Embed Size (px)

Citation preview

Quantitative Easing & Tapering

Global Bond Yield Trends

Negative Interest Rates in Eurozone?

Global GDP & Inflationary Trend

Market Performance & Insights

Equity & Debt Market Overview

Snapshot of Recommended Funds

Facts and FiguresU

nit

ed

Sta

tes

•QE level - $35 billion.

•Fed plans to end QE in October 2014

•GDP (Q1 2014) - -2.9%

•Inflation (May 2014) - 2.1%

•ISM PMI (June 2014) - 55.3%

•Dow crossed the historic high to end at 17,068.26 on 3rd July owing to the fall in June unemployment rate to 6.1% from 6.3%.

•IMF growth forecast 2014 - 2% Eu

roZo

ne

•On 11th June 2014, ECB cut its benchmark interest rate to 0.15%

•Deposit rate - -0.1% (First major central bank to use negative interest rate)

•Euro area jobless rate at 11.6% in May

•Inflation (Expected) June 2014 - 0.5% (Economy gripped with deflationary fear)

•Q1 2014 GDP - 0.30%

•HSBC PMI June 2014 - 51.8%

•IMF growth forecast (2014) - 1.2% (2015) - 1.5%

Ch

ina

•Inflation (June 2014) - 2.3% (lower from 2.5% in May)

•GDP (Q1 2014) - 7.4%

•HSBC PMI (June 2014) - 50.7

•Current biggest challenge to the Chinese economy - Shadow Banking

•IMF Growth forecast (2014) - 7.5%

•Growth forecast for 2015 has been cut from 7.3% to 7% (IMF)

Ind

ia

•GDP (Q1 2014 Calendar Year) - 4.61% (sub 5%, mainly due to contraction in manufacturing sector)

•WPI - 6.01% CPI - 8.28% (May 2014)

•Repo Rate - 8%

•SLR - 22.5% (from 23%, aiming to increase bank credit)

•Budget 2014-15 - Tax advantage of debt funds over fixed deposit eliminated

•HSBC PMI (June 2014) - 51.5%

•IMF growth forecast (2014) - 5.4%, (2015) - 6.4%

Quantitative Easing

It was tried first by a central bank in Japan to get it

out of a period of deflation following its asset

bubble collapse in the 1990s.

Under QE a central bank purchases government

bonds from insurance companies, pension funds and

Banks. This in turn pushes up the bond prices and

lowers the interest rates. Hence they become less

attractive investment and discourages savings

leading to rise in spending by individuals and

businesses for consumption of goods and services.

Such low interest rate scenario forces individuals and

businesses to invest in equity or fixed income

security to earn higher interest rate on their savings.

This floods money into investment institutions. Hope

is, this would inherently increase investment in the

economy (since the interest rates are low!!) and

boost the economy.

Usually, central banks try to raise the amount of

lending activity in the economy indirectly, by cutting

interest rates. But when interest rates cannot go any

lower, a central bank's only option is to pump money

into the economy directly. The way central bank

does this is by buying government bonds. Pumping

liquidity into the economy by sustained buying of

treasury and mortgage-backed securities from banks

results in cash injection into banks and lowers

interest rates which in turn should lead to larger

lending and a boost to economic activity.

Tapering

The term “taper” was introduced to the global

economy on 22nd

May, 2013, by the then Fed

Chairman Ben Bernanke, who stated that Fed may

taper the $85 bn bond buying program (QE) in the

coming months. This announcement lead the market

participants of believe, interest rates are likely to

increase in the investment safe heaven. Fed started

the taper talk when the US 2013 Q2 GDP came in at

2.5% and unemployment rate decreased to 7.4% in

July 2013. This lead to heavy capital outflow and

currency depreciation in EM countries with large

external deficits, particularly, Indonesia and India. It

further led to worsening current account deficit, thin

reserves and high inflation rates.

MACROECONOMIC OUTLOOK – GLOBAL

Global 10 year Government Security Rate Trends

United States of America Euro Zone (28 Members)

China India

United States of America

•Main factors affecting Bond Yield - GDP Growth, Inflation.

•Longest run of historically low interest rates - at 0 - 0.25% since December 2008.

•Fed has aggressively bought treasury and mortgage related securities.

•Observed artificially pressured long and short term interest rate.

•Fed is expected to end QE by the end of 2014, which will push up the bond yields and key interest rates.

Euro Zone

•From late 2009, upsurge in private and government debt levels and downgrading of government debt in some European states led to fear of sovereign debt crisis.

•Increasing debt levels and increasing default risks led to increase in their sovereign bond yields.

•ECB then planned to purchase sovereign bonds in unlimited quantities, driving down yields.

China

•The yield for the bonds have been increasing since 2009 but stalled during Q3-2011.

•Since the second half of 2013, bond investment demand reduced and issuing interest rate rose. It resulted in the increase of issuance cost.

India

•Movement in bond yields is an indicator of how interest rates have behaved .

•10 Year Benchmark yield from Jan 2009 to May 2014 has remained in the band of 6.19% to 8.65%.

•Inflation experienced is one of the prime reason which has forced the central bank to keep the interest rates high.

•Outflow of funds on account of possibility of taper is another reason to keep the interest rates high. FIIs invest to take advantage of higher interest rate differentials among the countries.

Negative Interest Rates in Eurozone – What does it mean?

Negative Interest Rates in Eurozone – What does it mean?

The ECB has cut its benchmark interest rate to 0.15% from 11 June’14, a new record low. Before, it had been

0.25%. By cutting it further, the ECB hopes to bring down interest rates. ECB wants banks to lend more to

businesses. This is because bank lending is falling in the 18-member state Eurozone.

In Eurozone, after several years of crisis, there are concerns that the recovery is not sustainable, in large part

due to falling bank lending.

Bank lending is a way of increasing the money supply. Growth relies on there being more money around for

consumers to spend and businesses to invest in expanding their output and hiring more staff. So if banks

aren't lending much then the prospects for economic growth are limited. Hence to stimulate the flow of more

credit, the ECB has slashed its key rate in the hope that borrowing costs will fall for firms.

But the ECB hasn't just cut its benchmark rate. It has also cut its deposit rate to a negative figure – minus

0.1%.

The ECB has a "deposit facility", which means banks can hold some of their excess cash at the central bank,

also ECB pays interest on those deposits.

Now that the deposit rate is negative, banks have to pay central bank for availing this facility of parking their

funds with it. This is to encourage banks to lend their cash out rather than hold it with the ECB.

It also slashed its marginal lending facility – where it offers cheap overnight credit to banks in need to some

quick funds – to 0.4% from its previous 0.75%.

Global GDP Trend

United States of America Euro Zone (28 Members)

China India

United States of America

•Abnormally cold weather curtailed investment and exports.

•Firms had to cut back on inventories in Q1 2014. Despite the weakness more than half a million jobs were added in Q1.

•Consumer lending is also growing at the same pace as in pre-crisis years.

•Rising household incomes coupled with reduced fiscal drag is boosting demand, business productivity, investment and hiring, hence is expected to lead to stronger growth.

•Surveys indicate a strong pick up in the second half of the year in business investment, which has so far lagged the recovery.

Euro Zone

•In the euro area, growth has turned positive.

•In Germany, supportive monetary conditions, robust labor market conditions, and improving confidence have underpinned a pickup in domestic demand, reflected mainly in higher consumption and a tentative revival in investment.

China

•The slowdown in GDP growth in China has been milder and largely policy engineered, and inflation has declined since mid-2011. It is therefore less clear whether the observed slowdown reflects lower potential growth.

•A recent study points out that China’s growth has slowed despite high levels of investment and credit growth. This would imply diminishing returns to investment, a misallocation of resources, and a limit to how far an economy can grow by reallocating labor from the country side into factories.

•Growth in China is expected to ease to 7.6 percent in 2014 and further to 7.5 percent in 2015 and 7.4 percent in 2016, reflecting the ongoing rebalancing of the economy.

India

•In the last two years, economic activity has expanded at its slowest pace in the last two decades. India has witnessed a steady decline in GDP growth rate from Q1 2011 with one or two spikes till date.

•This decline is being attributed to a host of reasons ranging from the low demand, lack of policy actions/reforms, drop in investments, infrastructural deficiencies, delay in project completion on account of procedural delays/bottlenecks, high inflation, high interest rates to general global economic weakness.

•The agricultural sector performed remarkably well during FY14 on the back of good monsoons. As per the advanced estimates, the agricultural sector recorded a growth of 4.6% in FY14 as against the growth of 1.4% in FY13.

•Advanced estimates for FY14 show that the manufacturing sector’s growth has dropped to 0.65% from 0.96% in FY13. The poor performance of the sector is mainly on account of the negative growth registered in the mining and manufacturing sub-sectors. Overall, depressed investments and a slump in consumer demand have resulted in the low growth in industry. High inflation had negatively impacted consumption demand and investments have declined on account of high interest rates and prevalence of spare capacity.

•The growth in the services sector has been subdued since the last few years – it declined from an average growth rate of 9.7% during FY05-FY12 to 6.2% in FY13 and FY14. The deceleration in the sector’s growth can be largely attributed to the slowdown in its 2 subsectors – (1) trade, hotel, transport & communications and (2) construction. The decline in these segments reflects slowdown in the economy. Low industrial growth has impacted the transport sector and less activity in the infra space has affected construction.

Global Inflationary Trend

United States of America Euro Zone (28 Members)

China India

United States of America

•The whole sub prime crisis is the reason behind the high deflation that existed in the economy and also the fall in the stock market that happened from 2007 to 2009.

•From Feb’2014 US has seen increase in inflation from 1.1% to 2.0% in April. Higher inflation is a sign of higher demand.

Euro Zone

•Since November’2011, according to Eurostat’s flash estimate, overall HICP inflation stood at 0.5% in May 2014.

•The subdued current rate of inflation reflects a stagnation of energy prices, food prices and non-energy industrial goods prices, as well as a subdued trend in services prices.

• Headline HICP inflation is expected to remain at low levels until the third quarter of 2014.

•Deflationary fears are gripping the Eurozone economy. If deflation were to occur, it would spark something called a "liquidity trap". This is where banks, businesses and individuals hold onto money because it will naturally increase in value as prices deflate. By holding onto cash it is not spent or invested – harming economic growth.

China

•CHINA'S consumer price index (CPI) increased 2.5 percent year on year in May, up from 1.8 percent in the previous month.

•CPI inflation declined to 2.3 percent (year on year) in the first quarter of 2014 due to a moderation of food prices. In April CPI inflation decelerated further to 1.8 percent, in part due to seasonality.

•In 2014, Inflation will stay contained. It is expected to be 3.0 percent, slightly higher than in 2013 but below the government’s target of 3.5 percent.

•There is a risk that food prices might increase more than expected due to the tensions in Ukraine, which appears increasingly likely this year and could cause considerable damage on crop yields.

India

•The upward trend witnessed from March 2009 to Jan 2010 was largely due to the QE effect. India has been the significant beneficiary of Global Monetary Easing program. This increase in global liquidity lead to the increase in commodity prices. Increased inflation reduced domestic saving and moderated profit margin.

•CPI for the month of May’14 saw a marginal decline (8.3%) following two successive months of increase. After rising to 9.7% in April’14 (y-o-y), the food, beverages and tobacco segment recorded a moderation in their price levels with inflation for May’14 being recorded at 9.4%. Moderation of inflation was mainly on account moderation in food articles and vegetable indices.

•Fuel and light inflation declined from 6% in April ’14 to 5.1% in May ’14.

•While CPI inflation has eased but its future path will stay contingent on monsoon, turmoil in Iraq, hike in rail freight. However the hike in rail freight (6.5%) would only put pressure on prices in near term. In long run, this step will help reduce the fiscal deficit.

