Embed Size (px)

Citation preview

Peruvian economic outlook and investment opportunities

Javier Correa Merchan Director, Investment Promotion Division Proinversión

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

Peru: Geography

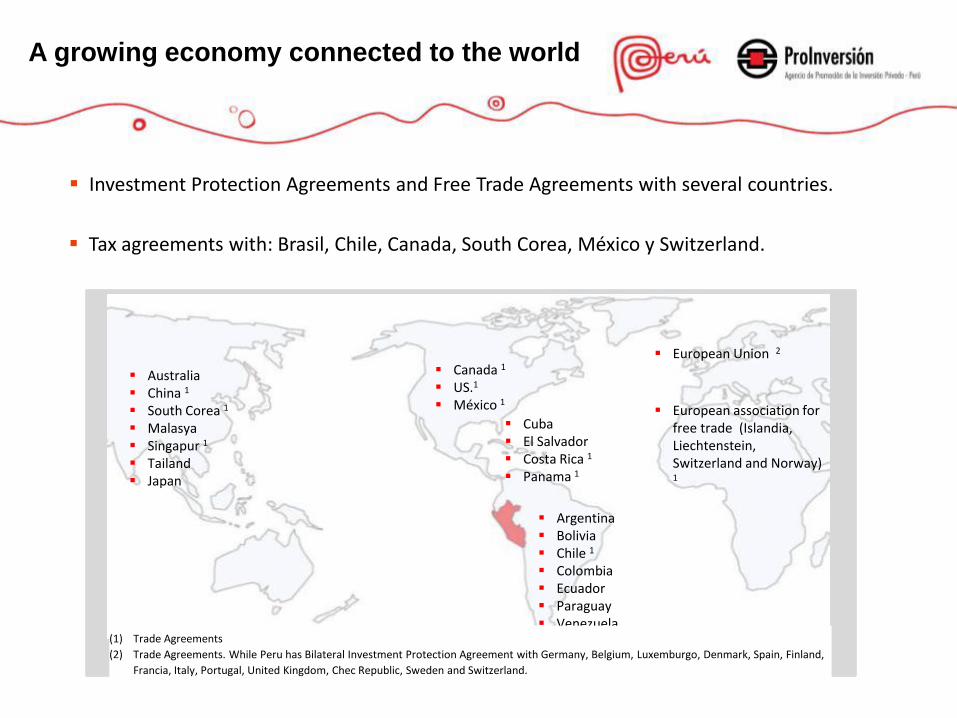

A growing economy connected to the world

Investment Protection Agreements and Free Trade Agreements with several countries.

Australia China 1

South Corea 1

Malasya Singapur 1 Tailand Japan

Argentina Bolivia Chile 1 Colombia Ecuador Paraguay Venezuela

Cuba El Salvador Costa Rica 1

Panama 1

European Union 2

European association for

free trade (Islandia, Liechtenstein, Switzerland and Norway)

1

Canada 1 US.1

México 1

(1) Trade Agreements

(2) Trade Agreements. While Peru has Bilateral Investment Protection Agreement with Germany, Belgium, Luxemburgo, Denmark, Spain, Finland,

Francia, Italy, Portugal, United Kingdom, Chec Republic, Sweden and Switzerland.

Tax agreements with: Brasil, Chile, Canada, South Corea, México y Switzerland.

2,353

1,283

540 385

258 206 203 44

202.77

119.72

47.66 41.96 31.42 30.46

17.82 3.93

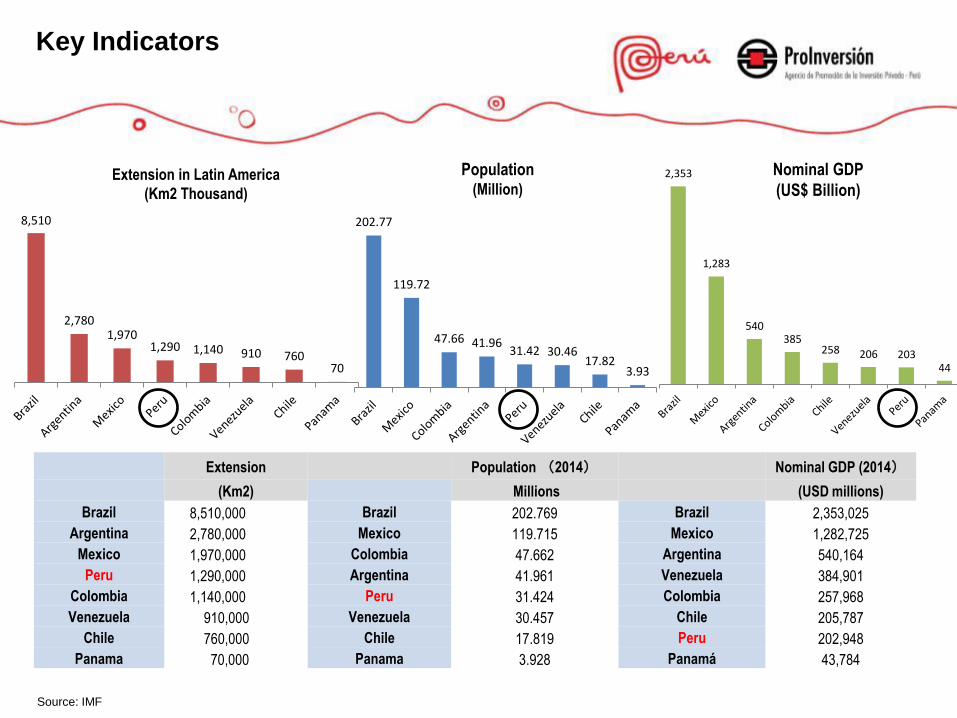

Key Indicators

Extension Population (2014) Nominal GDP (2014)

(Km2) Millions (USD millions)

Brazil 8,510,000 Brazil 202.769 Brazil 2,353,025

Argentina 2,780,000 Mexico 119.715 Mexico 1,282,725

Mexico 1,970,000 Colombia 47.662 Argentina 540,164

Peru 1,290,000 Argentina 41.961 Venezuela 384,901

Colombia 1,140,000 Peru 31.424 Colombia 257,968

Venezuela 910,000 Venezuela 30.457 Chile 205,787

Chile 760,000 Chile 17.819 Peru 202,948

Panama 70,000 Panama 3.928 Panamá 43,784

Nominal GDP

(US$ Billion)

Population

(Million) Extension in Latin America

(Km2 Thousand)

8,510

2,780 1,970

1,290 1,140 910 760 70

Source: IMF

Investm

ent a

s %

of G

DP

27,2

20,4 19,918,4

13,9 13,5

0

5

10

15

20

25

30

Chile México Colombia Brasil Perú Uruguay

26,825,0

23,122,2 21,9

17,0

0

5

10

15

20

25

30

Perú Colombia Uruguay Chile México Brasil

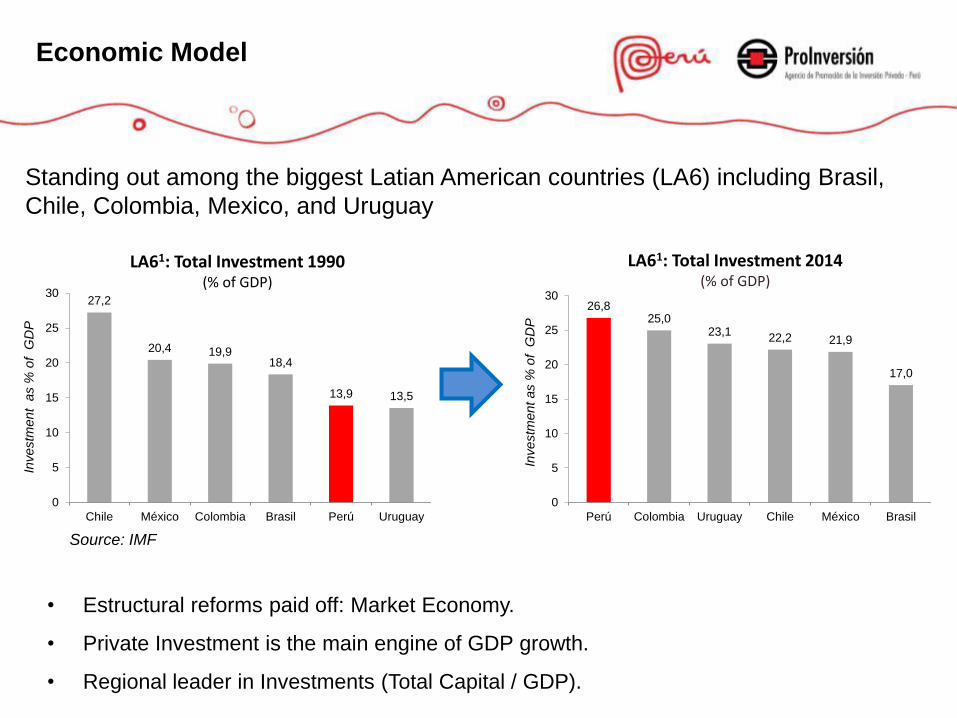

LA61: Total Investment 1990

(% of GDP)

LA61: Total Investment 2014 (% of GDP)

• Estructural reforms paid off: Market Economy.

• Private Investment is the main engine of GDP growth.

• Regional leader in Investments (Total Capital / GDP).

