Embed Size (px)

Citation preview

October 1999

Industry Structure and Competitiveness

REFINED CANE SUGAR INDUSTRY

Introduction

Refined sugar is sugar in granular/crystalline form, primarily composed of sucrose, and

obtained mainly from sugar cane and sugar beets.

There are three (3) major grades of refined cane sugar: (1) standard refined, which is

used primarily as table sugar; (2) premium sugar, which is used by food manufacturers;

and (3) bottlers grade sugar, which is used by the beverage industry.

The manufacturing process for refined cane sugar may be broken down into the

following phases:

➲ Raw sugar process

➲ Affination (washing-off of molasses film from crystals)

➲ Melting

➲ Clarification (removal of insoluble/suspended impurities, gums, pectins,

colloids)

➲ Vacuum filtration (removal of remaining fine particles)

➲ Decolorization (removal of colorants)

2

➲ Boiling/Crystallization

➲ Drying

Refined cane sugar serves as a major input to processed food manufacturing,

particularly in the production of sugar confectioneries, sugar preparations, pastry,

cakes, biscuits and other baker’s wares, preserved fruits and nuts, and beverages.

The objective of the study is to analyze the state of competition within the refined cane

sugar industry and how competition can help develop the refined cane sugar industry

into a viable industry as a potential major input to processed food manufacturing. An

analytical framework specially developed for this purpose will be utilized and

recommendations made, if necessary, on how to make the sector competitive or

improve its competitiveness. It is hypothesized that to improve the input sectors of the

Philippine export industry (such as refined cane sugar) will translate into

competitiveness or better competitiveness of Philippine exports.

Competition and Competitiveness Analysis

I Defining the Relevant Market A relevant market is defined as, “… a product or group of products and a geographical

area in which it is produced or sold such that a hypothetical profit-maximizing firm, not

subject to price regulation, that was the only present and future producer or seller of

those products in that area likely would impose at least a ‘small but significant and

nontransitory’ increase in price, assuming the terms of sale of all other products are

3

held constant. A relevant market is a group of products and a geographic area that is

no bigger than necessary to satisfy this test1”.

Simply put, a relevant market is defined by the product or service involved, the

geographical area in which said product or service is sold, and the sellers and buyers of

such product or service.

! Product Market

The relevant product market is defined as domestic refined cane

sugar.

In defining the relevant product market, the approach followed is: assuming a

hypothetical monopolist for a product, would said monopolist profit by imposing at

least a small but significant and non-transitory increase in price?

Restrictions currently exist on the importation of refined sugar. Given these

restrictions, food processors and beverage makers do not have the option to

switch to imported refined sugar assuming the existence of a hypothetical sugar

monopolist who imposes a price increase. The relevant product market is then

clearly defined – domestic refined cane sugar.

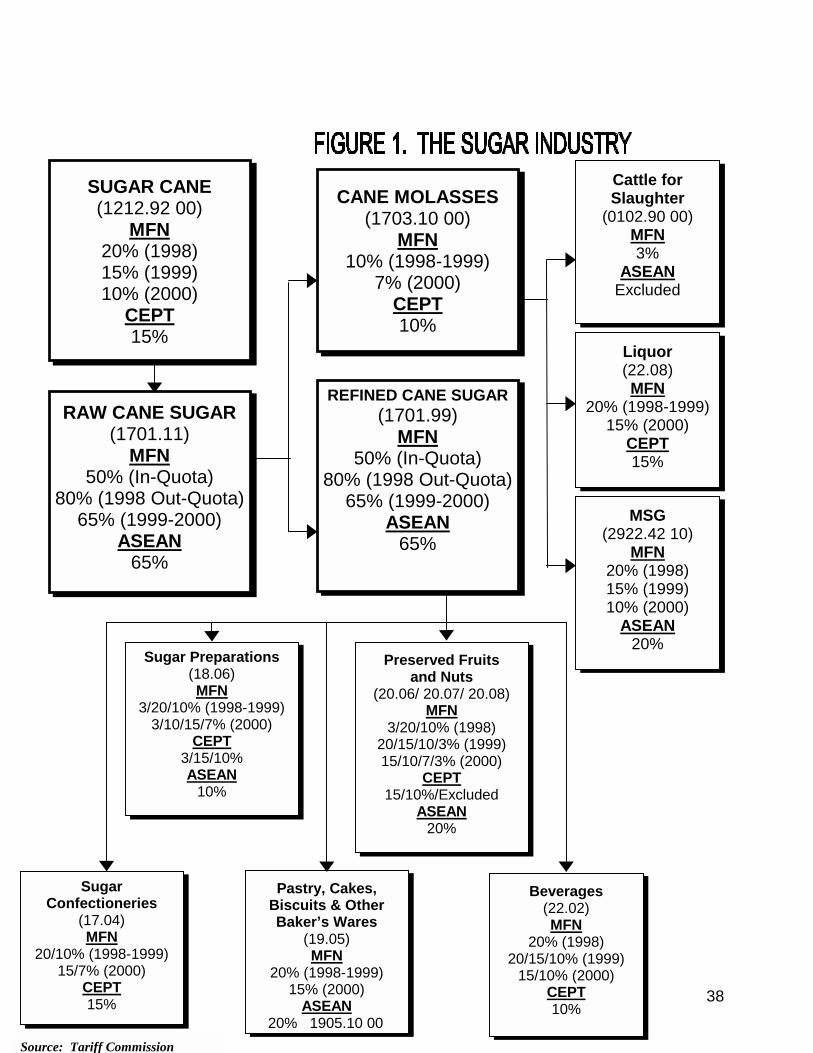

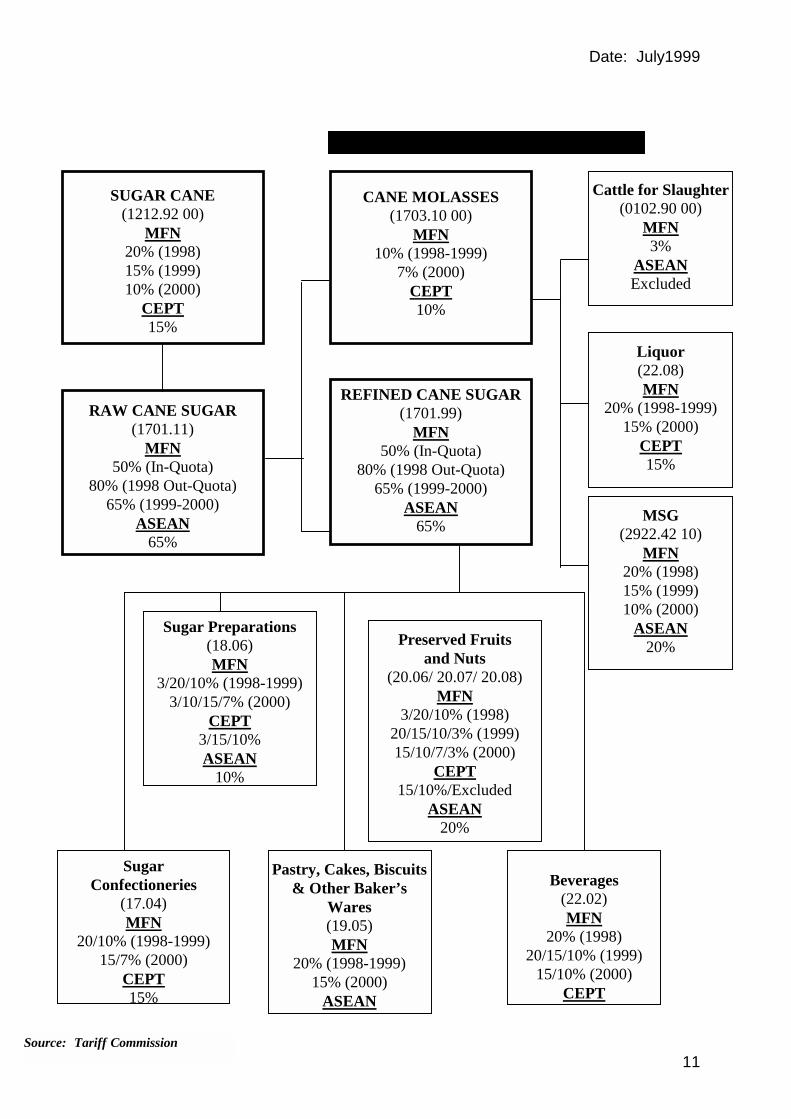

Figure 1 depicts the flow of commodities from the sugar industry to user

industries. Sugar cane goes into the production of raw cane sugar which, in

turn, is transformed into either cane molasses or refined cane sugar. As

previously mentioned, refined cane sugar is an input to the production of sugar

confectioneries, sugar preparations, pastry, cakes, biscuits and other baker’s

wares, preserved fruits and nuts, and beverages.

1 As defined by Section 1 of the U.S. Department of Justice and Federal Trade Commission Horizontal

Merger Guidelines dated 2 April 1992.

4

! Geographical Market

The geographical market for domestic refined cane sugar is defined

as the Philippine national territory.

The relevant geographical market is defined similarly as the product market. It is

the region where a hypothetical monopolist, being the only present or future

producer of the product, could make a profit from imposing at least a small but

significant and non-transitory price increase holding the terms of sale constant at

all other locations. The difficulty in determining the geographical market is made

more complicated with the increasing globalization of markets and the use of

electronic trade (e.g. through the Internet).

Considering, however, that local food processors and beverage makers are

effectively restricted to purchasing their sugar requirements from domestic

producers, the relevant geographical market for domestic refined cane sugar is

defined as the Philippine national territory, for purposes of this study.

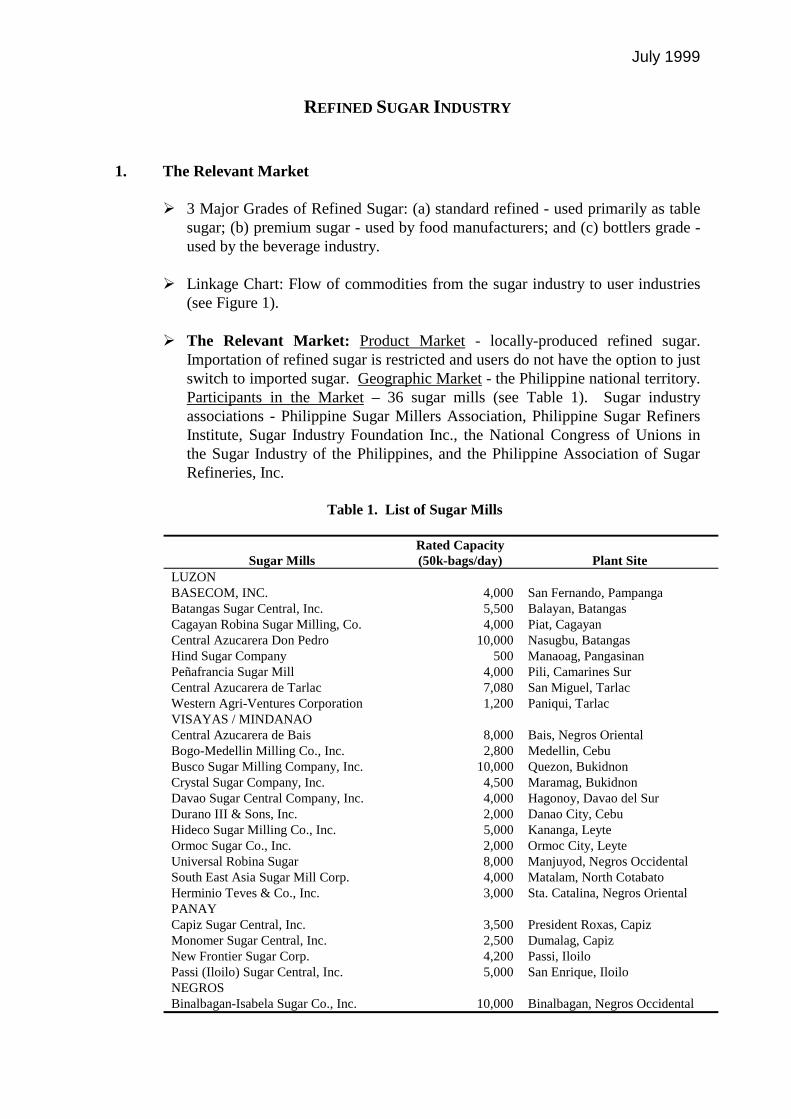

! Participants in the Market

The relevant participants in the market are the sixteen (16) cane sugar

mills and refineries with the highest revenues.

As of crop year 1998 - 1999, the total number of Philippine sugar mills was thirty

six (36) (see Table 1).

The sugar milling industry has a rated plant capacity of 185,000 tonnes of cane

per day or a daily utilization rate of 53%. The refiners’ actual capacity is 5,200

5

tonnes per day while rated capacity is 7,050 tonnes per day, so capacity

utilization is around 74%.2

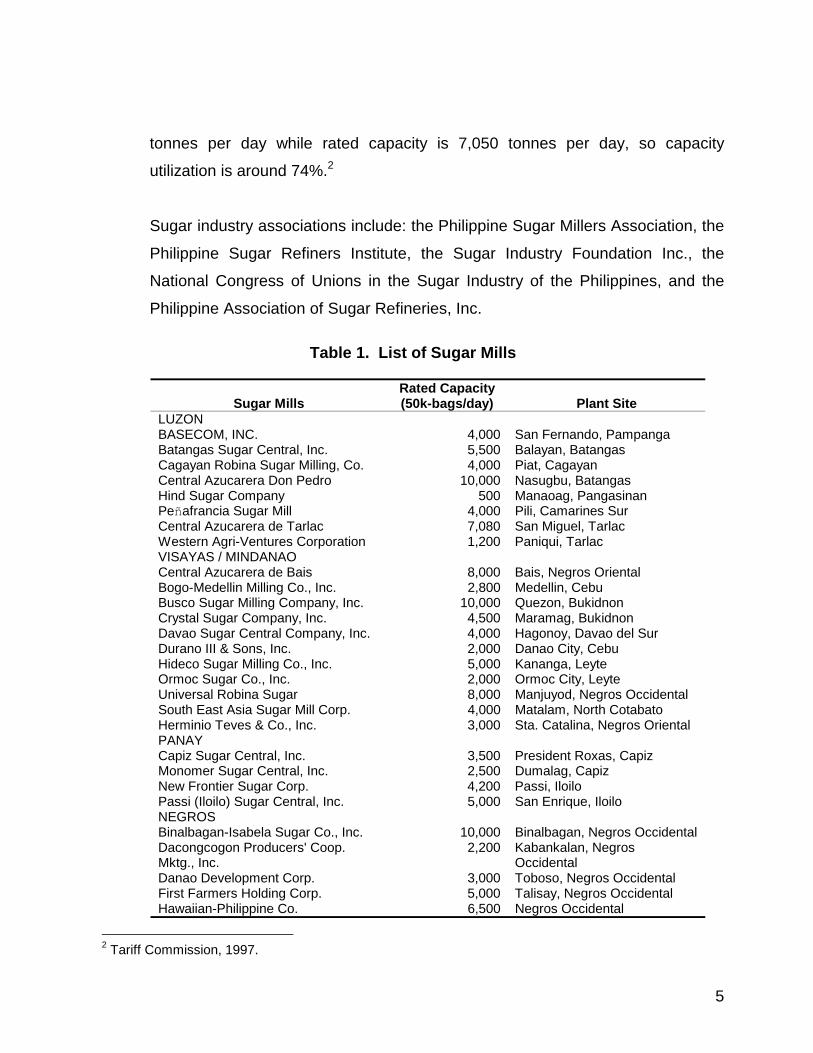

Sugar industry associations include: the Philippine Sugar Millers Association, the

Philippine Sugar Refiners Institute, the Sugar Industry Foundation Inc., the

National Congress of Unions in the Sugar Industry of the Philippines, and the

Philippine Association of Sugar Refineries, Inc.

Table 1. List of Sugar Mills

Sugar Mills

Rated Capacity (50k-bags/day)

Plant Site

LUZON BASECOM, INC. 4,000 San Fernando, Pampanga Batangas Sugar Central, Inc. 5,500 Balayan, Batangas Cagayan Robina Sugar Milling, Co. 4,000 Piat, Cagayan Central Azucarera Don Pedro 10,000 Nasugbu, Batangas Hind Sugar Company 500 Manaoag, Pangasinan Peñafrancia Sugar Mill 4,000 Pili, Camarines Sur Central Azucarera de Tarlac 7,080 San Miguel, Tarlac Western Agri-Ventures Corporation 1,200 Paniqui, Tarlac VISAYAS / MINDANAO Central Azucarera de Bais 8,000 Bais, Negros Oriental Bogo-Medellin Milling Co., Inc. 2,800 Medellin, Cebu Busco Sugar Milling Company, Inc. 10,000 Quezon, Bukidnon Crystal Sugar Company, Inc. 4,500 Maramag, Bukidnon Davao Sugar Central Company, Inc. 4,000 Hagonoy, Davao del Sur Durano III & Sons, Inc. 2,000 Danao City, Cebu Hideco Sugar Milling Co., Inc. 5,000 Kananga, Leyte Ormoc Sugar Co., Inc. 2,000 Ormoc City, Leyte Universal Robina Sugar 8,000 Manjuyod, Negros Occidental South East Asia Sugar Mill Corp. 4,000 Matalam, North Cotabato Herminio Teves & Co., Inc. 3,000 Sta. Catalina, Negros Oriental PANAY Capiz Sugar Central, Inc. 3,500 President Roxas, Capiz Monomer Sugar Central, Inc. 2,500 Dumalag, Capiz New Frontier Sugar Corp. 4,200 Passi, Iloilo Passi (Iloilo) Sugar Central, Inc. 5,000 San Enrique, Iloilo NEGROS Binalbagan-Isabela Sugar Co., Inc. 10,000 Binalbagan, Negros Occidental Dacongcogon Producers' Coop. Mktg., Inc.

