Embed Size (px)

Citation preview

Poverty Reduction Through Financial Inclusion

National Team for Acceleration of Poverty Reduction (TNP2K)Office of Vice President, Republik Indonesia

MARCH 2016

Elan SatriawanHead of Policy Working Group

2|

• Indonesia has famously known as one success story in poverty reduction: cut more than halved poverty during period 1976-1996.

• The crisis 1997/98 deviate the declining trend, but since early 2000, Indonesia was back on the trend until now

• Post 2000 trend in poverty reduction effort however has been characterized by slowing down of the reduction and increase in inequality

• While many ways can be done to address the two, financial inclusion is one of the main effort• Access to finance for the poor will arguably improve productivity• Financial inclusion targeting the poor and vulnerable associates with

more inclusive growth and development• This will explain the situation on access to finance among the

poor and general society, what has been done, and what the remaining challenges.

Background

3|

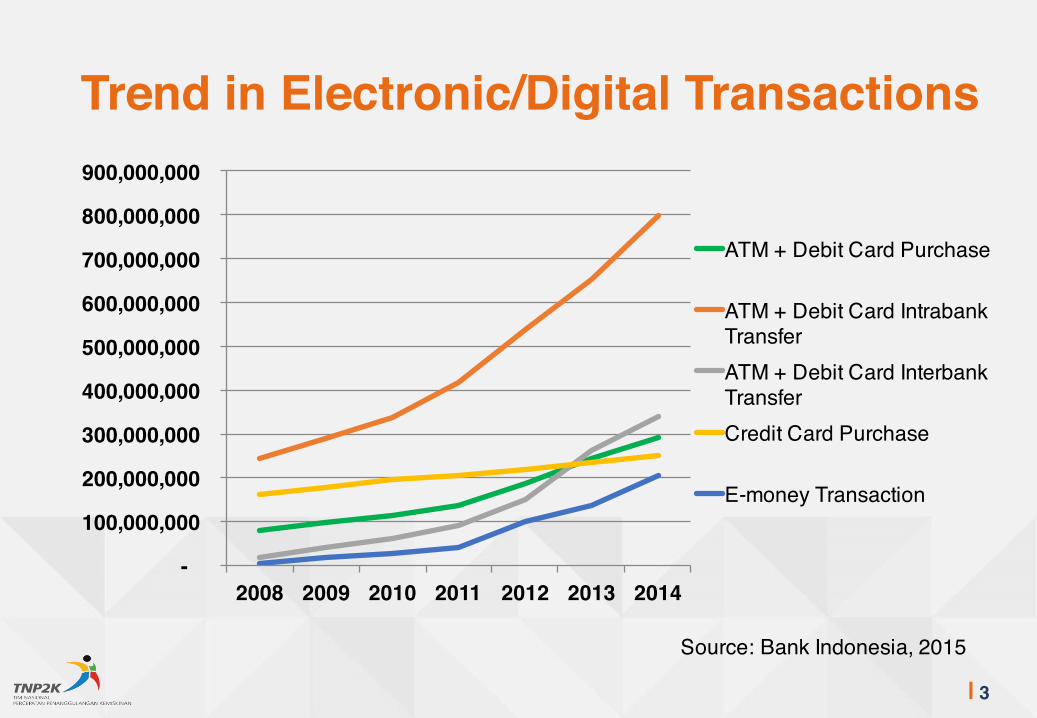

Trend in Electronic/Digital Transactions

-

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

800,000,000

900,000,000

2008 2009 2010 2011 2012 2013 2014

ATM + Debit Card Purchase

ATM + Debit Card Intrabank TransferATM + Debit Card Interbank TransferCredit Card Purchase

E-money Transaction

Source: Bank Indonesia, 2015

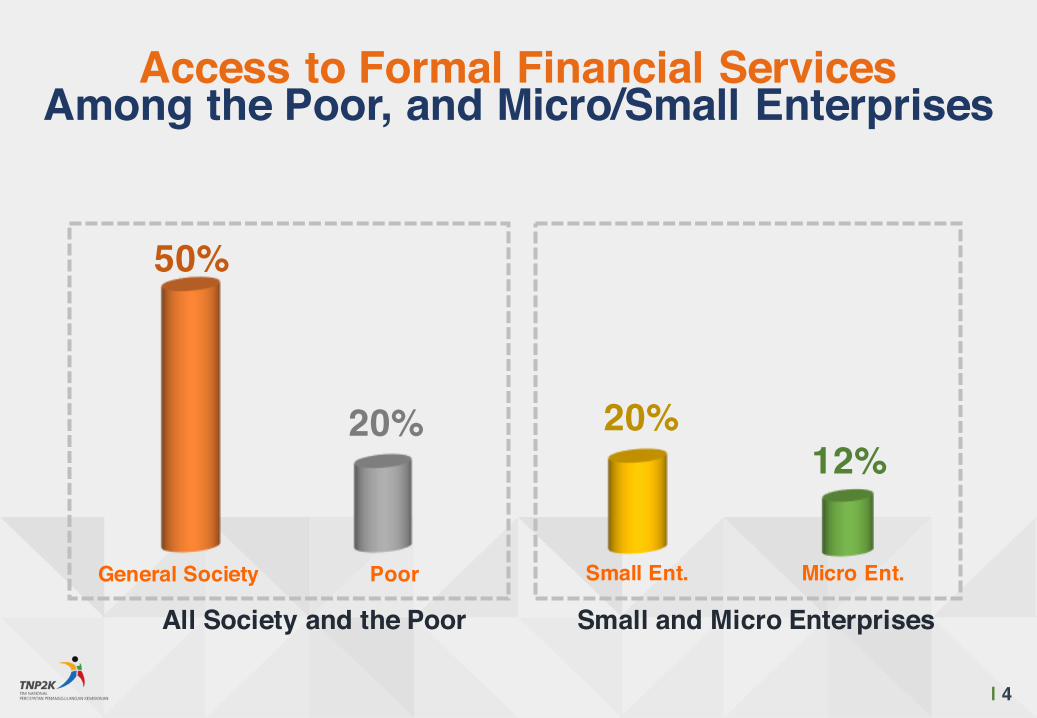

All Society and the Poor Small and Micro Enterprises

| 4

General Society

20%

50%

Poor Small Ent.

12%20%

Micro Ent.

Access to Formal Financial ServicesAmong the Poor, and Micro/Small Enterprises

5|

Using Cashless Services for Distribution of Social Assistance Benefits.

