Embed Size (px)

Citation preview

___________________________________________________________________________

2014/SMEWG38/025 Agenda Item: 11.2

Promoting Financial Inclusion and Literacy among SME – Indonesian Experience

Purpose: Information

Submitted by: Indonesia

38th Small and Medium Enterprises Working Group Meeting

Taichung, Chinese Taipei26-27 March 2014

4/7/2014

1

PROMOTING FINANCIAL INCLUSION AND LITERACY AMONG SME

Indonesian Experience

The 38th APEC SME WG MeetingTaichung, Chinese Taipei26 – 27 March 2014

2

OUTLINE

IAccess to Finance

IIThe Role of SMEs in Indonesian Economy

III

National Strategy for Financial Inclusion IV

Financial Education Experience V

The Way Forward VI

Financial Literacy Survey Findings

4/7/2014

2

5

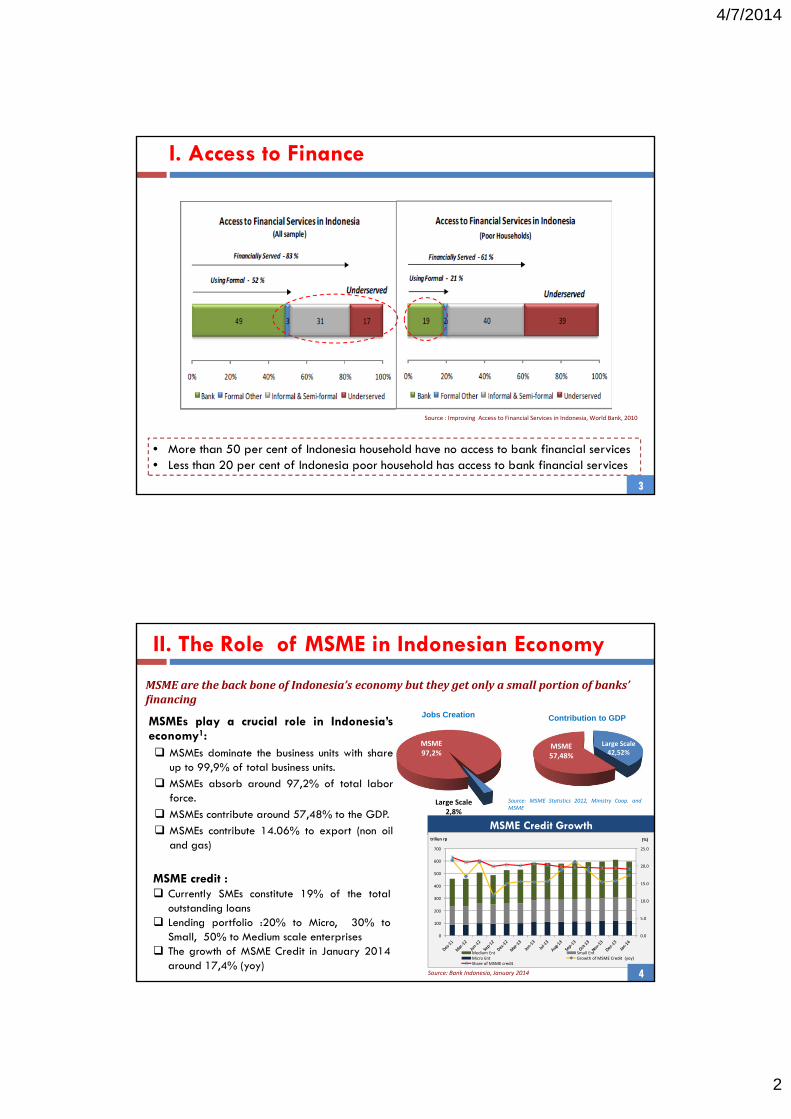

• More than 50 per cent of Indonesia household have no access to bank financial services• Less than 20 per cent of Indonesia poor household has access to bank financial services

