Embed Size (px)

Citation preview

Periodic Inventory Transactions

Periodic Inventory System

• Reminder: – Periodic Inventory System is when a business

counts their inventory once a fiscal period– Are more concerned with knowing the cost of

Purchases throughout a period– DOES NOT keep track of inventory throughout the

period

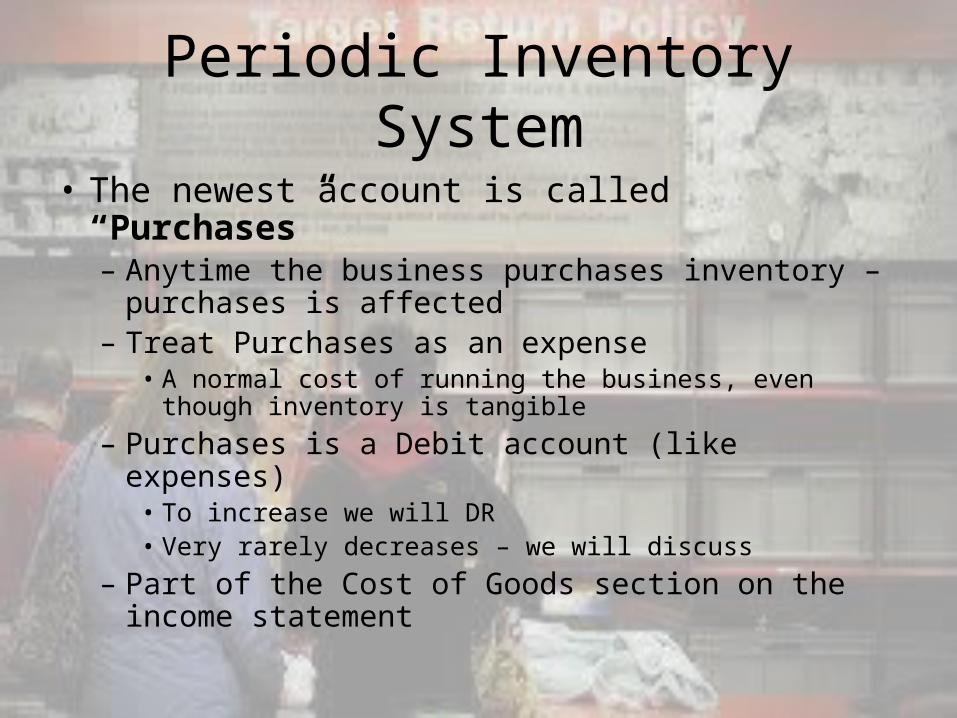

Periodic Inventory System

• The newest account is called “Purchases”– Anytime the business purchases inventory –

purchases is affected– Treat Purchases as an expense

• A normal cost of running the business, even though inventory is tangible

– Purchases is a Debit account (like expenses)• To increase we will DR• Very rarely decreases – we will discuss