Economic Model

Investm

ent as %

of G

DP

Standing out among the biggest Latian American countries (LA6) including Brasil,

Chile, Colombia, Mexico, and Uruguay

Source: IMF

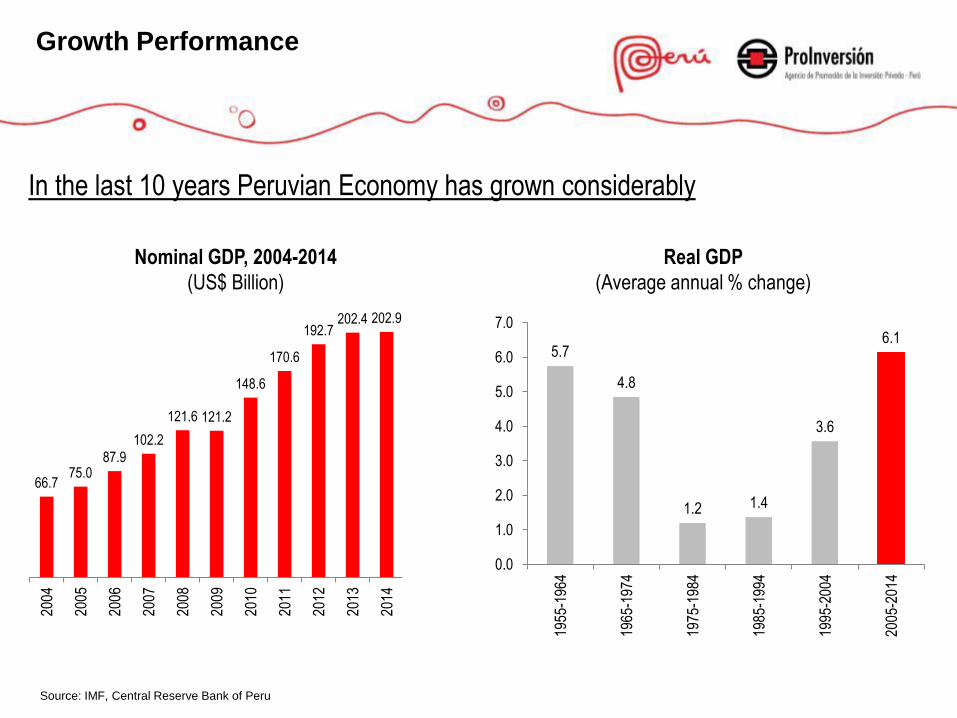

Growth Performance

In the last 10 years Peruvian Economy has grown considerably

Nominal GDP, 2004-2014

(US$ Billion)

Source: IMF, Central Reserve Bank of Peru

5.7

4.8

1.2 1.4

3.6

6.1

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1955

-196

4

1965

-197

4

1975

-198

4

1985

-199

4

1995

-200

4

2005

-201

4

Real GDP

(Average annual % change)

66.7 75.0

87.9

102.2

121.6 121.2

148.6

170.6

192.7 202.4 202.9

190.3 202.3

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

*

2016

*

Source: Ministry of Economy, IMF, Consensus Forecast (March 2015)

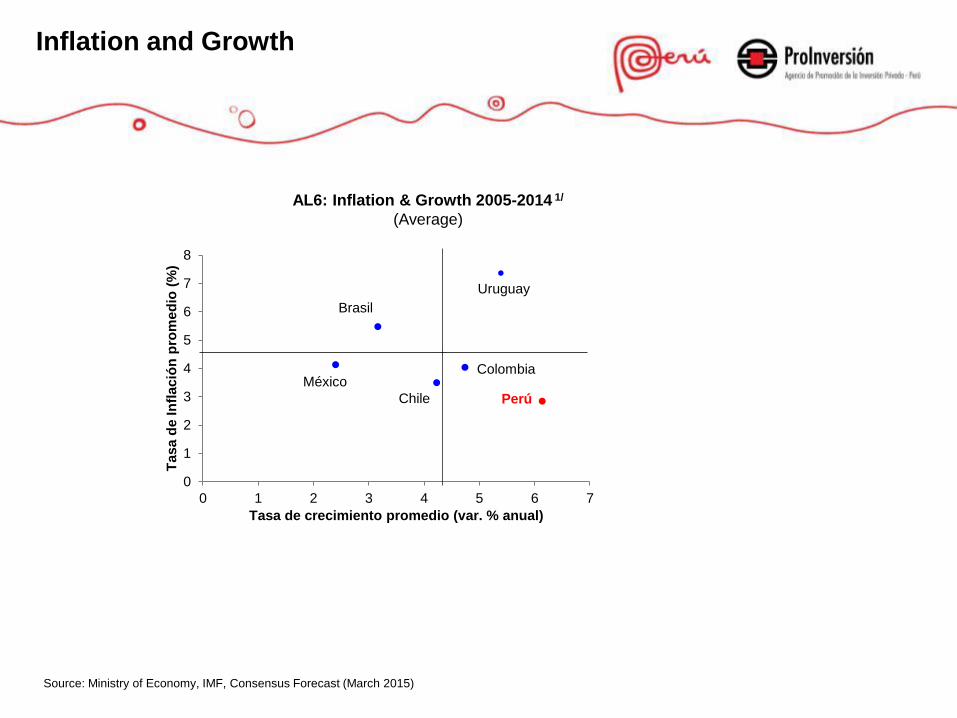

AL6: Inflation & Growth 2005-2014 1/

(Average)

Brasil

Chile

ColombiaMéxico

Perú

Uruguay

0

1

2

3

4

5

6

7

8

0 1 2 3 4 5 6 7

Ta

sa

de

In

fla

ció

n p

rom

ed

io (

%)

Tasa de crecimiento promedio (var. % anual)

Inflation and Growth

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

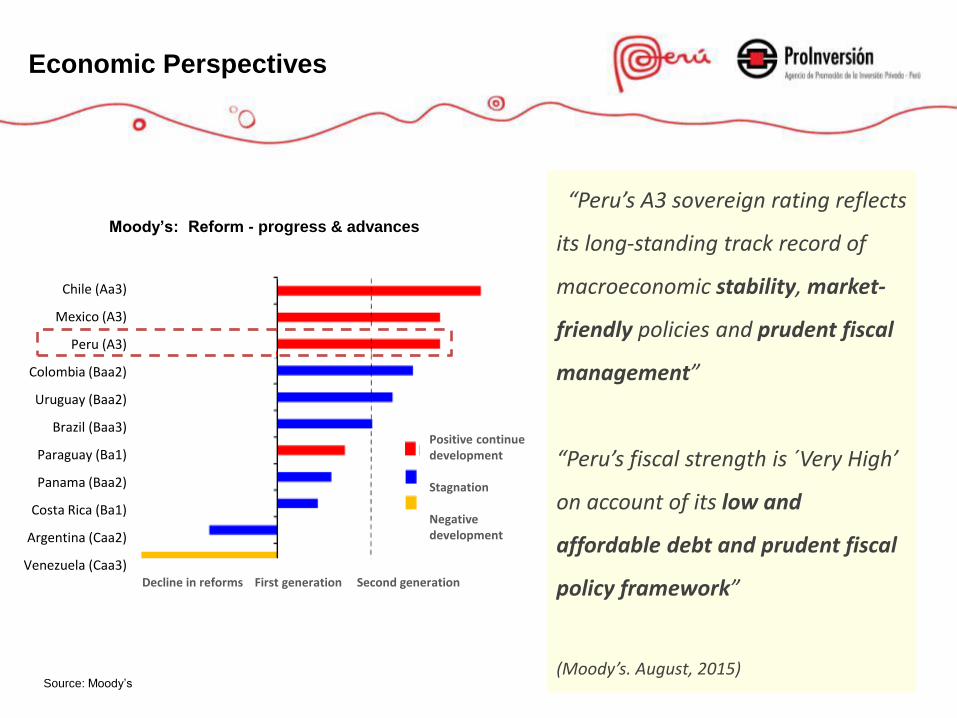

Economic Perspectives

Moody’s: Reform - progress & advances

Source: Moody’s

Chile (Aa3)

Mexico (A3)

Peru (A3)

Colombia (Baa2)

Uruguay (Baa2)

Brazil (Baa3)

Paraguay (Ba1)

Panama (Baa2)

Costa Rica (Ba1)

Argentina (Caa2)

Venezuela (Caa3)

Positive continue development Stagnation Negative development

Decline in reforms First generation Second generation

“Peru’s A3 sovereign rating reflects

its long-standing track record of

macroeconomic stability, market-

friendly policies and prudent fiscal

management”

“Peru’s fiscal strength is ´Very High’

on account of its low and

affordable debt and prudent fiscal

policy framework”

(Moody’s. August, 2015)