2,200 Kabankalan, Negros Occidental

Danao Development Corp. 3,000 Toboso, Negros Occidental First Farmers Holding Corp. 5,000 Talisay, Negros Occidental Hawaiian-Philippine Co. 6,500 Negros Occidental

2 Tariff Commission, 1997.

6

Central Azucarera de La Carlota 10,000 La Carlota City, Negros Occidental

Lopez Sugar Corp. 6,000 Sagay, Negros Occidental Ma-ao Sugar Central 5,000 Bago City, Negros Occidental Sagay Central, Inc. 3,000 Sagay, Negros Occidental San Carlos Milling Co., Inc. 4,800 San Carlos City, Negros

Occidental Southern Negros Development Corp. 4,000 Kabankalan, Negros

Occidental Sunnix Management Corp. 4,000 Silay City, Negros Occidental Victorias Milling Co. 12,000 Victorias, Negros Occidental

Source: Sugar Regulatory Administration

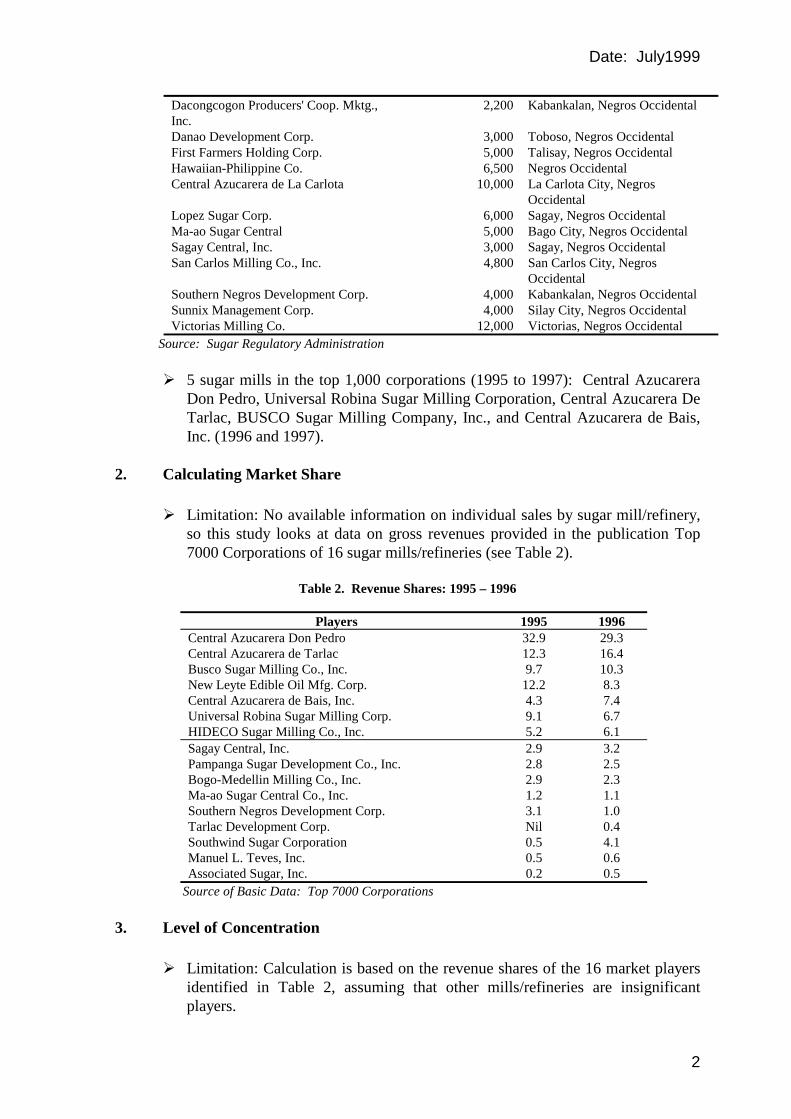

Five (5) sugar mills were included in the top 1,000 corporations from 1995 to

1997. These were: Central Azucarera Don Pedro, Universal Robina Sugar

Milling Corporation, Central Azucarera De Tarlac, BUSCO Sugar Milling

Company, Inc. and Central Azucarera de Bais, Inc. (in 1996 and 1997 only).

II Calculating Market Share

To determine the degree of competition within a market and the presence of market

dominance and abuse, the calculation of market shares is essential.

Ideally, market shares are computed based on sales that may be committed or so

profitably employed within the market. Sales are considered the best indicator of a

firm’s future competitive significance.

With no available information on individual sales by sugar mill/refinery, this study looks

at data on gross revenues provided in the publication Top 7000 Corporations. The

publication lists sixteen (16) sugar mills/refineries. The individual gross revenue shares

are shown below:

Table 2. Revenue Shares: 1995 – 1996

7

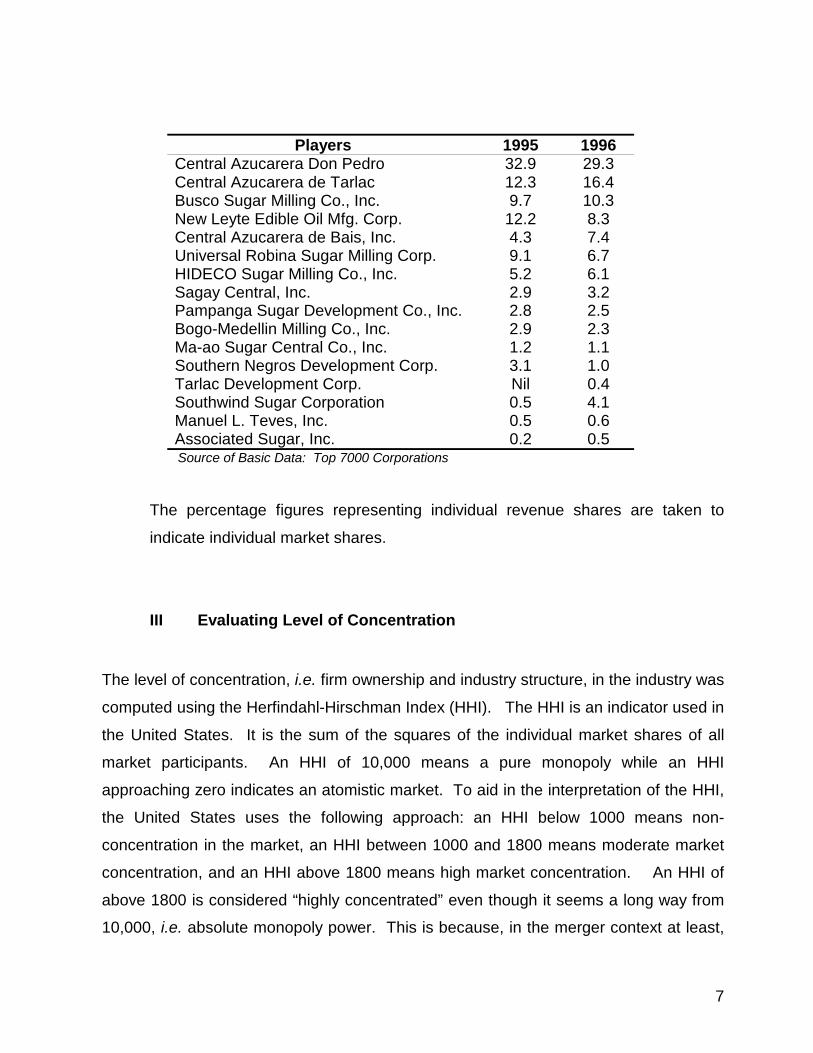

Players 1995 1996 Central Azucarera Don Pedro 32.9 29.3 Central Azucarera de Tarlac 12.3 16.4 Busco Sugar Milling Co., Inc. 9.7 10.3 New Leyte Edible Oil Mfg. Corp. 12.2 8.3 Central Azucarera de Bais, Inc. 4.3 7.4 Universal Robina Sugar Milling Corp. 9.1 6.7 HIDECO Sugar Milling Co., Inc. 5.2 6.1 Sagay Central, Inc. 2.9 3.2 Pampanga Sugar Development Co., Inc. 2.8 2.5 Bogo-Medellin Milling Co., Inc. 2.9 2.3 Ma-ao Sugar Central Co., Inc. 1.2 1.1 Southern Negros Development Corp. 3.1 1.0 Tarlac Development Corp. Nil 0.4 Southwind Sugar Corporation 0.5 4.1 Manuel L. Teves, Inc. 0.5 0.6 Associated Sugar, Inc. 0.2 0.5

Source of Basic Data: Top 7000 Corporations

The percentage figures representing individual revenue shares are taken to

indicate individual market shares.

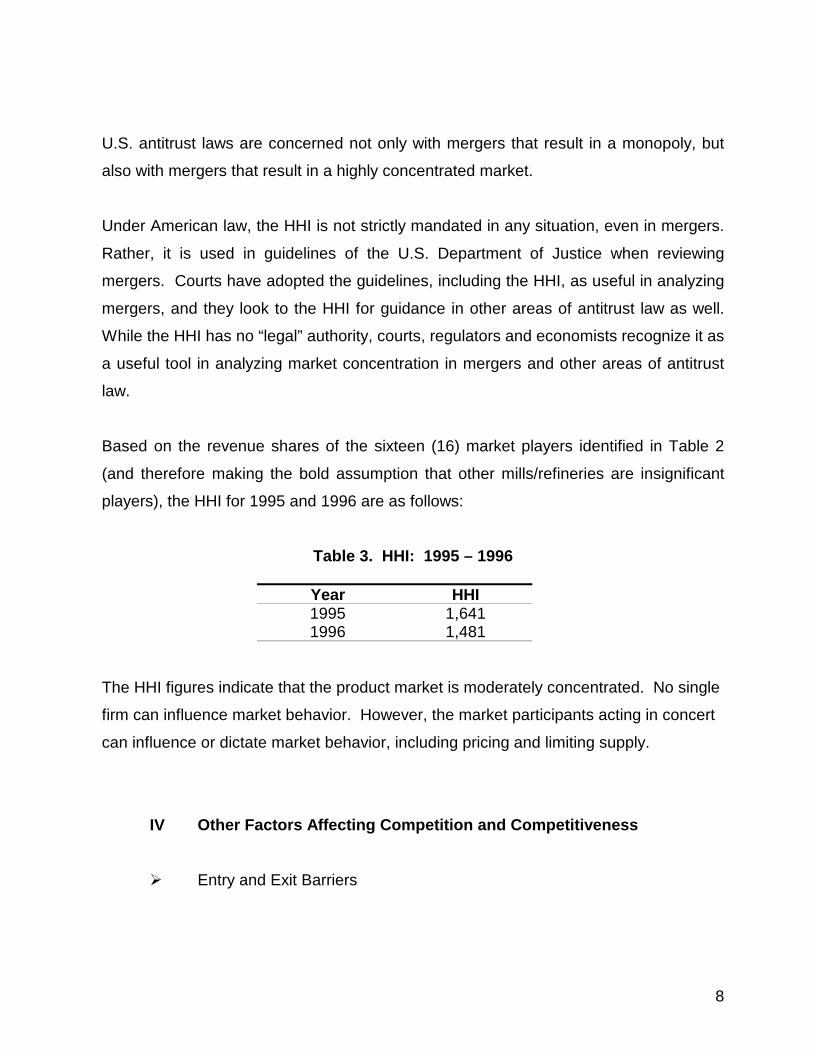

III Evaluating Level of Concentration

The level of concentration, i.e. firm ownership and industry structure, in the industry was

computed using the Herfindahl-Hirschman Index (HHI). The HHI is an indicator used in

the United States. It is the sum of the squares of the individual market shares of all

market participants. An HHI of 10,000 means a pure monopoly while an HHI

approaching zero indicates an atomistic market. To aid in the interpretation of the HHI,

the United States uses the following approach: an HHI below 1000 means non-

concentration in the market, an HHI between 1000 and 1800 means moderate market

concentration, and an HHI above 1800 means high market concentration. An HHI of

above 1800 is considered “highly concentrated” even though it seems a long way from

10,000, i.e. absolute monopoly power. This is because, in the merger context at least,

8

U.S. antitrust laws are concerned not only with mergers that result in a monopoly, but

also with mergers that result in a highly concentrated market.

Under American law, the HHI is not strictly mandated in any situation, even in mergers.

Rather, it is used in guidelines of the U.S. Department of Justice when reviewing

mergers. Courts have adopted the guidelines, including the HHI, as useful in analyzing

mergers, and they look to the HHI for guidance in other areas of antitrust law as well.

While the HHI has no “legal” authority, courts, regulators and economists recognize it as

a useful tool in analyzing market concentration in mergers and other areas of antitrust

law.

Based on the revenue shares of the sixteen (16) market players identified in Table 2

(and therefore making the bold assumption that other mills/refineries are insignificant

players), the HHI for 1995 and 1996 are as follows:

Table 3. HHI: 1995 – 1996

Year HHI 1995 1,641 1996 1,481

The HHI figures indicate that the product market is moderately concentrated. No single

firm can influence market behavior. However, the market participants acting in concert

can influence or dictate market behavior, including pricing and limiting supply.

IV Other Factors Affecting Competition and Competitiveness

! Entry and Exit Barriers

9

The attainment of greater competition in markets may be constrained by the

conditions of entry of new firms in said markets. Where entry is easy (i.e. the

market is contestable), the threat of potential entrants increases the competitive

pressure on incumbent firms. Incumbents are thus forced to become more

efficient and competitive, since failure to do so could mean the loss of market

share and power to new players. With easy entry, abuse of market power is

therefore unlikely and the efficiency benefits of competition are more easily

realized.

Where exit barriers exist, the release of unused or excess resources by failed

firms is made difficult. Attaining allocative efficiency is hindered.

Where entry or and/or exit barriers exist, however, the attainment of equilibrium

as close as possible to a case of perfect competition, becomes that much more

difficult.

In the domestic refined cane sugar industry, the conditions of entry and exit are

as follows:

(a) Investment Cost

According to the Sugar Regulatory Authority (SRA), there are no legal

barriers to entry, and exit, from the sugar industry.

However, both entry and exit would be difficult, entry in view of the heavy

investments required, and exit in view of the heavy investments, estimated

at P160 billion, already made. Around P80 billion has been spent on

sugar farms, P50 billion on mills, and P30 billion on refineries.

(b) Laws and Regulations

10

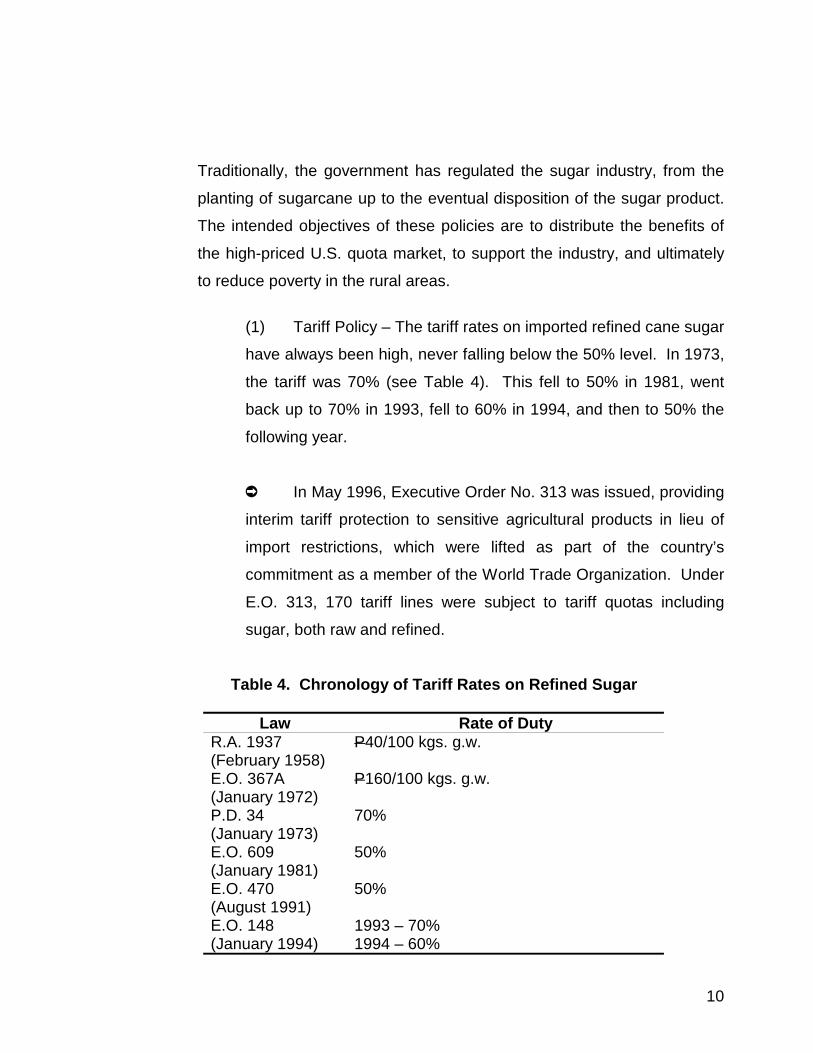

Traditionally, the government has regulated the sugar industry, from the

planting of sugarcane up to the eventual disposition of the sugar product.

The intended objectives of these policies are to distribute the benefits of

the high-priced U.S. quota market, to support the industry, and ultimately

to reduce poverty in the rural areas.

