Embed Size (px)

Citation preview

Quantsmile: Quantitative Portfolio Quantsmile: Quantitative Portfolio Management Management

IndexIndex Company Introduction

Why Quantsmile

Quantitative Investment Process

◦ Portfolio Construction

◦ Portfolio Optimization

◦ Execution Management

◦ Risk Management

◦ Rebalancing

Asset Management Services Offered by Quantsmile

Company IntroductionCompany Introduction

Quantsmile is one of the top leading technology driven portfolio management companies based in Hong Kong

Quantsmile is using quantitative approach in asset portfolio management

Why Quantsmile (1)Why Quantsmile (1)

1. Good Reputation Being a regulated entity, it has built up its reputation in using

advanced quantitative technology to earn alpha in portfolio management

It is licensed by Hong Kong Securities and Futures Commission to conduct asset management business

2. Competitive Advantage It combines the pro of value investing process of the traditional fund

and risk management solution of the hedge fund, to develop its own quantitative investment model

With the use of systematic and quantitative “Value Investing” solution, Quantsmile searches for under-valued companies. Their share prices would benefit from up-side adjustment of the non-efficient market in short term to the efficient market in long term

Why Quantsmile (2)Why Quantsmile (2)

3. Investment Team Quantsmile has experienced portfolio managers and strong

quantitative research team It has a stable management team, and most of its portfolio managers

have been working together for ten years at Quantsmile

4. Strive for Better Return Since management team allows research and investment process be

implemented at the unit level, and the responsible portfolio manager having a degree of autonomy, these enable the portfolio be flexibly managed for better return

5. Prudent Approach We aim to minimize investment risk and preserve capital. We build a

diversified portfolio with high quality and undervalued stocks, pre-determined constraints set in the model, and the use of derivatives products to hedge market risk

Quantitative Investment Process Quantitative Investment Process Involves: Involves: Portfolio Construction

Portfolio Optimization

Execution Management

Risk Management

Rebalancing

Portfolio Construction (1)Portfolio Construction (1)

Top-down investing approach

Over-weight sectors which have outperforming potential

Earn alpha through careful over- and under-weight different sectors against benchmark

Portfolio Construction (2)Portfolio Construction (2)

Select stocks within each sector in a value-investing framework

Quantitative fundamentals (PE, PB, DCF valuation) are applied in the stock screening process

One year target price will then be calculated based on the above assessment

Portfolio Construction (3)Portfolio Construction (3)

Research team provides fundamental studies on each sector and stocks for inclusion

Investment management committee regularly reviews macro economic environment variables

Review results will then be incorporated back to the stock selection process for portfolio adjustment