– Part of the Cost of Goods section on the income statement

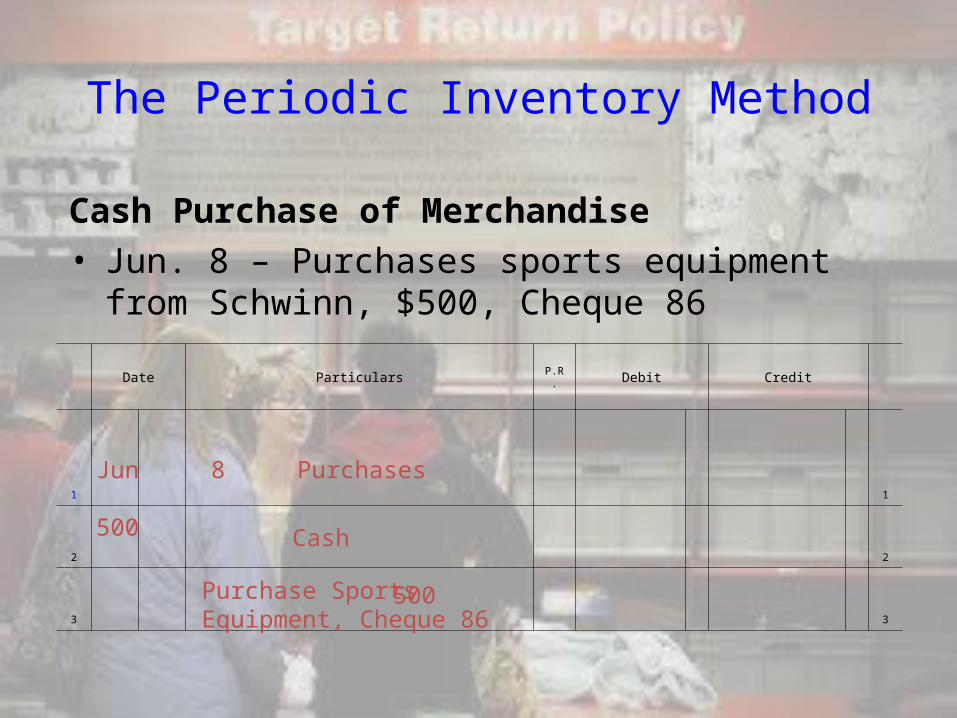

The Periodic Inventory Method

Cash Purchase of Merchandise• Jun. 8 – Purchases sports equipment from Schwinn,

$500, Cheque 86

Date Particulars P.R. Debit Credit

1 1

2 2

3 3

Jun 8 Purchases 500

Cash 500

Purchase Sports Equipment, Cheque 86

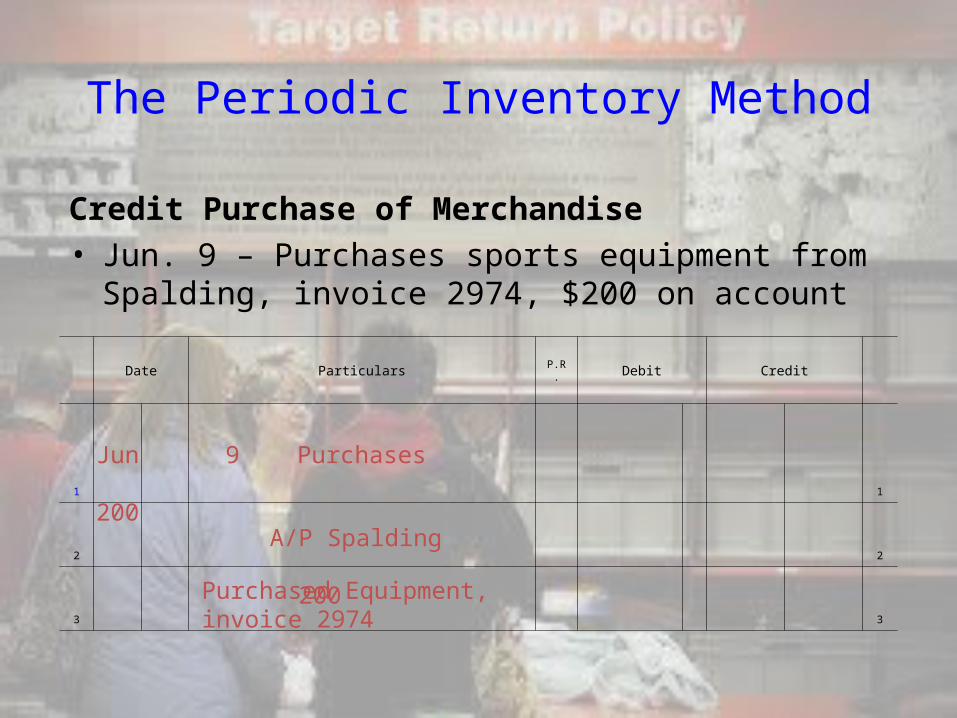

The Periodic Inventory Method

Credit Purchase of Merchandise• Jun. 9 – Purchases sports equipment from Spalding,

invoice 2974, $200 on account

Date Particulars P.R. Debit Credit

1 1

2 2

3 3

Jun 9 Purchases 200

A/P Spalding 200

Purchased Equipment, invoice 2974

Purchase Returns & Allowances

• As a consumer, you are well aware that we do not always keep everything we buy– Often it is necessary to return the goods for a

refund

• This occurs more often in business– Businesses purchase in much larger

quantities– Not uncommon to find a few

malfunctioning/errors in an order of an entire pallet, box, etc.