(1) Tariff Policy – The tariff rates on imported refined cane sugar

have always been high, never falling below the 50% level. In 1973,

the tariff was 70% (see Table 4). This fell to 50% in 1981, went

back up to 70% in 1993, fell to 60% in 1994, and then to 50% the

following year.

➲ In May 1996, Executive Order No. 313 was issued, providing

interim tariff protection to sensitive agricultural products in lieu of

import restrictions, which were lifted as part of the country’s

commitment as a member of the World Trade Organization. Under

E.O. 313, 170 tariff lines were subject to tariff quotas including

sugar, both raw and refined.

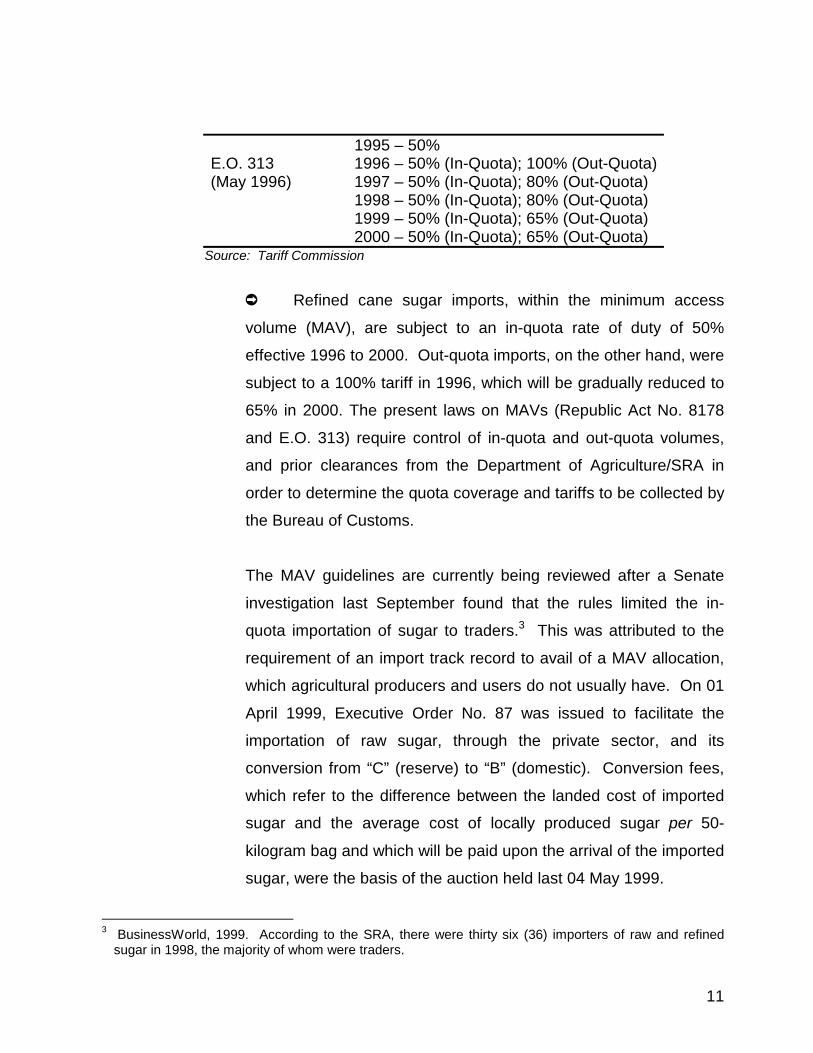

Table 4. Chronology of Tariff Rates on Refined Sugar

Law Rate of Duty R.A. 1937 (February 1958)

P40/100 kgs. g.w.

E.O. 367A (January 1972)

P160/100 kgs. g.w.

P.D. 34 (January 1973)

70%

E.O. 609 (January 1981)

50%

E.O. 470 (August 1991)

50%

E.O. 148 (January 1994)

1993 – 70% 1994 – 60%

11

1995 – 50% E.O. 313 (May 1996)

1996 – 50% (In-Quota); 100% (Out-Quota) 1997 – 50% (In-Quota); 80% (Out-Quota) 1998 – 50% (In-Quota); 80% (Out-Quota) 1999 – 50% (In-Quota); 65% (Out-Quota) 2000 – 50% (In-Quota); 65% (Out-Quota)

Source: Tariff Commission

➲ Refined cane sugar imports, within the minimum access

volume (MAV), are subject to an in-quota rate of duty of 50%

effective 1996 to 2000. Out-quota imports, on the other hand, were

subject to a 100% tariff in 1996, which will be gradually reduced to

65% in 2000. The present laws on MAVs (Republic Act No. 8178

and E.O. 313) require control of in-quota and out-quota volumes,

and prior clearances from the Department of Agriculture/SRA in

order to determine the quota coverage and tariffs to be collected by

the Bureau of Customs.

The MAV guidelines are currently being reviewed after a Senate

investigation last September found that the rules limited the in-

quota importation of sugar to traders.3 This was attributed to the

requirement of an import track record to avail of a MAV allocation,

which agricultural producers and users do not usually have. On 01

April 1999, Executive Order No. 87 was issued to facilitate the

importation of raw sugar, through the private sector, and its

conversion from “C” (reserve) to “B” (domestic). Conversion fees,

which refer to the difference between the landed cost of imported

sugar and the average cost of locally produced sugar per 50-

kilogram bag and which will be paid upon the arrival of the imported

sugar, were the basis of the auction held last 04 May 1999.

3 BusinessWorld, 1999. According to the SRA, there were thirty six (36) importers of raw and refined

sugar in 1998, the majority of whom were traders.

12

➲ Under the Agriculture and Fisheries Modernization Act

(AFMA), certain agriculture and fishery inputs, machinery and

equipment (including fertilizers, insecticides, tractors, hybrid seeds,

farm implements and machinery) may be imported duty-free for a

period of five years commencing 1999. Products falling under List

A may be imported duty-free with no restrictions, while importers of

products falling under List B need to get prior certification from the

Department of Agriculture as enterprises duly engaged in

agriculture and fishery. Combined with high output tariffs, the duty-

free importation of inputs in effect increases the protection enjoyed

by the sugar industry from the tariff system.

It is noted that the tariffs on sugar are higher than the tariffs on the

finished products (e.g. sugar confectioneries, sugar preparations,

pastry, cakes, biscuits and other baker’s wares, preserved fruits

and nuts, and beverages), which are at a maximum of 20% (see

Figure 1).

➲ With respect to the ASEAN Free Trade Area (AFTA)-

Common Effective Preferential Tariff (CEPT) Scheme, which

envisions duties falling within the 0-5% range for commodities

traded within the region, sugar is currently in the Temporary

Exclusion List of the Philippines. Thus, the MFN rate of 65%

currently prevails for sugar imports from within ASEAN.

Other ASEAN members such as Brunei, Indonesia, Malaysia,

Singapore and Vietnam also presently exclude sugar. The only

exception is Thailand, which excludes raw sugar but grants a CEPT

13

duty of 2.63 baht/kilogram (equivalent to about 20% ad valorem) on

refined sugar.

During the 6th ASEAN Summit held in Hanoi in December 1998, the

ASEAN Leaders decided to accelerate the implementation of AFTA

by one year from 2003 to 2002. The Philippines will likely exercise

the flexibility option and sugar will be phased into the Scheme by

2003 at a CEPT rate of 5%.

➲ On the country’s commitments to the World Trade

Organization (WTO), the final binding tariff rate on both raw and

refined sugar is 50% to be implemented in 2004. To reach the 50%

target by 2004, reductions must be implemented in 1997 and 2000.

Thus, from 100% in 1996, the out-quota rate of duty on refined

sugar was reduced to 80% in 1997 and further to 65% in 1999 and

2000.

➲ With respect to the Asia Pacific Economic Cooperation

(APEC), the goal is zero tariffs in 2010 and 2020 for developed and

developing countries, respectively.

(2) Factors Restricting Entry of Sugar Imports – Prior to 1982,

the importation of refined sugar was restricted. However, by virtue

of Central Bank Circular No. 850, the importation of refined sugar

was liberalized effective 15 February 1982. Together with the

oversupply and depressed prices of sugar in the world market, the

incentive to import should be high.

14

➲ In reality, however, the SRA continues to exercise regulatory

powers over sugar importation, affecting its entry and practically

isolating the domestic market from imports.

The SRA is the government agency responsible for overseeing the

development of the sugar industry. It is governed by the Sugar

Board, which is chaired by the Secretary of Agriculture, with one (1)

representative each from the sugar millers and sugar planters as

members. It is vested with the power to regulate production of,

establish market allocations for, and institute a quedaning system

for sugar.

Although sugar millers and sugar planters are represented in the

Sugar Board, food processors and other users and consumers are

not, making for a lop-sided policy in favor of the planters and

millers.

The SRA’s regulatory powers include monitoring of sugar imports,

imposing of monitoring fees, and prescribing administrative

procedures if the imported sugar is not used in food processing.

Among these monitoring fees are: “monitoring fee” of P10.00/50 kg

and a “clearance fee” imposed on exporters of sugar-based

products; P50.00/50 kg added to the world price for “B1” sugar

used by food processors and exporters; “clearance fee” of P0.45/50

kg imposed on sugar exporters to the U.S.; “import fee” of

P13.60/50 kg; PhilSURIN lien of P2.00/50 kg; SIFI of P4.75/50 kg;

SMDF of P0.70/50 kg.; PASUDECO of P1.00/50 kg; and P0.40/50

kg.4

4 Tolentino, 1999.

15

➲ The market quota system works in the following manner:

➘ Locally produced sugar is classified into five (5) categories

based on market destination. These are: “A” for the U.S. import

quota market, “B” for the domestic market, C” for reserve, “D” for

exports to countries other than the U.S., and “E” which may be

bought at the world price by exporting firms using sugar as input.

In 1992, the SRA created another quota category, B1, which is also

for the domestic market but may be withdrawn from storage only

after 120 days.

➘ According to sugar industry sources, the market allocation

system ensures the domestic supply of sugar, which is a vital

commodity, in instances where the world price is greater than the

domestic price, when U.S. prices are high (so domestic sugar

producers would rather export), or when the foreign exchange rate

is “uncooperative” (the peso depreciates against the dollar so

imports cost more). It is also claimed by industry sources that the

market allocation system is practised worldwide.

The quota system was devised to allow all planters and millers

proportionately equal access to the higher-priced U.S. quota

market. The SRA estimates production at the start of a crop year

and then prepares a “sugar order” containing the percentage

allocations of the sugar produced into the various destinations.

These allocations are adjusted as production estimates are

modified or the country’s share of the U.S. quota market changes.

16

➘ The market quota system is implemented through a quedan

system and controls on the withdrawal of sugar from warehouses.

All milled sugar is deposited in registered warehouses and the

owners provided quedans (as proof of ownership) which state the

classification, or market destination, of the sugar. The quedan is a

negotiable instrument and sugar is traded using these. Sugar may

be withdrawn from warehouses only with a sugar release order

from the SRA and upon surrender of the quedan.

➘ In 1992, the SRA began quedaning refined sugar.

Refineries issue the refined sugar quedan upon acceptance of raw

sugar for tolling. However, refineries are allowed to accept sugar

for tolling only when accompanied by a sugar release order issued

by the SRA. For integrated refineries (refineries attached to a

sugar mill), refining occurs only after surrender of the raw sugar

quedans and replacement with refined sugar quedans. Refined

sugar can be withdrawn only with the surrender of the refined sugar

quedans.

(3) Providing Access to Imported Sugar – According to the SRA,

exporters may import sugar duty-free. An exporter has to apply for

his sugar requirement with the SRA and submit two (2) pre-

requisites: sales invoice of previous performance and proof that the

exporter has an export commitment. From the point of view of the

SRA therefore, there is no problem for exporters with respect to

access to duty-free sugar.

According to an SRA representative, these requisites are

necessary in order to prevent cheaper imported sugar from finding

its way into the domestic market. Clearly, the

17

! Factors Affecting Competitiveness

(a) Backward Linkage

The Comprehensive Agrarian Reform Law (CARL) has contributed largely

to the declining hectarage planted to sugar, as well as declining yields per

hectare. Under the CARL, farm sizes have been reduced such that

mechanization has become too expensive. The small farmer cannot

afford the tractor that is needed for deep plowing. Sugar cane roots must

reach one meter (1m) deep for higher yields and more efficient harvesting.

Hence, sugar cane farming under the CARL is not cost effective. Industry

sources state that in Australia, sugar cane yield per hectare is two

hundred times more than sugar cane yield per hectare in the Philippines.

Sugar cane farms in Australia are fully mechanized, from soil preparation,

to planting to harvesting. Sugar is a plantation crop where economies of

scale are important. In Thailand and Indonesia, the average sugar

plantation is composed of seventy hectares (70 ha).

Moreover, some farmers who were granted land under the CARL, have

either sold it to developers who in turn develop these into subdivisions or

golf courses, lease it to small business entrepreneurs or leave the land

idle. Interest accruing to farmers, if they sell the land and deposit the

proceeds, as well as income from leasing are greater than profits they

may realize from planting sugar cane. On the other hand, some farmers

prefer to leave the land idle, as income generated from working the land is

not proportionate to taxes paid. Another reason for leaving lands idle is

the lack of capital to fund planting activities. Thus, the reduced hectarage

has led to a deficient supply of canes and the consequent underutilization

of milling capacity and lower sugar production.

18

(b) Technology

Some sugar mills have invested in modern technology and this has

resulted in higher mill output as well as more efficient operations.

However, a majority of the mills have outdated technology and are in need

of modernization to improve efficiencies.

The volume of sugar production depends on the amount of sugar cane

processed and the sugar content of the cane. The failure to mechanize

harvesting results in further decline in sugar cane yield per hectare.

Moreover, harvesting techniques employed affects the sugar content in

cane. Ideally, cane should be milled within twenty-four (24) hours from

cutting to maintain high sugar content. The practice of burning cane

before harvesting, as well as the amount of impurities attached to the

cane, e.g., soil, affects sugar recovery.

(c) Cane Sharing Scheme

The domestic sugar industry employs a cane-sharing scheme to pay

farmers for the sugar cane it brings to mills for processing. The sharing is

as follows: 65% to 70% of the mill output goes to the planters while the

remaining 30% to 35% is retained by the mill. There is little incentive to

improve mill efficiency under the cane-sharing scheme, as the sugar mill

spends for such undertaking but the benefits will accrue mostly to

planters.

(d) Additional Cost to Millers

19

Mills normally shoulder the transport cost of cane from farm to mill. This

aggregates to about 40% of the budget allocated to transportation cost.

Moreover, mills have to invest in water/pollution control system in line with

the legislated Clean Air Act.

(e) Access to Financing

According to industry sources, banks do not accept the plantation (or the

land itself) as loan collateral, which seriously inhibits the ability of planters

to source credit. Credit is especially crucial for investments in new

technology necessary for attaining greater efficiency and productivity. The

investment required to rehabilitate and modernize is huge. According to

an industry informant, P20 billion in modernization expenses have been

made since 1992. Another P40 billion is required but a loan interest rate

above 12% will not prove profitable for millers.

V Industry Performance Assessment

(a) Domestic Industry

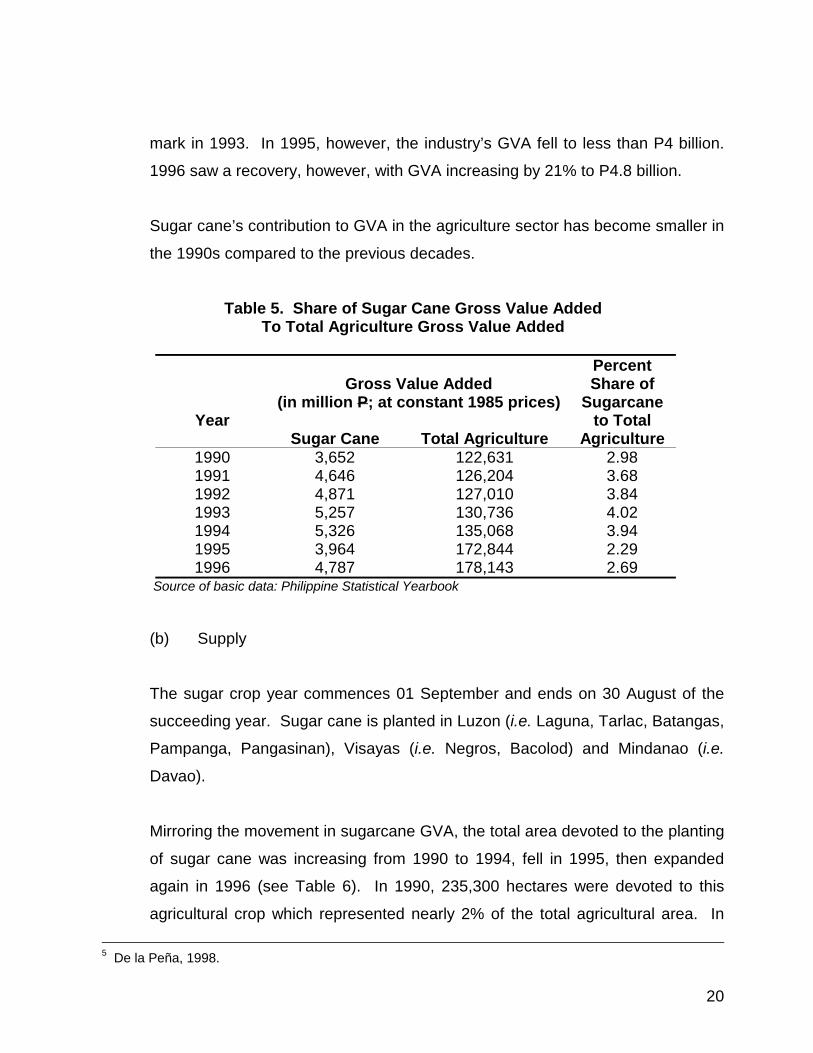

The sugar industry as a whole is one of the country’s oldest and most important

industries. Until the mid-1970s, the industry contributed approximately 9% to

agricultural gross value added (GVA).5 In the 1980s, the share of GVA from

sugar cane production to total agricultural GVA averaged 4%.

