2001-02 10660.25 15366.03 69.37

2002-03 12389.64 15481.22 80.03

2003-04 15292.62 14812.59 103.24

2004-05 16915.86 12685.02 133.35

2005-06 18282.75 10211.45 179.04

2006-07 18611.99 8773.16 212.15

2007-08 19009.99 8071.25 235.51

2008-09 17969.65 7132.11 251.95

Average 16141.59 11566.60 139.55

Source: Appendix 8.1

Figure 6.8

146

Since the publication of the Narsimham Committee

Report, the RBI published guidelines for making provisions against NPAs

for all banks, including Co. Op. banks. The total provisions against gross

NPAs must be such that its Net NPA comes to zero. It means that three

must be 100% provision, so that the above table, it is seen that all the

selected UCBs have made more than enough provisions for their gross

NPA. During the last eight years the provisions Ratio has been above 100%

expect in 2001-02 and 2002-03 due to The sardar Bhiladwala Pardi

People‟s Co.Op. Bank Ltd. This marks a very satisfactory position and it

signifies the satisfactory policy of the managements. It has even exceeded

the limits laid down by the RBI.

As per appendix 8.8 the gross NPA of The sardar

Bhiladwala Pardi People‟s Co.Op. Bank during 2001-02 to 2005-06 were

more than 40 to 50 percent of the total advances. But in the last three years

i.e. 2006-07 to 2008-09 the Net NPA is zero as enough provisions were

made against Gross NPA.

It should be noticed that in the last three years the

provision ratio has exceeded 200 percent which is a very positive sign.

147

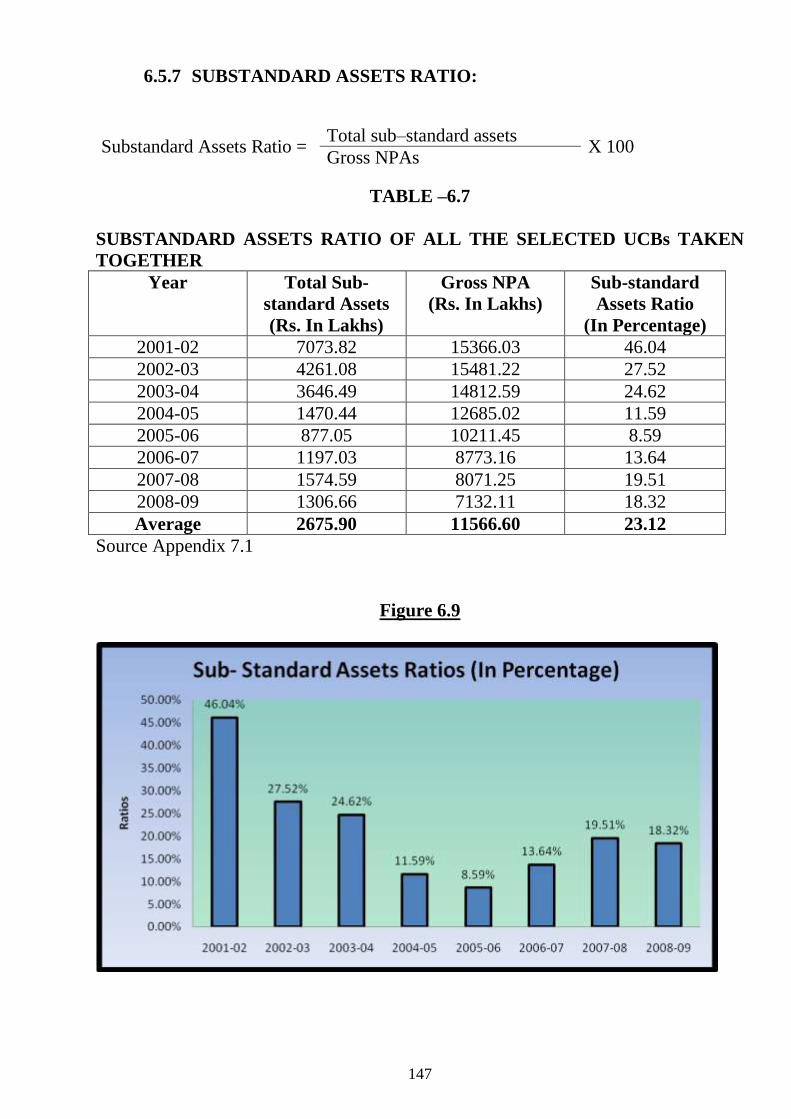

6.5.7 SUBSTANDARD ASSETS RATIO:

Substandard Assets Ratio = Total sub–standard assets

X 100 Gross NPAs

TABLE –6.7

SUBSTANDARD ASSETS RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER

Year Total Sub-

standard Assets

(Rs. In Lakhs)