Purchase Returns & Allowances

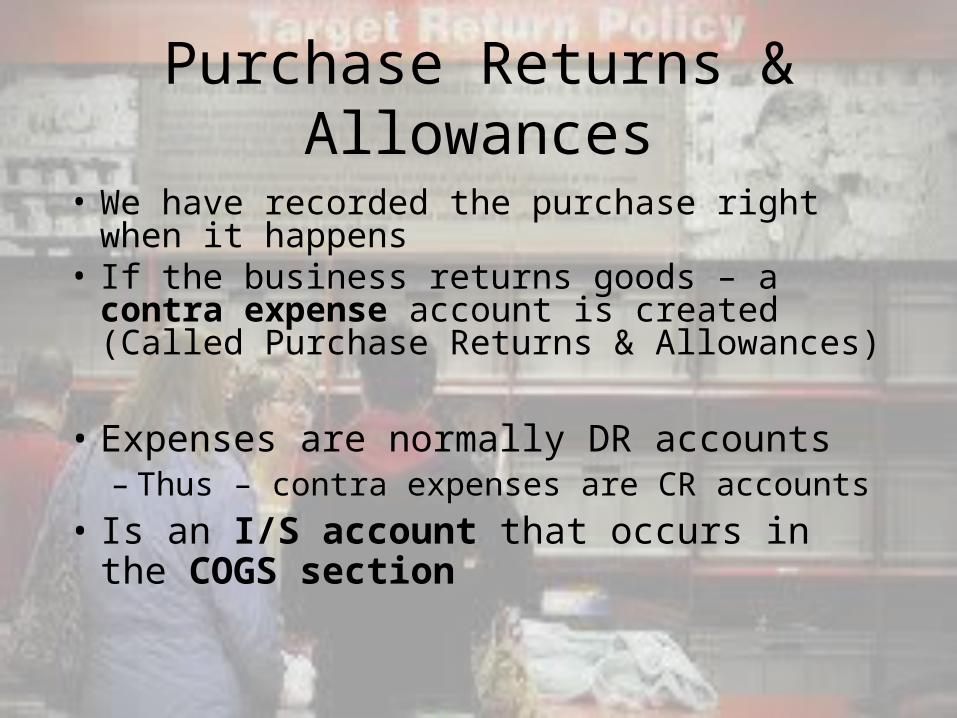

• We have recorded the purchase right when it happens

• If the business returns goods – a contra expense account is created (Called Purchase Returns & Allowances)