Source : Improving Access to Financial Services in Indonesia, World Bank, 2010

3

I. Access to Finance

7

MSME arethebackboneofIndonesia’seconomybuttheygetonlyasmallportionofbanks’financing

Large Scale2,8%

MSME97,2%

Jobs Creation

Large Scale42,52%

MSME57,48%

Contribution to GDP

Source: MSME Statistics 2012, Ministry Coop. andMSME

Source: Bank Indonesia, January 2014

MSME Credit Growth

MSMEs play a crucial role in Indonesia’seconomy1:

MSMEs dominate the business units with shareup to 99,9% of total business units.MSMEs absorb around 97,2% of total laborforce.MSMEs contribute around 57,48% to the GDP.MSMEs contribute 14.06% to export (non oiland gas)

II. The Role of MSME in Indonesian Economy

MSME credit :Currently SMEs constitute 19% of the totaloutstanding loansLending portfolio :20% to Micro, 30% toSmall, 50% to Medium scale enterprisesThe growth of MSME Credit in January 2014around 17,4% (yoy)

0.0

5.0

10.0

15.0

20.0

25.0

0

100

200

300

400

500

600

700

(%)triliun rp

Medium Ent Small EntMicro Ent Growth of MSME Credit (yoy)‐Share of MSME credit

4

4/7/2014

3

5

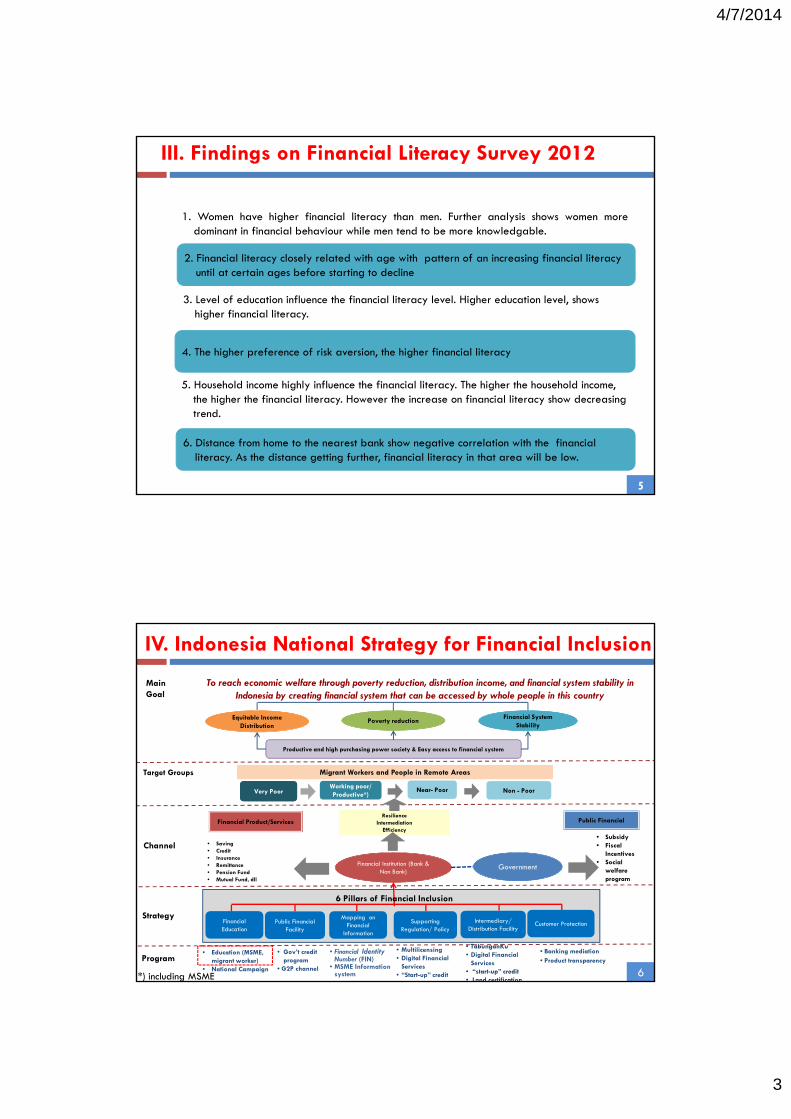

1. Women have higher financial literacy than men. Further analysis shows women moredominant in financial behaviour while men tend to be more knowledgable.

