Embed Size (px)

Citation preview

October 26, 2012

Presented at:

“Restructuring Financial Infrastructure to Speed

Recovery”

Brookings-Nomura-Wharton Conference on

Financial Markets 2012

Reconstructing and Revitalizing Japan's Financial Sector:

Policy Implications

Yuta Seki

Kei Kodachi

Hiroshi Yoshikawa

Nomura Institute of Capital Markets Research (Japan)

1

Major Concern: Containing System-Wide Shock and Rebuilding Confidence

Japanese Experiences

Removing Bad Assets Regarded as Critically Important Policy

Lack of Legal Framework and Practices for Transacting Distressed Assets/Businesses

Designing “Comprehensive” Policies for Reconstruction

Balancing Incentives of Senior Managers and Improved Transparency and Governance

Revitalizing Corporate Sector and Real Estate Market

Concerns and Issues

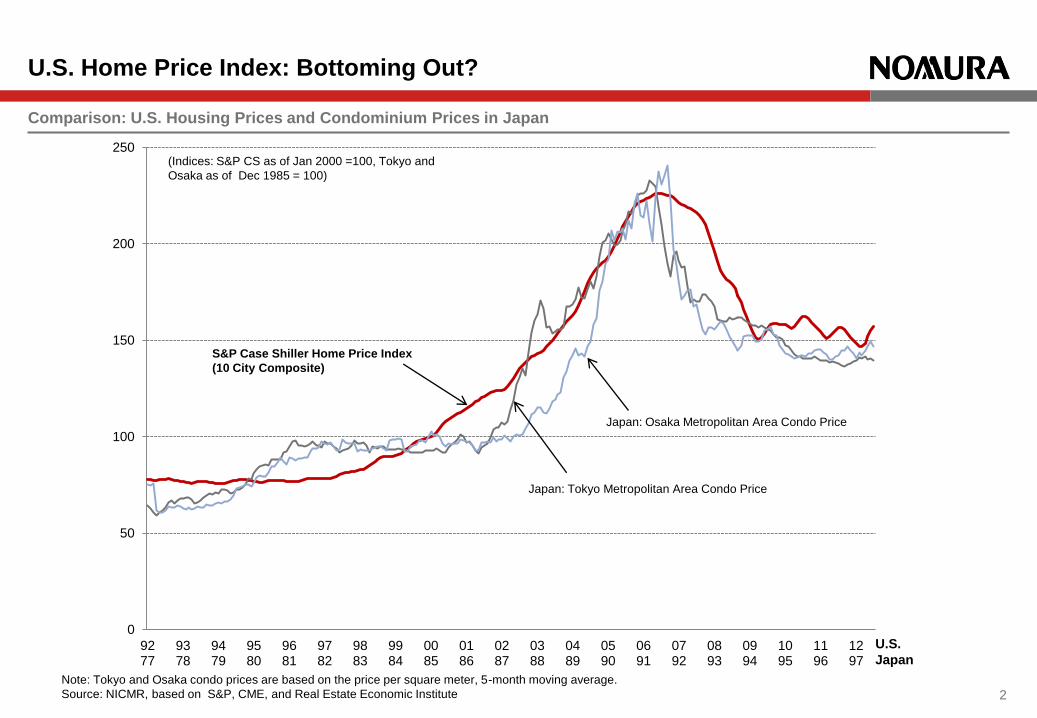

U.S. Home Price Index: Bottoming Out?

2

0

50

100

150

200

250

92 77

93 78

94 79

95 80

96 81

97 82

98 83

99 84

00 85

01 86

02 87

03 88

04 89

05 90

06 91

07 92

08 93

09 94

10 95

11 96

12 97

S&P Case Shiller Home Price Index

(10 City Composite)

Japan: Tokyo Metropolitan Area Condo Price

Japan: Osaka Metropolitan Area Condo Price

(Indices: S&P CS as of Jan 2000 =100, Tokyo and

Osaka as of Dec 1985 = 100)

Note: Tokyo and Osaka condo prices are based on the price per square meter, 5-month moving average.

Source: NICMR, based on S&P, CME, and Real Estate Economic Institute

Comparison: U.S. Housing Prices and Condominium Prices in Japan

U.S.

Japan

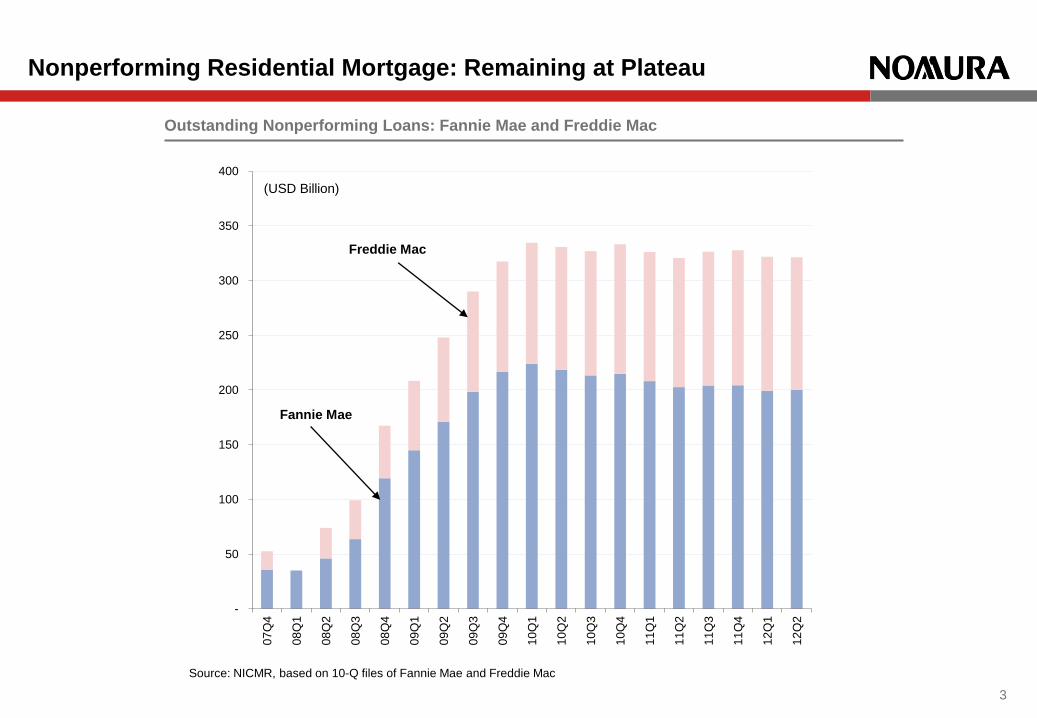

Nonperforming Residential Mortgage: Remaining at Plateau

3

Source: NICMR, based on 10-Q files of Fannie Mae and Freddie Mac

Outstanding Nonperforming Loans: Fannie Mae and Freddie Mac

-

50

100

150

200

250

300

350

400

07

Q4

08

Q1

08

Q2

08

Q3

08

Q4

09

Q1

09

Q2

09

Q3

09

Q4

10

Q1

10

Q2

10

Q3

10

Q4

11

Q1

11

Q2

11

Q3

11

Q4

12

Q1

12

Q2

(USD Billion)

Freddie Mac

Fannie Mae

0

50

100

150

200

250

300

350

400

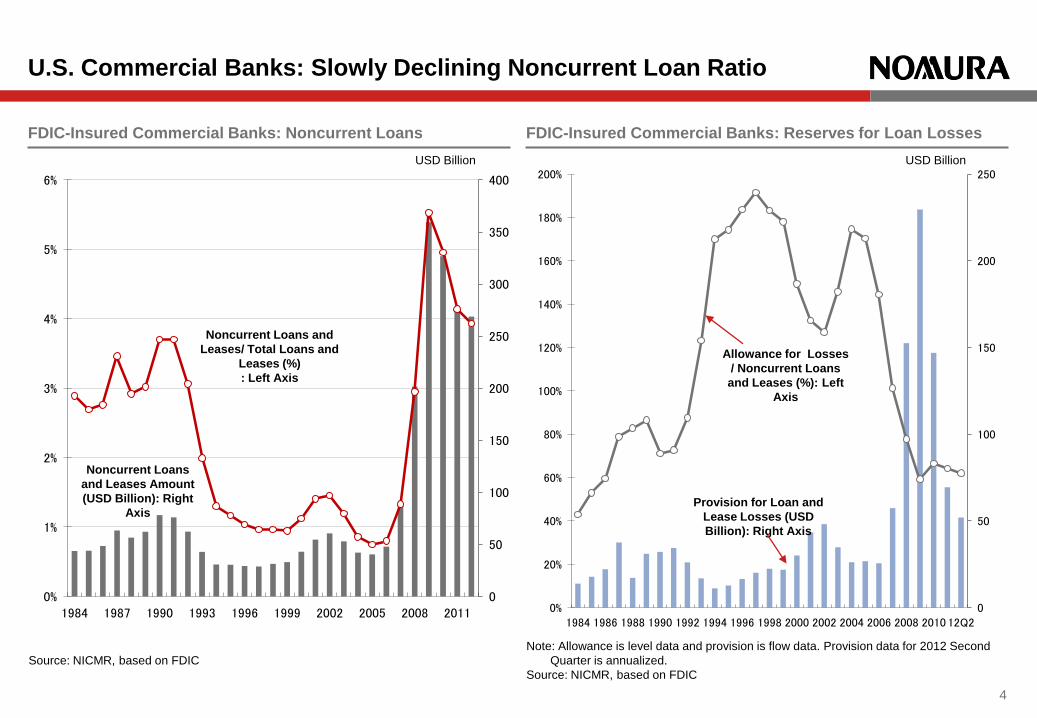

0%

1%

2%

3%

4%

5%

6%

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

Noncurrent Loans and

Leases/ Total Loans and

Leases (%)

: Left Axis

Noncurrent Loans

and Leases Amount

(USD Billion): Right

Axis

0

50

100

150

200

250

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 12Q2

Allowance for Losses

/ Noncurrent Loans

and Leases (%): Left

Axis

Provision for Loan and

Lease Losses (USD

Billion): Right Axis

U.S. Commercial Banks: Slowly Declining Noncurrent Loan Ratio

4

FDIC-Insured Commercial Banks: Noncurrent Loans FDIC-Insured Commercial Banks: Reserves for Loan Losses

Source: NICMR, based on FDIC

Note: Allowance is level data and provision is flow data. Provision data for 2012 Second

Quarter is annualized.