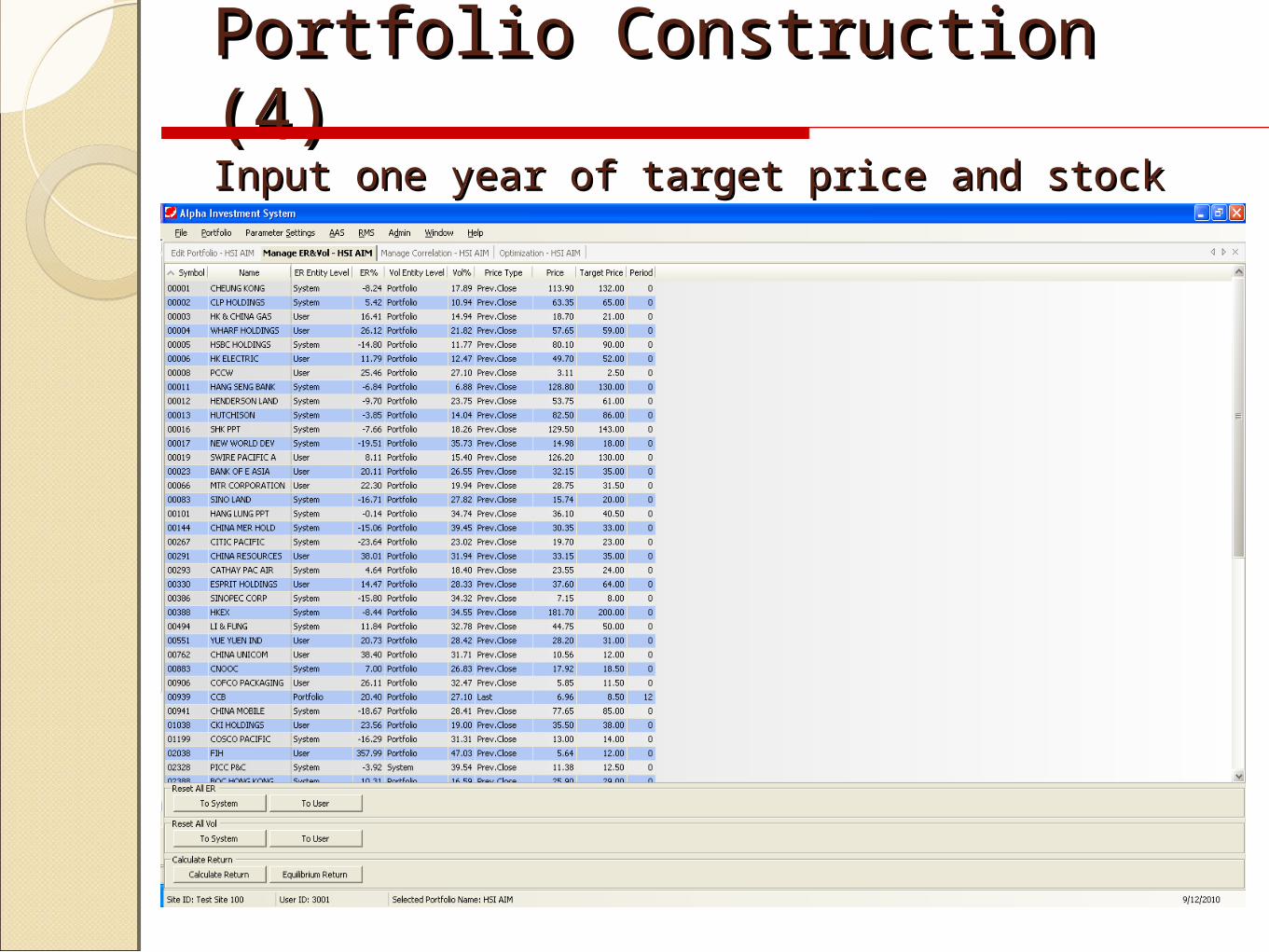

Portfolio Construction (4)Portfolio Construction (4)Input one year of target price and stock volatility Input one year of target price and stock volatility