Gross NPA

(Rs. In Lakhs)

Sub-standard

Assets Ratio

(In Percentage)

2001-02 7073.82 15366.03 46.04

2002-03 4261.08 15481.22 27.52

2003-04 3646.49 14812.59 24.62

2004-05 1470.44 12685.02 11.59

2005-06 877.05 10211.45 8.59

2006-07 1197.03 8773.16 13.64

2007-08 1574.59 8071.25 19.51

2008-09 1306.66 7132.11 18.32

Average 2675.90 11566.60 23.12

Source Appendix 7.1

Figure 6.9

148

The substandard assets ratio indicates the scope for

improvement in NPA. The higher the ratio, the better is position of

recovering the advances. From the above table and graph it is found that

ratio has been decreasing in the first five years of study and increased a

little in the last three years. The variations in the substandard assets ratio

are caused by the higher percentage of doubtful assets over sub standard

assets in some of the banks. The management should take necessary

measures to reduce doubtful assets and loss assets and to increase the

percentage of substandard assets.

149

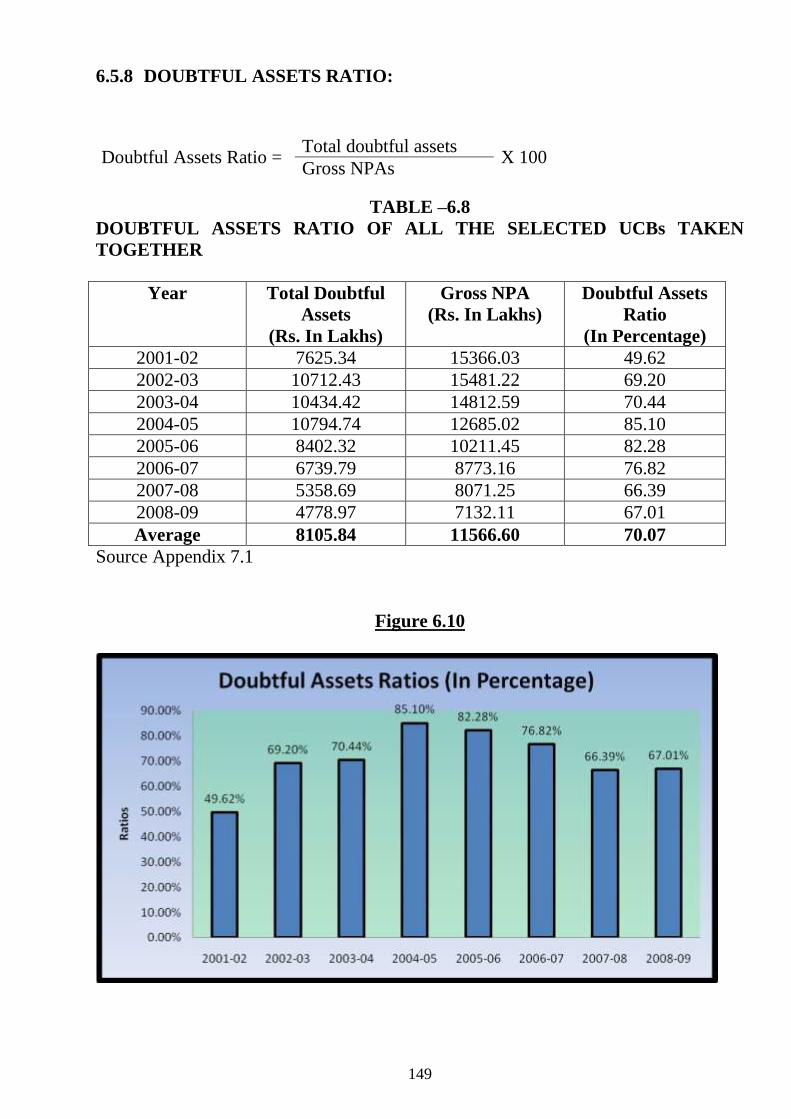

6.5.8 DOUBTFUL ASSETS RATIO:

Doubtful Assets Ratio = Total doubtful assets

X 100 Gross NPAs

TABLE –6.8

DOUBTFUL ASSETS RATIO OF ALL THE SELECTED UCBs TAKEN

TOGETHER

Year Total Doubtful

Assets

(Rs. In Lakhs)

