Embed Size (px)

Citation preview

Journal of Comumer Studies and Home Economics (1991) 15,161-175.

Physicians’ perceptions of consumers’ attitudes: satisfaction, quality and selection criteria

HOWARD G. SCHUTZ,* KATHERINE V. DIAZ-KNAUF* AND DEBRA S. JUDGE? California at Davis and tDepartment of Anthropology, University of California at Davis

*Department of Consumer Sciences, University of

A mail survey of physicians from Sacramento, California, elicited information on perceptions of consumer satisfaction, service quality for I0 rypes of service providers including physicians and the importance ratings of 12 choice criteria for the selection of a physician by coyumers. The two most important selection criteria for physicians as perceived for consumers by physicians were ‘consumer’s previous experience with provider’ and ‘reputationlrecommendation’. The results are compared with an earlier consumer survey.

Introduction

In the U.S.A. physicians are faced today with very special problems in marketing their services to consumers. An historically difficult area has been made more complex with the introduction and growth of Health Maintenance Organizations (HMO), private practice groups, increased regulation and consumer awareness in the health-care area. The concept of competitive marketing appears paradoxical to an area which has the Hippocratic oath as a main ethical dictum; however, the reality is that consumers choose among physicians in the service market-place. An understanding of the factors surrounding these choices and their satisfaction is an important part of the business of being a physician. This is vividly illustrated in a survey conducted by Cousins in Westwood, California, where 85% of the sample reported changing or thinking of changing physicians during the past 5 years for reasons other than relocation, physician’s retirement or death.’ Twenty-five per cent of the respondents cited incompetence as their . reason for changing physicians. Among some of the other reasons given were physician personality, style, lack of confidence, communication skills and office appearance (unorgan- ized, cluttered). Other studies have given us information on the degrees of consumer satisfaction and criteria that consumers use in making their choices and also what is likely to result in satisfa~tion.”~ In addition to ascertaining consumer attitudes with regard to physicians’ services, it would be valuable to explore physicians’ attitudes and their perceptions of consumer attitudes. One should be

Correspondence: Katherine V. Diaz-Knauf, Staff Research Associate, Department of

161

Consumer Sciences, University of California at Davis, Davis, CA 95616, U.S.A.

Physicians' perceptions of consumers' attitudes

able to determine the congruities and divergences between actual consumer perceptions and those physicians' report of consumer perceptions for the same set of characteristics. It should be possible to identify those areas which physicians could consider emphasizing when making decisions that influence their practices, both from the standpoint of the field of medicine and individual business practice. Since we had previously studied attitudes of consumers toward physician services in the Sacramento area, we developed a survey for physicians addressing those same issues for which we had consumer resp0nses.l'

Materials and methods

A mail survey of 500 physicians from Sacramento, California was conducted recently using the California Department of Consumers Affairs Board of Medical Quality Assurance listing of physicians and surgeons as the sampling frame and a systematic random, sampling procedure. The data were collected using a three- wave mailing technique in which a letter and questionnaire were mailed to each physician in the sample; subsequently, a reminder postcard was sent 1 week after the first mailing; and another letter and questionnaire were sent 3 weeks after the initial mailing to those physicians from whom no response had been received." Forty-five per cent of (n = 242) 478 deliverable questionnaires were completed and returned. For homogeneous groups such as physicians this level of response is considered appropriate with regards to non-response bias. l2 This six-page questionnaire required approximately 30 min to complete and contained 69 items assessing opinions on consumer satisfaction, quality of service, 10 categories of service providers including physicians, consumer selection criteria, consumer and physician attitudes and demographic characteristics. Cross-tabulations of 69 selected variables by week of return did not indicate any statistically significant monotonic trend differences over time; evidence that there is minimal non- responder bias. This is based on the assumption that non-responders most closely resemble in their answers those individuals who return their questionnaires late in the survey.

Physicians and surgeons were asked to provide information about their attitudes towards consumer services in general (e.g. quality, cost and govern- ment regulations). Ten categories of service providers were listed, and respon- dents were asked to provide ratings on consumer satisfaction and on the quality of the service. Types of services included repair of goods, personal, professional and home repairs. A list of 12 characteristics used by consumers to select a service provider was included, and the respondents were asked to provide importance ratings for each criterion for physicians and surgeons on a scale of 1 'not important' to 10 'very important'. The respondents were also asked to indicate their perceptions of consumers' ratings for each criterion. After examining the distribution of importance values, the 10-point scale was collapsed to 5 points to better approximate normality and the values were r e~oded . '~ . ' ~ A series of

162

€I. G. Schutz, K. V. Dim-Knauf and D. S. Judge

statements characterizing consumer attitudes towards five aspects of medical practices were measured on a 5-point Likert-type scale. Demographic informa- tion was requested from each respondent, as well as information on each respondent’s practice such as degree of specialization, clientele, business size, etc.

