Embed Size (px)

DESCRIPTION

Personal Financial Services - Achieving growth. Peter Hawkins Head of Personal Financial Services 18 July 2000. Today’s agenda:. Specialisation and growth 1)Product businesses 2)New customer businesses 3)Tomorrow’s growth. 1) Specialist product businesses. Cards Mortgages - PowerPoint PPT Presentation

Citation preview

Personal Financial Services - Achieving growth

Peter HawkinsHead of Personal Financial Services

18 July 2000

Today’s agenda:

Specialisation and growth

1) Product businesses

2) New customer businesses

3) Tomorrow’s growth

– Cards

– Mortgages

– Funds Management and Insurance

– anz.com

1) Specialist product businesses

In November 1997 we separated product from distribution:

• It has delivered:

– Higher profits/ lower costs

– Strong individual product businesses

– Doubled sales

– 200,000 more customers

– Increased share of wallet

• More recently, customer segmentation was overlaid on distribution

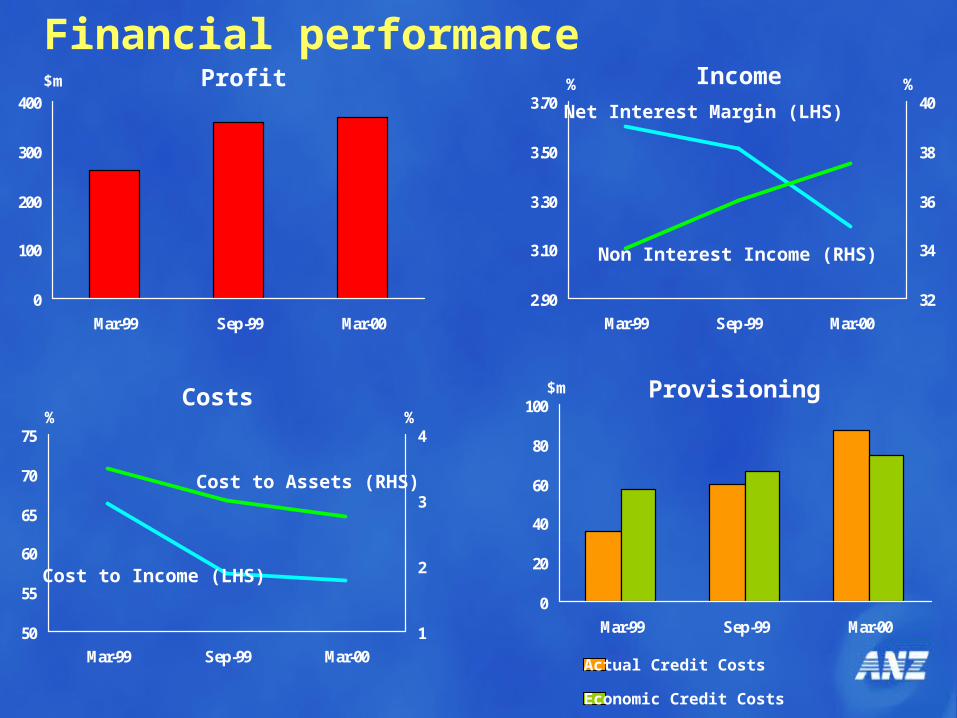

Financial performanceProfit

Costs

2.90

3.10

3.30

3.50

3.70

Mar-99 Sep-99 Mar-00

32

34

36

38

40Income% %

Net Interest Margin (LHS)

Non Interest Income (RHS)

50

55

60

65

70

75

Mar-99 Sep-99 Mar-00

1

2

3

4% %

Cost to Income (LHS)

Cost to Assets (RHS)

$m

Provisioning$m

0

20

40

60

80

100

Mar-99 Sep-99 Mar-00

Actual Credit Costs

Economic Credit Costs

0

100

200

300

400

Mar-99 Sep-99 Mar-00

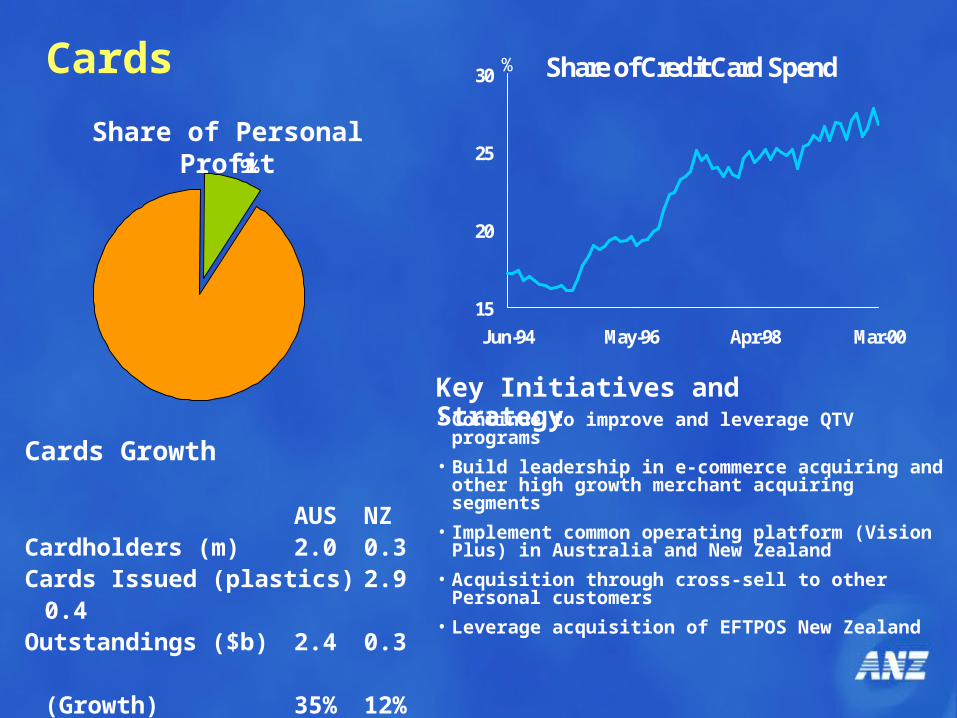

Cards Growth

AUS NZCardholders (m) 2.0 0.3Cards Issued (plastics) 2.9 0.4Outstandings ($b) 2.4 0.3 (Growth) 35% 12%

Share of Credit Card Spend

15

20

25

30

Jun-94 May-96 Apr-98 Mar-00

9%

Cards

Share of Personal Profit

%

• Continue to improve and leverage QTV programs

• Build leadership in e-commerce acquiring and other high growth merchant acquiring segments