Global Markets - Quarterly Performance

Global Markets Asian Markets

Economy Overview – India

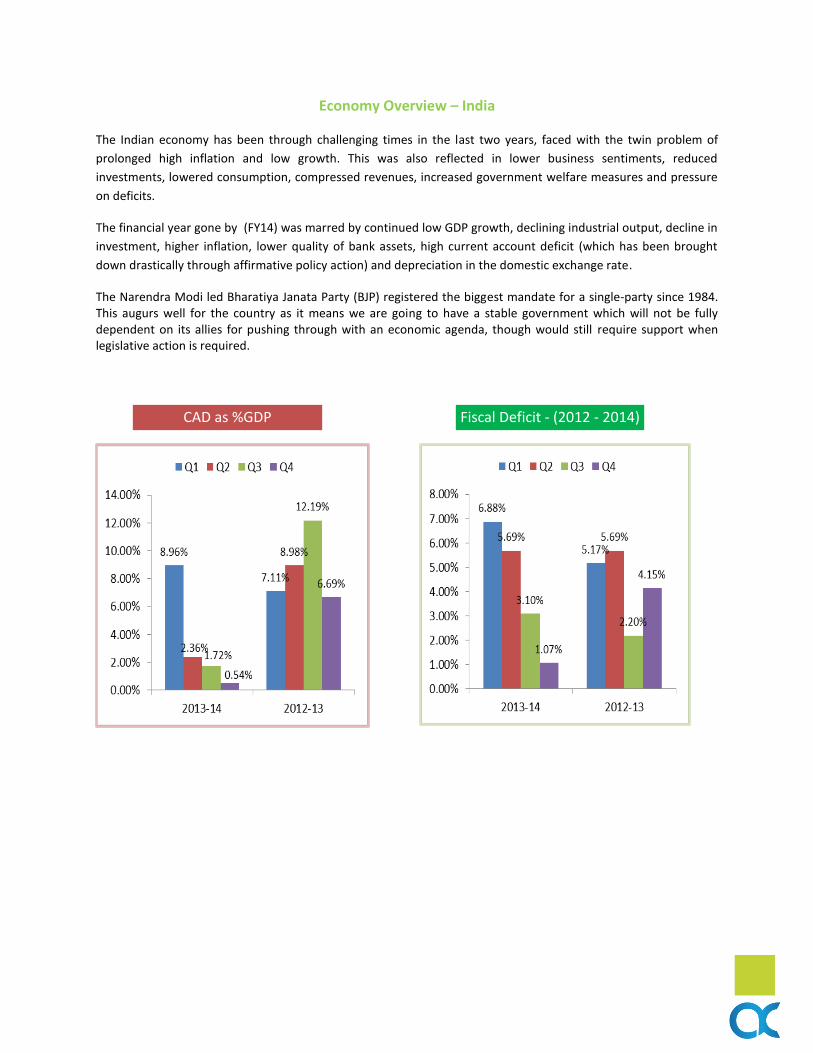

The Indian economy has been through challenging times in the last two years, faced with the twin problem of

prolonged high inflation and low growth. This was also reflected in lower business sentiments, reduced

investments, lowered consumption, compressed revenues, increased government welfare measures and pressure

on deficits.

The financial year gone by (FY14) was marred by continued low GDP growth, declining industrial output, decline in

investment, higher inflation, lower quality of bank assets, high current account deficit (which has been brought

down drastically through affirmative policy action) and depreciation in the domestic exchange rate.

The Narendra Modi led Bharatiya Janata Party (BJP) registered the biggest mandate for a single-party since 1984. This augurs well for the country as it means we are going to have a stable government which will not be fully dependent on its allies for pushing through with an economic agenda, though would still require support when legislative action is required.

CAD as %GDP Fiscal Deficit - (2012 - 2014)

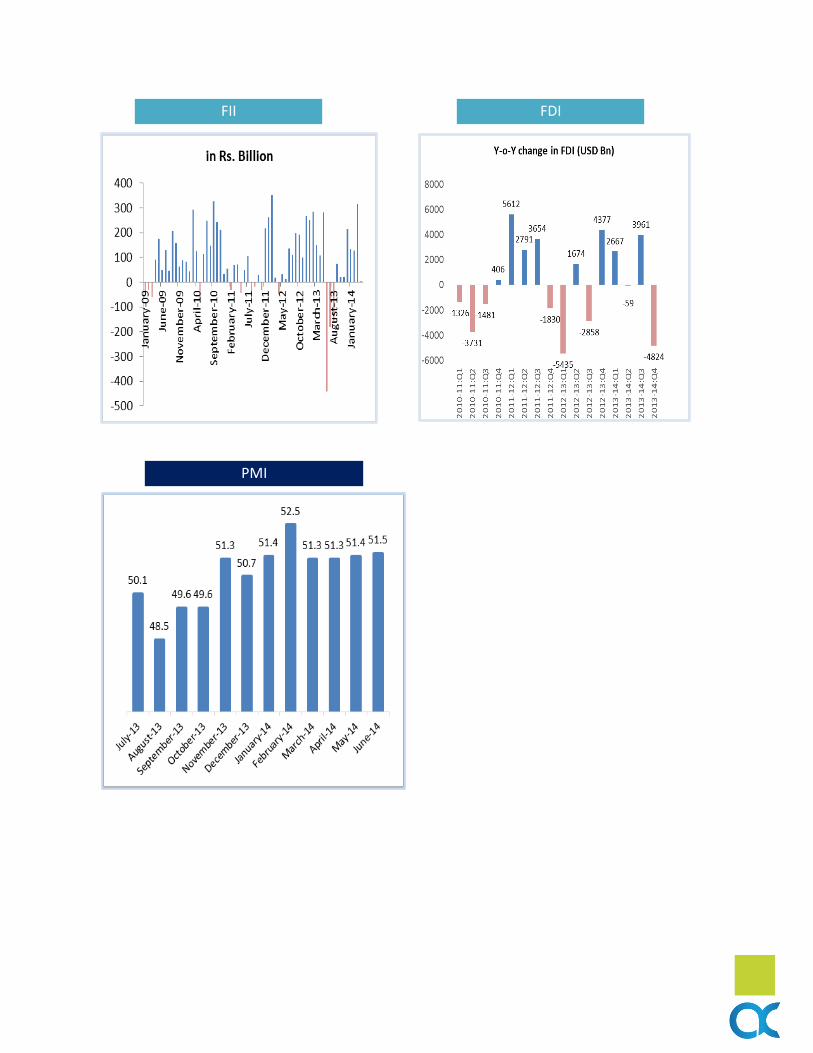

FII FDI

PMI

Current Account Deficit

•High inflation drove real deposit rate into negative territory, which led to decline in financial savings and increased saving in form of gold, leading to higher imports of gold. This further widened CAD.

•Curb on gold imports and weaker domestic economy led to sharp decline in overall imports.

•On the contrary, exports got a boost from recovery in the US and Euro. As a result CAD fell to 0.2% of GDP during the final quarter of FY2013-14.

•In FY15, CRISIL expects CAD to widen to 2.2% of GDP as steps towards removal of restrictions on gold imports have already begun. Since growth is expected to pick up, hence imports of capital and consumption are also expected to rise.

•Financing CAD might pose a challenge in FY15 as global liquidity declines with continued tapering of US Fed’s bond purchase program.

Fiscal Deficit

•Large increase in MSP for various crops, MNREGA Scheme, incomplete and delayed pass through of higher international oil prices to domestic prices added to the fiscal pressure.

FII

•In FY14, country witnessed a sudden and significant outflows of funds, which led to sharp drop in FII inflows and consequently for the year country saw a 66% decline in net inflows from previous year.

•Such a phenomenon was observed on news of US winding down its monetary stimulus program and stronger than expected growth in the US economy which prompted investors to shift their asset holding from emerging economies to the US market.

•Since Jan 2014, India has been the most favored nation for FII inflows.

Exchange Rate

•The steep decline in the Indian rupee was the matter of grave concern for a large part of FY14.

•Following a series of policy measures by the RBI and the government, the Rupee strengthened from its record lows (Rs.68/$) and has been fairly stable in recent months at Rs.60-61/$.

•The stability in the domestic currency is being aided by the improvements in the country’s economic fundamentals i.e. narrowing of CAD and the increase of foreign inflows into the country.

PMI

• The HSBC India Manufacturing Purchasing Managers' Index (PMI), a measure of factory production, rose marginally from 51.4 in May to 51.5 in June.

•Output picked up in June, supported by growing order flows, especially from overseas.

•Greater domestic & foreign demand led companies to increase production levels further.

•June data highlighted a marked and accelerated expansion of new export orders.

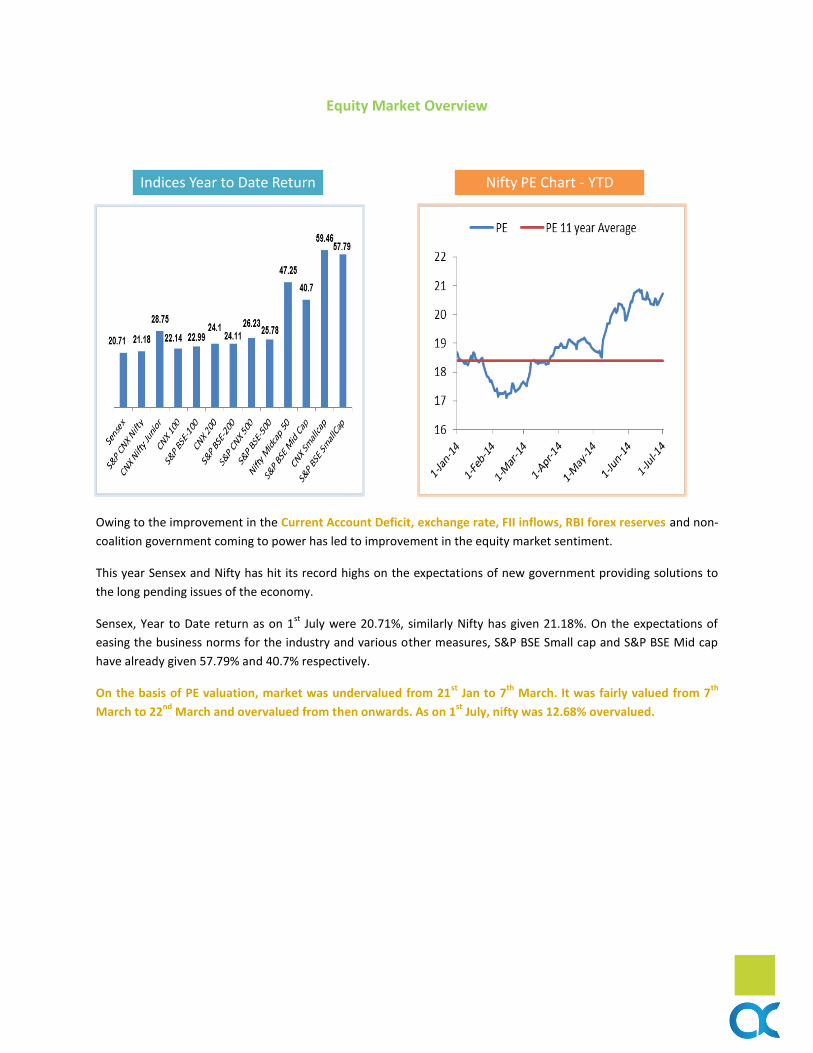

Equity Market Overview

Owing to the improvement in the Current Account Deficit, exchange rate, FII inflows, RBI forex reserves and non-

coalition government coming to power has led to improvement in the equity market sentiment.

This year Sensex and Nifty has hit its record highs on the expectations of new government providing solutions to

the long pending issues of the economy.

Sensex, Year to Date return as on 1st

July were 20.71%, similarly Nifty has given 21.18%. On the expectations of

easing the business norms for the industry and various other measures, S&P BSE Small cap and S&P BSE Mid cap

have already given 57.79% and 40.7% respectively.

On the basis of PE valuation, market was undervalued from 21st

Jan to 7th

March. It was fairly valued from 7th

March to 22nd

March and overvalued from then onwards. As on 1st

July, nifty was 12.68% overvalued.