Results and discussion

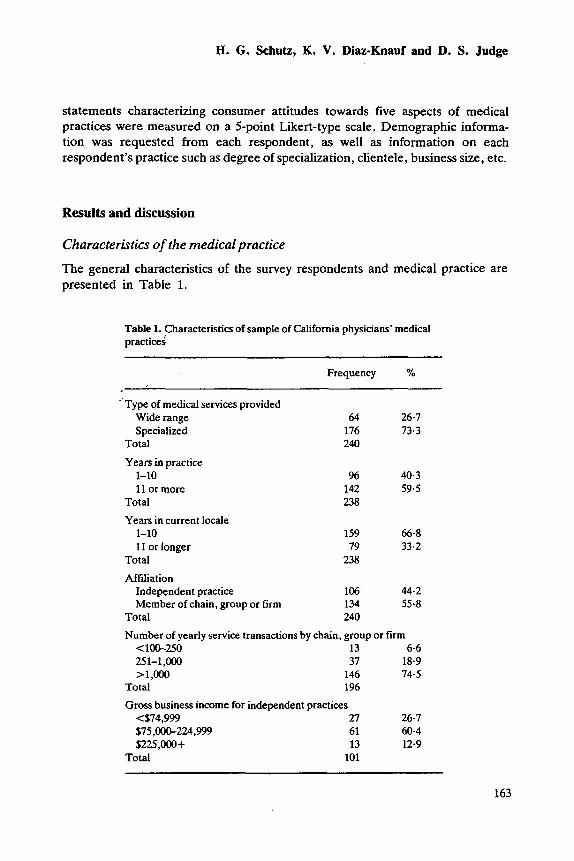

Characteristics of the medical practice

The general characteristics of the survey respondents and medical practice are presented in Table 1.

Table 1. ,Characteristics of sample of California physicians’ medical practices

Frequency YO

’ Type of medical services provided Wide range 64 26-7 Specialized 176 73-3

Total 240

Years in practice 1-10 % 40-3 11 or more 142 59.5

Total 238 Years in current locale

1-10 159 66.8 1 I or Ionger 79 33.2

Total 238

Affiliation Independent practice 106 44.2 Member of chain, group or firm 134 55.8

Total 240

Number of yearly service transactions by chain, group or firm <1W250 13 6.6 251-1,oOO 37 18-9 >l,OOo 146 74-5

Total 196

Gross business income for independent practices 474 ,999 27 26.7 $75,000-224.999 61 60.4 $225,000+ 13 12.9

Total 101

163

Physicians’ perceptions of consumers’ attitudes

General information

Sixty-eight per cent of the sample rated quality of general consumer services available in the market-place as ‘good’ or ‘very good‘ (Table 2). Thirty-six per cent of the respondents believed the overall quality of services over the last 10 years has ‘decreased’, 34% ‘stayed the same’, and 30% ‘increased’. Cost of services was viewed as ‘high’ by 81% of the respondents. Physicians as consumers are more positive than consumers in general with regard to these three questions. For example, only 36% of the consumers in the study by Schutz and Casey rated quality of service as ‘very good’ or ‘good’, 50% felt that quality of service had ‘decreased’ in the last 10 years, and 34% thought the cost of services was ‘extremely high’. l5

Thirty-six per cent of the physicians in our sample are satisfied with the ‘current’ level of government regulation of physicians’ qualifications, 51 % said they would like ‘less’, and 14% see the need for ‘more’ regulation (Table 2). Without solicitingidditional information it is difficult to ascertain the specific aspect of regulation that our sample of physicians consider too little or excessive. However, this attitude probably refers to a component of the regulations enforced by the California Board of Medical Quality Assurance.

Table 2. Physicians’ attitudes toward consumer services in general

Overall quality of consumer services (n = 236)

Good 58.9% Fair 28.4%

Very good 9.3%

Poor 3.4% Quality of services over the last 10 years (n = 233)

Increased 30.0% Stayed the same 34.3% Decreased 35.6%

Cost of services to consumer (n = 237) Extremely high 00.0%

Average 19.0% High 80.6%

LOW 0.4% Future government regulation of physicians’ qualifications (n = 241)