• Implement common operating platform (Vision Plus) in Australia and New Zealand

• Acquisition through cross-sell to other Personal customers

• Leverage acquisition of EFTPOS New Zealand

Key Initiatives and Strategy

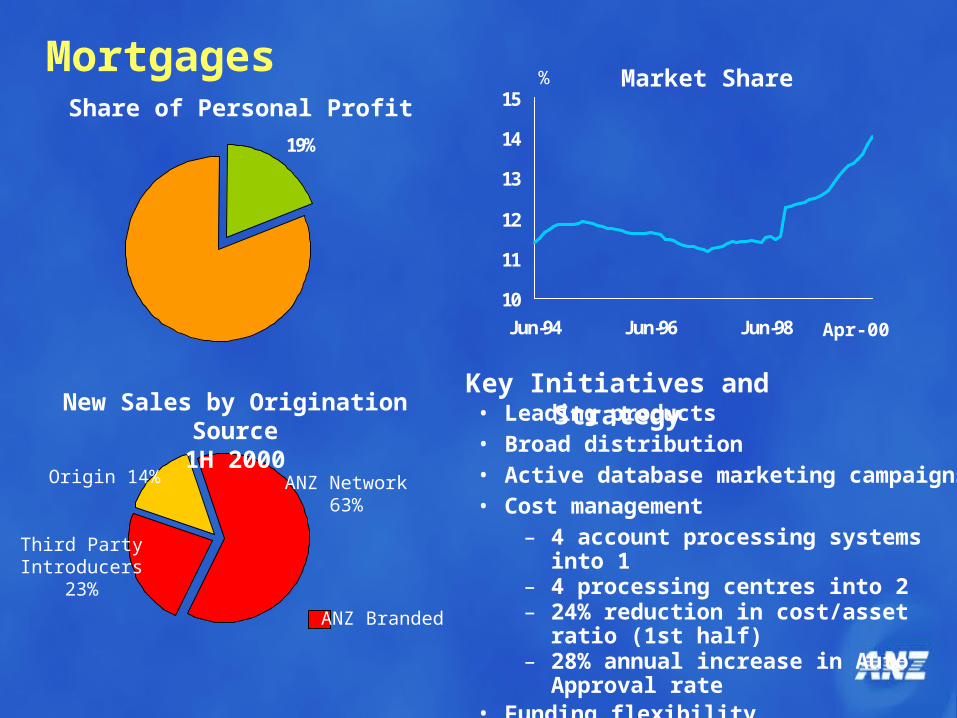

Mortgages

19%

Share of Personal Profit

New Sales by Origination Source1H 2000

Origin 14%

Third PartyIntroducers

23%

ANZ Network63%

• Leading products• Broad distribution• Active database marketing campaigns• Cost management

– 4 account processing systems into 1– 4 processing centres into 2– 24% reduction in cost/asset ratio (1st half)– 28% annual increase in Auto Approval rate

• Funding flexibility

Key Initiatives and Strategy

ANZ Branded

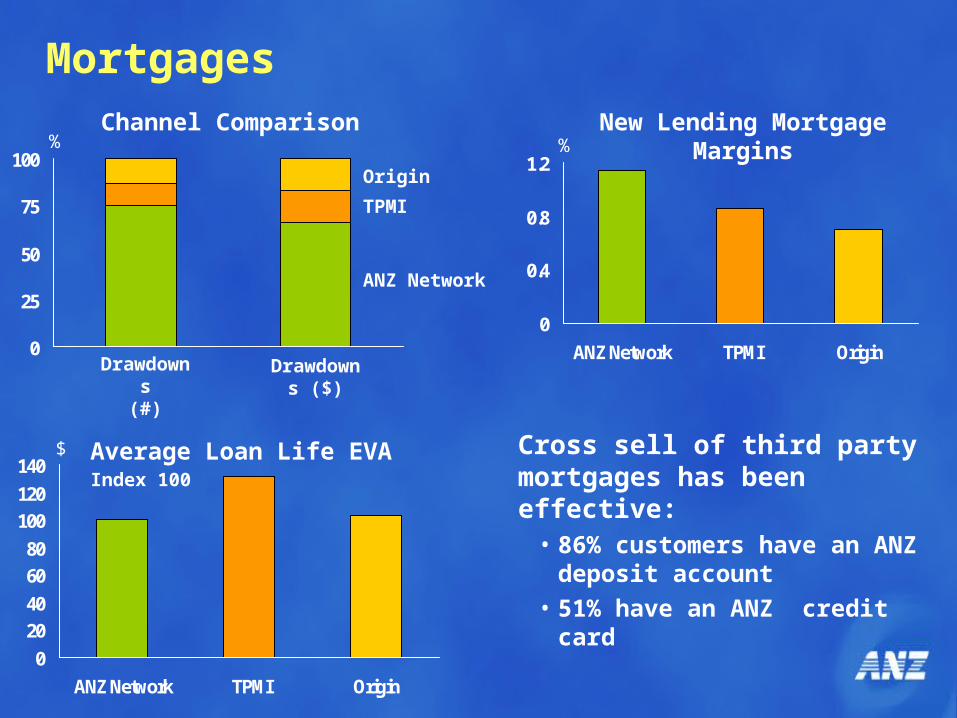

10

11

12

13

14

15

Jun-94 Jun-96 Jun-98

Market Share%

Apr-00

0

0.4

0.8

1.2

ANZ Network TPMI Origin

0

20

40

60

80

100

120

140

ANZ Network TPMI Origin

0

25

50

75

100

Cross sell of third party mortgages has been effective:

• 86% customers have an ANZ deposit account

• 51% have an ANZ credit card

MortgagesChannel Comparison New Lending Mortgage Margins

Average Loan Life EVA

ANZ Network

TPMI

Origin

Index 100

Drawdowns(#)

Drawdowns ($)