Source: NICMR, based on FDIC

USD Billion USD Billion

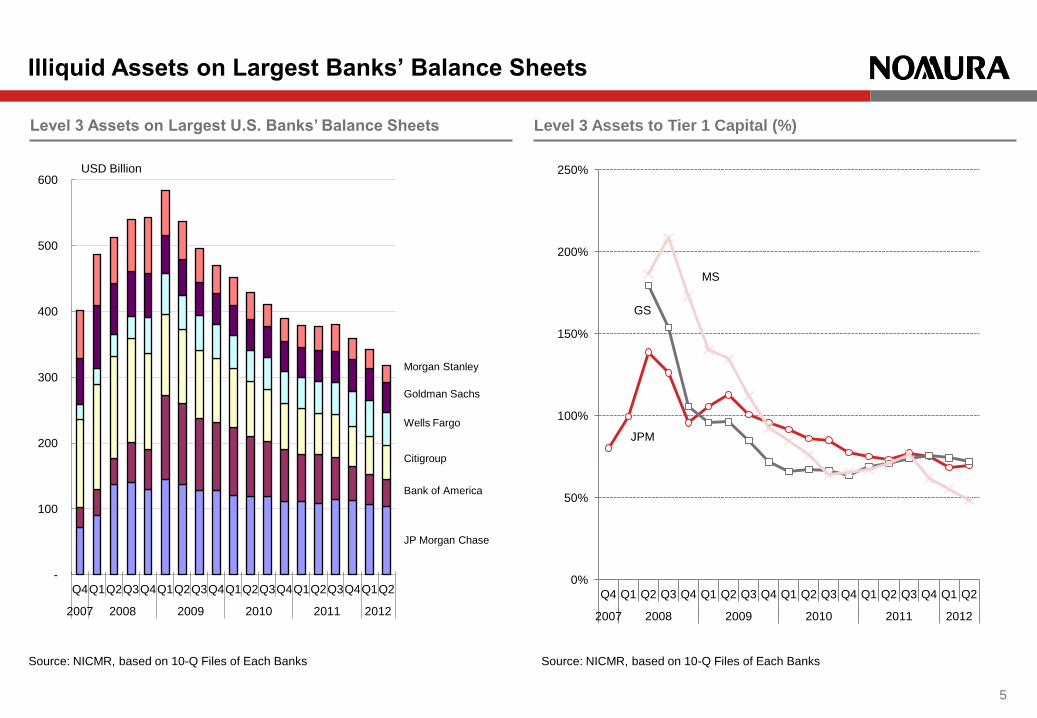

Illiquid Assets on Largest Banks’ Balance Sheets

Source: NICMR, based on 10-Q Files of Each Banks

5

Level 3 Assets on Largest U.S. Banks’ Balance Sheets Level 3 Assets to Tier 1 Capital (%)

Source: NICMR, based on 10-Q Files of Each Banks

-

100

200

300

400

500

600

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009 2010 2011 2012

USD Billion

JP Morgan Chase

Bank of America

Citigroup

Wells Fargo

Goldman Sachs

Morgan Stanley

0%

50%

100%

150%

200%

250%

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009 2010 2011 2012

JPM

MS

GS

0

100

200

300

400

500

600

700

Ja

n-0

4

Ju

n-0

4

No

v-0

4

Ap

r-0

5

Se

p-0

5

Fe

b-0

6

Ju

l-0

6

De

c-0

6

Ma

y-0

7

Oct-

07

Ma

r-0

8

Au

g-0

8

Ja

n-0

9

Ju

n-0

9

No

v-0

9

Ap

r-1

0

Se

p-1

0

Fe

b-1

1

Ju

l-1

1

De

c-1

1

Ma

y-1

2

Citi

BofA

JPM

Wells Fargo

GS

MS

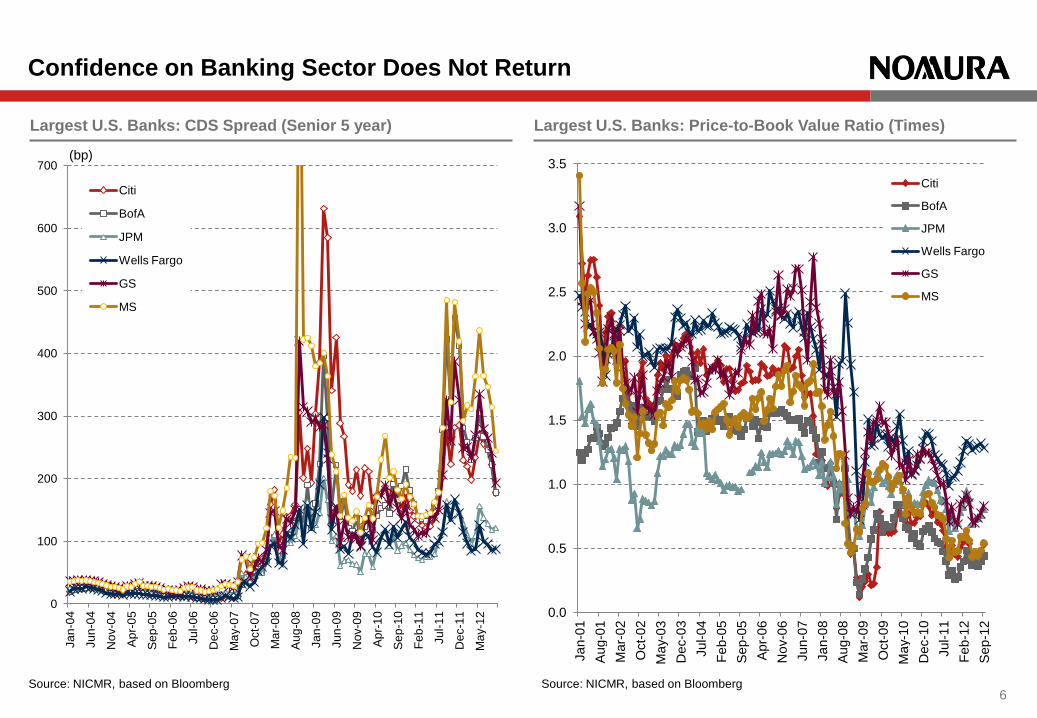

Confidence on Banking Sector Does Not Return

Source: NICMR, based on Bloomberg 6

Largest U.S. Banks: CDS Spread (Senior 5 year) Largest U.S. Banks: Price-to-Book Value Ratio (Times)

Source: NICMR, based on Bloomberg

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan-0

1

Aug-0

1

Mar-

02

Oct-

02

Ma

y-0

3

Dec-0

3

Jul-04

Feb-0

5

Sep-0

5

Apr-

06

Nov-0

6

Jun-0

7

Jan-0

8

Aug-0

8

Mar-

09

Oct-

09

Ma

y-1

0

Dec-1

0

Jul-11

Feb-1

2

Sep-1

2

Citi

BofA

JPM

Wells Fargo

GS

MS

(bp)

7

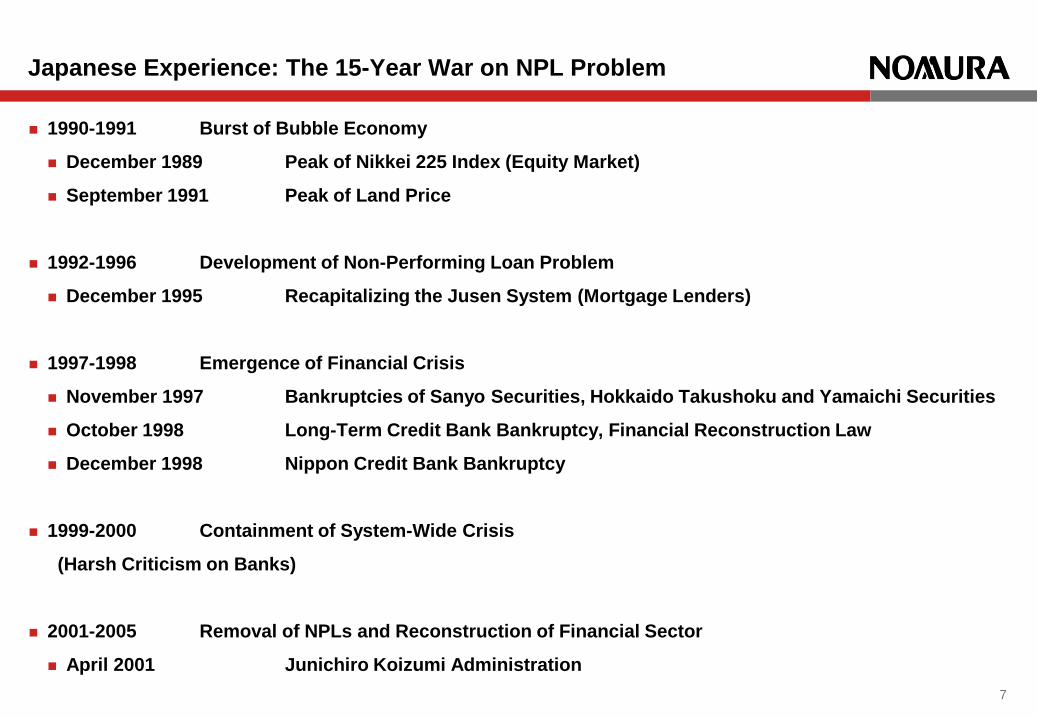

1990-1991 Burst of Bubble Economy

December 1989 Peak of Nikkei 225 Index (Equity Market)