• Expenses are normally DR accounts– Thus – contra expenses are CR accounts

• Is an I/S account that occurs in the COGS section

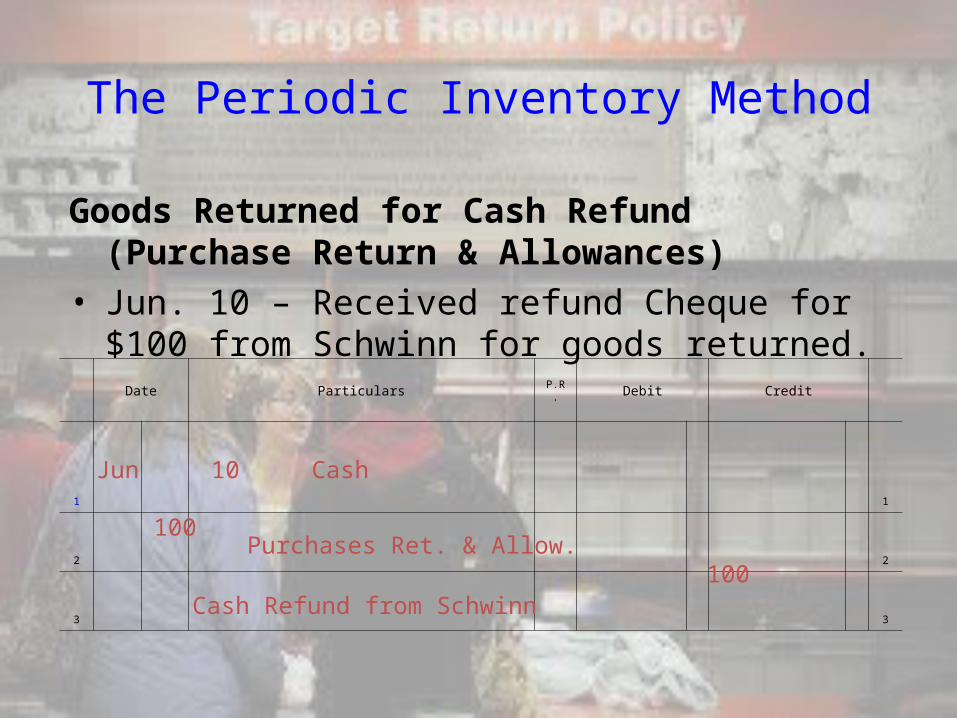

The Periodic Inventory Method

Goods Returned for Cash Refund (Purchase Return & Allowances)

• Jun. 10 – Received refund Cheque for $100 from Schwinn for goods returned.

Date Particulars P.R. Debit Credit

1 1

2 2

3 3

Jun 10 Cash 100

Purchases Ret. & Allow. 100

Cash Refund from Schwinn

The Periodic Inventory Method

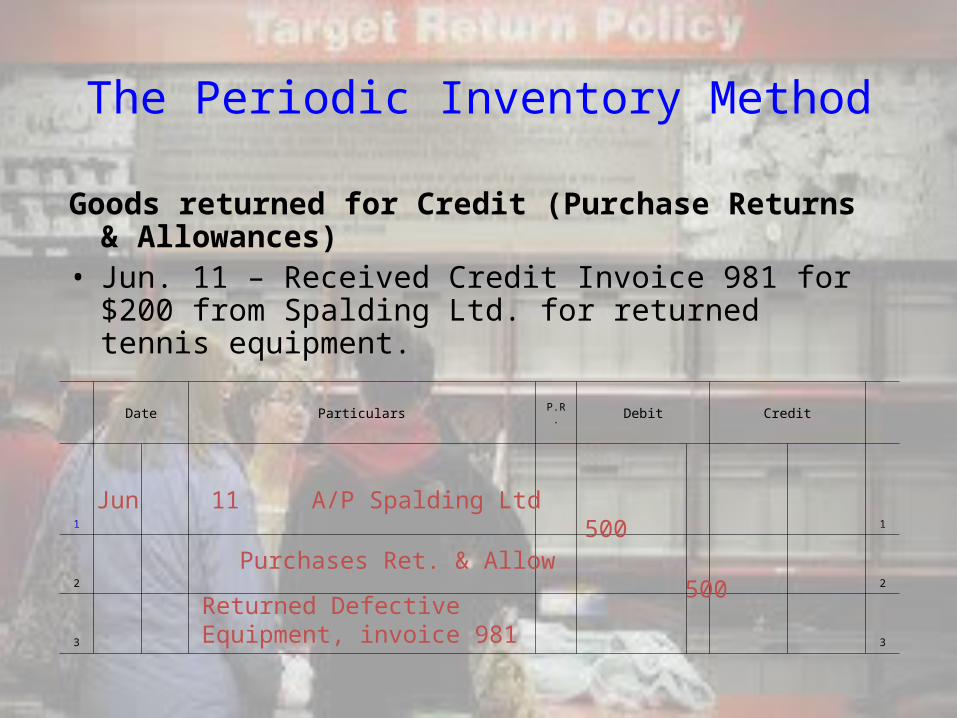

Goods returned for Credit (Purchase Returns & Allowances)

• Jun. 11 – Received Credit Invoice 981 for $200 from Spalding Ltd. for returned tennis equipment.