More regulation 13.7%

Less regulation 50.67’0 Same regulation 357%

164

H. G . Schutz, K. V. Dim-Knauf and D. S. Judge

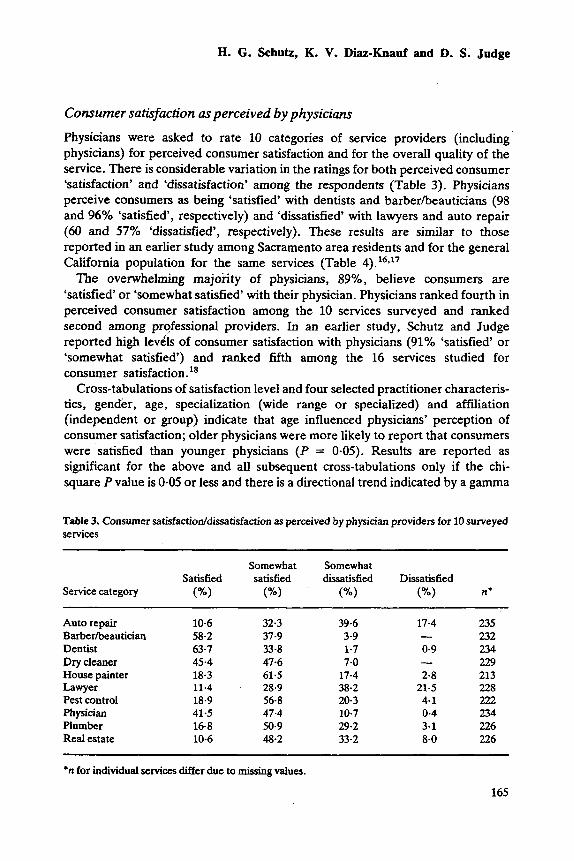

Consumer satisfaction as perceived by physicians

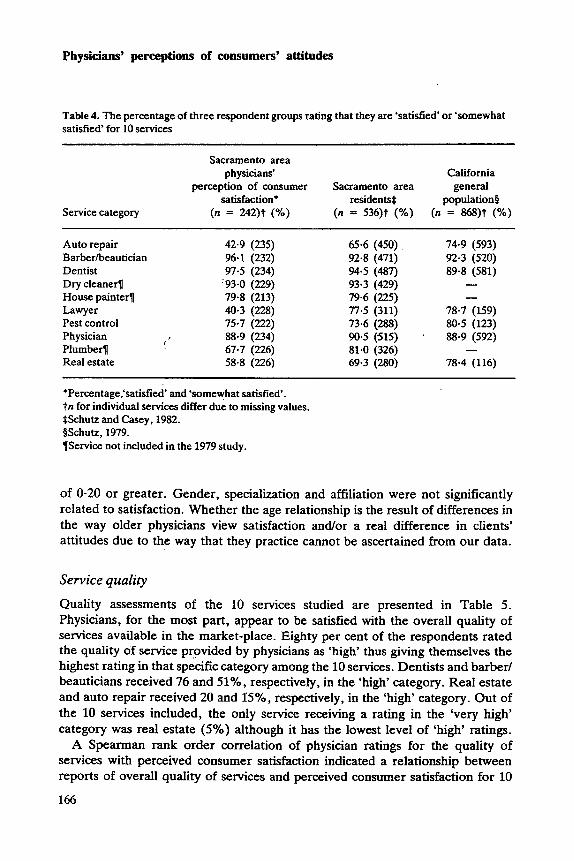

Physicians were asked to rate 10 categories of service providers (including physicians) for perceived consumer satisfaction and for the overall quality of the service. There is considerable variation in the ratings for both perceived consumer ‘satisfaction’ and ‘dissatisfaction’ among the respondents (Table 3). Physicians perceive consumers as being ‘satisfied’ with dentists and barberheauticians (98 and 96% ‘satisfied’, respectively) and ‘dissatisfied’ with lawyers and auto repair (60 and 57% ‘dissatisfied’, respectively). These results are similar to those reported in an earlier study among Sacramento area residents and for the general California population for the same services (Table 4). 16~17 The overwhelming majoiity of physicians, 89%, believe consumers are

‘satisfied‘ or ‘somewhat satisfied‘ with their physician. Physicians ranked fourth in perceived consumer satisfaction among the 10 services surveyed and ranked second among professional providers. In an earlier study, Schutz and Judge reported high levils of consumer satisfaction with physicians (910/, ‘satisfied’ or ‘somewhat satisfied’) and ranked fifth among the 16 services studied for consumer satisfaction.

Cross-tabulations of satisfaction level and four selected practitioner characteris- tics, gender, age, specialization (wide range or specialized) and affiliation (independent or group) indicate that age influenced physicians’ perception of consumer satisfaction; older physicians were more likely to report that consumers were satisfied than younger physicians (P = 0-05). Results are reported as significant for the above and all subsequent cross-tabulations only if the chi- square P value is 0.05 or less and there is a directional trend indicated by a gamma

Table 3. Consumer satisfactioddissatisfaction as perceived by physician providers for 10 surveyed services

Somewhat Somewhat Satisfied satisfied dissatisfied Dissatisfied

Service category (”/.I (%I (”/.I (”/I n*

Auto repair Barberibeautician Dentist Dry cleaner House painter Lawyer Pest control Physician Plumber Real estate

10.6 58-2 63.7 45.4 18.3 11.4 18.9 41.5 16-8 10-6

32.3 37-9 33-8 47.6 61.5

, 28-9 56.8 47.4 50.9 48.2

39.6 3.9 1-7 7-0 17.4 38-2 20-3 10.7 29.2 33-2

17-4

0.9

2-8 21.5 4-1 0-4 3-1 8.0

- -

- 235 232 234 229 213 228 222 234 226 226

*n for individual services W e r due to missing values.

165

Physicians’ perceptions of consumers’ attitudes

Table 4. The percentage of three respondent groups rating that they are ‘satisfied‘ or ‘somewhat satisfied‘ for 10 services

Sacramento area physicians’ California

satisfaction* residents* populations perception of consumer Sacramento area general

Service category (n = 242)t (YO) (R = 536)t (%) (n = 868)t (YO)

Auto repair Barberbeautician Dentist Dry cleaner1 House painter1 Lawyer Pest control Physician I

Plumber7 Real estate

42-9 (235) 96.1 (232) 97-5 (234) ‘.93.0 (229) 79.8 (213) 40.3 (228)

88.9 (234) 67.7 (226) 58-8 (226)

75.7 (222)

65.6 (450) . 92.8 (471) 94.5 (487) 93.3 (429) 79.6 (225) 77-5 (311) 73.6 (288) 90.5 (515) ‘

81.0 (326) 69.3 (280)

74.9 (593) 92-3 (520) 89.8 (581) - -

78-7 (159) 80-5 (123) 88.9 (592)

78.4 (116)

*Percentage-‘satisfied‘ and ‘somewhat satisfied’. tn for individual services differ due to missing values. SSchutz and Casey, 1982. BSchutz, 1979. TService not included in the 1979 study.

of 0-20 or greater. Gender, specialization and affiliation were not significantly related to satisfaction. Whether the age relationship is the result of differences in the way older physicians view satisfaction and/or a real difference in clients’ attitudes due to the way that they practice cannot be ascertained from our data.

