Embed Size (px)

Citation preview

Pricing Terminal Illness – Is there no cost?

Francis Burgess & Brendon Gerding

Agenda

• Terminal Illness – UK vs Australia

• UK Survival Study

• Adapting the results to 24 Month TI

• When TI was initially introduced the proportion of death

claims was approximately 5% and rate guarantees were

typically 3 years or longer.

• Assumption was that overlap with TPD was extremely high.

• Cost mainly perceived as lost interest and lost premiums.

• Typically priced at less than 1% of death premiums in a

market that was increasing member benefits.

• TI proportion of death claims and contract terms are very

different now!

Hasn’t the cost of TI always been immaterial?

4

Terminal Illness UK vs Australia

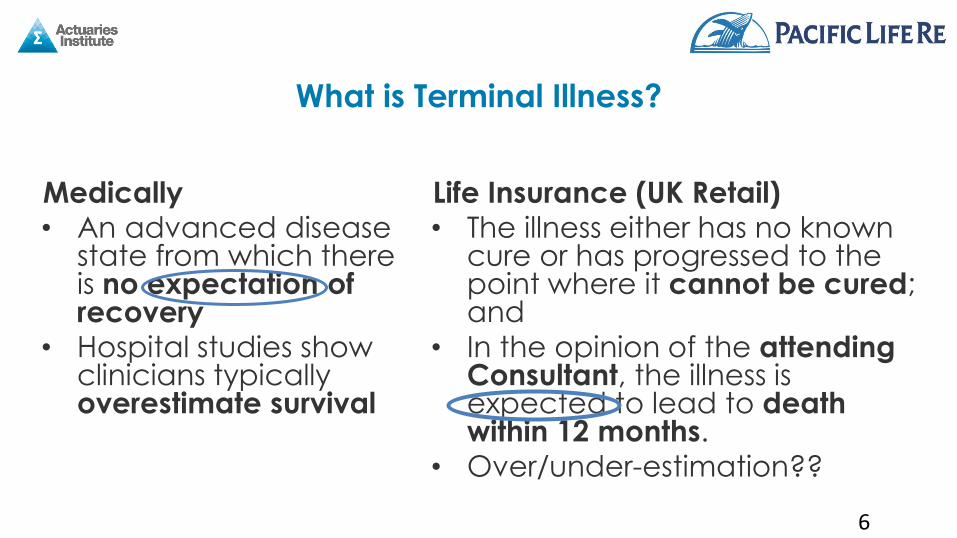

What is Terminal Illness?

Medically • An advanced disease

state from which there is no expectation of recovery

• Hospital studies show clinicians typically overestimate survival

Life Insurance (UK Retail) • The illness either has no known

cure or has progressed to the point where it cannot be cured; and

• In the opinion of the attending Consultant, the illness is expected to lead to death within 12 months.

• Over/under-estimation??

6

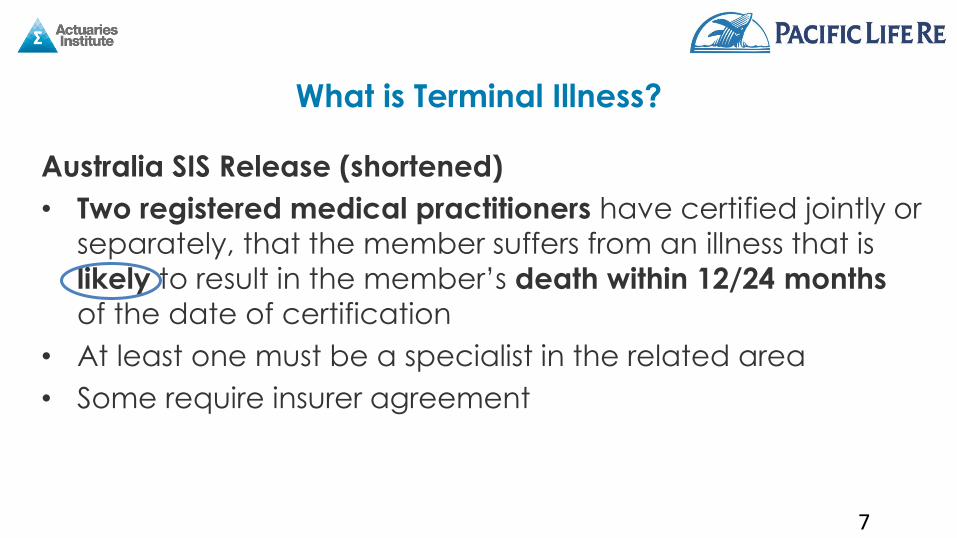

What is Terminal Illness?

Australia SIS Release (shortened)

• Two registered medical practitioners have certified jointly or

separately, that the member suffers from an illness that is

likely to result in the member’s death within 12/24 months

of the date of certification

• At least one must be a specialist in the related area

• Some require insurer agreement

7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 13 25 37 49 61 73 85 97 109

