Embed Size (px)

DESCRIPTION

a Wiener Chaos approach. Pricing the Convexity Adjustment. Eric Benhamou. Convexity and CMS Coherence and consistence Wiener Chaos Results Conclusion. Framework. The major result of this paper is an approximation formula for convexity adjustment for any HJM interest rate model. - PowerPoint PPT Presentation

Citation preview

Pricing the ConvexityPricing the ConvexityAdjustmentAdjustment

Eric Benhamou

a Wiener Chaos approacha Wiener Chaos approach

Pricing the Convexity adjustment. 28 April 1999 Slide 2

FrameworkFrameworkThe major result of this paper is an approximation formula for convexity adjustment for any HJM interest rate model.

It is actually based on Wiener Chaos expansion. The methodology developed here could be applied to other financial products

Convexity and CMS Coherence and

consistence

Wiener Chaos

Results

Conclusion

Pricing the Convexity adjustment. 28 April 1999 Slide 3

• Two intriguing and juicy facts for options market:– Volatility smile– Convexity

• Convexity– Different meanings– But one mathematical sense– Many rules of thumb (Dean Witter (94))

IntroductionIntroduction

Pricing the Convexity adjustment. 28 April 1999 Slide 4

• CMS/CMT products– Definition– OTC deals– Increasing popularity

• Actual way to price the convexity– Numerical Computation (MC)– Black Scholes Adjustment (Ratcliffe Iben (93))– Approximation with Taylor formula