Service quality

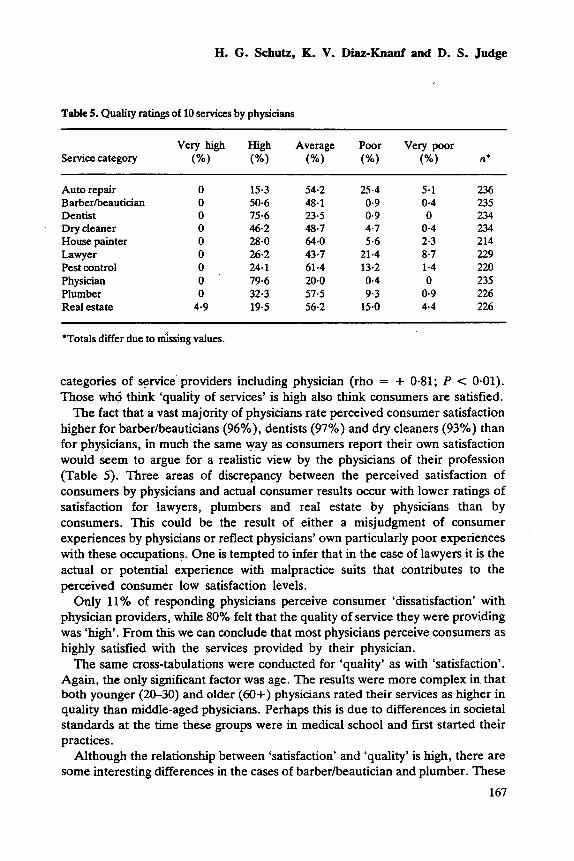

Quality assessments of the 10 services studied are presented in Table 5. Physicians, for the most part, appear to be satisfied with the overall quality of services available in the market-place. Eighty per cent of the respondents rated the quality of service provided by physicians as ‘high’ thus giving themselves the highest rating in that specific category among the 10 services. Dentists and barber/ beauticians received 76 and 5170, respectively, in the ‘high’ category. Real estate and auto repair received 20 and 15%, respectively, in the ‘high’ category. Out of the 10 services included, the only service receiving a rating in the ‘very high’ category was real estate (5%) although it has the lowest level of ‘high’ ratings.

A Spearman rank order correlation of physician ratings for the quality of services with perceived consumer satisfaction indicated a relationship between reports of overall quality of services and perceived consumer satisfaction for 10

166

€3. G. Schutz, K. V. Dim-Knauf and D. S. Judge

Table 5. Quality ratings of 10 services by physicians

Very high High Average Poor Very poor Service category (”/I (”/I (%I (”/.I W I n’

Auto repair Barberkautician Dentist Dry cleaner House painter Lawyer Pest control Physician Plumber Real estate

0 0 0 0 0 0 0 0 0

4.9

15.3 54.2 25.4 50.6 48.1 0.9 75-6 23-5 0.9 46-2 48.7 4.7 28.0 64.0 5.6 26-2 43.7 21-4 24.1 61.4 13-2 79-6 20.0 0-4 32-3 57.5 9-3 19-5 56.2 15.0

5.1 0.4 0

0.4 2-3 8.7 1.4 0

0.9 4.4

236 235 234 234 214 229 220 235 226 226

*Totals differ due to dssing values.

categories of service providers including physician (rho = + 0.81; P < 0-01). Those who think ‘quality of services’ is high also think consumers are satisfied.

The fact that a vast majority of physicians rate perceived consumer satisfaction higher for barberheauticians (96%0), dentists (97%) and dry cleaners (93%) than for physicians, in much the same way as consumers report their own satisfaction would seem to argue for a realistic view by the physicians of their profession (Table 5). Three areas of discrepancy between the perceived satisfaction of consumers by physicians and actual consumer results occur with lower ratings of satisfaction for lawyers, plumbers and real estate by physicians than by consumers. This could be the result of either a misjudgment of consumer experiences by physicians or reflect physicians’ own particularly poor experiences with these occupations. One is tempted to infer that in the case of lawyers it is the actual or potential experience with malpractice suits that contributes to the perceived consumer low satisfaction levels.

Only 11 ‘70 of responding physicians perceive consumer ‘dissatisfaction’ with physician providers, while 80% felt that the quality of service they were providing was ‘high’. From this we can conclude that most physicians perceive consumers as highly satisfied with the services provided by their physician.

