Embed Size (px)

Citation preview

REGIONAL INTEGRATION IN LATIN AMERICA

Luis Ángel MadridApril 2010

The LA region

Background

• Six years of economic bonanza 2002-2008 (induced by China’s appetite for natural resources $ commodities)

• Grappling with the global recession of 2008-2009 (how to be counter-cyclical)

• Structural problems: the world’s highest rates of inequality and public insecurity (poverty & unemployment)

• In which direction in the near future? Populism or market economics?

World Economic Forum in LA

• A stronger cooperation and integration in Latin America is needed

• The entire process has been jeopardized by ideological and political differences

• Trade should is being used as political weapon

Cartagena, April 7-8th 2010

TOPICS

1. Latin America at the WTO: ignorance or pessimism?

2. The regional environment: many steps backwards?

3. The preferred venue: bilateralism within and without.

MULTILATERALISM: THE WTO

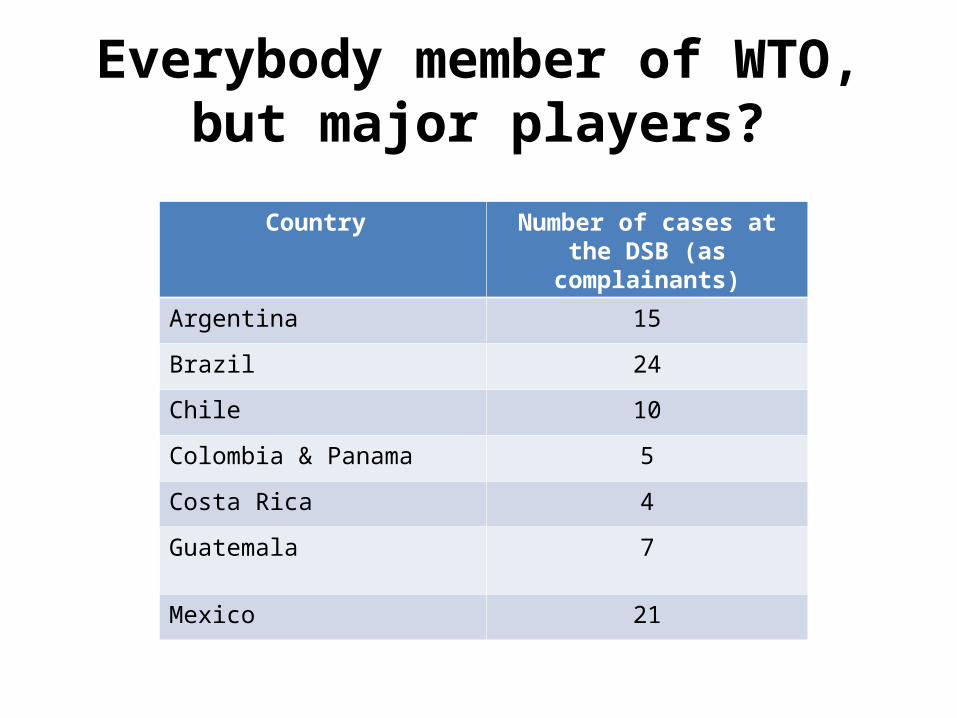

Everybody member of WTO, but major players?

Country Number of cases at the DSB (as complainants)