Over the period 1990 to 1994, the sugar industry’s GVA has been increasing

(see Table 5). From P3.65 billion in 1990, GVA from the sugar cane sector

topped the P4 billion mark the following year, then went on to pass the P5 billion

20

mark in 1993. In 1995, however, the industry’s GVA fell to less than P4 billion.

1996 saw a recovery, however, with GVA increasing by 21% to P4.8 billion.

Sugar cane’s contribution to GVA in the agriculture sector has become smaller in

the 1990s compared to the previous decades.

Table 5. Share of Sugar Cane Gross Value Added To Total Agriculture Gross Value Added

Gross Value Added (in million P; at constant 1985 prices)

Percent Share of

Sugarcane Year

Sugar Cane

Total Agriculture to Total

Agriculture 1990 3,652 122,631 2.98 1991 4,646 126,204 3.68 1992 4,871 127,010 3.84 1993 5,257 130,736 4.02 1994 5,326 135,068 3.94 1995 3,964 172,844 2.29 1996 4,787 178,143 2.69

Source of basic data: Philippine Statistical Yearbook

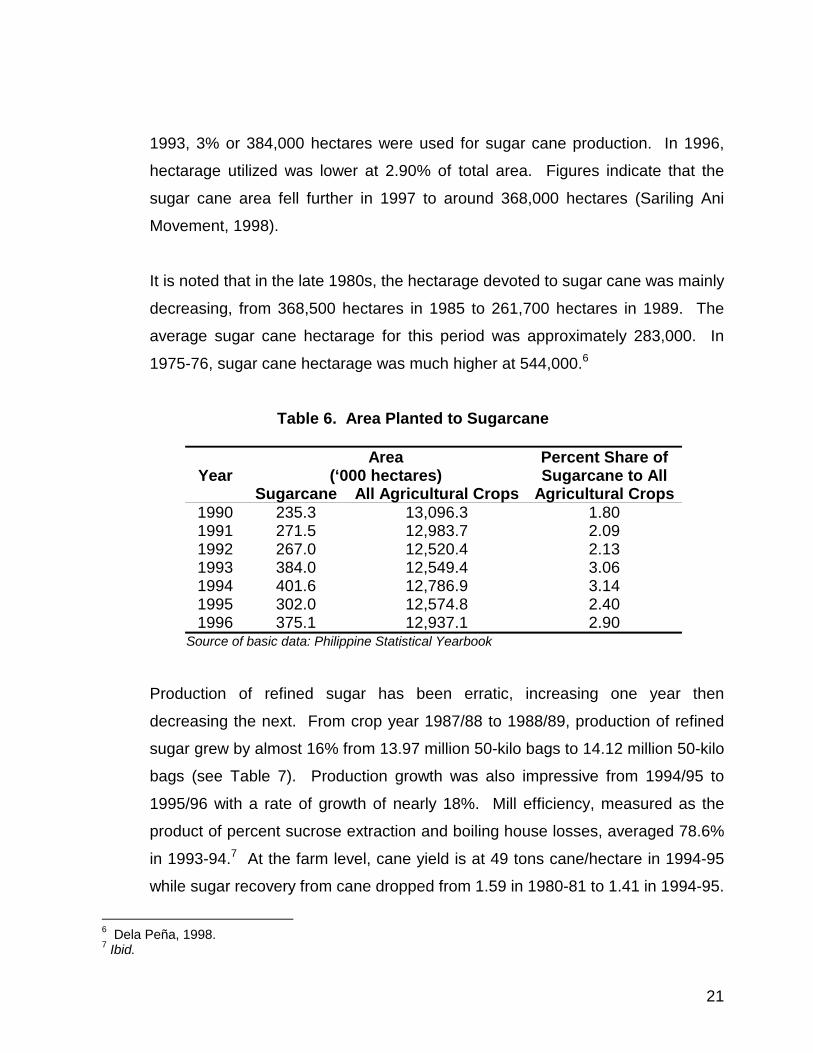

(b) Supply

The sugar crop year commences 01 September and ends on 30 August of the

succeeding year. Sugar cane is planted in Luzon (i.e. Laguna, Tarlac, Batangas,

Pampanga, Pangasinan), Visayas (i.e. Negros, Bacolod) and Mindanao (i.e.

Davao).

Mirroring the movement in sugarcane GVA, the total area devoted to the planting

of sugar cane was increasing from 1990 to 1994, fell in 1995, then expanded

again in 1996 (see Table 6). In 1990, 235,300 hectares were devoted to this

agricultural crop which represented nearly 2% of the total agricultural area. In

5 De la Peña, 1998.

21

1993, 3% or 384,000 hectares were used for sugar cane production. In 1996,

hectarage utilized was lower at 2.90% of total area. Figures indicate that the

sugar cane area fell further in 1997 to around 368,000 hectares (Sariling Ani

Movement, 1998).

It is noted that in the late 1980s, the hectarage devoted to sugar cane was mainly

decreasing, from 368,500 hectares in 1985 to 261,700 hectares in 1989. The

average sugar cane hectarage for this period was approximately 283,000. In

1975-76, sugar cane hectarage was much higher at 544,000.6

Table 6. Area Planted to Sugarcane

Year

Area (‘000 hectares)

Percent Share of Sugarcane to All

Sugarcane All Agricultural Crops Agricultural Crops 1990 235.3 13,096.3 1.80 1991 271.5 12,983.7 2.09 1992 267.0 12,520.4 2.13 1993 384.0 12,549.4 3.06 1994 401.6 12,786.9 3.14 1995 302.0 12,574.8 2.40 1996 375.1 12,937.1 2.90

Source of basic data: Philippine Statistical Yearbook

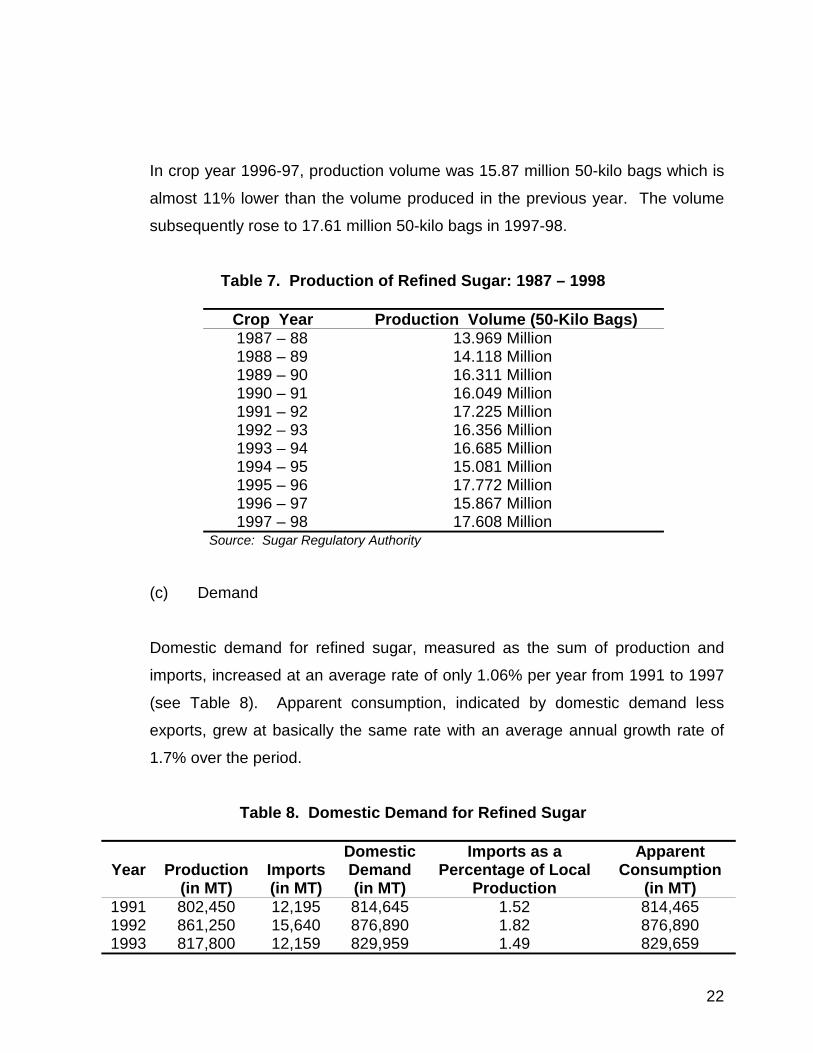

Production of refined sugar has been erratic, increasing one year then

decreasing the next. From crop year 1987/88 to 1988/89, production of refined

sugar grew by almost 16% from 13.97 million 50-kilo bags to 14.12 million 50-kilo

bags (see Table 7). Production growth was also impressive from 1994/95 to

1995/96 with a rate of growth of nearly 18%. Mill efficiency, measured as the

product of percent sucrose extraction and boiling house losses, averaged 78.6%

in 1993-94.7 At the farm level, cane yield is at 49 tons cane/hectare in 1994-95

while sugar recovery from cane dropped from 1.59 in 1980-81 to 1.41 in 1994-95.

6 Dela Peña, 1998. 7 Ibid.

22

In crop year 1996-97, production volume was 15.87 million 50-kilo bags which is

almost 11% lower than the volume produced in the previous year. The volume

subsequently rose to 17.61 million 50-kilo bags in 1997-98.

Table 7. Production of Refined Sugar: 1987 – 1998

Crop Year Production Volume (50-Kilo Bags) 1987 – 88 13.969 Million 1988 – 89 14.118 Million 1989 – 90 16.311 Million 1990 – 91 16.049 Million 1991 – 92 17.225 Million 1992 – 93 16.356 Million 1993 – 94 16.685 Million 1994 – 95 15.081 Million 1995 – 96 17.772 Million 1996 – 97 15.867 Million 1997 – 98 17.608 Million

Source: Sugar Regulatory Authority

(c) Demand

Domestic demand for refined sugar, measured as the sum of production and

imports, increased at an average rate of only 1.06% per year from 1991 to 1997

(see Table 8). Apparent consumption, indicated by domestic demand less

exports, grew at basically the same rate with an average annual growth rate of

1.7% over the period.

Table 8. Domestic Demand for Refined Sugar Year

Production

(in MT)

Imports (in MT)

Domestic Demand (in MT)

Imports as a Percentage of Local

Production

Apparent Consumption

(in MT) 1991 802,450 12,195 814,645 1.52 814,465 1992 861,250 15,640 876,890 1.82 876,890 1993 817,800 12,159 829,959 1.49 829,659

23

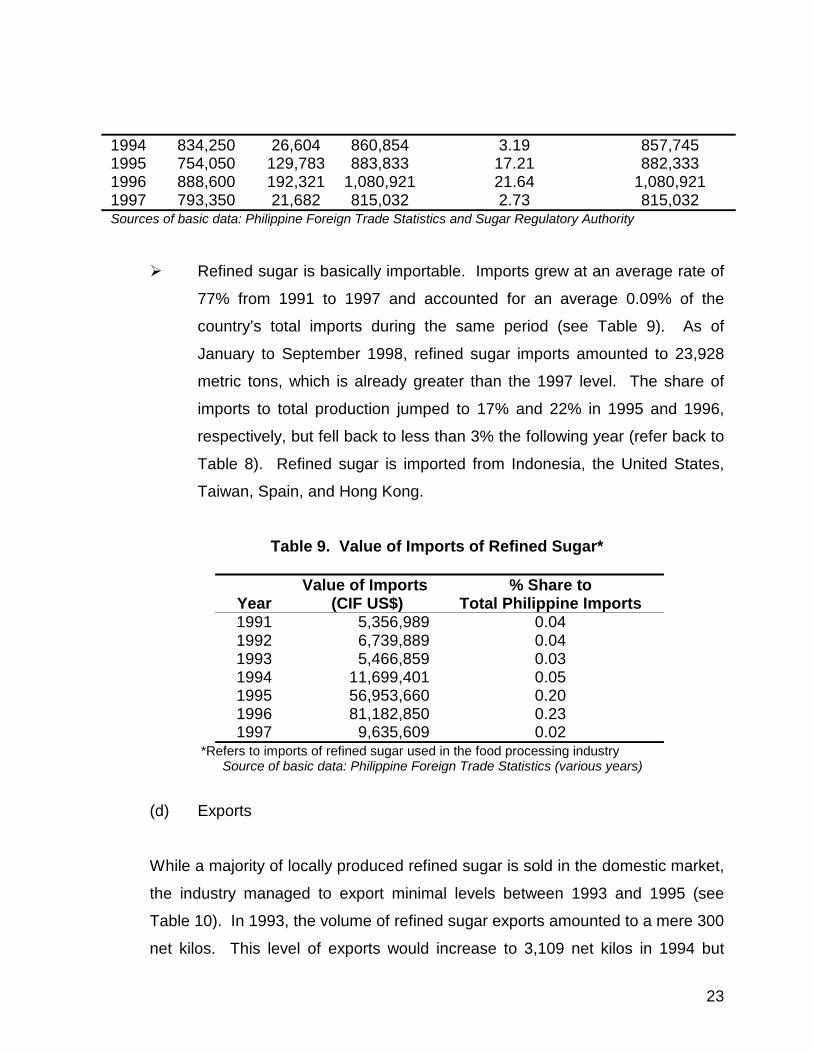

1994 834,250 26,604 860,854 3.19 857,745 1995 754,050 129,783 883,833 17.21 882,333 1996 888,600 192,321 1,080,921 21.64 1,080,921 1997 793,350 21,682 815,032 2.73 815,032

Sources of basic data: Philippine Foreign Trade Statistics and Sugar Regulatory Authority

! Refined sugar is basically importable. Imports grew at an average rate of

77% from 1991 to 1997 and accounted for an average 0.09% of the

country’s total imports during the same period (see Table 9). As of

January to September 1998, refined sugar imports amounted to 23,928

metric tons, which is already greater than the 1997 level. The share of

imports to total production jumped to 17% and 22% in 1995 and 1996,

respectively, but fell back to less than 3% the following year (refer back to

Table 8). Refined sugar is imported from Indonesia, the United States,

Taiwan, Spain, and Hong Kong.

Table 9. Value of Imports of Refined Sugar*

Year

Value of Imports (CIF US$)

% Share to Total Philippine Imports

1991 5,356,989 0.04 1992 6,739,889 0.04 1993 5,466,859 0.03 1994 11,699,401 0.05 1995 56,953,660 0.20 1996 81,182,850 0.23 1997 9,635,609 0.02

*Refers to imports of refined sugar used in the food processing industry Source of basic data: Philippine Foreign Trade Statistics (various years)

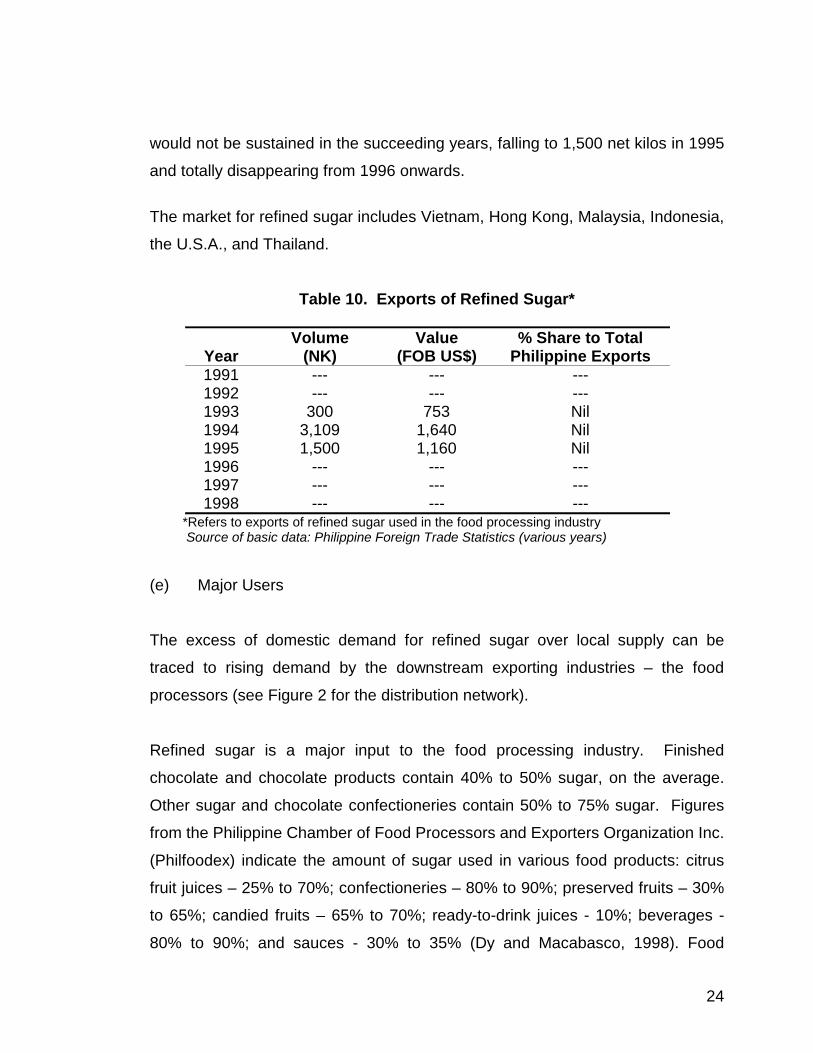

(d) Exports

While a majority of locally produced refined sugar is sold in the domestic market,

the industry managed to export minimal levels between 1993 and 1995 (see

Table 10). In 1993, the volume of refined sugar exports amounted to a mere 300

net kilos. This level of exports would increase to 3,109 net kilos in 1994 but

24

would not be sustained in the succeeding years, falling to 1,500 net kilos in 1995

and totally disappearing from 1996 onwards.