% S

urv

ivin

g

Months Since Diagnosis

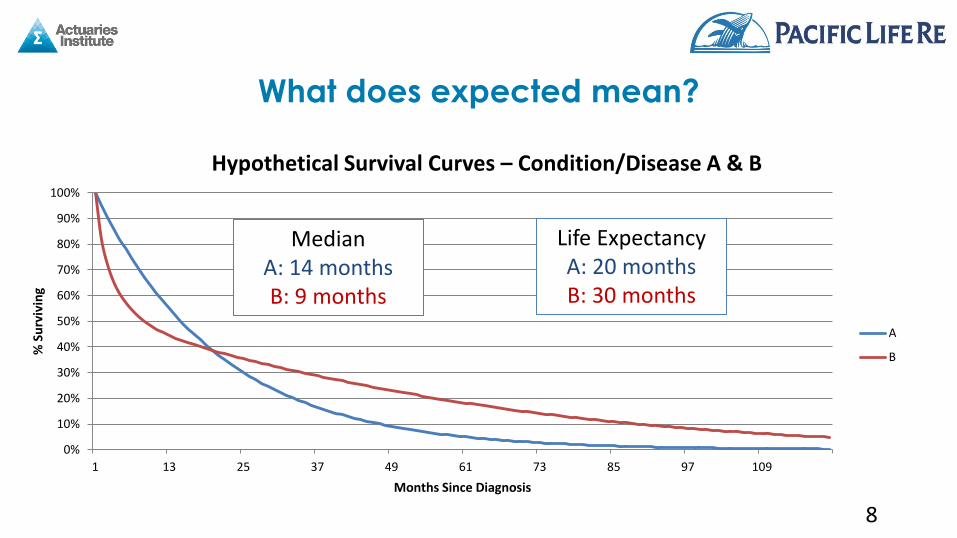

Hypothetical Survival Curves – Condition/Disease A & B

A

B

What does expected mean?

8

Median A: 14 months B: 9 months

Life Expectancy A: 20 months B: 30 months

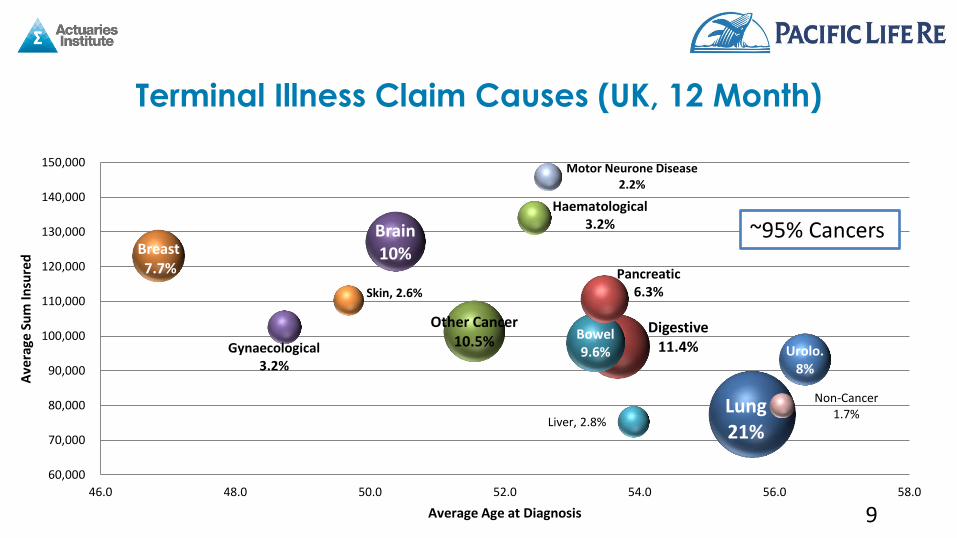

Terminal Illness Claim Causes (UK, 12 Month)

9

Lung 21%

Breast 7.7%

Digestive 11.4%

Other Cancer 10.5%

Brain 10%

Bowel 9.6% Urolo.

8%

Pancreatic 6.3%

Haematological 3.2%

Gynaecological 3.2%

Liver, 2.8%

Skin, 2.6%

Motor Neurone Disease 2.2%

Non-Cancer 1.7%

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

46.0 48.0 50.0 52.0 54.0 56.0 58.0

Ave

rage

Su

m In

sure

d

Average Age at Diagnosis

~95% Cancers

0%

5%

10%

15%

20%

25%

30%

35%

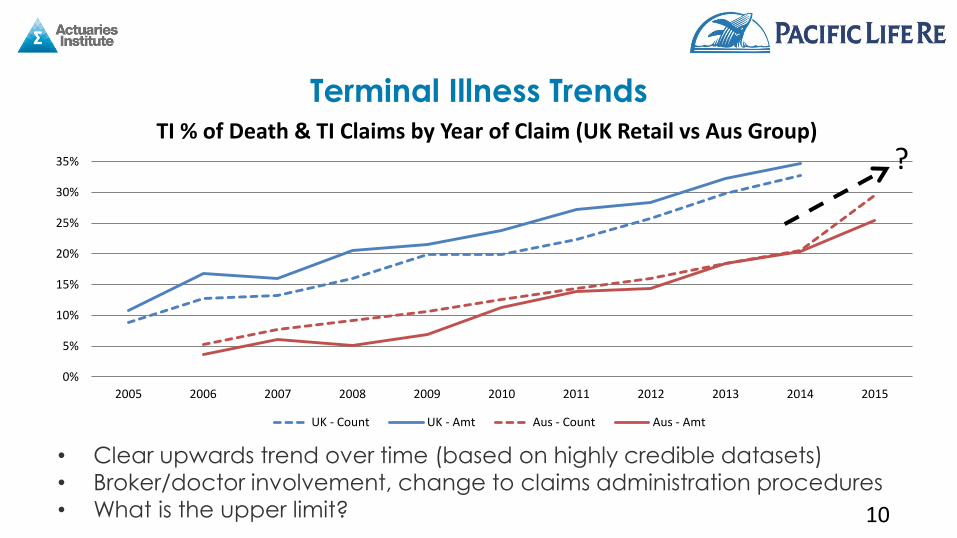

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

TI % of Death & TI Claims by Year of Claim (UK Retail vs Aus Group)

UK - Count UK - Amt Aus - Count Aus - Amt

• Clear upwards trend over time (based on highly credible datasets) • Broker/doctor involvement, change to claims administration procedures • What is the upper limit?