IntroductionIntroduction

Pricing the Convexity adjustment. 28 April 1999 Slide 5

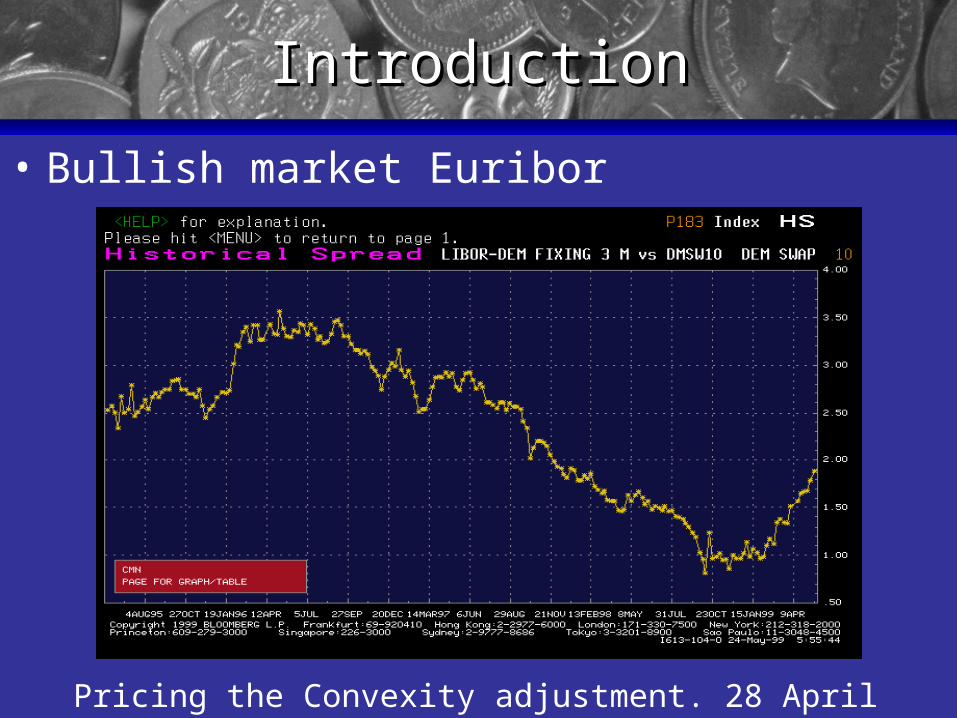

IntroductionIntroduction• Bullish market Euribor

Pricing the Convexity adjustment. 28 April 1999 Slide 6

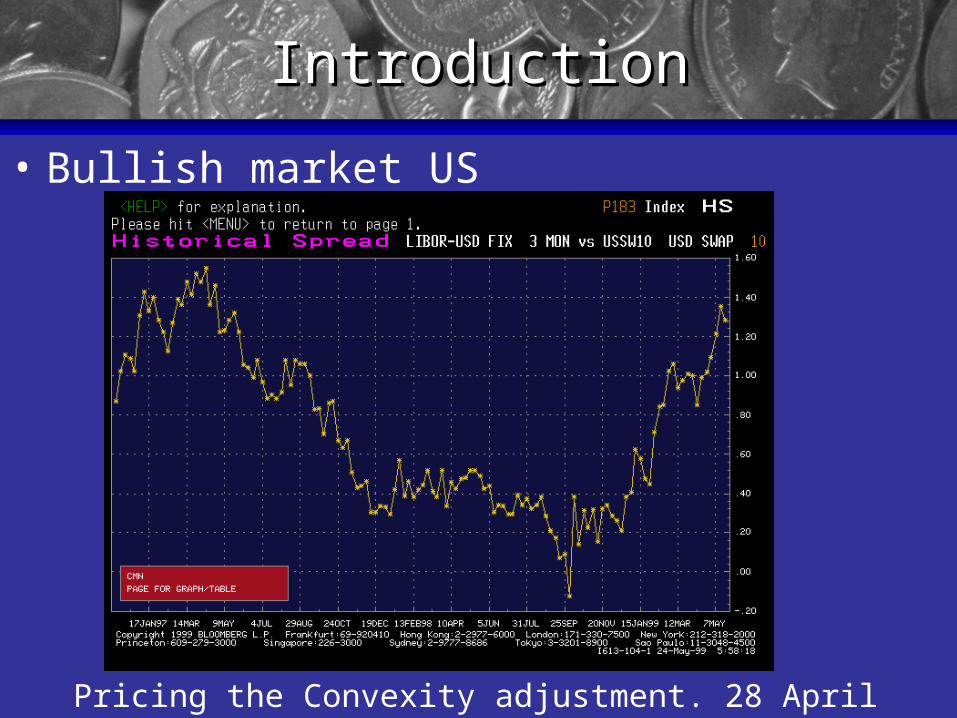

IntroductionIntroduction• Bullish market US

Pricing the Convexity adjustment. 28 April 1999 Slide 7

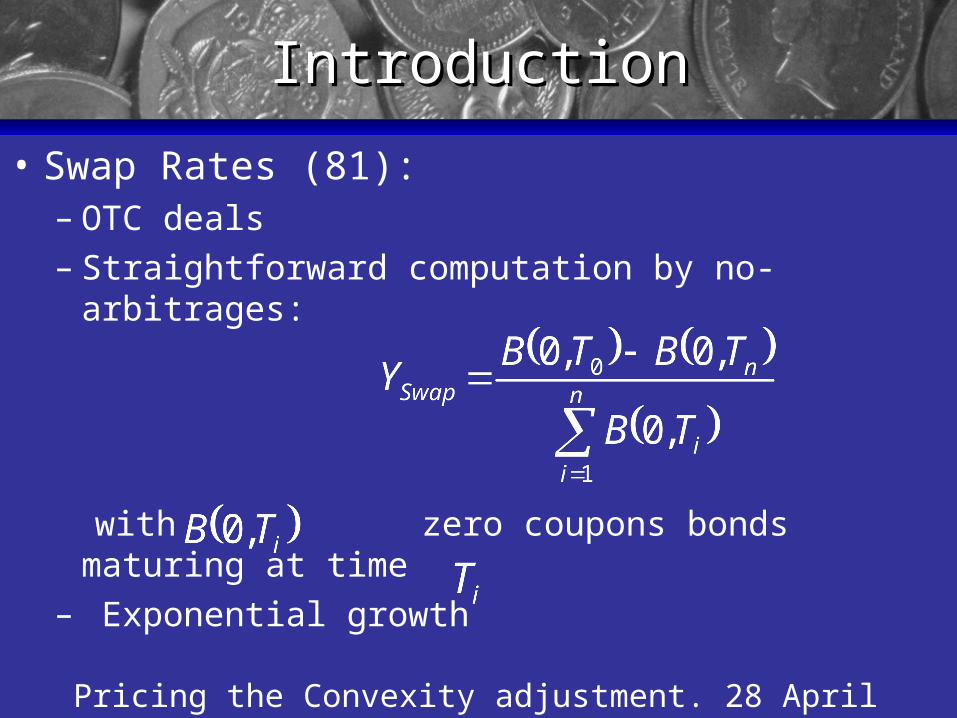

IntroductionIntroduction• Swap Rates (81):

– OTC deals– Straightforward computation by no-

arbitrages:

with zero coupons bonds maturing at time

– Exponential growth

Pricing the Convexity adjustment. 28 April 1999 Slide 8

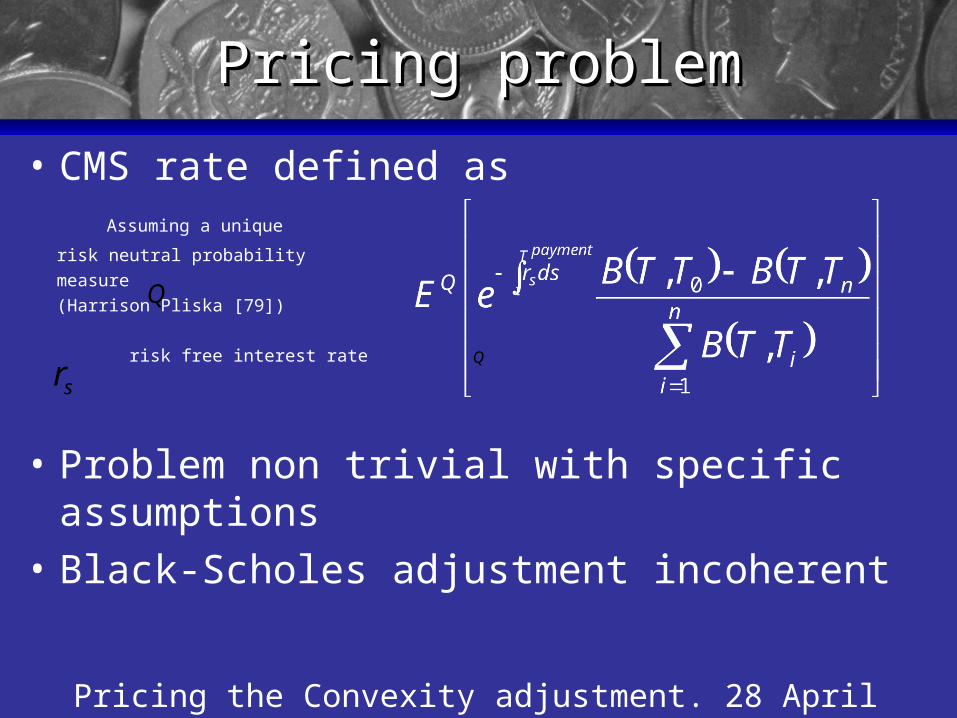

• CMS rate defined as Assuming a unique

risk neutral probability measure (Harrison Pliska [79])