The same cross-tabulations were conducted for ‘quality’ as with ‘satisfaction’. Again, the only significant factor was age. The results were more complex in that both younger (20-30) and older (60+) physicians rated their services as higher in quality than middle-aged physicians. Perhaps this is due to differences in societal standards at the time these groups were in medical school and first started their practices.

Although the relationship between ‘satisfaction’ and ‘quality’ is high, there are some interesting differences in the cases of barberbeautician and plumber. These

167

Physicians’ perceptions of consumers’ attitudes

two occupations do not fare as well in perception of quality as they do in perceived consumer satisfaction. This result is most likely due to the fact that satisfaction is strongly related to expectancy and physicians probably do not believe consumers expect a high level of quality from these two services.

Selection criteria

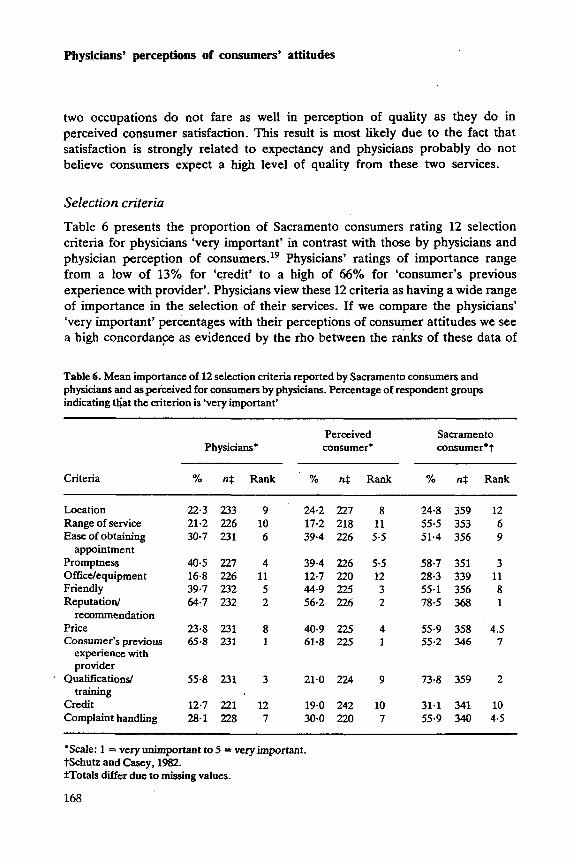

Table 6 presents the proportion of Sacramento consumers rating 12 selection criteria for physicians ‘very important’ in contrast with those by physicians and physician perception of con~umers.’~ Physicians’ ratings of importance range from a low of 13% for ‘credit’ to a high of 66% for ‘consumer’s previous experience with provider’. Physicians view these 12 criteria as having a wide range of importance in the selection of their services. If we compare the physicians’ ‘very important’ percentages with their perceptions of consumer attitudes we see a high concordanFe as evidenced by the rho between the ranks of these data of

Table 6. Mean importance of 12 selection criteria reported by Sacramento consumers and physicians and as perceived for consumers by physicians. Percentage of respondent groups indicating t ~ a t the criterion is ‘very important’

Perceived Sacramento Physicians* consumer* consumer t

Criteria % n$ Rank ‘YO n$ Rank ‘YO n$ Rank

Location Range of service Ease of obtaining

appointment Promptness Officdequipment Friendly Reputation/

recommendation Price Consumer’s previous

experience with provider

. Qualifications/ training

Credit Complaint handling

22.3 233 21.2 226 30.7 231

40.5 227 16-8 226 39.7 232 64.7 232

23.8 231 65-8 231

55-8 231

12.7 221 28.1 228

9 24.2 227 8 24.8 359 12 10 17.2 218 11 55.5 353 6 6 39.4 226 5.5 51.4 356 9

4 39-4 226 5.5 58-7 351 3 11 12.7 220 12 28.3 339 11 5 44.9 225 3 55.1 356 8 2 56.2 226 2 78-5 368 1

8 40.9 225 4 55-9 358 4.5 1 61.8 225 1 55.2 346 7

3 21.0 224 9 73-8 359 2

12 19-0 242 10 31.1 341 10 7 30-0 220 7 55.9 340 4.5

‘Scale: 1 = very unimportant to 5 = very important. tSchutz and b y , 1982. *Totals differ due to missing values.

168

H. G. Schutz, K. V. Diaz-Knauf and D. S. Judge

0.78 (P < 0.01). Physicians generally think that consumers echo their own values. One criterion where there is evidence of a discrepancy is that of ‘qualification/ training’, where physicians themselves rate it as 56% ‘very important’ as compared to their perception of consumers at 21%. The relationship between physicians’ importance ratings for these 12 criteria and actual Sacramento consumer ratings, had a rho of 0.66 (P < 0-02), not quite as high but still quite significant. The physicians’ perceptions of consumer importance and actual Sacramento consumers have lower concordance and were not significant (rho = 0.38, P > 0.1). Those criteria for which there appears to be the greatest discrepancy include ‘range of service’ (physicians’ importance = 21%, their perceptions of consumers = 17%, while 55% of consumers rated it ‘very important’). Here it appears that physicians have misjudged the importance to the consumer of the variety and ‘range of services’ offered by a particular physician as a criterion for the selection of a physician. The same trend holds true for ‘ease of obtaining an appjntment’ which is ‘very important’ to 31% of physicians and 39% perceive it as ‘very important’ by consumers, while 51% of consumers believed it was ‘very important’. ‘Promptness’ in which physicians own the perceived consumer importance levels are 41 and 39%, respectively. With a lower level of difference, however, but in the same order as the previous characteristic, ‘promptness’ is ‘very important’ to 59% of consumers but to only 41% of physicians. Results for ’friendly’ as a criterion are also in the same order as ‘promptness7 with physicians’ and perceived consumers’ importance at 40 and 45% , respectively, whereas consumers actually rate this criterion at 55%.