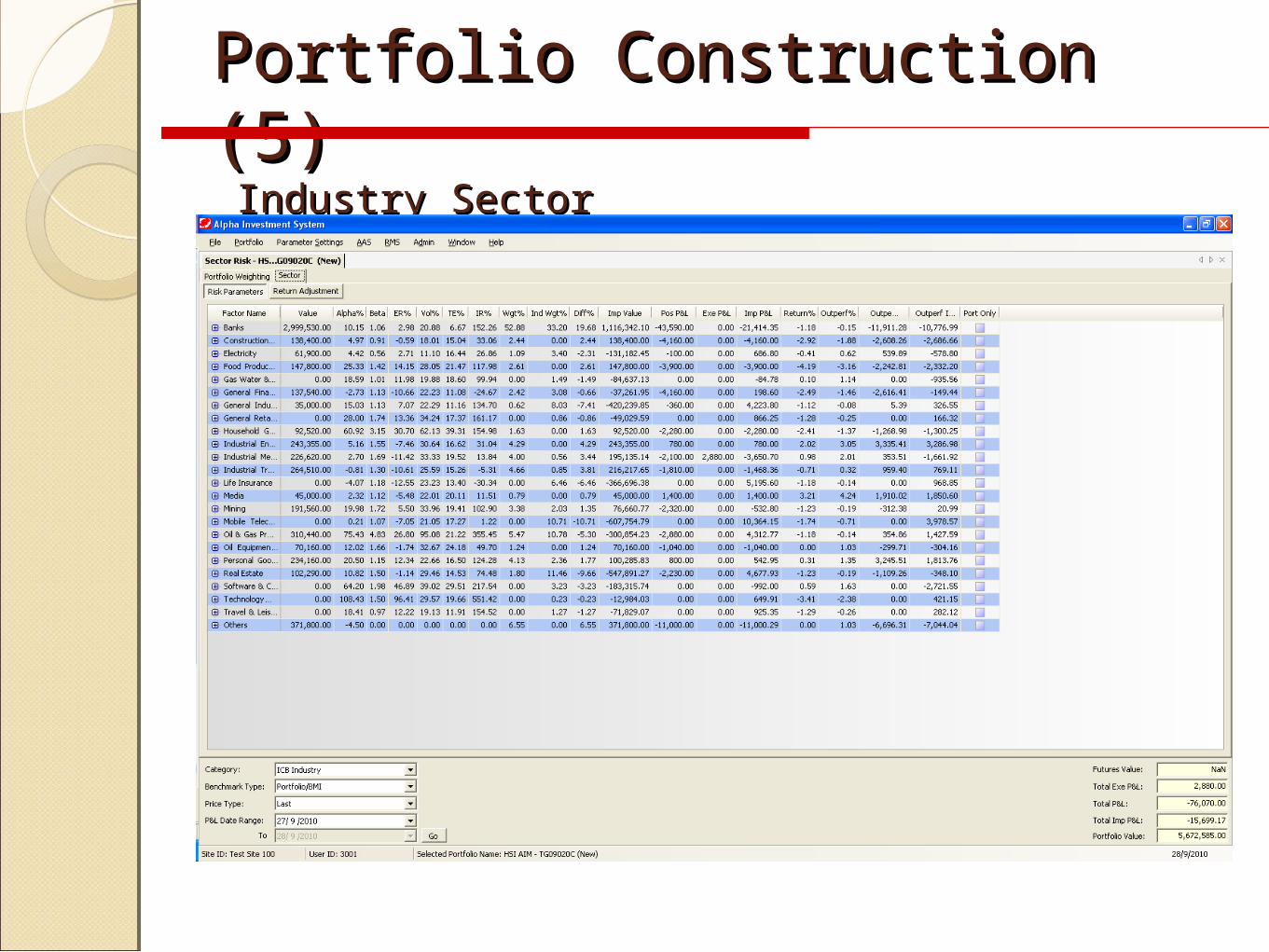

Portfolio Construction (5)Portfolio Construction (5) Industry Sector Industry Sector