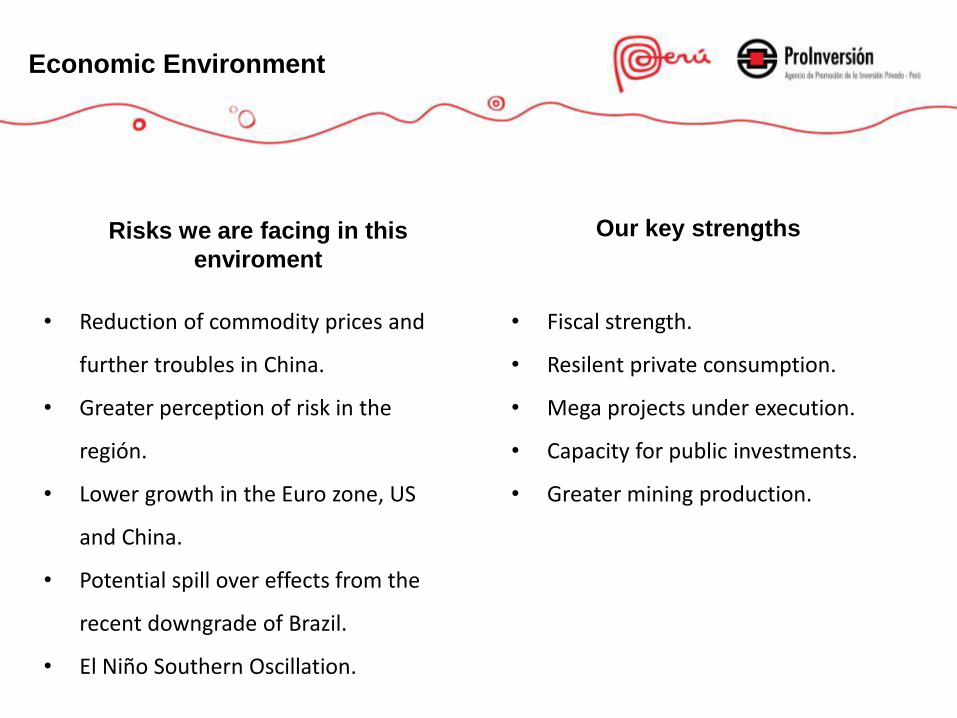

Economic Environment

• Reduction of commodity prices and

further troubles in China.

• Greater perception of risk in the

región.

• Lower growth in the Euro zone, US

and China.

• Potential spill over effects from the

recent downgrade of Brazil.

• El Niño Southern Oscillation.

• Fiscal strength.

• Resilent private consumption.

• Mega projects under execution.

• Capacity for public investments.

• Greater mining production.

Risks we are facing in this

enviroment

Our key strengths

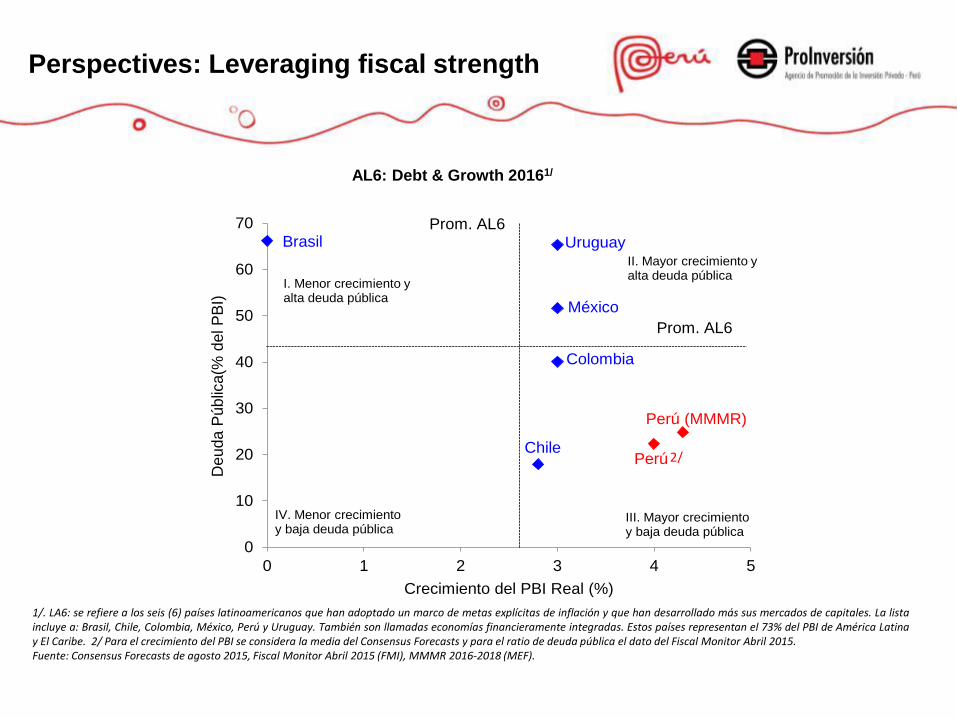

Perspectives: Leveraging fiscal strength

1/. LA6: se refiere a los seis (6) países latinoamericanos que han adoptado un marco de metas explícitas de inflación y que han desarrollado más sus mercados de capitales. La lista incluye a: Brasil, Chile, Colombia, México, Perú y Uruguay. También son llamadas economías financieramente integradas. Estos países representan el 73% del PBI de América Latina y El Caribe. 2/ Para el crecimiento del PBI se considera la media del Consensus Forecasts y para el ratio de deuda pública el dato del Fiscal Monitor Abril 2015. Fuente: Consensus Forecasts de agosto 2015, Fiscal Monitor Abril 2015 (FMI), MMMR 2016-2018 (MEF).

Chile

México

Perú

Colombia

Brasil Uruguay

Perú (MMMR)

0

10

20

30

40

50

60

70

0 1 2 3 4 5

Deuda P

úblic

a(%

del P

BI)

Crecimiento del PBI Real (%)

I. Menor crecimiento y alta deuda pública

IV. Menor crecimiento y baja deuda pública

II. Mayor crecimiento y alta deuda pública

III. Mayor crecimiento y baja deuda pública

2/

Prom. AL6

Prom. AL6

AL6: Debt & Growth 20161/

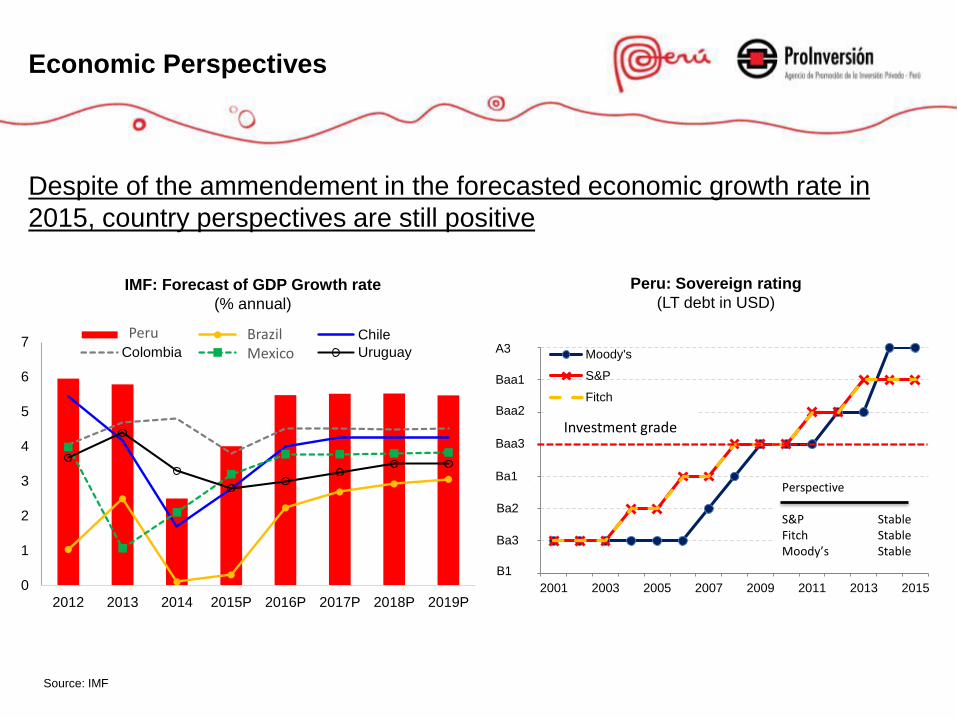

Economic Perspectives

Despite of the ammendement in the forecasted economic growth rate in

2015, country perspectives are still positive

Peru: Sovereign rating

(LT debt in USD) IMF: Forecast of GDP Growth rate

(% annual)

Source: IMF

0

1

2

3

4

5

6

7

2012 2013 2014 2015P 2016P 2017P 2018P 2019P

Perú Brasil Chile

Colombia Mexico Uruguay

Peru Brazil Mexico

15

17

19

21

23

25

27

29

2001 2003 2005 2007 2009 2011 2013 2015

Moody's

S&P

Fitch

Grado de inversión

Ba1

Ba3

Baa1

Baa2

Ba2

B1

Perspectivas

S&P

Fitch

Moody's

Estable

Estable

Estable

Baa3

A3

Investment grade

Perspective S&P Stable Fitch Stable Moody’s Stable

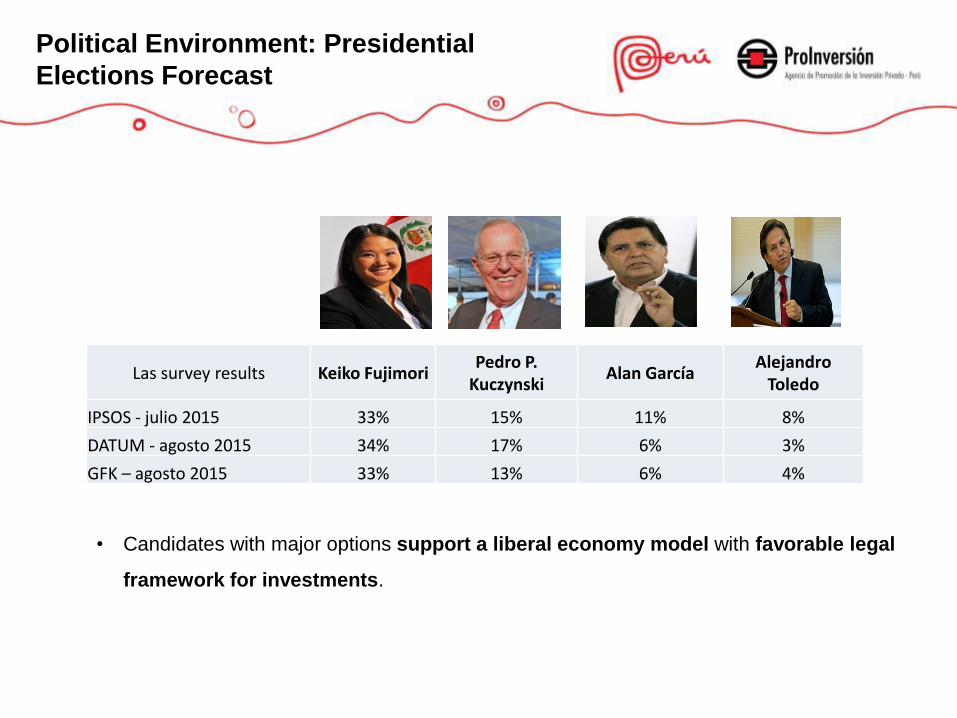

Political Environment: Presidential

Elections Forecast

• Candidates with major options support a liberal economy model with favorable legal

framework for investments.