risk free interest rate

• Problem non trivial with specific assumptions

• Black-Scholes adjustment incoherent

Pricing problemPricing problem

srQ

Q

Pricing the Convexity adjustment. 28 April 1999 Slide 9

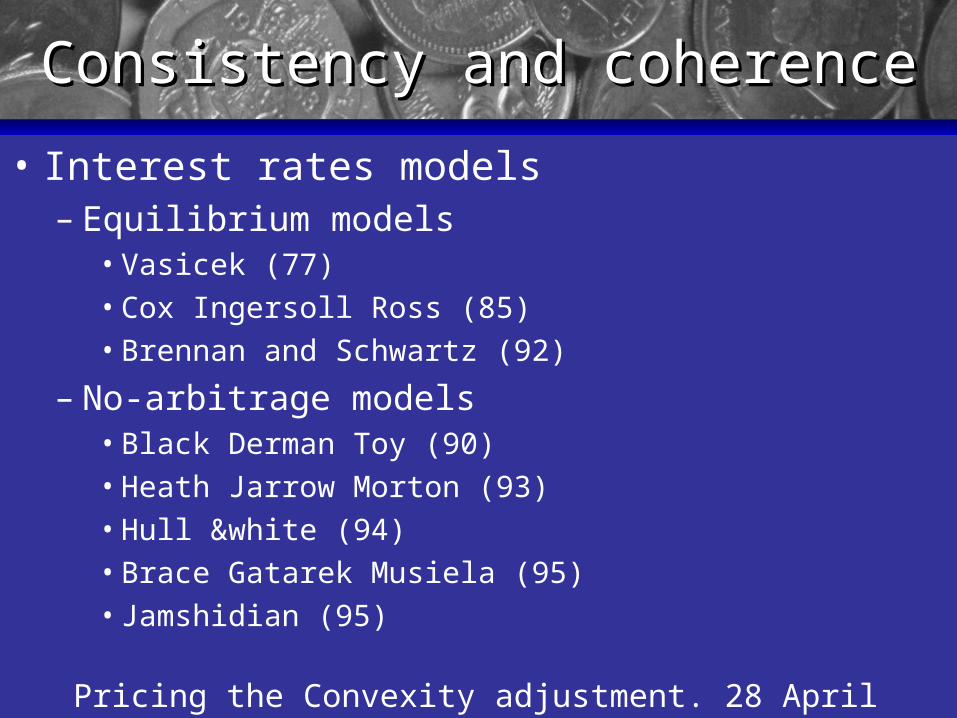

• Interest rates models– Equilibrium models

• Vasicek (77)• Cox Ingersoll Ross (85)• Brennan and Schwartz (92)

– No-arbitrage models• Black Derman Toy (90)• Heath Jarrow Morton (93) • Hull &white (94)• Brace Gatarek Musiela (95)• Jamshidian (95)

Consistency and coherenceConsistency and coherence

Pricing the Convexity adjustment. 28 April 1999 Slide 10

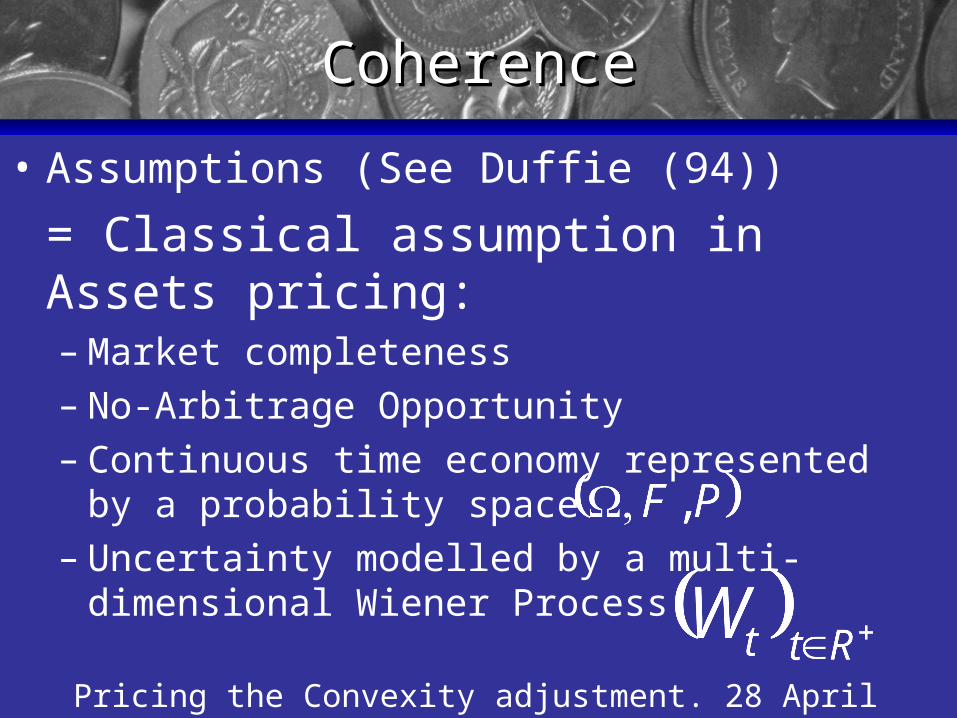

• Assumptions (See Duffie (94))= Classical assumption in Assets pricing:– Market completeness– No-Arbitrage Opportunity– Continuous time economy represented by a

