Embed Size (px)

Citation preview

7/27/2019 Q2 13 Quarterly Economic Survey

http://slidepdf.com/reader/full/q2-13-quarterly-economic-survey 1/2

A

Domestic Market

Most national domestic balances improved in Q2; they are

much higher than their average levels in the recession o

2008-09, and also above their long-term historical averages.

But all balances are still below their pre-recession levels in

2007. The manuacturing balance or home deliveries rose

our points to +16%, the best level since Q2 2011. The Q2

balance or manuacturers’ home orders stayed unchanged

at +14%, still the equal best level since Q4 2010. The service

sector’s balance or home deliveries rose eight points, to

+20%, the best level since Q4 2007. The Q2 balance or

service home orders rose ve points to +16%, also the best

level since Q4 2007.

Export Market

Most national export balances improved in Q2. The service

export balances are at historically high levels, but the

manuacturing export balances are still slightly below their

pre-recession levels in 2007. The manuacturing export

deliveries balance rose our points, to +23%, the best level

since Q2 2012. The manuacturing export orders balance

stayed unchanged in Q2 2013 at +22%, still the equal best

level since Q2 2012. The service export deliveries balance

rose three points in Q2 to +36%, the highest since our

survey started in Q1 1989. The service export orders balance

increased three points, to +29%, the best level since the all-

time high seen in Q4 1994, which was +31%.

Employment

National employment balances rose in Q2. The

manuacturing employment balance rose eight points, to

+19%, the best level since Q4 2010. The manuacturing

employment expectations balance rose six points, to +20%,

the best since Q1 2005. Both manuacturing balances

are above their pre-recession levels in 2007. The service

employment balance rose nine points, to +15%, the best

level since Q1 2008. The service employment expectations

balance rose 11 points, to +22%, the best since Q4 2007. Both

service balances are now above their long-term historical

averages but still below their pre-recession levels in 2007.

Investment

The Q2 national investment balances recorded divergent

movements, rising or manuacturing and alling or services.

The balance o manuacturing rms planning to increase

investment in plant & machinery rose nine points, to +23%,

the equal best level since Q3 2007. Manuacturing intentions

to invest in training rose one point, to +20%, the equal best

level since Q1 2008. The balance o service rms planning

to increase investment in plant & machinery ell two points,

to +7%. Service sector intentions to invest in training ell two

points, to +15%. All the investment balances are still below

their average 2007 pre-recession levels.

The Q2 2013 results show urther welcome progress. For both manuacturing

and services, most Q2 key balances are stronger than in Q1, but are still below

their pre-recession levels in 2007. The strength o the export balances, notably in

services, is again one o the most positive eatures o the results. It is remarkable

that the Q2 service export balances are at or near their all-time highs. Improved

condence, and strong employment balances are encouraging results. However, it

is disappointing that the service investment balances have allen, and remain weak

by historical standards. Cashow is weak in both sectors, and the services balance

worsened. Plans to raise prices eased, but ination remains a signicant concern in

both sectors. Price pressures rom pay settlements and raw materials receded, but

those rom nancial costs rose. Overall, the Q2 results support our view that the

economy will gradually strengthen over the next year, but serious risks still persist.

The domestic sales balance

rose or both manuacturing (+16%)

and services (+20%)

Summary 2nd Quarter 2013

Export sales increased in both sectors

Manufacturing +8% (-16pts) Services +15% (-4pts)

-14pts

to

-6%

-7pts

to -2%

+4pts

to

+ 16%

+8pts

to

+20% Manuacturing +23% (+4pts) Services +36% (+3pts)