Indices Year to Date Return Nifty PE Chart - YTD

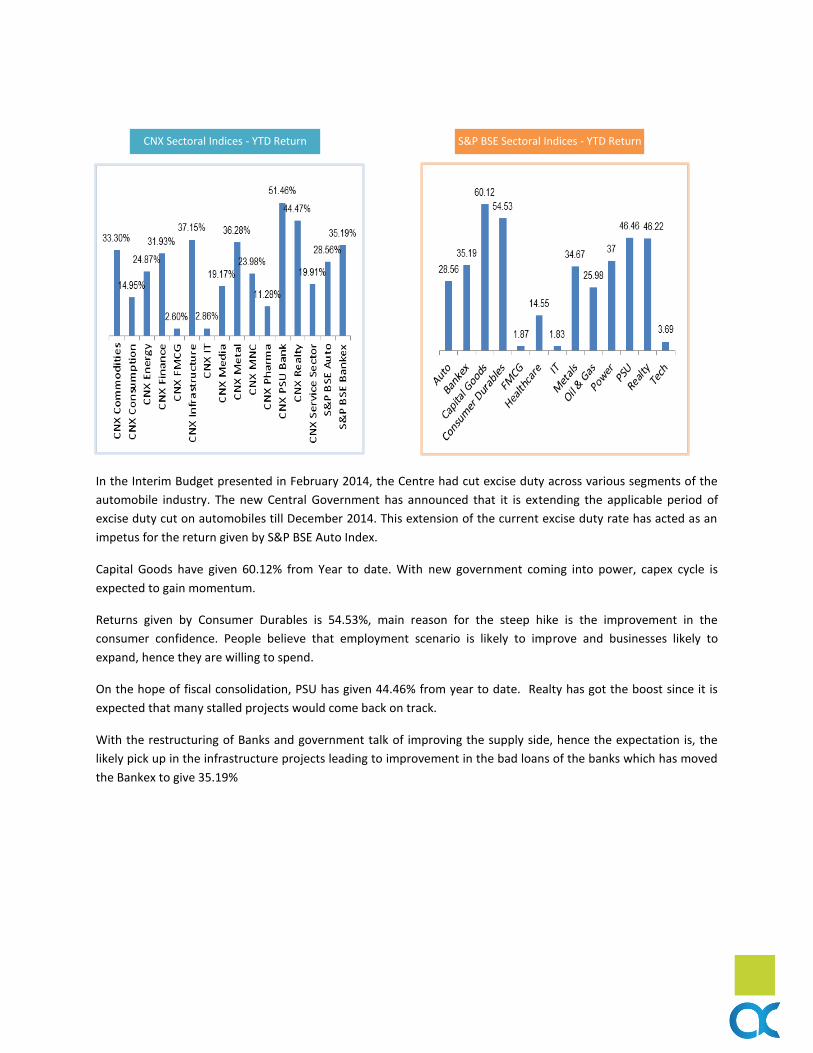

In the Interim Budget presented in February 2014, the Centre had cut excise duty across various segments of the

automobile industry. The new Central Government has announced that it is extending the applicable period of

excise duty cut on automobiles till December 2014. This extension of the current excise duty rate has acted as an

impetus for the return given by S&P BSE Auto Index.

Capital Goods have given 60.12% from Year to date. With new government coming into power, capex cycle is

expected to gain momentum.

Returns given by Consumer Durables is 54.53%, main reason for the steep hike is the improvement in the

consumer confidence. People believe that employment scenario is likely to improve and businesses likely to

expand, hence they are willing to spend.

On the hope of fiscal consolidation, PSU has given 44.46% from year to date. Realty has got the boost since it is

expected that many stalled projects would come back on track.

With the restructuring of Banks and government talk of improving the supply side, hence the expectation is, the

likely pick up in the infrastructure projects leading to improvement in the bad loans of the banks which has moved

the Bankex to give 35.19%

CNX Sectoral Indices - YTD Return S&P BSE Sectoral Indices - YTD Return

Debt Market Overview

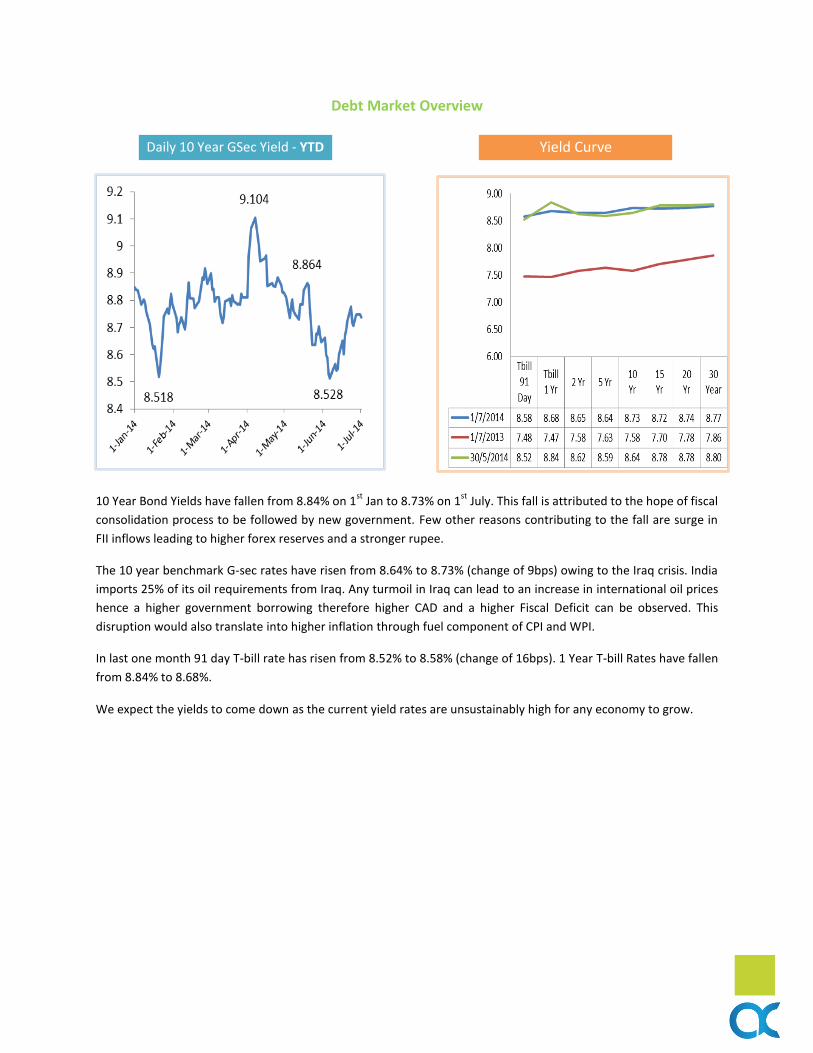

10 Year Bond Yields have fallen from 8.84% on 1st

Jan to 8.73% on 1st

July. This fall is attributed to the hope of fiscal

consolidation process to be followed by new government. Few other reasons contributing to the fall are surge in

FII inflows leading to higher forex reserves and a stronger rupee.

The 10 year benchmark G-sec rates have risen from 8.64% to 8.73% (change of 9bps) owing to the Iraq crisis. India

imports 25% of its oil requirements from Iraq. Any turmoil in Iraq can lead to an increase in international oil prices

hence a higher government borrowing therefore higher CAD and a higher Fiscal Deficit can be observed. This

disruption would also translate into higher inflation through fuel component of CPI and WPI.

In last one month 91 day T-bill rate has risen from 8.52% to 8.58% (change of 16bps). 1 Year T-bill Rates have fallen

from 8.84% to 8.68%.

We expect the yields to come down as the current yield rates are unsustainably high for any economy to grow.

Daily 10 Year GSec Yield - YTD Yield Curve

Commodities: Gold

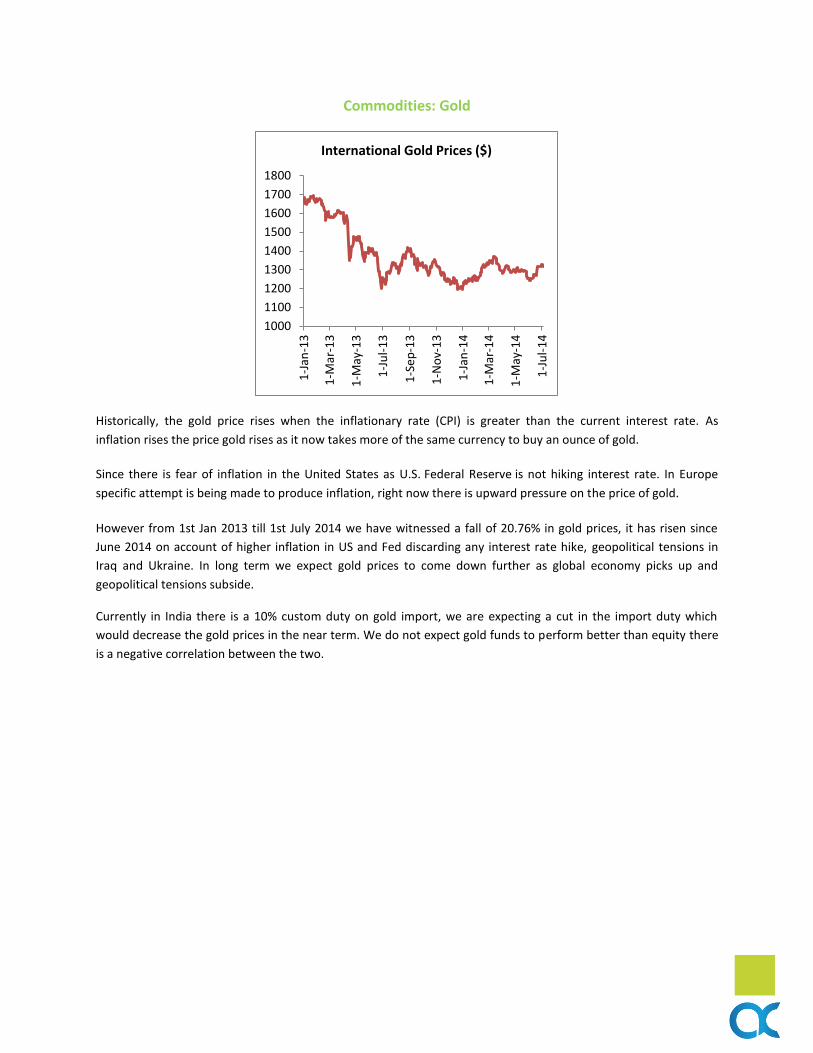

Historically, the gold price rises when the inflationary rate (CPI) is greater than the current interest rate. As

inflation rises the price gold rises as it now takes more of the same currency to buy an ounce of gold.

Since there is fear of inflation in the United States as U.S. Federal Reserve is not hiking interest rate. In Europe

specific attempt is being made to produce inflation, right now there is upward pressure on the price of gold.

However from 1st Jan 2013 till 1st July 2014 we have witnessed a fall of 20.76% in gold prices, it has risen since

June 2014 on account of higher inflation in US and Fed discarding any interest rate hike, geopolitical tensions in

Iraq and Ukraine. In long term we expect gold prices to come down further as global economy picks up and

geopolitical tensions subside.

Currently in India there is a 10% custom duty on gold import, we are expecting a cut in the import duty which

would decrease the gold prices in the near term. We do not expect gold funds to perform better than equity there

is a negative correlation between the two.

1000

1100

1200

1300

1400

1500

1600

1700

1800

1-J

an-1

3

1-M

ar-1

3

1-M

ay-1

3

1-J

ul-

13

1-S

ep

-13

1-N

ov-

13

1-J

an-1

4

1-M

ar-1

4

1-M

ay-1

4

1-J

ul-

14

International Gold Prices ($)

Snapshot of funds recommended by Alpha Cap

Equity – Large, Large & Mid Cap

ICICI Prudential Focused Bluechip Equity Regular

Birla Sun Life Frontline Equity

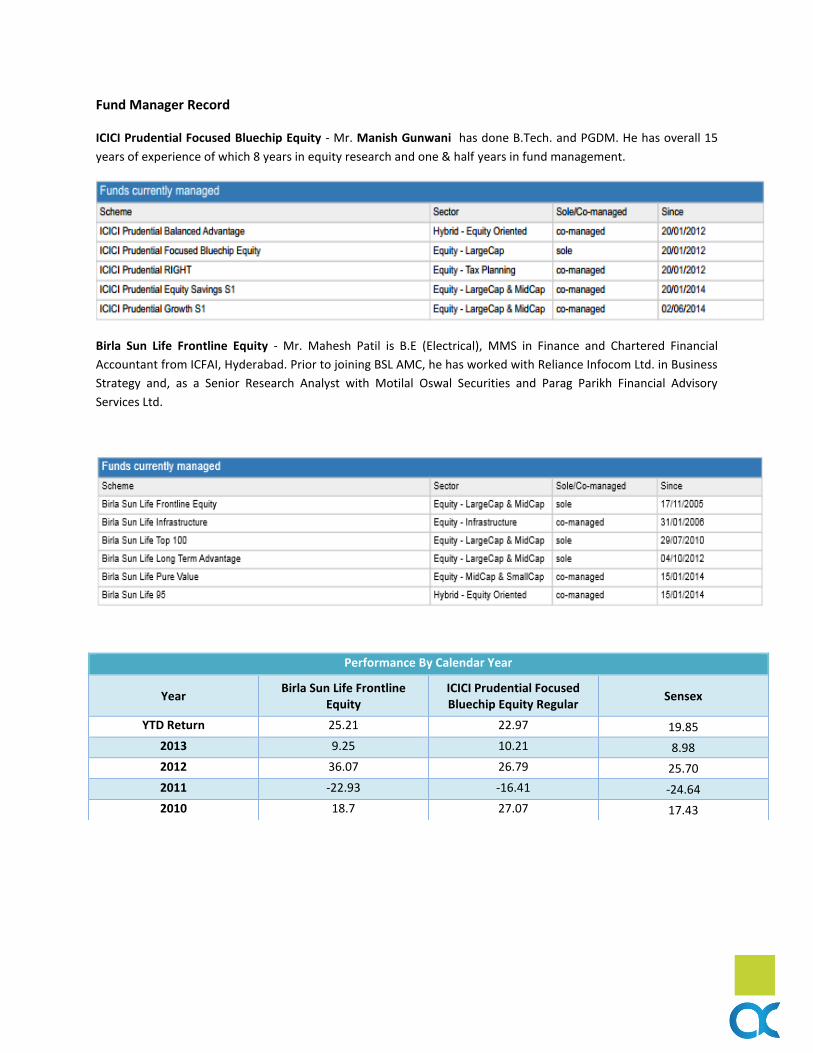

Fund Manager Record

ICICI Prudential Focused Bluechip Equity - Mr. Manish Gunwani has done B.Tech. and PGDM. He has overall 15

years of experience of which 8 years in equity research and one & half years in fund management.