Argentina 15

Brazil 24

Chile 10

Colombia & Panama 5

Costa Rica 4

Guatemala 7

Mexico 21

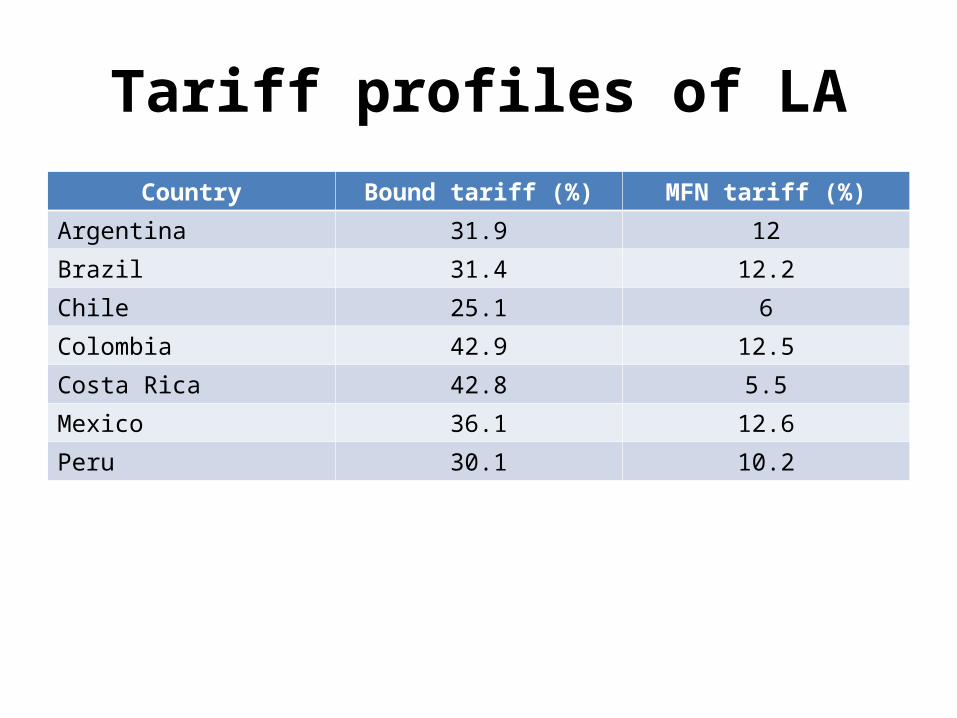

Tariff profiles of LACountry Bound tariff (%) MFN tariff (%)

Argentina 31.9 12

Brazil 31.4 12.2

Chile 25.1 6

Colombia 42.9 12.5

Costa Rica 42.8 5.5

Mexico 36.1 12.6

Peru 30.1 10.2

REGIONALISM

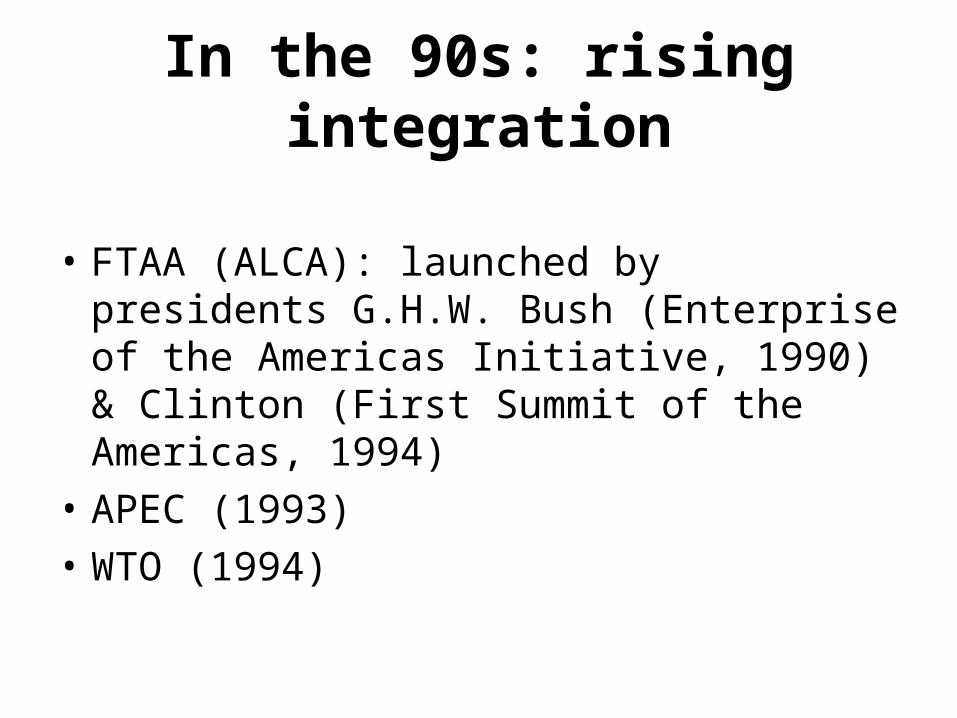

In the 90s: rising integration

• FTAA (ALCA): launched by presidents G.H.W. Bush (Enterprise of the Americas Initiative, 1990) & Clinton (First Summit of the Americas, 1994)

• APEC (1993)• WTO (1994)