‘Price’ is an interesting criterion in that physicians rate it fairly low in importance at 24% but believe that consumers perceive it as ‘very important’, 41%, respectively. However, in actuality, consumers rated it even higher in importance at 56%. An opposite trend occurs with the criterion ‘consumer’s previous experience with provider’ where physicians’ and physician-perceived consumer results are quite high in importance at 66 and 62%, respectively, whereas the consumer’s although high, is at a lower level with 55%.

‘Qualificationdtraining’ is another interesting criterion in that consumers’ actual ratings and physicians’ opinions tend to be more alike than what physicians feel consumers perceive. Physicians rate this at a 56% importance level, consumers even higher at 74% while physicians perceive consumers’ importance of this characteristics at only 21%. ‘Credit’ as a criterion falls into an earlier pattern in that physicians own perception and perceived consumer importance at 13 and 19%, respectively, and is much lower than actual consumer importance at 31%. This same pattern follows for ‘complaint handling’ with physicians’ and perceived consumer importance at 28 and 30%, respectively, whereas consumers actually rate this at 56%.

Cross-tabulations with the selected background characteristic, for each criterion both for physicians and perceived consumer importance were computed. For physicians on ‘location’, ‘promptness’, ‘friendliness’, ‘reputation’, ‘previous

169

Physicians’ perceptions of consumers’ attitudes

experience with provider’, and ‘qualificationdtraining’ there were no significant differences for any segment.

Older and independent practice physicians indicated higher importance of ‘range of service’. The ‘independent’ result is certainly due to the fact that they do not have the varied services of a group practice, while the results for older physicians may reflect more traditional beliefs about what patient services are appropriate (or increasing specialization ideology over time).

For ‘ease of appointment’ female physicians in our sample assigned a higher level of importance than their male counterparts. One might ask if female physicians are more sensitive to patients’ ability to obtain appointments than male physicians, or do they receive different feedback from patients in this area than males?

For ‘office equipment’ specialists, older physicians and those in individual practices indicated a lower level of importance than those practicing in group settings. The fac$,that those physicians in independent practice rate this more important is possibly due to the fact that they must have more equipment available than their ‘group member’ counterparts. Also, those physicians practicing in gUl0 settings might not consider an office as important as a physician who has an independent practice where an office is more a reflection of hidher own personality. ‘Price’ was considered more important for females than males, a result which could be related to the possible higher level of sensitivity to patient satisfaction as evidenced in ‘ease of appointment’ importance. For both ‘credit’ and ‘complaint handling’ older physicians had higher importance ratings. Perhaps this is due to a greater opportunity to experience the variation in consumers’ credit needs and areas of problems.

More independent physicians perceive that ‘range of service’ and ‘office equipment’ were important to consumers than do group members. The results are probably due to the same factors mentioned in the physicians’ own opinions mentioned in the previous discussion.

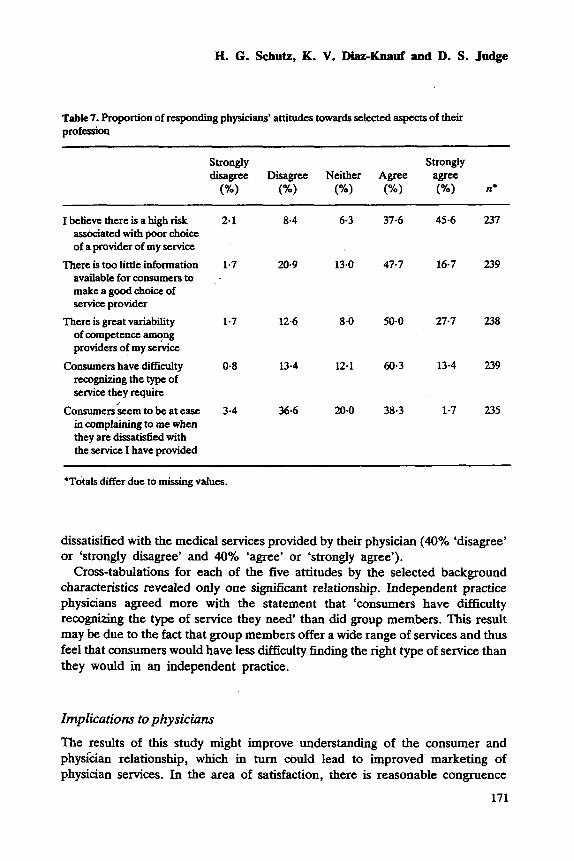

Consumer and physician provider attitudes Physicians were asked a series of attitudinal questions about the relationship between consumers and physician providers (Table 7). Eighty-three per cent of the respondents ‘agree’ or ‘strongly agree’ that there is a high risk associated with poor choice of a physician provider. Sixty-four per cent ‘agree’ or ‘strongly agree’ that there is too little information available for consumers to make a good choice of a physician provider. The majority of respondents feel that there is great variability among physician providers (78% ‘agree’ or ‘strongly agree’). Seventy- four per cent ‘agree’ or ‘strongly agree’ that consumers have difficulty recognizing the type of medical service needed. The sample was equally divided among those who felt that consumers seem to be at ease in complaining to them when

