Embed Size (px)

Citation preview

CORPORATE DIVISION

Vittorio Ogliengo

2

AGENDA

The new Corporate Division

Strategic guidelines and business model

Key targets

3

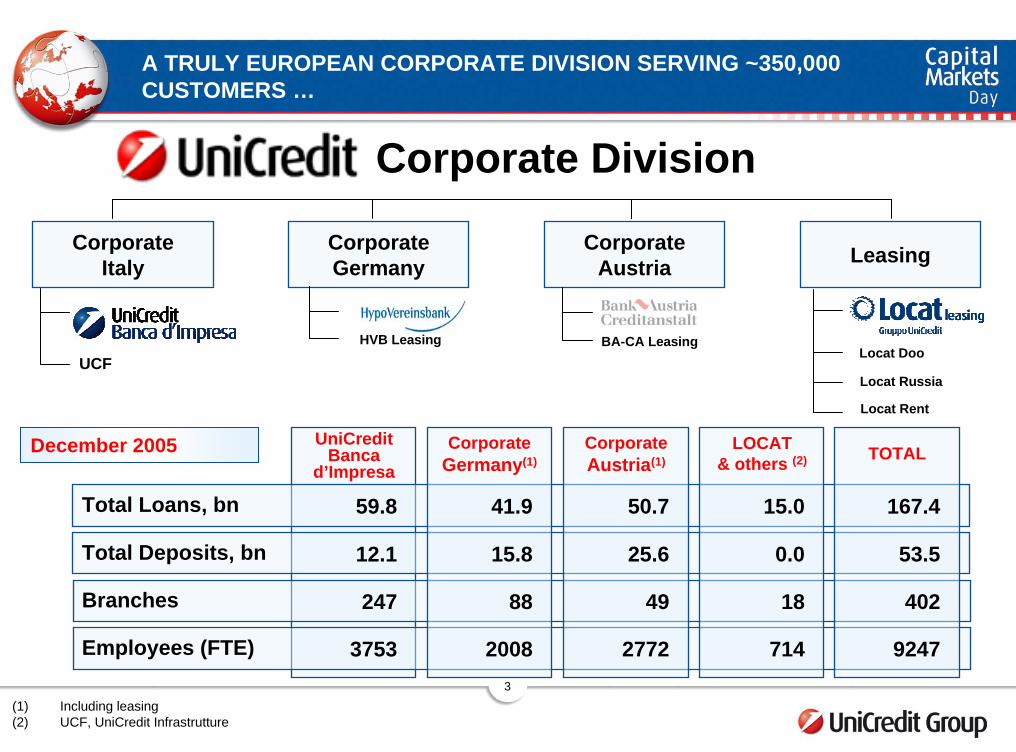

A TRULY EUROPEAN CORPORATE DIVISION SERVING ~350,000 CUSTOMERS …

Corporate Division

Corporate Italy

Corporate Germany

CorporateAustria Leasing

Total Loans, bn

Branches

Employees (FTE)

December 2005

59.8

247

3753

UniCredit Banca

d’Impresa

Total Deposits, bn 12.1

41.9

88

2008

CorporateGermany(1)

15.8

50.7

49

2772

CorporateAustria(1)

25.6

15.0

18

714

LOCAT & others (2)

0.0

167.4

402

9247

TOTAL

53.5

(1) Including leasing(2) UCF, UniCredit Infrastrutture

HVB Leasing BA-CA LeasingLocat Doo

UCFLocat Russia

Locat Rent

4

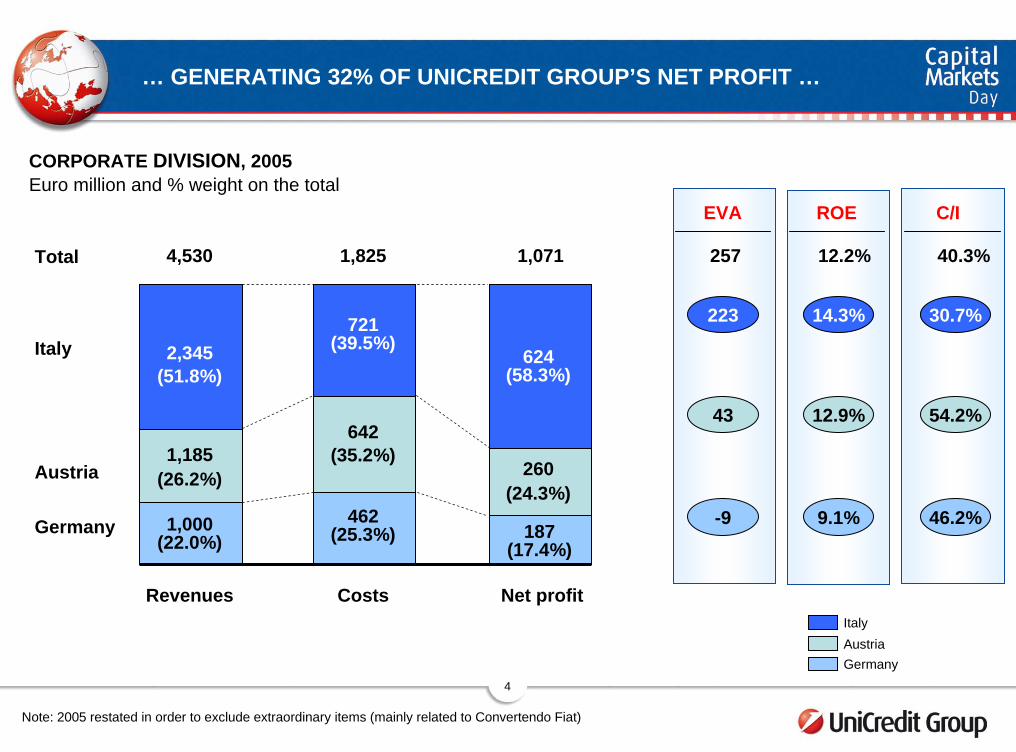

… GENERATING 32% OF UNICREDIT GROUP’S NET PROFIT …

CORPORATE DIVISION, 2005Euro million and % weight on the total

EVA

223

-9

43

257

ROE C/I

4,530 1,825 1,071Total 12.2% 40.3%

Revenues Costs Net profit

2,345(51.8%)

721(39.5%)

609

1,000(22.0%)

462(25.3%)

1,185(26.2%)

642(35.2%)

624(58.3%)

187(17.4%)

260(24.3%)

14.3%

9.1%

12.9%

30.7%

46.2%

54.2%

Italy

Austria

Germany

AustriaGermany

Italy

Note: 2005 restated in order to exclude extraordinary items (mainly related to Convertendo Fiat)