7/27/2019 Q2 13 Quarterly Economic Survey

http://slidepdf.com/reader/full/q2-13-quarterly-economic-survey 2/2

B

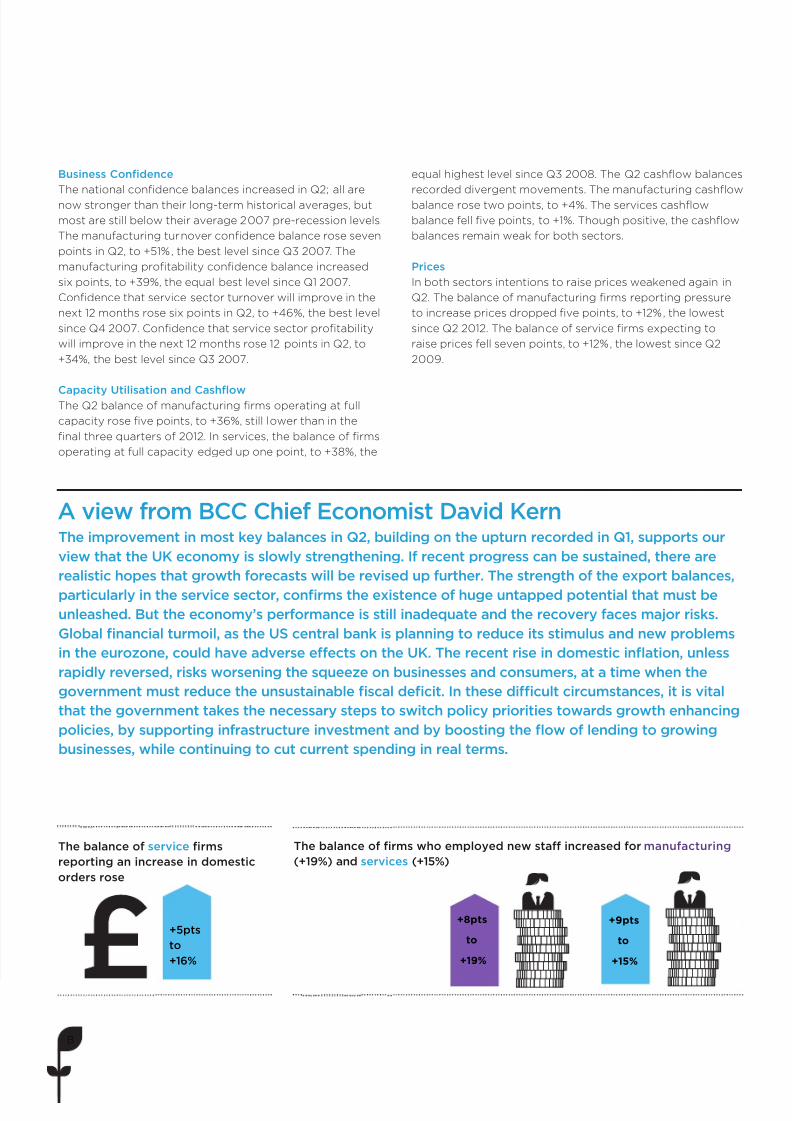

Business Condence

The national condence balances increased in Q2; all are

now stronger than their long-term historical averages, but

most are still below their average 2007 pre-recession levels.

The manuacturing turnover condence balance rose seven

points in Q2, to +51%, the best level since Q3 2007. The

manuacturing protability condence balance increased

six points, to +39%, the equal best level since Q1 2007.

Condence that service sector turnover will improve in the

next 12 months rose six points in Q2, to +46%, the best level

since Q4 2007. Condence that service sector protability

will improve in the next 12 months rose 12 points in Q2, to

+34%, the best level since Q3 2007.

Capacity Utilisation and CashowThe Q2 balance o manuacturing rms operating at ull

capacity rose ve points, to +36%, still lower than in the

nal three quarters o 2012. In services, the balance o rms

operating at ull capacity edged up one point, to +38%, the

equal highest level since Q3 2008. The Q2 cashfow balances

recorded divergent movements. The manuacturing cashfow

balance rose two points, to +4%. The services cashfow

balance ell ve points, to +1%. Though positive, the cashfow

balances remain weak or both sectors.

Prices

In both sectors intentions to raise prices weakened again in

Q2. The balance o manuacturing rms reporting pressure

to increase prices dropped ve points, to +12%, the lowest

since Q2 2012. The balance o service rms expecting to

raise prices ell seven points, to +12%, the lowest since Q2

2009.

The balance o service rms

reporting an increase in domestic

orders rose

The balance o rms who employed new sta increased or manuacturing

(+19%) and services (+15%)

The improvement in most key balances in Q2, building on the upturn recorded in Q1, supports our

view that the UK economy is slowly strengthening. I recent progress can be sustained, there are

realistic hopes that growth orecasts will be revised up urther. The strength o the export balances,

particularly in the service sector, conrms the existence o huge untapped potential that must be

unleashed. But the economy’s perormance is still inadequate and the recovery aces major risks.

Global nancial turmoil, as the US central bank is planning to reduce its stimulus and new problems

in the eurozone, could have adverse eects on the UK. The recent rise in domestic ination, unless

rapidly reversed, risks worsening the squeeze on businesses and consumers, at a time when the

government must reduce the unsustainable scal decit. In these difcult circumstances, it is vital

that the government takes the necessary steps to switch policy priorities towards growth enhancing

policies, by supporting inrastructure investment and by boosting the ow o lending to growing

businesses, while continuing to cut current spending in real terms.

A view rom BCC Chie Economist David Kern

+8pts

to +19%

+5pts

to

+16%

+9pts

to +15%