The market for refined sugar includes Vietnam, Hong Kong, Malaysia, Indonesia,

the U.S.A., and Thailand.

Table 10. Exports of Refined Sugar*

Year

Volume (NK)

Value (FOB US$)

% Share to Total Philippine Exports

1991 --- --- --- 1992 --- --- --- 1993 300 753 Nil 1994 3,109 1,640 Nil 1995 1,500 1,160 Nil 1996 --- --- --- 1997 --- --- --- 1998 --- --- ---

*Refers to exports of refined sugar used in the food processing industry Source of basic data: Philippine Foreign Trade Statistics (various years)

(e) Major Users

The excess of domestic demand for refined sugar over local supply can be

traced to rising demand by the downstream exporting industries – the food

processors (see Figure 2 for the distribution network).

Refined sugar is a major input to the food processing industry. Finished

chocolate and chocolate products contain 40% to 50% sugar, on the average.

Other sugar and chocolate confectioneries contain 50% to 75% sugar. Figures

from the Philippine Chamber of Food Processors and Exporters Organization Inc.

(Philfoodex) indicate the amount of sugar used in various food products: citrus

fruit juices – 25% to 70%; confectioneries – 80% to 90%; preserved fruits – 30%

to 65%; candied fruits – 65% to 70%; ready-to-drink juices - 10%; beverages -

80% to 90%; and sauces - 30% to 35% (Dy and Macabasco, 1998). Food

25

processors include: Philfoodex, the Philippine Chamber of Food Manufacturers

Inc., Nestle Philippines Inc., and Coca-Cola Bottlers Philippines Inc.

According to the Philippine Chamber of Food Manufacturers, Inc., about 200,000

metric tons of sugar are used yearly for various food products. According to the

Beverage Industry Association of the Philippines (BIAP), it consumes 37% of the

country’s production of refined sugar.

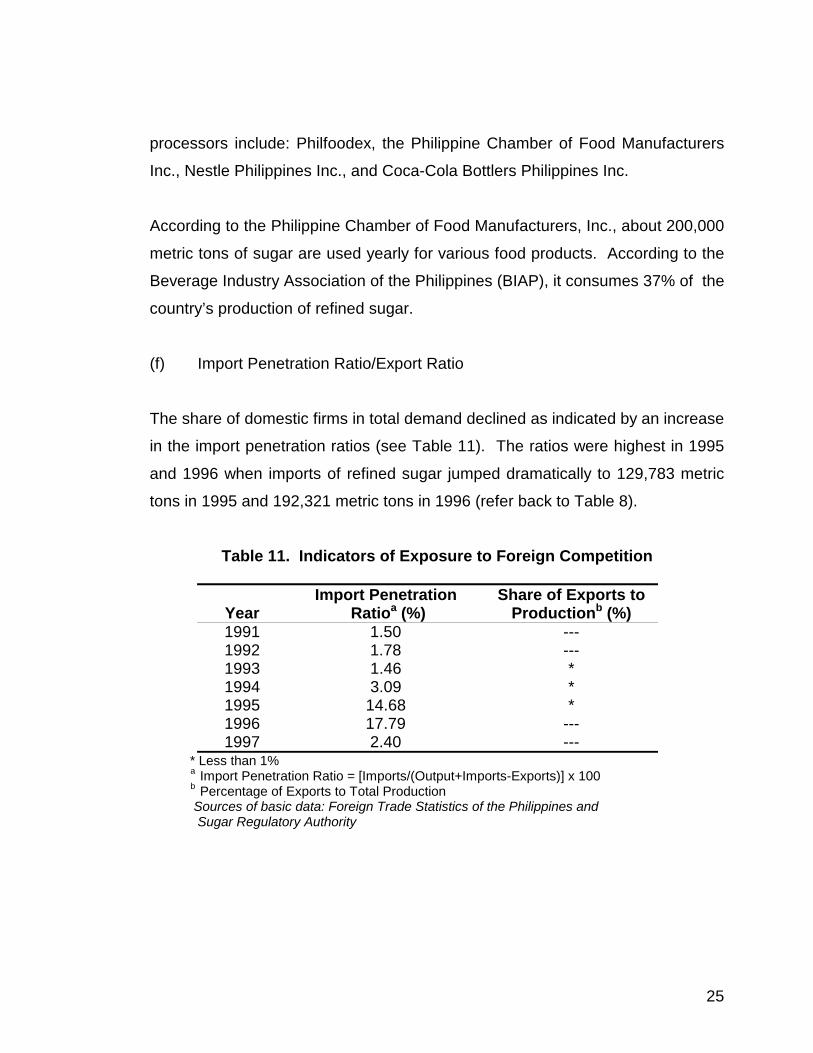

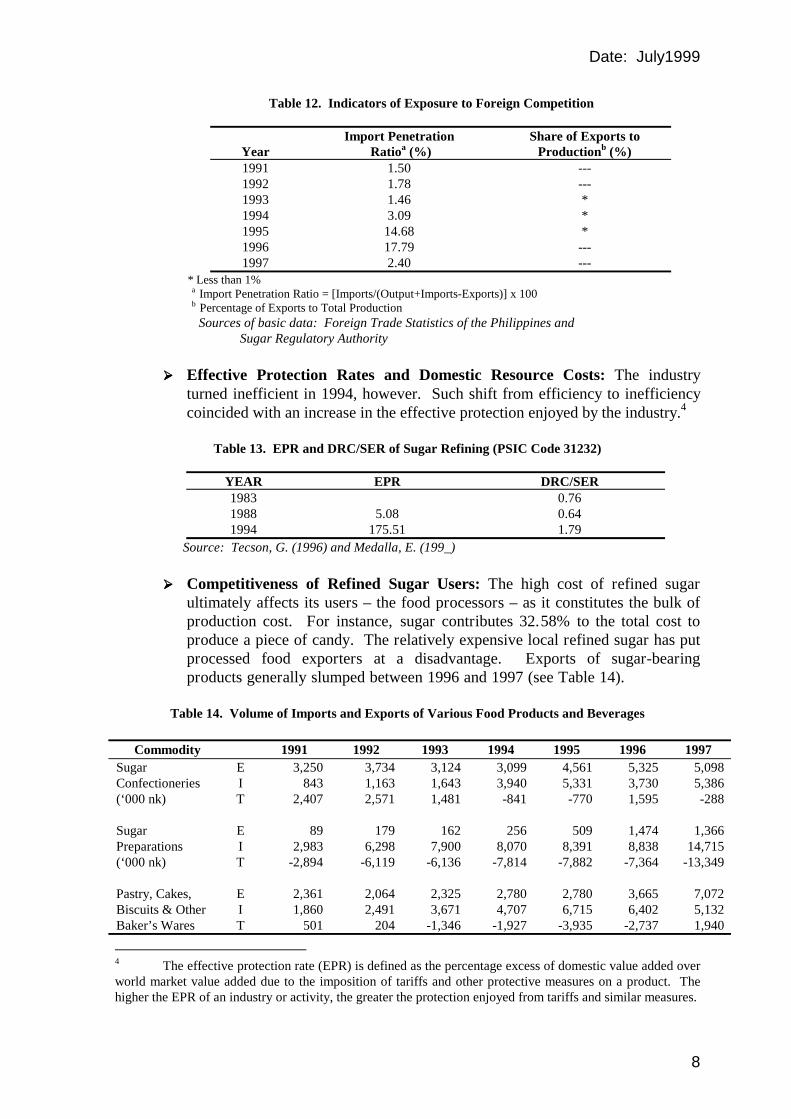

(f) Import Penetration Ratio/Export Ratio

The share of domestic firms in total demand declined as indicated by an increase

in the import penetration ratios (see Table 11). The ratios were highest in 1995

and 1996 when imports of refined sugar jumped dramatically to 129,783 metric

tons in 1995 and 192,321 metric tons in 1996 (refer back to Table 8).

Table 11. Indicators of Exposure to Foreign Competition

Year

Import Penetration Ratioa (%)

Share of Exports to Productionb (%)

1991 1.50 --- 1992 1.78 --- 1993 1.46 * 1994 3.09 * 1995 14.68 * 1996 17.79 --- 1997 2.40 ---

* Less than 1% a Import Penetration Ratio = [Imports/(Output+Imports-Exports)] x 100 b Percentage of Exports to Total Production Sources of basic data: Foreign Trade Statistics of the Philippines and

Sugar Regulatory Authority

26

(g) Effective Protection Rates and Domestic Resource Costs

In 1983, the sugar refining industry was an efficient earner of foreign exchange

based on a Domestic Resource Cost (DRC)/Shadow Exchange Rate (SER) ratio

of 0.76 (see Table 12).8 The industry further improved its efficiency in 1988. The

industry turned inefficient in 1994, however. Such shift from efficiency to

inefficiency coincided with an increase in the effective protection enjoyed by the

industry.9

Table 12. EPR and DRC/SER of Sugar Refining (PSIC Code 31232)

YEAR EPR DRC/SER 1983 0.76 1988 5.08 0.64 1994 175.51 1.79

Source: Tecson, G. (1996) and Medalla, E. (199_)

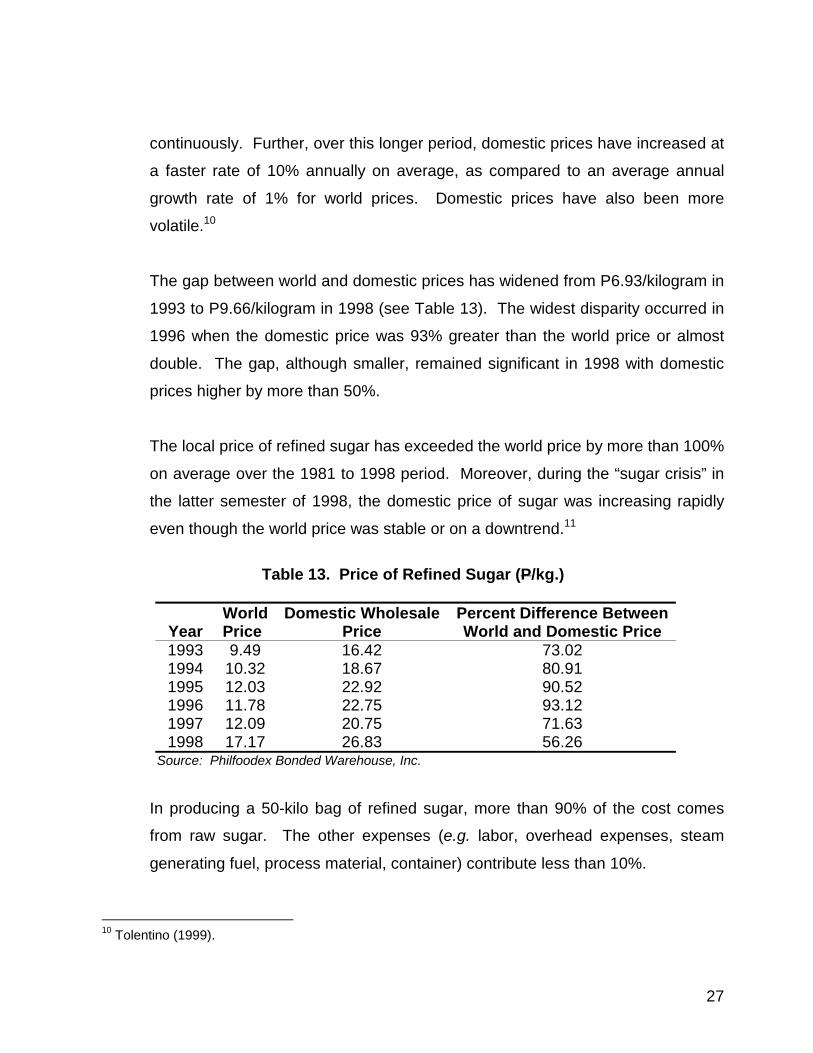

(h) Price Competitiveness

The world price of refined sugar increased by an average of 13.6% from 1993 to

1998. The increase in the domestic price of refined sugar is slightly less: the

average annual growth rate over the period is 11.2%. Nevertheless, the

domestic price of refined sugar has consistently been higher than the world price.

It has been determined that even over a longer period, from 1981 to 1998,

domestic prices of refined sugar have exceeded international prices

8 An activity or industry is said to have comparative advantage if the domestic cost it incurs (expressed in

shadow prices) to earn or save a unit of foreign exchange is less than or equal to the shadow price of foreign exchange. A decline in the DRC/SER ratio implies an improvement in an activity’s comparative advantage position. The criteria for efficiency used in Tecson (1996) was used to determine degree of efficiency.

9 The effective protection rate (EPR) is defined as the percentage excess of domestic value added over

world market value added due to the imposition of tariffs and other protective measures on a product. The higher the EPR of an industry or activity, the greater the protection enjoyed from tariffs and similar measures.

27

continuously. Further, over this longer period, domestic prices have increased at

a faster rate of 10% annually on average, as compared to an average annual

growth rate of 1% for world prices. Domestic prices have also been more

volatile.10

The gap between world and domestic prices has widened from P6.93/kilogram in

1993 to P9.66/kilogram in 1998 (see Table 13). The widest disparity occurred in

1996 when the domestic price was 93% greater than the world price or almost

double. The gap, although smaller, remained significant in 1998 with domestic

prices higher by more than 50%.

The local price of refined sugar has exceeded the world price by more than 100%

on average over the 1981 to 1998 period. Moreover, during the “sugar crisis” in

the latter semester of 1998, the domestic price of sugar was increasing rapidly

even though the world price was stable or on a downtrend.11

Table 13. Price of Refined Sugar (P/kg.)

World Domestic Wholesale Percent Difference Between

Year Price Price World and Domestic Price 1993 9.49 16.42 73.02 1994 10.32 18.67 80.91 1995 12.03 22.92 90.52 1996 11.78 22.75 93.12 1997 12.09 20.75 71.63 1998 17.17 26.83 56.26

Source: Philfoodex Bonded Warehouse, Inc.

In producing a 50-kilo bag of refined sugar, more than 90% of the cost comes

from raw sugar. The other expenses (e.g. labor, overhead expenses, steam

generating fuel, process material, container) contribute less than 10%.

10 Tolentino (1999).

28

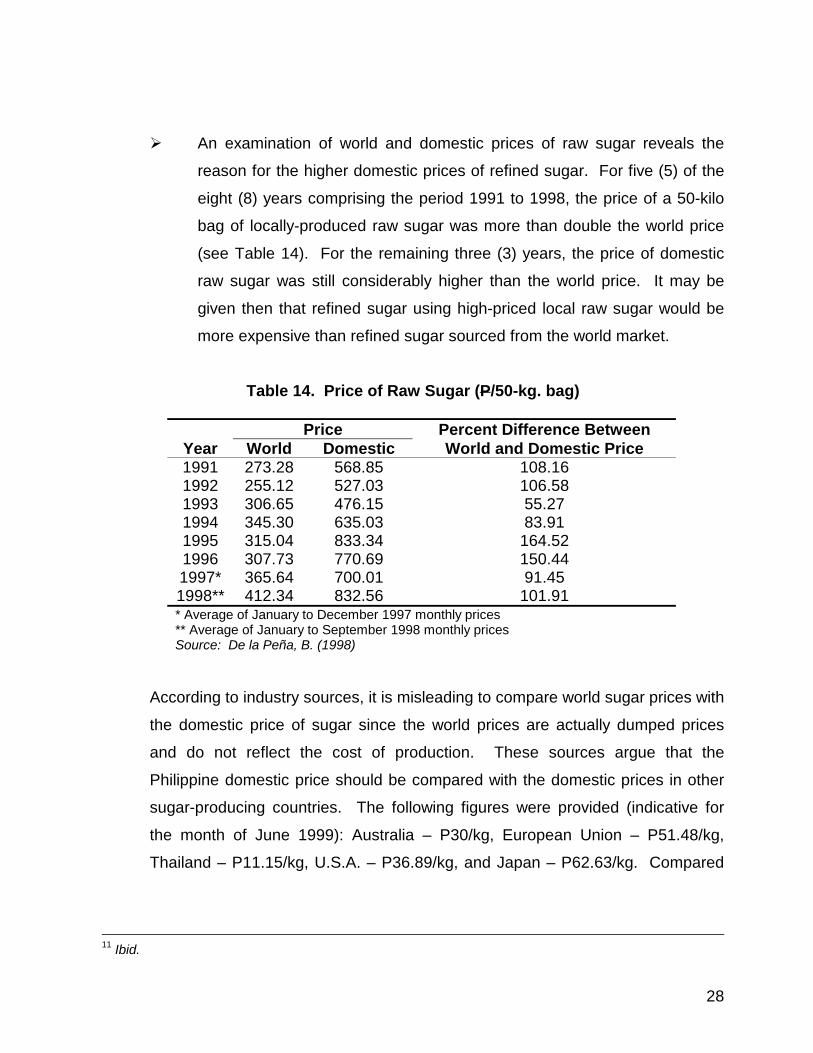

! An examination of world and domestic prices of raw sugar reveals the

reason for the higher domestic prices of refined sugar. For five (5) of the

eight (8) years comprising the period 1991 to 1998, the price of a 50-kilo

bag of locally-produced raw sugar was more than double the world price

(see Table 14). For the remaining three (3) years, the price of domestic

raw sugar was still considerably higher than the world price. It may be

given then that refined sugar using high-priced local raw sugar would be

more expensive than refined sugar sourced from the world market.