Las survey results Keiko Fujimori Pedro P.

Kuczynski Alan García

Alejandro Toledo

IPSOS - julio 2015 33% 15% 11% 8%

DATUM - agosto 2015 34% 17% 6% 3%

GFK – agosto 2015 33% 13% 6% 4%

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

Favorable legal framework

• Non discriminatory treatment of foreign investments

• Guarantees for Private Property

• A Market Economy that promotes free competition

• Legal stability agreements

Easiness for doing business and

competitiveness

“35th in the Doing Business Ranking 2015”

120

157

82

124

162

123

34

115

41

35

182

Argentina

Uruguay

Bolivia

Brasil

Surinam

Guyana Venezuela

Colombia

Perú

Chile

Ecuador

2014- 2015

País País

1 Switzerland 19 Luxemburgo

2 Singapur 20 Malasya

3 United States 21 Austria

4 Germany 22 Australia

5 Finlandia 23 France

6 Japan 24 Arabia Saudí

7 Hong Kong 25 Irleland

8 Netherland 26 South Corea

9 United Kingdom 27 Israel

10 Sweden 28 China

11 Norway

12 United Arab Emirates 33 Chile

13 Denmark 57 Brasil

14 Taiwan 61 Mexico

15 Canada 65 Peru

16 Qatar 66 Colombia

17 New Zeland 104 Argentina

18 Belgium 131 Venezuela

“65th Global competitiveness report 2014”

Source: World Bank Source: WEF

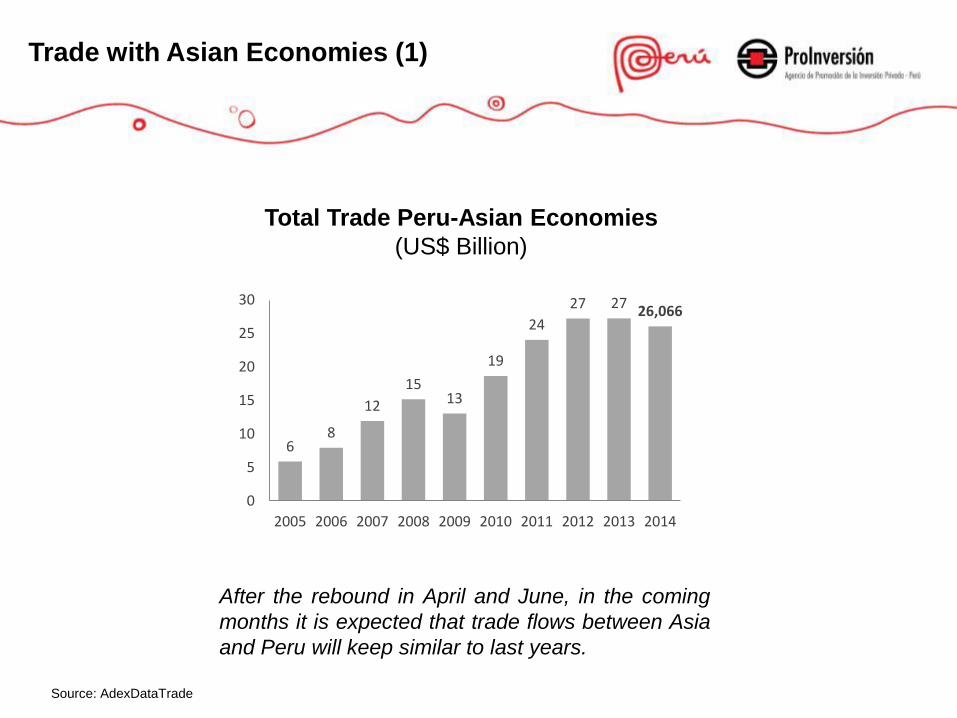

Trade with Asian Economies (1)

6 8

12

15 13

19

24

27 27 26,066

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Trade Peru-Asian Economies

(US$ Billion)

After the rebound in April and June, in the coming

months it is expected that trade flows between Asia

and Peru will keep similar to last years.

Source: AdexDataTrade

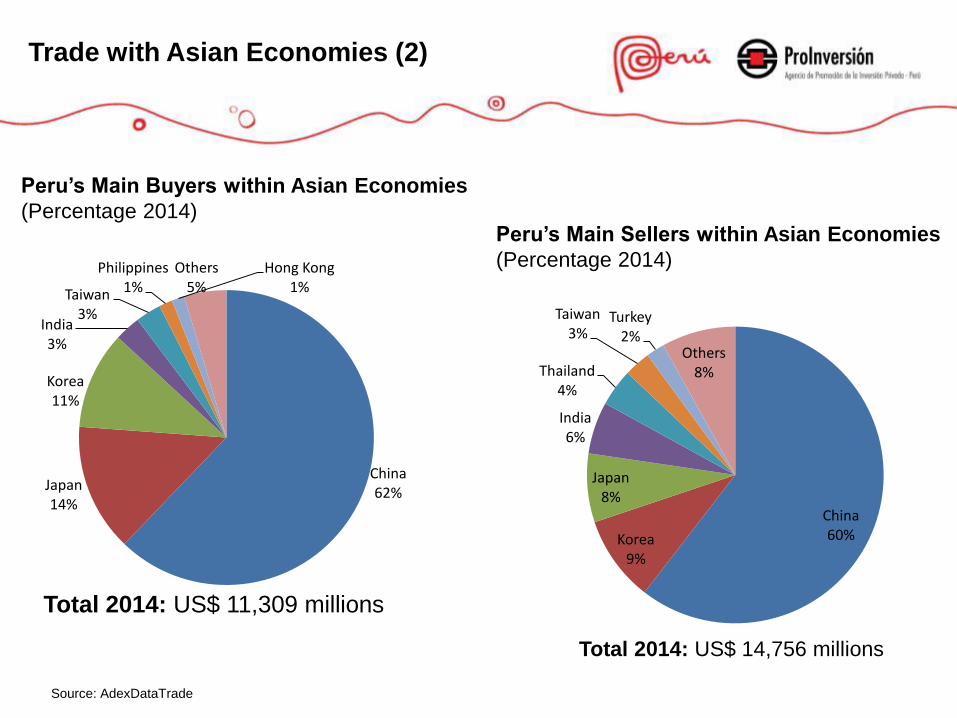

Peru’s Main Buyers within Asian Economies

(Percentage 2014)

Total 2014: US$ 11,309 millions

China 62% Japan

14%

Korea 11%

India 3%

Taiwan 3%

Philippines 1%

Hong Kong 1%

Others 5%

Peru’s Main Sellers within Asian Economies

(Percentage 2014)

Total 2014: US$ 14,756 millions

China 60% Korea

9%

Japan 8%

India 6%

Thailand 4%

Taiwan 3%

Turkey 2%

Others 8%

Source: AdexDataTrade

Trade with Asian Economies (2)

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

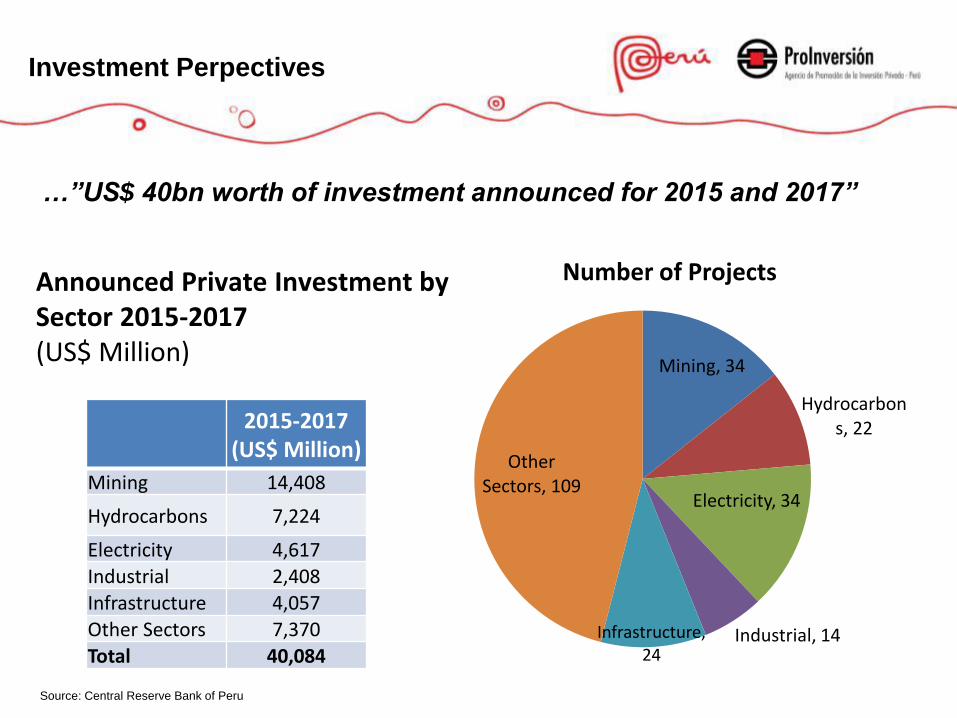

Investment Perpectives

Announced Private Investment by Sector 2015-2017 (US$ Million)