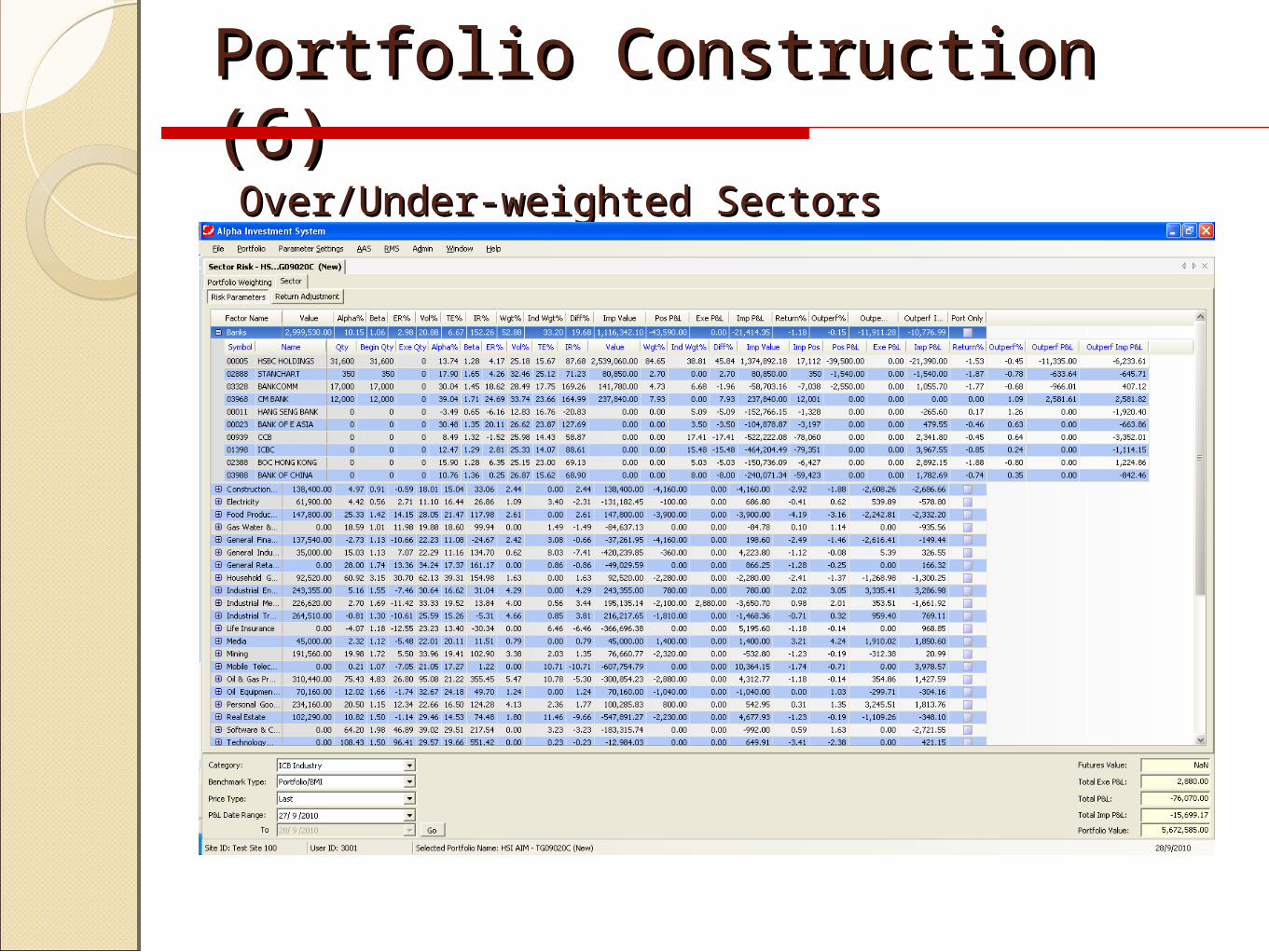

Portfolio Construction (6)Portfolio Construction (6) Over/Under-weighted SectorsOver/Under-weighted Sectors

Portfolio Optimization (1)Portfolio Optimization (1)

Selected stocks shall then undergo a series of fine-tuning

Clients’ risk tolerance and return target are part of the optimization consideration

Portfolio Optimization (2)Portfolio Optimization (2)

Efficient frontier derived from the CAPM model, combined with optimization parameters, will then generate an optimized portfolio set for implementation

Constraints with minimum and maximum allowable portfolio weightings could be imposed

Portfolio Optimization (3)Portfolio Optimization (3)Constraints with Minimum & Maximum Weighting Conditions Constraints with Minimum & Maximum Weighting Conditions

Portfolio Optimization (4) Portfolio Optimization (4) Portfolio After Optimization and the Efficient Frontier Portfolio After Optimization and the Efficient Frontier

Execution ManagementExecution Management

If market-neutral strategy is selected, delta hedging is applied to the equities portfolio

By eliminating the market exposure (beta), market out-performance becomes the alpha earned for the portfolio

In executing equities buy and sell orders, quantitative and adaptative execution algorithm is employed to maximize VWAP

Risk ManagementRisk Management

Quantitative risk control measures such as Value-at-risk (VaR) are real-time monitored

Portfolio with risk exceeding acceptable level will be scrutinized and appropriate action will be taken to bring risk exposure back to accepted level

Up-to-date risk reports are always online and available to management team for review and actions, as needed

RebalancingRebalancing

Market exposure is constantly reviewed and monitored using advanced reporting tools

When certain exposure parameters have essentially shifted, dynamic rebalancing techniques will be put into action

To lock in alpha, dynamic rebalancing will strive to adjust hedging proportion and execute equities buy (at low) and sell (at high) transactions