6|

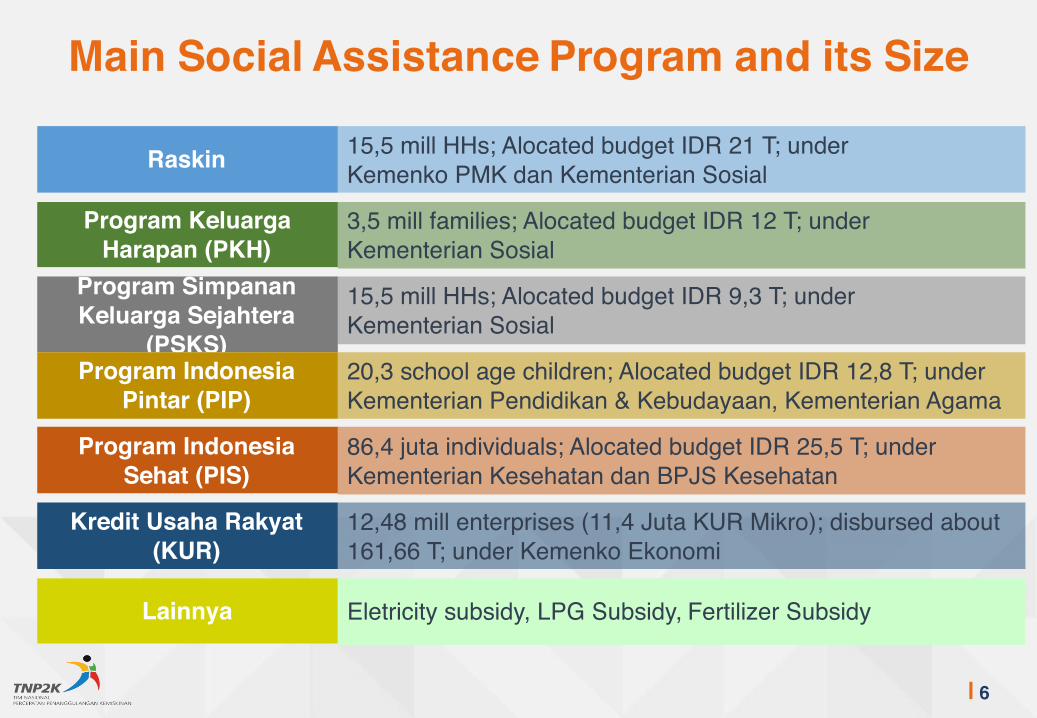

Raskin

Program KeluargaHarapan (PKH)

Program SimpananKeluarga Sejahtera

(PSKS)Program Indonesia

Pintar (PIP)

Program Indonesia Sehat (PIS)

Kredit Usaha Rakyat (KUR)

15,5 mill HHs; Alocated budget IDR 21 T; underKemenko PMK dan Kementerian Sosial

3,5 mill families; Alocated budget IDR 12 T; underKementerian Sosial

15,5 mill HHs; Alocated budget IDR 9,3 T; underKementerian Sosial

20,3 school age children; Alocated budget IDR 12,8 T; underKementerian Pendidikan & Kebudayaan, Kementerian Agama

86,4 juta individuals; Alocated budget IDR 25,5 T; underKementerian Kesehatan dan BPJS Kesehatan

12,48 mill enterprises (11,4 Juta KUR Mikro); disbursed about 161,66 T; under Kemenko Ekonomi

Lainnya Eletricity subsidy, LPG Subsidy, Fertilizer Subsidy

Main Social Assistance Program and its Size

7|

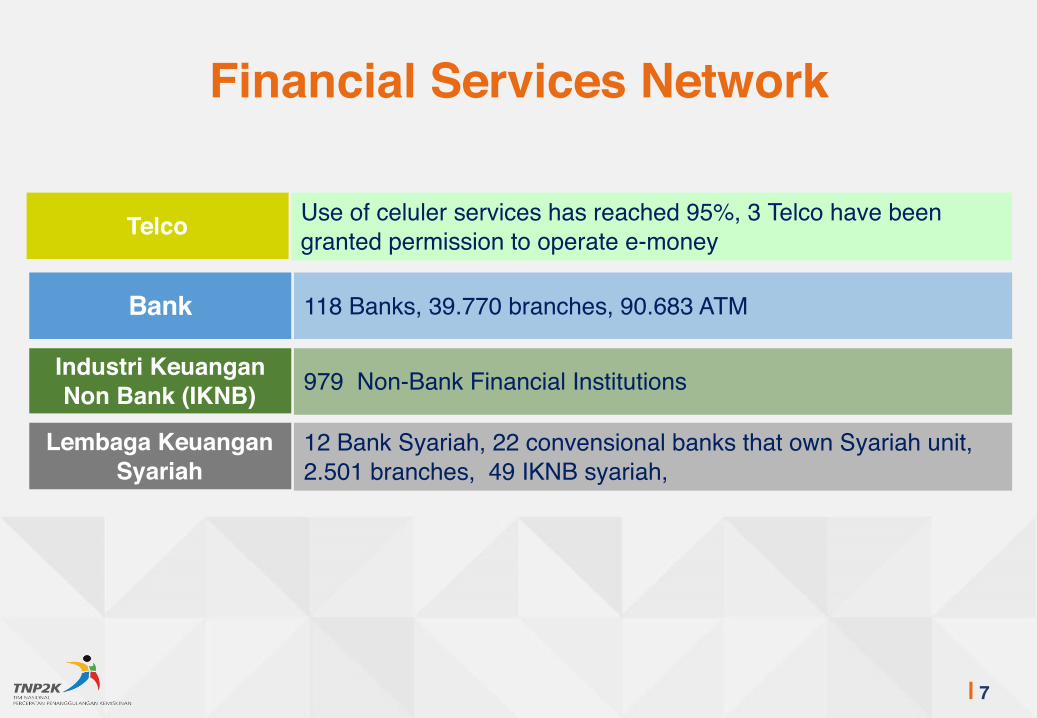

Bank

Industri KeuanganNon Bank (IKNB)

Lembaga KeuanganSyariah

118 Banks, 39.770 branches, 90.683 ATM

979 Non-Bank Financial Institutions

12 Bank Syariah, 22 convensional banks that own Syariah unit, 2.501 branches, 49 IKNB syariah,

Telco Use of celuler services has reached 95%, 3 Telco have been granted permission to operate e-money