Table 14. Price of Raw Sugar (P/50-kg. bag)

Price Percent Difference Between Year World Domestic World and Domestic Price 1991 273.28 568.85 108.16 1992 255.12 527.03 106.58 1993 306.65 476.15 55.27 1994 345.30 635.03 83.91 1995 315.04 833.34 164.52 1996 307.73 770.69 150.44 1997* 365.64 700.01 91.45 1998** 412.34 832.56 101.91

* Average of January to December 1997 monthly prices ** Average of January to September 1998 monthly prices Source: De la Peña, B. (1998)

According to industry sources, it is misleading to compare world sugar prices with

the domestic price of sugar since the world prices are actually dumped prices

and do not reflect the cost of production. These sources argue that the

Philippine domestic price should be compared with the domestic prices in other

sugar-producing countries. The following figures were provided (indicative for

the month of June 1999): Australia – P30/kg, European Union – P51.48/kg,

Thailand – P11.15/kg, U.S.A. – P36.89/kg, and Japan – P62.63/kg. Compared

11 Ibid.

29

with a Philippine domestic price of P25.23/kg, then the Philippines would actually

have the cheapest sugar.

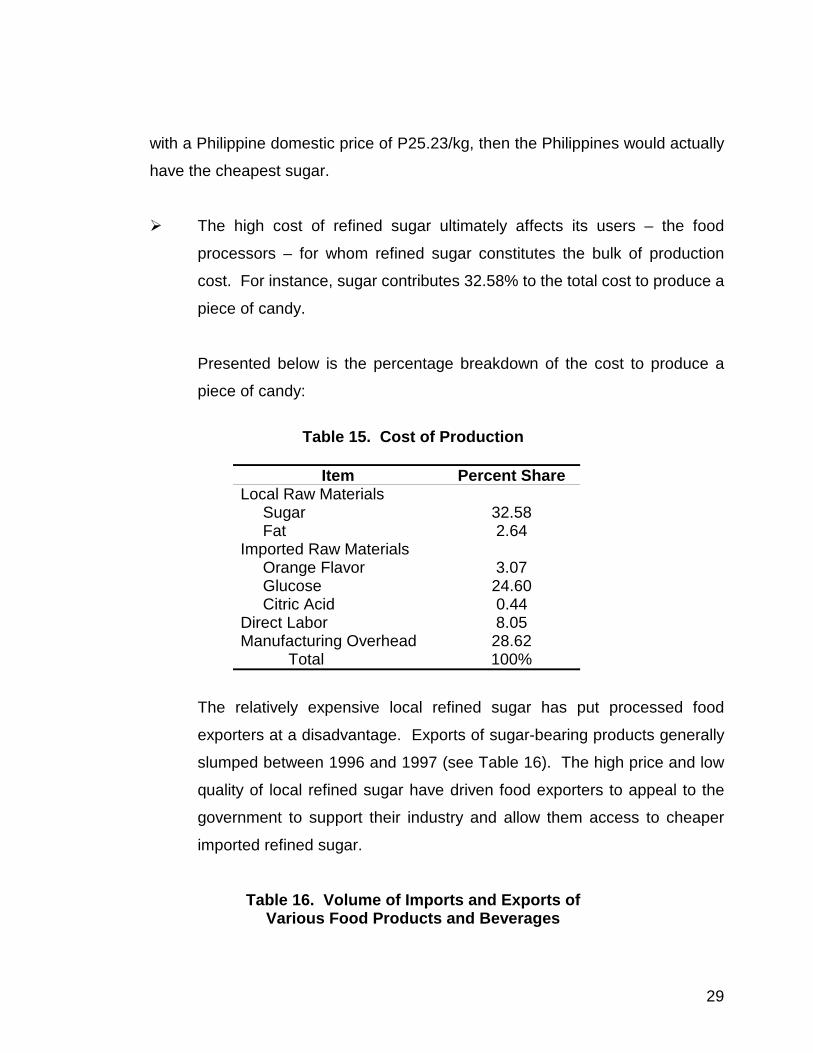

! The high cost of refined sugar ultimately affects its users – the food

processors – for whom refined sugar constitutes the bulk of production

cost. For instance, sugar contributes 32.58% to the total cost to produce a

piece of candy.

Presented below is the percentage breakdown of the cost to produce a

piece of candy:

Table 15. Cost of Production

Item Percent Share

Local Raw Materials Sugar 32.58 Fat 2.64 Imported Raw Materials Orange Flavor 3.07 Glucose 24.60 Citric Acid 0.44 Direct Labor 8.05 Manufacturing Overhead 28.62

Total 100%

The relatively expensive local refined sugar has put processed food

exporters at a disadvantage. Exports of sugar-bearing products generally

slumped between 1996 and 1997 (see Table 16). The high price and low

quality of local refined sugar have driven food exporters to appeal to the

government to support their industry and allow them access to cheaper

imported refined sugar.

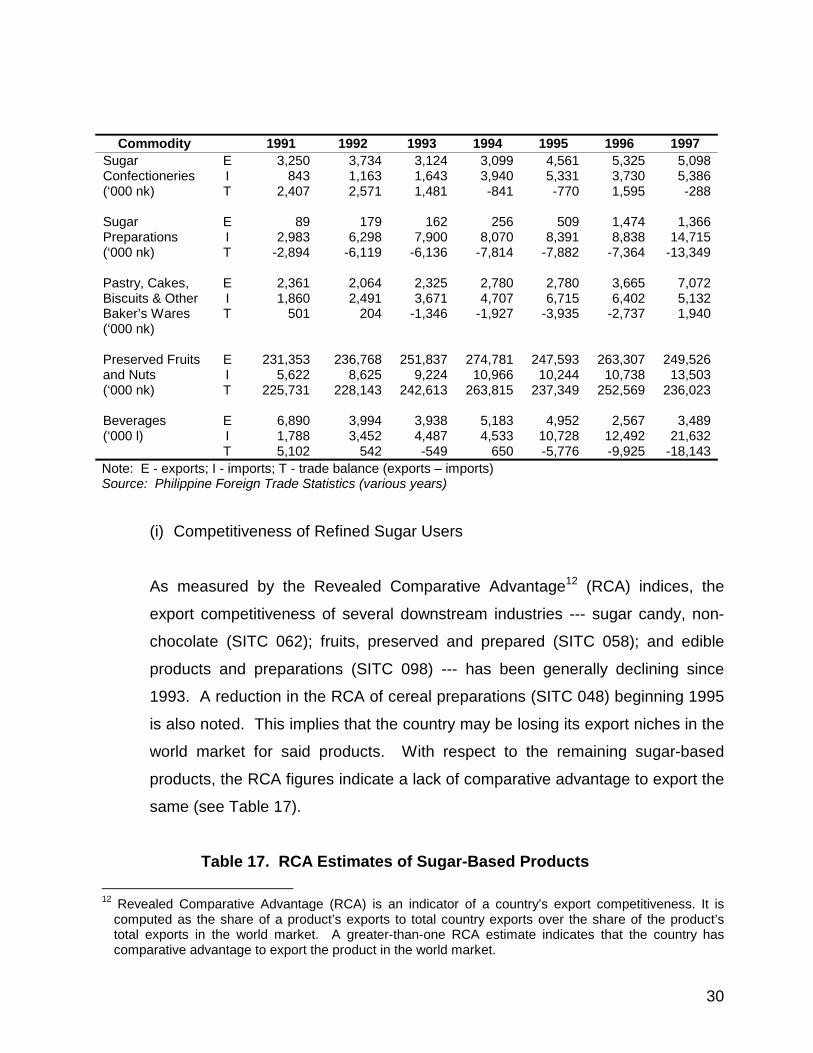

Table 16. Volume of Imports and Exports of Various Food Products and Beverages

30

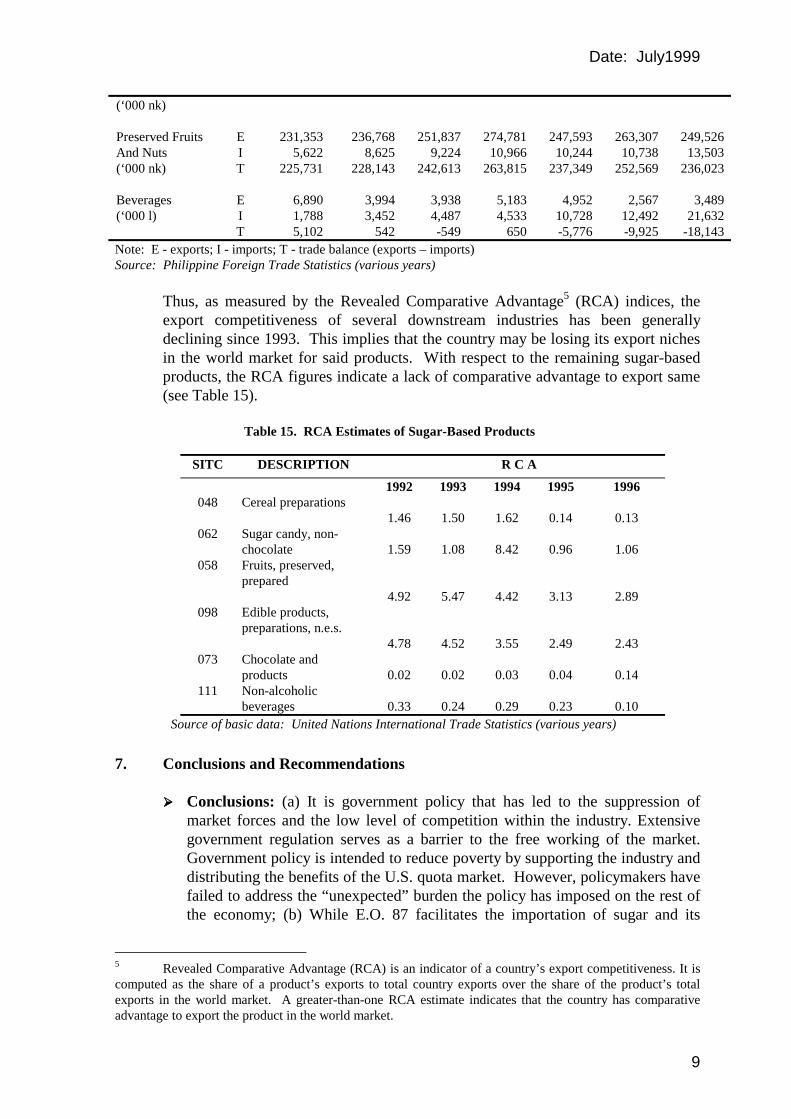

Commodity 1991 1992 1993 1994 1995 1996 1997 Sugar E 3,250 3,734 3,124 3,099 4,561 5,325 5,098 Confectioneries I 843 1,163 1,643 3,940 5,331 3,730 5,386 (‘000 nk) T 2,407 2,571 1,481 -841 -770 1,595 -288 Sugar E 89 179 162 256 509 1,474 1,366 Preparations I 2,983 6,298 7,900 8,070 8,391 8,838 14,715 (‘000 nk) T -2,894 -6,119 -6,136 -7,814 -7,882 -7,364 -13,349 Pastry, Cakes, E 2,361 2,064 2,325 2,780 2,780 3,665 7,072 Biscuits & Other I 1,860 2,491 3,671 4,707 6,715 6,402 5,132 Baker’s Wares T 501 204 -1,346 -1,927 -3,935 -2,737 1,940 (‘000 nk) Preserved Fruits E 231,353 236,768 251,837 274,781 247,593 263,307 249,526 and Nuts I 5,622 8,625 9,224 10,966 10,244 10,738 13,503 (‘000 nk) T 225,731 228,143 242,613 263,815 237,349 252,569 236,023 Beverages E 6,890 3,994 3,938 5,183 4,952 2,567 3,489 (‘000 l) I 1,788 3,452 4,487 4,533 10,728 12,492 21,632 T 5,102 542 -549 650 -5,776 -9,925 -18,143 Note: E - exports; I - imports; T - trade balance (exports – imports) Source: Philippine Foreign Trade Statistics (various years)

(i) Competitiveness of Refined Sugar Users

As measured by the Revealed Comparative Advantage12 (RCA) indices, the

export competitiveness of several downstream industries --- sugar candy, non-

chocolate (SITC 062); fruits, preserved and prepared (SITC 058); and edible

products and preparations (SITC 098) --- has been generally declining since

1993. A reduction in the RCA of cereal preparations (SITC 048) beginning 1995

is also noted. This implies that the country may be losing its export niches in the

world market for said products. With respect to the remaining sugar-based

products, the RCA figures indicate a lack of comparative advantage to export the

same (see Table 17).

Table 17. RCA Estimates of Sugar-Based Products 12 Revealed Comparative Advantage (RCA) is an indicator of a country’s export competitiveness. It is

computed as the share of a product’s exports to total country exports over the share of the product’s total exports in the world market. A greater-than-one RCA estimate indicates that the country has comparative advantage to export the product in the world market.

31

SITC DESCRIPTION R C A

1992 1993 1994 1995 1996 048 Cereal

preparations

1.46

1.50

1.62

0.14

0.13 062 Sugar candy,

non-chocolate

1.59

1.08

8.42

0.96

1.06 058 Fruits,

preserved, prepared

4.92

5.47

4.42

3.13

2.89 098 Edible products,

preparations, n.e.s.

4.78

4.52

3.55

2.49

2.43 073 Chocolate and

products

0.02

0.02

0.03

0.04

0.14 111 Non-alcoholic

beverages

0.33

0.24

0.29

0.23

0.10 Source of basic data: United Nations International Trade Statistics (various years)

VI Conclusions and Recommendations

(a) Conclusions

! Market Concentration

The Philippine refined sugar industry can hardly be characterized as a perfectly

competitive market. The indicative HHI figures show that the sugar market is

moderately concentrated.

While there are no legal barriers to entry and exit, exit is constrained by the huge

investments that have already been made. Entry, too, is constrained by the

prevailing environment of excess capacity in mills and refineries caused by the

fragmentation of sugar lands under the CARL (Republic Act No. 6657) and

32

declining sugar productivity in terms of hectarage and piculs per tons cane or

sugar yields.

! Anti-Competitive Behavior

Despite moderate market concentration, the anti-competitive behavior of market

participants, evident in the industry’s pricing behavior, is reinforced by

government regulations. The industry has long been subject of extensive

government regulation, which serves as a barrier to the free working of the

market. Government policy would seem to be well-intentioned: to reduce poverty

by supporting the industry and distributing the benefits of the U.S. quota market.

However, policymakers have failed to address the “unexpected” burden policy

has imposed on the rest of the economy.

➲ Restrictions imposed on sugar imports – Since sugar has

traditionally been considered a sensitive agricultural commodity, it has

always been highly protected. Tariffs have been at the high-end13 and

while imports are supposed to have been liberalized, import controls are

maintained by the SRA. While E.O. 87 facilitates the importation of sugar

and its conversion from “C” to “B,” a new tax on imports has effectively

been imposed. According to some sources, the conversion fee paid by

the bidders during the 04 May auction would add P8/kilo to the price of

sugar currently pegged at P21/kilo14.

➲ Incentives to entry reinforce anti-competitive behavior – While

tariffs and import restrictions serve as incentives to entry since potential

13 The mechanism of using bonded warehouses to take advantage of reduced tariffs on imported inputs is

generally limited to those with the capability and resources to utilize such and process all the required paperwork in Manila (Tolentino, 1999).

14 Philippine Daily Inquirer, 1999.

33

players are assured of a protected domestic environment, it also

discourages entry if they allow incumbents to “entrench” themselves as

seems to be the case in the sugar industry. Sugar

producers/millers/refiners form a well-organized group willing to pay the

costs of ensuring that their interests remain protected and the government

incentives they have long enjoyed stay. In contrast, consumers are

scattered, the awareness level with respect to the burden from high local

sugar prices is low, so an effective counterforce to the sugar-producing

group that can influence policy does not exist.

➲ The goal of government’s trade liberalization initiatives is to induce

Philippine industries to attain global competitiveness. Essentially, the

strategy is to introduce greater competition into the economy through the

lowering/elimination of trade barriers --- the competitive pressure from

imports would push domestic firms to innovate and work towards greater

efficiency and ultimately, world competitiveness. This liberalization

strategy has been sparingly applied to the sugar industry. Thus, the

degree of competition within the industry is less than desirable.

➲ Quota allocation and quedaning system – Aside from trade barriers,

another obstacle to a more competitive sugar market is the quota

allocation and quedaning system. Since market destination is pre-

determined, producers/mills need not compete with each other for a share

of the market.

The quota allocation and quedaning system has clearly dulled any

competitive edge that the refined sugar industry may have developed had

it been allowed to face competition. When asked what steps the sugar

producers are taking or have taken with respect to the probable reduction

of the U.S. sugar quota allocation to Mexico (under the North American

34

Free Trade Accord), an industry source merely said that they (sugar

planters and millers) are “watching with concern” and that the reduction is

“farfetched yet anyway.”

(b) Recommendations

It is apparent that government policy that has led to the suppression of market

forces and the low level of competition within the refined sugar industry.