$

% %

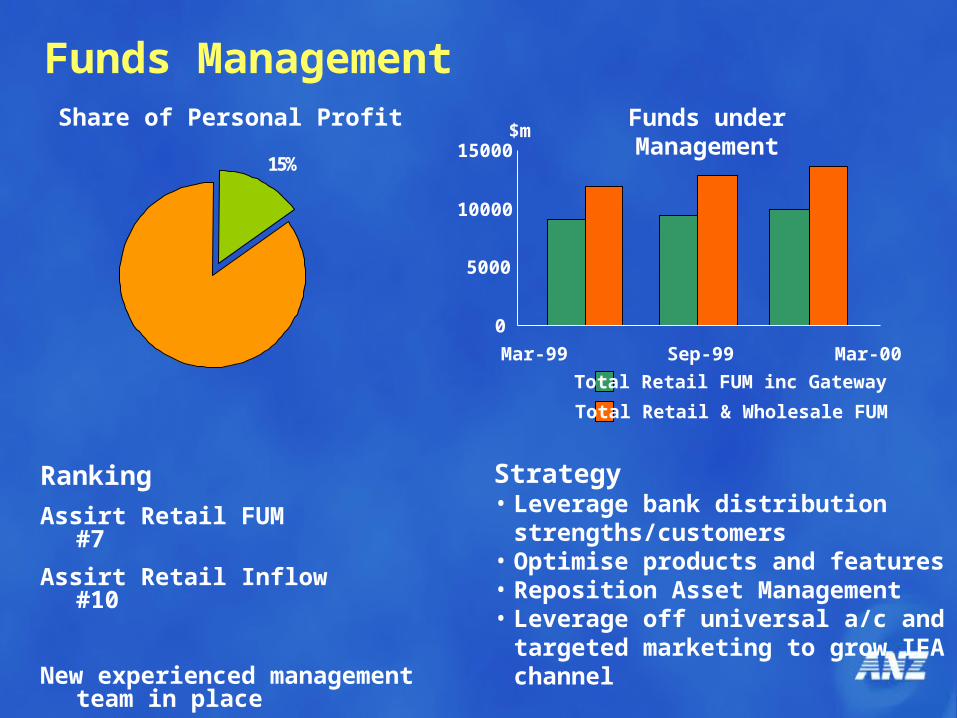

Funds Management

0

5000

10000

15000

Mar-99 Sep-99 Mar-00

Total Retail FUM inc Gateway

Total Retail & Wholesale FUM

Ranking

Assirt Retail FUM #7

Assirt Retail Inflow #10

New experienced management team in place

Strategy• Leverage bank distribution

strengths/customers• Optimise products and features• Reposition Asset Management• Leverage off universal a/c and targeted

marketing to grow IFA channel

Funds under Management$m

Share of Personal Profit

15%

0

10

20

30

40

Oct-99 Feb-00 Jun-00

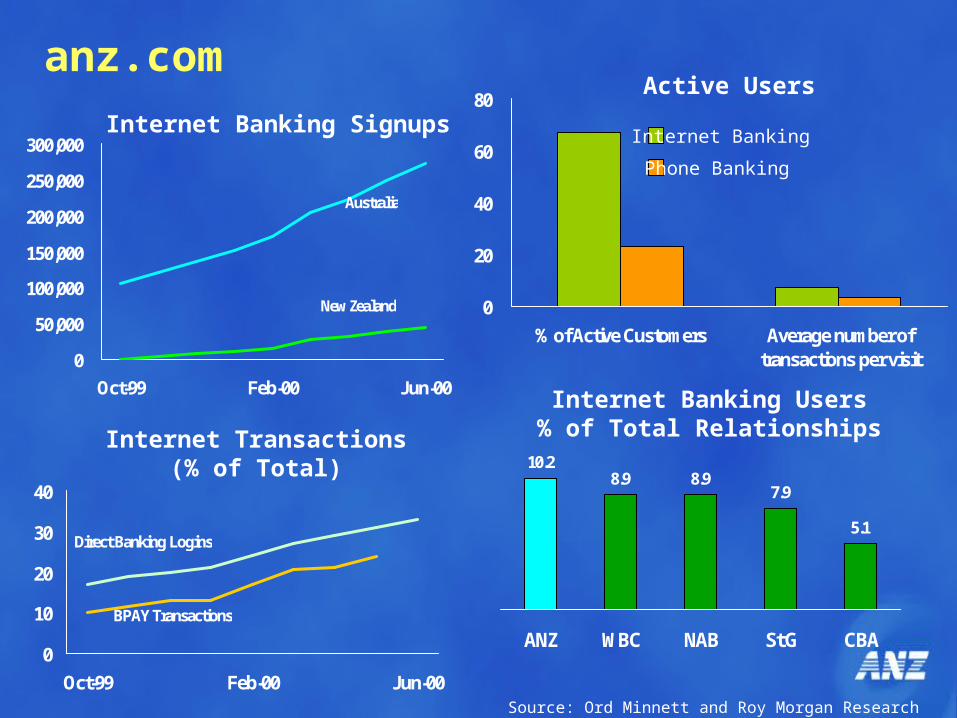

BPAY Transactions

Direct Banking Logins

Internet Transactions(% of Total)