Financial Services Network

8|

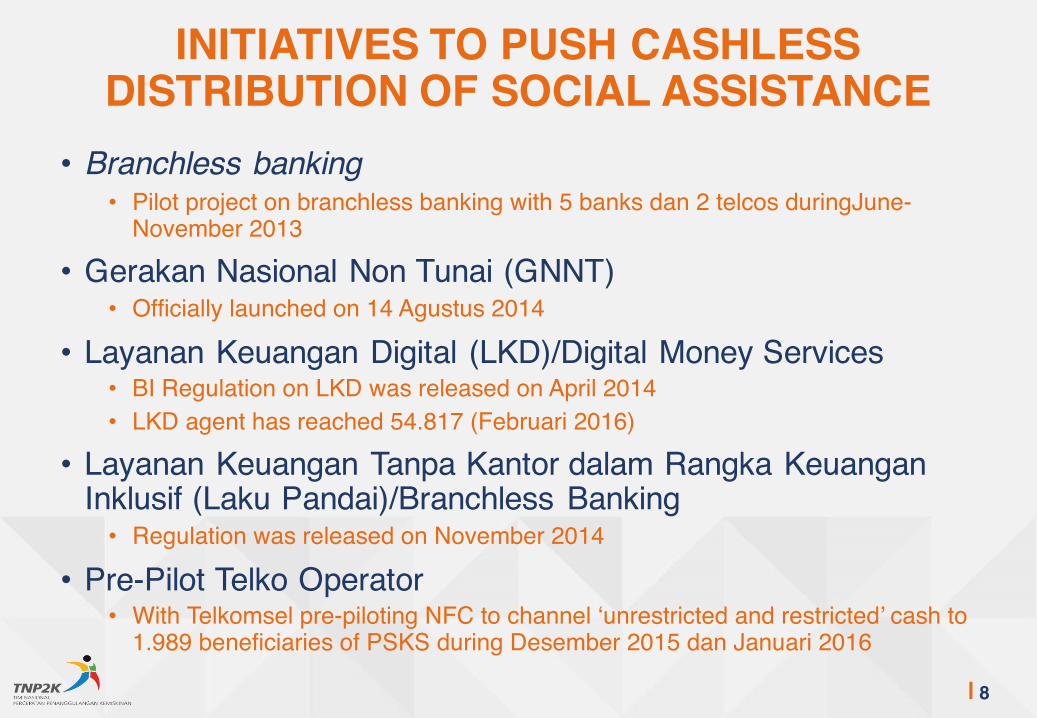

• Branchless banking• Pilot project on branchless banking with 5 banks dan 2 telcos duringJune-

November 2013

• Gerakan Nasional Non Tunai (GNNT)• Officially launched on 14 Agustus 2014

• Layanan Keuangan Digital (LKD)/Digital Money Services• BI Regulation on LKD was released on April 2014• LKD agent has reached 54.817 (Februari 2016)

• Layanan Keuangan Tanpa Kantor dalam Rangka Keuangan Inklusif (Laku Pandai)/Branchless Banking• Regulation was released on November 2014

• Pre-Pilot Telko Operator• With Telkomsel pre-piloting NFC to channel ‘unrestricted and restricted’ cash to

1.989 beneficiaries of PSKS during Desember 2015 dan Januari 2016

INITIATIVES TO PUSH CASHLESS DISTRIBUTION OF SOCIAL ASSISTANCE

9|

• Program Keluarga Harapan (PKH)• Pilot on distribution of PKH benefits using LKD through individual agents

on Oktober 2014• 1.860 beneficiaries in Cirebon, Pasuruan, Jakarta, and Kupang• BRI and Bank Mandiri as implementing banks

• Program Simpanan Keluarga Sejahtera (PSKS)• Pilot on distribution of PSKS benefit using LKD through PT Pos

Indonesia during November 2014-Maret 2015• 1.023.553 beneficiaries PSKS in 19 Kabupaten/Kota• Bank Mandiri as implementing bank

• Program Indonesia Pintar (PIP)• Pushing the use of virtual account, TabunganKu dan SimPel, as a way

to distribute PIP benefits• BRI and BNI as implementing banks

FINANCIAL INCLUSION RELATED INIATIVES ON EXISTING PROGRAM

10|

Improving Access to Credit for Micro and Small Enterprises

11|

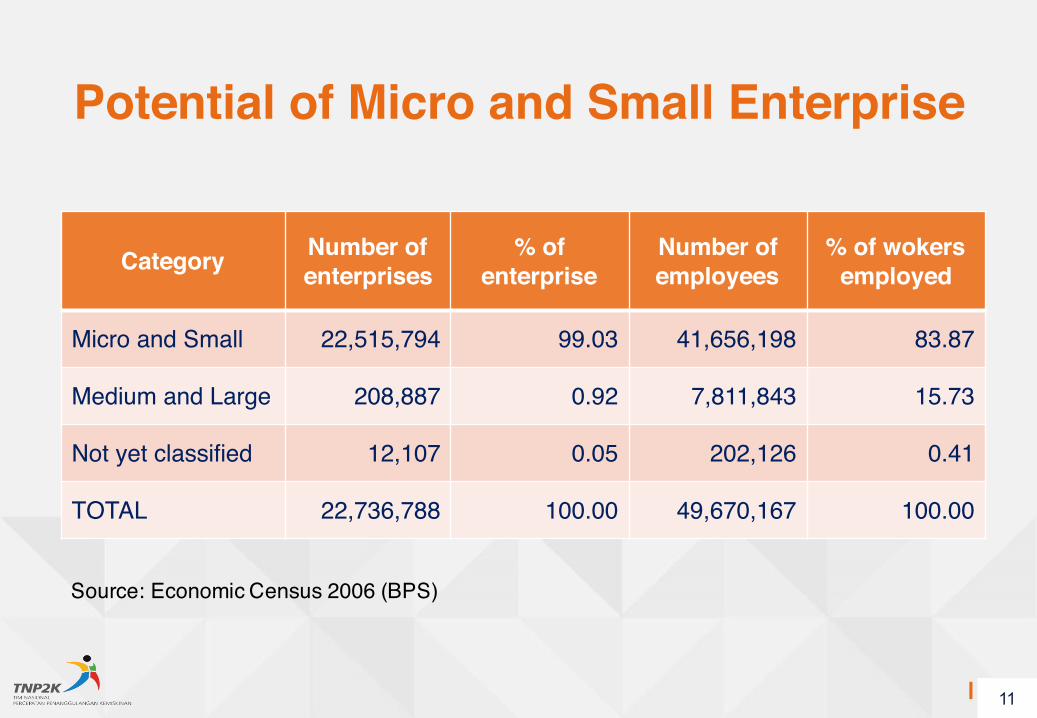

Category Number of enterprises

% of enterprise

Number of employees

% of wokersemployed

Micro and Small 22,515,794 99.03 41,656,198 83.87

Medium and Large 208,887 0.92 7,811,843 15.73

Not yet classified 12,107 0.05 202,126 0.41

TOTAL 22,736,788 100.00 49,670,167 100.00

Source: Economic Census 2006 (BPS)