Gross NPA

(Rs. In Lakhs)

Doubtful Assets

Ratio

(In Percentage)

2001-02 7625.34 15366.03 49.62

2002-03 10712.43 15481.22 69.20

2003-04 10434.42 14812.59 70.44

2004-05 10794.74 12685.02 85.10

2005-06 8402.32 10211.45 82.28

2006-07 6739.79 8773.16 76.82

2007-08 5358.69 8071.25 66.39

2008-09 4778.97 7132.11 67.01

Average 8105.84 11566.60 70.07

Source Appendix 7.1

Figure 6.10

150

The doubtful assets ratios of the selected UCBs taken together are

presented in the above table and graph. Banks can recover more of the

advances through compromise and that is the stage of compromise. The

doubtful assets ratio indicates the proportion of total doubtful assets to

gross NPAs. If the ratio is higher, there is more scope for compromising

and reducing NPAs. From the table we understand that the ratio had been

satisfactory except for three years i.e. 2004-05 (85.10%), 2005-06 (82.28%)

and 2006-07 (76.82%). Nevertheless, the doubtful assets ratio is less than

sub standard assets ratio which is a positive sign. The managements‟ must

try to recover as much doubtful advances as possible so that the Gross

NPAs are reduced.

151

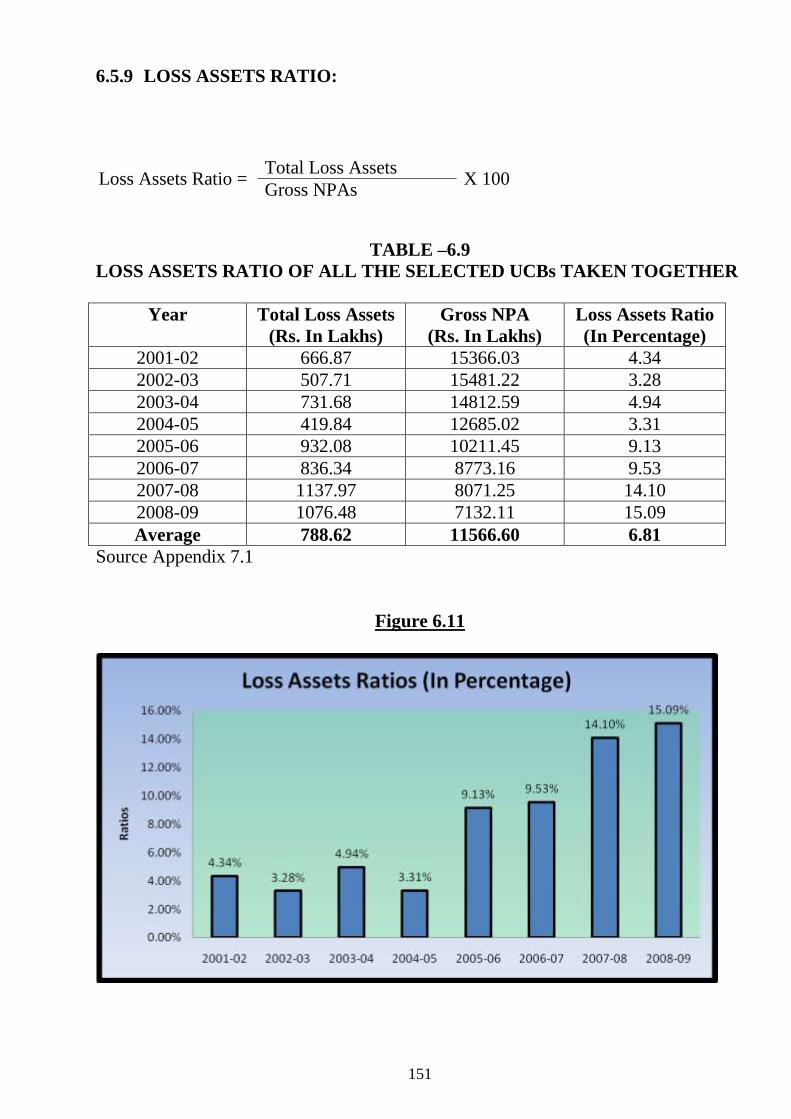

6.5.9 LOSS ASSETS RATIO:

Loss Assets Ratio = Total Loss Assets

X 100 Gross NPAs

TABLE –6.9

LOSS ASSETS RATIO OF ALL THE SELECTED UCBs TAKEN TOGETHER

Year Total Loss Assets

(Rs. In Lakhs)

Gross NPA

(Rs. In Lakhs)

Loss Assets Ratio

(In Percentage)

2001-02 666.87 15366.03 4.34

2002-03 507.71 15481.22 3.28

2003-04 731.68 14812.59 4.94

2004-05 419.84 12685.02 3.31

2005-06 932.08 10211.45 9.13

2006-07 836.34 8773.16 9.53

2007-08 1137.97 8071.25 14.10

2008-09 1076.48 7132.11 15.09

Average 788.62 11566.60 6.81

Source Appendix 7.1

Figure 6.11

152

Loss assets ratio shows the proportion of loss that the banks are

likely to suffer as compared to Gross NPAs. The ratio must be

minimum, as it will indicate that the assets to be lost would be lower

as compared to Gross NPAs. The loss assets are not likely to be

recovered at all and so a higher ratio would suggest higher losses.

From the above table it is understood that the loss assets ratio had

been very low in the first four years of study i.e. 2001-02 to 2004-05

(3.31%) but it increased in the next four years i.e. 2005-06 to 2008-09

(15.09%). The increase is due to the higher loss assets in The Sutex

Co. Op. Bank Ltd. (Appendix 7.3). The loss assets ratio in the

remaining nine banks is very satisfactory. The Sutex bank in question

should take its condition seriously and work out action plans to reduce

the loss assets ratio.

153

6.6 GENERAL CAUSES OF NON PERFORMING ASSETS