Terminal Illness Trends

10

?

11

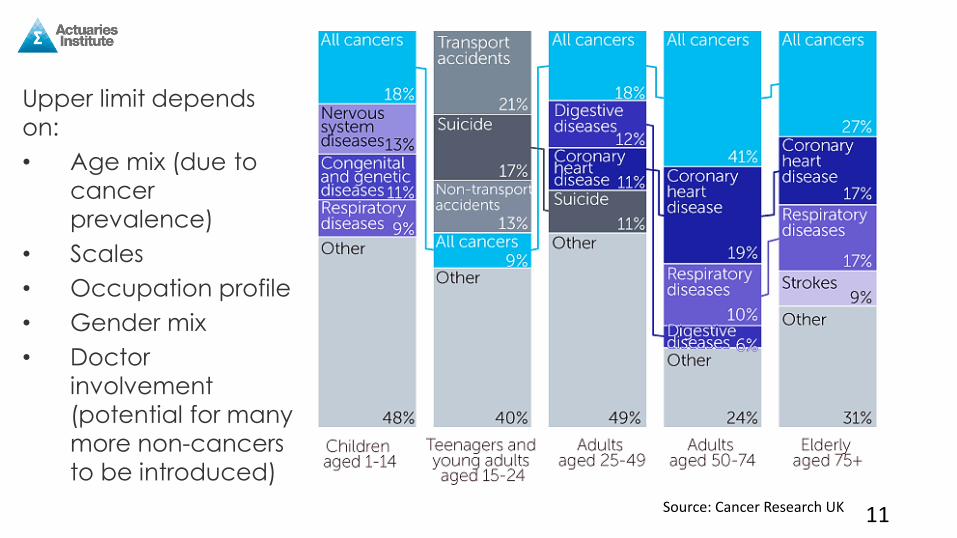

Upper limit depends

on:

• Age mix (due to

cancer

prevalence)

• Scales

• Occupation profile

• Gender mix

• Doctor

involvement

(potential for many

more non-cancers

to be introduced)

Source: Cancer Research UK

As TI becomes more prevalent, cost becomes material:

• “New” claims - survivors to end of term or new insurer

• Higher benefit levels (DTA, Benefit Scales)

• Transfer from TPD (if lower scale)

• Foregone premiums/Interest lost on reserves

• Claims expenses

The Cost of Terminal Illness

12

UK Survival Study

• Given the increasing trends, we wanted to find out what was

happening post-claim

• TI Claims data sourced from leading UK retail companies (12

month definition)

• ~3,500 TI claims over ~10 years

• Tracing exercise performed using our longevity tracing

systems

Study Overview

14

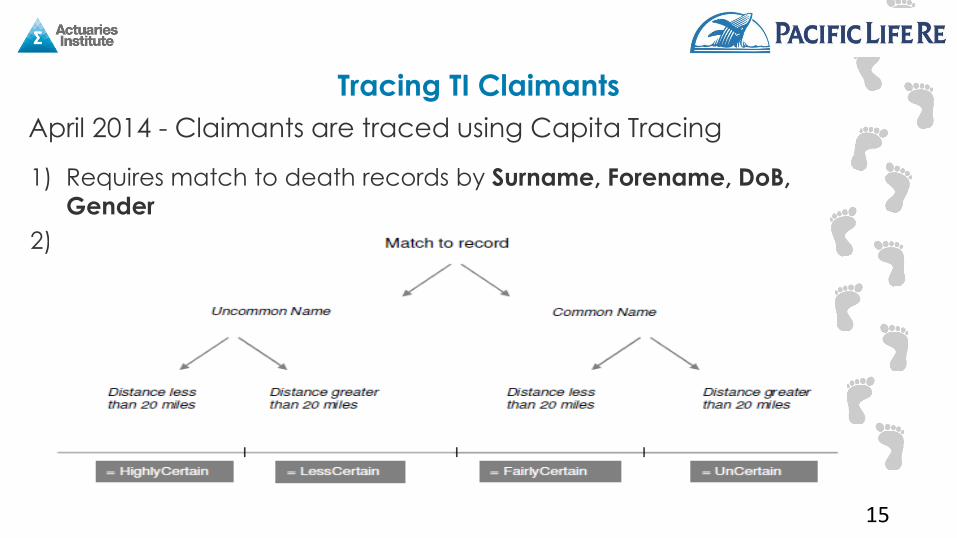

April 2014 - Claimants are traced using Capita Tracing

1) Requires match to death records by Surname, Forename, DoB,

Gender

2) Then assigns “grading” to the match as follows:

Tracing TI Claimants

15

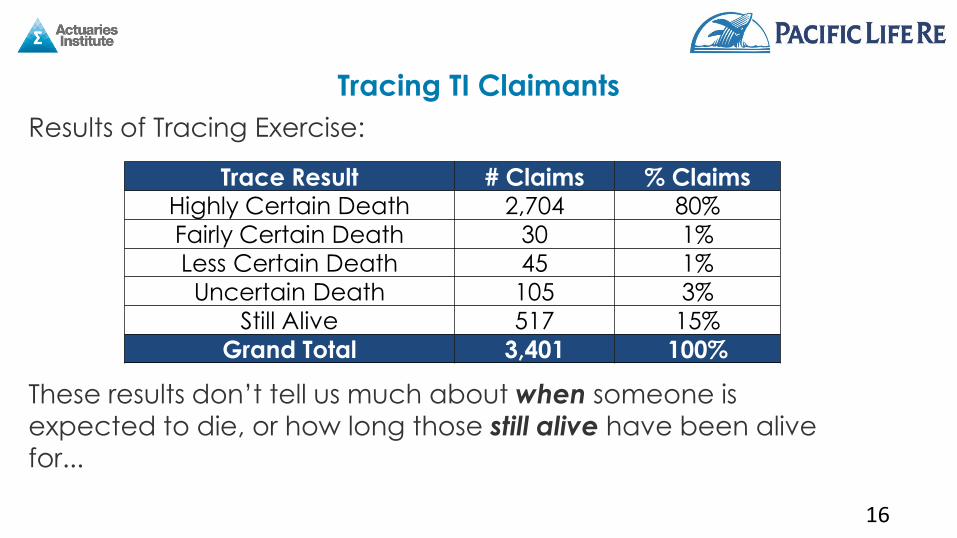

Results of Tracing Exercise:

These results don’t tell us much about when someone is

expected to die, or how long those still alive have been alive

for...