September 1991 Peak of Land Price

1992-1996 Development of Non-Performing Loan Problem

December 1995 Recapitalizing the Jusen System (Mortgage Lenders)

1997-1998 Emergence of Financial Crisis

November 1997 Bankruptcies of Sanyo Securities, Hokkaido Takushoku and Yamaichi Securities

October 1998 Long-Term Credit Bank Bankruptcy, Financial Reconstruction Law

December 1998 Nippon Credit Bank Bankruptcy

1999-2000 Containment of System-Wide Crisis

(Harsh Criticism on Banks)

2001-2005 Removal of NPLs and Reconstruction of Financial Sector

April 2001 Junichiro Koizumi Administration

Japanese Experience: The 15-Year War on NPL Problem

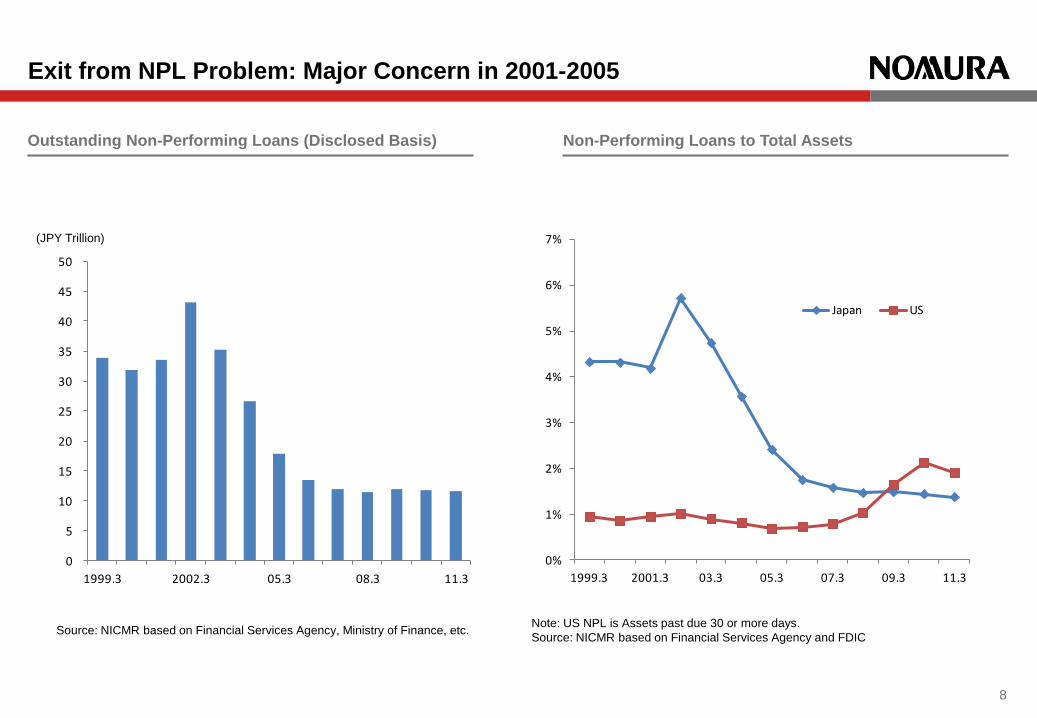

Outstanding Non-Performing Loans (Disclosed Basis)

Exit from NPL Problem: Major Concern in 2001-2005

8

Source: NICMR based on Financial Services Agency, Ministry of Finance, etc.

0

5

10

15

20

25

30

35

40

45

50

1999.3 2002.3 05.3 08.3 11.3

(JPY Trillion)

0%

1%

2%

3%

4%

5%

6%

7%

1999.3 2001.3 03.3 05.3 07.3 09.3 11.3

Japan US

Non-Performing Loans to Total Assets

Note: US NPL is Assets past due 30 or more days.

Source: NICMR based on Financial Services Agency and FDIC

9

“Too Many To Fail”

Depressed Macro Economy

Disorganization of Industrial Sector

“Kicking the Can Down the Road”

Painful Secondary Loss by Sales

Remote from Fair Value Accounting

Lack of Incentives for Bank Management

“Extend and Pretend”, “Zombie” Companies

Complicated Debtor-Creditor Relationships

Recourse Loans

Multiple Mortgages on Single Property

Why Japan’s Financial Sector Struggled for So Long?

Lack of Market for Distressed Assets

No Legal Framework for Corporate

Reorganization or Out-of-Court Workouts

Debtor-in-Possession (DIP) Financing

Stagnant Real Estate Market

SPC Laws for Securitization (Enacted in 1998)

J-REIT Market (Launched in 2001)

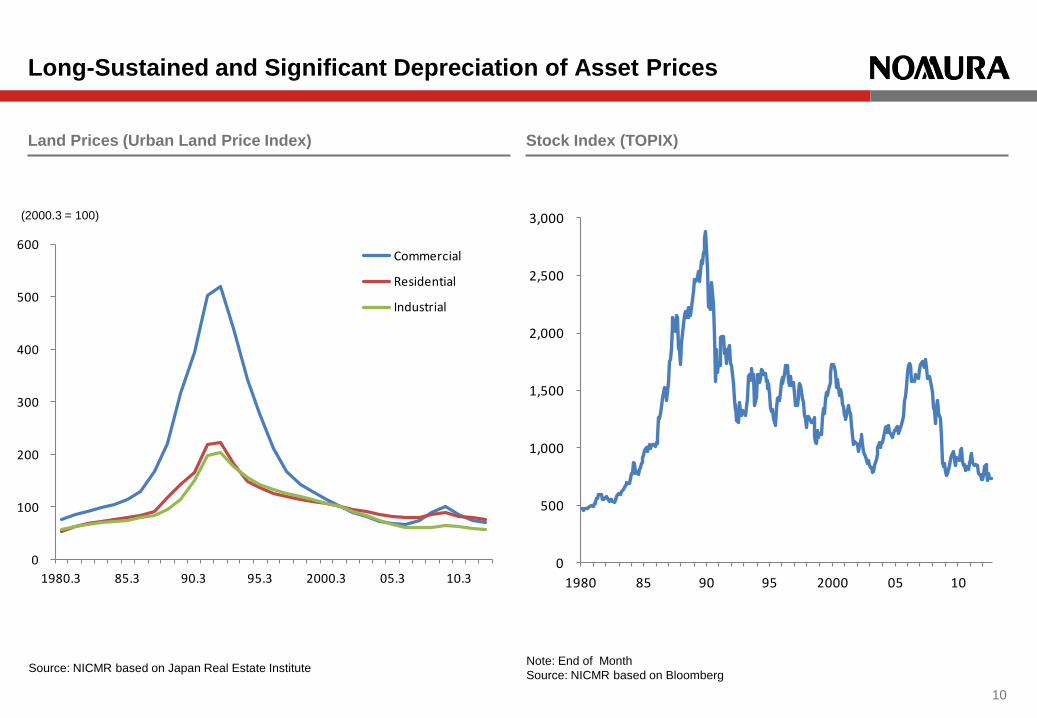

Long-Sustained and Significant Depreciation of Asset Prices

10

Land Prices (Urban Land Price Index) Stock Index (TOPIX)

Source: NICMR based on Japan Real Estate Institute Note: End of Month

Source: NICMR based on Bloomberg

(2000.3 = 100)