! Issues That Can Be Addressed by Competition Policy

The combination of trade restrictions and the regulatory system of sugar

marketing have adversely affected the sugar industry’s development. The

industry has not been encouraged to “shape up” and work towards greater

efficiency and competitiveness. Indeed, where is the incentive for restructuring

when the industry is protected from competition from lower-priced imports,

access to the high-priced U.S. market is assured, and market destination is pre-

determined. As proof, the industry remains characterized by low farm cane

productivity and low sugar mill efficiency relative to world standards as well as

high sugar prices.15 Domestic production efficiency and supply have fallen

behind domestic demand. The DRC/SER ratios indicate a shift from efficiency to

inefficiency as effective protection to the industry increased. Moreover, it has

been claimed that the plight of the sacadas16 has not really improved. The

industry’s contribution to GVA has been falling along with the hectarage devoted

to sugar cane, which means that scarce resources continue to be diverted to a

shrinking sector.

15 Tolentino, 1999. 16 Sacada is the local term for sugar tenant farmer.

35

The inefficiencies of the sugar industry, graphically illustrated by high domestic

prices for sugar, penalize downstream and export industries (like the food

processors) and the Filipino consumer. The high cost of food impacts on the

cost of labor which, in turn, impacts on the country’s competitiveness. With

respect to the export industries, these have proven potential in the world market.

However, the high cost of refined sugar is certainly a factor in the decline in

export competitiveness of sugar confectioneries and preserved fruits and nuts

during the past three (3) years. This suggests that the country may lose potential

export niches. How many other export industries were prevented from emerging

due to the high cost of sugar?

➲ Providing competition in the market – Since government policy on

sugar has produced unintended outcomes to the detriment of a large

sector of the economy, then a modification of policy would seem to be in

order. Competition policy would help greatly with respect to providing

direction in freeing the market and allowing the interplay of market forces.

Permitting competition among the industry players and allowing further

competitive pressure from imports would provide the incentive for striving

towards higher efficiency levels and world competitiveness.17

➲ Reviewing the mandate of the Sugar Regulatory Administration -

Consistent with this, the SRA’s mandate should be reviewed. With a

national competition policy in place, the role of the SRA would have to be

assessed within the framework of encouraging greater competition within

the market. What is required in these times is a responsive bureaucracy.

The government should apply competition policy to its own activities and

17 Competition policy would have to be supported by an integrated package of reforms. Industry sources

cite the following problems, among others: poor infrastructure leading to high transport costs, inadequate irrigation, insufficient funds for research and development, outdated production sharing system, lack of countryside credit, the adverse effects of CARL.

36

devolve certain services that it currently performs to the more efficient

private sector.

➲ “Save-Us-Save-Yourselves” – This should be the lobbying cry of

domestic industrial users of refined sugar. Both the refined sugar and

domestic food processing industries can utilize competition policy to

improve their respective sectors. An efficient sugar industry can support a

highly developed food processing industry. Instead of working against

each other, both industries should work together in lobbying the

government for reforms to make the sugar industry competitive. The

competitiveness of the sugar industry will translate into competitiveness

for the food processing industry. The objective is to develop

competitiveness not extend protectionism.

An advocacy group, whether composed of members of the industries or

independently contracted professional lobbyists, is vital in order to ensure

the passage of executive and/or legislative measures designed to assist

both sectors in developing and/or improving their competitiveness, to rally

members of the industries into active participation, and to raise public

awareness and support for the industries.

! Temporary and/or Additional Measures

The effects of competition policy will not necessarily be immediate. Pending the

same, temporary and/or additional measures may be taken:

➲ Consolidation of B1 Requirements – The B1 quota category, which

is also for the domestic market but may be withdrawn from storage only

after 120 days, are available for the use of food processors and other

industrial domestic consumers. According to an industry source, the

37

problem on the supply side is that the millers/traders do not have the

resources to deliver the individual orders of each industrial consumer.

Industrial consumers should therefore organize their own centralized

distribution network where their sugar orders may be placed and

consolidated with other orders. All orders will be delivered to the

distribution network office, which will then make the deliveries to the

individual industrial consumer or groups of industrial consumers.

➲ Milling Waste Products as Income Source – Bagasse, which is

sugar cane residue, can be made into paper and boards of various

grades, including fine writing and printing papers. The paper industry is

looking for other sources of fiber for making paper. Selling bagasse to the

paper industry can be a major source of funds for financing the

modernization of the sugar industry as well as an economical and

environmentally sound way to dispose of milling waste products.

In fine, the urgency for the sugar industry to gain even domestic competitiveness is

highlighted by the reduction and probable disappearance of the U.S. sugar quota with

the implementation of the NAFTA. Without a sure source of income, the sugar industry

must look closer to home to sustain and develop itself. The most logical and profitable

way is to supply the domestic market at competitive prices. To charge uncompetitive

prices would undoubtedly be self-destructive, for to bleed to death the domestic food

processing industry is to ultimately kill the sugar industry as well.

Competition policy could play a key role in ensuring that not only this objective is

realized but also the national goal of attaining sustainable economic development

through the strengthening of exports.

38

SUGAR CANE (1212.92 00)

MFN 20% (1998) 15% (1999) 10% (2000)

CEPT 15%

RAW CANE SUGAR (1701.11)

MFN 50% (In-Quota)

80% (1998 Out-Quota) 65% (1999-2000)

ASEAN 65%

CANE MOLASSES

(1703.10 00) MFN

10% (1998-1999) 7% (2000)

CEPT 10%

REFINED CANE SUGAR (1701.99)

MFN 50% (In-Quota)

80% (1998 Out-Quota) 65% (1999-2000)

ASEAN 65%

MSG (2922.42 10)

MFN 20% (1998) 15% (1999) 10% (2000)

ASEAN 20%

Liquor (22.08) MFN

20% (1998-1999) 15% (2000)

CEPT 15%

Cattle for Slaughter

(0102.90 00) MFN 3%

ASEAN Excluded

Sugar Confectioneries

(17.04) MFN

20/10% (1998-1999) 15/7% (2000)

CEPT 15%

Sugar Preparations (18.06) MFN

3/20/10% (1998-1999) 3/10/15/7% (2000)

CEPT 3/15/10% ASEAN

10%

Pastry, Cakes, Biscuits & Other Baker’s Wares

(19.05) MFN

20% (1998-1999) 15% (2000)

ASEAN 20% 1905.10 00

Beverages (22.02) MFN

20% (1998) 20/15/10% (1999)

15/10% (2000) CEPT 10%

Preserved Fruits and Nuts

(20.06/ 20.07/ 20.08) MFN

3/20/10% (1998) 20/15/10/3% (1999) 15/10/7/3% (2000)

CEPT 15/10%/Excluded

ASEAN 20%

Source: Tariff Commission

July 1999

REFINED SUGAR INDUSTRY

1. The Relevant Market

! 3 Major Grades of Refined Sugar: (a) standard refined - used primarily as table sugar; (b) premium sugar - used by food manufacturers; and (c) bottlers grade - used by the beverage industry.

! Linkage Chart: Flow of commodities from the sugar industry to user industries

(see Figure 1). ! The Relevant Market: Product Market - locally-produced refined sugar.

Importation of refined sugar is restricted and users do not have the option to just switch to imported sugar. Geographic Market - the Philippine national territory. Participants in the Market – 36 sugar mills (see Table 1). Sugar industry associations - Philippine Sugar Millers Association, Philippine Sugar Refiners Institute, Sugar Industry Foundation Inc., the National Congress of Unions in the Sugar Industry of the Philippines, and the Philippine Association of Sugar Refineries, Inc.

Table 1. List of Sugar Mills

Sugar Mills Rated Capacity (50k-bags/day)

Plant Site

LUZON BASECOM, INC. 4,000 San Fernando, Pampanga Batangas Sugar Central, Inc. 5,500 Balayan, Batangas Cagayan Robina Sugar Milling, Co. 4,000 Piat, Cagayan Central Azucarera Don Pedro 10,000 Nasugbu, Batangas Hind Sugar Company 500 Manaoag, Pangasinan Peñafrancia Sugar Mill 4,000 Pili, Camarines Sur Central Azucarera de Tarlac 7,080 San Miguel, Tarlac Western Agri-Ventures Corporation 1,200 Paniqui, Tarlac VISAYAS / MINDANAO Central Azucarera de Bais 8,000 Bais, Negros Oriental Bogo-Medellin Milling Co., Inc. 2,800 Medellin, Cebu Busco Sugar Milling Company, Inc. 10,000 Quezon, Bukidnon Crystal Sugar Company, Inc. 4,500 Maramag, Bukidnon Davao Sugar Central Company, Inc. 4,000 Hagonoy, Davao del Sur Durano III & Sons, Inc. 2,000 Danao City, Cebu Hideco Sugar Milling Co., Inc. 5,000 Kananga, Leyte Ormoc Sugar Co., Inc. 2,000 Ormoc City, Leyte Universal Robina Sugar 8,000 Manjuyod, Negros Occidental South East Asia Sugar Mill Corp. 4,000 Matalam, North Cotabato Herminio Teves & Co., Inc. 3,000 Sta. Catalina, Negros Oriental PANAY Capiz Sugar Central, Inc. 3,500 President Roxas, Capiz Monomer Sugar Central, Inc. 2,500 Dumalag, Capiz New Frontier Sugar Corp. 4,200 Passi, Iloilo Passi (Iloilo) Sugar Central, Inc. 5,000 San Enrique, Iloilo NEGROS Binalbagan-Isabela Sugar Co., Inc. 10,000 Binalbagan, Negros Occidental

Date: July1999

2

Dacongcogon Producers' Coop. Mktg., Inc.

2,200 Kabankalan, Negros Occidental

Danao Development Corp. 3,000 Toboso, Negros Occidental First Farmers Holding Corp. 5,000 Talisay, Negros Occidental Hawaiian-Philippine Co. 6,500 Negros Occidental Central Azucarera de La Carlota 10,000 La Carlota City, Negros

Occidental Lopez Sugar Corp. 6,000 Sagay, Negros Occidental Ma-ao Sugar Central 5,000 Bago City, Negros Occidental Sagay Central, Inc. 3,000 Sagay, Negros Occidental San Carlos Milling Co., Inc. 4,800 San Carlos City, Negros

Occidental Southern Negros Development Corp. 4,000 Kabankalan, Negros Occidental Sunnix Management Corp. 4,000 Silay City, Negros Occidental Victorias Milling Co. 12,000 Victorias, Negros Occidental

Source: Sugar Regulatory Administration

! 5 sugar mills in the top 1,000 corporations (1995 to 1997): Central Azucarera Don Pedro, Universal Robina Sugar Milling Corporation, Central Azucarera De Tarlac, BUSCO Sugar Milling Company, Inc., and Central Azucarera de Bais, Inc. (1996 and 1997).

2. Calculating Market Share

! Limitation: No available information on individual sales by sugar mill/refinery, so this study looks at data on gross revenues provided in the publication Top 7000 Corporations of 16 sugar mills/refineries (see Table 2).

Table 2. Revenue Shares: 1995 – 1996

Players 1995 1996

Central Azucarera Don Pedro 32.9 29.3 Central Azucarera de Tarlac 12.3 16.4 Busco Sugar Milling Co., Inc. 9.7 10.3 New Leyte Edible Oil Mfg. Corp. 12.2 8.3 Central Azucarera de Bais, Inc. 4.3 7.4 Universal Robina Sugar Milling Corp. 9.1 6.7 HIDECO Sugar Milling Co., Inc. 5.2 6.1 Sagay Central, Inc. 2.9 3.2 Pampanga Sugar Development Co., Inc. 2.8 2.5 Bogo-Medellin Milling Co., Inc. 2.9 2.3 Ma-ao Sugar Central Co., Inc. 1.2 1.1 Southern Negros Development Corp. 3.1 1.0 Tarlac Development Corp. Nil 0.4 Southwind Sugar Corporation 0.5 4.1 Manuel L. Teves, Inc. 0.5 0.6 Associated Sugar, Inc. 0.2 0.5

Source of Basic Data: Top 7000 Corporations 3. Level of Concentration

! Limitation: Calculation is based on the revenue shares of the 16 market players identified in Table 2, assuming that other mills/refineries are insignificant players.

Date: July1999

3

! Level of Concentration: Moderately concentrated.

4. Conditions Affecting Competitiveness

! Government Regulation: Republic Act No. 809 (1952) regulates the sugar industry from the planting of sugarcane up to the eventual disposition of the sugar product. Regulatory Agency - Sugar Regulatory Administration (SRA) Executive Order (EO) No. 18, s. 1986, governed by the Sugar Board, chaired by the Secretary of Agriculture, with a representative each of sugar millers and sugar planters as members. It has the power to regulate production of, establish market allocations for, and institute a quedaning system for sugar.

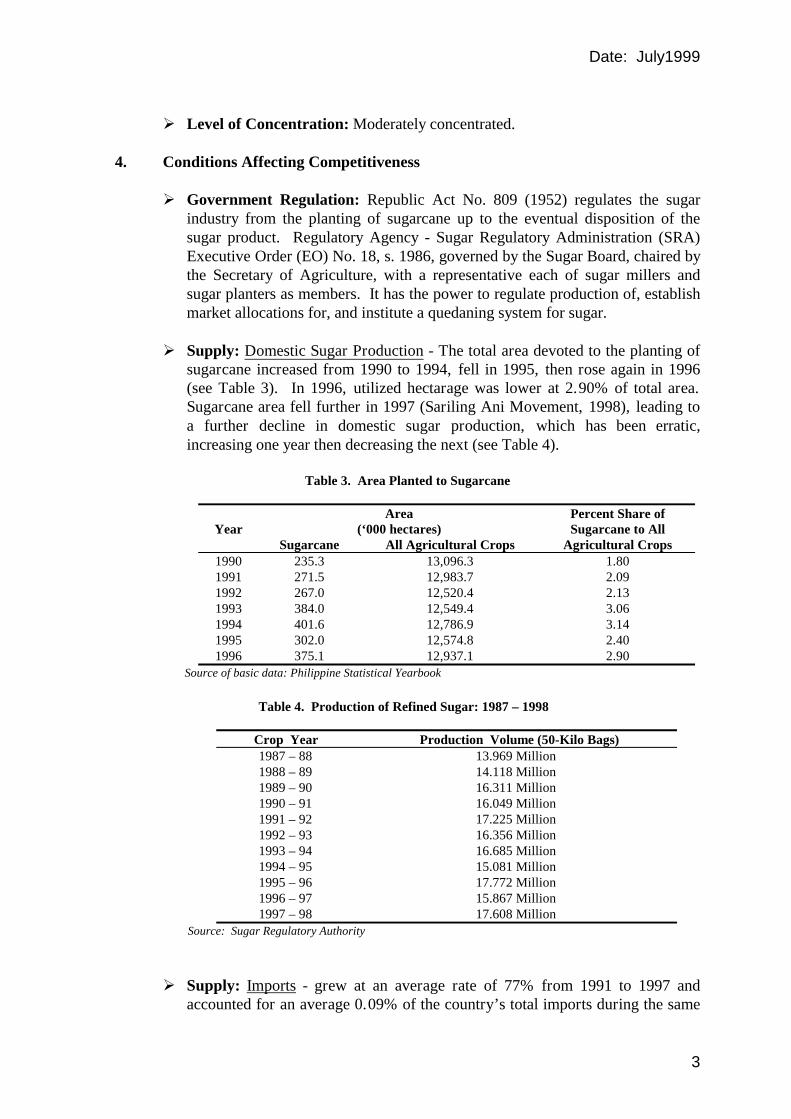

! Supply: Domestic Sugar Production - The total area devoted to the planting of

sugarcane increased from 1990 to 1994, fell in 1995, then rose again in 1996 (see Table 3). In 1996, utilized hectarage was lower at 2.90% of total area. Sugarcane area fell further in 1997 (Sariling Ani Movement, 1998), leading to a further decline in domestic sugar production, which has been erratic, increasing one year then decreasing the next (see Table 4).