probability space – Uncertainty modelled by a multi-

dimensional Wiener Process

CoherenceCoherence

Pricing the Convexity adjustment. 28 April 1999 Slide 11

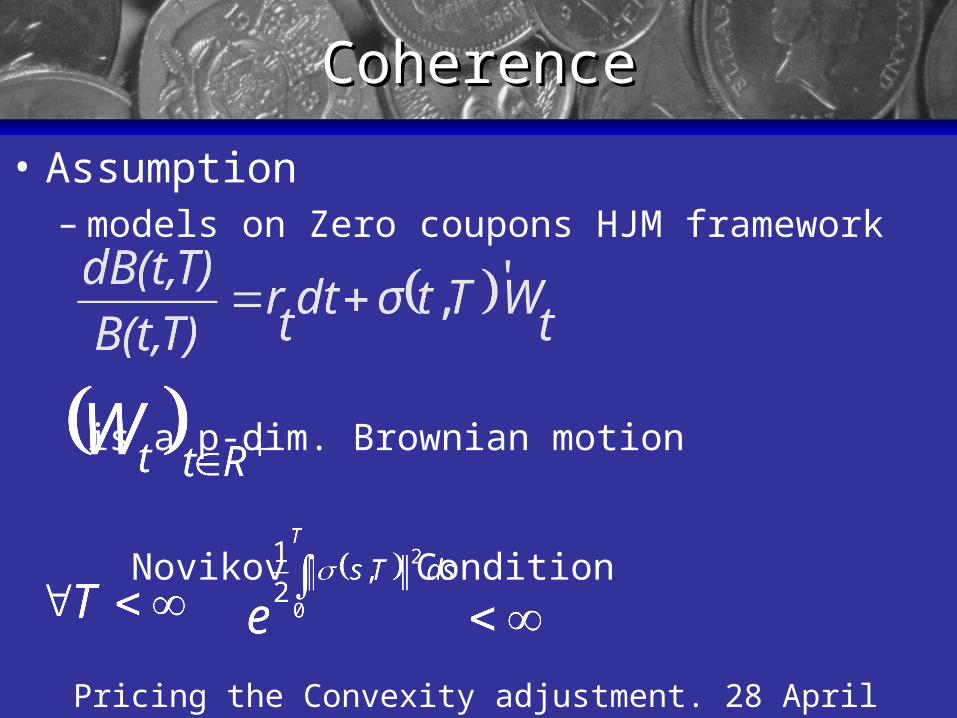

• Assumption– models on Zero coupons HJM framework

is a p-dim. Brownian motion

Novikov Condition

CoherenceCoherence

Pricing the Convexity adjustment. 28 April 1999 Slide 12

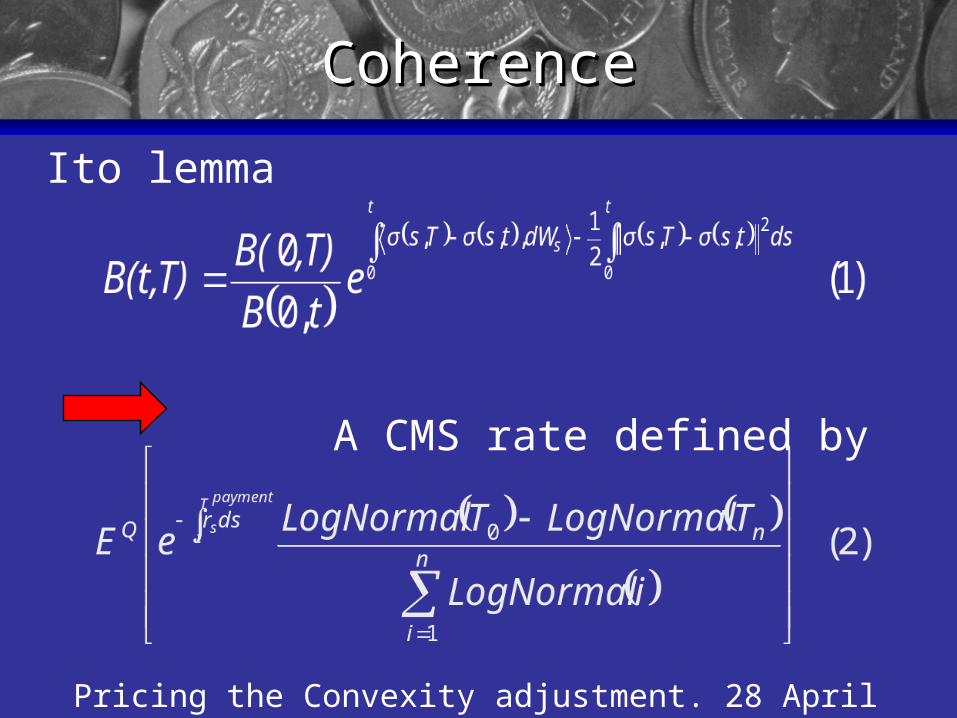

Ito lemma

A CMS rate defined by

CoherenceCoherence

Pricing the Convexity adjustment. 28 April 1999 Slide 13