0

100

200

300

400

500

600

1980.3 85.3 90.3 95.3 2000.3 05.3 10.3

Commercial

Residential

Industrial

0

500

1,000

1,500

2,000

2,500

3,000

1980 85 90 95 2000 05 10

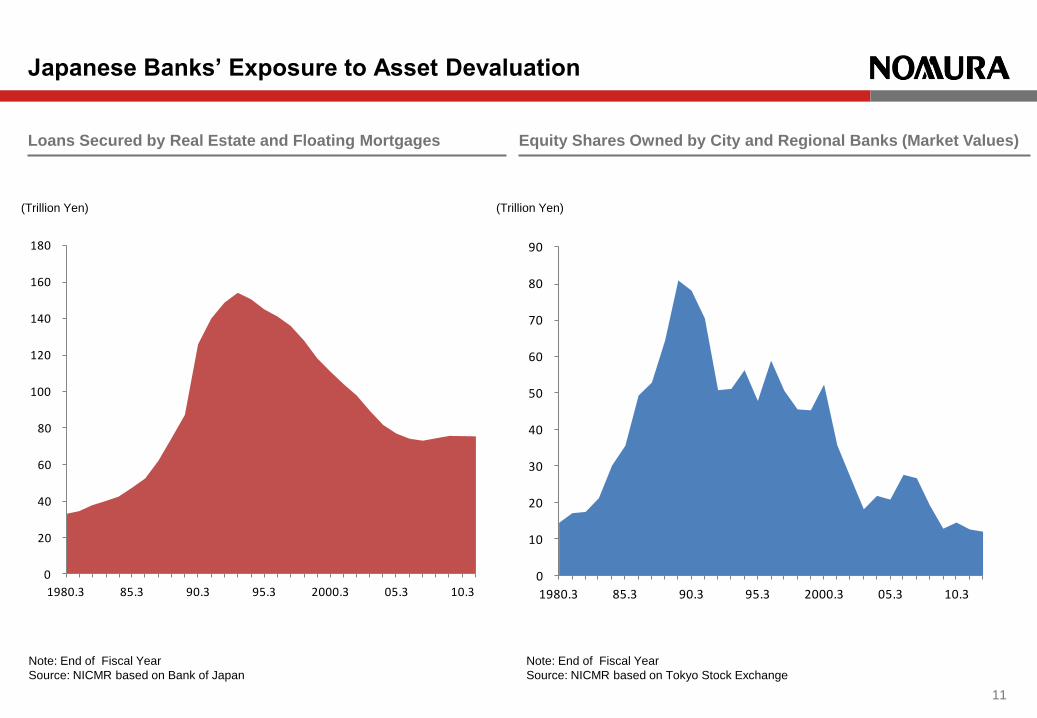

Japanese Banks’ Exposure to Asset Devaluation

11

Loans Secured by Real Estate and Floating Mortgages Equity Shares Owned by City and Regional Banks (Market Values)

Note: End of Fiscal Year

Source: NICMR based on Bank of Japan

Note: End of Fiscal Year

Source: NICMR based on Tokyo Stock Exchange

(Trillion Yen) (Trillion Yen)

0

20

40

60

80

100

120

140

160

180

1980.3 85.3 90.3 95.3 2000.3 05.3 10.30

10

20

30

40

50

60

70

80

90

1980.3 85.3 90.3 95.3 2000.3 05.3 10.3

Tightened

Monitoring and

Governance

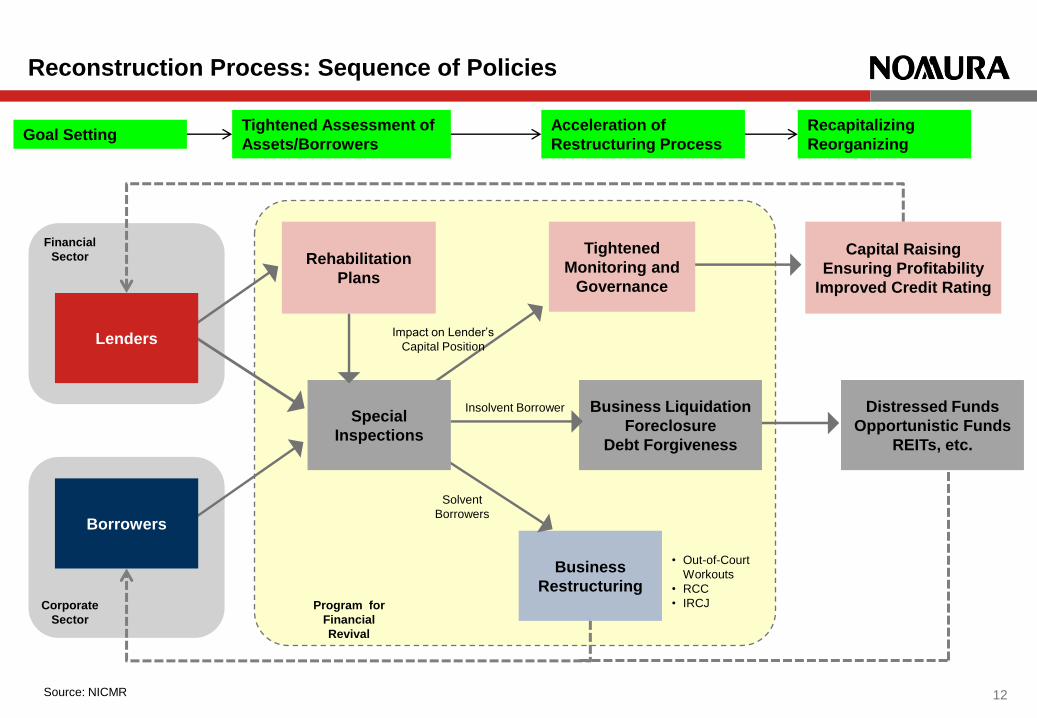

Reconstruction Process: Sequence of Policies

12

Goal Setting

Solvent

Borrowers Borrowers

Business

Restructuring

• Out-of-Court

Workouts

• RCC

• IRCJ

Source: NICMR

Business Liquidation

Foreclosure

Debt Forgiveness

Tightened Assessment of

Assets/Borrowers

Recapitalizing

Reorganizing

Capital Raising

Ensuring Profitability

Improved Credit Rating

Insolvent Borrower Distressed Funds

Opportunistic Funds

REITs, etc.

Acceleration of

Restructuring Process

Special

Inspections

Impact on Lender’s

Capital Position Lenders

Rehabilitation

Plans

Financial

Sector

Corporate

Sector

Program for

Financial

Revival

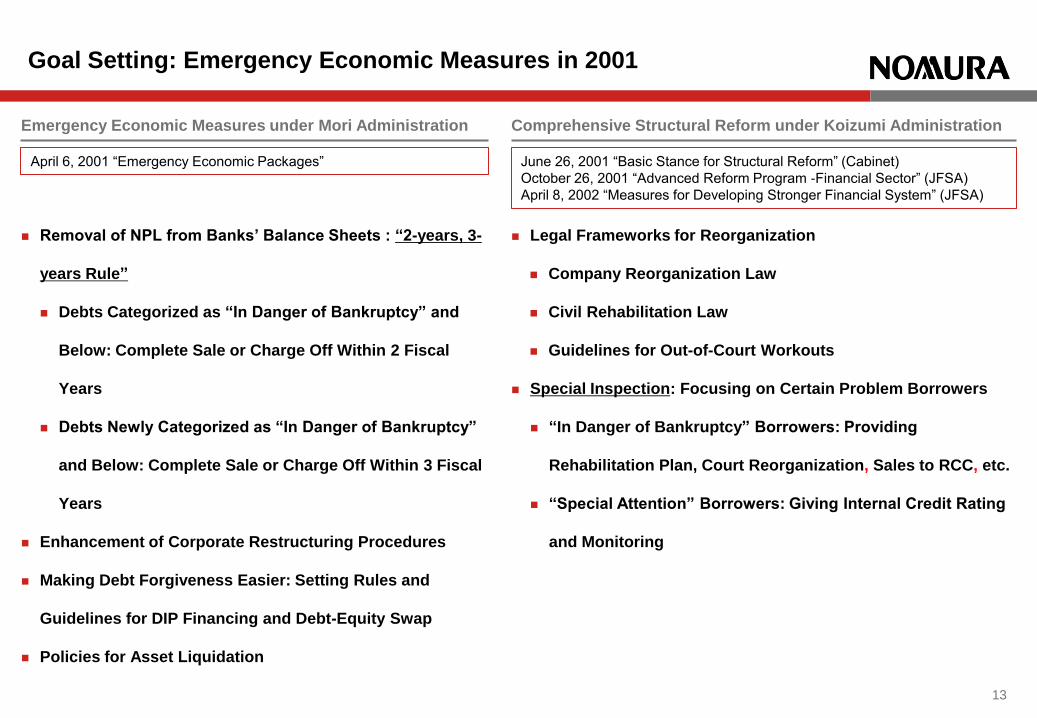

Removal of NPL from Banks’ Balance Sheets : “2-years, 3-

years Rule”

Debts Categorized as “In Danger of Bankruptcy” and

Below: Complete Sale or Charge Off Within 2 Fiscal

Years

Debts Newly Categorized as “In Danger of Bankruptcy”

and Below: Complete Sale or Charge Off Within 3 Fiscal

Years

Enhancement of Corporate Restructuring Procedures

Making Debt Forgiveness Easier: Setting Rules and

Guidelines for DIP Financing and Debt-Equity Swap

Policies for Asset Liquidation

Legal Frameworks for Reorganization

Company Reorganization Law

Civil Rehabilitation Law

Guidelines for Out-of-Court Workouts

Special Inspection: Focusing on Certain Problem Borrowers

“In Danger of Bankruptcy” Borrowers: Providing

Rehabilitation Plan, Court Reorganization, Sales to RCC, etc.