5

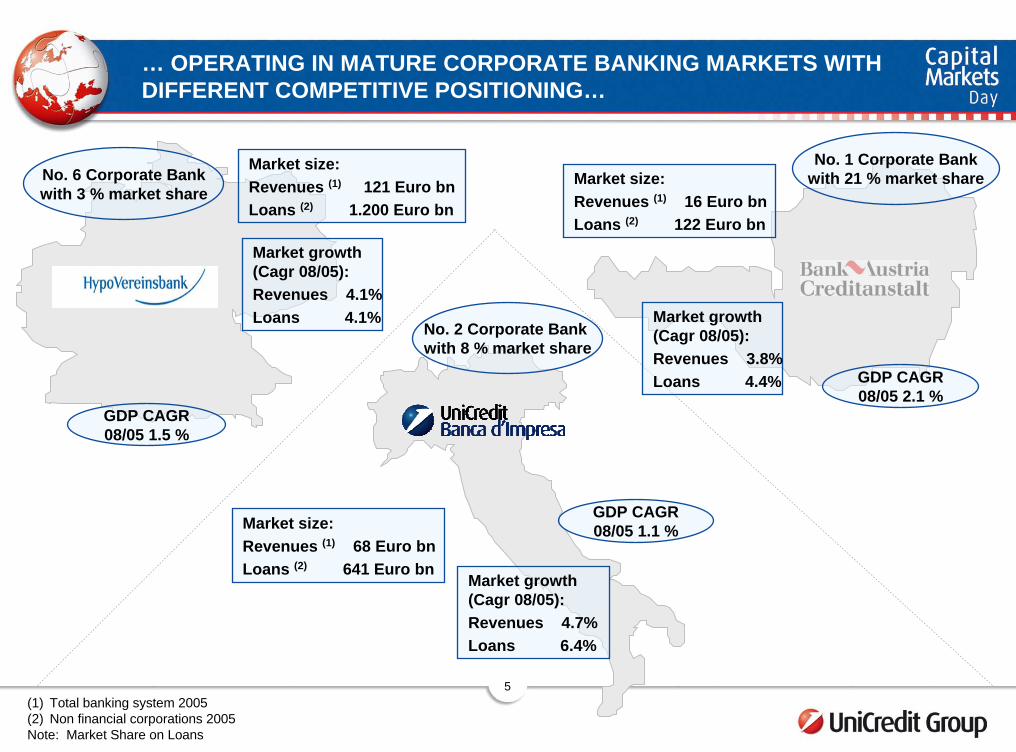

… OPERATING IN MATURE CORPORATE BANKING MARKETS WITH DIFFERENT COMPETITIVE POSITIONING…

No. 6 Corporate Bankwith 3 % market share

Market size: Revenues (1) 121 Euro bnLoans (2) 1.200 Euro bn

GDP CAGR 08/05 1.5 %

Market growth(Cagr 08/05): Revenues 4.1%Loans 4.1%

No. 2 Corporate Bank with 8 % market share

Market size: Revenues (1) 68 Euro bnLoans (2) 641 Euro bn

Market growth (Cagr 08/05): Revenues 4.7%Loans 6.4%

GDP CAGR 08/05 1.1 %

GDP CAGR 08/05 2.1 %

No. 1 Corporate Bankwith 21 % market shareMarket size:

Revenues (1) 16 Euro bn Loans (2) 122 Euro bn

Market growth (Cagr 08/05): Revenues 3.8%Loans 4.4%

(1) Total banking system 2005(2) Non financial corporations 2005Note: Market Share on Loans

6

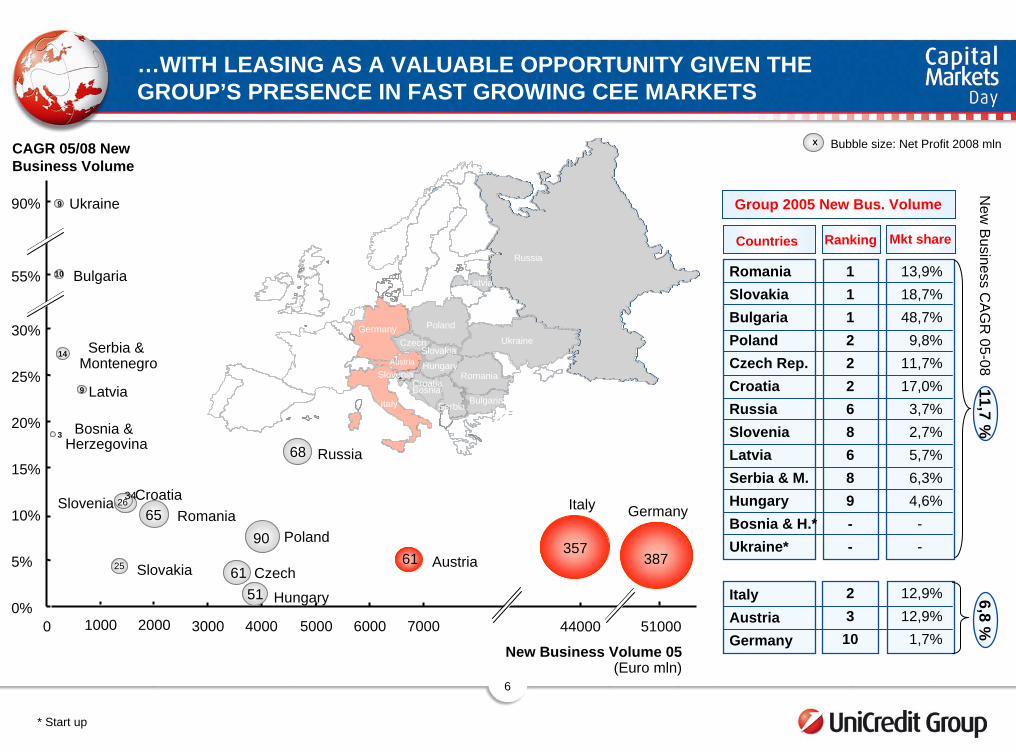

…WITH LEASING AS A VALUABLE OPPORTUNITY GIVEN THE GROUP’S PRESENCE IN FAST GROWING CEE MARKETS

Bubble size: Net Profit 2008 mln

PolandUkraine

Russia

RomaniaHungary

Czech Slovakia

Latvia

Italy

Germany

Austria

Bulgaria

CroatiaSlovenia

Bosnia

Serbia

9

X

Austria

Serbia & Montenegro

Bosnia & Herzegovina

0%

5%

10%

15%

20%

25%

30%

1000 2000 3000 4000 5000 6000 7000

Russia

Poland

Hungary

Czech

Slovenia CroatiaRomania

Slovakia

Latvia

55%

90%

44000

Italy Germany

0 51000

Ukraine

Bulgaria

35738761

90

6151

34

25

14

3

10

65

9

9

68

CAGR 05/08 New Business Volume

Group 2005 New Bus. Volume

RomaniaSlovakiaBulgariaPolandCzech Rep.CroatiaRussiaSloveniaLatviaSerbia & M.HungaryBosnia & H.*Ukraine*