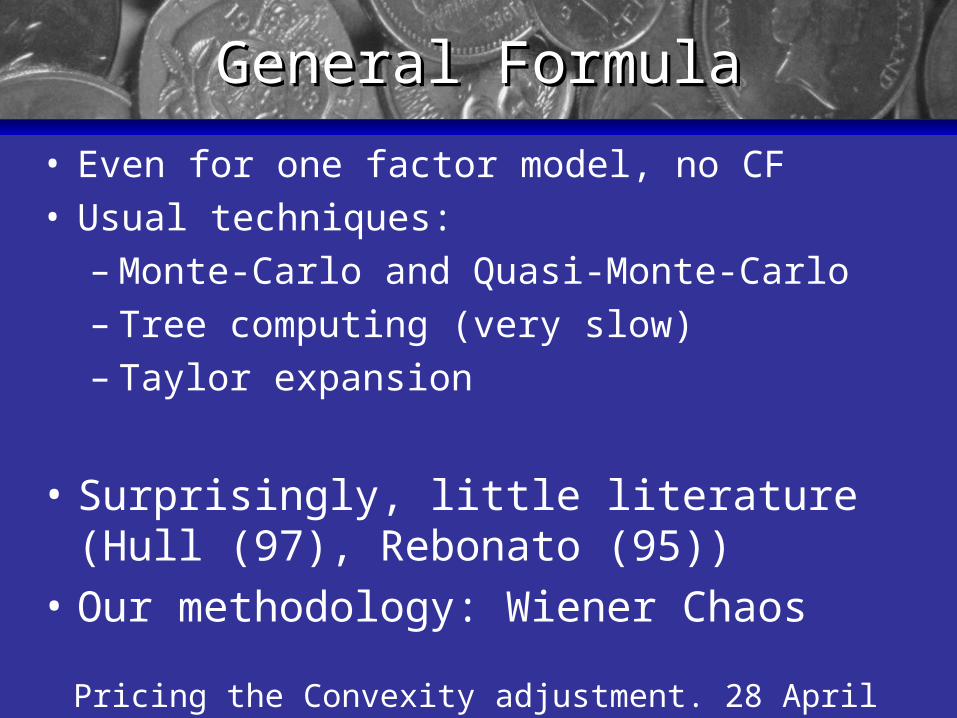

General FormulaGeneral Formula• Even for one factor model, no CF• Usual techniques:

– Monte-Carlo and Quasi-Monte-Carlo– Tree computing (very slow)– Taylor expansion

• Surprisingly, little literature (Hull (97), Rebonato (95))

• Our methodology: Wiener Chaos

Pricing the Convexity adjustment. 28 April 1999 Slide 14

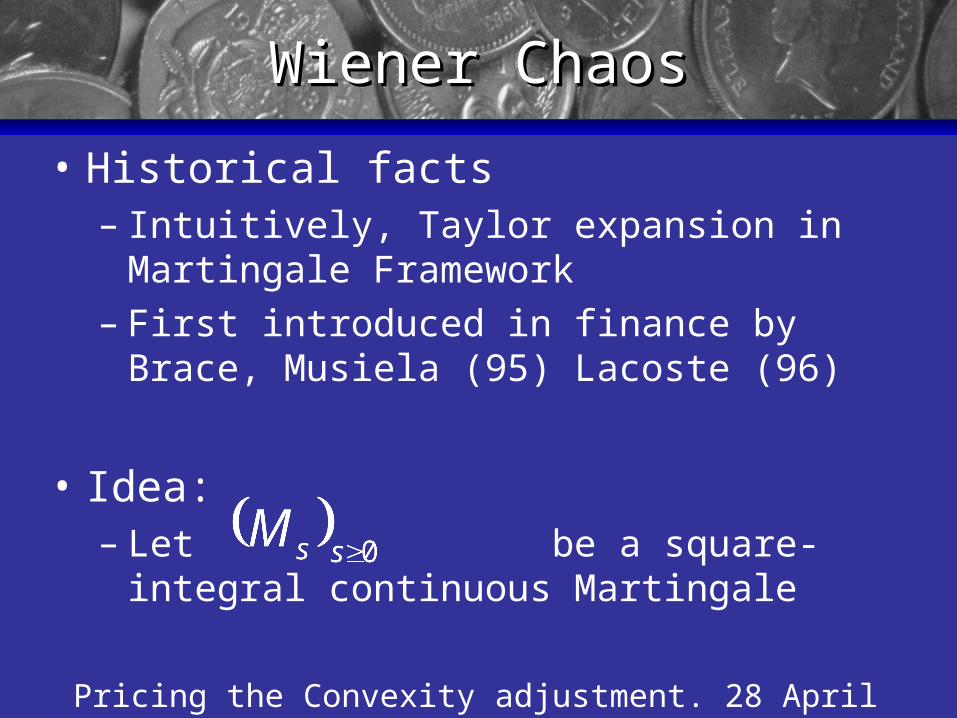

• Historical facts– Intuitively, Taylor expansion in

Martingale Framework – First introduced in finance by Brace,

Musiela (95) Lacoste (96)