16

Trace Result # Claims % Claims Highly Certain Death 2,704 80%

Fairly Certain Death 30 1%

Less Certain Death 45 1%

Uncertain Death 105 3%

Still Alive 517 15%

Grand Total 3,401 100%

Tracing TI Claimants

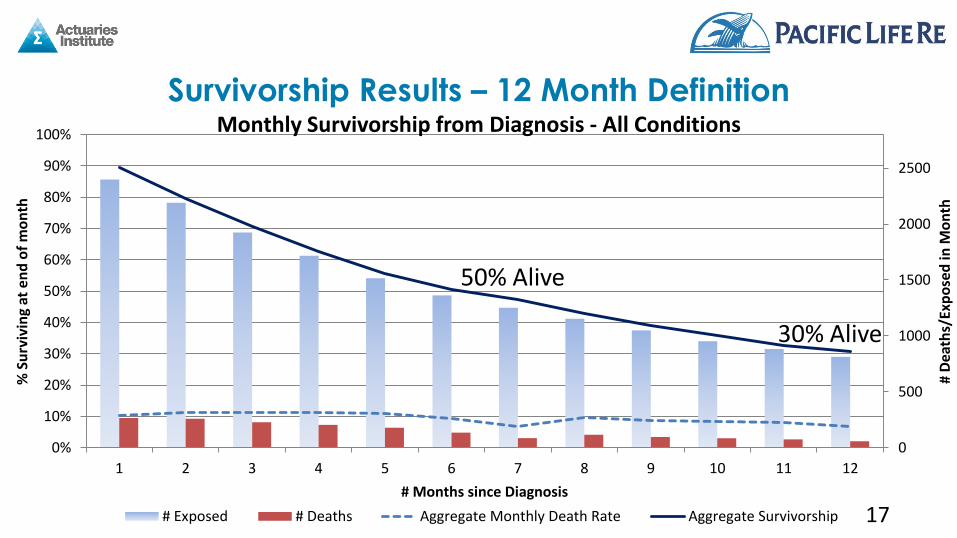

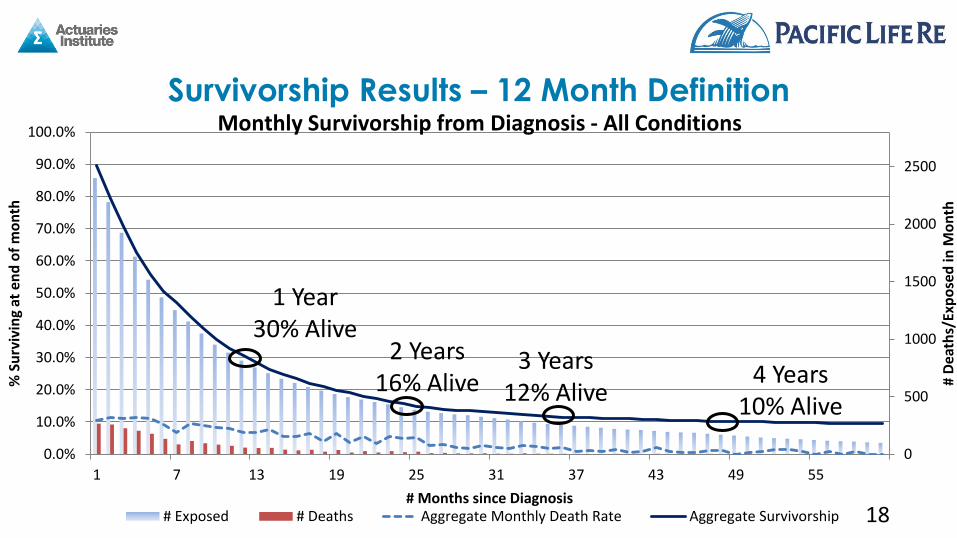

Survivorship Results – 12 Month Definition

17

0

500

1000

1500

2000

2500

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12

# D

eath

s/Ex

po

sed

in M

on

th

% S

urv

ivin

g at

en

d o

f m

on

th

# Months since Diagnosis

Monthly Survivorship from Diagnosis - All Conditions

# Exposed # Deaths Aggregate Monthly Death Rate Aggregate Survivorship

50% Alive

30% Alive

0

500

1000

1500

2000

2500

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1 7 13 19 25 31 37 43 49 55

# D

eath

s/Ex

po

sed

in M

on

th

% S

urv

ivin

g at

en

d o

f m

on

th

# Months since Diagnosis

Monthly Survivorship from Diagnosis - All Conditions

# Exposed # Deaths Aggregate Monthly Death Rate Aggregate Survivorship 18

1 Year 30% Alive

2 Years 16% Alive 4 Years