Ranking Mkt shareCountries

New Business Volume 05 (Euro mln)

* Start up

26

* Start up

ItalyAustriaGermany

23

10

12,9%12,9%

1,7%

11122268689--

13,9%18,7%48,7%

9,8%11,7%17,0%

3,7%2,7%5,7%6,3%4,6%

--

11,7 %N

ew B

usiness CA

GR

05-086,8 %

7

AGENDA

The new Corporate Division

Strategic guidelines and business model

Key targets

8

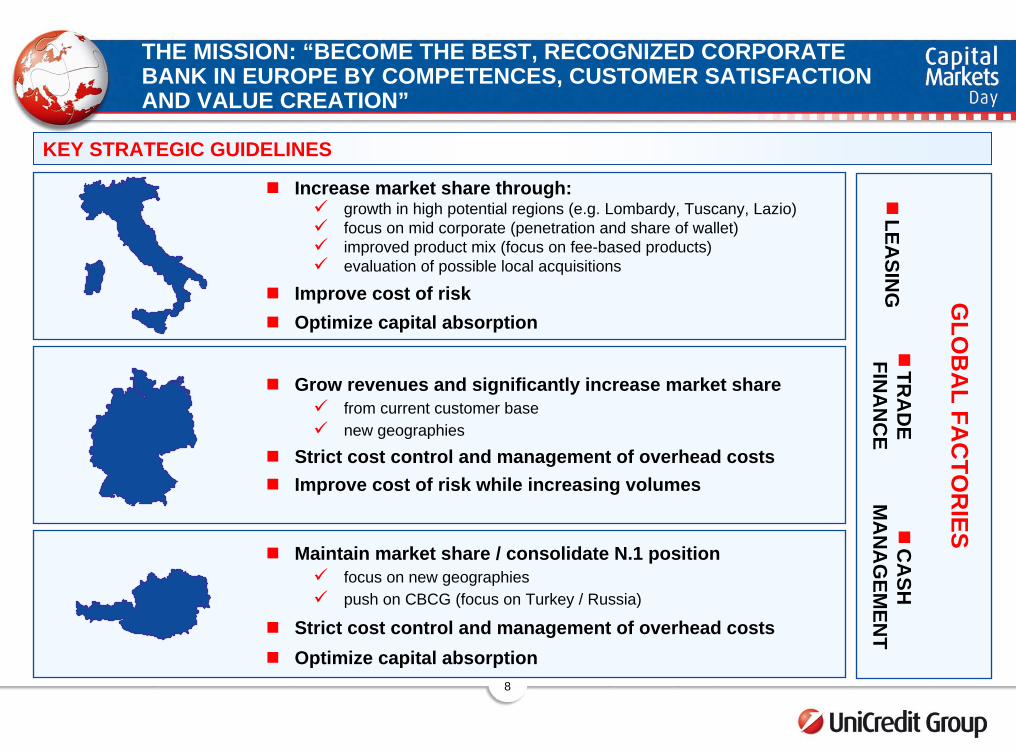

THE MISSION: “BECOME THE BEST, RECOGNIZED CORPORATE BANK IN EUROPE BY COMPETENCES, CUSTOMER SATISFACTION AND VALUE CREATION”

KEY STRATEGIC GUIDELINES

Increase market share through:growth in high potential regions (e.g. Lombardy, Tuscany, Lazio)focus on mid corporate (penetration and share of wallet)improved product mix (focus on fee-based products)evaluation of possible local acquisitions

Improve cost of riskOptimize capital absorption

Grow revenues and significantly increase market sharefrom current customer basenew geographies

Strict cost control and management of overhead costsImprove cost of risk while increasing volumes

Maintain market share / consolidate N.1 positionfocus on new geographiespush on CBCG (focus on Turkey / Russia)

Strict cost control and management of overhead costsOptimize capital absorption

GLO

BA

L FAC

TOR

IES

LEASIN

GTR

AD

E FIN

AN

CE

CA

SH

MA

NA

GEM

ENT

9

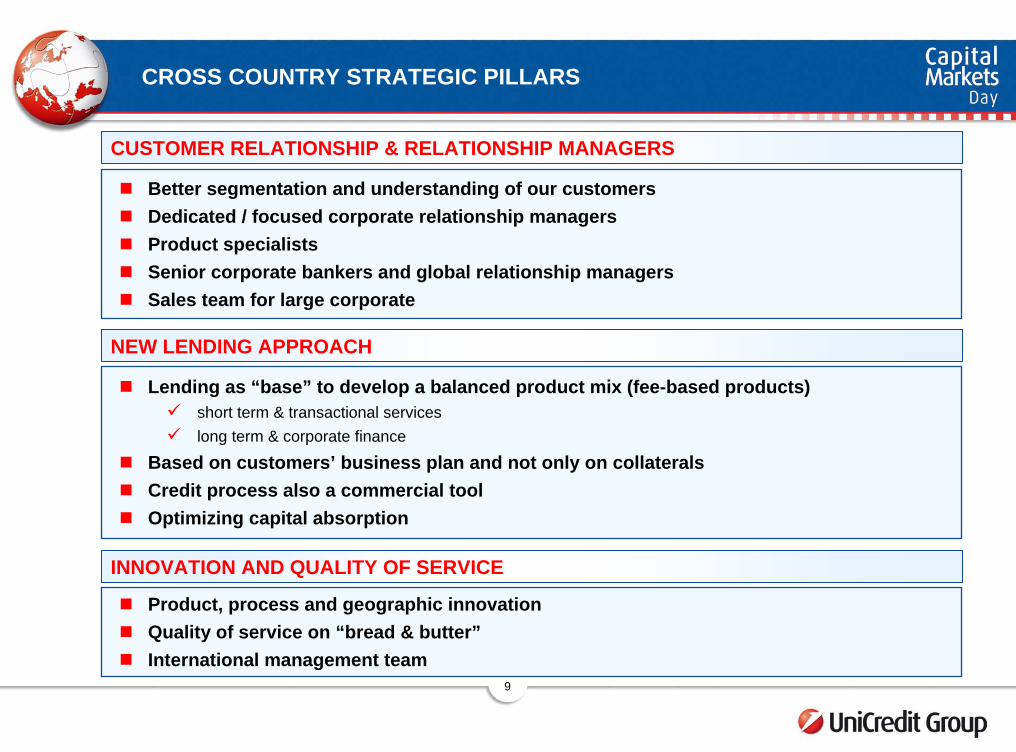

CROSS COUNTRY STRATEGIC PILLARS

Better segmentation and understanding of our customersDedicated / focused corporate relationship managersProduct specialists Senior corporate bankers and global relationship managersSales team for large corporate