2. Financial literacy closely related with age with pattern of an increasing financial literacy until at certain ages before starting to decline

3. Level of education influence the financial literacy level. Higher education level, shows higher financial literacy.

4. The higher preference of risk aversion, the higher financial literacy

5. Household income highly influence the financial literacy. The higher the household income, the higher the financial literacy. However the increase on financial literacy show decreasing trend.

6. Distance from home to the nearest bank show negative correlation with the financial literacy. As the distance getting further, financial literacy in that area will be low.

III. Findings on Financial Literacy Survey 2012

5

Intermediary/Distribution Facility

Supporting Regulation/ Policy

Mapping on Financial

Information

Public Financial Facility

Financial Institution (Bank & Non Bank)

• Banking mediation• Product transparency

• TabunganKu• Digital Financial

Services• “start-up” credit• Land certification

• Multilicensing• Digital Financial

Services• “Start-up” credit

• Education (MSME, migrant worker)

• National Campaign

• Financial IdentityNumber (FIN)

• MSME Information system

Poverty reduction Financial System Stability

Equitable IncomeDistribution

Productive and high purchasing power society & Easy access to financial system

Program

Strategy

Channel

6 Pillars of Financial Inclusion

Customer Protection

Target Groups

Financial Education

Public Financial

• Subsidy• Fiscal

Incentives• Social

welfare program

Financial Product/Services

• Saving• Credit• Insurance• Remittance• Pension Fund• Mutual Fund, dll

Migrant Workers and People in Remote AreasMigrant Workers and People in Remote Areas

Very PoorVery PoorWorking poor/ Productive*) Non - Poor

• Gov’t credit program

• G2P channel

ResilienceIntermediation

Efficiency

Government

Main Goal

To reach economic welfare through poverty reduction, distribution income, and financial system stability in Indonesia by creating financial system that can be accessed by whole people in this country