2015-2017 (US$ Million)

Mining 14,408

Hydrocarbons 7,224

Electricity 4,617

Industrial 2,408 Infrastructure 4,057

Other Sectors 7,370 Total 40,084

Number of Projects

Mining, 34

Hydrocarbons, 22

Electricity, 34

Industrial, 14 Infrastructure, 24

Other Sectors, 109

Source: Central Reserve Bank of Peru

…”US$ 40bn worth of investment announced for 2015 and 2017”

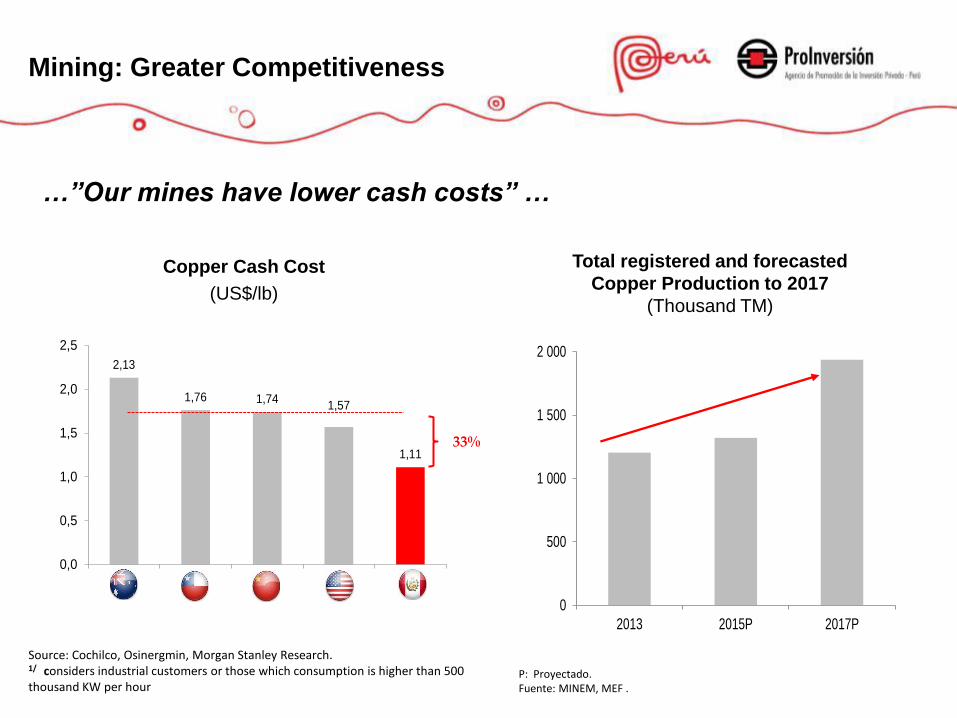

Mining: Greater Competitiveness

2,13

1,76 1,741,57

1,11

0,0

0,5

1,0

1,5

2,0

2,5

Australia Chile China EE.UU. Perú

33%

Copper Cash Cost

(US$/lb)

Source: Cochilco, Osinergmin, Morgan Stanley Research. 1/ considers industrial customers or those which consumption is higher than 500 thousand KW per hour

P: Proyectado. Fuente: MINEM, MEF .

Total registered and forecasted

Copper Production to 2017

(Thousand TM)

0

500

1 000

1 500

2 000

2013 2015P 2017P

…”Our mines have lower cash costs” …

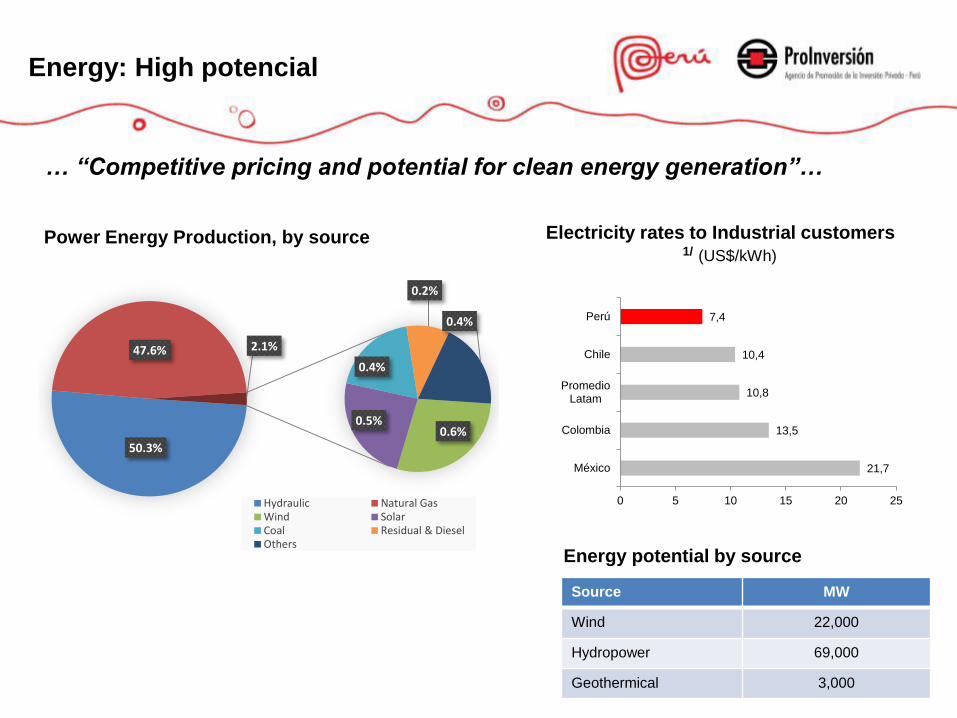

Energy: High potencial

21,7

13,5

10,8

10,4

7,4

0 5 10 15 20 25

México

Colombia

PromedioLatam

Chile

Perú

Electricity rates to Industrial customers 1/ (US$/kWh)

50.3%

47.6%

0.6% 0.5%

0.4%

0.2%

0.4%

2.1%

Power Energy Production, by source

Hydraulic Natural GasWind SolarCoal Residual & DieselOthers

Energy potential by source

Source MW

Wind 22,000

Hydropower 69,000

Geothermical 3,000

… “Competitive pricing and potential for clean energy generation”…

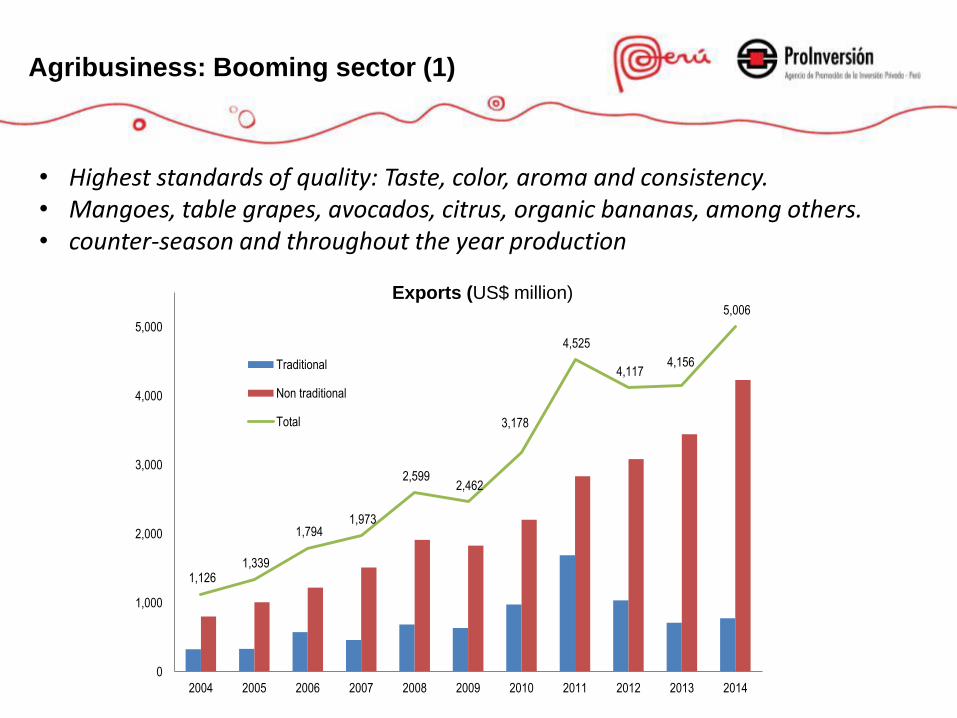

1,126 1,339

1,794 1,973

2,599 2,462

3,178

4,525

4,117 4,156

5,006

0

1,000

2,000

3,000

4,000

5,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Traditional

Non traditional

Total

Exports (US$ million)