CUSTOMER RELATIONSHIP & RELATIONSHIP MANAGERS

NEW LENDING APPROACH

Lending as “base” to develop a balanced product mix (fee-based products)short term & transactional serviceslong term & corporate finance

Based on customers’ business plan and not only on collateralsCredit process also a commercial toolOptimizing capital absorption

INNOVATION AND QUALITY OF SERVICE

Product, process and geographic innovationQuality of service on “bread & butter”International management team

10

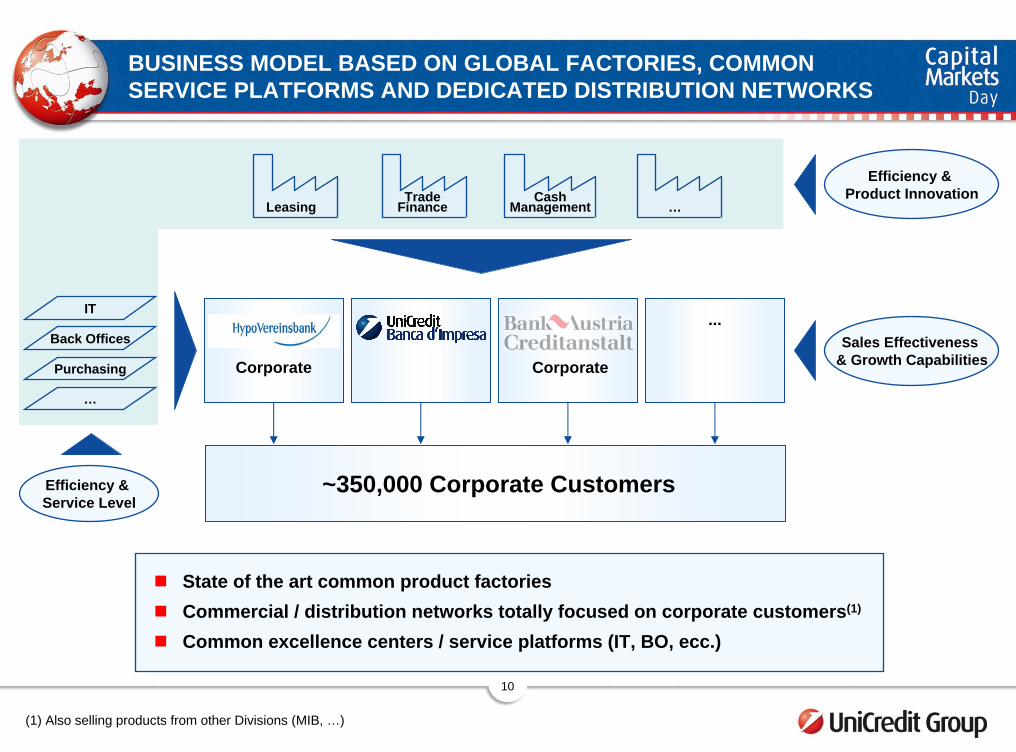

BUSINESS MODEL BASED ON GLOBAL FACTORIES, COMMON SERVICE PLATFORMS AND DEDICATED DISTRIBUTION NETWORKS

~350,000 Corporate Customers

Efficiency & Product Innovation

IT

Purchasing

Back Offices

…

LeasingCash

Management …Trade

Finance

Corporate

...

Efficiency & Service Level

Sales Effectiveness & Growth CapabilitiesCorporate

State of the art common product factoriesCommercial / distribution networks totally focused on corporate customers(1)

Common excellence centers / service platforms (IT, BO, ecc.)

(1) Also selling products from other Divisions (MIB, …)

11

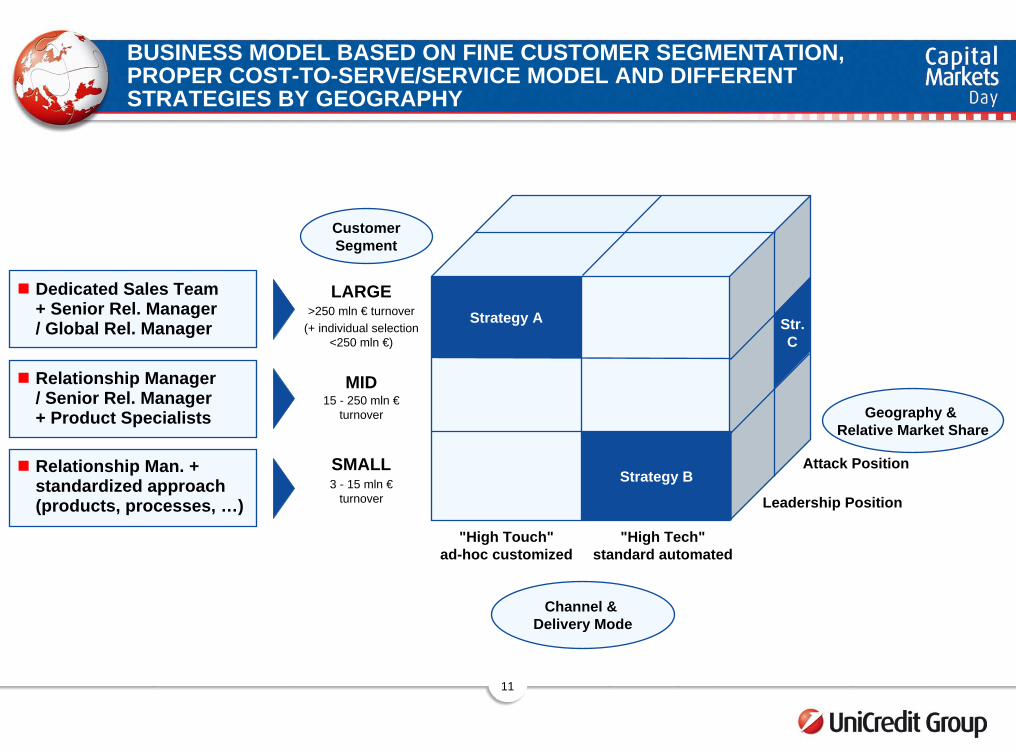

BUSINESS MODEL BASED ON FINE CUSTOMER SEGMENTATION, PROPER COST-TO-SERVE/SERVICE MODEL AND DIFFERENT STRATEGIES BY GEOGRAPHY

CustomerSegment

Dedicated Sales Team + Senior Rel. Manager / Global Rel. Manager

Relationship Manager / Senior Rel. Manager + Product Specialists

Relationship Man. + standardized approach (products, processes, …)

LARGE

MIDGeography &

Relative Market Share

SMALL

Leadership Position

Attack Position

>250 mln € turnover (+ individual selection

<250 mln €)