0

50,000

100,000

150,000

200,000

250,000

300,000

Oct-99 Feb-00 Jun-00

Australia

New Zealand 0

20

40

60

80

% of Active Customers Average number oftransactions per visit

10.28.9 8.9

7.9

5.1

ANZ WBC NAB St G CBA

Source: Ord Minnett and Roy Morgan Research

anz.com

Internet Banking Signups Internet Banking

Phone Banking

Active Users

Internet Banking Users% of Total Relationships

0

100

200

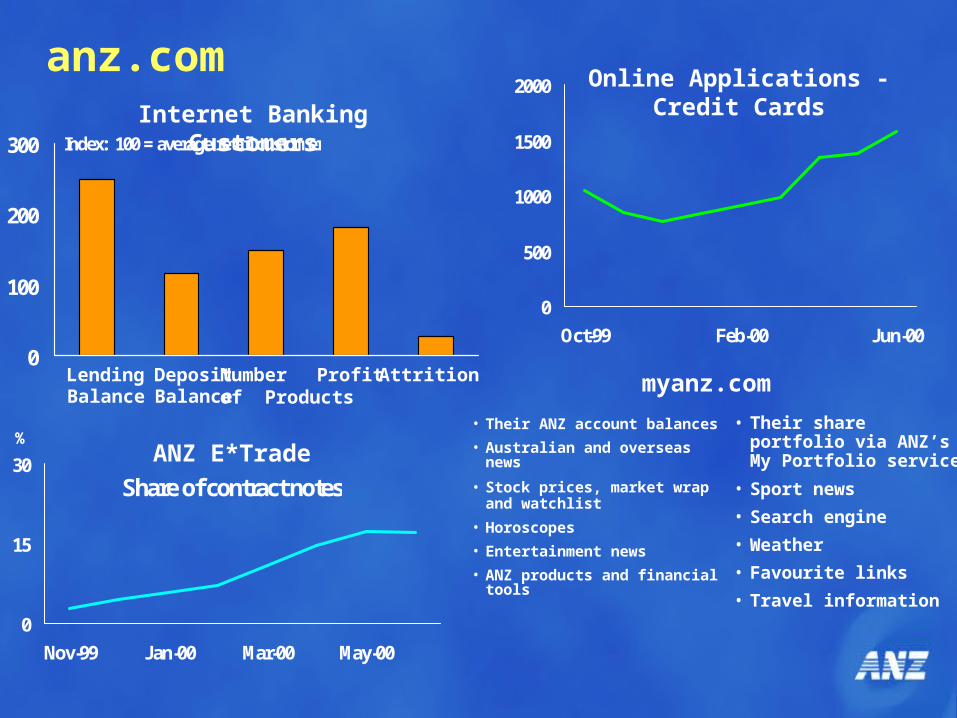

300 Index: 100 = average retail customer

Number of Products

0

15

30

Nov-99 Jan-00 Mar-00 May-00

%

Share of contract notes

0

500

1000

1500

2000

Oct-99 Feb-00 Jun-00

anz.com

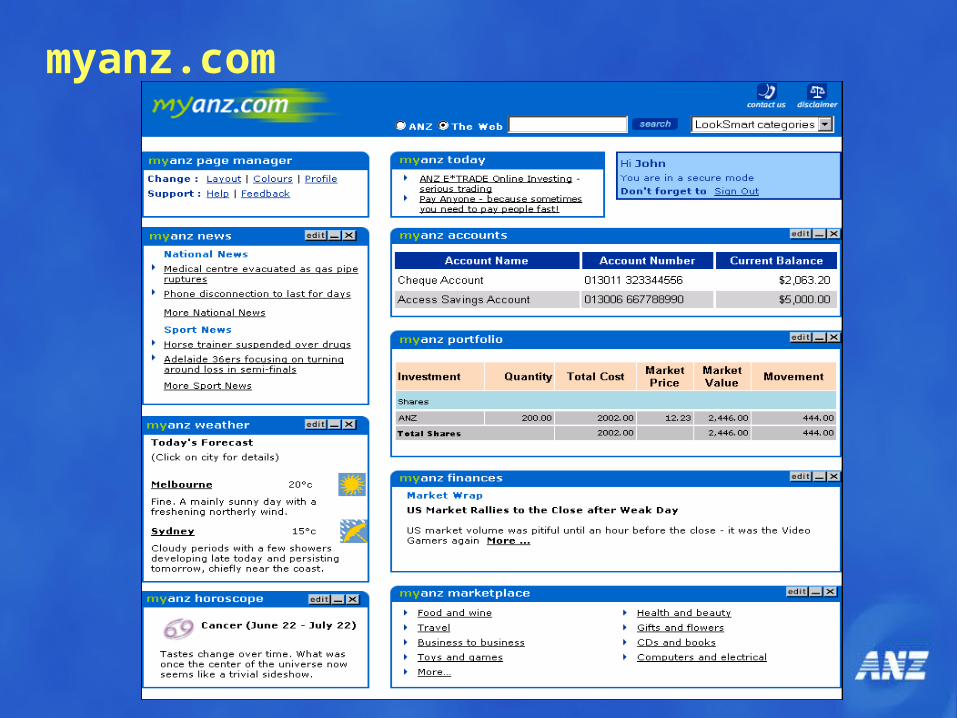

myanz.com

ANZ E*Trade

Online Applications - Credit Cards

LendingBalance

DepositBalance

Profit Attrition

Internet Banking Customers

• Their ANZ account balances

• Australian and overseas news

• Stock prices, market wrap and watchlist

• Horoscopes

• Entertainment news

• ANZ products and financial tools

• Their share portfolio via ANZ’s My Portfolio service

• Sport news

• Search engine

• Weather

• Favourite links

• Travel information

myanz.com

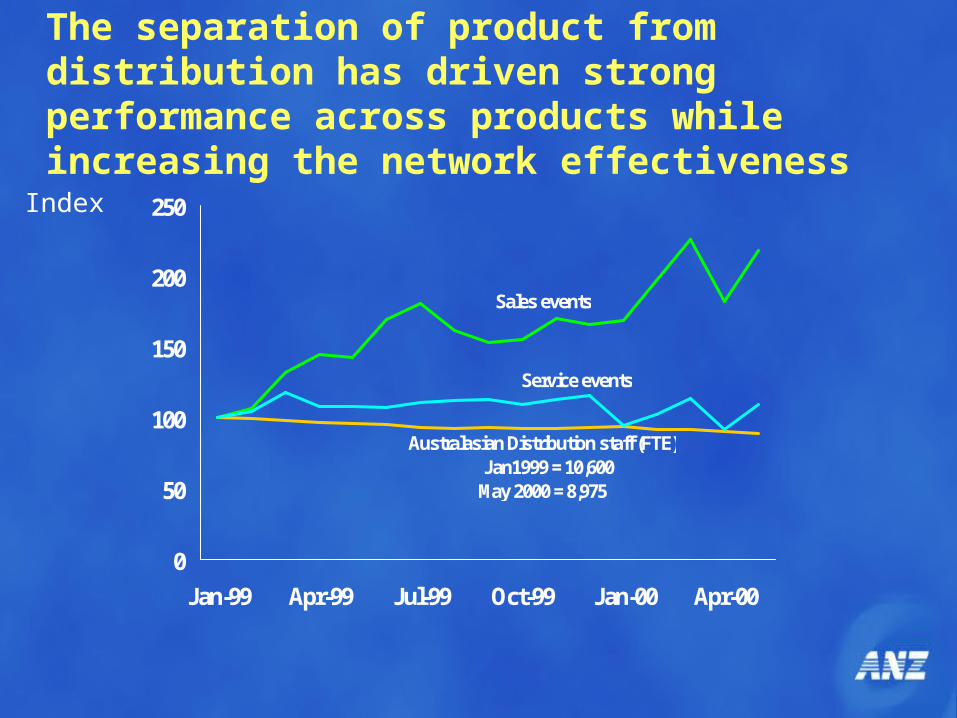

The separation of product from distribution has driven strong performance across products while increasing the network effectiveness