10% Alive

3 Years 12% Alive

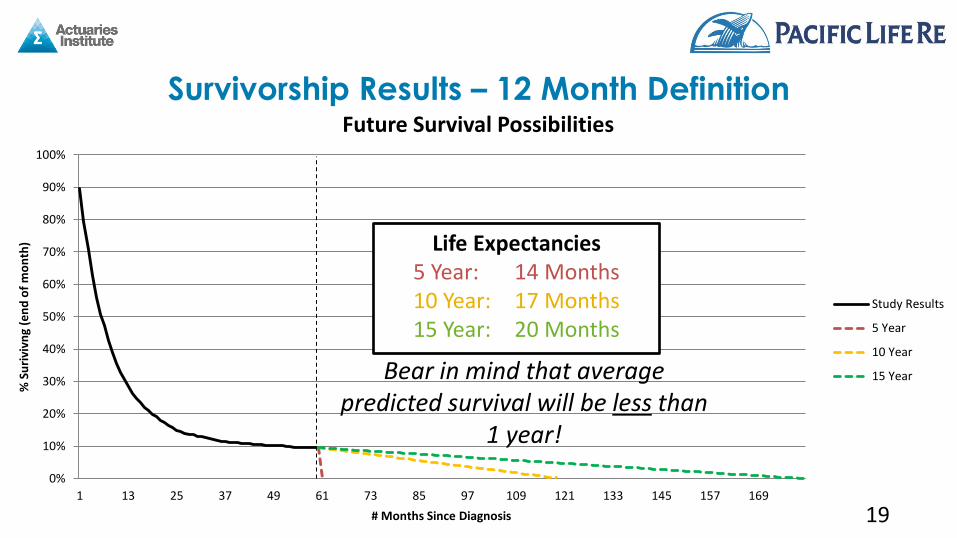

Survivorship Results – 12 Month Definition

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 13 25 37 49 61 73 85 97 109 121 133 145 157 169

% S

uri

vivn

g (e

nd

of

mo

nth

)

# Months Since Diagnosis

Future Survival Possibilities

Study Results

5 Year

10 Year

15 Year

Survivorship Results – 12 Month Definition

Life Expectancies 5 Year: 14 Months 10 Year: 17 Months 15 Year: 20 Months

Bear in mind that average predicted survival will be less than

1 year!

19

0

50

100

150

200

250

300

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59

# D

eath

s in

Mo

nth

% D

yin

g in

Mo

nth

# Months since Diagnosis

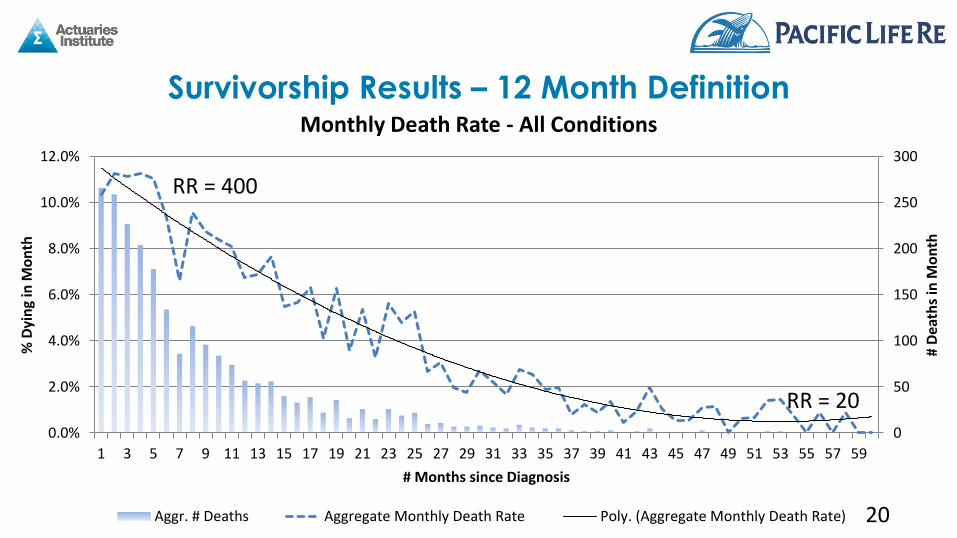

Monthly Death Rate - All Conditions

Aggr. # Deaths Aggregate Monthly Death Rate Poly. (Aggregate Monthly Death Rate)

Survivorship Results – 12 Month Definition

RR = 400

RR = 20

20

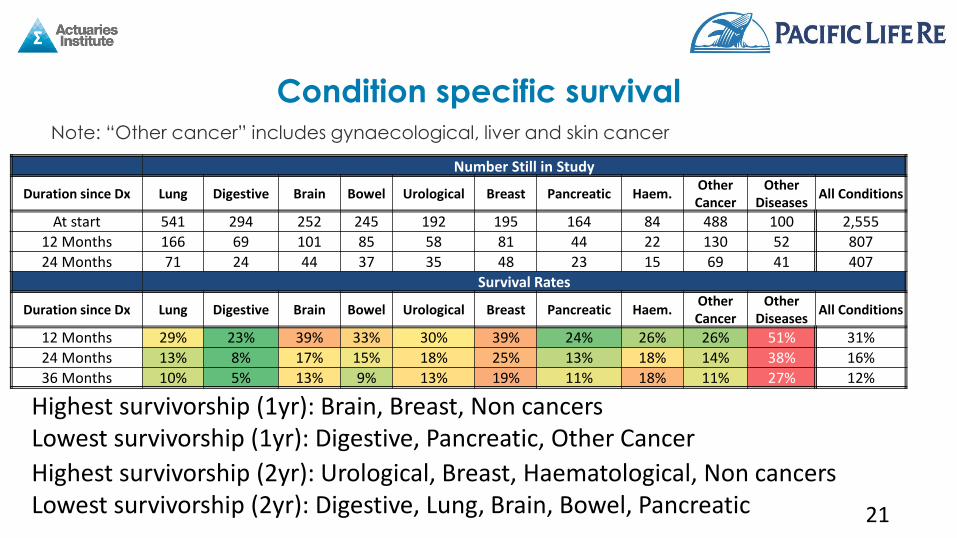

Condition specific survival Note: “Other cancer” includes gynaecological, liver and skin cancer