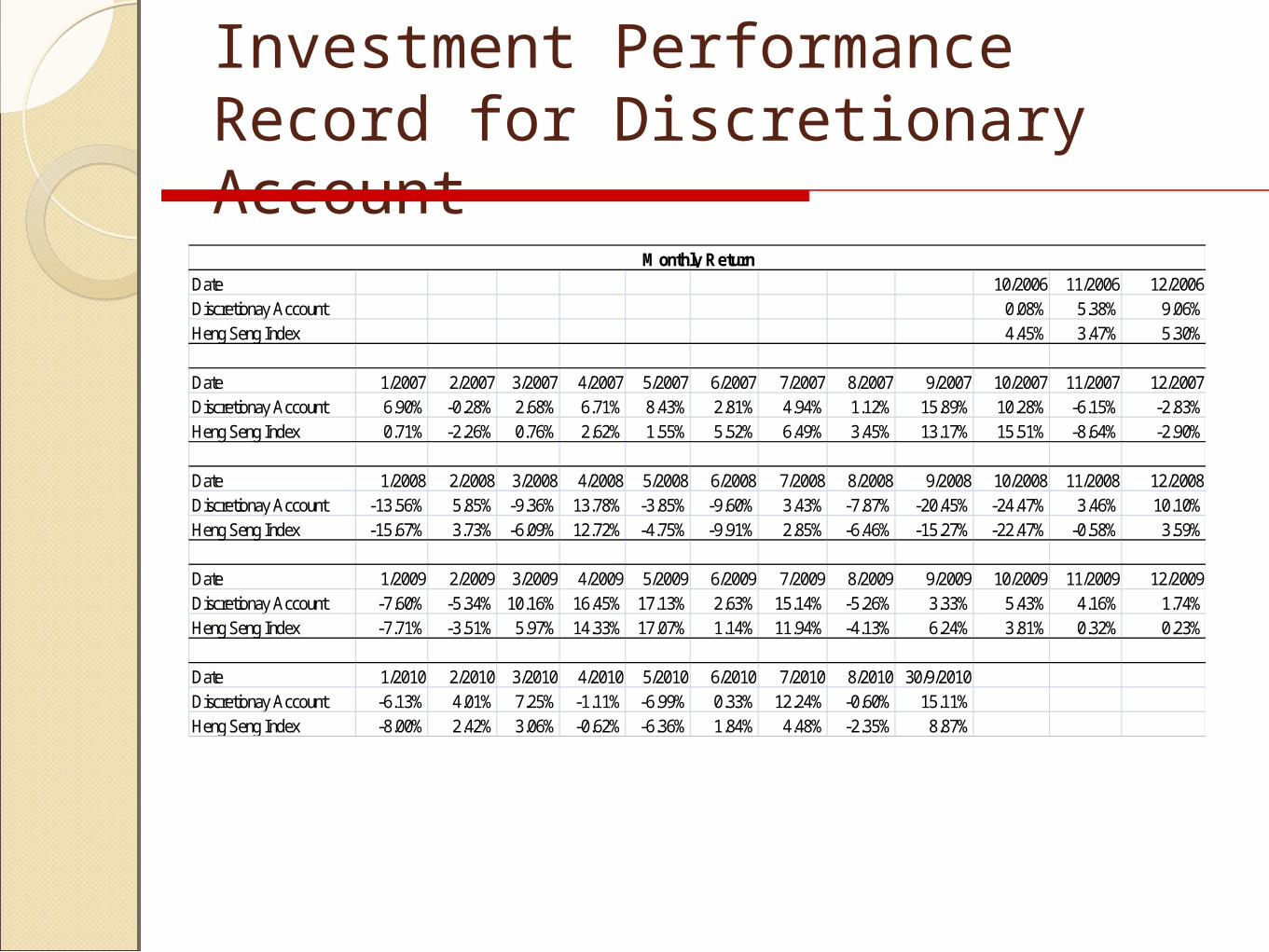

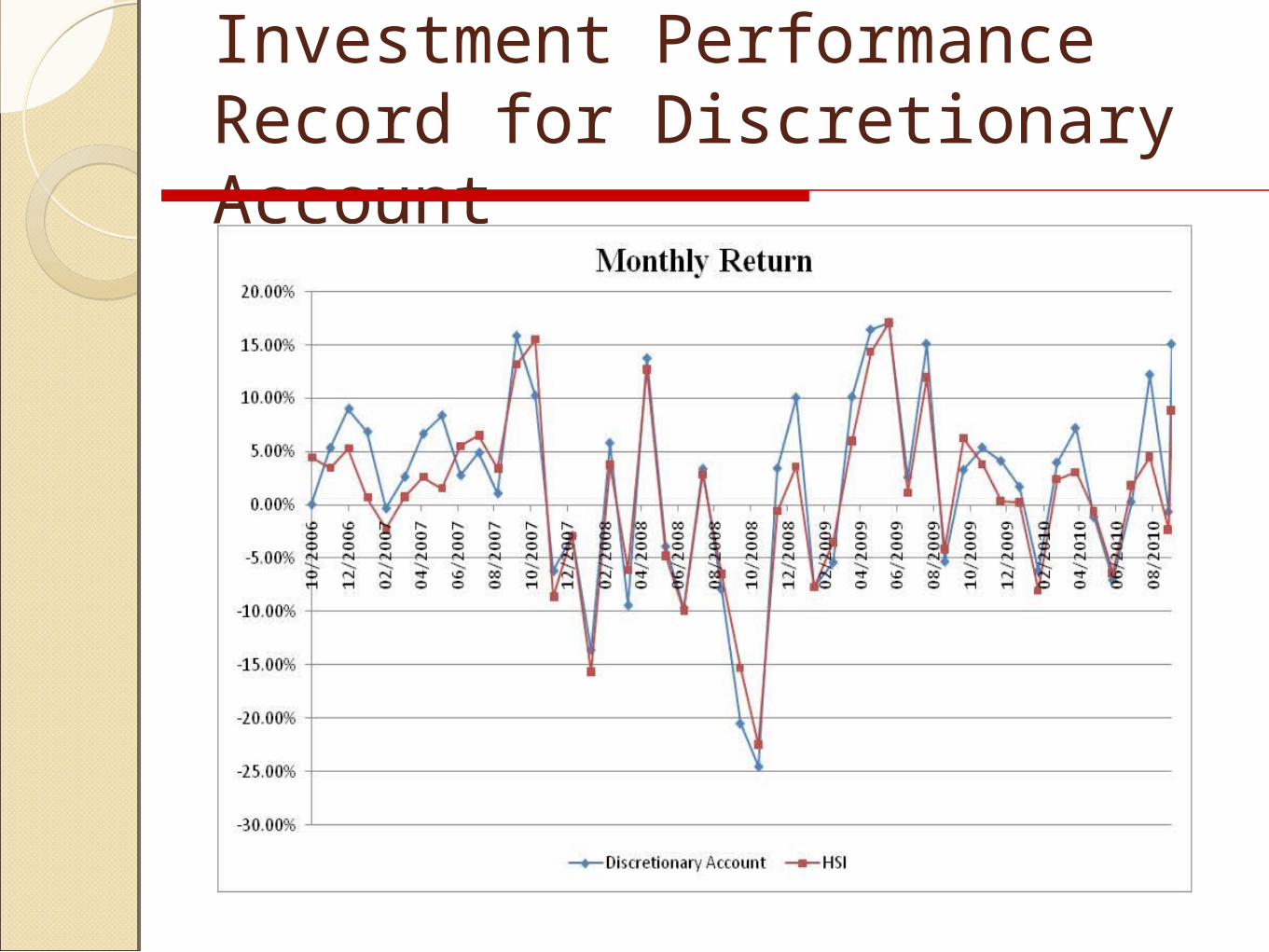

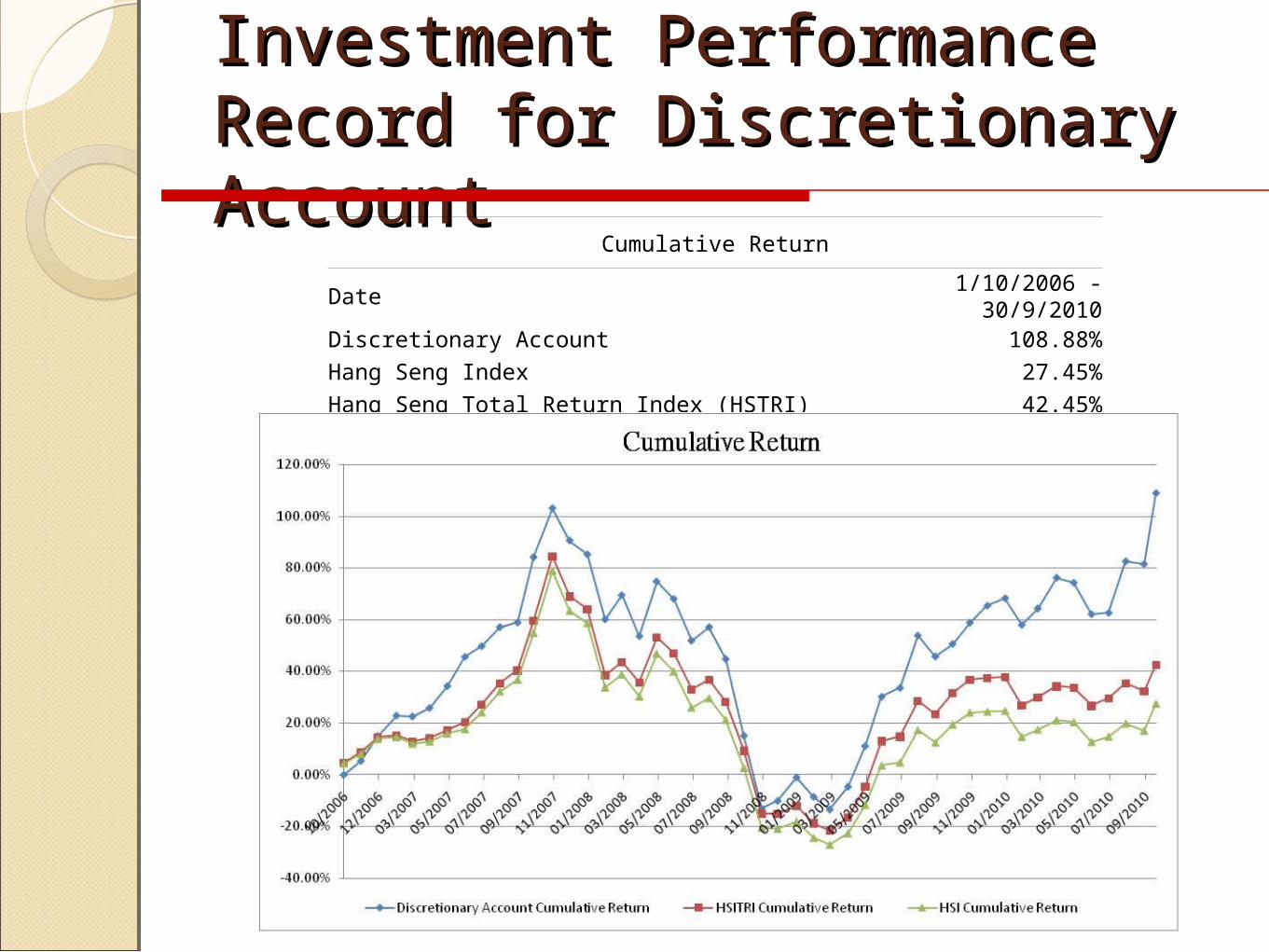

Investment Performance Record for Discretionary Account

Date 10/2006 11/2006 12/2006Discretionay Account 0.08% 5.38% 9.06%Heng Seng Index 4.45% 3.47% 5.30%

Date 1/2007 2/2007 3/2007 4/2007 5/2007 6/2007 7/2007 8/2007 9/2007 10/2007 11/2007 12/2007Discretionay Account 6.90% -0.28% 2.68% 6.71% 8.43% 2.81% 4.94% 1.12% 15.89% 10.28% -6.15% -2.83%Heng Seng Index 0.71% -2.26% 0.76% 2.62% 1.55% 5.52% 6.49% 3.45% 13.17% 15.51% -8.64% -2.90%