“Special Attention” Borrowers: Giving Internal Credit Rating

and Monitoring

Goal Setting: Emergency Economic Measures in 2001

Emergency Economic Measures under Mori Administration Comprehensive Structural Reform under Koizumi Administration

13

April 6, 2001 “Emergency Economic Packages” June 26, 2001 “Basic Stance for Structural Reform” (Cabinet)

October 26, 2001 “Advanced Reform Program -Financial Sector” (JFSA)

April 8, 2002 “Measures for Developing Stronger Financial System” (JFSA)

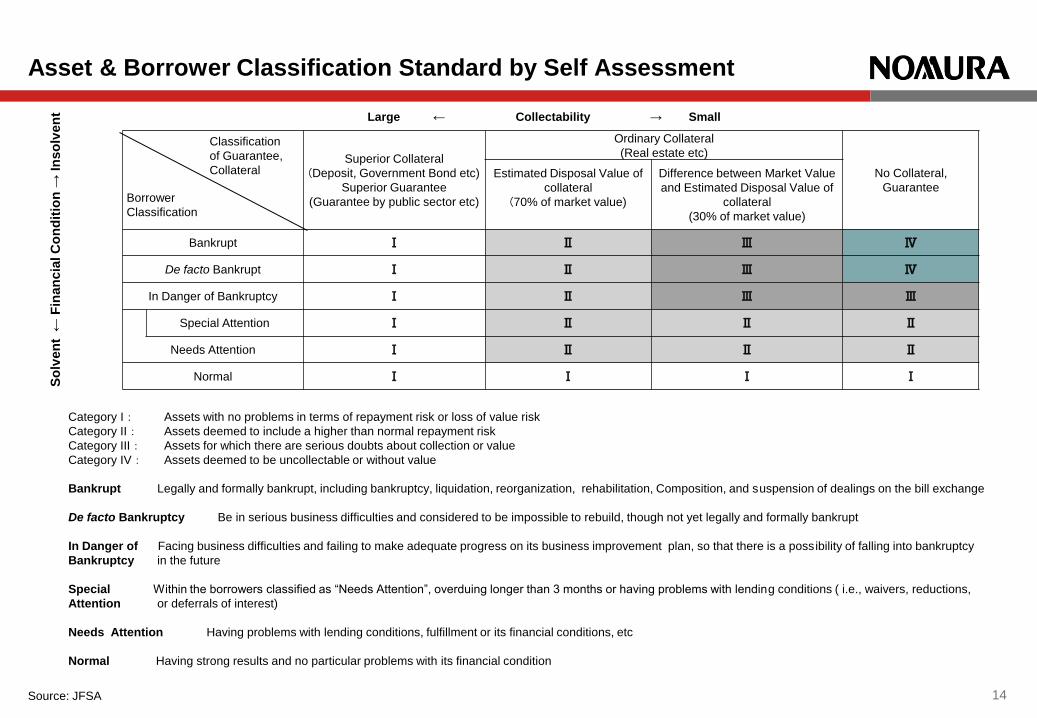

Superior Collateral

(Deposit, Government Bond etc)

Superior Guarantee

(Guarantee by public sector etc)

Ordinary Collateral

(Real estate etc)

No Collateral,

Guarantee

Estimated Disposal Value of

collateral

(70% of market value)

Difference between Market Value

and Estimated Disposal Value of

collateral

(30% of market value)

Bankrupt Ⅰ Ⅱ Ⅲ Ⅳ

De facto Bankrupt Ⅰ Ⅱ Ⅲ Ⅳ

In Danger of Bankruptcy Ⅰ Ⅱ Ⅲ Ⅲ

Special Attention Ⅰ Ⅱ Ⅱ Ⅱ

Needs Attention Ⅰ Ⅱ Ⅱ Ⅱ

Normal Ⅰ Ⅰ Ⅰ Ⅰ

Asset & Borrower Classification Standard by Self Assessment

14

Borrower

Classification

Classification

of Guarantee,

Collateral

So

lven

t ←

Fin

an

cia

l C

on

dit

ion

→ In

so

lven

t Large ← Collectability → Small

Category I: Assets with no problems in terms of repayment risk or loss of value risk

Category II: Assets deemed to include a higher than normal repayment risk

Category III: Assets for which there are serious doubts about collection or value

Category IV: Assets deemed to be uncollectable or without value

Bankrupt Legally and formally bankrupt, including bankruptcy, liquidation, reorganization, rehabilitation, Composition, and suspension of dealings on the bill exchange

De facto Bankruptcy Be in serious business difficulties and considered to be impossible to rebuild, though not yet legally and formally bankrupt

In Danger of Facing business difficulties and failing to make adequate progress on its business improvement plan, so that there is a possibility of falling into bankruptcy

Bankruptcy in the future

Special Within the borrowers classified as “Needs Attention”, overduing longer than 3 months or having problems with lending conditions ( i.e., waivers, reductions,

Attention or deferrals of interest)

Needs Attention Having problems with lending conditions, fulfillment or its financial conditions, etc

Normal Having strong results and no particular problems with its financial condition

Source: JFSA

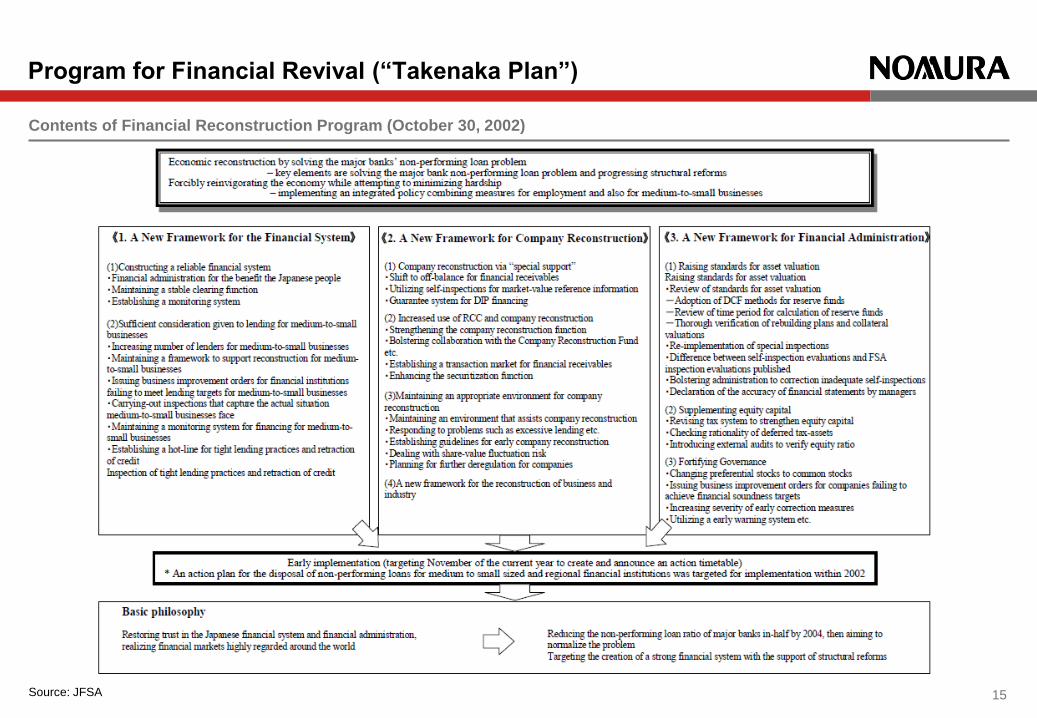

Program for Financial Revival (“Takenaka Plan”)

15 Source: JFSA

Contents of Financial Reconstruction Program (October 30, 2002)

16

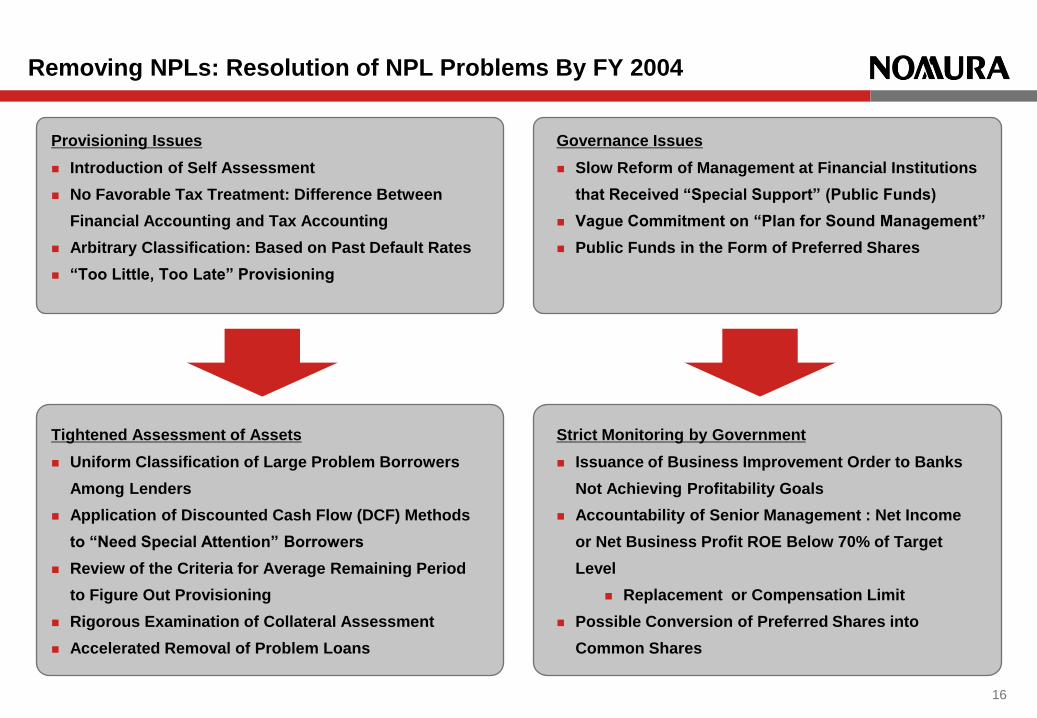

Removing NPLs: Resolution of NPL Problems By FY 2004

Governance Issues

Slow Reform of Management at Financial Institutions

that Received “Special Support” (Public Funds)