• Highest standards of quality: Taste, color, aroma and consistency. • Mangoes, table grapes, avocados, citrus, organic bananas, among others. • counter-season and throughout the year production

Agribusiness: Booming sector (1)

New 100 thousand

of

hectares

Area for modern agriculture

(thousand of hectares)

78%

Chavimochic III

Majes-Siguas II

180 218

63

38

2013 2020

Agribusiness: Booming sector (2)

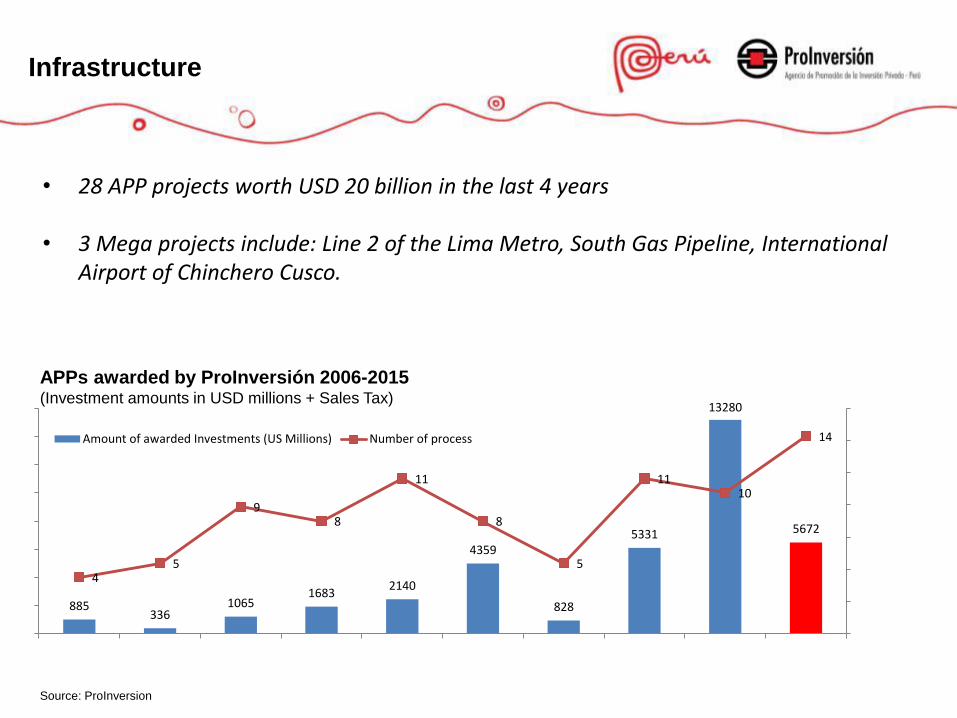

Infrastructure

APPs awarded by ProInversión 2006-2015 (Investment amounts in USD millions + Sales Tax)

885 336

1065 1683

2140

4359

828

5331

13280

5672

4 5

9 8

11

8

5

11 10

14

0

2000

4000

6000

8000

10000

12000

14000

0

2

4

6

8

10

12

14

16

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Amount of awarded Investments (US Millions) Number of process

• 28 APP projects worth USD 20 billion in the last 4 years

• 3 Mega projects include: Line 2 of the Lima Metro, South Gas Pipeline, International Airport of Chinchero Cusco.

Source: ProInversion

• Our country: Peru

• Economic perspectives

• Investment environment

• Investment perspectives

• Infrastructure

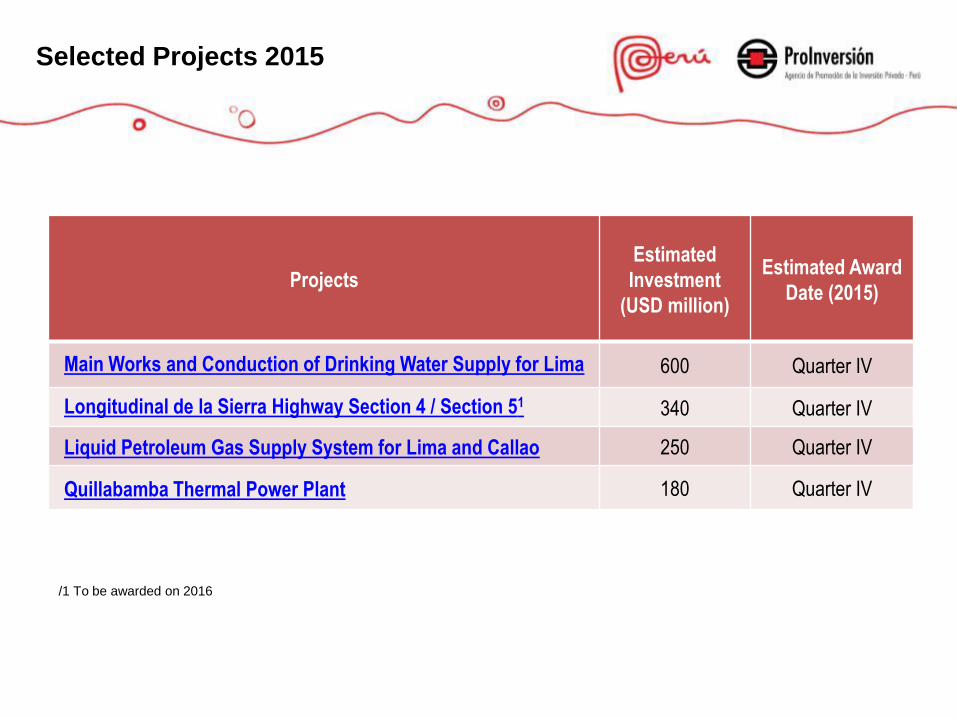

Projects

Estimated

Investment

(USD million)

Estimated Award

Date (2015)

Main Works and Conduction of Drinking Water Supply for Lima 600 Quarter IV

Longitudinal de la Sierra Highway Section 4 / Section 51 340 Quarter IV

Liquid Petroleum Gas Supply System for Lima and Callao 250 Quarter IV

Quillabamba Thermal Power Plant 180 Quarter IV

Selected Projects 2015

/1 To be awarded on 2016

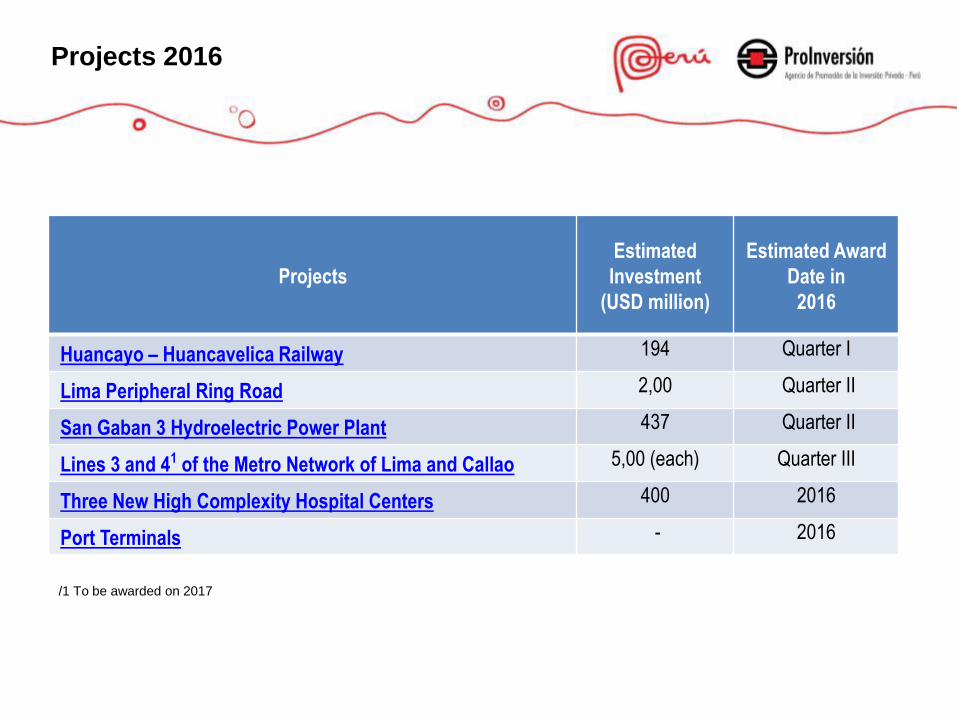

Projects

Estimated

Investment

(USD million)