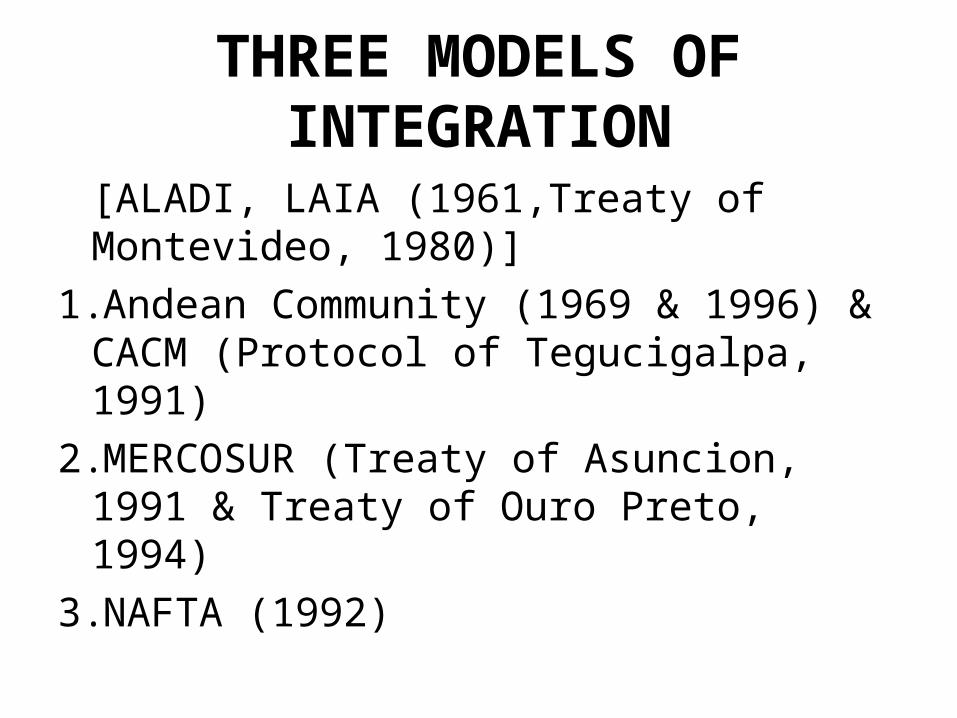

THREE MODELS OF INTEGRATION

[ALADI, LAIA (1961,Treaty of Montevideo, 1980)]

1.Andean Community (1969 & 1996) & CACM (Protocol of Tegucigalpa, 1991)

2.MERCOSUR (Treaty of Asuncion, 1991 & Treaty of Ouro Preto, 1994)

3.NAFTA (1992)

ANDEAN COMMUNITY

Intra-regional trade (exports)