0

50

100

150

200

250

Jan-99 Apr-99 Jul-99 Oct-99 Jan-00 Apr-00

Sales events

Service events

Australasian Distribution staff (FTE) Jan1999 = 10,600 May 2000 = 8,975

Index

– Wealth Management

– Small Business

– General Banking

2) New customer businesses

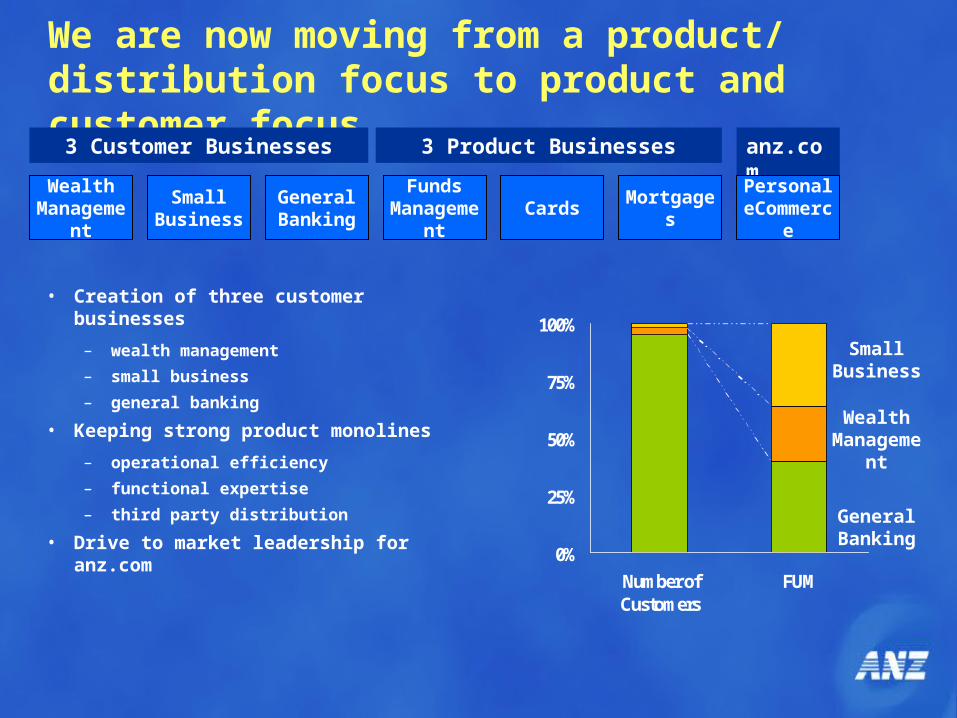

We are now moving from a product/ distribution focus to product and customer focus

• Creation of three customer businesses

– wealth management

– small business

– general banking

• Keeping strong product monolines

– operational efficiency

– functional expertise

– third party distribution

• Drive to market leadership for anz.com

Cards MortgagesWealth

ManagementSmall

BusinessGeneral Banking

3 Product Businesses3 Customer Businesses

Funds Management

anz.com

Personal eCommerce

General Banking

Wealth Management

Small Business

0%

25%

50%

75%

100%

Number ofCustomers

FUM

Develop a Wealth Management offer that will truly differentiate us

Strategy

• Schwab-like offer, but with higher level of lending

• extensive third party offering for FM & I, in addition to proprietary FM product

• heavily bricks-and-clicks

• underpinned by Universal Account CMA

• offers customers choice from a menu of options

– advice– product – value

14%Share of Personal Profit

05

1015202530354045

Sep-97 Jun-98 Mar-99 Dec-99

CBA

WestpacANZNAB

St George

Share of High Net Worth Customers

Source: Roy Morgan Research

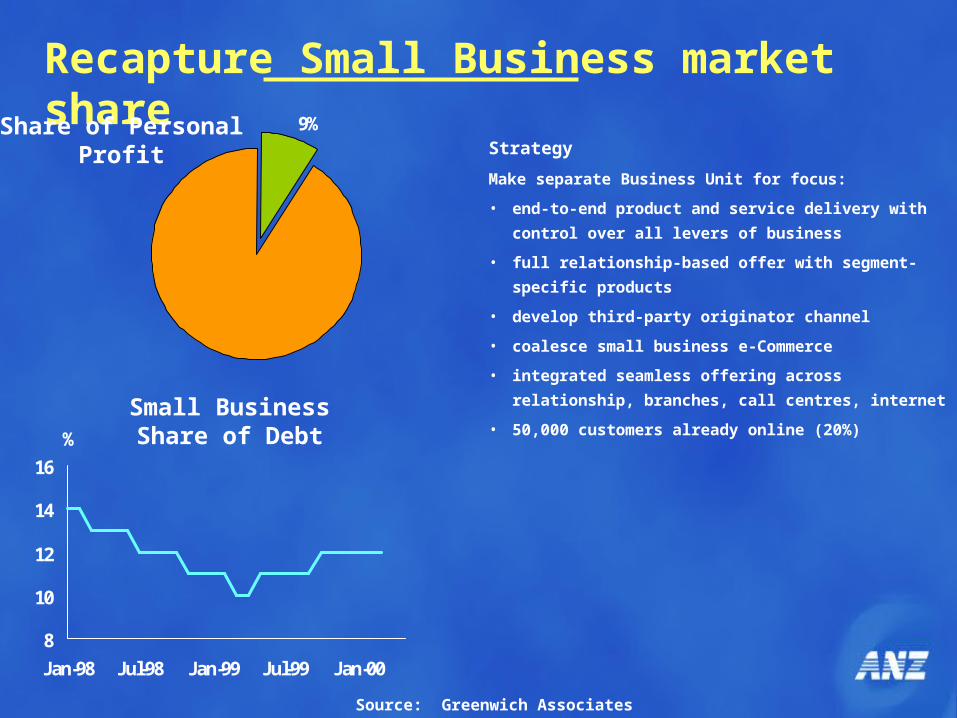

Recapture Small Business market share

Strategy

Make separate Business Unit for focus:

• end-to-end product and service delivery with control over

all levers of business

• full relationship-based offer with segment-specific products

• develop third-party originator channel

• coalesce small business e-Commerce

• integrated seamless offering across relationship, branches,

call centres, internet

• 50,000 customers already online (20%)