• Idea:– Let be a square-integral

continuous Martingale

Wiener ChaosWiener Chaos

Pricing the Convexity adjustment. 28 April 1999 Slide 15

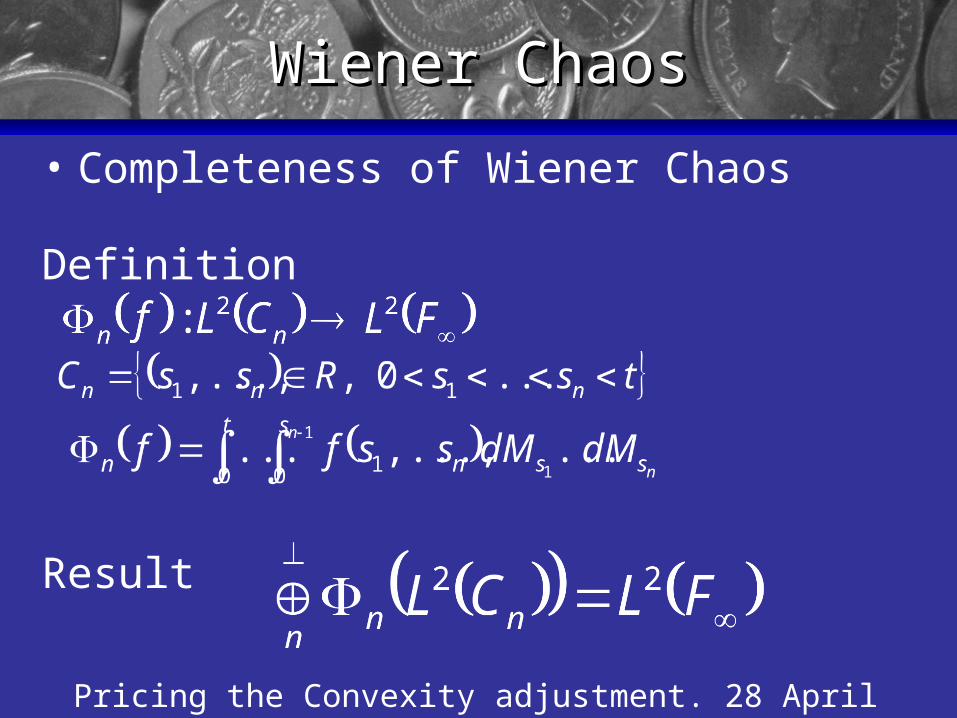

Wiener ChaosWiener Chaos• Completeness of Wiener Chaos

Definition

Result

Pricing the Convexity adjustment. 28 April 1999 Slide 16

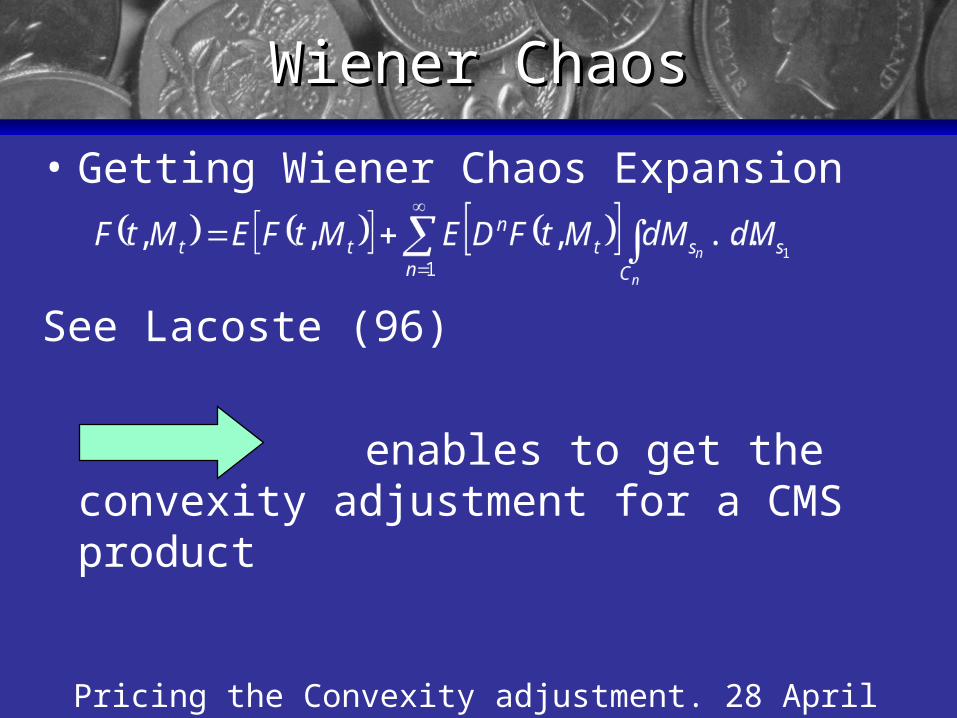

• Getting Wiener Chaos Expansion

See Lacoste (96)