11

Potential of Micro and Small Enterprise

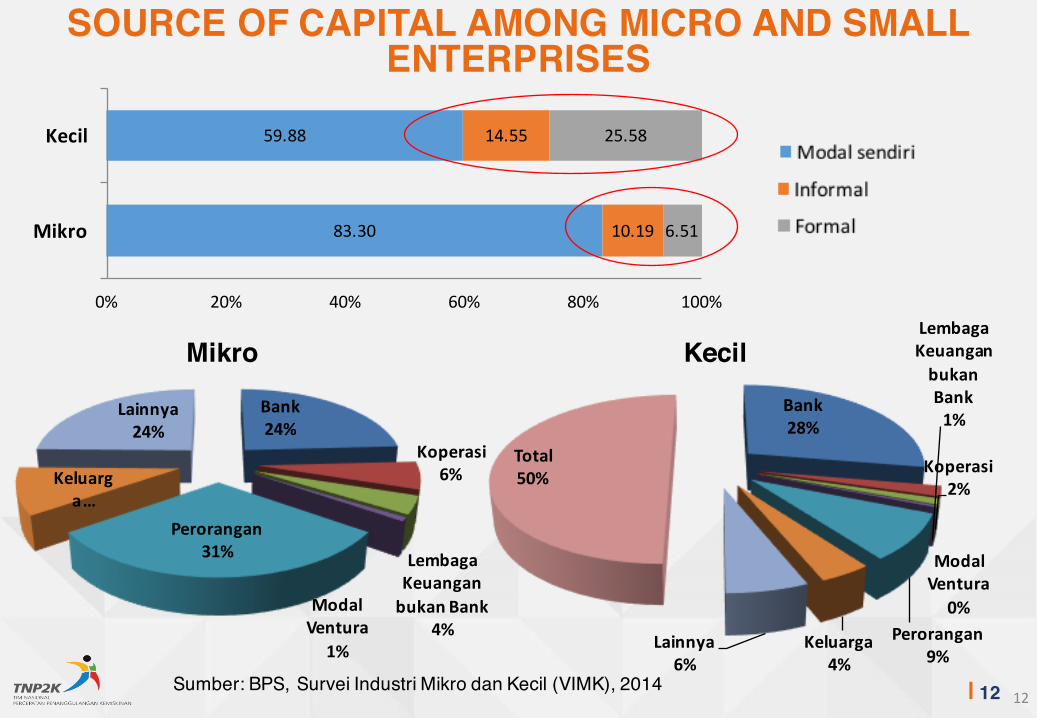

12|Sumber: BPS, Survei Industri Mikro dan Kecil (VIMK), 201412

83.30

59.88

10.19

14.55

6.51

25.58

0% 20% 40% 60% 80% 100%

Mikro

Kecil

Bank24%

Koperasi6%

Lembaga Keuangan bukan Bank

4%Modal Ventura

1%

Perorangan31%

Keluarga…

Lainnya24%

Mikro

Bank28%

Koperasi2%

Lembaga Keuangan bukan Bank1%

Modal Ventura

0%Perorangan

9%Keluarga

4%Lainnya

6%

Total50%

Kecil

SOURCE OF CAPITAL AMONG MICRO AND SMALL ENTERPRISES

13|Sumber: BPS, Survei Industri Mikro dan Kecil (VIMK), 2014

13

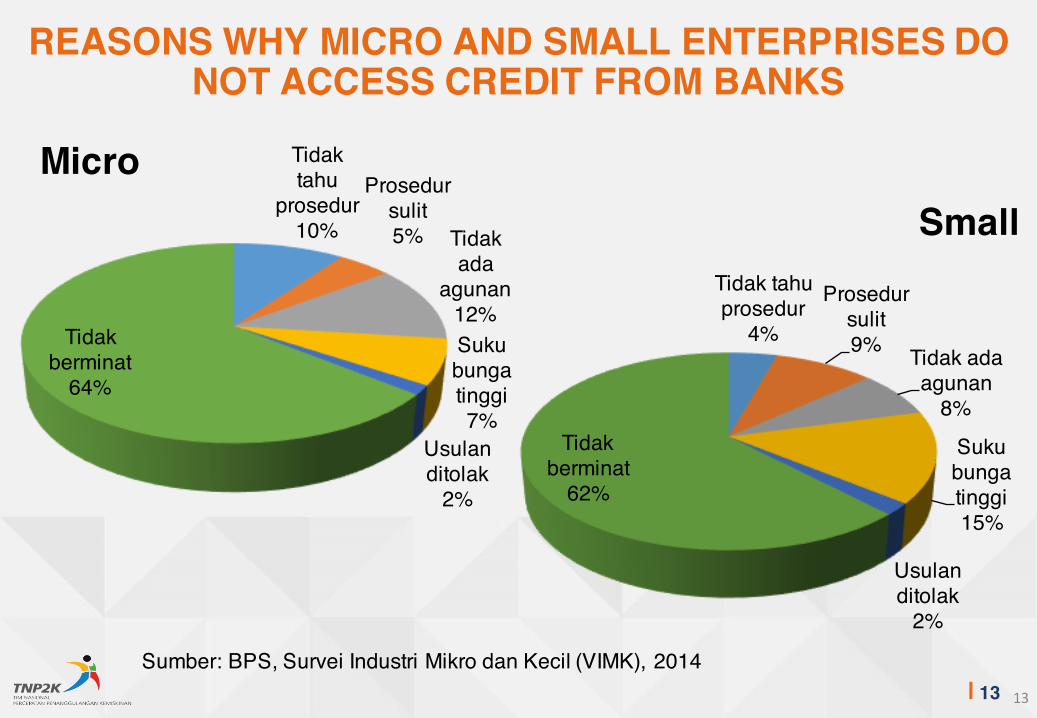

Tidak tahu

prosedur10%

Prosedur sulit5% Tidak

ada agunan

12%Suku bunga tinggi7%

Usulan ditolak

2%

Tidak berminat

64%

Micro

Tidak tahu prosedur

4%

Prosedur sulit9% Tidak ada

agunan8%

Suku bunga tinggi15%

Usulan ditolak

2%

Tidak berminat

62%

Small

REASONS WHY MICRO AND SMALL ENTERPRISES DO NOT ACCESS CREDIT FROM BANKS

14|

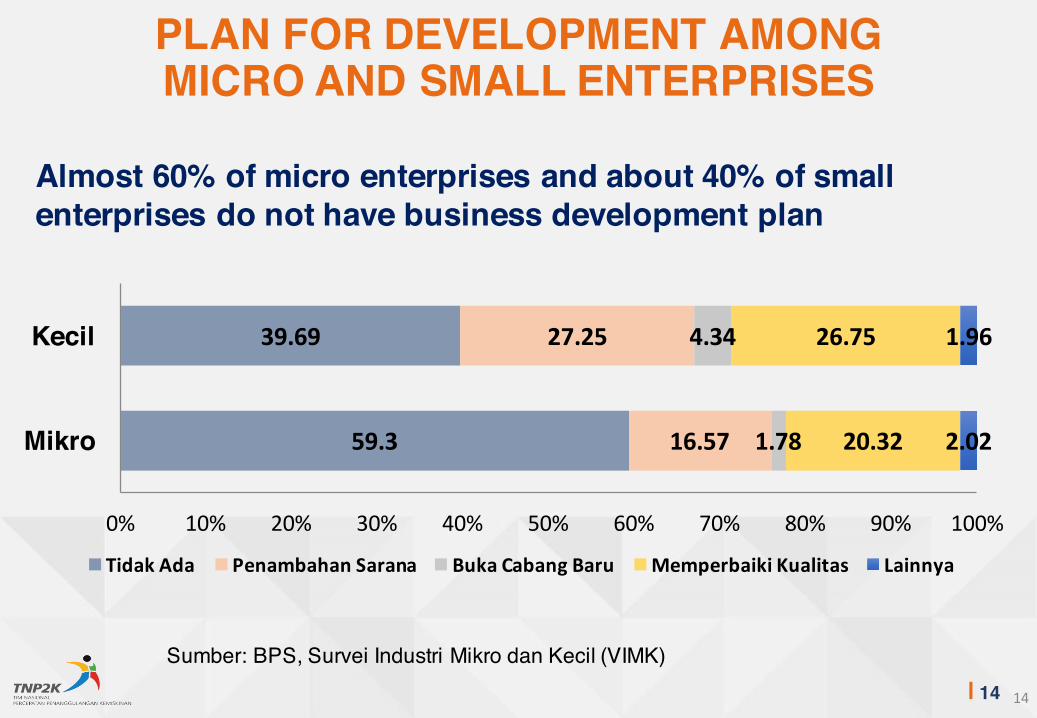

Almost 60% of micro enterprises and about 40% of small enterprises do not have business development plan