170

H. G. Schutz, I(. V. Dim-Knauf and D. S. Judge

Tabk 7. Proportion of responding physicians’ attitudes towards selected aspects of their profession

Strongly Strongly disagree Disagree Neither Agree agree

(Yo) (%) (“A) (Yo) n*

I believe there is a high risk associated with poor choice of a provider of my service

There is too little information available for consumers to make a good choice of service provider

There is great variability of competence among providers of my service

Consumers have difficulty recognizing the type of service they require

Consumerskem to be at ease in complaining to me when they are dissatisfied with the service I have provided

2.1 8-4 6-3 37.6 45-6 237

1-7 20-9 13.0 47.7 16-7 239

1.7 12.6 8.0 50-0 27.7 238

0.8 13-4 12.1 60.3 13-4 239

3.4 36-6 20-0 38.3 1-7 235

‘Totals differ due to missing values.

dissatisified with the medical services provided by their physician (40% ‘disagree’ or ‘strongly disagree’ and 40% ‘agree’ or ‘strongly agree’).

Cross-tabulations for each of the five attitudes by the selected background characteristics revealed only one significant relationship. Independent practice physicians agreed more with the statement that ‘consumers have difficulty recognizing the type of service they need‘ than did group members. This result may be due to the fact that group members offer a wide range of services and thus feel that consumers would have less difficulty finding the right type of service than they would in an independent practice.

Implications to physicians

The results of this study &ght improve understanding of the consumer and physi‘cian relationship, which in turn could lead to improved marketing of physician services. In the area of satisfaction, there is reasonable congruence

171

Physicians’ perceptions of consumers’ attitudes

between consumers’ and physicians’ satisfaction (both groups indicate approxi- mately 90% satisfaction). One might conclude from this that there is little room for improvement in the quality of physician services since there is such a high level of satisfaction reported. However, we know from other research that satisfaction is highly influenced by expectancy; an alternative explanation could be that consumers are not expecting as much from physician services and thus are relatively satisfied.?’ Some support for this hypothesis derives from the fact that Schutz and Casey report that the level of ‘very high’ and ‘high’ physician quality is rated at only 57%, even though the satisfaction level reported was 90% There appears to be some room for raising the absolute level of perceived quality as one mechanism for increasing the likelihood of selection of a particular physician’s services. It is clear that the approximately 80% high quality satisfaction level reported by physicians about their service is not judged by the consumer at this same high level.

When examining the data for importance of selection criteria we can obtain some insight into those areas in which positive changes might result in improved consumer estimates of quality and satisfaction with physician services. The area of ‘range of service’ would appear to be one which might bear some attention, since there is a major discrepancy between importance to physicians and consumers. It is more difficult to offer an implementation for improvement of this criterion, and obviously for the physician in an individual practice it cannot mean being a specialist in a variety of areas. However, this may indicate a tendency for the consumer to want to utilize either a group practice or an HMO because of the wide range of services offered.

There is some opportunity for improving consumer satisfaction by addressing ‘ease of obtaining appointments’ since this is one area considered more important by consumers than by physicians. Also related to ‘appointments’ is the area of ‘promptness’. Certainly ‘prompt-

ness’ in obtaining appointments (it could be embedded in the previous criterion) would be one consideration, however another aspect that certainly must be considered is the waiting time period in a physician’s office. Clearly, any techniques which would minimize real or perceived waiting time, for example, filling up time with interesting activities such as health education videos in offices would be beneficial to both physicians and consumers.

Some effort to develop a more ‘friendly’ atmosphere might be beneficial. Consumers feel that friendliness is more important than do physicians. The data indicate that ‘reputationhecommendation’ is considered quite important by both physicians and consumers and is perceived at a slightly lower level of importance by physicians of consumers. Thus it would appear some attention given to ways in which this criterion might be communicated to consumers in a more efficient manner would be appropriate.

The area of ‘price’ as might be expected is considered much more important by consumers than by physicians and physicians underestimate its importance to

172

H. G. Schutz, K. V. Diaz-Knauf and D. S. Judge

consumers. It would not appear to be a criterion which is easily changed and perhaps it would be more appropriate to think about value than it would be price with regard to this particular characteristic. Certainly the enhancement of the current trend to be more open about costs would be in order.

The slightly lower degree of importance ascribed to ‘previous experience with the provider’ by consumers than physicians certainly should not lead to the conclusion that individuals do not in any way relate their previous experience to their selection in the future. However, it does seem to indicate a zone of tolerance with regard to this characteristic.