enables to get the convexity adjustment for a CMS product

Wiener ChaosWiener Chaos

Pricing the Convexity adjustment. 28 April 1999 Slide 17

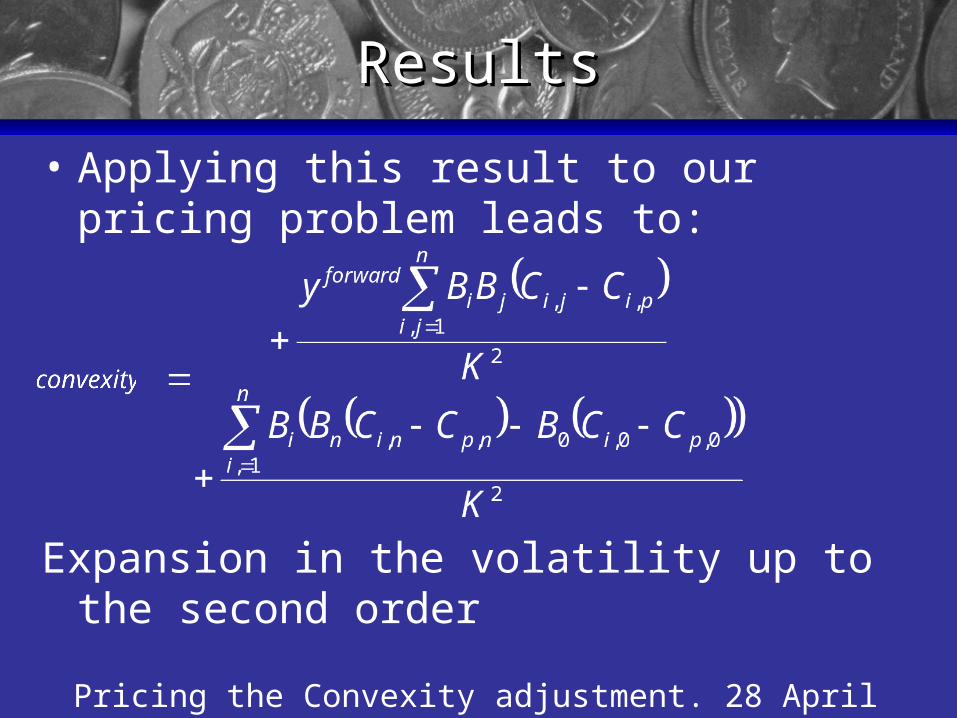

ResultsResults • Applying this result to our pricing

problem leads to:

Expansion in the volatility up to the second order

Pricing the Convexity adjustment. 28 April 1999 Slide 18

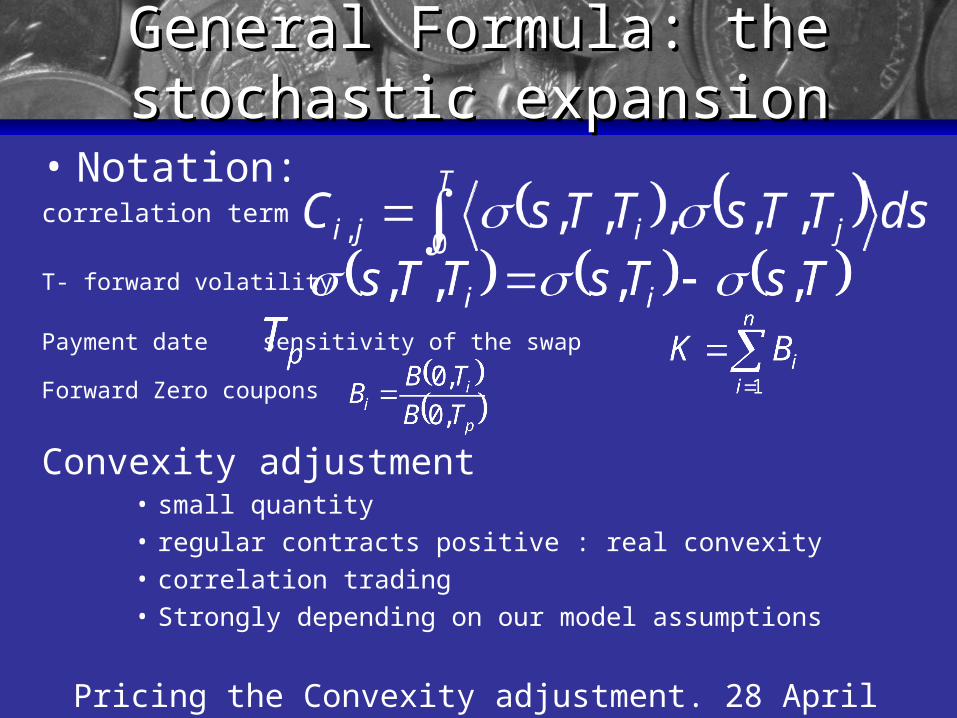

• Notation:correlation term

T- forward volatility

Payment date sensitivity of the swap Forward Zero coupons

Convexity adjustment• small quantity• regular contracts positive : real convexity• correlation trading• Strongly depending on our model assumptions

General Formula: the General Formula: the stochastic expansionstochastic expansion