Vague Commitment on “Plan for Sound Management”

Public Funds in the Form of Preferred Shares

Strict Monitoring by Government

Issuance of Business Improvement Order to Banks

Not Achieving Profitability Goals

Accountability of Senior Management : Net Income

or Net Business Profit ROE Below 70% of Target

Level

Replacement or Compensation Limit

Possible Conversion of Preferred Shares into

Common Shares

Provisioning Issues

Introduction of Self Assessment

No Favorable Tax Treatment: Difference Between

Financial Accounting and Tax Accounting

Arbitrary Classification: Based on Past Default Rates

“Too Little, Too Late” Provisioning

Tightened Assessment of Assets

Uniform Classification of Large Problem Borrowers

Among Lenders

Application of Discounted Cash Flow (DCF) Methods

to “Need Special Attention” Borrowers

Review of the Criteria for Average Remaining Period

to Figure Out Provisioning

Rigorous Examination of Collateral Assessment

Accelerated Removal of Problem Loans

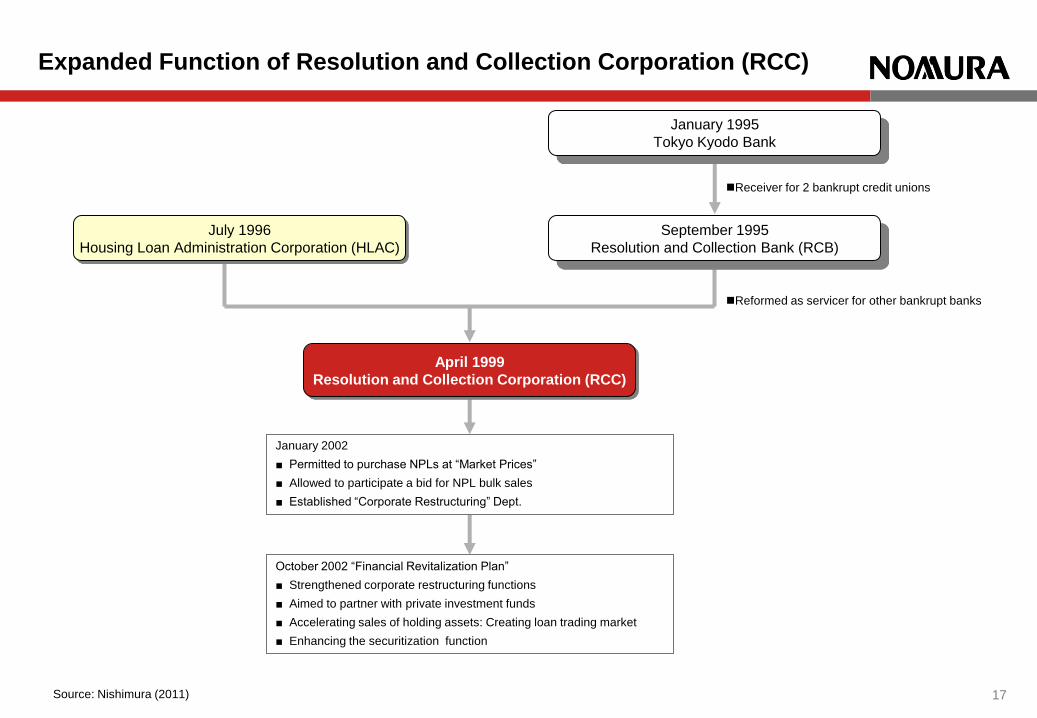

Expanded Function of Resolution and Collection Corporation (RCC)

Receiver for 2 bankrupt credit unions

September 1995

Resolution and Collection Bank (RCB)

April 1999

Resolution and Collection Corporation (RCC)

January 2002

■ Permitted to purchase NPLs at “Market Prices”

■ Allowed to participate a bid for NPL bulk sales

■ Established “Corporate Restructuring” Dept.

Source: Nishimura (2011) 17

January 1995

Tokyo Kyodo Bank

Reformed as servicer for other bankrupt banks

July 1996

Housing Loan Administration Corporation (HLAC)

October 2002 “Financial Revitalization Plan”

■ Strengthened corporate restructuring functions

■ Aimed to partner with private investment funds

■ Accelerating sales of holding assets: Creating loan trading market

■ Enhancing the securitization function

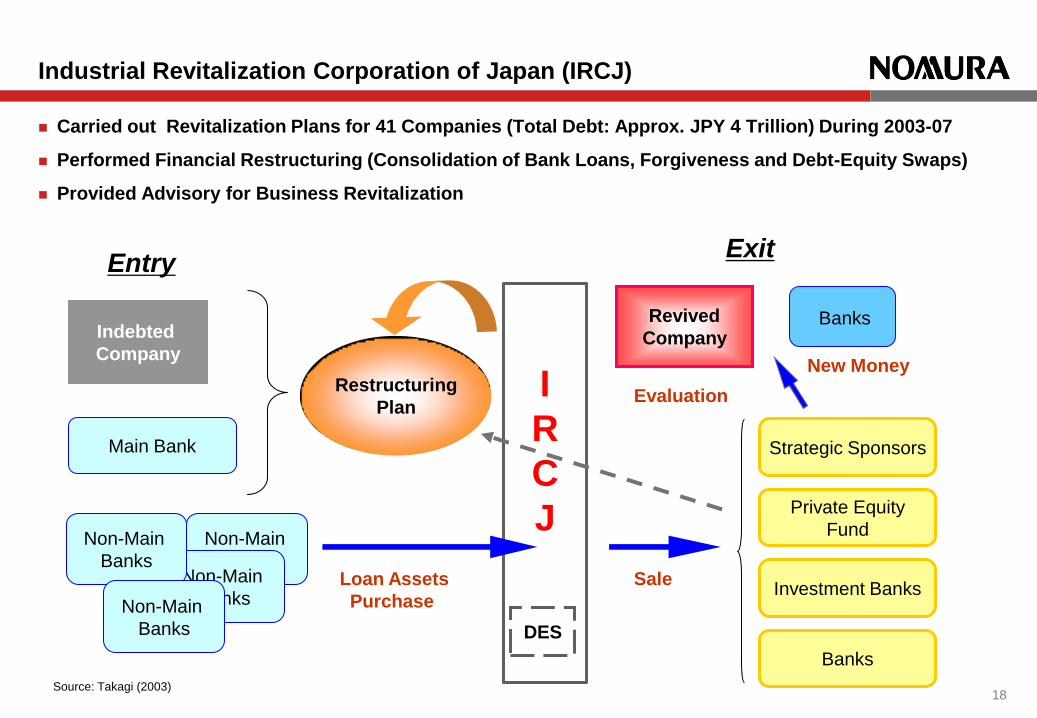

Industrial Revitalization Corporation of Japan (IRCJ)

18

Carried out Revitalization Plans for 41 Companies (Total Debt: Approx. JPY 4 Trillion) During 2003-07

Performed Financial Restructuring (Consolidation of Bank Loans, Forgiveness and Debt-Equity Swaps)

Provided Advisory for Business Revitalization

Non-Main

Banks Non-Main

Banks

I

R

C

J

Entry Exit

Indebted

Company

Main Bank

Non-Main

Banks

Restructuring

Plan

Revived

Company

Loan Assets

Purchase

Sale

DES

Evaluation

Banks

New Money

Private Equity

Fund

Investment Banks

Strategic Sponsors

Non-Main

Banks

Banks

Source: Takagi (2003)

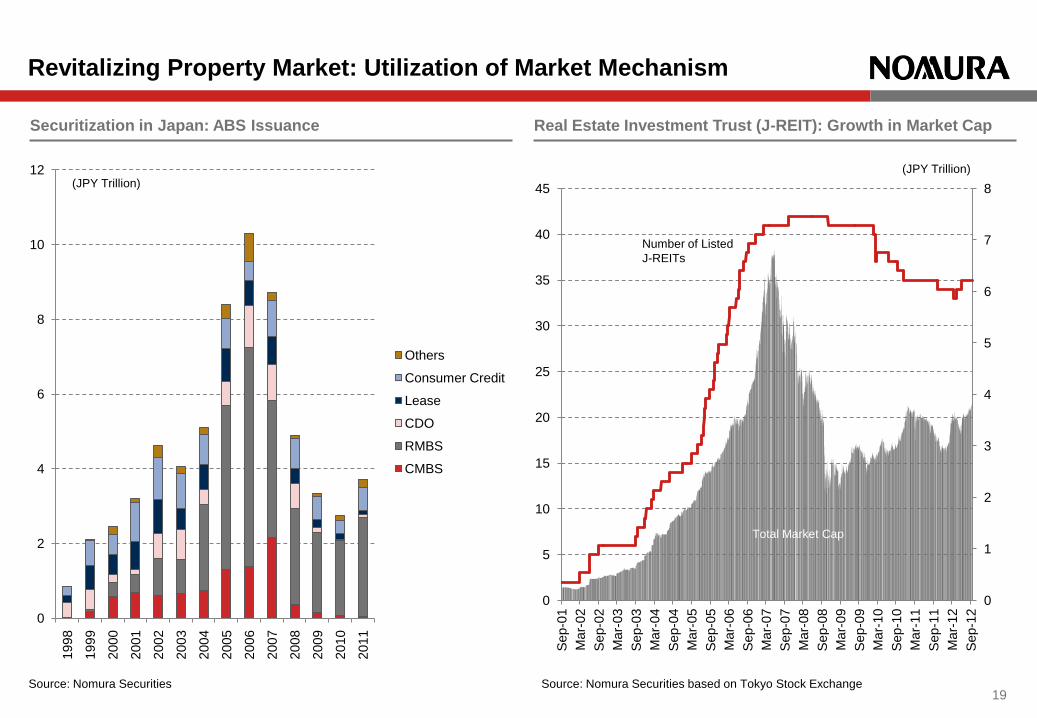

Revitalizing Property Market: Utilization of Market Mechanism

Source: Nomura Securities 19

Securitization in Japan: ABS Issuance Real Estate Investment Trust (J-REIT): Growth in Market Cap