CAN countries 1990-1999 2000-2006

Bolivia 41,8 51,3

Colombia 24,6 31,9

Ecuador 22 30,4

Peru 17,5 19,1

Venezuela 50,7 35,7

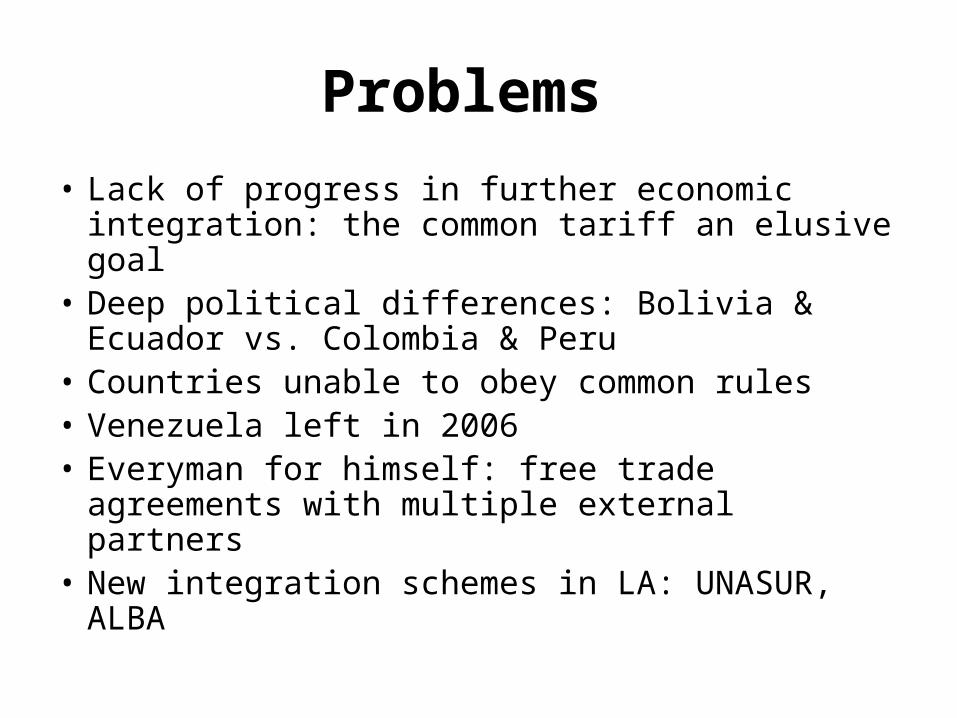

Problems

• Lack of progress in further economic integration: the common tariff an elusive goal

• Deep political differences: Bolivia & Ecuador vs. Colombia & Peru

• Countries unable to obey common rules • Venezuela left in 2006• Everyman for himself: free trade agreements