Estimated Award

Date in

2016

Huancayo – Huancavelica Railway 194 Quarter I

Lima Peripheral Ring Road 2,00 Quarter II

San Gaban 3 Hydroelectric Power Plant 437 Quarter II

Lines 3 and 41 of the Metro Network of Lima and Callao 5,00 (each) Quarter III

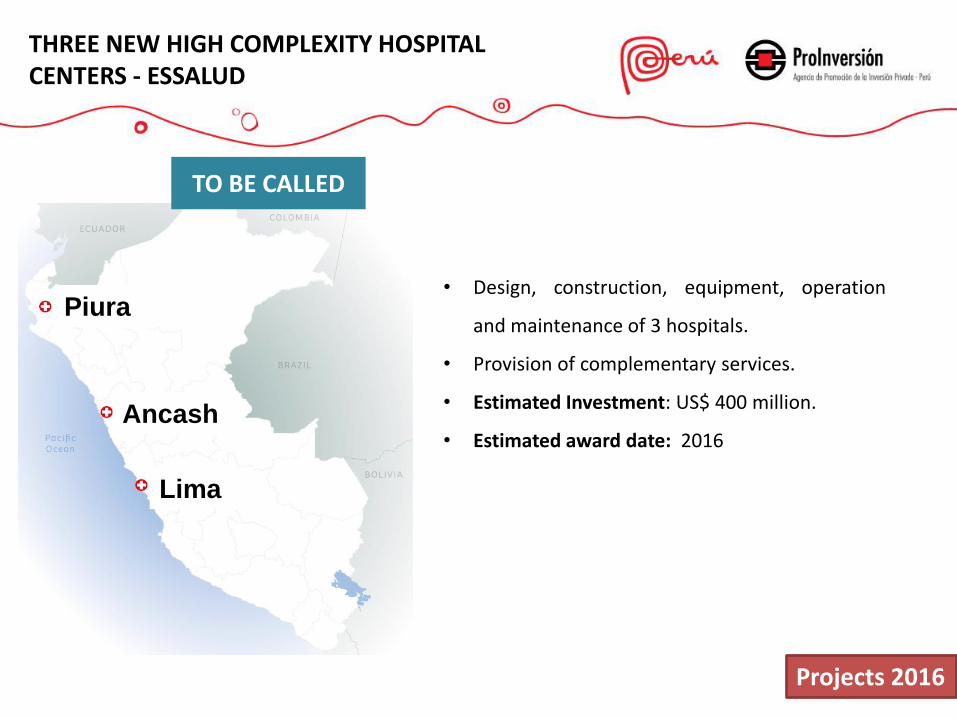

Three New High Complexity Hospital Centers 400 2016

Port Terminals - 2016

Projects 2016

/1 To be awarded on 2017

www.proinversion.gob.pe [email protected]

TO BE ANNOUNCED

represas

CALLED

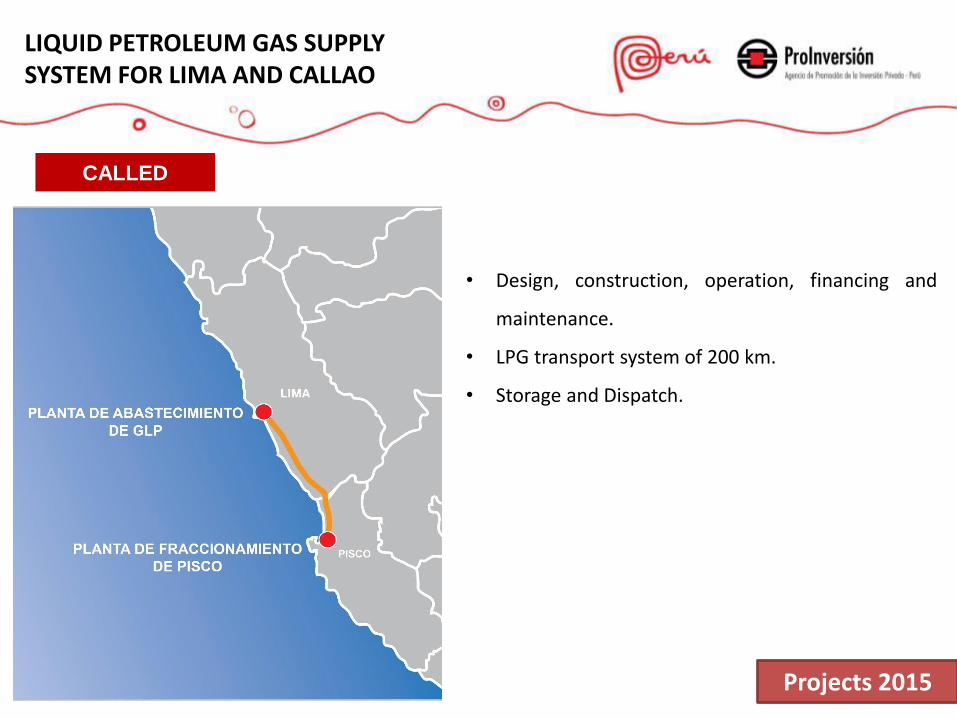

MAIN WORKS AND CONDUCTION OF DRINKING WATER SUPPLY FOR LIMA

DBFO including: Re-enlargement of two dams 10 Km trans-andean tunnel New drinking water plant of 5 m3/ 40km pipeline Seven reservoirs 90km interconnection lines Operation and maintenance of existing facilities: Water intake (12 m3/s) Drinking water plant (5 m3/s) 27km pipelines 4 compensation reservoirs (Storage volume:

23,000 m3 )

Projects 2015

• Design, construction, operation, financing and

maintenance.

• LPG transport system of 200 km.

• Storage and Dispatch.

CALLED

LIQUID PETROLEUM GAS SUPPLY SYSTEM FOR LIMA AND CALLAO

Projects 2015

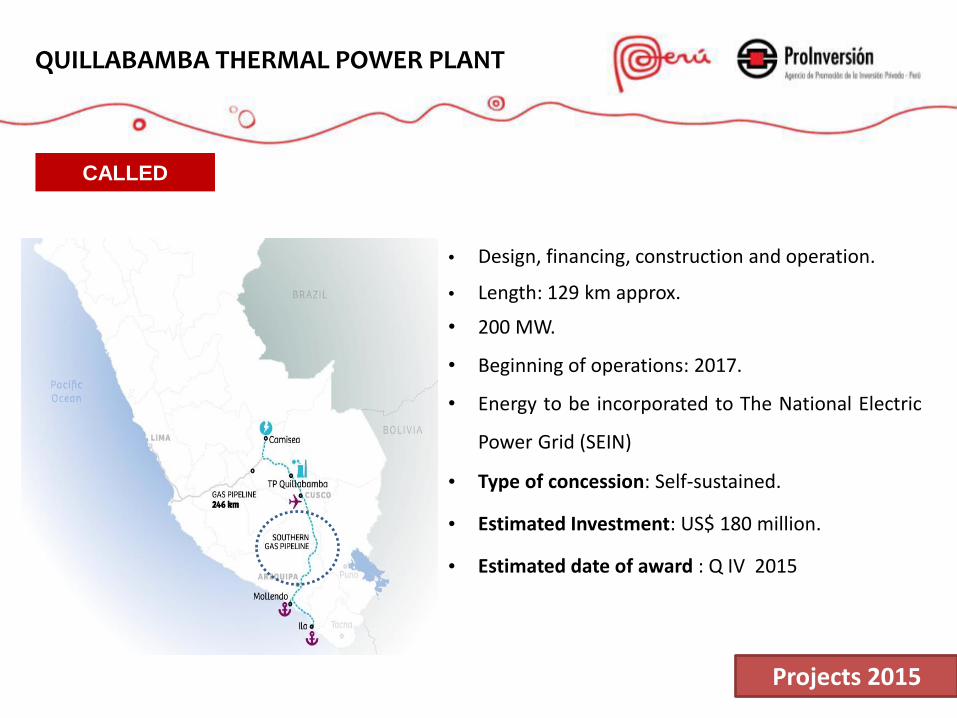

• Design, financing, construction and operation.

• Length: 129 km approx.

• 200 MW.

• Beginning of operations: 2017.

• Energy to be incorporated to The National Electric

Power Grid (SEIN)

• Type of concession: Self-sustained.

• Estimated Investment: US$ 180 million.

• Estimated date of award : Q IV 2015

QUILLABAMBA THERMAL POWER PLANT

Projects 2015

CALLED

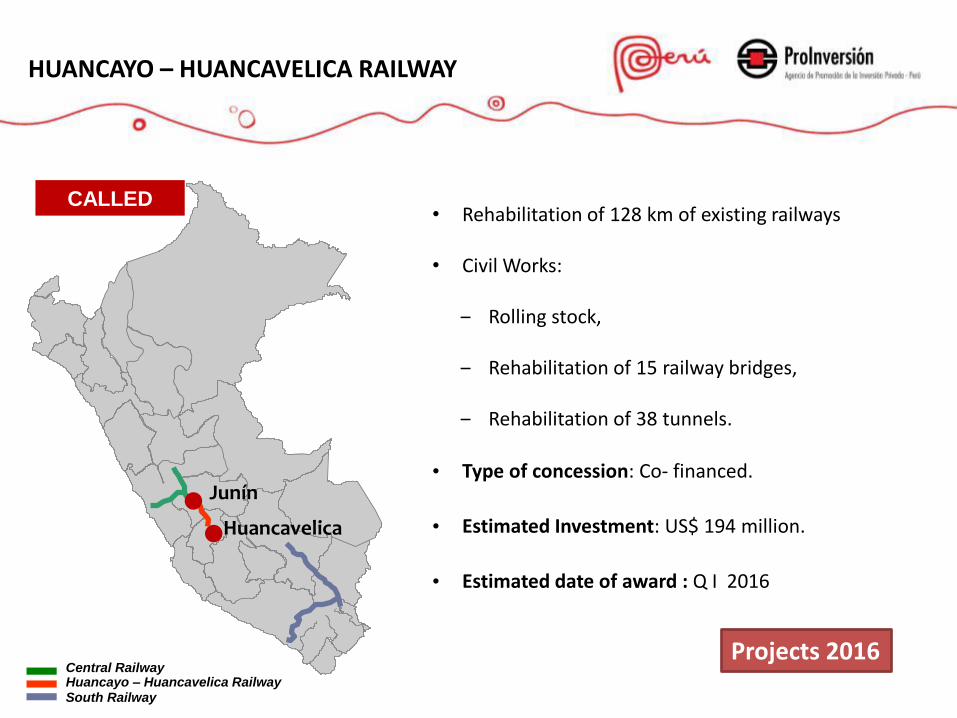

• Rehabilitation of 128 km of existing railways

• Civil Works:

‒ Rolling stock,

‒ Rehabilitation of 15 railway bridges,

‒ Rehabilitation of 38 tunnels.