Birla Sun Life Frontline Equity - Mr. Mahesh Patil is B.E (Electrical), MMS in Finance and Chartered Financial

Accountant from ICFAI, Hyderabad. Prior to joining BSL AMC, he has worked with Reliance Infocom Ltd. in Business

Strategy and, as a Senior Research Analyst with Motilal Oswal Securities and Parag Parikh Financial Advisory

Services Ltd.

Performance By Calendar Year

Year Birla Sun Life Frontline

Equity ICICI Prudential Focused Bluechip Equity Regular

Sensex

YTD Return 25.21 22.97 19.85

2013 9.25 10.21 8.98

2012 36.07 26.79 25.70

2011 -22.93 -16.41 -24.64

2010 18.7 27.07 17.43

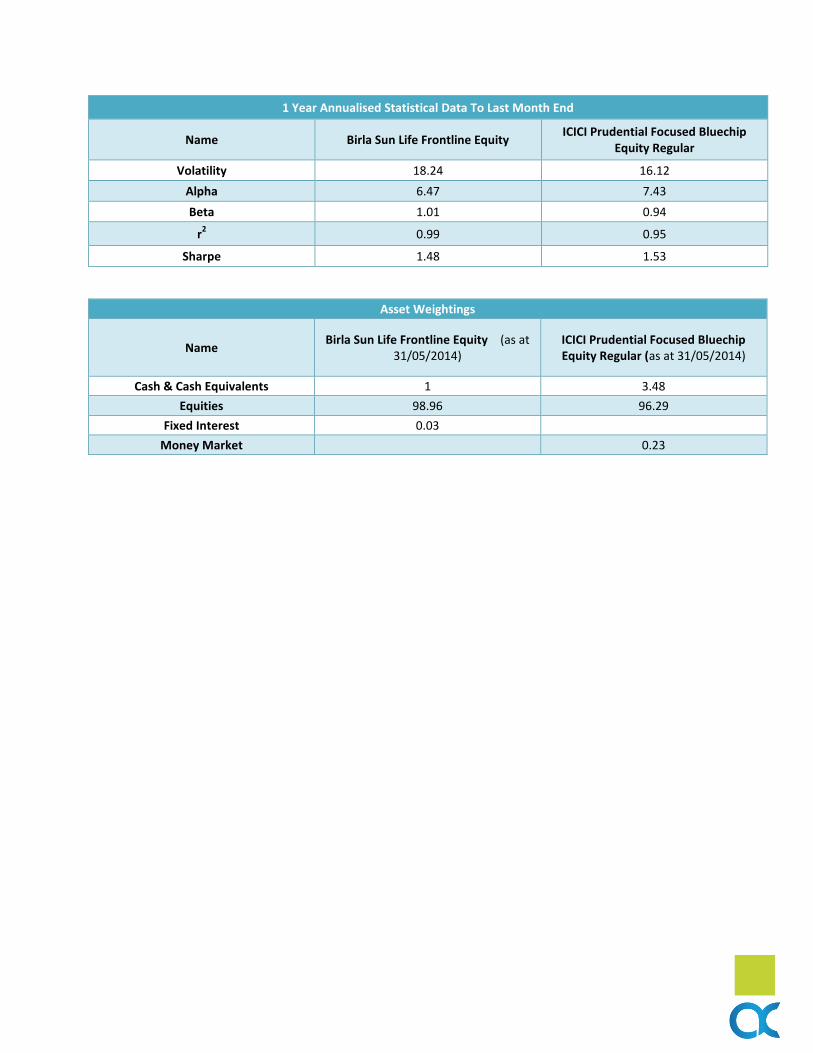

1 Year Annualised Statistical Data To Last Month End

Name Birla Sun Life Frontline Equity ICICI Prudential Focused Bluechip

Equity Regular

Volatility 18.24 16.12

Alpha 6.47 7.43

Beta 1.01 0.94

r2 0.99 0.95

Sharpe 1.48 1.53

Asset Weightings

Name Birla Sun Life Frontline Equity (as at

31/05/2014) ICICI Prudential Focused Bluechip Equity Regular (as at 31/05/2014)

Cash & Cash Equivalents 1 3.48

Equities 98.96 96.29

Fixed Interest 0.03

Money Market

0.23

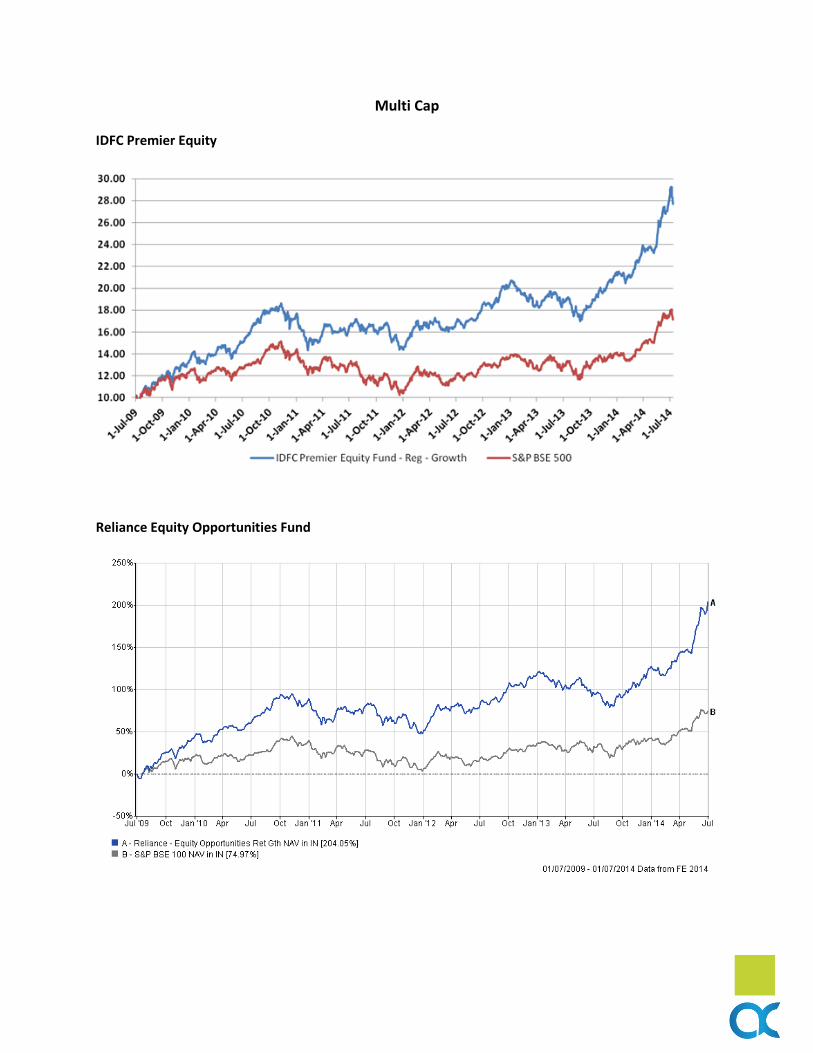

Multi Cap

IDFC Premier Equity

Reliance Equity Opportunities Fund

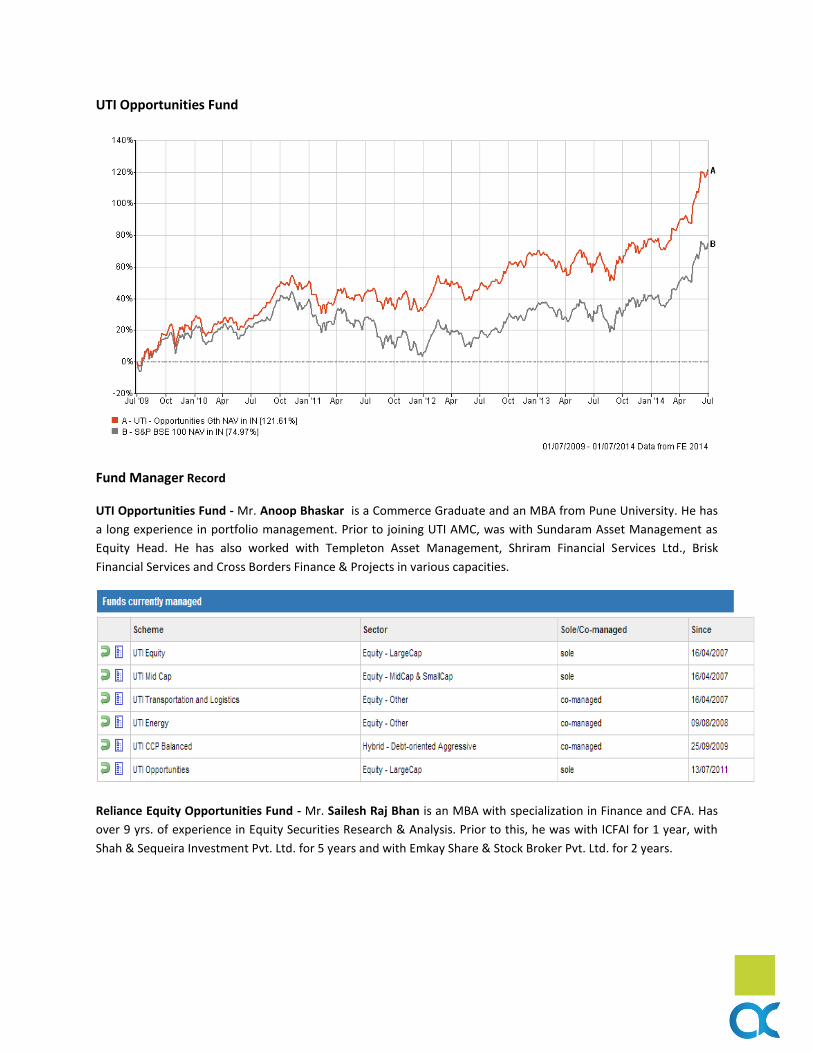

UTI Opportunities Fund

Fund Manager Record

UTI Opportunities Fund - Mr. Anoop Bhaskar is a Commerce Graduate and an MBA from Pune University. He has

a long experience in portfolio management. Prior to joining UTI AMC, was with Sundaram Asset Management as

Equity Head. He has also worked with Templeton Asset Management, Shriram Financial Services Ltd., Brisk

Financial Services and Cross Borders Finance & Projects in various capacities.

Reliance Equity Opportunities Fund - Mr. Sailesh Raj Bhan is an MBA with specialization in Finance and CFA. Has

over 9 yrs. of experience in Equity Securities Research & Analysis. Prior to this, he was with ICFAI for 1 year, with

Shah & Sequeira Investment Pvt. Ltd. for 5 years and with Emkay Share & Stock Broker Pvt. Ltd. for 2 years.