8

10

12

14

16

Jan-98 Jul-98 Jan-99 Jul-99 Jan-00

%

Small Business Share of Debt

9%Share of Personal Profit

Source: Greenwich Associates

0

2

4

6

8

10

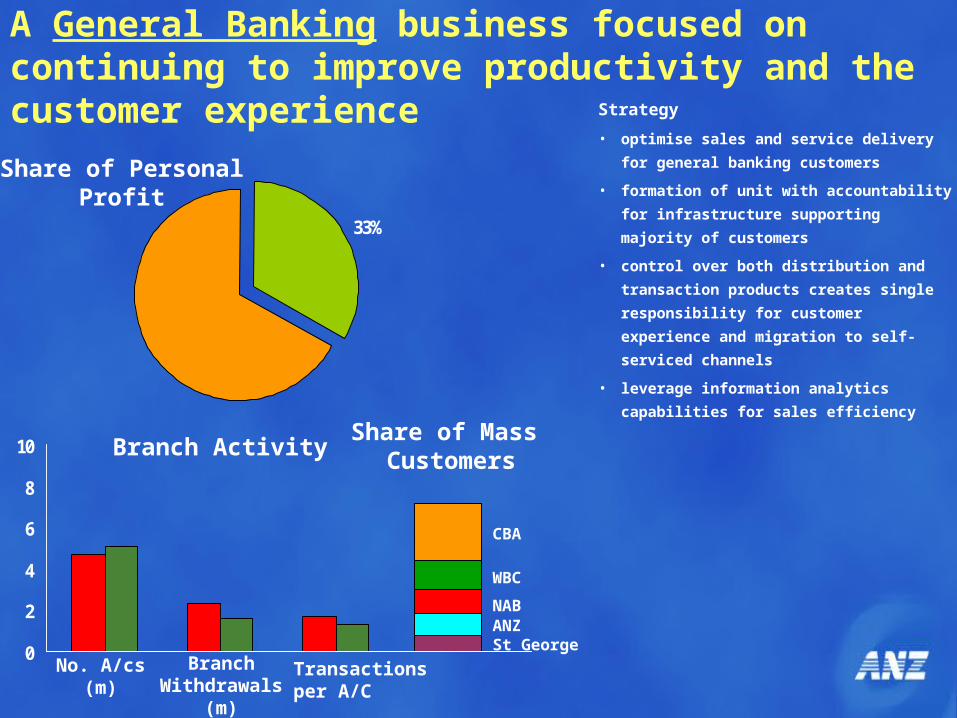

A General Banking business focused on continuing to improve productivity and the customer experience

Strategy

• optimise sales and service delivery for general

banking customers

• formation of unit with accountability for

infrastructure supporting majority of customers

• control over both distribution and transaction

products creates single responsibility for

customer experience and migration to self-

serviced channels

• leverage information analytics capabilities for

sales efficiency

Branch Activity

33%

Share of Personal Profit

No. A/cs(m)

BranchWithdrawals (m)

Transactionsper A/C

Share of Mass Customers

NAB

WBC

CBA

St GeorgeANZ

– Building capabilities

3) Tomorrow’s growth

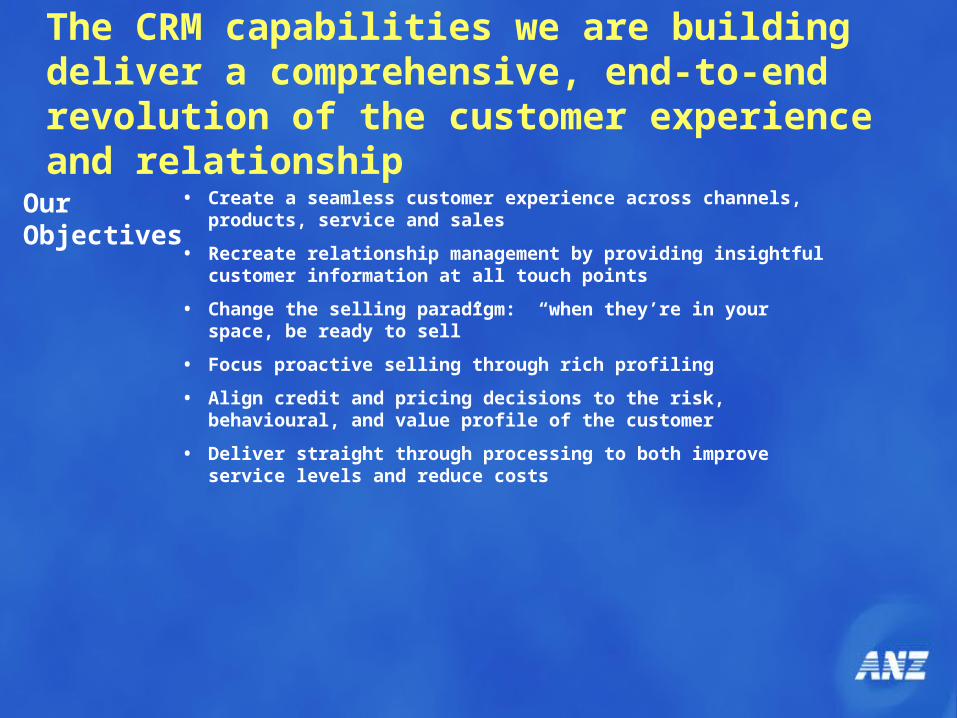

The CRM capabilities we are building deliver a comprehensive, end-to-end revolution of the customer experience and relationship

• Create a seamless customer experience across channels, products, service and sales

• Recreate relationship management by providing insightful customer information at all touch points

• Change the selling paradigm: “when they’re in your space, be ready to sell”

• Focus proactive selling through rich profiling

• Align credit and pricing decisions to the risk, behavioural, and value profile of the customer

• Deliver straight through processing to both improve service levels and reduce costs