• Type of concession: Co- financed.

• Estimated Investment: US$ 194 million.

• Estimated date of award : Q I 2016

HUANCAYO – HUANCAVELICA RAILWAY

Junín

Central Railway Huancayo – Huancavelica Railway South Railway

Huancavelica

CALLED

Projects 2016

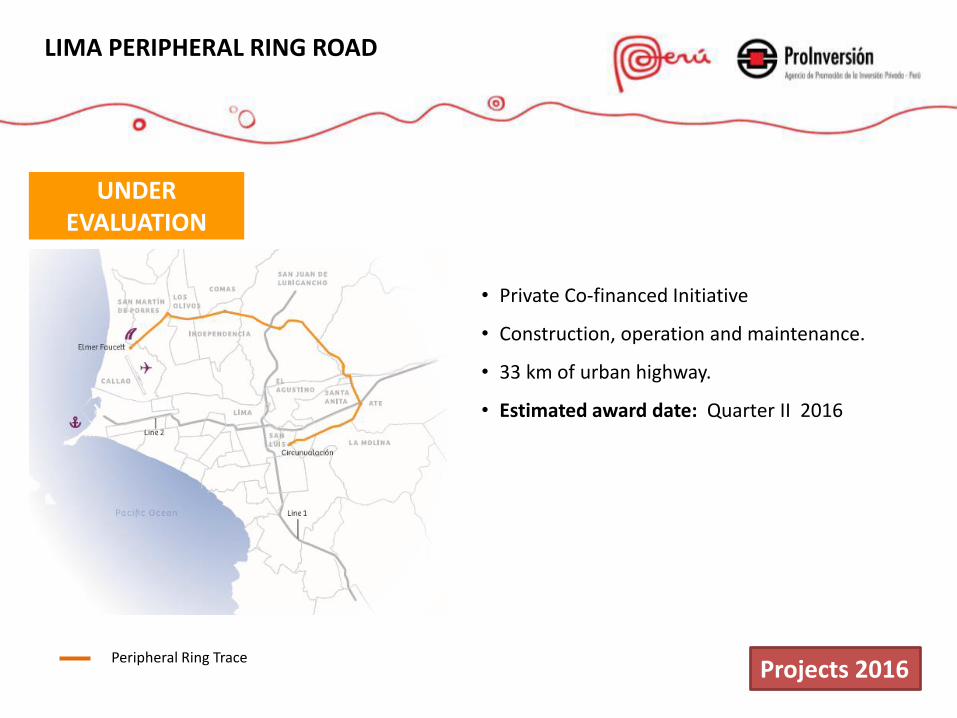

LIMA PERIPHERAL RING ROAD

• Private Co-financed Initiative

• Construction, operation and maintenance.

• 33 km of urban highway.

• Estimated award date: Quarter II 2016

UNDER EVALUATION

Peripheral Ring Trace Projects 2016

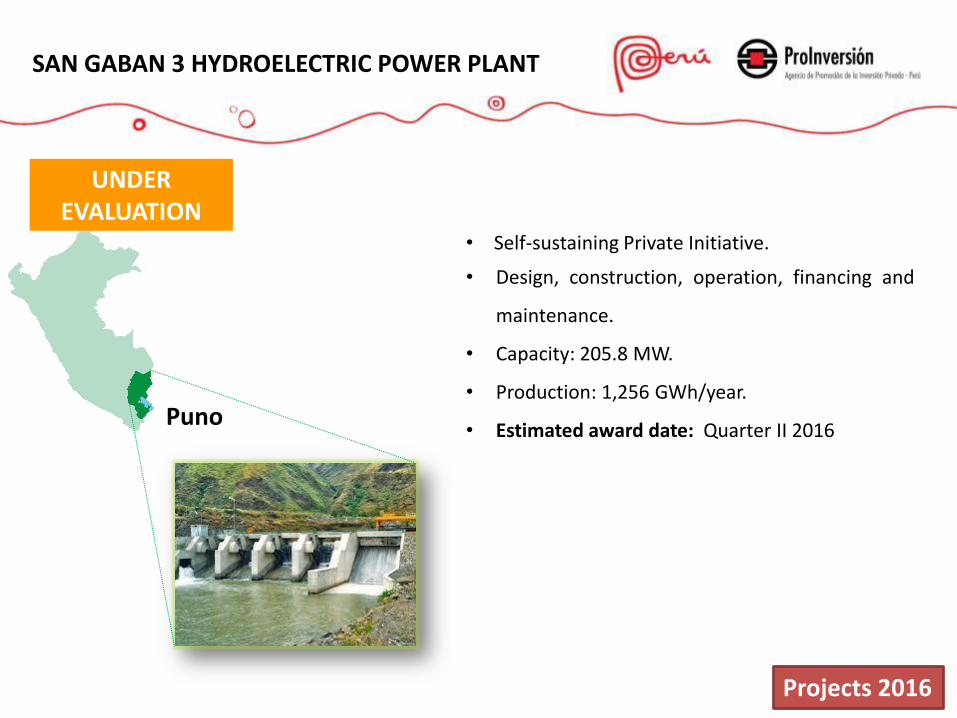

• Self-sustaining Private Initiative.

• Design, construction, operation, financing and

maintenance.

• Capacity: 205.8 MW.

• Production: 1,256 GWh/year.

• Estimated award date: Quarter II 2016 Puno

UNDER EVALUATION

SAN GABAN 3 HYDROELECTRIC POWER PLANT

Projects 2016

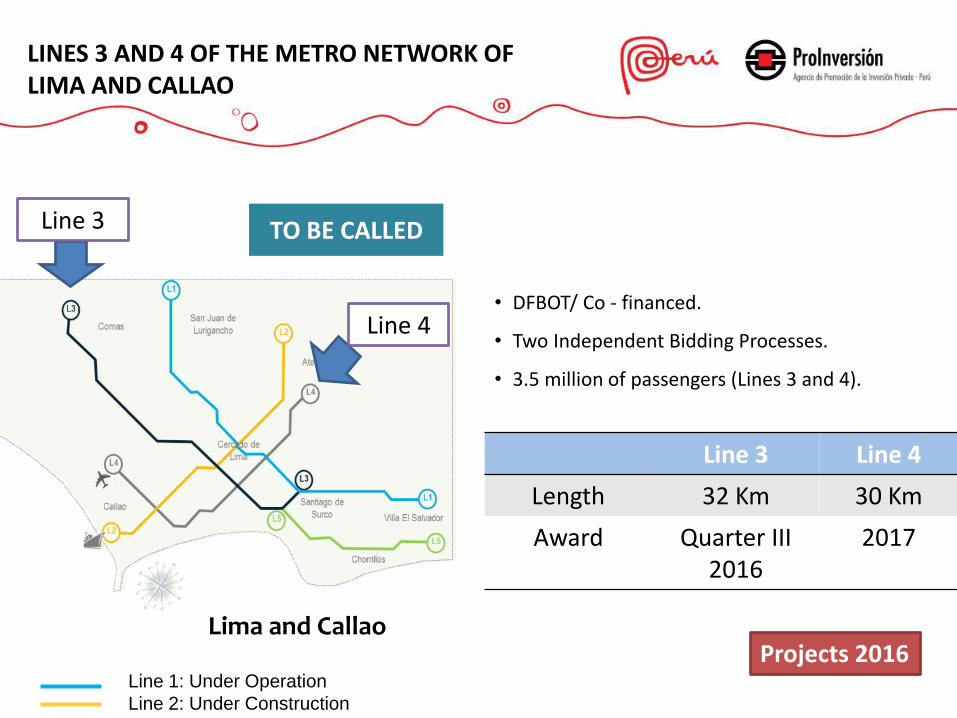

• DFBOT/ Co - financed.

• Two Independent Bidding Processes.

• 3.5 million of passengers (Lines 3 and 4).

Line 3 Line 4

Length 32 Km 30 Km

Award Quarter III 2016

2017

Lima and Callao

Line 1: Under Operation

Line 2: Under Construction

Line 4

Line 3

LINES 3 AND 4 OF THE METRO NETWORK OF LIMA AND CALLAO

TO BE CALLED

Projects 2016

• Design, construction, equipment, operation

and maintenance of 3 hospitals.

• Provision of complementary services.

• Estimated Investment: US$ 400 million.

• Estimated award date: 2016

Piura

Ancash

Lima

THREE NEW HIGH COMPLEXITY HOSPITAL CENTERS - ESSALUD

Projects 2016

TO BE CALLED

PORT TERMINALS

• Private Self-sustaining Initiatives:

1. Salaverry: Modernizing and developing the Multipurpose Terminal Salaverry. 2. Chimbote: Design, financing, construction, operation and maintenance of a port container terminal. 3. Ilo: Development and operation of the Ilo Multipurpose Terminal Port.

Under

evaluation

• Estimated award date: 2016

Ilo

Chimbote

Salaverry

Projects 2016