IV. Indonesia National Strategy for Financial Inclusion

6

Near- Poor

*) including MSME

4/7/2014

4

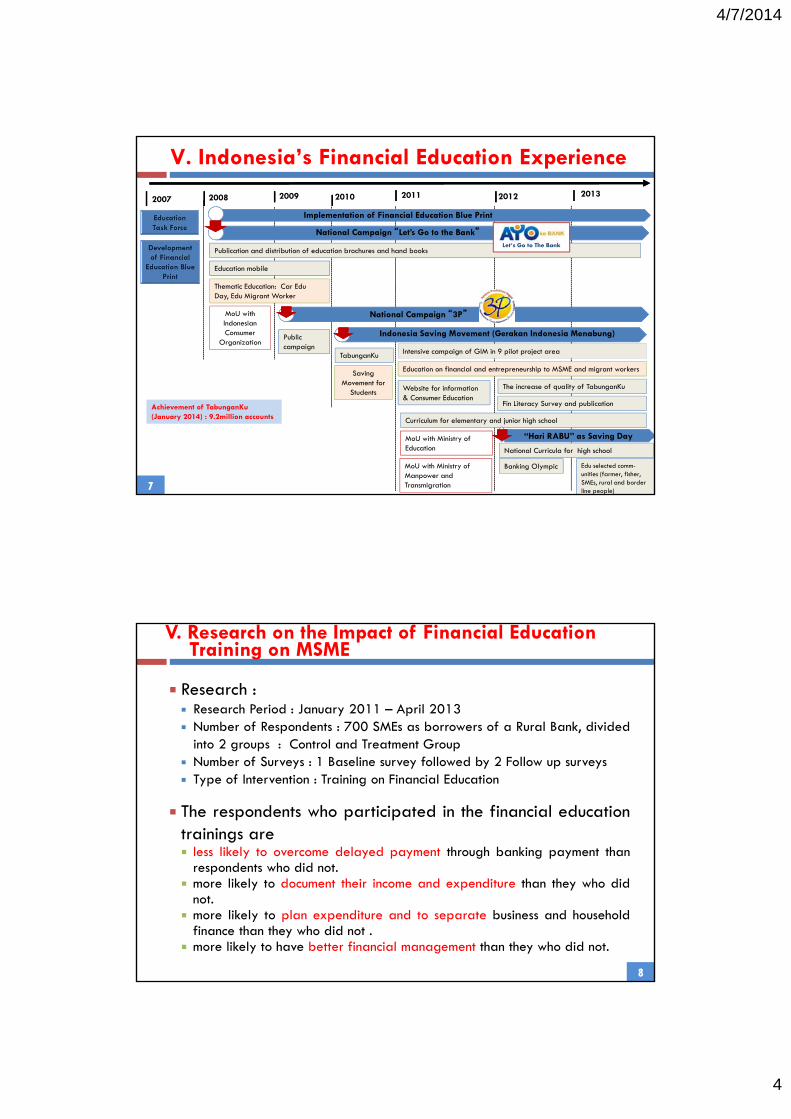

2007 2008 2009 2010 2011 2012 2013

Implementation of Financial Education Blue Print

National Campaign “Let’s Go to the Bank”

National Campaign “3P”

Indonesia Saving Movement (Gerakan Indonesia Menabung)

Publication and distribution of education brochures and hand books

Education mobile

MoU with Indonesian Consumer

Organization

Thematic Education: Car Edu Day, Edu Migrant Worker

Public campaign

TabunganKu Intensive campaign of GIM in 9 pilot project area

MoU with Ministry of Manpower and Transmigration

Saving Movement for

Students

Education on financial and entrepreneurship to MSME and migrant workers

Website for information & Consumer Education

Curriculum for elementary and junior high school

National Curricula for high school

The increase of quality of TabunganKu

Fin Literacy Survey and publication

Let’s Go to The Bank

MoU with Ministry of Education

“Hari RABU” as Saving Day

Edu selected comm-unities (farmer, fisher, SMEs, rural and border line people)

Banking Olympic

Achievement of TabunganKu(January 2014) : 9.2million accounts

V. Indonesia’s Financial Education Experience

7

Research :Research Period : January 2011 – April 2013Number of Respondents : 700 SMEs as borrowers of a Rural Bank, dividedinto 2 groups : Control and Treatment GroupNumber of Surveys : 1 Baseline survey followed by 2 Follow up surveysType of Intervention : Training on Financial Education

The respondents who participated in the financial educationtrainings are

less likely to overcome delayed payment through banking payment thanrespondents who did not.more likely to document their income and expenditure than they who didnot.more likely to plan expenditure and to separate business and householdfinance than they who did not .more likely to have better financial management than they who did not.