59.3

39.69

16.57

27.25

1.78

4.34

20.32

26.75

2.02

1.96

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Mikro

Kecil

Tidak Ada Penambahan Sarana Buka Cabang Baru Memperbaiki Kualitas Lainnya

Sumber: BPS, Survei Industri Mikro dan Kecil (VIMK)

14

PLAN FOR DEVELOPMENT AMONG MICRO AND SMALL ENTERPRISES

15|

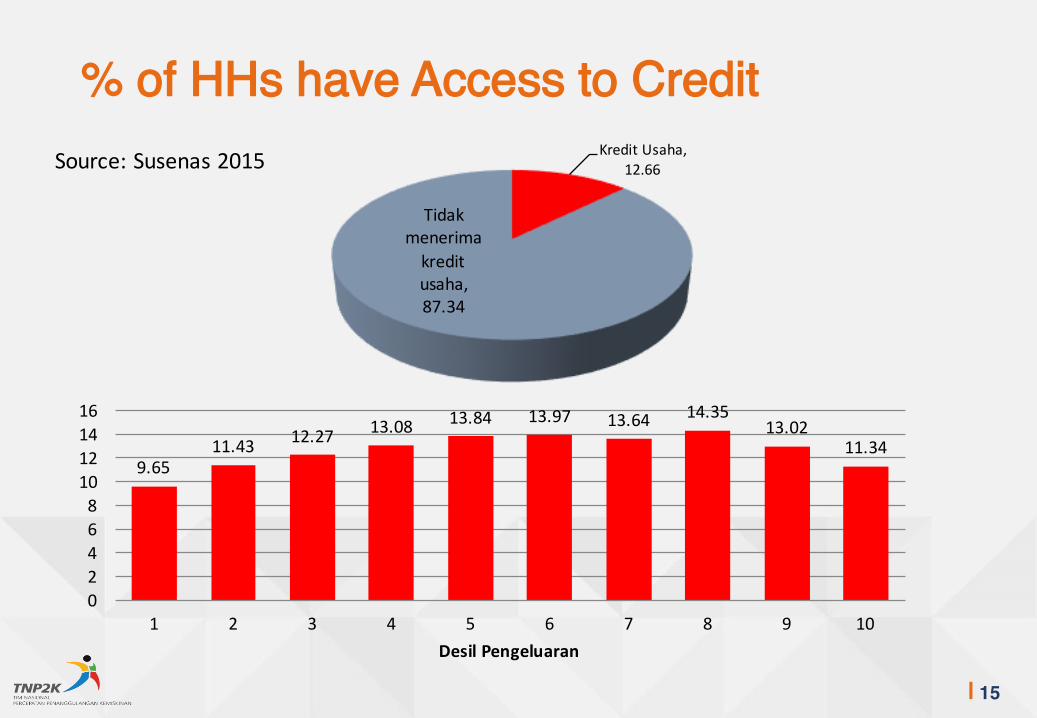

% of HHs have Access to Credit

9.6511.43 12.27 13.08 13.84 13.97 13.64 14.35

13.0211.34

0246810121416

1 2 3 4 5 6 7 8 9 10Desil Pengeluaran

Kredit Usaha, 12.66

Tidak menerima kredit usaha, 87.34

Source: Susenas 2015

16|

INISIATIF YANG SUDAH DILAKUKANKREDIT

• Credit Rating• Telah dilakukan Pilot Project, penelitian dan serangkaian sosialisasi

terkait dengan pemeringkatan UKM.

• Perusahaan Penjamin Kredit Daerah (PPKD)/Regional Credit Guarantee Agency• Telah dilakukan fasilitasi dalam rangka pembentukan PPKD di beberapa

daerah yang memungkinkan.• Terdapat 16 PPKD yang didirikan di beberapa daerah.

• Kredit Usaha Rakyat (KUR)• Penyaluran KUR dengan sasaran unbankable UMKM • 12,48 Juta Debitur (11,4 Juta KUR Mikro); • 178,838 Triliun sudah tersalurkan (2007 – 2014)

• KUR TKI• 2011 – 2014: Penyaluran sebesar 52,437 miliar rupiah, sebanyak 3.629

debitur

17|

PROGRAM KREDIT USAHA RAKYAT (KUR)

18

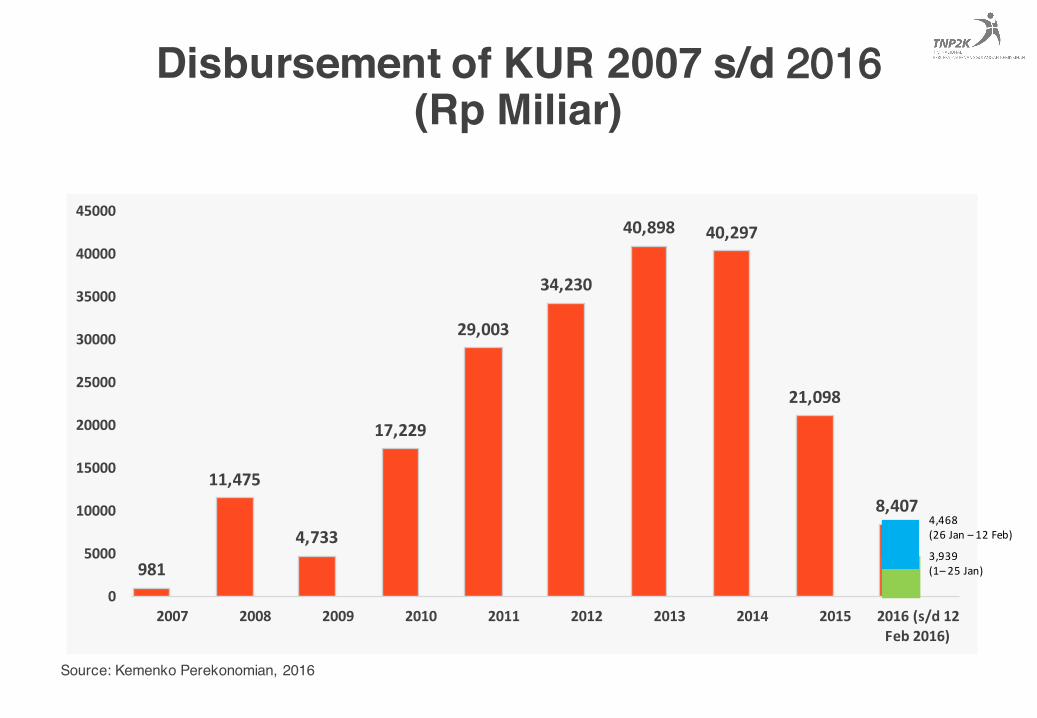

Disbursement of KUR 2007 s/d 2016 (Rp Miliar)