Date Particulars P.R. Debit Credit

1 1

2 2

3 3

Jun 11 A/P Spalding Ltd 500

Purchases Ret. & Allow 500

Returned Defective Equipment, invoice 981

Freight - In

• Often, a business has to pay for the shipping of the inventory to their location– Establishing an account called Freight In

• Does not always occur – is negotiated during the terms of purchase who is paying for the freight

• Freight – In is adds to the purchase cost– Thus, is a Debit account– Also, an I/S account that occurs in the COGS

section

The Periodic Inventory Method

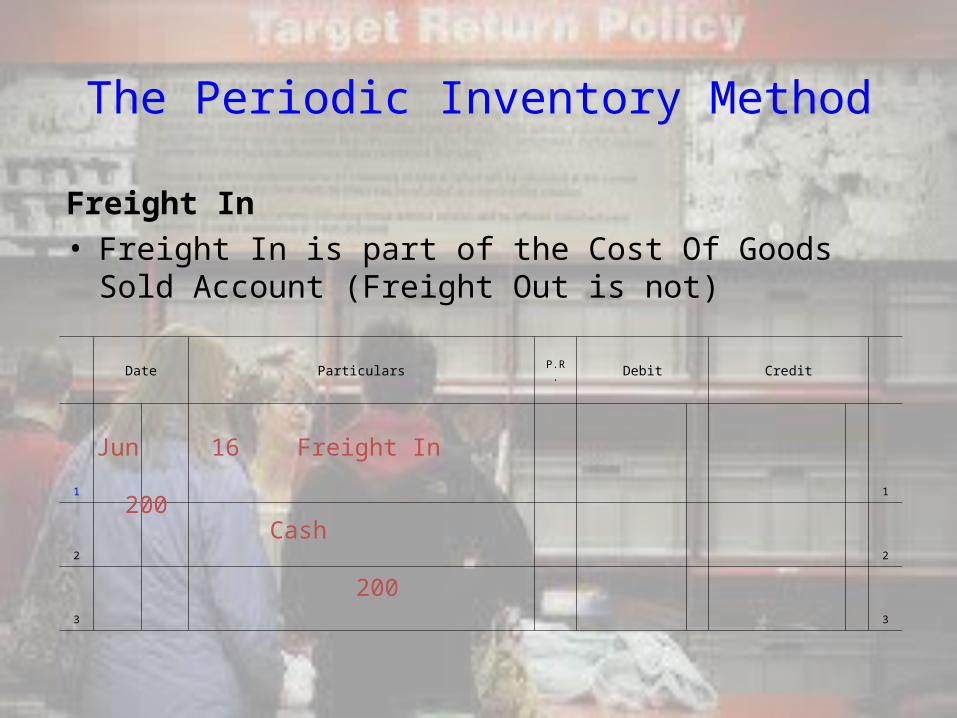

Freight In• Freight In is part of the Cost Of Goods Sold Account

(Freight Out is not)

Date Particulars P.R. Debit Credit

1 1

2 2

3 3

Jun 16 Freight In 200

Cash 200

The Merchandising CompanyNew Account Type of Account

1. Sales Revenue

2. Sales Discounts Contra-Revenue

3. Sales Returns & Allowances

Contra-Revenue

4. Purchases COGS (expense)

5. Purchase Discounts COGS (Contra-Expense)

6. Purchase Returns & Allowances

COGS (Contra-Expense)

7. Freight In COGS (expense)

The Merchandising Company

• Updated Chart of Accounts– Assets 100-199– Liabilities 200-299– Capital (including Drawings) 300-399– Revenues 400-499– COGS Expenses 500-599– Operating Expenses 600-699

Homework

• Page 311-312– 11a, 13

![Comparison of a Perpetual and PD Inventory Control System ...€¦ · system [13]. A perpetual inventory system is a superior to the older periodic inventory system because it keeps](https://img.pdfslide.net/doc/110x75/5f1838c412cfe1213e01342d/comparison-of-a-perpetual-and-pd-inventory-control-system-system-13-a-perpetual.jpg)