V. Research on the Impact of Financial Education Training on MSME

8

4/7/2014

5

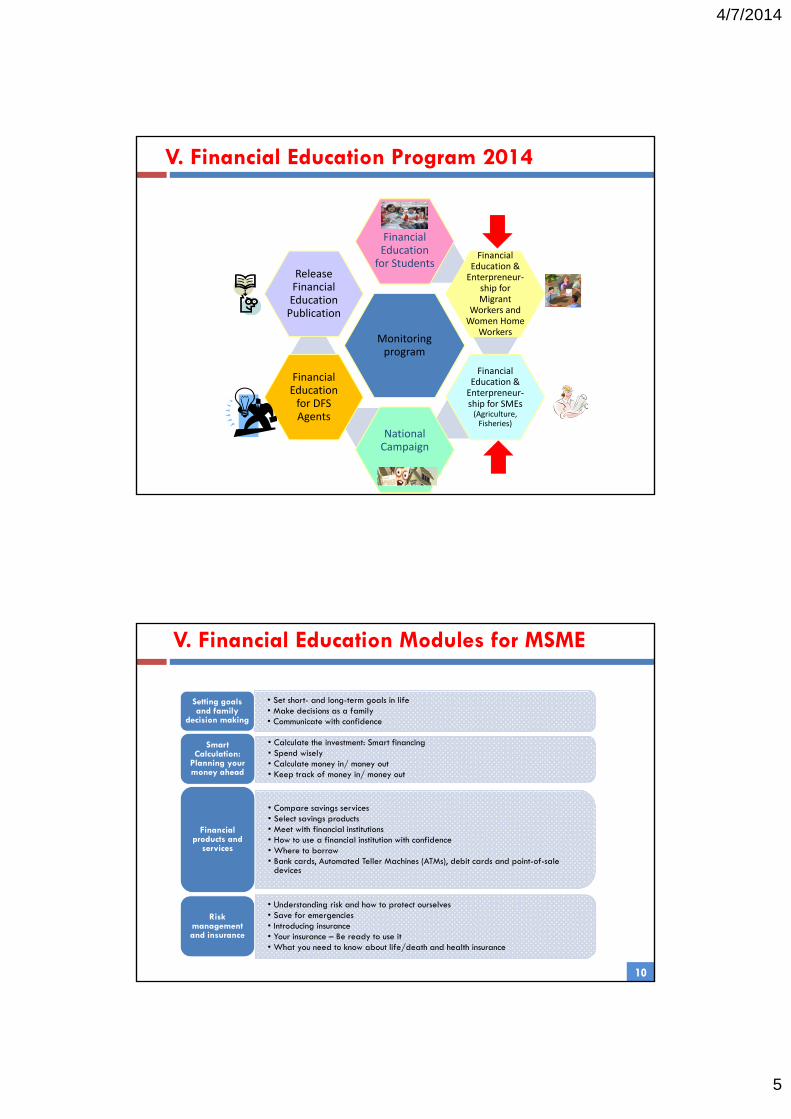

V. Financial Education Program 2014 9

Monitoring program

Financial Education for Students

Financial Education & Enterpreneur‐

ship for Migrant

Workers and Women Home

Workers

Financial Education & Enterpreneur‐ship for SMEs (Agriculture, Fisheries)

National Campaign

Financial Education for DFS Agents

Release Financial Education Publication

V. Financial Education Modules for MSME 10

• Set short- and long-term goals in life • Make decisions as a family • Communicate with confidence

Setting goals and family

decision making

• Calculate the investment: Smart financing • Spend wisely • Calculate money in/ money out• Keep track of money in/ money out

Smart Calculation:

Planning your money ahead

• Compare savings services • Select savings products • Meet with financial institutions • How to use a financial institution with confidence • Where to borrow • Bank cards, Automated Teller Machines (ATMs), debit cards and point-of-sale

devices

Financial products and

services

• Understanding risk and how to protect ourselves • Save for emergencies • Introducing insurance • Your insurance – Be ready to use it • What you need to know about life/death and health insurance

Risk management and insurance

10

4/7/2014

6

VI. The Way Forward

Financial Education will be integrated with other SME developmentprograms such as clusters.

Financial education will be focused on Training of Trainers (ToT), so that theToT participants are expected to provide education directly to thecommunity.

Replicate the financial education program at national level to improvefinancial literacy that can increase financial capability and assist theeffectiveness of financial inclusion through financial education.

Target groups of financial education will be expanded, not only to SMEs inagriculture and fisheries sector but also in other sectors such as industry,trade, mining sectors in cooperation with related stakeholders

11