Date 1/2008 2/2008 3/2008 4/2008 5/2008 6/2008 7/2008 8/2008 9/2008 10/2008 11/2008 12/2008Discretionay Account -13.56% 5.85% -9.36% 13.78% -3.85% -9.60% 3.43% -7.87% -20.45% -24.47% 3.46% 10.10%Heng Seng Index -15.67% 3.73% -6.09% 12.72% -4.75% -9.91% 2.85% -6.46% -15.27% -22.47% -0.58% 3.59%

Date 1/2009 2/2009 3/2009 4/2009 5/2009 6/2009 7/2009 8/2009 9/2009 10/2009 11/2009 12/2009Discretionay Account -7.60% -5.34% 10.16% 16.45% 17.13% 2.63% 15.14% -5.26% 3.33% 5.43% 4.16% 1.74%Heng Seng Index -7.71% -3.51% 5.97% 14.33% 17.07% 1.14% 11.94% -4.13% 6.24% 3.81% 0.32% 0.23%

Date 1/2010 2/2010 3/2010 4/2010 5/2010 6/2010 7/2010 8/2010 30/9/2010Discretionay Account -6.13% 4.01% 7.25% -1.11% -6.99% 0.33% 12.24% -0.60% 15.11%Heng Seng Index -8.00% 2.42% 3.06% -0.62% -6.36% 1.84% 4.48% -2.35% 8.87%

Monthly Return

Investment Performance Record for Discretionary Account

Investment Performance Record for Investment Performance Record for Discretionary AccountDiscretionary Account