981

11,475

4,733

17,229

29,003

34,230

40,898 40,297

21,098

8,407

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 (s/d 12 Feb 2016)

Source: Kemenko Perekonomian, 2016

4,468 (26 Jan – 12 Feb)

3,939(1– 25 Jan)

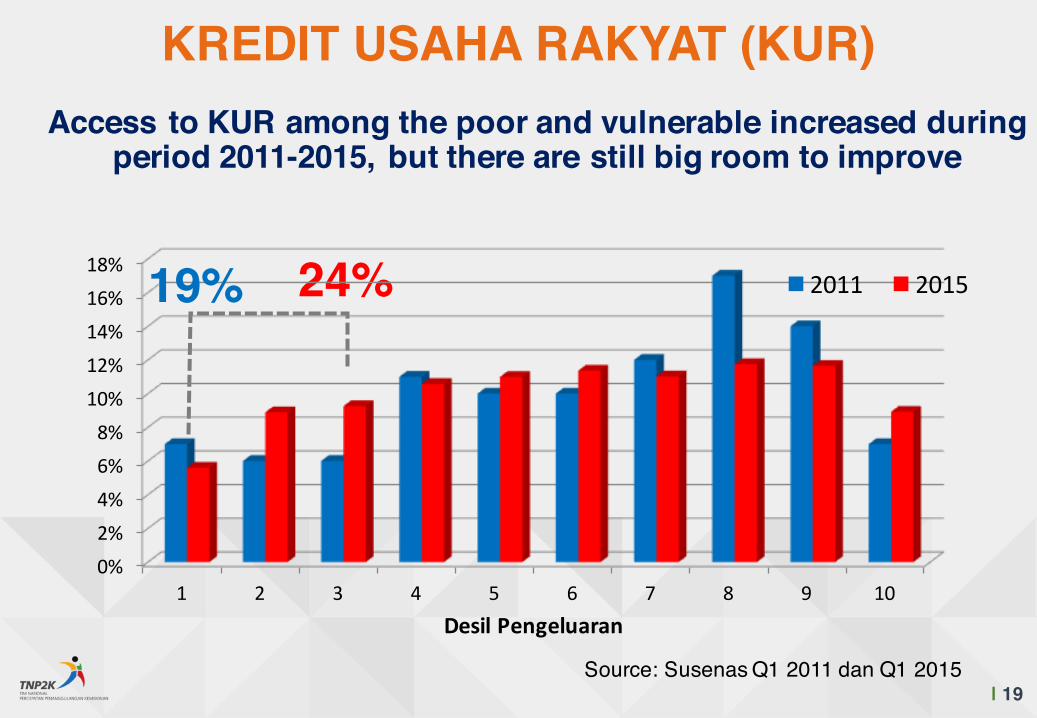

19| | 19Source: Susenas Q1 2011 dan Q1 2015

24%

Access to KUR among the poor and vulnerable increased during period 2011-2015, but there are still big room to improve

0%2%4%6%8%10%12%14%16%18%

1 2 3 4 5 6 7 8 9 10Desil Pengeluaran

2011 2015

KREDIT USAHA RAKYAT (KUR)

19%

20

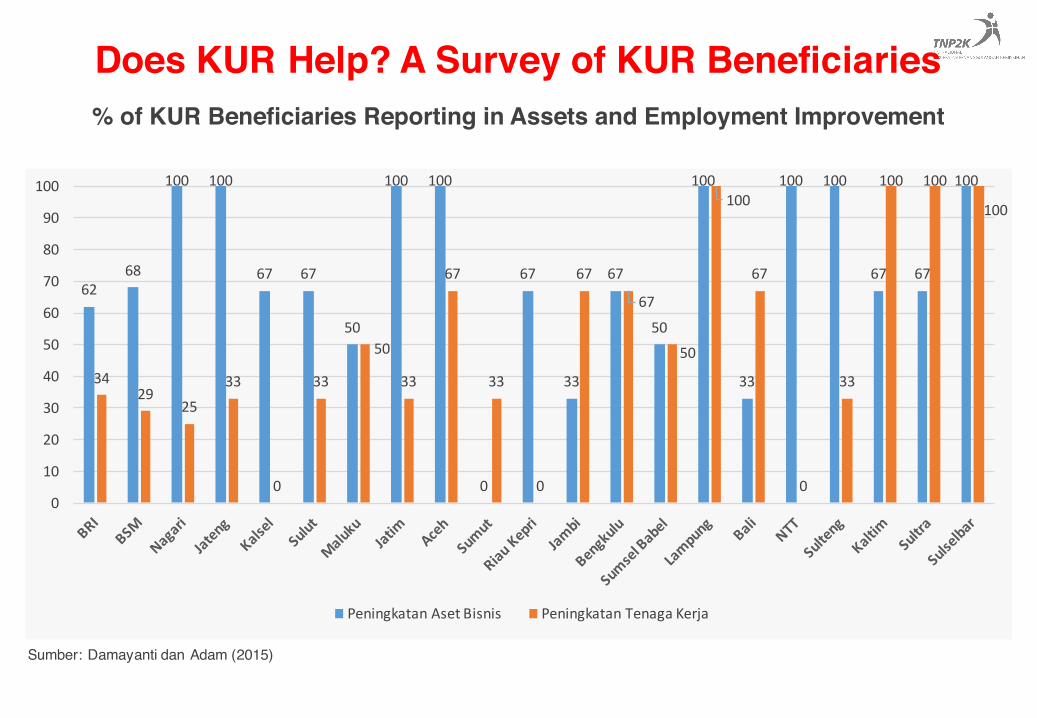

Does KUR Help? A Survey of KUR Beneficiaries

Sumber: Damayanti dan Adam (2015)