15 - 250 mln €turnover

3 - 15 mln €turnover

Strategy A

Strategy B

Str.C

"High Touch" ad-hoc customized

"High Tech" standard automated

Channel & Delivery Mode

12

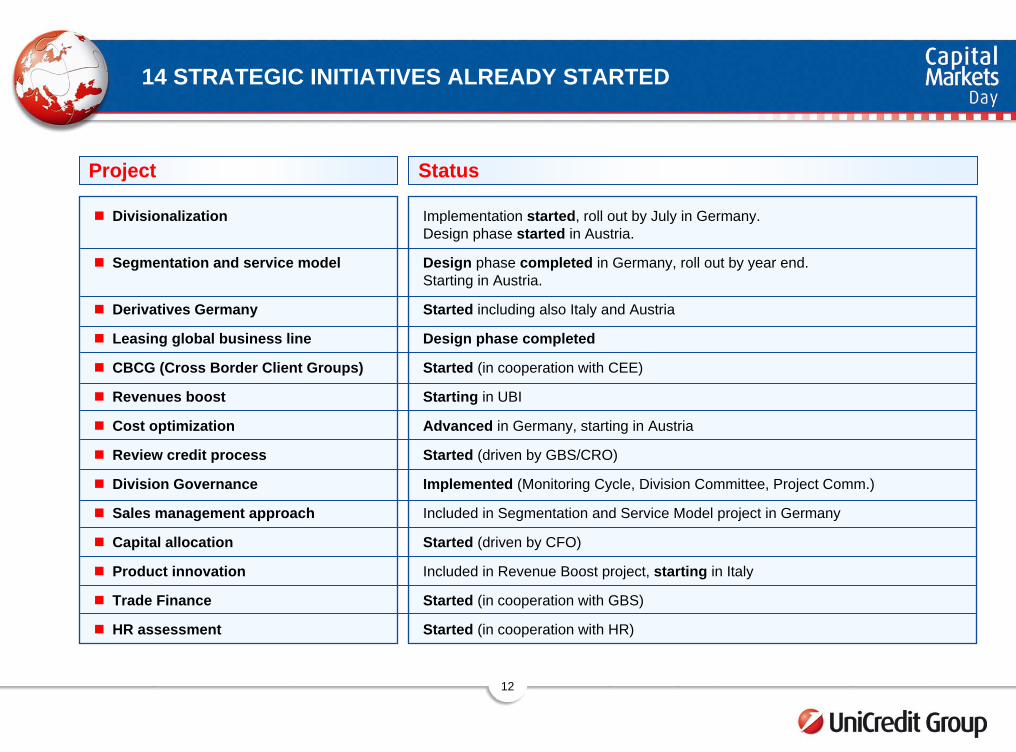

14 STRATEGIC INITIATIVES ALREADY STARTED

Project Status

Divisionalization

Segmentation and service model

Derivatives Germany

Leasing global business line

CBCG (Cross Border Client Groups)

Revenues boost

Cost optimization

Review credit process

Division Governance

Sales management approach

Capital allocation

Product innovation

Trade Finance

HR assessment

Implementation started, roll out by July in Germany. Design phase started in Austria.

Design phase completed in Germany, roll out by year end. Starting in Austria.

Started including also Italy and Austria

Design phase completed

Started (in cooperation with CEE)

Starting in UBI

Advanced in Germany, starting in Austria

Started (driven by GBS/CRO)

Implemented (Monitoring Cycle, Division Committee, Project Comm.)

Included in Segmentation and Service Model project in Germany

Started (driven by CFO)

Included in Revenue Boost project, starting in Italy

Started (in cooperation with GBS)

Started (in cooperation with HR)

13

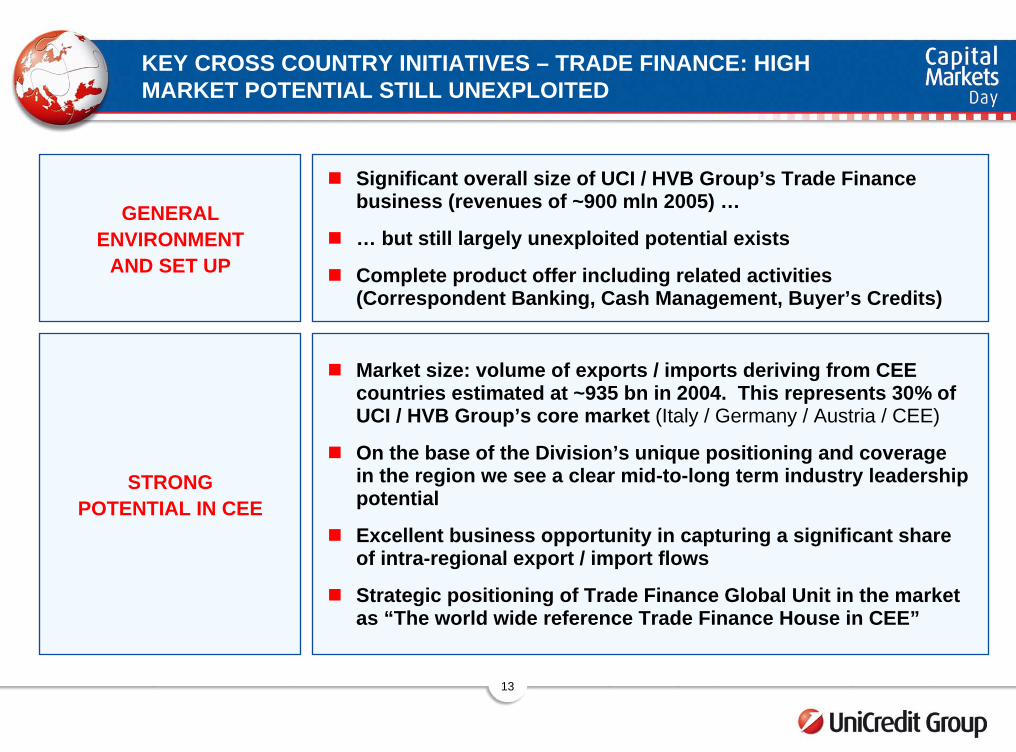

Market size: volume of exports / imports deriving from CEE countries estimated at ~935 bn in 2004. This represents 30% of UCI / HVB Group’s core market (Italy / Germany / Austria / CEE)

On the base of the Division’s unique positioning and coverage in the region we see a clear mid-to-long term industry leadership potential

Excellent business opportunity in capturing a significant share of intra-regional export / import flows

Strategic positioning of Trade Finance Global Unit in the marketas “The world wide reference Trade Finance House in CEE”

KEY CROSS COUNTRY INITIATIVES – TRADE FINANCE: HIGH MARKET POTENTIAL STILL UNEXPLOITED

Significant overall size of UCI / HVB Group’s Trade Finance business (revenues of ~900 mln 2005) …