21

Number Still in Study

Duration since Dx Lung Digestive Brain Bowel Urological Breast Pancreatic Haem. Other Cancer

Other Diseases

All Conditions

At start 541 294 252 245 192 195 164 84 488 100 2,555

12 Months 166 69 101 85 58 81 44 22 130 52 807

24 Months 71 24 44 37 35 48 23 15 69 41 407

Survival Rates

Duration since Dx Lung Digestive Brain Bowel Urological Breast Pancreatic Haem. Other Cancer

Other Diseases

All Conditions

12 Months 29% 23% 39% 33% 30% 39% 24% 26% 26% 51% 31%

24 Months 13% 8% 17% 15% 18% 25% 13% 18% 14% 38% 16%

36 Months 10% 5% 13% 9% 13% 19% 11% 18% 11% 27% 12%

Highest survivorship (1yr): Brain, Breast, Non cancers Lowest survivorship (1yr): Digestive, Pancreatic, Other Cancer Highest survivorship (2yr): Urological, Breast, Haematological, Non cancers Lowest survivorship (2yr): Digestive, Lung, Brain, Bowel, Pancreatic

• TI Claims have increased materially, and no immediate sign of respite

• In the UK, people are living

longer than predicted, with 1

in 10 still alive after 5 years

• Life expectancy (mean) is a

more sensible measure of

“expected”, but median is the

more common approach

Key Takeaway – UK Study

22

Adapting the Results 24 Month TI

Key Assumptions Needed:

Adapting the Results

24

Proportion TI Claims (over time)

TI Survival Rates

Policy Length

TPD Conversions

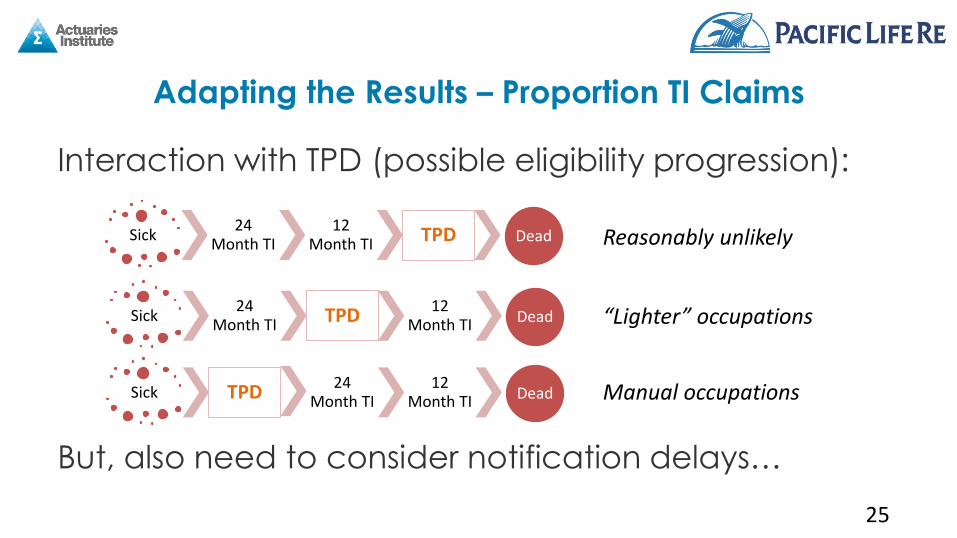

Interaction with TPD (possible eligibility progression):

But, also need to consider notification delays…

Adapting the Results – Proportion TI Claims

25

Sick 24

Month TI 12

Month TI TPD Dead

Sick 24

Month TI TPD 12

Month TI Dead

Sick TPD 24

Month TI 12

Month TI Dead

Reasonably unlikely

“Lighter” occupations

Manual occupations

• Day 1 – All those in the 13-24 period now eligible to claim

• Expect some awareness growth – “phasing in”

• Following initial peak, expect track back to 12 month

proportions (which are currently increasing)

• But, some permanent uplift will apply

– Recoveries, deaths

– Transfers from TPD

– Increased doctor error (or siding with patient)

Adapting the Results – Proportion TI Claims

26

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

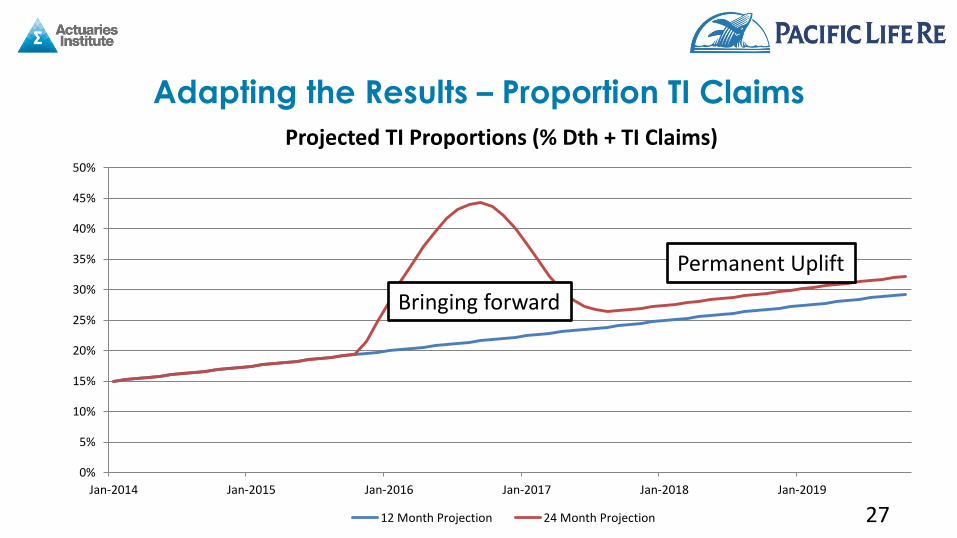

Jan-2014 Jan-2015 Jan-2016 Jan-2017 Jan-2018 Jan-2019

Projected TI Proportions (% Dth + TI Claims)