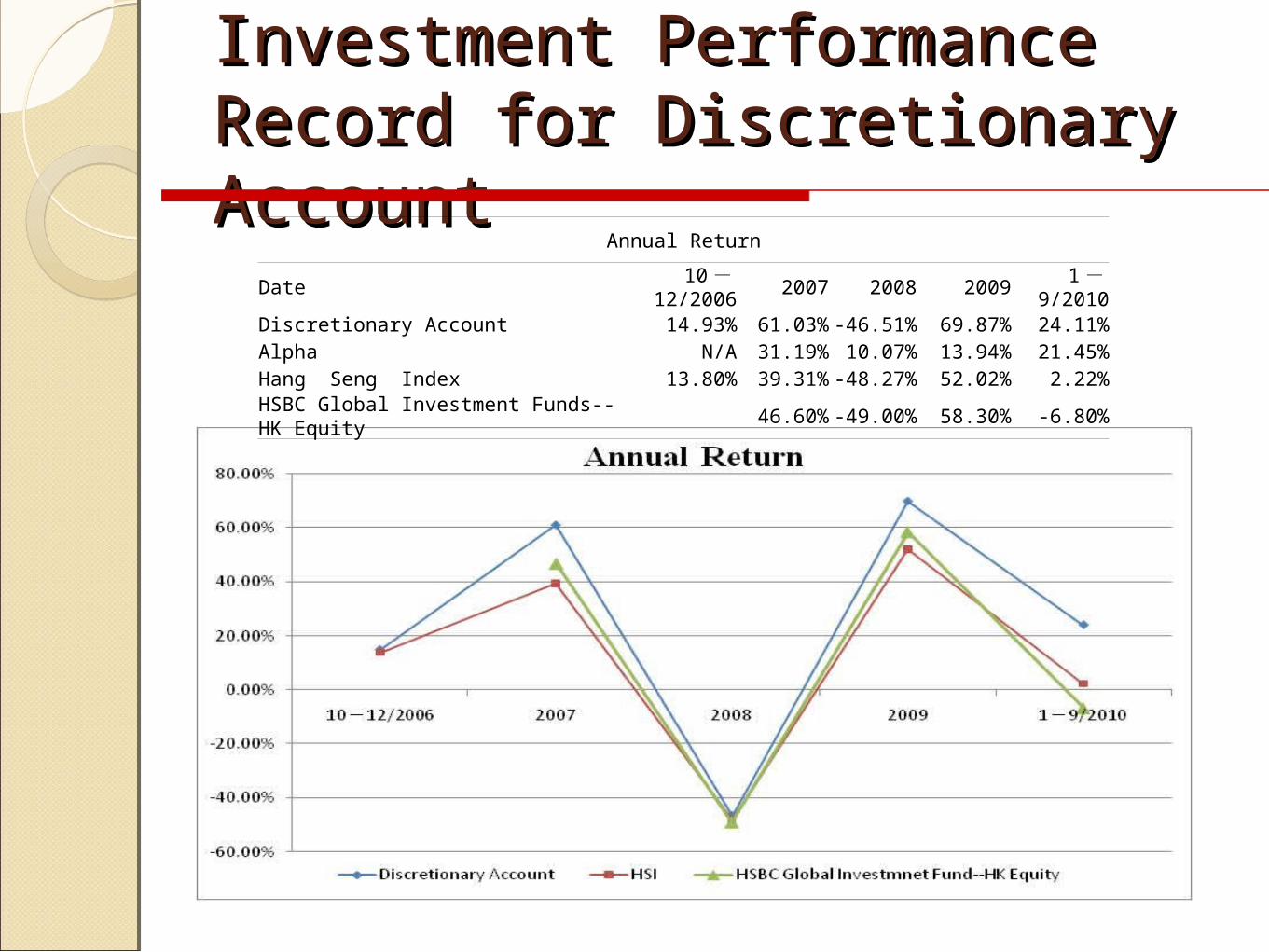

Annual Return

Date 10 - 12/2006 2007 2008 2009 1 - 9/2010Discretionary Account 14.93% 61.03% -46.51% 69.87% 24.11%Alpha N/A 31.19% 10.07% 13.94% 21.45%Hang Seng Index 13.80% 39.31% -48.27% 52.02% 2.22%

HSBC Global Investment Funds--HK Equity 46.60% -49.00% 58.30% -6.80%

Investment Performance Record for Investment Performance Record for Discretionary AccountDiscretionary Account

Cumulative Return

Date 1/10/2006 - 30/9/2010

Discretionary Account 108.88%

Hang Seng Index 27.45%

Hang Seng Total Return Index (HSTRI) 42.45%

Asset Management Services Offered Asset Management Services Offered by Quantsmileby Quantsmile

Quantsmile has a full asset management licence and offers the following wealth management products:

Discretionary asset management to all types of investors

Portfolio Management Service as an outsourced fund manager for private equity fund and fund management company. This service will utilise the in-house developed AIS model to strive for higher Alpha return

Thank You