with multiple external partners• New integration schemes in LA: UNASUR, ALBA

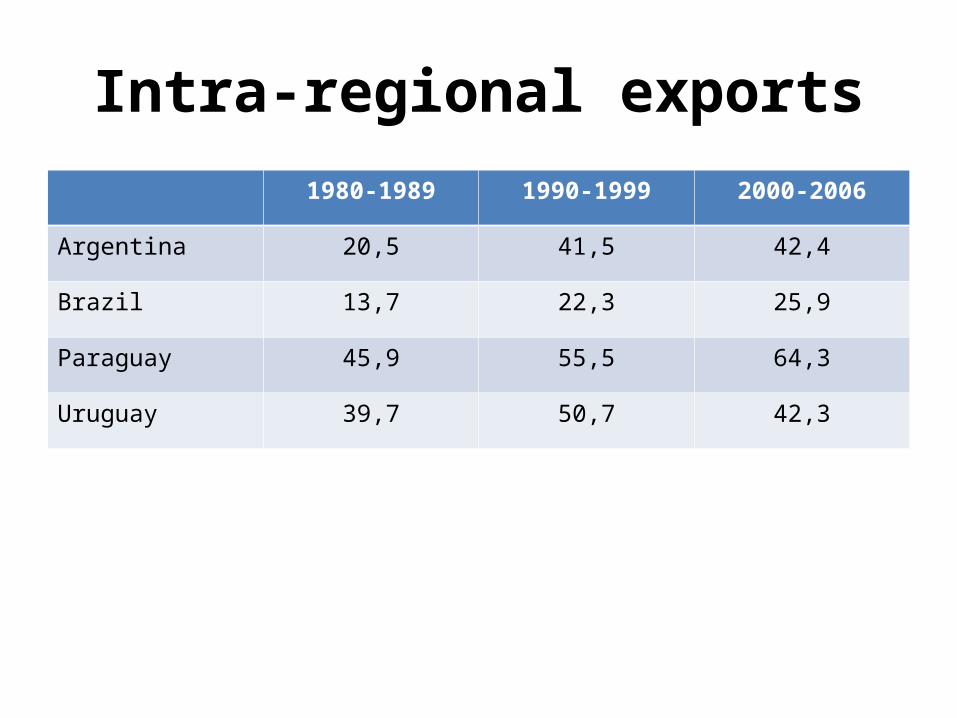

MERCOSUR

Intra-regional exports1980-1989 1990-1999 2000-2006

Argentina 20,5 41,5 42,4

Brazil 13,7 22,3 25,9

Paraguay 45,9 55,5 64,3

Uruguay 39,7 50,7 42,3

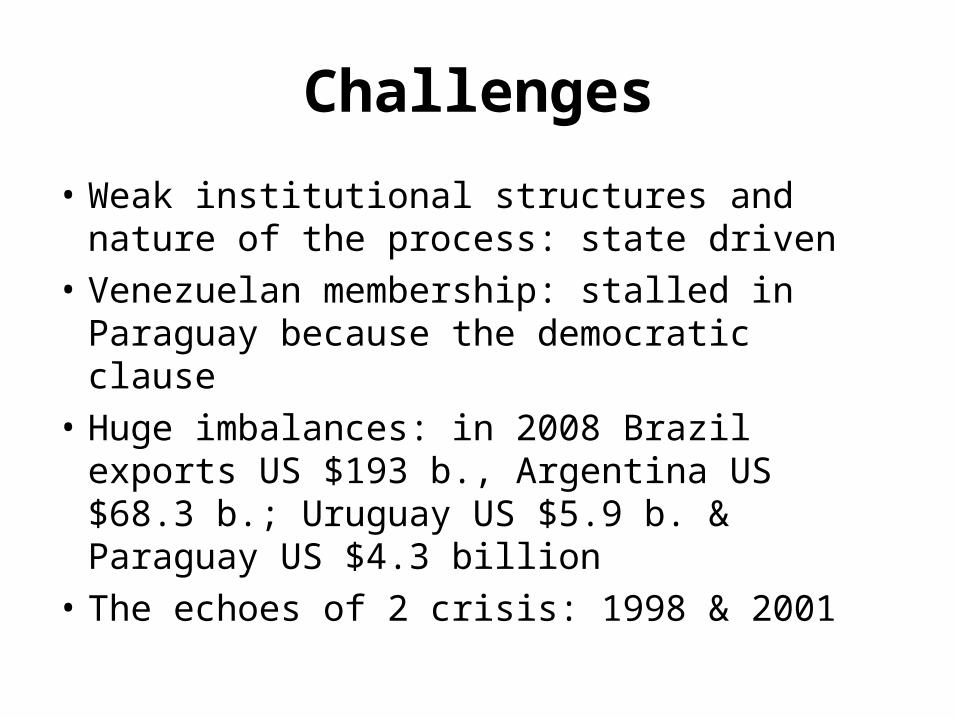

Challenges

• Weak institutional structures and nature of the process: state driven

• Venezuelan membership: stalled in Paraguay because the democratic clause

• Huge imbalances: in 2008 Brazil exports US $193 b., Argentina US $68.3 b.; Uruguay US $5.9 b. & Paraguay US $4.3 billion

• The echoes of 2 crisis: 1998 & 2001

BILATERALISM

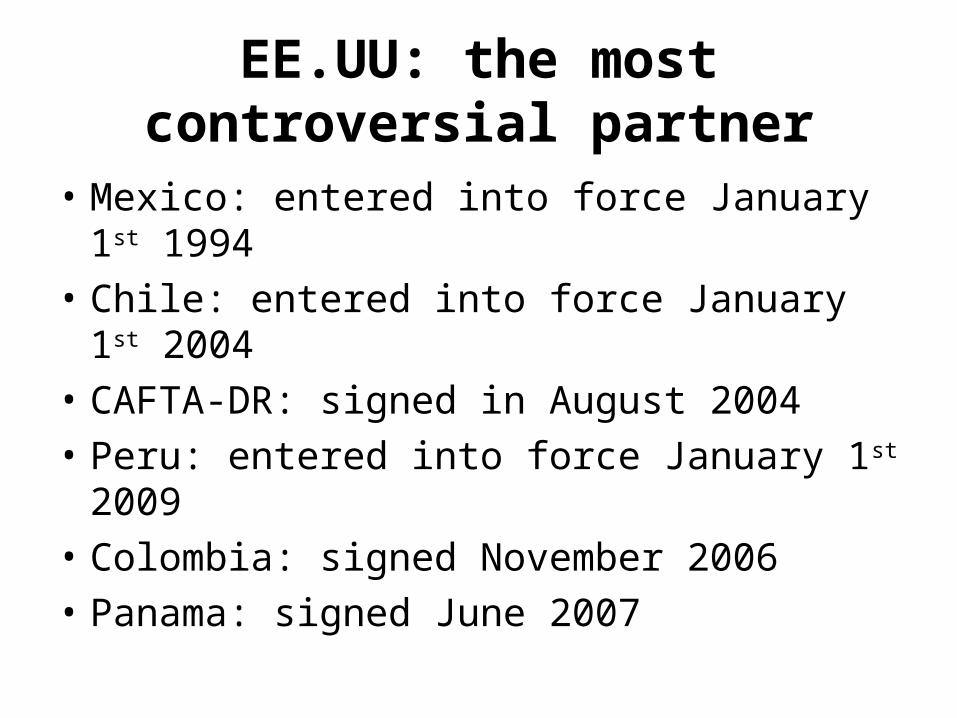

EE.UU: the most controversial partner

• Mexico: entered into force January 1st 1994• Chile: entered into force January 1st 2004• CAFTA-DR: signed in August 2004• Peru: entered into force January 1st 2009• Colombia: signed November 2006• Panama: signed June 2007