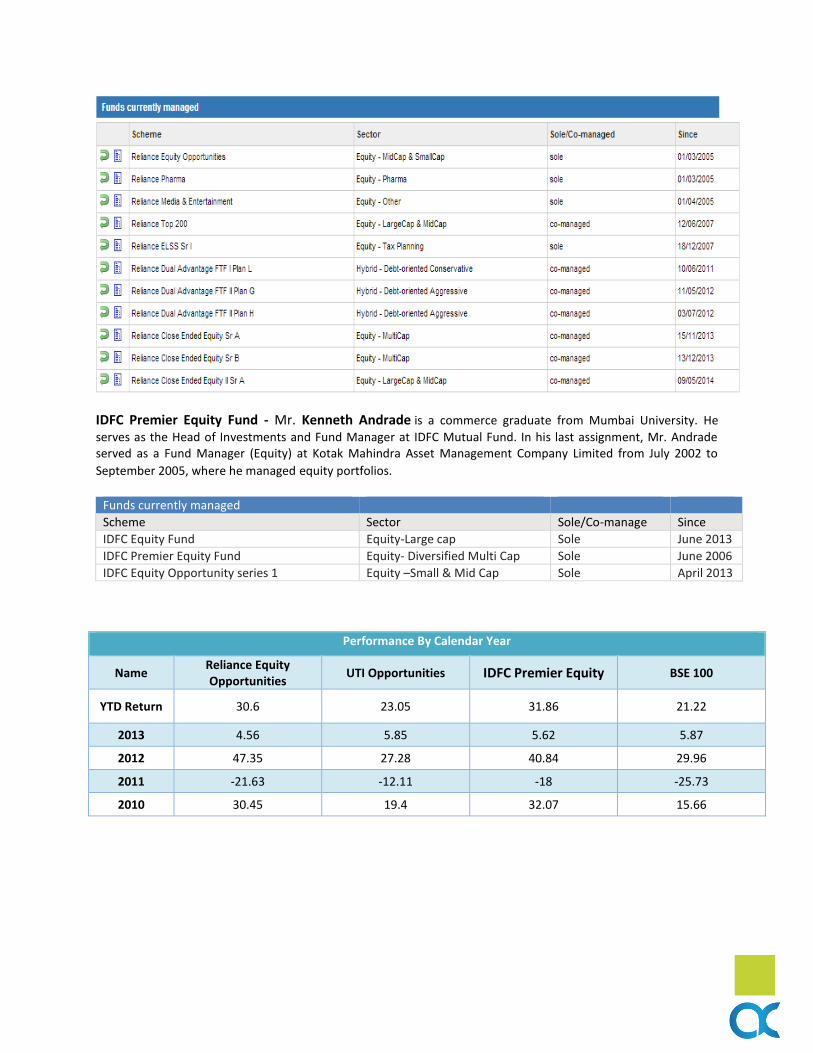

IDFC Premier Equity Fund - Mr. Kenneth Andrade is a commerce graduate from Mumbai University. He

serves as the Head of Investments and Fund Manager at IDFC Mutual Fund. In his last assignment, Mr. Andrade served as a Fund Manager (Equity) at Kotak Mahindra Asset Management Company Limited from July 2002 to

September 2005, where he managed equity portfolios.

Funds currently managed

Scheme Sector Sole/Co-manage Since

IDFC Equity Fund Equity-Large cap Sole June 2013

IDFC Premier Equity Fund Equity- Diversified Multi Cap Sole June 2006

IDFC Equity Opportunity series 1 Equity –Small & Mid Cap Sole April 2013

Performance By Calendar Year

Name Reliance Equity Opportunities

UTI Opportunities IDFC Premier Equity BSE 100

YTD Return 30.6 23.05 31.86 21.22

2013 4.56 5.85 5.62 5.87

2012 47.35 27.28 40.84 29.96

2011 -21.63 -12.11 -18 -25.73

2010 30.45 19.4 32.07 15.66

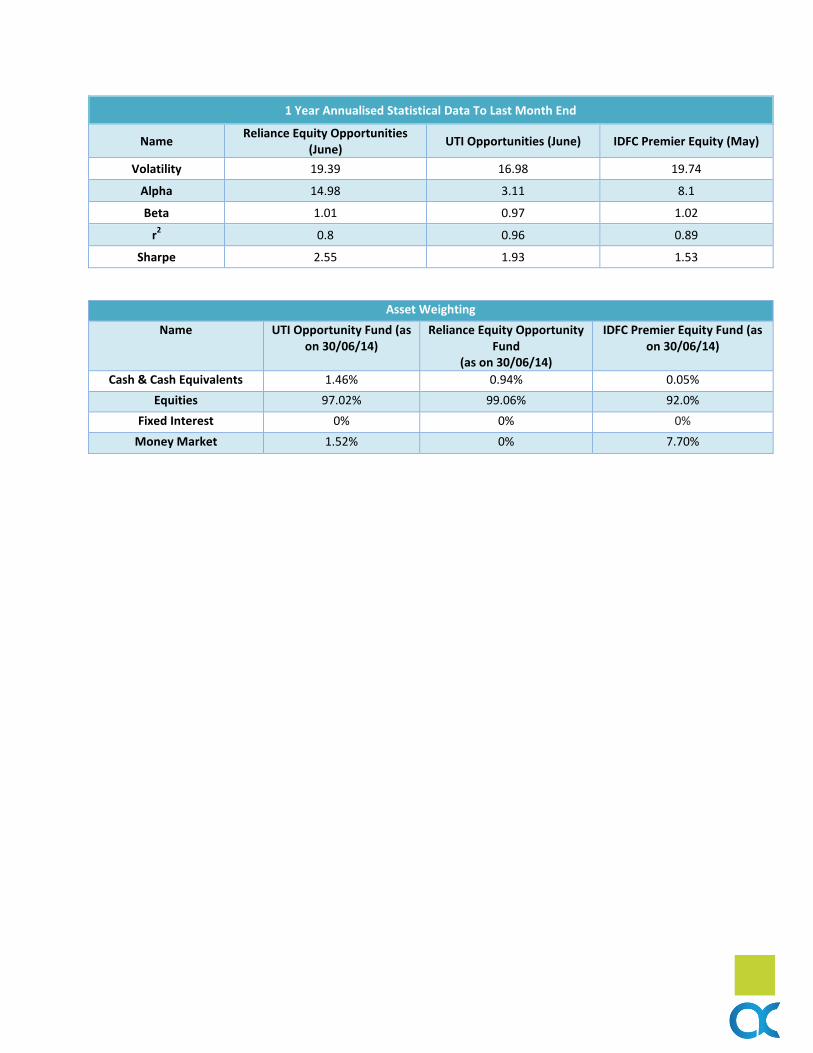

1 Year Annualised Statistical Data To Last Month End

Name Reliance Equity Opportunities

(June) UTI Opportunities (June) IDFC Premier Equity (May)

Volatility 19.39 16.98 19.74

Alpha 14.98 3.11 8.1

Beta 1.01 0.97 1.02

r2 0.8 0.96 0.89

Sharpe 2.55 1.93 1.53

Asset Weighting

Name UTI Opportunity Fund (as on 30/06/14)

Reliance Equity Opportunity Fund

(as on 30/06/14)

IDFC Premier Equity Fund (as on 30/06/14)

Cash & Cash Equivalents 1.46% 0.94% 0.05%

Equities 97.02% 99.06% 92.0%

Fixed Interest 0% 0% 0%

Money Market 1.52% 0% 7.70%

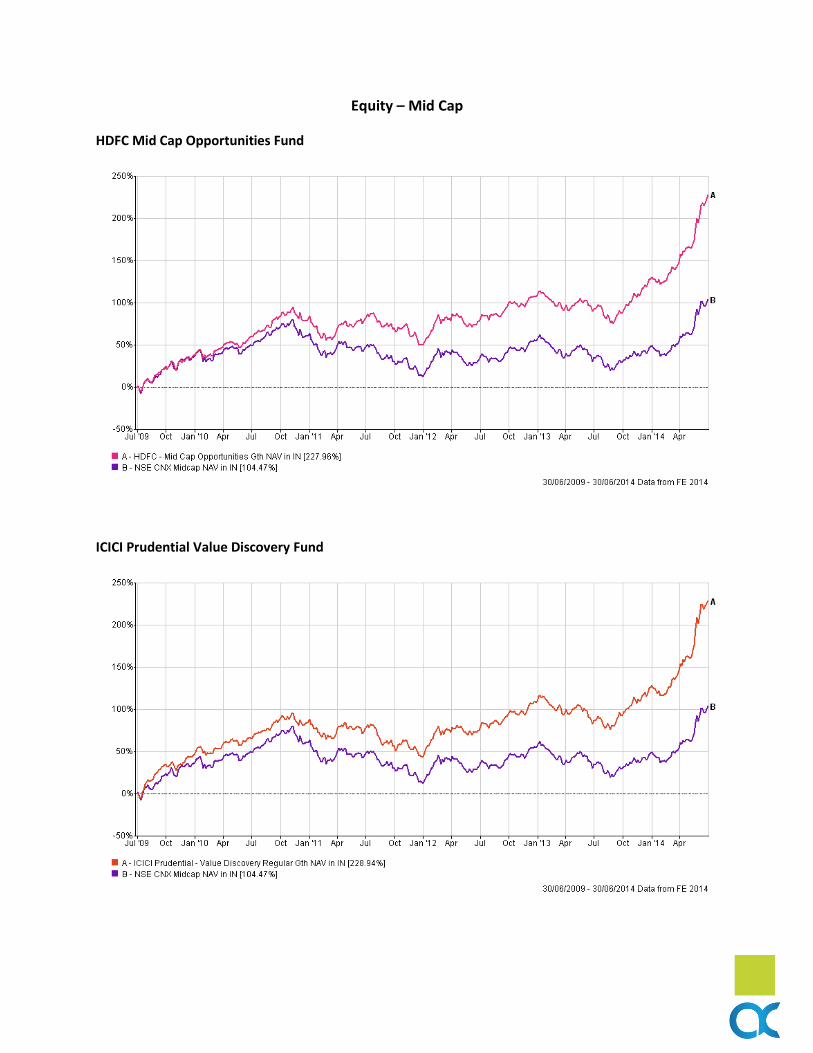

Equity – Mid Cap

HDFC Mid Cap Opportunities Fund

ICICI Prudential Value Discovery Fund

Performance By Calendar Year

Name HDFC Mid Cap Opportunities ICICI Prudential Value

Discovery Regular NSE CNX MidCap

YTD Return 40.66 42.46 37.49

2013 9.64 8.31 -5.1

2012 39.62 46.01 39.16

2011 -18.31 -23.73 -31

2010 32.13 27.71 19.16

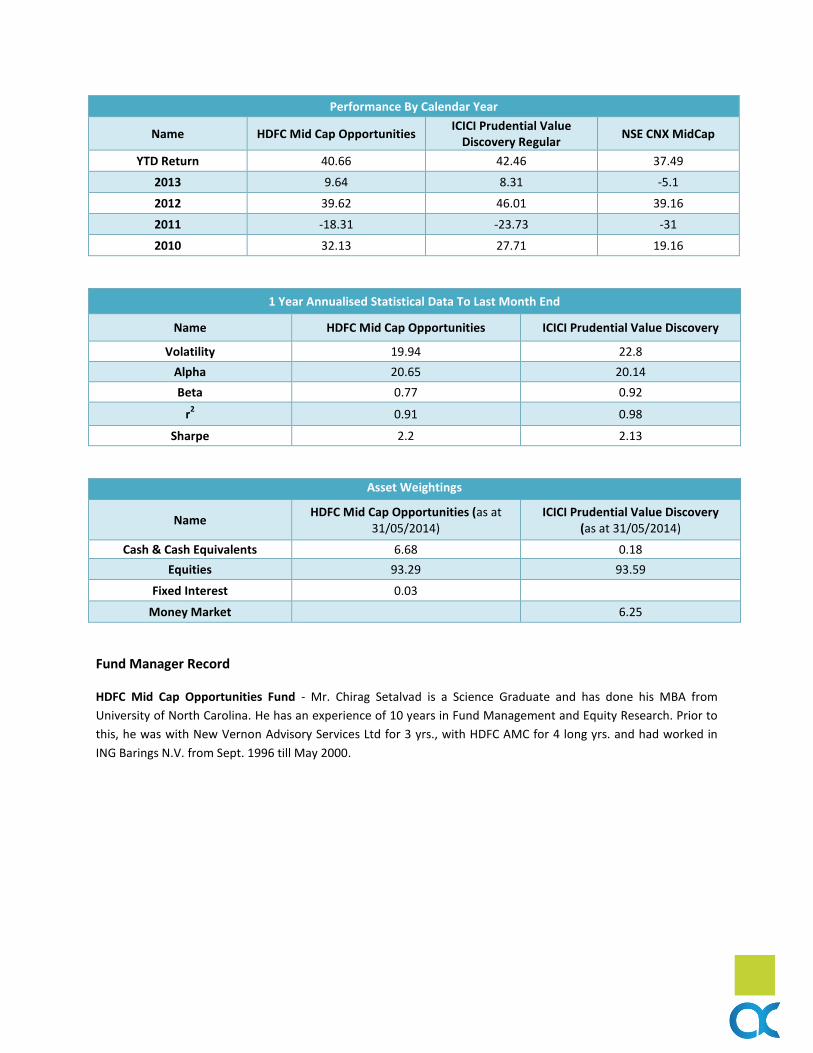

1 Year Annualised Statistical Data To Last Month End

Name HDFC Mid Cap Opportunities ICICI Prudential Value Discovery

Volatility 19.94 22.8

Alpha 20.65 20.14

Beta 0.77 0.92

r2 0.91 0.98

Sharpe 2.2 2.13

Asset Weightings

Name HDFC Mid Cap Opportunities (as at

31/05/2014) ICICI Prudential Value Discovery

(as at 31/05/2014)