A bank with 100% performing assets is quite impossible as NPAs are sure to

occur at one stage or another. The causes of such NPAs are many which may be

broadly classified into three, viz. internal factors, external factors and internal and

external factors together.

INTERNAL FACTORS

The internal factors leading to NPAs may work at either institutional level or

borrower‟s level or both.

A. Institutional level:

The Institution‟s philosophy, its policy, procedure and people should be well co-

ordinated. Very often aggressive lending policy and absence of well designed

procedures for sanctioning advances result in high NPA levels. Before sanctioning

loans gathering, processing and analyzing information are at the heart of decision

making, failing which the bank‟s loan portfolio gets ruined. Appraisal deficiencies

have put many banks in difficult conditions. In addition, delays in sanctioning loans

and inappropriate repayment schedules worsen the situation. At post sanction stage

inappropriate disbursement and Lack of adequate supervision / monitoring develop

problems and losses. For example, sound loans at the initial stage are not good for any

bank.

Other Causes :

Credit concentration deficiency causes NPAs as lack of information regarding

repaid or growing areas for financing hinder accuracy. Secondly, credit process issues

like sanctioning advances under unsatisfactory terms, violating credit principles lead

to destruction of the bank. Over extension of credit to directors, large share holders

and lending under pressure from interested parties also cause trouble.

Technical in competence and lack of complacency also cause NPAs. Inadequate

supervision unfamiliar borrowers and dependence on oral information instead of

reliable complete financial data, optimistic interpretation of credit weakness are

dangerous.

154

Poor selection of risks involving highly leveraged loans to establish business

situation were bank financed share of required capitals is large related to the equity

investment of owners, may also cause unpleasant situation.

Lack of assessment of the credit worthiness of borrowers is get another reason

for high NPAs. Loans based on expectations of successful completions of business

rather than borrowers‟ creditworthiness are always at risk. Loans made because of

benefits such as large balance in deposits in a bank rather than on sound security or

collateral are also not advisable. Loans against problematic collaterals might also

cause NPAs. Liquidation of such collaterals and loans against collaterals without

adequate margin create hurdles for a bank.