% of KUR Beneficiaries Reporting in Assets and Employment Improvement

6268

100 100

67 67

50

100 100

0

67

33

67

50

100

33

100 100

67 67

100

3429

2533

0

33

50

33

67

33

0

67

67

50

100

67

0

33

100 100

100

0

10

20

30

40

50

60

70

80

90

100

Peningkatan Aset Bisnis Peningkatan Tenaga Kerja

21

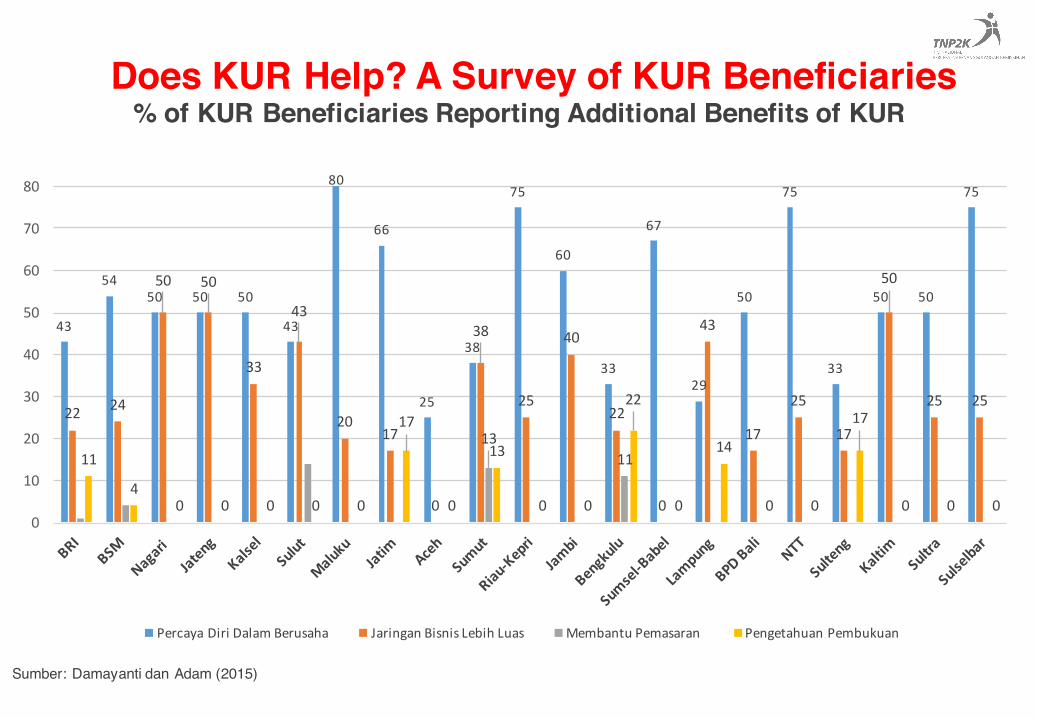

% of KUR Beneficiaries Reporting Additional Benefits of KUR

43

5450 50 50

43

80

66

25

38

75

60

33

67

29

50

75

33

50 50

75

22 24

50 50

33

43

2017

0

38

25

40

22

0

43

17

25

17

50

25 25

131111

40 0 0 0 0

17

0

13

0 0

22

0

14

0 0

17

0 0 00

10

20

30

40

50

60

70

80

Percaya Diri Dalam Berusaha Jaringan Bisnis Lebih Luas Membantu Pemasaran Pengetahuan Pembukuan

Sumber: Damayanti dan Adam (2015)

Does KUR Help? A Survey of KUR Beneficiaries

22

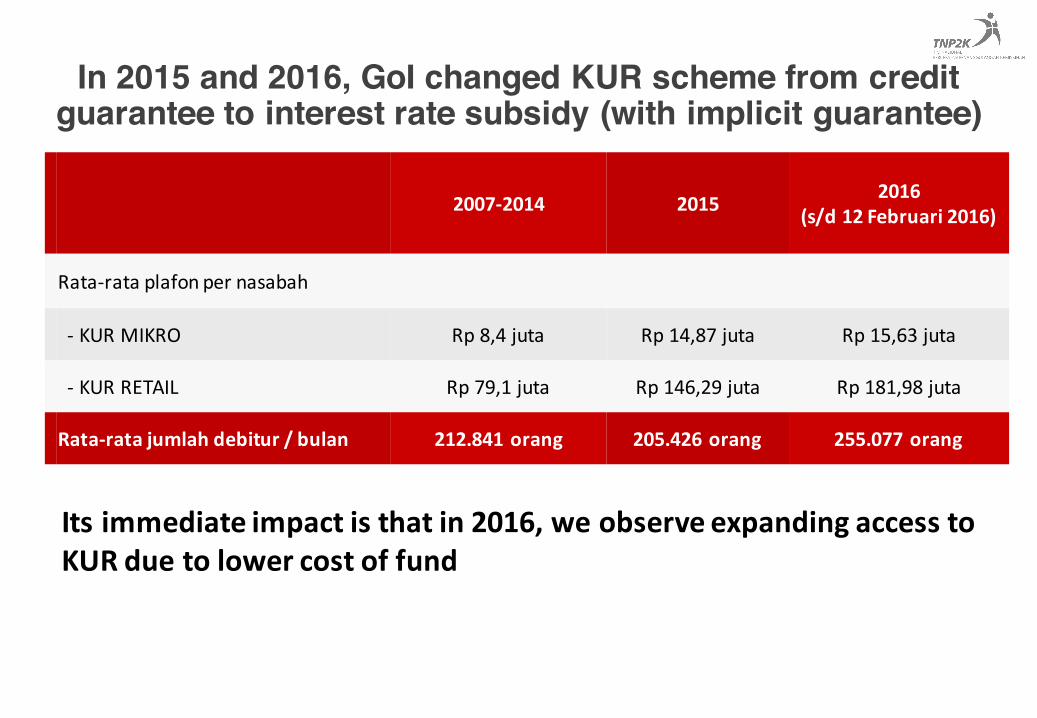

In 2015 and 2016, GoI changed KUR scheme from credit guarantee to interest rate subsidy (with implicit guarantee)

2007-‐2014 2015 2016 (s/d 12 Februari 2016)

Rata-‐rata plafon per nasabah

-‐ KUR MIKRO Rp 8,4 juta Rp 14,87 juta Rp 15,63 juta

-‐ KUR RETAIL Rp 79,1 juta Rp 146,29 juta Rp 181,98 juta

Rata-‐rata jumlah debitur / bulan 212.841 orang 205.426 orang 255.077 orang

Its immediate impact is that in 2016, we observe expanding access to KUR due to lower cost of fund