Cash & Cash Equivalents 6.68 0.18

Equities 93.29 93.59

Fixed Interest 0.03

Money Market

6.25

Fund Manager Record

HDFC Mid Cap Opportunities Fund - Mr. Chirag Setalvad is a Science Graduate and has done his MBA from

University of North Carolina. He has an experience of 10 years in Fund Management and Equity Research. Prior to

this, he was with New Vernon Advisory Services Ltd for 3 yrs., with HDFC AMC for 4 long yrs. and had worked in

ING Barings N.V. from Sept. 1996 till May 2000.

ICICI Prudential Value Discovery Fund – Mr. Mittul Kalawadia has done B.Com. from Mithibai College, M.Com.

from University of Mumbai and CA. from ICAI. He has overall 5 years of experience of which 3 years as Equity

Analyst with ICICI Pru AMC only.

Mr. Sankaran Naren is a B.Tech from IIT, Chennai and holds a MBA in Finance from IIM Kolkata. Prior to joining

ICICI Prudential AMC, he has worked with various financial services companies like Refco Sify Securities India Pvt.

Ltd., HDFC Securities Ltd. and Yoha Securities in various positions.

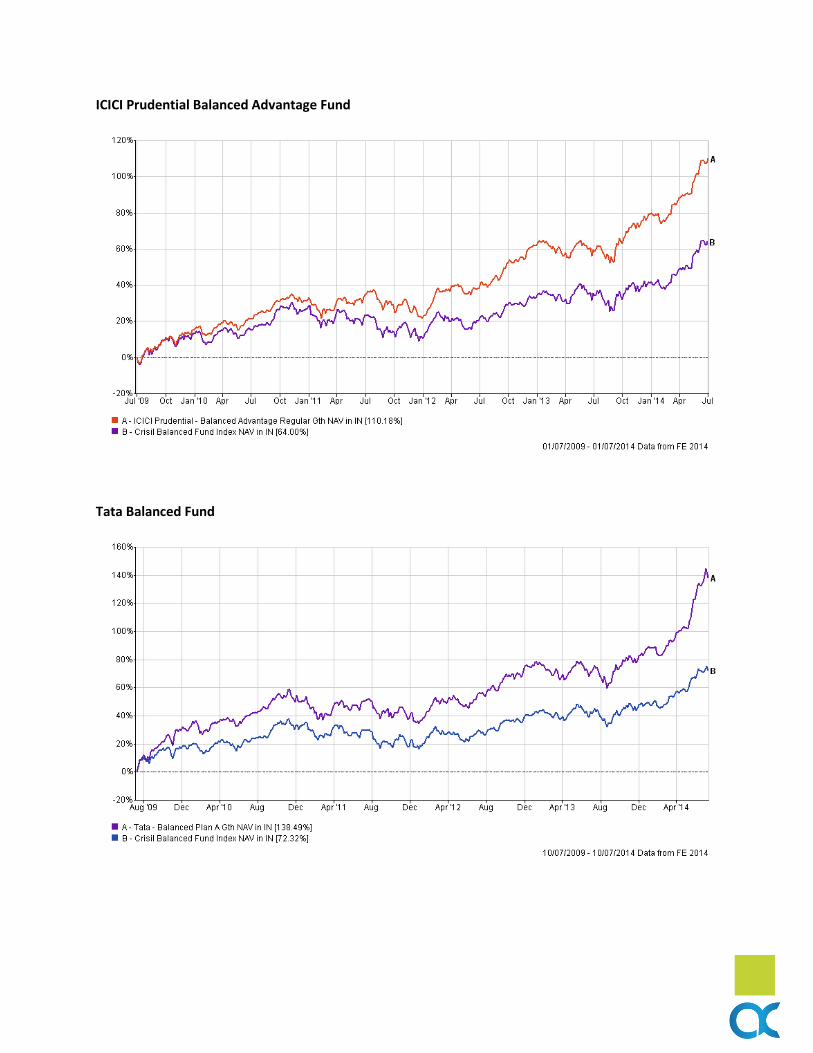

Hybrid Funds – Balanced Funds

HDFC Prudence

HDFC – Balanced Fund

ICICI Prudential Balanced Advantage Fund

Tata Balanced Fund

Fund Manager Record

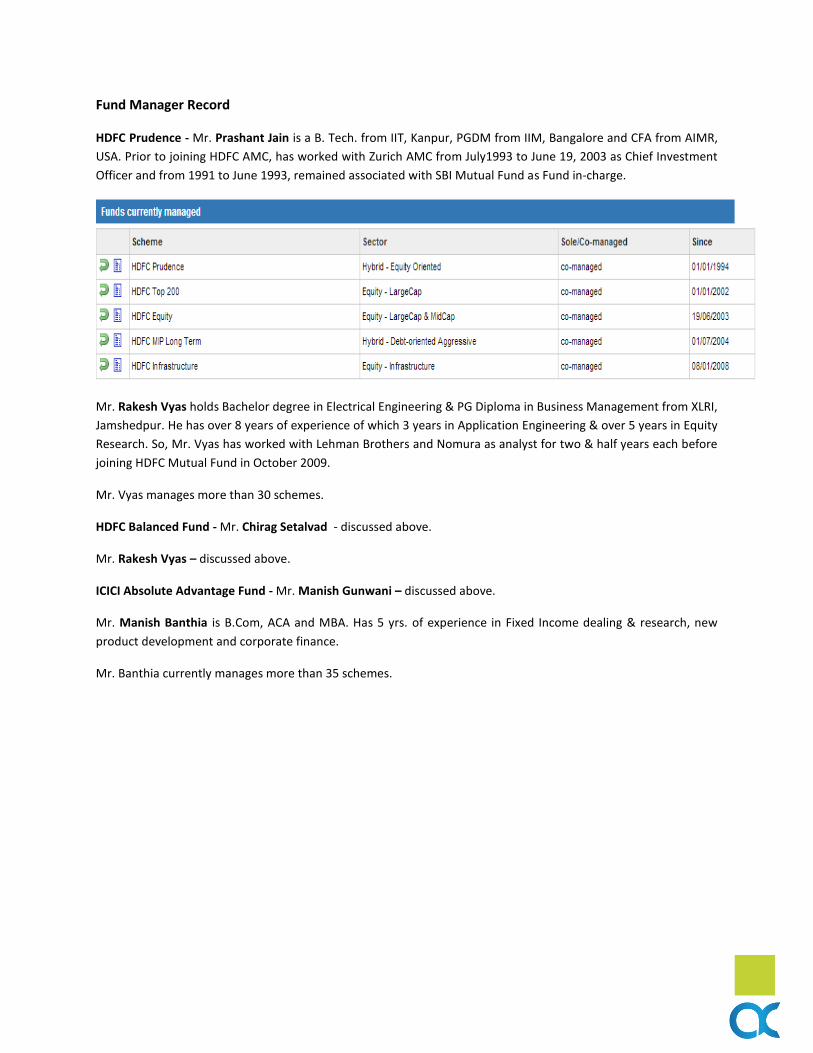

HDFC Prudence - Mr. Prashant Jain is a B. Tech. from IIT, Kanpur, PGDM from IIM, Bangalore and CFA from AIMR,

USA. Prior to joining HDFC AMC, has worked with Zurich AMC from July1993 to June 19, 2003 as Chief Investment

Officer and from 1991 to June 1993, remained associated with SBI Mutual Fund as Fund in-charge.

Mr. Rakesh Vyas holds Bachelor degree in Electrical Engineering & PG Diploma in Business Management from XLRI,

Jamshedpur. He has over 8 years of experience of which 3 years in Application Engineering & over 5 years in Equity

Research. So, Mr. Vyas has worked with Lehman Brothers and Nomura as analyst for two & half years each before

joining HDFC Mutual Fund in October 2009.

Mr. Vyas manages more than 30 schemes.

HDFC Balanced Fund - Mr. Chirag Setalvad - discussed above.

Mr. Rakesh Vyas – discussed above.

ICICI Absolute Advantage Fund - Mr. Manish Gunwani – discussed above.

Mr. Manish Banthia is B.Com, ACA and MBA. Has 5 yrs. of experience in Fixed Income dealing & research, new

product development and corporate finance.

Mr. Banthia currently manages more than 35 schemes.

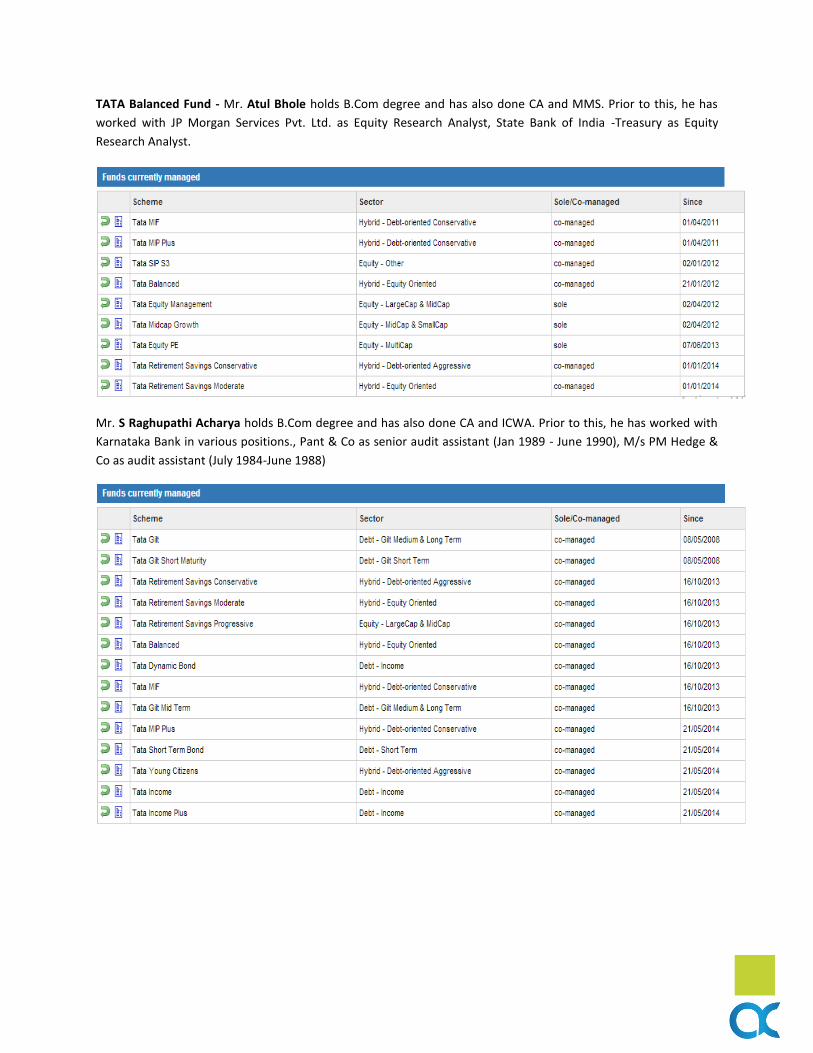

TATA Balanced Fund - Mr. Atul Bhole holds B.Com degree and has also done CA and MMS. Prior to this, he has

worked with JP Morgan Services Pvt. Ltd. as Equity Research Analyst, State Bank of India -Treasury as Equity

Research Analyst.