12 Month Projection 24 Month Projection

Adapting the Results – Proportion TI Claims

27

Bringing forward

Permanent Uplift

• UK Retail survival starting point

• Expect roughly +12 months life expectancy,

assuming accuracy stays the same

• But, accuracy ↓ as timeframe ↑

• Highly dependant on doctor behaviour

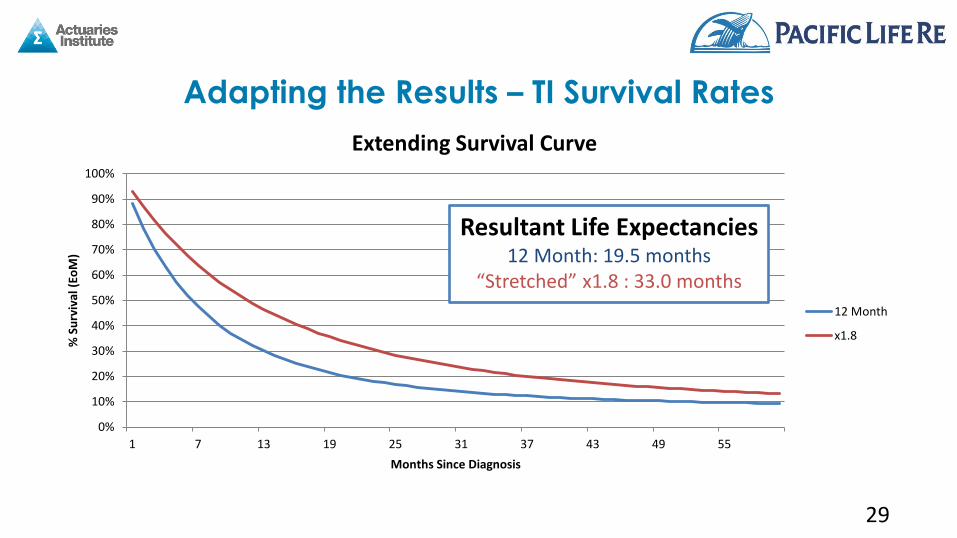

Adapting the Results – TI Survival Rates

28

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 7 13 19 25 31 37 43 49 55

% S

urv

ival

(Eo

M)

Months Since Diagnosis

Extending Survival Curve

12 Month

x1.8

Adapting the Results – TI Survival Rates

29

Resultant Life Expectancies 12 Month: 19.5 months

“Stretched” x1.8 : 33.0 months

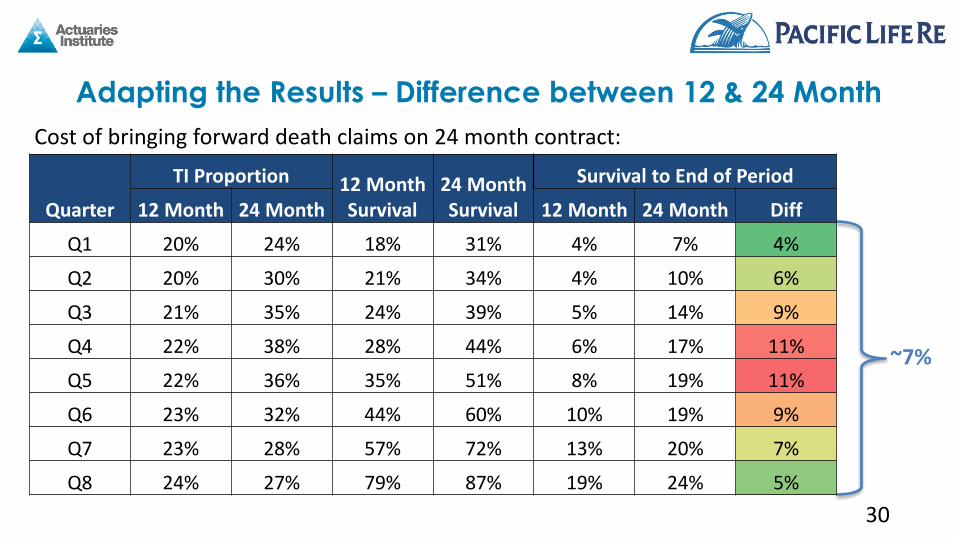

Adapting the Results – Difference between 12 & 24 Month

30

~7%

Quarter

TI Proportion 12 Month Survival

24 Month Survival

Survival to End of Period

12 Month 24 Month 12 Month 24 Month Diff

Q1 20% 24% 18% 31% 4% 7% 4%

Q2 20% 30% 21% 34% 4% 10% 6%

Q3 21% 35% 24% 39% 5% 14% 9%

Q4 22% 38% 28% 44% 6% 17% 11%

Q5 22% 36% 35% 51% 8% 19% 11%

Q6 23% 32% 44% 60% 10% 19% 9%

Q7 23% 28% 57% 72% 13% 20% 7%

Q8 24% 27% 79% 87% 19% 24% 5%

Cost of bringing forward death claims on 24 month contract:

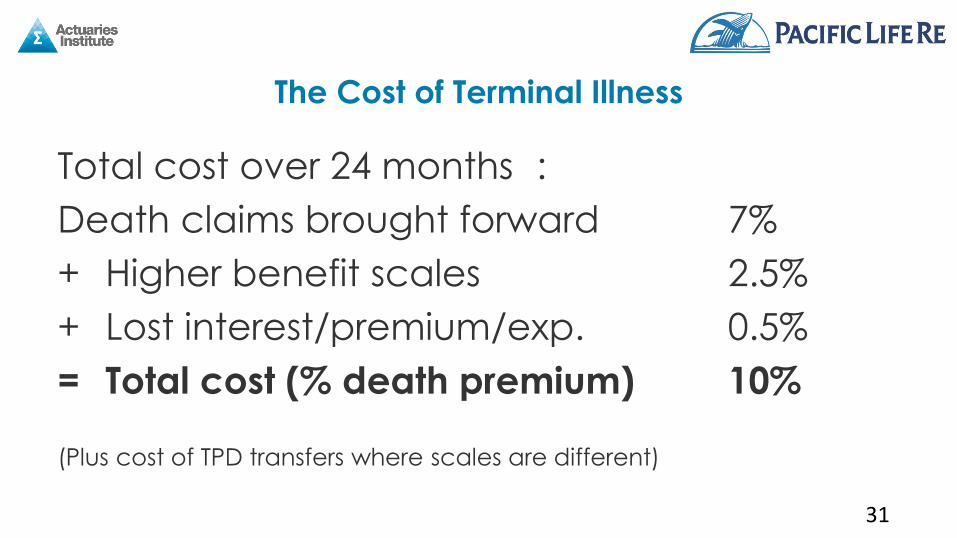

The Cost of Terminal Illness

31

Total cost over 24 months :

Death claims brought forward 7%

+ Higher benefit scales 2.5%

+ Lost interest/premium/exp. 0.5%

= Total cost (% death premium) 10%

(Plus cost of TPD transfers where scales are different)

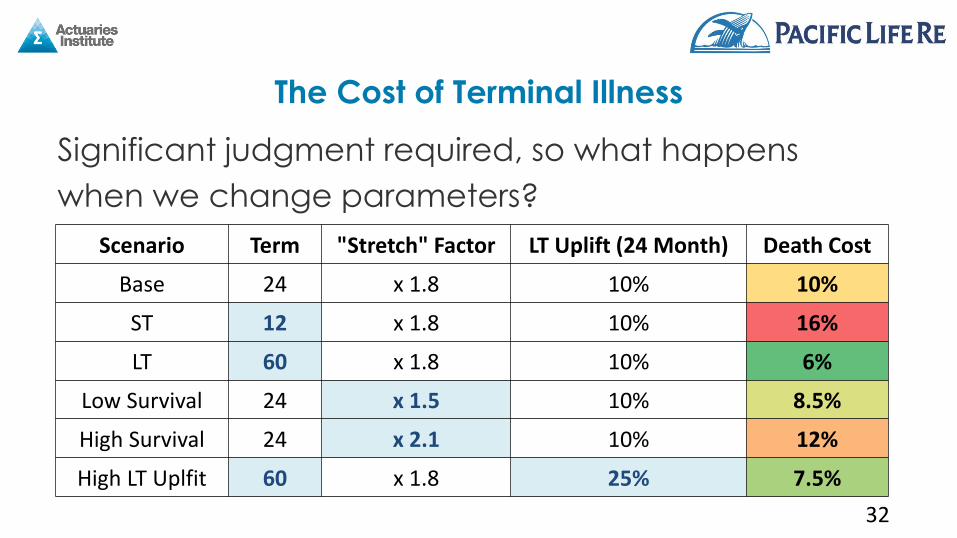

Significant judgment required, so what happens

when we change parameters?

The Cost of Terminal Illness

32

Scenario Term "Stretch" Factor LT Uplift (24 Month) Death Cost

Base 24 x 1.8 10% 10%

ST 12 x 1.8 10% 16%

LT 60 x 1.8 10% 6%

Low Survival 24 x 1.5 10% 8.5%

High Survival 24 x 2.1 10% 12%

High LT Uplfit 60 x 1.8 25% 7.5%

Concluding Thoughts

• TI Proportions Increasing

• Survival underestimated

• Guarantee periods shortened

+

• 24 Month TI Change

=

• Significant price increase

• Significant risk increase

Concluding Thoughts

34

Concluding Thoughts

35

Member Perspective

• Strong argument for alignment of insurance and SIS definitions.

• BUT arguments for different “burden of proof” for accessing member account balance compared to an insurance benefit.

• Consistency between different superannuation products (industry funds, master trusts and individual retail insurance policies).

Concluding Thoughts

36

Trustee Perspective

• Strong argument for alignment of insurance and SIS definitions.

• 24 month TI is predominately a one off transfer cost. Cost materially different for Industry Funds versus MT and retail policies.

• Implications for member equity as premium is being brought forward and issues of intergenerational equity.

• Timing of potential member premium increases. Equity and timing issues may be addresses by specific exit clauses by current insurer.

Concluding Thoughts

37

Alternative Product Designs

• Alignment of insurance and SIS definitions is NOT the only answer.

• Members could access their own money at 24 months and

insurance benefit at 12 months. Insurance cover would continue despite account balance being exhausted.

• Free cover would continue after SIS TI release for death / TI

insurance benefits.

• Horse has bolted!

• All that is left is to price this appropriately.

• Need to collect the data now to price this for the next five years – more detailed claims forms.

Concluding Thoughts

38