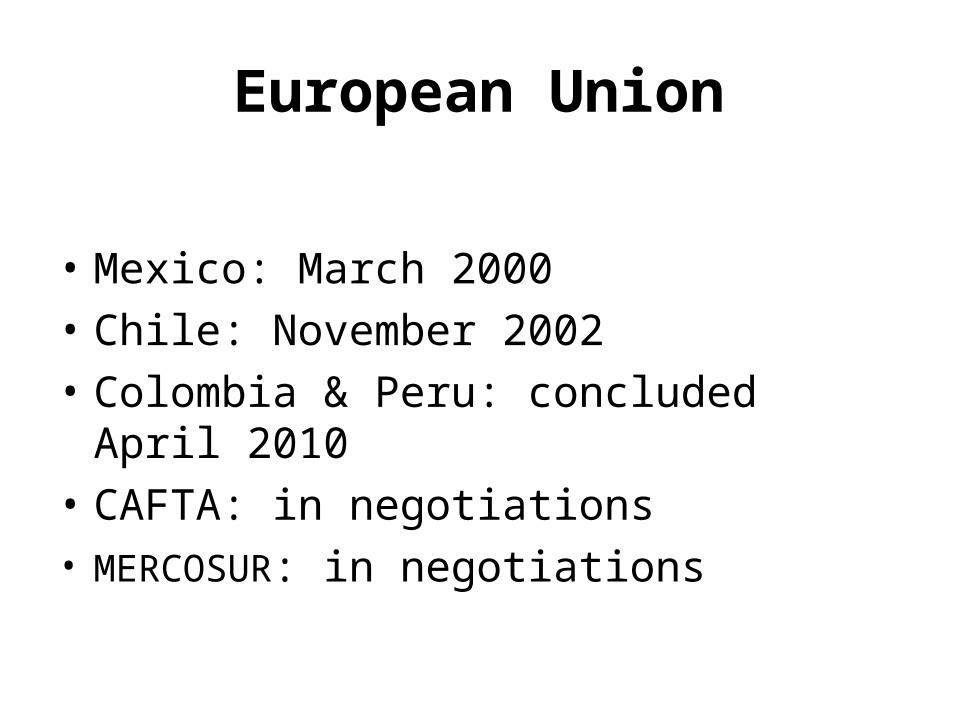

European Union

• Mexico: March 2000• Chile: November 2002• Colombia & Peru: concluded April 2010• CAFTA: in negotiations• MERCOSUR: in negotiations