Mr. S Raghupathi Acharya holds B.Com degree and has also done CA and ICWA. Prior to this, he has worked with

Karnataka Bank in various positions., Pant & Co as senior audit assistant (Jan 1989 - June 1990), M/s PM Hedge &

Co as audit assistant (July 1984-June 1988)

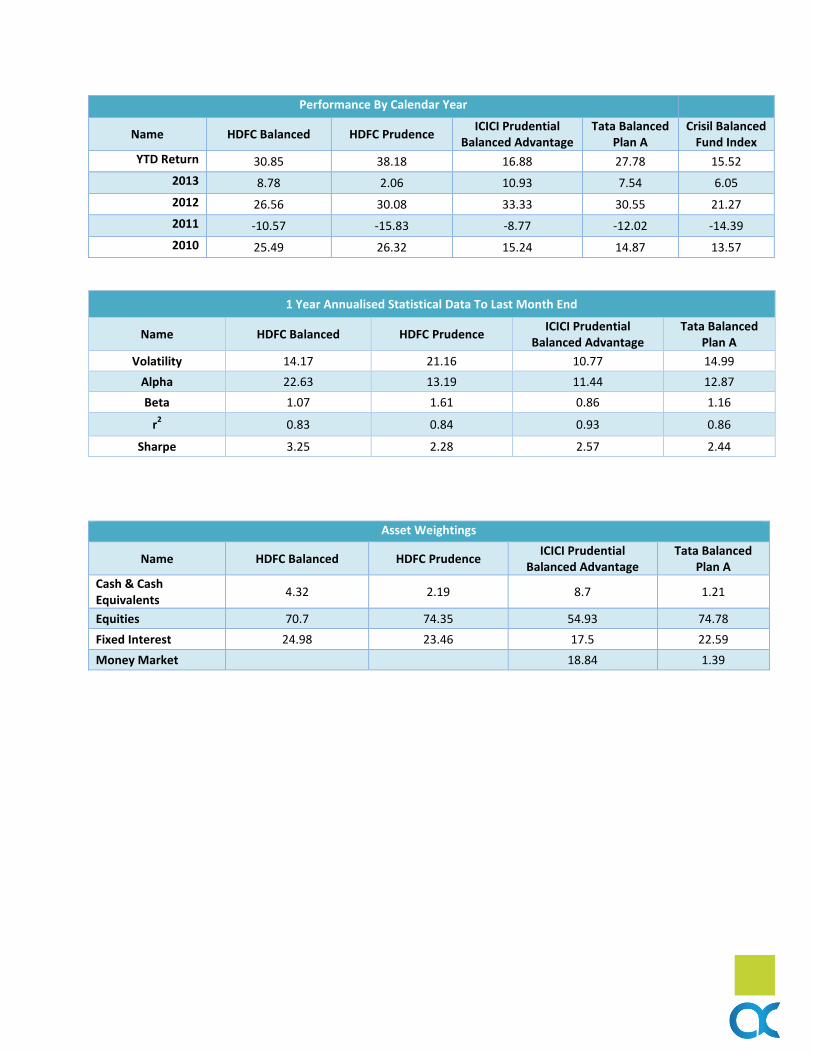

Performance By Calendar Year

Name HDFC Balanced HDFC Prudence ICICI Prudential

Balanced Advantage Tata Balanced

Plan A Crisil Balanced

Fund Index

YTD Return 30.85 38.18 16.88 27.78 15.52

2013 8.78 2.06 10.93 7.54 6.05

2012 26.56 30.08 33.33 30.55 21.27

2011 -10.57 -15.83 -8.77 -12.02 -14.39

2010 25.49 26.32 15.24 14.87 13.57

1 Year Annualised Statistical Data To Last Month End

Name HDFC Balanced HDFC Prudence ICICI Prudential

Balanced Advantage Tata Balanced

Plan A

Volatility 14.17 21.16 10.77 14.99

Alpha 22.63 13.19 11.44 12.87

Beta 1.07 1.61 0.86 1.16

r2 0.83 0.84 0.93 0.86

Sharpe 3.25 2.28 2.57 2.44

Asset Weightings

Name HDFC Balanced HDFC Prudence ICICI Prudential

Balanced Advantage Tata Balanced

Plan A

Cash & Cash Equivalents

4.32 2.19 8.7 1.21

Equities 70.7 74.35 54.93 74.78

Fixed Interest 24.98 23.46 17.5 22.59

Money Market

18.84 1.39

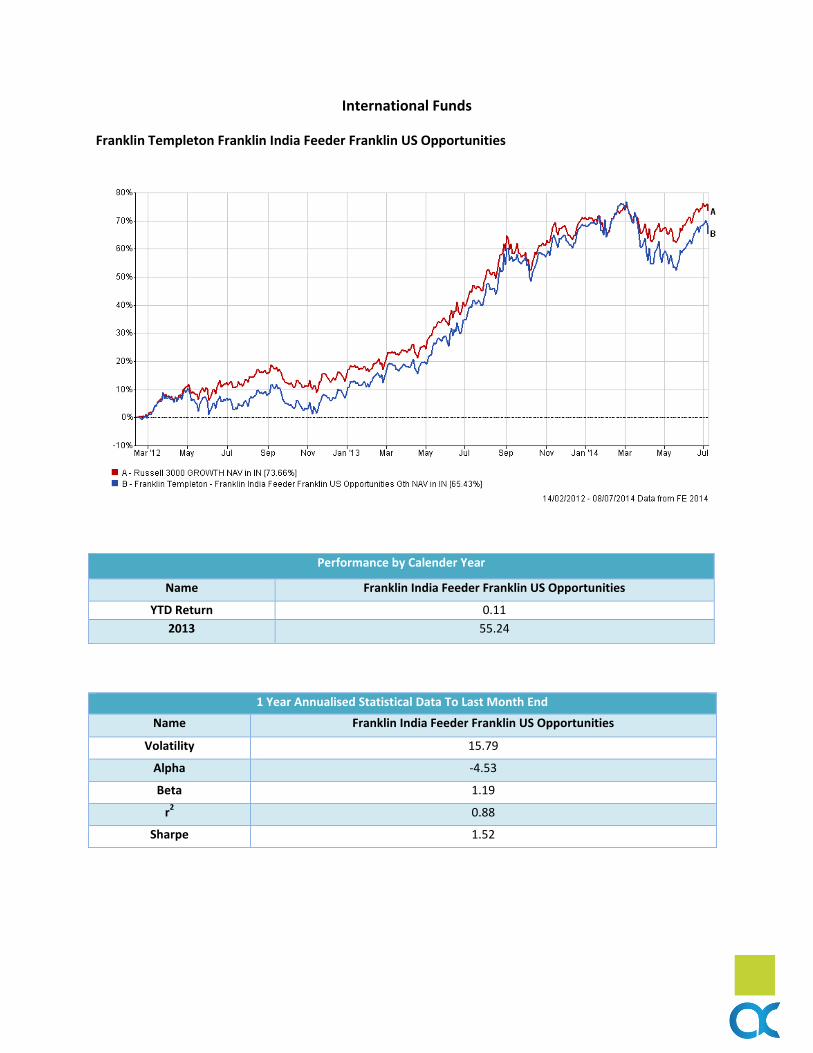

International Funds

Franklin Templeton Franklin India Feeder Franklin US Opportunities

Performance by Calender Year

Name Franklin India Feeder Franklin US Opportunities

YTD Return 0.11

2013 55.24

1 Year Annualised Statistical Data To Last Month End

Name Franklin India Feeder Franklin US Opportunities

Volatility 15.79

Alpha -4.53

Beta 1.19

r2 0.88

Sharpe 1.52

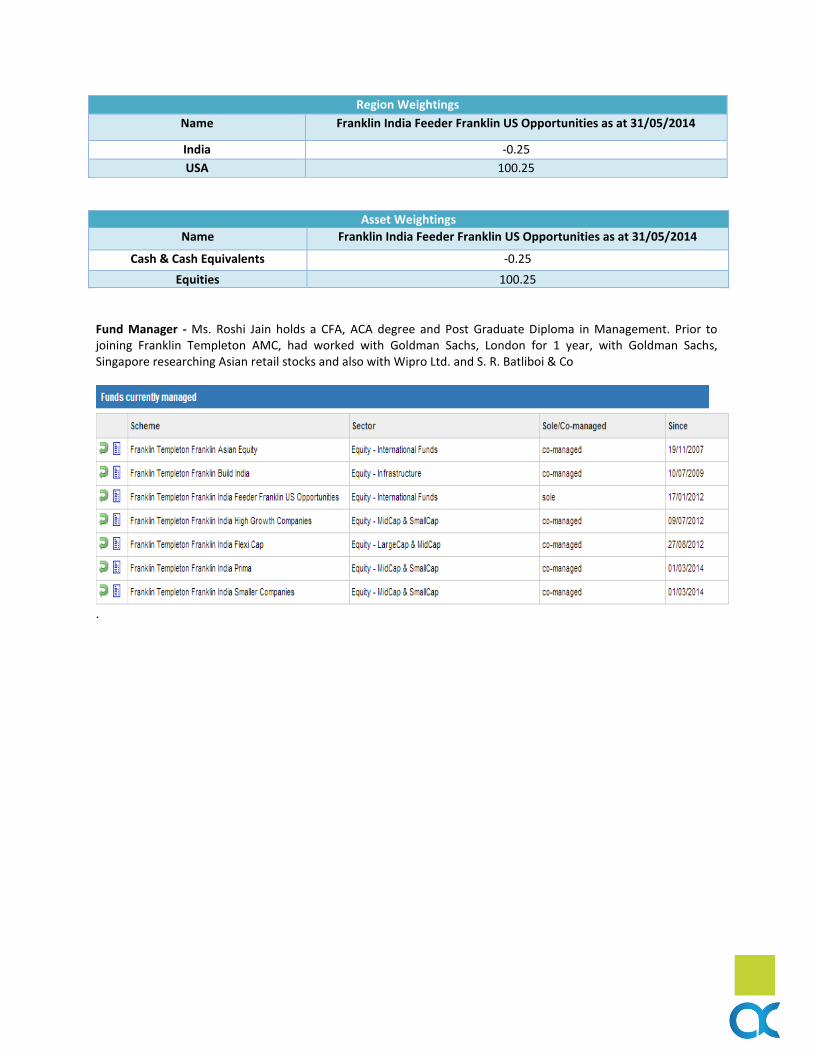

Region Weightings

Name Franklin India Feeder Franklin US Opportunities as at 31/05/2014

India -0.25

USA 100.25

Asset Weightings

Name Franklin India Feeder Franklin US Opportunities as at 31/05/2014

Cash & Cash Equivalents -0.25

Equities 100.25

Fund Manager - Ms. Roshi Jain holds a CFA, ACA degree and Post Graduate Diploma in Management. Prior to joining Franklin Templeton AMC, had worked with Goldman Sachs, London for 1 year, with Goldman Sachs, Singapore researching Asian retail stocks and also with Wipro Ltd. and S. R. Batliboi & Co

.