Table 3. Area Planted to Sugarcane

Year Area

(‘000 hectares) Percent Share of Sugarcane to All

Sugarcane All Agricultural Crops Agricultural Crops 1990 235.3 13,096.3 1.80 1991 271.5 12,983.7 2.09 1992 267.0 12,520.4 2.13 1993 384.0 12,549.4 3.06 1994 401.6 12,786.9 3.14 1995 302.0 12,574.8 2.40 1996 375.1 12,937.1 2.90

Source of basic data: Philippine Statistical Yearbook

Table 4. Production of Refined Sugar: 1987 – 1998

Crop Year Production Volume (50-Kilo Bags) 1987 – 88 13.969 Million 1988 – 89 14.118 Million 1989 – 90 16.311 Million 1990 – 91 16.049 Million 1991 – 92 17.225 Million 1992 – 93 16.356 Million 1993 – 94 16.685 Million 1994 – 95 15.081 Million 1995 – 96 17.772 Million 1996 – 97 15.867 Million 1997 – 98 17.608 Million

Source: Sugar Regulatory Authority

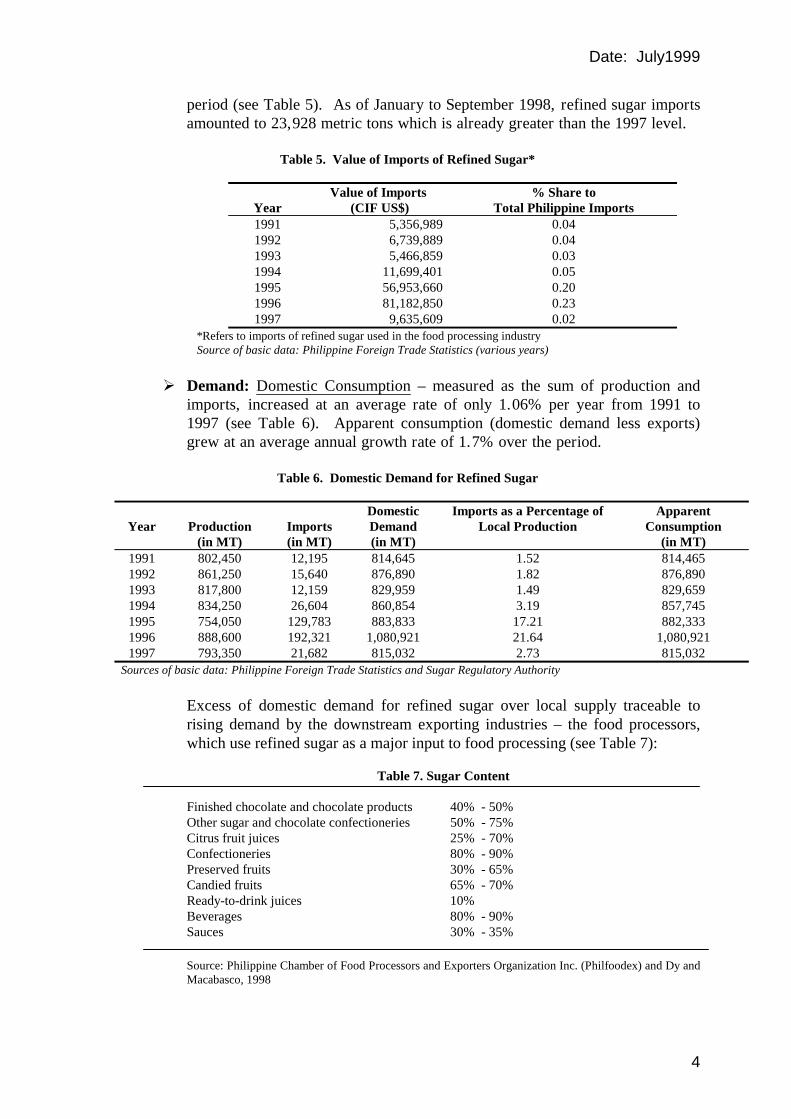

! Supply: Imports - grew at an average rate of 77% from 1991 to 1997 and

accounted for an average 0.09% of the country’s total imports during the same

Date: July1999

4

period (see Table 5). As of January to September 1998, refined sugar imports amounted to 23,928 metric tons which is already greater than the 1997 level.

Table 5. Value of Imports of Refined Sugar*

Year Value of Imports

(CIF US$) % Share to

Total Philippine Imports 1991 5,356,989 0.04 1992 6,739,889 0.04 1993 5,466,859 0.03 1994 11,699,401 0.05 1995 56,953,660 0.20 1996 81,182,850 0.23 1997 9,635,609 0.02

*Refers to imports of refined sugar used in the food processing industry Source of basic data: Philippine Foreign Trade Statistics (various years)

! Demand: Domestic Consumption – measured as the sum of production and imports, increased at an average rate of only 1.06% per year from 1991 to 1997 (see Table 6). Apparent consumption (domestic demand less exports) grew at an average annual growth rate of 1.7% over the period.

Table 6. Domestic Demand for Refined Sugar

Year

Production

(in MT)

Imports (in MT)

Domestic Demand (in MT)

Imports as a Percentage of Local Production

Apparent Consumption

(in MT) 1991 802,450 12,195 814,645 1.52 814,465 1992 861,250 15,640 876,890 1.82 876,890 1993 817,800 12,159 829,959 1.49 829,659 1994 834,250 26,604 860,854 3.19 857,745 1995 754,050 129,783 883,833 17.21 882,333 1996 888,600 192,321 1,080,921 21.64 1,080,921 1997 793,350 21,682 815,032 2.73 815,032

Sources of basic data: Philippine Foreign Trade Statistics and Sugar Regulatory Authority

Excess of domestic demand for refined sugar over local supply traceable to rising demand by the downstream exporting industries – the food processors, which use refined sugar as a major input to food processing (see Table 7):

Table 7. Sugar Content

Finished chocolate and chocolate products 40% - 50% Other sugar and chocolate confectioneries 50% - 75% Citrus fruit juices 25% - 70% Confectioneries 80% - 90% Preserved fruits 30% - 65% Candied fruits 65% - 70% Ready-to-drink juices 10% Beverages 80% - 90% Sauces 30% - 35%

Source: Philippine Chamber of Food Processors and Exporters Organization Inc. (Philfoodex) and Dy and Macabasco, 1998

Date: July1999

5

According to the Philippine Chamber of Food Manufacturers, Inc., about 200,000 metric tons of sugar are used yearly for various food products. The Beverage Industry Association of the Philippines (BIAP) for its part, consumes 37% of the country’s production of refined sugar.

! Exports: The industry managed to export minimal levels between 1993 and

1995. Exports totally disappeared from 1996 onwards.

! Price Competitiveness: The world price of refined sugar increased by an average of 13.6% from 1993 to 1998. The domestic price of refined sugar has consistently been higher than the world price (see Table 8).

Table 8. Price of Refined Sugar (P/kg.)

World Domestic Wholesale Percent Difference Between

Year Price Price World and Domestic Price 1993 9.49 16.42 73.02 1994 10.32 18.67 80.91 1995 12.03 22.92 90.52 1996 11.78 22.75 93.12 1997 12.09 20.75 71.63 1998 17.17 26.83 56.26

Source: Philfoodex Bonded Warehouse, Inc.

To produce a 50-kilo bag of refined sugar, more than 90% of the cost comes from raw sugar. Other expenses (e.g. labor, overhead expenses, steam generating fuel, process material, container) contribute less than 10%. World prices of raw sugar is much lower than domestic prices (see Table 9).

Table 9. Price of Raw Sugar (P/50-kg. bag)

Price Percent Difference Between Year World Domestic World and Domestic Price 1991 273.28 568.85 108.16 1992 255.12 527.03 106.58 1993 306.65 476.15 55.27 1994 345.30 635.03 83.91 1995 315.04 833.34 164.52 1996 307.73 770.69 150.44

1997* 365.64 700.01 91.45 1998** 412.34 832.56 101.91

* Average of January to December 1997 monthly prices ** Average of January to September 1998 monthly prices Source: De la Peña, B. (1998)

Observations on price competitiveness of domestic sugar (Tolentino, 1999): (a) during the last 18 years, domestic sugar prices have been higher than world prices; (b) since 1981, domestic prices have exceeded world prices by more than 100% on the average; (c) although both domestic and world prices have increased steadily, domestic prices have increased at a faster rate and have also been more volatile; (d) during the “sugar crisis” in the latter semester of 1998, the domestic price of sugar was increasing rapidly even though the world price was stable or on a downtrend.

Date: July1999

6

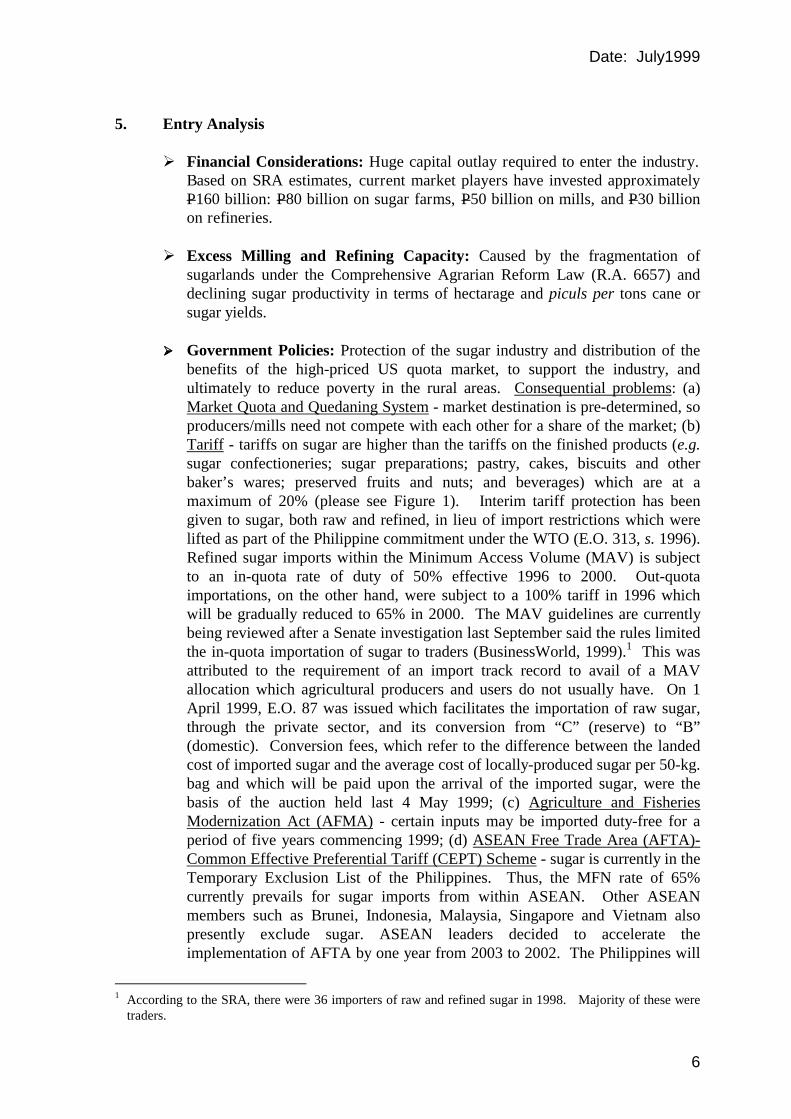

5. Entry Analysis

! Financial Considerations: Huge capital outlay required to enter the industry. Based on SRA estimates, current market players have invested approximately P160 billion: P80 billion on sugar farms, P50 billion on mills, and P30 billion on refineries.

! Excess Milling and Refining Capacity: Caused by the fragmentation of

sugarlands under the Comprehensive Agrarian Reform Law (R.A. 6657) and declining sugar productivity in terms of hectarage and piculs per tons cane or sugar yields.

!!!! Government Policies: Protection of the sugar industry and distribution of the

benefits of the high-priced US quota market, to support the industry, and ultimately to reduce poverty in the rural areas. Consequential problems: (a) Market Quota and Quedaning System - market destination is pre-determined, so producers/mills need not compete with each other for a share of the market; (b) Tariff - tariffs on sugar are higher than the tariffs on the finished products (e.g. sugar confectioneries; sugar preparations; pastry, cakes, biscuits and other baker’s wares; preserved fruits and nuts; and beverages) which are at a maximum of 20% (please see Figure 1). Interim tariff protection has been given to sugar, both raw and refined, in lieu of import restrictions which were lifted as part of the Philippine commitment under the WTO (E.O. 313, s. 1996). Refined sugar imports within the Minimum Access Volume (MAV) is subject to an in-quota rate of duty of 50% effective 1996 to 2000. Out-quota importations, on the other hand, were subject to a 100% tariff in 1996 which will be gradually reduced to 65% in 2000. The MAV guidelines are currently being reviewed after a Senate investigation last September said the rules limited the in-quota importation of sugar to traders (BusinessWorld, 1999).1 This was attributed to the requirement of an import track record to avail of a MAV allocation which agricultural producers and users do not usually have. On 1 April 1999, E.O. 87 was issued which facilitates the importation of raw sugar, through the private sector, and its conversion from “C” (reserve) to “B” (domestic). Conversion fees, which refer to the difference between the landed cost of imported sugar and the average cost of locally-produced sugar per 50-kg. bag and which will be paid upon the arrival of the imported sugar, were the basis of the auction held last 4 May 1999; (c) Agriculture and Fisheries Modernization Act (AFMA) - certain inputs may be imported duty-free for a period of five years commencing 1999; (d) ASEAN Free Trade Area (AFTA)-Common Effective Preferential Tariff (CEPT) Scheme - sugar is currently in the Temporary Exclusion List of the Philippines. Thus, the MFN rate of 65% currently prevails for sugar imports from within ASEAN. Other ASEAN members such as Brunei, Indonesia, Malaysia, Singapore and Vietnam also presently exclude sugar. ASEAN leaders decided to accelerate the implementation of AFTA by one year from 2003 to 2002. The Philippines will

1 According to the SRA, there were 36 importers of raw and refined sugar in 1998. Majority of these were

traders.

Date: July1999

7

likely exercise the flexibility option and sugar will be phased into the Scheme by 2003 at a CEPT rate of 5%; (e) WTO - To reach the 50% target by 2004, reductions must be implemented in 1997 and 2000. Thus, from 100% in 1996, the out-quota rate of duty on refined sugar was reduced to 80% in 1997 and further to 65% in 1999 and 2000; and (f) Asia Pacific Economic Cooperation (APEC), the goal is zero tariffs in 2010 and 2020 for developed and developing countries, respectively.

!!!! Import Restrictions: Under Central Bank Circular 850, the importation of

refined sugar was liberalized effective 15 February 1982. In reality, the SRA continues to exercise regulatory powers by way of monitoring sugar imports2, imposing monitoring fees3, and prescribing administrative procedures if the imported sugar is not used in food processing.

6. Assessment of Industry Performance

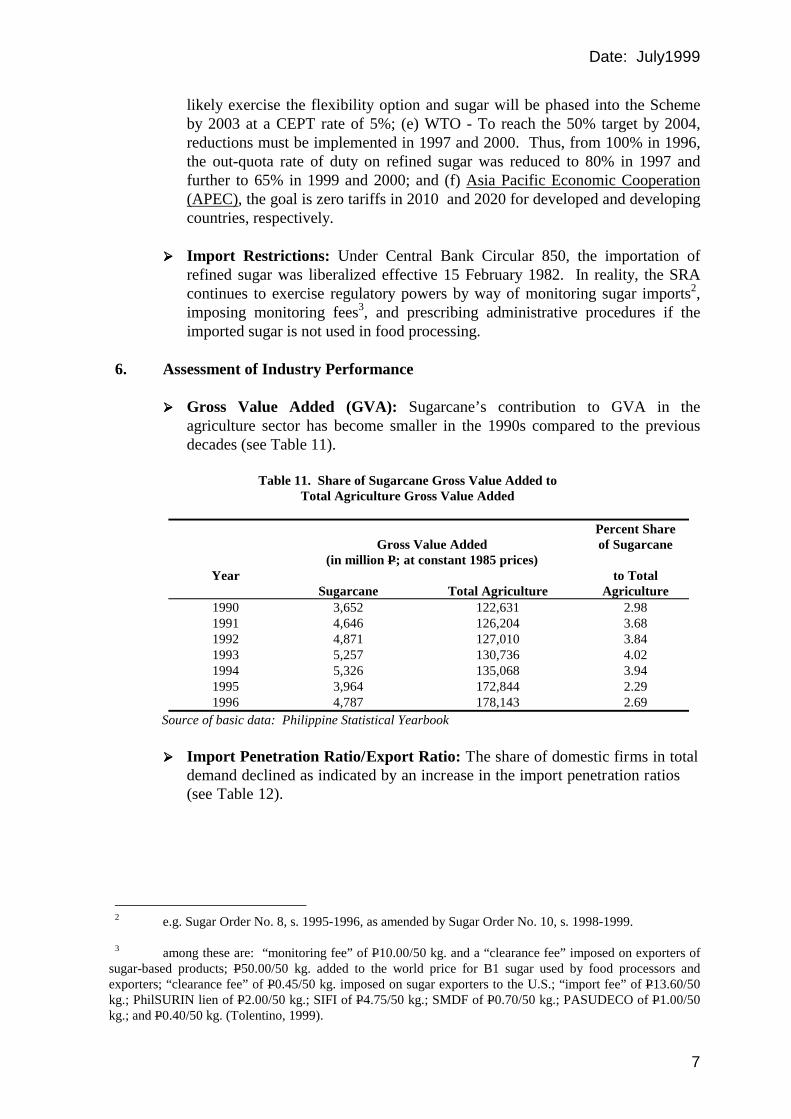

!!!! Gross Value Added (GVA): Sugarcane’s contribution to GVA in the agriculture sector has become smaller in the 1990s compared to the previous decades (see Table 11).

Table 11. Share of Sugarcane Gross Value Added to

Total Agriculture Gross Value Added

Gross Value Added

(in million P; at constant 1985 prices)

Percent Share of Sugarcane

Year Sugarcane

Total Agriculture

to Total Agriculture

1990 3,652 122,631 2.98 1991 4,646 126,204 3.68 1992 4,871 127,010 3.84 1993 5,257 130,736 4.02 1994 5,326 135,068 3.94 1995 3,964 172,844 2.29 1996 4,787 178,143 2.69

Source of basic data: Philippine Statistical Yearbook

!!!! Import Penetration Ratio/Export Ratio: The share of domestic firms in total demand declined as indicated by an increase in the import penetration ratios (see Table 12).

2 e.g. Sugar Order No. 8, s. 1995-1996, as amended by Sugar Order No. 10, s. 1998-1999. 3 among these are: “monitoring fee” of P10.00/50 kg. and a “clearance fee” imposed on exporters of

sugar-based products; P50.00/50 kg. added to the world price for B1 sugar used by food processors and exporters; “clearance fee” of P0.45/50 kg. imposed on sugar exporters to the U.S.; “import fee” of P13.60/50 kg.; PhilSURIN lien of P2.00/50 kg.; SIFI of P4.75/50 kg.; SMDF of P0.70/50 kg.; PASUDECO of P1.00/50 kg.; and P0.40/50 kg. (Tolentino, 1999).

Date: July1999

8

Table 12. Indicators of Exposure to Foreign Competition

Year

Import Penetration Ratioa (%)

Share of Exports to Productionb (%)

1991 1.50 --- 1992 1.78 --- 1993 1.46 * 1994 3.09 * 1995 14.68 * 1996 17.79 --- 1997 2.40 ---