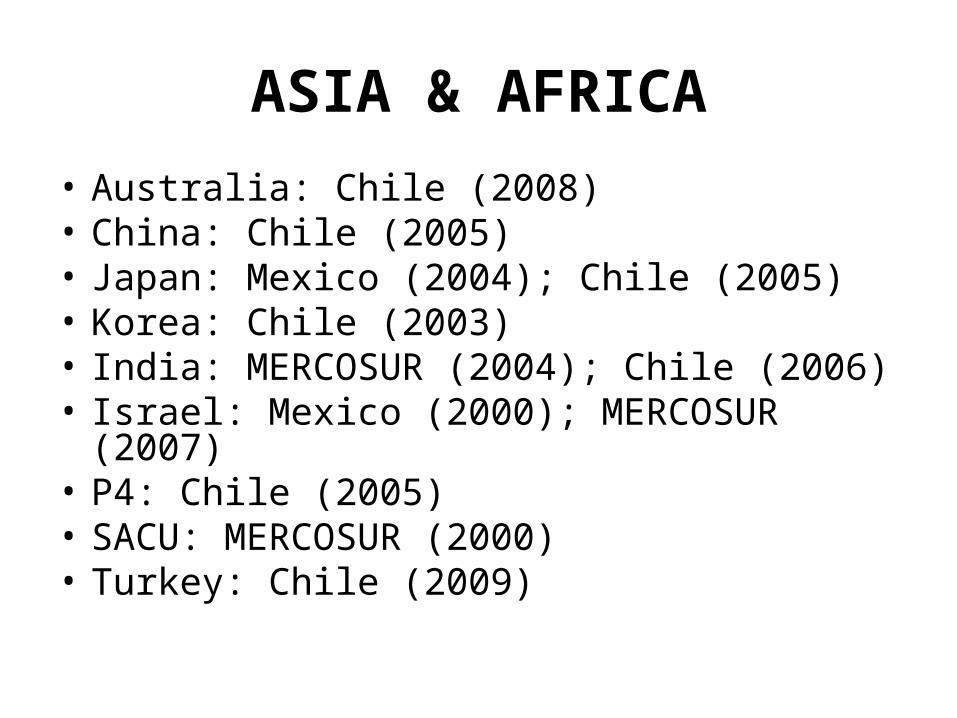

ASIA & AFRICA• Australia: Chile (2008)• China: Chile (2005) • Japan: Mexico (2004); Chile (2005)• Korea: Chile (2003)• India: MERCOSUR (2004); Chile (2006)• Israel: Mexico (2000); MERCOSUR (2007)• P4: Chile (2005)• SACU: MERCOSUR (2000)• Turkey: Chile (2009)

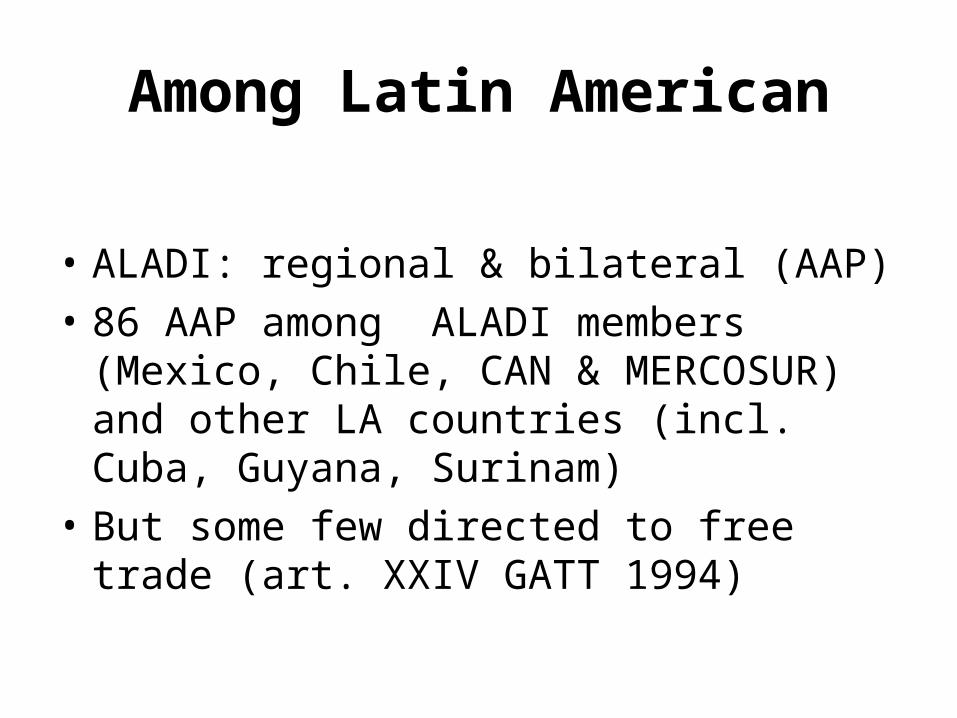

Among Latin American

• ALADI: regional & bilateral (AAP)• 86 AAP among ALADI members (Mexico,

Chile, CAN & MERCOSUR) and other LA countries (incl. Cuba, Guyana, Surinam)

• But some few directed to free trade (art. XXIV GATT 1994)

Conclusions

• NAFTA led the way with the US, but fraught with problems (Colombia, Panama, Ecuador, Venezuela, MERCOSUR)

• European Union in similar situation (plus CAFTA)• China the major question: Brazil signed several

mineral agreements on April 15th 2010; clashing interest remain (undervalued yuan undermines Brazilian industry, Brazil closed economy & bid for the SC).

MANY THANKS