… but still largely unexploited potential exists

Complete product offer including related activities (Correspondent Banking, Cash Management, Buyer’s Credits)

GENERAL ENVIRONMENT

AND SET UP

STRONG POTENTIAL IN CEE

14

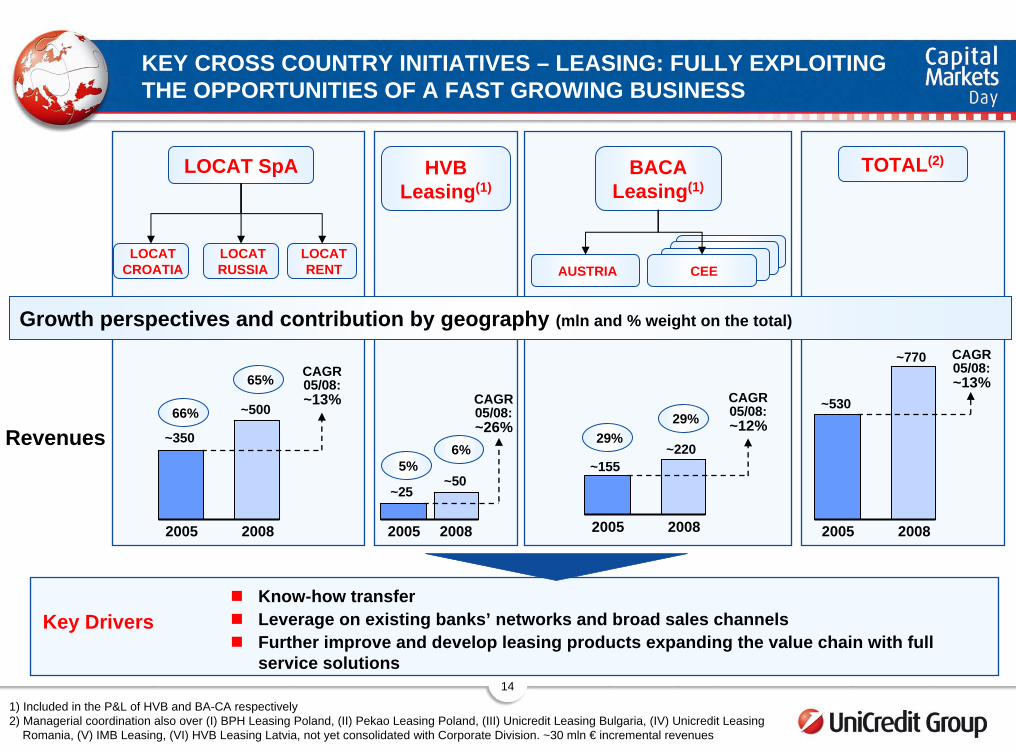

KEY CROSS COUNTRY INITIATIVES – LEASING: FULLY EXPLOITING THE OPPORTUNITIES OF A FAST GROWING BUSINESS

LOCAT SpA HVB Leasing(1)

BACA Leasing(1)

AUSTRIA

Growth perspectives and contribution by geography (mln and % weight on the total)

TOTAL(2)

LOCAT RUSSIA

LOCAT RENT

LOCAT CROATIA CEE

Revenues~530

2005 2008

CAGR 05/08:~13%

~770

~155

2005 2008

CAGR 05/08:~12%

~220~350

2005 2008

CAGR 05/08:~13%

~500

~25

2005 2008

CAGR 05/08:~26%

~50

66%

65%

5%6%

29%29%

Know-how transferLeverage on existing banks’ networks and broad sales channelsFurther improve and develop leasing products expanding the value chain with full service solutions

Key Drivers

1) Included in the P&L of HVB and BA-CA respectively2) Managerial coordination also over (I) BPH Leasing Poland, (II) Pekao Leasing Poland, (III) Unicredit Leasing Bulgaria, (IV) Unicredit Leasing

Romania, (V) IMB Leasing, (VI) HVB Leasing Latvia, not yet consolidated with Corporate Division. ~30 mln € incremental revenues

15

AGENDA

The new Corporate Division

Strategic guidelines and business model

Key targets

16

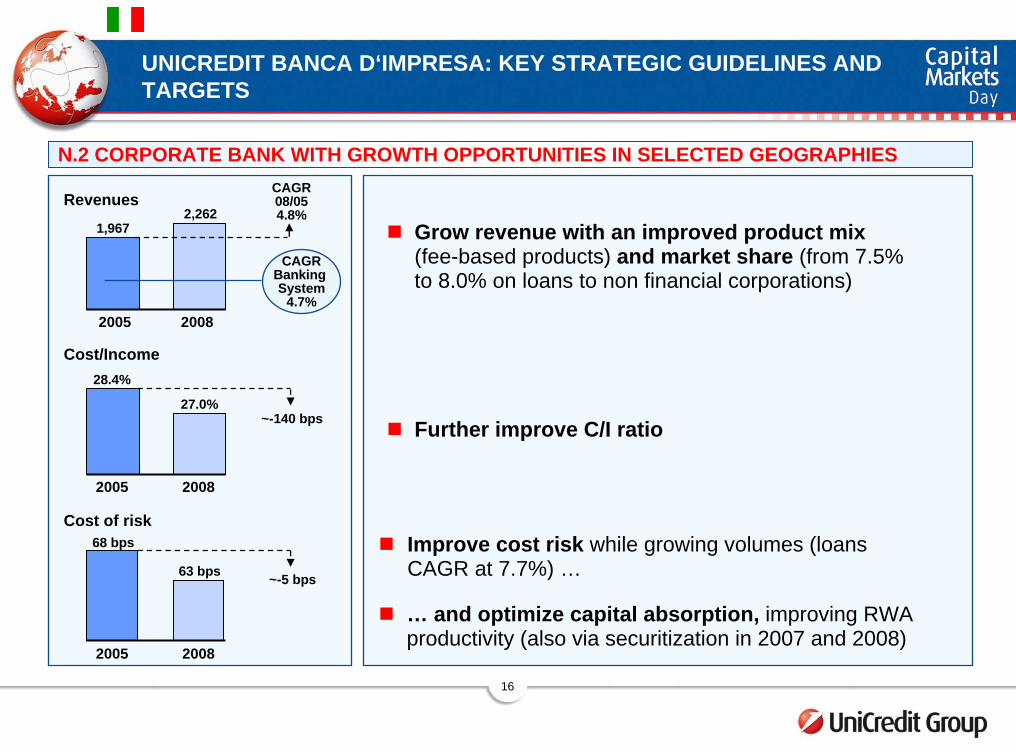

UNICREDIT BANCA D‘IMPRESA: KEY STRATEGIC GUIDELINES AND TARGETS

N.2 CORPORATE BANK WITH GROWTH OPPORTUNITIES IN SELECTED GEOGRAPHIES

Revenues1,967

2,262

2005 2008

CAGRBanking System

4.7%

CAGR08/054.8%

28.4%

27.0%

2005 2008

~-140 bps

Cost/Income

68 bps

63 bps

Cost of risk

~-5 bps

2005 2008

Grow revenue with an improved product mix (fee-based products) and market share (from 7.5% to 8.0% on loans to non financial corporations)