23|

ACEH

SUMATERA UTARA

SUMATERA BARAT

RIAU

JAMBISUMATERA SELATAN

BENGKULU

LAMPUNG

KEPULAUAN BANGKA BELITUNG

KEPULAUAN RIAU

DKI JAKARTA

JAWA BARAT

JAWA TENGAHD I YOGYAKARTA

JAWA TIMUR

BANTEN

BALI

NUSA TENGGARA BARAT

NUSA TENGGARA TIMUR

KALIMANTAN BARAT

KALIMANTAN TENGAH

KALIMANTAN SELATAN

KALIMANTAN TIMUR

KALIMANTAN UTARA SULAWESI UTARASULAWESI TENGAH

SULAWESI SELATAN

SULAWESI TENGGARA

GORONTALOSULAWESI BARAT

MALUKU

MALUKU UTARAPAPUA BARAT

0

20

40

60

80

100

0 10 20 30 40 50 60 70 80 90 100

12

3 4

% Villages with enterprise receiving KUR in a Province

% S

ubdi

stric

tsw

ith p

rese

nce

of B

anks

in a

pr

ovin

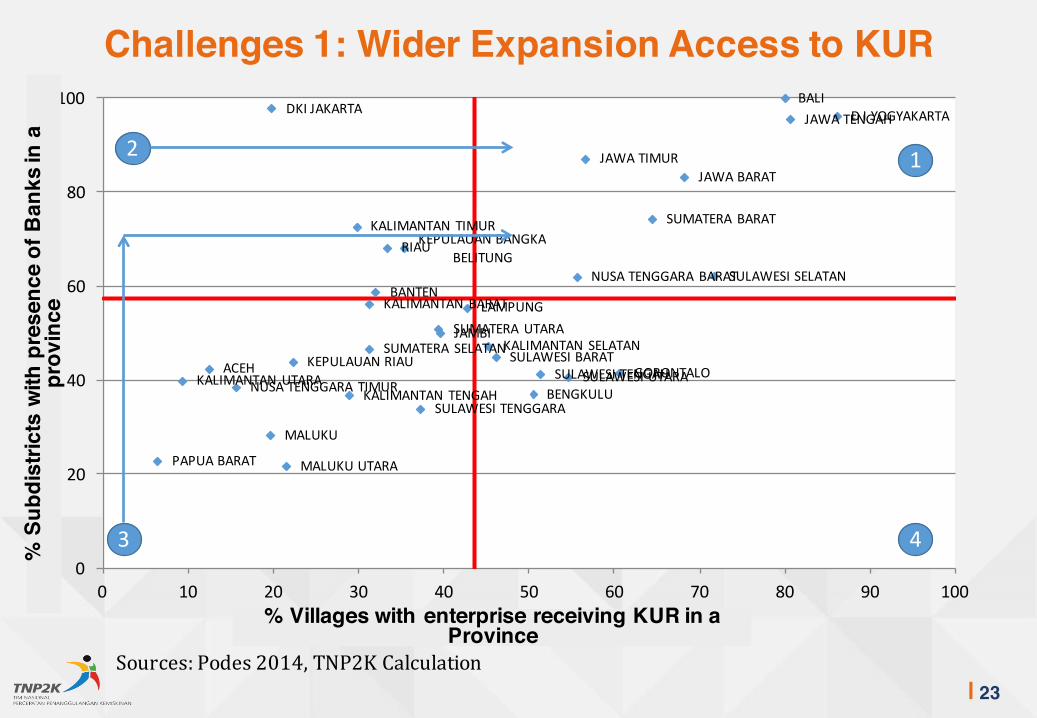

ceChallenges 1: Wider Expansion Access to KUR

Sources: Podes 2014, TNP2K Calculation

24|

ACEH

SUMATERA UTARA

SUMATERA BARAT

RIAU

JAMBI

SUMATERA SELATAN

BENGKULU

LAMPUNG

KEPULAUAN BANGKA BELITUNG

KEPULAUAN RIAUDKI JAKARTA

JAWA BARAT

JAWA TENGAH

D I YOGYAKARTA

JAWA TIMUR

BANTEN

BALI

NUSA TENGGARA BARAT

NUSA TENGGARA TIMUR

KALIMANTAN BARATKALIMANTAN TENGAH

KALIMANTAN SELATAN

KALIMANTAN TIMUR

KALIMANTAN UTARA

SULAWESI UTARASULAWESI TENGAH

SULAWESI SELATAN

SULAWESI TENGGARA

GORONTALO

SULAWESI BARAT

MALUKUMALUKU UTARA

PAPUA BARATPAPUA

0

20

40

60

80

100

20 25 30 35 40 45 50% of Self-Employed in the Province

% V

illag

es w

ith E

nter

pise

sre

ceiv

ing

KU

R in

a p

rovi

nce

(%)

24

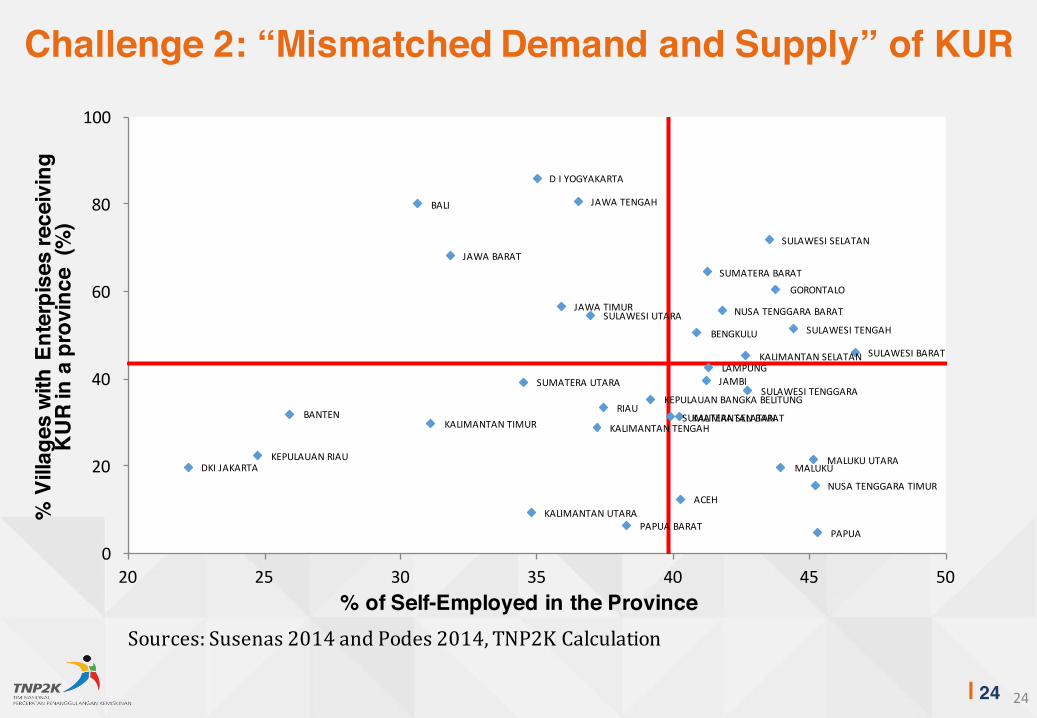

Challenge 2: “Mismatched Demand and Supply” of KUR

Sources: Susenas 2014 and Podes 2014, TNP2K Calculation

25|

• Does new KUR policy help to wider access –toward outer islands and non-existing beneficiaries?• Does involve non-bank as KUR participating

agencies help to reach the poor and vulnerable?• Does current policy lead to crowding out of non-

KUR credits –both within the same implementing bank or inter-credit agencies?

Some Remaining Questions to Explore

Terima Kasih