OurObjectives

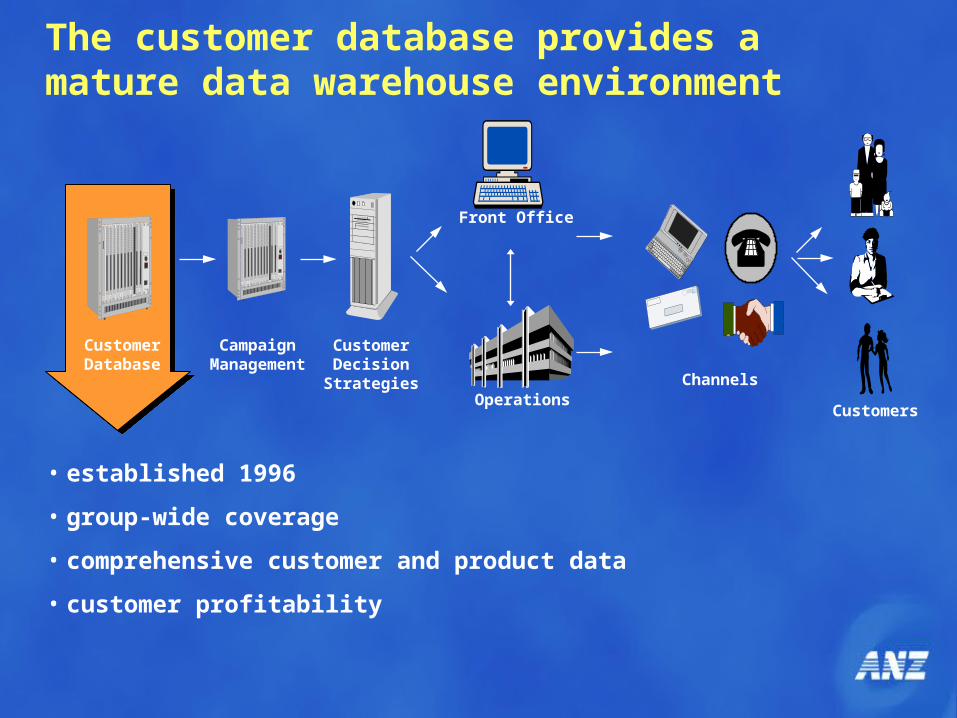

The customer database provides a mature data warehouse environment

• established 1996

• group-wide coverage

• comprehensive customer and product data

• customer profitability

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

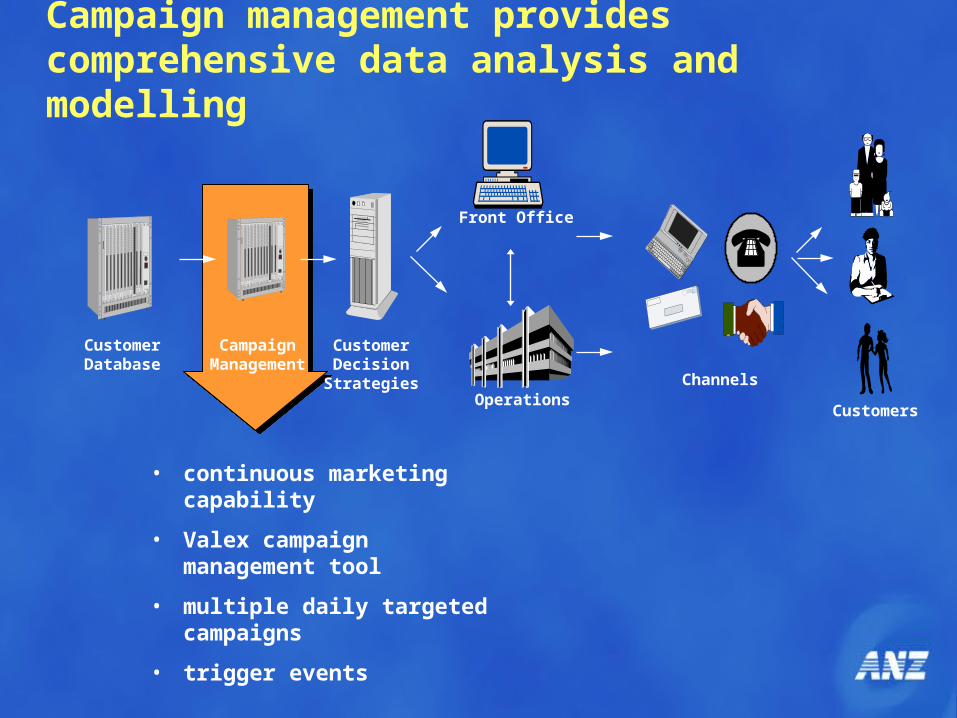

Campaign management provides comprehensive data analysis and modelling

• continuous marketing capability

• Valex campaign management tool

• multiple daily targeted campaigns

• trigger events

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

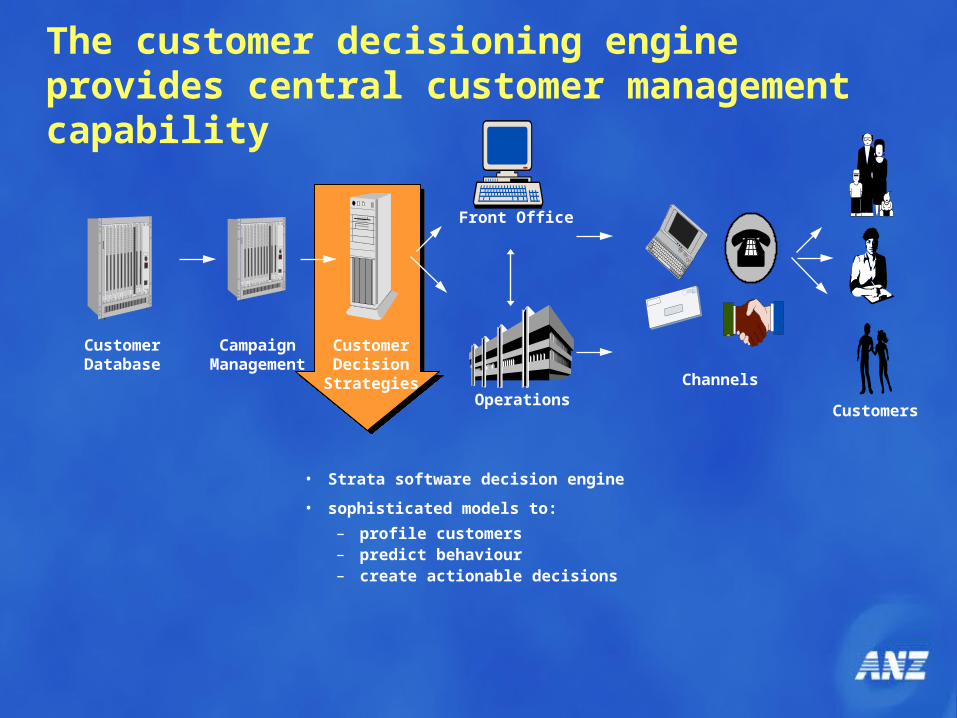

The customer decisioning engine provides central customer management capability

• Strata software decision engine

• sophisticated models to:

– profile customers– predict behaviour– create actionable decisions

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

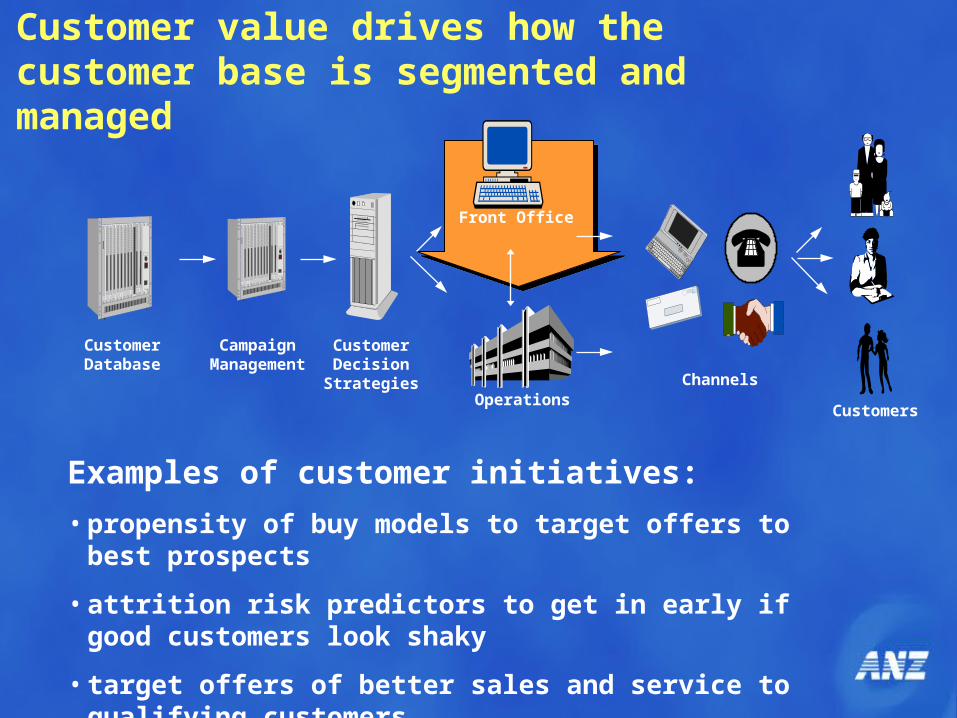

Examples of customer initiatives:

• propensity of buy models to target offers to best prospects

• attrition risk predictors to get in early if good customers look shaky

• target offers of better sales and service to qualifying customers

Customer value drives how the customer base is segmented and managed

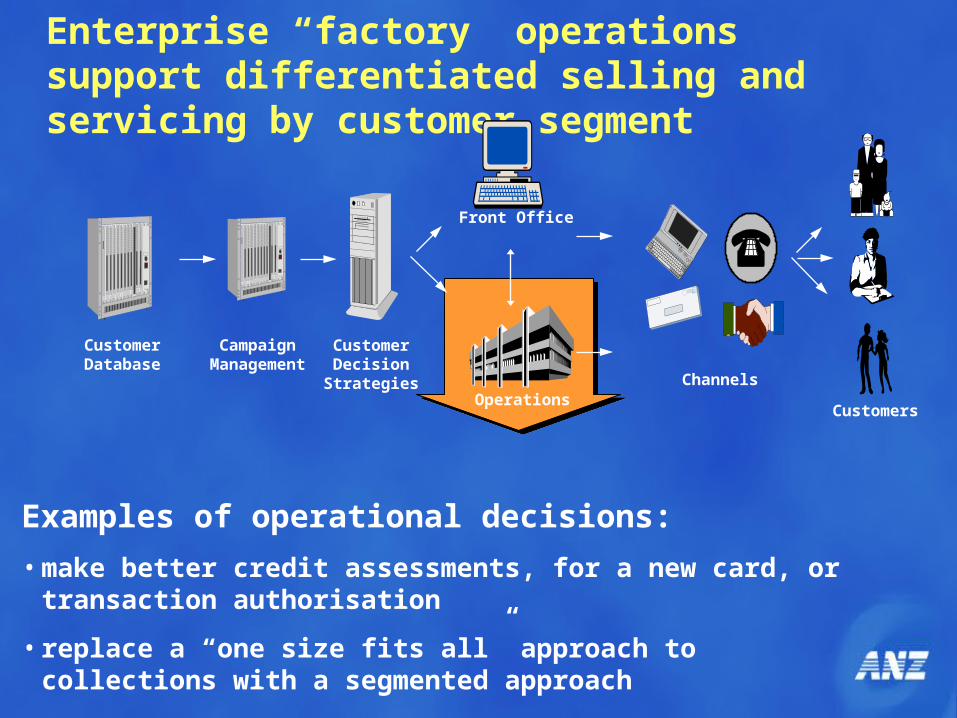

Enterprise “factory” operations support differentiated selling and servicing by customer segment

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

Examples of operational decisions:

• make better credit assessments, for a new card, or transaction authorisation

• replace a “one size fits all” approach to collections with a segmented approach

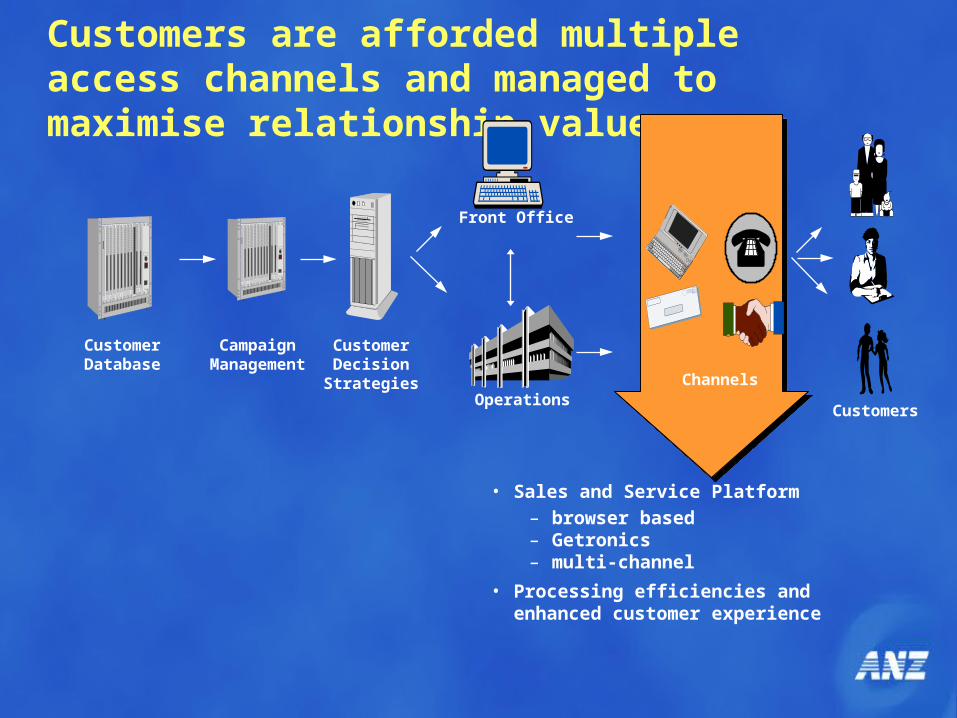

Customers are afforded multiple access channels and managed to maximise relationship value

• Sales and Service Platform – browser based – Getronics– multi-channel

• Processing efficiencies and enhanced customer experience

CampaignManagement

CustomerDecision

Strategies

Front Office

Customers

Customer Database

OperationsChannels

This is a substantial program which will deliver end-to-end transformation

• reengineering and automating servicing and credit fulfilment processes

• total capital investment in excess of $200 million

• deployment of over $100 million in improved infrastructure to deliver a paperless environment– communications bandwidth to branches– specialist peripherals such as scanners– high performance workstations at all touchpoints– windows 2000– middleware

• payback of about 2 years

• sales uplift of 5% in business case– other organisations have experienced up to 25% uplift

• implementation begins November 2000, completed by end 2001

Summary: Personal Financial Services

• Specialist Product Businesses well established

• Customer Businesses being elevated

• Capabilities being built to drive tomorrow’s growth