… and optimize capital absorption, improving RWA productivity (also via securitization in 2007 and 2008)

Improve cost risk while growing volumes (loans CAGR at 7.7%) …

Further improve C/I ratio

17

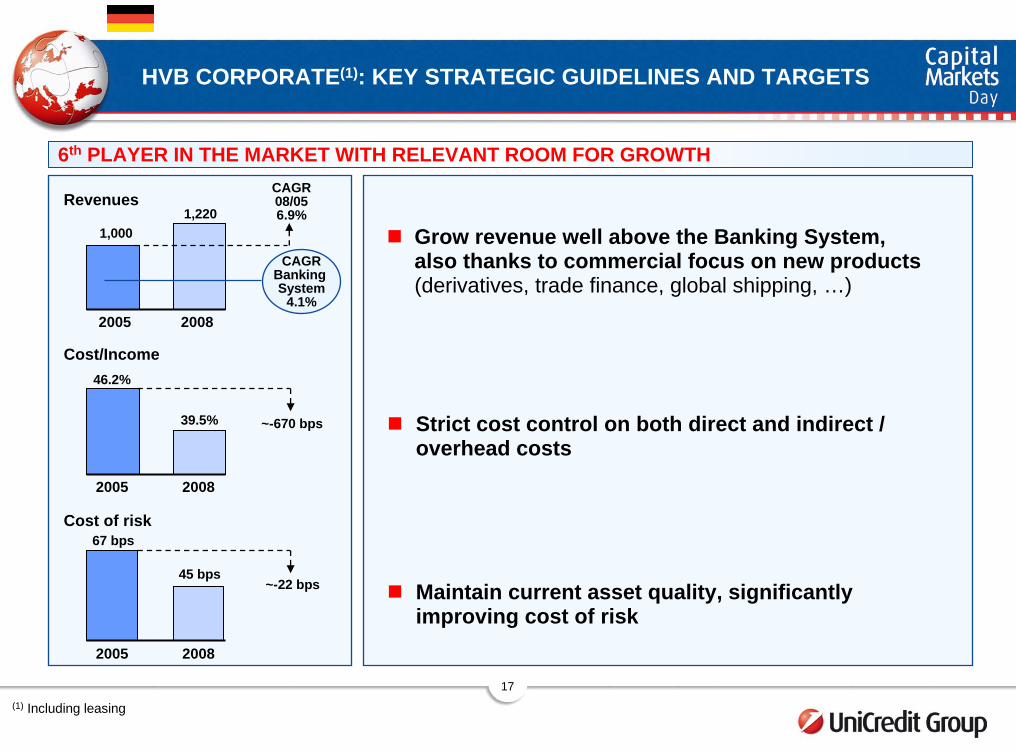

HVB CORPORATE(1): KEY STRATEGIC GUIDELINES AND TARGETS

6th PLAYER IN THE MARKET WITH RELEVANT ROOM FOR GROWTH

Revenues

1,0001,220

2005 2008

CAGRBanking System

4.1%

CAGR08/056.9%

46.2%

39.5%

2005 2008

~-670 bps

Cost/Income

67 bps

45 bps

Cost of risk

~-22 bps

2005 2008

Strict cost control on both direct and indirect / overhead costs

Grow revenue well above the Banking System, also thanks to commercial focus on new products (derivatives, trade finance, global shipping, …)

Maintain current asset quality, significantly improving cost of risk

(1) Including leasing

18

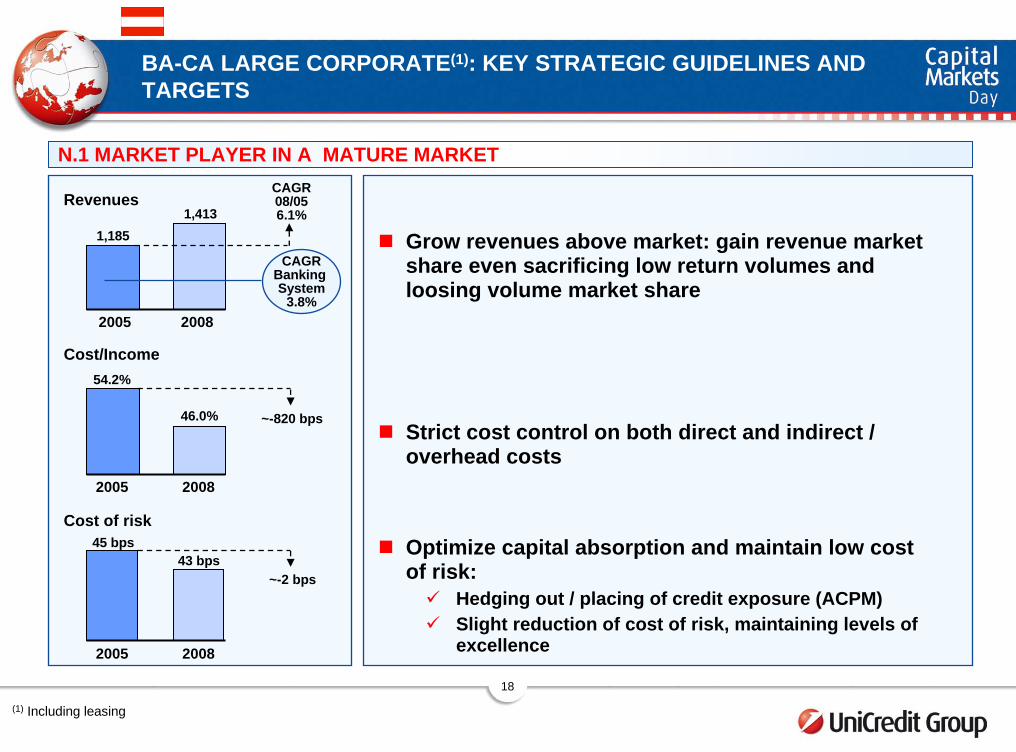

BA-CA LARGE CORPORATE(1): KEY STRATEGIC GUIDELINES AND TARGETS

N.1 MARKET PLAYER IN A MATURE MARKET

Revenues

1,1851,413

2005 2008

CAGRBanking System

3.8%

CAGR08/056.1%

54.2%

46.0%

2005 2008

~-820 bps

Cost/Income

45 bps43 bps

Cost of risk

~-2 bps

2005 2008

Grow revenues above market: gain revenue market share even sacrificing low return volumes and loosing volume market share