Pricing the Convexity adjustment. 28 April 1999 Slide 19

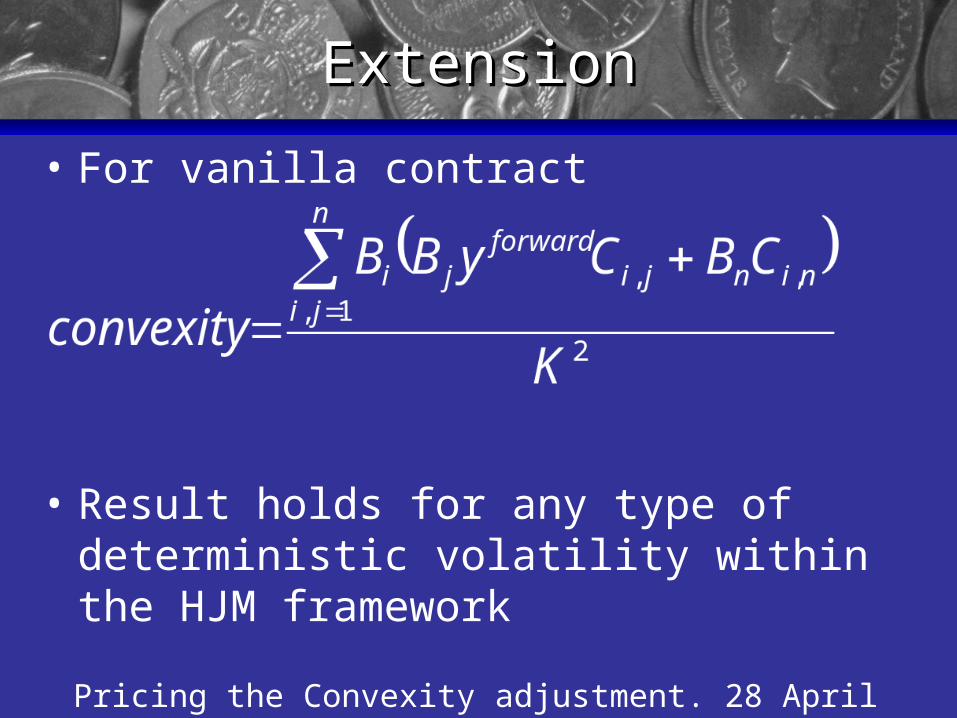

ExtensionExtension • For vanilla contract

• Result holds for any type of deterministic volatility within the HJM framework

Pricing the Convexity adjustment. 28 April 1999 Slide 20

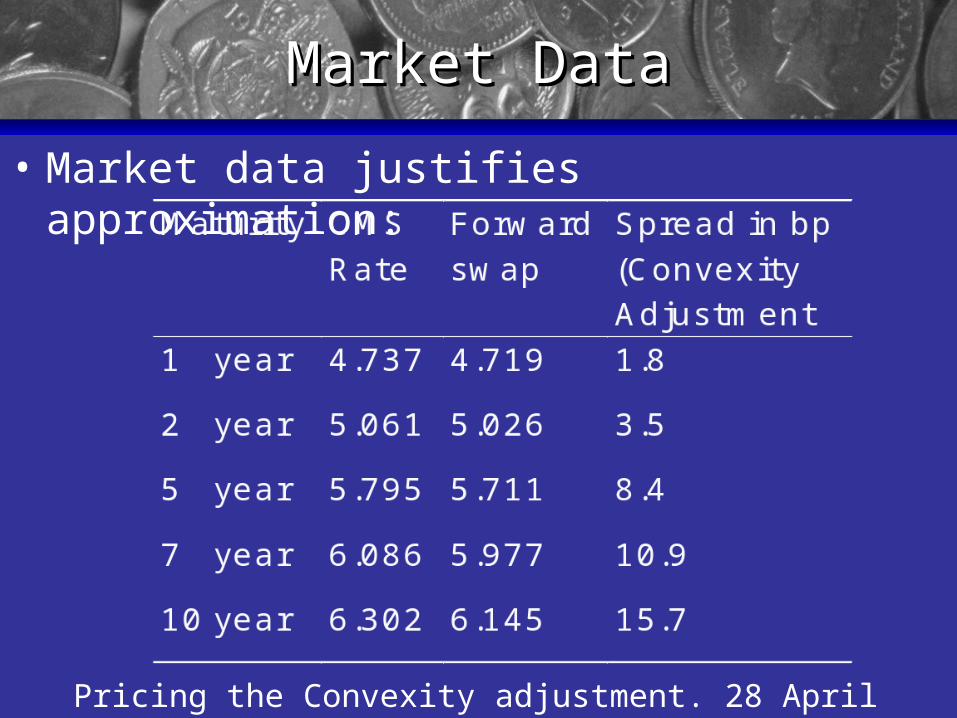

Market DataMarket Data• Market data justifies approximation:

Pricing the Convexity adjustment. 28 April 1999 Slide 21

INTERESTS:• Methodology could be applied to other

intractable options• Very interesting for multi-factor

models where numerical procedures time-consuming

• Enables to price convexity consistent with yield curve models

• Demystify convexity

ConclusionConclusion

Pricing the Convexity adjustment. 28 April 1999 Slide 22

ConclusionConclusion LIMITATIONS:

• Need Market completeness– No stochastic volatility– Need model given by its zero coupons

diffusions• Wiener Chaos only useful for small

correction (Swaptions, Asiatic should not work)