For ‘qualificationdtraining’ the results are interesting in that physicians consider it relatively important; they do not perceive consumers as perceiving it as very important, but consumers actually rate this characteristic the second highest in importance. Certainly the display of credentials around examination rooms and offices has been a typical method for communicating ‘qualifications and training’. Perhaps there aje other ways in which this type of information might be disseminated through a small vita, for example, or through some discussion between physician and consumer.

Not surprisingly, ‘credit’ was considered relatively unimportant by physicians and they1perceived consumers as not seeing this as very important. However, although it is not rated highly important by Consumers, it is clearly higher than the physicians’ ratings. Perhaps the use of credit cards and other forms of delayed payment are more important than physicians realize.

The last characteristic, ‘complaint handling’, is considered relatively unimpor- tant by physicians and perceived as unimportant by consumers by physicians, whereas it actually has a fairly high level of importance for consumers. This is a difficult characteristic to deal with. However, it would appear that discussion of the procedures by which consumers might express their dissatisfaction, which are presented early in the physiciadconsumer relationship would be a good idea.

Generally supportive of the comments made above are the fact that physicians overwhelmingly agreed that there is a high risk associated with a poor choice of their service. Thus those activities, which might lead to better or more appropriate choices, would certainly seem to be in order. The fact that physicians also overwhelmingly agree that consumers have difficulty in recognizing the type of service they need, and that there is great variability of competence among the providers, as well as too little information available, would seem to argue for some educational development by individual physicians or the profession as a whole so as to improve the informed consumer aspect of physician selection. The results of the question about the ease in which consumers have in complaining is more bipolar in nature and would indicate that at least some physicians feel this is something that consumers do rather easily whereas others do not agree. Whether this is the actual feeling of their patients or the perceptions of the physicians obviously cannot be determined from our data.

173

Physicians’ perceptions of consumers’ attitudes

In general, it appears there are several areas where knowledge of physicians’ attitudes andor the discrepancy between their attitudes and consumers’ could lead to the development of procedures that might improve the perceived quality of services and consumer satisfaction.

Acknowledgments

This research was supported by a Faculty Research Grant from the University of California at Davis and by a grant from the Center for Consumer Research, University of California at -Davis.

References ,, 1. Kelly, J.P., George, W.R. & Becherer, R.C. (1988) The retailing of health care services.

Journal of Consumer Satisfaction, Dissatisfaction and Complaining Behavior, 1, 38- 42.

2. Shopping fo; a new doctor. (June 1986) Changing Times, 40, 47-52. 3. Fees have little effect on choice of MD. February 18,1985 American Medical News, 28,41. 4. Rust, M. (April 26, 1985) Changes in market seen restructuring physicians’ practices.

American Medical News, 1. 3. 5 . Cousins, N. (1985) How patients appraise physicians. Occasional notes. New England

Journal of Medicine, 313, 1422-1424. 6. Jensen, J. & Miklovic, N. (January 17, 1986) Consumers cite physicians’ interest as most

important factor in selection. Modern Healthcare, 2 , 48-49. 7. Schutz, H.G. & Judge, D.S. (1983) Selected evaluative criteria importance in the choice of

service providers. Proceedings of the Division of Consumer Psychology, (Ed. by J. C. Anderson), pp. 111-114. American Psychological Association, 1983 Annual Convention in Anaheim, CA.

8. Hill, D. (1986) Satisfaction and consumer services. Advances in Consumer Research, 13,

9. Quelch, J.A. & Ash, S.B. (1981) Consumer satisfaction with professional services. In Marketing of Services (Ed. by J. H. Donnelly and W. R. George), pp. 82-85. Proceedings of the American Marketing Association, Special Conference on Services Marketing in Orlando, FL.

10. Schutz, H.G. & Judge, .D.S. (1986) Consumer satisfaction with physicians. Proceedings Advances in Health Care Research Conference (Ed. by M. Venkatesan and S. Lancaster). pp. 49-52. American Association for Advances in Health Care Research, Meetings, Snowbird, Utah.

11. Dillman, D.A. (1976) Mail and Telephone Surveys: The Total Design Method, John Wiley and Sons, New York, NY.

12. Leslie, L.L. (1972) Are high response rates essential to valid surveys? Social Science Research, 1, 325-334.’

13. Nie, N.H. et al. (1975) Srarirtical Package for the Social Sciences, McGraw Hill Company, New York, NY.

14. (1988) SPSSX User’s Guide, 3rd Edition. SPSS Inc. Chicago, IL.. 15. Schutz, H.G. & Casey, M. (1982) Consumersatisfaction with occupational services: Quality,

174

31 1-315.

H. G . Schutz, K. V. Dim-Knauf and D. S . Judge

frequency, attitudes, and information sources. Proceedings, Consumer Satisfaction (Ed. by R. L. Day and K. Hunt), pp. 81-86. Dissatisfaction and Complaining Behavior Conference, Knoxville, TN.

16. Zbid. 17. Schutz. H.G. (1979) California Consumers' Satisfaction with Goods anddervices: Problems,

Actions and Attitudes, pp. 12-46. (A report to the Director of Consumer Affairs), University of California, Davis, CA.

18. Schutz, H.G. & Judge, D.S., op. cit. 19. Schutz, H.G. & Casey, M., op. cir. 20. Zbid. 21. Ibid.

175