Strict cost control on both direct and indirect / overhead costs

Optimize capital absorption and maintain low cost of risk:

Hedging out / placing of credit exposure (ACPM)Slight reduction of cost of risk, maintaining levels of excellence

(1) Including leasing

19

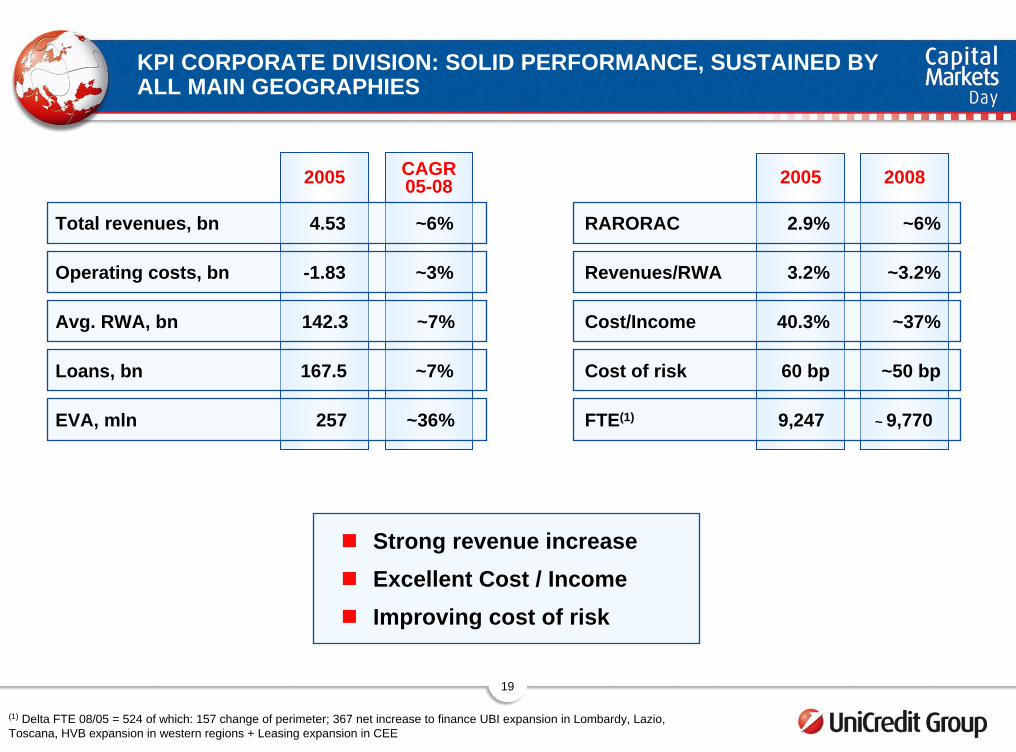

KPI CORPORATE DIVISION: SOLID PERFORMANCE, SUSTAINED BY ALL MAIN GEOGRAPHIES

CAGR 05-08

(1) Delta FTE 08/05 = 524 of which: 157 change of perimeter; 367 net increase to finance UBI expansion in Lombardy, Lazio, Toscana, HVB expansion in western regions + Leasing expansion in CEE

FTE(1) 9,247

2.9%

3.2%

RARORAC

Revenues/RWA

2005

167.5

4.53

142.3

-1.83

Loans, bn

~ 9,770

~6%

~3.2%

Total revenues, bn ~6%

~7%

~3%Operating costs, bn

Avg. RWA, bn Cost/Income 40.3% ~37%

60 bp

2005

~50 bp

2008

~7%

~36%

Cost of risk

257EVA, mln

Strong revenue increaseExcellent Cost / IncomeImproving cost of risk

20

ANNEX

21

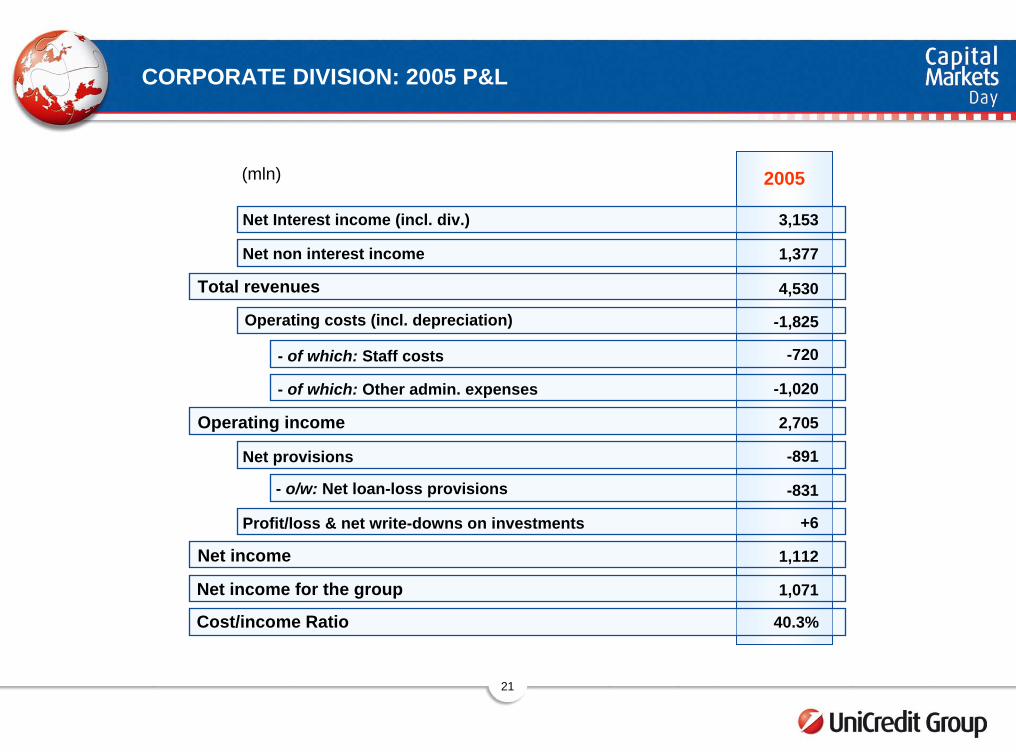

CORPORATE DIVISION: 2005 P&L

(mln)

Net Interest income (incl. div.)

Net non interest income

Total revenues

Operating costs (incl. depreciation)

Operating income

Net income

Net provisions

Net income for the group

- of which: Staff costs

- of which: Other admin. expenses

- o/w: Net loan-loss provisions

Cost/income Ratio

2005

3,153

1,377

4,530

2,705

-1,020

-720

-1,825

1,112

1,071

40.3%

-831

-891

Profit/loss & net write-downs on investments +6