Source: Nomura Securities based on Tokyo Stock Exchange

0

2

4

6

8

10

12

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Others

Consumer Credit

Lease

CDO

RMBS

CMBS

(JPY Trillion)

0

1

2

3

4

5

6

7

8

0

5

10

15

20

25

30

35

40

45

Sep-0

1

Mar-

02

Sep-0

2

Mar-

03

Sep-0

3

Mar-

04

Sep-0

4

Mar-

05

Sep-0

5

Mar-

06

Sep-0

6

Mar-

07

Sep-0

7

Mar-

08

Sep-0

8

Mar-

09

Sep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

Sep-1

2

Number of Listed

J-REITs

Total Market Cap

(JPY Trillion)

Source: NICMR based on Japanese Bankers Association

Change in Capital Positions of Major Japanese Banks

Heterogeneity of Major Banks’ Responses to NPL Problems

20

0

3

6

9

12

15

0 3 6 9 12 150

3

6

9

12

15

0 3 6 9 12 15

0

3

6

9

12

15

0 3 6 9 12 15

0

3

6

9

12

15

0 3 6 9 12 15

0

3

6

9

12

15

0 3 6 9 12 15

2000.3 2001.3 2002.3

2004.3 2003.3

(NPL/Total assets, %) (NPL/Total assets, %) (NPL/Total assets, %)

(NPL/Total assets, %) (NPL/Total assets, %)

(Capital ratio, %) (Capital ratio, %) (Capital ratio, %)

(Capital ratio, %) (Capital ratio, %)

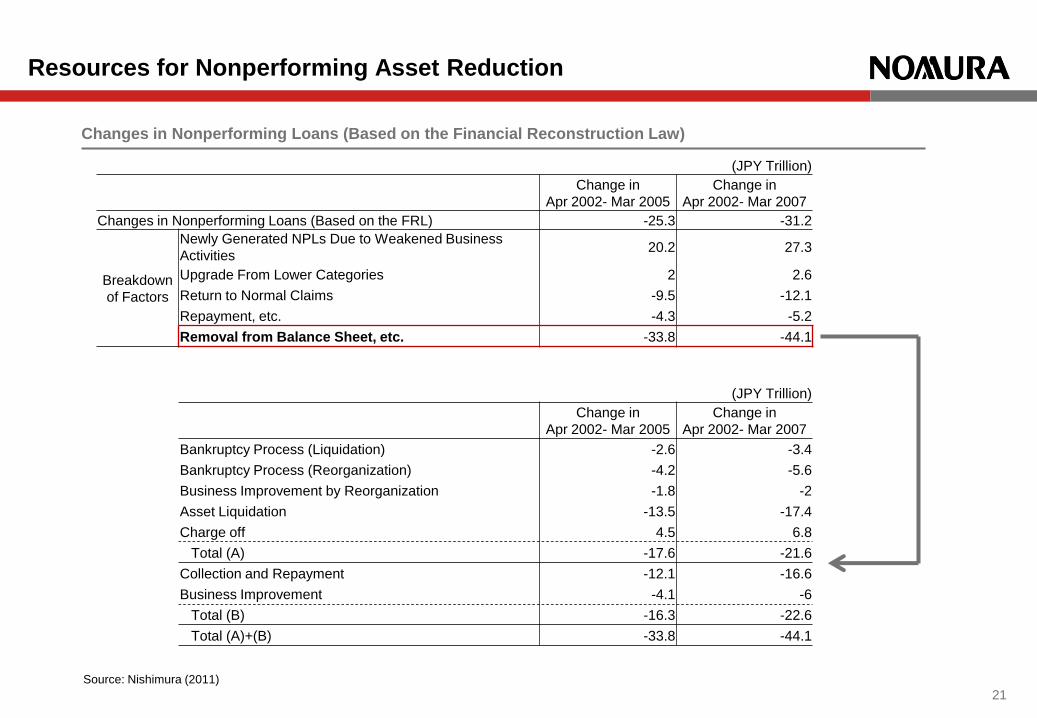

Changes in Nonperforming Loans (Based on the Financial Reconstruction Law)

Resources for Nonperforming Asset Reduction

21

(JPY Trillion)

Change in

Apr 2002- Mar 2005

Change in

Apr 2002- Mar 2007

Changes in Nonperforming Loans (Based on the FRL) -25.3 -31.2

Breakdown

of Factors

Newly Generated NPLs Due to Weakened Business

Activities 20.2 27.3

Upgrade From Lower Categories 2 2.6

Return to Normal Claims -9.5 -12.1

Repayment, etc. -4.3 -5.2

Removal from Balance Sheet, etc. -33.8 -44.1

(JPY Trillion)

Change in

Apr 2002- Mar 2005

Change in

Apr 2002- Mar 2007

Bankruptcy Process (Liquidation) -2.6 -3.4

Bankruptcy Process (Reorganization) -4.2 -5.6

Business Improvement by Reorganization -1.8 -2

Asset Liquidation -13.5 -17.4

Charge off 4.5 6.8

Total (A) -17.6 -21.6

Collection and Repayment -12.1 -16.6

Business Improvement -4.1 -6

Total (B) -16.3 -22.6

Total (A)+(B) -33.8 -44.1

Source: Nishimura (2011)

Consideration for Financial Stability During 2001-2005

22

Depository Institution Resolutions in Japan

Year Bank Shinkin Bank

(Credit

Association)

Credit Union Total

1991 1 0 0 1

1992 0 1 0 1

1993 0 1 1 2

1994 0 0 4 4

1995 2 0 4 6

1996 1 0 4 5

1997 3 0 14 17

1998 5 0 25 30

1999 5 10 29 44

2000 0 2 12 14

2001 2 13 41 56

2002 0 0 0 0

2003 1 0 0 1

2004 0 0 0 0

2005 0 0 0 0

Introduction of Deposit Protection Limits

Partially in Force in April 2002

Protection Limits on Savings Account:

Effective until April 2005 (initially scheduled to

end in April 2003, extended on October 8,

2002)

Resona Bank

Ashikaga Bank

Source: NICMR based on Deposit Insurance Corporation of Japan

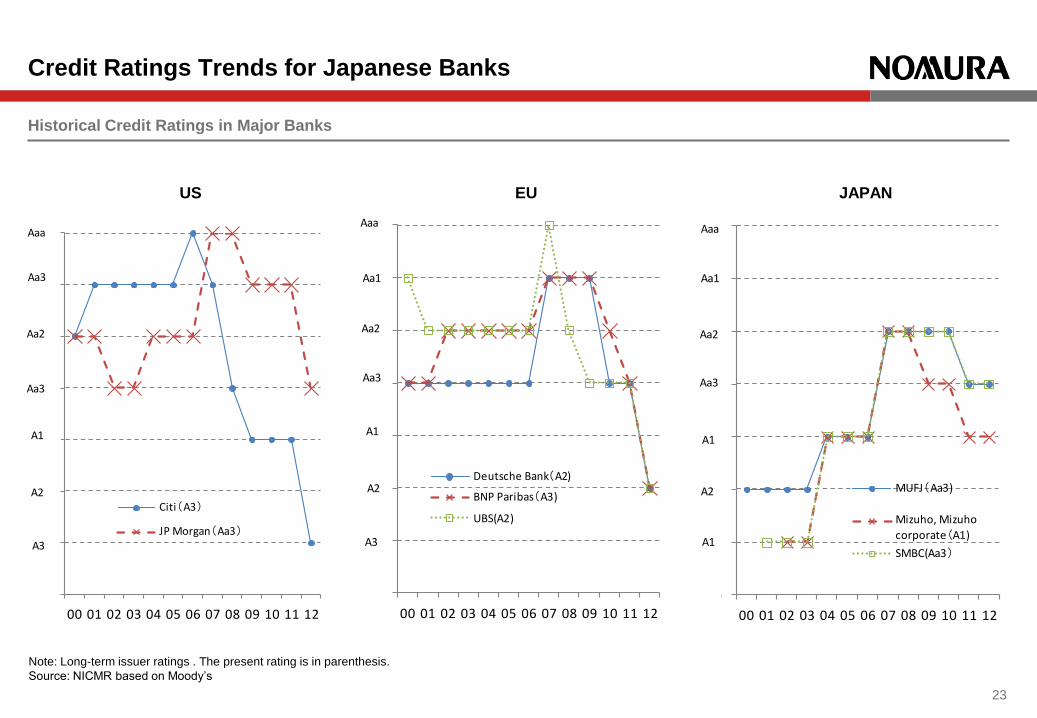

Historical Credit Ratings in Major Banks

Credit Ratings Trends for Japanese Banks

Note: Long-term issuer ratings . The present rating is in parenthesis.