B. Borrowers’ Level;

Project related problems, managerial aspects like failure in marketing,

inefficient management, labour problems and product obsolesces cause NPAs. Also,

financial indiscipline like diversion of funs for different purposes is another cause of

this situation.

EXTERNAL FACTORS

The external factors are those factors that lead advances into NPA beyond the

control of borrowers or institution i.e. banks. Such factors are natural calamities, state

of economy, recession or competition, trade policy, technological , advances,

regulatory advances , environmental pollution control requirements, lack of adequate

support from the legal system , loan waivers etc. These factors are not exhaustive but

inclusive. The factors that affect the NPAs would reflect in the policies of the bank

especially for lending, recovery management, monitoring and effective supervision. If

proper attention is not given to recovery Management of NPAs, banks will lose their

profitability and will not be able to satisfy its creditors and share holders.

The internal and external factors lending accounts to NPAs are enlisted below:

155

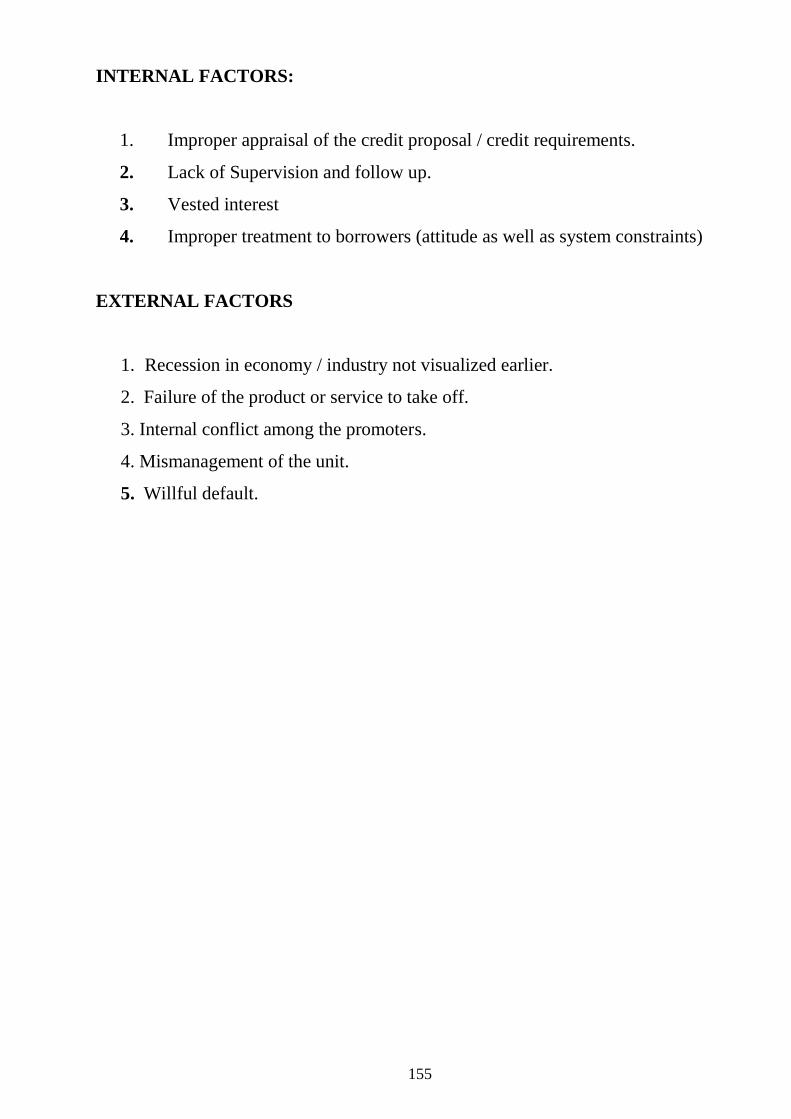

INTERNAL FACTORS:

1. Improper appraisal of the credit proposal / credit requirements.

2. Lack of Supervision and follow up.

3. Vested interest

4. Improper treatment to borrowers (attitude as well as system constraints)

EXTERNAL FACTORS

1. Recession in economy / industry not visualized earlier.

2. Failure of the product or service to take off.

3. Internal conflict among the promoters.

4. Mismanagement of the unit.

5. Willful default.