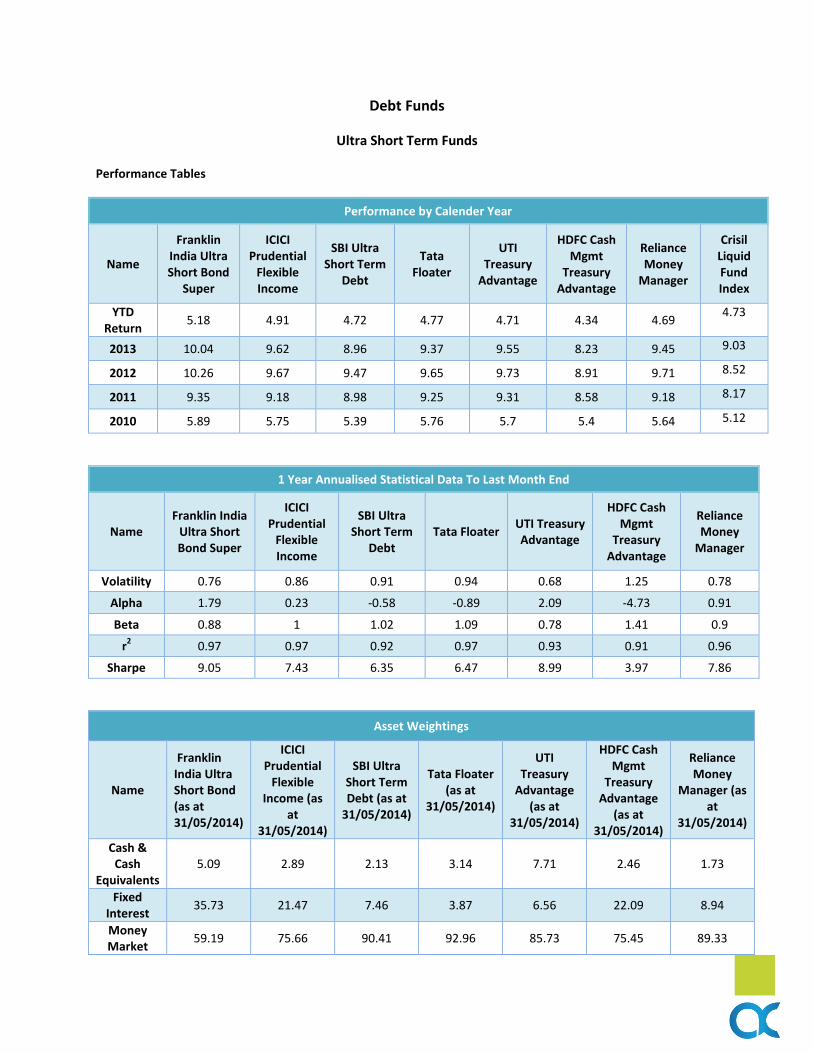

Debt Funds

Ultra Short Term Funds

Performance Tables

Performance by Calender Year

Name

Franklin India Ultra Short Bond

Super

ICICI Prudential

Flexible Income

SBI Ultra Short Term

Debt

Tata Floater

UTI Treasury

Advantage

HDFC Cash Mgmt

Treasury Advantage

Reliance Money

Manager

Crisil Liquid Fund Index

YTD Return

5.18 4.91 4.72 4.77 4.71 4.34 4.69 4.73

2013 10.04 9.62 8.96 9.37 9.55 8.23 9.45 9.03

2012 10.26 9.67 9.47 9.65 9.73 8.91 9.71 8.52

2011 9.35 9.18 8.98 9.25 9.31 8.58 9.18 8.17

2010 5.89 5.75 5.39 5.76 5.7 5.4 5.64 5.12

1 Year Annualised Statistical Data To Last Month End

Name Franklin India

Ultra Short Bond Super

ICICI Prudential

Flexible Income

SBI Ultra Short Term

Debt Tata Floater

UTI Treasury Advantage

HDFC Cash Mgmt

Treasury Advantage

Reliance Money

Manager

Volatility 0.76 0.86 0.91 0.94 0.68 1.25 0.78

Alpha 1.79 0.23 -0.58 -0.89 2.09 -4.73 0.91

Beta 0.88 1 1.02 1.09 0.78 1.41 0.9

r2 0.97 0.97 0.92 0.97 0.93 0.91 0.96

Sharpe 9.05 7.43 6.35 6.47 8.99 3.97 7.86

Asset Weightings

Name

Franklin India Ultra Short Bond (as at 31/05/2014)

ICICI Prudential

Flexible Income (as

at 31/05/2014)

SBI Ultra Short Term Debt (as at

31/05/2014)

Tata Floater (as at

31/05/2014)

UTI Treasury

Advantage (as at

31/05/2014)

HDFC Cash Mgmt

Treasury Advantage

(as at 31/05/2014)

Reliance Money

Manager (as at

31/05/2014)

Cash & Cash

Equivalents 5.09 2.89 2.13 3.14 7.71 2.46 1.73

Fixed Interest

35.73 21.47 7.46 3.87 6.56 22.09 8.94

Money Market

59.19 75.66 90.41 92.96 85.73 75.45 89.33

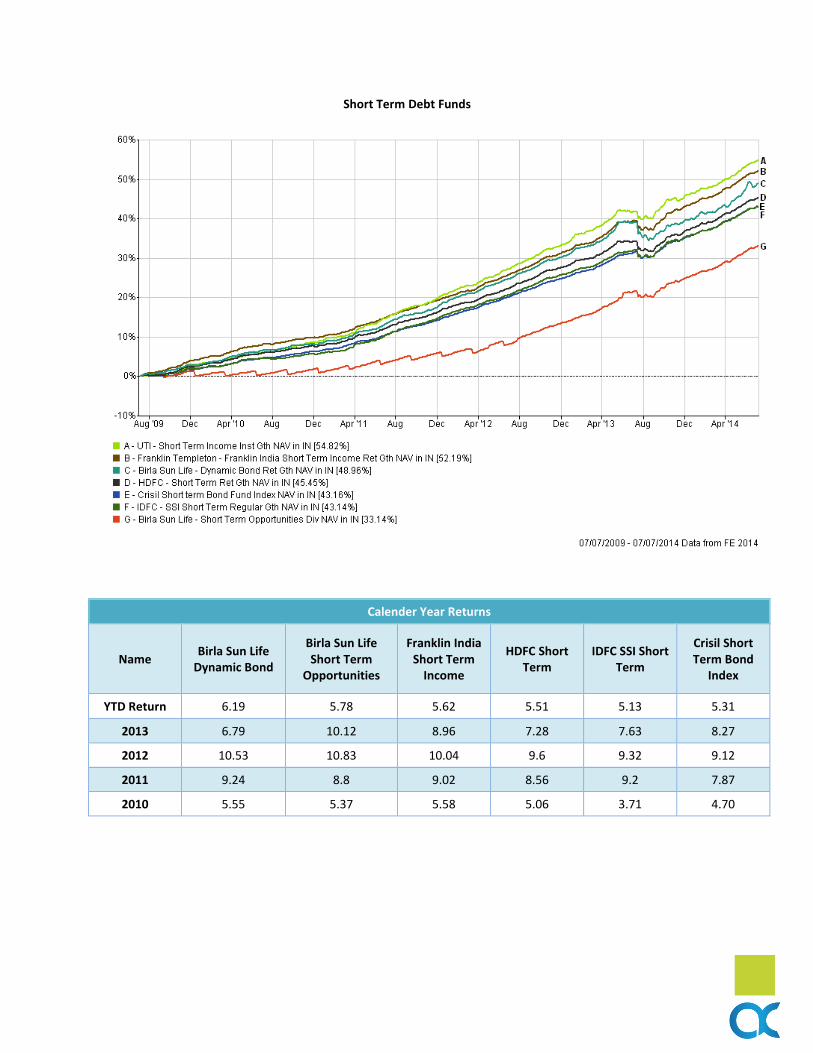

Short Term Debt Funds

Calender Year Returns

Name Birla Sun Life

Dynamic Bond

Birla Sun Life Short Term

Opportunities

Franklin India Short Term

Income

HDFC Short Term

IDFC SSI Short Term

Crisil Short Term Bond

Index

YTD Return 6.19 5.78 5.62 5.51 5.13 5.31

2013 6.79 10.12 8.96 7.28 7.63 8.27

2012 10.53 10.83 10.04 9.6 9.32 9.12

2011 9.24 8.8 9.02 8.56 9.2 7.87

2010 5.55 5.37 5.58 5.06 3.71 4.70

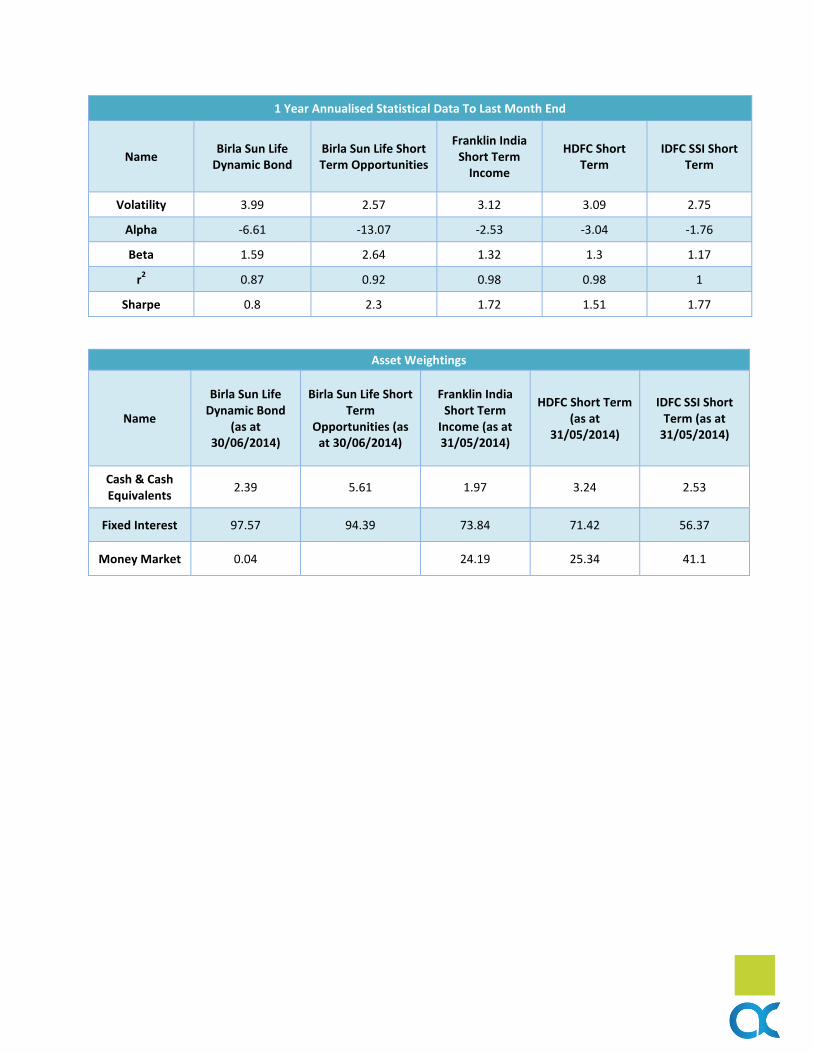

1 Year Annualised Statistical Data To Last Month End

Name Birla Sun Life

Dynamic Bond Birla Sun Life Short Term Opportunities

Franklin India Short Term

Income

HDFC Short Term

IDFC SSI Short Term

Volatility 3.99 2.57 3.12 3.09 2.75

Alpha -6.61 -13.07 -2.53 -3.04 -1.76

Beta 1.59 2.64 1.32 1.3 1.17

r2 0.87 0.92 0.98 0.98 1

Sharpe 0.8 2.3 1.72 1.51 1.77

Asset Weightings

Name

Birla Sun Life Dynamic Bond

(as at 30/06/2014)

Birla Sun Life Short Term

Opportunities (as at 30/06/2014)

Franklin India Short Term

Income (as at 31/05/2014)

HDFC Short Term (as at

31/05/2014)

IDFC SSI Short Term (as at

31/05/2014)

Cash & Cash Equivalents

2.39 5.61 1.97 3.24 2.53

Fixed Interest 97.57 94.39 73.84 71.42 56.37

Money Market 0.04

24.19 25.34 41.1

This report has been prepared by Investment Committee:

Mukesh Jindal CFA, CAIA, CFP Akhil Bhardwaj

Partner, Alpha Capital Partner, Alpha Capital

Shruti Singh Rovind Kumar

Senior Analyst, Research Desk Senior Analyst, Research Desk

Pankaj Kumar

Senior Analyst

For further queries and clarification please contact: [email protected]

Disclaimer

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

In the preparation of the material contained in this document, Alpha Capital has used information that is publicly

available, including information developed in-house. Some of the material used in the document may have been

obtained from members/persons other than the company and/or its affiliates and which may have been made

available to the company and/or to its affiliates. Information gathered and material used in this document is

believed to be from reliable sources. The company however does not warrant the accuracy, reasonableness and /

or completeness of any information. We have included statements / opinions / recommendations in this

document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or

variations of such expressions that are “forward looking statements”. Actual results may differ materially from

those suggested by the forward looking statements due to risk or uncertainties associated with our expectations

with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and

other countries globally, which have an impact on our services and / or investments, the monetary and interest

policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity

prices or other rates or prices etc.

Alpha Capital, the Mutual Fund, The Trust and any of its officers, directors, personnel and employees, shall not

liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary,

consequential, as also any loss of profit in any way arising from the use of this material in any manner.