Source: NICMR based on Moody’s

23

0

5

10

15

20

25

30

35

00 01 02 03 04 05 06 07 08 09 10 11 12

Deutsche Bank(A2)

BNP Paribas(A3)

UBS(A2)

Aaa

Aa1

Aa3

Aa2

A1

A2

A3

0

5

10

15

20

25

30

35

00 01 02 03 04 05 06 07 08 09 10 11 12

MUFJ(Aa3)

Mizuho, Mizuho

corporate(A1)

SMBC(Aa3)

Aaa

Aa1

Aa2

Aa3

A1

A2

A1

0

5

10

15

20

25

30

35

00 01 02 03 04 05 06 07 08 09 10 11 12

Citi(A3)

JP Morgan(Aa3)

Aaa

Aa1

A1

A2

A3

Aa3

Aa2

Aa3

US EU JAPAN

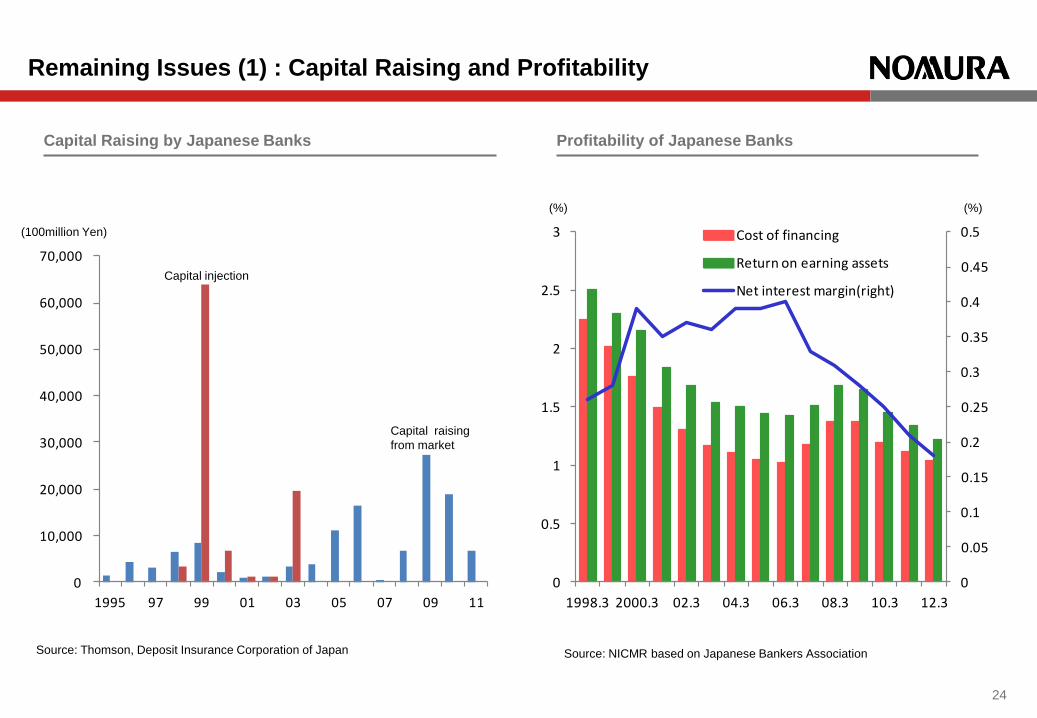

Remaining Issues (1) : Capital Raising and Profitability

Source: Thomson, Deposit Insurance Corporation of Japan

24

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0

0.5

1

1.5

2

2.5

3

1998.3 2000.3 02.3 04.3 06.3 08.3 10.3 12.3

Cost of financing

Return on earning assets

Net interest margin(right)

(%) (%)

Source: NICMR based on Japanese Bankers Association

(100million Yen)

Capital Raising by Japanese Banks Profitability of Japanese Banks

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1995 97 99 01 03 05 07 09 11

Capital injection

Capital raising

from market

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

300

350

400

450

500

550

600

650

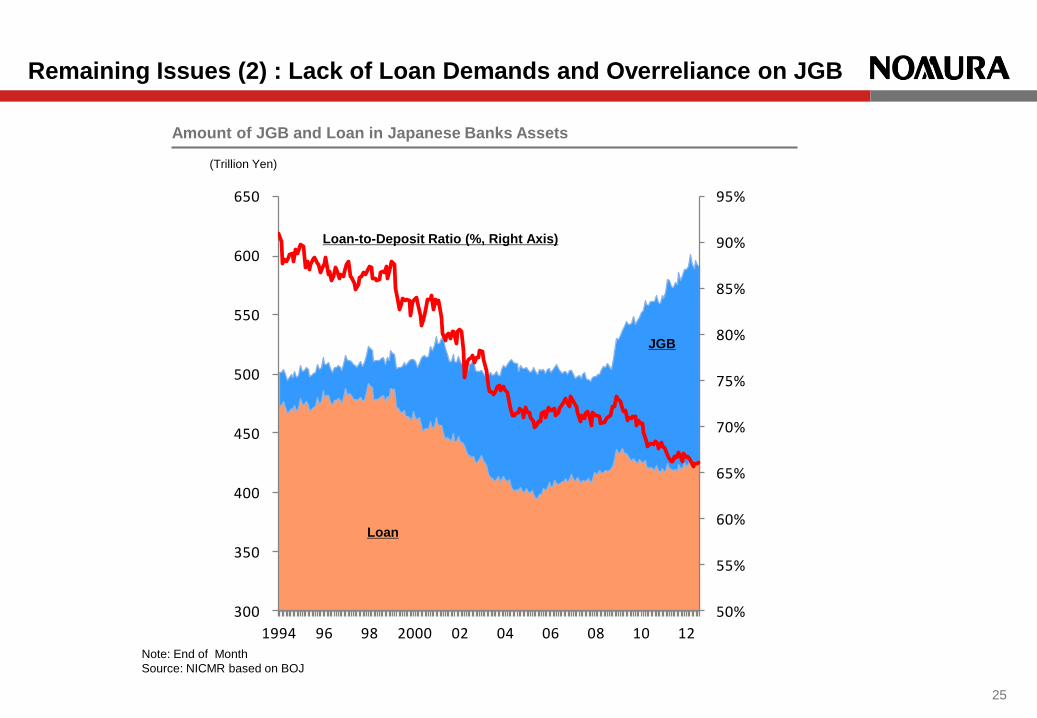

1994 96 98 2000 02 04 06 08 10 12

Amount of JGB and Loan in Japanese Banks Assets

Remaining Issues (2) : Lack of Loan Demands and Overreliance on JGB

25

Note: End of Month

Source: NICMR based on BOJ

(Trillion Yen)

Loan-to-Deposit Ratio (%, Right Axis)

Loan

JGB

26

Removal of Bad Assets: Speedy Policy Implementation by Political Leadership

“Convoy System” to “Segregation Policy”

Sequence of Policies: Appropriate Timing of Capital Raising?

Consideration for Borrowers: “Simultaneous” Reconstruction Needed?

Use of Market Mechanism: Benefit of Securitization

Implications for Asian Countries

Lessons from Japanese Experience

27

Financial Services Agency (2001) “The Advanced Reform Program –Financial Sector-”, October 26 2001

(http://www.fsa.go.jp/news/newse/e20011026-1.html)

Financial Services Agency (2002a) “Measures for Developing Stronger Financial System”, April 12 2002

(http://www.fsa.go.jp/news/newse/e20011026-1.html)

Financial Services Agency (2002b) “”Program for Financial Revival -Revival of the Japanese Economy through Resolving Non-

Performing Loans”, October 30 2002 (http://www.fsa.go.jp/news/newse/e20021030.pdf)

Kinoshita, Nobuyuki (2011) “Kin’yu Gyosei no Genjitsu to Riron (Facts and Theories of Financial Administration Policies)”, Kinzai

Institute for Financial Affairs (in Japanese)

Nishimura, Yoshimasa (2011) “Kin’yuu Sisutemu Kaikaku Gojunen no Kiseki (50 Years of Financial System Reform)”, Kinzai Institute

for Financial Affairs (in Japanese)

Okina, Yuri (2009) “Activity of IRCJ and Banking Crisis in Japan”, Public Policy Review, Vol. 5, No. 2, Policy Research Institute,

Ministry of Finance, November 2009

Omura, Keiichi and Shinji Mizukami (2007) “Kin’yu Saisei: Kiki no Honshitsu (Financial Reconstruction: Essence of the Crisis)”, Nikkei

Book (in Japanese)

Takagi, Shinjiro (2003a) “Maximizing Value of Non-Performing Assets”, Paper for Forum for Asian Insolvency Reform, November

2003

Takagi, Shinjiro (2003b) “Industrial Revitalization Corporation of Japan”, Presentation on Forum for Asian Insolvency Reform,

November 2003

References